Embed Size (px)

Citation preview

INDIA INVESTMENT CONFERENCE 2014 THE ROAD AHEAD FOR INDIA AND EMERGING

ECONOMIES

17 January 2014

Taj Lands End

Mumbai, India

Page 2

India Investment Conference - 2014

Disclaimer: Please note that the content of this note should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or Indian Association of Investment Professionals. This is a collation of proceedings of

the India Investment Conference 2014 and CFA Institute publications on India for private briefing circulation amongst IAIP members. Some of the material may be protected by copyrights and may require prior owner permission for reproduction.

Page 3

India Investment Conference - 2014

Contents

Inaugural Session .......................................................................................5

The End of Quantitative Easing, the Outlook for Emerging Economies &

Rupee ........................................................................................................9

Corruption of Capitalism – Challenges to Sustainable Growth & Asset

Allocations............................................................................................... 11

Future of Finance – Key Issues Facing the Finance Industry........................ 15

A Changing Global Energy Landscape – Implications for India .................... 18

India Investment Outlook – Panel Discussion ............................................ 21

Select India Specific Publications by CFA Institute ..................................... 24

Page 4

India Investment Conference - 2014

The fourth India Investment Conference held on January 17th 2014 at

Mumbai, was yet again received with enthusiasm by the members. It had

plenary sessions by distinguished speakers like Avinash Persaud (Chairman,

Elara Capital and Intelligence Capital and adviser to India’s FSLRC), Richard

Duncan (Chief Economist, Blackhorse Asset Management), Frederic Lebel,

CFA (Co-CEO of OFI MGA and owner of HFS Hedge Fund Selection S.A. and

Planning Committee Chair of CFA Institute Board of Governors) and Dr.

Fereidun Fesharaki (Chairman, FGE) in that order. The last session was the

panel discussion on investment in Indian markets with illustrious market

experts like Samir Arora (Founder, Helios Capital), Manish Chokhani (MD,

Alliance Holdings), Abhay Laijawala (Head of India Equities Research at

Deutsche Bank), and Jayesh Mehta (MD & Country Treasurer, Bank of

America (India)). Each of the session was moderated by yet another set of

reputed professionals like Navneet Munot, CFA (Director IAIP & CIO SBI Funds

Management), Sandeep Sabharwal, CFA (Senior Director Capital Markets,

CRISIL Research), Paul Smith, CFA (MD, APAC, CFA Institute) Namit Arora, CFA

(Vice President IAIP and Director, Standard Chartered Private Equity) and

Sunil Singhania, CFA (CIO Equity Investment, Reliance Capital and member of

Board of Governors at CFA Institute) respectively.

The welcome and inaugural addresses were made by Paul Smith, CFA (MD

APAC, CFA Institute), Jayesh Gandhi, CFA (President, IAIP and ED, Morgan

Stanley Investment Management, India) and Vikram Kuriyan, CFA (Director,

Centre for Investment at ISB). Anil Ghelani, CFA (Director, IAIP and Business

Head & CIO DSP Blackrock Pension Funds) was the conference moderator.

Vidhu Shekhar, CFA (Consultant, CFA Institute) closed the conference with a

vote of thanks.

CFA Institute, ISB (Indian School of Business) and IAIP were the host of the

events. NiSM was the knowledge partner. Sponsors include Factset, Stoxx,

BSE and NSE as Gold Partners and S&P Capital IQ as Silver Partners. Exhibitors

include Morningstar and Thomson Reuters. Supporting Partners include

Ambit, DSP BlackRock and Reliance Mutual Fund.

Page 5

India Investment Conference - 2014

Inaugural Session

Write-up Credit : Priyank Singhvi, CFA and Chetan Shah, CFA, Director IAIP & Senior

Portfolio Manager, Religare Invesco AMC

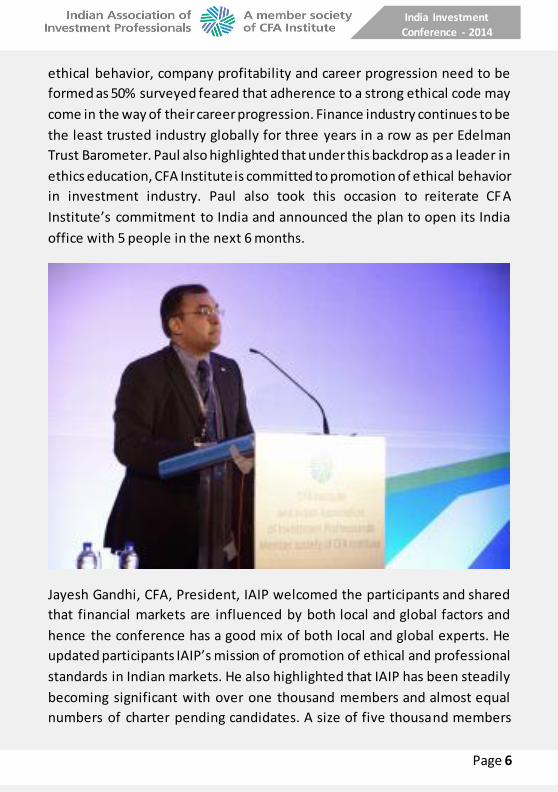

In the Inaugural address, Paul Smith, CFA updated the audience that CFA

Institute’s members’ outlook on India’s economic growth is most positive in

the entire non-Japan Asia1. However, he reminded the audience on need for

a stable source of financing to achieve this growth and highlighted the role of

channelization of India’s domestic savings in productive investment for

achieving sustainable economic growth. He also touched upon the findings by

Economist Intelligence Unit wherein it found that ethical behavior needs to

be encouraged by the senior executives and top management and linkages in

1 CFA Institute’s Global Market Sentiment Survey 2014 can be found here:

http://www.cfainstitute.org/about/research/surveys/Pages/global_market_sentime

nt_survey.aspx?WPID=Strategic_Home&PageName=Homepage

Page 6

India Investment Conference - 2014

ethical behavior, company profitability and career progression need to be

formed as 50% surveyed feared that adherence to a strong ethical code may

come in the way of their career progression. Finance industry continues to be

the least trusted industry globally for three years in a row as per Edelman

Trust Barometer. Paul also highlighted that under this backdrop as a leader in

ethics education, CFA Institute is committed to promotion of ethical behavior

in investment industry. Paul also took this occasion to reiterate CFA

Institute’s commitment to India and announced the plan to open its India

office with 5 people in the next 6 months.

Jayesh Gandhi, CFA, President, IAIP welcomed the participants and shared

that financial markets are influenced by both local and global factors and

hence the conference has a good mix of both local and global experts. He

updated participants IAIP’s mission of promotion of ethical and professional

standards in Indian markets. He also highlighted that IAIP has been steadily

becoming significant with over one thousand members and almost equal

numbers of charter pending candidates. A size of five thousand members

Page 7

India Investment Conference - 2014

doesn’t look too far. He also apprised the participants about the current twin

focus areas of IAIP of continued education and networking and various

activities carried by IAIP:

Over sixty speaker events across seven cities in India with local and

international experts

Continued engagement with key regulators like SEBI, RBI, Ministry of

Finance etc. in areas of advocacy and for promotion of ethics

Annual equity research challenge which now covers around 40

leading business schools and in addition to imparting technical

knowledge also attempts to instil ethical values in the participants

Access scholarships – last year 250 access scholarships were given

covering almost one in every four candidates, etc.

Jayesh also updated that all these activities have been managed on an

entirely voluntary basis and taken the occasion to thank the key 30-40

volunteers across India for their continued support. He highlighted that India

is now the third largest in terms of number of CFA candidates and welcomed

the CFA Institute’s move to open an office in India to be able to better serve

the candidates and members.

Page 8

India Investment Conference - 2014

Vikram Kuriyan, CFA, informed the participants on ISB’s centre for investment

and its labs in areas of (i) investments, and, (ii) risk and governance. Based on

the research performed in the investment lab he emphasised the need for

diversification of portfolios including access to global products for Indian

investors. He highlighted that though in times of crisis correlations in markets

significantly increase but in the long run a globally diversified portfolio turns

out to be the most optimum. Ironically, global pension funds invest into

Indian equities while its own pension funds don’t do it. Job of the

professionals is to develop products that truly add value to the society and

that’s the road ahead for India’s investment professionals .

Page 9

India Investment Conference - 2014

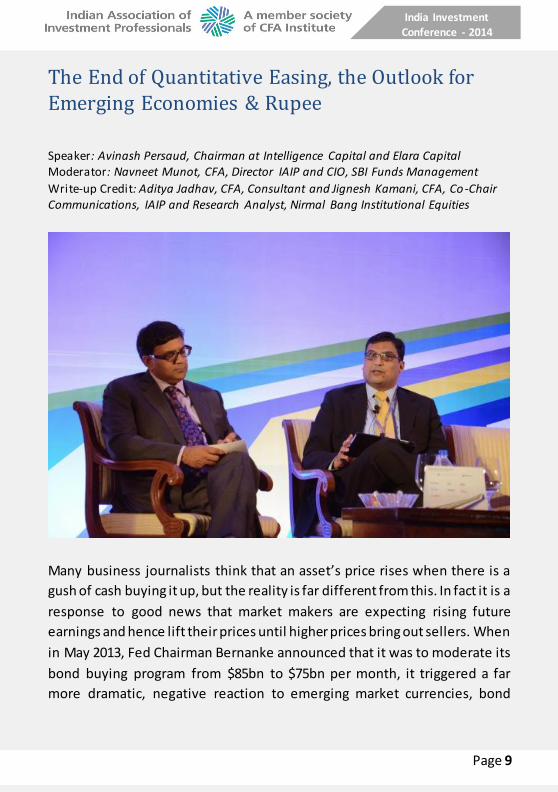

The End of Quantitative Easing, the Outlook for Emerging Economies & Rupee

Speaker: Avinash Persaud, Chairman at Intelligence Capital and Elara Capital Moderator: Navneet Munot, CFA, Director IAIP and CIO, SBI Funds Management

Write-up Credit: Aditya Jadhav, CFA, Consultant and Jignesh Kamani, CFA, Co-Chair Communications, IAIP and Research Analyst, Nirmal Bang Institutional Equities

Many business journalists think that an asset’s price rises when there is a

gush of cash buying it up, but the reality is far different from this. In fact it is a

response to good news that market makers are expecting rising future

earnings and hence lift their prices until higher prices bring out sellers. When

in May 2013, Fed Chairman Bernanke announced that it was to moderate its

bond buying program from $85bn to $75bn per month, it triggered a far

more dramatic, negative reaction to emerging market currencies, bond

Page 10

India Investment Conference - 2014

markets suggesting that this is the final phase of the stock market rally and it

will spark renewed pressure on the rupee.

Persaud is of opinion that asset prices have risen from rising future earnings

being discounted to the present by a near zero level of interest rate policy,

which started in 2008 post collapse of Lehman Brothers. He also cited that

the future of market has little to do with the reversal of Quantitative Easing

(QE), as QE has merely played the role of interest rate signal and its taper

should be seen as a signal to communicate with the bond markets that the

interest rate cycle is reversing. Federal Reserve mere acted as a buyer of last

resort in 1st round of QE in 2008, when it started buying bonds from the

public to defrost the frozen bond market and till now it has created $5trn out

of thin air.

Later rounds of QE were larger, focused on long dated bonds with an

expectation that banks would use this cash to buy long term corporate bonds

encouraging corporations to finance new investment. Far from wanting to

invest their cash in real economy, banks and corporates have been hoarding

it. According to the U.S. Federal Reserve Flow of Funds Accounts, non-

financial corporate businesses held an unprecedented $1.8trn of liquid assets

at the end of 2012 and corporate private investment is still lower than 2008

level. Cash balances have been trapped in a broken system and actual cross

border flows were no greater than before. To prove his point Persaud also

cited that foreign asset ownership by central bank of countries offering QE is

just 17% of emerging market’s assets.

But it doesn’t bring any respite to Indian rupee, as the dollar will enter a

cyclical upturn and rupee will come under renewed downward pressure. But

the headwinds against rupee may be mitigated if Indian economy rebounds

backed by the growth of domestic consumption industry.

The webcast of the session is available at:

http://new.livestream.com/livecfa/Persaud

Page 11

India Investment Conference - 2014

Corruption of Capitalism – Challenges to Sustainable Growth & Asset Allocations Speaker: Richard Duncan, Chief Economist, Blackhorse Asset Management Moderator: Sandeep Sabharwal, CFA, Senior Director, Capital Markets, CRISIL

Research Write-up Credit: Priyank Singhvi, CFA and Jignesh Kamani, CFA, Co-Chair Communication, IAIP and Research Analyst, Nirmal Bang Institutional Equities

In the 19th century business men invested their capital into enterprises,

made profits, saved and reinvested their money back into the business and in

the process built their capital. Economic growth was driven by investment

and savings. Now it is driven by credit creation and consumption. Capitalism

has evolved into ‘Creditism’ and has been corrupted. With this background

Richard Duncan showed how credit has been driving GDP growth since 1980s,

why the quarterly credit needs to grow at real rate of 1.8% in the US to just

Page 12

India Investment Conference - 2014

stay out of recession and why he expects QE to stay in the one form or the

other in 2014 & 2015.

During gold standard Fed 25% of the reserves were backed by gold. In 1968

the US broke the link between money and gold. With constraints removed

total credit or debt has exploded from around $1.0trn to $50trn in 2007 and

$58trn currently. The total credit to GDP ratio has increased from 150% in

1964 to 360% in 2012. Richard analyzed this into key sectors viz. households,

corporates, federal government, government sponsored enterprises (GSEs)

and ABS issuers. He mentioned that government budget deficit was in excess

of $1trn / year from 2009 to 2012, driving credit growth which helped US

from collapsing. However budget deficit declined to $680bn in 2013 and

expected to decline further which would impact credit growth in the US.

Based on credit growth in each individual sectors, Richard forecasts total

credit growth of 3.2%/3.8%/3.8% for CY13/CY14/CY15 respectively. Assuming

inflation of 1.5% for CY13 and 2% for CY14/CY15, he got credit growth after

inflation of 1.7%/1.8%/1.8% for CY13/CY14/CY15 respectively which is still

below 2%, recession threshold.

Another analysis of total credit growth and GDP growth (adjusted for

inflation) during 1952-2012 also concluded that every time credit grew by

less than 2% it was followed by a recession. In line with these findings, for US

to come out of recession, its credit growth has to be more than 2% or $2.3trn

in 2014. Total credit growth has turned positive in the past few quarters but

total credit growth at $1.84trn is lower than $2.3trn. As a result, Richard

believes more QEs is likely to be required.

Richard mentioned that the global economy is like a big rubber raft, but one

inflated with credit instead of air. The raft is defective as global debt has

expanded to such an extent that the income of the world’s population is

insufficient to service it. As the raft is defective and the credit is leaking out

through numerous holes as it is destroyed by defaults, so the raft’s natural

tendency is to sink. Without more government borrowing, spending and

printing, the raft will sink.

Page 13

India Investment Conference - 2014

Richard also checked possibility of tapper off through liquidity gauge.

Liquidity gauge is creation of liquidity (by Fed) less absorption of liquidated

(due to current account deficit). Last year $1trn was created by Fed but

$700bn was absorbed due to budget deficit, resulting liquidity gauge of

$300bn, which resulted into 30% increase in stock market. Based on the Fed’s

taper schedule, the liquidity gauge would become negative (liquidity drain) in

Q3 2014 onward. The liquidity drain beginning in Q3 2014 would push up

interest rates and cause a new recession. Hence, Richard expects the taper

schedule to be revised and QE expanded into 2015. Richard expects between

$500bn and $1trn of QE both in 2014 and 2015. As per Richard, quantum of

liquidity created by Fed will be such that it increases stock market by 10-15%

and housing market by 7% so that the wealth effect led economic activity

continues.

The US current account deficit (‘CAD’) used to be the driver of global

economic growth. Till 1982 US CAD was close to zero, from 1992 it expanded

continuously to $800bn in 2006 and drove growth in global economy. US was

financing its CAD with fiat money, in form of US$ denominated bonds. As the

crisis started US economy started importing less, which impacted global

demand. The US CAD continues to show a contracting trend due to various

reasons like reduced economic activity, reduced oil imports with discovery of

shale gas, etc.

On China Richard mentioned that moderating growth in imports from China,

which will reduce growth in China. China has created excess capacities and

stock piles that can’t be optimally used, because US and UK are not buying

and China can’t consume locally due to low average income. Linked to that,

he also shared his concerns on the potential NPA issues in China.

Richard expressed his concerns that the money that is being created is largely

used for non-productive purposes and suggested that US needs to explore

options to invest money in real economy and programs focused on new

technologies like nano-tech, etc. Drawing parallels with the Industrial

revolution some 200 years ago, he suggested increase in real wages across

Page 14

India Investment Conference - 2014

countries to fix the problems of the global economy. This could be by way of

some minimum global wages for manufacturing and increasing the same by

small amount every year. This will distribute more money into the hands of

common man and lead to growth in consumption.

Page 15

India Investment Conference - 2014

Future of Finance – Key Issues Facing the Finance Industry Speaker: Frederic Lebel, Co-CEO, OFI MGA and Owner HFS S.A. and Member of the Board of Governors, CFA Institute

Moderator: Paul Smith, CFA, MD, APAC, CFA Institute Write-up Credit: Chetan Shah, CFA, Director, IAIP and Senior Portfolio Manager, Religare Invesco AMC

According to the Edelman Trust barometer, the financial services industry is

the least trusted industry globally with a score of 46% and banks having score

of 49%. Even chemicals and pharmaceutical industries perceived to be

hazardous or less compliant of quality standards are better placed with 51%

and 57% respectively. Technology and consumer electronics manufacturing

industries have the highest scores of 73% and 70%. So what could be the

reason for such low level of trust for financial services industry, which has

been at the bottom for three consecutive years? Some of the words for the

Page 16

India Investment Conference - 2014

industry which come out of consumers’ mind are corrupt, greedy, crooks,

bad, street money etc.

So what could be done to improve and win back the trust of investors and

clients? Frederic P. Lebel, CFA, Member of the Board of Governors, CFA

Institute very lucidly explained through his presentation what all the people

in the investment profession should do and what all CFA Institute is doing

through its various projects under Future of Finance (FoF)? The FoF topic

areas include 1) putting investors first or acting in the fiduciary capacity to

protect investors’ interests, 2) empowering investors with Financial

Knowledge to make better decisions, 3) Safeguarding the system, 4)

enforcing Regulation to protect investors and preserving capital market

integrity, 5) bringing Transparency & Fairness by promoting open and honest

financial system and 6) providing Retirement Security through sensible

solutions to protect pension systems worldwide.

Citing the results of the Global Market Sentiment Survey 2014, members

have pointed out that improving the culture of the organisation by senior

executives, adherence to the ethical code, improved compensation practices,

clarification on fiduciary responsibilities, increasing staff training & education

are the measures to be implemented to win back investors. The Edelman

2013 investor trust study conducted in the developed markets highlights

investment managers/advisors acting in client’s best interest as the single

most important attribute by the investors while selecting one. Second and

third most important attributes were achieving more returns and

commitment to ethical conduct. Fees were the last in their list of the

parameters while selecting investment manager.

Frederic also pointed to the cost of failure of trust as well. Investors who do

not trust the industry are unlikely to save and invest for their future and

hence unlikely to achieve their long term financial objectives. This may l ead

to “savings gaps” which in-turn will lead to longer working lives, lower quality

of life and inter-generational stress.

Page 17

India Investment Conference - 2014

CFA Institute with around 140 societies worldwide and its 120,000 members

globally has been a champion of ethics for the last 52 years. On its 50th

anniversary it released list of simple things to be done by investment

professionals to win back and restore trust.

To know more about Future of Finance kindly click on the following URL:

http://www.cfainstitute.org/learning/future/Pages/index.aspx. Follow it

on Twitter at #FutureFinance

Page 18

India Investment Conference - 2014

A Changing Global Energy Landscape – Implications for India

Speaker: Dr. Fereidum Fesharaki, Chairman, FGE

Moderator: Namit Arora, CFA, Vice President & Director IAIP and Director Standard

Chartered Private Equity

Write-up Credit: Chetan Shah, CFA, Director IAIP and Senior Portfolio Manager,

Religare Invesco AMC

Dr. Fesharaki mesmerized the participants with his sharp & frank insights on

the oil & gas sector around the globe and India in particular. These included

his views on oil & gas prices, incremental sources of demand & supply, India’s

antiquated oil policy, NELP (New Exploration Licencing Policy), shale gas

revolution, refineries and so on. Both on lighter and serious note he noted

the key factors determining crude oil prices – God, Saudi and Oil market in

that order with the last having lowest denominator. FGE has 20 year

forecasts of crude oil price (Brent) within the band of $80 to $120 per barrel

Page 19

India Investment Conference - 2014

initially falling to lower end by 2016-18. The market forces are allowed to

play between this range; broadly agreed by the big forces viz. Saudis and the

US. If the oil prices go above $120 bad things happen such as consumer

backlash, fall in demand etc. If it goes below $80 it will result into closure of

non-conventional sources of energy, fall in budget for oil producing

governments etc. It seems there is a general consensus between consumers

& producing governments that Brent prices of $100-$110 per barrel are okay.

Else why would the oil price remain the same over the last 2-3 years despite

serious changes like Libya going out initially and coming back, and ban

imposed on Iran oil (1.0mn barrels per day). Saudi has successfully played a

significant balancing role increasing or decreasing production by a million

barrels and containing the same within the range of 8mn to 10mn barrels per

day.

India’s 10th NELP is a failed policy as nobody bids except for ONGC because of

the antiquated oil policy wherein the subsidy burden is borne by the

upstream resulting into net payment of only $40-45 per barrel by the state.

Multinational companies are not interested in India’s oil. There are many

other countries, which are more inviting & attractive than India. However,

there have been few attempts & announcements to correct the policies

including subsidy sharing burden but whether the government will do this

before its term remains to be seen. Likewise gas prices will be doubled to

$8.0-$8.5 per mnBTU w.e.f. from April 1st. ONGC will be the biggest

beneficiary of this increase. GSPC has been asking for the price of $16 per

mnBTU. It is a misconception that LNG from the US is cheap. The cost of

liquefaction, transportation, and infrastructure are very high. Besides, there

is excessive taxation in India resulting higher prices for industrial consumers.

Nearly 20GW of gas based power plant are not running due to non-

availability of gas, which in turn is due to wrong gas pricing policy.

Currently, the private sector refineries export most of their refined products

with Reliance Industries forming 90% of the exports and Essar Oil 10%. The

domestic prices are not remunerative due to subsidies on diesel. However, if

Page 20

India Investment Conference - 2014

crude prices fall to levels of $80/bbl then the subsidies go to zero and

marketing products in the domestic market may become lucrative for the

private refiners.

The chairman of public sector oil marketing companies in India having the

term of 3 years and they have the tendency to announce and set up new

refineries as a “claim to fame”. India doesn’t need additional refining capacity

and fortunately its appetite for building new ones has dropped. Coal is

making a comeback in Europe, Australia and Japan. India will have to

compete with other countries for the same. Though it has huge reserves the

same has not been unlocked efficiently.

Answering to question on China versus India, Fereidum said that in China

government works for the state oil companies. Oil companies retain profits

and are allowed to take their own investment decisions like acquisitions of oil

fields with substantially higher limits ($50bn) with little questions from

government or press. The Indian oil companies have to get government

approval beyond $900mn (as in case of OVL) and by the time they get it

Chinese companies have already bought the asset.

It is not that shale gas is only available in the USA. China has highest reserves

in the world but there are challenges in extracting the same. These include

the fact that the gas is dry, lack of enough water for fracking, small earth

tremors on account of fracking disturbing the birds (like hen not laying eggs),

investment in pipelines which pass through farmlands etc. The cost of

production is much higher than importing. In the USA shale gas has been a

revolution as it is in areas with little habitation, it has well developed markets

(including paper/forward markets) and infrastructure in place to support.

These fields were owned by number of independent players. Multinational

companies like Exxon have bought them later and might have 10% of the

assets.

The webcast of the session is available at:

http://new.livestream.com/livecfa/Fesharaki

Page 21

India Investment Conference - 2014

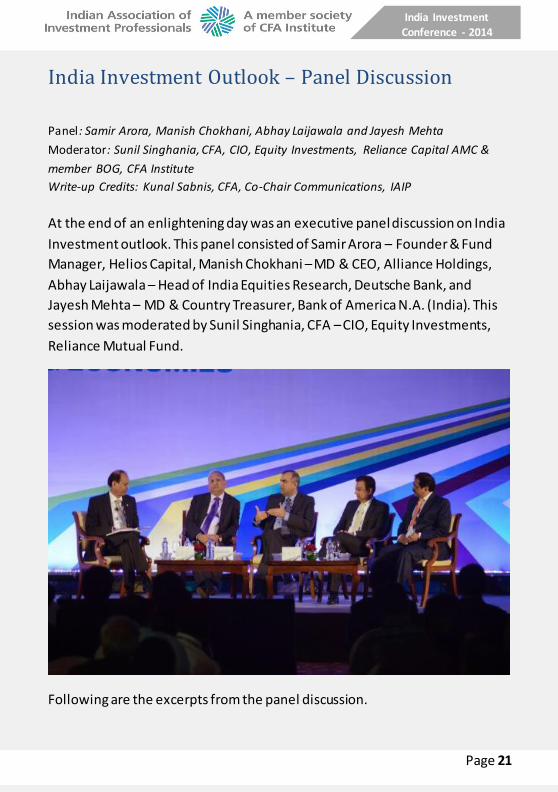

India Investment Outlook – Panel Discussion

Panel : Samir Arora, Manish Chokhani, Abhay Laijawala and Jayesh Mehta

Moderator: Sunil Singhania, CFA, CIO, Equity Investments, Reliance Capital AMC &

member BOG, CFA Institute

Write-up Credits: Kunal Sabnis, CFA, Co-Chair Communications, IAIP

At the end of an enlightening day was an executive panel discussion on India

Investment outlook. This panel consisted of Samir Arora – Founder & Fund

Manager, Helios Capital, Manish Chokhani – MD & CEO, Alliance Holdings,

Abhay Laijawala – Head of India Equities Research, Deutsche Bank, and

Jayesh Mehta – MD & Country Treasurer, Bank of America N.A. (India). This

session was moderated by Sunil Singhania, CFA – CIO, Equity Investments,

Reliance Mutual Fund.

Following are the excerpts from the panel discussion.

Page 22

India Investment Conference - 2014

Samir Arora – Founder & Fund Manager, Helios Capital

In the aftermath of the many scams in the UPA II tenure, policy paralysis

crept in as many bureaucrats and ministers were sceptical to take decision

owing to higher scrutiny. The only way to kick start investments again is that

either Prime Minister or any other very senior minister should take the

responsibility of the decisions taken by the cabinet. Samir dashed the general

pessimism that markets will correct since they are trading at the all time

highs. He pointed out that markets have barely reached the level which they

were at six years ago. In the current uncertain times stocks with consistent

earnings growth will continue to do well. There has been an increasing

interest amongst FIIs about India but elections which can change the policy

dynamics drastically will add to the uncertainly. Samir favours the midcaps

stocks which he believes will outperform the large caps but e ven amongst

large caps there are certain stocks which are very attractive on risk adjusted

basis. 80% of his portfolio is in the long term growth stocks while the

remaining is in short term momentum ideas and is currently bullish in the US

IT stocks.

Manish Chokhani – MD & CEO, Alliance Holdings

The government consistently raised the expectations which got eroded each

time leading to increasing pessimism in the economy. With bottoming growth

and peaking inflation, Manish believes that domestically things are changing.

Sectors such as Pharma, FMCG, IT, Telecom, Media which have limited

correlation to the real economy, have done well over the past couple of

years. The next rally is expected in the cyclical sectors which are closely

linked to the real economy. He believes that Real assets are preferred in the

times of higher inflation since their value keeps in increasing. For example,

the cost of setting up an average cement plant was INR 650 mn in 1980s

which has increased to INR 7.5 bn today. He bel ieves that people aged in

their 40s make the best entrepreneurs and with the many industrial houses

having 40 year olds at the helm, makes him hopeful that things will improve

from here on. Foreign money is highly concentrated in top 20-30 stocks

Page 23

India Investment Conference - 2014

which leave open the scope to invest in the next 30-50 stocks which have

higher delta as well as are attractively priced.

Abhay Laijawala – Head of India Equities Research, Deutsche Bank

Most of the funds invested by FIIs in the letter half of 2013 came through the

ETF route and hence were concentrated in stocks with higher earning

visibility and growth. Active money will return to the Indian markets which

will be a big positive. QE taper by the US Fed is likely to accelerate which will

keep rupee volatile. Emerging market currencies will be distinguished based

on the ability of their central banks to internally strengthen and perform.

Abhay expects Sensex earnings growth to be 14-15% in FY15 based on

broader recovery while consumer sector will underperform as compared to

cyclical sectors. The only risk for this expectation is the delay in the turning of

economic fundamentals.

Jayesh Mehta – MD & Country Treasurer, Bank of America N.A. (India)

Inflation will trend downwards and Interest rate will follow. Rupee

depreciated the most in the months of June and September when FII flows

were negative mainly in debt segment. Jayesh feels that the Fed taper fears

are blown out of proportion and doesn’t expect much volatility henceforth.

Questioning the widely accepted belief that fed taper has led to money being

pulled out of debt securities, he said that foreign debt investors have not

pulled out investments from India whereas others who look for arbitrage

opportunities, lock in a spread and hence are neutral towards currency

movements. Long term bonds are preferable since shorter end of the yield

curve lacks liquidity and doesn’t permit building a portfolio. He is of a firm

view that unless government takes hard decisions, rupee is unlikely to

strengthen.

Page 24

India Investment Conference - 2014

Select India Specific Publications by CFA Institute

Here are links to select thought provoking publications from CFA Institute in

context of India:

Special Reports and Articles

Is Corporate India Healthy?

As we continue our special coverage of India, it becomes important to ask the

obvious. How are Indian companies doing? For that, we turn to the chief

investment officer of SBI Mutual funds, Navneet Munot, CFA. Listen or read

on to hear our discussion…

Building an India Resistant to Currency Shocks and Inflation

Inflation, currency shocks, and their unequal impact on the Indian population

as a whole have been brought up repeatedly in this week’s coverage of India.

In part one of a two-part interview with Pradip Shah, the founding managing

director of Crisil, Chairman at IndAsia Fund Advisors, and a board member at

several India-based companies.

Corporate Governance in India: The Rise of the Minority Shareholder

It was heartening to see in a recent edition of the Economic Times that the

Securities and Exchange Board of India (SEBI) would likely discuss an overhaul

of its corporate governance code at a board meeting the next day. Although

it is too early to know whether the SEBI board ultimately discussed the code

at the meeting, it is clear based on SEBI’s Consultative Paper on Review of

Corporate Governance Norms in India that there is a discernible shi ft towards

empowering shareholders to take management to task on corporate affairs…

Page 25

India Investment Conference - 2014

Understanding India's Economy and Capital Markets: Past, Present, and

Future

Satyajit Das, former banker and author of Traders, Guns, and Money, and

Extreme Money, discusses and assesses India's recent reform efforts. Mr. Das

examines the key issues for its economy, its capital markets and foreign

direct investment. Additionally, he discusses policies from a current and

historical perspective compared to China, while reviewing the outlook going

forward in light of lessons learnt from the global financial crisis in this Take 15

series…

India Education and Economic Growth

Indian government’s focus on education reform and economic expansion not

only may help the country recognize its potential to become an economic

power but also will facilitate the CFA Institute mission in that market.

Leading from Behind!

With such strong prospects, why are emerging markets slumping so badly?...

India : Codes, Standards, and Position Papers

Standards and practices can differ dramatically throughout the world’s

financial markets, and shareowners must know their rights in the markets

where they invest. Shareowner Rights across the Markets is designed to

provide shareowners a clear understanding of their rights, current practices,

recent developments, and legal and regulatory frameworks in 28 jurisdictions

around the world…

Page 26

India Investment Conference - 2014

CFA Digest Summaries

India’s Opportunities in Tomorrow’s World

India’s rapidly growing population will not automatically translate into a

demographic dividend. The country must address its underperforming

educational system and the threat of losing unskilled jobs to robotics. India

can succeed by leveraging its low-cost labor force and strategically

positioning itself as a global provider of high-quality goods to affluent

consumers…

Start Me Up!

Prospects for a revival of India’s economy are unclear. It appears that the

measures being taken by India’s government are geared toward keeping the

economy afloat, but deep-rooted reforms will have to wait until after the

elections in 2014.

Is China or India More Financially Open?

Because of the current and potential sizes of China’s and India’s economies,

the world has a huge stake in the integration of their financial systems into

global markets. The authors use various measures to examine the absolute

and relative openness of these two economies. They challenge the popular

measures that suggest that China and India restrict capital flows to a similar

extent and that rank China as a more open economy than India…

The Truth about Gold: Why It Should (or Should Not) Be Part of Your Asset

Allocation Strategy

Most arguments for holding gold in a portfolio are not supported by an

analysis of the data. Nonetheless, an argument can be made for including

gold as a commodity in a well-diversified portfolio, particularly if investors

and central banks increase their demand—even moderately—for gold…

Page 27

India Investment Conference - 2014

The Information Content of Stock Markets around the World: A Cultural

Explanation

The information content of stock markets seems to be higher in countries

with investors who are more individualistic and less likely to avoid

uncertainty. The authors explore whether these differences in information

content are the result of cross-country cultural differences…

Page 28

India Investment Conference - 2014

IIC14 is also covered at

Twitter #IIC14

Facebook http://www.facebook.com/CFAInstitute

CFA Institute Blog http://blogs.cfainstitute.org/investor/2014/01/22/roundup-

india-investment-conference-the-road-ahead-for-india-and-

emerging-economies/

IAIP Blog http://iaip.wordpress.com/category/events/india-investment-

conference/