Embed Size (px)

Citation preview

Hedging Currency and IR Risks

Think Further. Control the Risk.

Dorin Alex Badea, CFA

International Insurance-Reinsurance Forum 2010Sinaia, May 26th 2010

2

AGENDA

Background

Currency Risk Hedging

Interest Risk Hedging

3

The World Today

The New Economy

Volatility and Heteroskedasticity

Priorities and Challenges

Did the Global Crisis end?

Did the Global Crisis start?

4

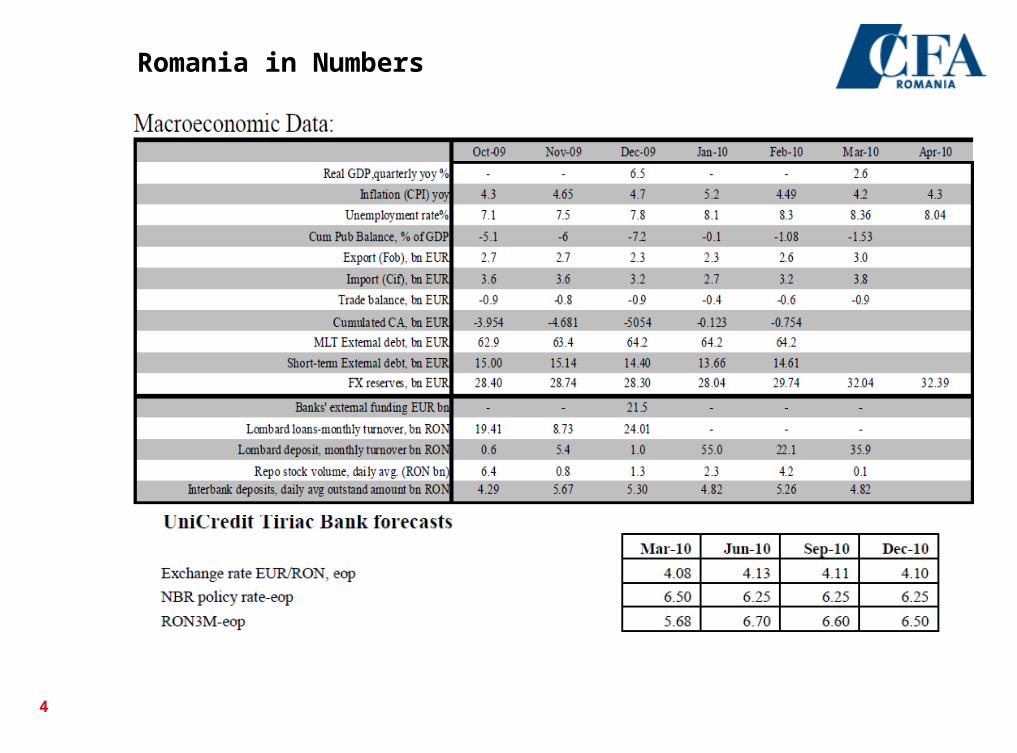

Romania in Numbers

5

CEE FX Rates Forecasts

6

CEE Interest Rates Forecasts

7

Hedging

Risks and Uncertainties to Forecasts

Currency Risk

Interest Rate Risk

Credit Risk

Other Market Risks

8

Classical Solutions & Tools

No Risk Active Hedging Survival Protection Relative Advantage/Improving Strategies

“Expected volatility around the forecastWorst Case scenario

9

AGENDA

Background

Currency Risk HedgingStandard Short Term Currency Exposures HedgingAlternative Solutions for Hedging Long Term FX Exposures

Interest Risk Hedging

10

Short Term FX Risk Exposures – EURRON

26%

17%

5%

11

FX Risk – Short Term Cash Flow & Reval Hedging

Approach - cover fx risk, eliminate uncertainty, relative vs absolute advantage, specific payoff profiles

FX Options

FX Forward

Structured Solutions

12

Illustrative Examples

FX Forward- Agreement to buy or sell one currency agst the other (eg Euro agst Ron)- Current 3M Forward price (august 2010) is 4.2625

FX Option - Gives the right but not the obligation to buy or sell one currency agst another- It involves paying a premium (like an insurance premium)- Employed in numerous structures (with premium or zero-cost depending on desired payout profile and risk/cost appetite)

Improved forward

In comparison with forward rate, allows the client to buy at the expiry date the necessary amount at an “improved level”

Spot rate = 4.1900

FX Forward Rate 4.2625

Improved forward 4.2200 / 4.3200

Cost = “Zero cost” structure

Possible situation at expiry:

Spot < 4.2200 => client has to buy 1 mio EUR at 4.2200

Spot between 4.2200 and 4.3200 => client exercises the right to buy 1 mio EUR at 4.2200

Spot > 4.3200 => client will benefit from a relative advantage – can buy 1 mio EUR at the current Spot minus a discount of 0.1000 pips

Example: Spot = 4.4300 => client buys 1 mio EUR at 4.4300 – 0.1000 = 4.3300

13

FX Risk – Hedging Long-Dated Exposures

Left unhedged, FX risk can dramatically affect returns from cross-border/currency investments

Similarly FX denominated liabilities can be affected by drastic FX movements

We analyze further the impact of having a short Euro / long CEE currency position unhedged over a multi-year period, evaluate the performance of traditional hedging instruments in covering such an exposure and then propose alternative and potentially more efficient ways of hedging a long-dated CEE FX exposure

We can perform a similar in depth analysis for a RON based environment on the basis of a specific portfolio

14

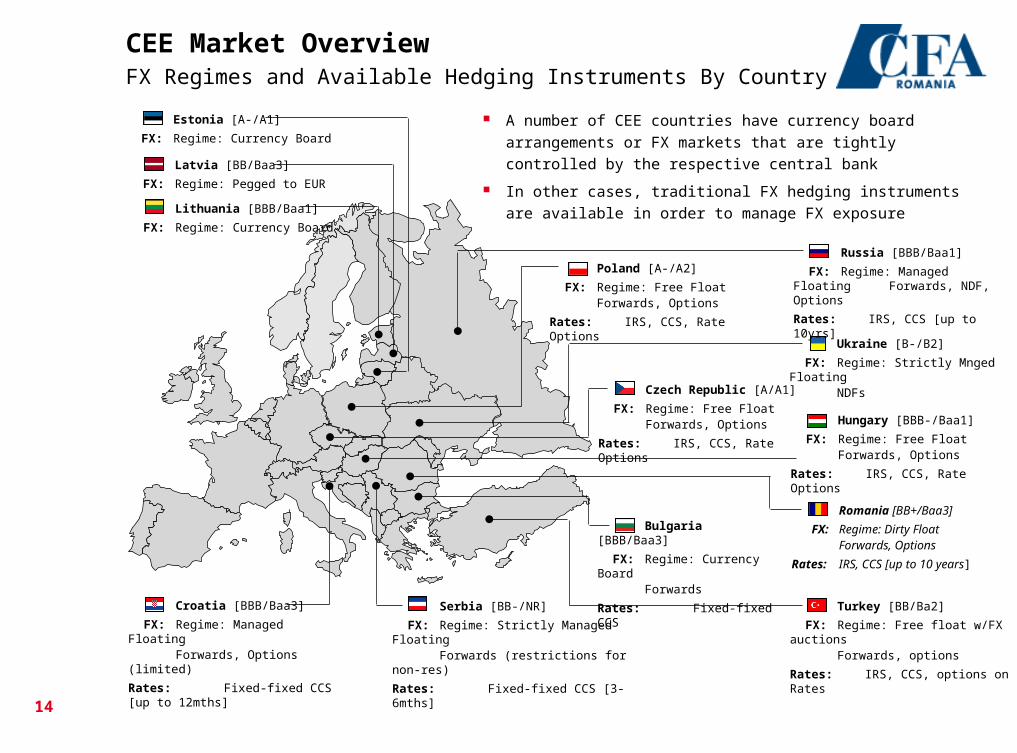

CEE Market OverviewFX Regimes and Available Hedging Instruments By Country

Estonia [A-/A1]

FX: Regime: Currency Board

Russia [BBB/Baa1]

FX: Regime: Managed Floating Forwards, NDF, Options

Rates: IRS, CCS [up to 10yrs]

Latvia [BB/Baa3]

FX: Regime: Pegged to EUR

Lithuania [BBB/Baa1]

FX: Regime: Currency Board

Croatia [BBB/Baa3]

FX: Regime: Managed FloatingForwards, Options (limited)

Rates: Fixed-fixed CCS [up to 12mths]

Serbia [BB-/NR]

FX: Regime: Strictly Managed FloatingForwards (restrictions for non-res)

Rates: Fixed-fixed CCS [3-6mths]

Turkey [BB/Ba2]

FX: Regime: Free float w/FX auctionsForwards, options

Rates: IRS, CCS, options on Rates

Bulgaria [BBB/Baa3]

FX: Regime: Currency BoardForwards

Rates: Fixed-fixed CCS

Romania [BB+/Baa3]

FX: Regime: Dirty FloatForwards, Options

Rates: IRS, CCS [up to 10 years]

Czech Republic [A/A1]

FX: Regime: Free FloatForwards, Options

Rates: IRS, CCS, Rate Options

Hungary [BBB-/Baa1]

FX: Regime: Free FloatForwards, Options

Rates: IRS, CCS, Rate Options

Poland [A-/A2]

FX: Regime: Free FloatForwards, Options

Rates: IRS, CCS, Rate Options

Ukraine [B-/B2]

FX: Regime: Strictly Mnged FloatingNDFs

A number of CEE countries have currency board arrangements or

FX markets that are tightly controlled by the respective central

bank

In other cases, traditional FX hedging instruments are available in

order to manage FX exposure

15

Euro-based investors that have investments in CEE countries are exposed to a significant sell-off of a

CEE currency versus the Euro that may even threaten their solvency ratios. Similarly CEE borrowers

that tap the deeper Euro capital markets are exposed to a sudden weakening of the CEE currencies

they use to service the Euro debt.

As the charts on the next page show, the general pattern is for CEE currencies to steadily appreciate

against the Euro before a dramatic sell-off driven by a drying up of risk appetite. In the 2008-09

financial crisis, the rapid reduction in risk appetite generated FX sell offs combined with dramatic fall in

market instruments’ liquidity

Given the managed float regime of RON, and the unstable correlation vs the region currencies and

global risk aversion, we can further employ similar strategies for RON liable companies

In order to protect against the potentially harmful impact of a sell-off in the local currency, Euro based

investors may look to put in place hedging. Natural hedges where investments are matched in the

liability currency to the extent possible is an obvious first step to take in mitigating net investment

exposure, obviously limiting further the investment universe though

After natural hedging opportunities have been exhausted, the obvious traditional hedge would be a

forward contract and therefore we assess the historic performance of long-dated forward contracts to

buy Euro / sell CEE currency in the pages that follow

Traditional FX Hedging Solutions

16

Historical Performance of CEE currencies vs the EuroCEE currencies steadily appreciate vs Euro but can sell-off dramatically

3.00

3.50

4.00

4.50

5.00

99 00 01 02 03 04 05 06 07 08 09 10

20.00

25.00

30.00

35.00

40.00

99 00 01 02 03 04 05 06 07 08 09 10

225

250

275

300

325

99 00 01 02 03 04 05 06 07 08 09 10

0.35

0.85

1.35

1.85

2.35

99 00 01 02 03 04 05 06 07 08 09 10

1.00

2.00

3.00

4.00

5.00

99 00 01 02 03 04 05 06 07 08 09 10

20

26

32

38

44

50

99 00 01 02 03 04 05 06 07 08 09 10

3.00

5.50

8.00

10.50

13.00

99 00 01 02 03 04 05 06 07 08 09 10

7.00

7.25

7.50

7.75

8.00

99 00 01 02 03 04 05 06 07 08 09 10

0

25

50

75

100

99 00 01 02 03 04 05 06 07 08 09 10

/

/

/

/ /

/

/

/

/

Data source: Bloomberg

17

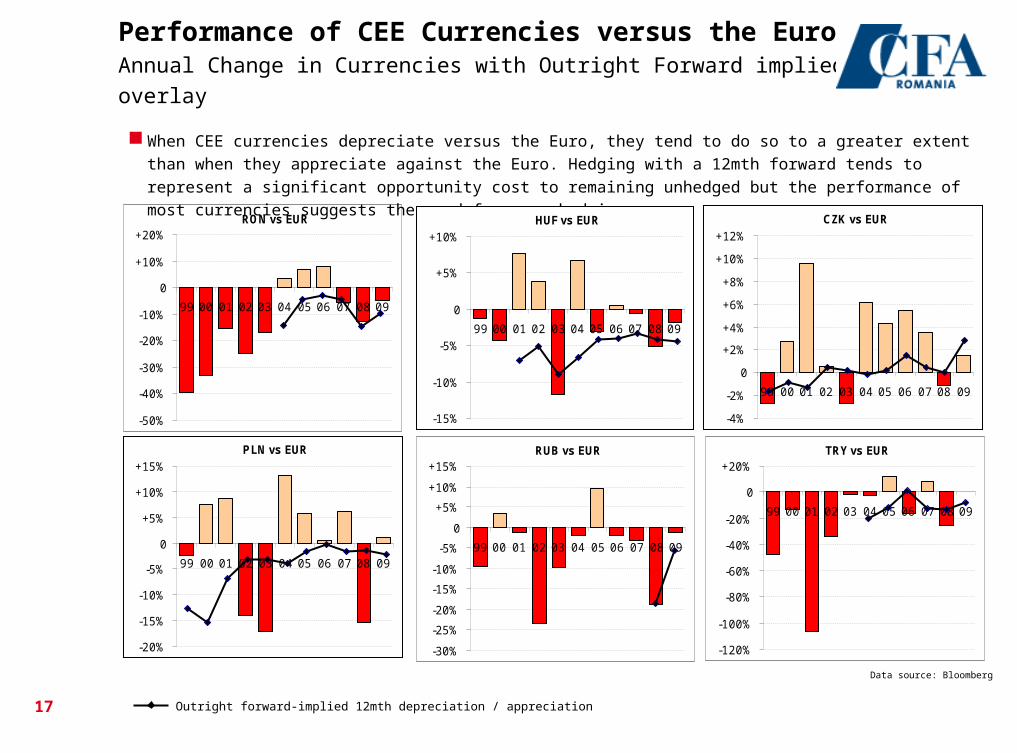

Performance of CEE Currencies versus the EuroAnnual Change in Currencies with Outright Forward implied change overlay

When CEE currencies depreciate versus the Euro, they tend to do so to a greater extent than when they appreciate

against the Euro. Hedging with a 12mth forward tends to represent a significant opportunity cost to remaining unhedged

but the performance of most currencies suggests the need for some hedging

PLN vs EUR

-20%

-15%

-10%

-5%

0

+5%

+10%

+15%

99 00 01 02 03 04 05 06 07 08 09

HUF vs EUR

-15%

-10%

-5%

0

+5%

+10%

99 00 01 02 03 04 05 06 07 08 09

CZK vs EUR

-4%

-2%

0

+2%

+4%

+6%

+8%

+10%

+12%

99 00 01 02 03 04 05 06 07 08 09

TRY vs EUR

-120%

-100%

-80%

-60%

-40%

-20%

0

+20%

99 00 01 02 03 04 05 06 07 08 09

RUB vs EUR

-30%

-25%

-20%

-15%

-10%

-5%

0

+5%

+10%

+15%

99 00 01 02 03 04 05 06 07 08 09

RON vs EUR

-50%

-40%

-30%

-20%

-10%

0

+10%

+20%

99 00 01 02 03 04 05 06 07 08 09

Outright forward-implied 12mth depreciation / appreciation

Data source: Bloomberg

18

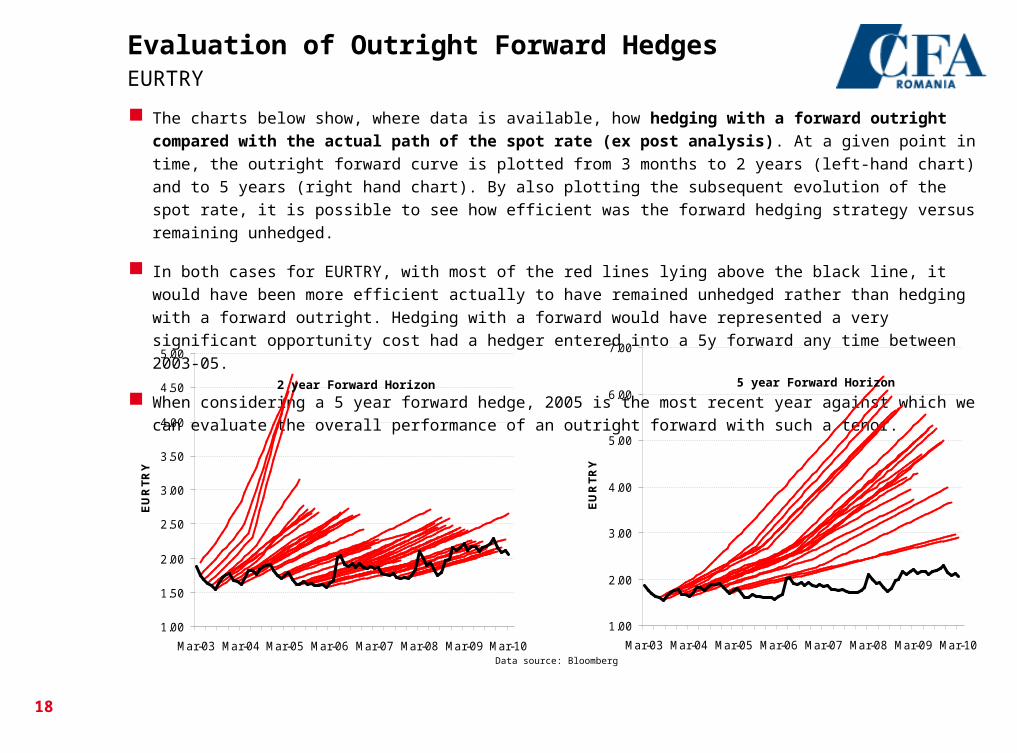

The charts below show, where data is available, how hedging with a forward outright compared with the actual

path of the spot rate (ex post analysis). At a given point in time, the outright forward curve is plotted from 3 months

to 2 years (left-hand chart) and to 5 years (right hand chart). By also plotting the subsequent evolution of the spot

rate, it is possible to see how efficient was the forward hedging strategy versus remaining unhedged.

In both cases for EURTRY, with most of the red lines lying above the black line, it would have been more efficient

actually to have remained unhedged rather than hedging with a forward outright. Hedging with a forward would have

represented a very significant opportunity cost had a hedger entered into a 5y forward any time between 2003-05.

When considering a 5 year forward hedge, 2005 is the most recent year against which we can evaluate the overall

performance of an outright forward with such a tenor.

Evaluation of Outright Forward Hedges EURTRY

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

EU

RT

RY

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

EU

RT

RY

2 year Forward Horizon 5 year Forward Horizon

Data source: Bloomberg

19

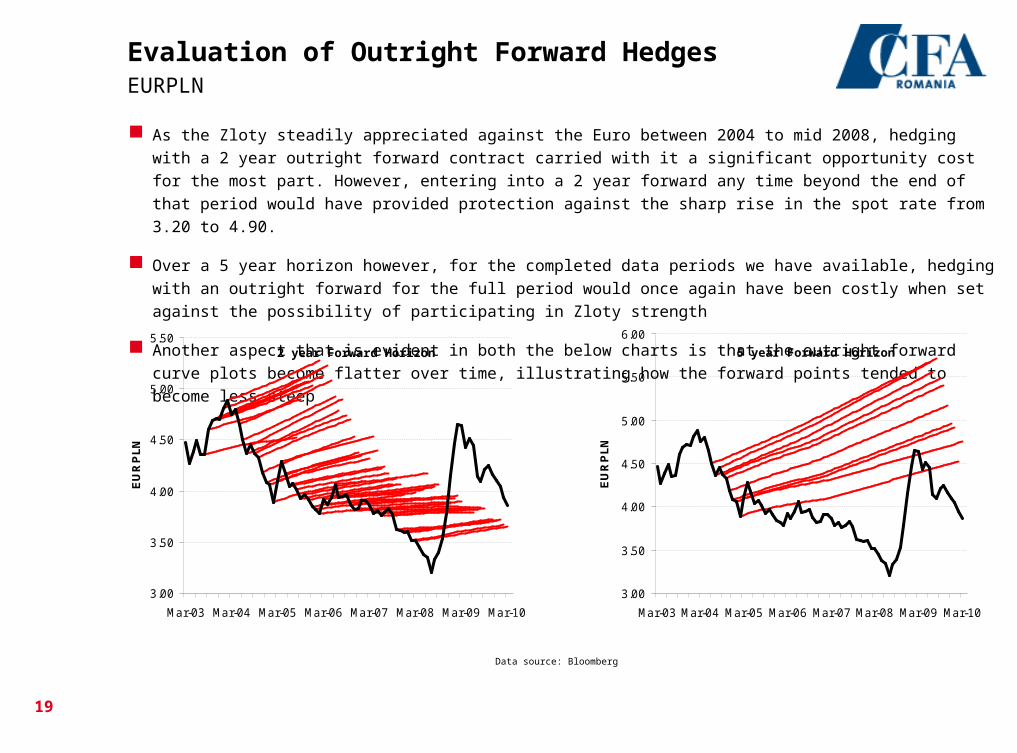

As the Zloty steadily appreciated against the Euro between 2004 to mid 2008, hedging with a 2 year outright forward

contract carried with it a significant opportunity cost for the most part. However, entering into a 2 year forward any time

beyond the end of that period would have provided protection against the sharp rise in the spot rate from 3.20 to 4.90.

Over a 5 year horizon however, for the completed data periods we have available, hedging with an outright forward for

the full period would once again have been costly when set against the possibility of participating in Zloty strength

Another aspect that is evident in both the below charts is that the outright forward curve plots become flatter over time,

illustrating how the forward points tended to become less steep

Evaluation of Outright Forward Hedges EURPLN

3.00

3.50

4.00

4.50

5.00

5.50

6.00

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10E

UR

PL

N3.00

3.50

4.00

4.50

5.00

5.50

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

EU

RP

LN

2 year Forward Horizon 5 year Forward Horizon

Data source: Bloomberg

20

Outright forwards would have been of more benefit over a 2 year horizon in the case of EURHUF relative to EURTRY

and EURPLN. However the ends of many of the red lines are above the black line, indicating again that it would have

been preferable to remain unhedged.

Again, in the case of the 5 year outright forward hedge, it would have always been preferable to have remained

unhedged over such a horizon as the cost of buying EUR / selling HUF at the end would have been cheaper in the

spot market than at a forward rate contracted 5 years previously.

Evaluation of Outright Forward Hedges EURHUF

225

245

265

285

305

325

345

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

EU

RH

UF

225

235

245

255

265

275

285

295

305

315

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

EU

RH

UF

2 year Forward Horizon 5 year Forward Horizon

Data source: Bloomberg

21

On the one hand, the ex ante opportunity cost of having hedged with a 2 year outright forward contract in EURCZK

has been relatively small, with the outright forward rate being close to the market spot rate. However ex post

opportunity cost shows once again that it would have been preferable not to have had in place an outright forward

hedge as the Koruna has steadily appreciated against the Euro over most of the available data horizon.

We were unable to obtain any data on 5yr EURCZK forward outrights from at least 5 years ago

Evaluation of Outright Forward HedgesEURCZK

20

23

26

29

32

35

Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10

EU

RC

ZK

2 year Forward Horizon

Data source: Bloomberg

22

Consequently, given a need to hedge a short EUR / long CEE exposure, long-dated outright FX

forwards have a relatively high opportunity cost when comparing the long-dated outright forward rate

to the spot rate realised at the end of the hedge horizon.

The fact that a number of CEE currencies are actively seeking to enter into currency convergence

with the Euro within the next 5 years should at least be considered by any long-dated hedging

strategy

Further we look at ways that such an exposure may be hedged without the need to commit to a

long-dated FX forward.

First there are “standard” solutions we considered before

– Cross Currency Swaps

– Options

Then we look at dynamic alternatives to long-dated forwards for hedging:

– Rolling Forwards

– Contingent Hedging

Alternative Hedging SolutionsOverview

23

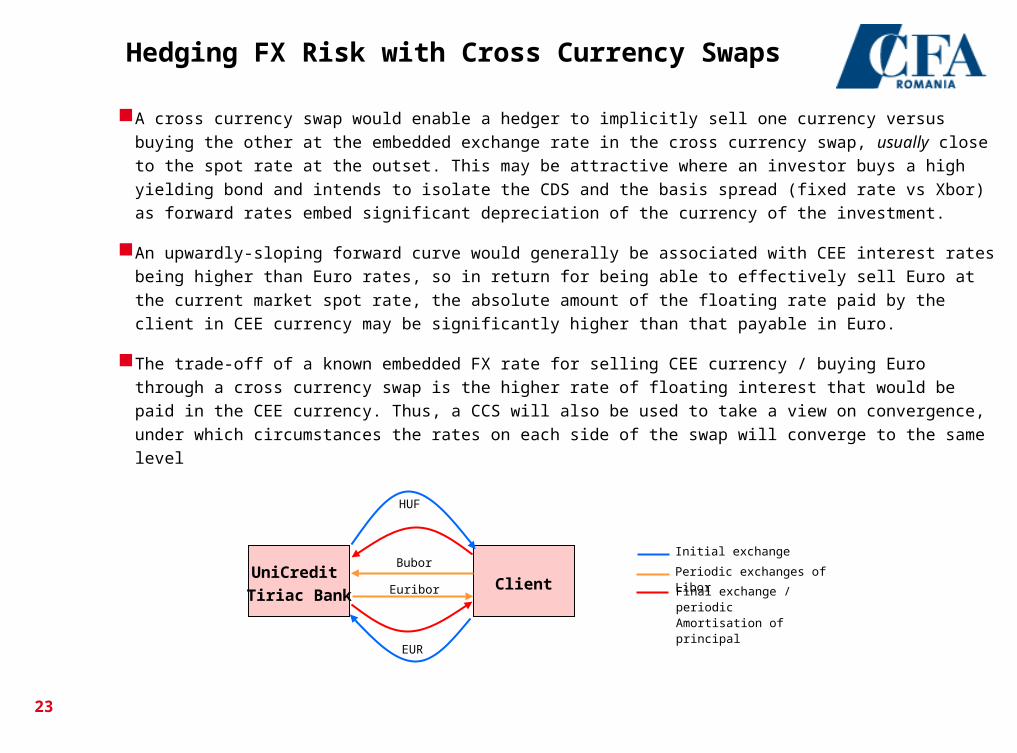

Hedging FX Risk with Cross Currency Swaps

A cross currency swap would enable a hedger to implicitly sell one currency versus buying the other at

the embedded exchange rate in the cross currency swap, usually close to the spot rate at the outset.

This may be attractive where an investor buys a high yielding bond and intends to isolate the CDS and

the basis spread (fixed rate vs Xbor) as forward rates embed significant depreciation of the currency of

the investment.

An upwardly-sloping forward curve would generally be associated with CEE interest rates being higher

than Euro rates, so in return for being able to effectively sell Euro at the current market spot rate, the

absolute amount of the floating rate paid by the client in CEE currency may be significantly higher than

that payable in Euro.

The trade-off of a known embedded FX rate for selling CEE currency / buying Euro through a cross

currency swap is the higher rate of floating interest that would be paid in the CEE currency. Thus, a

CCS will also be used to take a view on convergence, under which circumstances the rates on each

side of the swap will converge to the same level

ClientUniCredit

Tiriac Bank

HUF

EUR

Bubor

Euribor Final exchange / periodic Amortisation of principal

Initial exchange

Periodic exchanges of Libor

24

Hedging Extreme ScenariosOptions

Out-of-the-money EUR calls / CEE currency puts may be a preferable alternative to long-dated

forwards, especially as outright forward rates tend to be a “costly” way of hedging a long-dated short

EUR / long CEE currency exposure. The risk of forward rates not being realised is increased when

the possibility of EMU convergence of a CEE currency is taken into account

The strikes must be relatively far from current spot rates, driving the annualised cost of the options

significantly lower than the cost implicit in a forward contract.

It is true of course that the protection conferred by the option is at a higher spot rate than that of the

forward; however the option allows the hedger unlimited participation in CEE currency strength

below the option strike

The overall cost of hedging can be reduced by taking a portfolio approach to the hedging and leaving

part of the exposure unhedged

Similar to outright forwards, it is also possible to implement a rolling option hedge programme, which

would reduce up-front premium payment and also enable the hedger to benefit from lower forward-

embedded CEE currency depreciation in the future. Up-front premium payment can also be reduced

through it being financed over time by the bank, subject to the availability of credit lines.

25

Options – Advantages and Limitations

Benefits of hedging long-dated FX exposure with optionsFlexibility: a hedging strategy can use multiple strikes in order to optimise the cost /

protection profileKnown maximum cost: the up-front premium paidOpportunity to fully participate in CEE currency outperformance against the outright

forward rate versus the EuroPossibility for premium to be recovered through early unwind of optionWhere forwards embed an appreciation of the Euro, options may be a better hedge where

there is a good chance of the underlying CEE currency entering EMU within the hedge horizon and at which point forwards will be zero

Lower bank credit line utilization than forwards

Limitations of hedging long-dated CEE FX exposure with optionsPremium: an up-front premium amount is payable for option protection. Cost is positively

related to time to maturity, the strike rate relative to the outright forward rate to the option’s delivery date and the level of market implied volatility

Pricing driven off the outright forward rate, which may embed CEE currency depreciation If a currency does move towards EMU convergence, the implied volatility of its exchange

rate versus the Euro will fall, reducing the time-related element of an option’s value

26

EUR hedge notional amount to be rolled at each cashflow date is the previous notional

amount less intervening EUR equiv debt service cashflows [principal and interest]

The idea behind a rolling hedge is to hedge the full outstanding notional amount of a medium- to long-term exposure over a shorter term

horizon. The chart below profiles a 5 year asset with annual straight line amortization

The full amount outstanding debt service payments [principal and interest] are hedged on a period-by-period basis; the advantage of this

approach to hedging a long local currency / short EUR position is that a hedger does not have to lock into the wide interest differential

between the respective rates for the long term and it also offers more flexibility

If a rolling hedge is used as an alternative to a strip of long-dated outright forwards, it will also have positive implications regarding credit

line utilization; the company would however need to be sure of having access to a credit line when coming to roll the hedge and there

would be a liquidity impact on the client in the event of the CEE currency appreciating versus the Euro over the term of a rolling hedge

Rolling ForwardRationale and Methodology

0

20

40

60

80

100

120

5y 4y9m 4y6m 4y3m 4y 3y9m 3y6m 3y3m 3y 2y9m 2y6m 2y3m 2y 1y9m 1y6m 1y3m 1y 0y9m 0y6m 0y3m

Time to Final Cashflow

Ca

sh

flo

ws

Ou

tsta

nd

ing

[E

UR

mn

]

Principal

Periodic Debt Service Am ountsTotal Outstanding EUR

Loan Service Cashflows

EUR annual debt service

cashflow amount

27E

UR

De

bt S

ervice

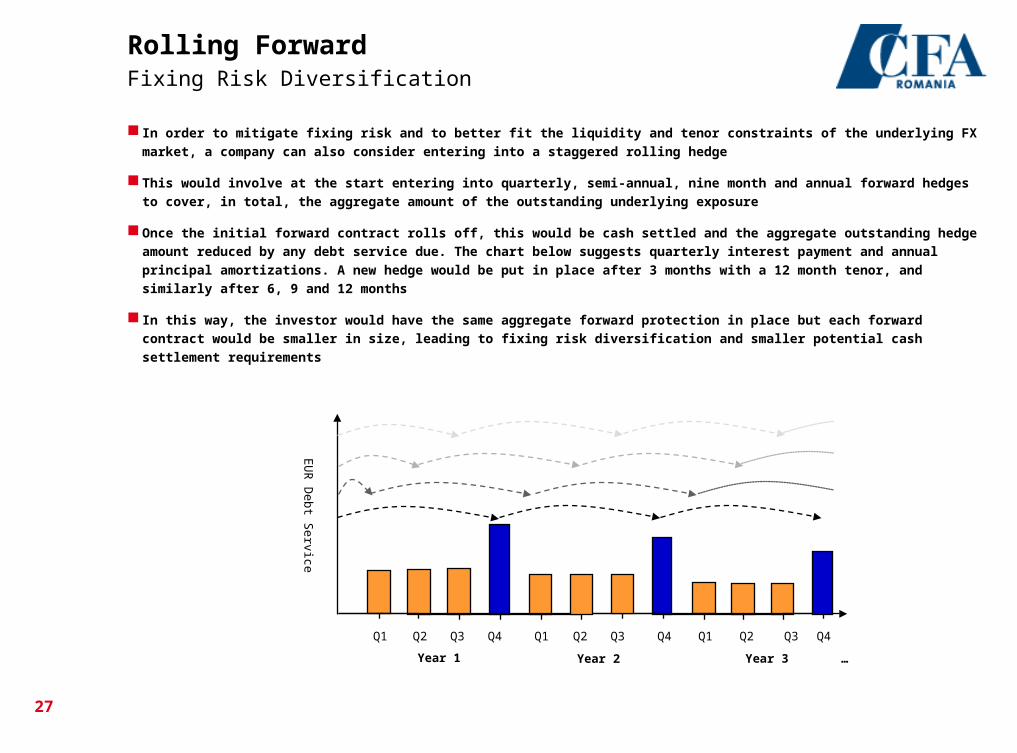

In order to mitigate fixing risk and to better fit the liquidity and tenor constraints of the underlying FX market, a company

can also consider entering into a staggered rolling hedge

This would involve at the start entering into quarterly, semi-annual, nine month and annual forward hedges to cover, in

total, the aggregate amount of the outstanding underlying exposure

Once the initial forward contract rolls off, this would be cash settled and the aggregate outstanding hedge amount

reduced by any debt service due. The chart below suggests quarterly interest payment and annual principal

amortizations. A new hedge would be put in place after 3 months with a 12 month tenor, and similarly after 6, 9 and 12

months

In this way, the investor would have the same aggregate forward protection in place but each forward contract would be

smaller in size, leading to fixing risk diversification and smaller potential cash settlement requirements

Rolling ForwardFixing Risk Diversification

Year 1

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Year 2 Year 3 …

28

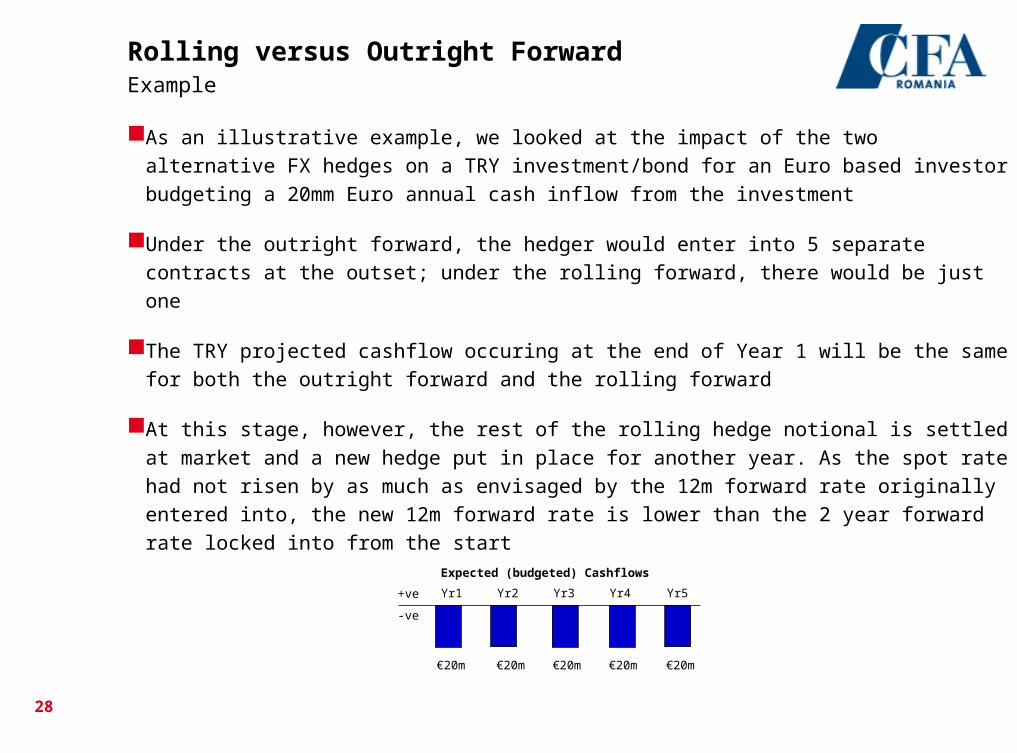

As an illustrative example, we looked at the impact of the two alternative FX hedges on a

TRY investment/bond for an Euro based investor budgeting a 20mm Euro annual cash

inflow from the investment

Under the outright forward, the hedger would enter into 5 separate contracts at the outset;

under the rolling forward, there would be just one

The TRY projected cashflow occuring at the end of Year 1 will be the same for both the

outright forward and the rolling forward

At this stage, however, the rest of the rolling hedge notional is settled at market and a new

hedge put in place for another year. As the spot rate had not risen by as much as envisaged

by the 12m forward rate originally entered into, the new 12m forward rate is lower than the 2

year forward rate locked into from the start

+ve

-ve

Expected (budgeted) Cashflows

€20m €20m €20m €20m €20m

Yr1 Yr2 Yr3 Yr4 Yr5

Rolling versus Outright ForwardExample

29

In a potential ‘crash scenario’, where for example the EURTRY spot

rate doubles over a short period of time, the rolling hedge provides

adequate protection despite its short tenor.

So in our example, the actual rate in 12 months’ time jumps from 2.00

to 4.00.

For example, today’s 12 month forward rate is 2.25, which is an

implicit depreciation of 12.0% (as implied by current forward points).

All the future debt obligations in TRY are hedged for 12 months using

a forward contract. EUR 100m = TRY 225m at 2.25

The depreciation of TRY causes the EUR 100m obligation to become

TRY 400m.

Investor receives a compensatory payment of TRY 175m via the

rolling hedge, and hence is fully hedged as the benchmark for a

future-dated cashflow in 12 months’ time was the forward (2.25) at

the start; the client has achieved an effective hedge rate of 2.25 with

the rolling forward (= [TRY 400m – TRY 175m] / EUR 100m)

The hedge is rolled for a further 12 months at the new FX levels.

Client is relatively indifferent to the depreciation as they have

received compensation in TRY that fully covers the change in the

value of their future obligations.

EURTRY

2.00

4.00

t0 t1

PV of all future debt obligations is hedged

TRY 175m

50% TRY depreciation results in compensatory payment

€100m

Rolling Forward “Crash Scenario”

30

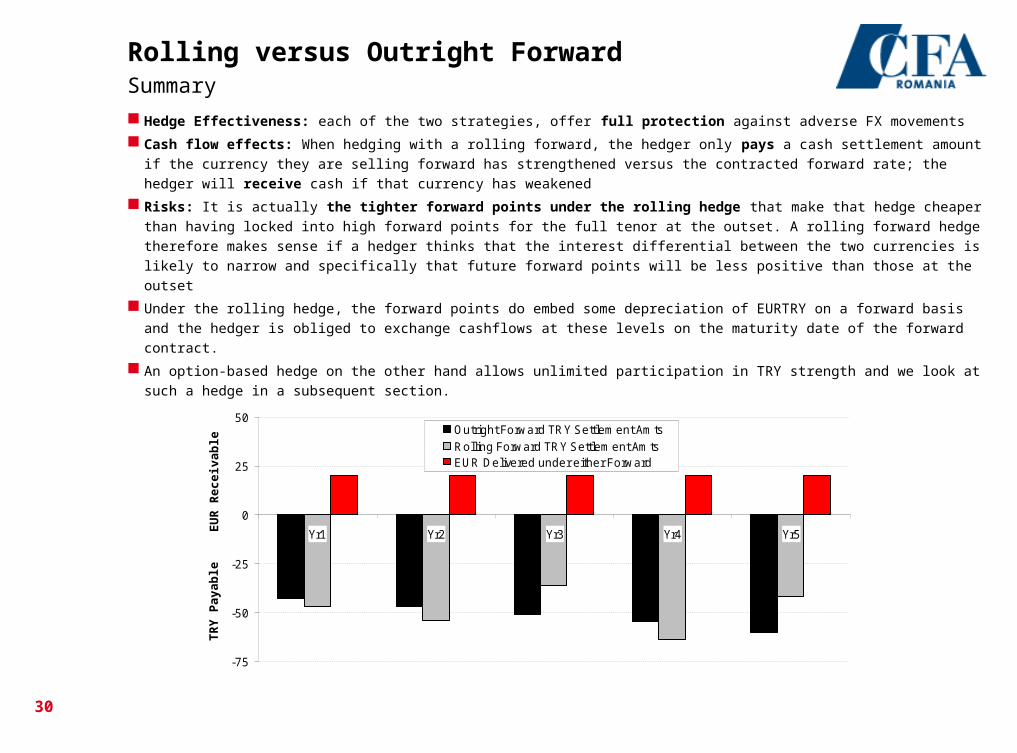

Rolling versus Outright ForwardSummary

Hedge Effectiveness: each of the two strategies, offer full protection against adverse FX movements

Cash flow effects: When hedging with a rolling forward, the hedger only pays a cash settlement amount if the

currency they are selling forward has strengthened versus the contracted forward rate; the hedger will receive cash if

that currency has weakened

Risks: It is actually the tighter forward points under the rolling hedge that make that hedge cheaper than having

locked into high forward points for the full tenor at the outset. A rolling forward hedge therefore makes sense if a

hedger thinks that the interest differential between the two currencies is likely to narrow and specifically that future

forward points will be less positive than those at the outset

Under the rolling hedge, the forward points do embed some depreciation of EURTRY on a forward basis and the

hedger is obliged to exchange cashflows at these levels on the maturity date of the forward contract.

An option-based hedge on the other hand allows unlimited participation in TRY strength and we look at such a hedge

in a subsequent section.

EU

R R

ec

eiv

ab

leT

RY

Pay

ab

le

-75

-50

-25

0

25

50

Yr1 Yr2 Yr3 Yr4 Yr5

Outright Forward TRY Settlem ent Am ts

Rolling Forward TRY Settlem ent Am tsEUR Delivered under either Forward

31

Contingent Hedging of CEE FX RiskOverview

Hedging with options requires the hedger to pay an up-front premium (alternatively this can be

financed over the term of the option, subject to bank credit lines).

Up-front option cost can be reduced by placing the option strike further out-of-the-money, reducing

option tenor or covering less than the full amount of the exposure. However, up-front option premium

can be reduced in a further way, through the option hedging only being put in place according to a

tailored FX Algorithm.

Following a rule-based algorithm increases the transparency surrounding when contingent hedging is

put in place.

Rather than paying up-front option premium, the client invests in a floating rate note whose outstanding

amount will only be drawn upon in the event that the FX Algorithm determines that FX hedging – in the

form of FX options – needs to be put in place.

The FX Algorithm is designed to determine how much incremental notional hedging needs to be put in

place and at what strike rate.

If the contingent amount is fully used up, the investor will have to draw on other resources if it want to

protect against subsequent adverse FX movements.

32

Contingent Hedging of CEE FX RiskThe Algorithm Mechanics

The Maximum Loss rate is determined by the client - for example, a loss of 25% due to adverse FX movements

Reference market levels are calculated based on the client’s stated Maximum Loss scenario and are expressed in terms

of option deltas in order to reflect the likelihood that a certain market level will be reached. In this way they reflect

prevailing market implied volatilities and the relevant time horizon.

The Trigger level signal to add incremental option notional is the rate at which, under prevailing market conditions, the

Maximum Loss is equivalent to a 12 month 15Delta strike. A 12 month reference tenor is chosen rather than the full

maturity term in order to mitigate premium spend associated with protecting against temporary spikes in the FX rate

The Hedge Rate strike at which further option notional would be bought is a 25Delta strike relative to the Trigger Level.

Sufficient notional is bought at the Hedge Rate to push the Maximum Loss Rate from being a 15Delta event to being a

10Delta event. The spot rate would therefore have to reach a higher spot rate for the hedger to lose the 25% worst case

determined at the outset.

OriginalMax LossHedge RateTrigger LevelCurrent Spot

25Δ Option Strike with respect to Trigger

15Δ Option Strike with respect to Trigger

OriginalMax LossHedge RateTrigger Level

10Δ Option Strike with respect to Trigger

New Max Loss

EUR strength / CEE weakness

At Start

If Euro strengthens above Trigger Level

33

Contingent Hedging of CEE FX RiskAnalysis

If the trigger is never hit the option protection is never needed, and the client will not have spent any premium and will

not have been locked into any forward contracts embedding significant costs. The hedger retains the potential to

participate in currency strength following any temporary spike higher of the FX rate; at the same time, peace of mind

comes from the fact that protection is available to be put in place should it be required and whilst the contingent

premium resource has not been exhausted.

Deltas can be defined with respect to a shorter horizon than the full term of the exposure. This is to avoid the cost of

implementing contingent hedging to the end of the exposure when a move higher in the FX rate may prove to be only

temporary. However, if the spot rate remains persistently higher, beyond the expiry date of the contingent hedge

originally implemented, additional premium may need to be spent in order to replace the expired hedge.

Higher market volatility will tend to push the Trigger closer to the current spot rate, thereby increasing the chances that

incremental hedging needs to be put in place. However, referencing specific Deltas helps to mitigate the cost of putting

in place that contingent hedging.

Market parameters can be checked as frequently as required and then the Trigger Level revised to reflect market

movements.

Contingent hedging is suitable for clients that have a relatively bullish view on the expected performance of the

investment currency versus the base currency but whom would like to put in place “insurance” on a contingent basis in

the event that the FX rate does in fact move considerably against expectations.

There is a minimal opportunity cost of the contingent premium as it is invested in a UniCredit Bank AG FRN.

34

AGENDA

Background

Currency Risk Hedging

Interest Risk Hedging

35

Interest Rate Risk

Held to Maturity vs AFS vs Held for Trading

Visibility, Correlation and Added Uncertainties – Interest Rate and Credit

Hedge Accounting

Products IRS and the likes IR Options Structured solutions

36

Interest Rate Risk

Duration Gap

Benchmarking Issues

Regulatory Framework

Available Instruments & Liquidity

Need for Structured Solutions (classical example – Reverse Floater notes or Long Receiver Swaps)

37

Think the (Im)possible?

USD 1M Rates in the 80s

Monthly QUSD1MD= 31/01/1982 - 30/09/2009 (GMT)

Line, QUSD1MD=, Bid(Last)

Price

.12

1

2

3

4

5

6

7

8

9

10

11

12

13

14

1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

1980 1990 2000

38

Thank you!