Embed Size (px)

Citation preview

Horlings is a world-wide network of independent accountants and consultants firms

6 February 2009

The Dutch co-operative

Nexia European Tax Group Meeting

Dorine FraaiSenior Tax Manager

Horlings Tax Advisors Amsterdam

The Netherlands+ 31 20 5700259

2

April 20, 2023

2

Content

1. Introduction

2. Civil law aspects

3. Taxation of co-operative

4. Taxation of members of co-operative

5. Dividend withholding tax and international aspects

6. Structures

3

April 20, 2023

3

Introduction

Use of a co-operative

• Traditionally the Dutch co-operative was used by farmers;• Originally for civil law purposes, nowadays use is tax driven• The Dutch co-operative is used more often in international holding structures;• Main advantage: no Dutch dividend withholding tax on dividends distributed by

co-operatives, while use of treaties is possible, sometimes in combination with a BV;

• Dutch tax authorities are willing to grant an Advance Transaction Ruling for the use of the co-operation under certain circumstances;

• Other advantage of co-operatives is the very flexible company law regime that applies;

4

April 20, 2023

4

Civil law (1)

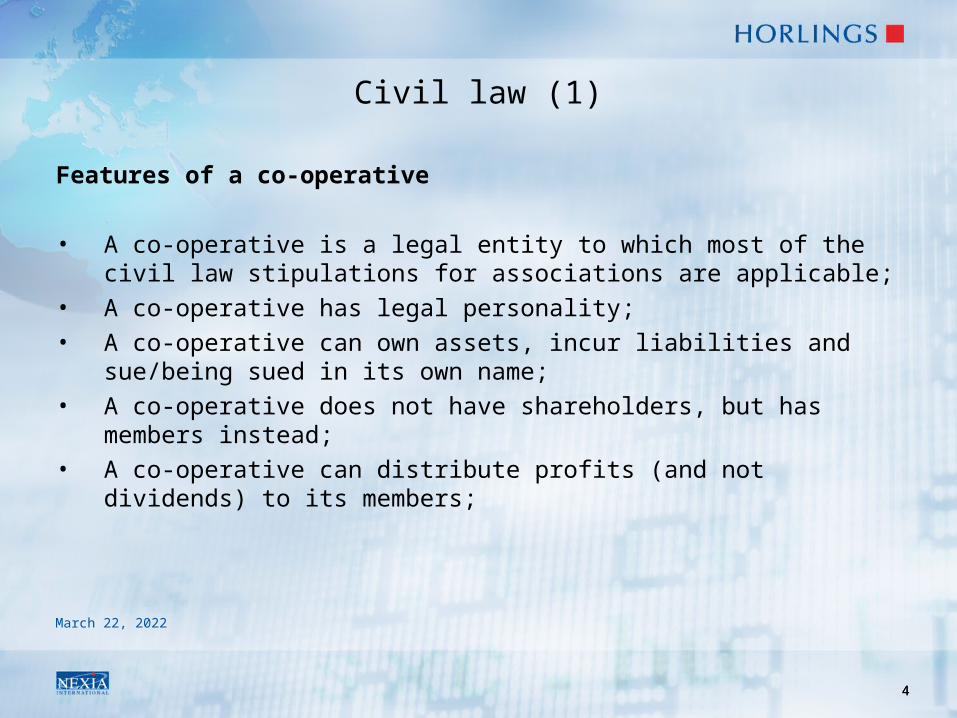

Features of a co-operative

• A co-operative is a legal entity to which most of the civil law stipulations for associations are applicable;

• A co-operative has legal personality;• A co-operative can own assets, incur liabilities and sue/being sued in its own

name;• A co-operative does not have shareholders, but has members instead;• A co-operative can distribute profits (and not dividends) to its members;

5

April 20, 2023

5

Civil law (2)

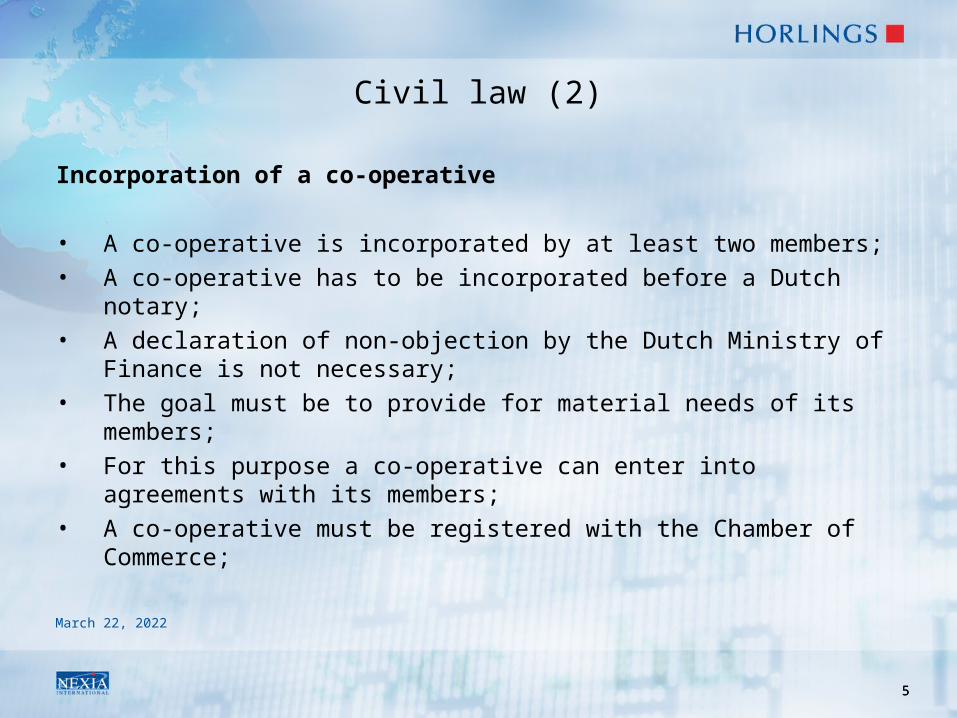

Incorporation of a co-operative

• A co-operative is incorporated by at least two members;• A co-operative has to be incorporated before a Dutch notary;• A declaration of non-objection by the Dutch Ministry of Finance is not necessary;• The goal must be to provide for material needs of its members;• For this purpose a co-operative can enter into agreements with its members;• A co-operative must be registered with the Chamber of Commerce;

6

April 20, 2023

6

Civil law (3)

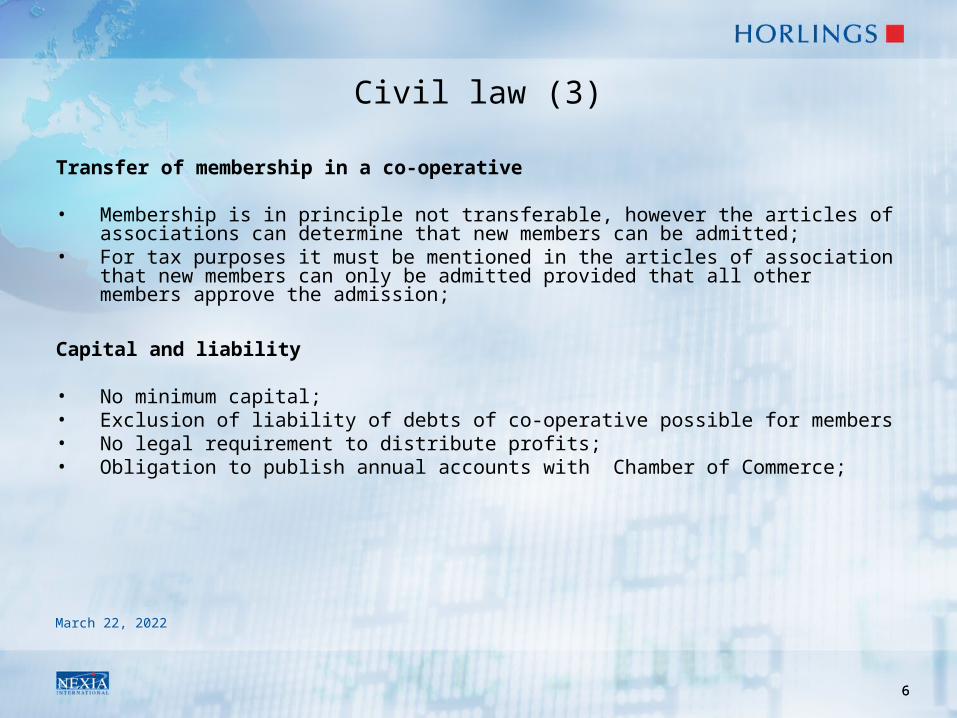

Transfer of membership in a co-operative

• Membership is in principle not transferable, however the articles of associations can determine that new members can be admitted;

• For tax purposes it must be mentioned in the articles of association that new members can only be admitted provided that all other members approve the admission;

Capital and liability

• No minimum capital;• Exclusion of liability of debts of co-operative possible for members• No legal requirement to distribute profits;• Obligation to publish annual accounts with Chamber of Commerce;

7

April 20, 2023

7

Civil law (4)

Board of co-operative

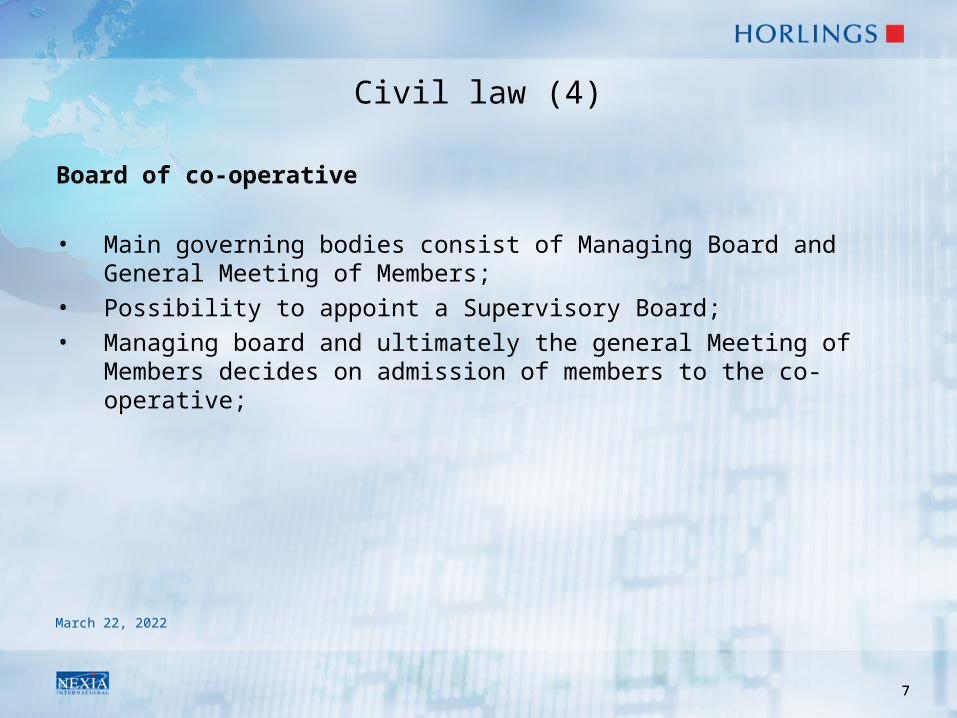

• Main governing bodies consist of Managing Board and General Meeting of Members;

• Possibility to appoint a Supervisory Board;• Managing board and ultimately the general Meeting of Members decides on

admission of members to the co-operative;

8

April 20, 2023

8

Tax law (1)

Corporate income tax

• A co-operative is subject to Dutch corporate income tax;• A co-operative can invoke the participation exemption on a qualifying

participation;• A co-operative can become a part of a fiscal unity;

Ad 1 Subject to corporate income tax A co-operative is subject to corporate income tax like a BV or an NV. A complicated

regime existsfor co-operatives having individuals as members, allowing for the deduction of profit

distributionsto members.

9

April 20, 2023

9

Tax law (2)

Corporate income tax: participation exemption

A qualifying participation is present provided that:

- A stake of at least 5% (5% of nominal share capital, or in some cases 5% of voting rights) is held in a company having a capital divided into shares; and

- The subsidiary cannot be regarded as a low taxed investment subsidiary, or - The subsidiary is a real estate subsidiary;

10

April 20, 2023

10

Tax law (3)

Corporate income tax: participation exemption

Low taxed investment participationA subsidiary qualifies as a low taxed investment participation if:

• more than 50% of the value of its assets comprises “non-business-related assets” (asset test), and

• the subsidiary is not subject to an effective rate of at least 10% on a taxable profit calculated established in accordance with Dutch standards (subject-to-tax test).

11

April 20, 2023

11

Tax law (4)

Corporate income tax: fiscal unity

A co-operative can form a fiscal unity with a BV (or another co-operative), in which the co-operative is the parent company, or can be the subsidiary of a BV and form a fiscal unity as such.

In international structures a co-operative is often set up holding the shares of a BV, forming afiscal unity.

Main features of a fiscal unity:- The parent company and the subsidiary can file one single tax return;- Assets and liabilities can be transferred free from corporate income tax within the fiscal

unity;- Losses of one member of a fiscal unity and gains of other members of a fiscal unity can be

offset within the same year;

12

April 20, 2023

12

Tax law (5)

Corporate income tax: fiscal unity

The main conditions for the formation of a fiscal unity are:

• Each subsidiary must be at least 95% owned (legal and beneficial ownership of the shares), although the holding may be indirect through another Dutch company, provided the intermediary company also forms a part of the fiscal unity;

• The accounting period for all companies forming part of the fiscal unity must coincide; • The companies involved must be subject to the same tax regime;• The companies must be resident in the Netherlands for corporate income tax purposes; • Both the parent company and the subsidiaries should have a certain legal form, such as the

NV, BV or co-operative, or a comparable foreign legal form.

13

April 20, 2023

13

Tax law (6)

Dividend withholding tax

Distributions of profit by a co-operative to its members are exempt from Dutch dividend withholding tax, since

the co-operative is not mentioned in the Dutch Dividend Withholding Tax Act.

In order to ensure that the Dutch dividend withholding tax applies, an Advance Tax Ruling (ATR) can be

negotiated with the Dutch tax authorities.

14

April 20, 2023

14

Taxation members of co-operative

• Co-operative can have private individuals as members and entities as members• We will only discuss taxation for (foreign) corporate members

Dutch corporate membersCorporate members of a co-operative can invoke the participation exemption on profit distributions derived from their membership.

No minimum requirement of the holding of 5% in a co-operative.

15

April 20, 2023

15

Taxation foreign members of co-operative

Foreign Corporate members of co-operative can become subject to Dutch corporate income on the basis of the following two stipulations of the Dutch Corporate Income Tax Act:

• The membership in the co-operative can be regarded as a share in the profit of an enterprise that has its effective management in the Netherlands, provided that that share in the profit can not be regarded as derived from holding securities; or

• The membership in the co-operative constitutes a substantial interest (entitles the member to 5% or more of the annual profit of the co-operative) and the membership cannot be allocated to an (active) trade or business of the member.

16

April 20, 2023

16

Co-operative: Dutch Advance Tax Ruling

The Dutch tax authorities are willing to grant an ATR confirming that:

No Dutch corporate income tax is due on membership in a co-operative; Distributions of profit by co-operative are not subject to Dutch dividend withholding tax.

Provided that:

• The co-operative is used an active structure. • No Dutch dividend withholding tax claim is lost by the use of a co-operative;• No individuals as members of the co-operative;• All other relevant tax aspects are covered in ATR. In some cases where the co-operative or

its Dutch subsidiary carry our finance activities, the ATR will be issued under the condition that an Advance Pricing Agreement is negotiated for finance activities;

• Co-operative must be a closed end co-operative;• Co-operative may not be an entity listed on the Amsterdam stock exchange.

17

April 20, 2023

17

International tax aspects of co-operative

• Co-operative is entitled to EU Directives, except for Interest and Royalty Directive,• As a result, a co-operative can invoke the Parent-Subsidiary Directive• Co-operative is entitled to tax treaties

18

April 20, 2023

18

Conclusion and questions

The advantages of using a co-operative in international structures can be summarized as follows:

• No dividend withholding tax upon distribution of profits by co-operative;• No capital tax (abolished);• Unlimited access EU Directives and Dutch tax treaty network;• Only one jurisdiction, therefore low annual maintenance cost;• Simple structure;• Flexible civil law stipulations and quick incorporation;• Easy exit, because capital gain not taxable;• Tax treatment can be confirmed through an ATR.

19

April 20, 2023

19

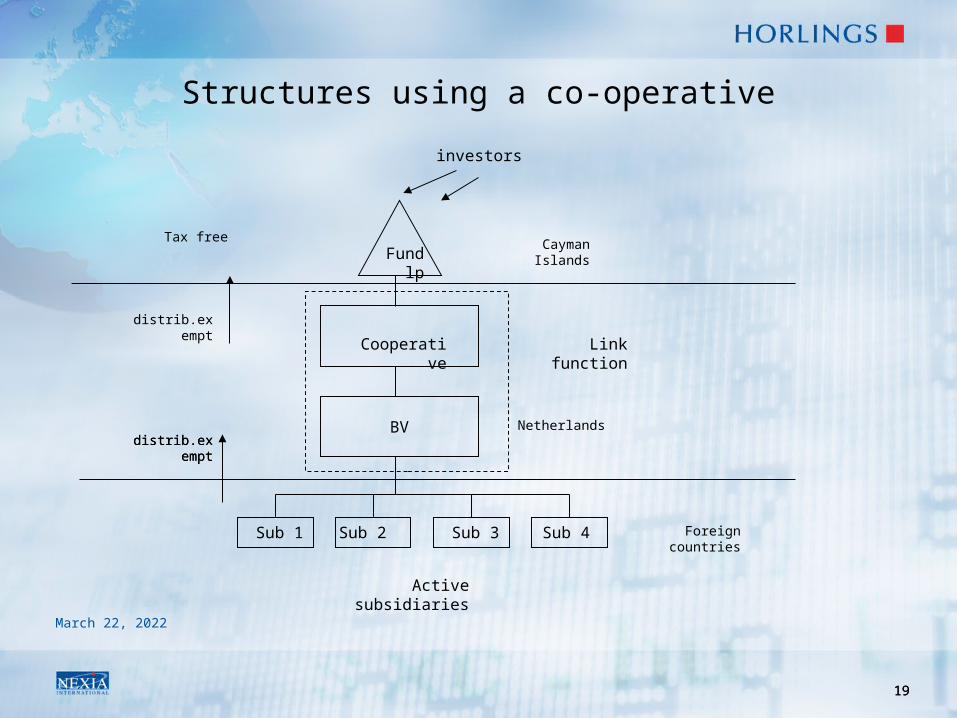

Structures using a co-operative

Sub 1 Sub 2

Fund lp

Sub 4

BV

Cooperative

Sub 3

investors

Active subsidiaries

Link function

Cayman Islands

Netherlands

Foreign countries

distrib.exemptdistrib.exempt

distrib.exempt

Tax free

20

April 20, 2023

20

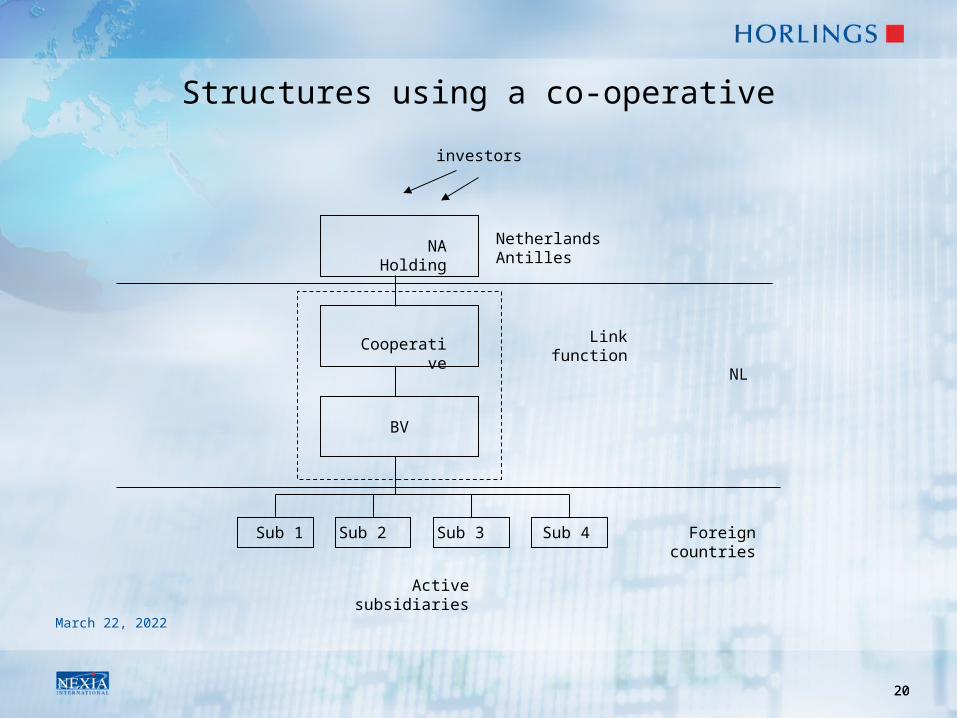

Structures using a co-operative

Sub 1 Sub 2

NA Holding

Sub 4

BV

Cooperative

Sub 3

investors

Active subsidiaries

Link function

NetherlandsAntilles

Foreign countries

NL

21

April 20, 2023

21

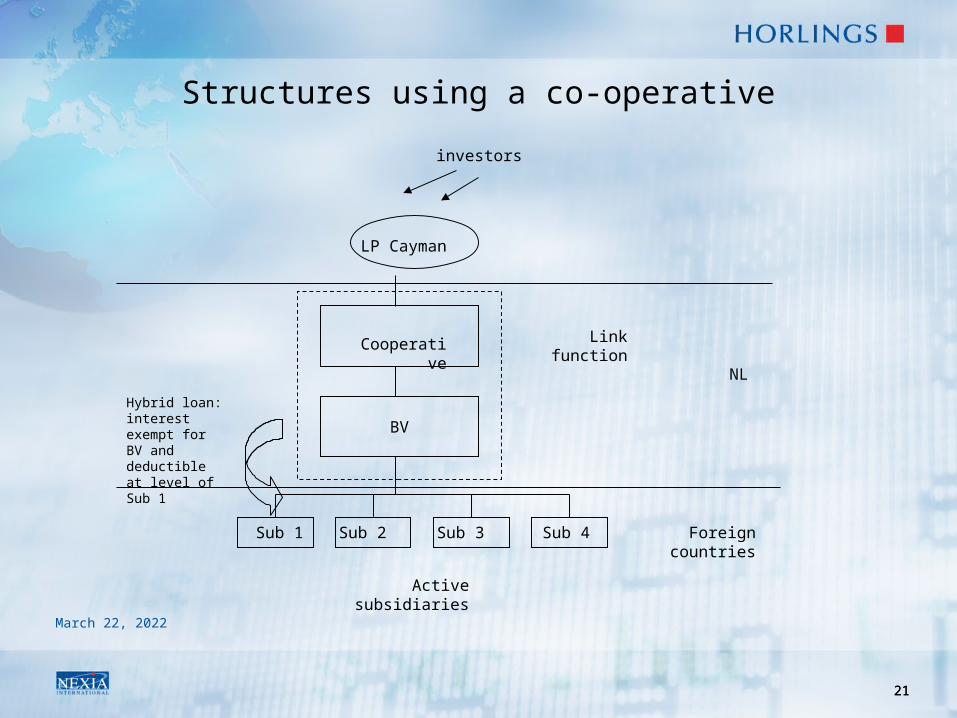

Structures using a co-operative

Sub 1 Sub 2

LP Cayman

Sub 4

BV

Cooperative

Sub 3

investors

Active subsidiaries

Link function

Foreign countries

NL

Hybrid loan: interest exempt for BV and deductible at level of Sub 1