Embed Size (px)

DESCRIPTION

HTT January 30th Business Annual

Citation preview

Monday, January 30, 2012

THE BUSINESS AND FASHION NEWSPAPER OF THE HOME TEXTILES INDUSTRY | hometextilestoday.com | Vol. 33, No. 4 | $85.00

2012BUSINESSANNUAL

htt120104_BizAnnualCover 1 1/18/2012 3:26:54 PM

2 Home Textiles Today

EDITOR-IN-CHIEF Jennifer Marks10 Ocean Blvd #8B

Atlantic Highlands, N.J. 07716(732) 204-2012 |

PUBLISHER/EDITORIAL DIRECTORWarren Shoulberg(646) 805-0226 |

SENIOR EDITOR Cecile B. Corral428 Bianca Ave. Coral Gables, FL 33146

(305) 661-7493 | [email protected]

MANAGING EDITOR Julie Murphy(646) 805-0224 |

CONTRIBUTING GRAPHIC ARTIST Desiree Nunez

(646) 805-0233 | [email protected]

DIRECTOR OF MARKET RESEARCH Dana French

(336) 605-1091 | [email protected]

ASSOCIATE PUBLISHERJeff Reeves (336) 605-1009 |

ACCOUNT MANAGER NORTHEAST/MIDWEST/CANADA

Mary McLoughlin(646) 805-0227 |

CLASSIFIED AD SALESSpencer Whittle (336) 605-1027

[email protected] Karen Hancock (336) 605-1047 [email protected]

MANAGER, EUROPE Mirek KraczkowskiTel: 48 22 401 70 01; Fax: 48 22 401 70 16 |

MANAGER, INDIA Kaushal ShahCell: 91-9821715431; Tel: 91-22-6663 4597

/ 24988658Fax: 91-22-66634596 | [email protected]

ONLINE SALES MANAGER Penny Schneck

(336) 605-1084 | [email protected]

PRODUCTION MANAGER Rich LambTel: (336) 605-1074; Fax: (336) 605-1143 |

rlamb@ sandowmedia.com

DIRECTOR, WEB OPERATIONS Chris Schultz | (336) 605-1076 | cschultz@

sandowmedia.com

MANAGER, CLIENT SERVICES, WEB ADVERTISING

Dan Sage | (336) 605-1080 | [email protected]

E-MEDIA PROJECT MANAGER Missy Axe | (336) 605-1005 |

DIRECTOR OF AUDIENCE MARKETING Allison Ternes (704) 573-9007 |

PRESIDENT, FURNITURE TODAY GROUP Kevin Castellani

(336) 605-1034 | [email protected]

FOUNDING EDITOR-IN-CHIEF Carole Sloan, 1979-2011

SANDOW MEDIA

PRESIDENT AND CEO Adam I. Sandow

CFO/COO Christopher Fabian

VP CREATIVE AND EDITORIAL Yolanda E. Yoh

EVP, GROUP PUBLISHER James N. Dimonekas

360 Park Avenue South, New York, N.Y. 10010Tel: (646) 805-0227; Fax: (646) 365-2307

www.hometextilestoday.com

THE BUSINESS AND FASHION NEWSPAPER OF THE HOME TEXTILES INDUSTRY®360 Park Avenue South, New York, NY 10010

Telephone: (646) 805-0227 Fax: (646) 365-2307 USPS 497-490

HOME TEXTILES TODAY (USPS 497-490) (ISSN 0195-3184) is published 29 times a year except for the weeks of 1/16, 2/6, 2/20, 3/12, 3/26, 4/9, 4/23, 5/7, 5/21, 6/4, 6/18, 7/2, 7/16, 7/30, 8/13, 8/27, 9/17, 10/1, 10/15, 10/29, 11/12, 11/26, 12/10, 12/24 by Furniture/Today Media Group, 360 Park Avenue South, 17th fl., New York, NY, 10010 a subsidiary of Sandow Media LLC, 3731 NW 8th Ave, Boca Raton, FL 33431. Periodicals postage paid at New York, NY, and additional mailing offices. HOME TEXTILES TODAY copyright ©2012 by Sandow Media LLC. Annual subscription rates: U.S. and Canada $169.97; 1 year, other countries $325.99 for surface mail . All payments must be made in U.S. currency. Subscription inquiries: HOME TEXTILES TODAY, PO Box 5879, Harlan, IA 51593-1379. Phone: (866) 456-0405. HOME TEXTILES TODAY and THE BUSINESS AND FASHION NEWSPAPER OF THE HOME TEXTILES INDUSTRY are registered trade-marks of Sandow Media LLC, used under license. Sandow Media LLC does not assume and hereby disclaims liability to any person for any loss or damage caused by errors or omissions in the material contained herein, regardless of whether such errors result from negligence, accident or any other cause whatsoever. (Posted under Canadian International Publication Agreement No.40624074. Sandow Media/CDS (Mint Hill)

POSTMASTER: Send address changes to HOME TEXTILES TODAY, P.O. Box 5879, Harlan, IA, 51593-1379 Email: [email protected]. Return undeliverable Canadian addresses to: RCS International; APC; PO Box 503, RPO West Beaver Creek, Rich Hill, ON L4B 4R6

SUBSCRIPTIONS: U.S.A. (866) 456-0405All other countries: (515) 247-2984

FAX SUBSCRIPTIONS: 1-866-310-7181

January 30, 2012

Retailing GiantsTop 50 home textiles retailers ............. 6

Supplier GiantsTop 15 home textiles manufacturers .. 20Top 5 manufacturers by product category ........................... 24

The FactsTop Of Bed .......................................... 34Utility Bedding .................................... 35Sheets .................................................. 36Bath ...................................................... 37Kitchen Textiles ................................... 38Area Rugs ............................................ 39Window Treatments ........................... 40

> hometextilestoday.comTable of Contents

htt120104_002 2 1/18/2012 11:15:17 AM

Softline.indd 1 1/17/2012 9:39:55 AM

CANDICE OLSEN

www.surya.com

To become a Suryadealer, please call

1.877.275.7847or email us at info@

surya.com.

SERVICES INVENTORY MERCHANDISING PRODUCT TECHNOLOGY COMMUNITY

Surya_Spread_Jan30th_Bus_Annual.2 2 1/17/2012 12:27:43 PM

30,279 FANS AND RISING!Come check us out at

facebook.com/SuryaSocial

JILL ROSENWALD

Scan this to s

ee

the whole coll ection

!

THE POWER OFTRUE ARTISTRY

SHOP SURYAto view over 1800 rug designs and hundreds of

coordinating pillows, poufs, throws and wall art.

All Surya accessories easily let you solidify your look at minimal cost. Go modern, fi ne tune or make a

personal statement.

Our knowledgeable and lively designers bring their fresh aesthetic to our rugs, all of which are as

impeccably crafted as they are gorgeously designed.

Surya_Spread_Jan30th_Bus_Annual.3 3 1/17/2012 12:27:47 PM

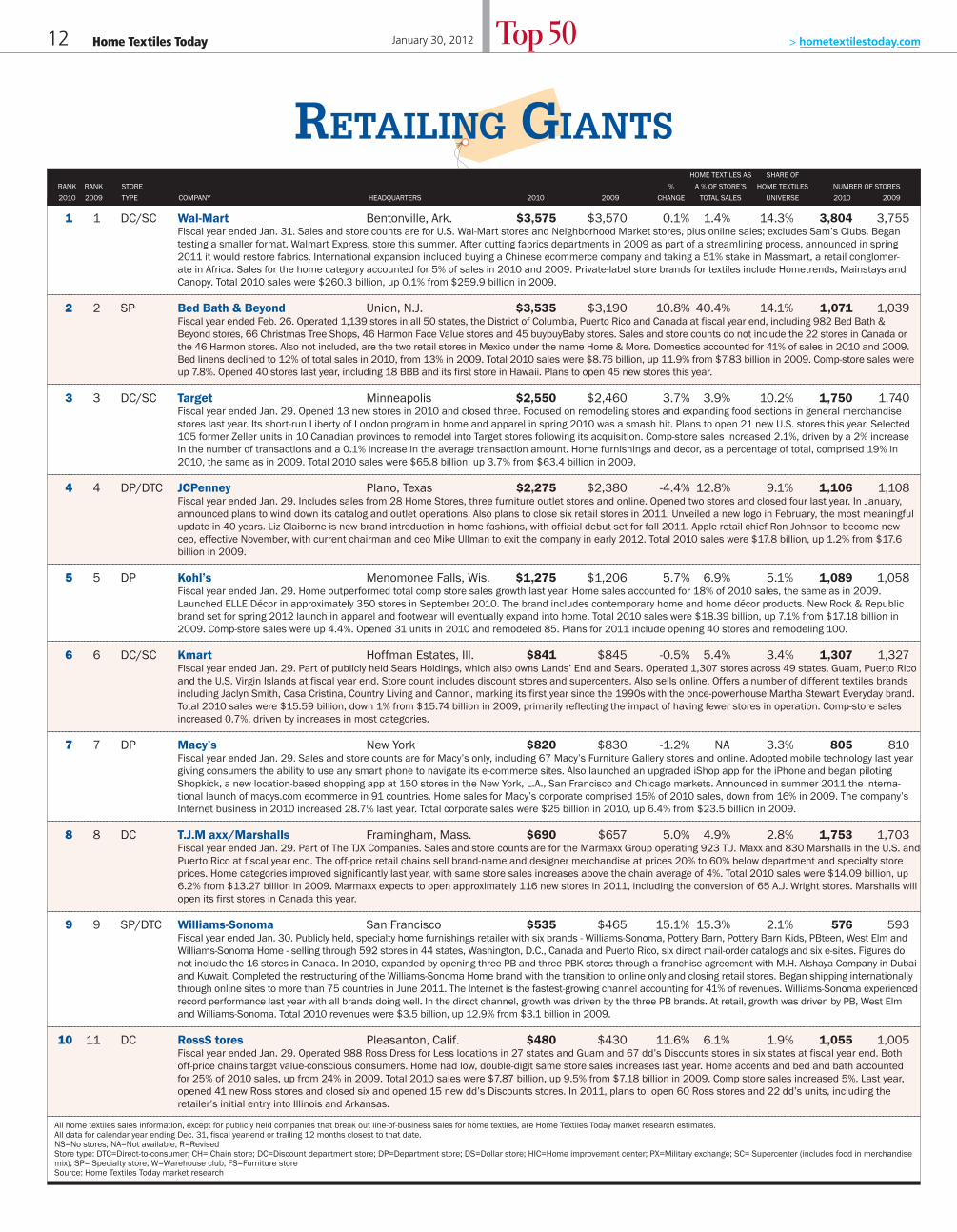

6 Home Textiles Today > hometextilestoday.comTop 50 January 30, 2012

TOP MULTI-DIVISION OPERATIONS

1 Wal-MartBentonville, Ark. $3,761 $3,760 0.0% 15.0% 4,413 4,360

2 Sears Holding Corp.Hoffman Estates, Ill. $1,220 $1,228 -0.7% 4.9% 2,163 2,189

3 TJX C ompaniesFramingham, Mass. $968 $919 5.3% 3.9% 2,089 2,026

4 Macy’s, I nc.New York $955 $968 -1.3% 3.8% 850 850

5 HSNiNew York $225 $198 13.6% 0.9% 10 11

1. Includes No. 1 Wal-Mart and No. 24 Sam’s Club2. Includes No. 6 Kmart, No. 15 Sears and No. 40 Lands’ End 3. Includes No. 8 T.J. Maxx/Marshalls and No. 17 HomeGoods4. Includes No. 7 Macy’s and No. 31 Bloominigdale’s5. Includes No. 26 Cornerstone Brands and No. 42 HSN

Source: Home Textiles Today market research

HOME TEXTILES SALES SHARE OF

($MILLIONS) PERCENT HOME TEXTILES NUMBER OF STORES

RANK COMPANY/CITY 2010 2009 CHANGE UNIVERSE 2010 2009

Top 50 Retailing GiantsBY JENNIFER MARKS

NEW YORK — In the weak econ-omy that prevailed through much of 2010, it was a battle of inches for retailers looking to garner greater market share in home textiles.

At the top of the heap, No. 2 ranked Bed Bath & Beyond is creeping close enough to Walmart to begin threatening its status as the largest seller of home textiles in the United States. In 2010, the volume distance between them was just $40 mil-lion — compared to $380 mil-lion in 2009 and $448 in 2008.

After brushing aside JCPen-ney to claim the No. 3 spot in last year’s ranking, Target wid-ened the gap. Target outsold JCP by $275 million in 2010 after out-pacing the department store by just $80 million in 2009.

The Top 5 retailers – Walmart, Bed Bath & Beyond, Target, JCPenney and Kohl’s – once again are the only companies generating $1 billion or more in home tex-tiles sales. As a group, their sales grew 3.2% to $13.2 billion, but their share of the Top 50’s $23.0 billion in 2010 remained stag-nant: 57.4% last year compared to 57.5% a year earlier.

The Top 50’s tot al sales rose 3.3%, compared to a 2.9% increase in total U.S. home tex-tiles sales from all sellers, which rang in at $25.05 billion last year. No retailer made a big leap up the ladder in HTT’s exclusive Retailing Giants report this year, but several stepped up rung — most notably Ross Stores, which moved into the Top 10 for the fi rst time.

Ross dislodged Family Dollar, last year’s No. 10, with an 11.6% jump in home textiles sales to $480 million.

The Top 10 saw a 3.4% increase in home textiles sales in 2010 to $16.576 billion while its share of the Top 50’s total sales remained fl at at 72.0%.

Among retailers ranked 11-20, Big Lots was the only one to move up the line in this year’s survey, displacing Ikea to become No. 12. Within that group, No. 16 Luxury Linens is poised to eclipse No. 15 Sears (once a Top 10 retailer) as their home textiles sales in 2010 were separated by only $3 million.

The Top 20 retailers generated a collective 3.5% gain in sales last

year and accounted for 86.0% of the Top 50’s home textiles sales, up slightly from 85.8% in last year’s report.

Four retailers in the rankings from 21-30 moved up in this year’s ranking: QVC (No. 23, moving ahead of Sam’s Club); Corner Stone Brands (No. 26, jumping ahead four places); Crate & Barrrel (No. 29, also up by four paces); and BrylaneHome (No. 30, up one spot).

Market share gainers in the remainder of the Top 50 include:

• Dollar General, No. 30;• Country Curtains, No. 37;

• Army & Air Force Exchange, No. 39;

• Ashley Furniture Stores, No. 41;

• Dollar Tree, No. 44;• Garden Ridge, No. 46;• Cost Plus World Market,

No. 49.Each of them moved up one

place in the ranking.Of the retailers that lost home

textiles market share among the Top 50, only two slipped more than one place. Bloomingdale’s fell to No. 31 from No. 38 while Restoration Hardware dropped to No. 32 from No. 29.

By channel of business, dis-

counters continue to hold the greatest market share, with 40.6% of the Top 50’s sales compared to 41.0% in the previous year.

Specialty stores constitute the second largest channel, with 26.4% of home textiles sales in 2010 compared to 25.0% a year earlier.

Direct-to-consumer accounts for 4.1% of home textiles sales — but this accounts only for the pure-play retailers. Major brick-and-mortar retailers as well as cat-alogers do big business in online retailing, but their ecommerce sales are included in their overall numbers. HTT

ELITE SPONSORS

Intertextile

For more information on these Home Textiles Today advertisers, scan their QR tags below using a free QR scanner available at synqware.com.

Lenzing

Manhattan Properties

Protect-A-Bed

Softline Home Fashions

Surya Rugs

QR tags provided by Synqware, a leading technology company supplying connectivity tools to the businesses. Synqware.com.

A D V E R T I S E M E N T

HOW THE TOP 50 WERE RANKED

Home Textiles Today’s exclusive survey of the Top 50 home textiles retailers ranks the top U.S. retailers by sales of 2010 home textiles. All home textiles categories, bed, bath, kitchen, ta-ble linen and window coverings, including al-ternative window coverings, custom decorating and accessories that are generally sold with tex-tile items, are included in the sales estimates.

In order to be eligible for the ranking, each retailer must sell more than one home textile category.

The ranking crosses all formats of home tex-tiles retailing. Companies are classifi ed by their primary channel of distribution. Channels include discounters; specialty stores; home improvement centers; department stores; dollar stores; nation-al chains, such as Sears; direct-to-consumer retail-ers that sell primarily through catalogs, televi-sion and/or the Internet; warehouse membership clubs; military exchanges; furniture stores; and supercenters, which sell both food and general merchandise in their mix.

For Wal-Mart, Kmart and Target, the ranking includes discount stores and supercenters.

All home textiles sales information, except for publicly held companies that break out line-of-business sales for home textiles, are Home Textiles Today market research estimates. Sales fi gures are given for the 12-month period end-ing closest to December 31, 2010. Individual re-tailer descriptions include the date of the fi scal year end or the 12-month periods that deviate signifi cantly from that date.

Sales estimates are based on information from a variety of sources including the com-panies themselves, public company fi lings with the Securities and Exchange Commission, dis-cussions with industry analysts and suppliers and published and unpublished reports, includ-ing newspaper articles in various retail trad-ing areas.

In cases where companies have identical sales of home textiles, the one with the fastest sales growth is ranked higher.

htt120104_006 6 1/17/2012 1:56:31 PM

Home Textiles Today8 Top 50January 30, 2012 > hometextilestoday.com

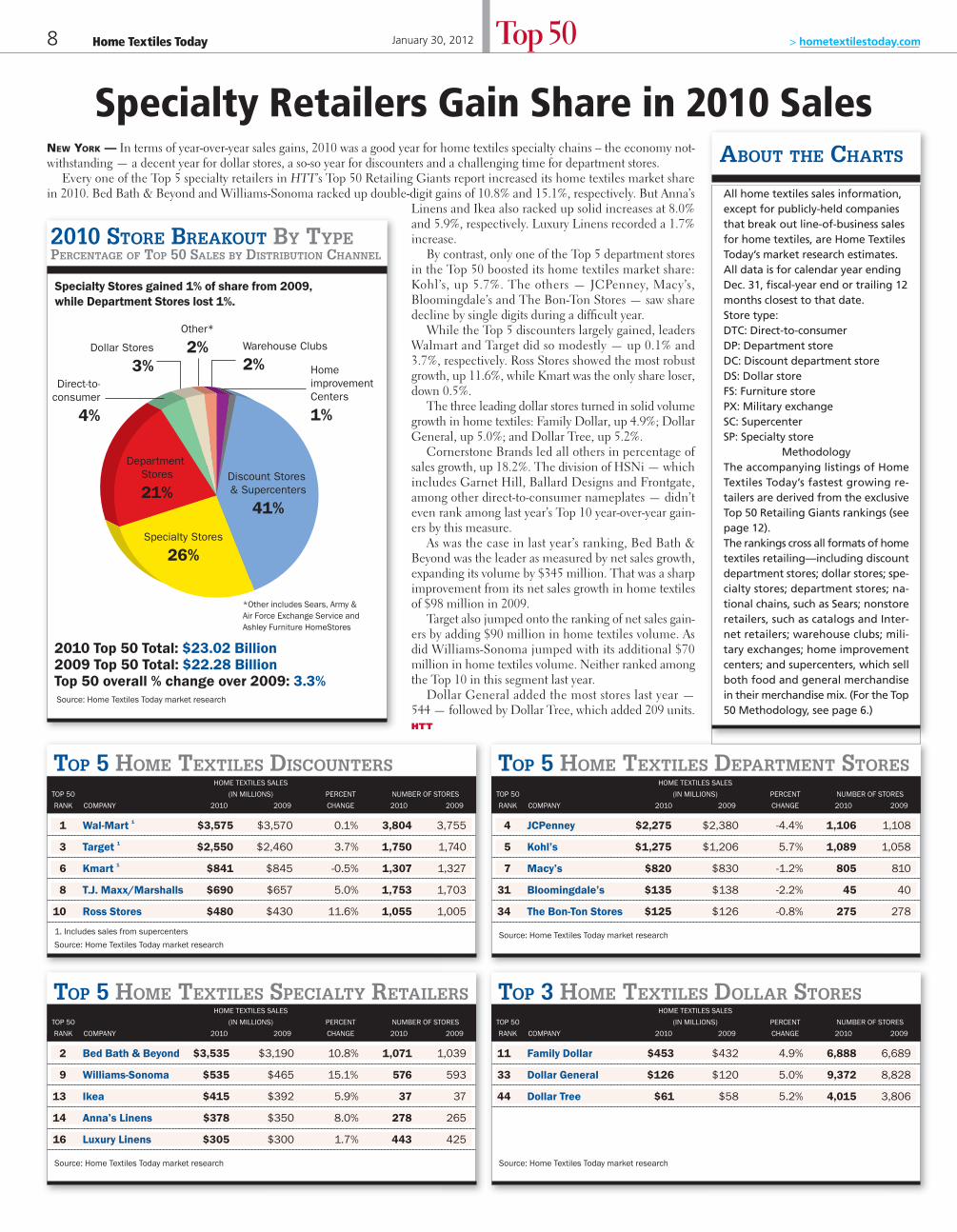

TOP 5 HOME TEXTILES DISCOUNTERS

1 Wal-Mart 1 $3,575 $3,570 0.1% 3,804 3,755

3 Target 1 $2,550 $2,460 3.7% 1,750 1,740

6 Kmart 1 $841 $845 -0.5% 1,307 1,327

8 T.J. Maxx/Marshalls $690 $657 5.0% 1,753 1,703

10 Ross Stores $480 $430 11.6% 1,055 1,005

HOME TEXTILES SALES

TOP 50 (IN MILLIONS) PERCENT NUMBER OF STORES

RANK COMPANY 2010 2009 CHANGE 2010 2009

1. Includes sales from supercenters

Source: Home Textiles Today market research

TOP 5 HOME TEXTILES DEPARTMENT STORES

4 JCPenney $2,275 $2,380 -4.4% 1,106 1,108

5 Kohl’s $1,275 $1,206 5.7% 1,089 1,058

7 Macy’s $820 $830 -1.2% 805 810

31 Bloomingdale’s $135 $138 -2.2% 45 40

34 The Bon-Ton Stores $125 $126 -0.8% 275 278

HOME TEXTILES SALES

TOP 50 (IN MILLIONS) PERCENT NUMBER OF STORES

RANK COMPANY 2010 2009 CHANGE 2010 2009

Source: Home Textiles Today market research

TOP 5 HOME TEXTILES SPECIALTY RETAILERS

2 Bed Bath & Beyond $3,535 $3,190 10.8% 1,071 1,039

9 Williams-Sonoma $535 $465 15.1% 576 593

13 Ikea $415 $392 5.9% 37 37

14 Anna’s Linens $378 $350 8.0% 278 265

16 Luxury Linens $305 $300 1.7% 443 425

HOME TEXTILES SALES

TOP 50 (IN MILLIONS) PERCENT NUMBER OF STORES

RANK COMPANY 2010 2009 CHANGE 2010 2009

Source: Home Textiles Today market research

TOP 3 HOME TEXTILES DOLLAR STORES

11 Family Dollar $453 $432 4.9% 6,888 6,689

33 Dollar General $126 $120 5.0% 9,372 8,828

44 Dollar Tree $61 $58 5.2% 4,015 3,806

HOME TEXTILES SALES

TOP 50 (IN MILLIONS) PERCENT NUMBER OF STORES

RANK COMPANY 2010 2009 CHANGE 2010 2009

Source: Home Textiles Today market research

NEW YORK — In terms of year-over-year sales gains, 2010 was a good year for home textiles specialty chains – the economy not-withstanding — a decent year for dollar stores, a so-so year for discounters and a challenging time for department stores.

Every one of the Top 5 specialty retailers in HTT’s Top 50 Retailing Giants report increased its home textiles market share in 2010. Bed Bath & Beyond and Williams-Sonoma racked up double-digit gains of 10.8% and 15.1%, respectively. But Anna’s

Linens and Ikea also racked up solid increases at 8.0% and 5.9%, respectively. Luxury Linens recorded a 1.7% increase.

By contrast, only one of the Top 5 department stores in the Top 50 boosted its home textiles market share: Kohl’s, up 5.7%. The others — JCPenney, Macy’s, Bloomingdale’s and The Bon-Ton Stores — saw share decline by single digits during a diffi cult year.

While the Top 5 discounters largely gained, leaders Walmart and Target did so modestly — up 0.1% and 3.7%, respectively. Ross Stores showed the most robust growth, up 11.6%, while Kmart was the only share loser, down 0.5%.

The three leading dollar stores turned in solid volume growth in home textiles: Family Dollar, up 4.9%; Dollar General, up 5.0%; and Dollar Tree, up 5.2%.

Cornerstone Brands led all others in percentage of sales growth, up 18.2%. The division of HSNi — which includes Garnet Hill, Ballard Designs and Frontgate, among other direct-to-consumer nameplates — didn’t even rank among last year’s Top 10 year-over-year gain-ers by this measure.

As was the case in last year’s ranking, Bed Bath & Beyond was the leader as measured by net sales growth, expanding its volume by $345 million. That was a sharp improvement from its net sales growth in home textiles of $98 million in 2009.

Target also jumped onto the ranking of net sales gain-ers by adding $90 million in home textiles volume. As did Williams-Sonoma jumped with its additional $70 million in home textiles volume. Neither ranked among the Top 10 in this segment last year.

Dollar General added the most stores last year — 544 — followed by Dollar Tree, which added 209 units. HTT

2010 STORE BREAKOUT BY TYPEPERCENTAGE OF TOP 50 SALES BY DISTRIBUTION CHANNEL

Specialty Stores gained 1% of share from 2009, while Department Stores lost 1%.

2010 Top 50 Total: $23.02 Billion2009 Top 50 Total: $22.28 BillionTop 50 overall % change over 2009: 3.3% Source: Home Textiles Today market research

Homeimprovement Centers

1%

Direct-to-consumer

4%

Warehouse Clubs

2%

Other*

2%Dollar Stores

3%

Department Stores

21%

Specialty Stores

26%

Discount Stores & Supercenters

41%

Specialty Retailers Gain Share in 2010 SalesABOUT THE CHARTS

*Other includes Sears, Army & Air Force Exchange Service and Ashley Furniture HomeStores

All home textiles sales information, except for publicly-held companies that break out line-of-business sales for home textiles, are Home Textiles Today’s market research estimates. All data is for calendar year ending Dec. 31, fi scal-year end or trailing 12 months closest to that date. Store type:DTC: Direct-to-consumerDP: Department storeDC: Discount department storeDS: Dollar storeFS: Furniture storePX: Military exchangeSC: SupercenterSP: Specialty store

MethodologyThe accompanying listings of Home Textiles Today’s fastest growing re-tailers are derived from the exclusive Top 50 Retailing Giants rankings (see page 12). The rankings cross all formats of home textiles retailing—including discount department stores; dollar stores; spe-cialty stores; department stores; na-tional chains, such as Sears; nonstore retailers, such as catalogs and Inter-net retailers; warehouse clubs; mili-tary exchanges; home improvement centers; and supercenters, which sell both food and general merchandise in their merchandise mix. (For the Top 50 Methodology, see page 6.)

htt120104_008_010 8 1/16/2012 4:51:18 PM

The Textile Building at 295 Fifth

New York is the market.

And the market in New York is the

home textiles

TEXTILEBUILDING

For 90 years, 295 Fifth Avenue has been the leading showcase for the home textiles industry, with the best location,

the best value per square foot, services that cater to your distinctive needs, high-profile traffic, high-tech security, a wi-fi buyers lounge

and the personal service of a staff of 15.

Give your business the best market, in the market. Call Lou Lombardi, President & CEO, Manhattan Properties, Inc.

212-685-0530 [email protected] on-site management

We are the market

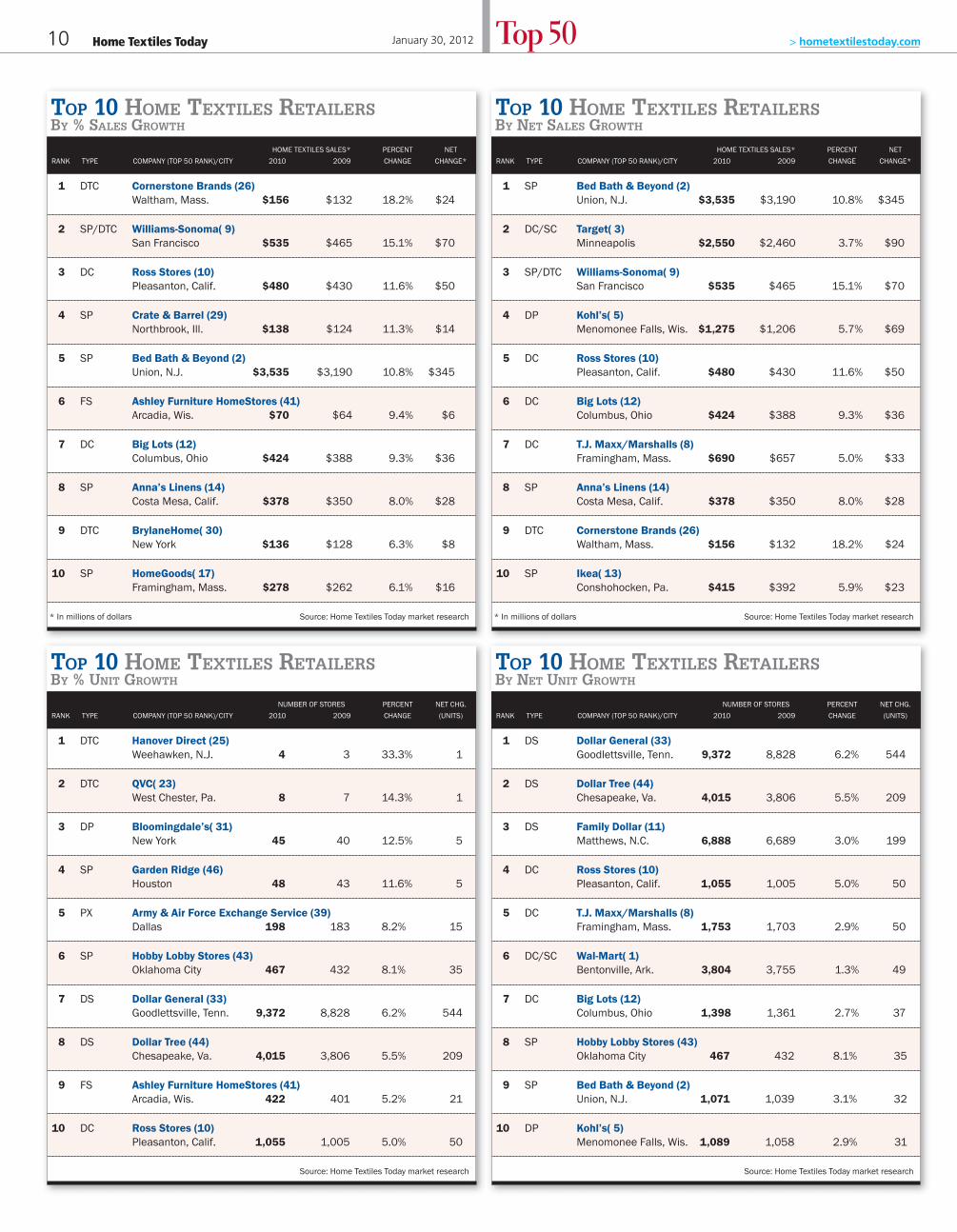

Home Textiles Today10 Top 50 > hometextilestoday.com

TOP 10 HOME TEXTILES RETAILERSBY % SALES GROWTH

1 DTC Cornerstone Brands (26)Waltham, Mass. $156 $132 18.2% $24

2 SP/DTC Williams-Sonoma ( 9)San Francisco $535 $465 15.1% $70

3 DC Ross Stores (10)Pleasanton, Calif. $480 $430 11.6% $50

4 SP Crate & Barrel (29)Northbrook, Ill. $138 $124 11.3% $14

5 SP Bed Bath & Beyond (2)Union, N.J. $3,535 $3,190 10.8% $345

6 FS Ashley Furniture HomeStores (41)Arcadia, Wis. $70 $64 9.4% $6

7 DC Big Lots (12)Columbus, Ohio $424 $388 9.3% $36

8 SP Anna’s Linens (14)Costa Mesa, Calif. $378 $350 8.0% $28

9 DTC BrylaneHome ( 30)New York $136 $128 6.3% $8

10 SP HomeGoods ( 17)Framingham, Mass. $278 $262 6.1% $16

* In millions of dollars Source: Home Textiles Today market research

HOME TEXTILES SALES* PERCENT NET

RANK TYPE COMPANY (TOP 50 RANK)/CITY 2010 2009 CHANGE CHANGE*

TOP 10 HOME TEXTILES RETAILERSBY NET SALES GROWTH

1 SP Bed Bath & Beyond (2)Union, N.J. $3,535 $3,190 10.8% $345

2 DC/SC Target ( 3)Minneapolis $2,550 $2,460 3.7% $90

3 SP/DTC Williams-Sonoma ( 9)San Francisco $535 $465 15.1% $70

4 DP Kohl’s ( 5)Menomonee Falls, Wis. $1,275 $1,206 5.7% $69

5 DC Ross Stores (10)Pleasanton, Calif. $480 $430 11.6% $50

6 DC Big Lots (12)Columbus, Ohio $424 $388 9.3% $36

7 DC T.J. Maxx/Marshalls (8)Framingham, Mass. $690 $657 5.0% $33

8 SP Anna’s Linens (14)Costa Mesa, Calif. $378 $350 8.0% $28

9 DTC Cornerstone Brands (26)Waltham, Mass. $156 $132 18.2% $24

10 SP Ikea ( 13)Conshohocken, Pa. $415 $392 5.9% $23

* In millions of dollars Source: Home Textiles Today market research

HOME TEXTILES SALES* PERCENT NET

RANK TYPE COMPANY (TOP 50 RANK)/CITY 2010 2009 CHANGE CHANGE*

TOP 10 HOME TEXTILES RETAILERSBY % UNIT GROWTH

1 DTC Hanover Direct (25)Weehawken, N.J. 4 3 33.3% 1

2 DTC QVC ( 23)West Chester, Pa. 8 7 14.3% 1

3 DP Bloomingdale’s ( 31)New York 45 40 12.5% 5

4 SP Garden Ridge (46)Houston 48 43 11.6% 5

5 PX Army & Air Force Exchange Service (39)Dallas 198 183 8.2% 15

6 SP Hobby Lobby Stores (43)Oklahoma City 467 432 8.1% 35

7 DS Dollar General (33)Goodlettsville, Tenn. 9,372 8,828 6.2% 544

8 DS Dollar Tree (44)Chesapeake, Va. 4,015 3,806 5.5% 209

9 FS Ashley Furniture HomeStores (41)Arcadia, Wis. 422 401 5.2% 21

10 DC Ross Stores (10)Pleasanton, Calif. 1,055 1,005 5.0% 50

Source: Home Textiles Today market research

NUMBER OF STORES PERCENT NET CHG.

RANK TYPE COMPANY (TOP 50 RANK)/CITY 2010 2009 CHANGE (UNITS)

TOP 10 HOME TEXTILES RETAILERSBY NET UNIT GROWTH

1 DS Dollar General (33)Goodlettsville, Tenn. 9,372 8,828 6.2% 544

2 DS Dollar Tree (44)Chesapeake, Va. 4,015 3,806 5.5% 209

3 DS Family Dollar (11)Matthews, N.C. 6,888 6,689 3.0% 199

4 DC Ross Stores (10)Pleasanton, Calif. 1,055 1,005 5.0% 50

5 DC T.J. Maxx/Marshalls (8)Framingham, Mass. 1,753 1,703 2.9% 50

6 DC/SC Wal-Mart ( 1)Bentonville, Ark. 3,804 3,755 1.3% 49

7 DC Big Lots (12)Columbus, Ohio 1,398 1,361 2.7% 37

8 SP Hobby Lobby Stores (43)Oklahoma City 467 432 8.1% 35

9 SP Bed Bath & Beyond (2)Union, N.J. 1,071 1,039 3.1% 32

10 DP Kohl’s ( 5)Menomonee Falls, Wis. 1,089 1,058 2.9% 31

Source: Home Textiles Today market research

NUMBER OF STORES PERCENT NET CHG.

RANK TYPE COMPANY (TOP 50 RANK)/CITY 2010 2009 CHANGE (UNITS)

January 30, 2012

htt120104_008_010 10 1/16/2012 4:53:06 PM

Lenzi

ng A

G,

A-4

860 L

enzi

ng,

Austr

ia

www.lenzing.com/tencel

The fiber brand for the botanic bed

TENCEL® is made from wood and is thus 100 % from Nature. TENCEL® can be used in lots of different ways in beds, starting with mat-

tresses and mattress overlays, to bed covers and bed linens, through to lingerie. Thus a completely botanic bed becomes a reality.

Lenzing Fibers, Inc.

530 Seventh Avenue, Suite 808, New York, NY 10018-3508

Phone: 212 944-7898, E-Mail: [email protected]

Home Textiles Today12 Top 50January 30, 2012 > hometextilestoday.com

1 1 DC/SC Wal-Mart Bentonville, Ark. $3,575 $3,570 0.1% 1.4% 14.3% 3,804 3,755Fiscal year ended Jan. 31. Sales and store counts are for U.S. Wal-Mart stores and Neighborhood Market stores, plus online sales; excludes Sam’s Clubs. Began testing a smaller format, Walmart Express, store this summer. After cutting fabrics departments in 2009 as part of a streamlining process, announced in spring 2011 it would restore fabrics. International expansion included buying a Chinese ecommerce company and taking a 51% stake in Massmart, a retail conglomer-ate in Africa. Sales for the home category accounted for 5% of sales in 2010 and 2009. Private-label store brands for textiles include Hometrends, Mainstays and Canopy. Total 2010 sales were $260.3 billion, up 0.1% from $259.9 billion in 2009.

2 2 SP Bed Bath & Beyond Union, N.J. $3,535 $3,190 10.8% 40.4% 14.1% 1,071 1,039Fiscal year ended Feb. 26. Operated 1,139 stores in all 50 states, the District of Columbia, Puerto Rico and Canada at fiscal year end, including 982 Bed Bath & Beyond stores, 66 Christmas Tree Shops, 46 Harmon Face Value stores and 45 buybuyBaby stores. Sales and store counts do not include the 22 stores in Canada or the 46 Harmon stores. Also not included, are the two retail stores in Mexico under the name Home & More. Domestics accounted for 41% of sales in 2010 and 2009. Bed linens declined to 12% of total sales in 2010, from 13% in 2009. Total 2010 sales were $8.76 billion, up 11.9% from $7.83 billion in 2009. Comp-store sales were up 7.8%. Opened 40 stores last year, including 18 BBB and its first store in Hawaii. Plans to open 45 new stores this year.

3 3 DC/SC Target Minneapolis $2,550 $2,460 3.7% 3.9% 10.2% 1,750 1,740Fiscal year ended Jan. 29. Opened 13 new stores in 2010 and closed three. Focused on remodeling stores and expanding food sections in general merchandise stores last year. Its short-run Liberty of London program in home and apparel in spring 2010 was a smash hit. Plans to open 21 new U.S. stores this year. Selected 105 former Zeller units in 10 Canadian provinces to remodel into Target stores following its acquisition. Comp-store sales increased 2.1%, driven by a 2% increase in the number of transactions and a 0.1% increase in the average transaction amount. Home furnishings and decor, as a percentage of total, comprised 19% in 2010, the same as in 2009. Total 2010 sales were $65.8 billion, up 3.7% from $63.4 billion in 2009.

4 4 DP/DTC JCPenney Plano, Texas $2,275 $2,380 -4.4% 12.8% 9.1% 1,106 1,108Fiscal year ended Jan. 29. Includes sales from 28 Home Stores, three furniture outlet stores and online. Opened two stores and closed four last year. In January, announced plans to wind down its catalog and outlet operations. Also plans to close six retail stores in 2011. Unveiled a new logo in February, the most meaningful update in 40 years. Liz Claiborne is new brand introduction in home fashions, with official debut set for fall 2011. Apple retail chief Ron Johnson to become new ceo, effective November, with current chairman and ceo Mike Ullman to exit the company in early 2012. Total 2010 sales were $17.8 billion, up 1.2% from $17.6 billion in 2009.

5 5 DP Kohl’s Menomonee Falls, Wis. $1,275 $1,206 5.7% 6.9% 5.1% 1,089 1,058Fiscal year ended Jan. 29. Home outperformed total comp store sales growth last year. Home sales accounted for 18% of 2010 sales, the same as in 2009. Launched ELLE Décor in approximately 350 stores in September 2010. The brand includes contemporary home and home décor products. New Rock & Republic brand set for spring 2012 launch in apparel and footwear will eventually expand into home. Total 2010 sales were $18.39 billion, up 7.1% from $17.18 billion in 2009. Comp-store sales were up 4.4%. Opened 31 units in 2010 and remodeled 85. Plans for 2011 include opening 40 stores and remodeling 100.

6 6 DC/SC Kmart Hoffman Estates, Ill. $841 $845 -0.5% 5.4% 3.4% 1,307 1,327Fiscal year ended Jan. 29. Part of publicly held Sears Holdings, which also owns Lands’ End and Sears. Operated 1,307 stores across 49 states, Guam, Puerto Rico and the U.S. Virgin Islands at fiscal year end. Store count includes discount stores and supercenters. Also sells online. Offers a number of different textiles brands including Jaclyn Smith, Casa Cristina, Country Living and Cannon, marking its first year since the 1990s with the once-powerhouse Martha Stewart Everyday brand. Total 2010 sales were $15.59 billion, down 1% from $15.74 billion in 2009, primarily reflecting the impact of having fewer stores in operation. Comp-store sales increased 0.7%, driven by increases in most categories.

7 7 DP Macy’s New York $820 $830 -1.2% NA 3.3% 805 810Fiscal year ended Jan. 29. Sales and store counts are for Macy’s only, including 67 Macy’s Furniture Gallery stores and online. Adopted mobile technology last year giving consumers the ability to use any smart phone to navigate its e-commerce sites. Also launched an upgraded iShop app for the iPhone and began piloting Shopkick, a new location-based shopping app at 150 stores in the New York, L.A., San Francisco and Chicago markets. Announced in summer 2011 the interna-tional launch of macys.com ecommerce in 91 countries. Home sales for Macy’s corporate comprised 15% of 2010 sales, down from 16% in 2009. The company’s Internet business in 2010 increased 28.7% last year. Total corporate sales were $25 billion in 2010, up 6.4% from $23.5 billion in 2009.

8 8 DC T.J. M axx/Marshalls Framingham, Mass. $690 $657 5.0% 4.9% 2.8% 1,753 1,703Fiscal year ended Jan. 29. Part of The TJX Companies. Sales and store counts are for the Marmaxx Group operating 923 T.J. Maxx and 830 Marshalls in the U.S. and Puerto Rico at fiscal year end. The off-price retail chains sell brand-name and designer merchandise at prices 20% to 60% below department and specialty store prices. Home categories improved significantly last year, with same store sales increases above the chain average of 4%. Total 2010 sales were $14.09 billion, up 6.2% from $13.27 billion in 2009. Marmaxx expects to open approximately 116 new stores in 2011, including the conversion of 65 A.J. Wright stores. Marshalls will open its first stores in Canada this year.

9 9 SP/DTC Williams-Sonoma San Francisco $535 $465 15.1% 15.3% 2.1% 576 593Fiscal year ended Jan. 30. Publicly held, specialty home furnishings retailer with six brands - Williams-Sonoma, Pottery Barn, Pottery Barn Kids, PBteen, West Elm and Williams-Sonoma Home - selling through 592 stores in 44 states, Washington, D.C., Canada and Puerto Rico, six direct mail-order catalogs and six e-sites. Figures do not include the 16 stores in Canada. In 2010, expanded by opening three PB and three PBK stores through a franchise agreement with M.H. Alshaya Company in Dubai and Kuwait. Completed the restructuring of the Williams-Sonoma Home brand with the transition to online only and closing retail stores. Began shipping internationally through online sites to more than 75 countries in June 2011. The Internet is the fastest-growing channel accounting for 41% of revenues. Williams-Sonoma experienced record performance last year with all brands doing well. In the direct channel, growth was driven by the three PB brands. At retail, growth was driven by PB, West Elm and Williams-Sonoma. Total 2010 revenues were $3.5 billion, up 12.9% from $3.1 billion in 2009.

10 11 DC Ross S tores Pleasanton, Calif. $480 $430 11.6% 6.1% 1.9% 1,055 1,005Fiscal year ended Jan. 29. Operated 988 Ross Dress for Less locations in 27 states and Guam and 67 dd’s Discounts stores in six states at fiscal year end. Both off-price chains target value-conscious consumers. Home had low, double-digit same store sales increases last year. Home accents and bed and bath accounted for 25% of 2010 sales, up from 24% in 2009. Total 2010 sales were $7.87 billion, up 9.5% from $7.18 billion in 2009. Comp store sales increased 5%. Last year, opened 41 new Ross stores and closed six and opened 15 new dd’s Discounts stores. In 2011, plans to open 60 Ross stores and 22 dd’s units, including the retailer’s initial entry into Illinois and Arkansas.

HOME TEXTILES AS SHARE OF

RANK RANK STORE % A % OF STORE’S HOME TEXTILES NUMBER OF STORES

2010 2009 TYPE COMPANY HEADQUARTERS 2010 2009 CHANGE TOTAL SALES UNIVERSE 2010 2009

All home textiles sales information, except for publicly held companies that break out line-of-business sales for home textiles, are Home Textiles Today market research estimates.All data for calendar year ending Dec. 31, fiscal year-end or trailing 12 months closest to that date.NS=No stores; NA=Not available; R=RevisedStore type: DTC=Direct-to-consumer; CH= Chain store; DC=Discount department store; DP=Department store; DS=Dollar store; HIC=Home improvement center; PX=Military exchange; SC= Supercenter (includes food in merchandise mix); SP= Specialty store; W=Warehouse club; FS=Furniture storeSource: Home Textiles Today market research

RETAILING GIANTS

htt120104_012_018 12 1/16/2012 4:56:22 PM

Trident.indd 1 1/18/2012 1:07:08 PM

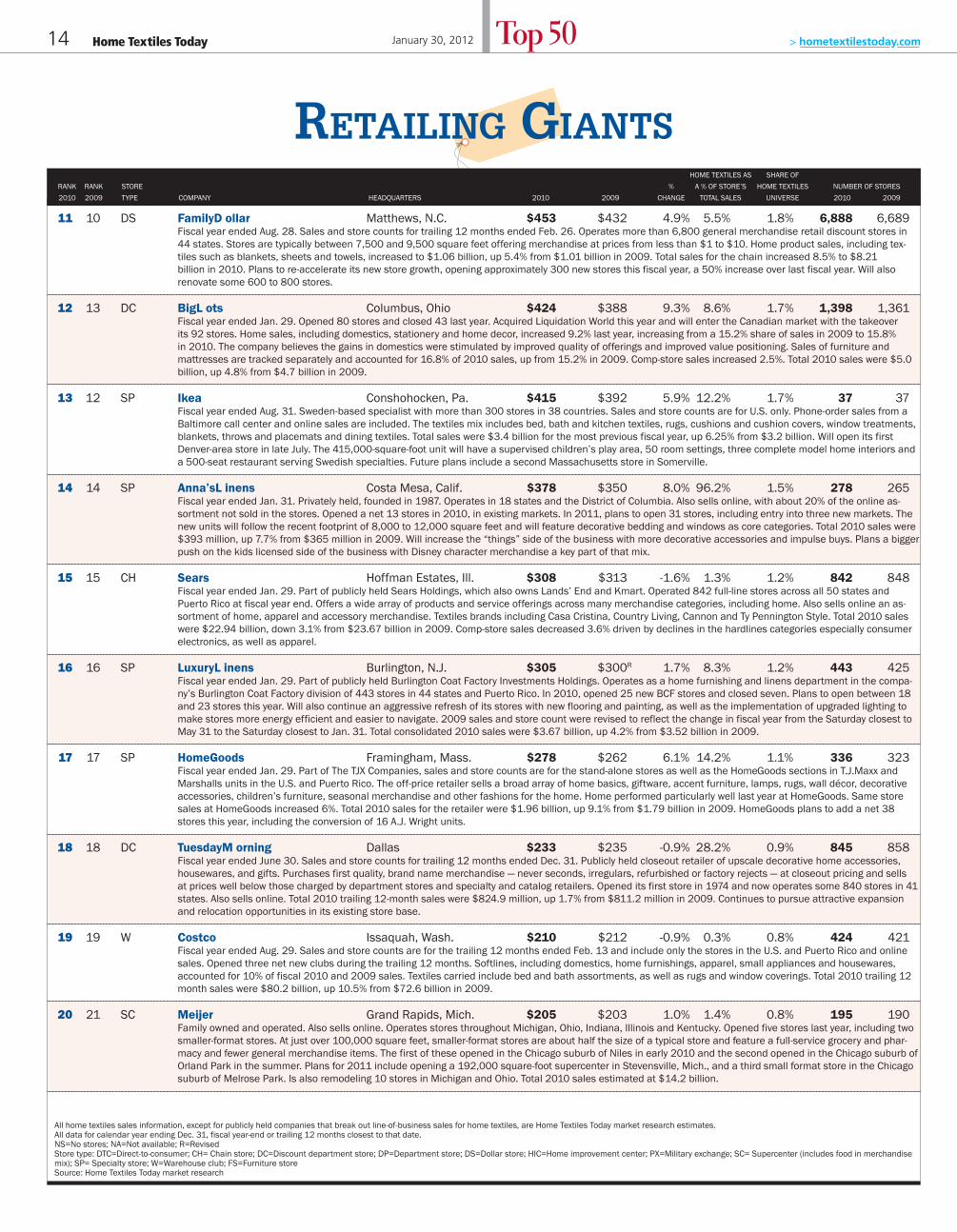

Home Textiles Today14 Top 50 > hometextilestoday.com

11 10 DS Family D ollar Matthews, N.C. $453 $432 4.9% 5.5% 1.8% 6,888 6,689Fiscal year ended Aug. 28. Sales and store counts for trailing 12 months ended Feb. 26. Operates more than 6,800 general merchandise retail discount stores in 44 states. Stores are typically between 7,500 and 9,500 square feet offering merchandise at prices from less than $1 to $10. Home product sales, including tex-tiles such as blankets, sheets and towels, increased to $1.06 billion, up 5.4% from $1.01 billion in 2009. Total sales for the chain increased 8.5% to $8.21 billion in 2010. Plans to re-accelerate its new store growth, opening approximately 300 new stores this fiscal year, a 50% increase over last fiscal year. Will also renovate some 600 to 800 stores.

12 13 DC Big L ots Columbus, Ohio $424 $388 9.3% 8.6% 1.7% 1,398 1,361Fiscal year ended Jan. 29. Opened 80 stores and closed 43 last year. Acquired Liquidation World this year and will enter the Canadian market with the takeover its 92 stores. Home sales, including domestics, stationery and home decor, increased 9.2% last year, increasing from a 15.2% share of sales in 2009 to 15.8% in 2010. The company believes the gains in domestics were stimulated by improved quality of offerings and improved value positioning. Sales of furniture and mattresses are tracked separately and accounted for 16.8% of 2010 sales, up from 15.2% in 2009. Comp-store sales increased 2.5%. Total 2010 sales were $5.0 billion, up 4.8% from $4.7 billion in 2009.

13 12 SP Ikea Conshohocken, Pa. $415 $392 5.9% 12.2% 1.7% 37 37Fiscal year ended Aug. 31. Sweden-based specialist with more than 300 stores in 38 countries. Sales and store counts are for U.S. only. Phone-order sales from a Baltimore call center and online sales are included. The textiles mix includes bed, bath and kitchen textiles, rugs, cushions and cushion covers, window treatments, blankets, throws and placemats and dining textiles. Total sales were $3.4 billion for the most previous fiscal year, up 6.25% from $3.2 billion. Will open its first Denver-area store in late July. The 415,000-square-foot unit will have a supervised children’s play area, 50 room settings, three complete model home interiors and a 500-seat restaurant serving Swedish specialties. Future plans include a second Massachusetts store in Somerville.

14 14 SP Anna’s L inens Costa Mesa, Calif. $378 $350 8.0% 96.2% 1.5% 278 265Fiscal year ended Jan. 31. Privately held, founded in 1987. Operates in 18 states and the District of Columbia. Also sells online, with about 20% of the online as-sortment not sold in the stores. Opened a net 13 stores in 2010, in existing markets. In 2011, plans to open 31 stores, including entry into three new markets. The new units will follow the recent footprint of 8,000 to 12,000 square feet and will feature decorative bedding and windows as core categories. Total 2010 sales were $393 million, up 7.7% from $365 million in 2009. Will increase the “things” side of the business with more decorative accessories and impulse buys. Plans a bigger push on the kids licensed side of the business with Disney character merchandise a key part of that mix.

15 15 CH Sears Hoffman Estates, Ill. $308 $313 -1.6% 1.3% 1.2% 842 848Fiscal year ended Jan. 29. Part of publicly held Sears Holdings, which also owns Lands’ End and Kmart. Operated 842 full-line stores across all 50 states and Puerto Rico at fiscal year end. Offers a wide array of products and service offerings across many merchandise categories, including home. Also sells online an as-sortment of home, apparel and accessory merchandise. Textiles brands including Casa Cristina, Country Living, Cannon and Ty Pennington Style. Total 2010 sales were $22.94 billion, down 3.1% from $23.67 billion in 2009. Comp-store sales decreased 3.6% driven by declines in the hardlines categories especially consumer electronics, as well as apparel.

16 16 SP Luxury L inens Burlington, N.J. $305 $300R 1.7% 8.3% 1.2% 443 425Fiscal year ended Jan. 29. Part of publicly held Burlington Coat Factory Investments Holdings. Operates as a home furnishing and linens department in the compa-ny’s Burlington Coat Factory division of 443 stores in 44 states and Puerto Rico. In 2010, opened 25 new BCF stores and closed seven. Plans to open between 18 and 23 stores this year. Will also continue an aggressive refresh of its stores with new flooring and painting, as well as the implementation of upgraded lighting to make stores more energy efficient and easier to navigate. 2009 sales and store count were revised to reflect the change in fiscal year from the Saturday closest to May 31 to the Saturday closest to Jan. 31. Total consolidated 2010 sales were $3.67 billion, up 4.2% from $3.52 billion in 2009.

17 17 SP HomeGoods Framingham, Mass. $278 $262 6.1% 14.2% 1.1% 336 323Fiscal year ended Jan. 29. Part of The TJX Companies, sales and store counts are for the stand-alone stores as well as the HomeGoods sections in T.J.Maxx and Marshalls units in the U.S. and Puerto Rico. The off-price retailer sells a broad array of home basics, giftware, accent furniture, lamps, rugs, wall décor, decorative accessories, children’s furniture, seasonal merchandise and other fashions for the home. Home performed particularly well last year at HomeGoods. Same store sales at HomeGoods increased 6%. Total 2010 sales for the retailer were $1.96 billion, up 9.1% from $1.79 billion in 2009. HomeGoods plans to add a net 38 stores this year, including the conversion of 16 A.J. Wright units.

18 18 DC Tuesday M orning Dallas $233 $235 -0.9% 28.2% 0.9% 845 858Fiscal year ended June 30. Sales and store counts for trailing 12 months ended Dec. 31. Publicly held closeout retailer of upscale decorative home accessories, housewares, and gifts. Purchases first quality, brand name merchandise — never seconds, irregulars, refurbished or factory rejects — at closeout pricing and sells at prices well below those charged by department stores and specialty and catalog retailers. Opened its first store in 1974 and now operates some 840 stores in 41 states. Also sells online. Total 2010 trailing 12-month sales were $824.9 million, up 1.7% from $811.2 million in 2009. Continues to pursue attractive expansion and relocation opportunities in its existing store base.

19 19 W Costco Issaquah, Wash. $210 $212 -0.9% 0.3% 0.8% 424 421Fiscal year ended Aug. 29. Sales and store counts are for the trailing 12 months ended Feb. 13 and include only the stores in the U.S. and Puerto Rico and online sales. Opened three net new clubs during the trailing 12 months. Softlines, including domestics, home furnishings, apparel, small appliances and housewares, accounted for 10% of fiscal 2010 and 2009 sales. Textiles carried include bed and bath assortments, as well as rugs and window coverings. Total 2010 trailing 12 month sales were $80.2 billion, up 10.5% from $72.6 billion in 2009.

20 21 SC Meijer Grand Rapids, Mich. $205 $203 1.0% 1.4% 0.8% 195 190Family owned and operated. Also sells online. Operates stores throughout Michigan, Ohio, Indiana, Illinois and Kentucky. Opened five stores last year, including two smaller-format stores. At just over 100,000 square feet, smaller-format stores are about half the size of a typical store and feature a full-service grocery and phar-macy and fewer general merchandise items. The first of these opened in the Chicago suburb of Niles in early 2010 and the second opened in the Chicago suburb of Orland Park in the summer. Plans for 2011 include opening a 192,000 square-foot supercenter in Stevensville, Mich., and a third small format store in the Chicago suburb of Melrose Park. Is also remodeling 10 stores in Michigan and Ohio. Total 2010 sales estimated at $14.2 billion.

HOME TEXTILES AS SHARE OF

RANK RANK STORE % A % OF STORE’S HOME TEXTILES NUMBER OF STORES

2010 2009 TYPE COMPANY HEADQUARTERS 2010 2009 CHANGE TOTAL SALES UNIVERSE 2010 2009

All home textiles sales information, except for publicly held companies that break out line-of-business sales for home textiles, are Home Textiles Today market research estimates.All data for calendar year ending Dec. 31, fiscal year-end or trailing 12 months closest to that date.NS=No stores; NA=Not available; R=RevisedStore type: DTC=Direct-to-consumer; CH= Chain store; DC=Discount department store; DP=Department store; DS=Dollar store; HIC=Home improvement center; PX=Military exchange; SC= Supercenter (includes food in merchandise mix); SP= Specialty store; W=Warehouse club; FS=Furniture storeSource: Home Textiles Today market research

RETAILING GIANTS

January 30, 2012

htt120104_012_018 14 1/16/2012 4:57:32 PM

15 Home Textiles Today> hometextilestoday.com

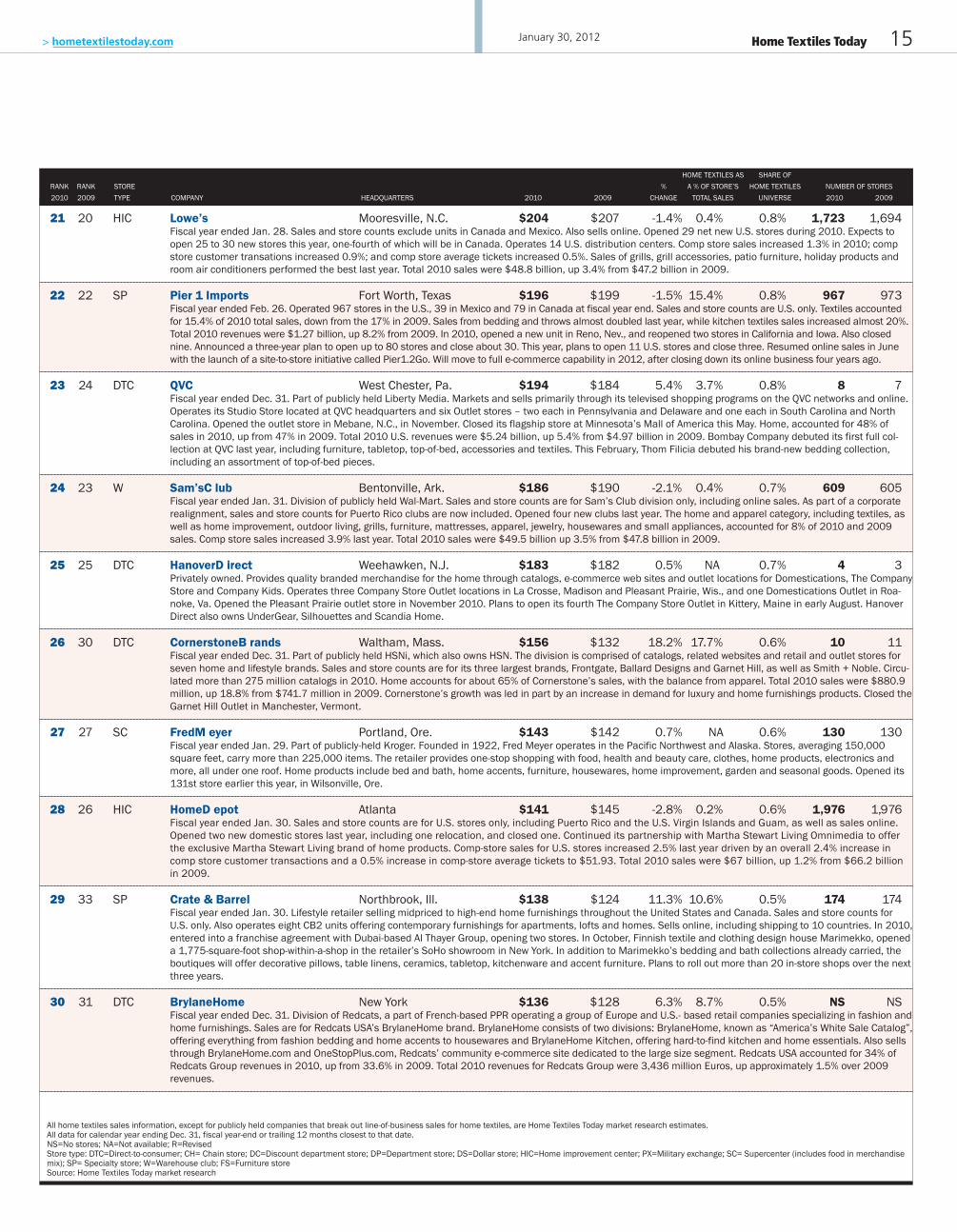

21 20 HIC Lowe’s Mooresville, N.C. $204 $207 -1.4% 0.4% 0.8% 1,723 1,694Fiscal year ended Jan. 28. Sales and store counts exclude units in Canada and Mexico. Also sells online. Opened 29 net new U.S. stores during 2010. Expects to open 25 to 30 new stores this year, one-fourth of which will be in Canada. Operates 14 U.S. distribution centers. Comp store sales increased 1.3% in 2010; comp store customer transations increased 0.9%; and comp store average tickets increased 0.5%. Sales of grills, grill accessories, patio furniture, holiday products and room air conditioners performed the best last year. Total 2010 sales were $48.8 billion, up 3.4% from $47.2 billion in 2009.

22 22 SP Pier 1 Imports Fort Worth, Texas $196 $199 -1.5% 15.4% 0.8% 967 973Fiscal year ended Feb. 26. Operated 967 stores in the U.S., 39 in Mexico and 79 in Canada at fiscal year end. Sales and store counts are U.S. only. Textiles accounted for 15.4% of 2010 total sales, down from the 17% in 2009. Sales from bedding and throws almost doubled last year, while kitchen textiles sales increased almost 20%. Total 2010 revenues were $1.27 billion, up 8.2% from 2009. In 2010, opened a new unit in Reno, Nev., and reopened two stores in California and Iowa. Also closed nine. Announced a three-year plan to open up to 80 stores and close about 30. This year, plans to open 11 U.S. stores and close three. Resumed online sales in June with the launch of a site-to-store initiative called Pier1.2Go. Will move to full e-commerce capability in 2012, after closing down its online business four years ago.

23 24 DTC QVC West Chester, Pa. $194 $184 5.4% 3.7% 0.8% 8 7Fiscal year ended Dec. 31. Part of publicly held Liberty Media. Markets and sells primarily through its televised shopping programs on the QVC networks and online. Operates its Studio Store located at QVC headquarters and six Outlet stores – two each in Pennsylvania and Delaware and one each in South Carolina and North Carolina. Opened the outlet store in Mebane, N.C., in November. Closed its flagship store at Minnesota’s Mall of America this May. Home, accounted for 48% of sales in 2010, up from 47% in 2009. Total 2010 U.S. revenues were $5.24 billion, up 5.4% from $4.97 billion in 2009. Bombay Company debuted its first full col-lection at QVC last year, including furniture, tabletop, top-of-bed, accessories and textiles. This February, Thom Filicia debuted his brand-new bedding collection, including an assortment of top-of-bed pieces.

24 23 W Sam’s C lub Bentonville, Ark. $186 $190 -2.1% 0.4% 0.7% 609 605Fiscal year ended Jan. 31. Division of publicly held Wal-Mart. Sales and store counts are for Sam’s Club division only, including online sales. As part of a corporate realignment, sales and store counts for Puerto Rico clubs are now included. Opened four new clubs last year. The home and apparel category, including textiles, as well as home improvement, outdoor living, grills, furniture, mattresses, apparel, jewelry, housewares and small appliances, accounted for 8% of 2010 and 2009 sales. Comp store sales increased 3.9% last year. Total 2010 sales were $49.5 billion up 3.5% from $47.8 billion in 2009.

25 25 DTC Hanover D irect Weehawken, N.J. $183 $182 0.5% NA 0.7% 4 3Privately owned. Provides quality branded merchandise for the home through catalogs, e-commerce web sites and outlet locations for Domestications, The Company Store and Company Kids. Operates three Company Store Outlet locations in La Crosse, Madison and Pleasant Prairie, Wis., and one Domestications Outlet in Roa-noke, Va. Opened the Pleasant Prairie outlet store in November 2010. Plans to open its fourth The Company Store Outlet in Kittery, Maine in early August. Hanover Direct also owns UnderGear, Silhouettes and Scandia Home.

26 30 DTC Cornerstone B rands Waltham, Mass. $156 $132 18.2% 17.7% 0.6% 10 11Fiscal year ended Dec. 31. Part of publicly held HSNi, which also owns HSN. The division is comprised of catalogs, related websites and retail and outlet stores for seven home and lifestyle brands. Sales and store counts are for its three largest brands, Frontgate, Ballard Designs and Garnet Hill, as well as Smith + Noble. Circu-lated more than 275 million catalogs in 2010. Home accounts for about 65% of Cornerstone’s sales, with the balance from apparel. Total 2010 sales were $880.9 million, up 18.8% from $741.7 million in 2009. Cornerstone’s growth was led in part by an increase in demand for luxury and home furnishings products. Closed the Garnet Hill Outlet in Manchester, Vermont.

27 27 SC Fred M eyer Portland, Ore. $143 $142 0.7% NA 0.6% 130 130Fiscal year ended Jan. 29. Part of publicly-held Kroger. Founded in 1922, Fred Meyer operates in the Pacific Northwest and Alaska. Stores, averaging 150,000 square feet, carry more than 225,000 items. The retailer provides one-stop shopping with food, health and beauty care, clothes, home products, electronics and more, all under one roof. Home products include bed and bath, home accents, furniture, housewares, home improvement, garden and seasonal goods. Opened its 131st store earlier this year, in Wilsonville, Ore.

28 26 HIC Home D epot Atlanta $141 $145 -2.8% 0.2% 0.6% 1,976 1,976Fiscal year ended Jan. 30. Sales and store counts are for U.S. stores only, including Puerto Rico and the U.S. Virgin Islands and Guam, as well as sales online. Opened two new domestic stores last year, including one relocation, and closed one. Continued its partnership with Martha Stewart Living Omnimedia to offer the exclusive Martha Stewart Living brand of home products. Comp-store sales for U.S. stores increased 2.5% last year driven by an overall 2.4% increase in comp store customer transactions and a 0.5% increase in comp-store average tickets to $51.93. Total 2010 sales were $67 billion, up 1.2% from $66.2 billion in 2009.

29 33 SP Crate & Barrel Northbrook, Ill. $138 $124 11.3% 10.6% 0.5% 174 174Fiscal year ended Jan. 30. Lifestyle retailer selling midpriced to high-end home furnishings throughout the United States and Canada. Sales and store counts for U.S. only. Also operates eight CB2 units offering contemporary furnishings for apartments, lofts and homes. Sells online, including shipping to 10 countries. In 2010, entered into a franchise agreement with Dubai-based Al Thayer Group, opening two stores. In October, Finnish textile and clothing design house Marimekko, opened a 1,775-square-foot shop-within-a-shop in the retailer’s SoHo showroom in New York. In addition to Marimekko’s bedding and bath collections already carried, the boutiques will offer decorative pillows, table linens, ceramics, tabletop, kitchenware and accent furniture. Plans to roll out more than 20 in-store shops over the next three years.

30 31 DTC BrylaneHome New York $136 $128 6.3% 8.7% 0.5% NS NSFiscal year ended Dec. 31. Division of Redcats, a part of French-based PPR operating a group of Europe and U.S.- based retail companies specializing in fashion and home furnishings. Sales are for Redcats USA’s BrylaneHome brand. BrylaneHome consists of two divisions: BrylaneHome, known as “America’s White Sale Catalog”, offering everything from fashion bedding and home accents to housewares and BrylaneHome Kitchen, offering hard-to-find kitchen and home essentials. Also sells through BrylaneHome.com and OneStopPlus.com, Redcats’ community e-commerce site dedicated to the large size segment. Redcats USA accounted for 34% of Redcats Group revenues in 2010, up from 33.6% in 2009. Total 2010 revenues for Redcats Group were 3,436 million Euros, up approximately 1.5% over 2009 revenues.

HOME TEXTILES AS SHARE OF

RANK RANK STORE % A % OF STORE’S HOME TEXTILES NUMBER OF STORES

2010 2009 TYPE COMPANY HEADQUARTERS 2010 2009 CHANGE TOTAL SALES UNIVERSE 2010 2009

All home textiles sales information, except for publicly held companies that break out line-of-business sales for home textiles, are Home Textiles Today market research estimates.All data for calendar year ending Dec. 31, fiscal year-end or trailing 12 months closest to that date.NS=No stores; NA=Not available; R=RevisedStore type: DTC=Direct-to-consumer; CH= Chain store; DC=Discount department store; DP=Department store; DS=Dollar store; HIC=Home improvement center; PX=Military exchange; SC= Supercenter (includes food in merchandise mix); SP= Specialty store; W=Warehouse club; FS=Furniture storeSource: Home Textiles Today market research

January 30, 2012

htt120104_012_018 15 1/16/2012 4:58:31 PM

Home Textiles Today16 Top 50January 30, 2012 > hometextilestoday.com

31 28 DP Bloomingdale’s New York $135 $138 -2.2% NA 0.5% 45 40Fiscal year ended Jan. 29, part of publicly-held Macy’s Inc. Opened a new full-line store in Santa Monica, Calif., in 2010. And, launched a new Bloomingdale’s Outlet store concept, with four new outlets opening last Fall: one each in Paramus, N.J., Woodbridge, Va., and Miami and Sunrise, Fla. Expects to open three new outlets this year. Opened in February 2010 a store in Dubai, United Arab Emirates, under a license agreement with Al Tayer Insignia. Has increased social media marketing efforts and adopted mobile technology. Last fall, allowed customers to check in at any Bloomingdale’s store on Foursquare to be automatically entered for prizes.

32 29 SP Restoration H ardware Corte Madera, Calif. $132 $134 -1.5% NA 0.5% 104 107Owned by private equity firms, Catterton Partners and Tower Three Partners. Upscale multi-channel retailer of premium goods, operating through stores in the U. S. and Canada, online and catalogs. Sales and store count for U.S. only. Catalogs include RH Home, RH Outdoor & Garden and RH Baby & Child. Continued to reposition itself to the high-end of the market, renovating 85 stores to the “gallery” format. First introduced this format with the opening of its new stores in New York City’s Flatiron District and the Town Center Corte Madera shopping center in 2009. Last fall, opened its first store for the design trade with a 9,500-square-foot flagship store in San Francisco’s Design District. May file an IPO in 2011 potentially raising as much as $300 million. The retailer went private in 2008.

33 34 DS Dollar G eneral Goodlettsville, Tenn. $126 $120 5.0% 1.0% 0.5% 9,372 8,828Fiscal year ended Jan. 28. Operates in 35 states. Units average 7,200 square feet offering merchandise at substantial discounts. Home accounted for 7% of 2010 sales, down from 7.4% in 2009. Total 2010 sales were $13.03 billion, up 10.5% from $11.8 billion in 2009. Same-store sales increased 4.9%. Launched the True Living line of home products in 2010. Will continue to upgrade selection, quality and presentation of its private brand offerings in home, including textiles. Made significant progress in expanding its private brand efforts in textiles last year. Plans to open 625 stores in 2011 entering Connecticut, New Hampshire and Nevada. Plans to open its first stores in California in 2012.

34 32 DP The Bon-Ton Stores York, Pa. $125 $126 -0.8% 4.2% 0.5% 275 278Fiscal year ended Jan. 29. Currently operates stores in 23 states in the Northeast, Midwest and upper Great Plains under the Bon-Ton, Bergner’s, Boston Store, Carson Pirie Scott, Elder-Beerman, Herberger’s and Younkers nameplates and, in the Detroit area, under the Parisian name. Also sells online. In textiles, offers exclusive private brands as well as national brands such as Calvin Klein, Croscill, LivingQuarters Loft, MaryJanes Home and Tommy Hilfiger. Home accounted for 16.8% of 2010 sales, the same as in 2009. Total 2010 sales were $2.98 billion, up 0.7% from $2.96 billion in 2009. Comp store sales increased 0.9% up from a decrease of 5.4% in 2009. Closed three stores at the end of its fiscal year. In November, will open a Herberger’s in Edina, Minn., and a Carson’s store in Kokomo, Ind., replacing the Elder-Beerman store there.

35 35 DC Shopko Green Bay, Wis. $94 $93 1.1% NA 0.4% 138 136Privately-held affiliate of Sun Capital Partners. Sales and store counts exclude five Shopko Express Rx stores. Operated 136 Shopko stores and two Shopko Hometown locations in 13 states throughout the Midwest, Mountain and Pacific Northwest regions at years end. Also sells online, having recently renovated its e-commerce site. Last summer, introduced Shopko Hometown, a new concept store designed to meet the needs of smaller, underserved markets, in Oconto and Kewaunee, Wis. The stores offer a broad merchandise selection, as well as pharmacy services and eye care centers, but in a smaller format, at 36,000 square feet. Both the Oconto and Kewaunee stores replaced Pamida stores. Plans to have a total of 10 Hometown stores by the end of 2011. Total 2010 sales esti-mated at $2 billion.

36 36 DP Belk Charlotte, N.C. $78 $75 4.0% 2.2% 0.3% 305 305Fiscal year ended Jan. 29. Operates stores in 16 states, primarily in the southern U. S. Also sells online. Opened a new store in Port Orange, Fla., last year and com-pleted major remodel projects in 10 stores. Plans to complete three store expansions and open one replacement store this year. Home accounted for 9% of 2010 sales, the same as in 2009. Total 2010 sales were $3.51 billion, up 5% from $3.35 billion in 2009. Comp store sales increased 5.1% compared to a decrease of 4.6% in 2009. Last year, launched a new logo and tag line, “Modern. Southern. Style,” representing the first significant change to Belk’s brand identity since 1967.

37 38 DTC Country C urtains Lee, Mass. $73 $72 1.4% 93.6% 0.3% 26 25Private family and employee owned company founded in 1956. Sells through its catalog, website and retail stores located in 13 states in Connecticut, Delaware, Illinois, Massachusetts, Maryland, New Hampshire, New Jersey, New York, Ohio, Pennsylvania, Rhode Island, Virginia and Vermont. Known for its quality window treatment designs and window decorating services, the company also offers bedding, pillows and coordinates, including chair pads and table linens and home décor, including rugs. In November 2010, opened its 26th store and first one in Pennsylvania, in Warrington.

38 37 DP Dillard’s Little Rock, Ark. $73 $75 -2.7% 1.2% 0.3% 308 309Fiscal year ended Jan. 29. Operates in 29 states. Carries a broad selection of apparel and home furnishings from national brand merchandise and exclusive brands. Accounting for 6% of total sales, the home and furniture category was down only 3.6% last year, compared to a 22.4% decrease in 2009 when the category accounted for 7% of total sales. Total 2010 sales were $6.02 billion, up 2.2% from $5.89 billion in 2009. Opened two stores last year in Austin and Fairview, Texas, and closed three in Helena, Mont., Coral Springs, Fla., and Miami. No planned store openings for 2011. Will close the unit in Decatur, Ala., midyear. Purchased a former Target distribution center in Maumelle, Ark., with plans of converting the building into a fulfillment center to support online growth.

39 40 PX Army & Air Force Exchange Svc. Dallas $72 $69 4.3% 1.0% 0.3% 198 183Revenues based on worldwide sales, excluding gasoline. Market areas include worldwide Army/Air Force posts and bases serving active-duty personnel, guard and reservists, retirees and their families, some 7 million customers. Receives no funds from the Department of Defense. Has main stores or shopping centers world-wide and in every state. Textiles are carried in 198 main stores, the online website AAFES.com, and in print catalogs. Customers can also shop and buy through mobile apps for the iPhone and Blackberry. Worldwide total 2010 sales were $7.3 billion.

40 39 DTC Lands’ E nd Dodgeville, Wis. $71 $70 1.4% NA 0.3% 14 14Fiscal year ended Jan. 29. Part of publicly held Sears Holdings, which also owns Kmart and Sears. Direct merchant offering traditionally-styled products for the home through catalogs, including the specialty Lands’ End Home catalog, its retail stores, its website and Sears full-line stores. Lands’ End retail stores, averag-ing 8,600 square feet, offer merchandise primarily from catalog and Internet channel overstocks. Lands’ End Shops inside Sears’ full-line stores numbered 292 at years end. Each shop offers products for women, men and kids and select stores offer items for the home.

HOME TEXTILES AS SHARE OF

RANK RANK STORE % A % OF STORE’S HOME TEXTILES NUMBER OF STORES

2010 2009 TYPE COMPANY HEADQUARTERS 2010 2009 CHANGE TOTAL SALES UNIVERSE 2010 2009

All home textiles sales information, except for publicly held companies that break out line-of-business sales for home textiles, are Home Textiles Today market research estimates.All data for calendar year ending Dec. 31, fiscal year-end or trailing 12 months closest to that date.NS=No stores; NA=Not available; R=RevisedStore type: DTC=Direct-to-consumer; CH= Chain store; DC=Discount department store; DP=Department store; DS=Dollar store; HIC=Home improvement center; PX=Military exchange; SC= Supercenter (includes food in merchandise mix); SP= Specialty store; W=Warehouse club; FS=Furniture storeSource: Home Textiles Today market research

RETAILING GIANTS

htt120104_012_018 16 1/16/2012 4:59:19 PM

Invistia.indd 1 1/13/2012 8:56:48 AM

Home Textiles Today18 January 30, 2012 > hometextilestoday.com

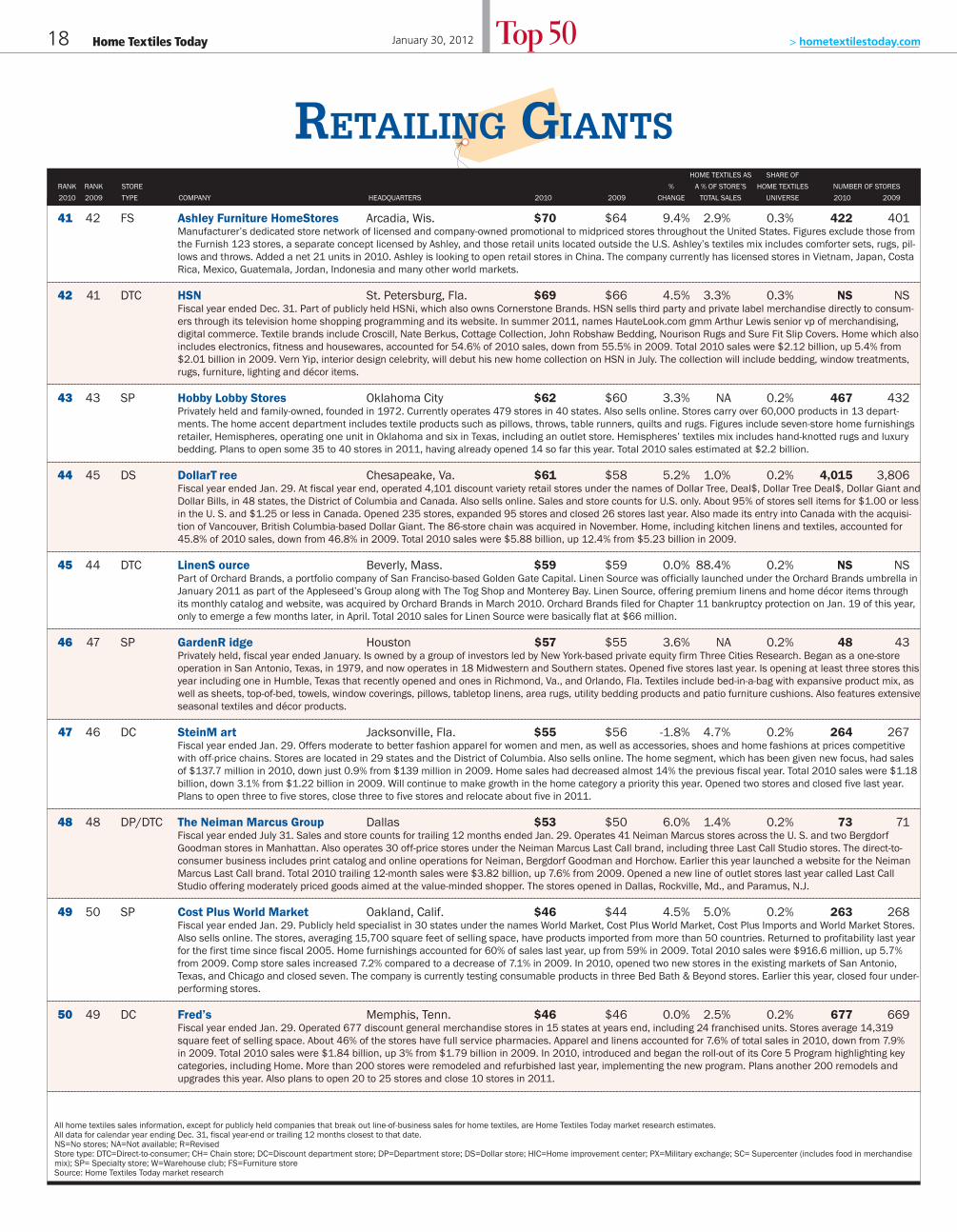

41 42 FS Ashley Furniture HomeStores Arcadia, Wis. $70 $64 9.4% 2.9% 0.3% 422 401Manufacturer’s dedicated store network of licensed and company-owned promotional to midpriced stores throughout the United States. Figures exclude those from the Furnish 123 stores, a separate concept licensed by Ashley, and those retail units located outside the U.S. Ashley’s textiles mix includes comforter sets, rugs, pil-lows and throws. Added a net 21 units in 2010. Ashley is looking to open retail stores in China. The company currently has licensed stores in Vietnam, Japan, Costa Rica, Mexico, Guatemala, Jordan, Indonesia and many other world markets.

42 41 DTC HSN St. Petersburg, Fla. $69 $66 4.5% 3.3% 0.3% NS NSFiscal year ended Dec. 31. Part of publicly held HSNi, which also owns Cornerstone Brands. HSN sells third party and private label merchandise directly to consum-ers through its television home shopping programming and its website. In summer 2011, names HauteLook.com gmm Arthur Lewis senior vp of merchandising, digital commerce. Textile brands include Croscill, Nate Berkus, Cottage Collection, John Robshaw Bedding, Nourison Rugs and Sure Fit Slip Covers. Home which also includes electronics, fitness and housewares, accounted for 54.6% of 2010 sales, down from 55.5% in 2009. Total 2010 sales were $2.12 billion, up 5.4% from $2.01 billion in 2009. Vern Yip, interior design celebrity, will debut his new home collection on HSN in July. The collection will include bedding, window treatments, rugs, furniture, lighting and décor items.

43 43 SP Hobby Lobby Stores Oklahoma City $62 $60 3.3% NA 0.2% 467 432Privately held and family-owned, founded in 1972. Currently operates 479 stores in 40 states. Also sells online. Stores carry over 60,000 products in 13 depart-ments. The home accent department includes textile products such as pillows, throws, table runners, quilts and rugs. Figures include seven-store home furnishings retailer, Hemispheres, operating one unit in Oklahoma and six in Texas, including an outlet store. Hemispheres’ textiles mix includes hand-knotted rugs and luxury bedding. Plans to open some 35 to 40 stores in 2011, having already opened 14 so far this year. Total 2010 sales estimated at $2.2 billion.

44 45 DS Dollar T ree Chesapeake, Va. $61 $58 5.2% 1.0% 0.2% 4,015 3,806Fiscal year ended Jan. 29. At fiscal year end, operated 4,101 discount variety retail stores under the names of Dollar Tree, Deal$, Dollar Tree Deal$, Dollar Giant and Dollar Bills, in 48 states, the District of Columbia and Canada. Also sells online. Sales and store counts for U.S. only. About 95% of stores sell items for $1.00 or less in the U. S. and $1.25 or less in Canada. Opened 235 stores, expanded 95 stores and closed 26 stores last year. Also made its entry into Canada with the acquisi-tion of Vancouver, British Columbia-based Dollar Giant. The 86-store chain was acquired in November. Home, including kitchen linens and textiles, accounted for 45.8% of 2010 sales, down from 46.8% in 2009. Total 2010 sales were $5.88 billion, up 12.4% from $5.23 billion in 2009.

45 44 DTC Linen S ource Beverly, Mass. $59 $59 0.0% 88.4% 0.2% NS NSPart of Orchard Brands, a portfolio company of San Franciso-based Golden Gate Capital. Linen Source was officially launched under the Orchard Brands umbrella in January 2011 as part of the Appleseed’s Group along with The Tog Shop and Monterey Bay. Linen Source, offering premium linens and home décor items through its monthly catalog and website, was acquired by Orchard Brands in March 2010. Orchard Brands filed for Chapter 11 bankruptcy protection on Jan. 19 of this year, only to emerge a few months later, in April. Total 2010 sales for Linen Source were basically flat at $66 million.

46 47 SP Garden R idge Houston $57 $55 3.6% NA 0.2% 48 43Privately held, fiscal year ended January. Is owned by a group of investors led by New York-based private equity firm Three Cities Research. Began as a one-store operation in San Antonio, Texas, in 1979, and now operates in 18 Midwestern and Southern states. Opened five stores last year. Is opening at least three stores this year including one in Humble, Texas that recently opened and ones in Richmond, Va., and Orlando, Fla. Textiles include bed-in-a-bag with expansive product mix, as well as sheets, top-of-bed, towels, window coverings, pillows, tabletop linens, area rugs, utility bedding products and patio furniture cushions. Also features extensive seasonal textiles and décor products.

47 46 DC Stein M art Jacksonville, Fla. $55 $56 -1.8% 4.7% 0.2% 264 267Fiscal year ended Jan. 29. Offers moderate to better fashion apparel for women and men, as well as accessories, shoes and home fashions at prices competitive with off-price chains. Stores are located in 29 states and the District of Columbia. Also sells online. The home segment, which has been given new focus, had sales of $137.7 million in 2010, down just 0.9% from $139 million in 2009. Home sales had decreased almost 14% the previous fiscal year. Total 2010 sales were $1.18 billion, down 3.1% from $1.22 billion in 2009. Will continue to make growth in the home category a priority this year. Opened two stores and closed five last year. Plans to open three to five stores, close three to five stores and relocate about five in 2011.

48 48 DP/DTC The Neiman Marcus Group Dallas $53 $50 6.0% 1.4% 0.2% 73 71Fiscal year ended July 31. Sales and store counts for trailing 12 months ended Jan. 29. Operates 41 Neiman Marcus stores across the U. S. and two Bergdorf Goodman stores in Manhattan. Also operates 30 off-price stores under the Neiman Marcus Last Call brand, including three Last Call Studio stores. The direct-to-consumer business includes print catalog and online operations for Neiman, Bergdorf Goodman and Horchow. Earlier this year launched a website for the Neiman Marcus Last Call brand. Total 2010 trailing 12-month sales were $3.82 billion, up 7.6% from 2009. Opened a new line of outlet stores last year called Last Call Studio offering moderately priced goods aimed at the value-minded shopper. The stores opened in Dallas, Rockville, Md., and Paramus, N.J.

49 50 SP Cost Plus World Market Oakland, Calif. $46 $44 4.5% 5.0% 0.2% 263 268Fiscal year ended Jan. 29. Publicly held specialist in 30 states under the names World Market, Cost Plus World Market, Cost Plus Imports and World Market Stores. Also sells online. The stores, averaging 15,700 square feet of selling space, have products imported from more than 50 countries. Returned to profitability last year for the first time since fiscal 2005. Home furnishings accounted for 60% of sales last year, up from 59% in 2009. Total 2010 sales were $916.6 million, up 5.7% from 2009. Comp store sales increased 7.2% compared to a decrease of 7.1% in 2009. In 2010, opened two new stores in the existing markets of San Antonio, Texas, and Chicago and closed seven. The company is currently testing consumable products in three Bed Bath & Beyond stores. Earlier this year, closed four under-performing stores.

50 49 DC Fred’s Memphis, Tenn. $46 $46 0.0% 2.5% 0.2% 677 669Fiscal year ended Jan. 29. Operated 677 discount general merchandise stores in 15 states at years end, including 24 franchised units. Stores average 14,319 square feet of selling space. About 46% of the stores have full service pharmacies. Apparel and linens accounted for 7.6% of total sales in 2010, down from 7.9% in 2009. Total 2010 sales were $1.84 billion, up 3% from $1.79 billion in 2009. In 2010, introduced and began the roll-out of its Core 5 Program highlighting key categories, including Home. More than 200 stores were remodeled and refurbished last year, implementing the new program. Plans another 200 remodels and upgrades this year. Also plans to open 20 to 25 stores and close 10 stores in 2011.

HOME TEXTILES AS SHARE OF

RANK RANK STORE % A % OF STORE’S HOME TEXTILES NUMBER OF STORES

2010 2009 TYPE COMPANY HEADQUARTERS 2010 2009 CHANGE TOTAL SALES UNIVERSE 2010 2009

All home textiles sales information, except for publicly held companies that break out line-of-business sales for home textiles, are Home Textiles Today market research estimates.All data for calendar year ending Dec. 31, fiscal year-end or trailing 12 months closest to that date.NS=No stores; NA=Not available; R=RevisedStore type: DTC=Direct-to-consumer; CH= Chain store; DC=Discount department store; DP=Department store; DS=Dollar store; HIC=Home improvement center; PX=Military exchange; SC= Supercenter (includes food in merchandise mix); SP= Specialty store; W=Warehouse club; FS=Furniture storeSource: Home Textiles Today market research

Top 50

RETAILING GIANTS

htt120104_012_018 18 1/16/2012 5:00:55 PM

20 Home Textiles Today Top 15

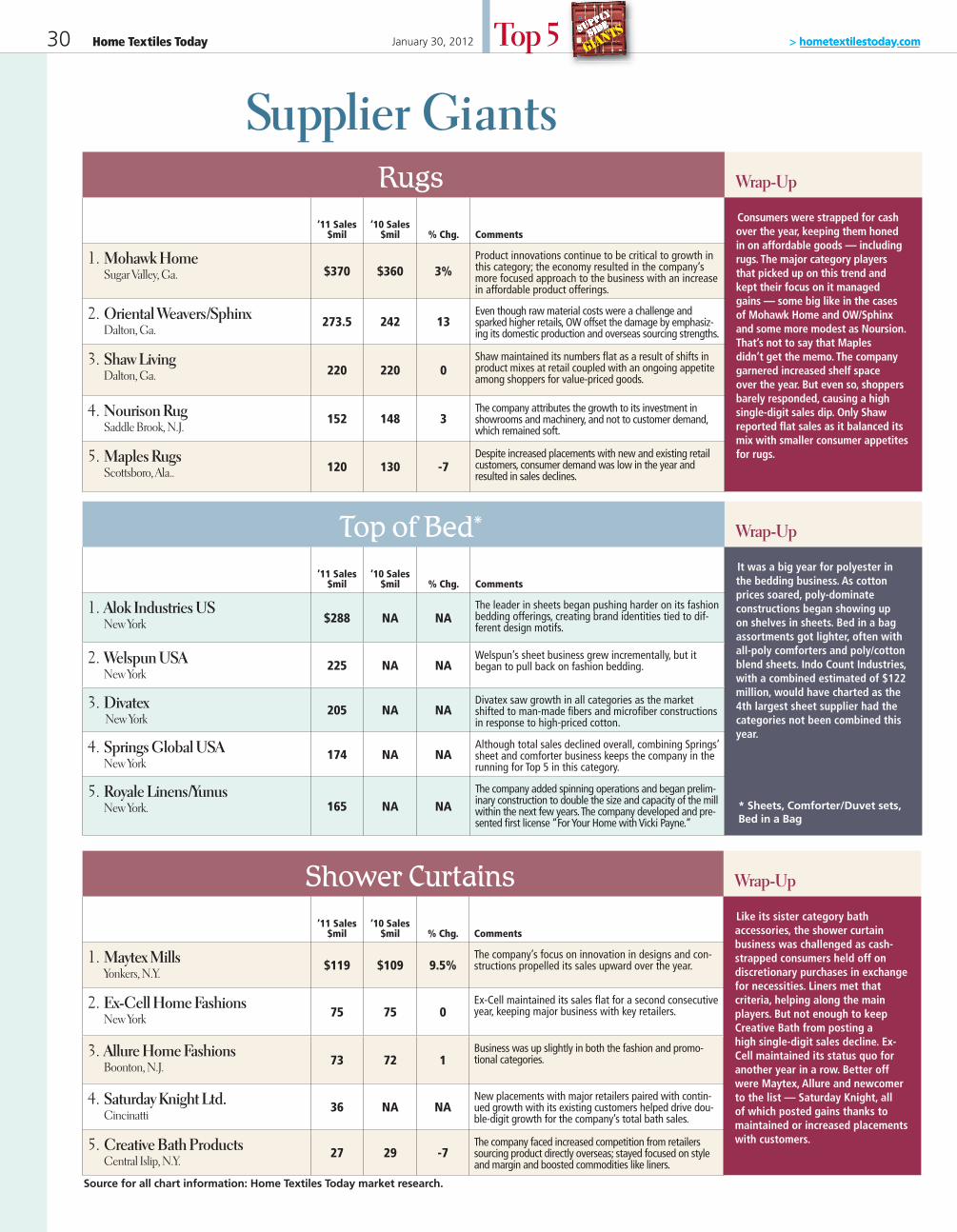

SIGNIFICANT EVENTS Thanks to high single-digit increases in bath rug sales and some more mod-est growth in its area and accent rug sales, Mohawk home was able to nudge up its total business performance for 2011 by almost 3%. Bath rugs enjoyed a strong year, generating a 7% increase to $210 million. New product innovations helped fuel growth, as did efforts to be more promotional with offerings. Sharper marketing was also credited with sales improvements and offsetting some volatile raw material costs. The rug category – which for Mohawk Home includes tufted, printed, and woven area and accent sizes – also posted gains, albeit a narrower 3%, to $370 million. The growth stemmed primarily from price-point stabilization. Product innovations continue to be criti-cal to the product growth in this category as well. The ongoing challenges in the macro-economy resulted in the company’s more focused approach to its rug business with a greater emphasis on value-oriented goods.

1

35 (’10)

62 (’10)

46(’10)

1 (’10)

SIGNIFICANT EVENTS Alok enhanced capacity in weaving and processing, helping to grow its already dominant sheet category. It strengthened US infrastructure and signed licensing agreements to expand into new retail channels. During its second full year in the towel busi-ness, Alok landed some major retail placements. The cotton blanket business grew substan-tially, and the mill added four new categories: soft window, table linens, shower curtains and basic bedding.

78 (’10)

(sales in $millions)

SIGNIFICANT EVENTS Carpenter scored a coup when the “2 Guys, 600 Pillows” promotional video it commissioned went viral, garnering more than 150,000 clicks and winning a Webby award. As part of an ongoing effort to communicate with consumers directly – both through its SleepBetter.org web site and direct campaigns — Carpenter tapped sleep specialty Dr. Lisa Shives – also known as “Dr. Lisa, The Sleep M.D.” — as its resident sleep authority under a multi-year contract.

SIGNIFICANT EVENTS Springs USA’s business continued to decline as a percentage of the Brazilian-based Springs Global’s overall business, contributing less than 50% of total sales through most of the year. The company continues to invest heavily in new branded programs – most of them involving Springs-manufactured hard goods as well as textiles. New launches announced in 2011 included Paula Dean and Nate Berkus, both scheduled to debut in 2012.

Mohawk Home Est. ‘11 Sales ‘10 Sales % Change

$636 $620 2.6%

23 (’10)

SIGNIFICANT EVENTS In a year of streamlining, Welspun closed its satellite office in North Carolina and idled its bedding plant in Mexico as it pulled back from fashion bedding to concentrate on category replenishment business. In February, the multi-category mill launched a line with designer Tom Filicia for QVC. It also continued to pursue expansion outside the U.S.

Welspun Est. ‘11 Sales ‘10 Sales % Change

$550 $498 10%

Alok US Est. ‘11 Sales ‘10 Sales % Change

$430 $396 8%

Carpenter Est. ‘11 Sales ‘10 Sales % Change

$348 $308 13%

Springs Global US Est. ‘11 Sales ‘10 Sales % Change

$319 $542 -41%

HTT’s Top 15 Supplier Giants

SIGNIFICANT EVENTS This is the first time PCF’s numbers include sales from United Feather and Down. The two companies announced their merger in March 2011. Overall, the combined numbers reflect a mixed year. Down and down alternative comforters sales declined; while pillows and mat-tress pads were up slightly.

Pacifi c Coast Feather Est. ‘11 Sales ‘10 Sales % Change

$294 $289 2%

SIGNIFICANT EVENTS WestPoint underwent a leadership shake-up in June as industry veteran Norman Savaria became the company’s new president and ceo, succeeding John Piazza. Savaria is the third ceo installed in the job since 2005 by billionaire investor Carl Icahn, whose Icahn Enterprises owns a majority stake in the company. In another key appointment, former Linens ’n Things vp Taran Chernin was named executive vp and chief merchandising officer.

WestPoint Home Est. ‘11 Sales ‘10 Sales % Change

$345 $423 -18%

54 (’10)

January 30, 2012 > hometextilestoday.com

htt120104_020_022 20 1/16/2012 5:05:12 PM

22 Home Textiles Today

SIGNIFICANT EVENTS Among the area rug companies on HTT’s top 15 list this year, Oriental Weavers/Sphinx posted the highest sales gain at 13%. Benefitting its business, the company noted, was its ability to make the best of both its worlds — domestic manufacturing and overseas production capabilities. OW/Sphinx was able to overcome negative impacts from unstable raw material costs and increases in retail price points by exploiting its U.S. manufacturing while still working with its Egypt-based roots.

Oriental Weavers/ Sphinx

Est. ‘11 Sales ‘10 Sales % Change

$273.5 $242 13%

913 (’10)

SIGNIFICANT EVENTS A house of domestically-made, synthetic fiber soft floor coverings, Shaw Living had its own share of challenges in 2011 with raw material costs and price point volatility — just like many of its closest competitors. Still, the company managed to maintain its rug sales status quo at $220 million and took only a 5% hit on bath rug sales, going to $51.3 million from 2010’s $54 million rates. Shaw blamed mostly shifts in product mixes at retail for the lackluster results in the year. Environmental initiatives continued to be important to Shaw’s mission, as the company furthered its efforts to offer recyclable rugs and employ eco-friendly production initia-tives at its many plants.

Shaw Living Est. ‘11 Sales ‘10 Sales % Change

$271.3 $274 -1

109 (’10)

SIGNIFICANT EVENTS 1888 Mills enjoyed double-digit sales gains thanks to what it called contin-ued growth in both its bath towels and kitchen textiles — which posted $200 million and $34 mil-lion in sales for 2011 respectively. Also giving business a lift: the launch of its exclusive partnership with HGTV celebrity designer David Bromstad for bath and bedding; the company’s acquisition of window covering manufacturer Beacon Looms; and the opening of a commercial apparel facility in Ghana.

1888 Mills Est. ‘11 Sales ‘10 Sales % Change

$270 240 12.5

1114 (’10)

SIGNIFICANT EVENTS Sleep Innovations took an “adapt or die” attitude with a push in product development. Michael Thompson, president and ceo noted that “aggressive customer programs and sell-through initiatives positioned us for continued growth in 2012.” The company tapped Olympic swimmer Dara Torres as a spokesperson and moved its gel-infused memory foam out of the bedroom with products for the bath as well as a foam chair for kids and teens.

Sleep Innovations Est. ‘11 Sales ‘10 Sales % Change

$261 $275 -5%

127 (’10)

SIGNIFICANT EVENTS Domestic manufacturer Maples Rugs, which has produced synthetic machine-made area, accent and bath rugs for three generations, was unable to fight off a single-digit sales decline this year. Even though the family-owned-and-operated company increased placements with new and existing retail customers, a sharp decline in consumer demand hurt the business. The pain was distributed evenly between area/accent rugs and bath rugs — each of which went down 7.7% to $120 million.

Maples Rugs Est. ‘11 Sales ‘10 Sales % Change

$240 $260 -7

1311 (’10)

SIGNIFICANT EVENTS Despite a lot of shifts in categories of business and channels of distribu-tion, CHF managed to hold the line on sales in 2011. While the bedding business declined, the bath business jumped significantly and window remained flat.

CHF Industries Est. ‘11 Sales ‘10 Sales % Change

$224 $224 0

1515 (’10)

SIGNIFICANT EVENTS A major force in sheets, Divatex also does enough business in its ancillary cat-egories — duvet sets and throws, in particular — to thrust it into the Top 15. The company marked its 25th anniversary last year the way it does most things: quietly and under the radar.

Divatex Est. ‘11 Sales ‘10 Sales % Change

$230 NA NA

14NA (’10)

810 (’10)

SIGNIFICANT EVENTS Hollander managed a modest increase in the difficult category of down and down alternative comforters as well as a boost in pillows. Sales of mattress pads remained even, however. This year, the company opened a Hollander full-service office in Mumbai and made key additions to its sales team.

Hollander HomeFashions

Est. ‘11 Sales ‘10 Sales % Change

$285 $272 5%

January 30, 2012 > hometextilestoday.comTop 15

htt120104_020_022 22 1/16/2012 5:06:57 PM

We’re The FolksThat Give You That

Warm Fuzzy Feeling.

Electric Heated Mattress Pads Electric Heated Plush Throws Electric Heated Blankets

For more information about Biddeford products, contact Maurice Hebert at: [email protected] or call 847.566.7442

Electric Heated Plush Blankets

At Biddeford we make nothing but electric heated blankets, mattress pads and plush throws. Because that’s all we do, we are able to offer our trade partners and their customers products of the highest quality at affordable prices. In addition to superior quality and competitive pricing,

we at Biddeford pride ourselves on providing the best customer service in the business. With Biddeford, in addition to quality, service and value. . . expect a warm fuzzy feeling.

Get That Warm Fuzzy Feeling.™

™

Bidderford Blankets.indd 1 1/4/2010 5:48:42 PM

24 Home Textiles Today > hometextilestoday.com

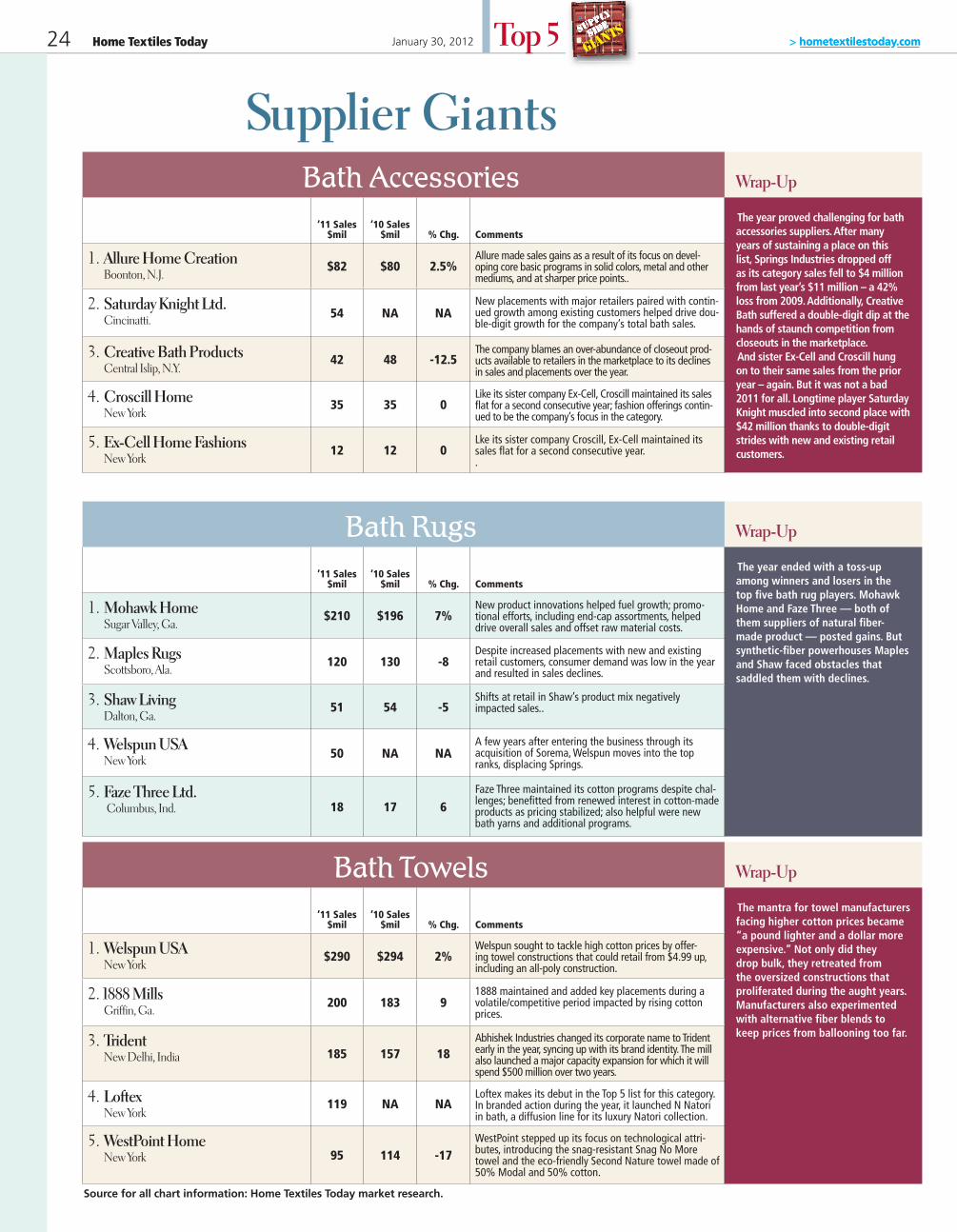

Bath Accessories Wrap-Up

’11 Sales$mil

’10 Sales$mil % Chg. Comments

The year proved challenging for bath accessories suppliers. After many years of sustaining a place on this list, Springs Industries dropped off as its category sales fell to $4 million from last year’s $11 million – a 42% loss from 2009. Additionally, Creative Bath suffered a double-digit dip at the hands of staunch competition from closeouts in the marketplace.And sister Ex-Cell and Croscill hung on to their same sales from the prior year – again. But it was not a bad 2011 for all. Longtime player Saturday Knight muscled into second place with $42 million thanks to double-digit strides with new and existing retail customers.

1. Allure Home CreationBoonton, N.J.

$82 $80 2.5%Allure made sales gains as a result of its focus on devel-oping core basic programs in solid colors, metal and other mediums, and at sharper price points..

2. Saturday Knight Ltd.Cincinatti. 54 NA NA

New placements with major retailers paired with contin-ued growth among existing customers helped drive dou-ble-digit growth for the company’s total bath sales.

3. Creative Bath ProductsCentral Islip, N.Y.

42 48 -12.5The company blames an over-abundance of closeout prod-ucts available to retailers in the marketplace to its declines in sales and placements over the year.

4. Croscill HomeNew York

35 35 0Like its sister company Ex-Cell, Croscill maintained its sales fl at for a second consecutive year; fashion offerings contin-ued to be the company’s focus in the category.

5. Ex-Cell Home FashionsNew York

12 12 0Lke its sister company Croscill, Ex-Cell maintained its sales fl at for a second consecutive year..

Supplier Giants

Bath Rugs Wrap-Up

’11 Sales$mil

’10 Sales$mil % Chg. Comments

The year ended with a toss-up among winners and losers in the top fi ve bath rug players. Mohawk Home and Faze Three — both of them suppliers of natural fi ber-made product — posted gains. But synthetic-fi ber powerhouses Maples and Shaw faced obstacles that saddled them with declines.

1. Mohawk HomeSugar Valley, Ga.