Embed Size (px)

Citation preview

Issue details

Face value (Rs) 10

Fresh issue (up to)

1.16cr Equity Shares

Offer for Sale (up to)

1.82cr Equity Shares

Issue type 100% Book building

Industry Healthcare

Shareholding pattern

(%) Pre IPO Post IPO

Promoter and Promoter group

28.75 NA

Others 71.25 NA

Share reservation (%)

QIB 75

Non institutional 15

Retail 10

Company management Dr. BS Ajai Kumar

Chairman and CEO

Mr. Gangadhara Ganapati

Non‐executive Director

Mr. Prakash Parthasarathy

Non‐executive Director

Issue manager

BRLM

Kotak Mahindra Capital Co. Ltd., Edelweiss Financial Services Ltd., Goldman Sachs (India) Securities Pvt. Ltd., IDFC Securities Ltd., IIFL Holdings Ltd., Yes Bank Ltd.

Registrar Karvy Computershare Private Limited

Listing BSE, NSE

HealthCare Global Enterprises Ltd.

Issue Opens: 16‐Mar‐16 Issue Closes: 18‐Mar‐16 Price Band: Rs205‐218

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

For further details, write to us at: [email protected]

IPO Note

March 10, 2016

Note: India Infoline Limited is a syndicate member in the issue; accordingly, this note is prepared based on the Red Herring Prospectus and is for informative purpose only.

This document summarizes a few key points related to the issue and should not be treated as a comprehensive summary. Investors are requested to refer the Draft Red Herring Prospectus/ Red Herring Prospectus for further details regarding the issue, the issuer company and the risk factors before taking any investment decision. Please note that investments in securities are subject to risks including loss of principal amount and past performance is not indicative of future performance. Nothing herein constitutes an offer of securities for sale in any jurisdiction where it is unlawful to do so.

Business Overview HCG HealthCare Global Enterprises Ltd. (HCG) is a provider of speciality healthcare, focused on cancer and fertility. Under the ‘HCG’ brand, it operates the largest cancer care network in India with a chain of 14 comprehensive cancer

centres, including a centre of excellence in Bengaluru, three freestanding diagnostic centres and one day care chemotherapy centre. Comprehensive cancer centre offers, at a single location, complete cancer diagnosis and treatment services (including radiation, medical oncology and surgical treatments). The freestanding diagnostic centres and day care chemotherapy centre offer diagnosis and medical oncology services. Company also acquired 50.1% equity interest in BACC Healthcare in 2013 which operates fertility centres under the ‘Milann’ brand, through itself and its wholly‐owned subsidiary, DKR Healthcare; pursuant to this acquisition, HCG now operates four Milann fertility centres in Bengaluru.

Large unmet demand for cancer treatment The prevalence of cancer in India is estimated at 39lakh people in 2015, with 11lakh new cancer cases reported during the year. However, the real incidence of cancer in India could be significantly higher than the reported figure; data from large randomized screening trials suggests real incidence of cancer could be 1.5‐2 times higher than the reported incidence or an estimated 16‐22lakh new cancer cases in 2015 (Source: Call for Action: Expanding cancer care in India dated July 2015 published by Ernst & Young).

Key strengths of HCG 1) Largest domestic provider of cancer care, in terms of total number of private cancer treatment centres, with a proven track record 2) Provides high quality cancer care at a competitive price 3) Entry into high potential fertility business; being an emerging segment of the healthcare industry which is relative underdeveloped and fragmented.

Financial Highlights (Restated consolidated) Y/e 31 Mar (Rs cr) FY11 FY12 FY13 FY14 FY15 8m FY16

Turnover (net) 215 267 338 451 519 379

Total revenues (incl other income) 216 270 341 455 524 381

yoy growth (%) ‐ 25.0 26.1 33.6 15.1 ‐

EBIDTA (incl other income)* 39 45 49 42 81 58

EBITDA Margin (%) 18.2 16.6 14.3 9.3 15.5 15.2

Net profit 6 (3) (11) (36) 1 (4)

Net Profit Margin (%) 2.9 (1.2) (3.1) (7.8) 0.1 (1.0)

EPS (Rs)@ 1.2 (0.6) (1.7) (5.2) 0.1 (0.5) Source: RHP, India Infoline Research, * EBIDTA – Earnings before interest, depreciation, tax and amortization @diluted EPS based on weighted average number of dilutive equity shares outstanding during the year/period

Page 2 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

HCG is the largest provider of cancer care in India and operates 18 cancer centers spread across 13 cities and towns across 8 states in India Company’s relationship with medical technology vendors and scale of purchase provides an advantage in sourcing and financing of medical equipment

Key Strengths

Largest domestic provider of cancer care with a proven track record HCG network is the largest provider of cancer care in India in terms of the total number of private cancer treatment centres licensed by the AERB as of May 31, 2015. (Source: Government of India, Atomic Energy Regulatory Board). As of December 31, 2015, the company operated 18 HCG cancer centres, including 14 comprehensive cancer centres, three freestanding diagnostic centres and 1 day care chemotherapy centre in India. The company began the expansion of network in 2006 and has since added 11 comprehensive cancer centres along with diagnostic and day care chemotherapy centres. HCG network is spread across 13 cities and towns across eight states in India. The extensive cancer network supports provision of cancer care beyond metropolitan cities to patients throughout India. The company has a strong reputation within the medical community due to deployment of advanced technologies, successful clinical outcomes and the extensive clinical experience of its specialist physicians.

HCG: Key Operational Data Particulars FY13 FY14 FY15 H1 FY16

Comprehensive cancer centres 14 15 15 14

New patient registrations 28,546 34,344 37,458 18,079

Patients treated with radiation therapy

10,225 11,181 12,647 6,163

PET‐CT procedures 17,750 21,040 23,988 12,253

Chemotherapy registrations 40,052 43,988 48,360 25,453

Surgeries 7,333 8,454 8,707 4,630

Number of available operational beds

746 829 875 912

AOR (%) 57.6 54.2 53.5 51.6

ALOS (days) 3.42 3.15 3.00 2.90

ARPOB (Rs/day) 19,034 21,850 24,647 26,685

Source: RHP, India Infoline Research

Provides high quality cancer care at a competitive price The company’s relationships with medical technology vendors, pharma and biotechnology companies along with R&D involvement helps drive introduction of the latest technology advances. For instance, HCG is amongst the first healthcare providers in India to standardize molecular diagnostics technologies, including genomic testing and molecular imaging, including 128 slice PET‐CT scans in the diagnosis and staging of cancer, as well as to introduce high intensity flattening filter free mode radiotherapy, stereotactic radio surgery and robotic radio surgery. The five year survival rate for breast cancer patients at HCG network is comparable to U.S. benchmarks. (Source: Delivering World‐Class Health Care, Affordably, published on Harvard Business Review, dated November 2013). Moreover, the scale of operations and relationships with vendors of specialized medical equipment provides competitive advantage in sourcing and financing of medical equipment.

Page 3 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Fertility is an emerging area of domestic healthcare industry with large untapped potential and fragmented market

In H1 FY16 and FY15, Milann fertility centres registered 5,575 and 8,027 new patients and performed 679 and 1,111 IVF procedures, respectively.

Entry into high potential fertility business Fertility treatment is an emerging segment of the domestic healthcare industry which is relatively underdeveloped and fragmented. There are an estimated 2.7cr couples suffering from infertility in India, which could increase to between 2.9cr and 3.2cr by 2020 due to demographic, lifestyle and the presence of various clinical risk factors among the population. Of the estimated 2.7cr infertile couples, less than 3lakh currently seek fertility treatment, owing to a lack of awareness and access to fertility treatment, as well as high cost of the same. Nonetheless, the number of IVF cycles performed in India has increased from 7,000 in 2001 to 1lakh in 2015. The number of IVF cycles performed in India is forecast to increase to 2.6lakh by 2020, representing a 21% CAGR. Company acquired 50.1% stake in BACC Healthcare which operates four Milann fertility centres in Bengaluru. Given the large untapped potential, we believe there is significant growth opportunity in the fertility segment. Moreover, the industry fragmentation creates an opportunity to leverage the expertise of HCG brand into a speciality healthcare brand as also to build and establish Milann brand across India. The Milann fertility centres provide comprehensive reproductive medicine services, including assisted reproduction, gynecological endoscopy and fertility preservation. In H1 FY16 and FY15, Milann fertility centres registered 5,575 and 8,027 new patients and performed 679 and 1,111 IVF procedures, respectively. Existing Milann Fertility Centres

Location Year of

operation

Number of operational

beds1 IVF OT

Endoscopy OT

Embryology

Laboratory

Neonatal ICU

Bengaluru‐Shivananda Circle

1989 38

Bengaluru‐Jayanagar

2010 26

Bengaluru‐Indiranagar

2012 6 ‐2 ‐3

Bengaluru‐MS Ramaiah Nagar

2015 6 4

Source: RHP, India Infoline Research 1. Number of available operational beds includes neonatal ICU beds (as applicable) 2. Utilizes endoscopy operation theatre of a neighbouring hospital 3. Utilizes neonatal ICU facilities of a neighbouring hospital 4. Utilizes the neonatal ICU facilities of our partner

Page 4 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Real incidence of cancer in India could be 1.5‐2 times the reported rate Lack of cancer awareness and lack of participation in screening programs are key reasons for relatively late stage of disease presentation in India compared to US and China

Cancer prevalence and incidence in India: an overview The prevalence of cancer in India is estimated at 39lakh people in 2015, with 11lakh new cancer cases reported during the year. However, the real incidence of cancer in India could be significantly higher than the reported figure; data from large randomized screening trials suggests real incidence of cancer could be 1.5‐2 times higher than the reported incidence or an estimated 16‐22lakh new cancer cases in 2015. Albeit even at this level, the age adjusted cancer incidence per 100,000 people in India is significantly lower than that for United States and China. The gap between reported and real cancer incidence is primarily attributed to under‐diagnosis of cancer in India. The under‐diagnosis of cancer is represented in the relatively late stage of presentation of cancer cases in India relative to China, UK and US. Indeed data collected between 2009 and 2011 show that only 43% of breast cancer cases were diagnosed at early stages (stage I or stage II) in India while it is 62% in the US and 72% in China. Lack of cancer awareness and low participation in screening programs are key factors for the relatively late stage of the disease presentation and consequently low reported cancer incidences in India. For instance, less than 1% of women in India aged between 40‐69 years participated in recommended breast screening mammograms once in 24 months, as compared to 30% in China and 65% in US in 2014.

Cancer incidence across countries India lags in early stage (I or II) cancer diagnosis

Source: RHP, India Infoline Research

911

16‐22

34

17

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Africa India (reported)

India (real) China US

Est. cancer incidence 2015 (lakhs)

62

71

31

81

70

30

72

91

19

43

10 8

0

10

20

30

40

50

60

70

80

90

100

Breast Cervical Head and Neck

USA UK China India%

Page 5 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Demographic changes (an ageing

population), exposure to risk

factors and growing cancer

awareness key reasons for

increase in cancer incidences

Cancer profiles have changed

since 2000 as breast cancer has

overtaken cervical cancer in

women

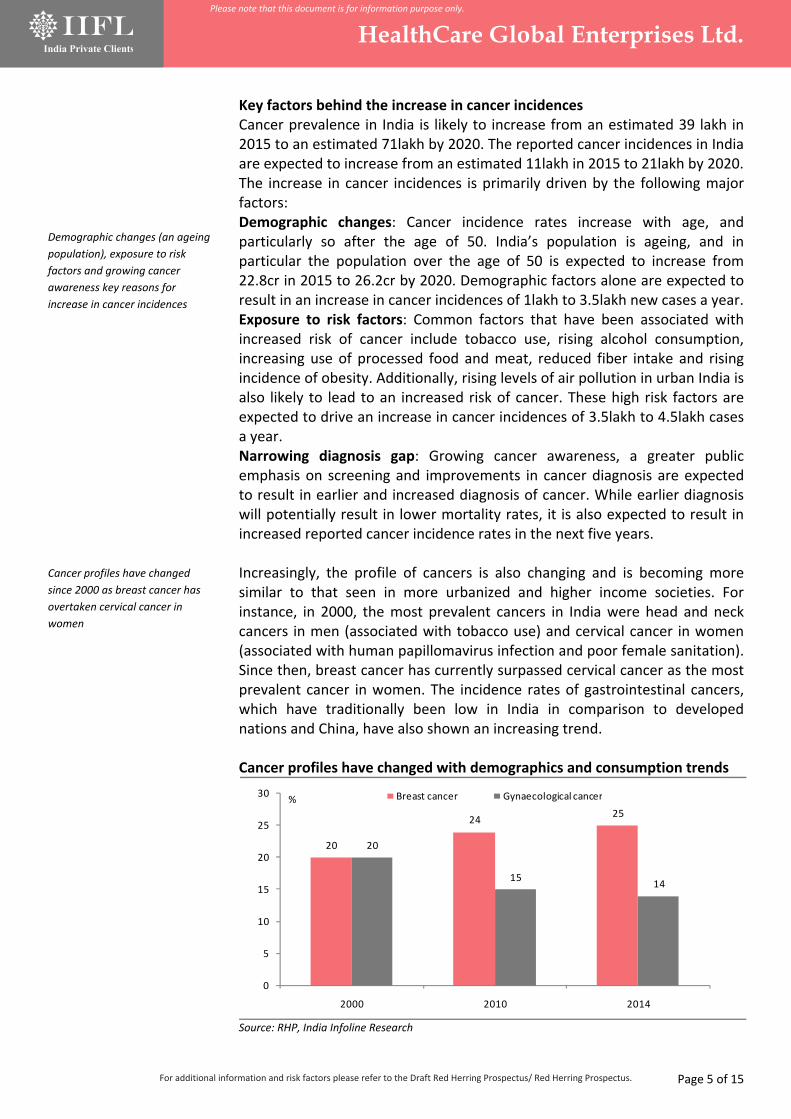

Key factors behind the increase in cancer incidences Cancer prevalence in India is likely to increase from an estimated 39 lakh in 2015 to an estimated 71lakh by 2020. The reported cancer incidences in India are expected to increase from an estimated 11lakh in 2015 to 21lakh by 2020. The increase in cancer incidences is primarily driven by the following major factors: Demographic changes: Cancer incidence rates increase with age, and particularly so after the age of 50. India’s population is ageing, and in particular the population over the age of 50 is expected to increase from 22.8cr in 2015 to 26.2cr by 2020. Demographic factors alone are expected to result in an increase in cancer incidences of 1lakh to 3.5lakh new cases a year. Exposure to risk factors: Common factors that have been associated with increased risk of cancer include tobacco use, rising alcohol consumption, increasing use of processed food and meat, reduced fiber intake and rising incidence of obesity. Additionally, rising levels of air pollution in urban India is also likely to lead to an increased risk of cancer. These high risk factors are expected to drive an increase in cancer incidences of 3.5lakh to 4.5lakh cases a year. Narrowing diagnosis gap: Growing cancer awareness, a greater public emphasis on screening and improvements in cancer diagnosis are expected to result in earlier and increased diagnosis of cancer. While earlier diagnosis will potentially result in lower mortality rates, it is also expected to result in increased reported cancer incidence rates in the next five years. Increasingly, the profile of cancers is also changing and is becoming more similar to that seen in more urbanized and higher income societies. For instance, in 2000, the most prevalent cancers in India were head and neck cancers in men (associated with tobacco use) and cervical cancer in women (associated with human papillomavirus infection and poor female sanitation). Since then, breast cancer has currently surpassed cervical cancer as the most prevalent cancer in women. The incidence rates of gastrointestinal cancers, which have traditionally been low in India in comparison to developed nations and China, have also shown an increasing trend. Cancer profiles have changed with demographics and consumption trends

Source: RHP, India Infoline Research

20

2425

20

1514

0

5

10

15

20

25

30

2000 2010 2014

Breast cancer Gynaecological cancer%

Page 6 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Even adjusted for purchasing

power parity, cancer treatment

costs in India are much cheaper as

compared to US

Large gap exists in terms of cancer

diagnosis and treatment

attributed to lack of adequate

infrastructure and absence of

mass screening programs

Though India cheaper than US in cancer treatment… The annual expenditure in India for the diagnosis and treatment of cancer is estimated to be between US$1.7‐2.0bn as of 2015. Even at for‐profit hospitals in India, the cost of cancer care, including treatment with the advanced technologies (such as PET‐CT and LINAC based radiation therapy) represents only a fraction of the cost of treatment in the United States even after adjusting for purchasing power parity. Even though the cost of cancer treatment in India is significantly lower than in US, high quality cancer care is still unaffordable and inaccessible to a large proportion of domestic population due to low penetration of public and private insurance and low average household income levels.

Cancer treatment is much cheaper in India Treatment India US US (PPP adjusted)

Chemotherapy Rs1,50,000‐2,40,000 US$1.3‐1.8mn Rs5,10,000‐7,20,000

Surgery Rs60,000‐1,00,000 US$1.5‐1.8mn Rs6,00,000‐7,20,000

Radiation therapy Rs60,000‐1,00,000 US$1.1‐1.4mn Rs4,20,000‐5,40,000

Source: RHP, India Infoline Research

…large gap exists in diagnosis and treatment of the same Though India would be better placed in terms of cancer treatment costs, a lack of adequate infrastructure and absence of mass screening programs remain key barriers to timely diagnosis. As of 2014, there is only 1 mammogram installed per 220,000 women, as compared to 1 per 10,000 women in US. Moreover, as of 2015, there are 121 PET‐CT scanners installed, of which around 50% are in metropolitan cities; PET‐CT scanners are essential for accurate diagnosis, staging and response monitoring of cancer and are therefore critical to providing comprehensive cancer care. Also as of 2014, only 30% of the cancer centres have advanced imaging technologies such as PET‐CT. PET‐CT scans use Fludeoxyglucose (FDG, a radioactive material), which is manufactured in a cyclotron and has limited shelf life, making it difficult to transport to remote locations. As of 2015, India has only 15 cyclotrons all of them located in the metropolitan areas.

LINACs per 10lakh population No. of PET CTs per 10lakh new cancer cases/year

Source: RHP, India Infoline Research

11.9

5

0.7 0.3

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

US UK China India

#

77 110 137 200

1,238

0

200

400

600

800

1,000

1,200

1,400

Africa India China UK US

#

Page 7 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Demographic and lifestyle

changes along with clinical factors

are key reasons for increase in

infertility incidences

Key factors behind increase in infertility incidences The prevalence of infertility in India has been rising owing to various factors. These include:

Demographic changes: The number of women of reproductive age in India is forecast to increase by 14% between 2010 and 2020 of which the number of women between 30 years and 44 years of age is forecast to increase by about 20% during the period which is likely to result in an increase in infertility prevalence.

Lifestyle changes: Changes in lifestyle such as increasing marital age, increasing number of working women, rising alcohol and tobacco consumption are among the factors responsible for growing infertility incidences in India.

Clinical factors: Prevalence of several known clinical risk factors among the Indian population is also responsible for growing infertility incidences. These include:

Poly‐Cystic Ovarian Syndrome (PCOS): PCOS is a condition caused by a hormone imbalance in women, which can result in insulin resistance, obesity, ovarian cysts and infertility. Various studies have reported PCOS prevalence in India to be between 3.7% and 22.5% among women.

Endometrium Tuberculosis: Genital tuberculosis causes tubal blockage and endometrial damage resulting in infertility. Studies published between 1997 and 2008 have estimated that about 18% of the infertile women of reproductive age in India were suffering from genital tuberculosis.

Obesity: Prevalence of obesity, a known risk factor for infertility, among Indian women has been steadily rising, from 10.6% in 1998 to around 24.7% in 2014.

Ethnicity: Research studies suggest that women of South Asian ethnicity might have poor ovarian reserves and an earlier onset of infertility compared to Caucasians.

Page 8 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

IVF market is underpenetrated in

India as compared to US

Underpenetrated market for IVFs The primary assisted reproduction treatment options include intrauterine insemination (IUI) and in‐vitro fertilization (IVF) though surgical procedures may also be required in certain patients. In a sign of under penetration, India recorded 2,786 IVF cycles per 10lakh infertile women aged between 20‐44 years in 2015, compared to 46,042 IVF cycles in US in 2013. As of 2015, around 1% of the 2.75cr couples suffering from infertility presented for fertility assessment. The number of IVF cycles performed in India has grown at a CAGR of 18.1% over the last 10 years which mirrors similar trends witnessed in most developed countries in lieu of increased prevalence of infertility. The number of couples presenting for infertility treatment is expected to increase from 2.7lakh in 2015 to around 6.5‐7lakh annually in 2020 along with rise in IVF cycles from 1lakh in 2015 to an estimated 2.6lakh in 2020. Snapshot of infertility treatment in India

Source: RHP, India Infoline Research

2.75cr

~2,70,00065,000 1,00,000

Infertile couples of reproductive age

Couples who come forward for evaluation

Couples availing IVF treatment

Total IVF cycles

1% of infertile couples

Page 9 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Company is in the midst of

developing 12 comprehensive

cancer care centers which would

be commercialized in FY16/17/18

Company would focus on brand

building through traditional and

digital advertising and grow the

existing base of physicians

Company would open cancer

centers in Africa in partnership

with CDC; it would open centers in

Kenya, Tanzania and Uganda in

the first phase

Strategies Expand the reach of cancer care network in India The company plans to expand HCG network by establishing new cancer centres across India and by expanding the capacity and service offerings of existing centres. As of December 31, 2015, HCG is in the midst of establishing 12 new comprehensive cancer centers which would be commercialized during FY16/17/18 along with expansion of existing centres at Cuttack and Ahmedabad. The company carries out competitive assessment of the target markets based on a number of factors which include 1) estimated incidence of cancer in the primary and secondary catchment population 2) number of comprehensive cancer centres, if any, in the catchment area and average distance patients have to travel to avail of such care 3) affordability of healthcare generally and cancer care in particular and 4 available third party payer options, whether corporate, government or private insurance.

Strengthen HCG brand to reach more cancer patients As the company establishes new comprehensive cancer centres across India, it also plans to invest in brand building, expanding market presence, brand image and visibility. It intends to strengthen patient support groups comprising cancer survivors to further spread awareness of cancer screening and to educate patients regarding cancer treatment options and their relative outcomes and benefits. These initiatives would further strengthen brand and commitment to the community, cancer patients and their families. HCG would continue to grow the base of referring physicians through ongoing community outreach programmes and continuing medical education programmes targeting such physicians. It would also strengthen brand through advertising in digital and traditional media like print, TV and outdoor primarily comprising of patient testimonials and socially relevant messages.

Expand cancer care network to Africa According to the company, there has been a rising incidence of cancer and shortage of cancer centres in many African countries; consequently, patients have to often travel outside the region at a significant cost for availing quality cancer care, including to HCG cancer centres in India. In the past, it has experienced an increase in the number of patients travelling from Africa to Bengaluru and other cancer centres for treatment. Thus international patients accounted for ~17.8% of H1 FY16 revenues and are the primary reason for current plans to establish a network of specialty cancer centres in Africa. Accordingly, it would partner with CDC, a development finance institution, which would invest in subsidiary, HCG Africa. In the first phase, HCG Africa plans to open centres in Kenya, Tanzania and Uganda and additional centres in other parts of Africa on a selective basis.

Page 10 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Domestic IVF market is under

penetrated as company estimates

potential demand for IVF cycles

could be 9‐12 times higher than

current number in key cities like

Delhi, Mumbai and Bengaluru

Expand and build Milann brand network of fertility centres The domestic IVF market is under‐penetrated as the company estimates potential demand for IVF cycles could be 9‐12 times higher than the current actual number of patients availing treatment in Delhi, Mumbai and Bengaluru. The number of infertile couples availing fertility treatment is estimated to rise to 6.5‐7lakh from current 2.7lakh by 2020. In order to address the growing demand for fertility treatment, company plans to expand Milann network by setting up green field centres and also by entering into partnership arrangements and undertaking selective acquisitions; as of December 2015, it is in the midst of establishing three fertility centres.

Objects of the issue Use of net proceeds Rs.cr

Purchase of medical equipment 42.21

Investment in IT software, services and hardware 30.19

Pre‐payment of debt 147.05

General corporate purpose1 ‐

Source: RHP, India Infoline Research 1. To be finalized upon determination of the Offer Price Proposed cancer centers under development

Location No. of beds1

No of RT‐LINAC No. of OT5

No. of PET‐CT

scanners Laboratory

Nagpur2 115 1 4 1

Mumbai‐Borivali2 105 1 5 1 Kochi 100 1 3 1 Delhi 95 1 1 ‐7 8

Kanpur3 90 1 3 1 Baroda2 60 1 4 1 Vishakhapatnam3 88 1 ‐6 1 Gulbarga 85 1 3 ‐ Jaipur 60 1 2 1 Kolkata2 50 1 2 ‐7 8

Bhavnagar4 35 1 3 ‐ Mumbai‐Cooperage 32 1 2 1

Source: RHP, India Infoline Research 1. Number of operational beds (as proposed) includes ICU beds and day‐care beds but excludes self‐care beds 2. Set up through limited liability partnership with partner(s) 3. Set up by through subsidiary 4. Existing multi‐speciality hospital at Bhavnagar will be upgraded into a comprehensive cancer centre through the addition of radiation and medical oncology capabilities 5. Including major and minor operation theatres. Major operation theatres are used to perform complex surgeries and minor operation theatres are used to perform minor surgical procedures 6. To utilize operation theatre of partner to provide surgical services 7. PET‐CT procedures will be performed by partner 8. Laboratory services will be provided by partner

Page 11 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Expansion of existing centres In addition to above, as of December 31, 2015, company is also expanding two of existing comprehensive cancer centres to cater to the increasing demand for cancer care at these centres. These include: Comprehensive cancer centre at Cuttack, where it is adding new

equipment, including a linear accelerator, and increasing the number of beds and

Comprehensive cancer centre at Ahmedabad, where it is adding new equipment, including a linear accelerator, a PET‐CT scanner, an MRI scanner and a gamma camera.

Page 12 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Background of promoters

Dr. BS Ajai Kumar is the Chairman and CEO of HCG. He has been a Director of the company since March 7, 2000 and was re‐appointed as the CEO with effect from July 1, 2015. He holds a bachelor’s degree in Medicine and Surgery from St. John’s Medical College, Bengaluru, India. He completed his residency in Oncology from the University of Virginia Hospital, Charlottesville and his residency in Radiotherapy from the University of Texas System Cancer Centre, MD Anderson Hospital and Tumour Institute, Texas, USA. He has been awarded the Ernst and Young Entrepreneur of the Year Award for the start‐up category in healthcare and the BC Roy Award by the Indian Science Monitor. He has also been awarded the CII Regional Emerging Entrepreneurs Award for the contribution made by the company in healthcare. Mr. Gangadhara Ganapati is a Non‐Executive Director of the company and has been a Director since December 21, 2005. He holds a bachelor’s degree in Mechanical Engineering from the IIT, Madras, and a Post Graduate Diploma in Management from the IIM, Ahmedabad. He also holds a master’s degree in Business Administration from the Wharton School, University of Pennsylvania. In the past, he has worked as the managing Director of Adamas India Pharmaceuticals Private Limited, and as vice president, corporate development of NeuroMolecular Pharmaceuticals, Inc. He founded Triesta Sciences, Inc. and served as its CEO from 2002 until 2006. He served in the Tata Administrative Service at Tata Industries Limited from 1990 to 1994. Mr. Prakash Parthasarathy is a Non‐Executive Director of the company since April 23, 2008. He holds a bachelor’s degree in Computer Science from the Birla Institute of Technology and Sciences, Pilani and a Post Graduate Diploma in Management from the IIM, Bangalore. He also serves as the chief investment officer of PremijiInvest and its affiliates and is a director on the boards of the NSE and FabIndia Overseas Private Limited.

Key management personnel Name Designation

Dr. BS Ajai Kumar Chairman and CEO

Mr. A Sadasivam Executive Director (Operations)

Dr. Mudit Saxena COO, Karnataka, MP and Rajasthan

Dr. Bharat Gadhavi COO, Gujarat

Dr. Kamini Rao Medical Director (Milann)

Mr. Dinesh Madhavan Director, Healthcare services

Mr. Krishnan Subramanian CFO

Mr. Anant Kittur Director (Projects)

Dr. Ramachandran Balaji Chief Medical and Information Officer

Mr. MC Jayaprakash Vice President (HR)

Dr. Naveen Nagar Vice President (Medical Services)

Mr. Sunu Manuel CS and Compliance Officer

Source: RHP, India Infoline Research

Page 13 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Financials (Restated consolidated)

Income statement (Rs cr) FY13 FY14 FY15 8m FY16

Turnover (net) 338 451 519 379

Other income 2 4 5 2

Total revenue 341 455 524 381

Total operating expense (292) (413) (443) (323)

EBIDTA 49 42 81 58

Depreciation (30) (36) (40) (29)

Finance costs (29) (32) (34) (24)

PBT (10) (27) 2 (0)

Tax (1) (5) 2 (1)

PAT (11) (36) 1 (4)

Balance sheet (Rs cr) FY13 FY14 FY15 8m FY16

Equity & liabilities

Share capital 67 68 70 73

Reserves 217 196 210 221

Net worth 283 264 279 295

Minority interest 13 18 25 27

Non‐curr liabilities

LT borrowings 239 252 280 358

Def tax liabilities 1 1 1 1

Other LT liabilities 13 2 1 1

LT provisions 3 2 2 2

Total non‐curr liab 257 257 284 362

Current liabilities

ST borrowings 38 18 29 27

Trade payables 53 71 83 99

Other cur liab 65 58 71 77

ST provisions 0 3 3 4

Total curr liab 156 149 187 207

Total liabilities 709 689 776 891

Assets

Non‐current assets

Goodwill on consol 61 60 61 61

Fixed assets 448 462 510 596

Non‐curr investments 0 2 0 0

Def tax assets 1 0 6 7

LT loans and adv 40 49 70 84

Other non‐curr assets 5 5 7 9

Total non‐curr assets 554 579 654 758

Current assets

Inventories 10 12 15 14

Trade receivables 60 53 64 75

Cash and Bank 11 25 27 20

ST loans and adv 7 12 8 9

Other curr assets 67 8 9 16

Total curr assets 155 110 122 133

Total assets 709 689 776 891

Cash flow statement (Rs cr) FY13 FY14 FY15 8m FY16

Cash Flow from operating activities

PBT (10) (27) 2 (0)

Dep & Amortization 30 36 41 30

Finance costs 28 30 32 22

Interest and Dividend (1) (2) (3) (1)

Liabilities write back (0) (0) (0) (0)

Prov for doubtful trade 3 15 3 2

Others ‐ ‐ 0 2

Op. profit/(loss) 49 54 76 55

Changes in working cap (11) 6 (10) (2)

Cash generation from ops 39 60 66 54

Net income tax (8) (9) (7) (6)

Net CF from op. activities 31 51 60 47

CF from investing activities

Capital expenditure (89) (51) (80) (135)

Purchase of LT inv (45) (17) (4) ‐

Current investment (60) 61 ‐ ‐

Settlement amount ‐ ‐ ‐ 13

Net ICDs ‐ (5) 3 ‐

Net margin money (2) (1) (2) (1)

Interest and Dividend 0 1 3 1

Net CF from inv. activities (197) (12) (80) (122)

CF from fin. activities

Issue of shares 80 15 10 18

Proposed IPO expenses ‐ ‐ ‐ (5)

Amount received from minority shareholders

1 2 2 2

Net LT borrowings 69 4 28 79

Net ST borrowings 27 (25) 16 (2)

Finance costs (26) (28) (30) (25)

ICD and unsecured loans ‐ 5 (5) 1

Subsidiary dividend (12) ‐ ‐ ‐

Net CF from fin activities 140 (27) 22 68

Cash generated/(utilized) (26) 13 2 (7)

Cash at start of the year/acquisition of subsidiaries during the year

36 9 23 25

Cash at end of the year 9 22 25 18

Cash and cash eq as per BS, as restated

11 25 27 20

Less deposit held as margin money not considered as cash

(1) (3) (2) (2)

Cash and cash eq as per AS3 CF statements

9 22 25 18

Page 14 of 15

HealthCare Global Enterprises Ltd. Please note that this document is for information purpose only.

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

Annexure

Key milestones of HCG Calendar year Event

2005 Entered into the clinical laboratory business through acquisition of Triesta Sciences Inc. and Triesta Sciences (India) Private Limited

2006 India Development Fund made its first investment of Rs.50cr in the company

2006 BMORCL became HCG subsidiary

2007 HCG Medi‐Surge became a subsidiary

2007 Evolvence made its first investment of Rs.22.5cr in the company

2008 NTICPL made its first investment of Rs.40cr in the company

2009 Amalgamation of Triesta Sciences (India) Private Limited and Triesta Sciences Inc. with company

2010 IL&FS Trust Company Limited a/c MPEF, through its scheme India Build Out Fund I and MAT made its first investment of Rs.31.2cr in the company

2011 Amalgamation of BMORCL with HCG

2011 PIOF became a shareholder by purchasing shares from NTICPL

2013 V‐Sciences made its first investment of Rs.60cr in the company

2013 Entered into the fertility business through acquisition of 50.1% stake in BACC Healthcare

2014 Demerger of multispecialty division from HCG Medi‐Surge and vesting of the same with the company

2015 HCG Regency became a subsidiary

2015 Amalgamation of HCG Vijay with the company

Existing HCG cancer care centers

Location Year of

operation No. of beds3

No. of RT‐LINAC No. of OT9

No. of PET‐CT scanners

Laboratory

Bengaluru‐Double Road 1989 92 1 4 ‐ 12

Shimoga1 2003 60 1 3 ‐ 13

Bengaluru‐Kalinga Rao Road2 2006 234 38 7 2

Bengaluru‐MS Ramaiah Nagar 2007 22 1 1 1 13

Nasik 2007 ‐4 1 ‐10 1 13

Delhi 2007 70 1 2 111 13

Hubli 2008 57 1 2 1 13

Ranchi 2008 54 1 2 ‐ Cuttack 2008 116 1 2 1

Vijaywada 2009 305 2 1 ‐ Chennai 2012 356 1 ‐10 ‐ 13

Ongole 2012 197 1 2 ‐

Ahmedabad1 2012 78 1 5 ‐

Tiruchirappalli 2014 35 1 ‐ 13 Source: RHP, India Infoline Research 1. Operated through subsidiary 2. Comprehensive cancer centre located at Kalinga Rao Road in Bengaluru is centre of excellence 3. Number of available operational beds includes ICU beds and day‐care beds (as applicable) but excludes self‐care beds 4. Utilize beds, including the ICU beds of partner 5. In addition, HCG has 120 self‐care beds at comprehensive cancer centre in Vijaywada 6. Utilize an additional 12 ICU beds of partner 7. In addition, it has 61 self‐care beds at comprehensive cancer centre in Ongole 8. Includes a WBRRS system 9. Includes major and minor operation theatres. Major operation theatres are used to perform complex surgeries and minor operation theatres are used to perform minor surgical procedures 10. Utilize operation theatre of partner to provide surgical services. 11. PET‐CT procedures are performed at the SMH DCA Imaging Centre, which is part of comprehensive cancer centre in Delhi 12. Laboratory services are provided by Triesta central reference laboratory. 13. Laboratory services are provided by partner

Page 15 of 15

For additional information and risk factors please refer to the Draft Red Herring Prospectus/ Red Herring Prospectus.

DISCLAIMER

This document has been prepared by India Infoline Limited (India Infoline). India Infoline Group (hereinafter referred as IIFL) is engaged in diversified financial services business including equity broking, DP services, merchant banking, portfolio management services, distribution of Mutual Fund, insurance products and other investment products and also loans and finance business. India Infoline Ltd (“hereinafter referred as IIL”) is a part of the IIFL Holdings Ltd. and is a member of the National Stock Exchange of India Limited (“NSE”) and the BSE Limited (“BSE”). IIL is a Depository Participant registered with NSDL & CDSL and a SEBI registered portfolio manager. IIL is also a large broking house catering to retail, HNI and institutional clients. It operates through its branches and authorised persons and sub‐brokers spread across the country and the clients are provided online trading through internet and offline trading through branches and Customer Care. IIFL Holdings Limited is a SEBI registered merchant banker. This document does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction or an invitation for an offer to invest. The information contained herein is sourced from publicly available data or sources believed to be reliable, but we do not represent that it is accurate or complete and it should not be relied on as such. India Infoline has not independently verified all the information given in this document. Accordingly, no representation or warranty, express or implied, is made as to the accuracy, completeness or fairness of the information and opinions contained in this document. India Infoline nor any of its affiliates shall be in any way responsible for any loss or damages whether direct or indirect, incidental, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. This document is provided for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Nothing in this document constitutes any investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to any specific circumstances. The securities discussed and opinions expressed in this document may not be suitable for all investors, and all investors must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. Each recipient of this document should make such necessary and independent investigation as may be necessary to arrive at an independent evaluation of an investment in the securities of company referred to in this document (including the merits and risks involved), and should consult his/her own professional advisors to determine the merits and risks of such investment. We, India Infoline and our affiliates, officers, directors, and employees may: (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of the company mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as advisor or lender / borrower to the company or have other potential conflict of interest with respect to any recommendation and related information and opinions. The information contained herein this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. The information contained herein is subject to change without any prior notice. India Infoline reserves the right to make any modifications or alterations to this statement as may be required from time to time. However, India Infoline is under no obligation to update or keep the information current. Neither India Infoline nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. HCG Ltd. is proposing, subject to market conditions and other considerations, a public issue of its equity shares and has filed the Red Herring Prospectus with the Registrar of Companies. The Draft Red Herring Prospectus/ Red Herring Prospectus is available on the websites of SEBI at www.sebi.gov.in and at the website of the Book Running Lead Manager(s) as mentioned in the Draft Red Herring Prospectus/ Red Herring Prospectus. The data would be provided to the clients on an "as is" and "where‐is" basis, without any warranty. India Infoline or its subsidiaries and associated companies shall not be liable for any delay or any other interruption which may occur in providing the data due to any reason including network (Internet) reasons or snags in the system, break down of the system or any other equipment, server breakdown, maintenance shutdown, breakdown of communication services or inability of the India Infoline or its subsidiaries and associated companies to provide the data. This document is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied, in whole or in part, for any purpose. Neither this document nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), directly or indirectly, in the United States or distributed or redistributed to any resident thereof. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject India Infoline to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. This report is published by IIFL ‘India Private Clients’ research desk. IIFL has other business units with independent research teams separated by 'Chinese walls' catering to different sets of customers having varying objectives, risk profiles, investment horizon, etc. The views and opinions expressed in this document may at times be contrary in terms of rating, target prices, estimates and views on sectors and markets. In no event shall the India Infoline or its subsidiaries and associated companies be liable for any damages, including without limitation direct or indirect, special, incidental, or consequential damages, losses or expenses arising in connection with the data provided by the India Infoline or its subsidiaries and associated companies and contained in this document. The document and the information contained herein is strictly confidential and meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent.

The Draft Red Herring Prospectus/ Red Herring Prospectus can be accessed at: iiflcap.com

Published in 2016. © India Infoline Ltd 2016

![ResearchReports … · 2019. 11. 12. · ResearchReports InterculturalProfilesandAdaptationAmongImmigrantandAutochthonous Adolescents CristianoInguglia*a,PasqualeMussoa [a]DepartmentofPsychological](https://img.pdfslide.us/doc/110x75/60817c6fdf091e14725176e4/researchreports-2019-11-12-researchreports-interculturalprofilesandadaptationamongimmigrantandautochthonous.jpg)