Embed Size (px)

Citation preview

Highlights and Lessons Learned from a National Symposium Series on Coastal Insurance Issues

THE TRAVELERS INSTITUTE

travelersinstitute.com

1travelersinstitute.com

Ta b l e o f C o n t e n t s

Introduction ......................................................................................3

South Carolina Coastal Risk Symposium ............................................4

Partnership on Mitigation..................................................................8

Improving Availability and Affordability of Coastal Windstorm Insurance .........................................................12

Opportunities for Integrating Disaster Mitigation and Energy Retrofit Programs .........................................................16

Mitigation Strategies for the Alabama Coastal Region .....................20

Travelers Coastal Wind Zone Plan....................................................23

Travelers Coastal Wind Zone Plan Press Coverage ...........................28

About the Travelers Institute ...........................................................33

2 travelersinstitute.com

The Travelers Companies, Inc. established the Travelers

InstituteSM in June 2009, as a means of participating in

public policy dialogue on matters of interest to the

property casualty insurance sector, as well as the

financial services industry more broadly.

T r a v e l e r s I n s t i t u t e M i s s i o n St a t e m e n t

3travelersinstitute.com

In 2009, the Travelers Institute launched a series of national symposia to bring together business,

government, and community leaders to identify strategies to address the availability and affordability

of coastal windstorm insurance for homeowners along the Atlantic and Gulf coasts. The symposia

were held in five cities – Charleston, South Carolina; Hartford, Connecticut; Austin, Texas;

Washington, DC; and Mobile, Alabama – and provided an opportunity for participants to raise

awareness of the importance of building more resilient communities. The Travelers Institute also

participated in Senator Roger Wicker’s insurance roundtable, held in Gulfport, Mississippi,

to explore solutions to rising insurance costs and barriers to certain kinds of insurance coverage on

the Gulf Coast. This report summarizes our coastal symposia series.

Highlights and Lessons Learned from a National Symposium Series on Coastal Insurance Issues.

Each discussion began with an acknowledgment that more

Americans are living along coasts every year, while at the

same time, the nation is facing the possibility of increased

frequency and severity of extreme weather events. To address

the crisis of availability and affordability of coastal

homeowners insurance, the Travelers

Institute developed The Travelers

Coastal Wind Zone Plan, which was

presented at each event to stimulate the

conversation around proposed

solutions. The plan is a comprehensive,

private market approach based on four

key principles: a stable and consistent

regulatory environment; transparency

in calculating insurance premiums; a

federal reinsurance mechanism for

extreme weather events; and building

stronger homes and risk-based,

land-use planning (see page 23 for a complete description of

the Travelers Coastal Wind Zone Plan).

Symposia panelists also identified action steps for individuals,

businesses, governments, and communities to increase

coastal resilience and reduce the economic toll extreme

weather events wreak on communities. Recommendations

include strengthening ecosystems, developing flexible

adaptation plans, and requiring infrastructure and building

code standards that meet future risk. Many panelists

presented research on the undeniable benefits of these and

other mitigation strategies, such as retrofitting older homes

and building to fortified construction standards.

While each city and state with coastal exposures faces its own

unique challenges, attendees and panelists from each

symposium agreed that in order for communities to become

more resilient, mitigation techniques must be broadly

adopted. In order to do this, residential incentives need to be

developed to encourage fortified

construction standards and retrofits to

create stronger homes. Additionally,

communities should implement

improved land use planning and

tougher, enforced building codes

designed to reduce catastrophe losses.

This greater focus on preparedness

through loss mitigation and risk

management should also help improve

the availability and affordability of

coastal wind insurance. Each

symposium demonstrated that

long-term solutions will come from a collective and

comprehensive effort, engaging all stakeholders to urge

federal, state, and local policymakers into action.

The Travelers Institute remains committed to continuing the

symposia series in order to highlight coastal communities at risk

and to facilitate partnerships with local leaders and government

entities that will lead to more solutions for coastal residents.

T r a v e l e r s I n s t i t u t e M i s s i o n St a t e m e n t

4 travelersinstitute.com

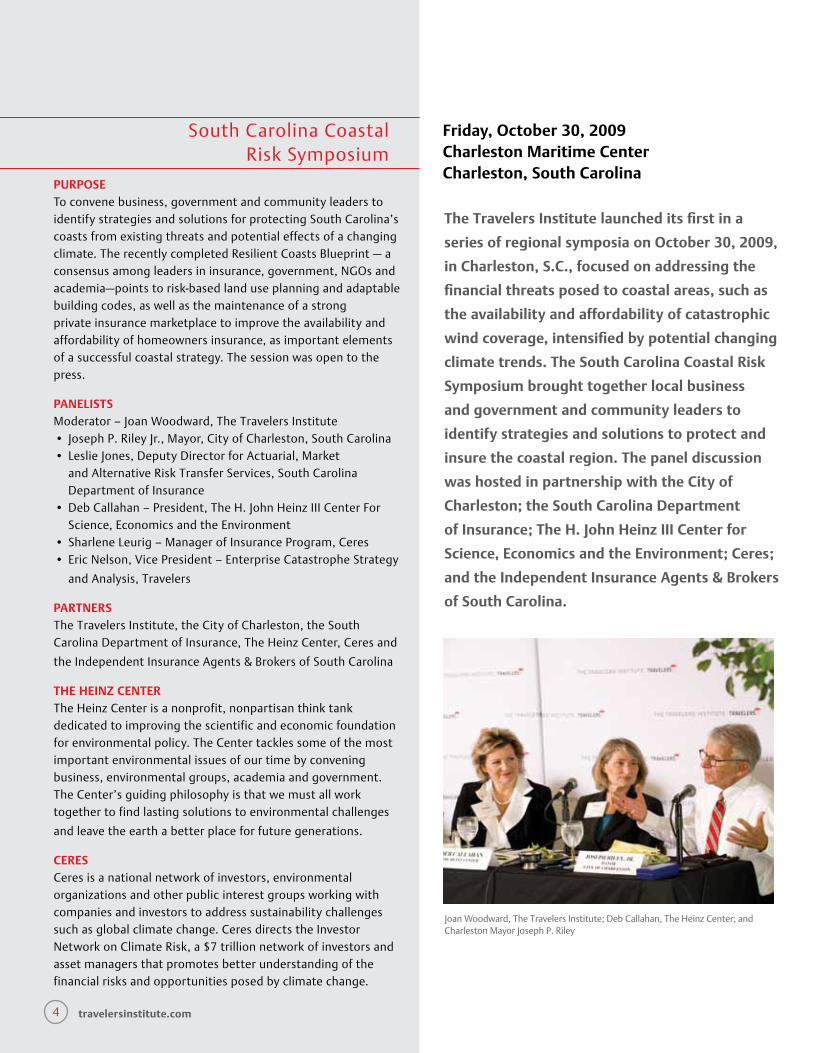

Friday, October 30, 2009 Charleston Maritime CenterCharleston, South Carolina

PuRPOSe To convene business, government and community leaders to identify strategies and solutions for protecting South Carolina’s coasts from existing threats and potential effects of a changing climate. The recently completed Resilient Coasts Blueprint — a consensus among leaders in insurance, government, NGOs and academia—points to risk-based land use planning and adaptable building codes, as well as the maintenance of a strong private insurance marketplace to improve the availability and affordability of homeowners insurance, as important elements of a successful coastal strategy. The session was open to the press.

PAnelISTS Moderator – Joan Woodward, The Travelers Institute• JosephP.RileyJr.,Mayor,CityofCharleston,SouthCarolina• LeslieJones,DeputyDirectorforActuarial,Market

and Alternative Risk Transfer Services, South Carolina Department of Insurance

• DebCallahan–President,TheH.JohnHeinzIIICenterForScience, Economics and the Environment

• SharleneLeurig–ManagerofInsuranceProgram,Ceres• EricNelson,VicePresident–EnterpriseCatastropheStrategy

and Analysis, Travelers

PARTneRS The Travelers Institute, the City of Charleston, the South CarolinaDepartmentofInsurance,TheHeinzCenter,Ceresand

the Independent Insurance Agents & Brokers of South Carolina

THe HeInz CenTeR TheHeinzCenterisanonprofit,nonpartisanthinktankdedicated to improving the scientific and economic foundation for environmental policy. The Center tackles some of the most important environmental issues of our time by convening business, environmental groups, academia and government. The Center’s guiding philosophy is that we must all work together to find lasting solutions to environmental challenges

and leave the earth a better place for future generations.

CeReSCeres is a national network of investors, environmental organizationsandotherpublicinterestgroupsworkingwithcompanies and investors to address sustainability challenges such as global climate change. Ceres directs the Investor Network on Climate Risk, a $7 trillion network of investors and asset managers that promotes better understanding of the financial risks and opportunities posed by climate change.

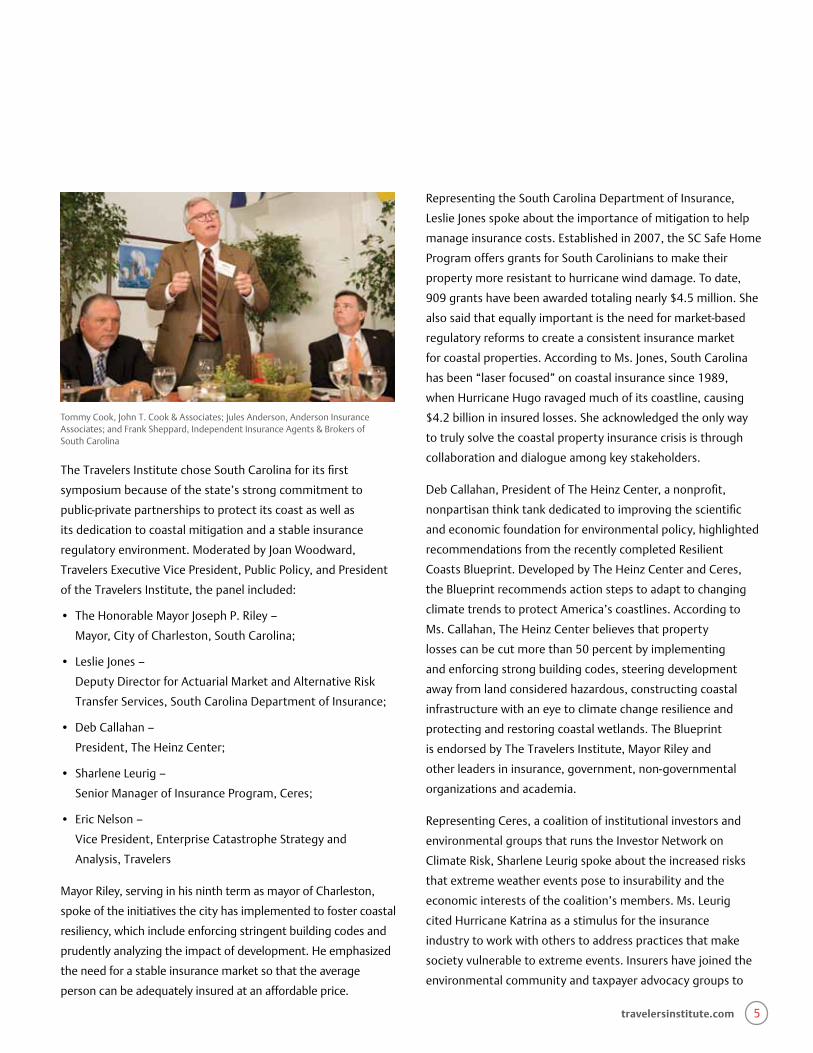

South Carolina Coastal Risk Symposium

The Travelers Institute launched its first in a

series of regional symposia on October 30, 2009,

in Charleston, S.C., focused on addressing the

financial threats posed to coastal areas, such as

the availability and affordability of catastrophic

wind coverage, intensified by potential changing

climate trends. The South Carolina Coastal Risk

Symposium brought together local business

and government and community leaders to

identify strategies and solutions to protect and

insure the coastal region. The panel discussion

was hosted in partnership with the City of

Charleston; the South Carolina Department

of Insurance; The H. John Heinz III Center for

Science, economics and the environment; Ceres;

and the Independent Insurance Agents & Brokers

of South Carolina.

JoanWoodward,TheTravelersInstitute;DebCallahan,TheHeinzCenter;andCharleston Mayor Joseph P. Riley

5travelersinstitute.com

The Travelers Institute chose South Carolina for its first

symposium because of the state’s strong commitment to

public-private partnerships to protect its coast as well as

its dedication to coastal mitigation and a stable insurance

regulatory environment. Moderated by Joan Woodward,

TravelersExecutiveVicePresident,PublicPolicy,andPresident

of the Travelers Institute, the panel included:

• TheHonorableMayorJosephP.Riley–

Mayor, City of Charleston, South Carolina;

• LeslieJones–

Deputy Director for Actuarial Market and Alternative Risk

Transfer Services, South Carolina Department of Insurance;

• DebCallahan–

President,TheHeinzCenter;

• SharleneLeurig–

Senior Manager of Insurance Program, Ceres;

• EricNelson–

VicePresident,EnterpriseCatastropheStrategyand

Analysis, Travelers

Mayor Riley, serving in his ninth term as mayor of Charleston,

spoke of the initiatives the city has implemented to foster coastal

resiliency, which include enforcing stringent building codes and

prudentlyanalyzingtheimpactofdevelopment.Heemphasized

the need for a stable insurance market so that the average

person can be adequately insured at an affordable price.

Representing the South Carolina Department of Insurance,

Leslie Jones spoke about the importance of mitigation to help

manage insurance costs. Established in 2007, the SC Safe Home

Program offers grants for South Carolinians to make their

property more resistant to hurricane wind damage. To date,

909 grants have been awarded totaling nearly $4.5 million. She

also said that equally important is the need for market-based

regulatory reforms to create a consistent insurance market

for coastal properties. According to Ms. Jones, South Carolina

has been “laser focused” on coastal insurance since 1989,

when Hurricane Hugo ravaged much of its coastline, causing

$4.2 billion in insured losses. She acknowledged the only way

to truly solve the coastal property insurance crisis is through

collaboration and dialogue among key stakeholders.

DebCallahan,PresidentofTheHeinzCenter,anonprofit,

nonpartisan think tank dedicated to improving the scientific

and economic foundation for environmental policy, highlighted

recommendations from the recently completed Resilient

CoastsBlueprint.DevelopedbyTheHeinzCenterandCeres,

the Blueprint recommends action steps to adapt to changing

climate trends to protect America’s coastlines. According to

Ms.Callahan,TheHeinzCenterbelievesthatproperty

losses can be cut more than 50 percent by implementing

and enforcing strong building codes, steering development

awayfromlandconsideredhazardous,constructingcoastal

infrastructure with an eye to climate change resilience and

protecting and restoring coastal wetlands. The Blueprint

is endorsed by The Travelers Institute, Mayor Riley and

other leaders in insurance, government, non-governmental

organizationsandacademia.

Representing Ceres, a coalition of institutional investors and

environmental groups that runs the Investor Network on

Climate Risk, Sharlene Leurig spoke about the increased risks

that extreme weather events pose to insurability and the

economic interests of the coalition’s members. Ms. Leurig

cited Hurricane Katrina as a stimulus for the insurance

industry to work with others to address practices that make

society vulnerable to extreme events. Insurers have joined the

environmental community and taxpayer advocacy groups to

Tommy Cook, John T. Cook & Associates; Jules Anderson, Anderson Insurance Associates;andFrankSheppard,IndependentInsuranceAgents&Brokersof South Carolina

6 travelersinstitute.com

lobby for insurance rates that adequately reflect real risk and

federal programs to assist property owners in reducing their

risk.Forexample,theNationalFloodInsuranceProgrammust

be reformed to achieve financial stability in order to pay claims.

Further,Ms.Leurigbelievesinnovativefinancialmechanisms

should be explored in order to maintain a viable insurance

market and create affordability for consumers while allowing

insurers to remain solvent and serving customers, even after

catastrophic storms.

Citing the dramatic increase in coastal development, increased

frequency and severity of weather events, along with

underfunded government insurance programs, Eric Nelson

of The Travelers Companies, Inc. called for prompt action to

address the coastal insurance crisis. He presented the Travelers

Coastal Wind Zone Plan as a comprehensive, private market

approach to help improve the availability and affordability of

coastal windstorm insurance for homeowners (see page

23 for a complete description of the Travelers Coastal Wind

Zone Plan).

The symposium’s audience of community leaders, legislators

and insurance agents was generally supportive of the panelists’

recommendations and discussed next steps and a desire for

continued local forums. The policy discussion reinforced that

long-term solutions for protecting the Gulf and Atlantic coasts

will come from a broad base of leaders collaborating and urging

federal and state legislators to action. The lessons learned at

the South Carolina Coastal Risk Symposium will serve as the

foundation for future symposia in other coastal states that will

lead to action to improve the affordability and accessibility of

catastrophic wind insurance for coastal homeowners.

Sharlene Leurig, Ceres; Eric Nelson, Travelers; and Leslie Jones, South Carolina Department of Insurance

7travelersinstitute.com

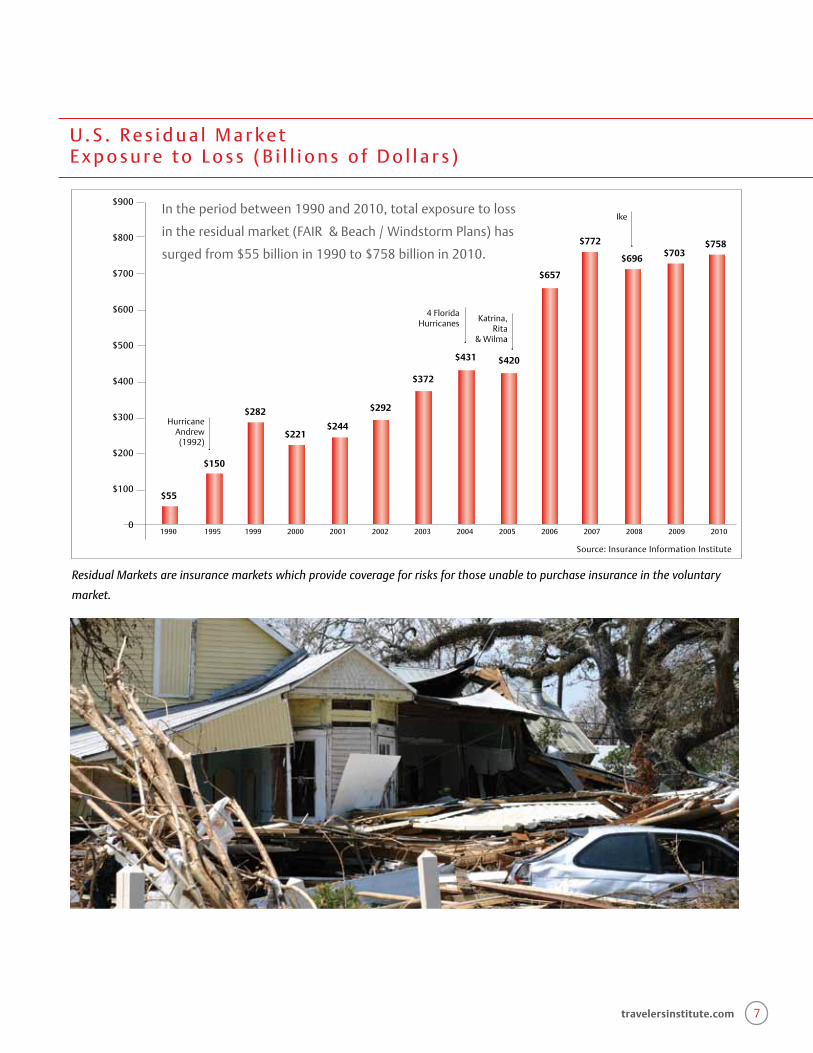

1990 1995 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

$900

$800

$700

$600

$500

$400

$300

$200

$100

0

Hurricane Andrew(1992)

4FloridaHurricanes

Ike

Katrina, Rita

& Wilma

In the period between 1990 and 2010, total exposure to loss

intheresidualmarket(FAIR&Beach/WindstormPlans)has

surged from $55 billion in 1990 to $758 billion in 2010.

$55

$150

$282

$221$244

$292

$372

$431 $420

$657

$772

$696 $703$758

U . S . Re s i d u a l M a r ke t E x p o s u r e t o L o s s ( B i l l i o n s o f D o l l a r s )

Source: Insurance Information Institute

Residual Markets are insurance markets which provide coverage for risks for those unable to purchase insurance in the voluntary

market.

8 travelersinstitute.com

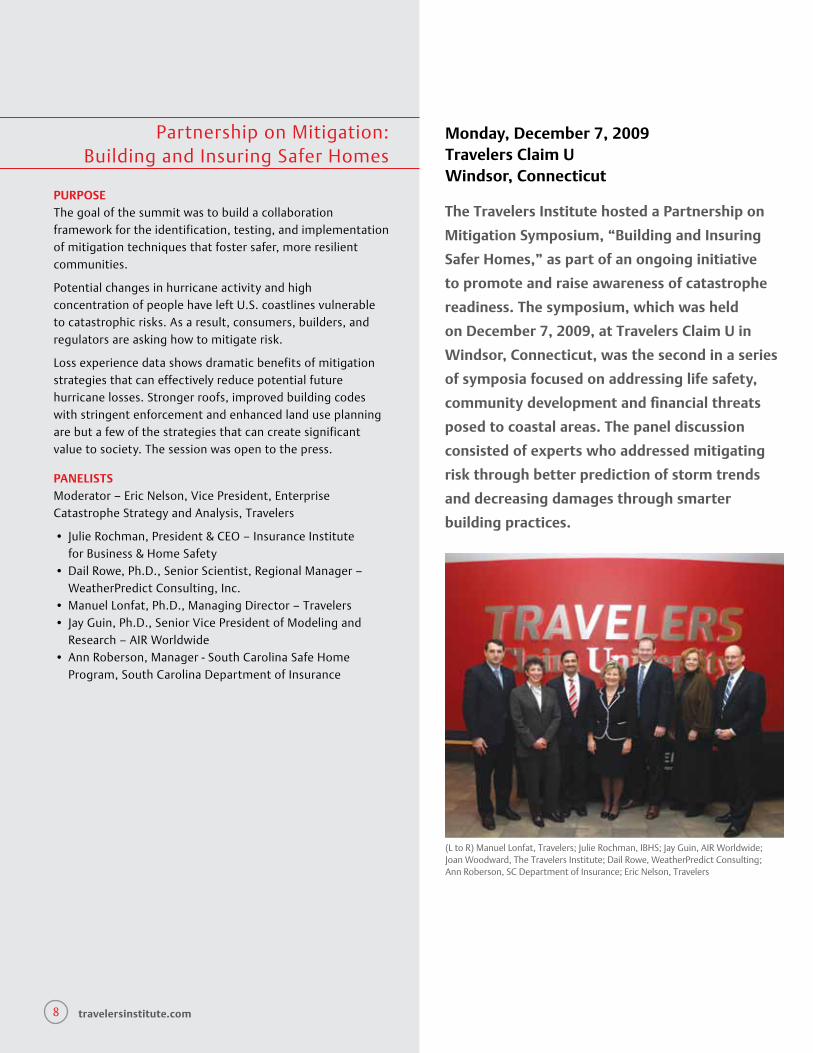

Partnership on Mitigation: Building and Insuring Safer Homes

The Travelers Institute hosted a Partnership on

Mitigation Symposium, “Building and Insuring

Safer Homes,” as part of an ongoing initiative

to promote and raise awareness of catastrophe

readiness. The symposium, which was held

on December 7, 2009, at Travelers Claim u in

Windsor, Connecticut, was the second in a series

of symposia focused on addressing life safety,

community development and financial threats

posed to coastal areas. The panel discussion

consisted of experts who addressed mitigating

risk through better prediction of storm trends

and decreasing damages through smarter

building practices.

(L to R) Manuel Lonfat, Travelers; Julie Rochman, IBHS; Jay Guin, AIR Worldwide; Joan Woodward, The Travelers Institute; Dail Rowe, WeatherPredict Consulting; Ann Roberson, SC Department of Insurance; Eric Nelson, Travelers

Monday, December 7, 2009 Travelers Claim uWindsor, Connecticut

PuRPOSe The goal of the summit was to build a collaboration framework for the identification, testing, and implementation of mitigation techniques that foster safer, more resilient communities.

Potential changes in hurricane activity and high concentration of people have left U.S. coastlines vulnerable to catastrophic risks. As a result, consumers, builders, and regulators are asking how to mitigate risk.

Loss experience data shows dramatic benefits of mitigation strategies that can effectively reduce potential future hurricane losses. Stronger roofs, improved building codes with stringent enforcement and enhanced land use planning are but a few of the strategies that can create significant value to society. The session was open to the press.

PAnelISTS Moderator–EricNelson,VicePresident,EnterpriseCatastrophe Strategy and Analysis, Travelers

• JulieRochman,President&CEO–InsuranceInstitute for Business & Home Safety

• DailRowe,Ph.D.,SeniorScientist,RegionalManager–WeatherPredict Consulting, Inc.

• ManuelLonfat,Ph.D.,ManagingDirector–Travelers• JayGuin,Ph.D.,SeniorVicePresidentofModelingand

Research – AIR Worldwide• AnnRoberson,Manager-SouthCarolinaSafeHome

Program, South Carolina Department of Insurance

9travelersinstitute.com

Connecticut policymakers, community leaders, insurance

agents and media members were among the attendees at the

panel discussion, which focused on how proactive measures to

mitigate losses before a catastrophe can benefit consumers,

government and the economy.

HostedbyJoanWoodward,TravelersExecutiveVicePresident,

Public Policy, and President of the Travelers Institute, and

moderatedbyEricNelson,VicePresident,TravelersEnterprise

Catastrophe Stategy and Analysis the panel included:

• JulieRochman,PresidentandCEO–InsuranceInstitutefor

Business & Home Safety (IBHS)

• DailRowe,Ph.D.,SeniorScientist,RegionalManager–

WeatherPredict Consulting, Inc.

• ManuelLonfat,Ph.D.,ManagingDirector–Travelers

• JayGuin,Ph.D.,SeniorVicePresidentofModelingand

Research – AIR Worldwide

• AnnRoberson,Manager–SCSafeHomeProgram,South

Carolina Department of Insurance

Mr. Nelson set the context for the discussion by noting that

50 percent of Americans live within 50 miles of a coastline with

more people moving there every year. He also suggested that

many experts now agree there is an increasing risk of extreme

weather events for coastal regions. In addition, Nelson identified

a trend of insurance risk shifting to states, regional wind pools,

and the federal government.

Mr. Nelson highlighted the fact that Travelers would soon be

introducing a pilot program to write discounted insurance

policies in select coastal states for homes meeting established

design standards to resist the impacts of tropical storm and

hurricane winds. Qualifying homes will be eligible for up to a

35 percent hurricane premium credit. He explained that building

stronger homes is a key principle of the Travelers Coastal Wind

Zone Plan, the company’s proposal to improve the availability

and affordability of catastrophic wind coverage in communities

along the Gulf and Atlantic coasts. Travelers wants to reward

those who are mitigating the risk of extreme weather events by

building to more stringent codes.

Julie Rochman outlined the efforts of the Institute for Building &

Home Safety (IBHS) to enhance building codes and strengthen

their enforcement across the country. She noted that while

codes vary greatly by region, those areas with stricter codes and

enforcement mechanisms face less impact when storms hit.

Ms.Rochmanalsogaveaprogressreportontheorganization’s

multi-peril research center in Chester County, S.C., which is

scheduled for completion in the summer of 2010. The facility

will be able to simulate Category 3 hurricane winds to test the

strength of residential structures. The research done in this

test facility should help insurers, builders and building product

manufacturers better understand the impact of hurricane force

winds both on the coast and throughout the country where

tornados are prevalent.

(L to R) Ann Roberson; Jay Guin; Manuel Lonfat; Dail Rowe; Julie Rochman; Eric Nelson

Dail Rowe, WeatherPredict Consulting and Julie Rochman, IBHS

10 travelersinstitute.com

Dr. Dail Rowe discussed smaller-scale catastrophe simulations

that are currently performed by WeatherPredict. Demonstrating

that mitigation does not have to be costly to be effective, Dr.

Rowe showed a video of a roof exposed to hurricane winds

before and after the application of AeroEdge™, aerodynamic

devices that enhance resistance to high winds. Inexpensive

techniques developed through simulations can have a significant

impact on securing a structure and reducing losses. Dr. Rowe

pointed out that approximately 90 percent of homes damaged

during hurricanes have roof damage. Although roofs may not

be expensive to repair, roof damage often leads to other losses,

including water intrusion and flooding.

Dr. Manuel Lonfat presented key findings from the Travelers

Personal Insurance catastrophe research team on the

effectiveness of mitigation techniques. He reported that during

Hurricane Ike in 2008, older construction (pre-1995) suffered

more than 70 percent of the losses, although houses from this

era represented only about half of the buildings. Dr. Lonfat said

the research team drilled down deeper into the losses and found

that 85 percent of the claims were linked to roof failures. He

welcomed the research being done by WeatherPredict and IBHS

and noted that it is very valuable for reducing risk.

Dr. Jay Guin supported the findings from Travelers with broader

industry analysis from AIR Worldwide, a catastrophe modeling

company. Dr. Guin outlined important engineering techniques

that can be implemented to enhance the resistance of roofs

and structures overall. Dr. Guin showed photos of two homes in

PuntaGorda,Fla.,followingHurricaneCharleyin2004.Onebuilt

incompliancewith2001Floridabuildingcodestandardsdidvery

well, with minimal damage. However, a similar home constructed

in 1988, in the same neighborhood, suffered thousands of

dollars in damage.

While much of the panel discussion focused on new construction,

the final panelist, Ann Roberson, talked about the success of

the SC Safe Home Program in encouraging mitigation methods

for existing structures. Through incentive programs, consumer

educationandpartnershipswithotherorganizations,SCSafe

Home has built a model program that addresses how public and

private enterprises can help homeowners mitigate their risk.

Travelers applauds the efforts of South Carolina and urges other

states to adopt similar incentives for homeowners to mitigate

their exposure.

Attendees at the summit were receptive to the panelists’

recommendations. They supported the need to communicate

the importance of implementing and enforcing strong building

codes in coastal areas as a way of improving safety and

decreasing the economic consequences of storm damage.

Joan Woodward, The Travelers Institute

Ann Roberson, SC Department of Insurance

travelersinstitute.com 11

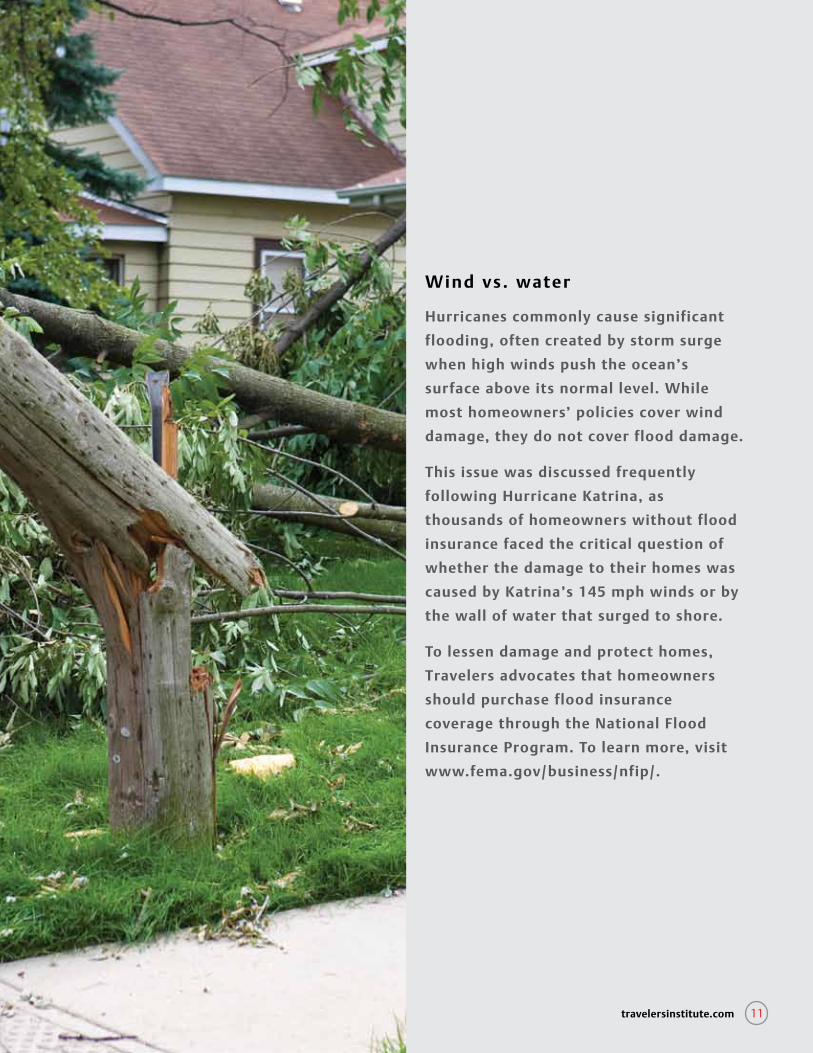

Wind vs . water

Hurricanes commonly cause significant

flooding, often created by storm surge

when high winds push the ocean’s

surface above its normal level. While

most homeowners’ policies cover wind

damage, they do not cover flood damage.

This issue was discussed frequently

following Hurricane Katrina, as

thousands of homeowners without flood

insurance faced the critical question of

whether the damage to their homes was

caused by Katrina’s 145 mph winds or by

the wall of water that surged to shore.

To lessen damage and protect homes,

Travelers advocates that homeowners

should purchase flood insurance

coverage through the national Flood

Insurance Program. To learn more, visit

www.fema.gov/business/nfip/.

12 travelersinstitute.com

Improving Availability and Affordability of Coastal

Windstorm Insurance

The Travelers Institute hosted a panel

discussion entitled, “Improving Availability

and Affordability of Coastal Windstorm

Insurance,” at the May 10, 2010, Regulatory

Roundup, an annual conference of insurance

industry professionals and regulators

from across the country in Austin, Texas.

The Travelers Institute panel presented

strategies and solutions to protect and

insure residential properties on the Gulf and

Atlantic coasts. The panel discussion was

the fourth in a series of events addressing

life safety, community development and

financial threats posed to coastal areas.

EleanorKitzman,FormerSouthCarolinaDirectorofInsuranceandcurrentTexas State Commissioner of Insurance

Monday, May 10, 2010 Hyatt Regency lost PinesAustin, Texas

PuRPOSe As part of the annual Regulatory Roundup, a gathering of insurance industry leaders and regulators convened to discuss pressing issues facing the insurance industry, the Travelers Institute hosted a panel discussion “Improving Availability and Affordability of Coastal Windstorm Insurance.” Discussion topics included improved land use planning and building codes, as well as the maintenance of a strong private insurance marketplace to improve the availability and affordability of named storm wind insurance for coastal homeowners.

PAnelISTS Moderator – Joan Woodward, the Travelers Institute

• EricNelson,VicePresident,EnterpriseCatastrophe Strategy and Analysis, Travelers;

• EleanorKitzman,FormerDirectorofInsurance, South Carolina and current Texas State Commissioner of Insurance;

• DebraT.Ballen,GeneralCounselandSeniorVicePresident of Public Policy, Insurance Institute for Business and Home Safety (IBHS).

13travelersinstitute.com

ModeratedbyJoanWoodward,TravelersExecutiveVice

President of Public Policy and President of the Travelers

Institute, the panel included:

• EleanorKitzman,formerDirectorofInsurance,

South Carolina and current Texas State Commissioner

of Insurance;

• DebraBallen,GeneralCounselandSeniorVicePresidentof

Public Policy, Institute for Business and Home Safety (IBHS);

and

• EricM.Nelson,VicePresident,EnterpriseCatastrophe

Strategy and Analysis, Travelers.

Setting the context for the panel, Ms. Woodward stated,

“The Travelers Institute is committed to participating in

public dialogue with policymakers to contribute to solutions

on matters of importance to our customers, our agents and

brokers, and the communities we serve.” She continued,

“The availability and affordability of named windstorm

insurance is a challenge for many coastal residents, and we

hope to encourage the public and private sectors to work

together to create effective, sustainable solutions to this crisis.”

In outlining South Carolina’s experiences in the residential

coastalpropertyinsurancecrisis,EleanorKitzmansharedthat

while she was the Director of Insurance, the issue of coastal

homeowners insurance consumed about 75 percent of her

time. In 2007, the state adopted several positive reforms

designed to create a consistent insurance market. Among

the reforms were market-based regulatory approaches and

establishment of SC Safe Home, a grant program for South

Carolina coastal homeowners to enhance their property’s

resistance to hurricane wind damage.

“There are few problems that can’t be solved with more

capital. The need several years ago and still today is to attract

new insurance carriers to the coast despite the risk of losses

andvolatileweather,”saidMs.Kitzman.Sheadded,“While

there is no silver bullet, educating consumers and legislators on

the importance of mitigation and building code enforcement

willmoveusclosertostabilizingthemarket.”

Debra Ballen addressed the efforts by IBHS to encourage

homeowners to adopt mitigation techniques and to enhance

building codes and strengthen their enforcement. She reviewed

the IBHS “building performance chain,” a comprehensive

approach which includes appropriate land use planning,

modern building codes, retrofitting of older homes, and

continued maintenance of homes, such as periodic inspections

of the roof and windows.

She also offered a real-life example of the benefits of

mitigation. In 2008, after Hurricane Ike hit the Bolivar Peninsula

in Texas, the only buildings remaining were 10 homes built to

theIBHSFORTIFIEDforSaferLiving® standard.

“While we were thrilled to see the benefits of building more

durable homes, the example of Bolivar Peninsula raises the

larger issue – while 10 homes survived, the community did

not,” said Ms. Ballen. “In order for communities to remain

JoanWoodward,TravelersInstitute;EleanorKitzman,formerSouthCarolinaDirector of Insurance; Debra Ballen, IBHS; Eric Nelson, Travelers

Debra Ballen, Insurance Institute for Business and Home Safety

14 travelersinstitute.com

intact as a result of devastating storms, we need broad

adoption of mitigation techniques and building codes to

minimizethesecatastrophiclosses.”

Additionally, Ms. Ballen gave the audience a preview of the

IBHS research center being built in Chester County, S.C. The

center, slated to open in October 2010, will simulate Category

3 hurricanes, as well as wind-borne hail, rain, and wildfire, and

will be used to identify and promote effective property loss

reduction, and prevention approaches. This research should

provide valuable, objective information for development of

meaningful public policy to reduce property losses.

Eric Nelson presented the Travelers Coastal Wind Zone Plan,

the company’s comprehensive proposal to improve availability

and affordability of coastal homeowners insurance. (see page

23 for a complete description of the Travelers Coastal Wind

Zone Plan)

Mr. Nelson placed particular emphasis on the need for stronger

buildings to lower potential losses from hurricanes. He

provided an example of the impact of mitigation techniques

on reducing losses by reporting key findings from the Travelers

Personal Insurance catastrophe research team. The research

showed that during Hurricane Ike, older construction

(pre-1995) suffered more than 70 percent of the losses;

although houses from this era represented only about half

of the buildings.

The panel presentations and discussion reinforced that the

solution for protecting the Gulf and Atlantic coasts is

dependent upon the maintenance of a strong private

insurance market, greater focus on loss mitigation and risk

management, improved land use planning, and stronger and

enforced building codes.

Bolivar Peninsula after Hurricane Ike in 2008

15travelersinstitute.com

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

30

20

10

0

Andrew$23B totalinsured loss

Charley,Frances, Ivan & Jeanne

$26B totalinsured loss

Katrina, Rita & Wilma$64B total

insured loss

Ike$13B total

insured loss

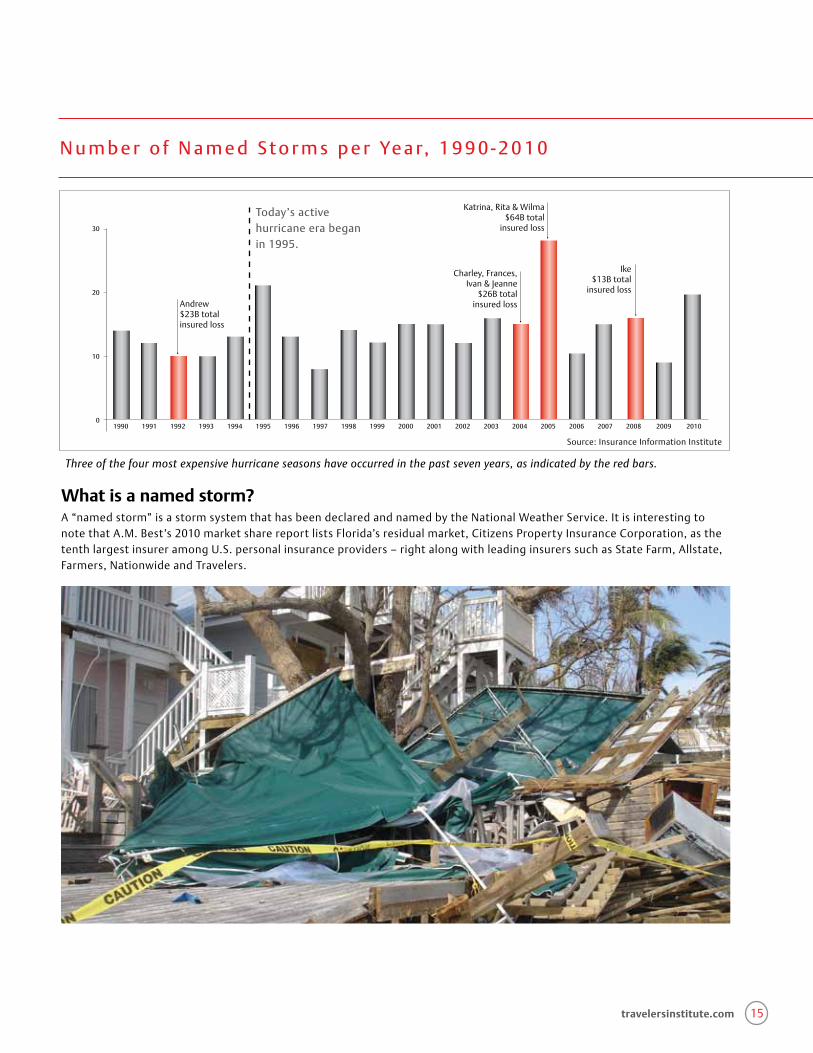

N u m b e r o f N a m e d St o r m s p e r Ye a r, 1 9 9 0 - 2 0 1 0

Three of the four most expensive hurricane seasons have occurred in the past seven years, as indicated by the red bars.

Today’s active hurricane era began in 1995.

Source: Insurance Information Institute

What is a named storm?A “named storm” is a storm system that has been declared and named by the National Weather Service. It is interesting to notethatA.M.Best’s2010marketsharereportlistsFlorida’sresidualmarket,CitizensPropertyInsuranceCorporation,asthetenthlargestinsureramongU.S.personalinsuranceproviders–rightalongwithleadinginsurerssuchasStateFarm,Allstate,Farmers,NationwideandTravelers.

16 travelersinstitute.com

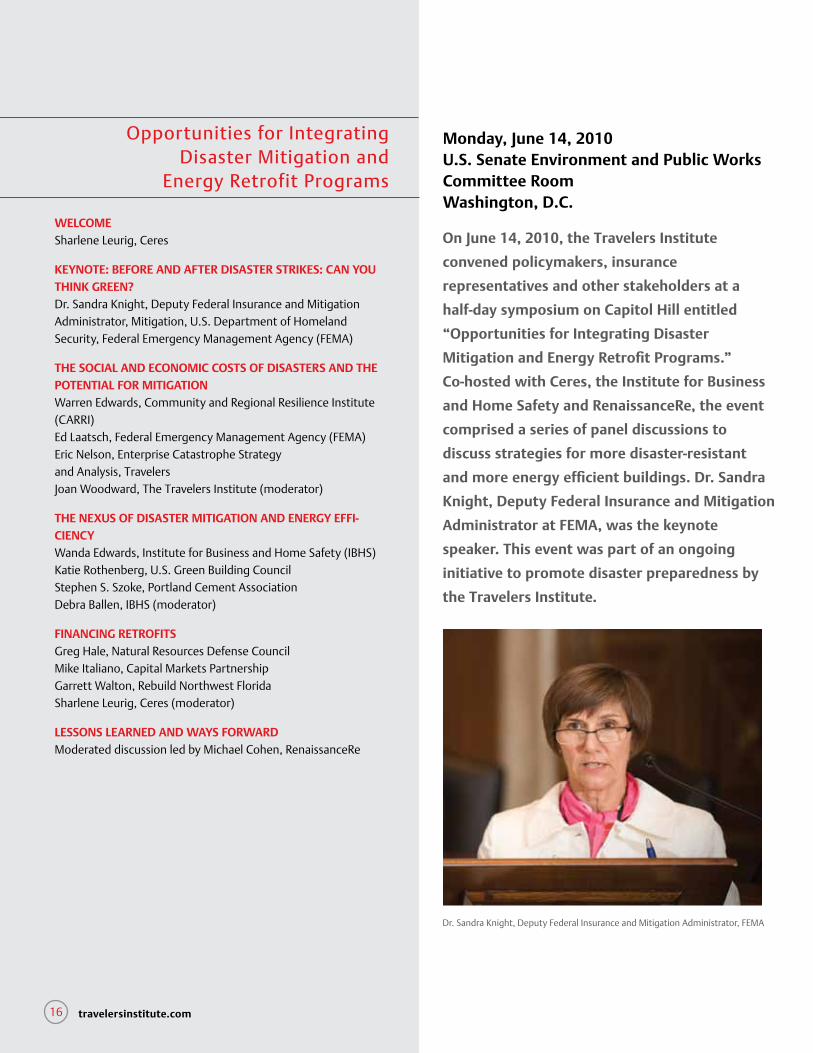

Opportunities for Integrating Disaster Mitigation and

Energy Retrofit Programs

On June 14, 2010, the Travelers Institute

convened policymakers, insurance

representatives and other stakeholders at a

half-day symposium on Capitol Hill entitled

“Opportunities for Integrating Disaster

Mitigation and energy Retrofit Programs.”

Co-hosted with Ceres, the Institute for Business

and Home Safety and RenaissanceRe, the event

comprised a series of panel discussions to

discuss strategies for more disaster-resistant

and more energy efficient buildings. Dr. Sandra

Knight, Deputy Federal Insurance and Mitigation

Administrator at FeMA, was the keynote

speaker. This event was part of an ongoing

initiative to promote disaster preparedness by

the Travelers Institute.

Dr.SandraKnight,DeputyFederalInsuranceandMitigationAdministrator,FEMA

Monday, June 14, 2010u.S. Senate environment and Public Works Committee RoomWashington, D.C.

WelCOMe Sharlene Leurig, Ceres

KeynOTe: BeFORe AnD AFTeR DISASTeR STRIKeS: CAn yOu THInK GReen?Dr.SandraKnight,DeputyFederalInsuranceandMitigationAdministrator, Mitigation, U.S. Department of Homeland Security,FederalEmergencyManagementAgency(FEMA)

THe SOCIAl AnD eCOnOMIC COSTS OF DISASTeRS AnD THe POTenTIAl FOR MITIGATIOnWarren Edwards, Community and Regional Resilience Institute (CARRI)EdLaatsch,FederalEmergencyManagementAgency(FEMA)Eric Nelson, Enterprise Catastrophe Strategy and Analysis, TravelersJoan Woodward, The Travelers Institute (moderator)

THe nexuS OF DISASTeR MITIGATIOn AnD eneRGy eFFI-CIenCy Wanda Edwards, Institute for Business and Home Safety (IBHS)Katie Rothenberg, U.S. Green Building CouncilStephenS.Szoke,PortlandCementAssociationDebra Ballen, IBHS (moderator)

FInAnCInG ReTROFITS Greg Hale, Natural Resources Defense CouncilMike Italiano, Capital Markets PartnershipGarrettWalton,RebuildNorthwestFloridaSharlene Leurig, Ceres (moderator)

leSSOnS leARneD AnD WAyS FORWARD Moderated discussion led by Michael Cohen, RenaissanceRe

17travelersinstitute.com

The Travelers Institute led the day’s first panel discussion,

“The Impact of Disasters and the Potential for Mitigation.”

ModeratedbyJoanWoodward,TravelersExecutiveVice

President of Public Policy and President of the Travelers

Institute, the panel included:

• EdLaatsch,Chief,BuildingScienceSectionRiskReduction

Branch,MitigationDivision,FEMA;

• WarrenEdwards,Director,CommunityandRegional

Resilience Institute (CARRI); and

• EricM.Nelson,VicePresident,EnterpriseCatastrophe

Strategy and Analysis, Travelers.

Setting the context for the panel, Ms. Woodward stated,

“Extreme weather events can cause massive damage, erase

the investments of property owners and displace vulnerable

populations into substandard housing. The Travelers Institute

is committed to collaborating with all stakeholders to advance

and raise awareness of mitigation strategies that create more

resilient communities.”

EdLaatschofFEMAsharedinformationonthemanyprograms

FEMAofferstoencouragemitigation,whichrangefrom

training to partnerships to awareness campaigns. He spoke

indepthonthetoolsFEMAprovidestothepublictoassess

damageandvulnerability,includingtheHazardsU.S.Multi-

Hazard(HAZUS-MH)tool.HAZUS-MHhelpspeopleunderstand

what their exposures are to earthquakes, floods and wind;

make educated decisions in terms of land use planning; and be

prepared for needs that will arise after a disaster.

“The focus after extreme weather events needs to be on

learning what can be done to prevent damage the next time,”

hesaid.“Forexample,thewidespreaddamagetofoundations

along the Gulf Coast resulting from storm surge is something

that needs to be addressed. We begin by issuing this guidance,

which spreads into construction practices and then into

building codes for strong foundation requirements. At the

current rate of construction, after 25 years we could affect half

the built environment.”

Mr. Laatsch also addressed the environmental benefit that

resilientcommunitiesbring.Forexample,ifahomeisstrong

enough to

survive a storm, the contents also survive and aren’t

contributing to debris in landfills. More than 100 tons of debris

filled landfills as a result of Hurricane Katrina.

Warren Edwards discussed the efforts by CARRI to build a

resilient America by focusing at the community level. CARRI

grew out of a project at the Oak Ridge Laboratory in Tennessee

to examine the issue of resiliency. The team spent time

speaking with the private and public sectors and individuals

in three Southeast communities – Memphis, Tenn.; Gulfport,

Miss.; and Charleston, S.C. -- around the concept of resiliency.

JoanWoodward,TravelersInstitute;WarrenEdwards,CARRI;EdLaatsch,FEMA;Eric Nelson, Travelers

Debra Ballen, IBHS; Wanda Edwards, IBHS; Katie Rothenberg, U.S. Green Building Council;StephenS.Szoke,PortlandCementAssociation

18 travelersinstitute.com

Sharlene Leurig, Ceres; Michael Cohen, RenaissanceRe; Joan Woodward, Travelers Institute; Debra Ballen, IBHS

Sharlene Leurig, Ceres; Greg Hale, Natural Resources Defense Council; Mike Italiano,CapitalMarketsPartnership;GarrettWalton,RebuildNorthwestFlorida

Their research found that communities want four things:

• Abetterunderstandingoftheconceptofresilience;

• Ameasurementofcommunityresilience;

• Processesandtoolstoimprovecommunityresilience;and

• Rewardstoencourageeffortstowardresiliency,including

discounts from insurance providers, and grants from the

federal government.

Fromtheresearchgathered,CARRIislaunchingtheCommunity

Resilience Systems Initiative, a system of tools and processes

designed to provide all communities with the action steps

needed to become resilient, regardless of the disasters they

face. The initiative will include best practices from other

communities, measurement tools and suggested processes.

To learn more, visit www.resilientus.org.

Travelers’ Eric Nelson placed particular emphasis on the need

for stronger buildings and consistent building codes to lower

potential losses. He talked about the statewide changes

Floridamadetobuildingcodeadoptionandenforcement

after Hurricane Andrew in August of 1992, citing a 50 percent

difference in loss from homes built pre-Hurricane Andrew and

those built after the hurricane. He encouraged the audience

to imagine the impact federally mandated, consistent

building codes across the country could have on the coastal

homeowners insurance crisis.

He also shared a new initiative by Travelers to insure fortified

homes along the coast. Homes in select states meeting

established design standards to resist the impacts of tropical

storm and hurricane winds are now eligible for up to a 35

percent hurricane premium credit.

“Travelers believes it is up to the public sector to enforce

proper building codes and the private sector to provide rewards

for creating stronger communities,” he said.

Attendees supported the panelists’ recommendations

for the broad adoption of mitigation techniques and the

implementation of incentives for communities that become

more resilient. There was also consensus that solutions will

come from a collective effort, and some attendees plan to form

a working group across sectors to continue conversation and

advance progress.

travelersinstitute.com 19

Coastal l iv ing and coastal proper ties on the increase

More Americans are living along the

coasts every year. According to the u.S.

Department of Commerce and the national

Oceanic & Atmospheric Administration

(nOAA), 53 percent of the nation’s

population live in coastal counties in 2011,

and their populations are expected to grow

by more than 13.6 million by 2020. The

trend is unmistakable.

Additionally, the properties in which

they live are escalating in exposure

value as modest beach bungalows give

way to sprawling homes and skyscraper

condominiums. In 2011, the collective

value of all coastal properties from Texas

to Maine is estimated by the Insurance

Information Institute (III) to be nearing

$9 trillion, with $2 trillion of that coastal

property concentrated in Florida. A

significant portion of those estimates are

residential properties.

In addition, “coastal” property perhaps

should no longer be defined as properties

with ocean views, but rather viewed

as properties that are vulnerable to

hurricanes – as far inland as 150 miles.

20 travelersinstitute.com

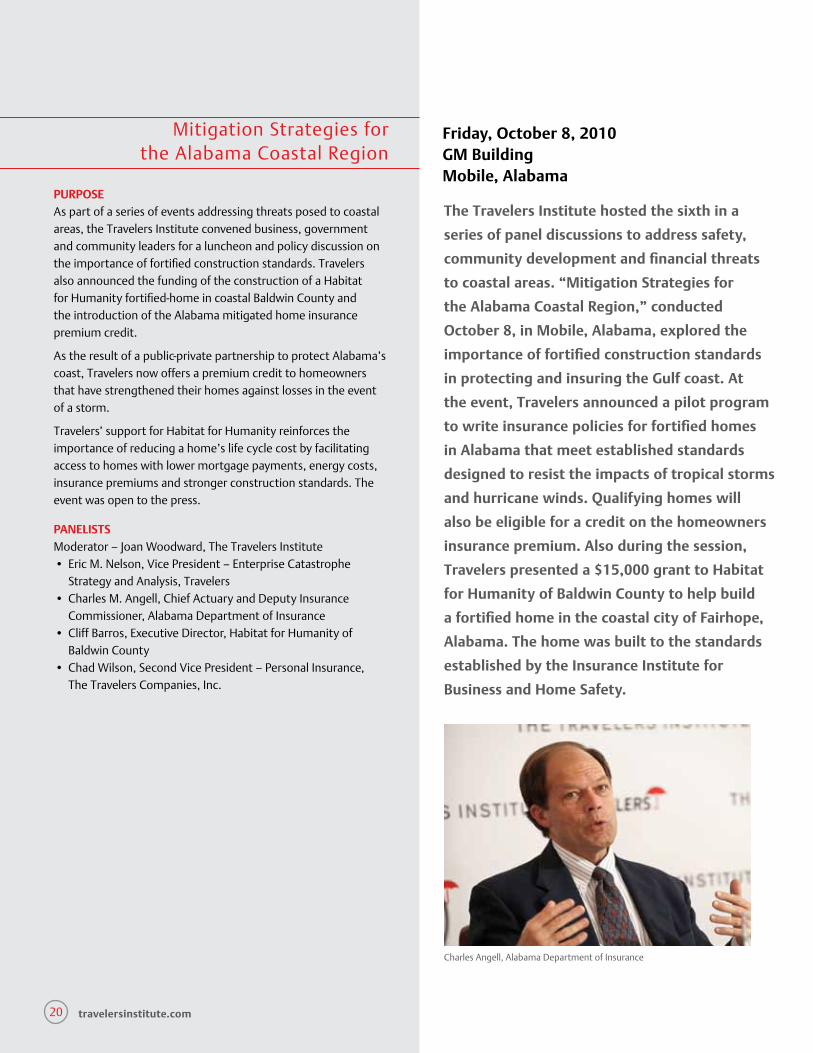

Mitigation Strategies for the Alabama Coastal Region

The Travelers Institute hosted the sixth in a

series of panel discussions to address safety,

community development and financial threats

to coastal areas. “Mitigation Strategies for

the Alabama Coastal Region,” conducted

October 8, in Mobile, Alabama, explored the

importance of fortified construction standards

in protecting and insuring the Gulf coast. At

the event, Travelers announced a pilot program

to write insurance policies for fortified homes

in Alabama that meet established standards

designed to resist the impacts of tropical storms

and hurricane winds. Qualifying homes will

also be eligible for a credit on the homeowners

insurance premium. Also during the session,

Travelers presented a $15,000 grant to Habitat

for Humanity of Baldwin County to help build

a fortified home in the coastal city of Fairhope,

Alabama. The home was built to the standards

established by the Insurance Institute for

Business and Home Safety.

Charles Angell, Alabama Department of Insurance

Friday, October 8, 2010GM BuildingMobile, Alabama

PuRPOSe As part of a series of events addressing threats posed to coastal areas, the Travelers Institute convened business, government and community leaders for a luncheon and policy discussion on the importance of fortified construction standards. Travelers also announced the funding of the construction of a Habitat for Humanity fortified-home in coastal Baldwin County and the introduction of the Alabama mitigated home insurance premium credit.

As the result of a public-private partnership to protect Alabama’s coast, Travelers now offers a premium credit to homeowners that have strengthened their homes against losses in the event of a storm.

Travelers’ support for Habitat for Humanity reinforces the importance of reducing a home’s life cycle cost by facilitating access to homes with lower mortgage payments, energy costs, insurance premiums and stronger construction standards. The event was open to the press.

PAnelISTS Moderator – Joan Woodward, The Travelers Institute• EricM.Nelson,VicePresident–EnterpriseCatastrophe

Strategy and Analysis, Travelers• CharlesM.Angell,ChiefActuaryandDeputyInsurance

Commissioner, Alabama Department of Insurance• CliffBarros,ExecutiveDirector,HabitatforHumanityof

Baldwin County• ChadWilson,SecondVicePresident–PersonalInsurance,

The Travelers Companies, Inc.

21travelersinstitute.com

ModeratedbyJoanWoodward,TravelersExecutiveVice

President of Public Policy and President of the Travelers Institute,

the panel included:

• CharlesM.Angell,ActingDeputyCommissioner&Casualty

Actuary, Alabama Department of Insurance;

• CliffBarros,ExecutiveDirector,HabitatforHumanityof

Baldwin County;

• EricM.Nelson,VicePresident,EnterpriseCatastrophe

Strategy and Analysis, Travelers; and

• ChadWilson,SecondVicePresident,

Personal Insurance, Travelers.

Setting the context for the panel, Ms. Woodward noted that the

Travelers Institute was formed to participate in public dialogue

with policymakers and to contribute to solutions on matters

of importance to the communities that Travelers serves. She

told attendees that protecting and insuring the Gulf coast is an

important issue for the Travelers Institute. She talked about the

Travelers Institute’s ongoing commitment to finding solutions

that protect residents and their property before the storm hits in

ordertominimizedamagetopropertyanddisruptiontolives.

Charles Angell outlined Alabama’s experiences in the residential

coastal property insurance crisis. He shared that the availability

and affordability of homeowners insurance has become a social

problem in Alabama, a state with a working coast. In order to

lower coastal homeowners insurance premiums, Alabama now

requires insurers to offer discounts to homeowners who build

and retrofit their homes to fortified standards. To encourage

more residents to build fortified and retrofit their homes,

Mr. Angell shared his hopes of eventually launching a state-run

grant program to assist residents with the costs of fortifying

their homes.

Cliff Barros discussed the tendency for low-income homeowners

to become underinsured in order to save money. He explained

that Habitat for Humanity has turned to mitigation techniques

asonesolutionfortheirhomeowners.Theorganizationrecently

launchedtheFortifiedExperiment,aprojecttobuildthree

differenthomesthatwilltestthelong-termcost/benefitof

building to fortified construction standards. The first home built

was a fortified concrete home with a concrete roof. The next

home, to be built in 2011 with funding from Travelers, will be

a fortified concrete home with a shingled roof. The final home

in the experiment will be a typical wood construction with a

fortified roof and windows. Mr. Barros told attendees that they will

compare the insurance and energy costs of the three homes to

determine the smartest way to build strong, affordable housing in

the future. To learn more, visit www.baldwinhabitat.org

Bob Schurke, Travelers; Cliff Barros, Habitat for Humanity of Baldwin County; Joan Woodward, Travelers Institute; and Arden Schell, Habitat for Humanity of Baldwin County Board of Directors

Cliff Barros, Habitat for Humanity of Baldwin County; Charles Angell, Alabama Department of Insurance; Joan Woodward, Travelers Institute; Eric M. Nelson, Travelers; Chad Wilson, Travelers

22 travelersinstitute.com

Eric Nelson provided background on the insurance availability

and affordability crisis coastal homeowners face. He shared the

statistic that 50 percent of the U.S. population is living within

50 miles of the coast. At the same time, many experts now

agree there is a greater likelihood of extreme weather events

intensified by potential changing climate trends. Mr. Nelson

also identified a trend of insurance risk being shifted to states,

regional wind pools, and the federal government. Mr. Nelson

presented the Travelers Coastal Wind Zone Plan, the company’s

comprehensive proposal to improve availability and affordability

of coastal homeowners insurance (see page 23 for a complete

description of the Travelers Coastal Wind Zone Plan).

Newer building codes and mitigation techniques are reducing

losses, according to Nelson, who pointed to findings from the

Travelers Personal Insurance catastrophe team. The research

showed that during Hurricane Ike, older construction (pre-1995)

suffered more than 70 percent of the losses, though houses from

this era represented only about half of the buildings.

Chad Wilson detailed of the Travelers pilot program in Alabama

to write insurance policies for fortified homes that meet

established standards designed to resist the impacts of tropical

storm and hurricane winds. The company is opening up areas

of eligibility for these homes to a broader geographic area, and

is now accepting applications for coverage up to $1 million in

insurance limits. Mr. Wilson also announced that Travelers is

marketing the Alabama insurance premium discount for fortified

homes. The company is offering policyholders of qualifying

homes a credit of up to 35 percent on their homeowners

insurance premium. Mr. Wilson told attendees that Travelers

recognizesthathomeownersshouldberewardedfortaking

steps to mitigate damage to the homes they insure.

The audience of insurance agents, government officials, and

builders supported the panelists’ recommendations for broad

adoption of fortified construction standards as part of the

long-term solution needed to protect Gulf coast residents

and property.

Cliff Barros, Habitat for Humanity of Baldwin County, and Charles Angell, Alabama Department of Insurance

23travelersinstitute.com

The united States faces a coastal insurance crisis

Hurricanes, tropical storms, and coastal property insurance

are subjects that unfortunately only generate public

discussion and search for answers at times of crisis. In 2005,

these topics were at the forefront, following a record $57

billion in insured losses and 3.3 million claims resulting from

Hurricanes Katrina, Rita, Wilma and Dennis.1 The 2006 and

2007 hurricane seasons produced no catastrophic landfalls in

the United States, and the coastal homeowners’ market

continued to erode. In 2008, when Hurricane Gustav slammed

into Louisiana and Hurricane Ike into Texas, they brought

renewed discussion but little improvement in the coastal

insurance marketplace. In 2011, Hurricane Irene hit the United

States, causing more than $7.3 billion in damages.2

This crisis of availability and affordability of named storm

coastal wind insurance warrants public attention now,

particularly given that experts are warning that we have

entered into a period of warming ocean temperatures, which

may result in an increase in the frequency and severity of

catastrophic storms for years to come. Trends in Atlantic

hurricane seasons generally span multiple decades, and

today’s active hurricane era began in 1995, so we could face

increased activity for some time.

To the extent that named storm activity increases, finding

insurance for wind coverage at affordable prices, if at all,

fromproperlycapitalizedinsurancecarriers,willbecome

increasingly difficult for coastal homeowners. As a result of

availability and affordability issues, significantly more coastal

homeowners now purchase insurance through state-created

residual market pools, so-called “insurers of last resort.”

(See chart on page 7.) Many of these pools are heavily

subsidizedbystategovernments–which,ineffect,resultin

subsidies for those living on the coast by those living inland. In

addition, many state pools rely on post-event bonding to pay

claims. Given today’s historic financial turmoil, one might

question the ability of even the most creditworthy state

programs to secure adequate financing following a major

catastrophic event.

Clearly, many consumers, public officials and insurers face a

major challenge in finding and funding coastal property

windstorm insurance; and there is a need for a responsible,

comprehensive solution to this insurance problem.

Travelers Coastal Wind zone Plan offers a solution

Travelersrecognizesthatthiscrisisisnotgoingtobesolved

singlehandedly by one company, one industry, or one state.

Effective and sustainable solutions can only come from the

coordinated efforts of all the stakeholders, and we believe

that the insurance industry has a leadership role to play in

the solution as individuals historically have looked to our

industry to protect their greatest asset and largest economic

obligation – their home.

At Travelers, we sought input from members of Congress;

other federal, state, and local officials; consumer groups;

insurance agents and brokers; and other insurance

industry leaders as we developed the comprehensive set

of principles that make up our Coastal Wind zone Plan.

This plan proposes a private, market-based system, without

federal subsidies for insurers, to address the problems of

homeowners’ insurance availability that coastal consumers

face today.

The comprehensive plan would provide the needed framework

to assist America’s coastal families in preparing to rebuild, repair

and recover from the aftermath of named storm catastrophes.

Travelers Coastal Wind Zone Plan: A Comprehensive Plan to Improve Availability and Affordability of Named Storm Wind Insurance for Coastal Homeowners

1 Insurance Information Institute2 National Oceanic and Atmospheric Administration

24 travelersinstitute.com

1. A stable and consistent regulatory environmentThe impact of constantly changing rules on the willingness

of insurers to commit capital in high-risk coastal markets is

underestimated and underappreciated. If an insurer does not

have confidence in the predictability and stability of the

regulatory environment, it cannot have confidence in the

underwriting decisions it is making; and under those

circumstances, it cannot be expected to make substantial

commitments of capital. In fact, the lack of predictability and

stability of the regulatory environment has been an issue in

states along the Gulf and Atlantic Coasts. A predictable and

stable set of rules is a necessary condition to insurers making

long-term commitments of capital. We propose that an

independent federal commission establish standards and rules

for coastal named windstorm rating and underwriting. This

commission would oversee this narrow portion of the

homeowners’ insurance market in the 18 coastal states.

The remainder of the homeowners’ insurance market would

remain subject to state regulation as it currently is today.

2. Transparency in calculation of premiumInthecoastalwindzonestates,underthisconcept,insurance

companies would individually and competitively set risk-based

and actuarially sound rates using approved standards and

certified windstorm risk models approved by the federal

commission. The proposed federal commission would certify

models after reviewing and validating underlying model

assumptions such as frequency, severity, vulnerability and

mitigation factors. This would ensure that rates are set in a

transparent manner. In addition, we endorse creating a rating

calculation mechanism to generate premium credits for

customers if models and actual experience become

misaligned over time such that actual losses are less than

predicted. This would eliminate the perception of insurers

“winning” and customers “losing.”

3. Cost-based federal reinsurance mechanism with savings passed on to consumers

To improve affordability and availability of insurance, we

envision the creation of a federal cost-based reinsurance

mechanism for extreme events, such as an event with losses

that are multiples of those arising out of Hurricane Katrina. In

order to provide financial protection for the unlikely, yet

possible, occurrence of multiple events within one year,

reinsurance coverage should be applied on a seasonal

aggregate basis. The reinsurance would be made available to

insurers at cost by the federal government so there would be

no subsidy, and insurers would be obligated to pass the

savings directly to their customers. This concept would

prevent any federal “bailout.”

4. Mitigation against losses Inthecoastalwindzonestates,mitigationmustbea

centerpiece of any effective catastrophe insurance proposal,

and there should be federal guidelines for strong building

codes, federal incentives for state and local adoption and

enforcement of those codes, enhanced construction

technology and land use planning requirements. In addition,

there should be meaningful premium credits for mitigation

and consideration of state and local property tax incentives

for retrofitting houses.

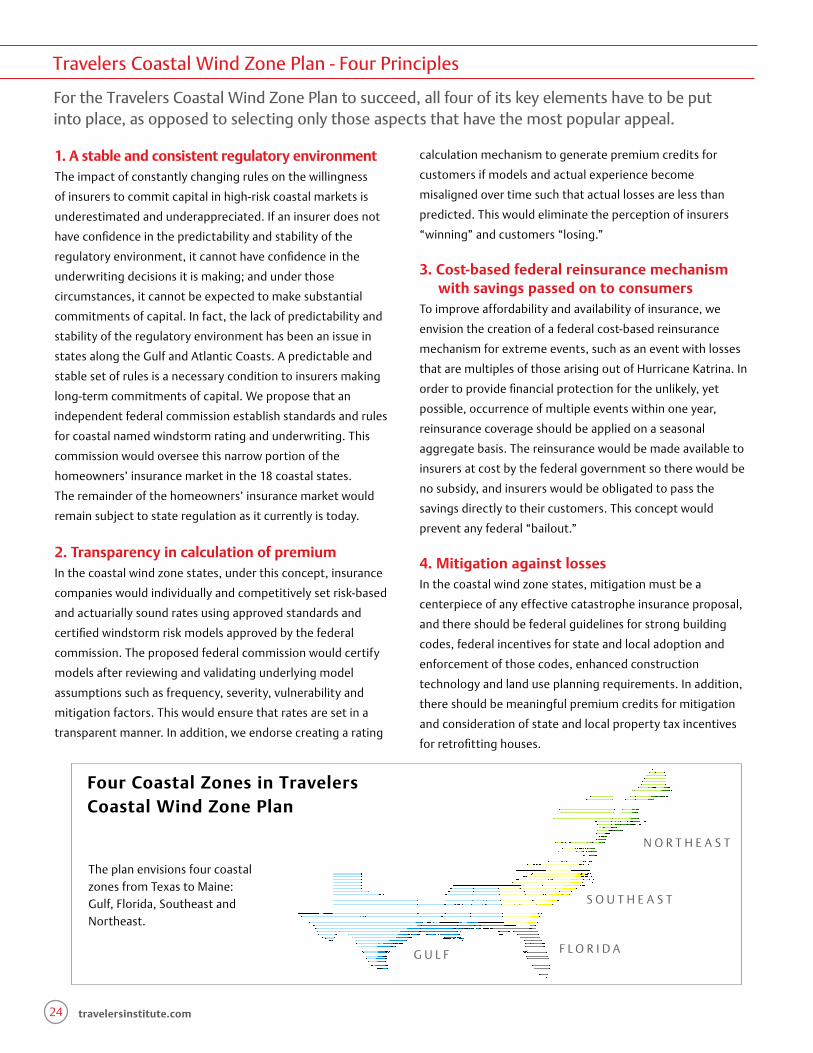

Travelers Coastal Wind Zone Plan - Four Principles

For the Travelers Coastal Wind Zone Plan to succeed, all four of its key elements have to be put into place, as opposed to selecting only those aspects that have the most popular appeal.

G U L F F L O R I D A

S O U T H E A S T

N O R T H E A S T

Four Coastal zones in Travelers Coastal Wind zone Plan

The plan envisions four coastal zonesfromTexastoMaine:Gulf,Florida,SoutheastandNortheast.

25travelersinstitute.com

•TheCoastalWindZonePlanisfairtoallhomeowners – across the united States.

This plan is based on the basic tenet of insurance, which is

to spread the risk among as many people as possible who are

subject to that same risk. Under the Travelers Coastal Wind

Zone Plan, only those with named windstorm exposure would

pay the premiums for the coverage, and there should be no

direct subsidy or other financial support from policyholders

with limited or no exposure to such storms.

Also,individualswithinthecoastalzoneswillbecharged

a premium commensurate with their risks, so people living

in higher risk areas would pay more than those living in

lower risk areas, and those living in lower risk areas would not

besubsidizingthoseinhigherriskareas.Asaresult,some

homeowners will be faced with increased premiums, and

significantly so. However, the impact of the proposed federal

reinsurance mechanism and non-insurance subsidies, such as

tax credits or direct government payments, means that

those who can least afford risk-based pricing should receive

some relief.

Several additional features of the Coastal Wind Zone Plan

make the coastal property insurance system fairer to

homeowners, including the transparency in ratemaking

(with the unique rating calculation mechanism to realign

premiums over time when the wind does not blow),

consumer protections, and assistance in protecting homes.

•TheCoastalWindZonePlanleavesthebusinessofinsurance to those who know it best – and that’s important when it comes to disaster recovery.

Unlike other plans that put federal and state governments

in the catastrophic insurance business, the Travelers Coastal

Wind Zone Plan leaves the business of providing insurance

coverage and responding to catastrophic losses to the private

market. At Travelers, for example, we have a national

Catastrophe Management Center that provides operational

and logistical support to our catastrophe response efforts.

Travelers’state-of-the-artClaimTrainingFacilitygives

Travelers claim professionals the in-depth training, Claim U,

and expertise needed to provide knowledgeable, accurate

and efficient claim service. A key component of our response

strategy is the deployment of highly trained claim

professionals drawn from our dedicated Catastrophe

Response Team and across our entire claim enterprise.

Our field catastrophe response efforts are supported by a

fleet of five Mobile Claim Headquarters vehicles and six claim

customer service centers staffed around the clock to ensure

customers can report claims 24 hours a day, 7 days a week.

The public market is not similarly equipped and cannot be

expected to provide the same level of speed, efficiency, and

customer service at a time when homeowners are at their

most vulnerable.

•TheCoastalWindZonePlancreatesastablemarket– for both insurers and customers.

Historically, at times, insurers have been faced with a situation

in which the rules put in place before a storm – in other words,

the rules under which those insurers based underwriting

decisions and committed capital to support the policies

written – were not the same as the rules adopted following a

storm. Constantly changing rules adversely impacted the

willingness of insurers to do business in high-risk coastal

markets. That has caused disruption for customers in the form

of non-renewals and fewer insurance availability options.

Moving responsibility for named storm wind coverage to an

independent federal commission would provide for a more

stable and consistent regulatory climate across the Gulf and

Atlantic Coasts. That would enable insurers to provide

catastrophic wind insurance, and consumers to obtain and

keep it, with greater certainty. A stable set of rules would

encourage insurers to make long-term business and capital

commitmentstothosezonesfornamedstormwindrisks,

increasing the availability of that insurance over time. Insurers

writingnamedstormwindcoverageinthezoneswouldbe

subject to federal oversight, and the remainder of the

homeowners’ coverage would continue to be regulated by

the states.

Features of Travelers Coastal Wind Zone Plan:

26 travelersinstitute.com

Byrecognizingthathurricanesdon’trecognizestateborders,

thezone-basedapproachprovidesamoreconsistentandfair

market throughout the Gulf and Atlantic coastal states. In

doing so, the plan responds to discrepancies that exist state to

state.Forconsumers,astheymovefromstatetostatewithin

azone,theirnamedstormwindinsurancewouldbesubjectto

the same set of rules, and they would have additional peace of

mind since insurers would be able to offer them coverage on a

more consistent basis.

•TheCoastalWindZonePlanprovidesfederalreinsurance to improve affordability in high-risk areas.

To improve affordability and availability of named storm wind

insurance, the plan calls for the creation of a federal reinsurance

mechanism for extreme events, such as an

event with losses that would be multiples of those arising out of

Hurricane Katrina. The federal reinsurance would

be made available to insurers at cost so there would be no

taxpayer subsidy, and insurers would be obligated to pass the

savings directly to their customers. The independent federal

commission would determine the premiums charged insurers,

oversee the operation of the reinsurance mechanism –including

payment of its claims – and ensure that savings are identified

and passed on to customers in the premiums they pay.

The intent is not to replace the private reinsurance market,

but rather to complement private reinsurance in the case

of “the biggest of the big” event. In order to provide financial

protection for the unlikely, yet possible, occurrence of multiple

events within one year, reinsurance coverage should be

applied on a seasonal aggregate basis. The federal commission

would be given the authority to adjust the loss level to which

themechanismrespondsifmarketstabilizationrequires

such action.

•TheCoastalWindZonePlanmakesinsuranceratemaking more transparent.

This plan, through its transparent process of setting rates, will

take much of the mystery out of named storm wind insurance

ratemaking for consumers and policymakers. As a result of this

plan, a new independent federal commission of five members

appointed by the President of the United States and confirmed

by the U.S. Senate, would be created to establish rating and

underwriting standards and oversee insurers writing this

coverage. Insurers would be required to file rates with the

federal board, which would be reviewed for compliance with

approved standards.

BeginningwithHurricaneAndrewin1992,insurersrealized

the need for better information to measure and understand

their coastal exposure, and they began to use catastrophe

models more extensively. The models factored in many

considerations,includingstormtrack,intensityandsizeof

past landfall events, as well as estimates of what their losses

would be today if those same events occurred. Because of

variable factors such as climate and demographics, the models

are not precise predictors, causing some to question heavy

reliance on them. Coastal states have differing views on the

acceptability and the use of models.

The plan does not envision the federal commission developing

its own model, but rather evaluating and certifying wind risk

catastrophe models developed by firms and insurers. This

improves past practices of leaving that task to various state

regulators and the insurance industry itself to evaluate, and

leaving consumers to wonder about the models’ reliability.

Everyone should have a better understanding of why rates are

what they are, the role of models in ratemaking and what

happens when the wind does and does not blow.

27travelersinstitute.com

•TheCoastalWindZonePlantakesintoaccounttheunpredictability of weather.

Weather losses are predictable only over the long term. While

everyone agrees that rates for property wind insurance should

be fair and equitable, often those rates can appear to be

misaligned with experience in any given year or even multiple

years. Also, significant losses one year can erase premiums and

profits from several years or more. Hurricane Andrew wiped

out all of the premiums collected by the insurance industry on

propertypoliciesinthestateofFloridaforalloftheyears

leading up to it.

To address the unpredictability of weather, the Coastal

Wind Zone Plan, through its unique Rating Calculation

Mechanism, assures that premium credits will be

generated if actual experience and wind risk models

become misaligned over time. Essentially, the process,

which would be transparent to regulators and consumers,

involves using certified exposure-based models to set

predetermined loss levels, then measuring experience against

those predetermined levels. Annual accounting reports would

be filed by each insurer with the independent federal

commission to ensure disclosure of losses paid against

predetermined loss levels. Over time, if actual experience is

less than the predetermined loss level, then a prospective

premium credit would be issued.

•TheCoastalWindZonePlanfocusesonpreventionand incentive measures for stronger homes.

One of the four principles of the Coastal Wind Zone Plan

advocates federal building code guidelines for wind-resistant

homes and incentives for state and local governments to

adopt and enforce those codes. Experience from recent

hurricanesinFloridashowstheimpactofwell-designedand

enforced building codes on reducing losses from windstorms.

The Institute for Business and Home Safety reported that if

allofsouthFlorida’shomesmetstrongbuildingcode

requirements, residential losses from a storm similar to

that of Hurricane Andrew would be cut in half – resulting

in lower insurance premiums. As we all know, premium

charges consider prior loss experience, so the smaller the

potential future losses, the lower the cost of insurance.

There should also be incentives to assist homeowners in

retrofitting their current homes so that their residences

are better able to withstand destructive catastrophic

windstorms. We advocate that federally funded incentive

programs should be adopted. State programs such as

MyFloridaSafeHomeandSouthCarolina’sSafeHome

Loss Mitigation Program, have been very effective but

need to be expanded with more grant funds being made

available. In addition, other coastal states should adopt similar

retrofitting assistance programs.

A key issue in the mitigation of damage to existing homes and

in new construction is the cost-effectiveness of suggested

improvements since homeowners are reluctant to enact

expensive measures. In response to those concerns, a team of

researchersatFloridaInternationalUniversitytested8-dring

shank nails for two years, finding that the rings along the nail’s

shaft double the resistance of a roof to high winds when the

nails were used to attach sheathing to roof rafters. The nails

have been required in Miami-Dade and Broward Counties since

2004 and only add about $10 to the cost of building a home.

Also, it’s important that homeowners heed warnings from

local authorities to prepare their homes appropriately when a

hurricane is approaching. Important just-in-time steps include

shuttering or boarding up windows, anchoring or securing all

outside equipment, and shutting off all power supplies.

To learn more about the Travelers Coastal Wind Zone Plan:If you are interested in the Travelers Coastal Wind Zone Plan, please visit travelersinstitute.com.

28 travelersinstitute.com

Travelers… believes that private insurers have a responsibility to put forth ideas to address the complex economic and social issues related to hurricane risk. Through the Travelers Institute, we combine insurance expertise with thought leadership — ideas gathered from federal, state and local officials, including members of Congress, insurance regulators, agents, brokers, consumer groups and other industry leaders — to develop solutions. In the case of hurricane preparedness, the Travelers Coastal Wind zone Plan, proposes a comprehensive set of principles to further address the availability and affordability of coastal windstorm insurance. – Joan Woodward Letter to the Editor, Miami Herald, January 20, 2012

WhileFlorida’ssituationmaybeunique,thecrisisofaffordability and availability of wind-storm insurance applies generally across all Gulf and Atlantic coastal states. Residents in these states deserve a concerted effort to develop a dependable, private-market solution that doesn’t rely on a financial bailout by taxpayers. – Jay Fishman Letter to the Editor, The Wall Street Journal, September 2, 2011

Our nation is not well prepared for the next catastrophic hurricane, but federal taxpayers shouldn’t have to bear the burden. And a long-term solution to the coastal insurance crisis is possible. At Travelers, we believe private insurers have a responsibility to put forth ideas to address the complex economic and social issues related to hurricane risk. Private market solutions are needed now to avoid a bailout later. – Joan Woodward Letter to the Editor, St. Petersburg Times, July 1, 2011

During this year’s legislative session, Gov. Robert Bentley repeated his campaign pledge to call a special session in his quest to solve coastal homeowners’ problem with affordable insurance… being looked at is the Travelers Coastal Wind zone Plan, a federally-guaranteed catastrophic wind-insurance plan put together by the Travelers Institute. What’s attractiveisthatitrecognizesthatcoastalinsuranceisnotsimply a state matter, but, rather, it has regional implications that require a federal response. – The Anniston Alabama Star, June 28, 2011

As the 2011 hurricane season progresses, it’s time for community leaders and their elected representatives to solve the growing crisis surrounding homeowners insurance on the Gulf Coast. One idea… that deserves consideration is the Travelers Coastal Wind zone Plan… The Travelers Plan offers promiseforseveralreasons:Itrecognizesthatstatesshouldn’thave to solve their own insurance problems alone. It also involves the insurance industry, as well as Congress and consumer groups. In short, it is a comprehensive, market-based plan that deserves a closer look by our representatives and senators in Washington as they cast about for answers at the federal level. – The Mississippi Press, June 19, 2011

Travelers Coastal Wind Zone Plan Press Coverage

Launched in August 2007 with an op-ed in The Wall Street Journal, by Jay S. Fishman, Travelers Chairman and CEO, the Travelers Coastal Wind Zone Plan has continued to receive positive press recognition in outlets around the country. The media coverage has contributed to the momentum the plan has built in the public policy arena.

Following are excerpts from some of the articles on the Travelers Coastal Wind zone Plan.

29travelersinstitute.com

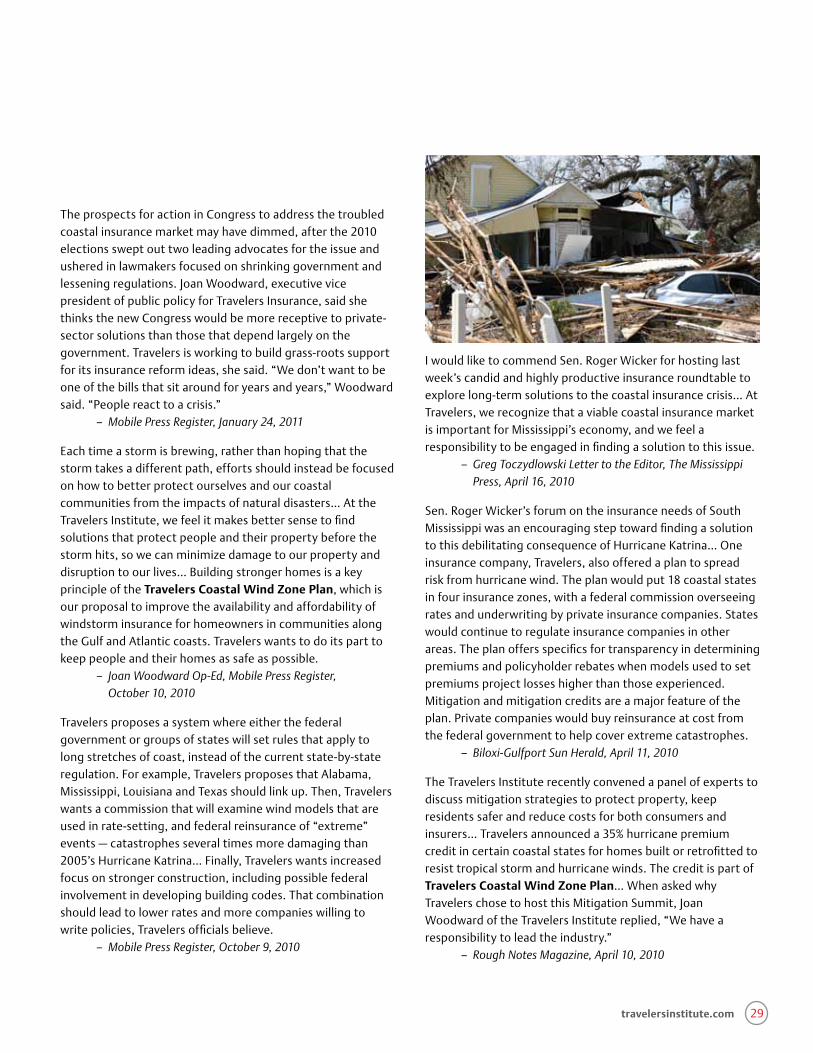

The prospects for action in Congress to address the troubled coastal insurance market may have dimmed, after the 2010 elections swept out two leading advocates for the issue and ushered in lawmakers focused on shrinking government and lessening regulations. Joan Woodward, executive vice president of public policy for Travelers Insurance, said she thinks the new Congress would be more receptive to private-sector solutions than those that depend largely on the government. Travelers is working to build grass-roots support for its insurance reform ideas, she said. “We don’t want to be one of the bills that sit around for years and years,” Woodward said. “People react to a crisis.” – Mobile Press Register, January 24, 2011

Each time a storm is brewing, rather than hoping that the storm takes a different path, efforts should instead be focused on how to better protect ourselves and our coastal communities from the impacts of natural disasters… At the Travelers Institute, we feel it makes better sense to find solutions that protect people and their property before the stormhits,sowecanminimizedamagetoourpropertyanddisruption to our lives… Building stronger homes is a key principle of the Travelers Coastal Wind zone Plan, which is our proposal to improve the availability and affordability of windstorm insurance for homeowners in communities along the Gulf and Atlantic coasts. Travelers wants to do its part to keep people and their homes as safe as possible. – Joan Woodward Op-Ed, Mobile Press Register, October 10, 2010

Travelers proposes a system where either the federal government or groups of states will set rules that apply to long stretches of coast, instead of the current state-by-state regulation.Forexample,TravelersproposesthatAlabama,Mississippi, Louisiana and Texas should link up. Then, Travelers wants a commission that will examine wind models that are used in rate-setting, and federal reinsurance of “extreme” events — catastrophes several times more damaging than 2005’sHurricaneKatrina…Finally,Travelerswantsincreasedfocus on stronger construction, including possible federal involvement in developing building codes. That combination should lead to lower rates and more companies willing to write policies, Travelers officials believe. – Mobile Press Register, October 9, 2010

I would like to commend Sen. Roger Wicker for hosting last week’s candid and highly productive insurance roundtable to explore long-term solutions to the coastal insurance crisis… At Travelers,werecognizethataviablecoastalinsurancemarketis important for Mississippi’s economy, and we feel a responsibility to be engaged in finding a solution to this issue. – Greg Toczydlowski Letter to the Editor, The Mississippi Press, April 16, 2010

Sen. Roger Wicker’s forum on the insurance needs of South Mississippi was an encouraging step toward finding a solution to this debilitating consequence of Hurricane Katrina… One insurance company, Travelers, also offered a plan to spread risk from hurricane wind. The plan would put 18 coastal states infourinsurancezones,withafederalcommissionoverseeingrates and underwriting by private insurance companies. States would continue to regulate insurance companies in other areas. The plan offers specifics for transparency in determining premiums and policyholder rebates when models used to set premiums project losses higher than those experienced. Mitigation and mitigation credits are a major feature of the plan. Private companies would buy reinsurance at cost from the federal government to help cover extreme catastrophes. – Biloxi-Gulfport Sun Herald, April 11, 2010

The Travelers Institute recently convened a panel of experts to discuss mitigation strategies to protect property, keep residents safer and reduce costs for both consumers and insurers… Travelers announced a 35% hurricane premium credit in certain coastal states for homes built or retrofitted to resist tropical storm and hurricane winds. The credit is part of Travelers Coastal Wind zone Plan… When asked why Travelers chose to host this Mitigation Summit, Joan Woodward of the Travelers Institute replied, “We have a responsibility to lead the industry.” – Rough Notes Magazine, April 10, 2010