Embed Size (px)

Citation preview

Hydrogen - Opportunities for Sustainable Mobility

WEC 2001

Don Huberts, CEO Shell HydrogenMay 18th, 2001

Shell Hydrogen’s position in the RD/Shell Group

CUSTOMERS

Operating Companies

Exploration and

Production Oil Products ChemicalsGas

and Power Renewables Hydrogen

Business Organisations

CORPORATE CENTRE

CMD

ProfessIonal

servIces

Global business of the Royal Dutch/Shell Group of companies

Head quarters in Amsterdam and regional bases in Houston, Hamburg and Tokyo

Set up in 1999 to pursue and develop business opportunities related to hydrogen and fuel cells

400

300

200

1001900 2000

CO Concentrations2

Drivers behind the hydrogen economy

Air Quality Local Emissions - HC’s,

NOx, CO, Particulates, SOx, Aromatics

Global Warming Fuel Economy / Energy

Efficiency

Import Dependency Security of supply, use

of local resources, balance of trade, local jobs ...

The transition is uncertain...

Internal Combustion Engine

led to the Oil Age

THE PAST THE FUTURETHE TRANSITION ISUNCERTAIN

Pro

du

ct P

erfo

rma

nce

Time

Coal Oil Gas Hydrogen

1.5 : 1 1 : 2 1 : 4 0: 1

Underlying Decarbonisation

Better satisfy customer needs

The Fuel Cell can lead to the Hydrogen Age

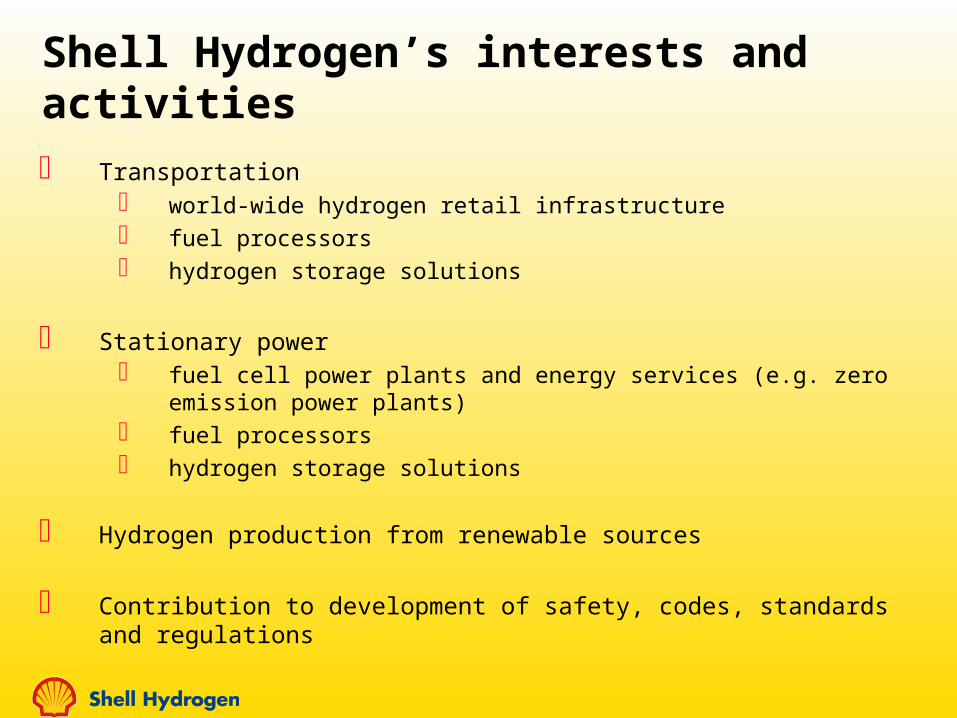

Shell Hydrogen’s interests and activities Transportation

world-wide hydrogen retail infrastructure fuel processors hydrogen storage solutions

Stationary power fuel cell power plants and energy services (e.g. zero emission

power plants) fuel processors hydrogen storage solutions

Hydrogen production from renewable sources

Contribution to development of safety, codes, standards and regulations

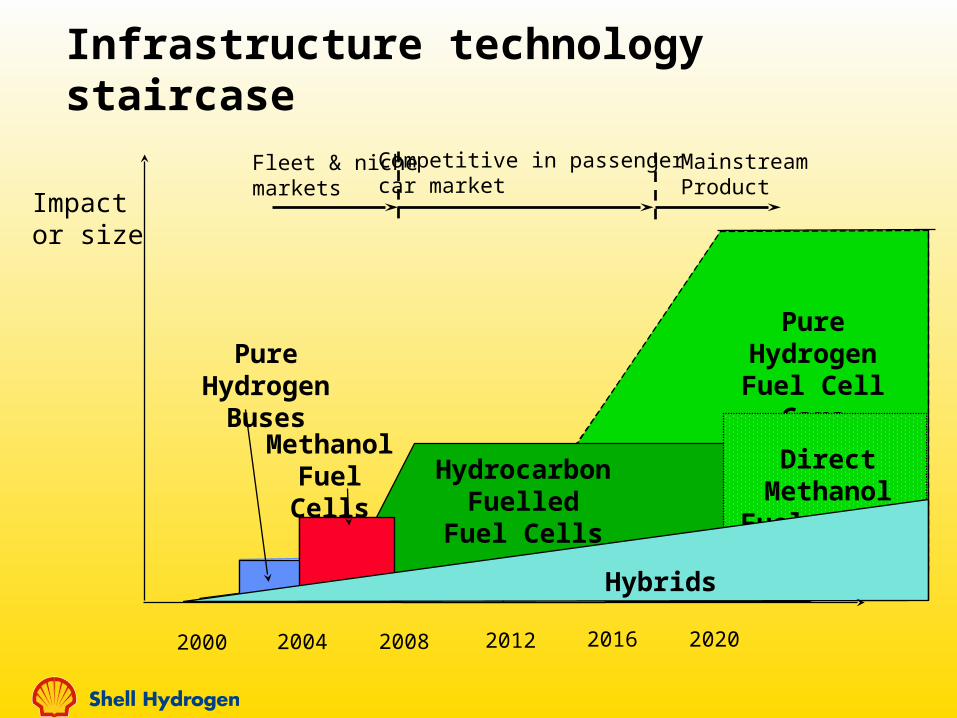

Infrastructure technology staircase

2000 2004 2008 2012 2016 2020

Impactor size

MethanolFuel Cells

Pure HydrogenBuses

Pure HydrogenFuel Cell Cars

Direct Methanol Fuel Cell ?

HydrocarbonFuelled

Fuel Cells

Hybrids

Fleet & nichemarkets

Competitive in passengercar market

MainstreamProduct

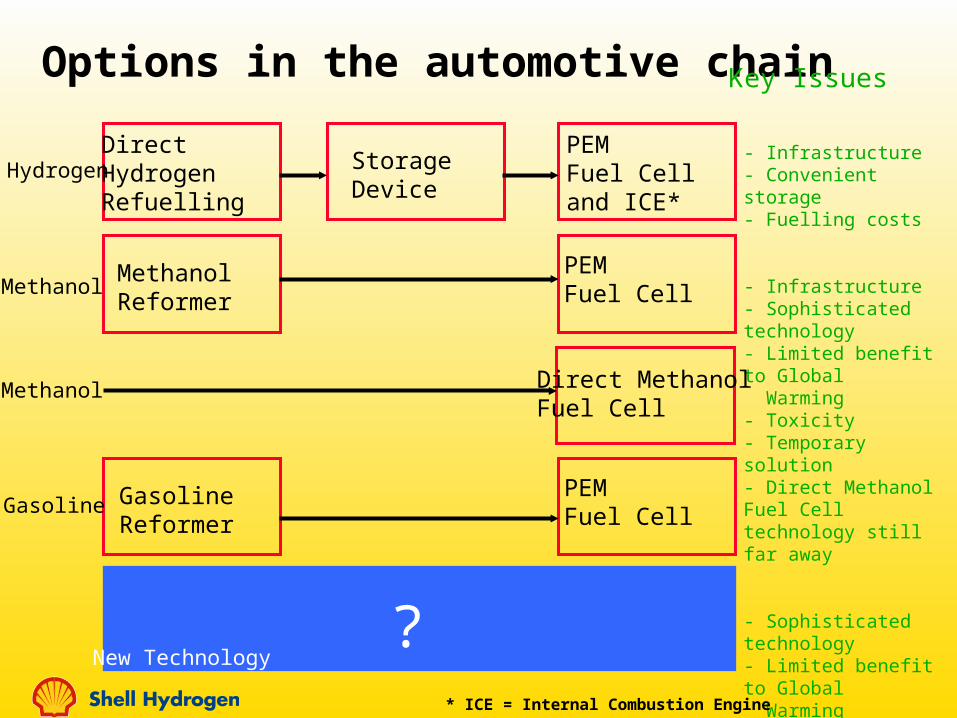

Options in the automotive chain

Hydrogen

Methanol

Gasoline

New Technology?

Direct HydrogenRefuelling

Methanol Reformer

GasolineReformer

StorageDevice

PEMFuel Celland ICE*

PEMFuel Cell

PEMFuel Cell

Key Issues

- Infrastructure- Convenient storage- Fuelling costs

- Infrastructure- Sophisticated technology- Limited benefit to Global Warming- Toxicity- Temporary solution- Direct Methanol Fuel Cell technology still far away

- Sophisticated technology- Limited benefit to Global Warming

- Not available short-term

* ICE = Internal Combustion Engine

Methanol Direct MethanolFuel Cell

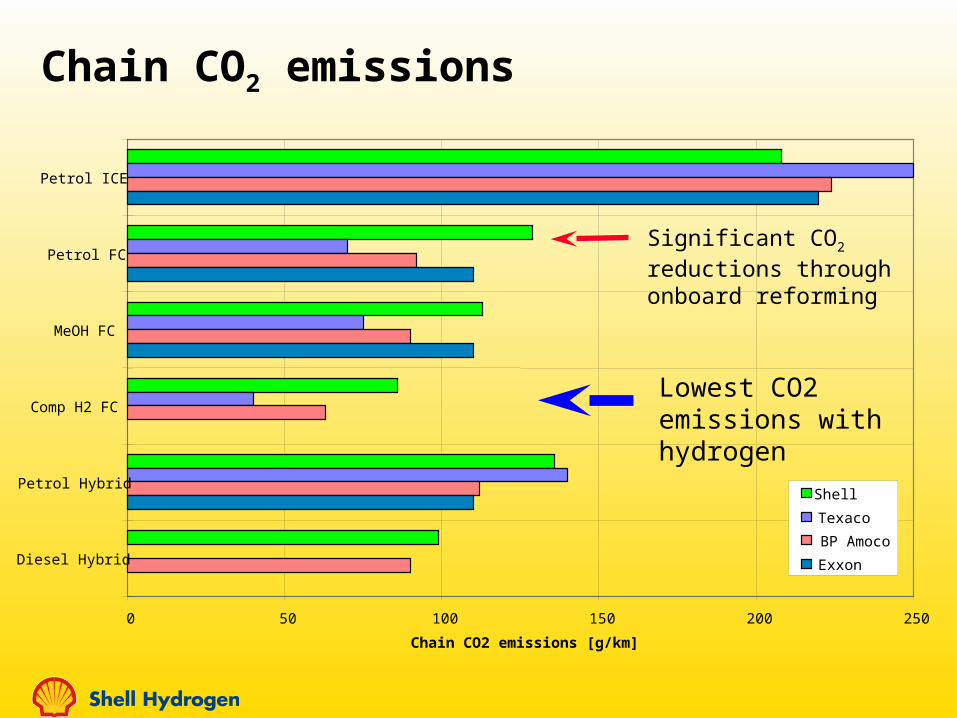

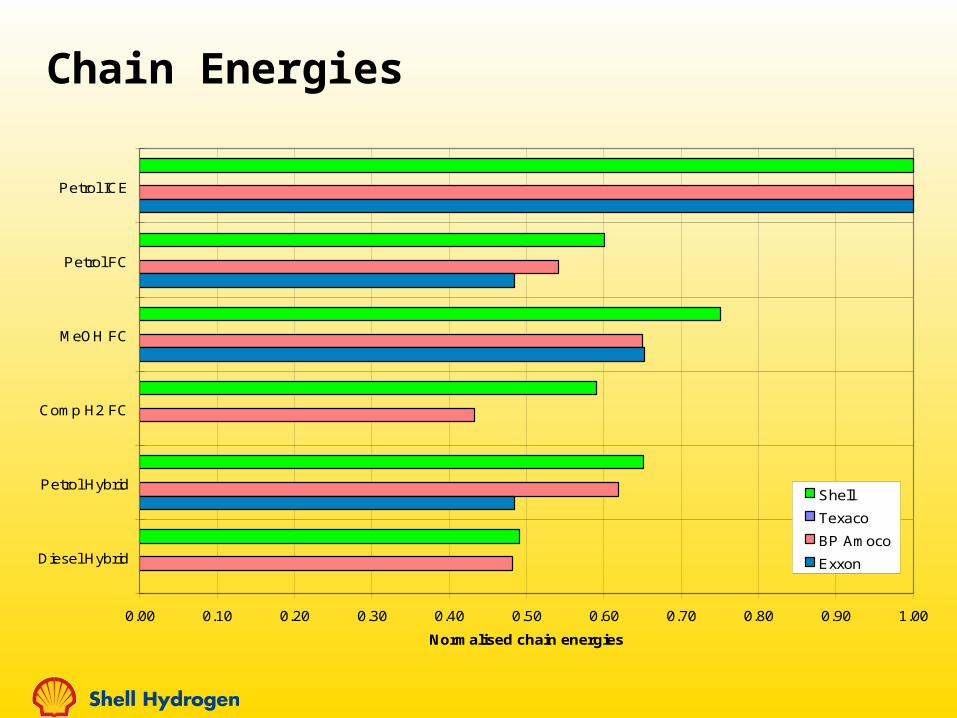

Chain CO2 emissions

0 50 100 150 200 250

Petrol ICE

Petrol FC

MeOH FC

Comp H2 FC

Petrol Hybrid

Diesel Hybrid

Chain CO2 emissions [g/km]

Shell

Texaco

BP Amoco

Exxon

Significant CO2 reductions through onboard reforming

Lowest CO2 emissions with hydrogen

AUTOMOTIVEHyundai SUV

PPT01394011

CA0862Source: IFC

HYUNDAI FUEL CELL VEHICLE

PPT011487012504

Source: IFC

Single refuelling site

Multiple refuelling sites innarrow geographical region

National coverage

Service vehicles (e.g road sweepers, dustcarts etc.)

(local) Delivery vehiclesBuses

No.

of

reta

il st

ati

on

sTim

e(regional) Delivery vehicles

Taxis

Fleets of company vehicles

Cars used mainly for commuting

Pan-national coverage(e.g W. Europe)

Main family car

Fleet Market

Mass Market

Hydrogen fuelAn evolution from fleet markets to a mass market

Increasing economies of scaleIncreasingproportion of renewable hydrogen.

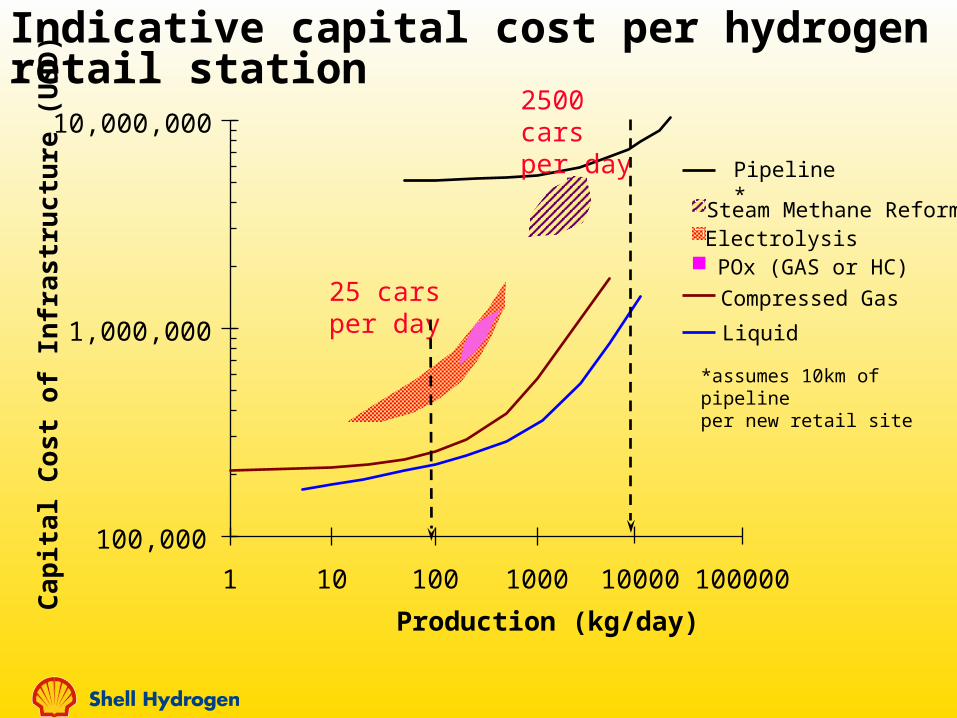

For given throughput cheapest option depends on• Electricity Price• Ex-works cost of centrally produced H2

• Gas (liquid HC) price.• Delivery distance for liquid or gaseous H2.

*assumes 80% load factor and no tax

Indicative delivered hydrogen cost per kgIncreasing capital cost

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1 10 100 1000 10000 100000Throughput (kg/day)

Hyd

rog

en

Cost

(US

D/k

g)*

Liquid Trucks (c)Gaseous Trucks (c)or Electrolysis (onsite)

OnsitePartial Oxidation

OnsiteSteam Reforming

Pipelines (c)

Retail Gasoline US(1kg H2 ~1 USG)

Retail Gasoline UK

25 cars per day

2500 cars per day

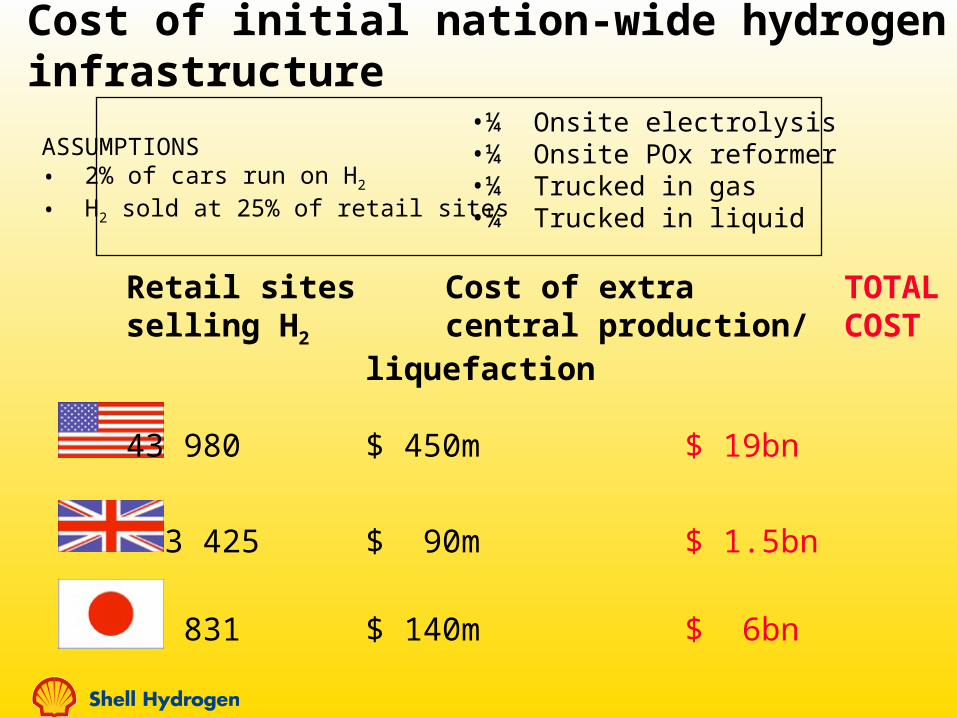

Cost of initial nation-wide hydrogen infrastructure

Retail sites Cost of extra TOTALselling H2 central production/ COST

liquefaction

43 980 $ 450m $ 19bn

3 425 $ 90m $ 1.5bn

13 831 $ 140m $ 6bn

ASSUMPTIONS• 2% of cars run on H2 • H2 sold at 25% of retail sites

•¼ Onsite electrolysis•¼ Onsite POx reformer•¼ Trucked in gas•¼ Trucked in liquid

Shell Hydrogen - positioned for successActivities

Hydrogen Infrastructure- California Fuel Cell Partnership

Hydrogen Refuelling- Iceland Hydrogen Economy- Amsterdam Bus

Hydrogen Generation- in car- stationary power

Hydrogen Storage/Handling

Zero Emission Power

Technology/approach

Multi-fuel demonstrationPublic education

Project approachRenewable hydrogen

Patented reforming technology (CPO)

Metal hydride storageSafety R&D

Solid oxide fuel cell + CO2 recovery

Partners

- government- fuel partners- all major car OEMs- IFC, Ballard

- DaimlerChrysler- Norske Hydro - Vistorka- EU

International Fuel Cells (IFC/UTC)

Hydro Quebec and GfEin-house

Siemens-Westinghouse(SWPC)

Our Vision for Sustainable Mobility

Fleet vehicles on hydrogen - 2005Experience of hydrogen FCVs. Familiarise public with safe hydrogen

refuelling

Transition via onboard hydrocarbon reforming - 2010Familiar fuel. No new infrastructure required. Hazards understood.Significant CO2 reduction. Enables commercialisation of FC vehicles

Mass market hydrogen fuel cell vehicles - 2020Full infrastructure develops by incremental steps. Major CO2 emission benefits

Carbon-free hydrogen fuel cell Vehicles - 2050Increasing proportion of H2 generation from renewables.

Geological CO2 sequestration. Carbon free mobility

-> Back up

Fuel processor

Fuel cell Inverter

fuel cleanhydrogen

DC power AC power

Fuel cell system

balance of the plant

Fuel cells history

Old technology (since 1839), always too expensive; NASA first to recognise its commercial potential (1960’s)

Since 1990, technology revival

Currently FC power not price-competitive with power from central generators

In the automotive area different lifetime requirements, and different cost targets

Most natural fuels:

Stationary: natural gas

Transportation: clean gasoline, hydrogen

Portable: LPG, methanol, hydrogen

Chain Energies

0.00 0.10 0.20 0.30 0.40 0.50 0.60 0.70 0.80 0.90 1.00

Petrol ICE

Petrol FC

MeOH FC

Comp H2 FC

Petrol Hybrid

Diesel Hybrid

Normalised chain energies

Shell

Texaco

BP Amoco

Exxon

Production (kg/day)

Ca

pit

al C

ost

of

Infr

astr

uc

ture

(U

SD

)Indicative capital cost per hydrogen retail station

Liquid

Pipeline*

ElectrolysisSteam Methane Reformer

Compressed Gas

POx (GAS or HC)25 cars per day

100,000

1,000,000

10,000,000

1 10 100 1000 10000 100000

*assumes 10km of pipeline per new retail site

2500 cars per day

Renewables and Hydrogen will meet in the future

0

5

10

15

20

25

1990 1995 2000 2005 2010 2015 2020

¢/k

Wh

Photovoltaic

Biomass

Wind

Grid

Wholesale Gasoline Price (1999)

![Photoelectrochemical Production of Hydrogen · stainless steel), for solar hydrogen production [Miller & Rocheleau, 2001]. In the illustration of a generic hydrogen photoelectrode](https://img.pdfslide.us/doc/110x75/5ea93ce75a148409cd011fb5/photoelectrochemical-production-of-hydrogen-stainless-steel-for-solar-hydrogen.jpg)