Embed Size (px)

Citation preview

How Can Knowledge Capital

Become Better Accepted in

Norway?

Hans Henrik Ramm

Petroleum Strategy Advisor

Ramm Kommunikasjon

Petroleum Technology at a Crossroads

26 January 2005

Knowledge Creates Value

Technology export

Much larger resources

The Government's innovation plan – the vision:

“Norway should be among the world's most innovative countries,

where firms and ambitious and creative people should have good

opportunities for developing profitable activities. In important

sectors, Norway should be in the international front with regard to

knowledge, technology and value creattion”

Value Creation Capability = Capital

Knowledge Capital =

Intellectual Capital = IC =

Intangible Assets

Carried by humans:

Human Capital

Carried by firms, institutions, clusters:

Organisational Capital

Relational Capital

Structural Capital

How is IC Created and Put to Use?

R&D

Organisation

Procurement

strategy

Leaders and

followers

Risk assessment

Early implementation

Acqusitions

Alignment to needs

A Lot is About Cooperation

Pilots and first

use

Taking the long

term view

R&D institutions

and suppliers

Commercial focus

Critical mass

Incentives

Authorities +

oil companies +

suppliers

CLUSTER

FUNCTIONS

The “Micro” View:

* KNOWLEDGE COUNTS AGAINST

BOTTOM LINE

* COMPANIES ARE DIFFERENT

* WE MUST COOPERATE AND COMPETE

* FRAMEWORK CONDITIONS COUNT

* WE MUST IMPROVE CONTINOUSLY

How is this Matched by the “Macro” View?

Classic Theory: Knowlegde Emerges

Uniformly Everywhere

Firms' Efforts Make No Difference

Norwegian R&D Makes No Difference

Framework Conditions Make No Difference

Stabilisation & Competition Policies Sufficient

GROWTH

=

CHANGE IN CAPITAL BASE

+

CHANGE IN LABOUR SUPPLY

+

CHANGE IN TOTAL FACTOR

PRODUCTIVITY(TFP = UNIFORM KNOWLEDGE)

Futile to encourage

WHAT HAPPENS IF

WE INSERT THE

“MICRO” VIEW

INTO “MACRO”

GROWTH THEORY?

GROWTH

=

CHANGE IN CAPITAL BASE

+

CHANGE IN LABOUR SUPPLY

+

CHANGE IN IC BASE(ACCUMULATED KNOWLEDGE

CREATED BY PEOPLE, FIRMS,

INSTITUTIONS AND CLUSTERS = TFP)

Crucial that it is encouraged

The Consequences Are Larger Than

We Think:* R&D – Public Grants & Tax Treatment

> R&D benefits all society

> “Externalities” should be “internalised”

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

> People choose between spending time on leisure,

work or education

> Lifetime post-tax benefits influences choices

> Tax about far more than redistribution

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

> Take a Look At Capital Value Theory >>>

Capital Value Theory – Classic Version:* Knowledge is uniform and equally available to all

* Capital markets are free and competitive

* Capital flows to highest profits

* If somebody make high profits, others will attack

* Others buy same knowledge = same costs, same products

* Profits will equalize to “normal rate of return”

A COMPANY'S PROFIT

=

Normal returns on risk free finance capital

+

Risk premium

+

Extraordinary (“clean”) profits

(monopoly rent, resource rent etc)

Capital Value Theory - Innovation Theory:* The best knowledge is company specific and hard to copy

* Others will not find same knowledge available

* Companies differ – the best make better profits

A COMPANY'S PROFIT

=

Normal returns on risk free finance capital

+

Risk premium

+

Knowledge rent

+

Extraordinary (“clean”) profits

(monopoly rent, resource rent etc)

In the Petroleum Industry,

There are Natural Resources As

Well

+ +

Resource Rent Finance Rent Knowledge Rent

In the Petroleum Industry,

There are Natural Resources As

Well

+ +

Resource Rent Finance Rent Knowledge Rent

TAX

78%

In the Petroleum Industry,

There are Natural Resources As

Well

+ +

Resource Rent Finance Rent Knowledge Rent

TAX

78%

TAX

28%

In the Petroleum Industry,

There are Natural Resources As

Well

+ +

Resource Rent Finance Rent Knowledge Rent

TAX

78%

TAX

28%TAX

??%

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

> Special Tax (Petroleum, Hydropower, Fisheries?)

intended to take resource rent and other“clean

profit” is also applied for knowledge rent

> New Capital Earnings Tax works same way for all

firms, albeit only on receiver's hand

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

> Knowledge intensive firms underevaluated

> “Spin doctors” can exaggerate IC (Enron)

> Stock market poorly informed, favors insiders

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

* Primary Risk Capital Tied to Home Market - Poor

Norwegian Equity Capital Market is a Real Problem

> Hard to assess real value of remote firms

> Investors require higher risk payment or stay away

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

* Primary Risk Capital Tied to Home Market - Poor

Norwegian Equity Capital Market is a Real Problem

* Discount on Norwegian Shares Worse for Knowledge

Intensive Firms - Tilted Playing Field for Mergers etc

> Makes better sense for owners to sell than to buy

or stay

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

* Primary Risk Capital Tied to Home Market - Poor

Norwegian Equity Capital Market is a Real Problem

* Discount on Norwegian Shares Worse for Knowledge

Intensive Firms - Tilted Playing Field for Mergers etc

* Insufficient focus on cluster effects

> Government's innovation strategy

> Oil companies and “best practise”

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

* Primary Risk Capital Tied to Home Market - Poor

Norwegian Equity Capital Market is a Real Problem

* Discount on Norwegian Shares Worse for Knowledge

Intensive Firms - Tilted Playing Field for Mergers etc

* Insufficient focus on cluster effects

* Aspects of competition policy

> Clusters must cooperate as well as compete

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

* Primary Risk Capital Tied to Home Market - Poor

Norwegian Equity Capital Market is a Real Problem

* Discount on Norwegian Shares Worse for Knowledge

Intensive Firms - Tilted Playing Field for Mergers etc

* Insufficient focus on cluster effects

* Aspects of competition policy

* Errors in Macro-Economic Planning

> Technology shocks interpreted as business cycles

The Consequences Are Larger Than

We Think:* R&D - Public Grants & Tax Treatment

* Personal Taxation - Progressive Tax is Disincentive

* Company Tax - Progressive Tax is Disincentive

* Petroleum Tax - Mixes Resource & Knowledge Rent

* Accounting - IC Not Visible in Financial Statements

* Primary Risk Capital Tied to Home Market - Poor

Norwegian Equity Capital Market is a Real Problem

* Discount on Norwegian Shares Worse for Knowledge

Intensive Firms - Tilted Playing Field for Mergers etc

* Insufficient focus on cluster effects

* Aspects of competition policy

* Errors in Macro-Economic Planning

* Errors in Planning of Education Policy Etc Etc

Realising that knowledge is a kind of capital that exists

in different kinds and various amounts is crucial to

decide on many policy matters in Government as well

as companies.

IC is in many ways similar to financial capital, in

many ways very different.

It is vital to know much more about:* How knowledge creation is influenced by fiscal and other

policies

* How Human Capital is put to use in commercial entities

* The functionalty of the Norwegian clusters

* The impact of knowledge and technology on the macro

economy

* ..and so on

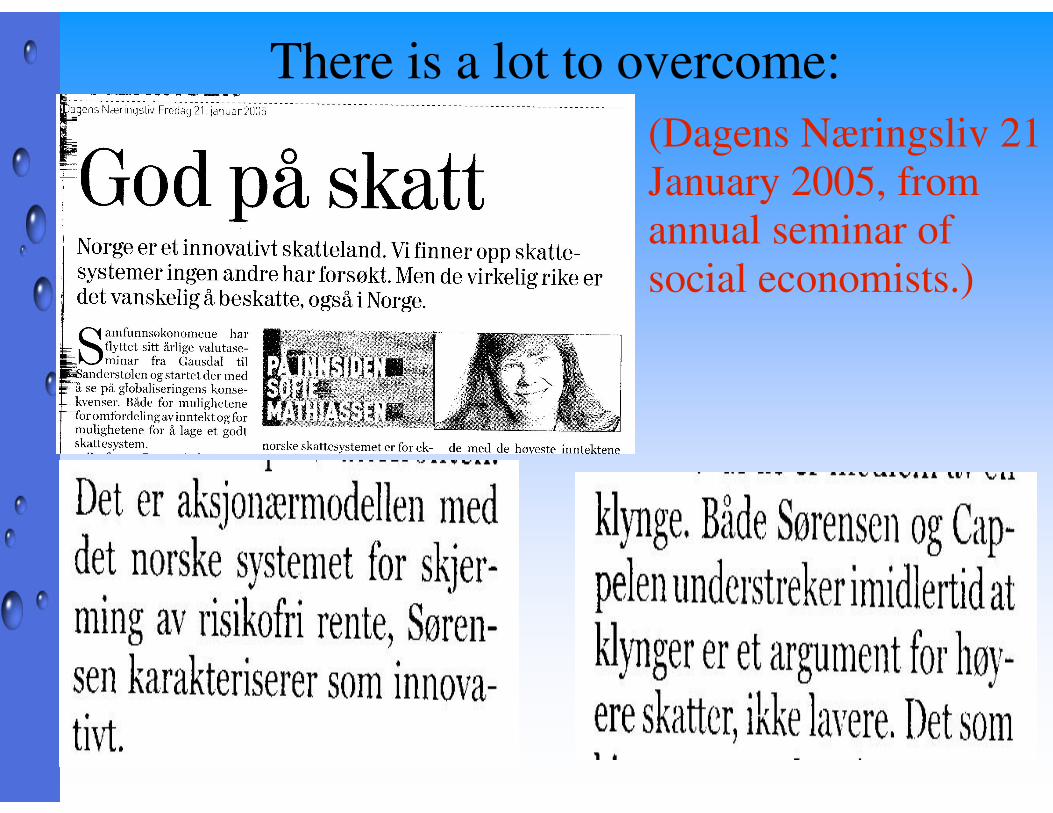

There is a lot to overcome:

(Dagens Næringsliv 21

January 2005, from

annual seminar of

social economists.)

But definitely also progress:

What must be dealt with:

* Too many conflicting social paradigms cemented by media

* Insufficient focus on value creation

* Business community has abdicated in debate over

fundamental economic and political paradigms

* Society's intellectuals and opinion leaders must be mobilized

* We need think-tanks and academic institutions focusing on

micro/macro interface, knowledge economy and cluster issues

This is important for authorities, and they are moving slowly,

but need supporting momentum.

Who is closest to do it?

Of course, the main knowledge value creators themselves-->

Other

industry

Petroleum is the frontline cluster:

ICTPower

Shipping

Process

Finance

Petroleum

Fisheries

&

fish

farming

The answer to the “how” is not

about easy PR etc. It is about hard

qualified research and analysis.

The industry must invest in

research about the behaviour of

knowledge as capital and its own

functionality. Potential returns are

very high.