Embed Size (px)

Citation preview

4

Human emotions and behaviors

often influence the decision-

making process of an investor.

Several studies in the field of

behavioral finance suggest that

most investors are emotional

and try to time the market,

which often lead to below

average returns on their

portfolio, as compared to

broader markets.

This is the case, not only with

Indian investors, but also with

investors across the globe. For

instance, the latest report on

'investor behavior analysis' by

Dalbar, a research agency,

shows that in the last 20 years,

Anup BagchiMD & CEO

ICICI Securities Ltd.

the average equity investor has earned significantly less

(5.02%) than the broad equity markets (9.22% by S&P 500).

During the same period, the average fixed-income investor

has earned less (0.71%) than the rate of inflation (2.37%).

This is mainly because of our behavioral biases, which lead to

the large gap between broader market returns and actual

investor returns. Our emotional reaction, or rather over-

reaction, to good news or to bad news, causes irrational

investment decisions. Such decisions can be avoided by

adopting a goal-based investing approach, as it helps us stay

focused on our goals - the true purpose behind making an

investment.

1ICICIdirect Money Manager February 2015

For instance, the 'herding' behavior - the tendency to imitate

other investors - can be avoided through a goal-based

investing approach - as the investor then is less influenced by

public opinion and is focused on his goals. Similarly, the

'Myopic loss aversion' behavior - paying excessive attention to

the market's short-term ups and downs - can be avoided as the

investor then looks beyond intermittent market volatility.

Likewise, our behavioral biases can be controlled with a goal-

based investing approach.

Goal-based investing is nothing, but a simple approach, where

the focus is on funding the financial goals rather than

achieving the higher return on investment or exceeding the

market return. In this approach, our assets and investments

are closely matched with liabilities (requirement of funds) and

goals, to create an optimum portfolio. Having this closer

alignment of assets and liabilities helps us avoiding some

common investment mistakes. The best part about this

approach is that it provides us a better understanding of what

needs to be done to achieve our goals.

You may speak to our financial planners about building a goal

based investment portfolio. They will help you determine your

financial profile, including your investment goals, time

horizon, and risk tolerance. Our planners will also work with

you to understand, anticipate, and overcome the any unique

investment challenges that you could face over time.

Our message remains the same - 'Keep investing and stay

invested for your life goals'. Through this magazine and our

website www.icicidirect.com we want to make an earnest

attempt to partner with you in setting and achieving your

financial goals. Do walk into any of your Neighbourhood

Financial Superstore and talk to us.

2

A core expectation for most investors is growth and return. Returns could be absolute or relative to a benchmark. The absolute return strategy chases a target return, having a target return in mind works well for an investor. However, being anchored to a target return expectation always is neither practical nor advisable.

A goal-based investment strategy works better. Unlike absolute return strategy, it measures progress toward goals rather than returns versus the benchmark. In a goal-based investment strategy, our investments are matched to our liabilities (or requirement of funds) and to our life goals by proper planning. It may look like a new concept, but it is not. Financial institutions such as banks and insurance firms have always followed this strategy of matching their assets with their expected liabilities.

When we have a clear idea of our goals, we can effectively invest in products that are best suited for achieving our goals. Our cover story of this edition takes you through the fine details of goal-based investing to help you better manage your finances.

The edition also features a piece on how should debt investors invest in the current scenario, as the Reserve Bank of India (RBI) has recently cut the repo rate, which indicates of easing interest rate cycle going ahead. We also feature an interview with R Sivakumar, Head - Fixed Income, Axis Mutual Fund, who expects the entire yield curve to benefit from the rate cut cycle.

I would also like to draw your attention to our new section 'Debt market outlook', where we present the key recent developments of debt market along with the outlook going ahead. So read on, stay updated and involved. Do write in with your feedback at moneymanager@ icicisecurities.com and share your thoughts.

Editor & Publisher : Abhishake Mathur, CFA

Coordinating Editor : Yogita Khatri

Editorial Board : Sameer Chavan, CWM®, Pankaj Pandey

CMEditorial Team : Azeem Ahmad, Nithyakumar VP CFP , Nitin Kunte, Sachin Jain, Sheetal Ashar

ICICIdirect Money Manager February 2015

Your magazine is now also available on www.magzter.com, a digital newsstand.

3

MD Desk.............................................................................................1

Editorial.............................................................................................. 2

Contents..............................................................................................3

News..................................................................................................4

Equity Market Round-up & Outlook.........................................................5

Debt Market Round-up & Outlook...........................................................8

Getting Technical with Dharmesh Shah..................................................10

Derivatives Strategy by Amit Gupta.......................................................12

Stock Ideas: Century Plyboard and KSB Pumps.......................................21

Flavour of the Month: Goal-based Investing Read on to find out how by adopting a goal-based investing approach you can have a better chance of meeting your goals................................................................................................. 29

Tête-à-tête: 'Longer duration strategies to benefit the most' An interview with R Sivakumar, Head - Fixed Income, Axis Mutual Fund…...............................................................................................37

Ask Our PlannerYour personal finance queries answered…....................................41

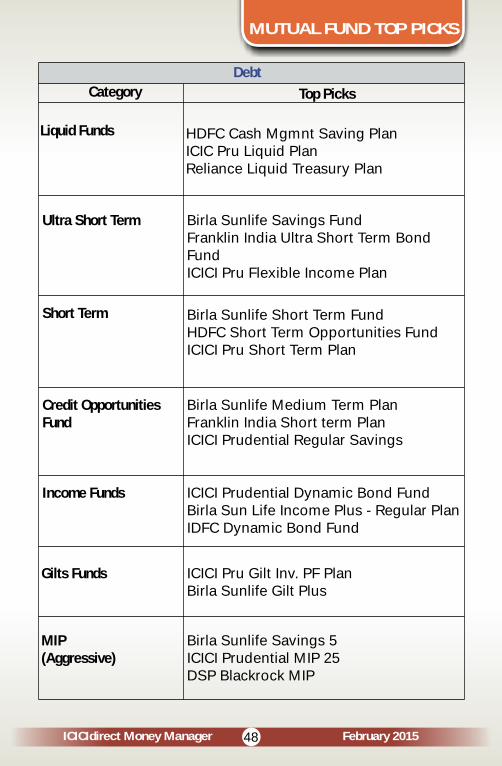

Mutual Fund Analysis: Category – Debt Funds Read on to know how to invest in debt funds post RBI's recent rate cut…..................................................................................................44

Mutual Fund Top PicksHere we present our research team's top mutual fund recommendations, across equity and debt categories…...............47

Equity Model Portfolio...........................................................................49

Quiz Time............................................................................................54

Monthly Trends....................................................................................55

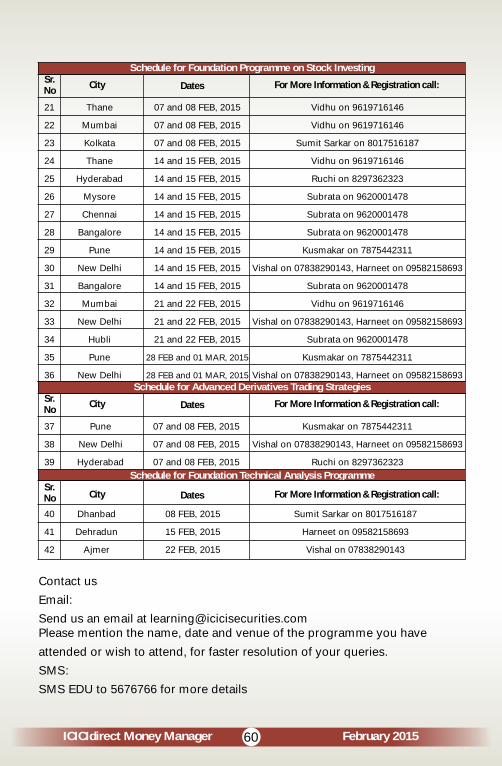

Premium Education Programmes Schedule.............................................59

ICICIdirect Money Manager February 2015

4ICICIdirect Money Manager

Budget 2015: Government looking at SEBI proposal to introduce MF retirement plans with tax benefits

Investors may soon get tax benefits in retirement plans run by mutual funds. The government is considering a proposal by the capital market regulator to introduce retirement savings plan under section 80CCD of the Income Tax Act, which allows investors to claim tax deductions. The government may announce this in the Budget. Currently, individuals investing in National Pension Scheme (NPS) are eligible to claim income tax deductions under section 80CCD.

Courtesy: The Economic Times

Mutual fund houses plan to come up with special schemes focused on the manufacturing sector that is expecting a big boost from the Centre's 'Make in India' initiative. ICICI Prudential Mutual Fund (MF), which has filed offer documents with market regulator SEBI, plans to launch an open ended equity scheme 'ICICI Prudential Manufacture in India Fund'. Besides, Pramerica MF has filed draft papers to launch 'Pramerica Build in India Fund', while the 'Birla Sun Life manufacturing equity fund' is already being launched. These schemes are aimed at investment in equity and equity-related securities that are likely to benefit from the Government's 'Make in India' initiative.

Courtesy: The Hindu Business Line

Mutual funds plan schemes to cash in on 'Make in India' campaign

If you are an insurance policy holder confused about jargon such as pure-term, non-linked, co-pay cover, et al, here's some good news. The insurance sector is working on simple, plain-vanilla products to cater to people like you. In a recent meeting at Hyderabad between state-owned insurers, regulatory and finance ministry officials, the government has asked public sector insurers to launch products that are simple, cheap and something that a layman can understand. The insurers have already begun to work on them.

Courtesy: Business Standard

No more confusion: Plain vanilla insurance products coming up

The government is likely to increase the lock-in period for Public Provident Fund (PPF) by at least two years, reports ET Now. According to ET Now sources in the Finance Ministry, those who invest in PPF will be able to withdraw after 8 years, as against the current 6-year lock-in period. The government is also likely to increase the tenure of PPF from 15 years to 20 years. "While it will be up to the saver to opt for either a 15-year or a 20-year saving period, the government will look to lure people with a higher interest rate for the 20-year tenure, under Section 80C," reported ET Now. "This implies that if the saver is willing to invest in PPF for 20 years, the subsequent tax benefit will be higher," the channel said. According to ET Now, the government is considering this move in order to ensure a stable source of infrastructure funding.

Courtesy: The Economic Times

Government may increase lock-in period for PPF; to offer higher interest rate for 20-year tenure

February 2015

5ICICIdirect Money Manager

Markets likely to consolidate as Budget countdown begins

February 2015

EQUITY MARKET ROUND UP& OUTLOOK

-

Domestic equity benchmarks

posted strong gains in January,

ending the month ~6% higher

as the market took positive

cues from a sharp fall in global

commodity prices and a

dovish monetary policy stance

by the Reserve Bank of India

(RBI) besides encouraging

f isca l pr ints . December

Consumer Price Index (CPI)

inflation came in at 5% year-

on-year (YoY), below Street

expectation of 5.3%. The Index

of Industrial Production (IIP) for

November 2014 was recorded

at 3.8% after a sharp decline of

4.2% in the previous month.

The growth was driven by all

t h r e e s e c t o r s , m i n i n g ,

manufacturing and electricity,

which registered growth of

3 . 4 % , 3 % a n d 1 0 % ,

respectively. Easing inflation

was the main influential factor

behind the RBI's surprise move

of a 25 basis points (bps) repo

rate cut to 7.75%. The move

was cheered by the equity as

well as debt markets.

The Q3FY15 numbers have

been a mixed bag with a

negative bias. For IT, the

cons tant cur rency (CC)

revenue growth for tier-I IT

companies was notably

stronger in a seasonally weak

quarter. In the auto space, the

results were subdued barring

Bharat Forge and Maruti. On

the banking front, divergence

b e t w e e n t h e e a r n i n g

performance of private &

public sector undertaking

(PSU) banks continued. While

private banks sustained their

h e a l t h y o p e r a t i o n a l

performance with asset quality

staying under control, PSU

banks continued to reel under

asset quality pressure thereby

leading to declining/muted

profitability. In the consumer

discretionary space, the results

were below expectations on

account of a weak demand

scenario. Even fast moving

consumer goods (FMCG)

companies continued to

witness muted volume growth

due to a slowdown in urban

d i s c r e t i o n a r y d e m a n d .

However, with a sharp fall in

commodity prices, operating

margins witnessed an uptick.

6ICICIdirect Money Manager February 2015

Global markets continued to

be influenced by falling crude

prices and the pol i t ical

situation in Greece during the

month besides the stimulus

a n n o u n c e m e n t b y t h e

European Central Bank (ECB).

Crude plunged to as low as

$45.2 per barrel in the month

as Organ iza t ion o f the

Petroleum Exporting Countries

(OPEC) lowered its demand

forecast for 2015 to 28.8 million

barrels per day. The downward

revision of growth forecast for

the global economy by the

International Monetary Fund

(IMF) from 3.8% to 3.5% for

CY15 and from 4% to 3.7% for

CY16 a lso we ighed on

sent iments. Though the

markets received some boost

from the ECB announcement

of bond buying programme of

€ 6 0 b i l l i o n p e r m o n t h

(including investment grade

sovereign bonds), the gains

could not offset the losses in

the month. Concerns due to

negative implications from

falling crude prices kept the US

markets in the red territory. The

European markets remained

more or less flat.

With softening inflation, the

benchmark 10-year bond yield

fell to 7.69%, the lowest since

September 2013. During the

m o n t h , c r u d e ( B r e n t )

continued the decline and

ended at ~US$ 50.7/barrel vs.

US$ 55.7/barrel at the end of

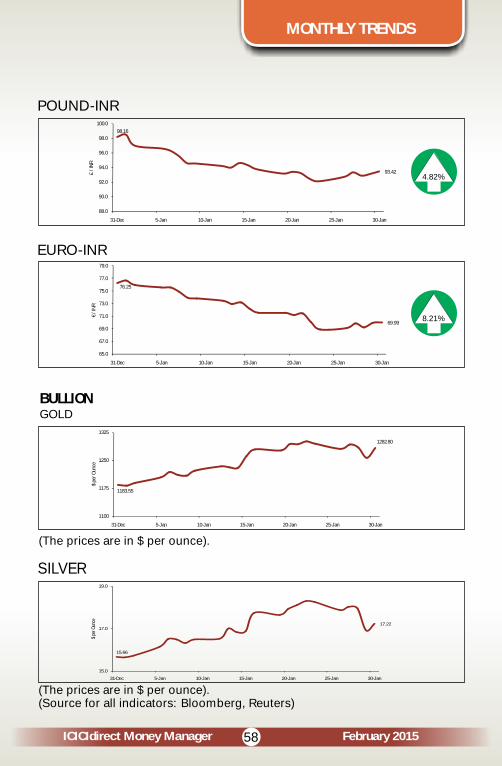

December. Gold prices ended

the month with gains of 8% at

US$ 1,283.7/ounce.

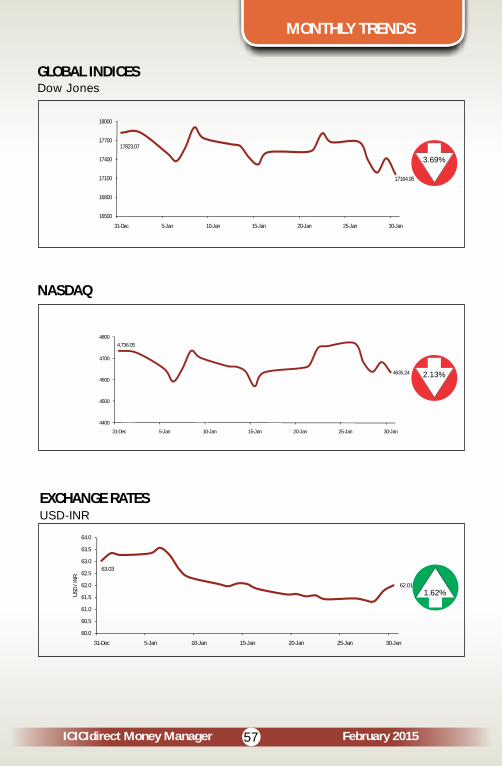

Global markets

The US markets ended on a

negative note as sentiments

were dampened owing to

falling crude prices and the

political situation in Greece.

The Dow Jones, S&P 500 and

Nasdaq were down 4.5%,

4.1% and 3%, respectively,

during the month. The UK

FTSE, German Dax and French

CAC gained 3.1%, 9.1% and

8.4%, respectively. In Asian

markets, Nikkei and Shanghai

SSEC ended the month up

1 . 3 % a n d d o w n 0 . 8 % ,

respectively, while the Hang

Seng was up 3.8%.

Domestic markets

Foreign institutional investors

(FIIs) bought heavily to the tune

of ~ Rs. 17,689.09 crore on the

EQUITY MARKET ROUND UP& OUTLOOK

-

7ICICIdirect Money Manager February 2015

b a c k o f s t r e n g t h e n i n g

confidence on the Indian

economy vis-à-vis the rest of

the emerging markets. Though

the domestic institutional

investors (DII) investment

remained relatively subdued,

they continued to be net

buyers with a net inflow of

~Rs. 879.5 crore.

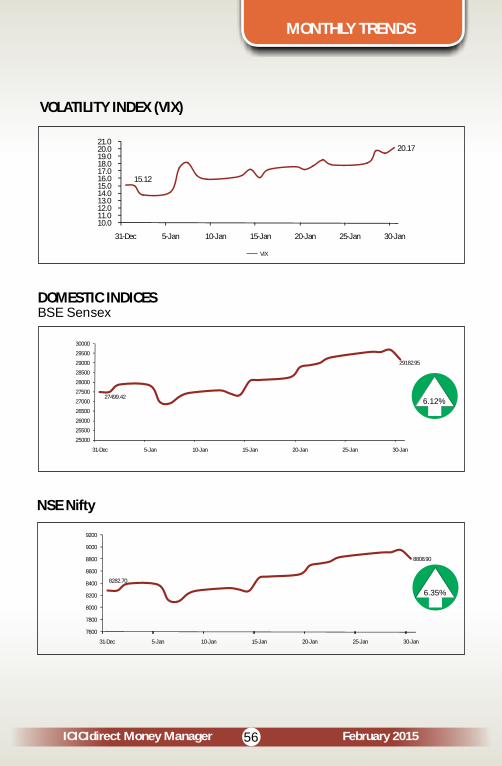

The Nifty and Sensex posted

decent gains and were up 6.4%

and 6.1%, respectively, during

the month. Except the BSE

Metal Index (-5.2%) and BSE

FMCG Index (-4.9%) all other

indices ended January in the

positive territory. Some of the

sectoral indices gainers were

BSE Realty (16.5%), BSE Auto

(7.3%), BSE Bankex (5.9%),

BSE Healthcare (6.6%), BSE IT

(5.6%), BSE Power (6.3%) and

BSE Technology (5.0%).

Outlook: Focus firmly on Budget in

backdrop of weak global cues,

subdued Q3 numbers

The Budget, which will be the

first full-fledged Budget of

NDA-2 (the July Budget was a

kind of formality), will be a

major catalyst. The new

government will be put to the

task to match the long list of

expectations and unfinished

agendas o f the ea r l i e r

government. The July Budget,

albeit a formality, has already

addressed the strategic need

to improve the investment

climate by emphasising on

m e a s u r e s t o c r e a t e a

framework for low & stable

inflation, setting fiscal deficit

on a sustainable path through

tax and expenditure reforms

and setting up a broad based

inclusive growth framework

for a sustainable market

e c o n o m y. H e n c e , t h e

expectations have already

been amplified. After taking

into account the RBI's positive

surprise of an unscheduled

rate cut, expectations may go

through the roof. On the

earnings front, the trend was

more or less subdued with

very positive beats till date.

Globally, the liquidity gush is

likely to continue with ECB

joining the bandwagon amid

Greece's false bravado and

subsequent submission. In this

backdrop, markets are likely to

focus solely on the Budget

outcome.

EQUITY MARKET ROUND UP& OUTLOOK

-

8ICICIdirect Money Manager February 2015

DEBT MARKET ROUND UP& OUTLOOK

-

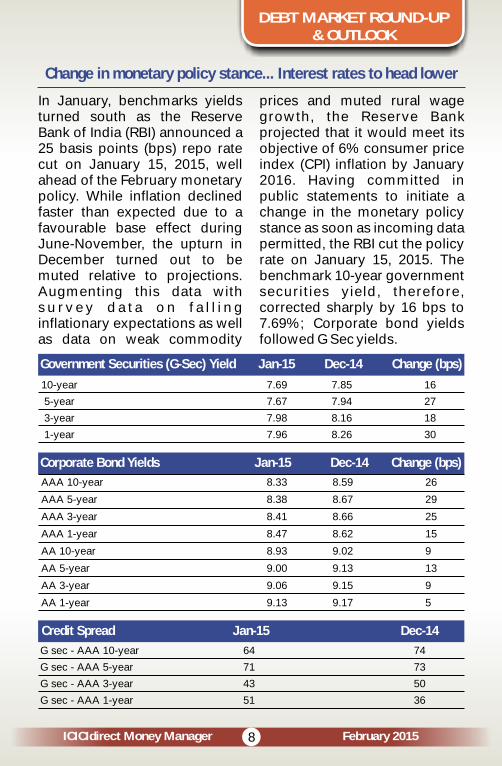

Change in monetary policy stance... Interest rates to head lower

In January, benchmarks yields turned south as the Reserve Bank of India (RBI) announced a 25 basis points (bps) repo rate cut on January 15, 2015, well ahead of the February monetary policy. While inflation declined faster than expected due to a favourable base effect during June-November, the upturn in December turned out to be muted relative to projections. Augmenting this data with s u r v e y d a t a o n f a l l i n g inflationary expectations as well as data on weak commodity

prices and muted rural wage growth, the Reserve Bank projected that it would meet its objective of 6% consumer price index (CPI) inflation by January 2016. Having committed in public statements to initiate a change in the monetary policy stance as soon as incoming data permitted, the RBI cut the policy rate on January 15, 2015. The benchmark 10-year government securities yield, therefore, corrected sharply by 16 bps to 7.69%; Corporate bond yields followed G Sec yields.

Government Securities (G-Sec) Yield Jan-15 Dec-14 Change (bps)

10-year 7.69 7.85 16

5-year 7.67 7.94 27

3-year 7.98 8.16 18

1-year 7.96 8.26 30

Corporate Bond Yields Jan-15 Dec-14 Change (bps)

AAA 10-year 8.33 8.59 26

AAA 5-year 8.38 8.67 29

AAA 3-year 8.41 8.66 25

AAA 1-year 8.47 8.62 15

AA 10-year 8.93 9.02 9

AA 5-year 9.00 9.13 13

AA 3-year 9.06 9.15 9

AA 1-year 9.13 9.17 5

Credit Spread Jan-15 Dec-14

G sec - AAA 10-year 64 74

G sec - AAA 5-year 71 73

G sec - AAA 3-year 43 50

G sec - AAA 1-year 51 36

9ICICIdirect Money Manager February 2015

DEBT MARKET ROUND UP& OUTLOOK

-

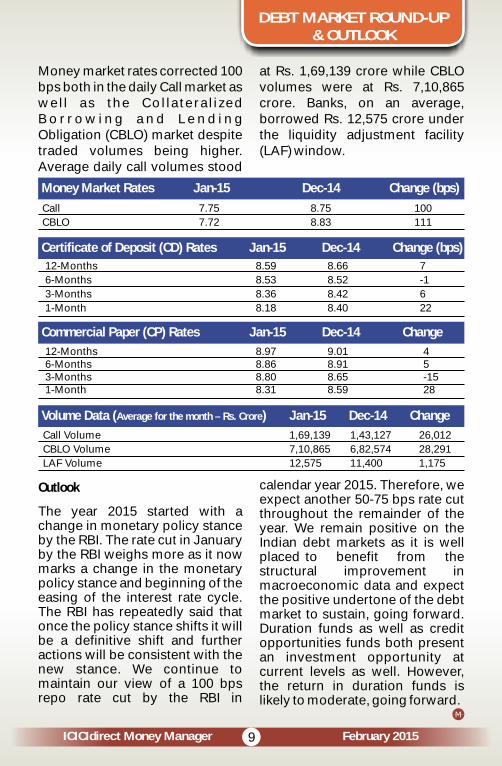

Money market rates corrected 100 bps both in the daily Call market as wel l as the Col lateral ized B o r r o w i n g a n d L e n d i n g Obligation (CBLO) market despite traded volumes being higher. Average daily call volumes stood

at Rs. 1,69,139 crore while CBLO volumes were at Rs. 7,10,865 crore. Banks, on an average, borrowed Rs. 12,575 crore under the liquidity adjustment facility (LAF) window.

Money Market Rates Jan-15 Dec-14 Change (bps)

Call 7.75 8.75 100

CBLO 7.72 8.83 111

Certificate of Deposit (CD) Rates Jan-15 Dec-14 Change (bps)

12-Months 8.59 8.66 7

6-Months 8.53 8.52 -1

3-Months 8.36 8.42 6

1-Month 8.18 8.40 22

Commercial Paper (CP) Rates Jan-15 Dec-14 Change

Outlook

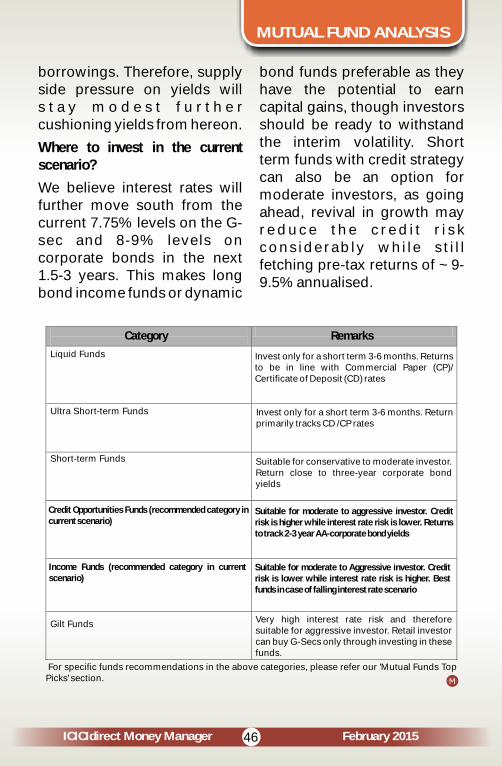

The year 2015 started with a change in monetary policy stance by the RBI. The rate cut in January by the RBI weighs more as it now marks a change in the monetary policy stance and beginning of the easing of the interest rate cycle. The RBI has repeatedly said that once the policy stance shifts it will be a definitive shift and further actions will be consistent with the new stance. We continue to maintain our view of a 100 bps repo rate cut by the RBI in

calendar year 2015. Therefore, we expect another 50-75 bps rate cut throughout the remainder of the year. We remain positive on the Indian debt markets as it is well placed to benefit from the structural improvement in macroeconomic data and expect the positive undertone of the debt market to sustain, going forward. Duration funds as well as credit opportunities funds both present an investment opportunity at current levels as well. However, the return in duration funds is likely to moderate, going forward.

12-Months 8.97 9.01 4 6-Months 8.86 8.91 5 3-Months 8.80 8.65 -15 1-Month 8.31 8.59 28

Volume Data (Average for the month – Rs. Crore) Jan-15 Dec-14 Change

Call Volume 1,69,139 1,43,127 26,012

CBLO Volume 7,10,865 6,82,574 28,291

LAF Volume 12,575 11,400 1,175

ICICIdirect Money Manager

TECHNICAL OUTLOOK

Pendulum to tilt towards 30400

February 2015

Domestic equity benchmarks began 2015 with renewed zeal and surged over 7% to achieve our short-term target of 29500/8900 (Sensex/Nifty) as elaborated in the January edition.

We believe the markets will continue to ride the positive momentum and extend the c u r r e n t r a l l y t o w a r d s 30400/9200 in the run-up towards the Union Budget. The short-term base for the benchmarks has shif ted upwards to 28800/8600. Any intermediate cool-off towards these levels should be used as a n i n c r e m e n t a l b u y i n g opportunity.

The current up-move from December 2014 low of 26469 to the life-time high of 29786 (3317 points) is the largest in magnitude since February 2014. In the entire up-move from February 2014 onwards,

the index had followed a peculiar tendency as price-wise each major up-leg measured 3000 points (900 points on Nifty). After every 3000-point rally, the index ventured into a short-term consolidation phase to form a h i g h e r b a s e b e f o r e continuance of the larger uptrend. The current rally exceeding the magnitude of all preceding up-moves over the past year signals an extending market, which holds further u p s i d e p o t e n t i a l . T h e minimum 138.2% Fibonacci extension of the October – D e c e m b e r 2 0 1 4 r a l l y measured from December 2014 low of 26469/7961 projects an upside target of 30400/9200 in the coming month.

The index continues to stride northwards in a rising peaks and troughs manner as the support base keeps shifting higher with every subsequent rally. The strong resolve past the December 2014 high of 28822/8626 has confirmed a significant higher bottom in place at the December low of

10

ICICIdirect Money Manager

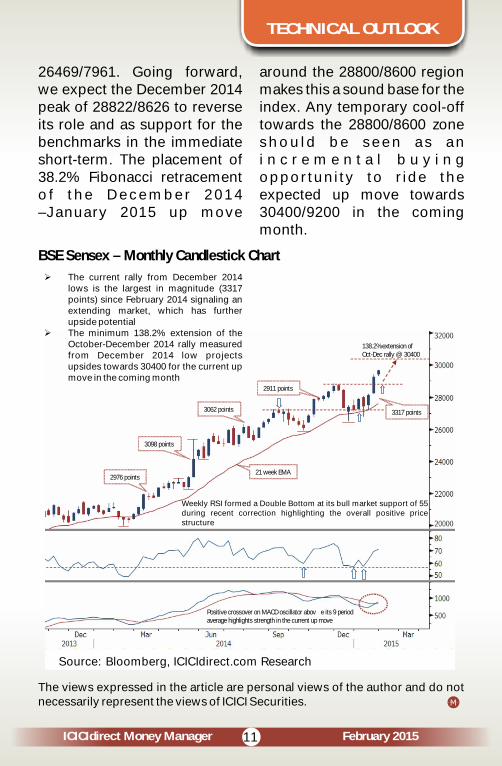

BSE Sensex – Monthly Candlestick Chart

February 201511

26469/7961. Going forward, we expect the December 2014 peak of 28822/8626 to reverse its role and as support for the benchmarks in the immediate short-term. The placement of 38.2% Fibonacci retracement o f the December 2014 –January 2015 up move

around the 28800/8600 region makes this a sound base for the index. Any temporary cool-off towards the 28800/8600 zone s h o u l d b e s e e n a s a n i n c r e m e n t a l b u y i n g opportunity to r ide the expected up move towards 30400/9200 in the coming month.

21 week EMA

2976 points

2911 points

3062 points

3098 points

3317 points

Positive crossover on MACD oscillator abov e its 9 period average highlights strength in the current up move

138.2% extension of Oct-Dec rally @ 30400

Weekly RSI formed a Double Bottom at its bull market support of 55 during recent correction highlighting the overall positive price structure

Source: Bloomberg, ICICIdirect.com Research

The views expressed in the article are personal views of the author and do not necessarily represent the views of ICICI Securities.

Ø The current rally from December 2014 lows is the largest in magnitude (3317 points) since February 2014 signaling an extending market, which has further upside potential

Ø The minimum 138.2% extension of the October-December 2014 rally measured from December 2014 low projects upsides towards 30400 for the current up move in the coming month

TECHNICAL OUTLOOK

ICICIdirect Money Manager

DERIVATIVES STRATEGY

Nifty likely to move towards 9300/9500; Key support near 8500

Amit Gupta

Head - Derivatives Research,ICICI Securities

February 201512

Nifty clocking strongest expiry performance in well over a year, with broad based participation from various sectors

After seeing profit booking in the December series, the Nifty saw a strong pullback as the Reserve Bank of India (RBI) surprised the market with a repo rate cut on January 15, 2015. Since then, buying momentum was seen across sectors. For the month, the Nifty registered strong returns of close to 10% for the January series. This is the highest expiry return in well over a year.

We believe the up-move could continue as expectations are still running high from the Union Budget on February 28. However, bouts of profit booking are not ruled out as the Nifty has already moved up over 900 points on the trot.

Looking at the sectoral performance for the month, broad-based buying was seen during the month. At the start of the series, consumer durables started to move up. Then capital goods stocks witnessed buying. Towards the expiry, banking stocks were back in the reckoning. Driven by dol lar s t rength, the commodity space, including metals remained weak and closed negative despite the strong move in the broader markets.

This sectoral buoyancy is likely t o c o n t i n u e a s t h e consumption, cyclical and capex stories are likely to attract focus.

Nifty expiry returns in trailing12 months

9%

-4%

4%3%3%3%4%

6%

3%

6%

3%

-1%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Jan'

15Dec

NovOct

Sep

AugJu

l

Jun

MayApr

Mar

Feb

13ICICIdirect Money Manager February 2015

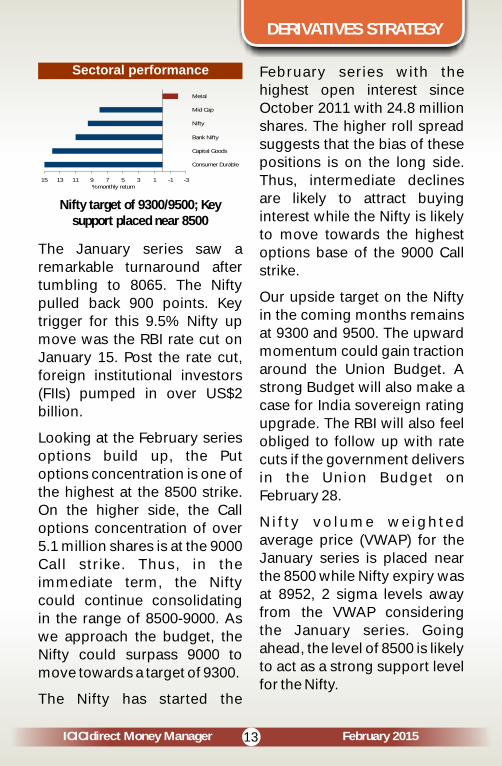

Sectoral performance

-3-113579111315

Consumer Durable

Capital Goods

Bank Nifty

Nifty

Mid Cap

Metal

% monthly return

Nifty target of 9300/9500; Key support placed near 8500

The January series saw a remarkable turnaround after tumbling to 8065. The Nifty pulled back 900 points. Key trigger for this 9.5% Nifty up move was the RBI rate cut on January 15. Post the rate cut, foreign institutional investors (FIIs) pumped in over US$2 billion.

Looking at the February series options build up, the Put options concentration is one of the highest at the 8500 strike. On the higher side, the Call options concentration of over 5.1 million shares is at the 9000 Call strike. Thus, in the immediate term, the Nifty could continue consolidating in the range of 8500-9000. As we approach the budget, the Nifty could surpass 9000 to move towards a target of 9300.

The Nifty has started the

February series with the highest open interest since October 2011 with 24.8 million shares. The higher roll spread suggests that the bias of these positions is on the long side. Thus, intermediate declines are likely to attract buying interest while the Nifty is likely to move towards the highest options base of the 9000 Call strike.

Our upside target on the Nifty in the coming months remains at 9300 and 9500. The upward momentum could gain traction around the Union Budget. A strong Budget will also make a case for India sovereign rating upgrade. The RBI will also feel obliged to follow up with rate cuts if the government delivers in the Union Budget on February 28.

N i f t y vo lume we igh ted average price (VWAP) for the January series is placed near the 8500 while Nifty expiry was at 8952, 2 sigma levels away from the VWAP considering the January series. Going ahead, the level of 8500 is likely to act as a strong support level for the Nifty.

DERIVATIVES STRATEGY

14ICICIdirect Money Manager February 2015

As seen in the sigma level chart below, the Nifty had bounced from the 100 DMA line in the middle of the January series and is currently trading near mean + 2 sigma level of 8700. Thus, the Nifty is likely to consolidate before scaling higher.

Nifty options build-up in February series

0

1

2

3

4

5

6

7

8

8500

8600

8700

8800

8900

9000

9100

9200

9300

9400

9500

OI i

n M

illio

n S

hare

s

Call OI Put OI

Nifty 2 sigma Band: consolidation initially

5700

6200

6700

7200

7700

8200

8700

9200

Jan-

14

Feb

-14

Ma

r-14

Apr

-14

Ma

y-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec-

14

Jan

-15

Close UBB(2) BollMA (100) on Close LBB(2)

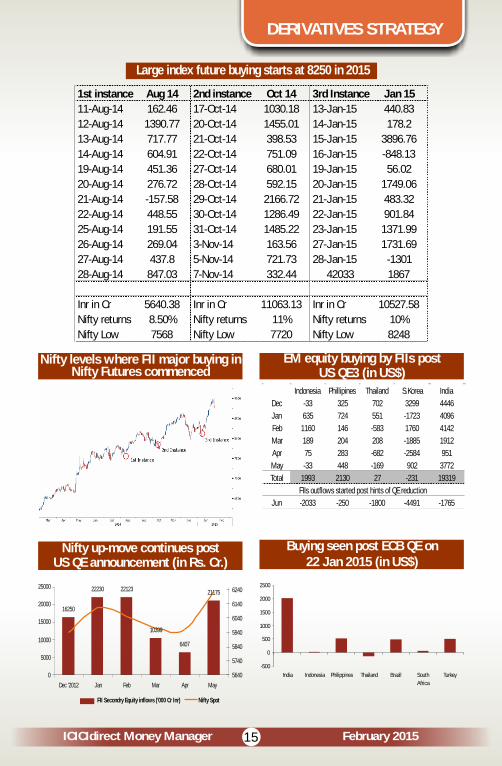

FII buying in Nifty futures commenced at 8250, which remains critical support for coming months

Since the election verdict,

Indian markets have displayed

new found strength as the new

government in place has taken

s t rong re formis t po l icy

initiatives. This was further

helped by a cool-off in crude oil

prices, improving India's fiscal

condition. This strength has

seen good participation from

FIIs inflow not only via cash

buying in equities but also

through long Index futures

blocks.

Since the election verdict, FIIs

have created long index future

p o s i t i o n s o n m u l t i p l e

occasions. In the first Instance,

the Nifty moved up 8.5%, in the

second instance it moved up

11% while recently in January

2015, the Nifty moved up 10%.

The key takeaway from this

analysis is from the point from

where buying in index future

commences the level is not

violated. The chart below

displays the same.

T h e r e c e n t b u y i n g

commenced from 8250 on

January 13, 2015. Hence, the

Nifty was unlikely to dip below

this level. This will remain a

positional support for the Nifty

i n t h e c u r r e n t u p w a r d

momentum, which started

post elections verdict in 2015.

DERIVATIVES STRATEGY

15ICICIdirect Money Manager February 2015

Large index future buying starts at 8250 in 2015

1st instance Aug 14 2nd instance Oct 14 3rd Instance Jan 15

11-Aug-14 162.46 17-Oct-14 1030.18 13-Jan-15 440.83

12-Aug-14 1390.77 20-Oct-14 1455.01 14-Jan-15 178.2

13-Aug-14 717.77 21-Oct-14 398.53 15-Jan-15 3896.76

14-Aug-14 604.91 22-Oct-14 751.09 16-Jan-15 -848.13

19-Aug-14 451.36 27-Oct-14 680.01 19-Jan-15 56.02

20-Aug-14 276.72 28-Oct-14 592.15 20-Jan-15 1749.06

21-Aug-14 -157.58 29-Oct-14 2166.72 21-Jan-15 483.32

22-Aug-14 448.55 30-Oct-14 1286.49 22-Jan-15 901.84

25-Aug-14 191.55 31-Oct-14 1485.22 23-Jan-15 1371.99

26-Aug-14 269.04 3-Nov-14 163.56 27-Jan-15 1731.69

27-Aug-14 437.8 5-Nov-14 721.73 28-Jan-15 -1301

28-Aug-14 847.03 7-Nov-14 332.44 42033 1867

Inr in Cr 5640.38 Inr in Cr 11063.13 Inr in Cr 10527.58

Nifty returns 8.50% Nifty returns 11% Nifty returns 10%

Nifty Low 7568 Nifty Low 7720 Nifty Low 8248

Nifty levels where FII major buying in Nifty Futures commenced

EM equity buying by FIIs post US QE3 (in US$)

Indonesia Phillipines Thailand S.Korea India

Dec -33 325 702 3299 4446

Jan 635 724 551 -1723 4096

Feb 1160 146 -583 1760 4142

Mar 189 204 208 -1885 1912

Apr 75 283 -682 -2584 951

May -33 448 -169 902 3772

Total 1993 2130 27 -231 19319

Jun -2033 -250 -1800 -4491 -1765

FIIs outflows started post hints of QE reduction

Nifty up-move continues postUS QE announcement (in Rs. Cr.)

Buying seen post ECB QE on 22 Jan 2015 (in US$)

-500

0

500

1000

1500

2000

2500

India Indonesia Philippines Thailand Brazil South

Africa

Turkey

DERIVATIVES STRATEGY

16250

22230 22123

10399

6407

21175

0

5000

10000

15000

20000

25000

Dec '2012 Jan Feb Mar Apr May

5640

5740

5840

5940

6040

6140

6240

FII Secondry Equity inflows ('000 Cr Inr) Nifty Spot

16ICICIdirect Money Manager February 2015

Last liquidity infusion cycle

was triggered by the US QE 3

of US$80 billion per month on

December 12, 2012.

As visible in the first chart

above, India stood to gain from

this liquidity infusion with

largest inflows of close to

US$20 billion in six months.

Also visible in the second chart

above is the price performance

of the Nifty (monthly high

values used in chart). There is a

c l e a r t r e n d o f p r i c e

performance from the Nifty as

FIIs flows increase.

On January 22, 2015 the

European Central Bank (ECB)

announced the US-styled QE

of buying €60 billion per month

until Sept ember 2016 totaling

€ 1.1 trillion. Along with this,

l iquidity is also gett ing

generated from Bank of Japan

(BoJ) and Peoples Bank of

China (PBOC).

FIIs are likely to allocate a lion's

share of equity allocation to

Ind ia as Ind ia ' s macro

conditions have improved

significantly.

Hence, the Nifty is likely to

FII flows in January: Win-win for Indian equities and debt at start of 2015

FIIs cash activity: strong buying post RBI rate cut

-5000

0

5000

10000

15000

20000

25000

30000

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

INR

is C

r

Debt markets flows stayed strong

-15000

-10000

-5000

0

5000

10000

15000

20000

Jan-

14

Feb-

14

Mar

-14

Apr-1

4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct-1

4

Nov

-14

Dec-

14

Jan-

15

INR

in C

r

As suggested in the previous

pages as well, FII inflows are

likely to see a pick-up in pace.

Historical evidence also

supports this view. Barring Q4

of 2008, 2009 & 2011, Q4 in last

10 fiscal years has attracted

strong FII equity inflows.

Hence, we believe FIIs inflows

will not only be eyeing existing

scale up higher as FII buying is

likely to be in blue chip stocks,

where sufficient float is

available.

DERIVATIVES STRATEGY

17ICICIdirect Money Manager February 2015

blue chip stocks to keep the

positive bias intact in Nifty. It

will also keep an eye on

impending OFS, which are

likely to be announced in the

foreseeable future.

FII buying in the debt segment

remained intact & they bought

over US$1.7 billion in January

as yields dipped over 20 basis

points to 7.70 on 10-year

benchmark (in the last three

months). From here on, yields

on the shorter end are likely to

remain more volatile than long

dated yields, as the RBI action

is likely to mainly impact the

shorter end.

India centric data points that

FIIs will be focusing on

includes consumer price index

(CPI) numbers and index of

industrial production (IIP)

numbers that could provide

insights into the RBI rate action

and, more importantly, the

Union Budget on February 28.

Bank Nifty: Likely to move towards

22000 above highest Put base of

20000

The Bank Nifty continues to

hold leadership position and

registered gains of over 12%

for the series. However, within

the banking space, there was a

clear preference for private

banking stocks as they posted

the strong set of quarterly

numbers while public sector

undertakings (PSU) banking

tumbled.

After struggling to move

beyond 2.27 for over a month,

the Bank Nifty/ Nifty price ratio

moved to 2.31 in the later part

of series. The price ratio is

likely to move towards 2.38

and the recent declines should

be bought with stop loss of

2.14.

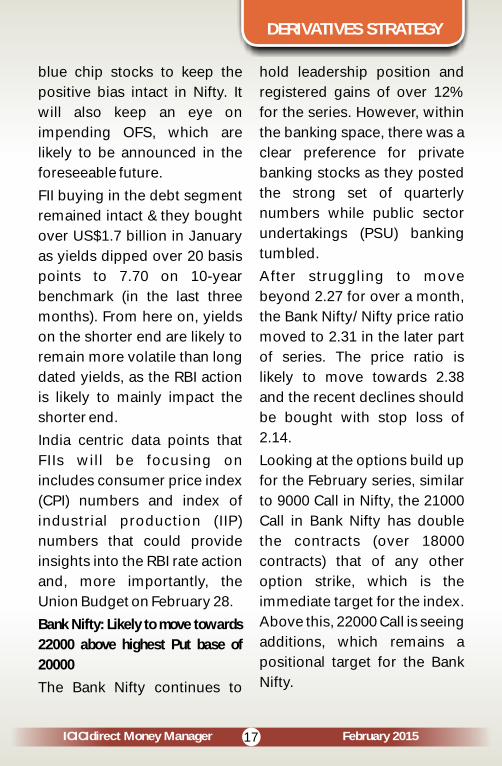

Looking at the options build up

for the February series, similar

to 9000 Call in Nifty, the 21000

Call in Bank Nifty has double

the contracts (over 18000

contracts) that of any other

option strike, which is the

immediate target for the index.

Above this, 22000 Call is seeing

additions, which remains a

positional target for the Bank

Nifty.

DERIVATIVES STRATEGY

18ICICIdirect Money Manager February 2015

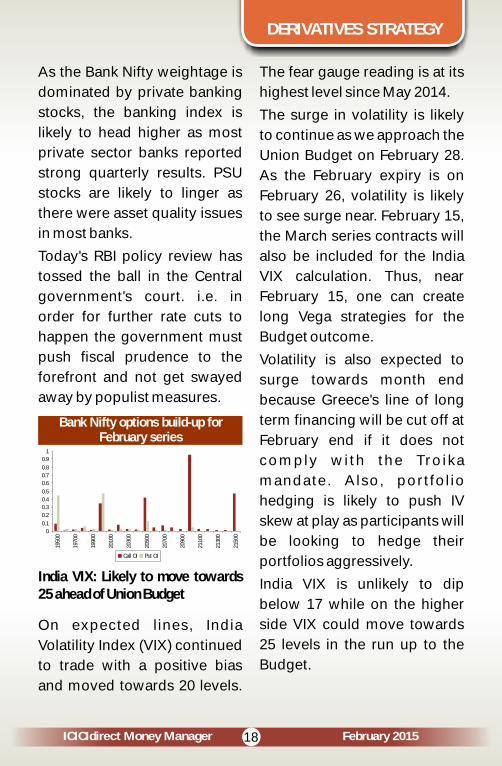

As the Bank Nifty weightage is

dominated by private banking

stocks, the banking index is

likely to head higher as most

private sector banks reported

strong quarterly results. PSU

stocks are likely to linger as

there were asset quality issues

in most banks.

Today's RBI policy review has

tossed the ball in the Central

government's court. i.e. in

order for further rate cuts to

happen the government must

push fiscal prudence to the

forefront and not get swayed

away by populist measures.

Bank Nifty options build-up forFebruary series

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

1950

0

1970

0

1990

0

2010

0

2030

0

2050

0

2070

0

2090

0

2110

0

2130

0

2150

0

Call OI Put OI

India VIX: Likely to move towards 25 ahead of Union Budget

On expected lines, India

Volatility Index (VIX) continued

to trade with a positive bias

and moved towards 20 levels.

The fear gauge reading is at its

highest level since May 2014.

The surge in volatility is likely

to continue as we approach the

Union Budget on February 28.

As the February expiry is on

February 26, volatility is likely

to see surge near. February 15,

the March series contracts will

also be included for the India

VIX calculation. Thus, near

February 15, one can create

long Vega strategies for the

Budget outcome.

Volatility is also expected to

surge towards month end

because Greece's line of long

term financing will be cut off at

February end if it does not

comply with the Troika

mandate. Also, portfolio

hedging is likely to push IV

skew at play as participants will

be looking to hedge their

portfolios aggressively.

India VIX is unlikely to dip

below 17 while on the higher

side VIX could move towards

25 levels in the run up to the

Budget.

DERIVATIVES STRATEGY

19ICICIdirect Money Manager February 2015

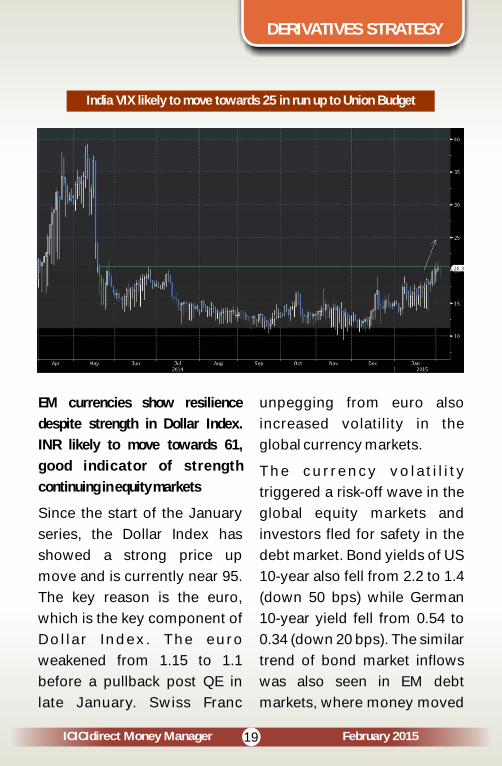

India VIX likely to move towards 25 in run up to Union Budget

EM currencies show resilience

despite strength in Dollar Index.

INR likely to move towards 61,

good indicator of strength

continuing in equity markets

Since the start of the January

series, the Dollar Index has

showed a strong price up

move and is currently near 95.

The key reason is the euro,

which is the key component of

Dol lar Index. The euro

weakened from 1.15 to 1.1

before a pullback post QE in

late January. Swiss Franc

unpegging from euro also

increased volatility in the

global currency markets.

The cu r rency vo la t i l i t y

triggered a risk-off wave in the

global equity markets and

investors fled for safety in the

debt market. Bond yields of US

10-year also fell from 2.2 to 1.4

(down 50 bps) while German

10-year yield fell from 0.54 to

0.34 (down 20 bps). The similar

trend of bond market inflows

was also seen in EM debt

markets, where money moved

DERIVATIVES STRATEGY

90

92

94

96

98

100

102

104

106

26

-Dec

28-

De

c

30

-Dec

1-J

an

3-J

an

5-Ja

n

7-J

an

9-Ja

n

11

-Jan

13

-Ja

n

15-

Jan

17

-Ja

n

19-

Jan

21

-Jan

23-J

an

25

-Jan

27-J

an

Dollar Index Euro Australian Dollar Japanese Yen

20ICICIdirect Money Manager February 2015

out from equities and moved

into the debt segment. These

strong debt market inflows

helped EM currencies to

prevent a depreciation trend.

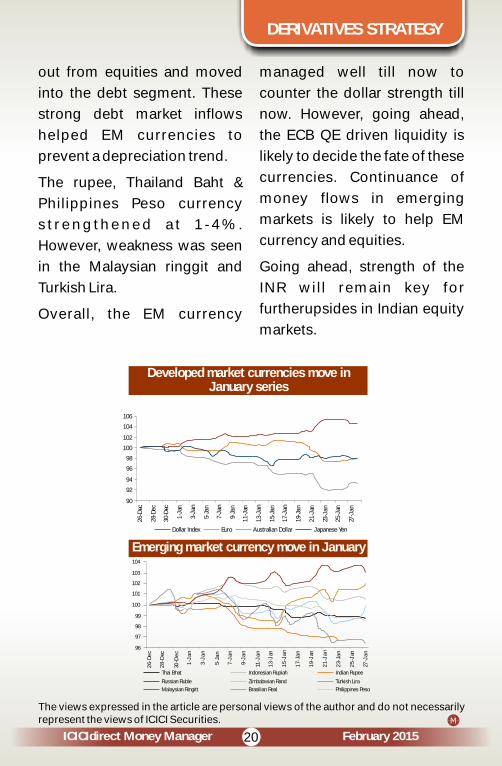

The rupee, Thailand Baht &

Philippines Peso currency

s t r e n g t h e n e d a t 1 - 4 % .

However, weakness was seen

in the Malaysian ringgit and

Turkish Lira.

Overall, the EM currency

managed well till now to

counter the dollar strength till

now. However, going ahead,

the ECB QE driven liquidity is

likely to decide the fate of these

currencies. Continuance of

money flows in emerging

markets is likely to help EM

currency and equities.

Going ahead, strength of the

INR will remain key for

furtherupsides in Indian equity

markets.

Developed market currencies move in January series

Emerging market currency move in January

96

97

98

99

100

101

102

103

104

26-

De

c

28

-Dec

30-D

ec

1-J

an

3-J

an

5-Ja

n

7-J

an

9-J

an

11-J

an

13

-Jan

15

-Ja

n

17-

Jan

19

-Jan

21

-Ja

n

23-

Jan

25

-Jan

27-J

an

Thai Bhat Indonesian Rupiah Indian Rupee

Russian Ruble Zimbabwian Rand Turkish Lira

Malaysian Ringitt Brasilian Real Philippines Peso

The views expressed in the article are personal views of the author and do not necessarily represent the views of ICICI Securities.

DERIVATIVES STRATEGY

21

STOCK IDEAS

ICICIdirect Money Manager February 2015

Century Plyboard (India): Structural shift… New thrust to growth…

Company Background

Century Plyboard (India) Ltd.

(CPIL) is India 's largest

plywood manufacturer with

~23-30% share of India's

organised plywood sector and

a market share of ~6-7.5% in

the overall market. The

company was promoted by

first generation entrepreneurs

Sajjan Bhajanka (Chairman),

Hari Prasad Agarwal (Vice

Chairman) and Sanjay Agarwal

(Managing Director) and ably

supported by Prem Kumar

Bhajanka (Joint MD), Vishnu

Khemani (Joint MD) as well as

experienced professionals.

CPIL is engaged in the

manufacture of plywood,

laminates, veneer, MDF,

blockboards and doors,

among others. The company is

also engaged in the Container

Freight Station (CFS) business,

managing the first private CFS

at the Kolkata Port. CPIL

recently launched retai l

furniture chain (brand Nesta)

with the launch of two owned

stores. CPIL has retained its

leadership in India's plywood

sector for more than two

decades, accounting for nearly

a third of all branded plywood

sold in India. The company

countered the progressive

c o m m o d i t i s a t i o n w i t h

increased average realisations

for its premium brands. Hence,

whereas the plywood industry

g r e w a t 5 - 7 % C A G R

(compounded annual growth

rate) over the last five years,

CPIL has grown at 17% CAGR

led by market share gains from

the unorganised segment.

Leading player with strong brand

equity & robust distribution

network

The Indian plywood industry is

worth ~ 15,000-16,000 crore

where the organised segment

accounts for ~25-30% of the

overall market. CPIL, with a

capacity of 2,09,420 cubic

metres (CBM) in FY14, is the

leading player in the plywood

industry. The company enjoys

Investment Rationale

`

22ICICIdirect Money Manager February 2015

~ 2 3 - 3 0 % s h a r e o f t h e

organised market with strong

b r a n d s a c r o s s p r o d u c t

categories and a robust pan-

India distribution network

comprising 33 marketing

offices, 1,424 dealers, 6,333

employees and more than

13,000 retail outlets.

Myanmar ban & GST roll out –

structurally positive for organised

pie

In April 2014, Myanmar

banned the export of raw

timber logs, putting Indian

plywood players at a huge

disadvantage as they were

h e a v i l y d e p e n d e n t o n

Myanmar for raw timber.

However, CPIL had proactively

set up a plant in Myanmar to

process raw timber providing

security on face veneer (key

component for plywood). This

has helped the company to

gain a first mover advantage

over others. Secondly, with the

rollout of GST (goods &

services tax), the pricing

difference between organised

and unorganised players due

to tax inequalities is likely to

narrow down providing a level

playing field to organised

players. Hence, we believe

CPIL will reap the benefits of a

s t ructura l shi f t towards

organised players.

Set to ride expanding organised pie;

initiate with BUY

Like other building materials

such as tiles, we envisage the

Indian organised plywood

player's pie (currently stands at

~ 3,500-4,500 crore) will

expand in coming years on the

back of structural changes like

rollout of GST, ban on raw

material from Myanmar and

higher brand aspirations. CPIL

is likely to see exponential

earnings growth of 52% in

FY14-17E with a significant

improvement in return ratios

and leverage making a strong

case for a further re-rating.

Hence, we initiate coverage on

C P I L w i t h a B U Y

recommendation and a target

price of 254 (24x FY17E EPS

implying a PEG (price/earnings

to growth) of 0.5x).

`

`

STOCK IDEAS

STOCK IDEAS

23ICICIdirect Money Manager February 2015

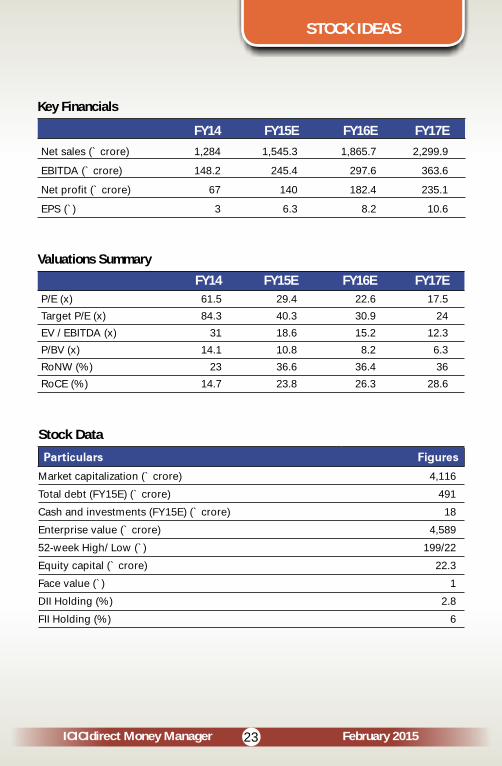

Key Financials

Net sales ( crore) 1,284 1,545.3 1,865.7 2,299.9

EBITDA ( crore) 148.2 245.4 297.6 363.6

Net profit ( crore) 67 140 182.4 235.1

EPS ( ) 3 6.3 8.2 10.6

FY14 FY15E FY16E FY17E

`

`

`

`

Valuations Summary

P/E (x) 61.5 29.4 22.6 17.5

Target P/E (x) 84.3 40.3 30.9 24

EV / EBITDA (x) 31 18.6 15.2 12.3

P/BV (x) 14.1 10.8 8.2 6.3

RoNW (%) 23 36.6 36.4 36

RoCE (%) 14.7 23.8 26.3 28.6

FY14 FY15E FY16E FY17E

Stock Data

Market capitalization ( crore) 4,116

Total debt (FY15E) ( crore) 491

Cash and investments (FY15E) ( crore) 18

Enterprise value ( crore) 4,589

52-week High/ Low ( ) 199/22

Equity capital ( crore) 22.3

Face value ( ) 1

DII Holding (%) 2.8

FII Holding (%) 6

`

`

`

`

`

`

`

STOCK IDEAS

Key RisksLack of raw material availability

and high raw material costThe industry procures majority

of its raw material from

Myanmar as well as countries

l ike Vietnam, Indonesia,

Thailand, Germany, etc. We

believe the biggest risk for

CPIL/industry is its inability to

procure raw material due to

any unforeseen regulation in

the respective jurisdiction e.g.

Myanmar's ban on raw timber

export. However, we believe

CPIL is well placed in terms of

raw material security after

setting up a peeling unit in

Myanmar to facilitate the

sourcing of face veneers.

Forex volatilityT h e c o m p a n y i m p o r t s

substantially for its raw

material requirements. CPIL

reviews foreign currency risk

periodically and takes hedging

initiatives accordingly. If the

anticipated forex (foreign

exchange) loss is more than

the cost of hedging only then

does CPIL prefer to hedge.

Otherwise, CPIL defers its

forex liabilities by availing

overseas buyer 's credit ,

avoiding exchange losses and

s u b s t a n t i a l l y l o w e r i n g

borrowing costs. On account

of this strategy, CPIL lost Rs. 44

crore in FY14. This deeply

impacted its profitability.

Recently, CPIL reduced its

buyer's credit exposure. Also,

g o i n g f o r w a r d , t h e

management is expecting the

same trend to continue, hence,

mitigating the forex related

volatility.

(EBITDA: Earnings before

interest, taxes, depreciation,

a n d a m o r t i z a t i o n ;

EPS:Earnings per share; P/E:

P r i c e - t o - e a r n i n g s ; E V :

Enterprise value; P/BV: Price-

to-book value; RoNW: Return

on Net Worth; RoCE: Return on

C a p i t a l E m p l o y e d ; D I I :

D o m e s t i c I n s t i t u t i o n a l

I n v e s t o r s ; F I I : Fo r e i g n

Institutional Investors)

24ICICIdirect Money Manager February 2015

25ICICIdirect Money Manager February 2015

KSB Pumps: Quality play, master of fluid control

Company BackgroundKSB Pumps (KSB), a subsidiary of KSB AG, Germany (global l e a d e r i n p u m p manufacturing), is a pumps & v a l v e s m a n u f a c t u r e r domestically based out of Pune. The company has been at the forefront of importing technology from its parent for delivering cutting edge, high quality products in the domestic market. Globally, KSB AG is one of the largest pump manufacturers with sales in excess of €2.2 billion (~US$2.8 billion) out of the total pump market, which is pegged at US$47 billion as of 2014. In India, KSB supplies pumps and valves to all major industries viz. power, waste water treatment, irrigation (agriculture), chemicals, etc. KSB's products are used for pumping, transportation and flow control of fluids, which include clean or contaminated w a t e r, e x p l o s i v e f l u i d s , corrosive and viscous fluids, slurries and fluid/solid mixtures. In India, KSB has a wide distr ibut ion network that includes four zonal offices, 15 branch off ices, over 800 authorised dealers, four service stations, 110 authorised service centres and 22 warehouses. In

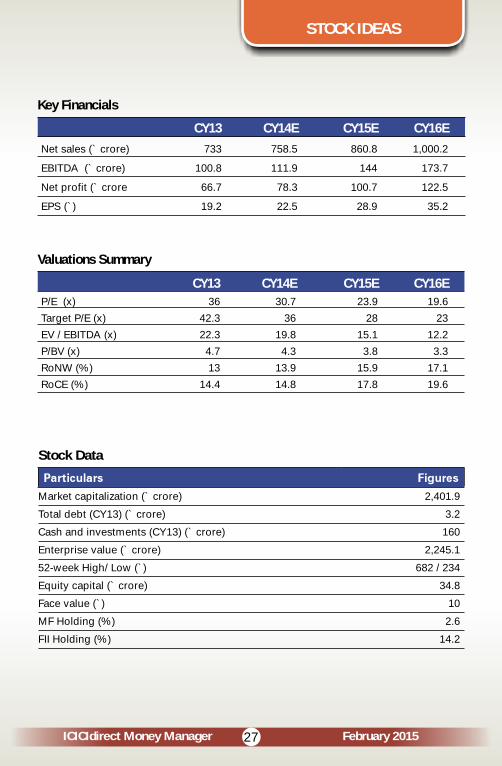

Cy13, pumps comprised 82% ( 603 c rore ) wh i le va lves comprised 17% ( 122 crore) of total sales ( 733 crore). The company clocked an EBITDA (earnings before interest, taxes, depreciation, and amortization) of Rs. 101 crore (EBITDA margins 14%) in CY13 with corresponding PAT (profit after tax) at 67 crore.

Indian pump market on strong footing; KSB well placed

As per industry sources, the global pump market size is pegged at US$47 billion as of 2014 and is expected to reach US$56 billion in 2017, growing at a CAGR (compounded annual growth rate) of 6% in CY14-17E. The Indian pump market size is pegged at ~Rs. 8,500 crore as of 2014; wherein a majority of it i.e. ~95% (~ 8,000 crore) consists of centrifugal pumps while the remaining i.e. 5% (~ 500 crore) c o m p r i s e s p o s i t i v e displacement pumps. The Indian pump market is expected to grow at a CAGR of 10% in FY14-17E to 11,300 crore in FY17E on the back of thrust of the new government on augmenting the domestic

`

``

`

`

`

`

Investment Rationale

STOCK IDEAS

26ICICIdirect Money Manager February 2015

manufacturing and pumps being an integral part of process manufacturing. In India, KSB commands a market share of ~7% (pump sales of 603 crore in Cy13), wherein it supplies ~35% of its pumps in the standard pumps segment (used for irrigation & building services) while it supplies the remaining 65% of its pumps (~ 400 crore sales vis-à-vis market size of ~ 4,500 crore, market share ~9%) to the industrial segment, which is technology intensive. Going forward, we expect KSB's pump sales to grow at a CAGR of 13.1% in CY13-16E to Rs. 876 crore in CY16E.

Valves segment, focus on increasing profitability; not chasing growth

Valves constitute ~17% ( 122 crore in CY13) of consolidated sales. The performance of valves has been a laggard in the past few quarters on account of fierce competition and subdued demand (a majority of which is accounted by oil & gas sector). Going forward, KSB expects to consolidate its position in the valves market with focus on increasing profitability rather than chasing sales growth. Going forward, post a blip in CY14E, we expect valves sales to largely remain flat with CY16E sales at 122 crore. KSB also

`

``

`

`

owns 49% in MIL Controls Ltd (51% ownership with KSB AG) with an initial investment of 6.3 crore, on which it is reaping rich benefits (share of profit at 9.6 crore in CY13; RoI (return on investment) ~150%).

Likely beneficiary of capex cycle revival; balance sheet strength to grow; initiate with BUY

By virtue of KSB focusing only on non-project businesses (unlike its peers) it generates robust free cash flows and maintains working capital discipline with CY13 Free Cash Flow (FCF) yield at 4.2%. KSB is likely to realise operating leverage benefits (margin expansion of 360 basis points (bps) and PAT CAGR of 22.5% in CY13-16E) in the form of higher demand for its products. This may lead to improvement in return on equity (RoE) & return on capital employed (RoCE) and strong FCF generation of 90 crore in CY15E and Rs. 114 crore in CY16E. Going forward, we expect KSB's sales and PAT to grow at a CAGR of 10.8% and 22.5%, respectively, in Cy13- 16E. We assign a 23x P/E (1x PEG (price/earnings to growth)) on KSB's CY16E EPS of 35.2 to arrive at a target price of 810 and assign a BUY rating on the stock.

`

`

`

``

STOCK IDEAS

27ICICIdirect Money Manager February 2015

STOCK IDEAS

Key Financials

Net sales ( crore) 733 758.5 860.8 1,000.2

EBITDA ( crore) 100.8 111.9 144 173.7

Net profit ( crore 66.7 78.3 100.7 122.5

EPS ( ) 19.2 22.5 28.9 35.2

CY13 CY14E CY15E CY16E

`

`

`

`

Valuations Summary

P/E (x) 36 30.7 23.9 19.6

Target P/E (x) 42.3 36 28 23

EV / EBITDA (x) 22.3 19.8 15.1 12.2

P/BV (x) 4.7 4.3 3.8 3.3

RoNW (%) 13 13.9 15.9 17.1

RoCE (%) 14.4 14.8 17.8 19.6

CY13 CY14E CY15E CY16E

Stock Data

Market capitalization ( crore) 2,401.9

Total debt (CY13) ( crore) 3.2

Cash and investments (CY13) ( crore) 160

Enterprise value ( crore) 2,245.1

52-week High/ Low ( ) 682 / 234

Equity capital ( crore) 34.8

Face value ( ) 10

MF Holding (%) 2.6

FII Holding (%) 14.2

`

`

`

`

`

`

`

28ICICIdirect Money Manager February 2015

STOCK IDEAS

Key Risks

Volatility in raw materials prices, especially steel price

Iron derivative products like pig iron, iron castings, stampings, metal scrap, etc. form the major raw material costs for pumps & valves with the management guiding that ~35% of the sales value is composed of iron p r o d u c t s ( 3 5 % o f s a l e s equivalent to ~80% of raw material costs; raw material as a percentage of sales at ~45%). We have modeled steel price to be a complete pass through for the company. However, any inability of the company to pass through the increase in steel costs will dent EBITDA margins and will have a consequent negative impact on our target price calculation. It has been observed that for every 5% increase in steel price and KSB's pump realisation remaining same; our target price reduces by ~12.7% i.e. Rs. 103/share.

Increase in royalty to the parent i.e. KSB AG

By virtue of technology transfer and support from the parent group i.e. KSB AG; KSB pays a royalty fee amounting to ~2% of its sales. The company's management has guided for a royalty payment of 2-5% (of sales value) depending upon the product to its parent company. The total royalty outgo consists of direct royalty payments,

professional fee and technical fee. Therefore, any increase in the roya l ty outgo (as a percentage of sales), going forward, will have an adverse impact on the company's profitability with a direct impact on our target price calculations.

Increase in commission to sole selling agent i.e. KSB Singapore

KSB has appointed its sister concern i.e. KSB Singapore (Asia Pacific) Pte Ltd as its sole selling agent in all territories outside India (exports) for a period of three years from February 20, 2014. The company is authorised to pay up to 12.5% of sales (value) as commission to the aforesaid entity. However, currently, for the past few years i.e. CY10-13, this commission is being paid at ~10%. Therefore, going forward, any increase in this commission paid to this sole selling agent i.e. KSB Singapore will have adverse impact on the company profitability, thereby directly impacting our target price calculation.

(EBITDA : Earnings before interest, taxes, depreciation, and amortization; EPS:Earnings per share; P/E: Price-to-earnings; EV: Enterprise value; P/BV: Price-to-book value; RoNW: Return on net worth; RoCE: Return on Capital Employed; MF: Mutual Funds; F I I : Fore ign Ins t i tu t iona l Investors)

29ICICIdirect Money Manager

FLAVOUR OF THE MONTH

A goal-based approach to investing

February 2015

For most of investors, “return” is the basic criterion for choosing an investment. In this race, we generally miss out on the bigger picture. We miss to ask whether our investments will be able to help us reach our financial goals, which is the core purpose of making an investment. Instead of paying greater attention to products and their performance, it is important to focus on our goals and invest accordingly. Investing towards a specific goal is more precise and detailed way of investing. It goes beyond the performance of a portfolio and focuses more on matching your financial resources with your financial goals and liabilities. There is a 50% greater probability of reaching your goals with a goal-based investing compared to traditional product-centric approach, says an international study. Read on to find out how by adopting a goal-based investing approach you can have a better chance of meeting your goals.

We aren't always rational

Most of us understand the

importance of sticking to a

d i s c i p l i n e d i n v e s t m e n t

strategy. Yet, we can often

make investment decisions

that could hurt our financial

well-being and our goals. For

instance, we may fall prey to

buying the latest hot stock or

get panicked by market

volatility and dump a well-

designed investment plan.

This behavior, known as

'irrational investment behavior'

in behavioral finance parlance,

is common among investors.

The challenge is to overcome

such behavior and stay

invested for goals. That is

w h e r e t h e g o a l - b a s e d

investing comes into picture.

For most of us, the investing

process goes like this usually:

We identify two or three goals

and then invest into avenues

by creating a single portfolio.

We expect a standard rate of

return on our investmentbased

on the historic performance,

and strive to achieve that

return or even greater than

that.

However, it does not make

Goal-based investing: What is it and

how is it different?

30ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

sense to identify different

goals and creating a single

portfolio for all the goals.

This is because, our goals

differ in terms of importance,

time horizon and the level of

risk we are comfortable taking

relative to each goal. For

example, we would want to

take less risk with the funds

designated for critical goals

that are short-term in nature,

while would be ok to accept

more risk for discretionary

goals, which are long-term in

nature.

Creating a separate portfolio or

a bucket for each goal provides

a much clearer picture of how

well we are succeeding. This

approach also greatly reduces

the influence of emotions that

often play a role in our financial

decisions and goals.

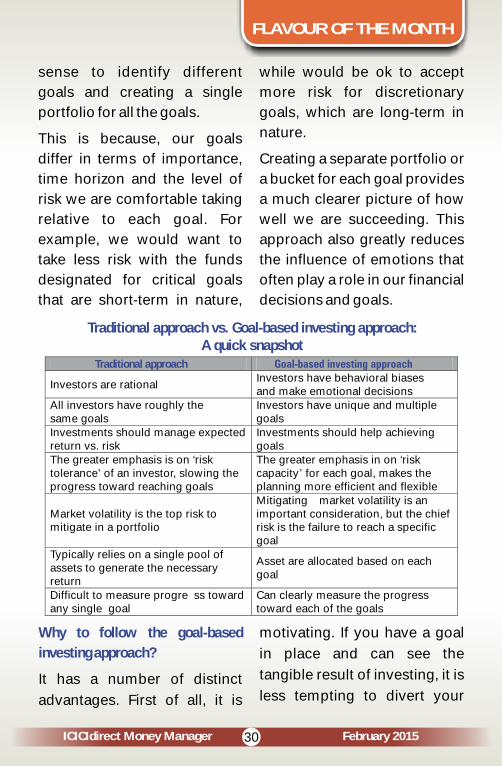

Traditional approach vs. Goal-based investing approach: A quick snapshot

Traditional approach

Investors are rational Investors have behavioral biasesand make emotional decisions

All investors have roughly the

same goals

Investors have unique and multiple goals

Investments should manage expected return vs. risk

Investments should help achieving goals

The greater emphasis is on ‘risk tolerance’ of an investor, slowing the progress toward reaching goals

The greater emphasis in on ‘risk capacity’ for each goal, makes the planning more efficient and flexible

Market volatility is the top risk to mitigate in a portfolio

Mitigating market volatility is an important consideration, but the chief risk is the failure to reach a specific goal

Typically relies on a single pool of assets to generate the necessary return

Asset are allocated based on each goal

Difficult to measure progre ss toward any single goal

Can clearly measure the progress toward each of the goals

Why to follow the goal-based

investing approach?

It has a number of distinct

advantages. First of all, it is

motivating. If you have a goal

in place and can see the

tangible result of investing, it is

less tempting to divert your

31ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

money towards discretionary

items such as a vacation.

Investing based on goals also

imposes discipline. It helps

you focus on exactly what you

are trying to achieve. It then in

turn helps you invest in

avenues based on your goals

and time horizon.

Further, goal-based investing

helps you take the amount of

risk that is needed. It helps you

avoid taking excessive risk by

trading or churning your

portfolios, either to recoup the

losses or to reach an anchored

target rate of return.

Goal-based investing also

helps to track down the

progress towards our goals. It

then helps in making the

necessary changes to our

investment strategy and

contribution level if we move

ahead of our target or fall

behind.

Amit, Anil and Pankaj, each 35

years of age, are married and

The story of three friends

have a child of 3 years old. The

trio works with an IT company

and has a similar income level.

However, when it comes to

managing personal finances,

their approach is quite different

than each other.

For instance, Amit has little

idea of investments and

invests mainly into fixed

deposits. He has no idea how

inflation affects one's finances

and has no plans for the future.

Anil, on the other hand, is

aware of a few financial goals

that he wants to achieve in his

life. However, most of his

investments are for the

purpose of saving taxes. While

Pankaj is the most organized

among the lot; he is well aware

of his financial goals and has

also written and quantified it

down.

Let's take a look at their current

financial position and their

investment plans.

32ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

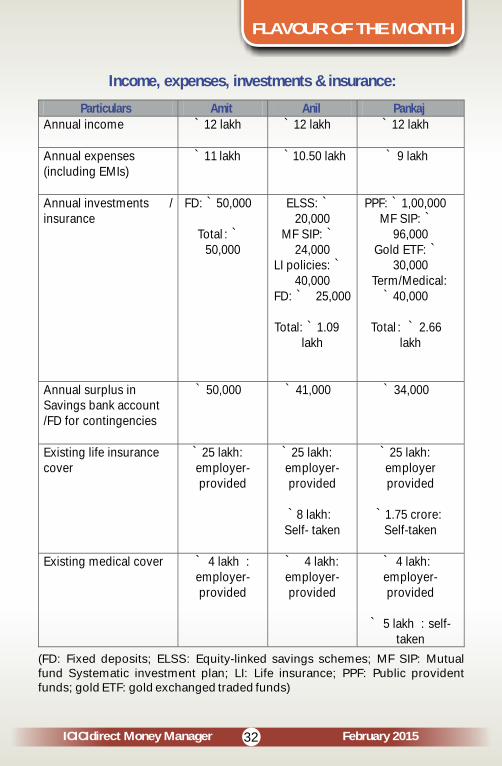

Income, expenses, investments & insurance:

Particulars

Amit

Anil

PankajAnnual income

` 12 lakh

` 12 lakh

` 12 lakh

Annual expenses

(including EMIs)

` 11

lakh

` 10.50 lakh

` 9 lakh

Annual investments / insurance

FD: ` 50,000

Total : `50,000

ELSS: `20,000

MF SIP: ` 24,000

LI policies: ` 40,000

FD: ` 25,000

Total: `

1.09 lakh

PPF: 1,00,000`MF SIP: `

96,000Gold ETF: `

30,000Term/Medical:

` 40,000

Total : ` 2.66 lakh

Annual surplus in Savings bank account

/FD for contingencies

` 50,000

` 41,000

` 34,000

Existing life insurancecover

` 25 lakh: employer-provided

` 25 lakh: employer-provided

` 8 lakh: Self- taken

` 25 lakh: employer provided

` 1.75 crore: Self-taken

Existing medical cover ` 4 lakh :employer-provided

` 4 lakh:employer-provided

` 4 lakh: employer-provided

` 5 lakh : self-taken

(FD: Fixed deposits; ELSS: Equity-linked savings schemes; MF SIP: Mutual fund Systematic investment plan; LI: Life insurance; PPF: Public provident funds; gold ETF: gold exchanged traded funds)

33ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

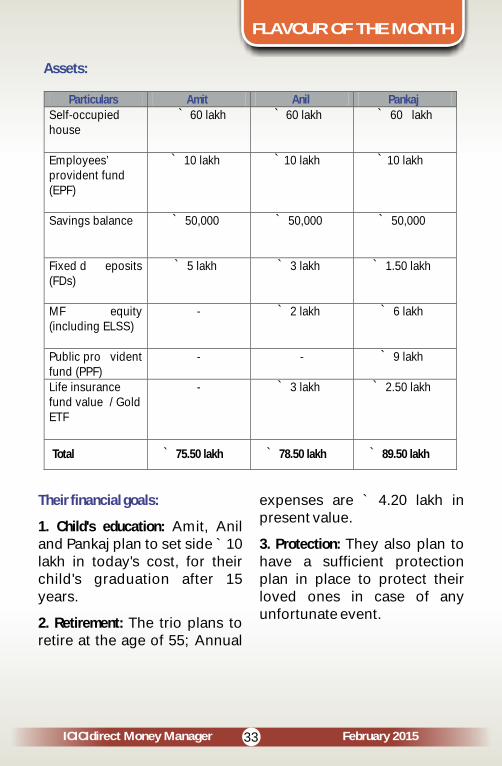

Assets:

Particulars Amit Anil PankajSelf-occupied house

` 60 lakh

` 60 lakh ` 60 lakh

Employees’ provident fund (EPF)

` 10 lakh

` 10 lakh

` 10 lakh

Savings balance

` 50,000

` 50,000

` 50,000

Fixed d eposits

(FDs)` 5 lakh

` 3 lakh

` 1.50 lakh

MF equity (including ELSS)

- ` 2 lakh

` 6 lakh

Public pro vident fund (PPF)

-

-

` 9 lakh

Life insurance fund value

/ Gold

ETF

-

` 3 lakh

` 2.50 lakh

Total ` 75.50 lakh ` 78.50 lakh ` 89.50 lakh

Their financial goals:

1. Child's education: Amit, Anil and Pankaj plan to set side 10 lakh in today's cost, for their child's graduation after 15 years.

2. Retirement: The trio plans to retire at the age of 55; Annual

`

expenses are 4.20 lakh in present value.

3. Protection: They also plan to have a sufficient protection plan in place to protect their loved ones in case of any unfortunate event.

`

34ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

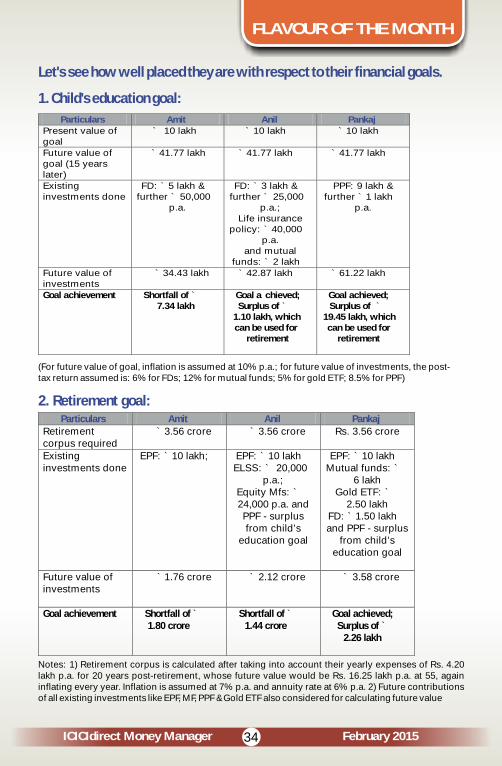

Let's see how well placed they are with respect to their financial goals.

1. Child's education goal:

Particulars Amit Anil PankajPresent value of goal

` 10 lakh ` 10 lakh ` 10 lakh

Future value of goal (15 years later)

` 41.77 lakh

` 41.77 lakh

` 41.77 lakh

Existing investments done

FD: 5 lakh & `further ` 50,000

p.a.

FD: 3 lakh & `further ` 25,000

p.a.;

Life insurance policy: 40,000 `

p.a.

and mutual

funds: `

2 lakh

PPF: 9 lakh & further 1 lakh `

p.a.

Future value of investments

` 34.43 lakh

` 42.87 lakh

` 61.22 lakh

Goal achievement

Shortfall of `7.34 lakh

Goal a chieved; Surplus of `

1.10 lakh, which can be used for

retirement

Goal achieved; Surplus of `

19.45 lakh, which can be used for

retirement

(For future value of goal, inflation is assumed at 10% p.a.; for future value of investments, the post-tax return assumed is: 6% for FDs; 12% for mutual funds; 5% for gold ETF; 8.5% for PPF)

2. Retirement goal:Particulars Amit Anil Pankaj

Retirement corpus required

` 3.56 crore ` 3.56 crore Rs. 3.56 crore

Existing investments done

EPF: 10 lakh;` EPF: 10 lakh` ELSS: 20,000 `

p.a.;

Equity

Mfs: `24,000 p.a. and PPF

-

surplus from child’s

education goal

EPF: 10 lakh`Mutual funds: `

6 lakhGold ETF: `

2.50 lakhFD: 1.50 lakh `and PPF - surplus

from child’s education goal

Future value of investments

` 1.76 crore

` 2.12 crore

` 3.58 crore

Goal achievement

Shortfall of `1.80 crore

Shortfall of `1.44 crore

Goal achieved; Surplus of `

2.26 lakh

Notes: 1) Retirement corpus is calculated after taking into account their yearly expenses of Rs. 4.20 lakh p.a. for 20 years post-retirement, whose future value would be Rs. 16.25 lakh p.a. at 55, again inflating every year. Inflation is assumed at 7% p.a. and annuity rate at 6% p.a. 2) Future contributions of all existing investments like EPF, MF, PPF & Gold ETF also considered for calculating future value

35ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

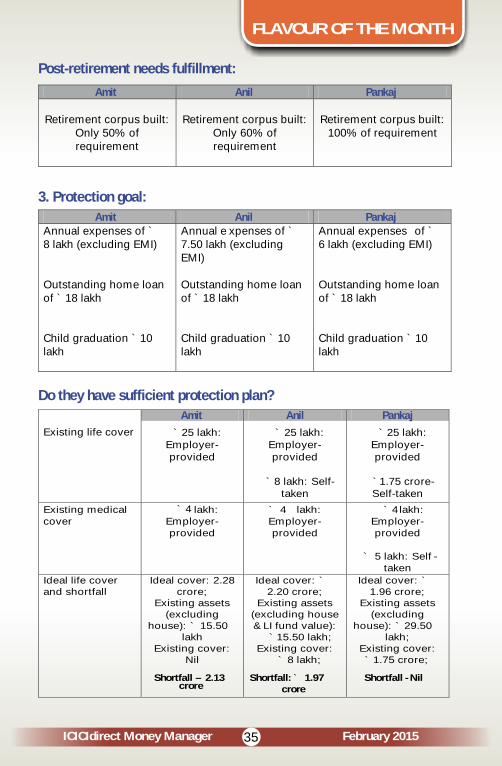

Post-retirement needs fulfillment:

Amit

Anil

Pankaj

Retirement corpus built: Only 50% of requirement

Retirement corpus built: Only 60% of requirement

Retirement corpus built: 100% of requirement

3. Protection goal:

Amit Anil PankajAnnual expenses of `8 lakh (excluding

EMI)

Outstanding home loan of 18 lakh ̀

Child graduation 10 `lakh

Annual e xpenses of `7.50 lakh (excluding EMI)

Outstanding home loan of 18 lakh`

Child graduation 10 `

lakh

Annual expenses of `6 lakh (excluding EMI)

Outstanding home loan of 18 lakh`

Child graduation 10 `

lakh

Do they have sufficient protection plan?

Existing life cover

Amit Anil Pankaj

` 25 lakh: Employer-provided

` 25 lakh: Employer-provided

`

8 lakh: Self-taken

` 25 lakh:

Employer-provided

` 1.75 crore-Self-taken

Existing medical cover

` 4

lakh: Employer-provided

` 4

lakh: Employer-provided

` 4lakh:

Employer-provided

` 5 lakh: Self -taken

Ideal life cover and shortfall

Ideal cover:

2.28 crore;

Existing assets (excluding

house): ` 15.50 lakh

Existing cover: Nil

Shortfall – 2.13 crore

Ideal cover: ` 2.20 crore;

Existing assets (excluding house & LI fund value):

` 15.50 lakh;Existing cover:

` 8 lakh;

Shortfall: ` 1.97 crore

Ideal cover: ` 1.96 crore;

Existing assets (excluding

house): ` 29.50 lakh;

Existing cover: ` 1.75 crore;

Shortfall - Nil

36ICICIdirect Money Manager

FLAVOUR OF THE MONTH

February 2015

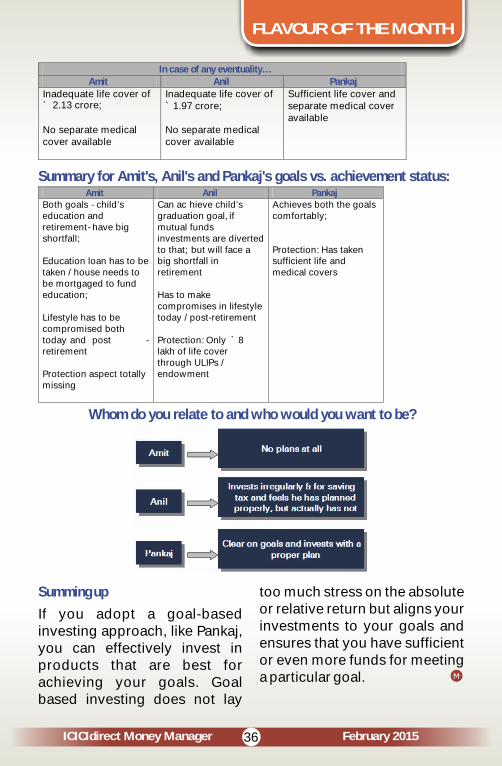

In case of any eventuality…Amit Anil

Pankaj

Inadequate life cover of ` 2.13 crore;

No separate medical cover available

Inadequate life cover of ` 1.97 crore;

No separate medical cover available

Sufficient life cover and separate medical cover available

Summary for Amit's, Anil's and Pankaj's goals vs. achievement status:Amit Anil Pankaj

Both goals - child’s education and retirement - have big shortfall;

Education loan has to be taken / house needs to be mortgaged to fund education;

Lifestyle has to be compromised both today and post -retirement

Protection aspect totally missing

Can ac hieve child’sgraduation goal, if mutual funds investments are diverted to that; but will face a big shortfall in retirement

Has to make compromises in lifestyle today / post-retirement

Protection: Only ` 8lakh of life cover through ULIPs / endowment

Achieves both the goals comfortably;

Protection: Has taken sufficient life andmedical covers

Whom do you relate to and who would you want to be?

Summing up

If you adopt a goal-based investing approach, like Pankaj, you can effectively invest in products that are best for achieving your goals. Goal based investing does not lay

too much stress on the absolute or relative return but aligns your investments to your goals and ensures that you have sufficient or even more funds for meeting a particular goal.

37ICICIdirect Money Manager

'Longer duration strategies to benefit the most'

The rate cut by RBI was widely expected by the market with only the timing in question. 2015 may see an extended rate cut cycle, which will allow yields to fall across the curve, says R Sivakumar, Head - Fixed Income, Axis Mutual Fund, in an interview with ICICIdirect Money Manager. In a scenario like this, the longer duration strategies have the highest potential for mar-to-market gains as compared to short-term funds that run a lower duration, he adds. Excerpts:

R Sivakumar,

Head - Fixed Income,

Axis Mutual Fund

Tête-à-tête

February 2015

Q:

A:

How do you sum up the calendar

year 2014 for debt market and what

is your assessment for the year

2015?

The bond markets had a

great run in the second half of

2014. Markets spent the first

half of the year worrying about

El Nino, monsoon and food

inflation and potential for

further rate hikes from the

Reserve Bank of India (RBI).

However, our reading right

through the year was that

inflation momentum was

waning and would be reflected

in the headline numbers

shortly. The confidence on the

dis-inflationary trend was on

account of muted Minimum

Support Price (MSP) hikes,

weak growth and low pricing

power, and large output gap in

the economy. As these forces

played out in the second half of

the year and were supported

by the sharp fall in global

commodity prices, the market

started pricing rate cuts from

the RBI and the bond rally

started in earnest.

What is your take on the

surprising rate cut by RBI ahead of

its monetary policy? How extensive

Q:

38ICICIdirect Money Manager February 2015

Tête-à-tête

would the future rate cuts be?

The rate cut was widely

expected by the market with

only the timing in question.

2015 may see an extended rate

cut cycle by the RBI which will

allow yields to fall across the

curve. The extent of rate cuts

will depend on the inflation

trajectory. RBI will look beyond

the current inflation prints to

the medium term outlook for

inflation. The factors that the

RBI will look apart from

inflation to determine policy

action are fiscal outlook and

global market developments -

especially potential rate hikes

by the US Fed.

How do you expect the entire

yield curve to move in 2015?

The yield curve will take its

cues from policy expectations

and incoming data. We expect

yields to fall across the curve

during the rate cut cycle but

the fall in yields may be front

loaded as the market is not

likely to wait for RBI action

o n c e t h e d a t a s e e m s

supportive.

A:

Q:

A:

Q:

A:

Q:

A:

Foreign institutional inflows into

Indian debt market have been

strong in 2014. Will this continue

and why?

India will continue to see

strong interest from foreign

investors due to the high yields

a n d a t t r a c t i v e m a c r o

prospects. However the extent

of flows will also depend on the

elbow room made available by

RBI on additional foreign debt

limits.

Why the crude oil prices have

been falling lately? How do you

think it will affect globally and

domestically? How is India

prepared for any sharp rebound in

prices?

Oil prices are reacting to the

changed demand-supply

dynamics - specifically the

sharply higher supply from US

as also the weaker prospects

f r o m g l o b a l d e m a n d

(especially China). Indian

macro is currently on a sound

footing and we expect that the

economy should be able to

handle any shorter term

volatility in crude prices going

39ICICIdirect Money Manager February 2015

Tête-à-tête

forward. Sustained higher

prices will however have an

i m p a c t o n i n f l a t i o n

expectations.

Rupee has been depreciating

against US dollar. What are the