Embed Size (px)

Citation preview

Holden New Zealand Ltd

Financial statements for the financial year ended 31 December 2017

Contents

Directors' declaration

Independent audit report

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Statement of profit or loss and other comprehensive income

Statement of financial position

Page

2

3

6

7

8

9

Statement of changes in equity

Statement of cash flows

Notes to the financial statements 10

1

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Directors' declaration

In the opinion of the directors of Holden New Zealand Ltd, the financial statements and notes on pages 6 to 28:

..

..

comply with New Zealand generally accepted accounting practice and presents fairly the financial position of the Company as at 31 December 2017 and the results of their operations and cash flows for the year ended on that date; and

have been prepared using appropriate accounting policies, which have been consistently applied and supported by reasonable judgements and estimates.

The directors believe that proper accounting records have been kept which enable, with reasonable accuracy, the determination of the financial position of the Company and facilitate compliance of the financial statements with the Companies Act 1993.

The directors consider that they have taken adequate steps to safeguard the assets of the Company and to prevent and detect fraud and other irregularities. Internal control procedures are also considered to be sufficient to provide reasonable assurance as to the integrity and reliability of the financial statements.

Director Auckland, 28 March 2018

J. Th ley!Direct r 1

Melbourne, 28 arch 2018

Deloitte.

Independent Auditor's Report to the Members of Holden New Zealand Ltd

Opinion

Deloitte Touche Tohmatsu A.B.N. 74 490 121 060

550 Bourke Street Melbourne VIC 3000 GPO Box 78 Melbourne VIC 3001 Australia

DX 111 Tel: +61 (0) 3 9671 7000 Fax: +61 (0) 3 9671 7001 www.deloitte.com.au

We have audited the financial statements of Holden New Zealand Ltd (the "Entity") which comprise the statement of financial position as at 31 December 2017, the statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies as set out on pages 6 to 28.

In our opinion, the accompanying financial statements present fairly, in all material respects, the Entity's financial position as at 31 December 2017 and its financial performance and its cash flows for the year then ended in accordance with New Zealand Equivalents to International Financial Reporting Standards Reduced Disclosure Regime.

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (New Zealand) (ISAs (NZ)). Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report.

We are independent of the Entity in accordance with the ethical requirements of Professional and Ethical Standard 1 (Revised) Code of Ethics for Assurance Practitioners issued by the New Zealand Auditing and Assurance Standards Board (the Code) that are relevant to our audit of the financial statements, and we have fulfilled our other ethical responsibilities in accordance with the Code.

Other than in our capacity as auditor, we have no relationship with or interests in the Entity, except that partners and employees of our firm deal with the Entity on normal terms within the ordinary course of trading activities of the business of the Entity.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Other Information

The directors on behalf of the Entity are responsible for the other information. The other information comprises the information included in the Entity's annual report for the year ended 31 December 2017, but does not include the financial statements and our auditor's report thereon.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with

Liability limited by a scheme approved under Professional Standards Legislation. Member of Deloitte Touche Tohmatsu Limited

3

Deloitte

the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Director's Responsibility for the Financial Statements

The directors of the Entity are responsible on behalf of the Entity for the preparation and fair presentation of the financial statements in accordance with New Zealand Equivalents to International Financial Reporting Standards Reduced Disclosure Regime, and for such internal control as the directors determine is necessary to enable the preparation of the financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible on behalf of the Entity for assessing the ability of the Entity to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intend to liquidate the Entity or to cease operations, or has no realistic alternative but to do so.

Auditor's Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (NZ) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs (NZ), we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whetherdue to fraud or error, design and perform audit procedures responsive to those risks, andobtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.The risk of not detecting a material misstatement resulting from fraud is higher than for oneresulting from error, as fraud may involve collusion, forgery, intentional omissions,misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose of expressingan opinion on the effectiveness of the Entity's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness ofaccounting estimates and related disclosures made by the Directors.

• Conclude on the appropriateness of the Directors' use of the going concern basis ofaccounting and, based on the audit evidence obtained, whether a material uncertainty existsrelated to events or conditions that may cast significant doubt on the Entity's ability tocontinue as a going concern. If we conclude that a material uncertainty exists, we arerequired to draw attention in our auditor's report to the related disclosures in the financialstatements or, if such disclosures are inadequate, to modify our opinion. Our conclusions arebased on the audit evidence obtained up to the date of our auditor's report. However, futureevents or conditions may cause the Entity to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the financial statements, includingthe disclosures, and whether the financial statements represent the underlying transactionsand events in a manner that achieves fair presentation.

4

Deloitte

We communicate with the directors regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

DELOITTE TOUCHE TOHMATSU

Stephen Roche Partner Chartered Accountants Melbourne, 28 March 2018

5

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

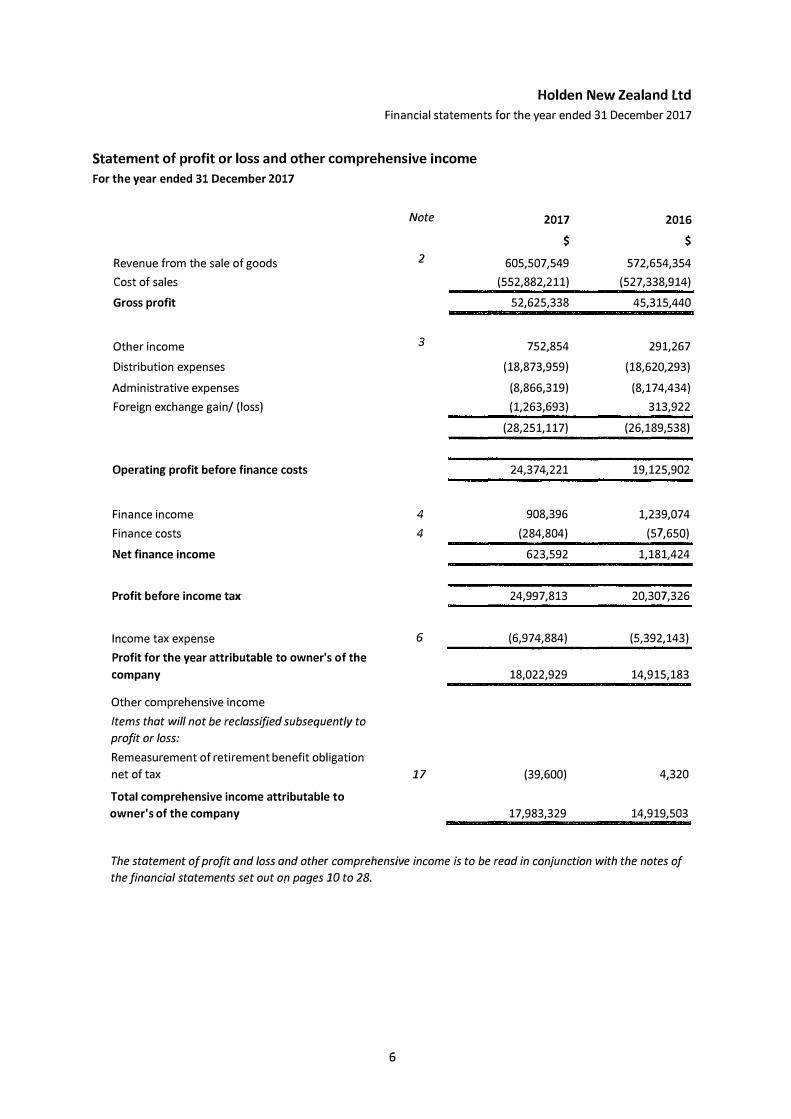

Statement of profit or loss and other comprehensive income

For the year ended 31 December 2017

Revenue from the sale of goods

Cost of sales

Gross profit

Other income

Distribution expenses

Administrative expenses

Foreign exchange gain/ (loss)

Operating profit before finance costs

Finance income

Finance costs

Net finance income

Profit before income tax

Note

2

3

4

4

Income tax expense 6

Profit for the year attributable to owner's of the

company

Other comprehensive income

Items that will not be reclassified subsequently to

profit or loss:

Remeasurement of retirement benefit obligation

net of tax

Total comprehensive income attributable to

owner's of the company

17

2017 2016

$ $

605,507,549 572,654,354

(552,882,211) (527,338,914)

52,625,338 45,315,440

752,854 291,267

(18,873,959) (18,620,293)

(8,866,319) (8,174,434)

(1,263,693) 313,922

(28,251,117) (26,189,538)

24,374,221 19,125,902

908,396 1,239,074

(284,804) (57,650)

623,592 1,181,424

24,997,813 20,307,326

(6,974,884) (5,392,143)

18,022,929 14,915,183

(39,600) 4,320

17,983,329 14,919,503

The statement of profit and loss and other comprehensive income is to be read in conjunction with the notes of

the financial statements set out on pages 10 to 28.

6

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

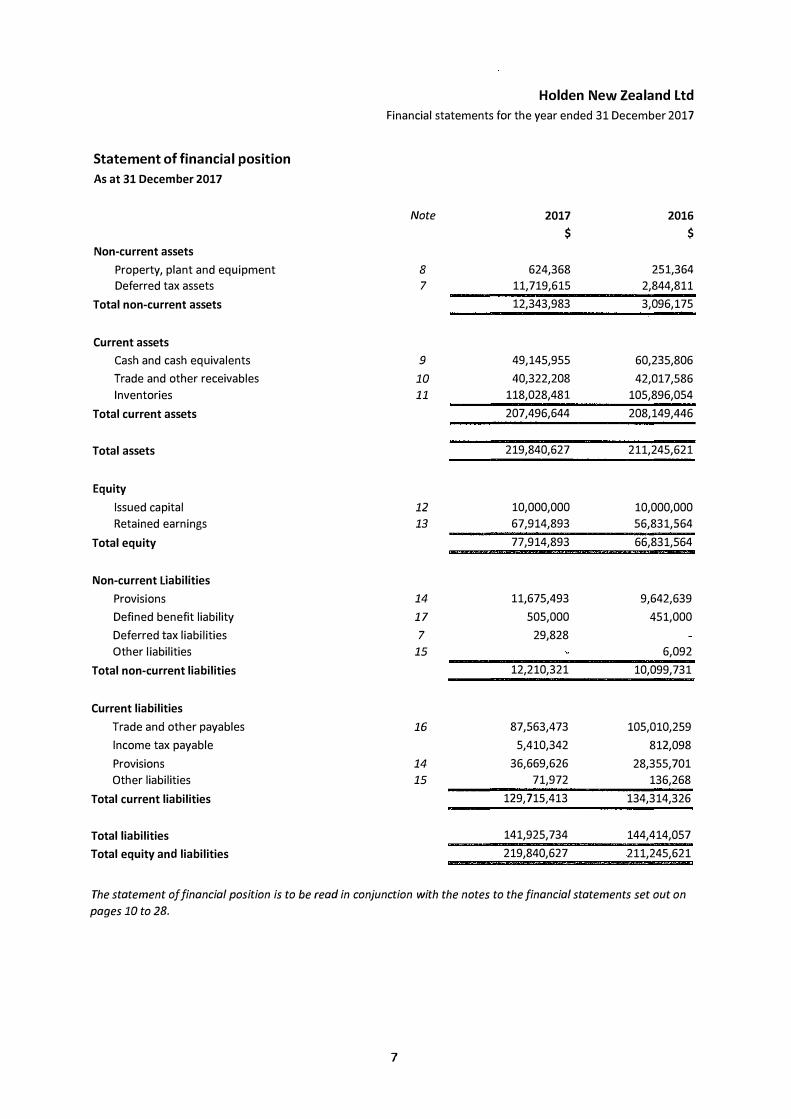

Statement of financial position

As at 31 December 2017

Note 2017 2016

$ $

Non-current assets

Property, plant and equipment 8 624,368 251,364

Deferred tax assets 7 11,719,615 2,844,811

Total non-current assets 12,343,983 3,096,175

Current assets

Cash and cash equivalents 9 49,145,955 60,235,806

Trade and other receivables 10 40,322,208 42,017,586

Inventories 11 118,028,481 105,896,054

Total current assets 207,496,644 208,149,446

Total assets 219,840,627 211,245,621

Equity

Issued capital 12 10,000,000 10,000,000

Retained earnings 13 67,914,893 56,831,564

Total equity 77,914,893 66,831,564

Non-current Liabilities

Provisions 14 11,675,493 9,642,639

Defined benefit liability 17 505,000 451,000

Deferred tax liabilities 7 29,828

Other liabilities 15 6,092

Total non-current liabilities 12,210,321 10,099,731

Current liabilities

Trade and other payables 16 87,563,473 105,010,259

Income tax payable 5,410,342 812,098

Provisions 14 36,669,626 28,355,701

Other liabilities 15 71,972 136,268

Total current liabilities 129,715,413 134,314,326

Total liabilities 141,925,734 144,414,057

Total equity and liabilities 219,840,627 211,245,621

The statement of financial position is to be read in conjunction with the notes to the financial statements set out on

pages 10 to 28.

7

Holden New Zealand ltd

Financial statements for the year ended 31 December 2017

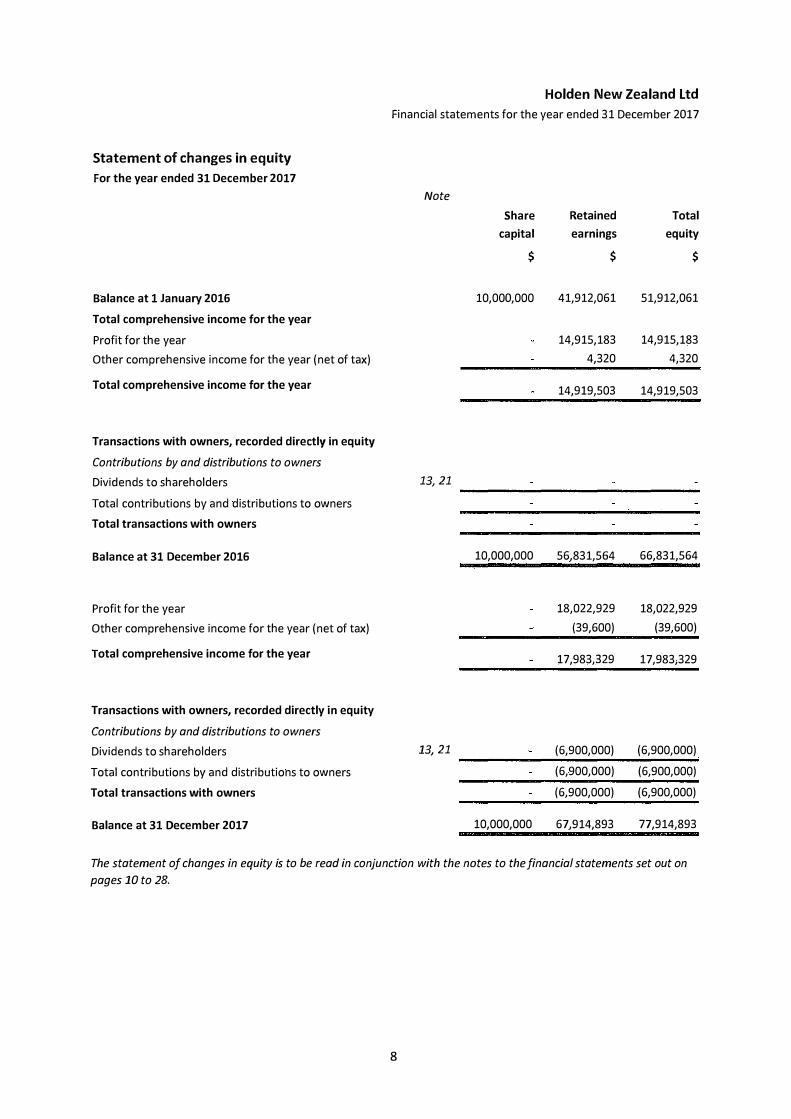

Statement of changes in equity

For the year ended 31 December 2017

Note

Share Retained Total

capital earnings equity

$ $ $

Balance at 1 January 2016 10,000,000 41,912,061 51,912,061

Total comprehensive income for the year

Profit for the year 14,915,183 14,915,183

Other comprehensive income for the year (net of tax) 4,320 4,320

Total comprehensive income for the year 14,919,503 14,919,503

Transactions with owners, recorded directly in equity

Contributions by and distributions to owners

Dividends to shareholders 13, 21

Total contributions by and distributions to owners

Total transactions with owners

Balance at 31 December 2016 10,000,000 56,831,564 66,831,564

Profit for the year 18,022,929 18,022,929

Other comprehensive income for the year (net of tax) (39,600) (39,600)

Total comprehensive income for the year 17,983,329 17,983,329

Transactions with owners, recorded directly in equity

Contributions by and distributions to owners

Dividends to shareholders 13, 21 (6,900,000) (6,900,000)

Total contributions by and distributions to owners (6,900,000) (6,900,000)

Total transactions with owners (6,900,000) (6,900,000)

Balance at 31 December 2017 10,000,000 67,914,893 77,914,893

The statement of changes in equity is to be read in conjunction with the notes to the financial statements set out on

pages 10 to 28.

8

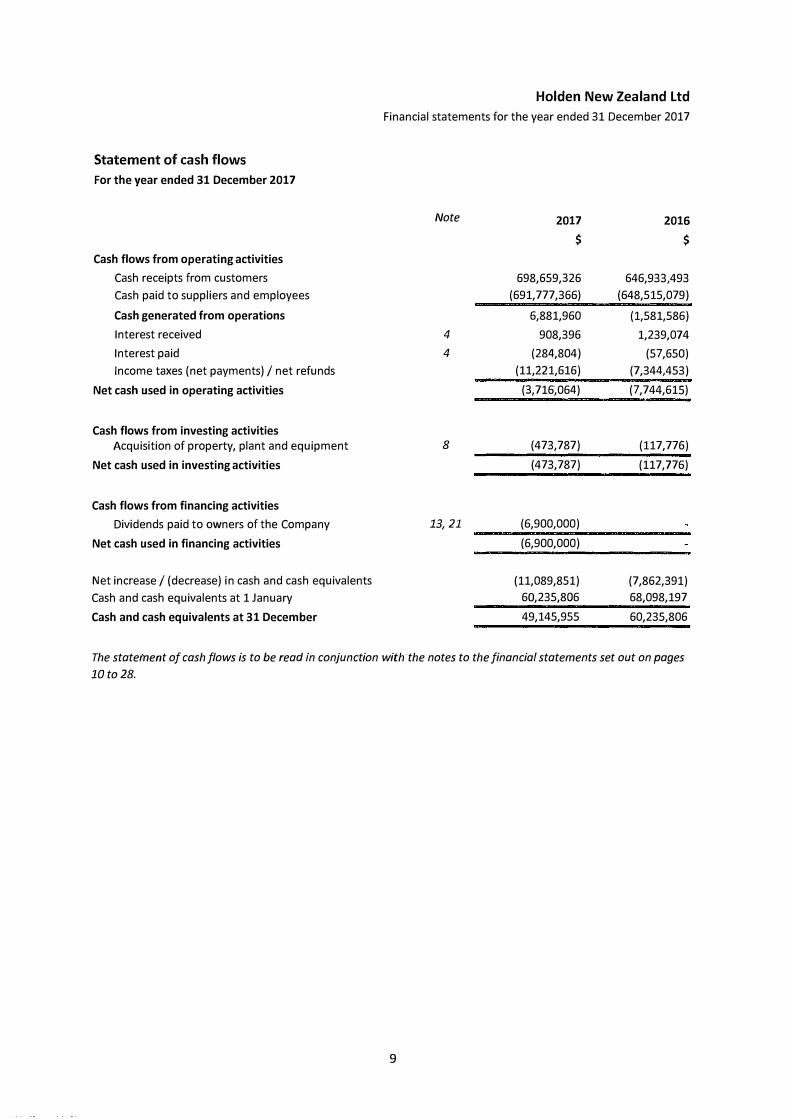

Statement of cash flows

For the year ended 31 December 2017

Cash flows from operating activities

Cash receipts from customers

Cash paid to suppliers and employees

Cash generated from operations

Interest received

Interest paid

Income taxes (net payments)/ net refunds

Net cash used in operating activities

Cash flows from investing activities

Acquisition of property, plant and equipment

Net cash used in investing activities

Cash flows from financing activities

Dividends paid to owners of the Company

Net cash used in financing activities

Net increase/ (decrease) in cash and cash equivalents

Cash and cash equivalents at 1 January

Cash and cash equivalents at 31 December

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Note

4

4

8

13, 21

2017

$

698,659,326

(691,777,366)

6,881,960

908,396

(284,804)

(11,221,616)

(3,716,064)

(473,787)

(473,787)

(6,900,000)

(6,900,000)

(11,089,851)

60,235,806

49,145,955

2016

$

646,933,493

(648,515,079)

(1,581,586)

1,239,074

(57,650)

(7,344,453)

(7,744,615)

(117,776)

(117,776)

(7,862,391)

68,098,197

60,235,806

The statement of cash flows is to be read in conjunction with the notes to the financial statements set out on pages

10to28.

9

Contents

Summary of accounting policies

Revenue

Other income

Net financing income

Superannuation expense

Income tax expense

Deferred tax balances

Property, plant and equipment

Cash and cash equivalents

Trade and other receivables

Inventories

Issued capital

Retained earnings and dividends

Provisions

Other liabilities

Trade and other payables

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Note

1

2

3

4

5

6

7

8

9

Defined benefit scheme - Holden New Zealand Pension Plan

Operating leases

10

11

12

13

14

15

16

17

18

19

20

21

22

23

Commitments

Contingencies

Related parties

Events after the reporting period

Company Directory

10

Notes to the financial statements

1. Summary of accounting policies

a) General information

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Holden New Zealand Ltd (the "Company") is a profit-oriented company domiciled in New Zealand, registered under

the Companies Act 1993. The immediate parent of the Company is GM Holding LLC and the ultimate parent of the

Company is General Motors Company.

b} Application of new standards

The Company is eligible for, and has prepared the financial statements in accordance with NZ International

Financial Reporting Standards Reduced Disclosure Regime (NZ IFRS (RDR)) for the period commencing 1 January

2017. The Company has taken advantage of a number of disclosure concessions; however there was no material

recognition or measurement impact on adoption of NZ IFRS (RDR).

In the current year, there are no new or revised NZ IFRS RDR issued by the External Reporting Board (XRB) that are

relevant to the Company, for an accounting period that begins on or after 1 January 2017.

Standards and interpretations in issue not yet adopted

IFRS 15 Revenue from Contracts with Customers IFRS 15 establishes a comprehensive framework for determining whether, how much, and when revenue is

recognised. It replaces existing revenue recognition guidance, including IAS 18 Revenue, IAS 11 Construction

contracts and IFRIC 13 Customer Loyalty Programmes. IFRS 15 is effective for annual reporting periods beginning

on or after 1 January 2018, with early adoption permitted.

IFRS 9 Financial Instruments

IFRS 9 Financial Instruments sets out requirements for recognising and measuring financial assets, financial

liabilities and some contracts to buy or sell non-financial items. This standard replaces IAS 39 Financial Instruments:

Recognition and Measurement. IFRS 9 is effective for annual reporting periods beginning on or after 1 January

2018, with early adoption permitted.

IFRS 16 Leases

IFRS 16 replaces existing leases guidance, including IAS 17 Leases, IFRIC 4 Determining whether an Arrangement

contains a Lease, SIC-15 Operating Leases - Incentives and SIC-27 Evaluating the Substance of Transactions

Involving the Legal Form of a Lease. The standard is effective for annual periods beginning on or after 1 January

2019. Early adoption is permitted for entities that apply IFRS 15 at or before the date of initial application of IFRS

16.

The Company has completed a preliminary assessment of the potential impact on its financial statements resulting

from the application of IFRS 15 and does not currently anticipate there to be a material impact on revenue

recognition on its adoption. For all other new standards, the directors are in the process of completing an

assessment of the impact of these new standards and interpretations.

11

Notes to the financial statements

1. Summary of accounting policies (continued)

c) Statement of compliance and reporting framework

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

The financial statements have been prepared in accordance with New Zealand generally accepted accounting

practice (NZ GAAP). For the purposes of complying with NZ GAAP, the Company is a for-profit entity. These financial

statements comply with New Zealand equivalents to International Financial Reporting Standards Reduced Disclosure

Regime (NZ IFRS (RDR)).

The Company qualifies for NZ IFRS (RDR) as it does not have public accountability and it is not a large for-profit

public sector entity. The Company has elected to apply NZ IFRS (RDR) and has applied disclosure concessions.

The financial statements have been prepared in accordance with the Companies Act 1993.

The financial statements were authorised for issue by the directors on 28 March 2018.

d} Basis of preparation

Historical Cost Convention

The financial statements have been prepared on the historical cost basis except for the defined benefit liability

which is measured as the difference between the present value of the defined benefit obligation and the fair value

of the plan assets.

Functional and presentation currency

These financial statements are presented in New Zealand dollars($), which is the Company's functional currency. All

amounts have been rounded to the nearest dollar.

e) Revenue recognition

Sale of goods Revenue from the sale of goods is recognised when the goods are delivered and titles have passed, at which time all

the following conditions are satisfied: • the Company has transferred to the buyer the significant risks and rewards of ownership of the goods;• the Company retains neither continuing managerial involvement to the degree usually associated with

ownership nor effective control over the goods sold;• the amount of revenue can be measured reliably;• it is probable that the economic benefits associated with the transaction will flow to the Company; and• the costs incurred or to be incurred in respect of the transaction can be measured reliably.

Interest income Interest income from a financial asset is recognised when it is probable that the economic benefits will flow to the

Company and the amount of income can be measured reliably. Interest income is accrued on a time basis, by

reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly

discounts estimated future cash receipts through the expected life of the financial asset to that asset's net carrying

amount on initial recognition.

12

Notes to the financial statements

1. Summary of accounting policies (continued)

/) Leasing

Holden New Zealand ltd

Financial statements for the year ended 31 December 2017

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards

of ownership to the lessee. All other leases are classified as operating leases.

The Company as lessee Operating lease payments are recognised as an expense on a straight-line basis over the lease term, except where

another systematic basis is more representative of the time pattern in which economic benefits from the leased

asset are consumed. Contingent rentals arising under operating leases are recognised as an expense in the period in

which they are incurred.

In the event that lease incentives are received to enter into operating leases, such incentives are recognised as a

liability. The aggregate benefit of incentives is recognised as a reduction of rental expense on a straight-line basis,

except where another systematic basis is more representative of the time pattern in which economic benefits from

the leased asset are consumed.

g) Foreign currency

The financial statements of the Company are presented in the currency of the primary economic environment in

which the entity operates (its functional currency). For the purpose of the financial statements, the results and

financial position of the Company are expressed in New Zealand dollars ('$'), which is the functional currency of the

Company and the presentation currency for the financial statements.

In preparing the financial statements, transactions in currencies other than the entity's functional currency (foreign

currencies) are recognised at the rates of exchange prevailing at the dates of the transactions. At the end of each

reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at that

date. Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the

rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of

historical cost in a foreign currency are not retranslated.

Exchange differences are recognised in profit or loss in the period in which they arise.

h) Employee benefits

Retirement benefit costs and termination benefits Payments to defined contribution retirement benefit plans are recognised as an expense when employees have

rendered service entitling them to the contributions.

For defined benefit retirement benefit plans, the cost of providing benefits is determined using the projected unit

credit method, with actuarial valuations being carried out at the end of each annual reporting period. Re

measurement, comprising actuarial gains and losses, the effect of the changes to the asset ceiling (if applicable) and

the return on plan assets (excluding interest), is reflected immediately in the statement of financial position with a

charge or credit recognised in other comprehensive income in the period in which they occur. Re-measurement

recognised in other comprehensive income is reflected immediately in retained earnings and will not be reclassified

to profit or loss. Past service cost is recognised in profit or loss in the period of a plan amendment. Net interest is

calculated by applying the discount rate at the beginning of the period to the net defined benefit liability or asset.

Defined benefit costs are categorised as follows:

• service cost (including current service cost, past service cost, as well as gains and losses on curtailments and

settlements);• net interest expense or income; and• remeasurement.

13

Notes to the financial statements

1. Summary of accounting policies (continued)

h) Employee benefits (continued)

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Retirement benefit costs and termination benefits (continued) The retirement benefit obligation recognised in the statement of financial position represents the actual deficit or

surplus in the Company's defined benefit plan. Any surplus resulting from this calculation is limited to the present

value of any economic benefits available in the form of refunds from the plan or reductions in future contributions

to the plan.

A liability for a termination benefit is recognised at the earlier of when the Company can no longer withdraw the

offer of the termination benefit and when the Company recognises any related restructuring costs.

Short-term and other long-term employee benefits A liability is recognised for benefits accruing to employees in respect of wages and salaries, annual leave and sick

leave in the period the related service is rendered at the undiscounted amount of the benefits expected to be paid in

exchange for that service.

Liabilities recognised in respect of short-term employee benefits, are measured at the undiscounted amount of the

benefits expected to be paid in exchange for the related service.

Liabilities recognised in respect of long term employee benefits are measured as the present value of the estimated

future cash outflows to be made by the Company in respect of services provided by employees up to reporting date.

i) Taxation

Income tax expense represents the sum of the tax currently payable and deferred tax.

Current tax

The tax currently payable is based on taxable profit for the year. Taxable profit differs from profit before tax as

reported in the statement of profit or loss and other comprehensive income because of items of income or expense

that are taxable or deductible in other years and items that are never taxable or deductible. The Company's current

tax is calculated using tax rates that have been enacted or substantively enacted by the end of the reporting period.

Deferred tax Deferred tax is recognised on temporary differences between the carrying amounts of assets and liabilities in the

financial statements and the corresponding tax bases used in the computation of taxable profit. Deferred tax

liabilities are generally recognised for all taxable temporary differences. Deferred tax assets are generally recognised

for all deductible temporary differences to the extent that it is probable that taxable profits will be available against

which those deductible temporary differences can be utilised. Such deferred tax assets and liabilities are not

recognised if the temporary difference arises from goodwill or from the initial recognition (other than in a business

combination) of other assets and liabilities in a transaction that affects neither the taxable profit nor the accounting

profit.

The carrying amount of deferred tax assets is reviewed at the end of each reporting period and reduced to the

extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to

be recovered.

14

Notes to the financial statements

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

1. Summary of accounting policies (continued)

i) Taxation (continued)

Deferred tax (continued) Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the period in which the

liability is settled or the asset realised, based on tax rates (and tax laws) that have been enacted or substantively

enacted by the end of the reporting period.

The measurement of deferred tax liabilities and assets reflects the tax consequences that would follow from the

manner in which the Company expects to recover or settle the carrying amount of its assets and liabilities.

Current and deferred tax for the period

Current and deferred tax are recognised in profit or loss, except when they relate to items that are recognised in

other comprehensive income or directly in equity, in which case, the current and deferred tax are also recognised in

other comprehensive income or directly in equity, respectively. Where current or deferred tax arises from the initial

accounting for a business combination, the tax effect is included in the accounting for the business combination.

j) Goods and services tax

Revenue, expenses, assets and liabilities are recognised net of the amount of goods and services tax (GST) except:

• where the amount of GST incurred is not recovered from the taxation authority, it is recognised as part of the

cost of acquisition of an asset or as part of an item of expense; or• for receivables and payables which are recognised inclusive of GST. (The net amount of GST recoverable from

or payable to the taxation authority is included as part of receivables or payables).• cash flows included in the statement of cash flows are on a gross basis.

k) Property, plant and equipment

All items of property, plant and equipment are stated at cost less accumulated depreciation and accumulated

impairment losses.

Depreciation is recognised so as to write off the cost or valuation of assets less their residual values over their useful

lives, using the straight-line method. The estimated useful lives, residual values and depreciation method are

reviewed at the end of each reporting period, with the effect of any changes in estimate accounted for on a

prospective basis. The following useful lives are used in the calculation of depreciation:

• Furniture and office equipment 3 - 30 years

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are

expected to arise from the continued use of the asset. Any gain or loss arising on the disposal or retirement of an

item of property, plant and equipment is determined as the difference between the sales proceeds and the carrying

amount of the asset and is recognised in profit or loss.

15

Notes to the financial statements

1. Summary of accounting policies (continued)

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

I} Impairment of tangible and intangible assets excluding goodwill

At the end of each reporting period, the Company reviews the carrying amounts of its tangible and intangible assets

to determine whether there is any indication that those assets have suffered an impairment loss. If any such

indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the

impairment loss (if any).

When it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the

recoverable amount of the cash-generating unit to which the asset belongs. When a reasonable and consistent basis

of allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise

they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation

basis can be identified.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the

estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current

market assessments of the time value of money and the risks specific to the asset for which the estimates of future

cash flows have not been adjusted.

If the recoverable amount of an asset (or cash-generating unit) is estimated to be less than its carrying amount, the

carrying amount of the asset (or cash-generating unit) is reduced to its recoverable amount. An impairment loss is

recognised immediately in profit or loss.

Where an impairment loss subsequently reversed, the carrying amount of the asset (or cash-generating unit) is

increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not

exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset

(or cash-generating unit) in prior years. A reversal of an impairment loss is recognised immediately in profit or loss.

m) Inventories

Inventories are stated at the lower of cost and net realisable value. Net realisable value is the estimated selling price

in the ordinary course of business, less the estimated costs of completion (if applicable) and selling expenses.

Cost is based on the weighted average cost of stock purchased and includes expenditure incurred in acquiring the

inventories and bringing them to their existing location and condition.

n) Provisions

Provisions are recognised when the Company has a present obligation (legal or constructive) as a result of a past

event, it is probable that the Company will be required to settle the obligation, and a reliable estimate can be made

of the amount of the obligation.

The amount recognised as a provision is the best estimate of the consideration required to settle the present

obligation at the end of the reporting period, taking into account the risks and uncertainties surrounding the

obligation. When a provision is measured using the cash flows estimated to settle the present obligation, its carrying

amount is the present value of those cash flows (where the effect of the time value of money is material).

16

Notes to the financial statements

1. Summary of accounting policies (continued)

n) Provisions (continued)

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third

party, a receivable is recognised as an asset if it is virtually certain that reimbursement will be received and the

amount of the receivable can be measured reliably.

Warranties Provisions for the expected cost of warranty obligations under local sale of goods legislation are recognised at the

date of sale of the relevant products, at the directors' best estimate of the expenditure required to settle the

Company's obligation.

o) Non-derivative financial instruments

Financial assets and financial liabilities are recognised when the Company becomes a party to the contractual

provisions of the instruments.

Financial assets and financial liabilities are initially measured at fair value. Transaction costs that are directly

attributable to the acquisition or issue of financial assets and financial liabilities (other than financial assets and

financial liabilities at fair value through profit or loss) are added to or deducted from the fair value of the financial

assets or financial liabilities, as appropriate, on initial recognition. Transaction costs directly attributable to the

acquisition of financial assets or financial liabilities at fair value through profit or loss are recognised immediately in

profit or loss.

The Company derecognises a financial asset when contractual rights to the cash flows from the financial assets

expire or if the Company transfers the financial asset to another party without retaining control or substantially all

risks and rewards of the asset. Financial liabilities are derecognised if the Company's obligations specified in the

contract expire or are discharged or cancelled.

p) Non-derivative financial assets

Non-derivative financial assets are classified into the following specified categories: financial assets 'at fair value

through profit or loss' (FVTPL), 'held-to-maturity' investments, 'available-for-sale' (AFS) financial assets and 'loans

and receivables'. The classification depends on the nature and purpose of the financial assets and is determined at

the time of initial recognition.

Cash and cash equivalents For the purpose of presentation in the statement of cash flows, cash and cash equivalents includes cash on hand,

deposits held at call with financial institutions, other short-term, highly liquid investments with original maturities of

three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant

risk of changes in value and bank overdrafts (if any). Bank overdrafts are shown within borrowings in current

liabilities in the balance sheet.

17

Notes to the financial statements

1. Summary of accounting policies (continued)

p) Non-derivative financial assets (continued)

Loans and receivables

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in

an active market. Loans and receivables are measured at amortised cost using the effective interest method, less any

impairment. Interest income is recognised by applying the effective interest rate, except for short-term receivables

when the effect of discounting is immaterial.

q) Non-derivative financial liabilities

Financial liabilities are classified as either financial liabilities 'at FVTPL' or 'other financial liabilities'.

Other financial liabilities Other financial liabilities (including trade and other payables) are subsequently measured at amortised cost using the

effective interest method.

r) Impairment of financial assets

Financial assets, other than those at FVTPL, are assessed for indicators of impairment at each reporting date.

Financial assets are impaired where there is objective evidence that, as a result of one or more events that occurred

after the initial recognition of the financial asset, the estimated future cash flows of the investment have been

affected.

For certain categories of financial assets, such as trade receivables, assets are assessed for impairment on a

collective basis even if they were assessed not to be impaired individually. Objective evidence of impairment for a

portfolio of receivables could include the Company's past experience of collecting payments, an increase in the

number of delayed payments in the portfolio past the average credit period of 11 days, as well as observable

changes in national or local economic conditions that correlate with default on receivables.

For financial assets carried at amortised cost, the amount of the impairment is the difference between the asset's

carrying amount and the present value of the estimated future cash flows, discounted at the original effective

interest rate.

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the

exception of trade receivables where the carrying amount is reduced through the use of an allowance account.

When a trade receivable is uncollectible, it is written off against the allowance account. Changes in the carrying

amount of the allowance account are recognised in profit or loss.

For financial assets measured at amortised cost, if, in a subsequent period, the amount of the impairment loss

decreases and the decrease can be related objectively to an event occurring after the impairment loss was

recognised, the previously recognised impairment loss is reversed through profit or loss to the extent that the

carrying amount of the investment at the date the impairment is reversed does not exceed what the amortised cost

would have been had the impairment not been recognised.

18

Notes to the financial statements

1. Summary of accounting policies (continued)

Holden New Zealand ltd

Financial statements for the year ended 31 December 2017

s) Critical accounting judgements and key sources of estimation uncertainty

In the application of the Company's accounting policies, which are described above, the directors are required to

make judgements, estimates and assumptions about the carrying amounts of assets and liabilities that are not

readily apparent from other sources. The estimates and associated assumptions are based on historical experience

and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are

recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of

the revision and future periods if the revision affects both current and future periods.

The areas involving significant estimates or judgements are:

Warranties and sales allowances The Company recognises the estimated costs of providing Warranty services and Sales and Marketing. Refer note

l(n) and note 14 of the financial statements for details of the accounting treatment for these provisions.

Defined benefit obligation

A liability or asset in respect of defined benefit superannuation plans is recognised in the statement of financial

position, and is measured as the present value of the defined benefit obligation determined according to the

projected unit credit method at the reporting date less the fair value of the superannuation fund's assets at the date.

The present value of the defined benefit obligation is based on expected future payments which arise from

membership of the fund to the reporting date, calculated annually by independent actuaries. Consideration is given

to the expected future wage and salary levels, experience of employee departures and periods of service.

Expected future payments are discounted using pre-tax market yields at the reporting date on corporate bonds with

terms to maturity that match, as closely as possible, the estimated future cash outflows. Actuarial gains and losses

arising from experience adjustments and changes in actuarial assumptions are charged or credited to the other

comprehensive income. Refer note 17 of the financial statements for details of the key assumptions used in

determining the accounting for these plans. The main categories of assumptions used are the discount rate and

future salary increases and those applied in determining the fair value of plan assets at the measurement date.

The assumptions made have a significant impact on the calculations and any adjustments arising therefrom. Changes

in these assumptions and other external factors, including fair values of plan assets, could result in possible future

changes to the amount of the pension obligations recognised in the balance sheet.

Employee Benefits The Company recognises liabilities with respect to short-term employee benefits. Refer note l(h) of the financial

statements for details of the accounting treatment for Employee Benefits.

19

Notes to the financial statements

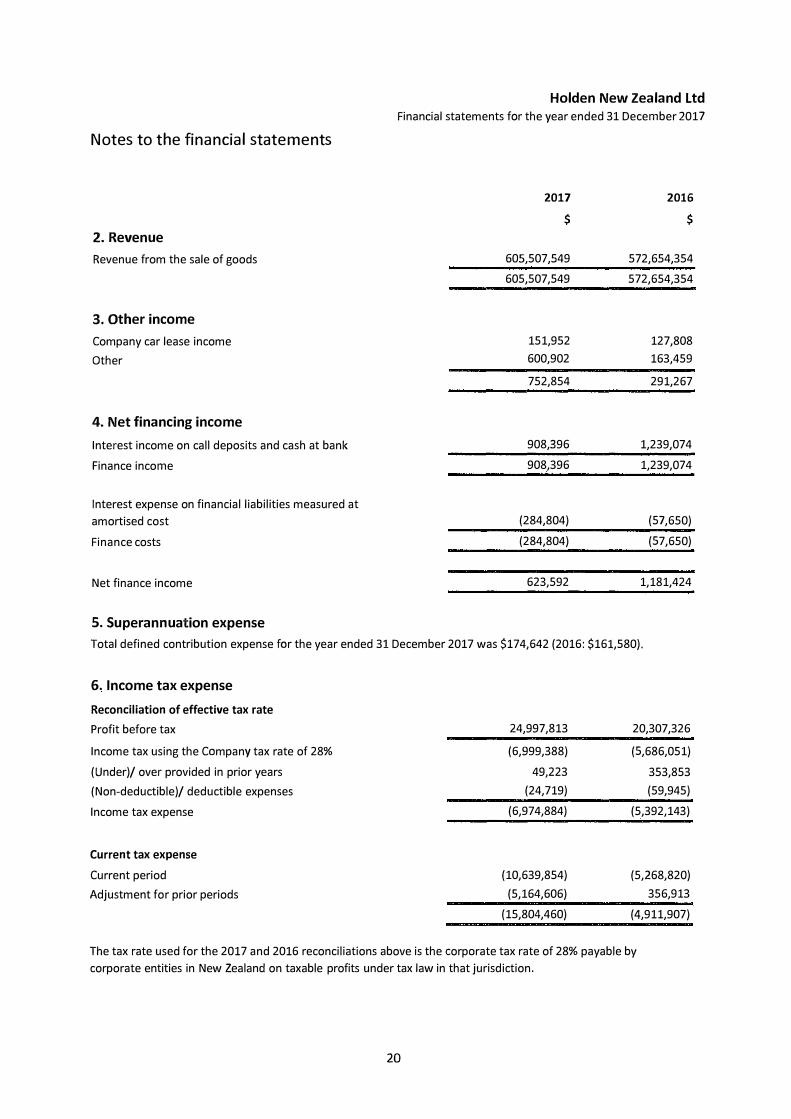

2.Revenue

Revenue from the sale of goods

3. Other income

Company car lease income

Other

4. Net financing income

Interest income on call deposits and cash at bank

Finance income

Interest expense on financial liabilities measured at

amortised cost

Finance costs

Net finance income

5. Superannuation expense

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

2017 2016

$ $

605,507,549 572,654,354

605,507,549 572,654,354

151,952 127,808

600,902 163,459

752,854 291,267

908,396 1,239,074

908,396 1,239,074

(284,804) (57,650)

(284,804) (57,650)

623,592 1,181,424

Total defined contribution expense for the year ended 31 December 2017 was $174,642 (2016: $161,580).

6. Income tax expense

Reconciliation of effective tax rate

Profit before tax

Income tax using the Company tax rate of 28%

(Under)/ over provided in prior years

(Non-deductible)/ deductible expenses

Income tax expense

Current tax expense

Current period

Adjustment for prior periods

24,997,813

(6,999,388)

49,223

(24,719)

(6,974,884)

(10,639,854)

(5,164,606)

(15,804,460)

20,307,326

(5,686,051)

353,853

(59,945)

(5,392,143)

(5,268,820)

356,913

(4,911,907)

The tax rate used for the 2017 and 2016 reconciliations above is the corporate tax rate of 28% payable by

corporate entities in New Zealand on taxable profits under tax law in that jurisdiction.

20

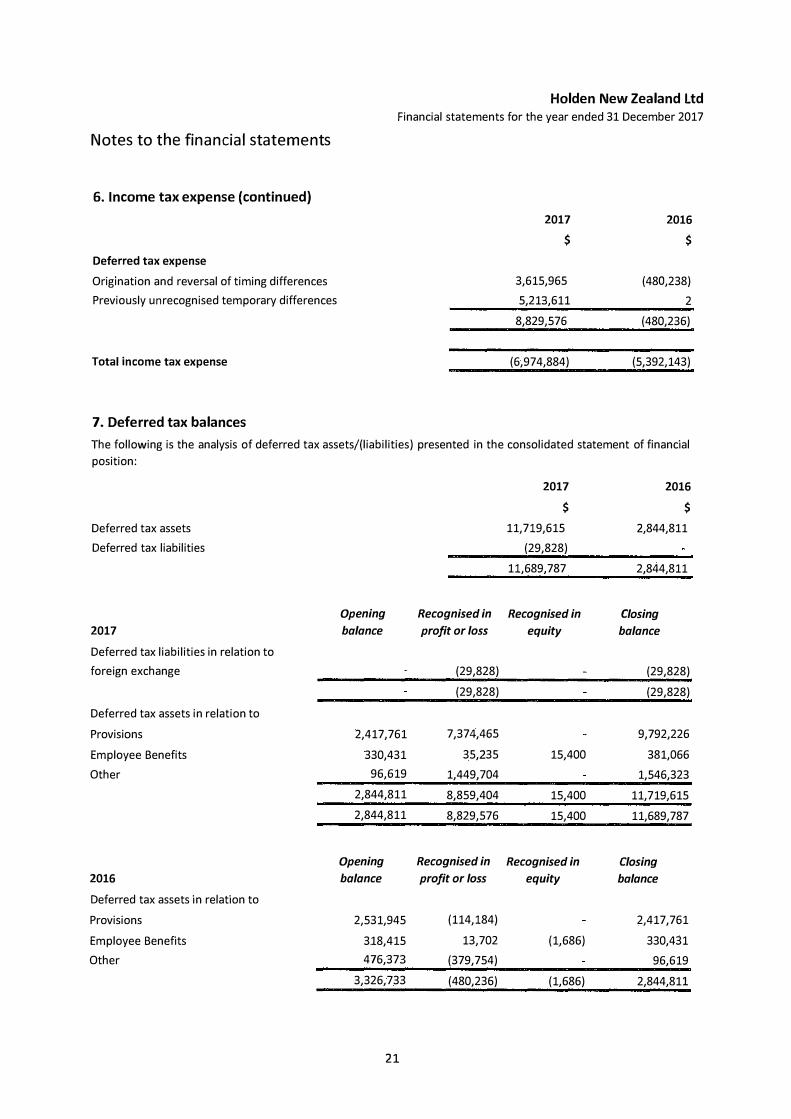

Notes to the financial statements

6. Income tax expense (continued)

Deferred tax expense

Origination and reversal of timing differences

Previously unrecognised temporary differences

Total income tax expense

7. Deferred tax balances

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

2017 2016

$ $

3,615,965 (480,238)

5,213,611 2

8,829,576 (480,236)

(6,974,884) (5,392,143)

The following is the analysis of deferred tax assets/(liabilities) presented in the consolidated statement of financial

position:

2017 2016

$ $

Deferred tax assets 11,719,615 2,844,811

Deferred tax liabilities (29,828)

11,689,787 2,844,811

Opening Recognised in Recognised in Closing

2017 balance profit or loss equity balance

Deferred tax liabilities in relation to

foreign exchange (29,828) (29,828)

(29,828) (29,828)

Deferred tax assets in relation to

Provisions 2,417,761 7,374,465 9,792,226

Employee Benefits 330,431 35,235 15,400 381,066

Other 96,619 1,449,704 1,546,323

2,844,811 8,859,404 15,400 11,719,615

2,844,811 8,829,576 15,400 11,689,787

Opening Recognised in Recognised in Closing

2016 balance profit or loss equity balance

Deferred tax assets in relation to

Provisions 2,531,945 (114,184) 2,417,761

Employee Benefits 318,415 13,702 (1,686) 330,431

Other 476,373 (379,754) 96,619

3,326,733 (480,236) (1,686) 2,844,811

21

Notes to the financial statements

8. Property, plant and equipment

Cost

Balance at 1 January 2016

Additions

Balance at 31 December 2016

Additions

Disposals

Balance at 31 December 2017

Depreciation

Balance at 1 January 2016

Depreciation expense

Balance at 31 December 2016

Depreciation expense

Disposals

Balance at 31 December 2017

Net book value

As at 31 December 2016

As at 31 December 2017

9. Cash and cash equivalents

Cash at bank

Call deposits - Treasury Centre

10. Trade and other receivables

Trade receivables - related parties

Trade receivables

Allowance for doubtful debts

Movement in the allowance for doubtful debts

Balance at the beginning of the year

Amounts written off during the year as uncollectible

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Furniture and office

equipment$ Total$

1,601,371 1,601,371

117,776 117,776

1,719,147 1,719,147

473,787 473,787

(900,099) (900,099)

1,292,835 1,292,835

(1,401,870) (1,401,870)

(65,913) (65,913)

(1,467,783) (1,467,783)

(82,453) (82,453)

881,769 881,769

(668,467) (668,467)

251,364 251,364

624,368 624,368

2017 2016

$ $

23,841,627 58,873,193

25,304,328 1,362,613

49,145,955 60,235,806

112,220 75,376

40,345,132 41,991,907

(135,144) (49,697)

40,322,208 42,017,586

49,697 214,787

(39) (17)

Increase/ (decrease) in allowance recognised in profit and loss 85,486 (165,073)

135,144 49,697

22

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Notes to the financial statements

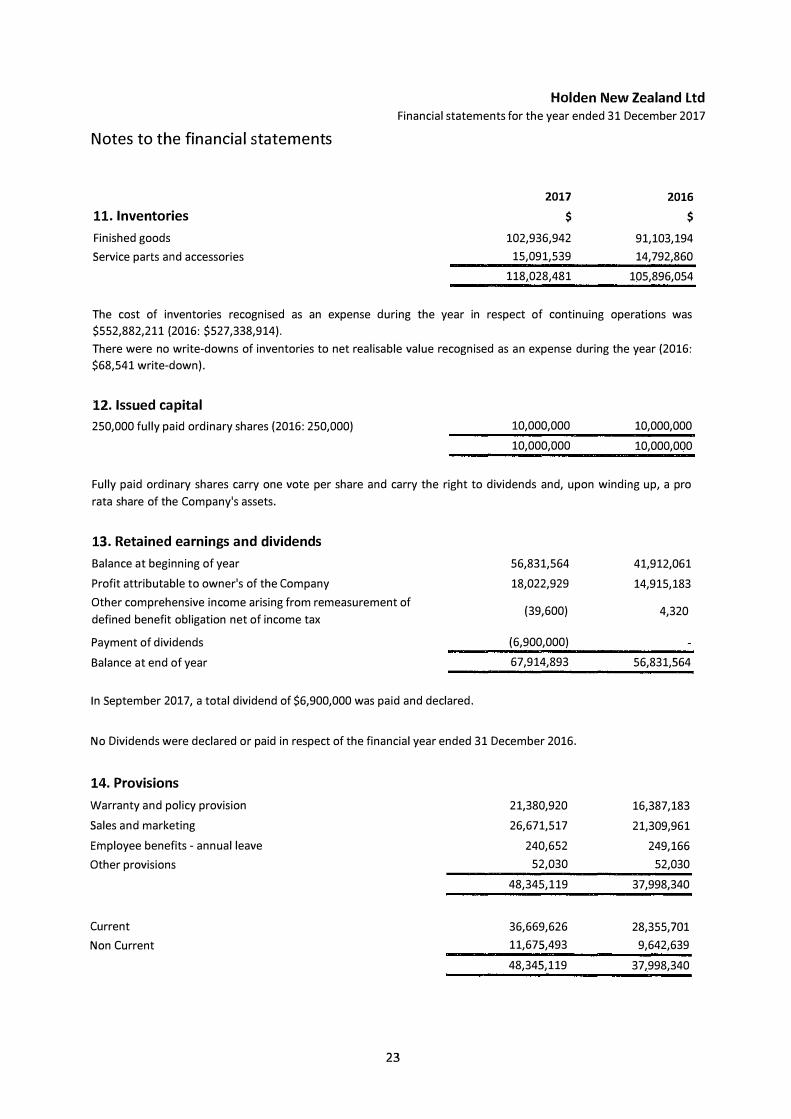

11. Inventories

Finished goods

Service parts and accessories

2017

$

102,936,942

15,091,539

118,028,481

2016

$

91,103,194

14,792,860

105,896,054

The cost of inventories recognised as an expense during the year in respect of continuing operations was $552,882,211 {2016: $527,338,914).

There were no write-downs of inventories to net realisable value recognised as an expense during the year {2016: $68,541 write-down).

12. Issued capital

250,000 fully paid ordinary shares (2016: 250,000) 10,000,000 10,000,000

10,000,000 10,000,000

Fully paid ordinary shares carry one vote per share and carry the right to dividends and, upon winding up, a pro

rata share of the Company's assets.

13. Retained earnings and dividends

Balance at beginning of year

Profit attributable to owner's of the Company

Other comprehensive income arising from remeasurement of

defined benefit obligation net of income tax

Payment of dividends

Balance at end of year

In September 2017, a total dividend of $6,900,000 was paid and declared.

56,831,564

18,022,929

(39,600)

(6,900,000)

67,914,893

No Dividends were declared or paid in respect of the financial year ended 31 December 2016.

14. Provisions

Warranty and policy provision

Sales and marketing

Employee benefits - annual leave

Other provisions

Current

Non Current

23

21,380,920

26,671,517

240,652

52,030

48,345,119

36,669,626

11,675,493

48,345,119

41,912,061

14,915,183

4,320

56,831,564

16,387,183

21,309,961

249,166

52,030

37,998,340

28,355,701

9,642,639

37,998,340

Notes to the financial statements

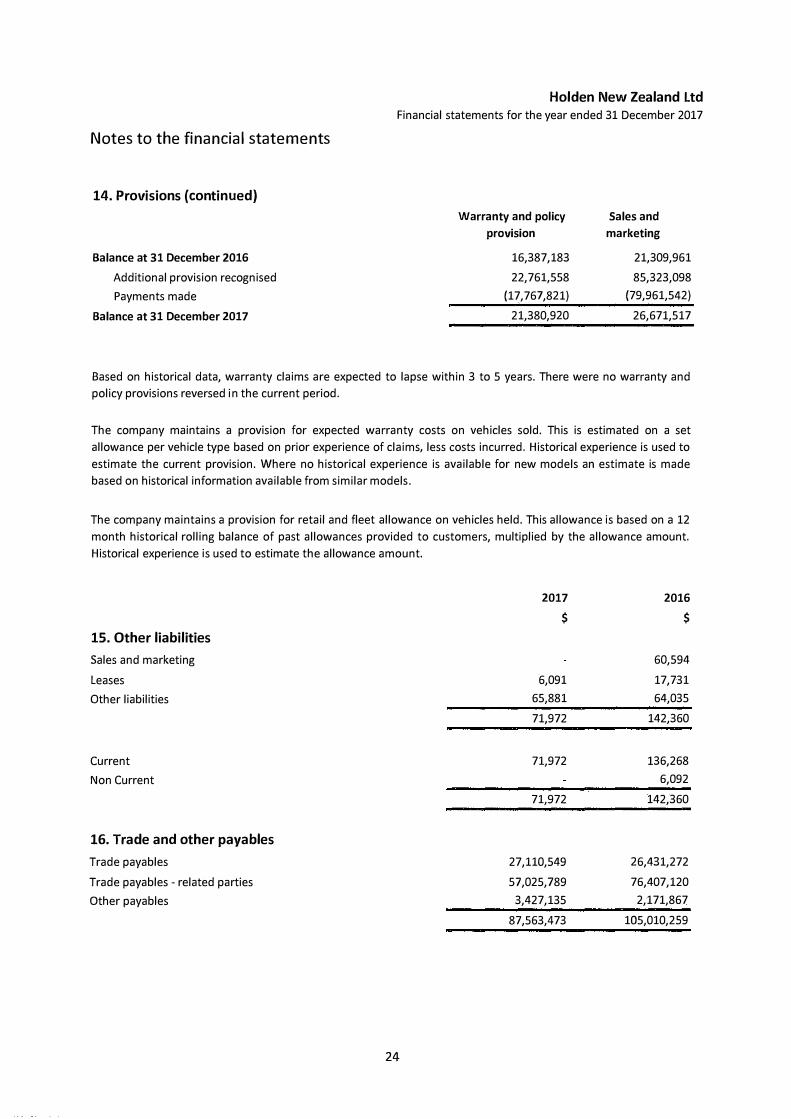

14. Provisions (continued)

Balance at 31 December 2016

Additional provision recognised

Payments made

Balance at 31 December 2017

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Warranty and policy

provision

16,387,183

22,761,558

(17,767,821)

21,380,920

Sales and

marketing

21,309,961

85,323,098

(79,961,542)

26,671,517

Based on historical data, warranty claims are expected to lapse within 3 to 5 years. There were no warranty and

policy provisions reversed in the current period.

The company maintains a provision for expected warranty costs on vehicles sold. This is estimated on a set

allowance per vehicle type based on prior experience of claims, less costs incurred. Historical experience is used to

estimate the current provision. Where no historical experience is available for new models an estimate is made

based on historical information available from similar models.

The company maintains a provision for retail and fleet allowance on vehicles held. This allowance is based on a 12

month historical rolling balance of past allowances provided to customers, multiplied by the allowance amount.

Historical experience is used to estimate the allowance amount.

2017 2016

$ $

15. Other liabilities

Sales and marketing 60,594

Leases 6,091 17,731

Other liabilities 65,881 64,035

71,972 142,360

Current 71,972 136,268

Non Current 6,092

71,972 142,360

16. Trade and other payables

Trade payables 27,110,549 26,431,272

Trade payables - related parties 57,025,789 76,407,120

Other payables 3,427,135 2,171,867

87,563,473 105,010,259

24

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Notes to the financial statements

17. Defined benefit scheme - Holden New Zealand Pension Plan

Plan Information

The majority of the active members have cash accumulation benefits with a lump sum payable on retirement. The

remaining active members have the option of a pension payable on retirement. The scheme is classified and

accounted for as a defined benefit plan. The plan has a large number of pensioners.

The plan in New Zealand typically expose the Company to actuarial risks such as: investment risk, mortality risk and

legislative risk.

Investment risk - The risk that investment returns will be lower than assumed and the Company will need to

increase contributions to offset this shortfall.

Mortality risk - The risk that the members of the Plan will live longer than assumed, increasing the number of

pension payments and thereby requiring additional contributions.

Legislative risk - The risk that legislative changes could be made which increase the cost of providing the

defined benefits.

The risk relating to benefits to be paid to the dependents of plan members (widow and orphan benefits) is

reinsured by an external insurance company. No other post-retirement benefits are provided to these employees.

The most recent actuarial valuation of the plan assets and the present value of the defined benefit obligation were

carried out at 31 December 2017 by Mercer. The present value of the defined benefit obligation, and the related

current service cost and past service cost, were measured using the projected unit credit method.

The principal assumptions used for the purposes of the actuarial valuations were as follows.

Discount rate(s)

Average longevity at retirement age for :

Life expectancy at age 80 of a pensioner currently aged 80*

Males

Females

Life expectancy at age 80 of a pensioner currently aged 65*

Males

Females

* Based on Mercer's standard mortality table.

25

Valuation at

2017

2.70%

9.9

11.1

11.3

12.1

2016

3.40%

9.8

11.1

11.2

12.1

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

Notes to the financial statements

17. Defined benefit scheme - Holden New Zealand Pension Plan (continued}

The remeasurement of the net defined benefit liability is included in other comprehensive income.

The amount included in the statement of financial position arising from the entity's obligation in respect of its defined benefit plans is as follows:

2017

$

Present value of funded defined benefit obligation 4,186,000 Fair value of plan assets 3,848,000

Deficit 338,000

Contributions tax 167,000

Net liability arising from defined benefit obligation 505,000

Amounts recognised in comprehensive income in respect of these defined benefit plans are:

Benefits paid (585,000)

Contributions from the employer

Contributions from plan participants

33,000

33,000

The fair value of the plan assets at the end of the reporting period for each category, are as follows:

Australasian equity 808,080

International equity 885,040

Fixed income 1,000,480

Property 423,280 Cash 731,120

3,848,000

The actual return on plan assets less interest income was $245,000 (2016: $106,000).

18. Operating leases

2016

$

4,311,000 4,009,000

302,000

149,000

451,000

(638,000)

37,000

38,000

841,890

922,070

1,082,430

481,080 681,530

4,009,000

Operating leases relate to leases of buildings and IT equipment with lease terms of 7 years and 3 years respectively. The Company does not have an option to purchase the leased building at the expiry of the lease period and the lease is cancellable subject to a termination fee. The Company does have an option to purchase the leased IT equipment at the expiry of the lease periods and the lease is non-cancellable.

2017 2016

$ $

Not later than 1 year 1,431,307 1,382,938

Later than 1 year and not later than 5 years 5,231,742 5,382,568 Later than 5 years 591,524

6,663,049 7,357,030

Total lease expense for the year ended 31 December 2017 was $1,336,990 (2016: $1,302,173).

26

Holden New Zealand ltd

Financial statements for the year ended 31 December 2017

Notes to the financial statements

19. Commitments

There were no commitments for capital expenditure at 31 December 2017 (2016: $Nil).

20. Contingencies

Contingent liabilities as at 31 December 2017 were $Nil (2016: $Nil).

21. Related parties

The Company has a related party relationship with other group entities, and its key management personnel which

are its directors and executive officers. Transactions with other group entities include the purchase of motor

vehicles and motor vehicle parts and accessories. Transactions with key management personnel include

remuneration and fees. The remuneration of directors and other members of key management personnel during

the year was $2,047,560 (2016: $1,596,315).

Total call deposits held with GM Global Treasury Centre Ltd (GMGTC) at year end is $25,304,328 (2016:

$1,362,613) which are separately disclosed on note 9 of the financial statements. Total interest received during the

year in relation to call deposits held with GMGTC and GM European Treasury Centre (GMETC) is $355,975 (2016:

GMETC $964,506) . No related party debts were written off or forgiven during the year (2016: $Nil).

Transactions during the year:

Dividends to parent entity (note 13)

Purchase of goods from other related parties

Management fee

Outstanding balances:

Payables

Receivables

2017

$

6,900,000

436,920,231

344,526

57,025,789

112,220

57,138,009

No interest is charged on the payables and receivables. The average payment period is 47 days.

22. Events after the reporting period

2016

$

421,845,350

446,168

76,407,120

75,376

76,482,496

At the end of February 2018, the Australian Government issued a compulsory recall for all vehicles with defective

Takata airbags, following a safety investigation by the Australian Competition and Consumer Commission (ACCC)

that uncovered a design defect in some airbags. Following on from this, Holden New Zealand will be looking at

issuing a voluntary recall notice for affected vehicles in April/May 2018. Preliminary estimates are that the recall

will cost approximately $4.0M.

27

Notes to the financial statements

23. Company Directory

REGISTERED OFFICE

2/118 Savill Drive Mangere East, Auckland 2024

New Zealand

COMPANY NUMBER

1602

Tax number: 10-164-494

AUDITOR

Deloitte Touche Tohmatsu, Australia

SOLICITORS

Minter Ellison

Holden New Zealand Ltd

Financial statements for the year ended 31 December 2017

DIRECTORS

K. Aquilina

J. Thorley

M. Samphier (appointed 4 January 2017)

BANKERS

Westpac New Zealand Ltd

28