Embed Size (px)

Citation preview

How to Save on Your Health Insurance

How Did We Get Here?

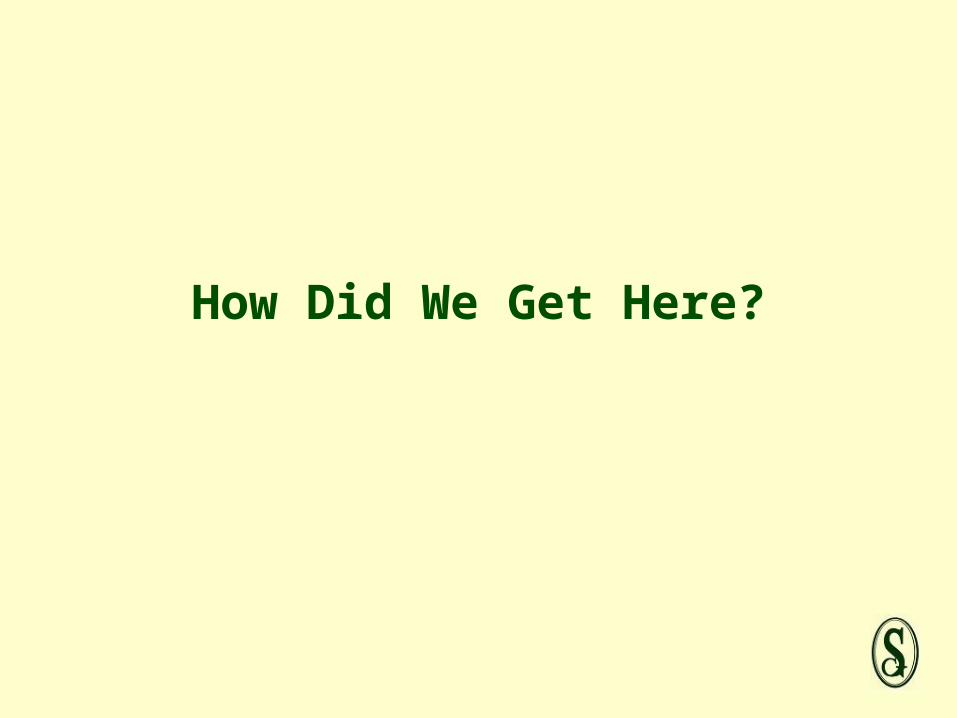

1970-1980 Indemnity Plans

• Deductibles and Co-insurance

• True Fringe Benefit

• Single Coverage $35.00

• Family Coverage $105.00

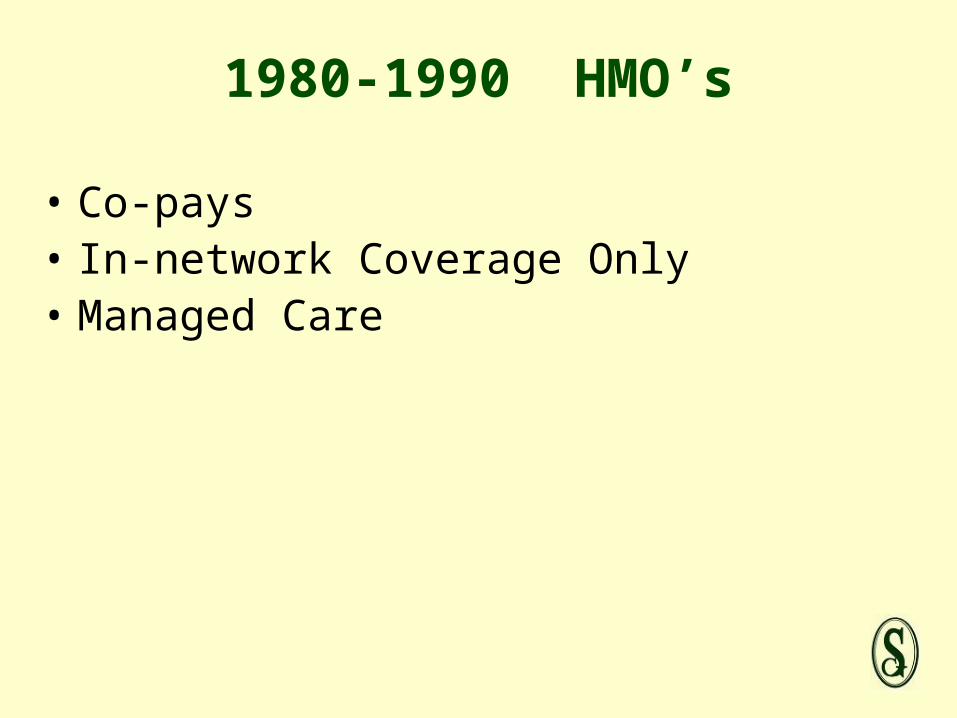

1980-1990 HMO’s

• Co-pays• In-network Coverage Only• Managed Care

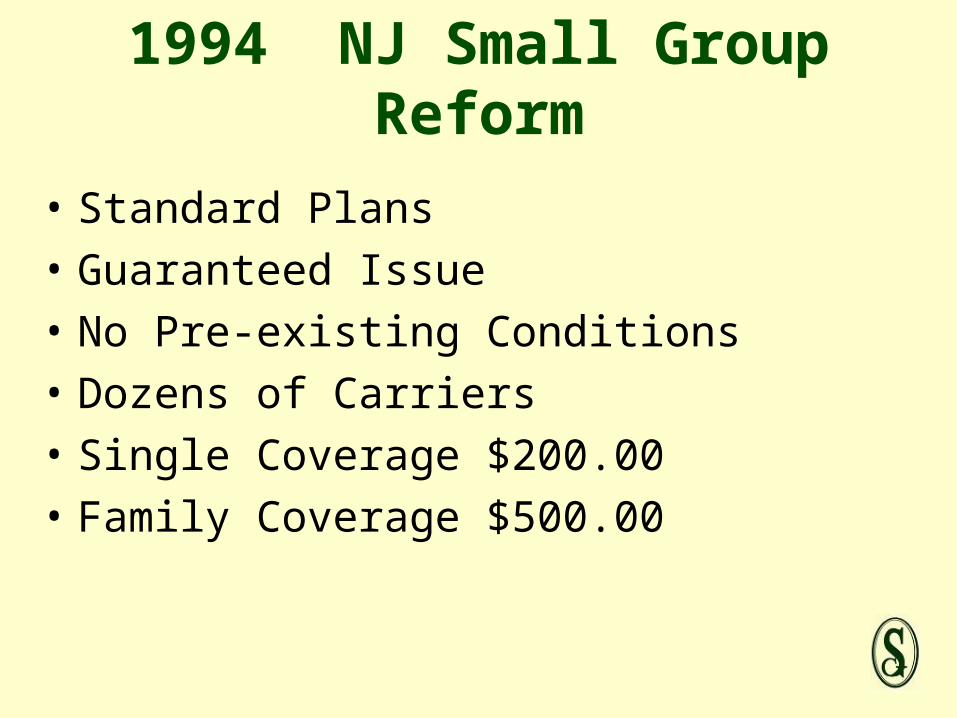

1994 NJ Small Group Reform

• Standard Plans

• Guaranteed Issue

• No Pre-existing Conditions

• Dozens of Carriers

• Single Coverage $200.00

• Family Coverage $500.00

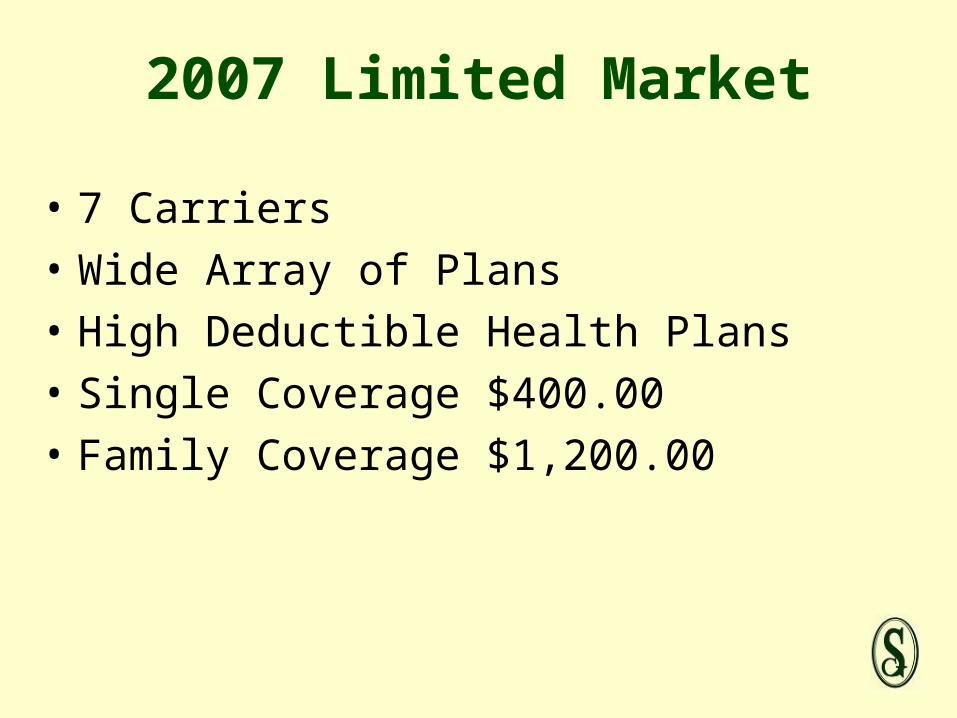

2007 Limited Market

• 7 Carriers

• Wide Array of Plans

• High Deductible Health Plans

• Single Coverage $400.00

• Family Coverage $1,200.00

Now That We Are Here, How Do We Save?

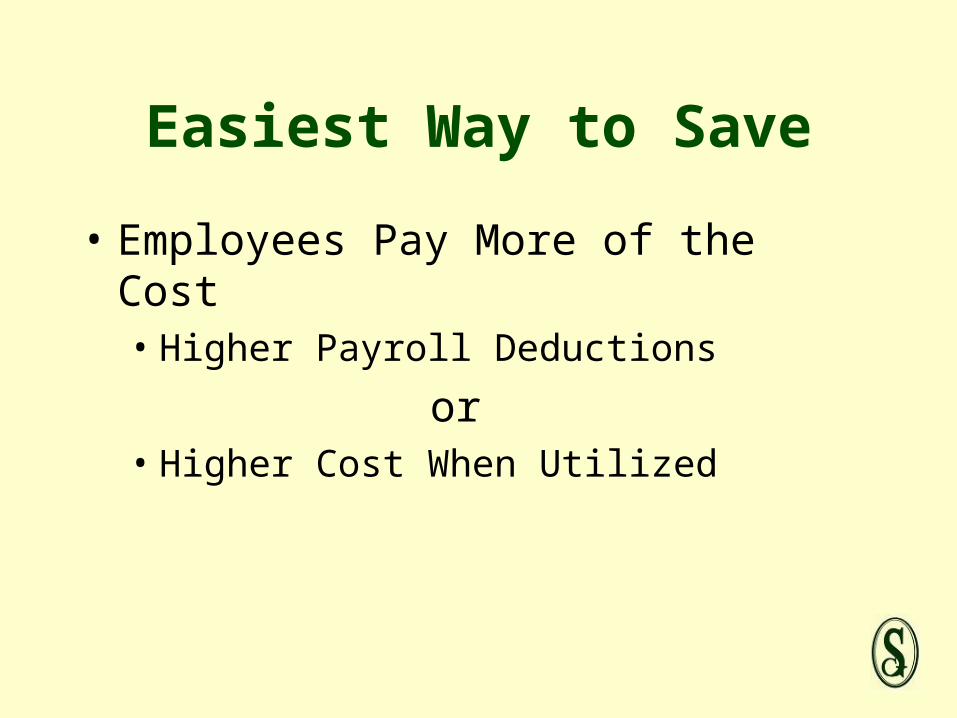

Easiest Way to Save

• Employees Pay More of the Cost• Higher Payroll Deductions

or• Higher Cost When Utilized

Raising Cost of Utilization to Lower Overall Premium

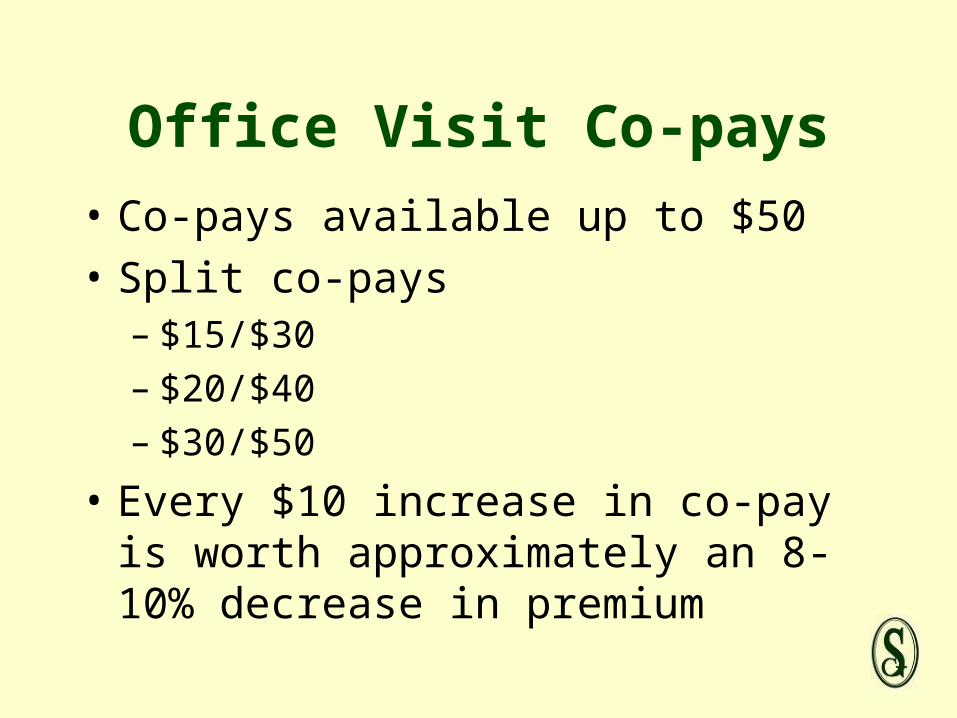

Office Visit Co-pays

• Co-pays available up to $50

• Split co-pays– $15/$30– $20/$40– $30/$50

• Every $10 increase in co-pay is worth approximately an 8-10% decrease in premium

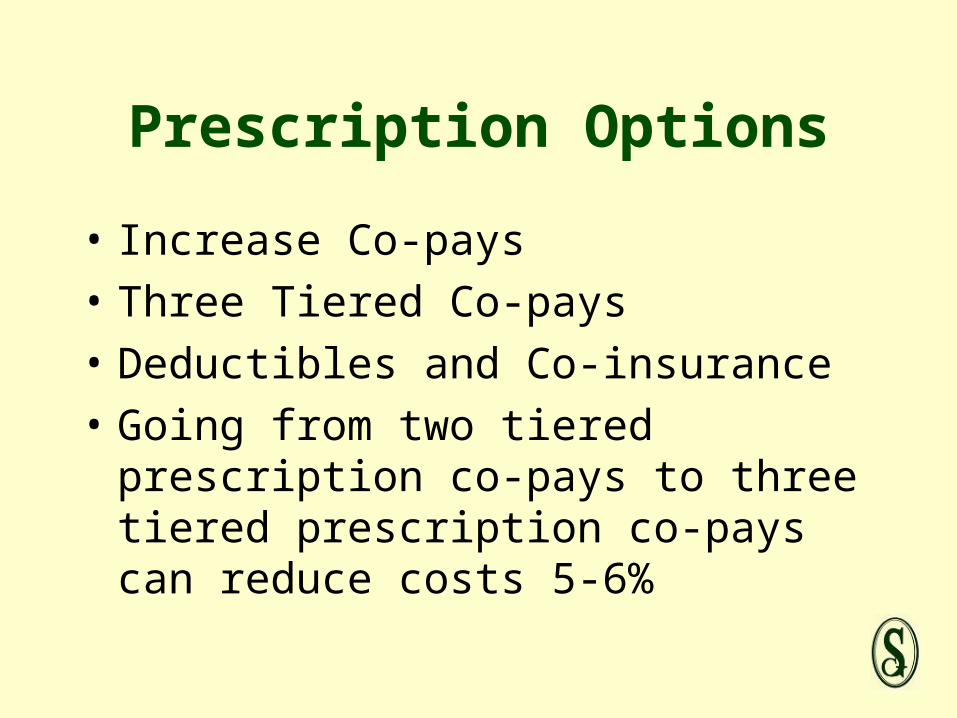

Prescription Options

• Increase Co-pays

• Three Tiered Co-pays

• Deductibles and Co-insurance

• Going from two tiered prescription co-pays to three tiered prescription co-pays can reduce costs 5-6%

Ways to Lower Costs Without Reducing Benefits

Self-Insurance and the Rule of 80/20

• Self-insurance means taking some risk away from the insurance company and putting it on the employer.

• This is done routinely on the property and casualty side through the use of higher deductibles.

• We can use the same concept with health insurance.

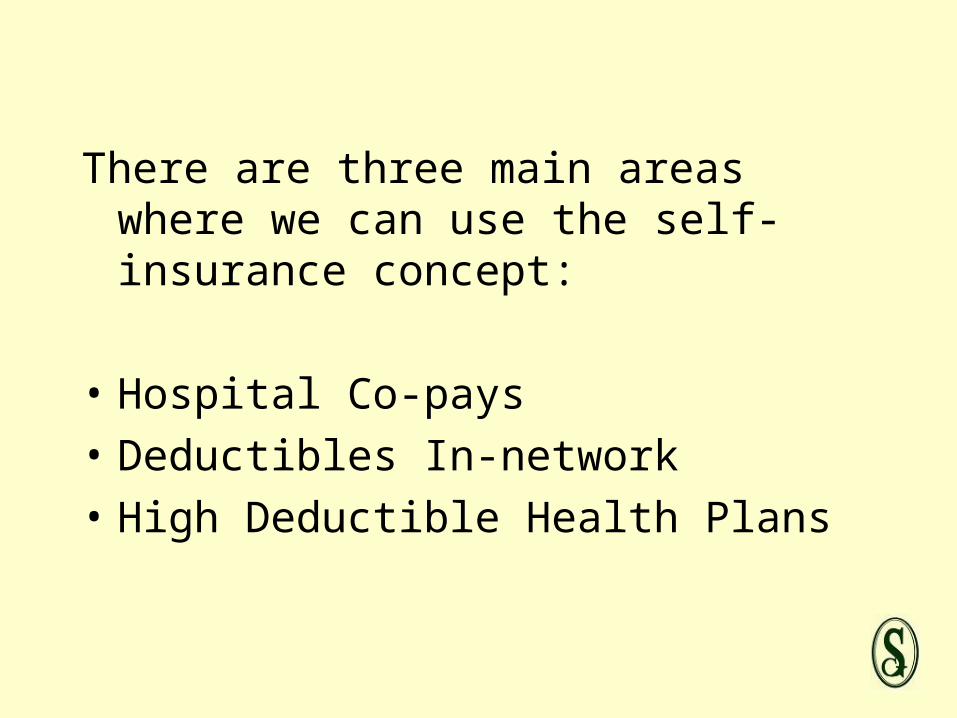

There are three main areas where we can use the self-insurance concept:

• Hospital Co-pays

• Deductibles In-network

• High Deductible Health Plans

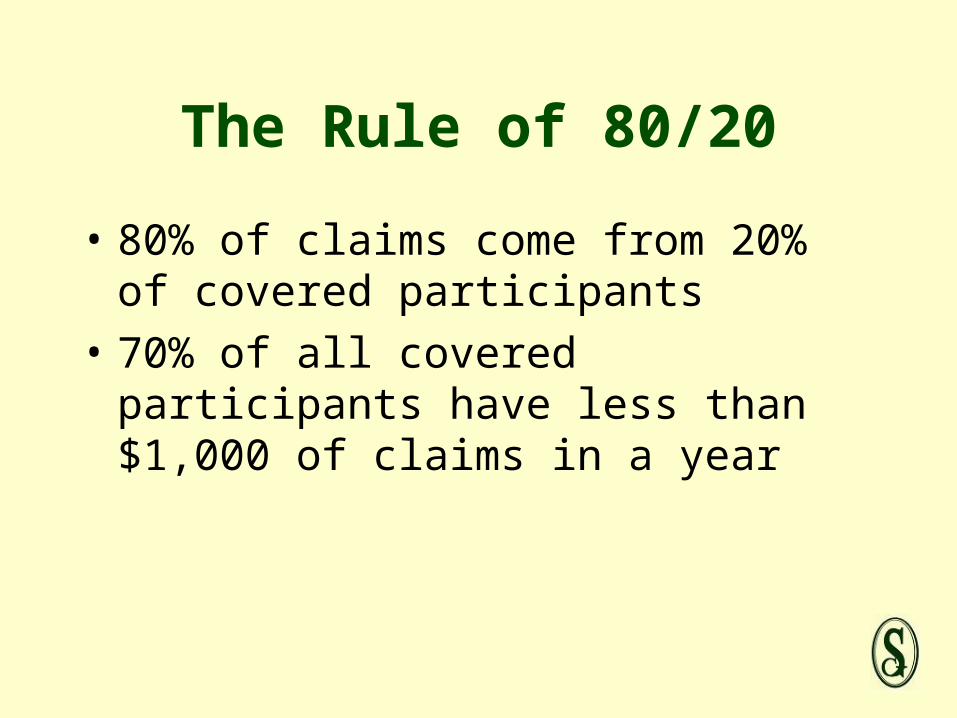

The Rule of 80/20

• 80% of claims come from 20% of covered participants

• 70% of all covered participants have less than $1,000 of claims in a year

Daily Hospital Co-pays

• Range from $125 to $750 per day or per admission

• Save premium dollars of approximately 8% and self-insure the hospital co-pay

Self Insure Hospital Co-pays

Example:Group of 15 singles and 15 familiesMonthly premium without hospital co-pay:

$30,315Monthly premium with $300 hospital co-pay:

$27,930Monthly Savings $2,385Annual Savings $28,620

Break even point 95 Hospital Days

In-Network Deductibles

• These deductibles apply only to hospital and facility charges and outpatient surgery

• Generally the deductible is from $1,000 to $2,500

Self-Insure the DeductibleExample:Group of 15 singles and 15 familiesMonthly premium without in-network deductible

$30,315Monthly premium with $1,500 in-network

deductible $17,775Monthly Savings $12,540Annual Savings $150,480

Maximum exposure of deductibles $67,500Net minimum savings to employer $82,980

High Deductible Health Plans

• These plans must have a minimum deductible of $1,100 per single and $2,200 per family.

• More common deductibles are $1,500 or $2,500 per single and $3,000 or $5,000 per family.

• All expenses, except preventive care, are subject to the deductible.

• These plans are eligible to be paired with Health Savings Accounts (HSA).

High Deductible Health Plans and Health Reimbursement Accounts

• Instead of contributing to a HSA for each employee, which becomes the employee’s money, self-insure the deductible through use of an employer funded Health Reimbursement Account (HRA).

• The HRA is only funded to the extent the deductibles are used. The employer pays as the expenses are incurred. As a result, the employer’s liability is reduced.

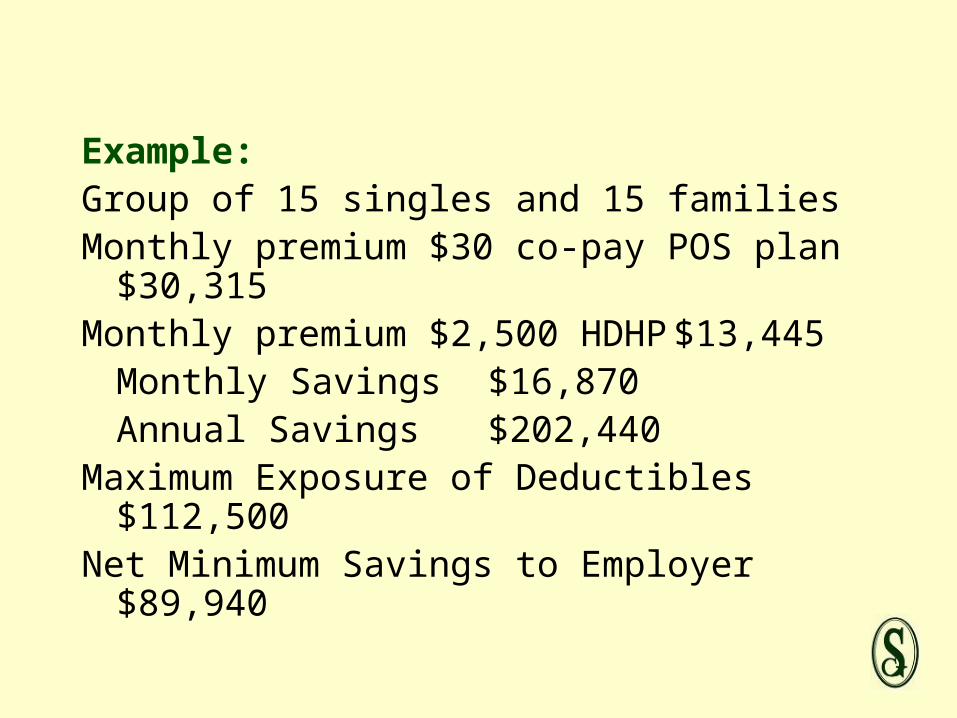

Example:Group of 15 singles and 15 familiesMonthly premium $30 co-pay POS plan

$30,315Monthly premium $2,500 HDHP

$13,445Monthly Savings $16,870Annual Savings $202,440

Maximum Exposure of Deductibles $112,500Net Minimum Savings to Employer $89,940

Samuel L. StettlerPO Box 937

Flemington, NJ 08822

908-806-3001 - phone908-806-3113 – fax

www.thestettlergroup.com