Embed Size (px)

Citation preview

1

BULGARI GROUP

FRANCESCO TRAPANI – Chief Executive OfficerFLAVIA SPENA – Chief Financial and Organization Officer

RENATA CASARO – Head of IR

HSBC LUXURY CONFERENCE

Paris, June 3rd 2009

2

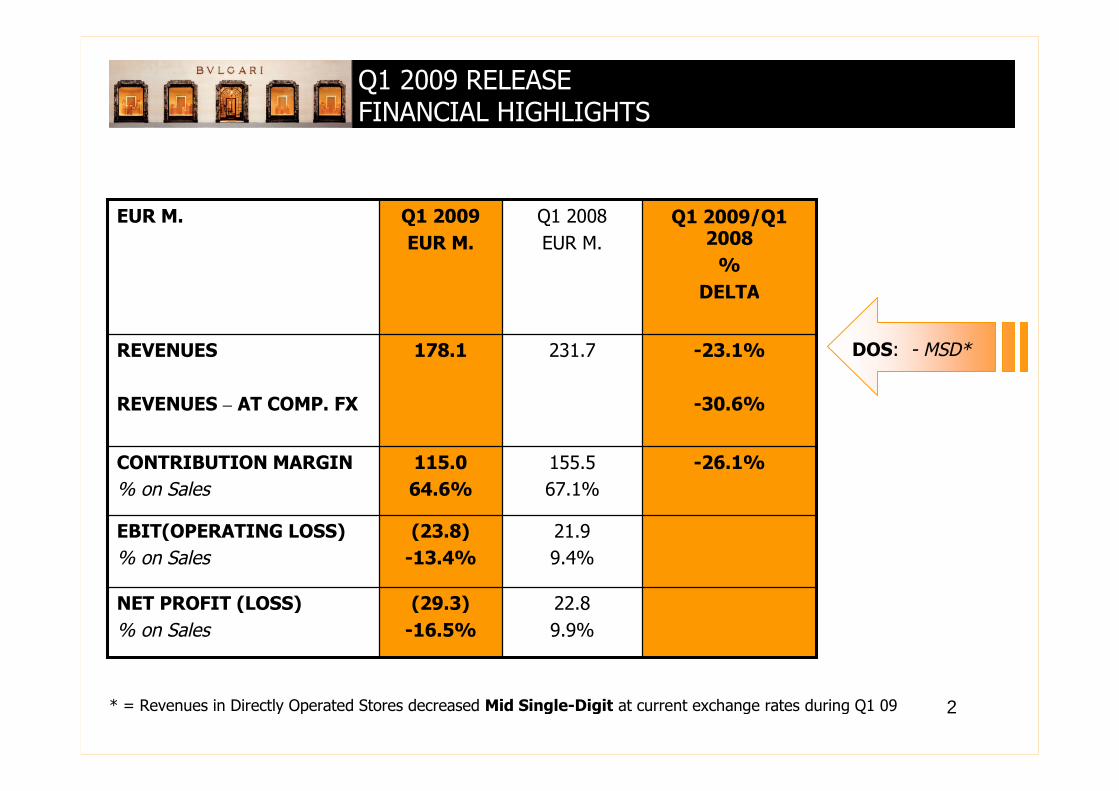

22.8

9.9%

(29.3)

-16.5%

NET PROFIT (LOSS)

% on Sales

21.9

9.4%

(23.8)

-13.4%

EBIT(OPERATING LOSS)

% on Sales

-26.1%155.5

67.1%

115.0

64.6%

CONTRIBUTION MARGIN

% on Sales

-23.1%

-30.6%

231.7178.1REVENUES

REVENUES – AT COMP. FX

Q1 2009/Q12008

%

DELTA

Q1 2008

EUR M.

Q1 2009

EUR M.

EUR M.

Q1 2009 RELEASEFINANCIAL HIGHLIGHTS

* = Revenues in Directly Operated Stores decreased Mid Single-Digit at current exchange rates during Q1 09

DOS: - MSD*

3

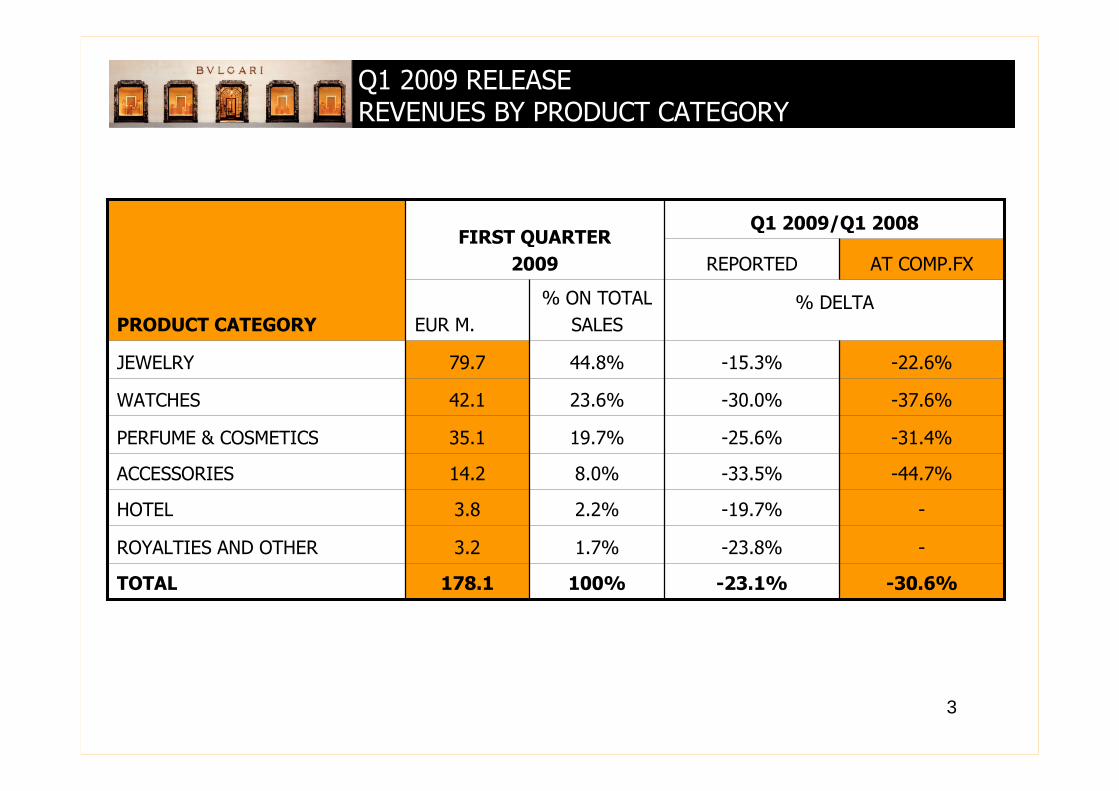

-44.7%-33.5%8.0%14.2ACCESSORIES

% ON TOTAL

SALESEUR M.% DELTA

-30.6%-23.1%100%178.1TOTAL

--23.8%1.7%3.2ROYALTIES AND OTHER

--19.7%2.2%3.8HOTEL

-31.4%-25.6%19.7%35.1PERFUME & COSMETICS

-37.6%-30.0%23.6%42.1WATCHES

-22.6%-15.3%44.8%79.7JEWELRY

AT COMP.FXREPORTED

Q1 2009/Q1 2008FIRST QUARTER

2009

PRODUCT CATEGORY

Q1 2009 RELEASEREVENUES BY PRODUCT CATEGORY

4

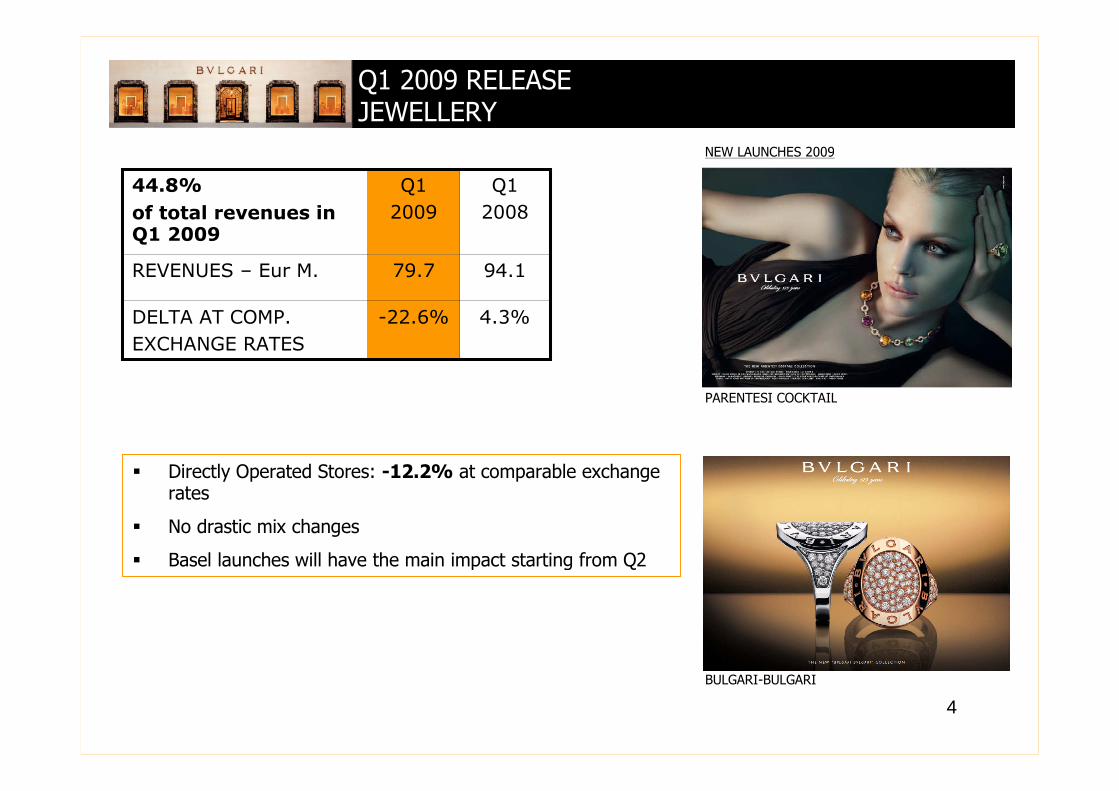

-22.6%

79.7

Q1

2009

Q1

2008

44.8%

of total revenues inQ1 2009

4.3%

94.1

DELTA AT COMP.

EXCHANGE RATES

REVENUES – Eur M.

PARENTESI COCKTAIL

Q1 2009 RELEASEJEWELLERY

BULGARI-BULGARI

Directly Operated Stores: -12.2% at comparable exchangerates

No drastic mix changes

Basel launches will have the main impact starting from Q2

NEW LAUNCHES 2009

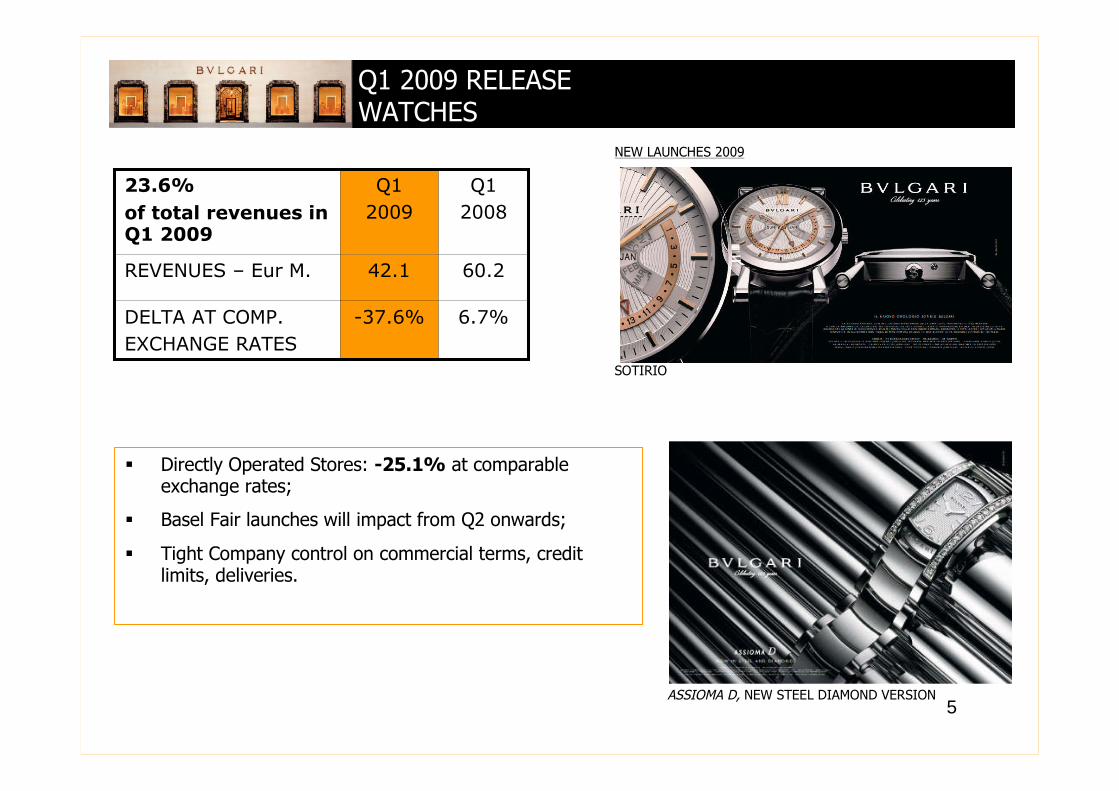

5

-37.6%

42.1

Q1

2009

Q1

2008

23.6%

of total revenues inQ1 2009

6.7%

60.2

DELTA AT COMP.

EXCHANGE RATES

REVENUES – Eur M.

SOTIRIO

Q1 2009 RELEASEWATCHES

Directly Operated Stores: -25.1% at comparableexchange rates;

Basel Fair launches will impact from Q2 onwards;

Tight Company control on commercial terms, creditlimits, deliveries.

ASSIOMA D, NEW STEEL DIAMOND VERSION

NEW LAUNCHES 2009

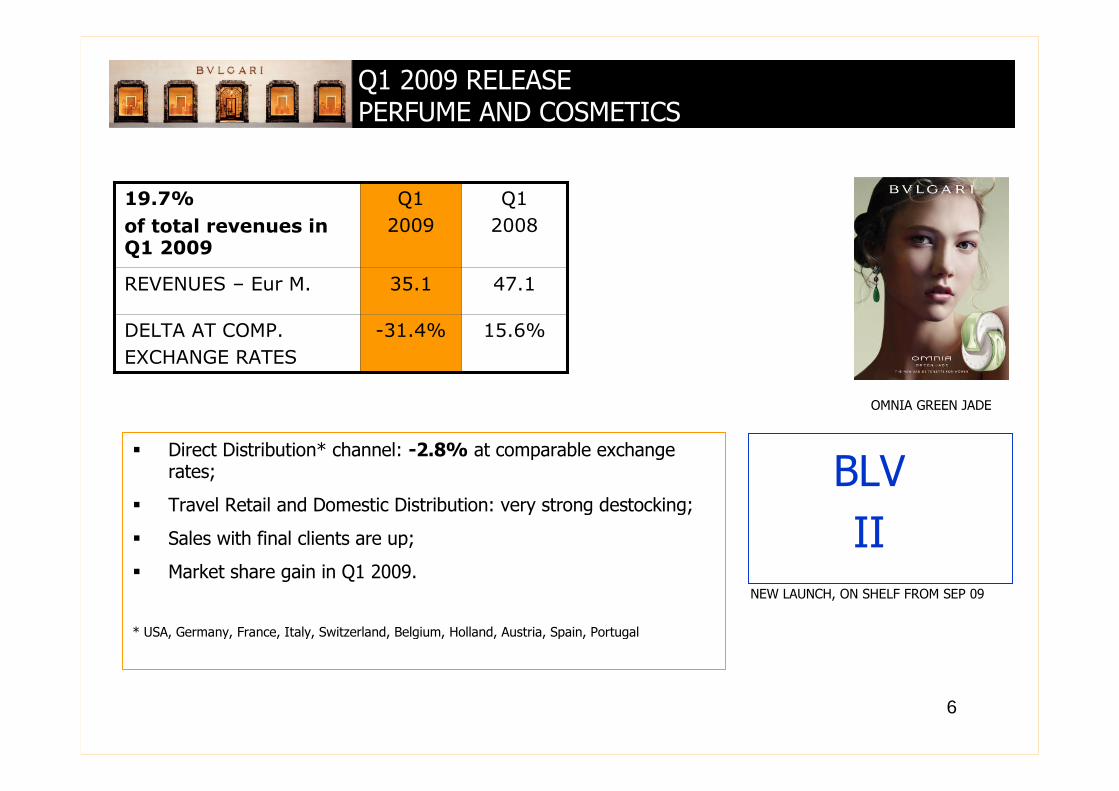

6

-31.4%

35.1

Q1

2009

Q1

2008

19.7%

of total revenues inQ1 2009

15.6%

47.1

DELTA AT COMP.

EXCHANGE RATES

REVENUES – Eur M.

NEW LAUNCH, ON SHELF FROM SEP 09

OMNIA GREEN JADE

Q1 2009 RELEASEPERFUME AND COSMETICS

Direct Distribution* channel: -2.8% at comparable exchangerates;

Travel Retail and Domestic Distribution: very strong destocking;

Sales with final clients are up;

Market share gain in Q1 2009.

* USA, Germany, France, Italy, Switzerland, Belgium, Holland, Austria, Spain, Portugal

BLV

II

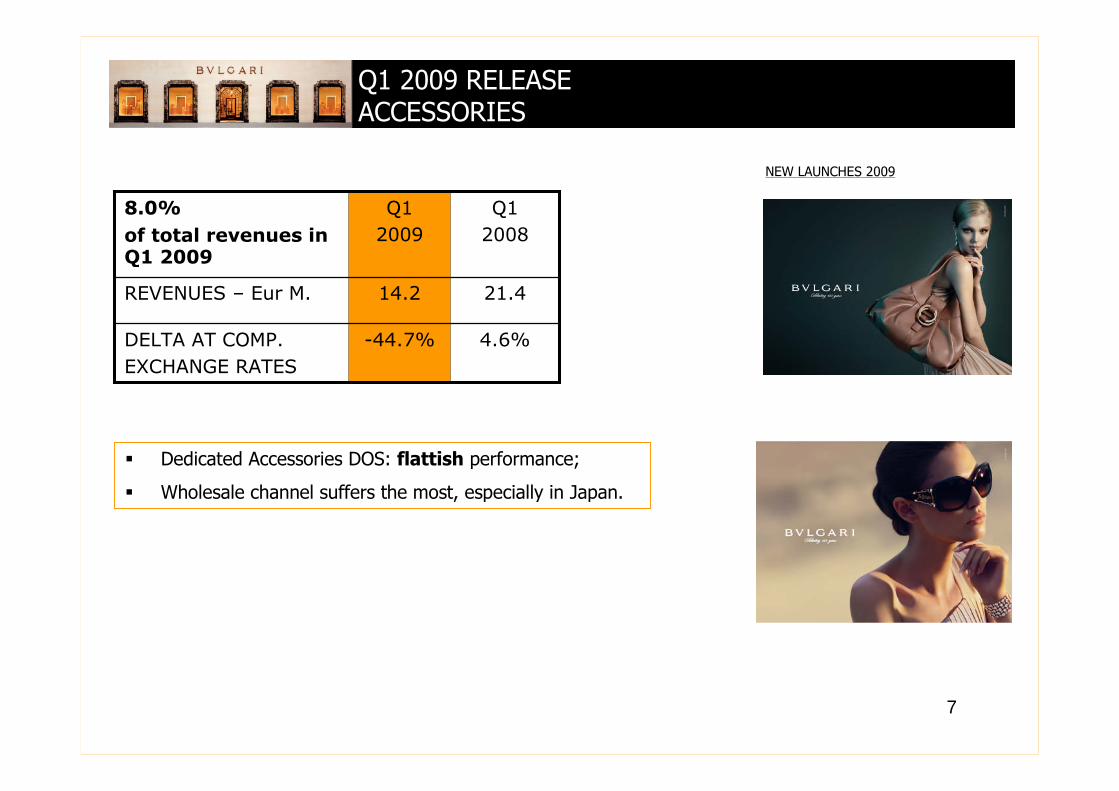

7

-44.7%

14.2

Q1

2009

Q1

2008

8.0%

of total revenues inQ1 2009

4.6%

21.4

DELTA AT COMP.

EXCHANGE RATES

REVENUES – Eur M.

Q1 2009 RELEASEACCESSORIES

Dedicated Accessories DOS: flattish performance;

Wholesale channel suffers the most, especially in Japan.

NEW LAUNCHES 2009

8

AT COMP.FX

-30.6%

-

-30.4%

-37.6%

-22.3%

-44.3%

-

-

-23.1%

-24.1%

-16.8%

-19.0%

-14.6%

-36.5%

-25.5%

-15.7%

REPORTED

% DELTA

Q1 2009/Q1 2008

100%178.1TOTAL

6.4%11.4MIDDLE EAST/ OTHER

46.5%

22.3%

24.2%

82.8

39.7

43.1

ASIA

Of which Japan

Of which Rest of Asia

10.8%19.3AMERICAS

36.3%

12.1%

64.6

21.6

EUROPE

Of which Italy

% ON TOTAL

SALESEUR M.

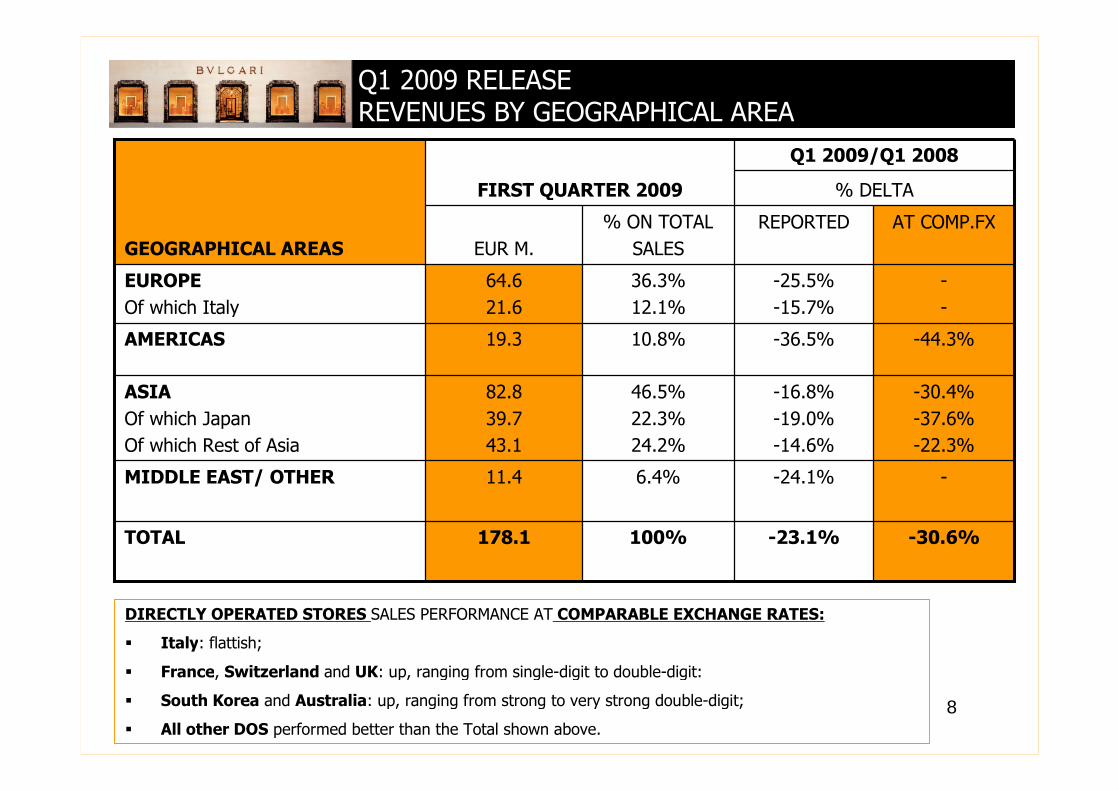

FIRST QUARTER 2009

GEOGRAPHICAL AREAS

Q1 2009 RELEASEREVENUES BY GEOGRAPHICAL AREA

DIRECTLY OPERATED STORES SALES PERFORMANCE AT COMPARABLE EXCHANGE RATES:

Italy: flattish;

France, Switzerland and UK: up, ranging from single-digit to double-digit:

South Korea and Australia: up, ranging from strong to very strong double-digit;

All other DOS performed better than the Total shown above.

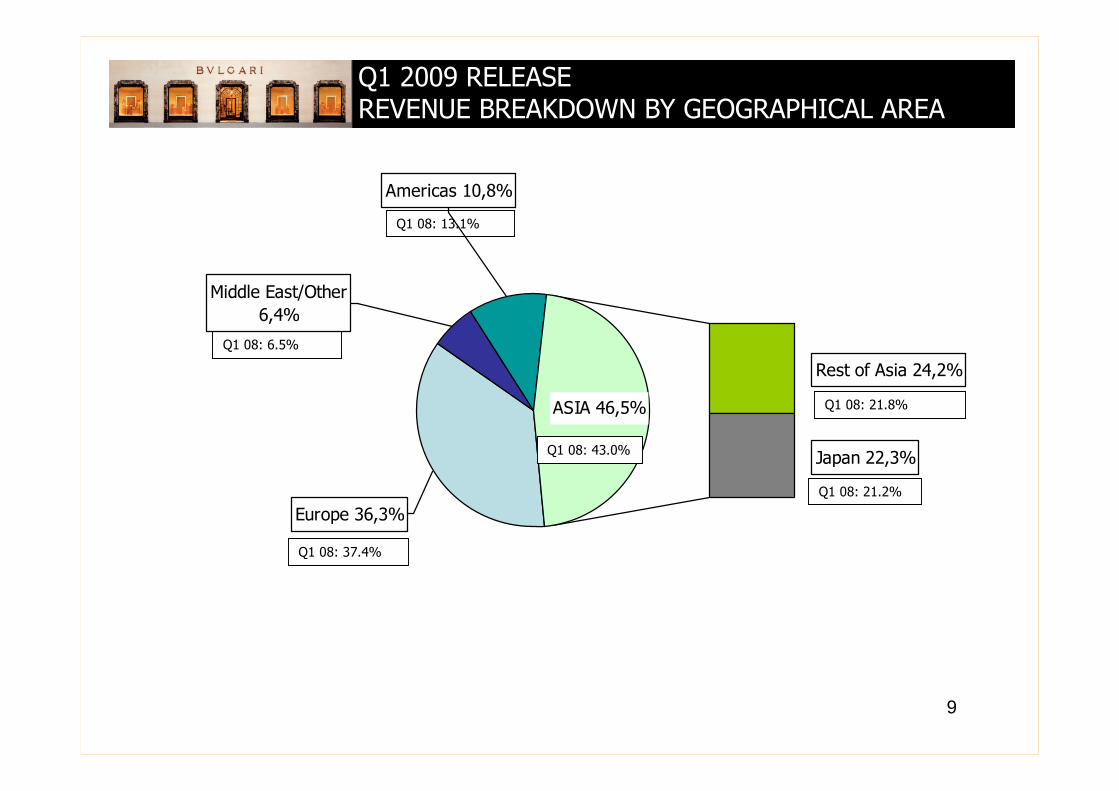

9

Rest of Asia 24,2%

Japan 22,3%

ASIA 46,5%

Americas 10,8%

Middle East/Other

6,4%

Europe 36,3%

Q1 2009 RELEASEREVENUE BREAKDOWN BY GEOGRAPHICAL AREA

Q1 08: 37.4%

Q1 08: 6.5%

Q1 08: 13.1%

Q1 08: 43.0%

Q1 08: 21.2%

Q1 08: 21.8%

10

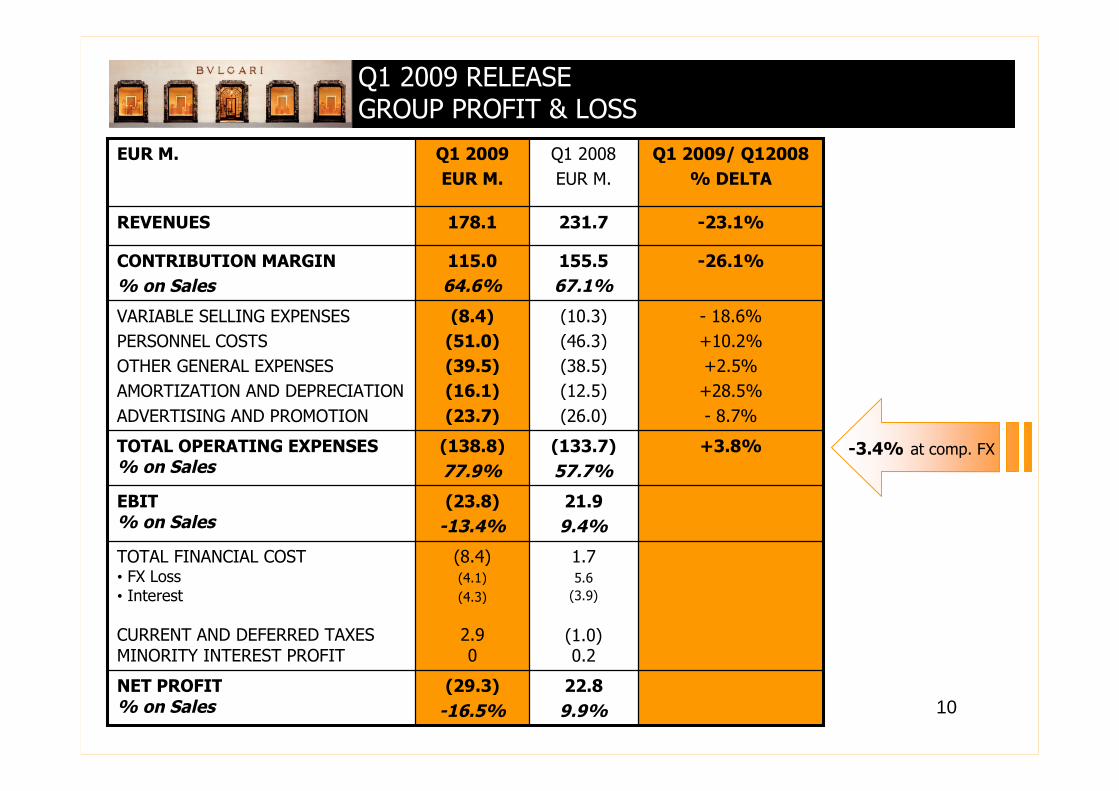

+3.8%(133.7)

57.7%

(138.8)

77.9%

TOTAL OPERATING EXPENSES% on Sales

21.9

9.4%

(23.8)

-13.4%

EBIT% on Sales

1.75.6

(3.9)

(1.0)0.2

(8.4)(4.1)

(4.3)

2.90

TOTAL FINANCIAL COST• FX Loss• Interest

CURRENT AND DEFERRED TAXESMINORITY INTEREST PROFIT

(29.3)

-16.5%

(8.4)

(51.0)

(39.5)

(16.1)

(23.7)

115.0

64.6%

178.1

Q1 2009

EUR M.

- 18.6%

+10.2%

+2.5%

+28.5%

- 8.7%

-26.1%

-23.1%

Q1 2009/ Q12008

% DELTA

(10.3)

(46.3)

(38.5)

(12.5)

(26.0)

VARIABLE SELLING EXPENSES

PERSONNEL COSTS

OTHER GENERAL EXPENSES

AMORTIZATION AND DEPRECIATION

ADVERTISING AND PROMOTION

22.8

9.9%

NET PROFIT% on Sales

155.5

67.1%

CONTRIBUTION MARGIN

% on Sales

231.7REVENUES

Q1 2008

EUR M.

EUR M.

Q1 2009 RELEASEGROUP PROFIT & LOSS

-3.4% at comp. FX

11

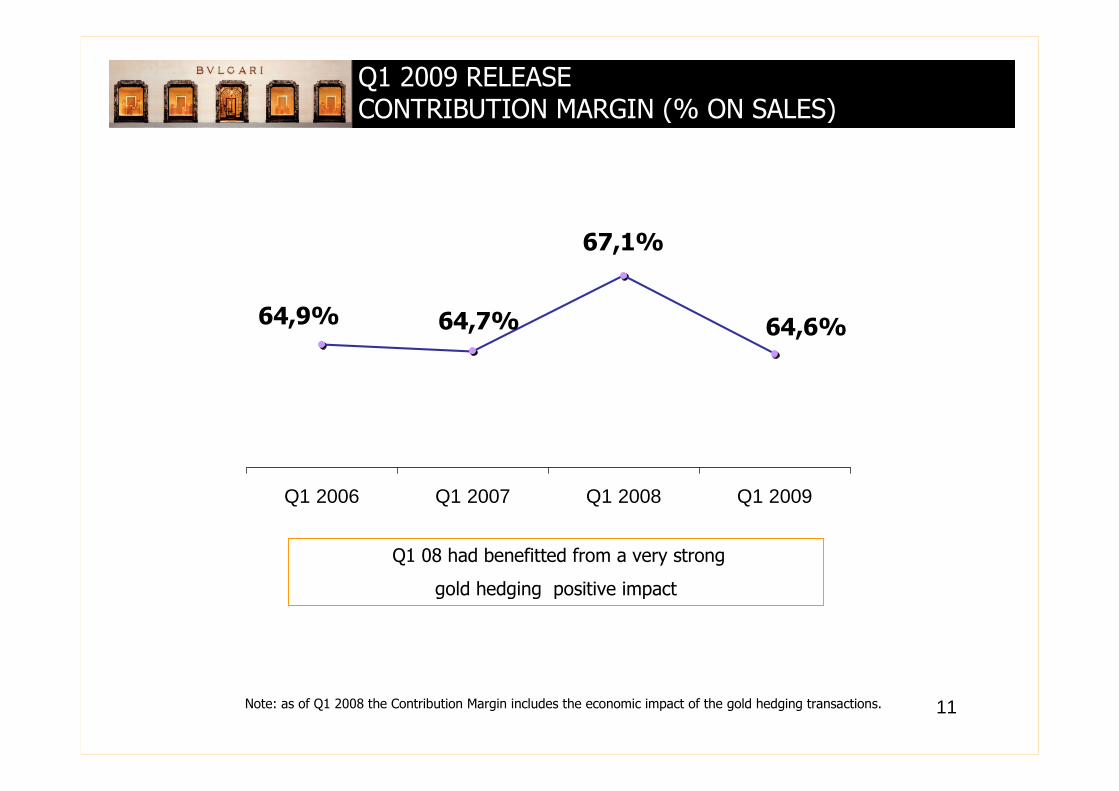

64,7%

67,1%

64,6%64,9%

Q1 2006 Q1 2007 Q1 2008 Q1 2009

Q1 2009 RELEASECONTRIBUTION MARGIN (% ON SALES)

Note: as of Q1 2008 the Contribution Margin includes the economic impact of the gold hedging transactions.

Q1 08 had benefitted from a very strong

gold hedging positive impact

12

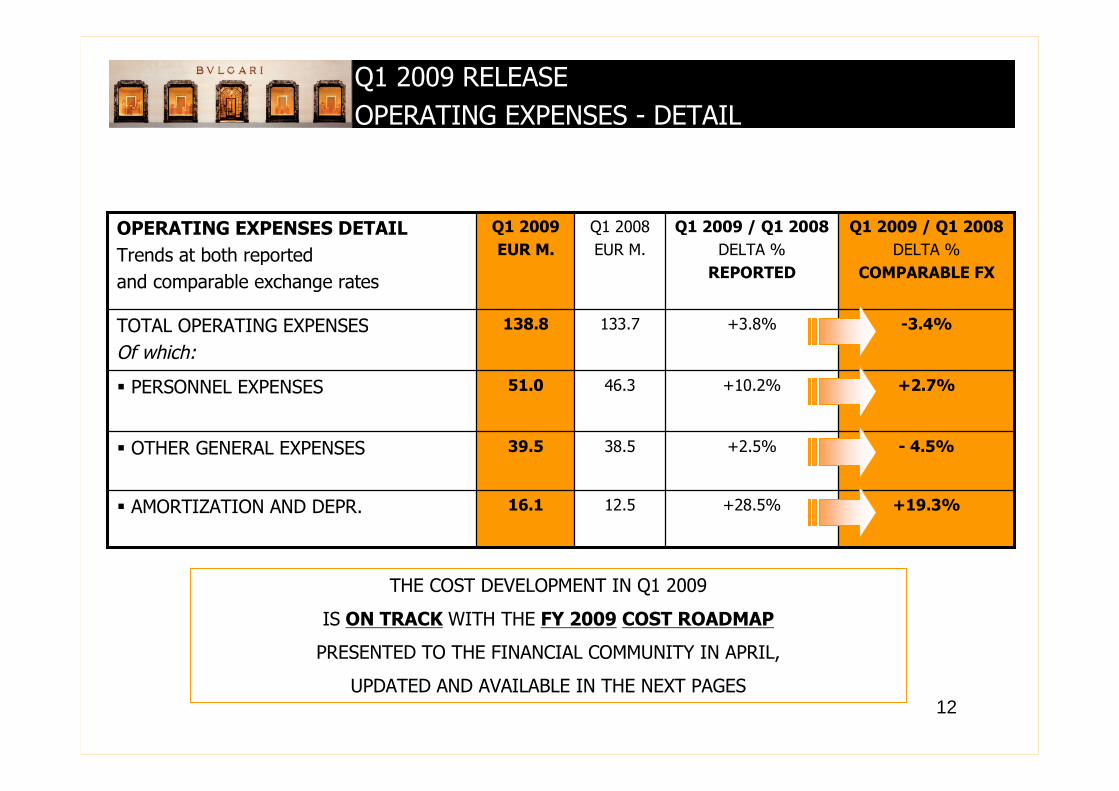

-3.4%+3.8%133.7138.8TOTAL OPERATING EXPENSES

Of which:

+28.5%

+2.5%

+10.2%

Q1 2009 / Q1 2008

DELTA %

REPORTED

- 4.5%38.539.5 OTHER GENERAL EXPENSES

+19.3%12.516.1 AMORTIZATION AND DEPR.

+2.7%46.351.0 PERSONNEL EXPENSES

Q1 2009 / Q1 2008

DELTA %

COMPARABLE FX

Q1 2008

EUR M.

Q1 2009

EUR M.

OPERATING EXPENSES DETAIL

Trends at both reported

and comparable exchange rates

Q1 2009 RELEASE

OPERATING EXPENSES - DETAIL

THE COST DEVELOPMENT IN Q1 2009

IS ON TRACK WITH THE FY 2009 COST ROADMAP

PRESENTED TO THE FINANCIAL COMMUNITY IN APRIL,

UPDATED AND AVAILABLE IN THE NEXT PAGES

13

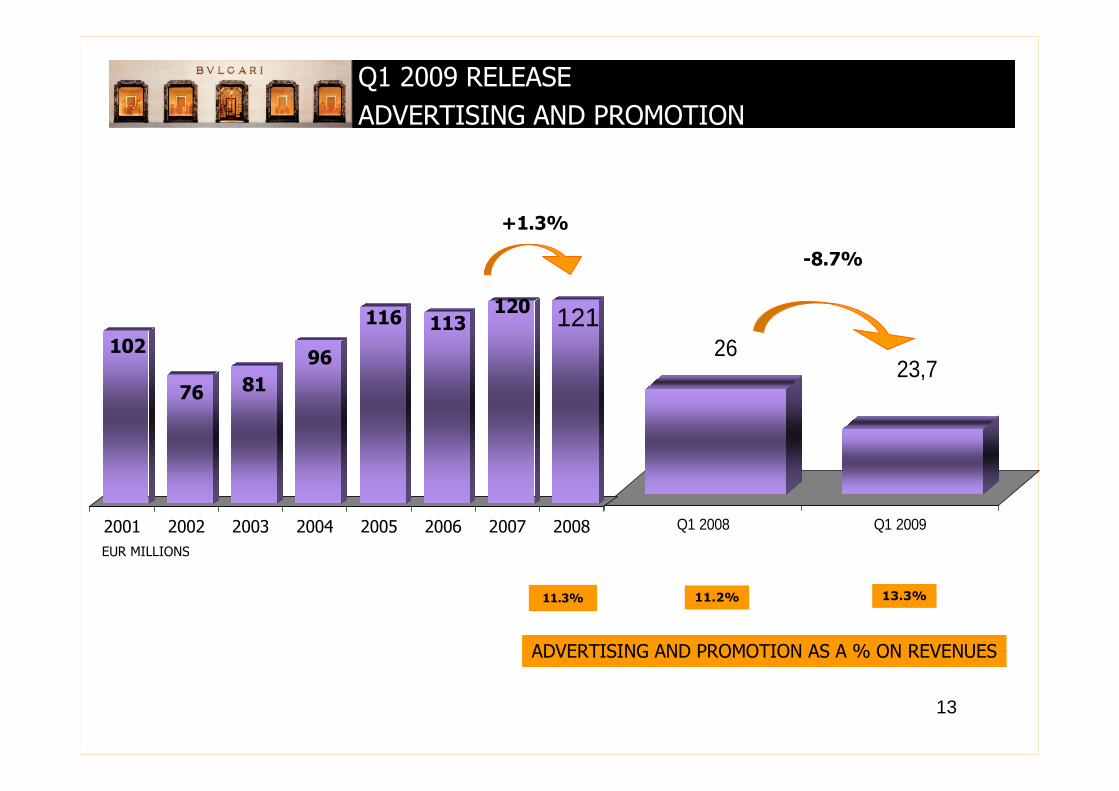

2623,7

Q1 2008 Q1 2009

11.2%

Q1 2009 RELEASE

ADVERTISING AND PROMOTION

102

76 81

96

116 113120

121

2001 2002 2003 2004 2005 2006 2007 2008

ADVERTISING AND PROMOTION AS A % ON REVENUES

+1.3%

11.3% 13.3%

-8.7%

EUR MILLIONS

14

BETWEEN ETERNITY AND HISTORY 1884-2009

125 YEARS OF ITALIAN JEWELS

PALAZZO DELLE ESPOSIZIONI EXHIBITION, 22 May 2009 – 13 Sept 2009

15

BETWEEN ETERNITY AND HISTORY 1884-2009

125 YEARS OF ITALIAN JEWELS

PALAZZO DELLE ESPOSIZIONI EXHIBITION, 22 May 2009 – 13 Sept 2009

16

BETWEEN ETERNITY AND HISTORY 1884-2009

125 YEARS OF ITALIAN JEWELS

OPENING – JESSICA ALBA

17

BETWEEN ETERNITY AND HISTORY 1884-2009

125 YEARS OF ITALIAN JEWELS

SAVE THE CHILDREN – “REWRITE THE FUTURE” CAMPAIGN

18

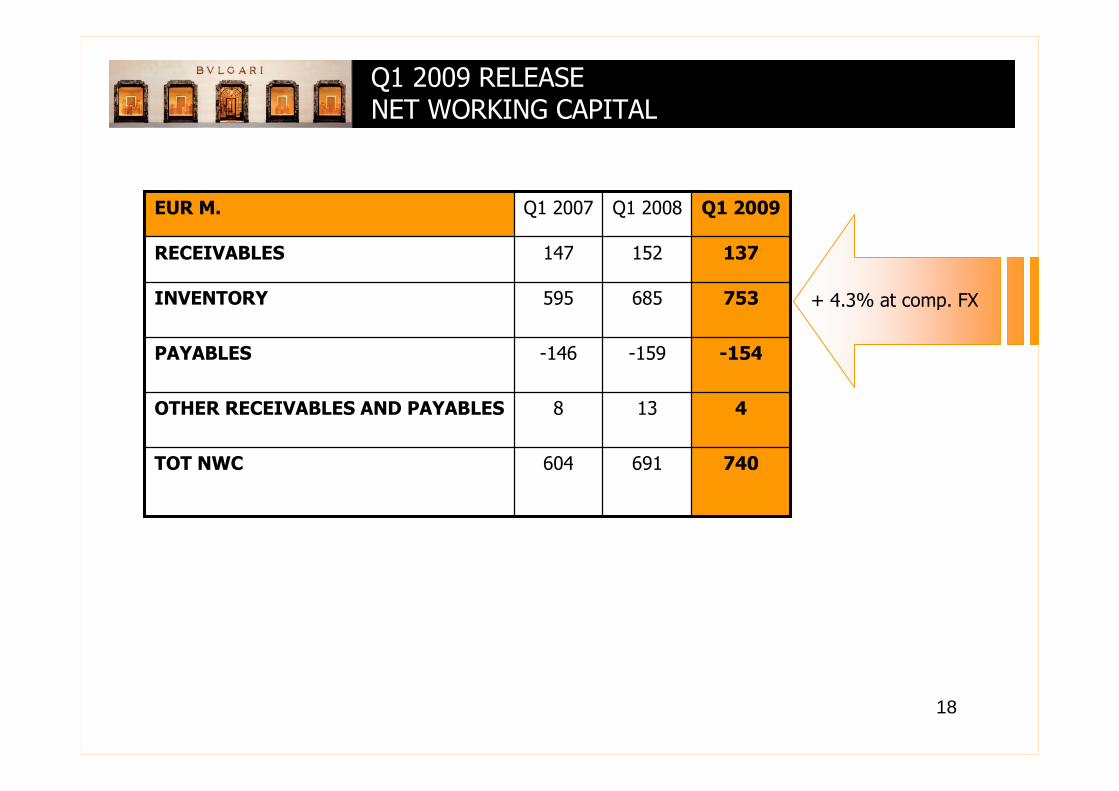

Q1 2009 RELEASENET WORKING CAPITAL

691

13

-159

685

152

Q1 2008

604

8

-146

595

147

Q1 2007

-154PAYABLES

740

4

753

137

Q1 2009

TOT NWC

OTHER RECEIVABLES AND PAYABLES

INVENTORY

RECEIVABLES

EUR M.

+ 4.3% at comp. FX

19

(184.8)

(43.9)

26.7

0.0

(19.4)

(16.0)

0.0

(1.4)

(2.0)

(86.6)

35.5

(140.9)

MARCH

2008

(80.6)

(33.7)

(9.5)

0.0

(6.5)

(12.2)

(2.8)

(0.6)

9.1

(51.3)

33.6

(46.9)

MARCH2007

(35.4)TOTAL

(338.9)NET INDEBTEDNESS AT 31.03.2009

(6.8)OTHER

0.0DIVIDENDS

(16.7)CASH FLOW from P&L

5.8CHANGE in WORKING CAPITAL

(17.8)

(13.2)

(5.4)

0.3

0.5

CASH FLOW from INVESTING ACTIVITY

• CAPITAL EXPENDITURE*

• ACQUISITION OF COMPANIES

• GUARANTEE DEPOSIT

• OTHER

(303.6)

MARCH

2009

NET INDEBTEDNESS AT 01.01.2009

EUR M.

Q1 2009 RELEASECASH FLOW DETAILS

* Both March 08 and March 09 include the Museum, 2008 figures were restated

20

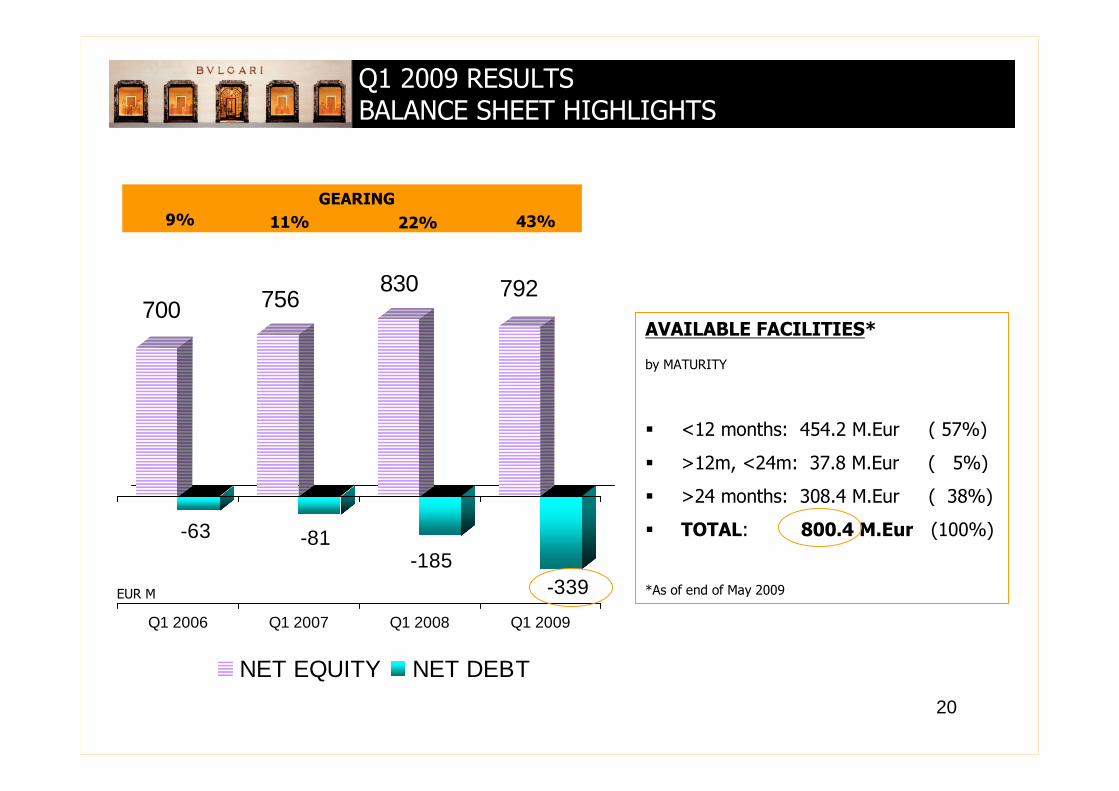

700

-63

756

-81

830

-185

792

-339

Q1 2006 Q1 2007 Q1 2008 Q1 2009

NET EQUITY NET DEBT

GEARING

9% 11%

Q1 2009 RESULTSBALANCE SHEET HIGHLIGHTS

22% 43%

AVAILABLE FACILITIES*

by MATURITY

<12 months: 454.2 M.Eur ( 57%)

>12m, <24m: 37.8 M.Eur ( 5%)

>24 months: 308.4 M.Eur ( 38%)

TOTAL: 800.4 M.Eur (100%)

*As of end of May 2009EUR M

21

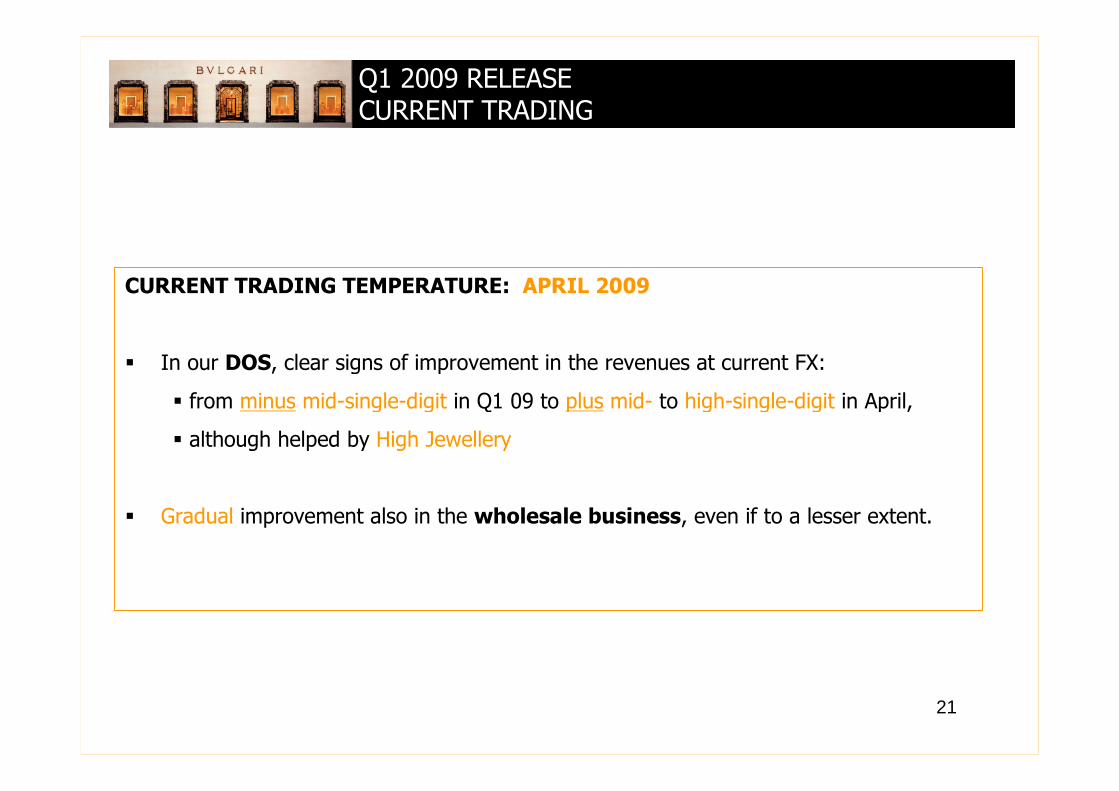

Q1 2009 RELEASECURRENT TRADING

CURRENT TRADING TEMPERATURE: APRIL 2009

In our DOS, clear signs of improvement in the revenues at current FX:

from minus mid-single-digit in Q1 09 to plus mid- to high-single-digit in April,

although helped by High Jewellery

Gradual improvement also in the wholesale business, even if to a lesser extent.

22

COSTS ROADMAP FOR 2009

AND

SELL-SIDE ANALYSTS’ FY2009 CONSENSUS*

*calculated on 25 broker estimates received from May 13 to May 25 2009

23

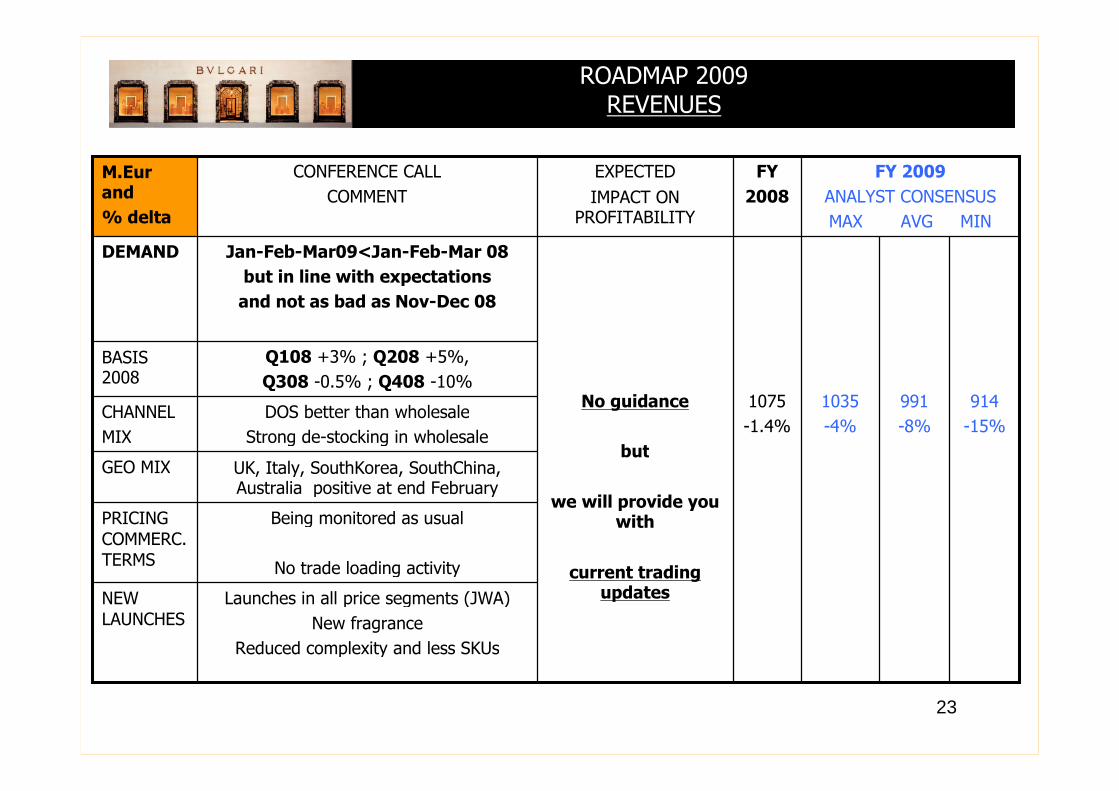

ROADMAP 2009REVENUES

991

-8%

1035

-4%

1075

-1.4%

FY

2008

Launches in all price segments (JWA)

New fragrance

Reduced complexity and less SKUs

Being monitored as usual

No trade loading activity

UK, Italy, SouthKorea, SouthChina,Australia positive at end February

DOS better than wholesale

Strong de-stocking in wholesale

Q108 +3% ; Q208 +5%,

Q308 -0.5% ; Q408 -10%

Jan-Feb-Mar09<Jan-Feb-Mar 08

but in line with expectations

and not as bad as Nov-Dec 08

CONFERENCE CALL

COMMENT

No guidance

but

we will provide youwith

current tradingupdates

EXPECTED

IMPACT ONPROFITABILITY

914

-15%

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

NEWLAUNCHES

BASIS2008

CHANNEL

MIX

GEO MIX

PRICINGCOMMERC.TERMS

DEMAND

M.Eurand

% delta

24

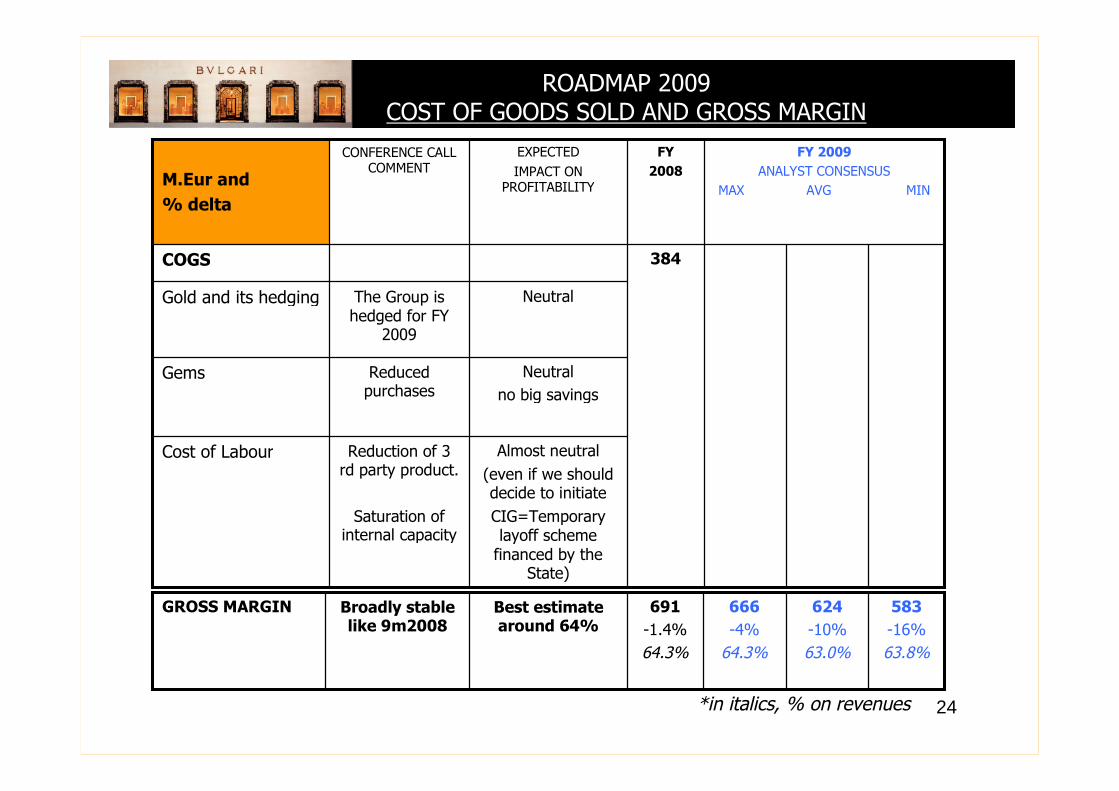

ROADMAP 2009COST OF GOODS SOLD AND GROSS MARGIN

NeutralThe Group ishedged for FY

2009

Gold and its hedging

384

FY

2008

Reduction of 3rd party product.

Saturation ofinternal capacity

Reducedpurchases

CONFERENCE CALLCOMMENT

Almost neutral

(even if we shoulddecide to initiate

CIG=Temporarylayoff scheme

financed by theState)

Neutral

no big savings

EXPECTED

IMPACT ONPROFITABILITY

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

Gems

Cost of Labour

COGS

M.Eur and

% delta

624

-10%

63.0%

666

-4%

64.3%

691

-1.4%

64.3%

Broadly stablelike 9m2008

Best estimatearound 64%

583

-16%

63.8%

GROSS MARGIN

*in italics, % on revenues

25

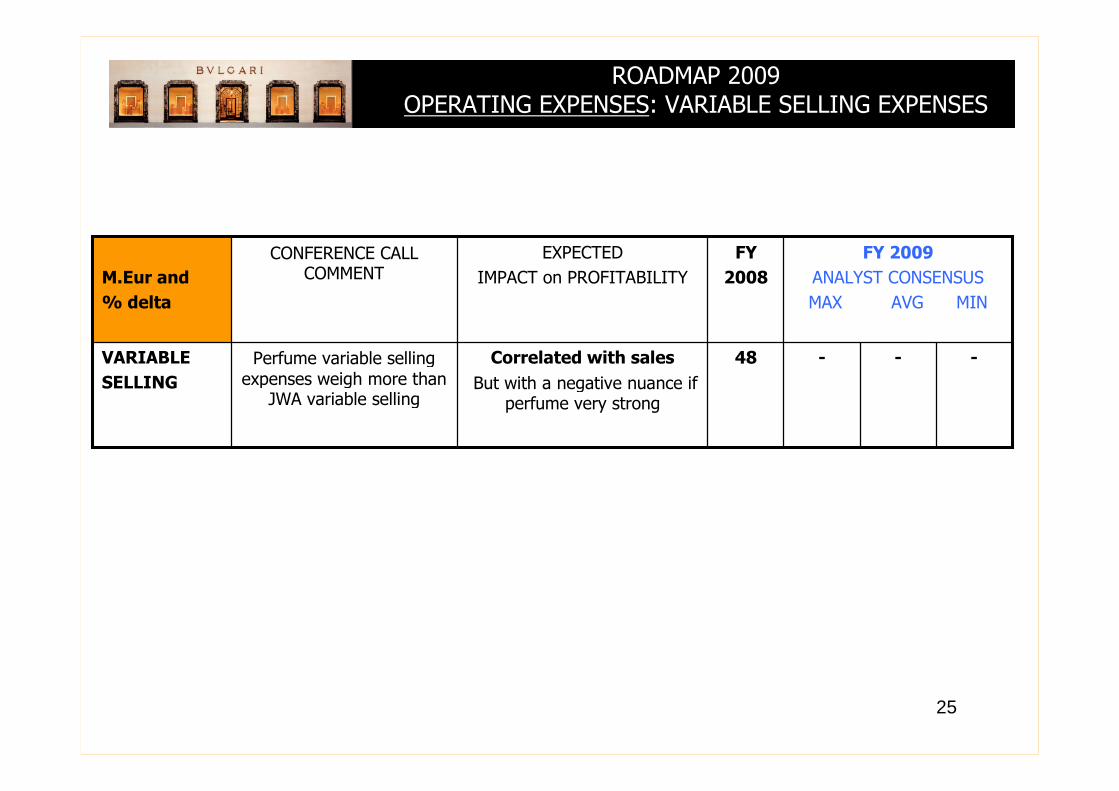

ROADMAP 2009OPERATING EXPENSES: VARIABLE SELLING EXPENSES

---48Correlated with sales

But with a negative nuance ifperfume very strong

VARIABLE

SELLING

Perfume variable sellingexpenses weigh more than

JWA variable selling

CONFERENCE CALLCOMMENT

FY

2008

EXPECTED

IMPACT on PROFITABILITY

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

M.Eur and

% delta

26

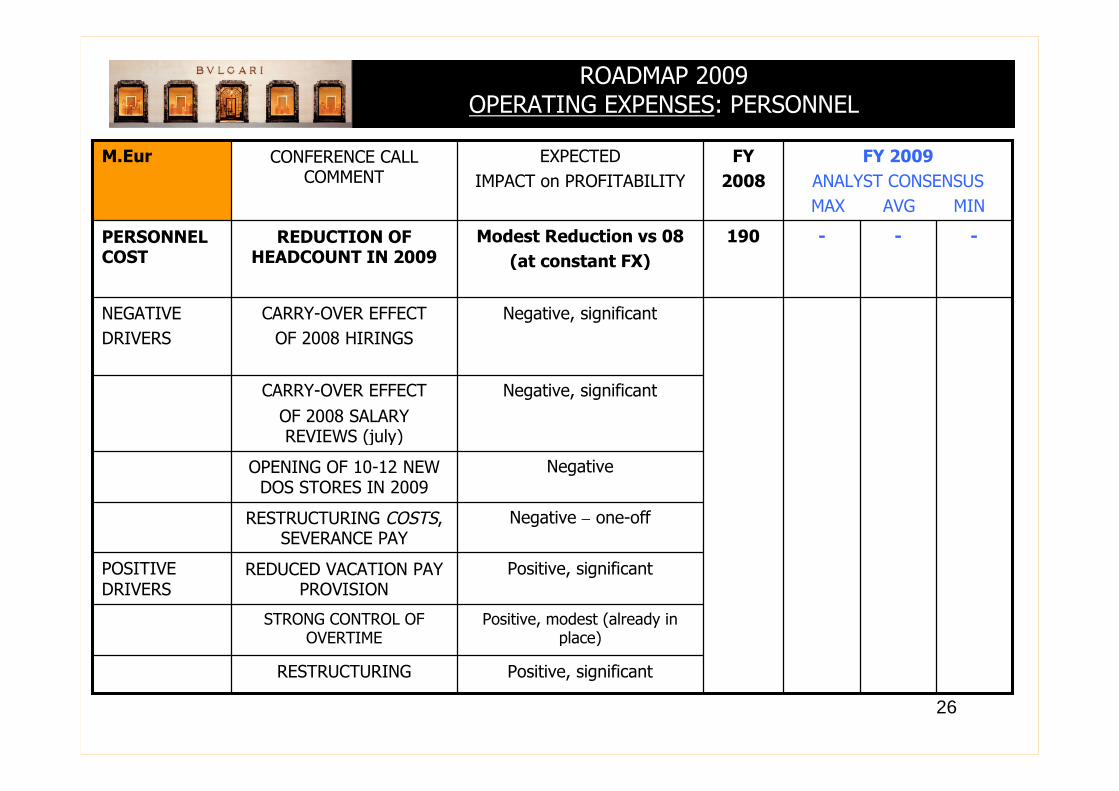

ROADMAP 2009OPERATING EXPENSES: PERSONNEL

---190Modest Reduction vs 08

(at constant FX)

REDUCTION OFHEADCOUNT IN 2009

PERSONNELCOST

RESTRUCTURING

STRONG CONTROL OFOVERTIME

REDUCED VACATION PAYPROVISION

RESTRUCTURING COSTS,SEVERANCE PAY

OPENING OF 10-12 NEWDOS STORES IN 2009

CARRY-OVER EFFECT

OF 2008 SALARYREVIEWS (july)

CARRY-OVER EFFECT

OF 2008 HIRINGS

CONFERENCE CALLCOMMENT

FY

2008

Positive, significant

Positive, modest (already inplace)

Positive, significant

Negative – one-off

Negative

Negative, significant

Negative, significant

EXPECTED

IMPACT on PROFITABILITY

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

POSITIVEDRIVERS

NEGATIVE

DRIVERS

M.Eur

27

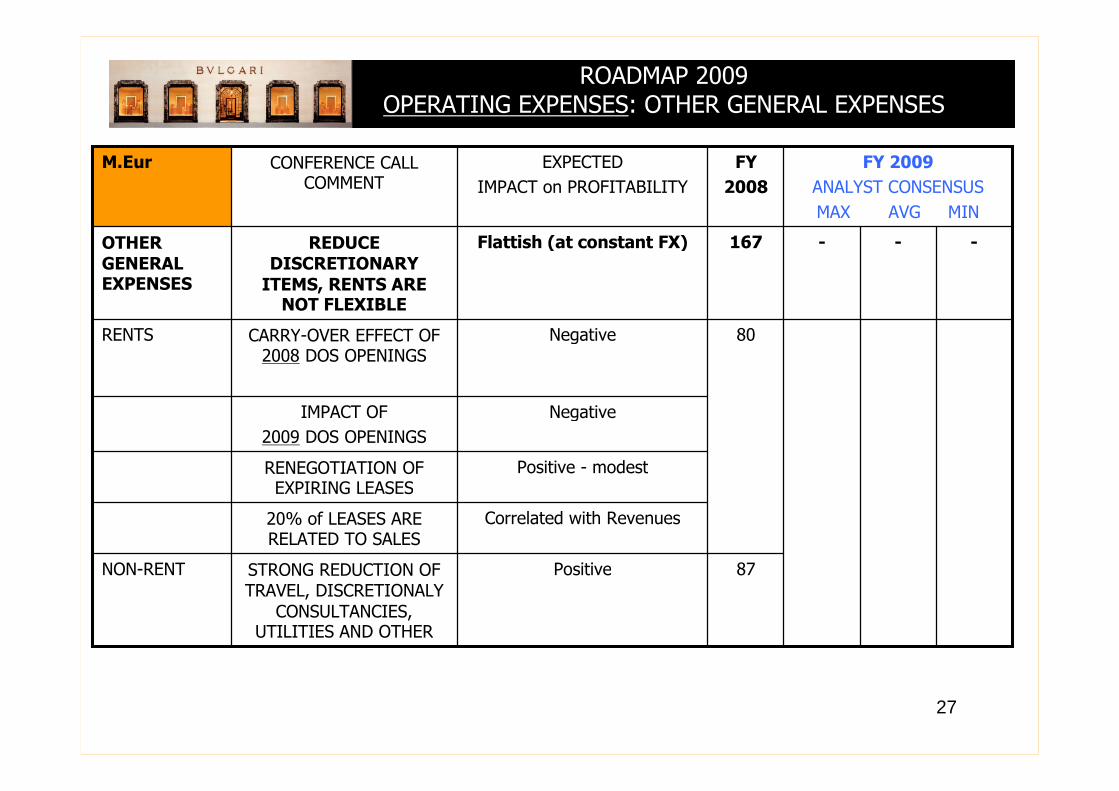

ROADMAP 2009OPERATING EXPENSES: OTHER GENERAL EXPENSES

87

---167Flattish (at constant FX)REDUCEDISCRETIONARY

ITEMS, RENTS ARENOT FLEXIBLE

OTHERGENERALEXPENSES

STRONG REDUCTION OFTRAVEL, DISCRETIONALY

CONSULTANCIES,UTILITIES AND OTHER

20% of LEASES ARERELATED TO SALES

RENEGOTIATION OFEXPIRING LEASES

IMPACT OF

2009 DOS OPENINGS

CARRY-OVER EFFECT OF2008 DOS OPENINGS

CONFERENCE CALLCOMMENT

80

FY

2008

Positive

Correlated with Revenues

Positive - modest

Negative

Negative

EXPECTED

IMPACT on PROFITABILITY

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

NON-RENT

RENTS

M.Eur

28

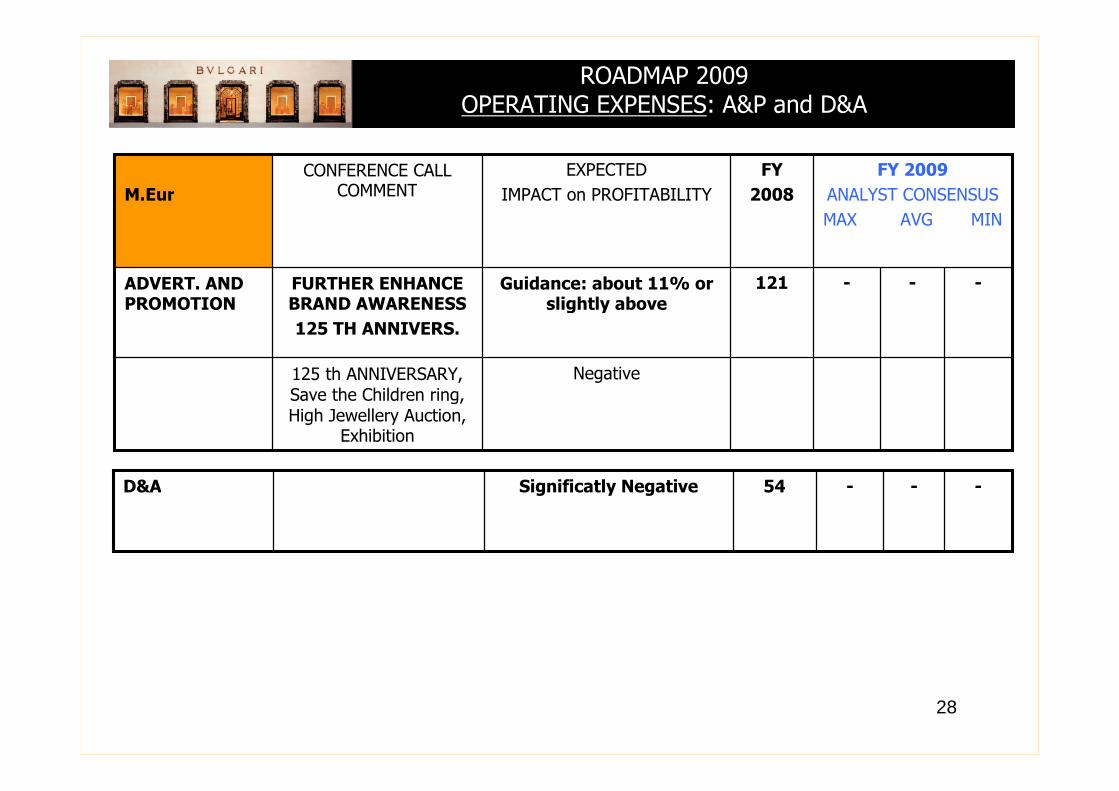

ROADMAP 2009OPERATING EXPENSES: A&P and D&A

---121Guidance: about 11% orslightly above

FURTHER ENHANCEBRAND AWARENESS

125 TH ANNIVERS.

ADVERT. ANDPROMOTION

125 th ANNIVERSARY,Save the Children ring,High Jewellery Auction,

Exhibition

CONFERENCE CALLCOMMENT

FY

2008

Negative

EXPECTED

IMPACT on PROFITABILITY

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

M.Eur

---54Significatly NegativeD&A

29

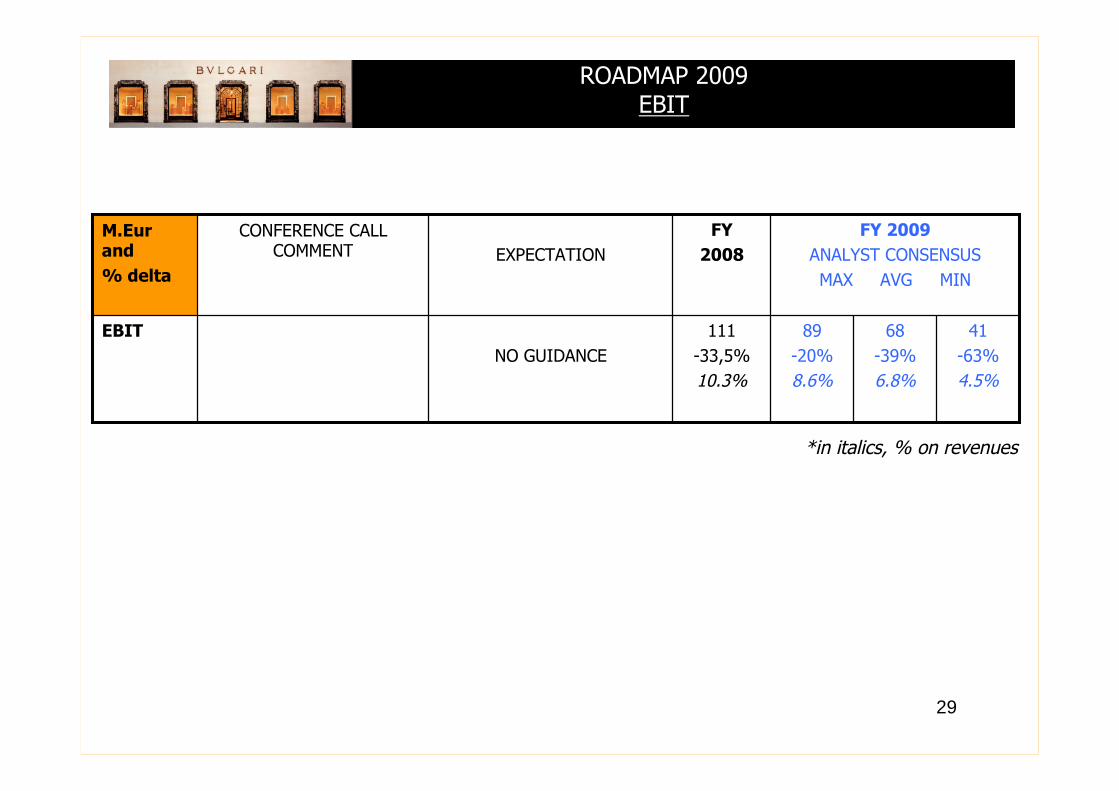

ROADMAP 2009EBIT

68

-39%

6.8%

89

-20%

8.6%

111

-33,5%

10.3%

FY

2008

CONFERENCE CALLCOMMENT

NO GUIDANCE

EXPECTATION

41

-63%

4.5%

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

EBIT

M.Eurand

% delta

*in italics, % on revenues

30

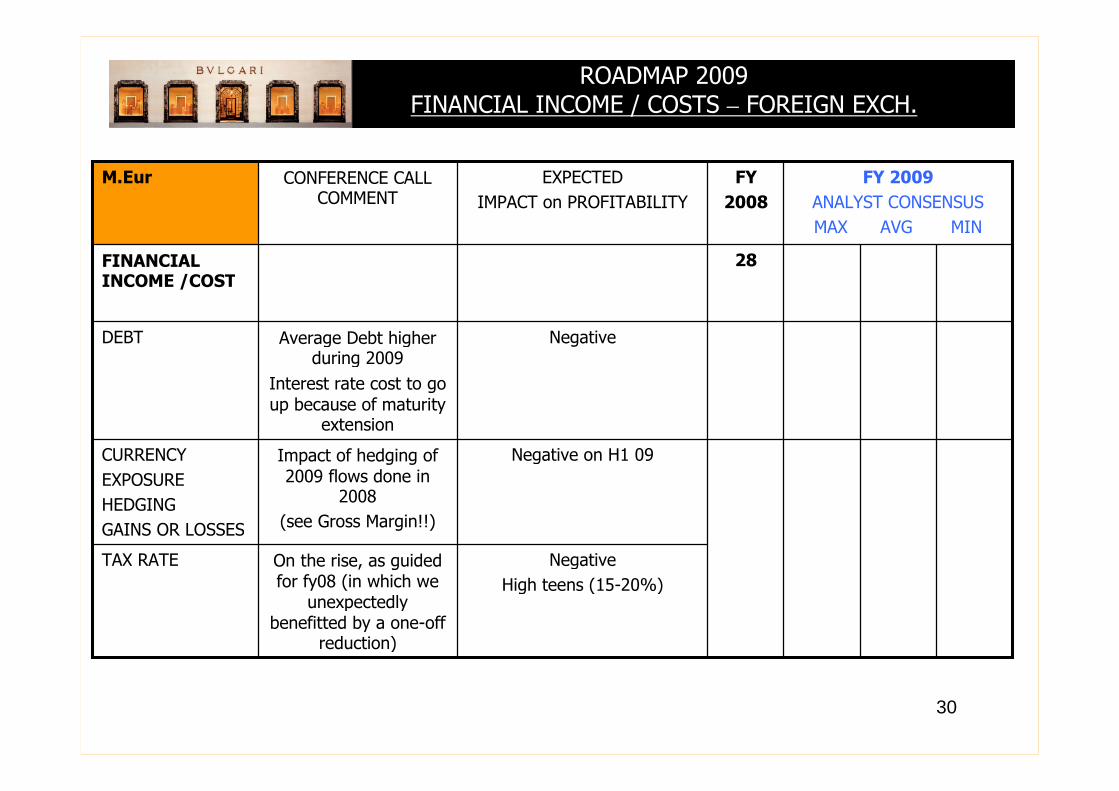

ROADMAP 2009FINANCIAL INCOME / COSTS – FOREIGN EXCH.

28FINANCIALINCOME /COST

NegativeAverage Debt higherduring 2009

Interest rate cost to goup because of maturity

extension

DEBT

On the rise, as guidedfor fy08 (in which we

unexpectedlybenefitted by a one-off

reduction)

Impact of hedging of2009 flows done in

2008

(see Gross Margin!!)

CONFERENCE CALLCOMMENT

FY

2008

Negative

High teens (15-20%)

Negative on H1 09

EXPECTED

IMPACT on PROFITABILITY

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

TAX RATE

CURRENCY

EXPOSURE

HEDGING

GAINS OR LOSSES

M.Eur

31

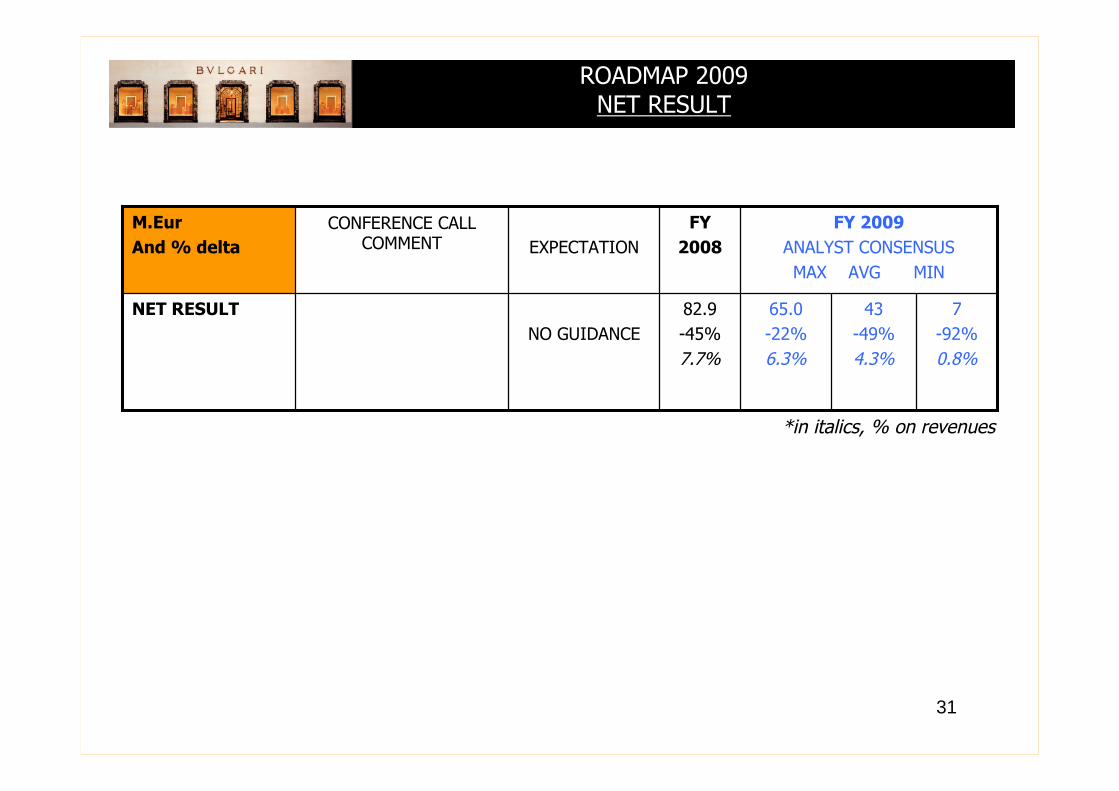

ROADMAP 2009NET RESULT

43

-49%

4.3%

65.0

-22%

6.3%

82.9

-45%

7.7%

FY

2008

CONFERENCE CALLCOMMENT

NO GUIDANCE

EXPECTATION

7

-92%

0.8%

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

NET RESULT

M.Eur

And % delta

*in italics, % on revenues

32

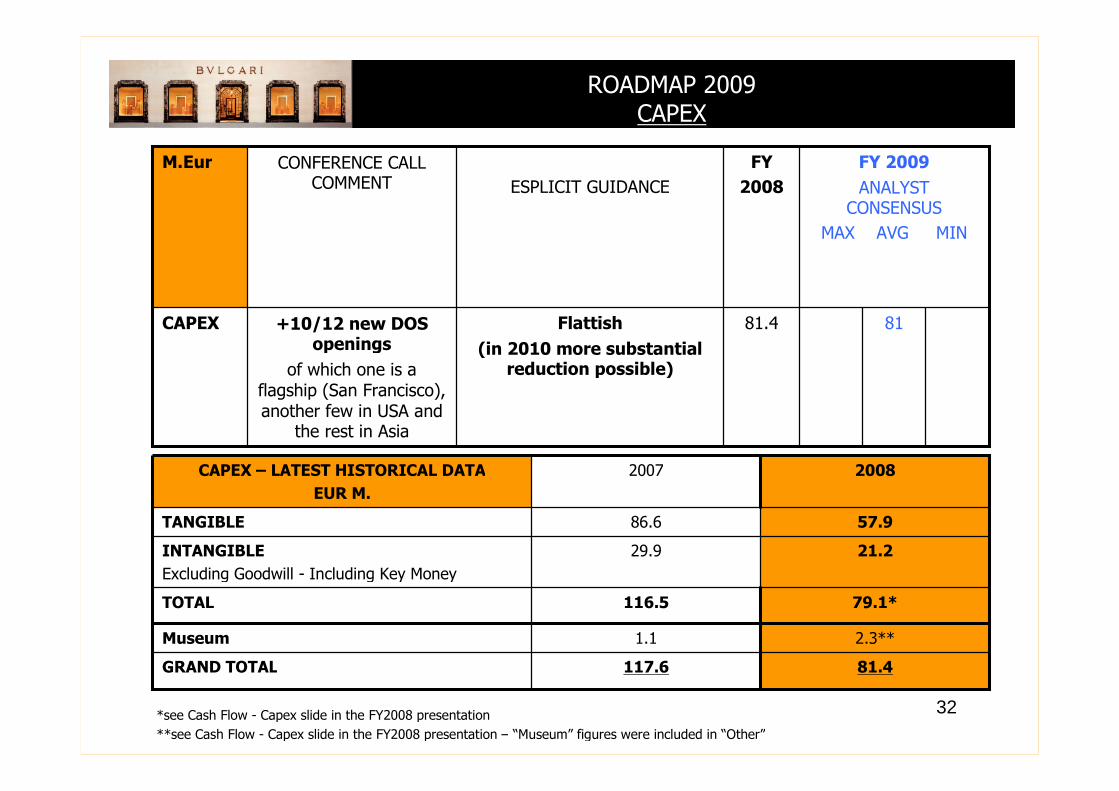

ROADMAP 2009CAPEX

8181.4

FY

2008

+10/12 new DOSopenings

of which one is aflagship (San Francisco),another few in USA and

the rest in Asia

CONFERENCE CALLCOMMENT

Flattish

(in 2010 more substantialreduction possible)

ESPLICIT GUIDANCE

FY 2009

ANALYSTCONSENSUS

MAX AVG MIN

CAPEX

M.Eur

2.3**1.1Museum

79.1*116.5TOTAL

117.6

29.9

86.6

2007

81.4

21.2

57.9

2008

INTANGIBLE

Excluding Goodwill - Including Key Money

GRAND TOTAL

TANGIBLE

CAPEX – LATEST HISTORICAL DATA

EUR M.

*see Cash Flow - Capex slide in the FY2008 presentation

**see Cash Flow - Capex slide in the FY2008 presentation – “Museum” figures were included in “Other”

33

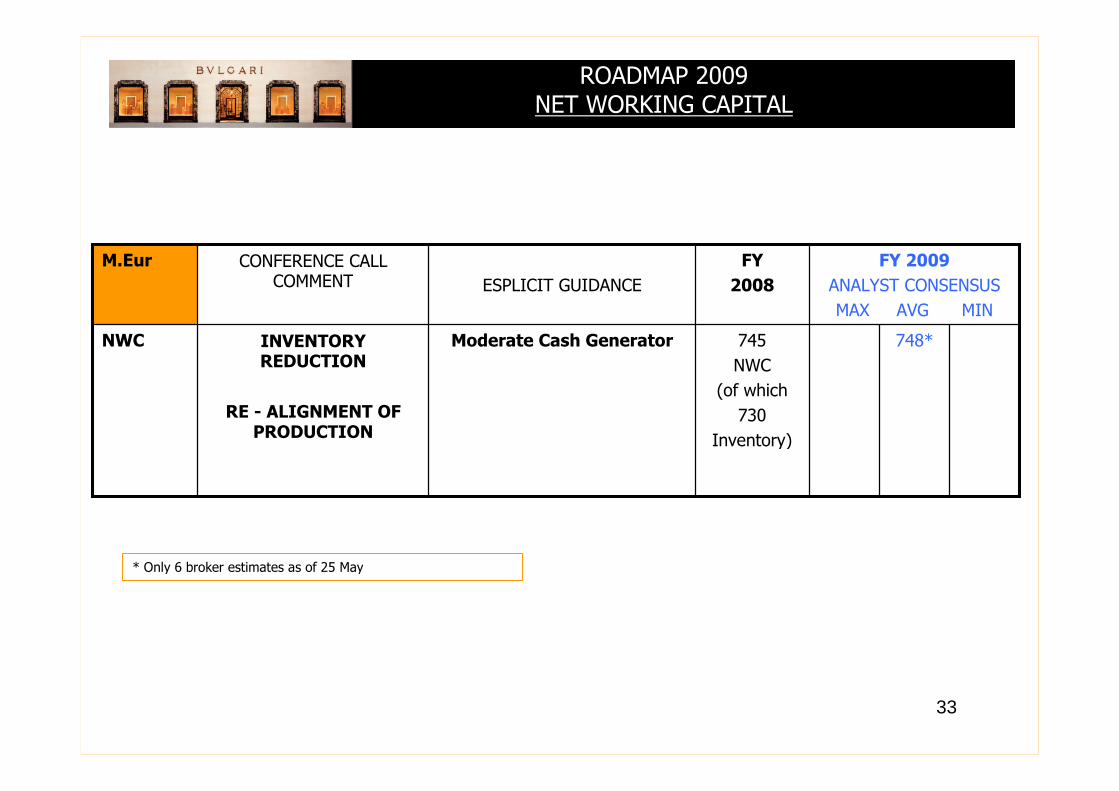

ROADMAP 2009NET WORKING CAPITAL

748*745

NWC

(of which

730

Inventory)

FY

2008

INVENTORYREDUCTION

RE - ALIGNMENT OFPRODUCTION

CONFERENCE CALLCOMMENT

Moderate Cash Generator

ESPLICIT GUIDANCE

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

NWC

M.Eur

* Only 6 broker estimates as of 25 May

34

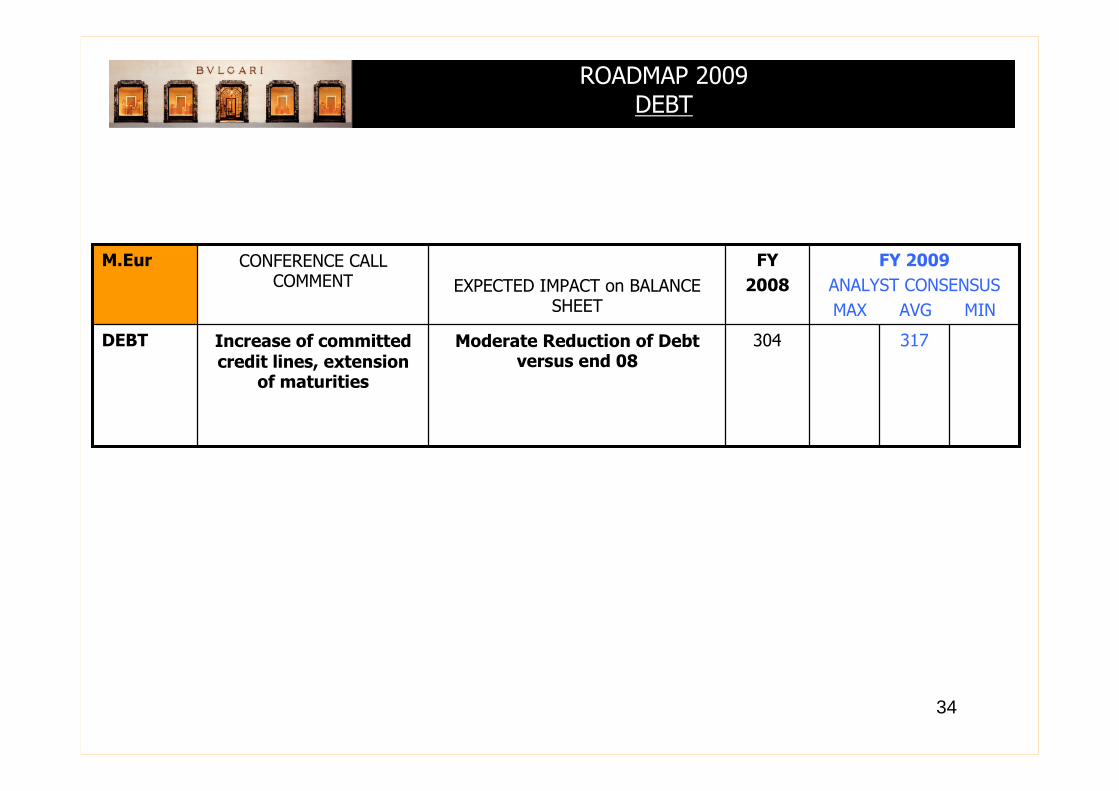

ROADMAP 2009DEBT

317304

FY

2008

Increase of committedcredit lines, extension

of maturities

CONFERENCE CALLCOMMENT

Moderate Reduction of Debtversus end 08

EXPECTED IMPACT on BALANCESHEET

FY 2009

ANALYST CONSENSUS

MAX AVG MIN

DEBT

M.Eur

35

ENDEND

QUESTION & ANSWERS

36

BVLGARI NEWSFLOWBVLGARI NEWSFLOW

BULGARI INVESTOR RELATIONS WEBSITES:http://ir.bulgari.com

http://ir.mobi.bulgari.com

BULGARI CORPORATE WEBSITEhttp://www.bulgari.com

NEXT IR EVENTS• June 3 2009 – HSBC Luxury Goods Conference - Paris

• July 30 2009 – H1 2009 Results - Conference Call 18.00 CET

37

DISCLAIMER

This document is for institutional investors only and is not available to private customers. This document isbeing supplied to a limited number of recipients and it may not be distributed, published or reproduced in wholeor in part or disclosed by recipients to any other person.Under no circumstances shall this document constitute an offer to sell, an invitation to acquire or the solicitationof an offer to buy securities in any jurisdiction.

Each investor contemplating purchasing securities issued by Bulgari S.p.A or any of its subsidiaries should makeits own independent investigation of the financial condition and affairs, and its own appraisal of thecreditworthiness, of Bulgari S.p.A or any of its subsidiaries and should carefully consider the high risks involvedin purchasing these securities.

This document contains certain forward looking statements and key financial goals which reflect management’scurrent views, estimates, and objectives. The forward looking statements and key financial goals involve certainrisks and uncertainties that could cause actual results to differ materially from those contained in the forwardlooking statements and key financial goals.

Potential risks and uncertainties include, amongst other things, internal, industry and external factors, such asgeneral economic conditions

38

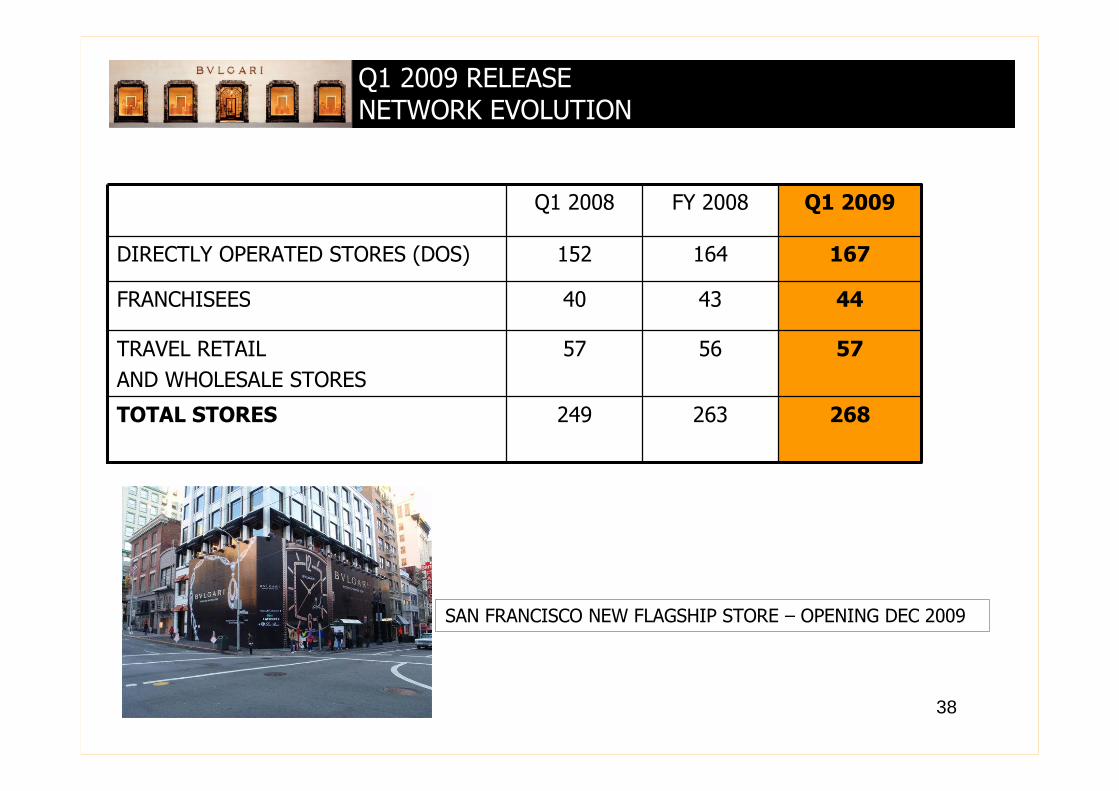

263

56

43

164

FY 2008

249

57

40

152

Q1 2008

268

57

44

167

Q1 2009

TRAVEL RETAIL

AND WHOLESALE STORES

DIRECTLY OPERATED STORES (DOS)

FRANCHISEES

TOTAL STORES

Q1 2009 RELEASENETWORK EVOLUTION

SAN FRANCISCO NEW FLAGSHIP STORE – OPENING DEC 2009