Embed Size (px)

Citation preview

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

ADMINISTRATIVE

Notice 2018–10, page 359.This notice provides guidance relating to the excise tax onmedical devices imposed by § 4191. Specifically, this noticeprovides temporary relief, for the first three calendar quartersof 2018, to medical device manufacturers, producers andimporters from the failure to deposit penalties imposed by§ 6656, where the taxpayer demonstrates good faith.

REG–118067–17, page 360.This document contains proposed regulations implementingsection 1101 of the Bipartisan Budget Act of 2015, which wasenacted into law on November 2, 2015. The Bipartisan BudgetAct repeals the current rules governing partnership audits andreplaces them with a new centralized partnership audit regimethat, in general, determines, assesses and collects tax at thepartnership level. These proposed regulations provide rulesaddressing how partnerships and their partners adjust taxattributes to take into account partnership adjustments underthe centralized partnership audit regime.

EXCISE TAX

Notice 2018–10, page 359.This notice provides guidance relating to the excise tax onmedical devices imposed by § 4191. Specifically, this noticeprovides temporary relief, for the first three calendar quartersof 2018, to medical device manufacturers, producers andimporters from the failure to deposit penalties imposed by§ 6656, where the taxpayer demonstrates good faith.

Finding Lists begin on page ii.

Bulletin No. 2018–8February 20, 2018

The IRS MissionProvide America’s taxpayers top-quality service by helpingthem understand and meet their tax responsibilities and en-force the law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument ofthe Commissioner of Internal Revenue for announcing officialrulings and procedures of the Internal Revenue Service and forpublishing Treasury Decisions, Executive Orders, Tax Conven-tions, legislation, court decisions, and other items of generalinterest. It is published weekly.

It is the policy of the Service to publish in the Bulletin allsubstantive rulings necessary to promote a uniform applicationof the tax laws, including all rulings that supersede, revoke,modify, or amend any of those previously published in theBulletin. All published rulings apply retroactively unless other-wise indicated. Procedures relating solely to matters of internalmanagement are not published; however, statements of inter-nal practices and procedures that affect the rights and dutiesof taxpayers are published.

Revenue rulings represent the conclusions of the Service onthe application of the law to the pivotal facts stated in therevenue ruling. In those based on positions taken in rulings totaxpayers or technical advice to Service field offices, identify-ing details and information of a confidential nature are deletedto prevent unwarranted invasions of privacy and to comply withstatutory requirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not berelied on, used, or cited as precedents by Service personnel inthe disposition of other cases. In applying published rulings andprocedures, the effect of subsequent legislation, regulations,court decisions, rulings, and procedures must be considered,and Service personnel and others concerned are cautioned

against reaching the same conclusions in other cases unlessthe facts and circumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A, TaxConventions and Other Related Items, and Subpart B, Legisla-tion and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to thesesubjects are contained in the other Parts and Subparts. Alsoincluded in this part are Bank Secrecy Act Administrative Rul-ings. Bank Secrecy Act Administrative Rulings are issued bythe Department of the Treasury’s Office of the Assistant Sec-retary (Enforcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The last Bulletin for each month includes a cumulative index forthe matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the last Bulletin of each semiannual period.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

February 20, 2018 Bulletin No. 2018–8

Part III. Administrative, Procedural, and MiscellaneousMedical Device Excise TaxDeposit Penalty Relief

Notice 2018–10

SECTION 1. PURPOSE

This notice provides guidance relatingto the excise tax on medical devices im-posed by § 4191 (the “medical deviceexcise tax”) of the Internal Revenue Code(the “Code”). Specifically, this notice pro-vides temporary relief to medical devicemanufacturers from the failure to depositpenalties imposed by § 6656.

SECTION 2. BACKGROUND

Section 4191 imposes a 2.3% excisetax on the sale of certain medical devicesby the manufacturer.

Section 174 of the Protecting Ameri-cans from Tax Hikes Act of 2015, enactedas part of the Consolidated AppropriationsAct, 2016, Division Q, Pub. L. 114–113,129 Stat. 2242, 3071 (December 18, 2015)(jointly, the Act), established a two-yearmoratorium on the medical device excisetax for the period that began on January 1,2016, and ended on December 31, 2017.Thus, sales of taxable medical devicesduring the moratorium period were notsubject to tax. Absent further legislativeaction, the medical device excise tax ap-plies to sales of taxable medical deviceson and after January 1, 2018.

The medical device excise tax is codifiedin subtitle D, chapter 32 of the Code (“chap-ter 32”), which pertains to excise taxes im-posed on the sale or use of taxable articlesby manufacturers, producers, and importers.Chapter 32 taxes, including the medical de-vice excise tax, are reported on Form 720,Quarterly Federal Excise Tax Return. See§§ 40.6011(a)–1(a)(1) and 40.0–1(a).

Section 6302 of the Code authorizesthe IRS to establish the mode and time forcollecting certain taxes, including thetaxes imposed by chapter 32. Section40.6302(c)–1(a)(1) of the Excise Tax Pro-cedural Regulations requires each personthat is required to file Form 720 to makedeposits of tax for each semimonthly pe-riod in which the tax liability is incurred.A semimonthly period is the first 15 days

of a calendar month or the portion of acalendar month following the 15th day ofthe month. See § 40.0–1(c).

The deposit for a tax imposed by chap-ter 32 for each semimonthly period mustnot be less than 95% of the amount of nettax liability incurred during the semi-monthly period unless the safe harbor in§ 40.6302(c)–1(b)(2)(ii) or (iii) applies.See § 40.6302(c)–1(b)(1). Under the safeharbor, any person that filed a Form 720reporting a tax imposed by chapter 32 forthe second preceding calendar quarter (thelook-back quarter) is considered to havemet the semimonthly deposit requirementfor the current quarter if: (i) the deposit foreach semimonthly period in the current cal-endar quarter is not less than 1/6 of the nettax liability reported for the look-back quar-ter; (ii) each deposit is made on time; (iii)the amount of any underpayment is paid bythe due date of the return; and (iv) the per-son’s liability does not include any tax thatwas not imposed during the look-back quar-ter. Section 40.6302(c)–1(b)(2)(v) providesthat if a person fails to make deposits asrequired, the IRS may withdraw the per-son’s right to use the safe harbor rules of§ 40.6302(c)–1(b)(2).

Section 6656 imposes a penalty in thecase of any failure by any person to maketimely deposits as required by § 6302. Ataxpayer may avoid penalties under § 6656for failure to make deposits of taxes if thetaxpayer makes an affirmative showing thatsuch failure is due to reasonable cause andnot due to willful neglect. See § 6656 andthe corresponding regulations.

SECTION 3. DEPOSIT PENALTYRELIEF

(a) Overview. With the end of the mor-atorium on the medical device excise tax,taxpayers are required to resume makingsemimonthly deposits of tax. The first de-posit, covering the first 15 days of January,is due by January 29, 2018. In considerationof the short time frame between the end ofthe moratorium period and the due date ofthe first deposit and in the interest of soundtax administration, the IRS and the TreasuryDepartment have decided to provide tempo-rary relief from the § 6656 penalty for thefirst three calendar quarters of 2018, as de-

scribed below. The normal rules under§ 6656 and the corresponding regulationswill apply with respect to deposits due dur-ing the fourth calendar quarter of 2018 andthereafter.

Beginning in the third calendar quarter of2018, medical device manufacturers mayuse the safe harbor rules of § 40.6302(c)–1(b)(2) for semimonthly deposits due duringthat quarter. For purposes of the safe harbor,the first calendar quarter of 2018 is the look-back quarter for deposits due during thethird calendar quarter.

(b) Relief. (i) During the first three cal-endar quarters of 2018, the IRS will notimpose the penalty provided in § 6656 on ataxpayer liable for the medical device excisetax that fails to make timely deposits of themedical device excise tax as required by§§ 40.6302(c)–1 and 40.6302(c)–2 (relatingto special deposits required in September),provided that the taxpayer demonstrates agood faith attempt to comply with require-ments of §§ 40.6302(c)–1 and 40.6302(c)–2and that the failure was not due to willfulneglect. Thereafter, a taxpayer may avoidpenalties if it makes an affirmative showingthat the failure to deposit is due to reason-able cause and not due to willful neglect.

(ii) During the third and fourth calen-dar quarters of 2018, the IRS will notexercise its authority under § 40.6302(c)–1(b)(2)(v) to withdraw the taxpayer’sright to use the deposit safe harbor rules of§ 40.6302(c)–1(b)(2) due to a failure tomake deposits as required, provided thetaxpayer satisfies the requirements of thefirst sentence of paragraph (b)(i) of thissection for the look-back quarter at issue.

SECTION 4. EFFECTIVE DATE

This notice is effective on and afterJanuary 1, 2018.

SECTION 5. DRAFTINGINFORMATION

The principal author of this notice isNatalie Payne of the Office of AssociateChief Counsel (Passthroughs & SpecialIndustries). For further information re-garding this notice, please contact Ms.Payne at (202) 317-6855 (not a toll-freenumber).

Bulletin No. 2018–8 February 20, 2018359

Part IV. Items of General InterestCentralized PartnershipAudit Regime: AdjustingTax Attributes

REG–118067–17

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Notice of proposed rulemaking.

SUMMARY: This document containsproposed regulations implementing sec-tion 1101 of the Bipartisan Budget Act of2015, which was enacted into law on No-vember 2, 2015. The Bipartisan BudgetAct repeals the current rules governingpartnership audits and replaces them witha new centralized partnership audit regimethat, in general, determines, assesses andcollects tax at the partnership level. Theseproposed regulations provide rules ad-dressing how partnerships and their part-ners adjust tax attributes to take into ac-count partnership adjustments under thecentralized partnership audit regime.

DATES: Written or electronic commentsand requests for a public hearing must bereceived by May 3, 2018.

ADDRESSES: Send submissions to: CC:PA:LPD:PR (REG–118067–17), Room5207, Internal Revenue Service, P.O.Box 7604, Ben Franklin Station, Wash-ington, DC 20044. Submissions may behand delivered Monday through Fridaybetween the hours of 8:00 a.m. and 4:00p.m. to CC:PA:LPD:PR (REG–118067–17), Courier’s Desk, Internal RevenueService, 1111 Constitution Avenue,NW, Washington, DC 20224. Alterna-tively, taxpayers may submit commentselectronically via the Federal eRulemak-ing Portal at http://www.regulations.gov(REG–118067–17).

FOR FURTHER INFORMATION CON-TACT: Concerning the proposed regula-tions, Allison R. Carmody or Meghan M.Howard of the Office of Associate ChiefCounsel (Passthroughs and Special Indus-tries), (202) 317-5279; concerning thesubmission of comments, Regina L.Johnson, (202) 317-6901 (not toll-freenumbers).

SUPPLEMENTARY INFORMATION:

Background

This document contains proposed reg-ulations that supplement the regulationsproposed in the notice of proposed rule-making (REG–136118–15) published inthe Federal Register on June 14, 2017(82 FR 27334) (the “June 14 NPRM”) andamend the Income Tax Regulations (26CFR part 1) under Subpart – Partners andPartnerships and the Procedure and Ad-ministration Regulations (26 CFR part301) under Subpart – Tax Treatment ofPartnership Items to implement the cen-tralized partnership audit regime. Further-more, certain provisions of the June 14NPRM are being amended.

1. The New Centralized PartnershipAudit Regime

For information relating to (1) thenew centralized partnership audit re-gime enacted by the Bipartisan BudgetAct (BBA), Pub. L. 114 –74 (129 Stat.58 (2015)) (as amended by the Protect-ing Americans from Tax Hikes Act of2015, Pub. L. 114 –113 (129 Stat. 2242(2015)); (2) Notice 2016 –23 (2016 –13I.R.B. 490 (March 28, 2016)), whichrequested comments on the new partner-ship audit regime enacted by the BBA;and (3) the temporary regulations (TD9780, 81 FR 51795 (August 5, 2016))and a notice of proposed rulemaking(REG–105005–16, 81 FR 51835 (Au-gust 5, 2016)), which provided the time,form, and manner for a partnership tomake an election into the centralizedpartnership audit regime for a partner-ship taxable year beginning before thegeneral effective date of the regime, seethe Background section of the June 14NPRM.

2. Proposed Regulations Implementingthe Centralized Partnership AuditRegime

The June 14 NPRM addressed variousissues concerning the scope and processof the new centralized partnership auditregime. Unless otherwise noted, all refer-ences to proposed regulations in this pre-

amble refer to the regulations proposed bythe June 14 NPRM.

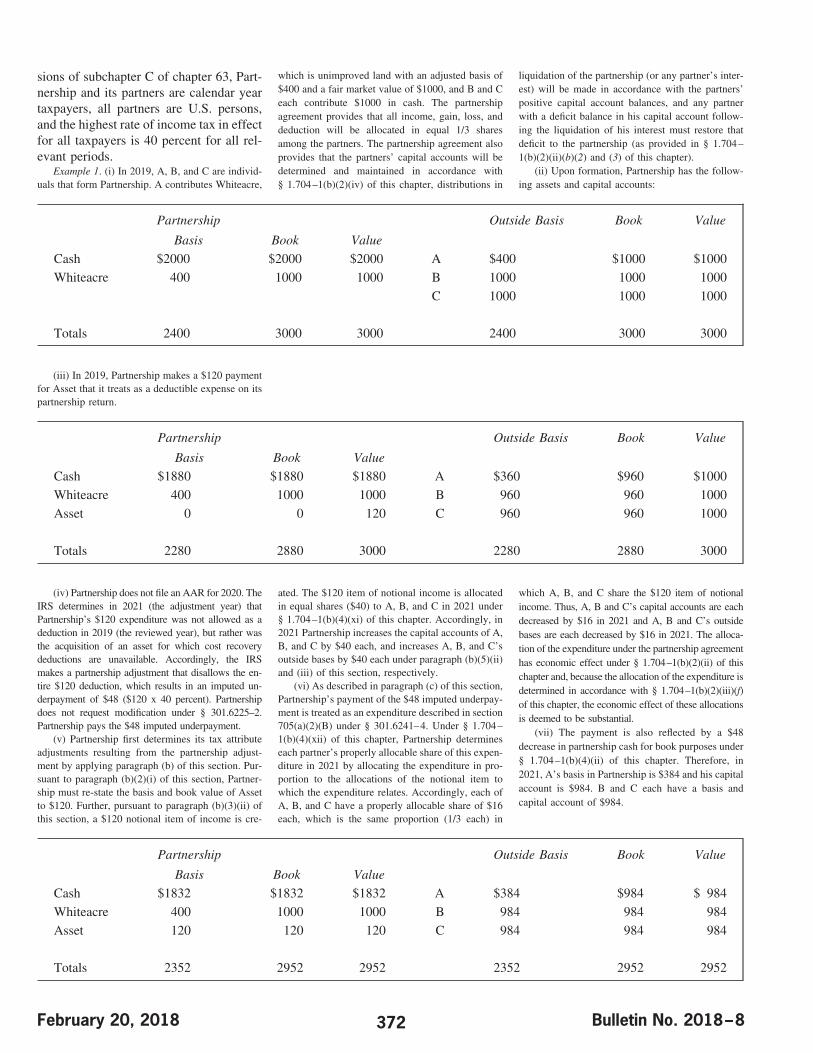

Proposed §§ 301.6225–1, 301.6225–2,and 301.6225–3 provide rules relating topartnership adjustments, including thecomputation of the imputed underpay-ment, modification of the imputed under-payment, and the treatment of adjustmentsthat do not result in an imputed underpay-ment.

Proposed § 301.6225–1 sets forth rulesfor computing the imputed underpayment,and proposed § 301.6225–2 sets forth therules under which the partnership mayrequest a modification to adjust the im-puted underpayment calculated under pro-posed § 301.6225–1. The modificationrules contained in proposed § 301.6225–2generally allow: (1) Modifications that re-sult in the exclusion of certain adjust-ments, or portions thereof, from the cal-culation of the imputed underpayment(such as a modification under proposed§ 301.6225–2(d)(2) (amended returns bypartners), (d)(3) (tax-exempt partners),(d)(5) (certain passive losses of publiclytraded partnerships), (d)(7) (partnershipswith partners that are qualified investmententities described in section 860 of theInternal Revenue Code (Code)), (d)(8)(partner closing agreements), and, if ap-plicable, (d)(9) (other modifications)); (2)rate modifications, which affect only thetaxable rate applied to the total nettedpartnership adjustment (described in pro-posed § 301.6225–2(d)(4)); and (3) mod-ifications to the number and compositionof imputed underpayments (described inproposed § 301.6225–2(d)(6)).

Proposed § 301.6225–3 sets forth rulesfor the treatment of adjustments that do notresult in an imputed underpayment. In gen-eral, pursuant to proposed § 301.6225–3(b)(1) the partnership takes the adjustmentinto account in the adjustment year as areduction in non-separately stated income oras an increase in non-separately stated lossdepending on whether the adjustment is toan item of income or loss. Proposed§ 301.6225–3(b)(2) provides that if an ad-justment is to an item that is required to beseparately stated under section 702 of theInternal Revenue Code (Code) the adjust-ment shall be taken into account by thepartnership on its adjustment year return as

February 20, 2018 Bulletin No. 2018–8360

an adjustment to such separately stated item.Proposed § 301.6225–3(b)(3) provides thatan adjustment to a credit is taken into ac-count as a separately stated item.

Proposed §§ 301.6226–1, 301.6226–2,and 301.6226–3 provide rules relating tothe election under section 6226 by a part-nership to have its reviewed year partnerstake into account the partnership adjust-ments in lieu of paying the imputed un-derpayment determined under section6225, the statements the partnership mustsend to its partners, and the rules for howthe partners take into account the adjust-ments, including the computation andpayment of the partners’ liability. If apartnership makes the election under sec-tion 6226 to “push out” adjustments to itsreviewed year partners, the partnership isnot liable for the imputed underpayment.Instead, under proposed § 301.6226–3,reviewed year partners must pay any ad-ditional chapter 1 tax that results fromtaking the adjustments reflected on thestatements into account in the reviewedyear and from changes to the tax attributesin the intervening years. In addition tobeing liable for the additional tax, thepartner must also calculate and pay anypenalties, additions to tax, or additionalamounts determined to be applicable dur-ing the partnership–level proceeding, andany interest determined in accordancewith proposed § 301.6226–3(d).

Finally, proposed § 301.6241–1 pro-vides definitions for purposes of the cen-tralized partnership audit regime.

On December 19, 2017, proposed rules(REG–120232–17 and REG–120233–17)were published in the Federal Register(82 FR 60144) that would allow tieredpartnerships to push out audit adjustmentsthrough to the ultimate taxpayers and pro-vides rules implementing the proceduraland administrative aspects of the partner-ship audit regime. For proposed rules re-garding international provisions under thecentralized partnership audit regime, see(REG–119337–17) published in the Fed-eral Register on November 30, 2017 (82FR 56765).

Explanation of Provisions

1. In General

These proposed regulations providerules that were reserved in the June 14

NPRM under proposed §§ 301.6225–4and 301.6226–4. It also provides relatedproposed amendments to §§ 1.704–1,1.705–1, and 1.706–4. Specifically, theserules address how and when partnershipsand their partners adjust tax attributes totake into account partnership adjustmentsunder both sections 6225 and 6226. Thepublic provided comments in response tothe June 14 NPRM, and some commentsdiscussed issues relevant to the reservedsections under proposed §§ 301.6225–4and 301.6226–4, which were taken intoconsideration in drafting these proposedregulations.

Because these regulations are supple-menting the regulations published in theJune 14 NPRM, the numbering and order-ing of some of the provisions do not fol-low typical conventions. The Departmentof the Treasury (Treasury Department)and the IRS anticipate that these provi-sions will be appropriately integratedwhen both these regulations and the pro-posed regulations in the June 14 NPRMare finalized.

These proposed rules are consistentwith the policy described in “The GeneralExplanation of Tax Legislation Enactedfor 2015” (Bluebook), which explainedthat “[u]nder the centralized partnershipaudit regime, the flowthrough nature ofthe partnership under subchapter K of theCode is unchanged, but the partnership istreated as a point of collection of under-payments that would otherwise be the re-sponsibility of partners.” Joint Comm. onTaxation, JCS-1–16, “General Explana-tions of Tax Legislation Enacted in 2015,”57 (2016).

The preamble to the June 14 NPRMannounced that the Treasury Departmentand the IRS intended to provide additionalrules providing for adjustments to the ba-sis of partnership property and book valueof any partnership property if the partner-ship adjustment is a change to an item ofgain, loss, amortization or depreciation(i.e., the change is basis derivative). Theseproposed regulations, when finalized, willprovide this guidance.

2. Provisions Relating to Section 6225

A. In general

The June 14 NPRM defines a partnershipadjustment as any adjustment to any item

of income, gain, loss, deduction, or creditof a partnership (as defined in proposed§ 301.6221(a)–1(b)(1)), or any partner’s dis-tributive share thereof (as described in pro-posed § 301.6221(a)–1(b)(2)). See proposed§ 301.6241–1(a)(6). Under the rules in pro-posed § 301.6225–1, each partnership ad-justment is either (i) taken into account inthe determination of an imputed underpay-ment, or (ii) considered a partnership adjust-ment that does not give rise to an imputedunderpayment. For a partnership adjustmentthat is taken into account in the determina-tion of the imputed underpayment, theseproposed regulations provide rules for ad-justing partnership asset basis and bookvalue, rules for the creation of notionalitems, rules for allocating these notionalitems under section 704(b), successor rulesfor situations in which reviewed year part-ners (as defined in proposed § 301.6241–1(a)(9)) are not adjustment year partners (asdefined in proposed § 301.6241–1(a)(2)),and rules for determining the impact of no-tional items on tax attributes in certain situ-ations. See section (2)(B) of this preamble.These regulations also provide rules for theallocation of any partnership expenditure re-lated to the imputed underpayment. See sec-tion (2)(B)(vii) of this preamble. Finally,these regulations provide guidance in thecase of a partnership adjustment that doesnot give rise to an imputed underpayment.See section (2)(C) of this preamble.

B. Adjustments in the case of apartnership adjustment that results in animputed underpayment

i. In General

Prior to the enactment of the central-ized partnership audit regime, in the caseof an adjustment to an item of income,gain, loss, deduction or credit in the con-text of an examination by the IRS for orrelated to a partnership, partnership ad-justments were generally taken into ac-count by the partners of the partnershipfor the year under examination by a newor corrected allocation of the relevantitem, and partners took those items intoaccount with respect to the partnershipyear under examination. In contrast, underthe centralized partnership audit regime,for a partnership adjustment that is takeninto account in the determination of an

Bulletin No. 2018–8 February 20, 2018361

imputed underpayment, the partnershipadjustment is generally taken into accountby the partnership in the year in which therelated payment obligation (the imputedunderpayment) arises. Further, in light ofthe fact that these partnership adjustmentsare with respect to a partnership year thatis earlier than the year in which the im-puted underpayment arises, the partners ofthe partnership may have changed in thelater year.

Under subchapter K, a partnership gen-erally computes items of income, gain,loss, deduction or credit under section703, which are then allocated to the part-ners under section 704. Under section705, a partner increases its basis in itspartnership interest (outside basis) by itsdistributive share of taxable income of thepartnership as determined under section703(a). However, in the case of a positivepartnership adjustment that is taken intoaccount in the determination of an im-puted underpayment, section 6225 doesnot itself provide for an item of taxableincome under section 703(a) to be allo-cated to partners. Instead, calculations aremade at the partnership level and the part-nership pays the liability in the form of animputed underpayment. Failure to provideadjustments to outside basis that reflectthe partnership adjustments that resultedin the imputed underpayment could leadto a partner being effectively taxed twiceon the same item of income, once indi-rectly on payment of the imputed under-payment and again on a disposition of thepartnership interest or on a distribution ofcash by the partnership. Taxing the sameitem of income twice is not consistentwith the flowthrough nature of partner-ships under subchapter K. Thus, theseproposed regulations provide for adjust-ment to a partner’s basis in its interest -and certain other tax attributes that areinterdependent with basis under subchap-ter K - in order to prevent effective doubletaxation or other distortions.

Specifically, under proposed § 301.6225–4(a)(1), when there is a partnership adjust-ment (as defined in proposed § 301.6241–1(a)(6)), the partnership and its adjustmentyear partners (as defined in proposed§ 301.6241–1(a)(2)) generally must adjusttheir specified tax attributes (as defined inproposed § 301.6225–4(a)(2)). Specifiedtax attributes are the tax basis and book

value of a partnership’s property, amountsdetermined under section 704(c), adjust-ment year partners’ bases in their partner-ship interests, and adjustment year partners’capital accounts determined and maintainedin accordance with § 1.704–1(b)(2). Seeproposed § 301.6225–4(a)(2).

In the case of a partnership adjustmentthat results in an imputed underpayment, theadjustments to specified tax attributes mustbe made on a partnership-adjustment-by-partnership-adjustment basis, and thus arecreated separately for each partnership ad-justment (whether a negative adjustment ora positive adjustment) without regard totheir summation as part of the determinationof the total netted partnership adjustment inproposed § 301.6225–1(c)(3). See proposed§ 301.6225–4(b)(1).

ii. Manner of Adjusting Specified TaxAttributes

The partnership must first make appro-priate adjustments to the book value andbasis of property to take into accountany partnership adjustment. See proposed§ 301.6225–4(b)(2). This rule also re-quires amounts determined under section704(c) to be adjusted to take into accountthe partnership adjustment. The partner-ship does not make any adjustments to thebook value or basis of partnership prop-erty with respect to property that was heldby the partnership in the reviewed yearbut is no longer held by the partnership inthe adjustment year. Comments are re-quested as to whether, in these situations,a partnership should be allowed to adjustthe basis (or book value) of other partner-ship property (such as in a manner similarto the rules that apply in allocating section734(b) adjustments under section 755(i.e., § 1.755–1(c)).

Proposed § 301.6225–4(b)(3) providesthat notional items are then created withrespect to the partnership adjustment, andthese notional items are then allocated ac-cording to the rules described in section(2)(B)(iii) of this preamble. The items areconsidered notional items because theirsole purpose is to affect partner-levelspecified tax attributes, and thus they arenot considered to be items for purposes ofadjusting other tax attributes.

In the case of a partnership adjustmentthat is an increase to income or gain, a

notional item of income or gain is createdin an amount equal to the partnership ad-justment. Similarly, in the case of a part-nership adjustment that is an increase toan expense or a loss, a notional item ofexpense or loss is created in an amountequal to the partnership adjustment. Seeproposed § 301.6225–4(b)(3)(ii) and (iii).

However, in the case of a partnershipadjustment that is a decrease to income orgain, a notional item of expense or loss iscreated in an amount equal to the partner-ship adjustment. Similarly, in the case of apartnership adjustment that is a decreaseto an expense or a loss, a notional item ofincome or gain is created in an amountequal to the partnership adjustment. Seeproposed § 301.6225–4(b)(3)(iv) and (v).These rules have the effect of reversingout the reviewed year allocation to theextent necessary to reflect the partnershipadjustment.

Thus, under these proposed regulations,an adjustment year partner increases its out-side basis for notional income that is allo-cated to it. Similarly, a partnership that de-termines and maintains capital accounts inaccordance with § 1.704–1(b)(2)(iv) alsoadjusts capital accounts for notional items.See proposed § 301.6225–4(e), Example 1.In the case of a partnership adjustment thatreflects a net increase or net decrease incredits as determined under proposed§ 301.6225–1(d), the partnership createsone or more notional items of income, gain,loss, or deduction that reflects the change inthe item giving rise to the credit. See pro-posed § 301.6225–4(b)(3)(vi).

Under these proposed regulations, onlyspecified tax attributes are adjusted. TheTreasury Department and the IRS consid-ered proposing broader rules for adjustingother tax attributes than those included inthese proposed regulations. Tax attributesare defined in the June 14 NPRM as any-thing that can affect, with respect to apartnership or a partner, the amount ortiming of an item of income, gain, loss,deduction, or credit (as defined in pro-posed § 301.6221(a)–1(b)(1)) or that canaffect the amount of tax due in any taxableyear. Examples of tax attributes include,but are not limited to, basis and holdingperiod, as well as the character of items ofincome, gain, loss, deduction, or creditand carryovers and carrybacks of suchitems. See proposed § 301.6241–1(a)(10).

February 20, 2018 Bulletin No. 2018–8362

Comments are requested as to whethertax attributes other than specified tax at-tributes should be adjusted, at either thepartner or the partnership level, when thepartnership pays an imputed underpayment.Specifically, commenters are requested toaddress whether guidance should provide ageneral rule that partnership adjustmentsand notional items are taken into account asitems for all purposes of Subtitle A, exceptto the extent of the partner’s actual tax due.For example, guidance could provide thatthe partner level tax calculation includes no-tional items for purposes of calculating thetentative tax due, but that for purposes ofdetermining the ultimate tax due, the part-ner’s share of the imputed underpaymentwould be subtracted. Alternatively, guid-ance could provide a list of tax attributesthat are generally adjusted, and a list ofthose that are not.

Specific tax attributes for which com-ments are requested include gross incomerules for publicly traded partnerships un-der section 7704(b) and qualified invest-ment entities described in section 860.Other tax attributes for which commentsare requested include net operating losscarryforwards, other tax accounting undersubchapter K, and those that contain lim-itations based on adjusted gross income(for example, the earned income creditallowed under section 32, the child taxcredit allowed under section 24). Com-ments are also requested as to whether anyspecial rules should be provided for adjust-ments to tax attributes in the cross-bordercontext, and how those adjustments shoulddiffer, if at all, from adjustments to tax at-tributes made in the domestic context.

These regulations also contain rules tocoordinate the changes to specified taxattributes made under these rules withother rules of the Code, including the restof the centralized partnership audit re-gime. See proposed § 301.6225–4(a)(4).To the extent a partner or partnership ap-propriately adjusted tax attributes prior toa final determination under subchapter Cof chapter 63 with respect to a partnershipadjustment (for example, in the context ofan amended return modification describedin proposed § 301.6225–2(d)(2) or a clos-ing agreement described in proposed§ 301.6225–2(d)(8)), those tax attributesare not adjusted under this section. Forexample, when a partnership requests a

modification of the imputed underpaymentwith respect to a partner-specific tax attri-bute (for example, a net operating loss) bythe filing of an amended return by a partneror by entering into a closing agreement, thepartner-specific tax attribute must be re-duced to the extent it is used to modify theimputed underpayment.

The IRS is considering providing informs, instructions, or other guidance thatpartnerships will be required to provideinformation to their partners about theamount and nature of changes to tax attri-butes and any other information neededby the partners.

iii. Allocation of Notional Items

Under section 704(b), a partner’s distrib-utive share of income, gain, loss, deduction,or credit (or item thereof) is determinedunder the partnership agreement if the allo-cation under the agreement has substantialeconomic effect. Section 1.704–1(b)(2)(i)provides that the determination of whetheran allocation of income, gain, loss, or de-duction (or item thereof) to a partner hassubstantial economic effect involves a two-part analysis that is made at the end of thepartnership year to which the allocation re-lates. In order for an allocation to have sub-stantial economic effect, the allocation musthave both economic effect (within themeaning of § 1.704–1(b)(2)(ii)) and be sub-stantial (within the meaning of § 1.704–1(b)(2)(iii)). If the allocation does not havesubstantial economic effect, or the partner-ship agreement does not provide for theallocation, then the allocation must be madein accordance with the partners’ interests inthe partnership under § 1.704–1(b)(3).

Commenters recommended applyingthe existing rules in subchapter K, includ-ing section 704(b), in the context of sec-tion 6225. While the basic principles ofsection 704(b) remain sound in the con-text of notional items, the unique natureof partnership adjustments under section6225 requires the application of theseprinciples to be modified. See proposed§ 1.704–1(b)(1)(viii)(a). Specifically, theallocation of notional items cannot havesubstantial economic effect because theallocation relates to two different years –while generally determined with respectto the reviewed year, notional items aretaken into account in the adjustment year.

Thus, the proposed regulations providethat the allocation of a notional item doesnot have substantial economic effect, but,to address this issue, further provide thatthe allocation will be deemed to be inaccordance with the partners’ interests inthe partnership if the allocation of a no-tional item of income or gain described inproposed § 301.6225–4(b)(3)(ii), or ex-pense or loss described in proposed§ 301.6225–4(b)(3)(iii), is made in themanner in which the corresponding actualitem would have been allocated in thereviewed year under the section 704 reg-ulations. Additionally, the allocation of anotional item of expense or loss described inproposed § 301.6225–4(b)(3)(iv), or a no-tional item of income or gain described inproposed § 301.6225–4(b)(3)(v), must beallocated to the reviewed year partners thatwere originally allocated that excess item inthe reviewed year (or their successors). Seeproposed § 1.704–1(b)(4)(xi). As describedin section (2)(B)(iv) of this preamble, how-ever, these rules require treating successorsas reviewed year partners.

iv. Successors

While the determination of partnershipadjustments under section 6225 is madewith respect to reviewed year partners, itis the adjustment year partners that bearthe economic burden (or benefit) of a part-nership adjustment. As noted in section(2)(B)(i) of this preamble, outside basisadjustments must be made to avoid effec-tively taxing the same item of incometwice. While this concern is clearest whena reviewed year partner remains a partnerin the adjustment year, the same concerngenerally exists when the interest is trans-ferred as the failure to provide outsidebasis would result in effectively taxing thesame item of income twice, just with re-spect to two different taxpayers. Thus,these regulations provide successor rulesunder proposed § 1.704–1(b)(1)(viii)(b)for purposes of adjusting specified tax at-tributes, including outside basis.

A reviewed year partner’s successor isgenerally defined as either a transfereethat succeeds to the transferor partner’scapital account under proposed § 1.704–1(b)(2)(iv)(l), or, in the case of a completeliquidation of a partner’s interest, as theremaining partners to the extent their in-

Bulletin No. 2018–8 February 20, 2018363

terests increased as a result of the liqui-dated partner’s departure. See proposed§§ 1.704–1(b)(1)(viii)(b) and 301.6225–4(e), Example 3.

The June 14 NPRM provides that ifany reviewed year partner with respect towhom an amount was reallocated is notalso an adjustment year partner, the por-tion of the adjustment that would other-wise be allocated to such reviewed yearpartner is allocated instead to the adjust-ment year partner or partners who are thesuccessor or successors to the reviewedyear partner. See proposed § 301.6225–3(b)(4). Further, this rule provides that ifthe partnership cannot identify an adjust-ment year partner that is a successor to thereviewed year partner described in theprevious sentence or if a successor doesnot exist, the portion of the adjustmentthat would otherwise be allocated to thatreviewed year partner is allocated amongthe adjustment year partners according tothe adjustment year partners’ distributiveshares.

A commenter stated that this rule in theJune 14 NPRM allocating a reallocationadjustment that does not result in an im-puted underpayment could result in situa-tions in which partners in a publiclytraded partnership described in section7704(b) own units that are not fungible. Inresponse to this comment and due to ad-ministrability concerns, the Treasury De-partment and the IRS reconsidered this ruleand have concluded that it is appropriate toprovide rules in these proposed regulationsrelating to any situation in which a partner-ship is unable, after exercising reasonablediligence, to determine a successor for apartnership adjustment under section 6225(not only reallocation adjustments). Theserules require that the proposed standard inthe June 14 NPRM be replaced with a newproposed regulation. Therefore, these regu-lations amend proposed § 301.6225–3(b)(4)by removing the final two sentences andprovide a rule in proposed § 1.704–1(b)(1)(viii)(b)(3) that if a partnership cannot de-termine the transferee for a partnership in-terest under proposed § 1.704–1(b)(1)(viii)(b)(2), the successor is deemed to be thosepartners in the adjustment year who werenot also partners in the reviewed year orotherwise identifiable as successors to re-viewed year partners, in proportion to theirrespective interests in the partnership.

Comments are requested as to whetherthese new proposed rules would similarlyresult in issues with respect to the fungi-bility of these partnership interests and, ifso, specific recommendations for the finalregulations to address fungibility concernsconsistent with the centralized partnershipaudit regime, the rules of subchapter K,and the general framework of these pro-posed regulations. Specifically, comment-ers are requested to consider how the suc-cessor rules should operate when, due tothe redemption of all reviewed year part-ners, there are no identifiable successorsto reviewed year partners in the adjust-ment year.

The Treasury Department and the IRSconsidered other alternatives to the suc-cessor rules in these proposed regulations,including allocating notional items only toadjustment year partners that were re-viewed year partners, either solely in theamount for which they would have beenallocated the notional item, or allocatingto them (and no other partners) the fullamount of the notional items. These pro-posed rules contain successor rules be-cause that approach preserves the eco-nomics of the partners that were partnersin both the reviewed and the adjustmentyear, and also facilitates any necessaryprivate contracts between buyers and sell-ers of partnership interests. Comments arerequested as to whether an approach otherthan successor rules are better suited topreserving the single-layer of tax in sub-chapter K while avoiding potential forabuse or other inappropriate tax results.

Comments are also requested as to howthese successor rules should apply in thecase of partnership mergers and divisions.

Finally, comments are requested on is-sues similar to those noted in the June 14NPRM in section (5)(D)(ii) of the pream-ble, namely whether the allocation of ad-justments to a successor of a reviewedyear partner that was a tax-exempt partnermay raise issues concerning private bene-fit to a person other than a tax-exemptpartner, including issues that might affectthe tax-exempt partner’s status under sec-tion 501(c); excise taxes under chapter 42of subtitle D of the Code or under sections4975, 4976, or 4980; or requirements un-der title I of the Employee RetirementIncome Security Act of 1974, Pub. L.93–406 (88 Stat. 829 (1974)) as amended

(ERISA), such as the fiduciary responsi-bility rules under part 4 thereof. The Trea-sury Department and the IRS requestcomments from the public on whetherthese potential issues may be adequatelyaddressed in partnership agreements orwhether guidance is needed to addressthese potential issues. Any comments re-lated to title I of ERISA will be sharedwith the Department of Labor.

v. Adjusting Specified Tax Attributes inCertain Circumstances

For certain types of partnership adjust-ments, notional items are not created. Spe-cifically, notional items are not created for apartnership adjustment that does not derivefrom items that would have been allocatedin the reviewed year under section 704(b),such as a partnership adjustment based upona partner’s failure to report gain under sec-tion 731, a partnership adjustment that is achange of an item of deduction to a section705(a)(2)(B) expenditure, or a partnershipadjustment to an item of tax-exempt in-come. See proposed § 301.6225–4(b)(4).Nevertheless, in these situations specifiedtax attributes are adjusted for the partnershipand its reviewed year partners (or their suc-cessors) in a manner that is consistent withhow the partnership adjustment would havebeen taken into account under the partner-ship agreement in effect for the reviewedyear taking into account all facts and cir-cumstances. See proposed § 301.6225–4(e),Example 5.

vi. Special Rules for Outside Basis inCertain Cases

As noted in section (2)(B)(i) of thispreamble, partners normally adjust theiroutside bases for notional items that areallocated to them. However, in certaincases, the proposed rules do not providefor adjustments to outside basis. Specifi-cally, when a tax-exempt partner transfersits interest to a partner that is not tax-exempt(taxable partner) between the reviewed yearand the adjustment year and the partnershiprequests a modification because of the re-viewed year partner’s status as a tax-exemptentity, the successor taxable partner is dis-allowed a basis adjustment. See proposed§ 301.6225–4(b)(6)(iii)(B). Without thisrule, a taxable successor partner would have

February 20, 2018 Bulletin No. 2018–8364

a basis increase when no imputed underpay-ment was paid with respect to the partner’sshare of the partnership adjustment. Com-ments are requested as to whether this ruleshould be extended to rate modificationsdescribed in proposed § 301.6225–2(d)(4)as well. A basis adjustment is also disal-lowed when a reviewed year partner trans-fers its interest to a related party in a trans-action in which not all gain or loss isrecognized during an administrative pro-ceeding under subchapter C of chapter 63 ofthe Code (subchapter C of chapter 63) and aprincipal purpose of the transfer was to shiftthe economic burden of the imputed under-payment among related parties. Commentsare requested regarding whether basis ad-justments should be disallowed in any othercircumstances.

vii. Accounting and Allocation ofPartnership Section 705(a)(2)(B)Expenditures

Proposed § 301.6225–4(c) describeshow the partnership’s expenditure arisingfrom an imputed underpayment and anyother amount under subchapter C of chap-ter 63 is taken into account by the part-nership and its partners. No deduction isallowed under subtitle A of the Code forany payment required to be made by apartnership under subchapter C of chapter63 and the amount is treated as an expen-diture described in section 705(a)(2)(B).See proposed § 301.6241–4(a).

For an allocation to have economic ef-fect, it must be consistent with the underly-ing economic arrangement of the partners.This means that, in the event that there is aneconomic benefit or burden that correspondsto the allocation, the partner to whom theallocation is made must receive such eco-nomic benefit or bear such economic bur-den. See § 1.704–1(b)(2)(ii). Generally, anallocation of income, gain, loss, or deduc-tion (or item thereof) to a partner will haveeconomic effect if, and only if, throughoutthe full term of the partnership, the part-nership agreement provides: (1) For thedetermination and maintenance of thepartners’ capital accounts in accordancewith § 1.704 –1(b)(2)(iv); (2) for liqui-dating distributions to the partners to bemade in accordance with the positivecapital account balances of the partners;and (3) for each partner to be uncondi-

tionally obligated to restore the deficitbalance in the partner’s capital accountfollowing the liquidation of the partner’spartnership interest. In lieu of satisfying thethird criterion, the partnership may satisfythe qualified income offset rules set forth in§ 1.704–1(b)(2)(ii)(d).

Section 1.704–1(b)(2)(iv)(i) providesspecific rules for determining whether anallocation of a section 705(a)(2)(B) ex-penditure has substantial economic effect.Specifically, it requires that a partner’scapital account be decreased by alloca-tions made to such partner of expendituresdescribed in section 705(a)(2)(B). Seealso § 1.704–1(b)(2)(iv)(b). Further, un-der section 705(a)(2)(B), the adjusted ba-sis of a partner’s interest in a partnershipis decreased (but not below zero) by ex-penditures of the partnership that are notdeductible in computing its taxable in-come and not properly chargeable to cap-ital account.

Several commenters addressed how thepartnership’s payment of an imputed un-derpayment should be allocated among itspartners and how the payment should begiven effect. With respect to the pay-ment’s allocation, commenters recom-mended that the expenditure be allocatedamong the partners in accordance withtheir partnership agreement, subject to therules of section 704(b) (including the reg-ulatory requirements for substantial eco-nomic effect). The Treasury Departmentand the IRS agree with the commentersthat the expenditure should be allocatedunder section 704. These proposed regu-lations contain special rules for allocatingthe expenditure under section 704(b).

With respect to book capital account ad-justments for the imputed underpayment,commenters recommended that partners’capital accounts be adjusted to reflect thepartnership’s payment of the imputed un-derpayment. The Treasury Department andthe IRS agree with this comment but con-clude that because the expenditure is treatedas an expenditure under section 705(a)(2)(B) pursuant to the June 14 NPRM (pro-posed § 301.6241–4(a)), existing rules pro-vide this result.

The Treasury Department and the IRShave concluded, however, that the existingrules that determine whether the economiceffect of an allocation is substantial shouldbe modified to take into account the unique

nature of these expenditures. When a part-nership pays an imputed underpayment un-der section 6225, it has the effect of con-verting what would have been a non-deductible partner-level expenditure into anon-deductible partnership-level expendi-ture. The proposed regulations provide thatan allocation of the nondeductible expendi-ture will be considered to be substantial onlyif the partnership allocates the expenditurein proportion to the notional item to which itrelates, taking into account appropriatemodifications. See proposed §§ 1.704–1(b)(2)(iii)(a) and (f), 301.6225–4(c) and301.6225–4(e), Example 4. This rule alignsthe economics of the income allocation (inthis case, the notional income allocation)with the directly associated imputed under-payment expense in a manner consistentwith the flowthrough nature of partnershipsunder subchapter K. Absent this substanti-ality rule in the regulations, partnershipscould inappropriately allocate expenses topartners in the adjustment year in a mannerinconsistent with the underlying economicarrangement of the partners. These new sub-stantiality rules also apply to a paymentmade by a pass-through partner under pro-posed § 301.6226–3(e)(4).

Similarly, for partnerships that do notmaintain capital accounts, the allocationof the expenditure cannot be in accor-dance with the partners’ interests in thepartnership to the extent it shifts the eco-nomic burden of the payment of the im-puted underpayment away from a partner(or its successor) that would have beenallocated the corresponding notional in-come item. However, the regulations pro-vide that an allocation of an expense thatsatisfies the new substantiality rule and inwhich the partner’s distribution rights arereduced by the partner’s share of the im-puted underpayment is deemed to be inaccordance with the partners’ interests inthe partnership. See proposed § 1.704–1(b)(4)(xii). These proposed regulationsdo not address the extent to which thepartnership may later reverse this alloca-tion with a special chargeback or similarprovision. Comments are requested onthis issue.

One commenter recommended rulesspecifying that a partner’s contribution offunds to the partnership for payment of animputed underpayment will result in anincrease in that partner’s capital account.

Bulletin No. 2018–8 February 20, 2018365

This comment is not adopted because theexisting rules in subchapter K provide suf-ficient guidance for this circumstance. Acommenter also recommended rules ad-dressing the availability of a corporation’sdeduction under temporary § 1.163–9T(b)(2) for a payment of interest in re-spect of an underpayment of tax. Thiscomment is not adopted because it is be-yond the scope of these proposed regula-tions.

The proposed regulations also providethat in order for an allocation of an expen-diture for interest, penalties, additions totax, or additional amounts as determinedunder section 6233 to be substantial, itmust be allocated to the reviewed yearpartner in proportion to the allocation ofthe related imputed underpayment, the re-lated payment made by a pass-throughpartner under proposed § 301.6226–3(e)(4), or the related notional item towhich it relates (whichever is appropri-ate), taking into account modifications un-der proposed § 301.6225–2 attributable tothat partner. See proposed § 1.704–1(b)(2)(iii)(f)(3). This rule has a similarpurpose as the rule in proposed § 1.704–1(b)(2)(iii)(f)(2) in that it aligns the eco-nomics of these expenses with the part-nership items to which they relate. Underthis rule, an expense for interest imposedunder the Code will generally be allocatedin proportion to the imputed underpay-ment from which it derives. Also, an ex-pense arising from a substantial under-statement of tax under section 6662(d) foran imputed underpayment will generallybe allocated in proportion to the notionalincome item to which it relates.

In situations in which the reviewedyear partner is not an adjustment yearpartner, the successor rules in proposed§ 1.704–1(b)(1)(viii)(b) apply to the allo-cation of these expenditures. Under thoserules, a partner admitted after the re-viewed year will not ordinarily be allo-cated any section 705(a)(2)(B) expendi-ture in the adjustment year.

C. Partnership adjustments that do notresult in an imputed underpayment

The June 14 NPRM provides that therules under subchapter K apply in the caseof a partnership adjustment that does notresult in an imputed underpayment. See

proposed § 301.6225–3(c). Further, pro-posed § 1.704–1(b)(4)(xiii) of these regu-lations provides that an allocation of an itemarising from a partnership adjustment thatdoes not result in an imputed underpayment(as defined in proposed § 301.6225–1(c)(2))does not have substantial economic effectbut will be deemed to be in accordance withthe partners’ interests in the partnership if itis allocated in the manner in which the itemwould have been allocated in the reviewedyear under the regulations under section704, taking into account the successor rulesdescribed in section (2)(B)(iv) of this pre-amble.

3. Provisions Relating to Section 6226

A. In general

Section 6226(b) describes how partner-ship adjustments are taken into account bythe reviewed year partners if a partnershipmakes an election under section 6226(a).Under section 6226(b)(1), each partner’stax imposed by chapter 1 of subtitle A ofthe Code (chapter 1 tax) is increased bythe aggregate of the adjustment amountsas determined under section 6226(b)(2).This increase in chapter 1 tax is reportedon the return for the partner’s taxableyear that includes the date the statementdescribed under section 6226(a) is fur-nished to the partner by the partnership(reporting year). The aggregate of theadjustment amounts is the aggregate ofthe correction amounts. See proposed§ 301.6226 –3(b).

The adjustment amounts determinedunder section 6226(b)(2) fall into two cat-egories. Under section 6226(b)(2)(A), inthe case of the taxable year of the partnerthat includes the end of the partnership’sreviewed year (first affected year), the ad-justment amount is the amount by whichthe partner’s chapter 1 tax would increasefor the partner’s first affected year if thepartner’s share of the adjustments weretaken into account in that year. Undersection 6226(b)(2)(B), in the case of anytaxable year after the first affected year,and before the reporting year (that is, theintervening years), the adjustment amountis the amount by which the partner’s chapter1 tax would increase by reason of the ad-justment to tax attributes determined undersection 6226(b)(3) in each of the interveningyears. The adjustment amounts determined

under section 6226(b)(2)(A) and (B) areadded together to determine the aggregate ofthe adjustment amounts for purposes of de-termining additional reporting year tax,which is the increase to the partner’s chapter1 tax in accordance with section 6226(b)(1).

Section 6226(b)(3) provides two rulesregarding adjustments to tax attributesthat would have been affected if the part-ner’s share of adjustments were taken intoaccount in the first affected year. First,under section 6226(b)(3)(A), in the caseof an intervening year, any tax attributemust be appropriately adjusted for pur-poses of determining the adjustmentamount for that intervening year in accor-dance with section 6226(b)(2)(B). Sec-ond, under section 6226(b)(3)(B), in thecase of any subsequent taxable year (thatis, a year, including the reporting year,that is subsequent to the intervening yearsreferenced in 6226(b)(3)(A)), any tax at-tribute must be appropriately adjusted.

Under the June 14 NPRM, a reviewedyear partner’s share of the adjustmentsthat must be taken into account by thereviewed year partner must be reported tothe reviewed year partner in the samemanner as originally reported on the re-turn filed by the partnership for the re-viewed year. See proposed § 301.6226–2(f). If the adjusted item was not reflectedin the partnership’s reviewed year return,the adjustment must be reported in accor-dance with the rules that apply with re-spect to partnership allocations, includingunder the partnership agreement. How-ever, under proposed § 301.6226–2(f)(1),if the adjustments, as finally determined,are allocated to a specific partner or in aspecific manner, the partner’s share of theadjustment must follow how the adjust-ment is allocated in that final determina-tion.

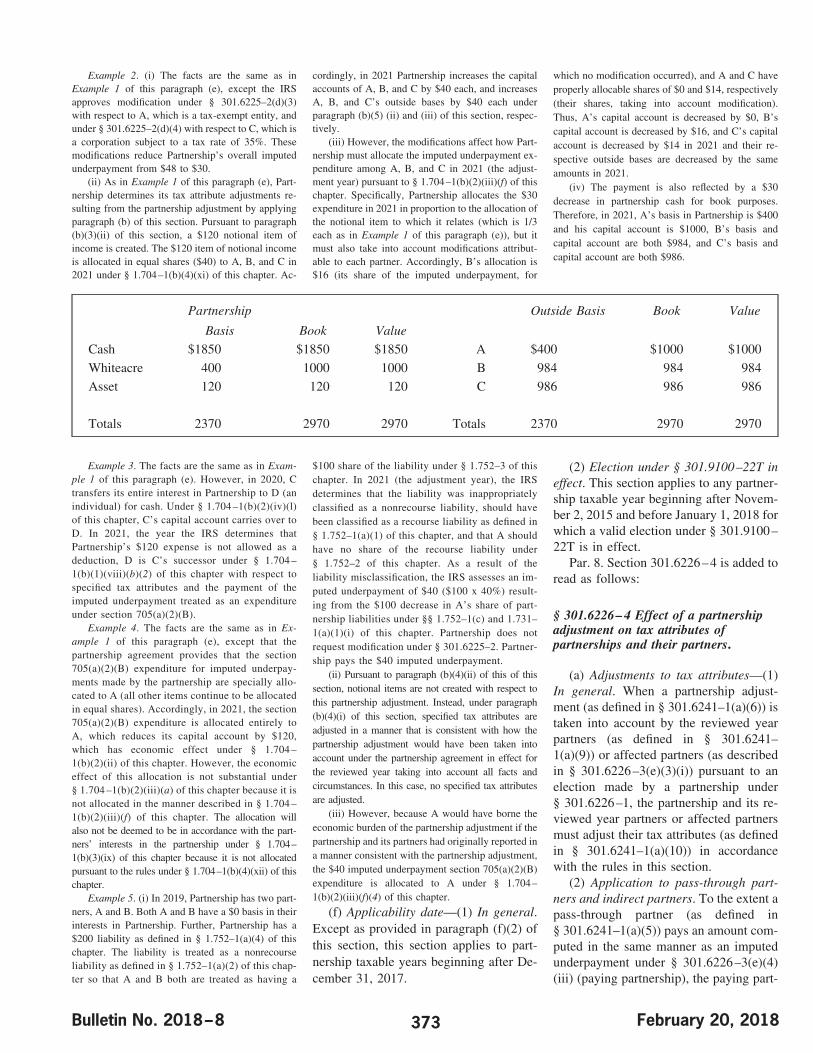

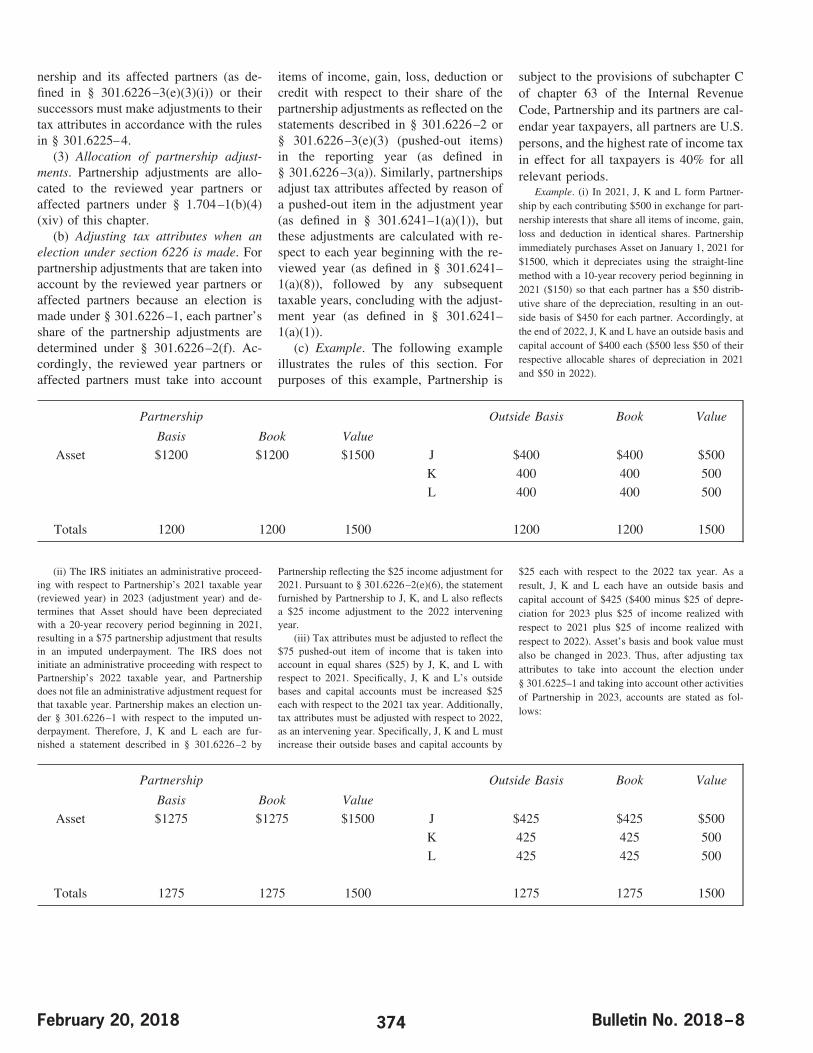

Section 301.6226–4(b) of these pro-posed regulations provides that the re-viewed year partners or affected partners(as described in § 301.6226–3(e)(3)(i))must take into account items of income,gain, loss, deduction or credit with respectto their share of the partnership adjust-ments as contained on the statementsdescribed in proposed § 301.6226–2(pushed-out items) in the reporting year(as defined in proposed § 301.6226–3(a)).Similarly, partnerships adjust tax attri-butes affected by reason of a pushed-out

February 20, 2018 Bulletin No. 2018–8366

item in the reviewed year. In the case ofa reviewed year partner that disposed ofits partnership interest prior to the re-porting year, that partner may take intoaccount any outside basis adjustmentunder these rules in an amended returnto the extent otherwise allowable underthe Code.

Unlike the proposed rules under sec-tion 6225 and subchapter K described insection 2 of this preamble, under section6226, all tax attributes (as defined in pro-posed § 301.6241–1(a)(10)) are adjustedfor pushed out items of income, gain, de-duction, loss or credit.

B. Section 704(b)

Section (2)(B)(iii) of this preamble dis-cusses the general mechanics of section704(b). In accordance with the principlesset forth in section 704(b), an allocation ofa pushed-out item does not have substan-tial economic effect within the meaning ofsection 704(b)(2). However, the allocationof such an item will be deemed to be inaccordance with the partners’ interests inthe partnership if it is allocated in theadjustment year in the manner in whichthe item would have been allocated underthe rules of section 704(b), including§ 1.704–1(b)(1)(i) (or otherwise takeninto account under subtitle A) in the re-viewed year (as defined in proposed§ 301.6241–1(a)(8)), followed by anysubsequent taxable years, concluding withthe adjustment year (as defined in pro-posed § 301.6241–1(a)(1)). See proposed§ 1.704–1(b)(4)(xiv).

C. Timing

Under the June 14 NPRM, a reviewedyear partner that is furnished a statementunder proposed § 301.6226 –2 is re-quired to pay any additional chapter 1tax (additional reporting year tax) forthe partner’s taxable year which in-cludes the date the statement was fur-nished to the partner in accordance withproposed § 301.6226 –2 (the reportingyear) that results from taking into ac-count the adjustments reflected in thestatement. See proposed § 301.6226 –3.The additional reporting year tax is theaggregate of the adjustment amounts, asdetermined in proposed § 301.6226 –

3(b) and described in (3)(A) of this pre-amble.

A commenter recommended that ad-justments to capital accounts and basisshould be made to the reviewed year part-ners in the reviewed year to prevent dis-tortions. This comment is not adopted be-cause, in this context, section 6226 clearlyapplies to the adjustment year. These pro-posed regulations provide that adjust-ments to partnership-level tax attributesare calculated with respect to each yearbeginning with the reviewed year, fol-lowed by subsequent taxable years, con-cluding with the adjustment year. See pro-posed § 301.6226–4(b).

D. Effect of a payment by pass-throughpartner

These proposed regulations providethat to the extent a pass-through partner(as defined in proposed § 301.6241–1(a)(5)) makes a payment in lieu of issu-ing statements to its owners described inproposed § 301.6226–3(e)(4), that pay-ment will be treated similarly to the pay-ment of an amount under subchapter C ofchapter 63 for purposes of any adjust-ments to bases and capital accounts, andaccordingly, the rules contained in proposed§ 301.6225–4 will apply to determine anyappropriate adjustments to bases and capitalaccounts. See proposed § 301.6226–3(e).To the extent that the pass-through partnercontinues to push out the partnership adjust-ments to its partners in accordance withproposed § 301.6226–3(e)(3), the partnersreceiving those adjustments will adjust theirbases and capital accounts in accordancewith the guidance provided in proposed§ 301.6226–4.

Comments are requested as to how Scorporations, trusts, and estates that arepass-through partners that pay an amountunder proposed § 301.6226–3(e), andtheir shareholders and beneficiaries, re-spectively, should take these paymentsinto account and adjust tax attributes.

Special Analyses

Certain IRS regulations, including thisone, are exempt from the requirements ofExecutive Order 12866, as supplementedand reaffirmed by Executive Order 13563.Therefore, a regulatory impact assessmentis not required. Because the proposed reg-

ulations would not impose a collection ofinformation on small entities, the Regula-tory Flexibility Act (5 U.S.C. chapter 6)does not apply.

Pursuant to section 7805(f), this noticeof proposed rulemaking has been submit-ted to the Chief Counsel for Advocacy ofthe Small Business Administration forcomment on its impact on small business.

Statement of Availability of IRSDocuments

IRS Revenue Procedures, RevenueRulings, Notices and other guidance citedin this preamble are published in the In-ternal Revenue Bulletin (or CumulativeBulletin) and are available from the Su-perintendent of Documents, U.S. Govern-ment Publishing Office, Washington, DC20402, or by visiting the IRS website athttp://www.irs.gov.

Comments and Requests for PublicHearing

Before these proposed regulations areadopted as final regulations, considerationwill be given to any electronic and writtencomments that are submitted timely to theIRS as prescribed in this preamble underthe ADDRESSES heading. The TreasuryDepartment and the IRS request com-ments on all aspects of the proposed rules.All comments will be available at http://www.regulations.gov or upon request. Apublic hearing will be scheduled if re-quested in writing by any person thattimely submits written comments. If apublic hearing is scheduled, then notice ofthe date, time, and place for the publichearing will be published in the FederalRegister.

* * * * *

Proposed Amendments to theRegulations

Accordingly, 26 CFR parts 1 and 301are proposed to be amended as follows:

PART 1—INCOME TAX

Paragraph 1. The authority citation forpart 1 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *Par. 2. Section 1.704–1 is amended by:

1. Adding paragraph (b)(1)(viii).

Bulletin No. 2018–8 February 20, 2018367

2. Adding a sentence to the end of para-graph (b)(2)(iii)(a).

3. Adding paragraphs (b)(2)(iii)(f), (b)(2)(iv)(i)(4), and (b)(4)(xi), (xii), (xiii),(xiv), and (xv).

The additions read as follows:

§ 1.704–1 Partner’s distributive share.

* * * * *(b) * * *(1) * * *(viii) Items relating to a final determi-

nation under the centralized partnershipaudit regime—(a) In general. Certainitems of income, gain, loss, deduction orcredit may result from a final determina-tion under subchapter C of chapter 63 ofthe Internal Revenue Code (subchapter Cof chapter 63) (relating to the centralizedpartnership audit regime). Special rulesunder section 704(b) and § 1.704–1(b)apply to these items that take into accountthat the item relates to the reviewed year(as defined in § 301.6241–1(a)(8) of thischapter) but occurs in the adjustment year(as defined in § 301.6241–1(a)(1) of thischapter). See paragraphs (b)(2)(iii)(a) and(f), (b)(2)(iv)(i)(4), and (b)(4)(xi), (xii),(xiii), (xiv), and (xv) of this section.

(b) Successors—(1) In general. In thecase of a transfer or liquidation of a part-nership interest subsequent to a reviewedyear, a successor has the meaning pro-vided in paragraph (b)(1)(viii)(b) of thissection. In the case of a subsequent trans-fer by a successor of a partnership interest,the principles of paragraph (b)(1)(viii)(b)of this section will also apply to the newsuccessor.

(2) Identifiable transferee partner. Ex-cept as otherwise provided in paragraph(b)(1)(viii)(b)(3) of this section, in thecase of a transfer of all or part of a part-nership interest during or subsequent tothe reviewed year, a successor is the part-ner to which the reviewed year transferorpartner’s capital account carried over (orwould carry over if the partnership main-tained capital accounts) under paragraph(b)(2)(iv)(l) of this section (an identifiabletransferee partner).

(3) Unidentifiable transferee partner.If, after exercising reasonable diligence,the partnership cannot determine an iden-tifiable transferee partner under paragraph(b)(1)(viii)(b)(2) of this section, each part-

ner in the adjustment year that is not anidentifiable transferee partner and was nota partner in the reviewed year, (an uniden-tifiable transferee partner) is a successorto the extent of the proportion of its inter-est in the partnership to the total interestsof unidentifiable transferee partners in thepartnership (considering all facts and cir-cumstances).

(4) Liquidation of partnership interest.In the case of a liquidation of a partner’sentire interest in the partnership during orsubsequent to the reviewed year, the succes-sors to the liquidated partner are certainadjustment year partners (as defined in§ 301.6241–1(a)(2) of this chapter) as pro-vided in this paragraph (b)(1)(viii)(b)(4).The determination of the extent to which theadjustment year partners are treated as suc-cessors under this section must be made in amanner that reflects the extent to which theadjustment year partners’ interests in thepartnership increased as a result of the liq-uidating distribution (considering all factsand circumstances).

(2) * * *(iii) * * *(a) * * *Notwithstanding any other

sentence of this paragraph (b)(2)(iii)(a),an allocation of any of the following willbe substantial only if the allocation is de-scribed in paragraph (b)(2)(iii)(f) of thissection: an expenditure for any paymentrequired to be made by a partnership un-der subchapter C of chapter 63 (relating tothe centralized partnership audit regime),adjustments reflected on a statement fur-nished to a pass-through partner (as de-fined in § 301.6241–1(a)(5) of this chap-ter) under § 301.6226–3(e)(4) of thischapter, or interest, penalties, additions totax, or additional amounts described insection 6233.* * * * *

(f) Certain expenditures under the cen-tralized partnership audit regime—(1) Ingeneral. The economic effect of an allo-cation of an expenditure for any paymentrequired to be made by a partnership un-der subchapter C of chapter 63 (as de-scribed in § 301.6241–4(a) of this chap-ter) is substantial only if the expenditure isallocated in the manner described in thisparagraph (b)(2)(iii)(f). For partnershipswith allocations that do not satisfy para-graph (b)(2)(ii) of this section, see para-graph (b)(4)(xi) of this section.

(2) Expenditures for imputed underpay-ments or similar amounts. Except as other-wise provided, an expenditure for an im-puted underpayment under § 301.6225–1 ofthis chapter (or for an amount computed inthe same manner as an imputed underpay-ment under § 301.6226–3(e)(4)(iii) of thischapter) is allocated to the reviewed yearpartner (or its successor, as defined in para-graph (b)(1)(viii)(b) of this section) in pro-portion to the allocation of the notional item(as described in § 301.6225–4(b) of thischapter) to which the expenditure relates,taking into account modifications under§ 301.6225–2 of this chapter attributable tothat partner.

(3) Interest, penalties, additions to tax,or additional amounts described in sec-tion 6233. An expenditure for interest,penalties, additions to tax, or additionalamounts as determined under section6233 (or penalties and interest describedin § 301.6226–3(e)(4)(iv) of this chapter)is allocated to the reviewed year partner(or its successor, as defined in paragraph(b)(1)(viii)(b) of this section) in propor-tion to the allocation of the portion of theimputed underpayment with respect towhich the penalty applies (or amountcomputed in the same manner as an im-puted underpayment under § 301.6226–3(e)(4) of this chapter) or related notionalitem to which it relates (whichever is ap-propriate), taking into account modifica-tions under § 301.6225–2 of this chapterattributable to that partner.

(4) Imputed underpayments unrelatedto notional items. In the case of an im-puted underpayment that results from apartnership adjustment for which no no-tional items are created under § 301.6225–4(b)(2) of this chapter, the expendituremust be allocated to the reviewed yearpartner (or its successor, as defined inparagraph (b)(1)(viii)(b) of this section)that would have borne the economic ben-efit or burden of the partnership adjust-ment if the partnership and its partnershad originally reported in a manner con-sistent with the partnership adjustmentthat resulted in the imputed underpaymentwith respect to the reviewed year.

(iv) * * *(i) * * *(4) Certain expenditures under the cen-

tralized partnership audit regime. Notwith-standing paragraph (b)(2)(iv)(i)(1) of this

February 20, 2018 Bulletin No. 2018–8368

section, the economic effect of an allocationof an expenditure for any payment requiredto be made by a partnership under subchap-ter C of chapter 63 (as described in§ 301.6241–4(a) of this chapter) is substan-tial only if the expenditure is allocated in themanner described in paragraph (b)(2)(iii)(f)of this section. For partnerships with alloca-tions that do not satisfy paragraph (b)(2)(ii)of this section, see paragraph (b)(4)(xii) ofthis section.*****

(4) * * *(xi) Notional items under the central-

ized partnership audit regime. An alloca-tion of a notional item (as described in§ 301.6225–4(b) of this chapter) does nothave substantial economic effect withinthe meaning of paragraph (b)(2) of thissection. However, the allocation of a no-tional item of income or gain described in§ 301.6225–4(b)(1)(ii) of this chapter, orexpense or loss described in § 301.6225–4(b)(1)(iii) of this chapter, will be deemedto be in accordance with the partners’interests in the partnership if the notionalitem is allocated in the manner in whichthe corresponding actual item would havebeen allocated in the reviewed year underthe rules of this section, treating succes-sors (as defined in paragraph (b)(1)(viii)(b) of this section) as reviewed year part-ners. Additionally, the allocation of a no-tional item of expense or loss described in§ 301.6225–4(b)(3)(iv) of this chapter, ora notional item of income or gain de-scribed in § 301.6225–4(b)(3)(v) of thischapter, will be deemed to be in accor-dance with the partners’ interests in thepartnership if the notional item is allo-cated to the reviewed year partners (ortheir successors as defined in paragraph(b)(1)(viii)(b) of this section) in the man-ner in which the excess item was allocatedin the reviewed year.

(xii) Certain section 705(a)(2)(B) ex-penditures under the centralized partner-ship audit regime. An allocation of anexpenditure for any payment required tobe made by a partnership under subchap-ter C of chapter 63 (relating to the cen-tralized partnership audit regime and asdescribed in § 301.6241–4(a) of thischapter) will be deemed to be in accor-dance with the partners’ interests in thepartnership, as provided in paragraph(b)(3) of this section, only if the expendi-

ture is allocated in the manner describedin paragraph (b)(2)(iii)(f) of this sectionand if the partners’ distribution rights arereduced by the partners’ shares of the im-puted underpayment.

(xiii) Partnership adjustments that donot result in an imputed underpaymentunder the centralized partnership auditregime. An allocation of an item arisingfrom a partnership adjustment that doesnot result in an imputed underpayment (asdefined in § 301.6225–1(c)(2) of thischapter) does not have substantial eco-nomic effect within the meaning of para-graph (b)(2) of this section. However, theallocation of such an item will be deemedto be in accordance with the partners’interests in the partnership if allocatedin the manner in which the item wouldhave been allocated in the reviewed yearunder the rules of this section, treatingsuccessors as defined in paragraph (b)(1)(viii)(b) of this section as reviewedyear partners.

(xiv) Partnership adjustments subjectto an election under section 6226. Anallocation of an item arising from a part-nership adjustment that results in an im-puted underpayment for which an electionis made under § 301.6226–1 of this chap-ter does not have substantial economic ef-fect within the meaning of paragraph (b)(2)of this section. However, the allocation ofsuch an item will be deemed to be in accor-dance with the partners’ interests in the part-nership if allocated in the adjustment year(as defined in § 301.6241–1(a)(1) of thischapter) in the manner in which the itemwould have been allocated under the rulesof this section (or otherwise taken into ac-count under subtitle A of the Code) in thereviewed year (as defined in § 301.6241–1(a)(8) of this chapter), followed by anysubsequent taxable years, concludingwith the adjustment year (as defined in§ 301.6241–1(a)(1) of this chapter).

(xv) Substantial economic effect undersections 168(h) and 514(c)(9)(E)(i)(ll).An allocation described in paragraphs(b)(4)(xi) through (xiv) of this section willbe deemed to have substantial economiceffect for purposes of sections 168(h) and514(c)(9)(E)(i)(ll) if the allocation isdeemed to be in accordance with the part-ners’ interests in the partnership under theapplicable rules set forth in paragraphs(b)(4)(xi) through (xiv) of this section.

*****Par. 3. Section 1.705–1 is amended by

adding paragraph (a)(10) to read as fol-lows:

§ 1.705–1 Determination of basis ofpartner’s interest.

(a) * * *(10) For rules relating to determining

the adjusted basis of a partner’s interest ina partnership following a final determina-tion under subchapter C of chapter 63 ofthe Internal Revenue Code (relating to thecentralized partnership audit regime), see§§ 301.6225–4 and 301.6226–4 of thischapter.*****

Par. 4. Section 1.706 – 4 is amendedby redesignating paragraphs (e)(2)(viii)through (xi) as paragraphs (e)(2)(ix)through (xii), respectively, and adding anew paragraph (e)(2)(viii) to read as fol-lows:

§ 1.706–4 Determination of distributiveshare when a partner’s interest varies.

* * * * *(e) * * *(2) * * *(viii) Any item arising from a final

determination under subchapter C ofchapter 63 of the Internal Revenue Code(relating to the centralized partnership au-dit regime) with respect to a partnershipadjustment resulting in an imputed under-payment for which no election is madeunder § 301.6226–1 of this chapter.*****

PART 301—PROCEDURE ANDADMINISTRATION

Par. 5. The authority citation for part301 continues to read in part as follows:

Authority: 26 U.S.C. 7805 * * *Par 6. Section 301.6225–3 as proposed

to be amended at 82 FR 27334 (June 14,2017) is further amended by revisingparagraph (b)(4) to read as follows:

§ 301.6225–3 Treatment of partnershipadjustments that do not result in animputed underpayment.

*****(b) ***

Bulletin No. 2018–8 February 20, 2018369

(4) Reallocation adjustments. A part-nership adjustment that does not result inan imputed underpayment pursuant to§ 301.6225–1(c)(2)(i) is taken into ac-count by the partnership in the adjustmentyear as a separately stated item or a non-separately stated item, as required by sec-tion 702. The portion of an adjustmentallocated under this paragraph (b)(4) isallocated to adjustment year partners (asdefined in § 301.6241–1(a)(2)) who arealso reviewed year partners (as defined in§ 301.6241–1(a)(9)) with respect to whomthe amount was reallocated.

*****Par. 7. Section 301.6225–4 is added to

read as follows:

§ 301.6225–4 Effect of a partnershipadjustment on specified tax attributes ofpartnerships and their partners.

(a) Adjustments to specified tax attri-butes—(1) In general. When there is apartnership adjustment (as defined in§ 301.6241–1(a)(6)), the partnership andits adjustment year partners (as defined in§ 301.6241–1(a)(2)) generally must adjusttheir specified tax attributes (as defined inparagraph (a)(2) of this section) in accor-dance with the rules in this section. For apartnership adjustment that results in animputed underpayment (as defined in§ 301.6241–1(a)(3)), specified tax attri-butes are generally adjusted by makingappropriate adjustments to the book valueand basis of partnership property underparagraph (b)(2) of this section, creatingnotional items based on the partnershipadjustment under paragraph (b)(3) of thissection, allocating those notional items asdescribed in paragraph (b)(5) of this sec-tion, and determining the effect of thosenotional items for the partnership and itsreviewed year partners (as defined in§ 301.6241–1(a)(9)) or their successors(as defined in § 1.704–1(b)(1)(viii)(b) ofthis chapter) under paragraph (b)(6) ofthis section. Paragraph (c) of this sectiondescribes how to treat an expenditure forany payment required to be made by apartnership under subchapter C of chapter63 of the Internal Revenue Code (sub-chapter C of chapter 63) including any im-puted underpayment. Paragraph (d) of thissection describes adjustments to tax attri-butes in the case of a partnership adjustment

that does not result in an imputed underpay-ment (as described in § 301.6225–1(c)(2)).

(2) Specified tax attributes. Specifiedtax attributes are the tax basis and bookvalue of a partnership’s property, amountsdetermined under section 704(c), adjust-ment year partners’ bases in their partner-ship interests, and adjustment year part-ners’ capital accounts determined andmaintained in accordance with § 1.704–1(b)(2) of this chapter.

(3) Timing. Adjustments to specifiedtax attributes under this section are madein the adjustment year (as defined in§ 301.6241–1(a)(1)). Thus, to the extentthat an adjustment to a specified tax attri-bute under this section is reflected on afederal tax return, the partnership adjust-ment is generally first reflected on anyreturn filed with respect to the adjustmentyear.