Embed Size (px)

Citation preview

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 1/9

Hawkamah Brief on Corporate Governance Codes of the GCC

Introduction

Corporate governance codes globally have become major instruments in restoring and maintaining public andinvestor confidence and in the promotion of sound management. Good corporate governance attracts investors,protects investors and other stakeholders, and enhances companies’ value. The first code in the GCC wasissued in 2002 by Oman and in 2010 Bahrain became the latest GCC country to draft a code. With five of theGCC countries having now issued their corporate governance codes, this Brief will provide a snapshotcomparison of some of their key provisions, highlighting similarities as well as the current best practices.

The major difference in the codes relate to the issue of enforcement. Most of the GCC countries have opted forvoluntary compliance (“comply or explain”), whereas in the UAE the provisions are mandatory (“comply or bepenalized”).

Role of the Board

The Board of Directors manages the company on behalf of its owners, the shareholders. In doing so, the Boardcarries out key tasks such as: establishing and maintaining vision, mission and values; deciding strategy andstructure; delegating to management; and accounting to shareholders and being responsible to stakeholders.

According to the international best practice the overarching role of the Board is to strategically guide and

oversee management. The 2008 Hawkamah-IFC survey found that the role of the board is often misunderstoodin the MENA region. According to the survey, 89.9% of MENA banks and listed companies stated that theBoard, and not management, was responsible for setting corporate management, which is contrary to the goodpractice that management develops, and the board reviews and guides corporate strategy.

It is therefore important for corporate governance codes to set out the roles of the key governance stakeholdersin very clear terms. All the GCC codes, with the exception of the UAE, have a separate section on the role of theboard. The Qatari code, for example, sets a clear overarching role for the Board that it is responsible for“approving the company’s strategic objectives, appointing and replacing management, setting forthmanagement compensation, reviewing management performance and ensuring succession planning” inaddition to “ensuring the company’s compliance with laws and regulations” (Art 5.2). The Bahraini codecontains a similar provision. Some GCC codes, such as the Saudi code assign very specific responsibilities to the

board such as “supervising the main capital expenses of the company and acquisition/disposal of assets”.

It is also useful for any corporate governance code to set out the duties of the various governance stakeholders.The UAE and Qatari codes, for example, specify the duties of the Board Chairman. Bahrain, Qatar and Omanall lay out the role of the Non-Executive Director (NED). Article 1.3 of the Bahraini code states that NEDs“should constructively scrutinize and challenge management including management performance of executivedirectors”. The Omani code helpfully also outlines the role of the executives. On the issue of delegation, Saudi,Bahrain and Qatari codes all remind the Board members that although they may delegate certain functions tocommittees or management, they may not delegate its ultimate responsibility.

The Board and Corporate Governance

The UAE Code states that the Board should develop procedural rules for corporate governance. The SaudiCode assigns the Board with the responsibility for drafting a Corporate Governance Code for the company.Bahraini Code calls for a Board Charter, specifying the matters reserved for the board. Similarly the QatariCode mandates the formulation of a Board Charter detailing the Board’s functions and responsibilities. Annex 2of the Code provides a sample Board Charter and this Charter should be publicly disclosed.

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 2/9

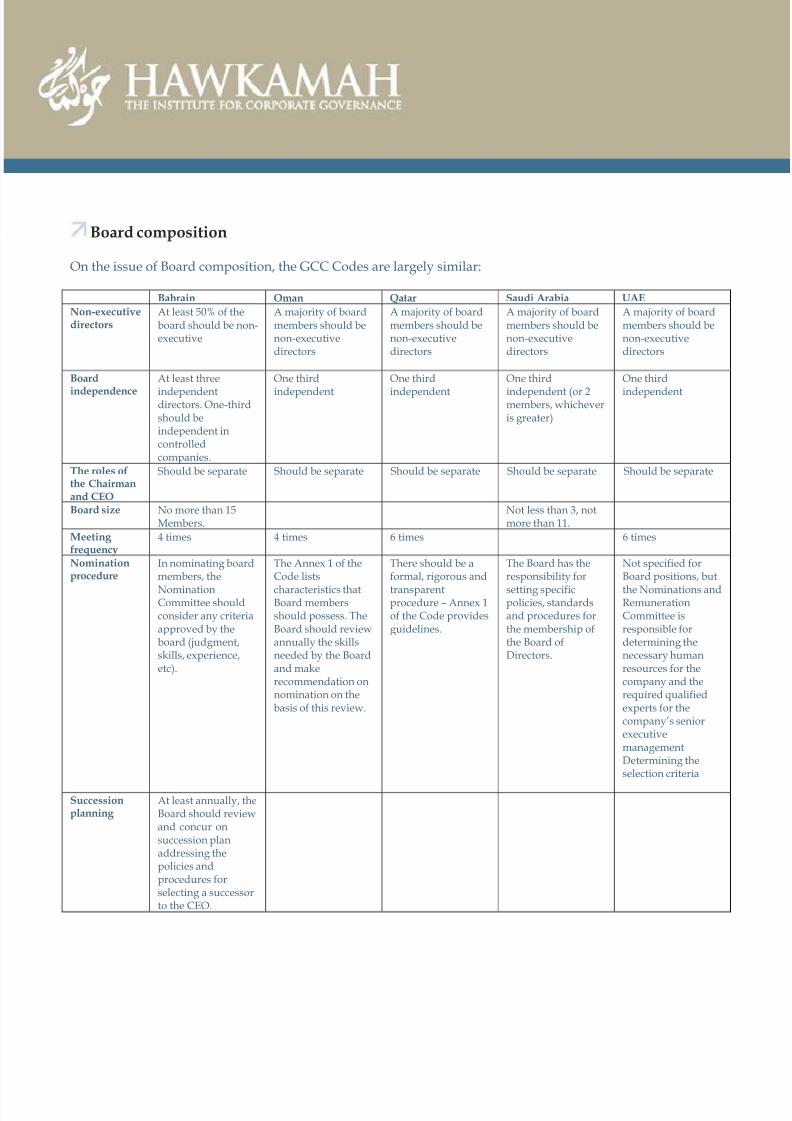

Board composition

On the issue of Board composition, the GCC Codes are largely similar:

Bahrain Oman Qatar Saudi Arabia UAE

Non-executivedirectors

At least 50% of theboard should be non-executive

A majority of boardmembers should benon-executivedirectors

A majority of boardmembers should benon-executivedirectors

A majority of boardmembers should benon-executivedirectors

A majority of boardmembers should benon-executivedirectors

Board

independence

At least three

independentdirectors. One-thirdshould beindependent incontrolledcompanies.

One third

independent

One third

independent

One third

independent (or 2members, whicheveris greater)

One third

independent

The roles ofthe Chairmanand CEO

Should be separate Should be separate Should be separate Should be separate Should be separate

Board size No more than 15Members.

Not less than 3, notmore than 11.

Meeting frequency

4 times 4 times 6 times 6 times

Nominationprocedure

In nominating boardmembers, the

NominationCommittee shouldconsider any criteriaapproved by theboard (judgment,skills, experience,etc).

The Annex 1 of theCode lists

characteristics thatBoard membersshould possess. TheBoard should reviewannually the skillsneeded by the Boardand makerecommendation onnomination on thebasis of this review.

There should be aformal, rigorous and

transparentprocedure – Annex 1of the Code providesguidelines.

The Board has theresponsibility for

setting specificpolicies, standardsand procedures forthe membership ofthe Board ofDirectors.

Not specified forBoard positions, but

the Nominations andRemunerationCommittee isresponsible fordetermining thenecessary humanresources for thecompany and therequired qualifiedexperts for thecompany’s seniorexecutivemanagementDetermining theselection criteria

Successionplanning

At least annually, theBoard should reviewand concur onsuccession planaddressing thepolicies andprocedures forselecting a successorto the CEO.

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 3/9

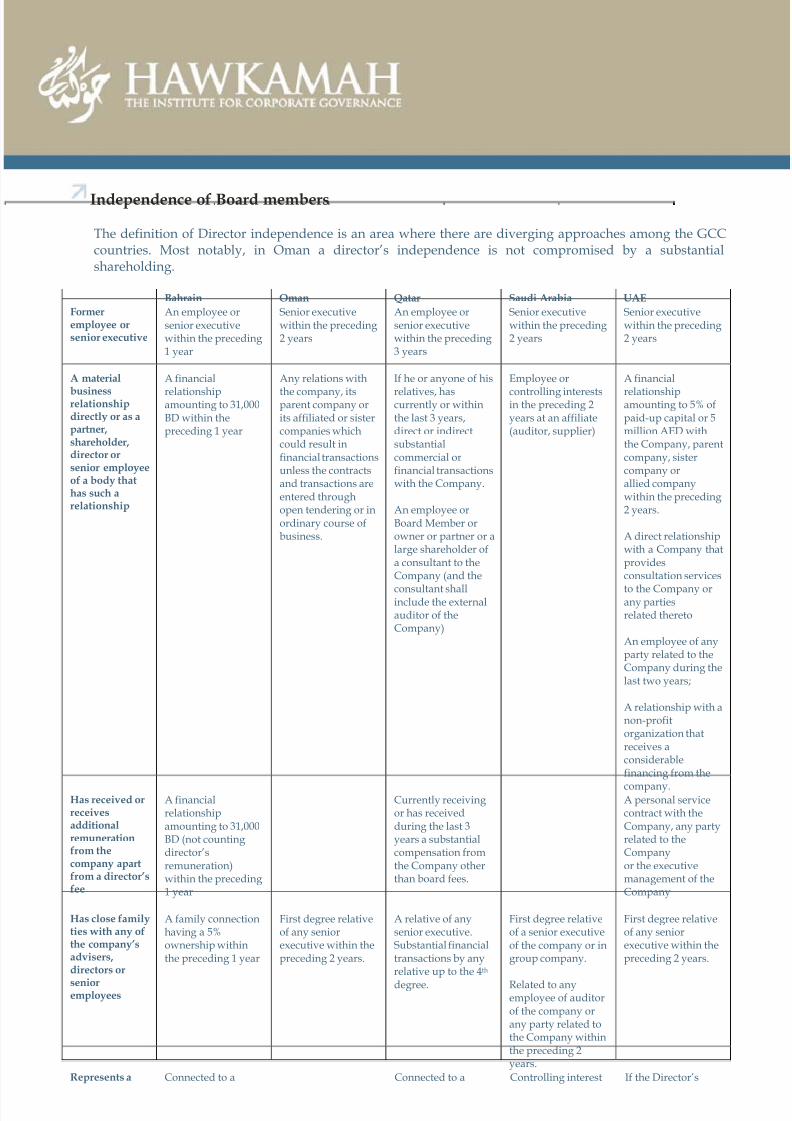

Independence of Board members

The definition of Director independence is an area where there are diverging approaches among the GCCcountries. Most notably, in Oman a director’s independence is not compromised by a substantialshareholding.

Bahrain Oman Qatar Saudi Arabia UAE

Formeremployee orsenior executive

An employee orsenior executivewithin the preceding1 year

Senior executivewithin the preceding2 years

An employee orsenior executivewithin the preceding3 years

Senior executivewithin the preceding2 years

Senior executivewithin the preceding2 years

A material

businessrelationshipdirectly or as apartner,shareholder,director orsenior employeeof a body thathas such arelationship

A financial

relationshipamounting to 31,000BD within thepreceding 1 year

Any relations with

the company, itsparent company orits affiliated or sistercompanies whichcould result infinancial transactionsunless the contractsand transactions areentered throughopen tendering or inordinary course ofbusiness.

If he or anyone of his

relatives, hascurrently or withinthe last 3 years,direct or indirectsubstantialcommercial orfinancial transactionswith the Company.

An employee orBoard Member orowner or partner or alarge shareholder ofa consultant to theCompany (and the

consultant shallinclude the externalauditor of theCompany)

Employee or

controlling interestsin the preceding 2years at an affiliate(auditor, supplier)

A financial

relationshipamounting to 5% ofpaid-up capital or 5million AED withthe Company, parentcompany, sistercompany orallied companywithin the preceding2 years.

A direct relationshipwith a Company thatprovidesconsultation services

to the Company orany partiesrelated thereto

An employee of anyparty related to theCompany during thelast two years;

A relationship with anon-profitorganization thatreceives aconsiderablefinancing from the

company.Has received orreceivesadditionalremunerationfrom thecompany apartfrom a director’sfee

A financialrelationshipamounting to 31,000BD (not countingdirector’sremuneration)within the preceding1 year

Currently receivingor has receivedduring the last 3years a substantialcompensation fromthe Company otherthan board fees.

A personal servicecontract with theCompany, any partyrelated to theCompanyor the executivemanagement of theCompany

Has close familyties with any ofthe company’sadvisers,directors or

senioremployees

A family connectionhaving a 5%ownership withinthe preceding 1 year

First degree relativeof any seniorexecutive within thepreceding 2 years.

A relative of anysenior executive.Substantial financialtransactions by anyrelative up to the 4th

degree.

First degree relativeof a senior executiveof the company or ingroup company.

Related to anyemployee of auditorof the company orany party related tothe Company withinthe preceding 2years.

First degree relativeof any seniorexecutive within thepreceding 2 years.

Represents a Connected to a Connected to a Controlling interest If the Director’s

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 4/9

significant

shareholder

shareholder holding

more than 10% ofvoting shares withinthe preceding 1 year

shareholder holding

more than 10% ofvoting shares.

in the company or in

a group company.

children have a share

ownership of morethan 10%

Holds cross-directorships orhas significantlinks with otherdirectorsthroughinvolvement inother companiesor bodies

An employee of alegal entity where asenior executivemanager of thecompany or anyoneof his relatives or anyother person who isunder the control ofeither of them; is amember of the boardof directors, or a

senior executive, or alarge shareholder (atleast 10% of votingshares) of that legalentity.

Board membershipin any groupcompany

Long Boardtenure

Serving more than 6years is relevant tothe determination ofindependence.

Board membershipfor more than 9consecutive years

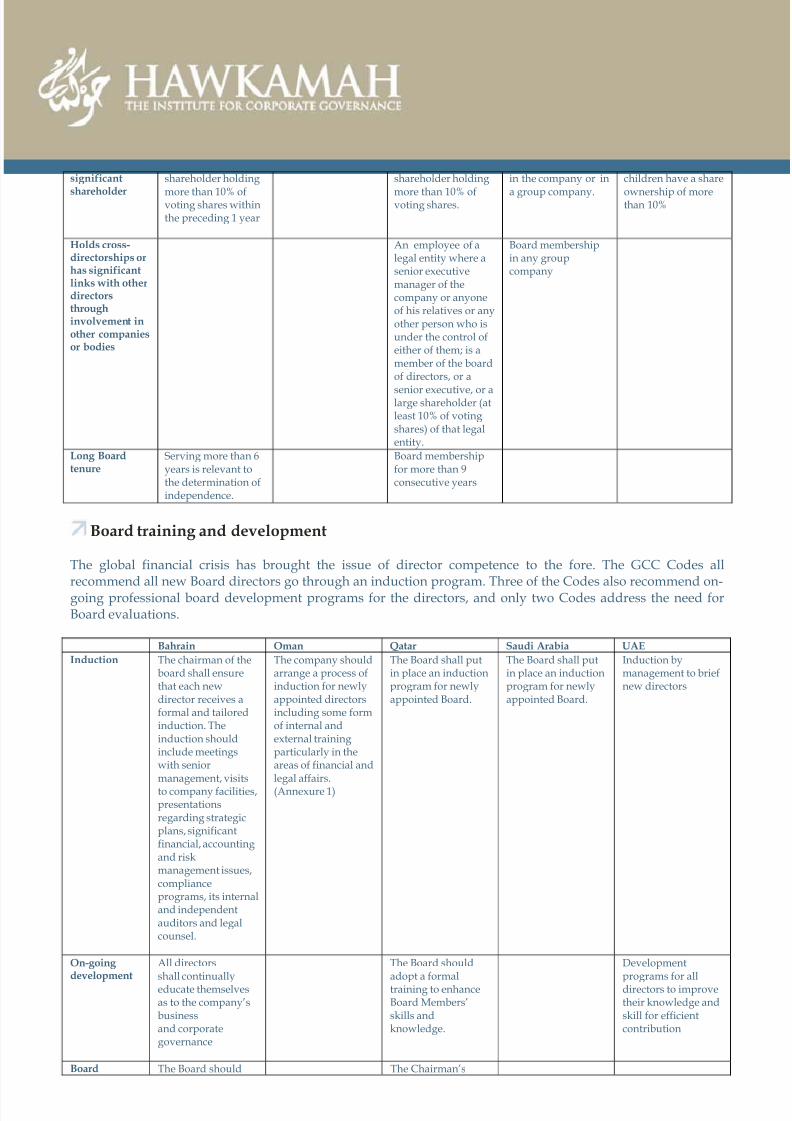

Board training and development

The global financial crisis has brought the issue of director competence to the fore. The GCC Codes allrecommend all new Board directors go through an induction program. Three of the Codes also recommend on-going professional board development programs for the directors, and only two Codes address the need forBoard evaluations.

Bahrain Oman Qatar Saudi Arabia UAE

Induction The chairman of theboard shall ensurethat each newdirector receives aformal and tailoredinduction. Theinduction shouldinclude meetingswith seniormanagement, visitsto company facilities,presentationsregarding strategicplans, significantfinancial, accountingand riskmanagement issues,complianceprograms, its internaland independentauditors and legalcounsel.

The company shouldarrange a process ofinduction for newlyappointed directorsincluding some formof internal andexternal trainingparticularly in theareas of financial andlegal affairs.(Annexure 1)

The Board shall putin place an inductionprogram for newlyappointed Board.

The Board shall putin place an inductionprogram for newlyappointed Board.

Induction bymanagement to briefnew directors

On-going development

All directors

shall continuallyeducate themselvesas to the company’sbusinessand corporategovernance

The Board should

adopt a formaltraining to enhanceBoard Members’skills andknowledge.

Development

programs for alldirectors to improvetheir knowledge andskill for efficientcontribution

Board The Board should The Chairman’s

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 5/9

evaluation conduct an

evaluation of its ownperformance, theperformance of itscommittees and itsindividual directors.

duties includes

ensuring an annualevaluation of theBoard’s performance.the NominationCommittee shouldcarry out an annualboard self-assessment

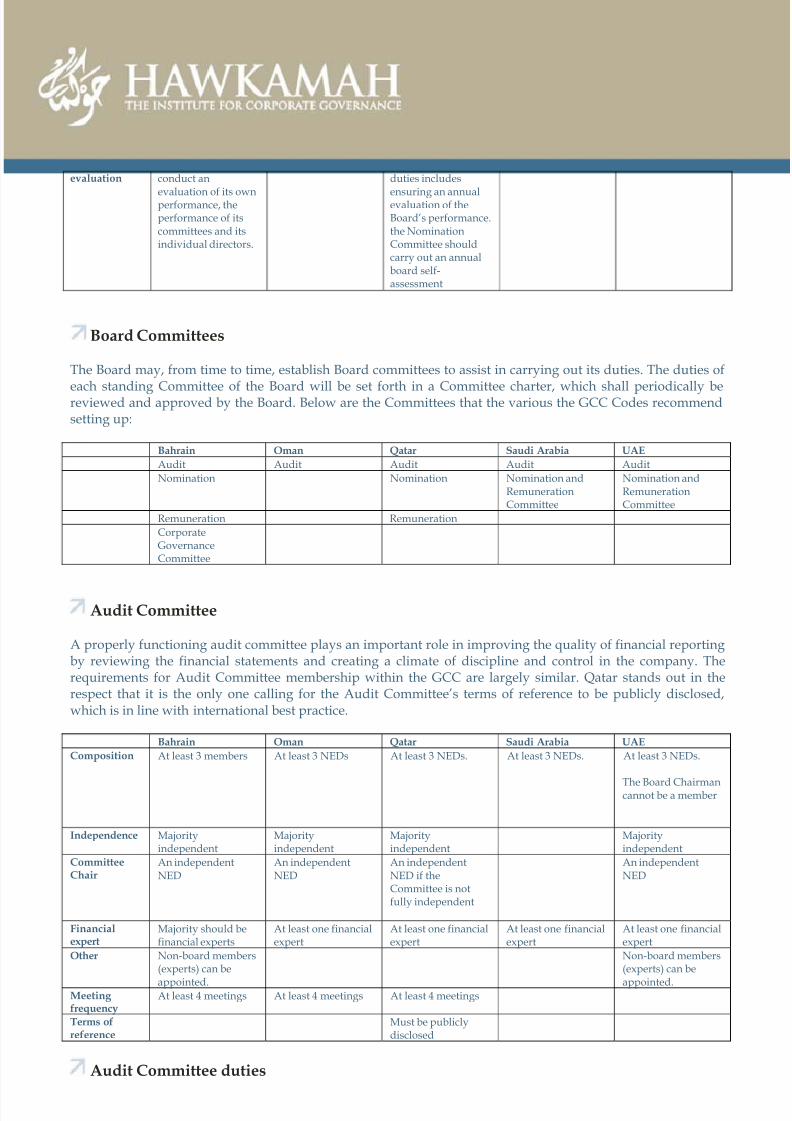

Board Committees

The Board may, from time to time, establish Board committees to assist in carrying out its duties. The duties of

each standing Committee of the Board will be set forth in a Committee charter, which shall periodically bereviewed and approved by the Board. Below are the Committees that the various the GCC Codes recommendsetting up:

Bahrain Oman Qatar Saudi Arabia UAE

Audit Audit Audit Audit Audit

Nomination Nomination Nomination andRemunerationCommittee

Nomination andRemunerationCommittee

Remuneration Remuneration

CorporateGovernanceCommittee

Audit Committee

A properly functioning audit committee plays an important role in improving the quality of financial reportingby reviewing the financial statements and creating a climate of discipline and control in the company. Therequirements for Audit Committee membership within the GCC are largely similar. Qatar stands out in therespect that it is the only one calling for the Audit Committee’s terms of reference to be publicly disclosed,which is in line with international best practice.

Bahrain Oman Qatar Saudi Arabia UAE

Composition At least 3 members At least 3 NEDs At least 3 NEDs. At least 3 NEDs. At least 3 NEDs.

The Board Chairmancannot be a member

Independence Majorityindependent

Majorityindependent

Majorityindependent

Majorityindependent

CommitteeChair

An independentNED

An independentNED

An independentNED if theCommittee is notfully independent

An independentNED

Financialexpert

Majority should befinancial experts

At least one financialexpert

At least one financialexpert

At least one financialexpert

At least one financialexpert

Other Non-board members(experts) can be

appointed.

Non-board members(experts) can be

appointed.Meeting frequency

At least 4 meetings At least 4 meetings At least 4 meetings

Terms ofreference

Must be publiclydisclosed

Audit Committee duties

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 6/9

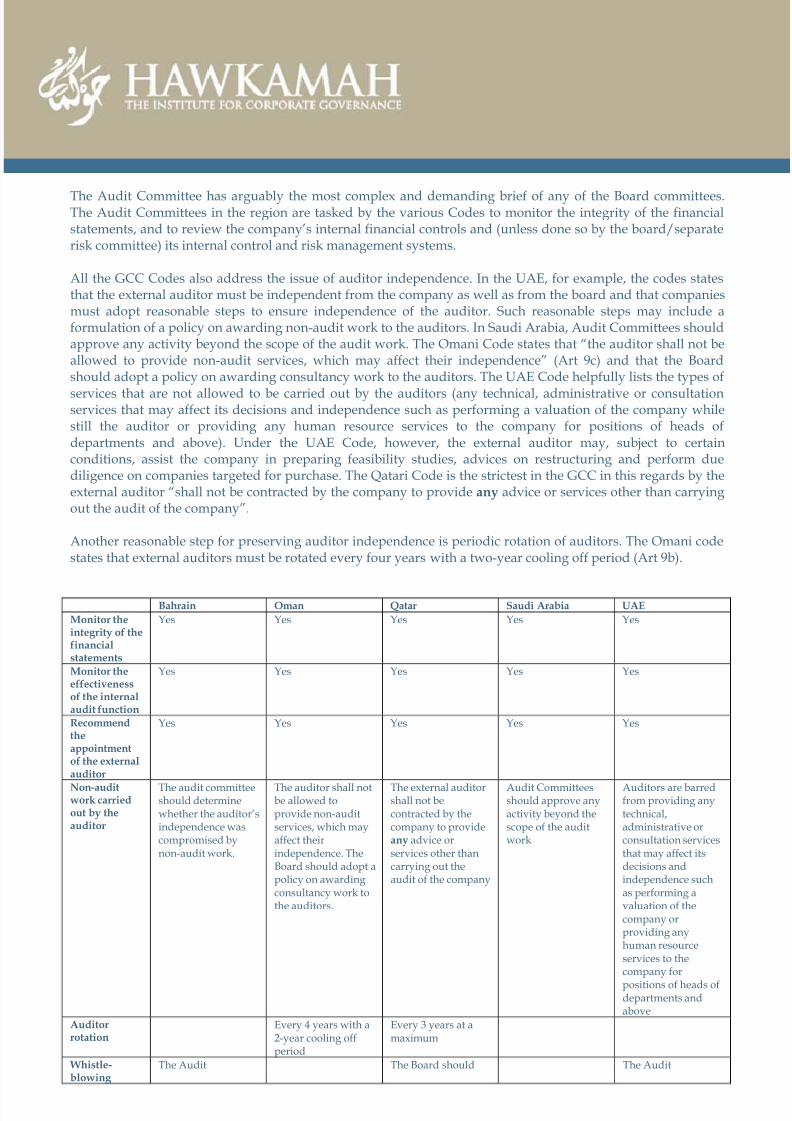

The Audit Committee has arguably the most complex and demanding brief of any of the Board committees.The Audit Committees in the region are tasked by the various Codes to monitor the integrity of the financialstatements, and to review the company’s internal financial controls and (unless done so by the board/separaterisk committee) its internal control and risk management systems.

All the GCC Codes also address the issue of auditor independence. In the UAE, for example, the codes statesthat the external auditor must be independent from the company as well as from the board and that companiesmust adopt reasonable steps to ensure independence of the auditor. Such reasonable steps may include aformulation of a policy on awarding non-audit work to the auditors. In Saudi Arabia, Audit Committees shouldapprove any activity beyond the scope of the audit work. The Omani Code states that “the auditor shall not beallowed to provide non-audit services, which may affect their independence” (Art 9c) and that the Boardshould adopt a policy on awarding consultancy work to the auditors. The UAE Code helpfully lists the types of

services that are not allowed to be carried out by the auditors (any technical, administrative or consultationservices that may affect its decisions and independence such as performing a valuation of the company whilestill the auditor or providing any human resource services to the company for positions of heads ofdepartments and above). Under the UAE Code, however, the external auditor may, subject to certainconditions, assist the company in preparing feasibility studies, advices on restructuring and perform duediligence on companies targeted for purchase. The Qatari Code is the strictest in the GCC in this regards by theexternal auditor “shall not be contracted by the company to provide any advice or services other than carryingout the audit of the company”.

Another reasonable step for preserving auditor independence is periodic rotation of auditors. The Omani codestates that external auditors must be rotated every four years with a two-year cooling off period (Art 9b).

Bahrain Oman Qatar Saudi Arabia UAE

Monitor theintegrity of thefinancialstatements

Yes Yes Yes Yes Yes

Monitor theeffectivenessof the internalaudit function

Yes Yes Yes Yes Yes

Recommendtheappointmentof the external auditor

Yes Yes Yes Yes Yes

Non-auditwork carriedout by theauditor

The audit committeeshould determinewhether the auditor’sindependence wascompromised bynon-audit work.

The auditor shall notbe allowed toprovide non-auditservices, which mayaffect theirindependence. TheBoard should adopt apolicy on awardingconsultancy work tothe auditors.

The external auditorshall not becontracted by thecompany to provideany advice orservices other thancarrying out theaudit of the company

Audit Committeesshould approve anyactivity beyond thescope of the auditwork

Auditors are barredfrom providing anytechnical,administrative orconsultation servicesthat may affect itsdecisions andindependence suchas performing avaluation of thecompany orproviding anyhuman resourceservices to thecompany for

positions of heads ofdepartments andabove

Auditorrotation

Every 4 years with a2-year cooling offperiod

Every 3 years at amaximum

Whistle-blowing

The Audit The Board should The Audit

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 7/9

Committee should

review whistle-blowingarrangements andensure thatindependent follow-up.

adopt a whistle-

blowing mechanism.The Board shouldensureconfidentiality andnon-retaliation

Committee should

develop a whistle-blowing mechanism

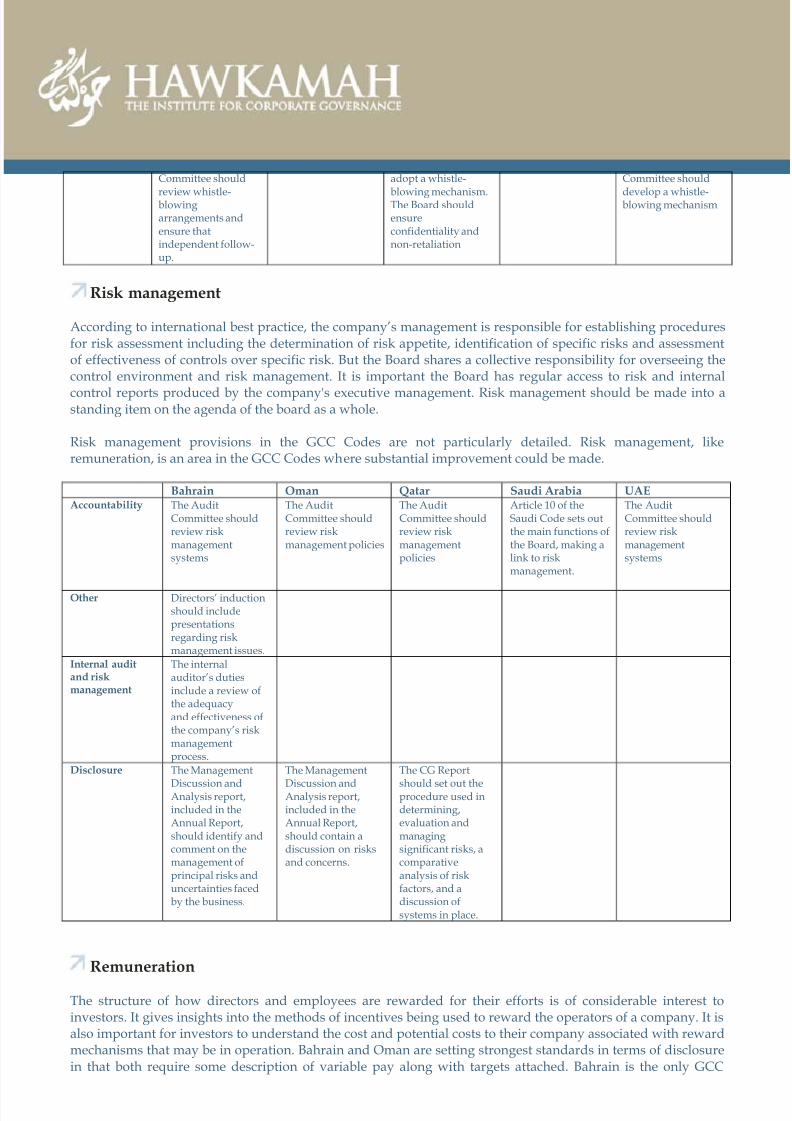

Risk management

According to international best practice, the company’s management is responsible for establishing proceduresfor risk assessment including the determination of risk appetite, identification of specific risks and assessmentof effectiveness of controls over specific risk. But the Board shares a collective responsibility for overseeing thecontrol environment and risk management. It is important the Board has regular access to risk and internal

control reports produced by the company's executive management. Risk management should be made into astanding item on the agenda of the board as a whole.

Risk management provisions in the GCC Codes are not particularly detailed. Risk management, likeremuneration, is an area in the GCC Codes where substantial improvement could be made.

Bahrain Oman Qatar Saudi Arabia UAEAccountability The Audit

Committee shouldreview riskmanagementsystems

The AuditCommittee shouldreview riskmanagement policies

The AuditCommittee shouldreview riskmanagementpolicies

Article 10 of theSaudi Code sets outthe main functions ofthe Board, making alink to riskmanagement.

The AuditCommittee shouldreview riskmanagementsystems

Other Directors’ inductionshould includepresentationsregarding riskmanagement issues.

Internal auditand riskmanagement

The internalauditor’s dutiesinclude a review ofthe adequacyand effectiveness ofthe company’s riskmanagementprocess.

Disclosure The Management

Discussion andAnalysis report,included in theAnnual Report,should identify andcomment on themanagement ofprincipal risks anduncertainties facedby the business.

The Management

Discussion andAnalysis report,included in theAnnual Report,should contain adiscussion on risksand concerns.

The CG Report

should set out theprocedure used indetermining,evaluation andmanagingsignificant risks, acomparativeanalysis of riskfactors, and adiscussion ofsystems in place.

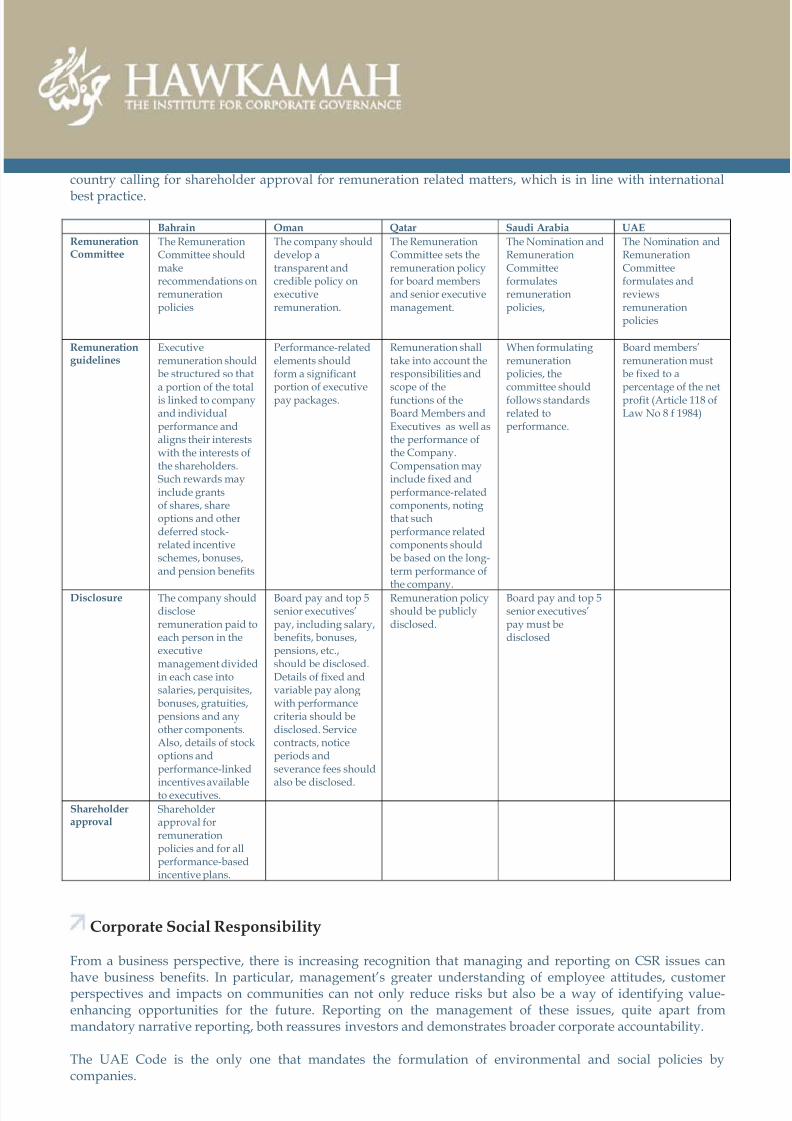

Remuneration

The structure of how directors and employees are rewarded for their efforts is of considerable interest toinvestors. It gives insights into the methods of incentives being used to reward the operators of a company. It isalso important for investors to understand the cost and potential costs to their company associated with rewardmechanisms that may be in operation. Bahrain and Oman are setting strongest standards in terms of disclosurein that both require some description of variable pay along with targets attached. Bahrain is the only GCC

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 8/9

country calling for shareholder approval for remuneration related matters, which is in line with international

best practice.

Bahrain Oman Qatar Saudi Arabia UAE

RemunerationCommittee

The RemunerationCommittee shouldmakerecommendations onremunerationpolicies

The company shoulddevelop atransparent andcredible policy onexecutiveremuneration.

The RemunerationCommittee sets theremuneration policyfor board membersand senior executivemanagement.

The Nomination andRemunerationCommitteeformulatesremunerationpolicies,

The Nomination andRemunerationCommitteeformulates andreviewsremunerationpolicies

Remunerationguidelines

Executiveremuneration shouldbe structured so that

a portion of the totalis linked to companyand individualperformance andaligns their interestswith the interests ofthe shareholders.Such rewards mayinclude grantsof shares, shareoptions and otherdeferred stock-related incentiveschemes, bonuses,and pension benefits

Performance-relatedelements shouldform a significant

portion of executivepay packages.

Remuneration shalltake into account theresponsibilities and

scope of thefunctions of theBoard Members andExecutives as well asthe performance ofthe Company.Compensation mayinclude fixed andperformance-relatedcomponents, notingthat suchperformance relatedcomponents shouldbe based on the long-term performance of

the company.

When formulatingremunerationpolicies, the

committee shouldfollows standardsrelated toperformance.

Board members’remuneration mustbe fixed to a

percentage of the netprofit (Article 118 ofLaw No 8 f 1984)

Disclosure The company shoulddiscloseremuneration paid toeach person in theexecutivemanagement dividedin each case intosalaries, perquisites,bonuses, gratuities,pensions and anyother components.Also, details of stockoptions andperformance-linked

incentives availableto executives.

Board pay and top 5senior executives’pay, including salary,benefits, bonuses,pensions, etc.,should be disclosed.Details of fixed andvariable pay alongwith performancecriteria should bedisclosed. Servicecontracts, noticeperiods andseverance fees should

also be disclosed.

Remuneration policyshould be publiclydisclosed.

Board pay and top 5senior executives’pay must bedisclosed

Shareholderapproval

Shareholderapproval forremunerationpolicies and for allperformance-basedincentive plans.

Corporate Social Responsibility

From a business perspective, there is increasing recognition that managing and reporting on CSR issues can

have business benefits. In particular, management’s greater understanding of employee attitudes, customerperspectives and impacts on communities can not only reduce risks but also be a way of identifying value-enhancing opportunities for the future. Reporting on the management of these issues, quite apart frommandatory narrative reporting, both reassures investors and demonstrates broader corporate accountability.

The UAE Code is the only one that mandates the formulation of environmental and social policies bycompanies.

8/4/2019 Hawkamah Brief on GCC Code

http://slidepdf.com/reader/full/hawkamah-brief-on-gcc-code 9/9

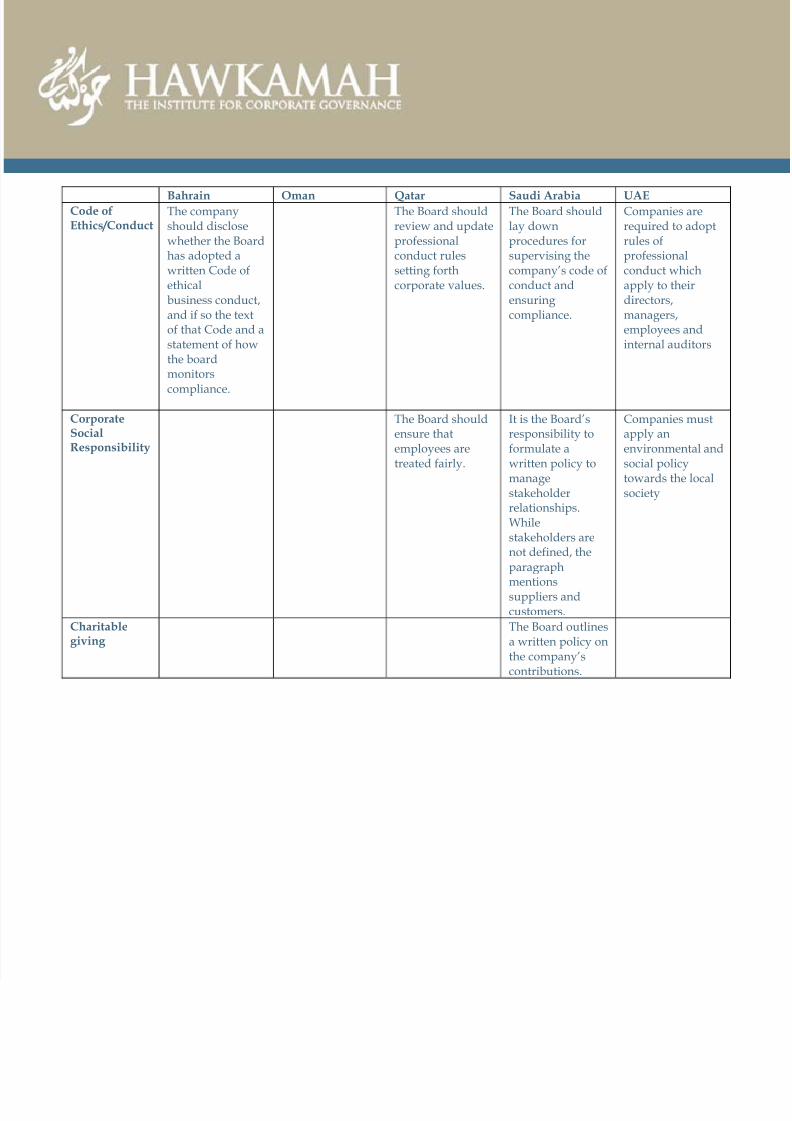

Bahrain Oman Qatar Saudi Arabia UAECode ofEthics/Conduct

The companyshould disclosewhether the Boardhas adopted awritten Code ofethicalbusiness conduct,and if so the textof that Code and astatement of howthe boardmonitors

compliance.

The Board shouldreview and updateprofessionalconduct rulessetting forthcorporate values.

The Board shouldlay downprocedures forsupervising thecompany’s code ofconduct andensuringcompliance.

Companies arerequired to adoptrules ofprofessionalconduct whichapply to theirdirectors,managers,employees andinternal auditors

CorporateSocialResponsibility

The Board shouldensure thatemployees aretreated fairly.

It is the Board’sresponsibility toformulate awritten policy tomanagestakeholderrelationships.Whilestakeholders arenot defined, theparagraphmentionssuppliers andcustomers.

Companies mustapply anenvironmental andsocial policytowards the localsociety

Charitablegiving

The Board outlinesa written policy onthe company’scontributions.