Embed Size (px)

Citation preview

How Long Can the Party Last For the New

Hampshire Economy?

Exeter Area Chamber of Commerce

January 10, 2017

Brian Gottlob

PolEcon Research

Yr.-Over-Yr. Private Sector Job Growth

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2012 2013 2014 2015 2016 2017

�H MA U.S.

After Lagging for Much of the Recovery, Private Sector Job Growth

in NH Has Accelerated Over the Past 2 Years

3 Mos. Moving Average

NH Once Again Leads New England in Private Sector Job Growth

and is Near the Top Among all States

�ovember 2015 to August 2016 Private Sector Job Growth

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

Wyom

ing

North D

akota

Alask

a

Oklahom

aK

ansa

s

Mississ

ippi

Ver

mont

New

Mex

ico

Louisiana

Connec

ticu

tW

est V

irgin

ia

Maine

New

Jer

sey

Illinois

Ohio

Pen

nsy

lvan

iaA

labam

a

Ark

ansa

sIo

wa

Wisco

nsin

Mar

yland

Virgin

iaN

ebra

ska

Ken

tuck

yRhode Island

Min

nes

ota

New

York

Indiana

Arizo

na

Montana

District of Colu

mbia

Delaw

are

Tex

asM

assa

chuse

tts

Michig

anN

orth C

arolina

Ten

nes

see

Californ

ia

Colo

rado

Misso

uri

Haw

aii

Geo

rgia

South

Dak

ota

South

Car

olina

Idah

oN

ew H

ampsh

ire

Nev

ada

Ore

gon

Was

hin

gto

nFlo

rida

Utah

�H

MA

VT

ME

CT

RI

14

16

18

20

22

24

26

28

30

32

09 10 11 12 13 14 15 16 17

-7.0%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

Help Wanted Ads in �H (000s)

Year-Over-Year Private Sector JobGrowth in �H (%)

Help Wanted Ads Have Declined During the Same Time – More and

Faster Hiring Reduced Repeat Ads?

3 Mos. Moving Average

Annual Rate of Labor Force Growth

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

�H Labor Force Growth

U.S. Labor Force Growth

After Years of Stagnation NH’s Labor Force Growth Supported

Greater Job Growth

95

100

105

110

115

120

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

NH Rock. County "Seacoast"

In-Migration and Population Growth Have Allowed the Seacoast Region’s Labor Force to Grow More and Support Higher Rates of

Job Growth

Private Sector Jobs Have Grown Faster in the Exeter Araea Chamber

Region Since the End of the Recession

Private Sector Emp. Growth 2010-QII2016

14.1%

7.6%

3.8%

2.8%

1.8%

10.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Exeter Chamber

Communities

Rockingham County State of �H

2015-QII2016

2010-15

$22.0

$22.5

$23.0

$23.5

$24.0

$24.5

$25.0

$25.5

$26.0

$26.5

12 13 14 15 16 17

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Avg. Hourly Wages in Private Sector(3 Mos Moving Avg.)

Yr.-Over-Yr. % Growth Private Emp.In %H

R = .80

R2 = .66

Markets Work! As Hiring Has Accelerated So Too Have

Private Sector Wages

$20.0

$21.0

$22.0

$23.0

$24.0

$25.0

$26.0

$27.0

08 09 10 11 12 13 14 15 16 17

-8.00

-7.00

-6.00

-5.00

-4.00

-3.00

-2.00

Avg. Hourly Wages in Private Sector (3 Mos Moving Avg.)

%H Unemployment Rate (Inverted)

Average Wages Also Track NH’s Unemployment Rate

NH is Second Only to Utah in Personal Income Growth

Since 2015

(2.00)

0.00

2.00

4.00

6.00

8.00

10.00

North Dakota

Wyoming

Alaska*

Oklahoma

West Virginia

Louisiana

New Mexico

Montana

South Dakota

Iowa

Texas

Kansas

Minnesota

Nebraska

Vermont

Pennsylvania

Alabama

Kentucky

Rhode Island

Delaware

Mississippi

Wisconsin

Arkansas

Idaho

Ohio

Connecticut

Illinois

New Jersey

Missouri

Colorado

Maryland

Virginia

Arizona

Michigan

Tennessee

New York

Indiana

North Carolina

Hawaii*

Maine

Massachusetts

Florida

Georgia

Washington

South Carolina

California

Nevada

Oregon

New Hampshire

Utah

% Growth in Personal Income 2015 to QIII 2016 �H

MA

VT

ME

CT

RI

Alternative Measures of Labor Underutiliation

2.83.4 3.6 3.8

6.46.0

5.4 5.65.2

4.23.4

2.9

0.7

0.6 0.60.8

1.2

0.9

1.1 1.11.0

1.0

0.8

0.8

2.42.1

2.3

3.2

4.9

4.94.8 4.5

4.7

4.5

3.8

3.2

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Q3-

2016Part-Time (Not by Choice)

Discouraged & Marginally Attached

Basic Unemp Rate

All is Not Perfect - Labor Utilization is Still Not Back to

Pre-Recession Levels

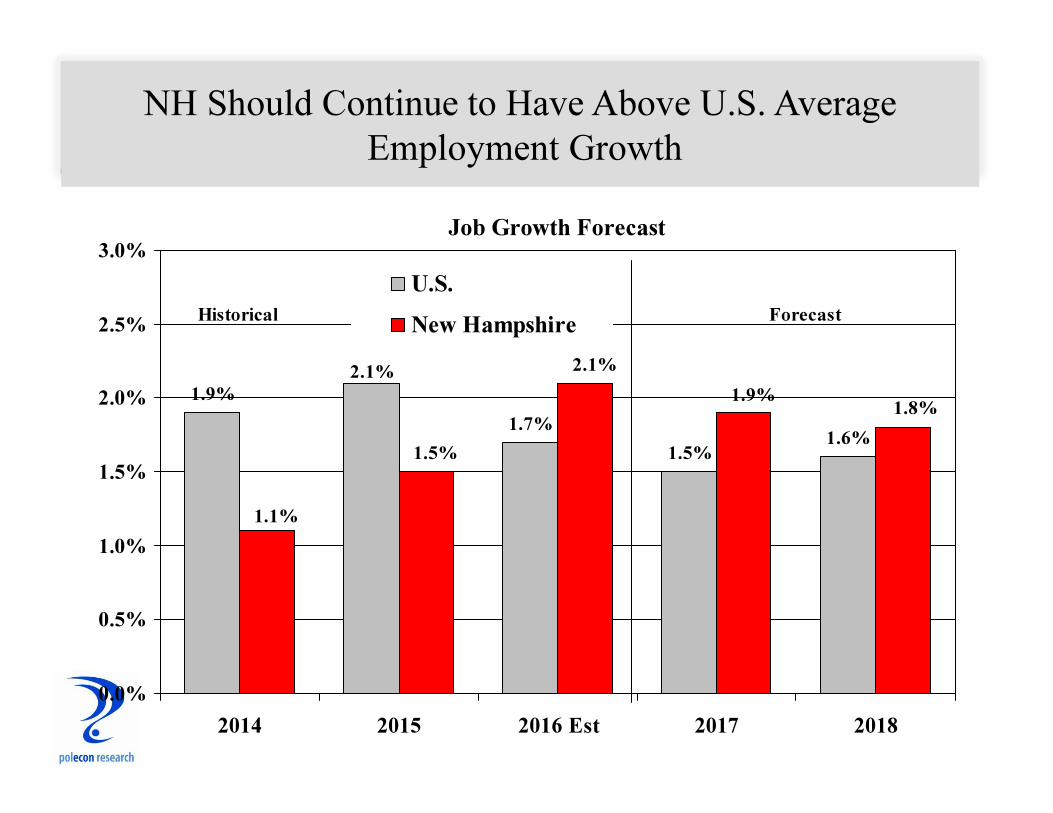

NH Should Continue to Have Above U.S. Average

Employment Growth

Job Growth Forecast

1.9%

1.7%

1.5%1.6%

2.1%2.1%

1.9%1.8%

1.5%

1.1%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2014 2015 2016 Est 2017 2018

U.S.

�ew HampshireHistorical Forecast

Key Factors Affecting NH’s

Growth

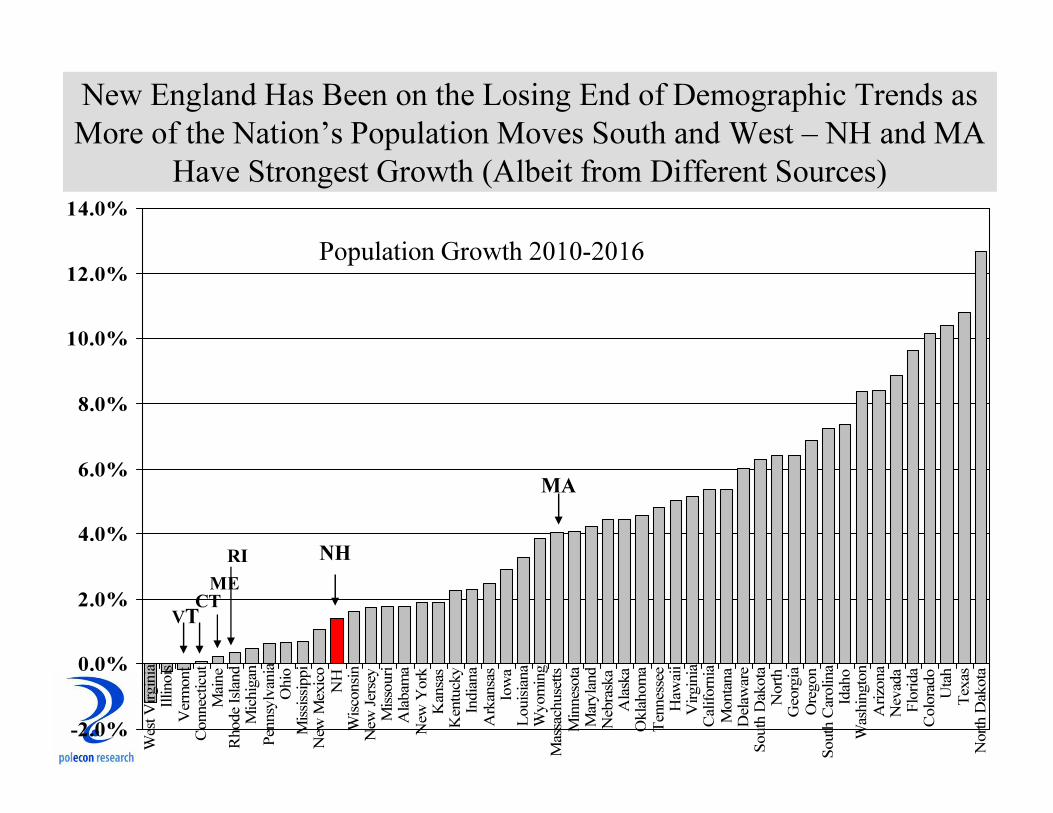

New England Has Been on the Losing End of Demographic Trends as

More of the Nation’s Population Moves South and West – NH and MA

Have Strongest Growth (Albeit from Different Sources)

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

West Virginia

Illinois

Vermont

Connecticut

Maine

Rhode Island

Michigan

Pennsylvania

Ohio

Mississippi

New Mexico

NH

Wisconsin

New Jersey

Missouri

Alabama

New York

Kansas

Kentucky

Indiana

Arkansas

Iowa

Louisiana

Wyoming

Massachusetts

Minnesota

Maryland

Nebraska

Alaska

Oklahoma

Tennessee

Hawaii

Virginia

California

Montana

Delaware

South Dakota

North

Georgia

Oregon

South Carolina

Idaho

Washington

Arizona

Nevada

Florida

Colorado

Utah

Texas

North Dakota

�H

MA

VT

ME

CT

RI

Population Growth 2010-2016

Population Growth From Migration

100,910

236,088

25,406

(72,605)

(28,565)

5,19612,5879,715

(9,272)(2,783)(1,962)

(135,684)

(200,000)

(150,000)

(100,000)

(50,000)

0

50,000

100,000

150,000

200,000

250,000

300,000

CT ME MA �H RI VT

Domestic

International

All of New England Lost Population Due to Net Out-Migration to

Other States but Gained From Net In-Migration From Other

Countries Between 2010 and 2016

Net Migration to NH

12,132

9,170

6,472

3,117

4,600

2,170

(2,389)(2,473)(2,602)

(773) (938)

(2,337)

2,854

(1,570)

2,187

(2,206)

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

�et State-to-State Migration

�et International Migration

Net State-to-State Migration to NH is Resuming and is the Most

Important Factor in Determining How Much We Grow

The Seacoast Has Accounted for Almost all of NH’s Net State-to-

State Migration Since the End of the Recession

(Providing Clues to What it Takes to Attract Individuals)

Net Domestic Migration 2010-2015

(6,685)

104

556

1,157

3,389

(93)

(667)

(1,360)

(1,038)

(887)

-8,000 -6,000 -4,000 -2,000 0 2,000 4,000

Hillsborough County

Cheshire County

Coos County

Grafton County

Sullivan County

Merrimack County

Carroll County

Belknap County

Strafford County

Rockingham County

Rockingham County Attracts a Range of Demographics But Higher

Rates of Early and Mid-Career Individuals Than Does NH Overall

Age Distribution of Out-of-State Movers to NH (2011-2015)

14.7%

12.7%

13.5%

23.0%

11.7%

9.9%

7.3%

7.1%

17.5%

3.1%

13.7%

25.0%

14.0%

10.6%

8.2%

8.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Under 18

18 to 19

20 to 24

25 to 34

35 to 44

45 to 54

55 to 64

65 +

The Impact of Baby Boom Retirements Will Make Net In-Migration Even More

Important to Labor Force Growth: The Gap Between The Number Who Will be

Entering vs. Exiting The Labor Force Over the Next 15 Years is Greatest in

Many Northeastern States

Pop.Age 5-19 Minus Pop. 50-64 as % of Working Age Population

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Maine

Vermont

West Virginia

NH

Montana

Florida

Pennsylvania

Oregon

Rhode Island

Hawaii

Massachusetts

Connecticut

Wyoming

Delaware

New York

Wisconsin

Michigan

Ohio

New Jersey

Washington

Maryland

Kentucky

ND

South

Tennessee

Virginia

Missouri

Alabama

Minnesota

Iowa

Colorado

North

South Dakota

Louisiana

Illinois

New Mexico

Nevada

Alaska

Arkansas

Indiana

Oklahoma

Nebraska

Kansas

Mississippi

California

Arizona

Georgia

Idaho

Texas

MAME

VTNH RI

CT

Utah 17%

Industries With a Lower Ratio of Younger Workers Relative to Workers

Near Retirement Will Have Worker Replacement Needs But Tend to

Attract Fewer Younger Workers

27.6%

53.4%

59.4%

62.2%

63.0%

66.8%

67.7%

72.8%

73.7%

80.3%

81.7%

83.3%

91.9%

106.5%

120.1%

138.3%

151.7%

156.6%

36.3%

0% 20% 40% 60% 80% 100% 120% 140% 160% 180%

Real Estate

Art, Ent., & Rec.

Durable Goods Manuf.

�on-Durable Manuf.

Educational Services

Utilities

Transp. & Warehousing

Health Care & Soc. Asst.

Prof., Sci., & Tech. Srvcs.

Public Administration

Wholesale trade

�H Total

Other Services

Construction

Mgmt, Admin. & Supprt Srvcs

Finance and Insurance

Information

Retail Trade

Accom. & Food Srvcs.

Ratio of Workers Age 25-34 to Workers 55-64 By Industry in NH

Combining The Age Composition of an Industry’s Workforce With Projected

Employment Growth Highlights Those Industries Most Likely to Face the Greatest

Labor Shortages (Some Occupations Will be in Short Supply in all Industries)

12.5%

9.3%

7.0%

1.6%

-7.1%

-7.2%

-8.1%

-11.0%

-13.3%

-14.8%

-3.2%

-0.4%

-0.6%

5.8%

3.9%

2.9%

10.0%

-20% -15% -10% -5% 0% 5% 10% 15%

Utilities

Information

Retail Trade

Manufacturing

Accom. & Food Srvcs.

Transp. & Warehousing

Public Administration

Finance and Insurance

Other Services

Educational Services

Wholesale trade

Art, Ent., & Rec.

Construction

Real Estate

Admin. & Supprt Srvcs

Prof., Sci., & Tech. Srvcs.

Health Care & Soc. Asst.

Projected Supply/Demand Balance of Labor by Industry in NH

NH is Not Monolithic When it Comes to Aging – Community’s are

Aging Differently and the Decisions They Make Will Have More

Impact Than State Policies

Median Age of Population

35.0

39.2

39.6

40.4

40.5

40.9

41.1

41.6

41.8

43.4

43.3

0.8

3.3

2.2

2.6

1.5

0.5

3.1

3.6

1.1

2.5

0.443.9

-2.1

(5) 5 15 25 35 45 55

�ewmarket

�ewfields

�H

Raymond

Rockingham Cnty

Brentwood

Epping

Stratham

Kingston

East Kingston

Kensington

Exeter

2005-2009

2010-2014

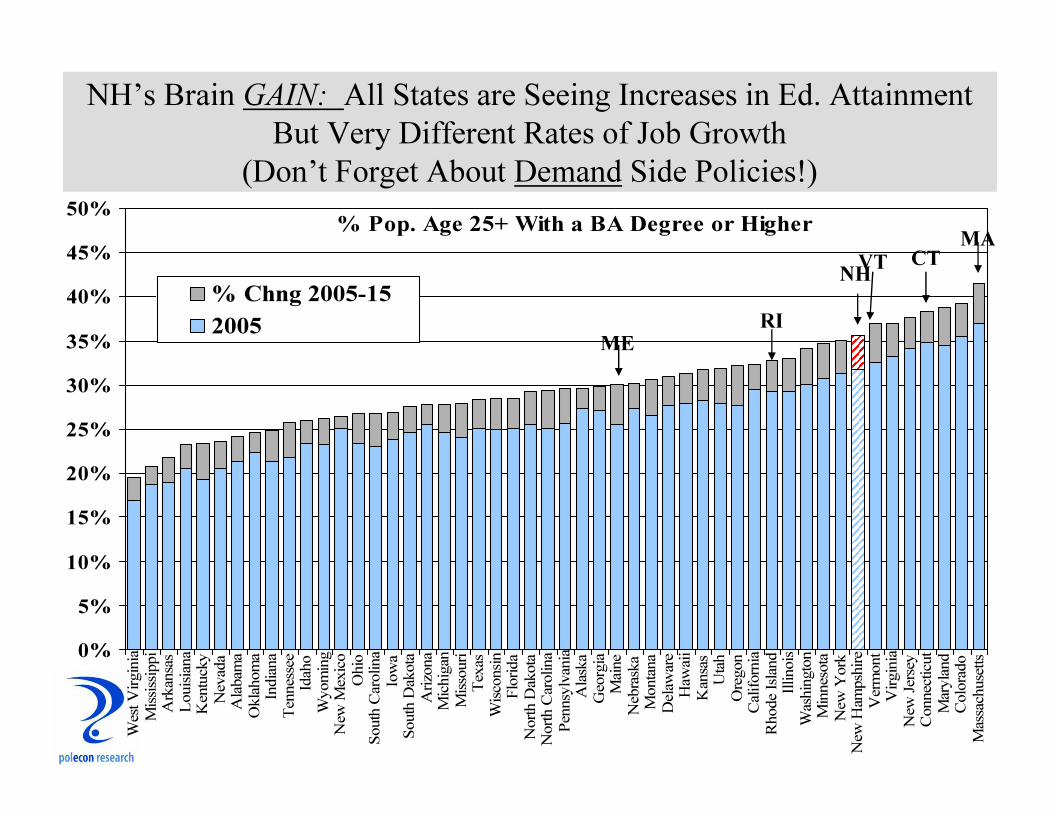

NH’s Brain GAI�: All States are Seeing Increases in Ed. Attainment

But Very Different Rates of Job Growth

(Don’t Forget About Demand Side Policies!)

% Pop. Age 25+ With a BA Degree or Higher

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

West Virginia

Mississippi

Arkansas

Louisiana

Kentucky

Nevada

Alabama

Oklahoma

Indiana

Tennessee

Idaho

Wyoming

New Mexico

Ohio

South Carolina

Iowa

South Dakota

Arizona

Michigan

Missouri

Texas

Wisconsin

Florida

North Dakota

North Carolina

Pennsylvania

Alaska

Georgia

Maine

Nebraska

Montana

Delaware

Hawaii

Kansas

Utah

Oregon

California

Rhode Island

Illinois

Washington

Minnesota

New York

New Hampshire

Vermont

Virginia

New Jersey

Connecticut

Maryland

Colorado

Massachusetts

% Chng 2005-15

2005

�H

MA

VT

ME

CT

RI

Over 50 Percent of the Individuals (Age 25+) Who Moved to Rockingham County

From Another State Have a Bachelor’s Degree or Higher

(Ed. Attainment of Individuals Age 25+ Who Moved to NH Between 2011 and 2015)

5.3%

21.1%

25.9%

29.2%

18.4%

4.9%

18.0%

24.6%

34.1%

18.3%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0%

Less Than HS Grad.

HS Grad.

Some College or

Associate's Degree

Bachelor's

Grad. Or Prof.

�H Rock. County

We AREAdding Educated Labor But We are Adding More Than is

Being Employed by NH Businesses (Demand Side Matters! And

Maybe Associate’s and Certificate Degrees are a Better Indicator)

31.8%

35.7%

31.6% 30.9%

10%

15%

20%

25%

30%

35%

40%

45%

50%

2005 2015

% of �H Pop Age 25+ With at BA Degree or Higher

% of �H Jobs Held by Someone Age 25+ With a BA Degree or Higher

The Region is Gaining “Brains” at a Much Faster Rate Than is

NH Overall

% Pop. Age 25+ With a Bachelor's Degree or Higher

13.2

15.4

24.4

25.9

28.2

18.3

32

41.3

(0.2)

(0.9)

4.3

4.7

9.2

6.0

8.3

11.2

13

5.6

11

16.9

9.9

9.4

5.8 6.3

(5) 5 15 25 35 45 55 65

Raymond

Epping

�H

Rockingham Cnty

�ewmarket

Brentwood

Exeter

Stratham

1990

2000

2010-2014

Corporate Taxes as a % of Private Sector Gross State Product

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

�H MA

A Key Policy is Tax Rates. Business Taxes as a Pct. of Private Sector

Gross State Product is a Better Relative Measure of Than Burden Than

is the Tax Rate – They are High in NH

Avg. NH Electricity Prices as a % of U.S. Average Prices

75%

95%

115%

135%

155%

175%

195%

215%

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Industrial Commercial Residential

Electricity Prices in NH are Especially Hard on Manufacturers.

Industrial Customers Pay About 80% More for Electricity in NH

Than the U.S. Avg..

Source: U.S. Energy Information Agency, PolEcon

First Year Energy Cost Savings in NH From NED ($Million)

$17.7

$24.1$20.9

$40.7

$40.9

$21.2

$0

$10

$20

$30

$40

$50

$60

$70

Residential Sector Commercial Sector Industrial Sector

Millions

Electricity

atural Gas

$58.4

(3.4% Reduction)

$65.0

(6.5% Reduction)

$42.1

(8.9% Reduction)

One Pipeline Project’s (NED) Impact on Natural Gas Prices in New England

Would Have Resulted in an Annual $165.5 Million in Energy Cost Savings in the

Residential, Commercial, and Industrial Sectors in NH

Annual Energy Savings in NH by Sector

$64.9 $69.7 $74.5 $79.3 $84.1 $88.9 $93.8 $98.7 $103.6 $108.5

$42.1$45.0

$48.0$51.1

$54.1$57.0

$60.0$62.9

$65.7$68.4

$58.4$62.4

$66.7$71.1

$75.6$80.0

$84.4$88.8

$93.2$97.7

$0

$50

$100

$150

$200

$250

$300

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

Millions

Commercial Industrial Residential

I Estimated Energy Savings to NH Consumers to be About

$2.2 Billion in the First 10 Years of NED Operation

Strong and Committed Local Banks are Key to the Strength of the Regional

Economy: Optima Bank and Trust Has Bucked the National Trend of Declining

Small Business Loans by Community Banks Following Passage of New Regulations

% Change Between 2010 and QIII2016

2.2%-25.0%

102.7%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Optima Bank and

Trust

All Community

Banks �ationally

<$1 Billion

All Banks �ationally

>$1 Billion