Embed Size (px)

Citation preview

How APIs Can Enable InsurTech and HR Platforms

to Build Individual Coverage HRA Solutions

ICHRA TOOLKITFOR INSURTECH + HR PLATFORMS

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

1

THE VERICRED PLATFORM: ENABLING INNOVATION WITH MODERN APIs------------------------------------

Health Reimbursement Arrangements (HRAs), a benefits option in which employers reimburse employees for qualified healthcare expenditures, have existed since the 1970s. HRAs have undergone several iterations since their inception, but the latest could revolutionize how many employers sponsor health coverage for their workers.

Recent updates to federal HRA regulations established a new type of HRA— the Individual Coverage HRA (ICHRA)— which, as of January 2020, enables businesses to reimburse employees tax-free for premiums for health insurance purchased in the individual market. Just as the shift from defined-benefit pensions to defined-contribution 401(k) plans altered how Americans save for retirement, ICHRAs could have a similar effect on how employers of all sizes fund and manage employee health benefits. In the age of personalized benefits and the consumerization of healthcare, ICHRAs are a significant step toward reinventing health insurance as a 401(k)-style benefit— customizable to meet the specific needs of each employee and transportable from one job to another, without loss of coverage.

ICHRAs, however, aren’t necessarily best for all circumstances. Navigating whether an ICHRA is right for businesses and their employees will require employers— directly and through their brokers— to fully examine the plan options available in both the group and individual health insurance markets. Technology platforms have an opportunity to help guide these stakeholders— brokers, employers and HR decision-makers— through this complex process by building digital experiences for plan comparison, decision-support, and the quoting and enrollment of individual health plans.

At Vericred, we simplify the exchange of health insurance and employee benefits data between health insurance carriers and technology companies. Acting as a translation layer between the two industry stakeholders, we are uniquely positioned to see the challenges faced by the constituents evaluating new ICHRA solutions. In this toolkit, we explore how, equipped with the appropriate data and APIs, tech platforms operating in the health insurance, benefits and HR space can seamlessly develop digital solutions for the ICHRA market.

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

2

WHAT YOU’LL FIND IN THIS TOOLKIT: ------------------------------------

HRA 101 The basics of HRAs and what’s new in 2020 (ICHRA)

The Details are in the Data: ICHRA Industry AnalysisCheck out Vericred’s research on the ICHRA market

Vericred’s Data Solution: APIs and the HRA Development KitLearn how Vericred’s APIs enable tech platforms to build digital solutions for the ICHRA market

Contact Us: Get set up with a free consultation and find out whether Vericred’s solutions are right for you

1234

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

3

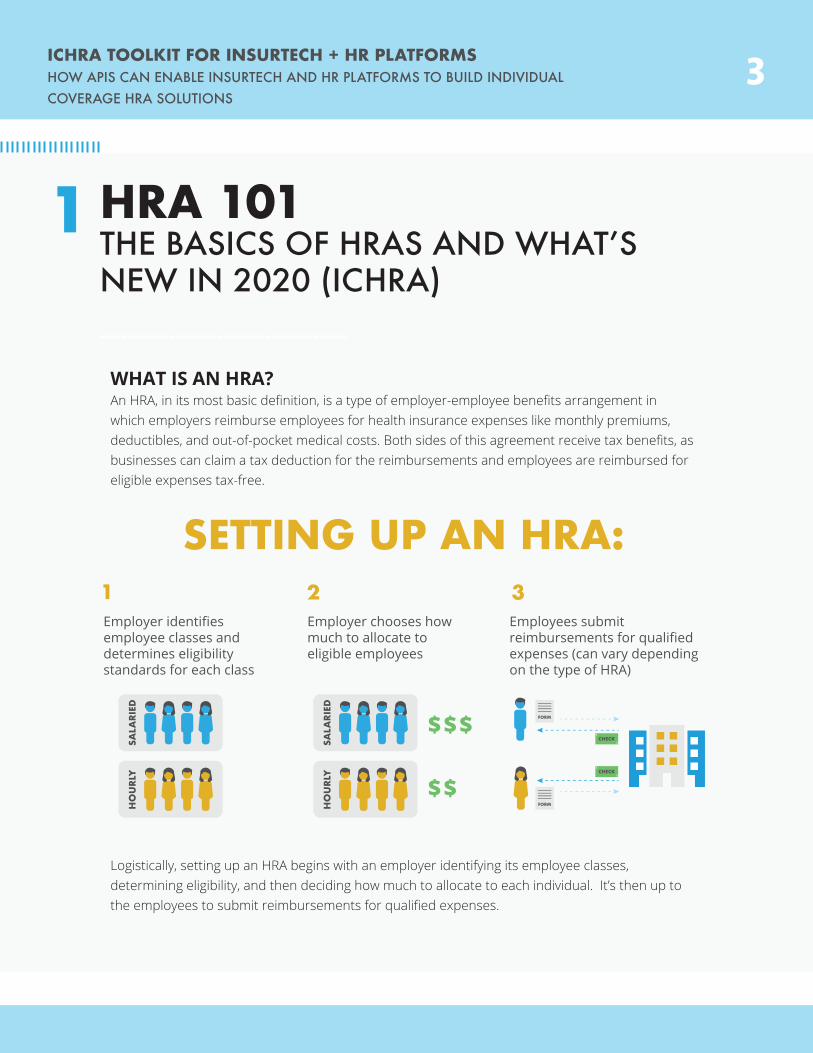

HRA 101THE BASICS OF HRAS AND WHAT’S NEW IN 2020 (ICHRA)------------------------------------

WHAT IS AN HRA?An HRA, in its most basic definition, is a type of employer-employee benefits arrangement in which employers reimburse employees for health insurance expenses like monthly premiums, deductibles, and out-of-pocket medical costs. Both sides of this agreement receive tax benefits, as businesses can claim a tax deduction for the reimbursements and employees are reimbursed for eligible expenses tax-free.

1

Logistically, setting up an HRA begins with an employer identifying its employee classes, determining eligibility, and then deciding how much to allocate to each individual. It’s then up to the employees to submit reimbursements for qualified expenses.

SETTING UP AN HRA:

Employer identifies employee classes and determines eligibility standards for each class

Employer chooses how much to allocate to eligible employees

Employees submit reimbursements for qualified expenses (can vary depending on the type of HRA)

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

4

WHAT’S THE RELATIONSHIP BETWEEN TRADITIONAL GROUP PLANS AND HRAS?Traditionally, most businesses that offer health benefits do so by selecting one or several insurance plans in which employees may enroll. However, for those companies that want to provide health coverage to their employees without managing and administering the benefit themselves, HRAs represent an appealing alternative. Instead of employers taking on the administrative burden of shopping for plans, enrolling members and handling other benefits tasks, most of these responsibilities would fall upon individual employees. HRAs permit employees to make the best health insurance decisions for them, while businesses simply provide reimbursements for qualified expenses. Most employers choose to offer either a group health plan or an HRA option— but not both.

THREE TYPES OF HRAS AND WHAT’S CHANGING IN 2020:

1. Qualified Small Employer Health Reimbursement Arrangement (QSEHRA):Beginning in 2017, small businesses— those with less than 50 employees— can offer HRAs that reimburse their employees for premiums and eligible healthcare expenses. These HRAs have contribution limits— $5,000 for an individual and $10,000 for a family— and must offer all employee classes the same terms.

2. Individual Coverage Health Reimbursement Arrangement (ICHRA):In June 2019, the Trump administration finalized new HRA rules that will create two new types of HRAs for 2020. ICHRAs, like QSEHRA, can be used to reimburse premiums and other expenses, but there are key differences:

• unlike QSEHRA, businesses of any size will be eligible to offer ICHRAs.

• no restrictions on the annual amount employers may reimburse employees.

• businesses may offer varying terms, and reimbursement allotments, to different employee classes (such as full-time, part-time, seasonal, non-salaried, etc.).

• ICHRAs enable applicable large employers (ALEs) to fulfill the Affordable Care Act’s employer mandate, which requires them to offer affordable, minimum essential health coverage to at least 95 percent of their full-time employees.

• ICHRA terms must remain uniform among employees of the same class, except that businesses may alter allotments based on the employee’s age or the number of dependents.

• ICHRA beneficiaries must maintain individual health coverage, through purchasing on-exchange or off-exchange insurance plans.

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

5

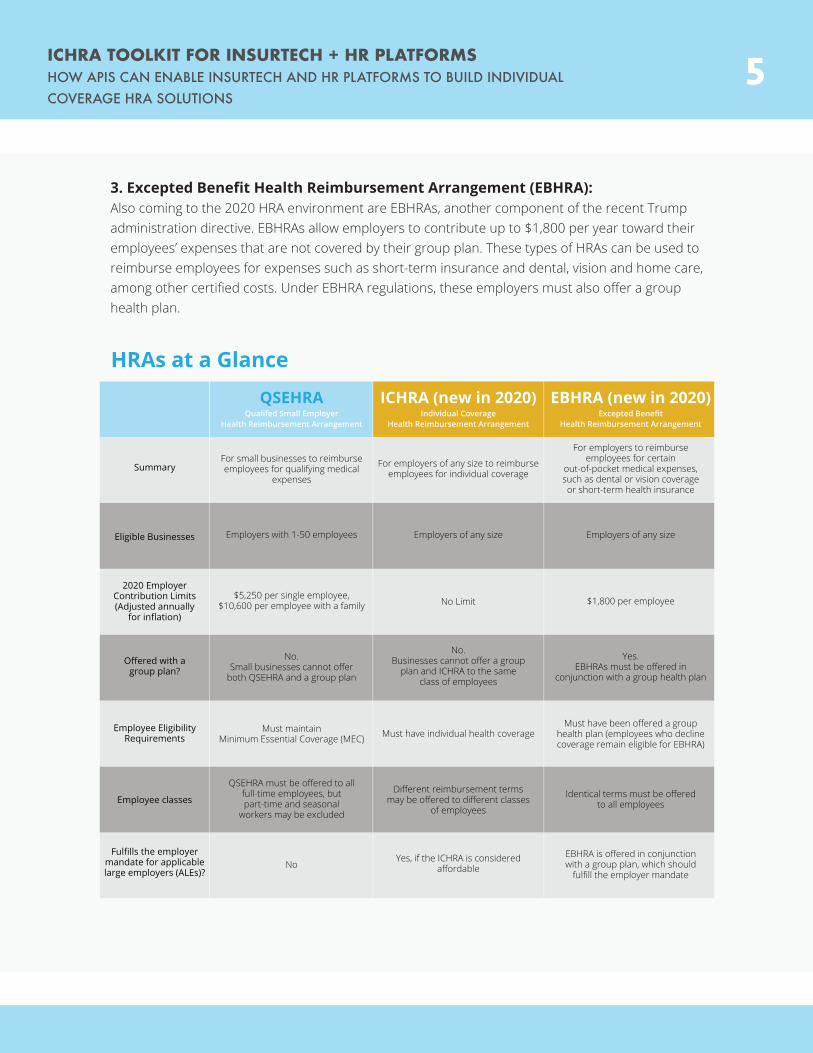

3. Excepted Benefit Health Reimbursement Arrangement (EBHRA):Also coming to the 2020 HRA environment are EBHRAs, another component of the recent Trump administration directive. EBHRAs allow employers to contribute up to $1,800 per year toward their employees’ expenses that are not covered by their group plan. These types of HRAs can be used to reimburse employees for expenses such as short-term insurance and dental, vision and home care, among other certified costs. Under EBHRA regulations, these employers must also offer a group health plan.

SummaryFor small businesses to reimburse employees for qualifying medical

expenses

For employers of any size to reimburse employees for individual coverage

No.Businesses cannot offer a group

plan and ICHRA to the same class of employees

Yes. EBHRAs must be offered in

conjunction with a group health plan

For employers to reimburse employees for certain

out-of-pocket medical expenses, such as dental or vision coverage or short-term health insurance

NoYes, if the ICHRA is considered

affordableEBHRA is offered in conjunction with a group plan, which should

fulfill the employer mandate

Must maintain Minimum Essential Coverage (MEC) Must have individual health coverage

Must have been offered a group health plan (employees who decline coverage remain eligible for EBHRA)

Identical terms must be offered to all employees

Eligible Businesses Employers with 1-50 employees

No. Small businesses cannot offer

both QSEHRA and a group plan

QSEHRA must be offered to all full-time employees, but part-time and seasonal

workers may be excluded

Different reimbursement terms may be offered to different classes

of employees

Employers of any sizeEmployers of any size

No Limit $1,800 per employee$5,250 per single employee, $10,600 per employee with a family

2020 Employer Contribution Limits (Adjusted annually

for inflation)

Offered with a group plan?

Employee Eligibility Requirements

Employee classes

Fulfills the employer mandate for applicable large employers (ALEs)?

ICHRA (new in 2020)Individual Coverage

Health Reimbursement Arrangement

QSEHRAQualifed Small Employer

Health Reimbursement Arrangement

EBHRA (new in 2020)Excepted Benefit

Health Reimbursement Arrangement

HRAs at a Glance

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

6

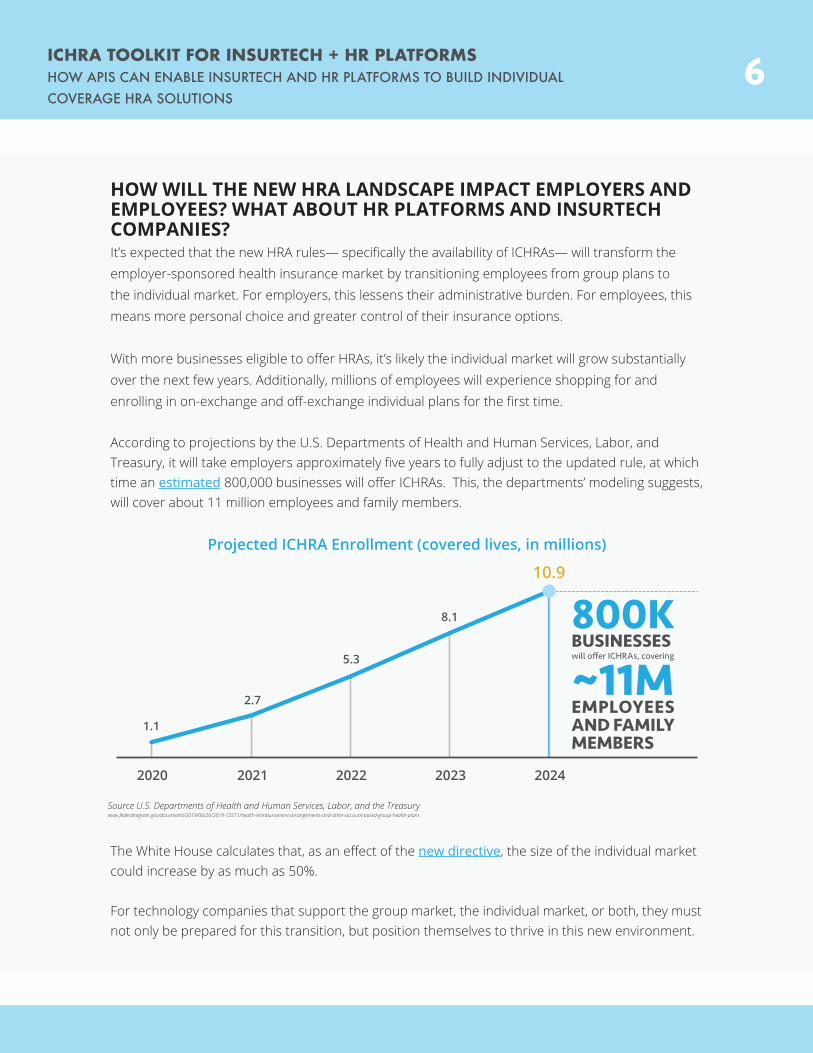

HOW WILL THE NEW HRA LANDSCAPE IMPACT EMPLOYERS AND EMPLOYEES? WHAT ABOUT HR PLATFORMS AND INSURTECH COMPANIES?It’s expected that the new HRA rules— specifically the availability of ICHRAs— will transform the employer-sponsored health insurance market by transitioning employees from group plans to the individual market. For employers, this lessens their administrative burden. For employees, this means more personal choice and greater control of their insurance options.

With more businesses eligible to offer HRAs, it’s likely the individual market will grow substantially over the next few years. Additionally, millions of employees will experience shopping for and enrolling in on-exchange and off-exchange individual plans for the first time.

According to projections by the U.S. Departments of Health and Human Services, Labor, and Treasury, it will take employers approximately five years to fully adjust to the updated rule, at which time an estimated 800,000 businesses will offer ICHRAs. This, the departments’ modeling suggests, will cover about 11 million employees and family members.

The White House calculates that, as an effect of the new directive, the size of the individual market could increase by as much as 50%.

For technology companies that support the group market, the individual market, or both, they must not only be prepared for this transition, but position themselves to thrive in this new environment.

Projected ICHRA Enrollment (covered lives, in millions)

2020

1.1

2.7

5.3

8.1

10.9

2021 2022 2023 2024

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

7

ICHRA & LARGE EMPLOYERS: A NEW ALTERNATIVE TO TRADITIONAL EMPLOYER-SPONSORED COVERAGEThough small groups— businesses with less than 50 employees— might be more likely to shift their employees to ICHRA, the new regulations create a viable benefits option for large employers as well. Unlike QSEHRA, businesses of any size will be eligible to offer ICHRAs.

Critically, ICHRA rules enable large employers to fulfill the Affordable Care Act’s employer mandate, which requires them to offer affordable, minimum essential health coverage to at least 95 percent of their full-time employees.

To fulfill this mandate, large employers must offer health insurance that is considered by the federal government to be affordable, relative to each individual’s income.

The IRS recently published a straightforward answer on what, exactly, is deemed “affordable”:

An ICHRA is affordable in 2020 if the remaining amount an employee has to pay for a self-only silver plan on the exchange is less than 9.78% of the employee’s household income.

To satisfy the employer mandate, large businesses must provide employees with a contribution such that, if used to purchase the lowest-cost silver plan, the excess amount an employee has to pay is less than 9.78% of the employee’s household income.

Affordability is yet another factor that employers, particularly those required to meet the employer mandate, will need to examine if they’re considering ICHRAs as an alternative to group coverage.

The onus will fall upon InsurTech and HR platforms to develop user-friendly, digital solutions that aid employers— and their brokers— through this complex decision.

Providing users with in-depth information regarding a full range of group and individual plans is an essential component of any ICHRA-ready tech solution, and pairing plan options with an affordability calculator would drive even more value to users.

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

8

THE DETAILS ARE IN THE DATA: ICHRA INDUSTRY ANALYSIS CHECK OUT VERICRED’S RESEARCH ON THE ICHRA MARKET------------------------------------

We’ve established that new HRA rules could potentially shift millions of employees from traditional group health plans to the individual ACA market. For businesses considering a move to ICHRAs, it is essential to determine how such a transition would alter their employees’ health insurance options

Vericred’s research team examined how the 2020 individual and group markets differ in plan design, networks, premiums and more. This crucial information enables employers to make cost-effective benefits decisions that best suit their— and their employees’— needs.

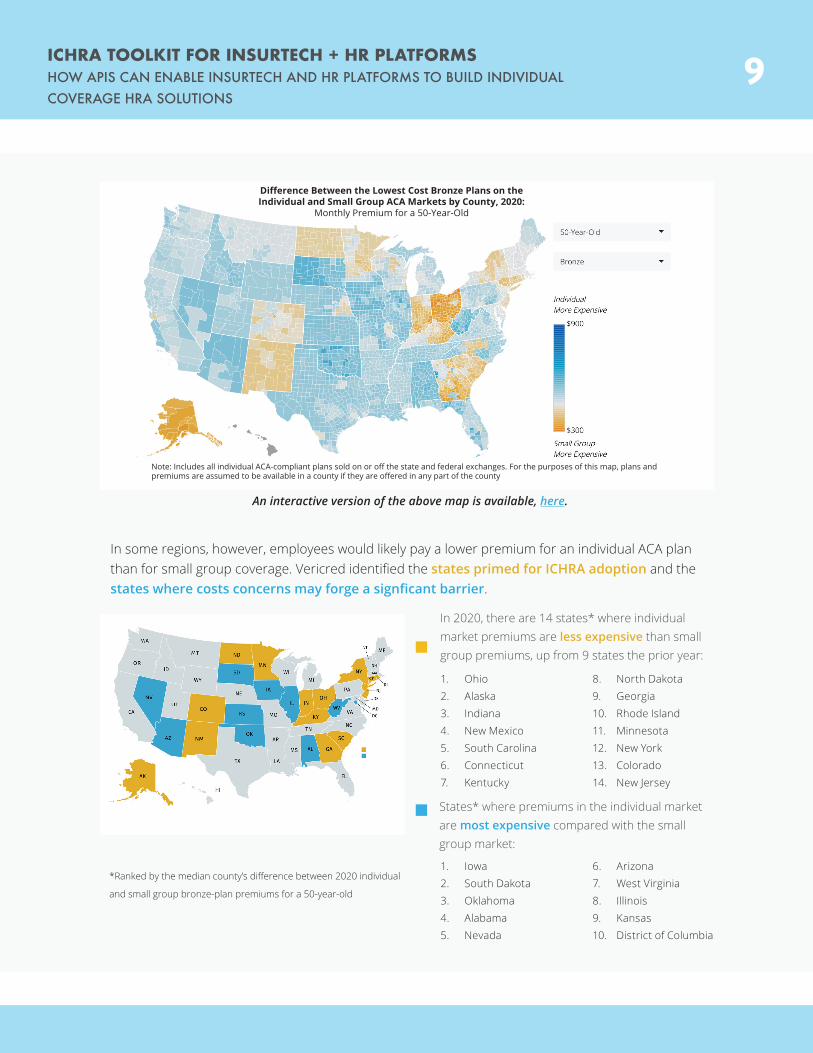

HOW TRANSITIONING TO INDIVIDUAL COVERAGE HRAS COULD IMPACT EMPLOYEES’ PREMIUMSTo uncover whether employees will have access to affordable health plans in the individual market, Vericred analyzed, at the county level, the difference in monthly premiums between the lowest-cost bronze plans in the individual and small group markets.

The data revealed the regions where individual ACA plans are competitively priced compared to small group plans. Such regions are likely more suitable for ICHRA adoption than those where employees would, in most cases, face significantly higher premiums in the individual market.

The lowest-priced bronze plan is more expensive on the individual market, compared with the small group market, in 74 percent of counties. In 46 percent of U.S. counties, a 50-year-old’s premium for the lowest-priced bronze plan would be at least $100 more in the individual market than in the small group market. This forms a potential hurdle that, in certain regions, might limit the number of companies that adopt ICHRAs.

2

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

9

In some regions, however, employees would likely pay a lower premium for an individual ACA plan than for small group coverage. Vericred identified the states primed for ICHRA adoption and the states where costs concerns may forge a signficant barrier.

An interactive version of the above map is available, here.

Difference Between the Lowest Cost Bronze Plans on theIndividual and Small Group ACA Markets by County, 2020:

Monthly Premium for a 50-Year-Old

Note: Includes all individual ACA-compliant plans sold on or off the state and federal exchanges. For the purposes of this map, plans and premiums are assumed to be available in a county if they are offered in any part of the county

In 2020, there are 14 states* where individual market premiums are less expensive than small group premiums, up from 9 states the prior year:

*Ranked by the median county’s difference between 2020 individual

and small group bronze-plan premiums for a 50-year-old

States* where premiums in the individual market are most expensive compared with the small group market:

1. Ohio2. Alaska3. Indiana4. New Mexico5. South Carolina6. Connecticut7. Kentucky

8. North Dakota9. Georgia10. Rhode Island11. Minnesota12. New York13. Colorado14. New Jersey

1. Iowa2. South Dakota3. Oklahoma4. Alabama5. Nevada

6. Arizona7. West Virginia8. Illinois9. Kansas10. District of Columbia

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

10

Cost differences between the individual and small group markets, however, are far from the only factor businesses must weigh in evaluating whether an ICHRA is right for them and their employees. ICHRAs provide employees with plan transportability and greater choice— advantages that are absent among traditional group plans— and should be primary considerations for employers, as well.

WHERE ARE PPO/POS PLANS AVAILABLE IN THE INDIVIDUAL ACA MARKET?The individual market differs from the small and large group markets in more than just premiums.

There are differences in plan design and networks that employers may wish to consider when

evaluating whether an ICHRA is right for them and their employees. The majority of employer-

sponsored coverage offered are PPO (preferred provider organization) or POS (point of service)

plans, but these are less common in the individual market. PPO and POS plans offer some degree

of out-of-network coverage, whereas HMO (health maintenance organization) and EPO (exclusive

provider organization) plans generally do not.

Vericred’s data science team analyzed, at the county level, where an employee switching to the

individual market would have available to them at least one PPO or POS plan.

Which Plan Types Are Available on the Individual ACA Market in 2020?Displaying: PPO and POS

Note: Includes all individual ACA-compliant plans sold on or off the state and federal exchanges. For the purposes of this map, plans and premiums are assumed to be available in a county if they are offered in any part of the county. Catastrophic plans were excluded from this analysis

An interactive version of the above map is available, here.

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

11

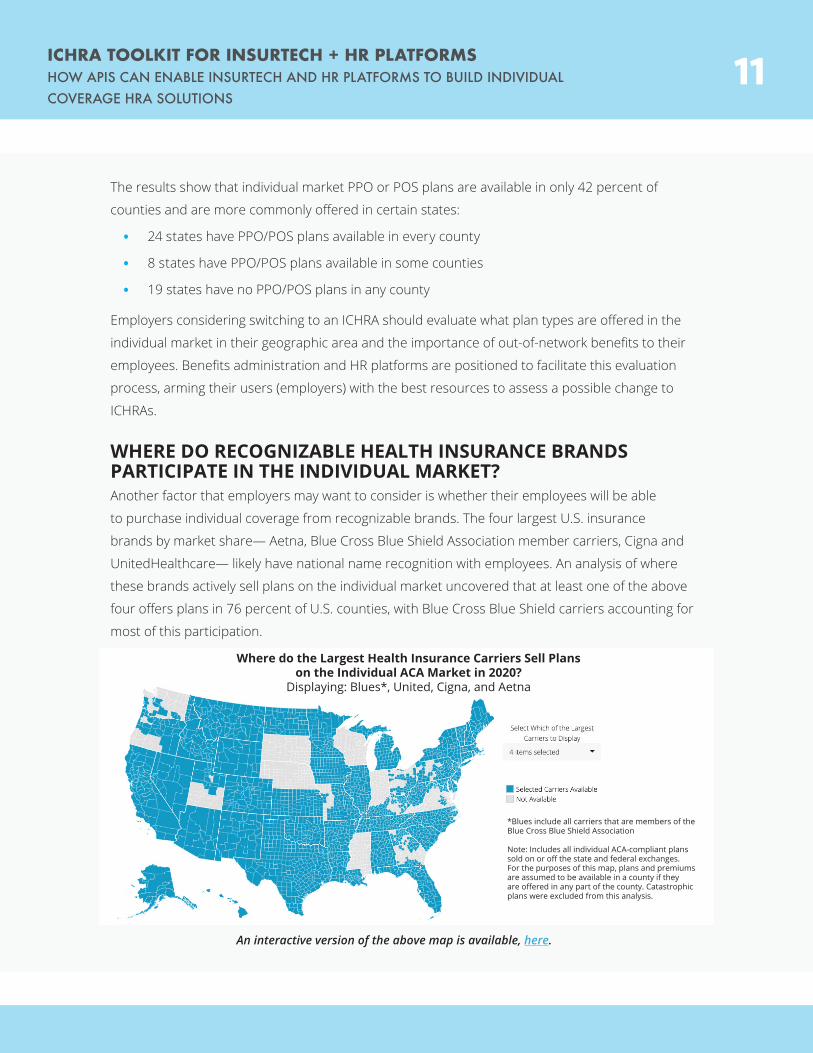

The results show that individual market PPO or POS plans are available in only 42 percent of

counties and are more commonly offered in certain states:

• 24 states have PPO/POS plans available in every county

• 8 states have PPO/POS plans available in some counties

• 19 states have no PPO/POS plans in any county

Employers considering switching to an ICHRA should evaluate what plan types are offered in the

individual market in their geographic area and the importance of out-of-network benefits to their

employees. Benefits administration and HR platforms are positioned to facilitate this evaluation

process, arming their users (employers) with the best resources to assess a possible change to

ICHRAs.

WHERE DO RECOGNIZABLE HEALTH INSURANCE BRANDS PARTICIPATE IN THE INDIVIDUAL MARKET?Another factor that employers may want to consider is whether their employees will be able

to purchase individual coverage from recognizable brands. The four largest U.S. insurance

brands by market share— Aetna, Blue Cross Blue Shield Association member carriers, Cigna and

UnitedHealthcare— likely have national name recognition with employees. An analysis of where

these brands actively sell plans on the individual market uncovered that at least one of the above

four offers plans in 76 percent of U.S. counties, with Blue Cross Blue Shield carriers accounting for

most of this participation.

Where do the Largest Health Insurance Carriers Sell Planson the Individual ACA Market in 2020?

Displaying: Blues*, United, Cigna, and Aetna

Note: Includes all individual ACA-compliant plans sold on or off the state and federal exchanges.For the purposes of this map, plans and premiums are assumed to be available in a county if they are offered in any part of the county. Catastrophic plans were excluded from this analysis.

An interactive version of the above map is available, here.

*Blues include all carriers that are members of the Blue Cross Blue Shield Association

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

12

CVS Aetna, among the most recognizable health insurance brands, offers plans in the employer

market, but no longer actively participates in the individual market.

Blue Cross Blue Shield Association member carriers are the most active of four national carriers

in the individual market offering individual plans across nearly every state. These Blue Cross Blue

Shield carriers also offer small and large group plans.

Cigna offers individual plans in ten states, generally in a small number of counties in and around

high-population metropolitan areas. In 2020, Cigna expanded its individual market presence into

metro areas in three additional states: Florida, Utah and Kansas.

UnitedHealthcare, like Aetna, no longer actively participates in the individual market, but the

insurer has discussed the possibility of adding more individual plans targeted at the ICHRA

audience.

While employees may take comfort in coverages from the well-established brands noted above,

new recognizable brands are emerging in the individual market. Ambetter (Centene), Bright

and Oscar are aggressively marketing themselves as a new generation of health insurance carrier.

Younger employees in particular may be less loyal to the four national brands, embracing these

new carriers.

Employers should consider how important name recognition is for their employees, as many of the

carriers with the largest employer market share have minimal participation in the individual market.

Note: All data as of January 2020

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

13

VERICRED’S DATA SOLUTION: APIS AND THE HRA DEVELOPMENT KITLEARN HOW VERICRED’S APIS ENABLE TECH PLATFORMS TO BUILD DIGITAL SOLUTIONS FOR THE ICHRA MARKET

------------------------------------

The size of the individual market, according to White House estimates, is projected to expand by 50 percent, thereby creating a mandate for InsurTech and HRtech platforms that are currently focused on the group market to offer individual plans as well. By supporting solutions for both plan types, InsurTechs and HRtechs can seamlessly migrate users from group plans to individual plans, therefore retaining customers who would otherwise be forced to shop elsewhere.

Taking a “develop-it-yourself” approach to building these solutions is an expensive, time-consuming drain on resources, as obtaining individual-market plan data from each insurance carrier would be an inefficient process.

Vericred’s HRA Development Kit, a suite of APIs that, with minimal development effort, deliver individual plans and their associated data to your platform. Using Vericred’s structured dataset, inclusive of all individual market plans, technology companies can mitigate the heavy-lifting that would otherwise be required to build and maintain user-facing ICHRA features.

As the only data platform partnered with hundreds of health insurance carriers serving both the group and individual markets, Vericred is uniquely positioned to help tech companies, and their customers, capitalize on changes to HRA regulations.

3

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

14

Vericred’s HRA Development Kit includes the following data solutions:

• Group and Individual Rating APIs, which provide technology platforms with a means to generate quotes in both markets from hundreds of health insurance carriers, thus enabling brokers and employers to evaluate the cost differences between group and individual health plans, and ultimately to enable employees to shop for individual insurance plans.

• Group to Individual Disruption Analysis, which empowers brokers and employers to examine how shifting employees from traditional group plans to individual market plans would impact in-network access to their favored providers.

• Shop by Doctor and Shop by Drug, enabling employees to shop for individual insurance plans based on their preferred doctors and prescription drug requirements.

Together, these solutions power decision support tools that inform employers, directly and through their brokers, as to whether ICHRAs are the right solution for their companies.

For InsurTech and HR platforms that primarily service the group markets, now is the time to implement solutions that help individuals shop for, enroll in and manage individual health insurance plans.

VERICRED’S DATA SOLUTIONSGROUP AND INDIVIDUAL RATING API:Our rating API is among our core offerings, providing technology platforms with a simple, one-to-many connection to generate quotes from thousands of health insurance carriers. By utilizing our API, InsurTech companies can easily add features that enable employees to shop for and enroll in insurance plans.

Vericred’s API documentation provides a detailed look into the power, accuracy and completeness of our individual plan and rate data:

• https://docs.vericred.com/#header-individual-quotes

• https://docs.vericred.com/#major-medical-plans

• https://docs.vericred.com/#major-medical-plans-major-medical-plans-post

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

15

GROUP TO INDIVIDUAL DISRUPTION ANALYSIS:Disruption analysis, traditionally, has been a complex process through which employers and insurance brokers evaluate how the transition to a different group health insurance network would impact employees’ in-network access to their preferred doctors, health systems and hospitals. Analyzing plans in this manner was typically a high-cost and inefficient process. Vericred offers an API that enables InsurTech platforms to build solutions that make disruption analysis more streamlined and automated.

Vericred’s Disruption Analysis API— which empowers users to quickly and dynamically analyze what percentage of employees would be affected by switching networks— isn’t only for comparing group plans. More businesses and insurance brokers will require disruption analysis in 2020, as the Trump Administration’s new policy on HRAs will afford employers another alternative to traditional group plans. During open enrollment, companies can utilize disruption analysis to investigate how switching from a group plan to an ICHRA would impact their employees’ in-network access to their favored providers.

More information about our Disruption Analysis API is available in Vericred’s documentation: https://docs.vericred.com/#networks-networks-post-1

PROVIDER NETWORK DATA / SHOP-BY-DOC:There are hundreds of millions of plan-provider relationships, and these change daily. Our provider-network data includes all details regarding which doctors and facilities participate in-network, creating a “who’s in and who’s out” dataset of all medical and dental plans that are available on the Vericred platform.

For InsurTech and HR platforms planning for next year’s new HRA environment, it’s incumbent upon them to offer employers and employees digital tools to smooth the transition from group plans to the individual market. Vericred’s provider-network data presents a fast, simple way to implement such features ahead of the annual open enrollment period.

As employees are shifted from their company’s group plan and must begin shopping for health coverage on the individual market, they will require information on which available plans include in-network access to their preferred doctors and hospitals. Using Vericred’s provider-network data, forward-thinking tech platforms can effortlessly enable employees to shop-by-doctor, a feature that allows users to evaluate health plan options based on whether specific medical providers are in-network.

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSHOW APIS CAN ENABLE INSURTECH AND HR PLATFORMS TO BUILD INDIVIDUAL COVERAGE HRA SOLUTIONS

16

Vericred’s API documentation affords a more detailed examination into the breadth and completeness of our provider and network data capabilities: https://docs.vericred.com/#header-network-and-provider-data

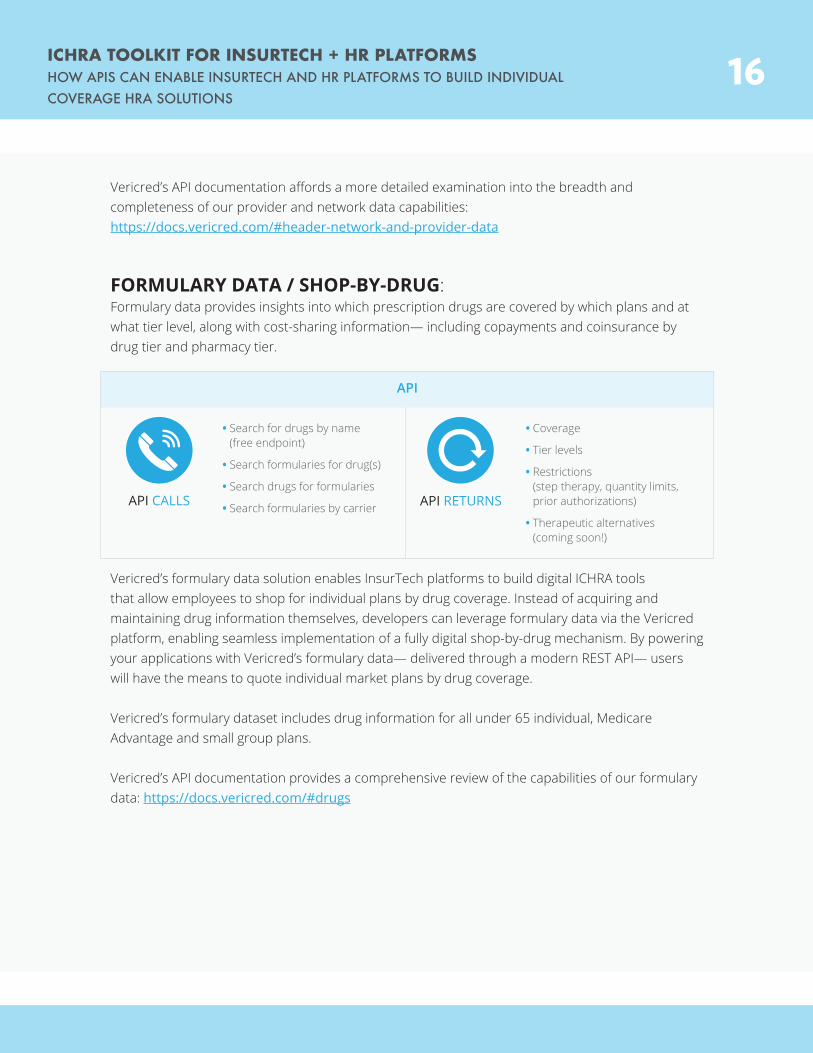

FORMULARY DATA / SHOP-BY-DRUG:Formulary data provides insights into which prescription drugs are covered by which plans and at what tier level, along with cost-sharing information— including copayments and coinsurance by drug tier and pharmacy tier.

• Search for drugs by name (free endpoint)

• Search formularies for drug(s)

• Search drugs for formularies

• Search formularies by carrier

• Coverage

• Tier levels

• Restrictions (step therapy, quantity limits, prior authorizations)

• Therapeutic alternatives (coming soon!)

API CALLS API RETURNS

API

Vericred’s formulary data solution enables InsurTech platforms to build digital ICHRA tools that allow employees to shop for individual plans by drug coverage. Instead of acquiring and maintaining drug information themselves, developers can leverage formulary data via the Vericred platform, enabling seamless implementation of a fully digital shop-by-drug mechanism. By powering your applications with Vericred’s formulary data— delivered through a modern REST API— users will have the means to quote individual market plans by drug coverage.

Vericred’s formulary dataset includes drug information for all under 65 individual, Medicare Advantage and small group plans.

Vericred’s API documentation provides a comprehensive review of the capabilities of our formulary data: https://docs.vericred.com/#drugs

ICHRA TOOLKIT FOR INSURTECH + HR PLATFORMSCONTACT US 17

CONTACT US: GET SET UP WITH A FREE CONSULTATION AND FIND OUT WHETHER VERICRED’S SOLUTIONS ARE RIGHT FOR YOU------------------------------------

Let us consult you on how to best take advantage of the newest changes in the HRA environment.

STEP 1: REACH OUTPlease let us know if you’re interested in learning more, by contacting us at [email protected].

STEP 2: CHECK IT OUT Review Vericred’s Documentation. There’s a lot of handy information here, so you can get

acquainted with the application of our products and stay up-to-date on new releases.

STEP 3: TRY IT OUT Create an account in the Vericred Developer Portal, to gain free access to your API Trial Key.

4

18ICHRA GLOSSARY

ANCILLARY BENEFITS: Employer-sponsored benefits programs that supplement health coverage, such as dental, vision, life and

disability insurance.

APPLICABLE LARGE EMPLOYERS (ALES): Employers that have at least 50 full-time employees. These companies are required to

fulfil the shared responsibility, reporting and minimum essential coverage provisions under the Affordable Care Act (ACA).

CONTRIBUTION LIMITS: Some types of HRAs— EBHRA and QSEHRA— cap the annual amount that employers may allocate to their

employees for eligible HRA reimbursements. For example, under EBHRA rules, businesses may reimburse employees up to $1,800

per year for certain excepted benefits.

DEDUCTIBLES: An established out-of-pocket payment a Medicare enrollee must pay before his or her insurance begins taking over

payment of the particular health care expense.

EMPLOYEE CLASS: A way for businesses to separate employees into groups, by job-based criteria, where within each class, the

business chooses the allowance amount. ICHRA allows businesses to use 11 different employee classes:

• Full-time employees

• Part-time employees

• Seasonal employees

• Temporary employees who work for a staffing firm

• Salaried employees

• Hourly employees

• Employees covered under a collective bargaining agreement

• Employees in a waiting period

• Foreign employees who work abroad

• Employees in different locations, based on rating areas

• A combination of two or more of the above

EMPLOYER DESIGN FLEXIBILITY: The degree to which businesses may customize the terms of an HRA. Some types of HRAs permit

employers to offer varying terms and reimbursement allotments to different classes of employees, while other types do not.

EMPLOYER-EMPLOYEE BENEFITS ARRANGEMENT: An arrangement in which a business subsidizes for its employees— fully or

partially— the cost of a benefit (health, dental, vision, gym membership, etc.)

EXCEPTED BENEFIT HEALTH REIMBURSEMENT ARRANGEMENT (EBHRA): A type of Health Reimbursement Arrangement (HRA)

that allows employers to contribute up to $1,800 per year toward their employees’ expenses that are not covered by their group

plan. Businesses may reimburse employees for expenses such as short-term insurance and dental, vision and home care, among

other eligible costs.

19ICHRA GLOSSARY

EXCLUSIVE PROVIDER ORGANIZATION (EPO): A type of health plan that requires policyholders to use the providers (doctors,

hospitals) within the plan’s network of service providers. EPOs only cover out-of-network in an emergency. EPO plans typically have

lower monthly premiums than PPO plans.

FORMULARY: A list of prescription drugs covered by a prescription drug plan or another insurance plan offering prescription drug

benefits. Also called a drug list.

GROUP AND INDIVIDUAL RATING APIS: These Vericred data solutions provide tech platforms with a means to generate quotes

in both markets from hundreds of health insurance carriers, thus enabling brokers and employers to evaluate the cost differences

between group and individual health plans

GROUP TO INDIVIDUAL DISRUPTION ANALYSIS: A Vericred offering that empowers brokers and employers to examine how

shifting employees from traditional group plans to individual market plans would impact in-network access to their favored

providers

HEALTH MAINTENANCE ORGANIZATION (HMO): A type of health plan that requires policyholders to receive care from providers

(doctors, hospitals, etc.) within the plan’s network of service providers. Under most HMO plans, beneficiaries must select a primary

care physician (PCP), and referrals to specialists must be directed through that PCP.

INDIVIDUAL COVERAGE HEALTH REIMBURSEMENT ARRANGEMENT (ICHRA): A type of Health Reimbursement Arrangement

(HRA) that enables businesses to reimburse employees tax-free for premiums for health insurance purchased in the individual

market.

OFF-EXCHANGE INDIVIDUAL PLANS: Health insurance plans that are purchased outside of government-run, public insurance

marketplaces, either directly from an insurance carrier, via a broker or on a non-government marketplace. Off-exchange plans

include both ACA-compliant insurance and non-ACA-compliant plans.

ON-EXCHANGE INDIVIDUAL PLANS: Health insurance plans that are purchased through government-run insurance marketplaces,

such as the federal exchange, healthcare.gov, and state-managed exchanges. To use a government subsidy, coverage must be

purchased via a public exchange.

OUT-OF-NETWORK COVERAGE: Coverage for medical services that policyholders receive from providers outside of the plan’s

network of doctors, hospitals and facilities. Some types of health plans cover out-of-network providers, while others do not.

OUT-OF-POCKET MEDICAL COSTS: Expenses, paid by the policyholder, that are not reimbursed by insurance. This includes

coinsurance payments, copayments, and deductibles for covered medical care, and costs for services that aren’t covered by the

insurance plan.

POS (POINT OF SERVICE): A type of health plan that incorporates aspects of HMOs and PPOs. Like HMOs, POS plans require

policyholders to select a primary care doctor and receive referrals from that physician as an entryway to specialists and their

services.

20ICHRA GLOSSARY

POS plans cover out-of-network services, but the beneficiary will likely incur a higher coinsurance payment compared with in-

network care.

PPO (PREFERRED PROVIDER ORGANIZATION): A type of health plan which gives policy holders an incentive to use the providers

(doctors, hospitals) within the plan’s network of service providers. In return, the plan pays a higher percentage of health care

expenses. Out-of-network care is also covered, albeit with higher out-of-pocket costs (this is in contrast to a plan like an HMO, which

generally won’t cover out-of-network costs at all).

PREMIUMS: The periodic payment to Medicare, an insurance company, or a health care plan for health or prescription drug

coverage.

PREMIUM TAX CREDIT (PTC) INTERACTION: Premium tax credits (PTC) help eligible individuals and families afford on-exchange

health plans by providing income-based refunds for monthly premiums. PTCs interact with various types of HRAs in different ways.

If the employee is offered an ICHRA that is considered affordable, based on their income, they are not eligible for a PTC. If, however,

the ICHRA allotment is not affordable, the employee can choose to receive the PTC instead.

PROVIDER NETWORK DATA: There are hundreds of millions of plan-provider relationships, and these change daily. Vericred’s

provider-network data includes all details regarding which doctors, providers and facilities participate in-network, creating a “who’s

in and who’s out” dataset of all medical and dental plans that are available on the Vericred platform.

QUALIFIED SMALL EMPLOYER HEALTH REIMBURSEMENT ARRANGEMENT (QSEHRA): A type of HRA that enables small

businesses (less than 50 employees) to reimburse their employees for premiums and eligible healthcare expenses. These HRAs

have contribution limits, must offer all employee classes the same terms and cannot be used for ancillary benefits like dental, vision,

etc.

SHOP BY DOCTOR AND SHOP BY DRUG: Functionalities that enable users to shop for insurance plans based on their preferred

doctors and prescription drug requirements.

SHORT-TERM INSURANCE: A type of health plan that provides beneficiaries with temporary medical coverage. These plans are not

required to fulfil Affordable Care Act regulations, and coverage varies considerably across short-term plans.