Embed Size (px)

DESCRIPTION

http://www.themusichall.org/pdfs/campaign/TTF_Brochure.pdf

Citation preview

plans: the lobby

Lob

by•

New

fam

ily re

stroo

m an

d la

rger

men

’s ro

om

• Sp

acio

us w

omen

’s ro

om w

ith ea

sy ac

cess

ibili

ty, n

ine s

talls

•

Dra

mat

ical

ly in

crea

sed

ener

gy effi

cien

cy w

ith n

ew L

ED

light

ing a

nd H

VAC

syst

em

• Lo

bby t

empe

ratu

re st

able

thro

ugh

all s

easo

ns w

ith zo

ned

heat

ing a

nd co

olin

g•

Expa

nded

new

conc

essio

n an

d ga

ther

ing s

pace

• Im

prov

ed el

evat

or w

ith in

crea

sed

acce

ssib

ility

and

ease

of u

se•

New

box

offi

ce, r

eloc

ated

to fr

ont o

f the

bui

ldin

g; n

ew ve

stibu

les

• Be

hind

the s

cene

s – g

roup

dre

ssin

g roo

m fo

r cho

ruse

s and

dan

ce tr

oupe

s

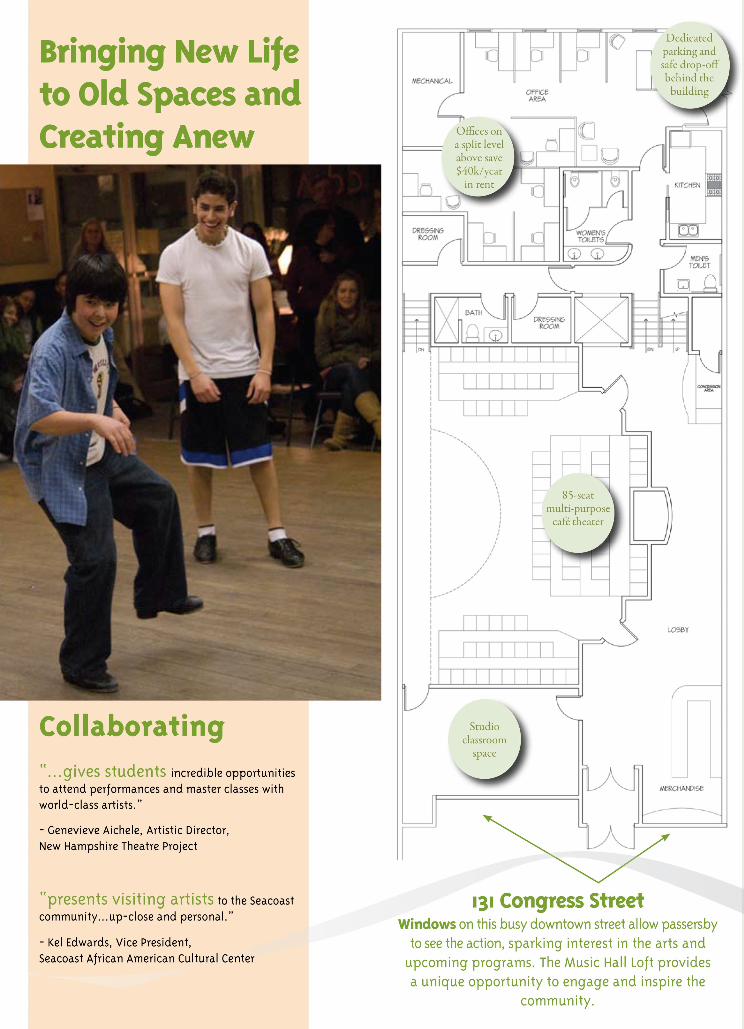

plans: the loft

Loft• Studio classroom space for master classes, workshops, programming and educational initiatives

• 85-seat multi-purpose café theater – could serve as a screening room, festival satellite site or lecture space

• Dedicated parking and safe drop off

• Relocated administrative offices save The Music Hall $40,000 in annual rent

• Windows on Congress Street allow passersby to see the action, sparking interest in the arts and upcoming programs. Music Hall literature and work by perform-ing artists and community partners on display and for sale

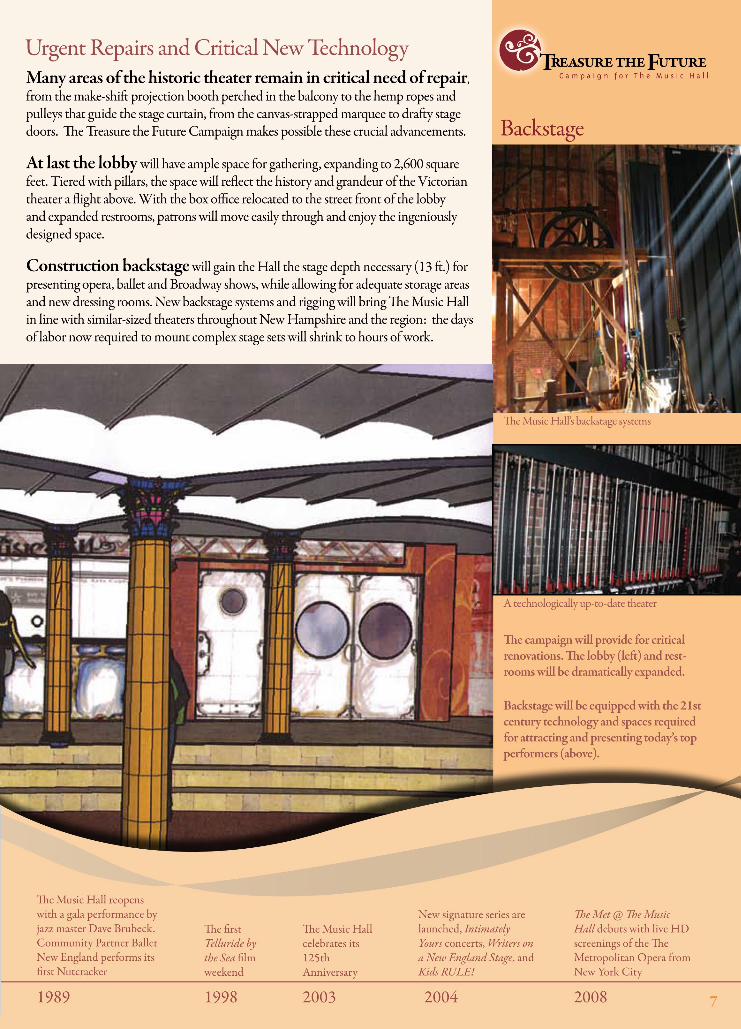

plans: backstage

Back

stag

e •

Rel

ocat

ed d

ress

ing r

oom

blo

ck –

pro

fess

iona

l spa

ce fo

r pe

rfor

mer

s with

new

gre

en ro

om an

d dr

essin

g roo

ms

• C

ritic

al sp

ace f

or p

rodu

ctio

n su

ppor

t inc

ludi

ng o

ffice

s an

d st

orag

e for

sets

, pro

ps, i

nstr

umen

ts, a

nd co

stum

es

• 19

01 h

emp

and

sand

bag s

yste

m re

tired

for n

ew te

chno

logy

Fu

ll el

ectr

ical

and

HVA

C u

pgra

de•

Stag

e ret

urne

d to

the 3

5-ft

dept

h re

quire

d fo

r cur

rent

tour

ing s

how

s–

new

capa

city

for b

alle

t, op

era a

nd b

road

way

per

form

ance

s

tax advantages of giving: new hampshire

1. Assume a five-year pledge period (2008-2012) or, for those solicited in 2007, six tax years, with an initial gift in 2007 and subsequent payments in 2008, 2009, 2010, 2011 and 2012.

2. Cost of giving: under current tax laws, the maximum tax benefit from a charitable gift is about 40% of the gift (lower than the sum of the 35% federal and 8.5% New Hampshire state rate because of the additional deduction resulting from the gift). For example, a gift of $25,000 requires a first payment of $4,167 plus five more payments. If the donor is in the 40% bracket, this gift will cost only $2,500 per year. ($4,166 - $1,666 = $2,500)

Examples — Assuming 35% Effective Federal Tax Bracket Total Gift Amount $5,000 $10,000 $15,000 $20,000 $25,000 $50,000 $100,000 $150,000 Tax Savings $1,750 $3,500 $5,250 $7,000 $8,750 $17,500 $35,000 $52,500 After Tax Cost $3,250 $6,500 $9,750 $13,000 $16,250 $32,500 $65,000 $97,500 Annual Payment $833 $1667 $2500 $3,333 $4,167 $ 8,333 $16,667 $25,000 Annual Tax Savings $292 $583 $875 $1,166 $1,458 $2,917 $5,833 $8,750 Annual After Tax Cost $541 $1083 $1,625 $2,167 $2,708 $5,417 $10,833 $16,250

3. Gifts of appreciated securities: the tax consequence of giving certain appreciated securities which one has owned more than twelve months are compared as follows (assuming a 35% tax bracket):

Example – Gift of Proceeds of Sale of Securities vs. Outright Gift of Securities Sale Gift of StockFair Market Value $30,000 $30,000Cost Basis $10,000 $10,000Long-term Gain (Line 1 – Line 2) $20,000 $20,000Capital Gain Tax (Line 3 x 15%) ($ 3,000) N/AAfter-Tax Proceeds (Line 1 – Line 4) $27,000 N/A

Income Tax Savings on Gift of $27,000 @ 35% bracket (Line 5 x 35%) $9,450

Income Tax Savings on Gift of $30,000 in Stock @ 35% (Line 1 x 35%) $10,500

Savings to Donor by transferring instead of selling Stock (Line 7 minus Line 6) $1,050

Additional Benefit to The Music Hall because you did not pay Capital Gains Taxes (Line 4) $3,000 Note: Gifts of appreciated property are deductible to the extent of 30% of Adjusted Gross Income (AGI). Excess contributions may be carried forward for five years. The AGI limitation with respect to cash gifts is 50%.

4. Charitable contributions can also be made from a “C Corporation.” The corporate charitable deduction limit is 10% of the corporation’s pre-tax net income. The maximum federal tax benefit of such corporate charitable gifts is 35%, but there may be no federal tax benefits if the corporation has no federal income tax liability as the result of other losses or credits. For gifts made through an “S Corporation” or partnership, individual rates do apply.

5. Advice of professional counsel: individual circumstances are unique, and prospective donors should seek advice from their accountant or attorney. Tax benefits are approximations only. Actual benefit may vary from these examples depending on personal tax situations. In some instances the deductions for charitable gifts may be further reduced as a result of limitations on total itemized deductions.

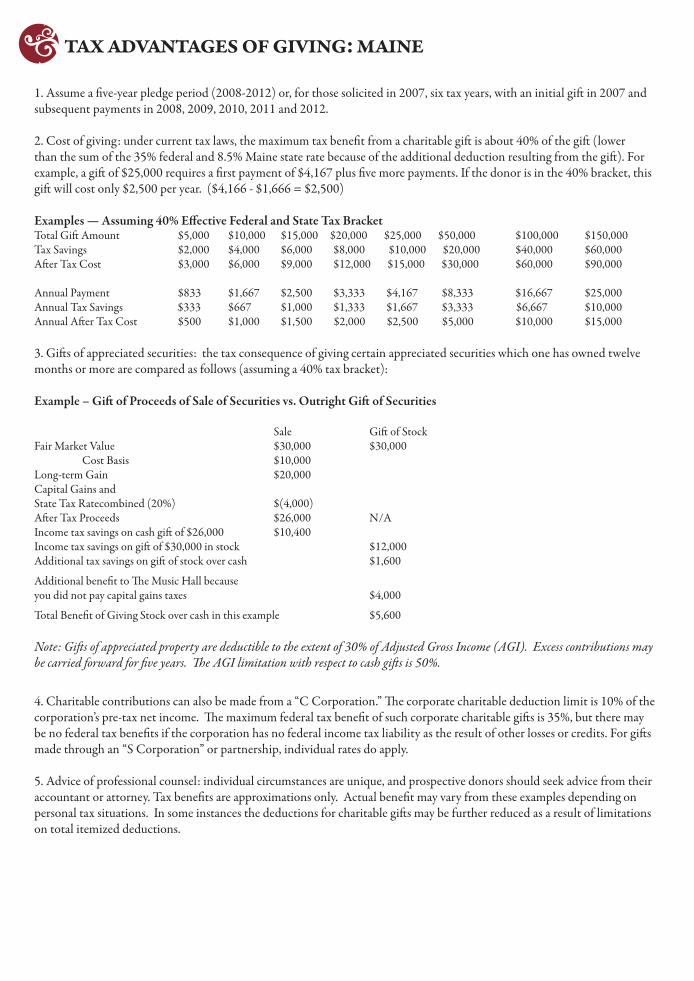

tax advantages of giving: maine

1. Assume a five-year pledge period (2008-2012) or, for those solicited in 2007, six tax years, with an initial gift in 2007 and subsequent payments in 2008, 2009, 2010, 2011 and 2012.

2. Cost of giving: under current tax laws, the maximum tax benefit from a charitable gift is about 40% of the gift (lower than the sum of the 35% federal and 8.5% Maine state rate because of the additional deduction resulting from the gift). For example, a gift of $25,000 requires a first payment of $4,167 plus five more payments. If the donor is in the 40% bracket, this gift will cost only $2,500 per year. ($4,166 - $1,666 = $2,500)

Examples — Assuming 40% Effective Federal and State Tax BracketTotal Gift Amount $5,000 $10,000 $15,000 $20,000 $25,000 $50,000 $100,000 $150,000 Tax Savings $2,000 $4,000 $6,000 $8,000 $10,000 $20,000 $40,000 $60,000 After Tax Cost $3,000 $6,000 $9,000 $12,000 $15,000 $30,000 $60,000 $90,000 Annual Payment $833 $1,667 $2,500 $3,333 $4,167 $8,333 $16,667 $25,000 Annual Tax Savings $333 $667 $1,000 $1,333 $1,667 $3,333 $6,667 $10,000 Annual After Tax Cost $500 $1,000 $1,500 $2,000 $2,500 $5,000 $10,000 $15,000

3. Gifts of appreciated securities: the tax consequence of giving certain appreciated securities which one has owned twelve months or more are compared as follows (assuming a 40% tax bracket):

Example – Gift of Proceeds of Sale of Securities vs. Outright Gift of Securities

Sale Gift of StockFair Market Value $30,000 $30,000 Cost Basis $10,000 Long-term Gain $20,000 Capital Gains and State Tax Ratecombined (20%) $(4,000) After Tax Proceeds $26,000 N/AIncome tax savings on cash gift of $26,000 $10,400 Income tax savings on gift of $30,000 in stock $12,000 Additional tax savings on gift of stock over cash $1,600

Additional benefit to The Music Hall because you did not pay capital gains taxes $4,000

Total Benefit of Giving Stock over cash in this example $5,600

Note: Gifts of appreciated property are deductible to the extent of 30% of Adjusted Gross Income (AGI). Excess contributions may be carried forward for five years. The AGI limitation with respect to cash gifts is 50%.

4. Charitable contributions can also be made from a “C Corporation.” The corporate charitable deduction limit is 10% of the corporation’s pre-tax net income. The maximum federal tax benefit of such corporate charitable gifts is 35%, but there may be no federal tax benefits if the corporation has no federal income tax liability as the result of other losses or credits. For gifts made through an “S Corporation” or partnership, individual rates do apply.

5. Advice of professional counsel: individual circumstances are unique, and prospective donors should seek advice from their accountant or attorney. Tax benefits are approximations only. Actual benefit may vary from these examples depending on personal tax situations. In some instances the deductions for charitable gifts may be further reduced as a result of limitations on total itemized deductions.

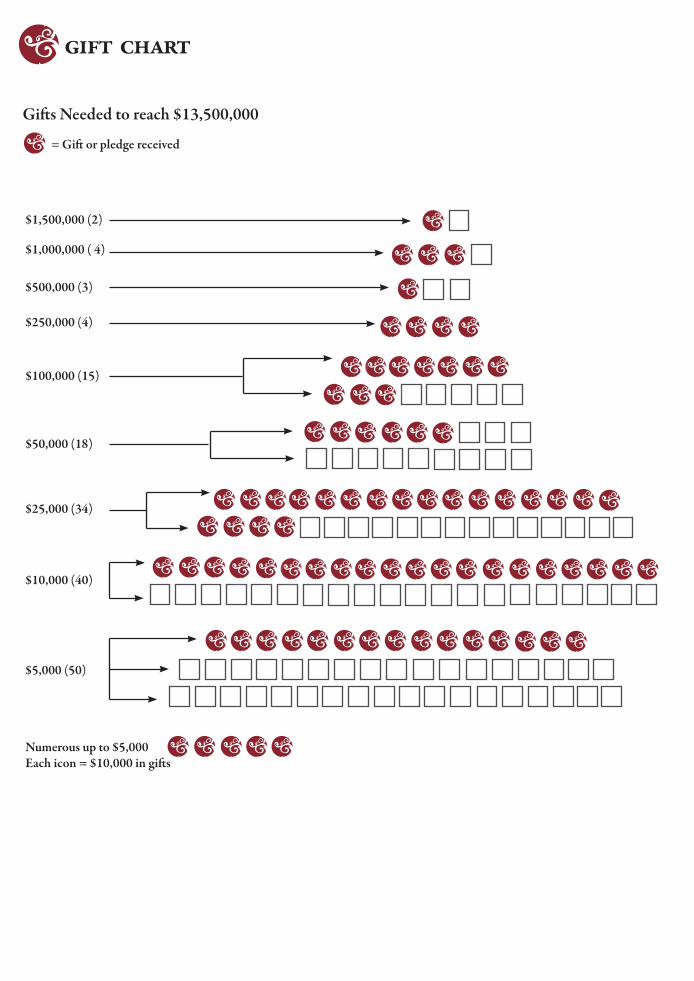

gift chart

Gifts Needed to reach $13,500,000

$1,500,000 (2)

$1,000,000 ( 4)

$500,000 (3)

$250,000 (4)

$100,000 (15)

$50,000 (18)

$25,000 (34)

$10,000 (40)

$5,000 (50)

= Gift or pledge received

Numerous up to $5,000 Each icon = $10,000 in gifts

frequently asked questionsWhat is the mission of The Music Hall?The mission of The Music Hall is to present the very best of diverse performing and related arts at The Music Hall as an active and vital arts center for the enrichment of the Seacoast community. Our vision is to be the Seacoast’s premier performing arts center fulfilling our role as the anchor cultural organization in our community and to emerge as an American Treasure through a combination of vibrant programming and a dynamic, respectful restoration that is historically valid while balanc-ing contemporary needs. As a highly focused performing arts center we will enliven our community with a diverse array of performance genres and an outlook that is contemporary, inclusive and classic. We are invested in the health of our commu-nity through our commitment to outreach to the underserved and to educational opportunities for children and adults alike.

How has The Music Hall historically raised funds? Over the last 10 years a number of small campaigns have been accomplished for the restoration of seats and the stage curtains and creation of our first operating reserve in honor of the Hall’s 125th Anniversary. In 2003, The Music Hall was designated an “American Treasure” by the National Park Service’s Save America’s Treasures Program. With funds from the program and matching contributions, The Music Hall restored key historical features of the Hall including the proscenium arch, audi-torium interior and ceiling dome; and repaired the roof and stairs. A major campaign, with a scope as large as Treasure the Future, has never been undertaken.

What’s the projected timeframe for the completion of the Treasure the Future Campaign and related projects? What’s the cost and what will be accomplished? The Treasure the Future project will be completed by 2011. The campaign for restoration, expansion and endowment includ-ing unrestricted operating reserves for programs of The Music Hall aims to raise $13.4 million. The comprehensive project includes:

Critical Repairs & Upgrades to Technology and Infrastructure: strengthen the historic wooden theater grid with a mod-ern steel grid; replace the antiquated HVAC system with new, greener system; upgrade the electrical and sound systems to meet 21st century standards; relocate and construct new projection booth, replace two outdated ticketing and fundraising systems with one fully integrated system. Historic Preservation, Restoration & Rehabilitation: repair and renovate the stage to its original size; complete the his-toric finishes throughout the theater; restore and rehabilitate the façade and windows; rehabilitate and expand the entrance lobby; reconfigure and renovate the upper lobby; replicate and hang the historic chandelier; reproduce the historic oleo curtain; and extend the historic presence of the theater to Congress Street, contributing to neighbors’ and city project to improve Chestnut Street with wider sidewalks and better lighting. The Music Hall Loft: the newly renovated space at 131 Congress Street includes a studio classroom, space for master classes, workshops, programming and educational initiatives; an 85-seat tiered theater for special events and performances; safe child drop off, and full accessibility for all ages. Endowment, including Unrestricted Operating Reserves: will preserve and protect the historic theater building for generations to come and build community capacity, ensuring the availability and accessibility of our highly valued educa-tional and community-geared programs. The endowment, including unrestricted operating reserves, ensures the long-term stewardship of the organization as an historical treasure, a community resource and a center of learning.

Funds raised in the Treasure the Future Campaign are in support of The Music Hall’s strategic plan to restore, rehabili-tate and expand The Music Hall, its programs and financial strength, to serve as a performing arts center for the 21st century. Gifts are unrestricted except for endowment funds.

frequently asked questionsWhat impact will the project have on other arts organizations and the community? The Music Hall has active partnerships with numerous local arts organizations. These Community Partners will benefit from the increased capacity, physical space, and endowment/operating reserves afforded by the Treasure the Future project. Over the next 25 years, the fully restored and expanded Music Hall will contribute $250 million to the local economy, strengthen-ing the region and its businesses.

Who will be asked to contribute to the campaign? There will be opportunities for everyone to contribute to Treasure the Future project: corporations, governmental agencies, foundations, and individuals.

How can I obtain additional information about Treasure the Future? For additional information about The Treasure Future project, please contact Laura Smith, Director of Institutional Advance-ment at 603-433-3100 ext 40, or [email protected].

ways of givingSupporters of The Music Hall may choose from a wide variety of methods for making their gifts to the campaign. Out-lined here are a few of these methods, but donors are encouraged to consult with their personal financial advisor for the one(s) best suited to meet their goals.

Planning A GiftBy carefully selecting the assets to be used in making a gift, a donor can achieve more than one objective. The primary reasons for making a contribution are the accomplishments that come about as a result of that gift and the personal satisfaction that is gained. While tax benefits are rarely the primary motive for giving, once a decision to contribute is made, the donor should consider the opportunities for gift enhancement available in the tax structure.

CashCash contributions give The Music Hall capital that is immediately accessible and allows the donor to deduct the amount of the gift in computing his/her income tax. Most donors find they are able to make more significant contributions and accom-modate personal cash flow more easily if pledge payments are spread out over a 60-month, or six tax-year, period.

The actual amount of savings each donor realizes in tax payments depends on level of income. For those in the highest personal income tax bracket of approximately 45% (lower than the sum of the 39.6% federal and 8.5% state rate because of the additional state tax deduction as a result of the gift), the actual cost of the gift, after deductions, is 55% of the amount given. Thus, a $10,000 gift could produce a $4,500 tax savings resulting in an “out of pocket” cost of only $5,500.

Giving Securities For many donors, giving appreciated stock to The Music Hall may be preferable to giving cash. Federal tax law offers special incentives for non-cash gifts of property, particularly if that property has appreciated in value.

Gifts of Appreciated Stock: The Benefits to You• You avoid capital gains tax. Any gain is taxable if you sell the stock yourself, but not if you give it to The Music Hall.• Your charitable deduction for federal income tax purposes is based on the full fair market value of the stock on the date the gift is made.• You receive credit from The Music Hall for the full fair market value of the stock, but the cost to you is only your original purchase price. Valuing a gift of securitiesThe value of a publicly traded security is the average of the high and low prices on the date of the gift. Corporate GivingUnder the current tax laws, a corporation may claim a charitable deduction up to 10 percent of pre-tax net income. Any excess in a year may be carried over to as many as five (5) years. The maximum federal savings of such charitable gifts is 35%.

(Note: Changes in the tax laws may alter the information given here. Consult your tax advisor for up-to-date information as it pertains to your situation.)

(continued)

ways of giving(continued)

Life InsuranceGifts of life insurance policies may be made to the campaign. When a fully paid-up policy is given, its value — and, therefore, the amount of the donor’s tax deduction — is measured by the policy’s replacement cost. If the policy is not paid-up, its value is approximately the cash surrender value. The exact value in either case may be obtained from the insurance company. A gift of insurance usually qualifies for the maximum deduction limitation (50 percent) of adjusted gross income. Merely designat-ing the organization as a beneficiary does not constitute an immediate gift.

Matching Corporate GiftsMany corporations have matching gift programs in which an employee’s gift to the campaign will be matched by the com-pany. Donors are urged to forward the company’s matching gift form with their own contribution or pledge payment.

Planned GiftsNormally, gifts to The Music Hall must be made within the five-year pledge period. However, donors who wish to make a sig-nificant gift to the organization, without losing income from specific assets, may decide upon a deferred gift. A planned gift is one made in trust to The Music Hall, with income or other benefits from the asset retained by the donor, or other beneficiary, for as long as they live. All planned gifts must be irrevocable and approved by the Campaign Cabinet if they do not fall under guidelines already established by the Board of Trustees or the Campaign Cabinet.

(Note: Changes in the tax laws may alter the information given here. Consult your tax advisor for up-to-date information as it pertains to your situation.)

philanthropic recognition

All donors to the Treasure the Future campaign will be listed on a single plaque prominently located in The Music Hall. Although gifts are unrestricted except endowment funds, major donors may be honored with recognition in these areas:

Center for Performing Arts & Education....$1,000,000Entrance Lobby....$750,000 Honored

Elevator....$150,000 HonoredProscenium Arch....$100,000Mezzanine Lobby....$100,000

CPEA Theater....$100,000 HonoredOleo Curtain....$100,000

Grid....$100,000Chandelier....$100,000

Opera Boxes (2)....$50,000 eachStar Dressing Rooms (2)....$50,000 each

Chorus Dressing Rooms (2)....$50,000 eachGreen Room....$50,000

Administration Area, CPEA....$50,000 CPEA Concession Area....$50,000

CPEA Box Office/Retail Kiosk....$50,000 Honored

For additional information, please contact Laura Smith, Director of Institutional Advancement, at (603) 433-3100 ext. 40 or [email protected]

Michael Harvell, Esq., President

David Hills, Vice President

Andrew Powell, Treasurer

Josephine A. Lamprey, Secretary

Douglas Nelson, Executive Committee At Large

Jameson French, Ex Officio

Patricia Lynch, Ex Officio

~

the music hall board of trustees 2009

Gail VanHoy Carolan

Geoffrey E. Clark, M.D.

Betsy Cole

Betsy Cosgrove

James Forbes

Joanne Francis

Brook W. Gassner

Angelynne Koromilas Hinson

Ann Kendall

Michael Kane

Philip A. Marcus

Albert Morales

Maxine K. Morse

Kathleen Rochefort Murray

Danny H. O’Brien

Elisabeth Robinson

Donna Ryan

Daniel Schwarz, Esq.

Jennifer Shulman

Toby Stowe, CPA