Embed Size (px)

Citation preview

COMPREHENSIVE ANNUAL FINANCIAL REPORT

of the

GUILFORD COUNTY BOARD OF EDUCATION

Greensboro, North Carolina

For the Fiscal Year Ended June 30, 2010

Prepared by:

Sharon Ozment, Chief Financial Officer

Angela Henry, Assistant Financial Officer

THIS PAGE LEFT INTENTIONALLY BLANK.

Guilford County Board of Education

TABLE OF CONTENTS INTRODUCTORY SECTION Page No. Letter of Transmittal .................................................................................. i Guilford County School System - Board Members and Principal

Officials .................................................................................................... xiii Guilford County Schools - Organizational Chart ....................................... xiv Certificates of Excellence .......................................................................... xv-xvi FINANCIAL SECTION Report of Certified Public Accountants Independent Auditors’ Report ................................................................... 1 Management’s Discussion and Analysis ............................................. 3 Exhibit Basic Financial Statements Government-Wide Financial Statements: 1 Statement of Net Assets ........................................................................ 19 2 Statement of Activities ........................................................................... 20 Fund Financial Statements: 3 Balance Sheet - Governmental Funds .................................................. 22 3 Reconciliation of the Balance Sheet to the Statement of Net

Assets ................................................................................................... 22 4 Statement of Revenues, Expenditures and Changes in Fund

Balances - Governmental Funds ......................................................... 23 4 Reconciliation of the Governmental Funds Statement of

Revenues, Expenditures and Changes in Fund Balances to the District-Wide Statement of Activities .............................................. 24

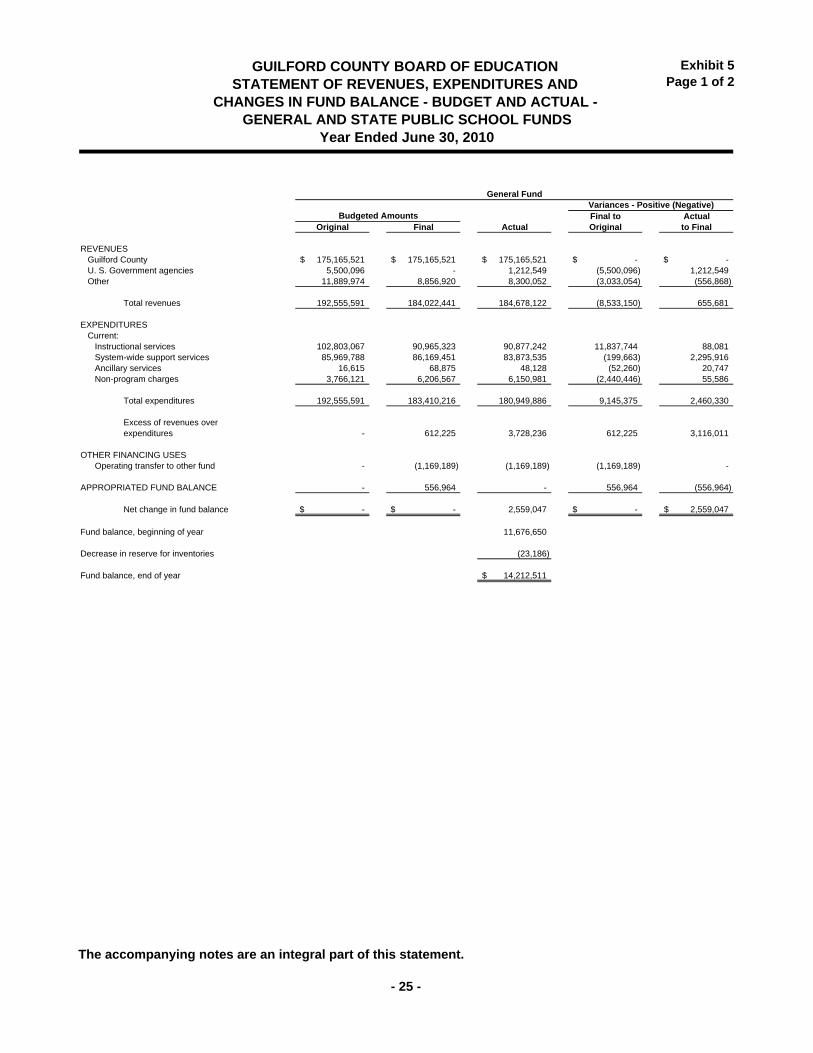

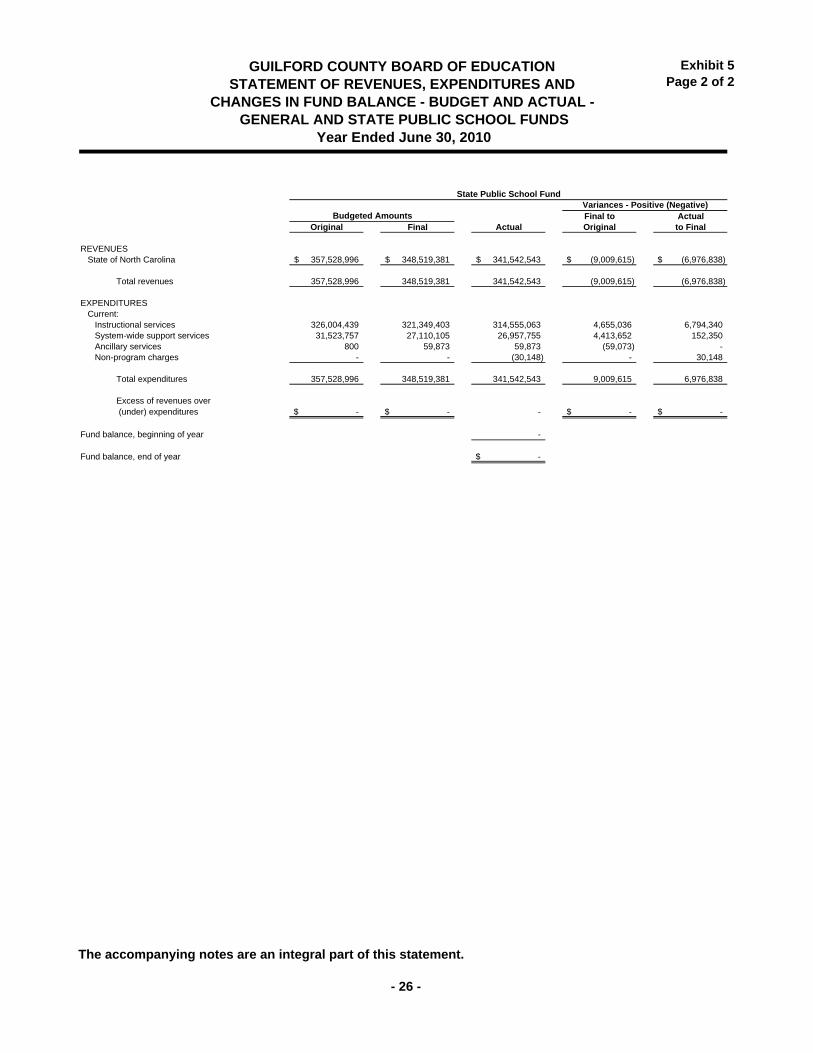

5 Statement of Revenues, Expenditures and Changes in Fund Balance - Budget and Actual - General and State Public School Funds ....................................................................................... 25

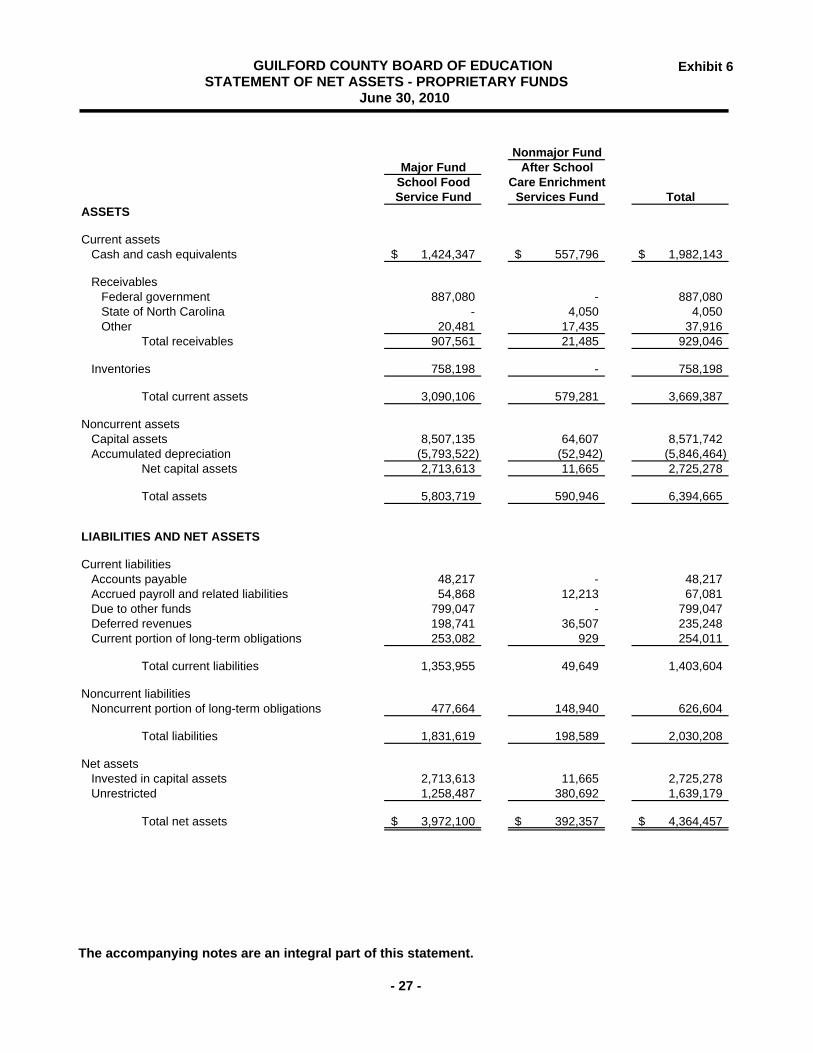

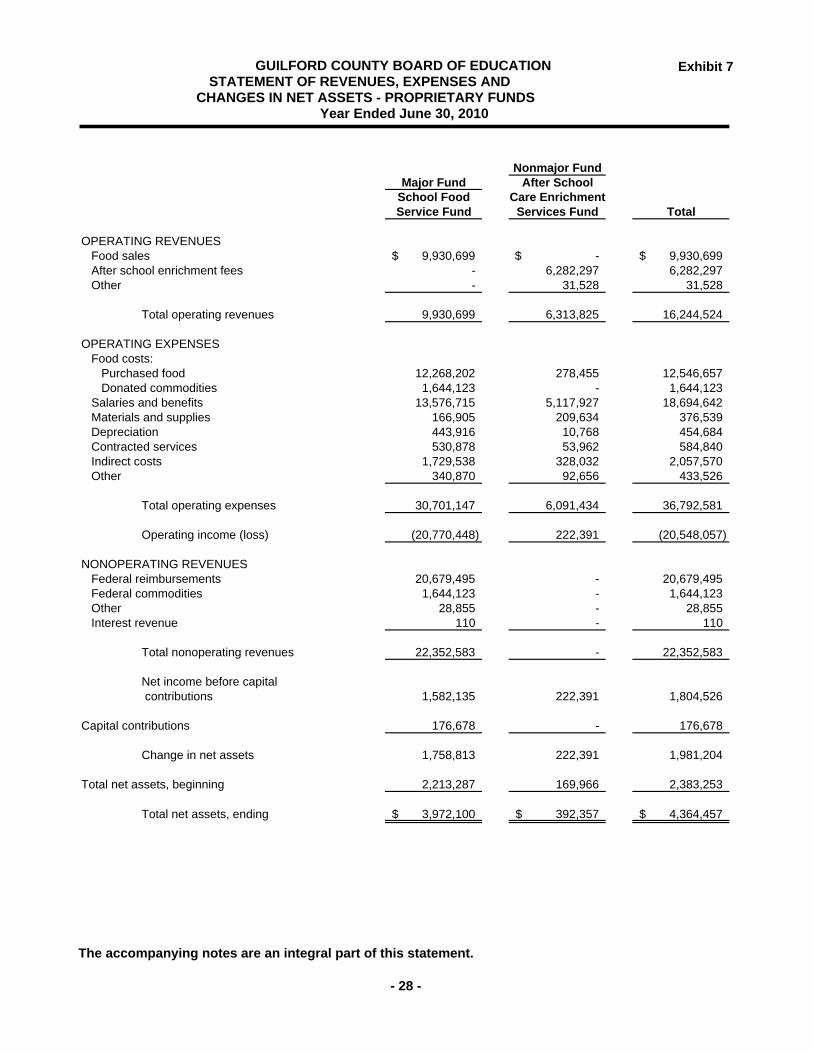

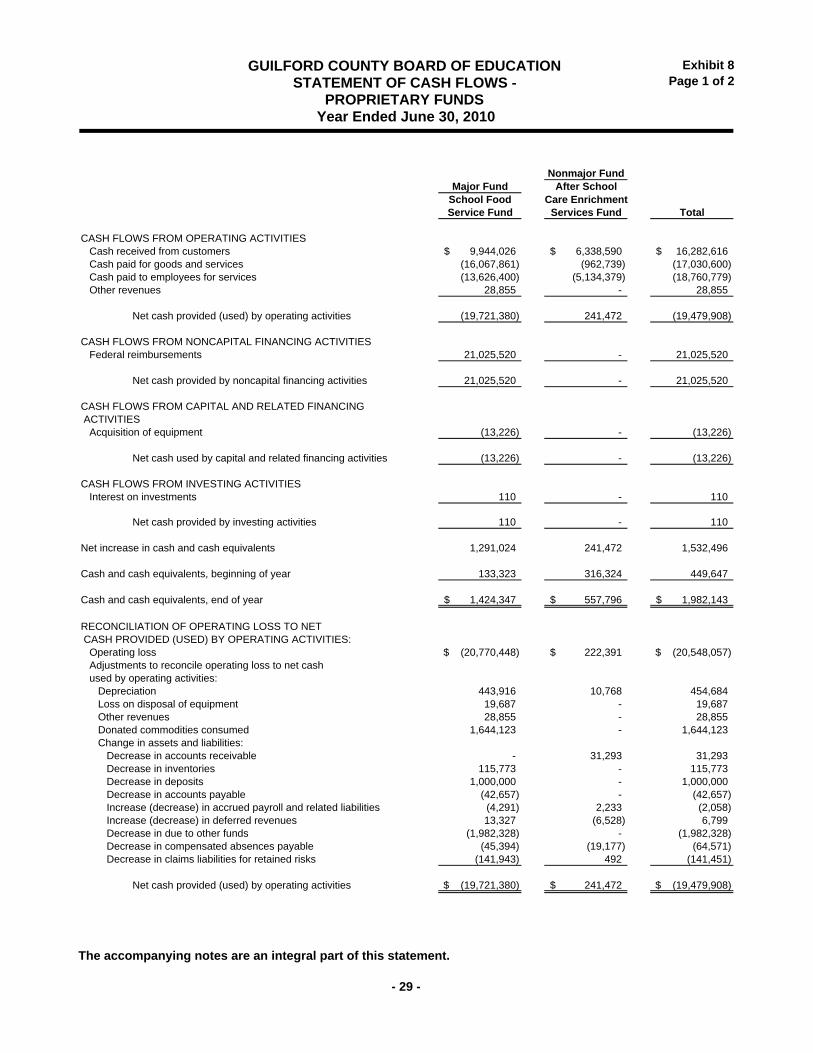

6 Statement of Net Assets - Proprietary Funds ....................................... 27 7 Statement of Revenues, Expenses and Changes in Net

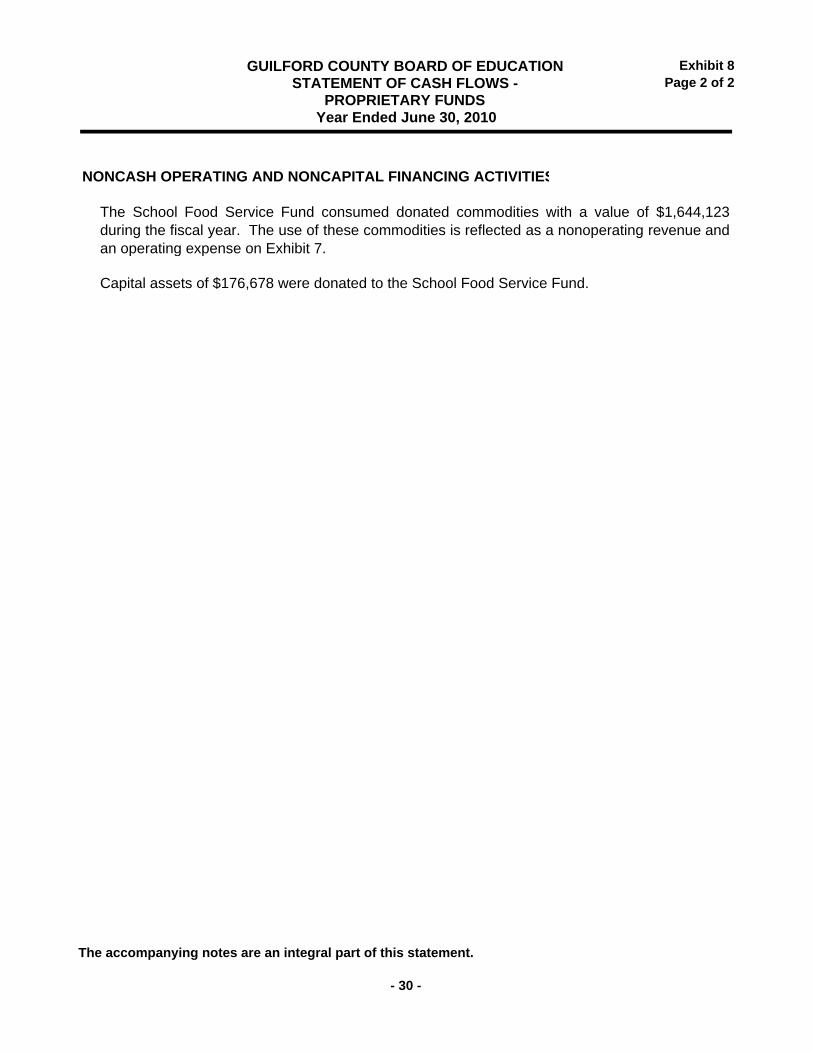

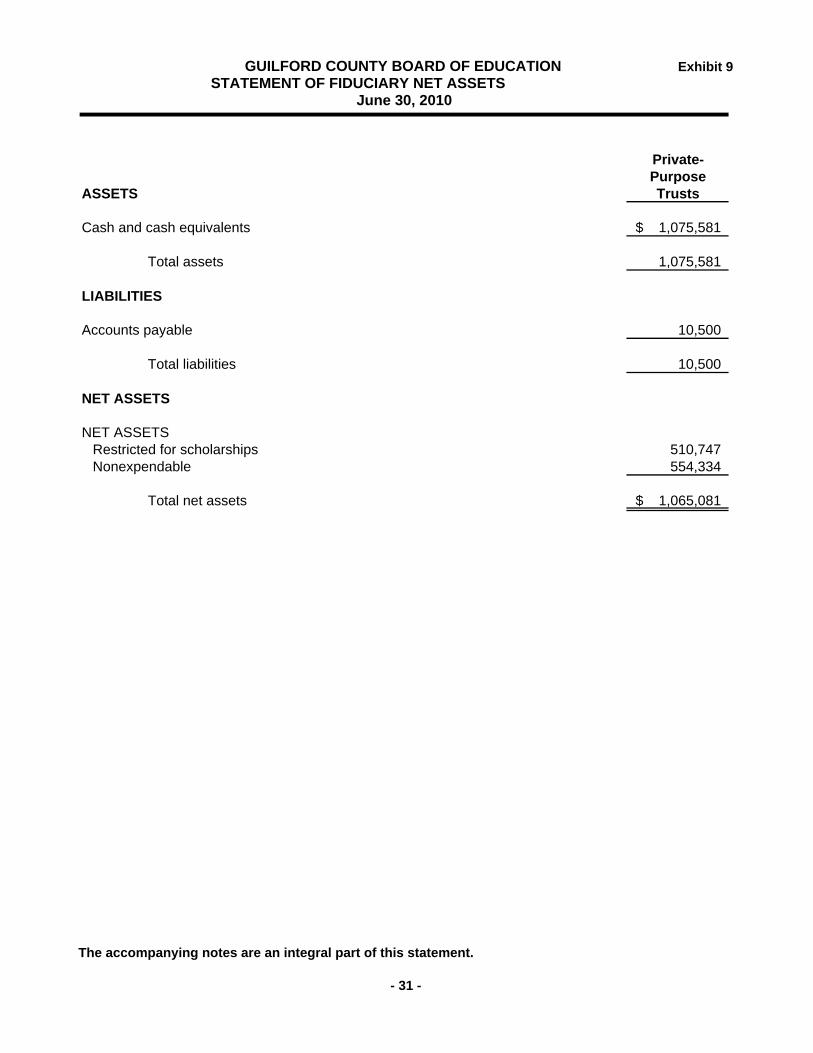

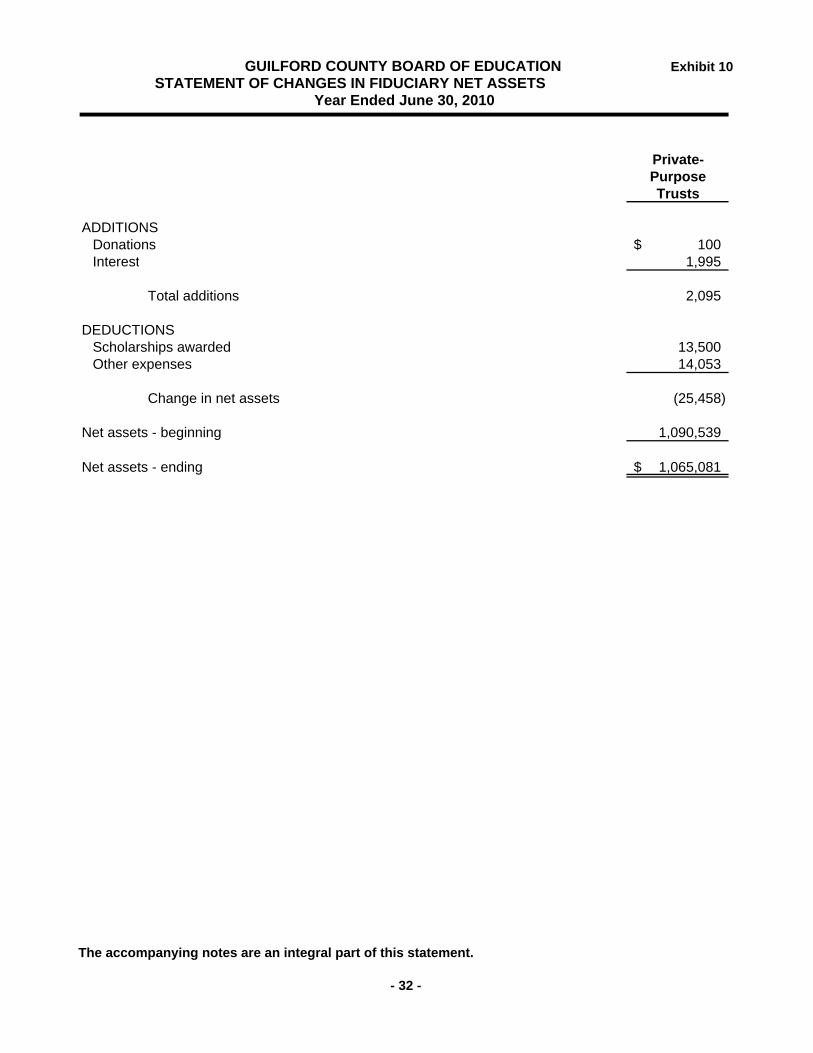

Assets - Proprietary Funds .................................................................. 28 8 Statement of Cash Flows - Proprietary Funds ...................................... 29 9 Statement of Fiduciary Net Assets ........................................................ 31 10 Statement of Changes in Fiduciary Net Assets .................................... 32 Notes to Financial Statements ............................................................... 33

Guilford County Board of Education

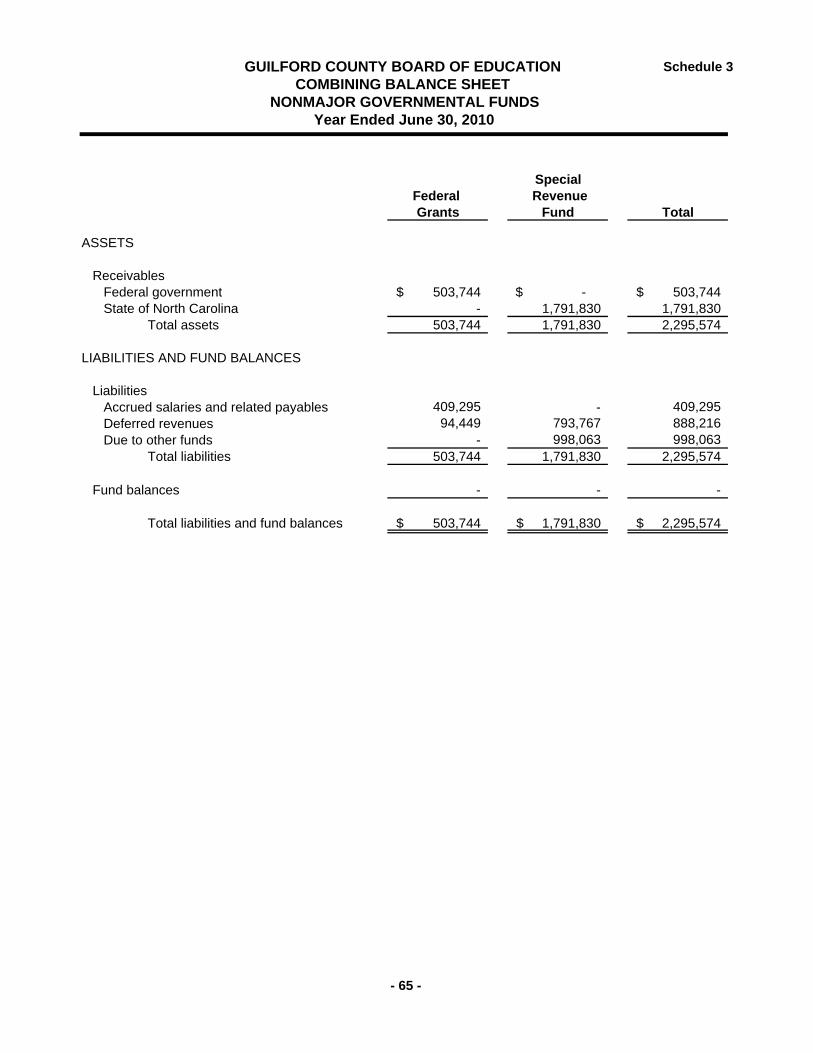

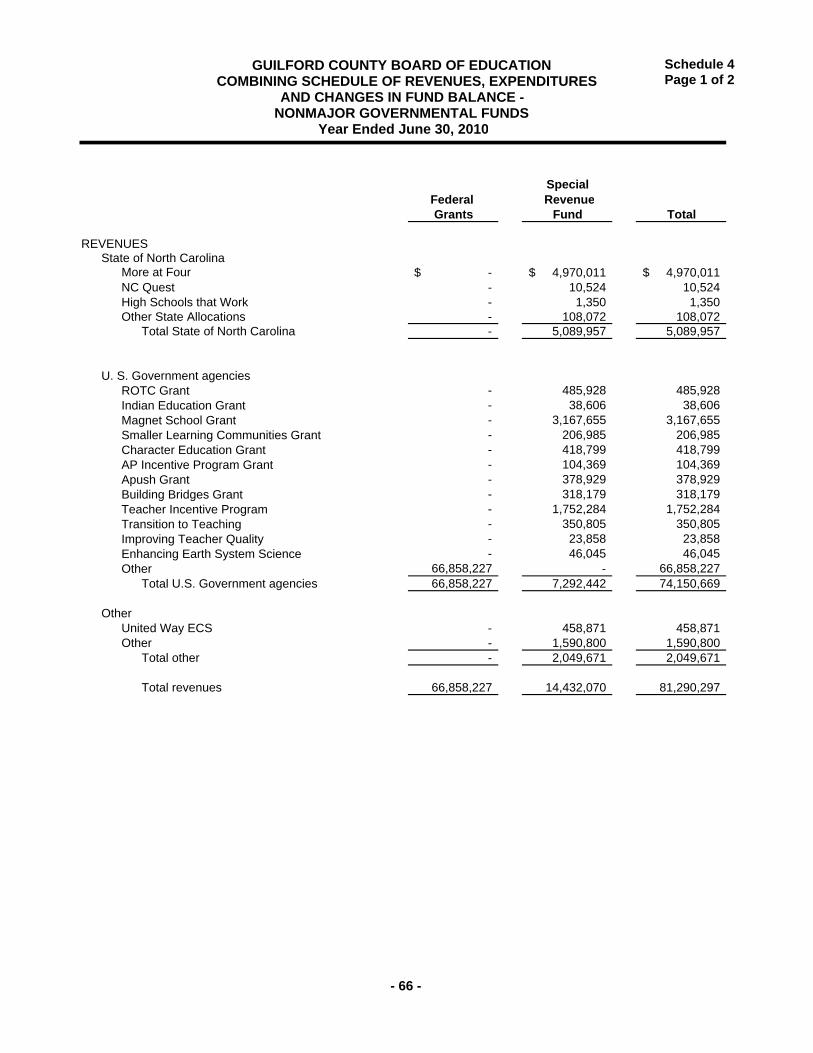

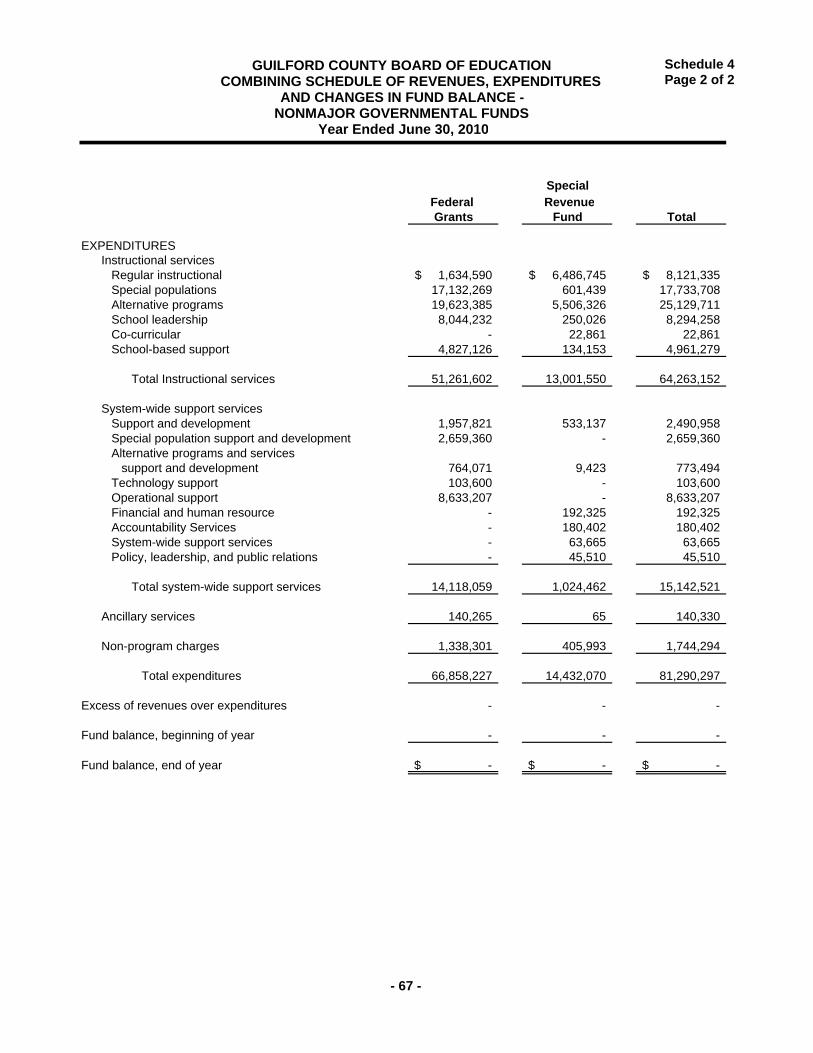

TABLE OF CONTENTS (Continued) Schedule SUPPLEMENTARY INFORMATION Page No. Combining and Individual Fund Statements and Schedules 1 Schedule of Revenues, Expenditures and Changes in Fund

Balance - Budget and Actual - General Fund ......................................... 58 2 Schedule of Revenues, Expenditures and Changes in Fund

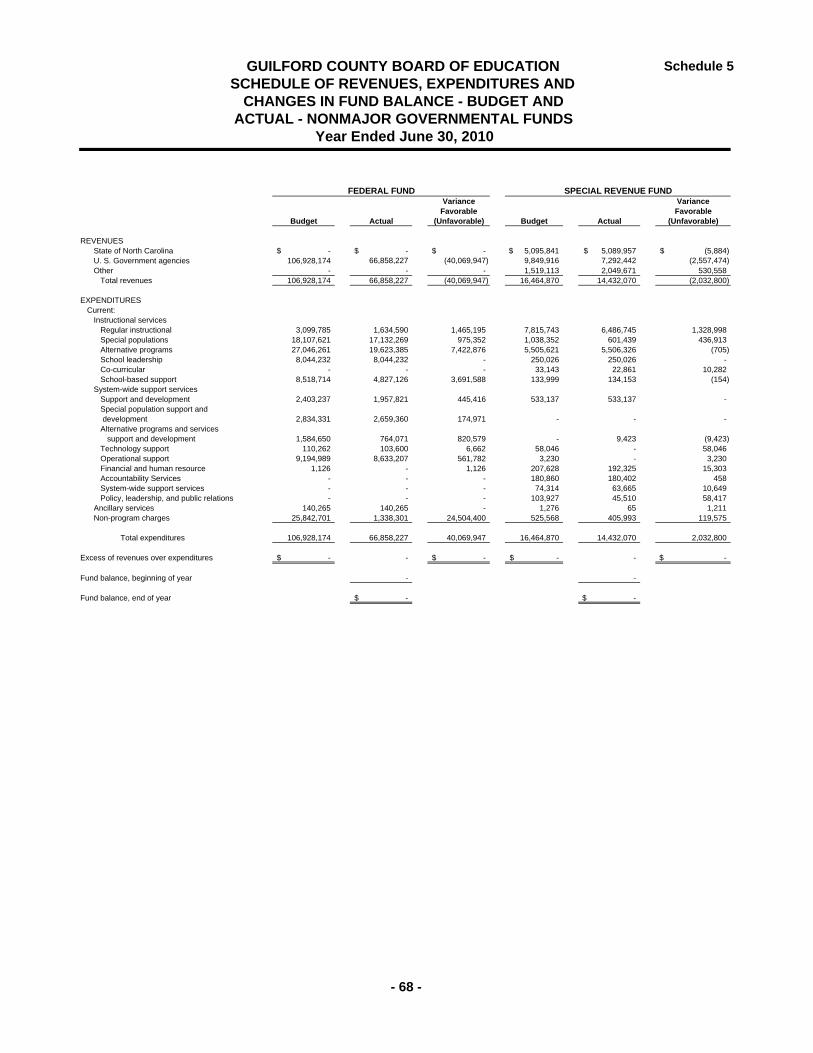

Balance - Budget and Actual - Capital Outlay Fund ............................... 62 3 Combining Balance Sheet - Nonmajor Governmental Funds .................. 65 4 Combining Schedule of Revenue, Expenditures and Changes in Fund Balance - Nonmajor Governmental Funds .................................... 66 5 Schedule of Revenues, Expenditures and Changes in Fund Balance - Budget and Actual - Nonmajor Governmental Funds ............ 68 6 Detailed Schedule of Revenues, Expenditures and Changes in

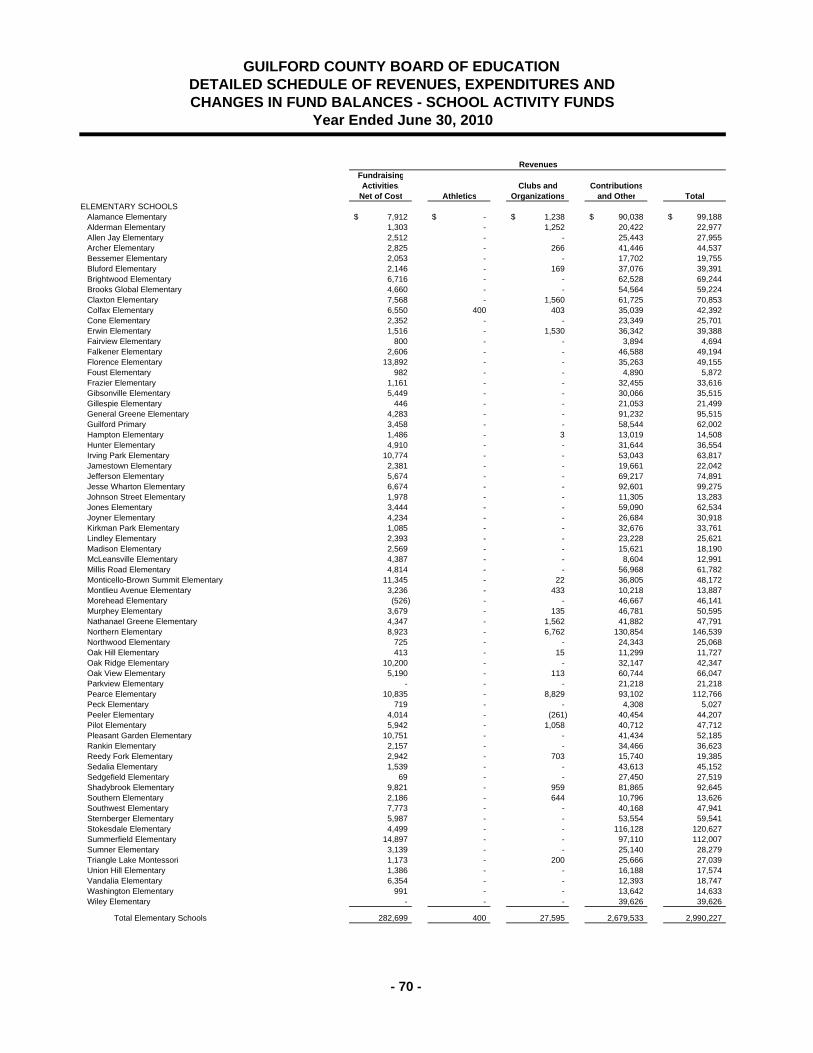

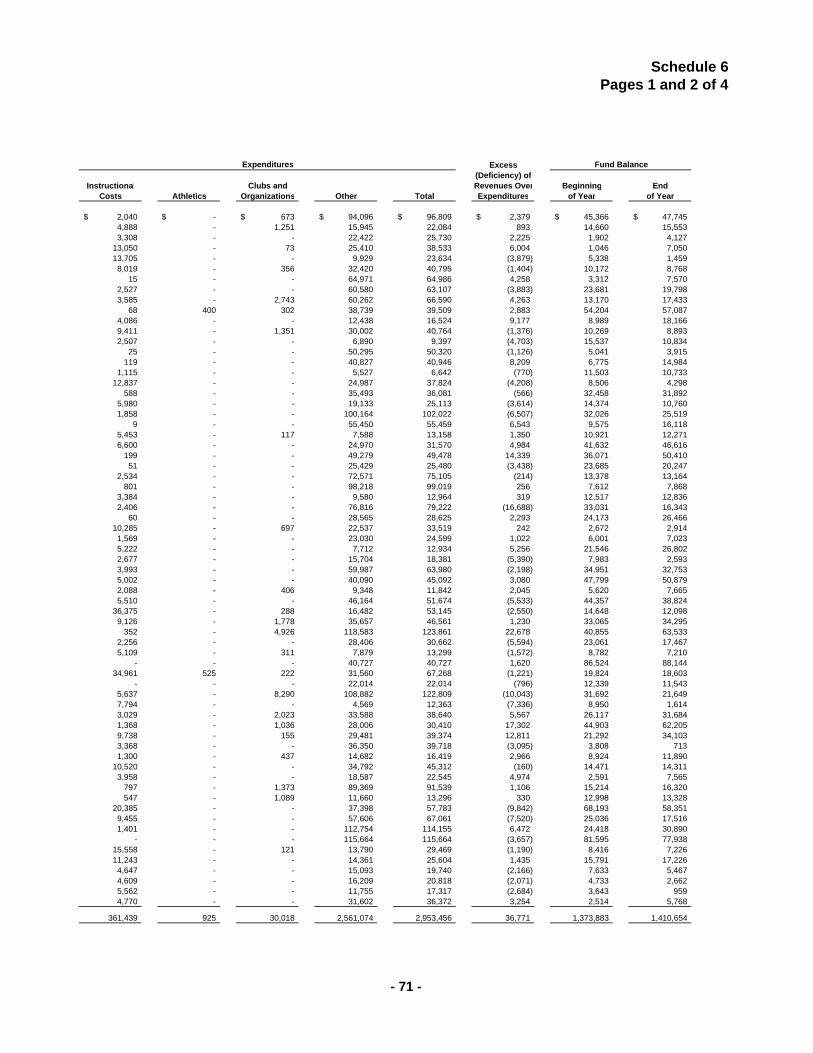

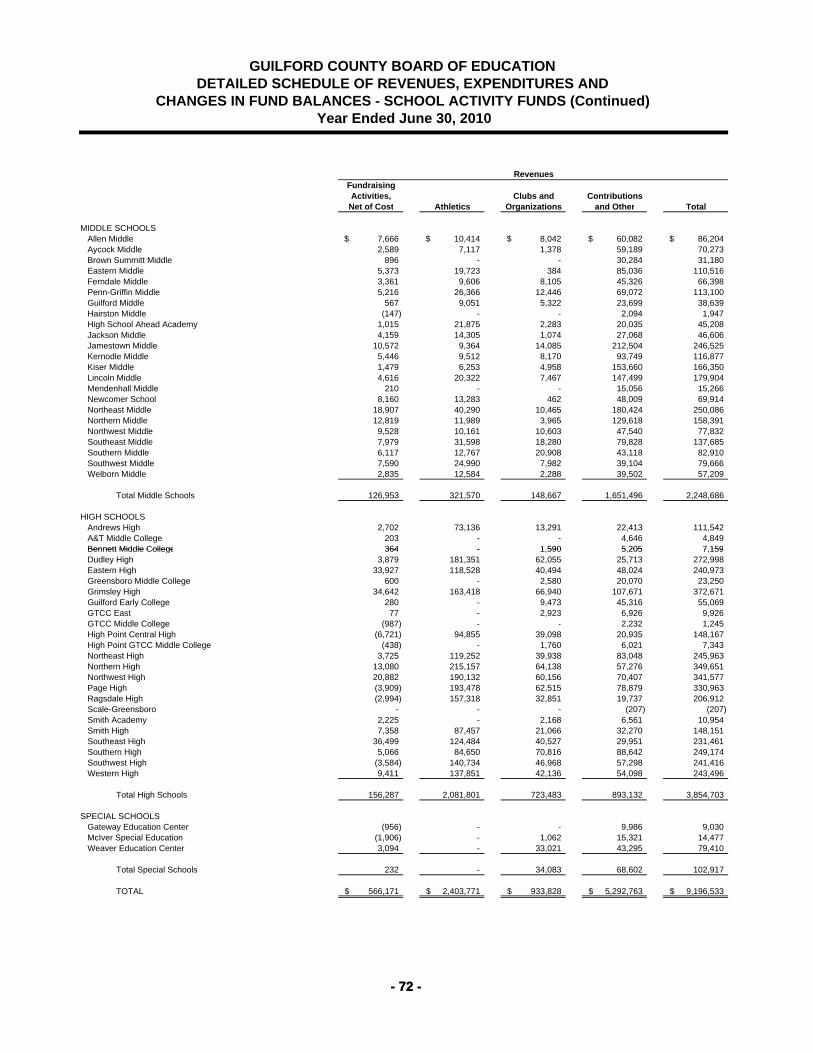

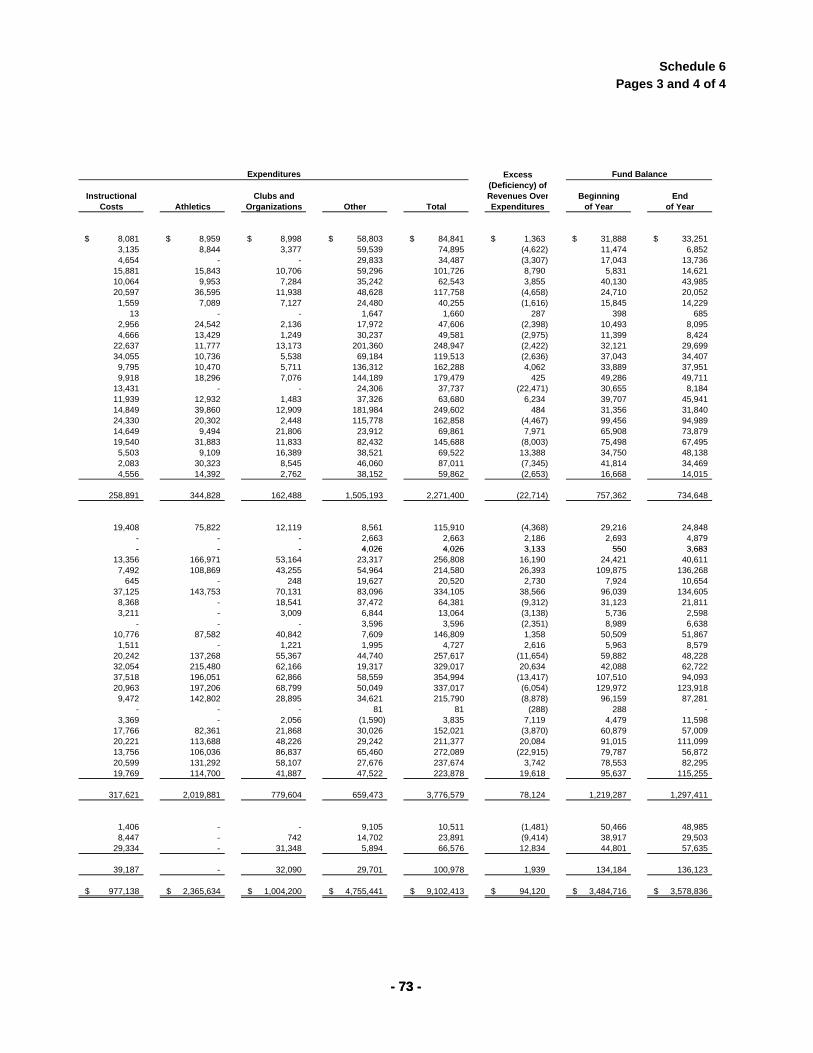

Fund Balances - School Activity Funds ................................................... 70 7 Schedule of Revenues and Expenditures - Budget and Actual

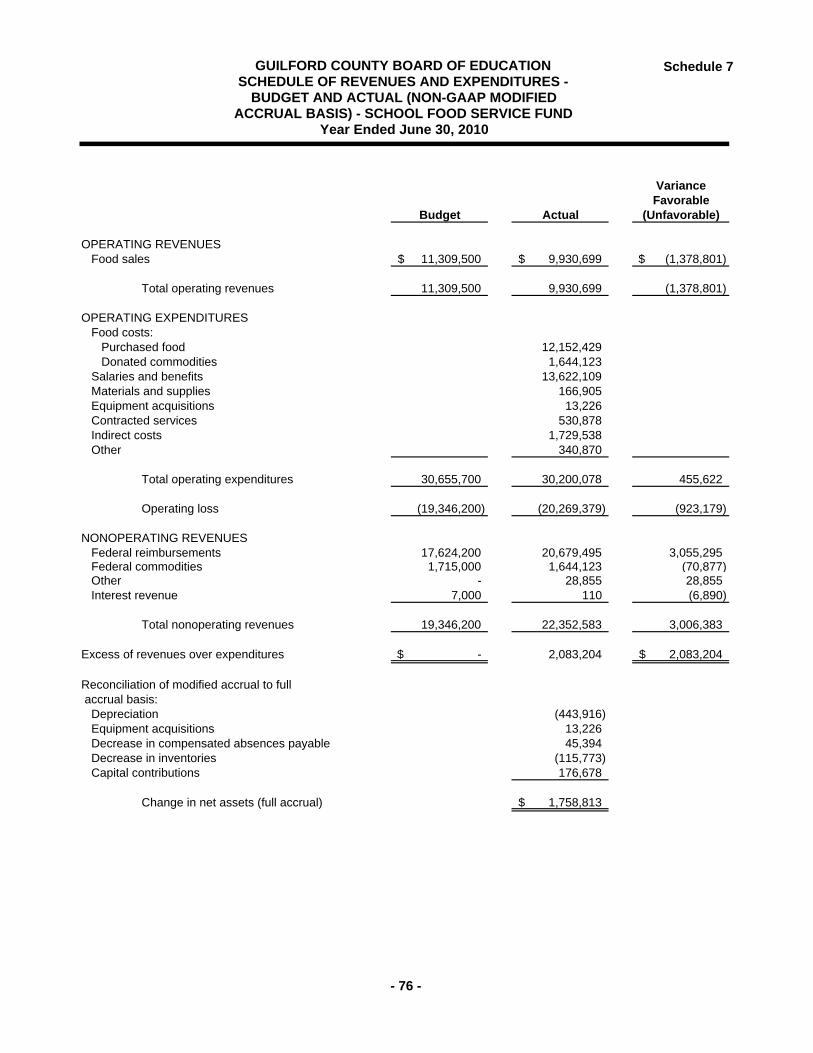

(Non-GAAP Modified Accrual Basis) - School Food Service Fund ......................................................................................................... 76

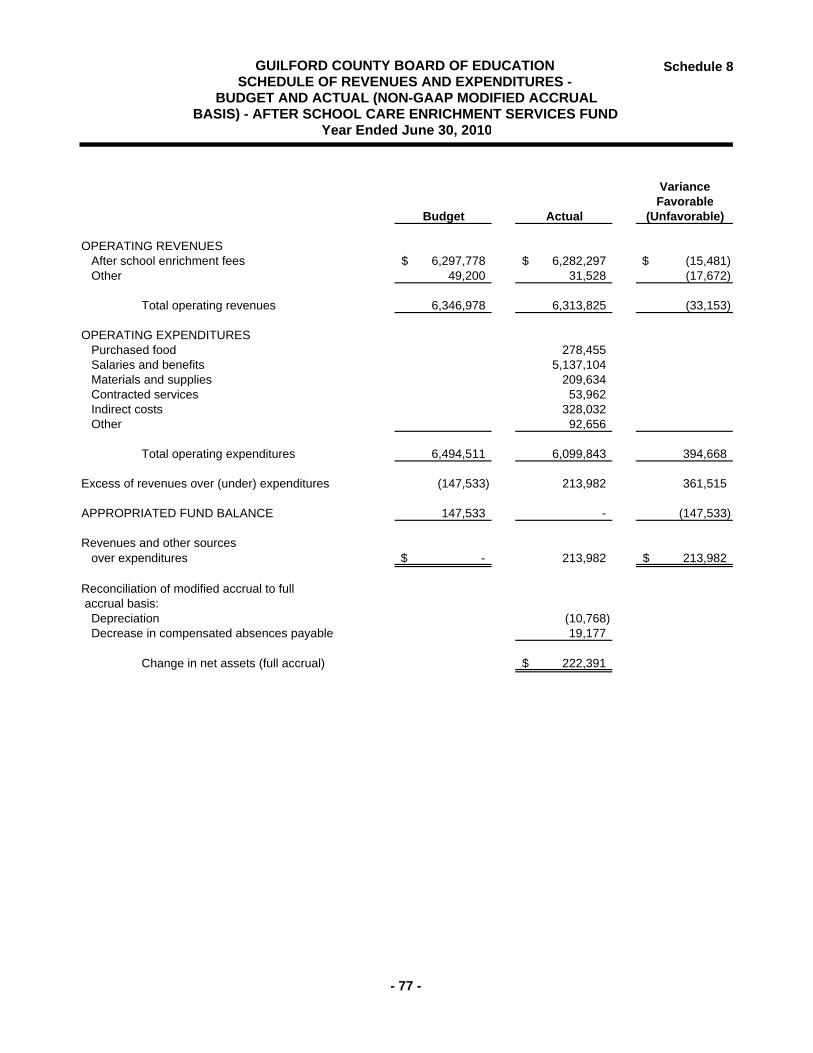

8 Schedule of Revenues and Expenditures - Budget and Actual (Non-GAAP Modified Accrual Basis) - After School Care Enrichment Services Fund ...................................................................... 77

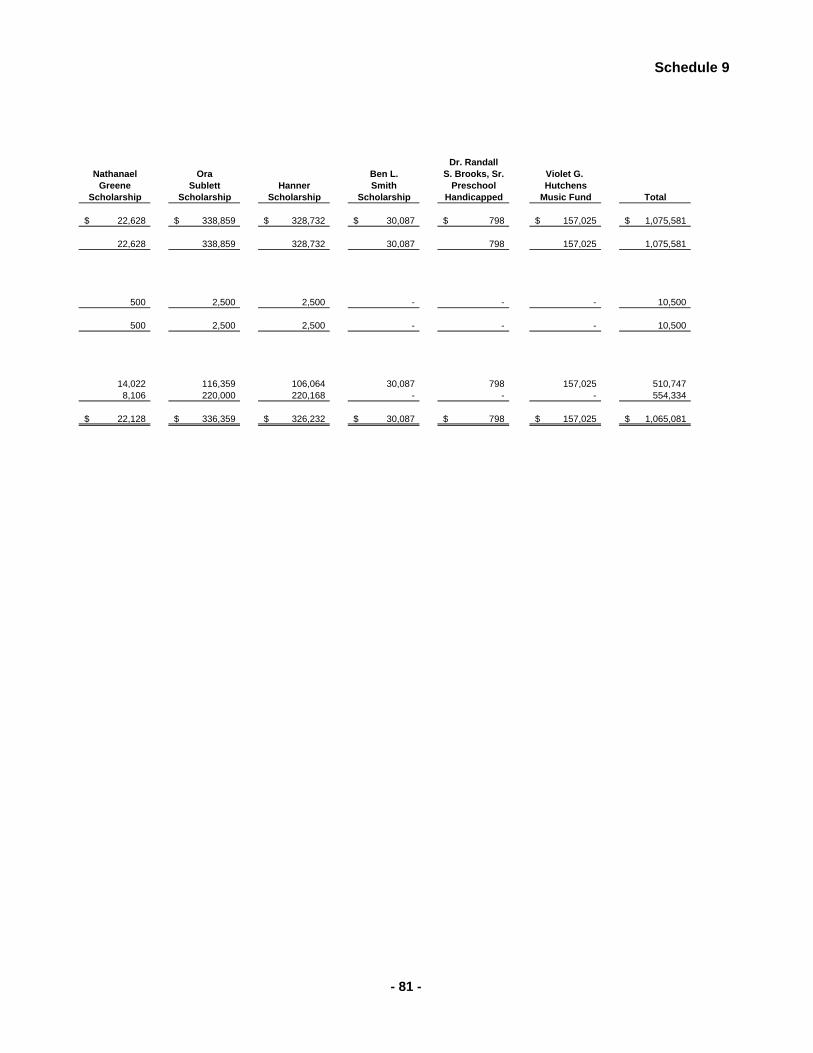

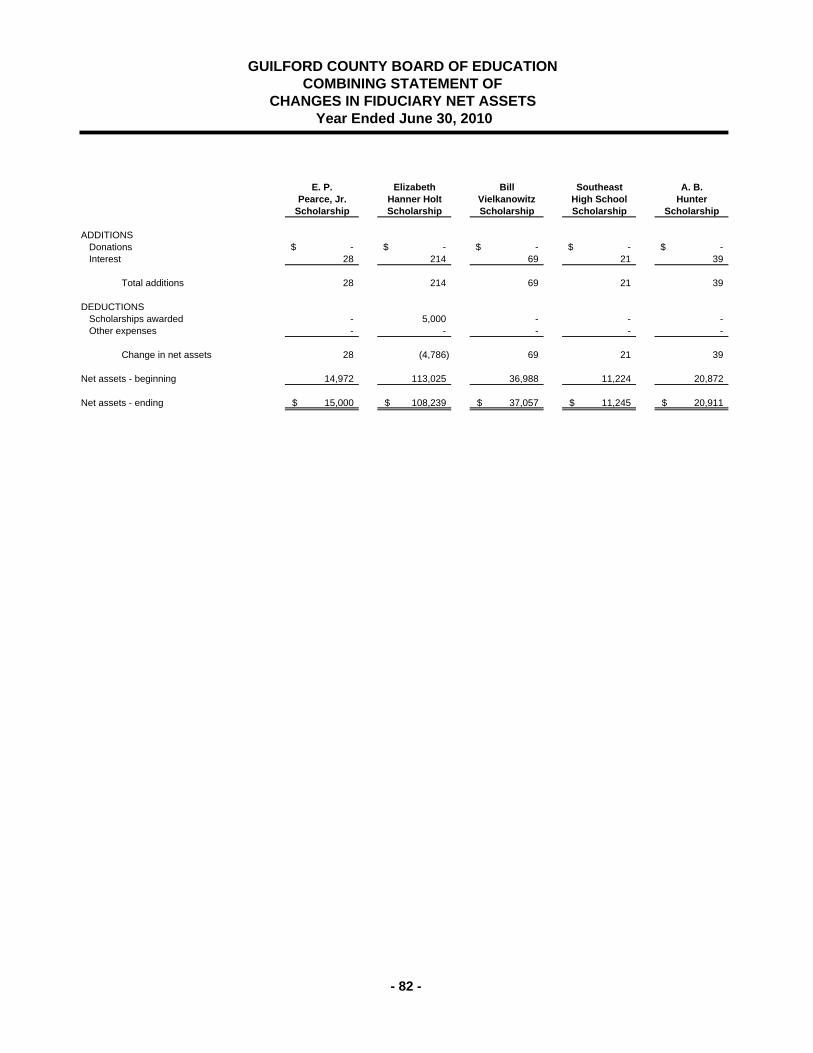

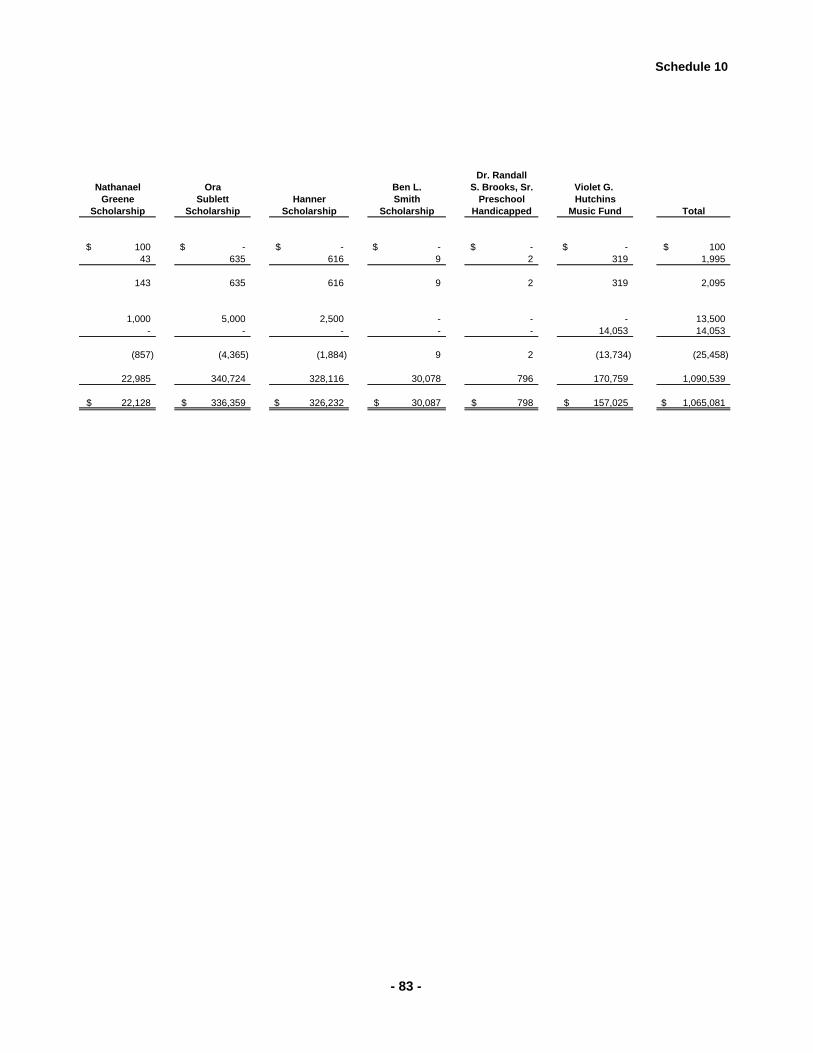

Fiduciary Funds 9 Combining Statement of Fiduciary Net Assets ..................................... 80 10 Combining Statement of Changes in Fiduciary Net Assets .................. 82 Table STATISTICAL SECTION 1 Net Assets by Component - Last Nine Fiscal Years ................................ 87 2 Changes in Net Assets - Last Nine Fiscal Years ...................................... 88 3 Governmental Funds - Fund Balance - Last Ten Fiscal Years ................ 90 4 Governmental Funds - Changes in Fund Balances - Last Ten

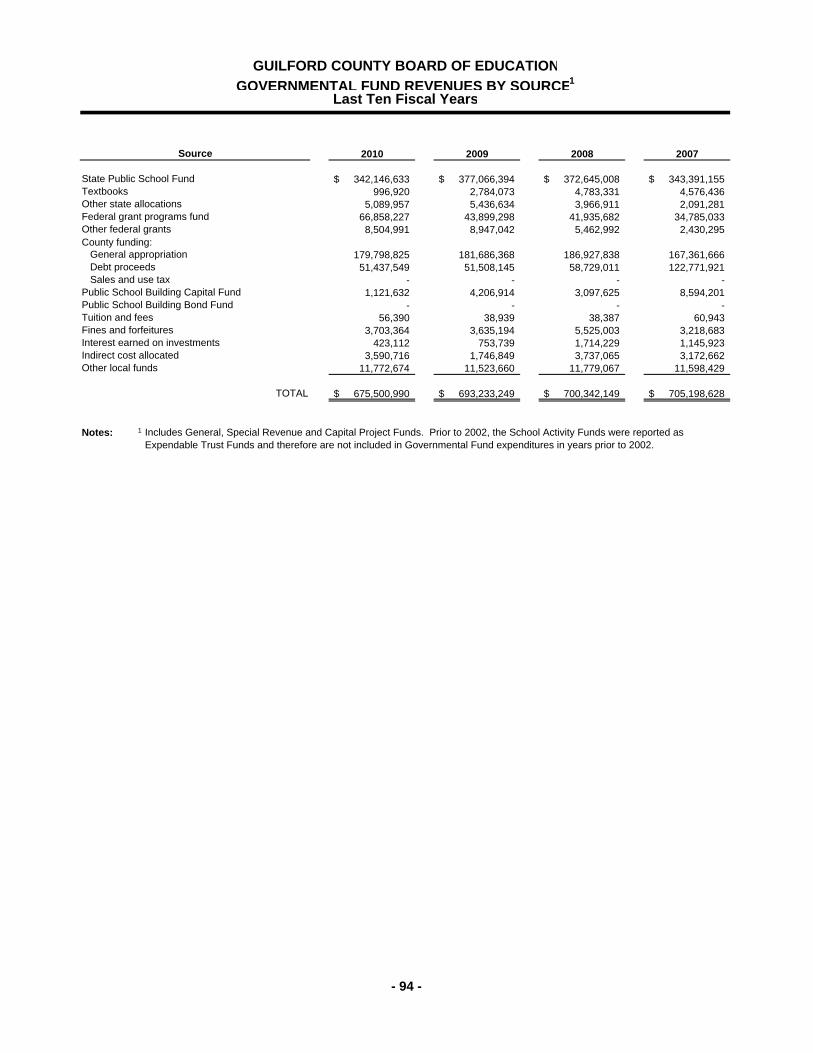

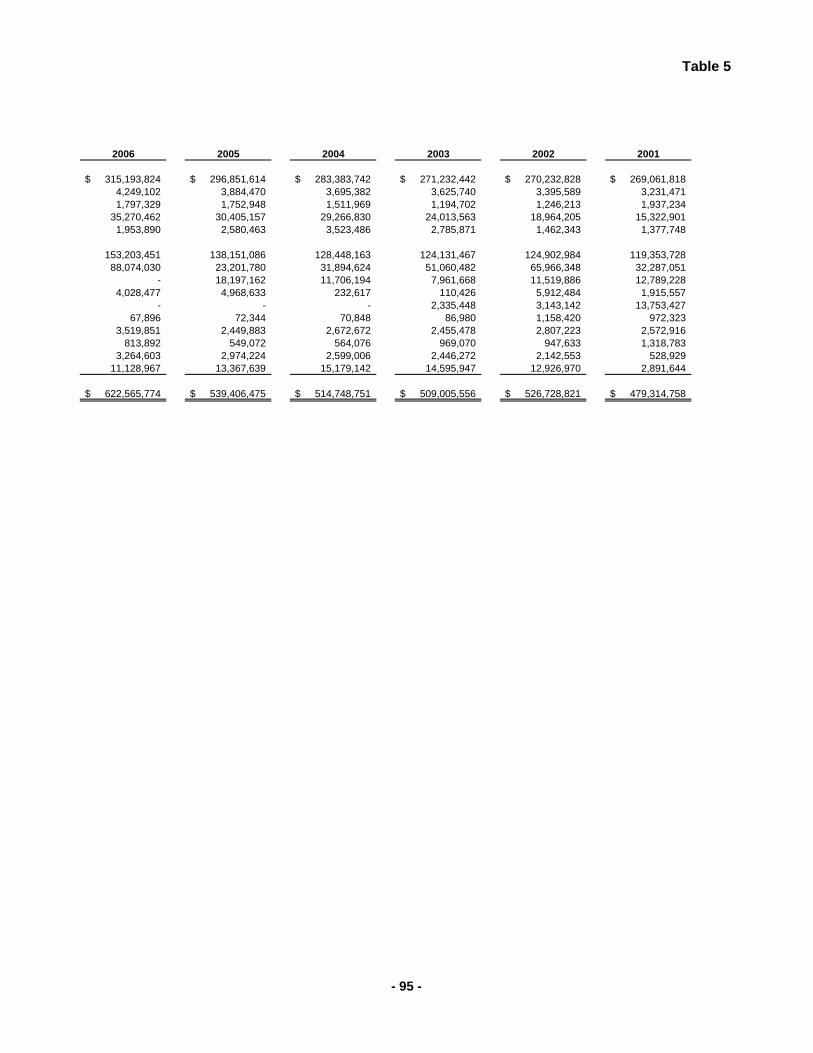

Fiscal Years ............................................................................................. 92 5 Governmental Fund Revenues by Source - Last Ten Fiscal

Years ........................................................................................................ 94 6 Governmental Fund Expenditures by Function - Last Ten Fiscal

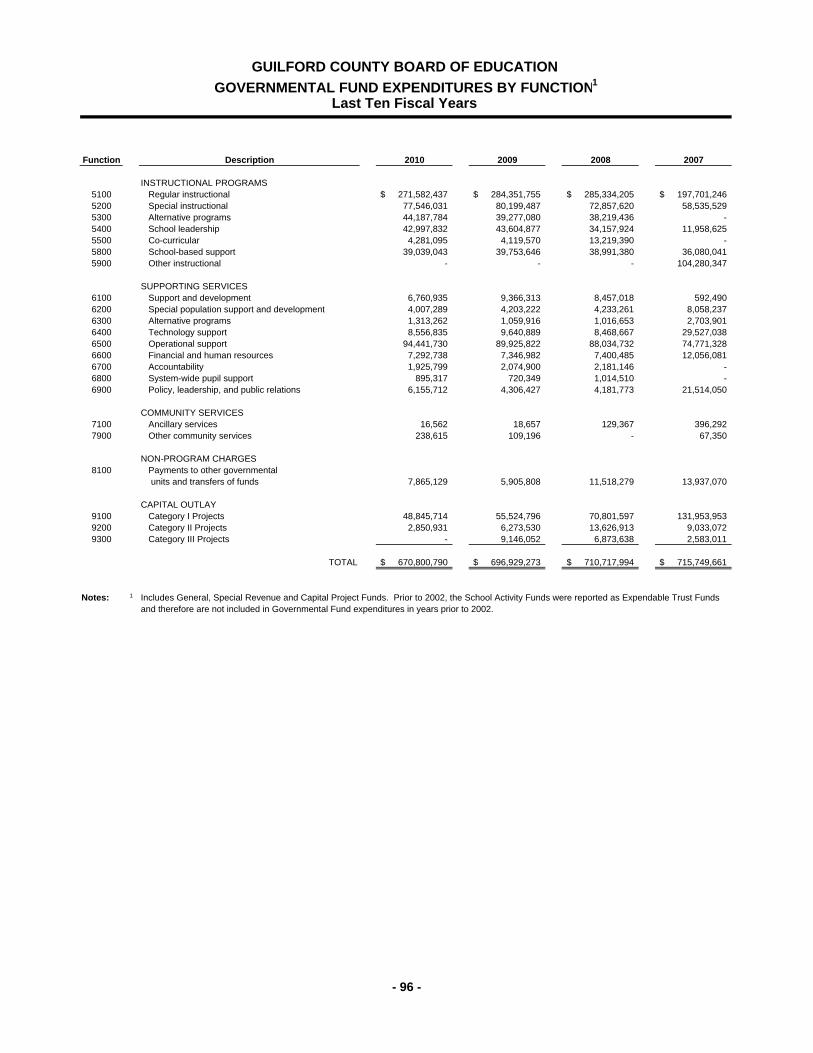

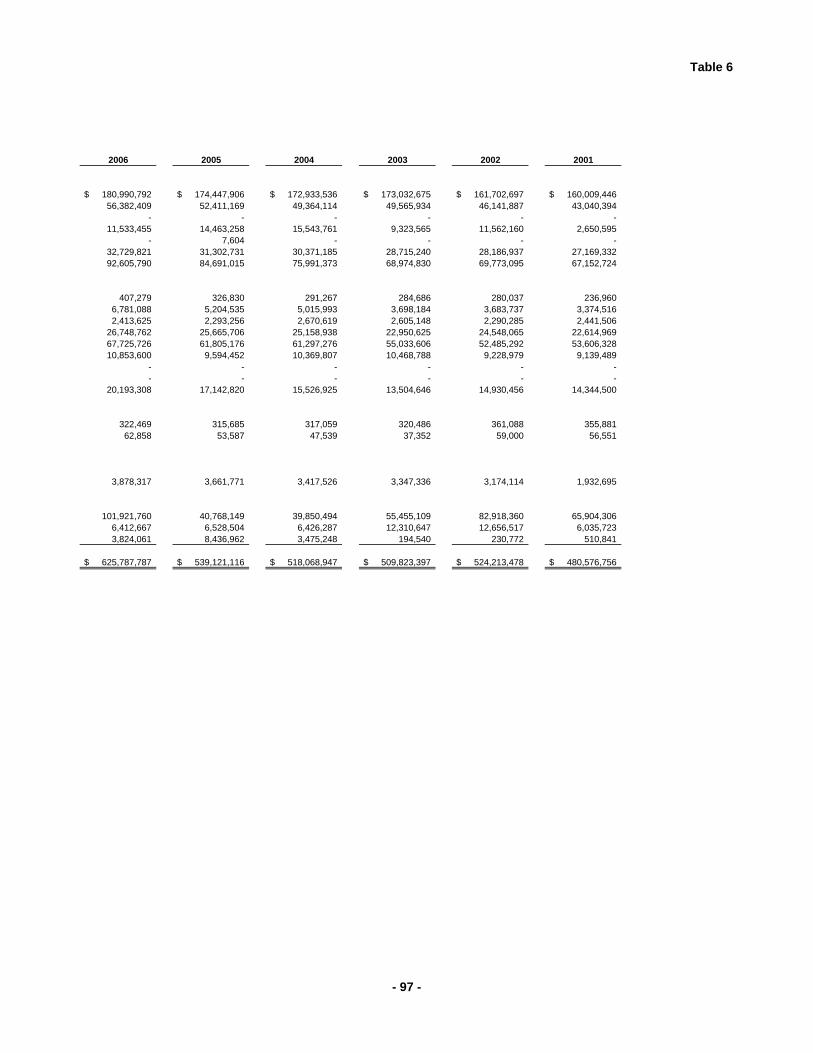

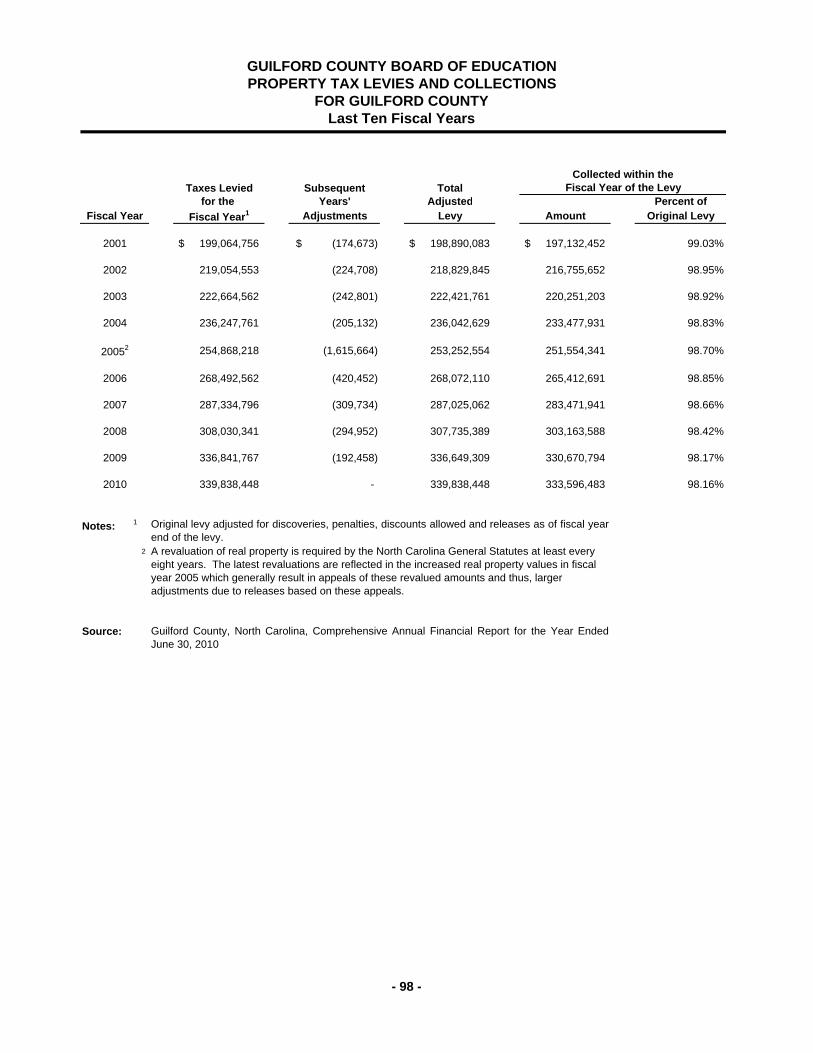

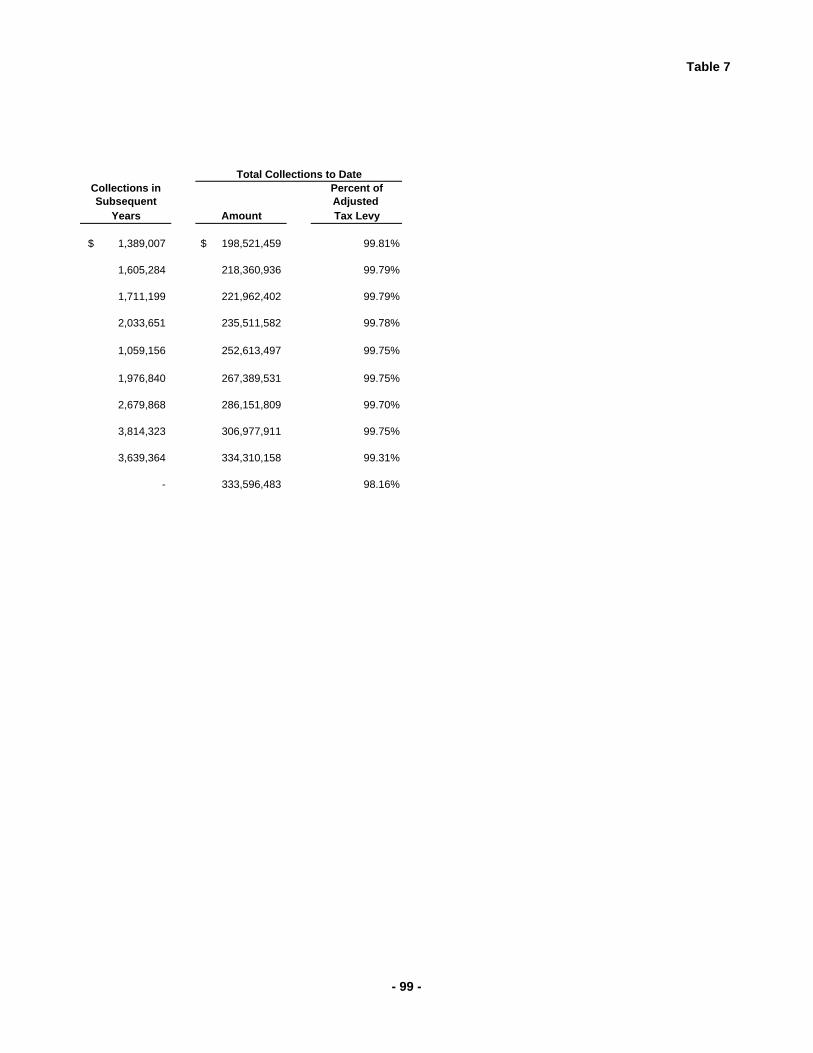

Years ........................................................................................................ 96 7 Property Tax Levies and Collections for Guilford County - Last

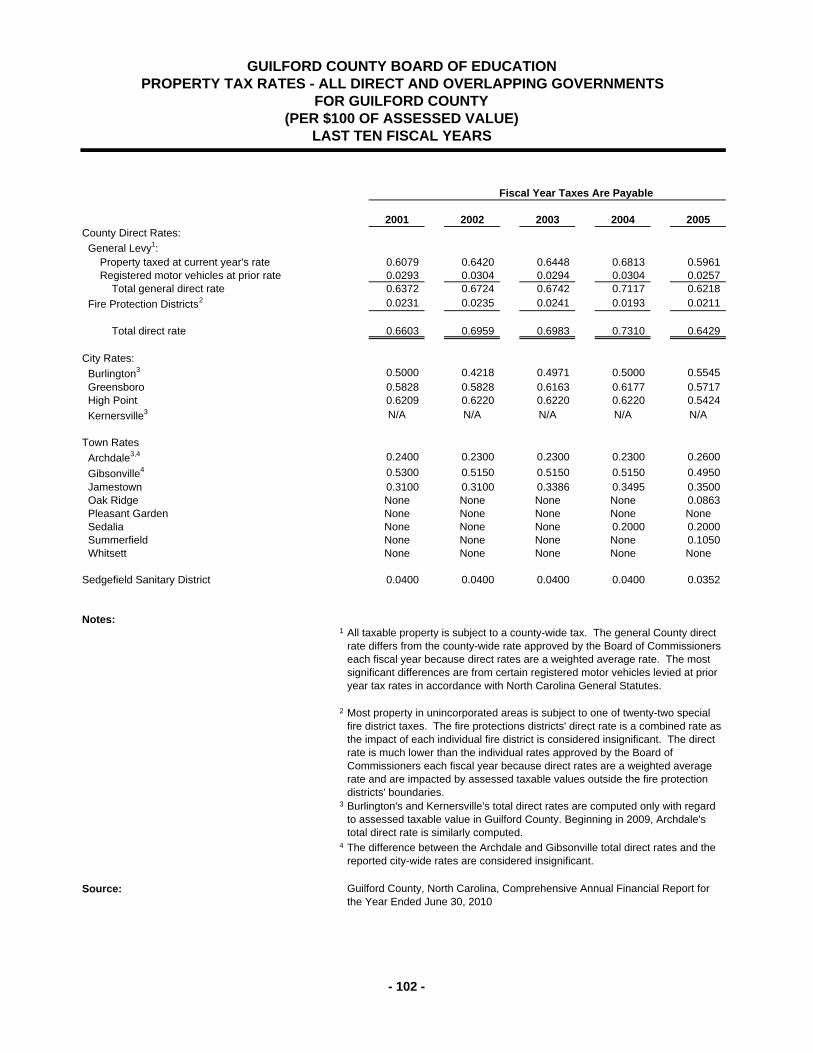

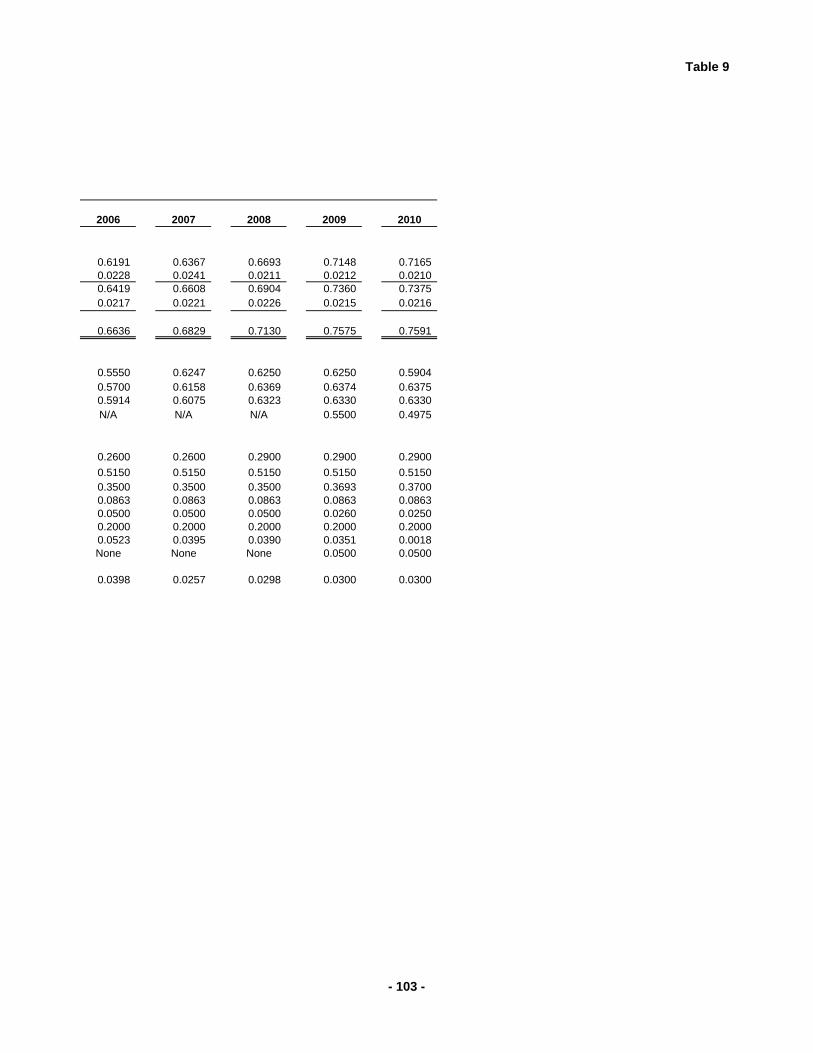

Ten Fiscal Years ...................................................................................... 98 8 Assessed and Estimated Actual Value of Taxable Property for

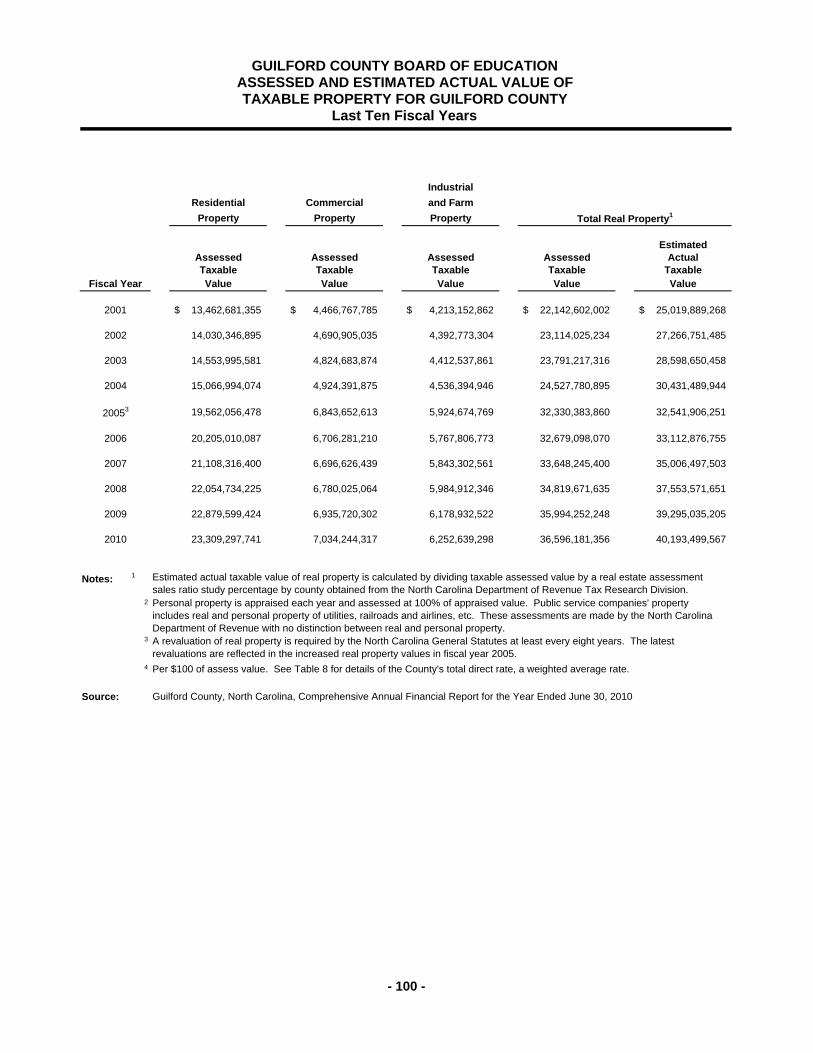

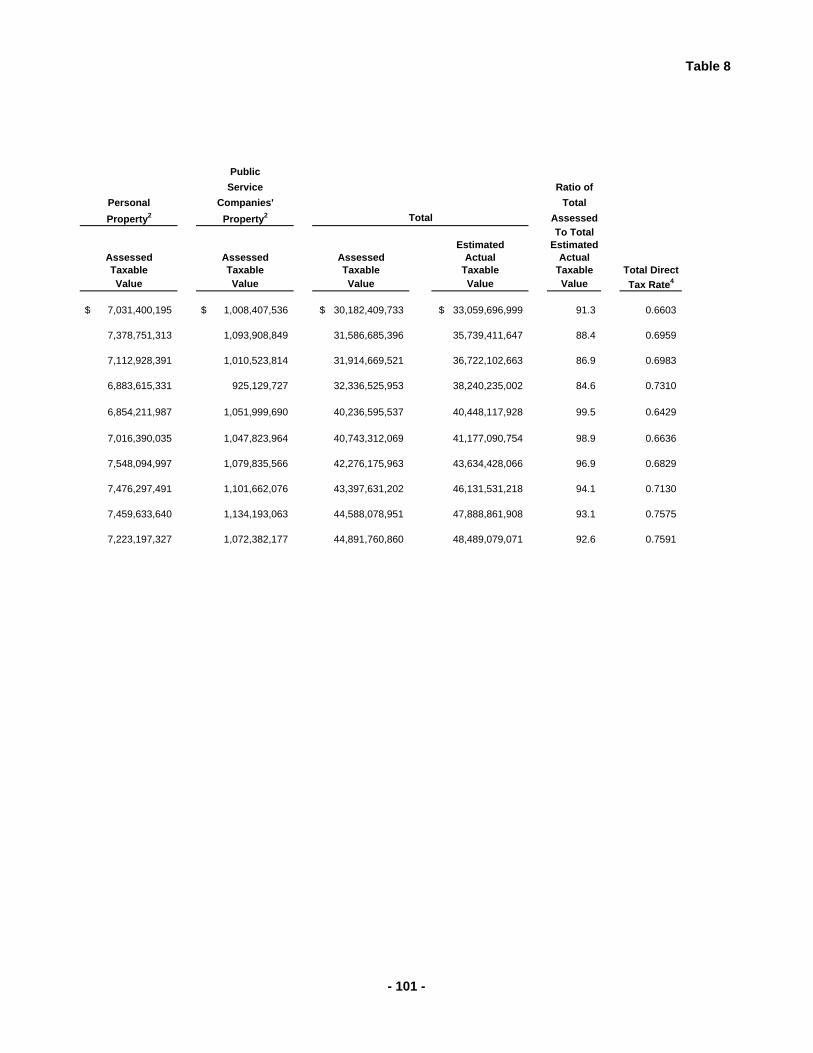

Guilford County - Last Ten Fiscal Years ................................................. 100 9 Property Tax Rates - All Direct and Overlapping Governments

for Guilford County - Last Ten Fiscal Years ............................................ 102

Guilford County Board of Education

TABLE OF CONTENTS (Continued) Table STATISTICAL SECTION (CONTINUED) Page No. 10 Ratio of Outstanding Debt by Type for Guilford County - Last

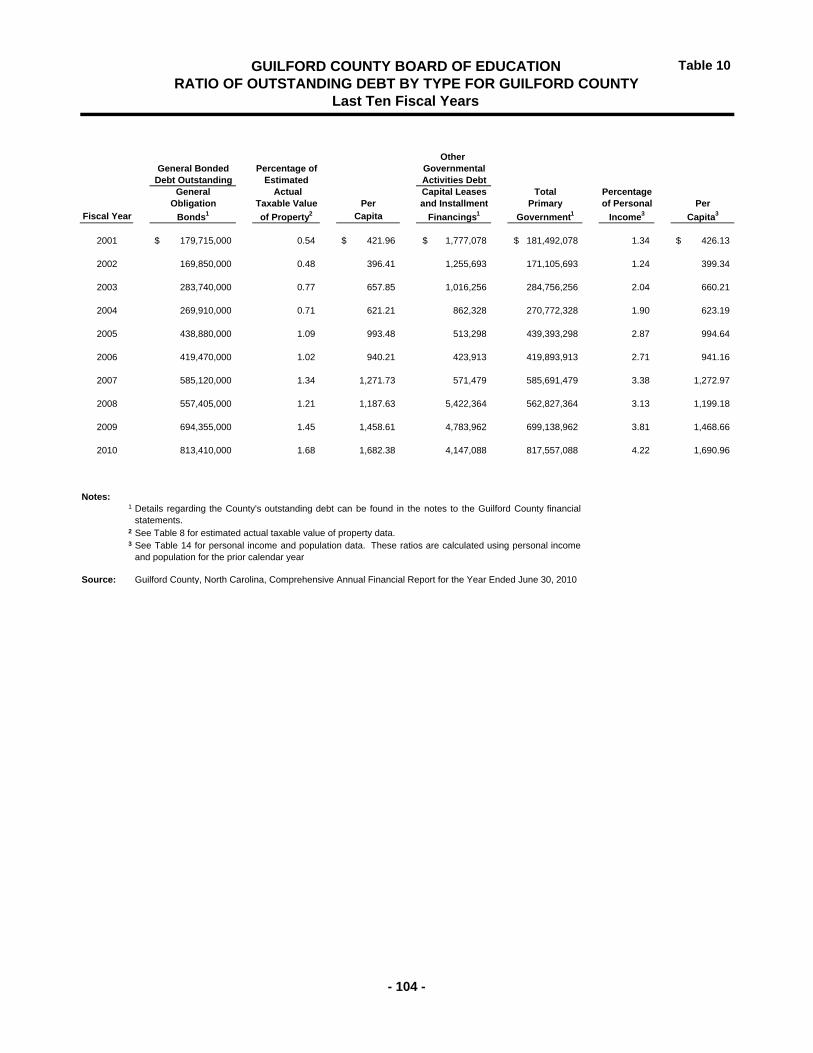

Ten Fiscal Years ...................................................................................... 104 11 Direct and Overlapping Governmental Activities Debt for

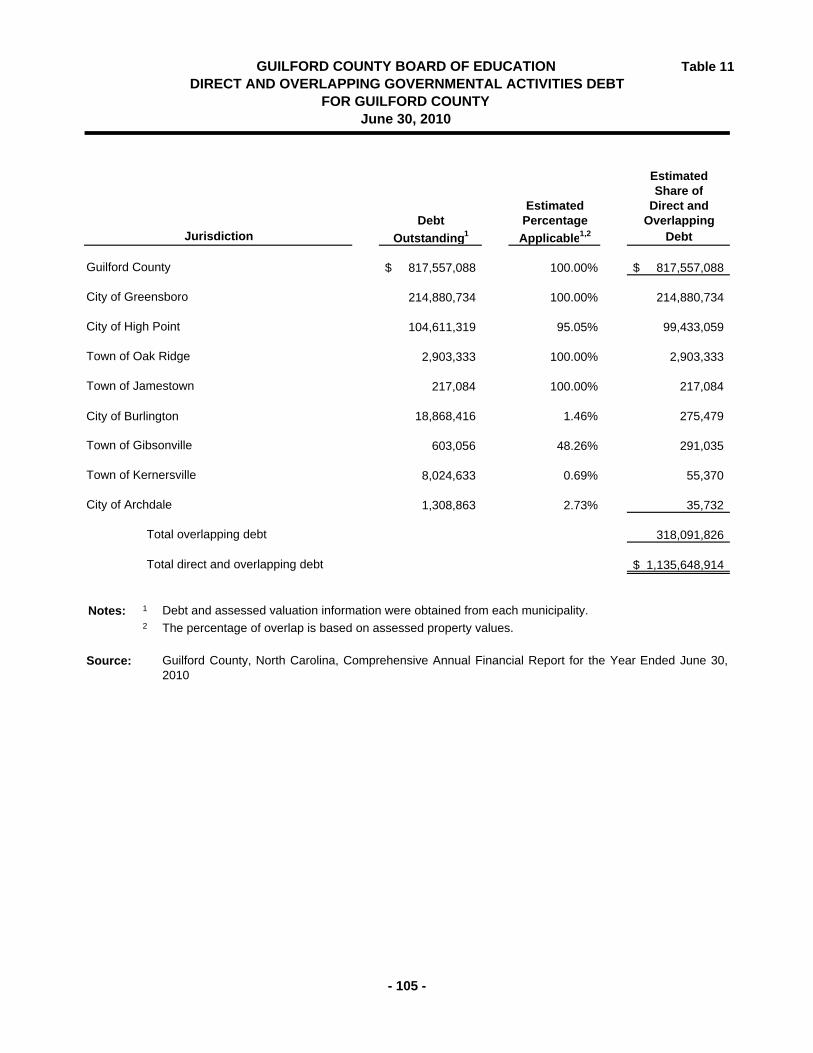

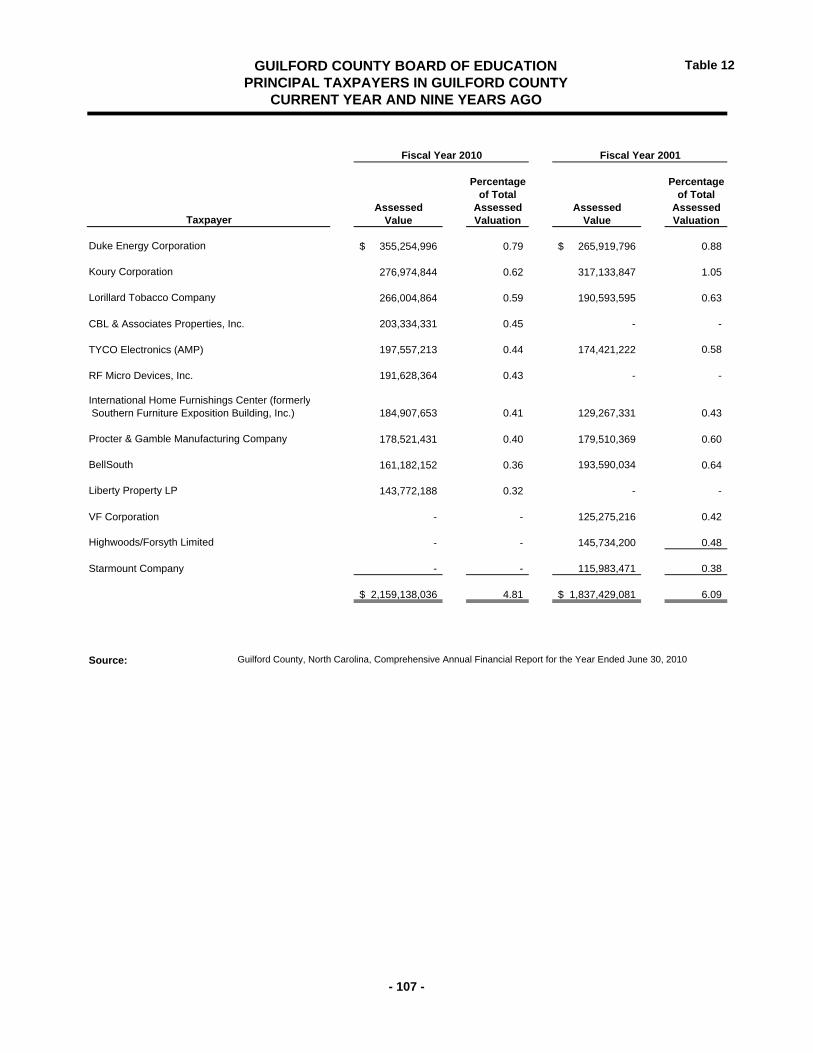

Guilford County - June 30, 2010 ............................................................. 105 12 Principal Taxpayers in Guilford County - Current Year and Nine

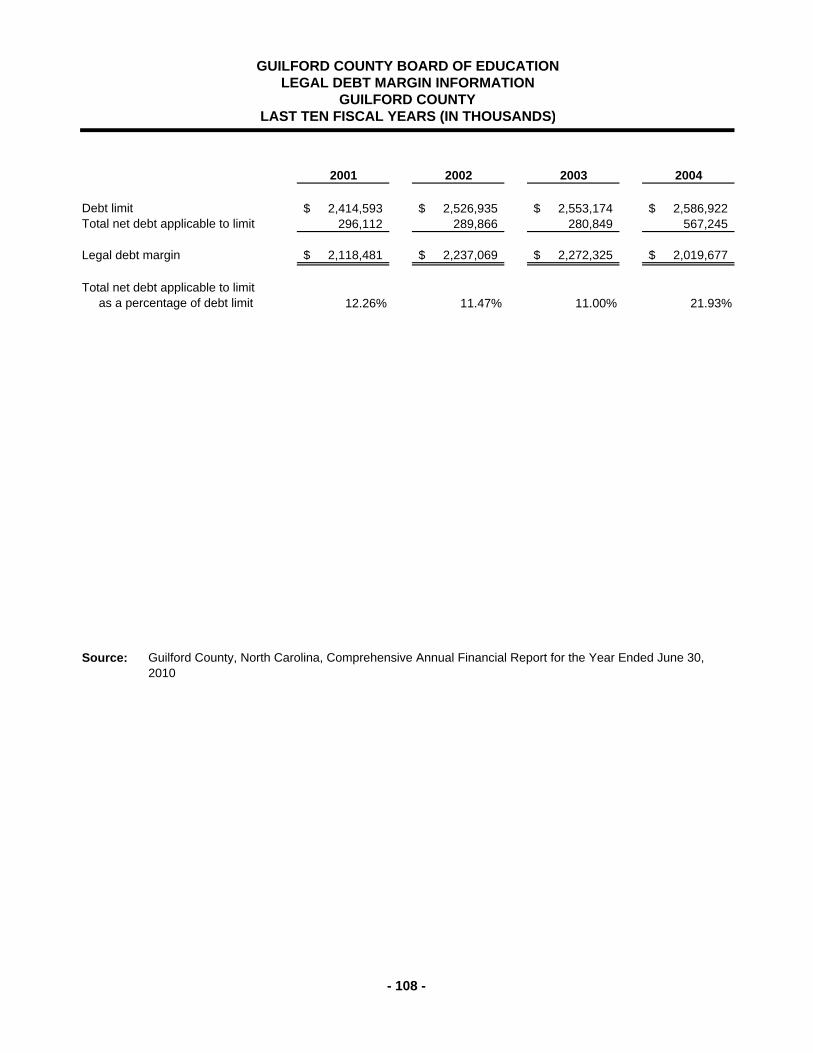

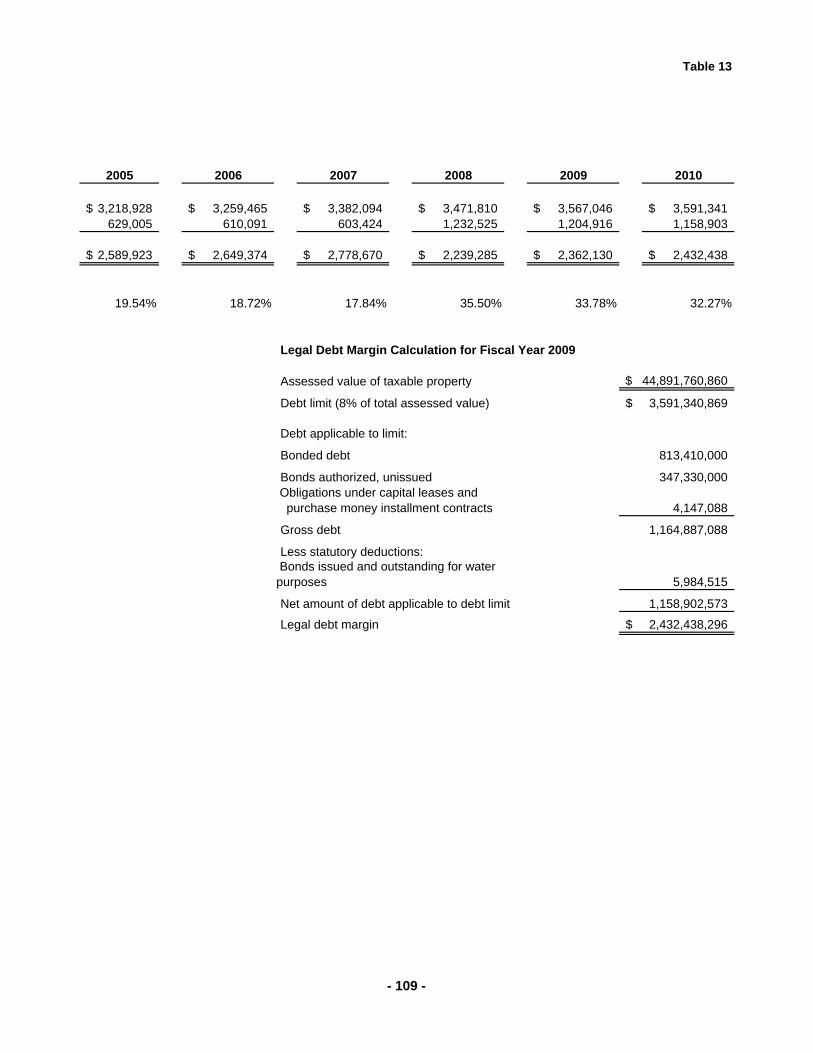

Years Ago ................................................................................................ 107 13 Legal Debt Margin Information - Guilford County - Last Ten

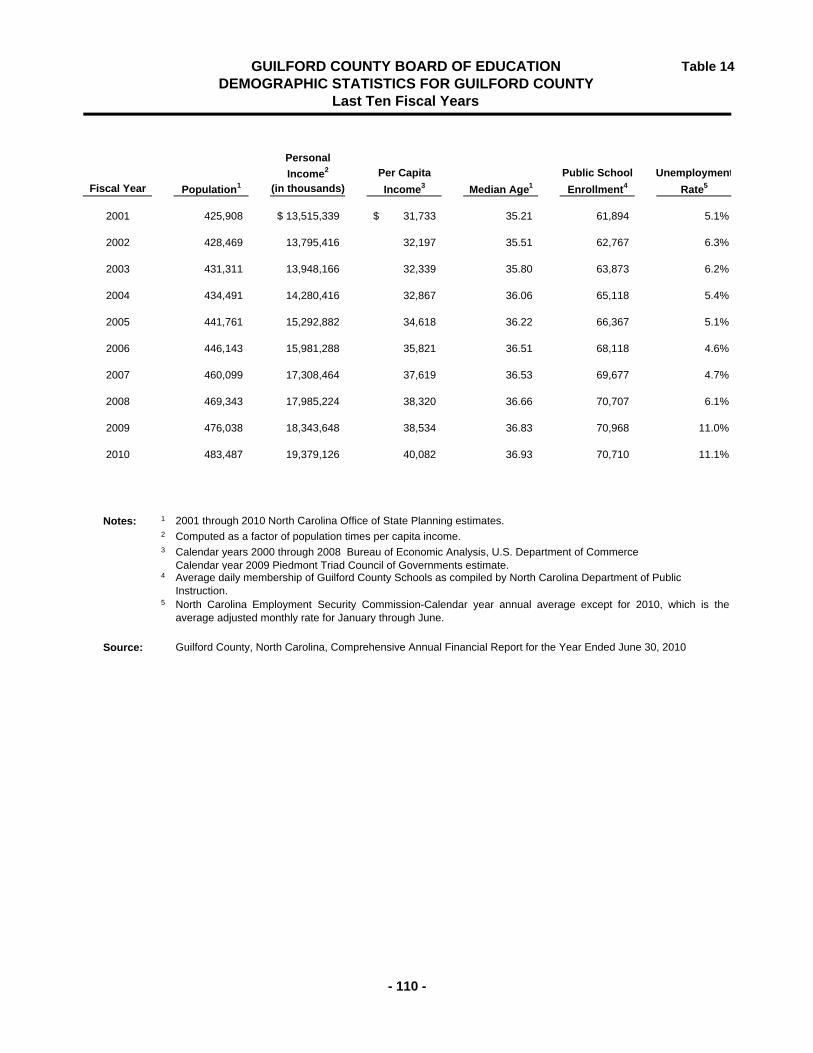

Fiscal Years ............................................................................................. 108 14 Demographic Statistics for Guilford County - Last Ten Fiscal

Years ........................................................................................................ 110 15 Principal Employers - Current Year and Nine Years Ago......................... 111 16 Full-time Equivalent Employers by Function - Last Ten Fiscal

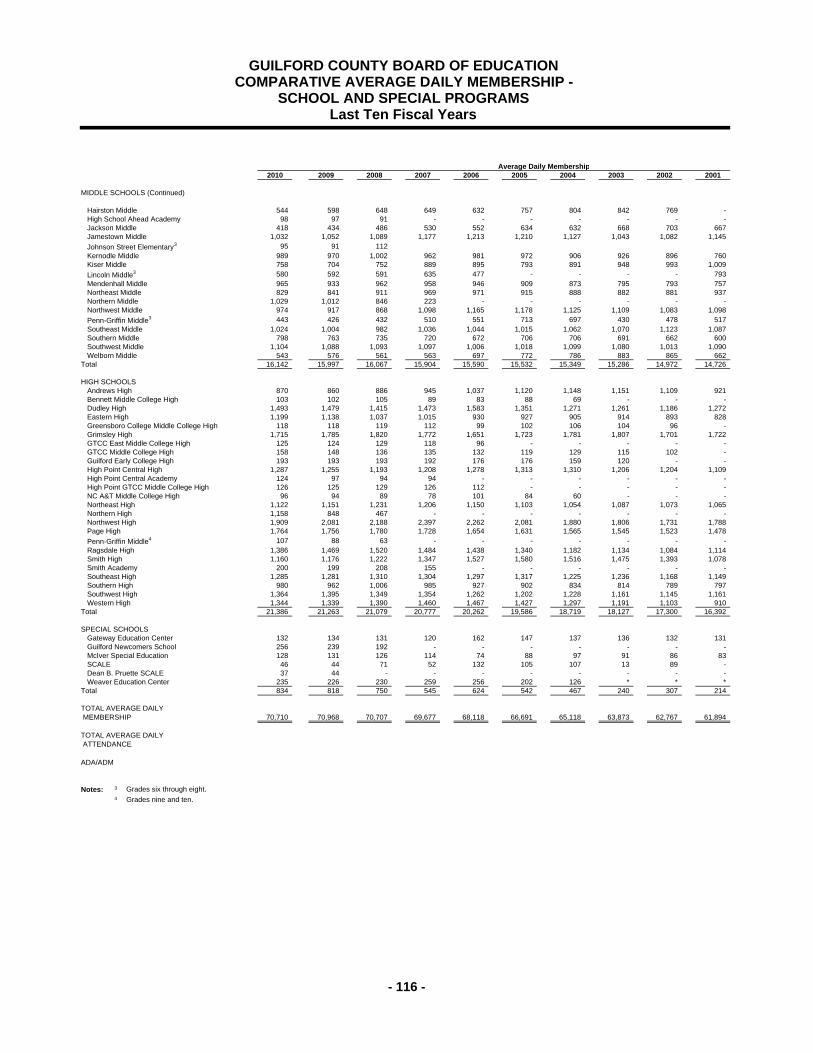

Years ........................................................................................................ 112 17 Comparative Average Daily Membership - School and Special

Programs - Last Ten Fiscal Years ........................................................... 114 18 Operating Statistics - Last Ten Fiscal Years ............................................. 118 19 Instructional Personnel - Last Ten Fiscal Years ....................................... 120 20 School Building Data - Elementary, Middle, High Schools and

Special Use Facilities ............................................................................... 121 Schedule COMPLIANCE SECTION Report on Internal Control Over Financial Reporting and on

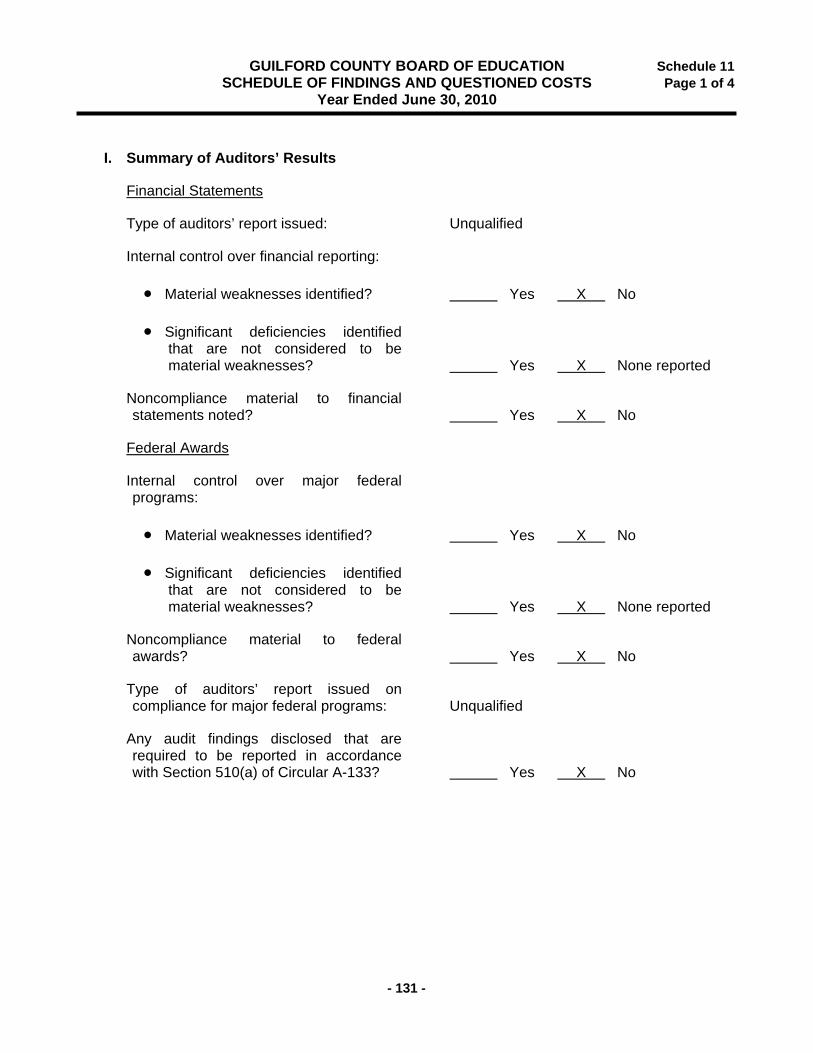

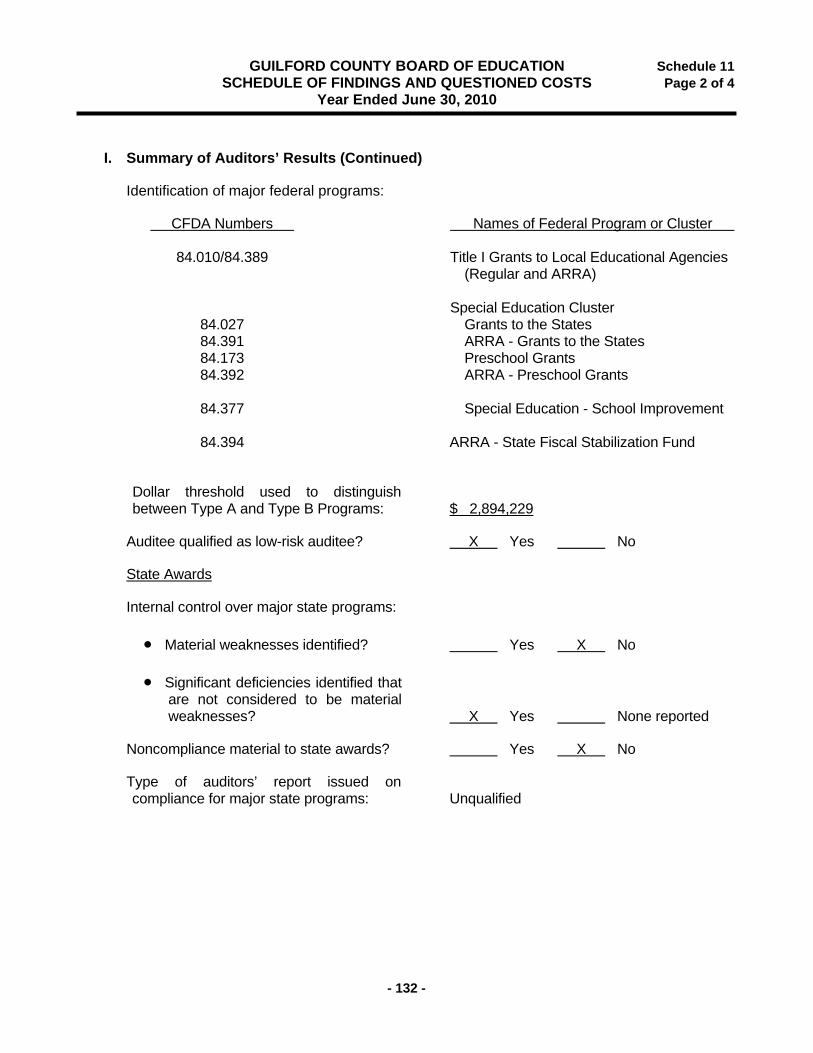

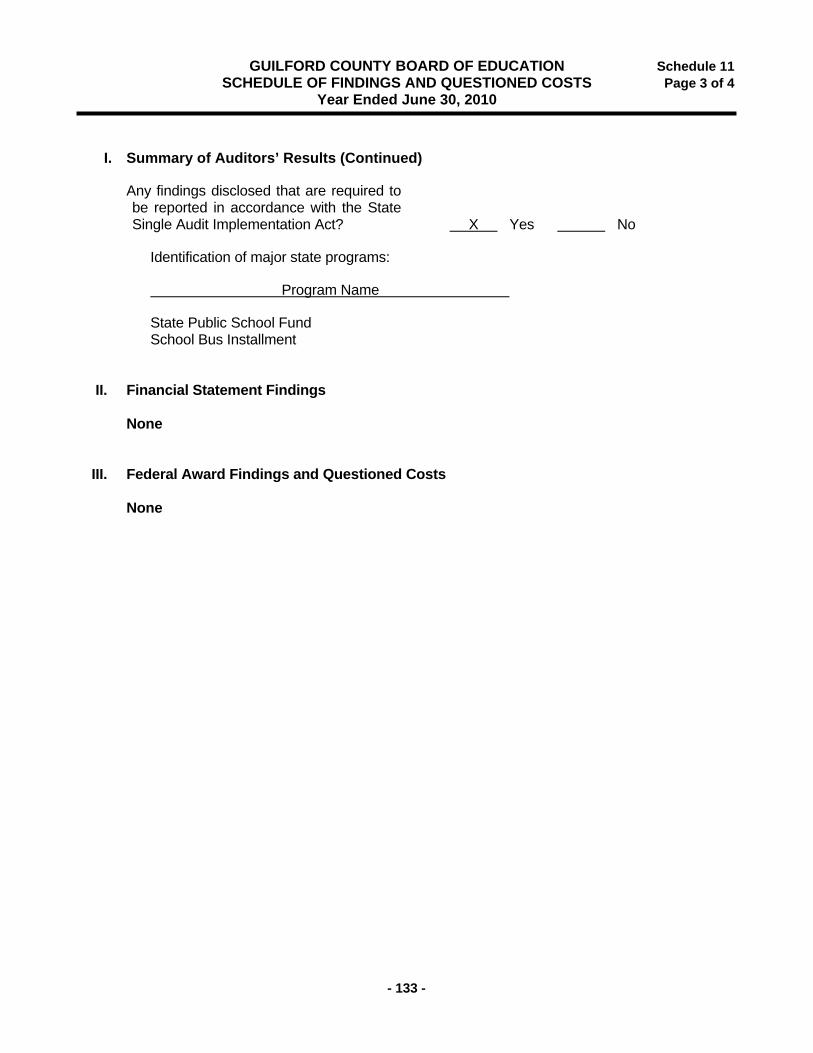

Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ......................................................... 125

Report on Compliance with Requirements That Could Have a Direct and Material Effect on Each Major Federal Program and Internal Control Over Compliance in Accordance with OMB Circular A-133 and the State Single Audit Implementation Act ..................................................................... 127

Report on Compliance with Requirements That Could Have a Direct and Material Effect on Each Major State Program and Internal Control Over Compliance in Accordance with OMB Circular A-133 and the State Single Audit Implementation Act ............................................................................... 129

11 Schedule of Findings and Questioned Costs ........................................... 131 12 Summary Schedule of Prior Year Audit Findings ..................................... 135 13 Corrective Action Plan ............................................................................... 136 14 Schedule of Expenditures of Federal and State Awards .......................... 137

THIS PAGE LEFT INTENTIONALLY BLANK.

INTRODUCTORY SECTION

THIS PAGE LEFT INTENTIONALLY BLANK.

- ii -

component unit is a legally separate organization for which the District is financially accountable and other organizations for which the nature and significance of their relationship with the District are such that exclusion would cause the reporting entity’s financial statements to be misleading or incomplete. The District is financially accountable if it appoints a voting majority of the organization’s governing body and (1) it is able to impose its will on that organization or (2) there is a potential for the organization to provide specific financial benefits to, or impose specific financial burdens on, the District. The District may also be financially accountable if an organization is fiscally dependent on the District, regardless of whether the organization has (1) a separately elected governing board, (2) a governing board appointed by a higher level of government or (3) a jointly appointed board. Using the GASB criteria, management has determined that the District has no component units, nor is it a component unit of any other organization. ECONOMIC CONDITION AND OUTLOOK Guilford County Schools (GCS) serves the diverse needs of the entire county, a 649 square mile area with an approximate population of 476,650. Our enrollment of approximately 71,000 students (our Average Daily Membership for 2009-10 was 70,710 per North Carolina Department of Public Instruction) mirrors the diversity of the community, representing some 142 cultural and ethnic groups and speaking 150 languages/dialects. Guilford County generally enjoys a favorable economic environment, which until the recent recession has enjoyed consistent stable growth. While gross retail sales information is unavailable, comparable State taxable sales figures are available to approximate retail sales growth. Due to the national streamlined sales tax initiative, taxable sales are reported beginning in fiscal year 2006 rather than gross retail sales. State taxable sales for Guilford County declined 9.3% and 8% in fiscal years 2010 and 2009, respectively, after growing 1.5% and 5.7% respectively, in the two previous fiscal years. Taxable sales are $5.07 billion for fiscal year 2010 as compared to $5.59 billion in fiscal year 2009. Guilford County has a labor force of approximately 246,000. During the recent economic downturn, the Piedmont Triad region was affected more strongly than in the past due to the strong negative impact on traditional manufacturing industries. Guilford County’s unemployment rate has historically been below both state and national averages, however, during 2001 this changed as the unemployment rate began to exceed the national average. After tracking the national average for the past two years, the County’s unemployment rate has exceeded the national average for fiscal 2010. The unemployment rate for Guilford County was 6.1% for calendar 2008 and 11.0% for 2009: the U.S. unemployment rate was 5.8% for 2008 and 9.3% for 2009. Guilford County’s unemployment rate of 11.1% for the first six months of 2010 is above the U.S. and North Carolina rates of 9.9% and 10.8%, respectively. Announcements of layoffs in excess of one hundred employees per event by large retail, financial and manufacturing concerns have contributed to the increasing unemployment rate. Guilford County’s economy has continued to change and diversify. In December 2009, manufacturing accounted for 13.5% of the County’s 227,824 jobs compared to 28.6% of the County’s 214,346 jobs in 1980. Manufacturing jobs have declined significantly in furniture and textiles but have shown growth in computer and electronic products, electrical equipment and transportation equipment. Major employers with headquarters or divisions within Guilford County include semiconductor, communications, chemical, bus, truck, pharmaceutical, insurance, aircraft maintenance, healthcare, real estate development, and distribution services. The County is home to two state universities, five private colleges, a private school of law, and a community college with a total enrollment exceeding 50,000 students. FedEx completed construction at Piedmont Triad International Airport (PTIA) of its fifth national hub, FedEx Mid-Atlantic Hub. Initial expenditures by FedEx and the Piedmont Triad Airport Authority are expected to total $300 million. The first phase of the hub became operational in June 2009. Full regional hub operations are slated to begin

- iii -

in the future. FedEx has 200 workers in Phase I, with a planned expansion to a total of 1,500 workers in Phase II. A 9,000-foot runway was constructed at PTIA to accommodate the FedEx hub. The $150 million runway was dedicated in June 2010. FedEx Ground continues construction of its $100 million distribution hub on its 125 acre, $13.3 million site in Triad Business Park. The 400,000 square-foot ground shipping hub will initially bring about 270 new jobs to the Triad. Ultimately, the operation could employ as many as 1,400 workers and contract drivers. Construction began in Spring 2009, with a 2011 projected opening date. Honda Aircraft Company, Inc. announced in February 2007 that it planned to locate its world headquarters and production facility at PTIA. The Company currently occupies an administrative building and its World Research and Development Center at PTIA and began construction of its 250,000 square-foot production hangar in late summer 2009 with expected completion in early 2011. The delivery of the first HondaJet (priced at $4.5 million) is projected to be in the 3rd quarter of 2012. The revitalization of downtown Greensboro continues to thrive. In 2009-2010, Downtown gained a net of 14 new storefront businesses with a total financial investment of $20.9 million. Downtown had 107 building renovation and construction projects generating $8 million, with 52 properties purchased generating investment of $12.9 million. The redevelopment of a vacant 17-story office tower including over 100 condominium units, one floor of office space, retail shops and a restaurant opened for occupancy in the Spring of 2009. A restaurant and bank opened on the first floor in August and December 2009, respectively. Mack Trucks, Inc., one of North America’s largest producers of heavy-duty trucks, celebrated the grand opening of its new world headquarters in Greensboro in September 2009, bringing or creating 493 jobs and investing an expected $17.7 million over the next three years. Ameritox, Ltd., specializing in pain prescription monitoring, opened its new laboratory and material analysis facility in a 70,000 square-foot facility in Greensboro in June 2010. At full capacity, the company will employ 228 people. Precor Incorporated, an exercise equipment manufacturer, celebrated a grand opening of its 230,000 square foot, $26.2 million facility in Rock Creek Center in March 2010. Precor plans to hire 142 new employees at an average salary in excess of $38,000 by 2011. Approximately 90 full-time employees have been hired as of September 2010. The County’s Board of Commissioners approved $294,000 in incentives for Precor in November 2008. American Express confirmed in May 2010 that it will invest up to $600 million in construction of a data center on two sites near Interstate 40 at Rock Creek Dairy Road. Timco Aviation Services officials announced in August 2010 that the Company has hired more than 200 employees since the beginning of 2010 to support its many contracts, and will need another 80 employees by the end of the year. High Point has continued to experience growth in its downtown as well as in outlying areas with $29.4 million of commercial additions or expansions, while creating or announcing 1,405 jobs in 2009. High Point University completed projects totaling $110 million and created 176 new jobs in 2009. Harland Clarke Corporation opened its 135,000 square-foot order fulfillment facility on Premier Drive in High Point in May 2009. The Company initially moved 200 employees from within the County; by August 2009, it had transferred 80 employees from facilities outside the County and by November 2009 it had hired an additional 70 new employees, resulting in 350 jobs at its High Point location.

- iv -

Three interrelated companies, Trans Tech Pharma, PharmaCore, and the Mendenhall Clinical Research Center opened new facilities in 2009 on their campus in High Point. The new facilities are a part of an ongoing project announced in 2007 which will create 205 new jobs over five years. BUDGET PROCESS The North Carolina School Budget and Fiscal Control Act mandates a uniform budget format and the adoption of an annual balanced budget resolution for the State Public School Fund, the Local Current Expense Fund, federal grants restricted as to use, and the Capital Outlay Fund. The district’s budget resolution also includes the Child Nutrition or School Food Service Fund and the ACES (After-School Care Enrichment Services) fund. Budget development is a year-round process that begins in the fall of each year and continues until a budget resolution is adopted by the Guilford County Board of Education on or before July 1. Participation at all levels of the school system is evident in this ongoing process. Schools and central office departments review their budget needs and submit their requests. Parent Teacher Associations (PTAs) offer input. The superintendent, chief financial officer and division chiefs develop the superintendent's budget request prioritizing all requests based on the vision, mission, goals, objectives and strategies outlined in the district’s strategic plan, Achieving Educational Excellence. Initial state and federal budget calculations are based on budget information provided by the North Carolina Department of Public Instruction, if any, and the state and federal planning allotments. A multi-year budget forecasting model was developed for the Local Current Expense Fund in order to facilitate long-range budget/financial planning for the school district by the Board of Education and the County Commission. Previous years’ budgets and development processes were reviewed in order to identify the major budgetary assumptions/variables of federal, state and local origin impacting the school district’s budget development/adoption. The Multi-Year Budget Forecasting Model includes the following budgetary assumptions/variables identified as a result of that review:

salary increase percentage for teachers/licensed staff; salary increase percentage for principals/assistant principals; salary increase percentage for classified employees; changes in employee benefit rates/amounts (social security, retirement, hospitalization, workers’

compensation, unemployment, dental insurance, life insurance); percentage of increase for annual utility/energy and gas/diesel fuel costs; percentage of increase for various risk management areas (i.e., liability/fleet/property/pupil scholastic

accident insurance lines of coverage); additional energy costs for newly constructed and or air conditioned square footage associated with the

district’s Capital Improvement Plan (CIP) Program; additional maintenance/staffing costs associated with newly constructed and/or renovated square footage

associated with the CIP Program; and increase in funding associated with projected growth in student enrollment (the County has, in several

recent fiscal years, funded the projected increase in tenth-day enrollment for the upcoming fiscal year at the same level of county appropriation per pupil funding as the district received in the current fiscal year).

- v -

The forecasting model does not include: strategic plan initiatives; funds to address “No Child Left Behind” accountability/achievement goals/requirements; or funds to offset anticipated state/federal budget cuts.

These items are funded from the increase in funding associated with projected growth in student enrollment, if available, and/or from the redirection of existing state/local/federal dollars and/or from additional funding requested from the county commission.

The district has two proprietary (enterprise) funds - the Child Nutrition or School Food Service Fund and the After School Care Enrichment Services (ACES) fund. Budgets for these funds are developed based on historical revenue, expenditure and participation data as well as anticipated legislated salary increases and/or changes in employee benefit rates/amounts and/or inflationary increases for food or supplies and/or student enrollment projections and/or changes in child nutrition meal costs or weekly ACES fees.

Nearly $100 billion in federal stimulus or American Recovery and Reinvestment Act of 2009 (ARRA) funds are dedicated to education. The U.S. Department of Education (USED) distributed ARRA funds to states to save and create jobs while advancing reforms and improvements that will create long-lasting results for K-12 students.

ARRA provides funding to North Carolina schools through existing federal formula and competitive grant programs including Title I, the Individuals with Disabilities Education Act (IDEA), and the McKinney-Vento Homeless Assistance program. Funds must be used consistent with statutory and regulatory requirements per each formula grant with some exceptions.

To receive these funds, states must agree to use the funds to: Improve teacher effectiveness and the equitable distribution of effective teachers in schools and

classrooms. Make progress toward college and career-ready standards and rigorous assessments. Improve student achievement in low-performing schools. Enhance data systems to track student progress.

Monitoring of budgets and funds: There are several avenues available to anyone suspecting fraud, waste or abuse of ARRA funds.

The hotline to report claims to the NC Office of Economic Recovery and Investment (OERI) of waste, mismanagement or any abuse related to use of federal recovery funds is 919.733.1433.

Internal Audit and Advisory Services manages the Department of Public Instruction Fraud Hotline established by the agency as part of its ongoing fraud detection and prevention efforts. Anyone suspecting fraud, waste, or abuse involving the Department's funds or programs should call the Internal Auditor at 919.807.3685 or submit a written complaint to: Internal Audit Hotline

North Carolina Department of Public Instruction 6301 Mail Service Center Raleigh, NC 27699-6301

The US Education Department Office of Inspector General Hotline is a toll free number: 1-800-MIS-USED, or you may complete and submit a complaint form (available at https://wdcrobcolp01.ed.gov/CFAPPS/OIG/englishhotlineform.cfm) to:

Inspector General's Hotline Office of Inspector General U.S. Department of Education 400 Maryland Avenue, SW Washington, DC 20202-1500

- vi -

Budget management includes three separate areas: pre-audit of disbursements and encumbrances amendments to the budget resolution

accounts for transfers of funds from one account to another within guidelines of the respective funding source(s)

tracks increases (new funds added to budget) or decreases (funds removed from budget) budget resolution specifies transfer authority and reporting requirements

meeting applicable reporting requirements (local, state and federal) Some of the tools/mechanisms used to evaluate budgets include:

internal audits external audits program audits analyzing expenditures and revenues analyzing staffing patterns developing multi-year budgets

The district incorporates the following practices in budget development and implementation:

integrating long-term planning with the budget process establishing measures for continuous performance monitoring obtaining citizen and other stakeholder involvement early in the budget process communicating goals, objectives, strategies and desired outcomes promoting a sense of ownership and empowerment to budget managers to implement effective practices

and achieve goals incorporating realistic revenue and expenditure forecasts reviewing budget-to-actual or budget-to-projected actual comparisons of revenues, expenditures, cash flow,

and fund balance periodically during budget development providing monthly summary and detail expenditure reports to budget managers providing quarterly financial reports to the Board of Education and the Board of County Commissioners using the district’s accounts payable, general ledger, payroll and purchasing systems to monitor available

funds before encumbering/spending occurs preparing a comprehensive annual financial report of the district’s operations

MAJOR INITIATIVES, SERVICE EFFORTS AND ACCOMPLISHMENTS

Our vision (what we will become), our mission and thematic goals (how we will get there), and our core values (what we believe) solidify the underlying foundation for all Guilford County Schools’ decisions and actions. Our vision is to become the top performing academic metropolitan school district in America. The mission of the district is that Guilford County students will graduate as responsible citizens prepared to succeed in higher education, or in the career of their choice.

The Board in partnership with parents and community members wants to share these district core values in order to strengthen our schools and improve the quality of life for all of our citizens.

Diversity. We are committed to creating an educational organization where a variety of persons and perspectives are welcome. We are committed to providing an environment where students and staff from all cultures and backgrounds may succeed.

- vii -

Empathy. We are committed to developing a culture where our employees identify with and understand the feelings of our students and parents and their colleagues.

Equality. We are committed to creating a school system where everyone is appreciated and judged based solely on their contributions and performance. Through the work of this institution, we will create awareness of and develop strategies to understand and eradicate prejudice, discrimination and racism on the individual and organizational level.

Innovativeness. We are committed to fostering a work environment where the goal is not to manage innovations, but to become innovative. Problems are identified, ownership of those problems is assumed by the adults in the district, and everyone works together as agents of the solution until the problems are solved. We will not stop until obstacles are removed, solutions found and clear and compelling goals are established.

Integrity. We are committed to creating a school district that acts with honesty and forthrightness, holding ourselves to high academic and ethical standards, and dealing with everyone with respect.

The Guilford County Schools (GCS) Strategic Plan serves as the district’s road map for achieving educational excellence. The plan includes strategies designed to boost student achievement, increase family and community involvement, improve district service, increase the teacher retention rate and improve school safety and discipline. Information captured through the “Mo Wants to Know” campaign and the superintendent’s listening and learning tour—along with the Board of Education’s mission and core values—guided the development of the strategic plan. The plan is divided into eight key areas: improving academic achievement; supportive family and community involvement; strategic human resource management; respectful and responsive service; safe schools and character development; optimal operations; transformational technology; and, clear baseline and equitable standards.

- viii -

ACHIEVING EDUCATIONAL EXCELLENCE GCS Points of Pride:

The number of schools earning the top Honor School of Excellence/School of Excellence rating based on the

state’s ABCs has increased from one in 2007-08 to 13 in 2009-10.

ABCs results showed that 91.4 percent of the district’s schools made expected or high growth in student academic achievement during the 2009-10 school year. This number is up from 75.4 percent in 2008-09.

Eighty-eight of 113 regular schools made positive gains on overall proficiency, and 39 schools exceeded a five-

percentage point gain. The GCS Class of 2010 earned $110 million in scholarships this year. This is almost $32 million more than the Class of

2009 earned last year. In 2009-10, five of the district’s high schools achieved 100 percent graduation rates - Weaver Academy, Penn-Griffin

School for the Arts, The Academy at Smith, Greensboro College Middle College and The Early College at Guilford. Seven other schools had graduation rates higher than 90 percent.

Overall performance on the AP exams rose from 43 percent passing in 2005 to more than 53 percent in 2010. Twelve district high schools made Newsweek’s Top High Schools. The Early College at Guilford was named to the

Elite Schools. GCS’ Alternative Certification Track (ACT) program was the first program in the state to offer lateral entry

candidates an in-house teacher preparation program that leads to licensure. The first Summer Arts Institute and district-wide musical were developed in response to the district’s Strategic Plan,

which calls for enrichment activities that support the academic and social growth of students. The musical, “Willy Wonka,” gathered the talents of hundreds of students, teachers and parent volunteers from across the county, while 240 students participated in week-long classes in visual art, orchestra, dance, theater, band and chorus.

About 290 GCS employee and student volunteers completed the district’s Habitat for Humanity house as part of

GCS’ character development initiative. Service learning, a component of character development, will be a major focus for all students across the district during the 2010-11 school year.

GCS Students Show Intelligence Plus Character:

Southeast High senior Alex Hughes was one of three winners in the “I Am What I Learn” video contest sponsored by

the U.S. Department of Education. His video and two others received the highest number of votes from viewers. Each student will receive a prize of $1,000.

Elizabeth Dzugan, a 2010 graduate of The Early College at Guilford, held the lucky key that unlocked the door to a new

2011 Scion xB at the 2010 Cool to Be Smart event. She was among more than 400 GCS graduates that qualified to win the car and other high-tech prizes. Thanks to Rice Toyota, Dzugan drove home in the new car, with taxes, tags and title included.

Edward Myers was outside near his house when he found a purse with $2,000 inside. Edward was a fifth-grader at Irving Park Elementary when he immediately knew what to do. He showed his mom, and they turned the money in to police. The student’s actions are an example of why character education is a priority for Guilford County Schools.

- ix -

Weaver Academy students supported literacy and helped to expand character education throughout GCS by publishing their own original children’s books. They donated the books to 12 schools during a presentation at Vandalia Elementary. During the past two years, music production and art students have written stories, provided illustrations and recorded sound effects for children’s books that focus on character education.

Nathanael Greene Elementary collected 818 pounds of cans for recycling as part of their involvement with the Guilford

County Environmental Services program, Kids, Cans & Ca$h Recycle Challenge. Nathanael Greene not only collected the most cans in their category, but they also collected more cans than any school that participated.

Students and faculty at the Doris Henderson Newcomers School planted a sustainable garden on the school’s campus.

The “Community in Peace Gardens” is rooted in the belief that gardening supports the wellbeing of the entire school community. While helping with the garden, students learn about life cycles, ecosystems, species diversity, environmental pollution and food economics.

Dickson “Doc” Hendley, a 1997 graduate of Ragsdale High, was one of CNN’s 10 finalists for Hero of the Year. He

was recognized for his efforts to provide clean water to communities worldwide. After learning about the world’s water crisis while travelling during college, Hendley started Wine to Water, a nonprofit organization that provides water to people in developing nations and gives them the means to solve their own water crisis in a sustainable way.

GCS Staff – Teaching Excellence By Example:

Rodney Boone, principal of The Academy at Lincoln, was the GCS nominee for Magnet Principal of the Year, which recognizes outstanding school leaders who succeed in providing innovative programs that promote equity, diversity and academic excellence for students in magnet schools.

Chief Financial Officer, Sharon Ozment, was named a co-winner of the Chief Financial Officer of the Year in the government category of the Business Journal.

Dr. Gongshu Zhang, the district’s Chief Accountability and Research Officer, was recognized by the Council of the Great City Schools with the Houghton Mifflin Harcourt Research and Assessment Leadership Award.

Pearce Elementary teacher Angela Osborne and Archer Elementary teacher Brandy Pinnix Widener each received a

Bright Ideas Grant from Energy United. Together, the two received nearly $4,000. Cynthia Sevier, the director of school nutrition services for GCS, received the annual Friend of Child Nutrition

award from the N.C. Department of Public Instruction.

Nora Carr, the district’s Chief of Staff, received the 2010 NSPRA Presidents Award given by the National School Public Relations Association (NSPRA).

Wanda Smith, a pre-K teacher at Archer Elementary, received a Certificate of Merit from the American Red Cross for actions she took to save a student’s life. The American Red Cross awards the Certificate of Merit as its highest honor to individuals who save a life using skills and knowledge learned in a Red Cross course.

INTERNAL CONTROLS Management of the district is responsible for establishing and maintaining internal controls designed to ensure that the assets of the district are protected from loss, theft, or misuse and to ensure that adequate accounting data are compiled to allow the preparation of financial statements in conformity with generally accepted accounting principles. The internal controls are designed to provide reasonable, but not absolute, assurance that these objectives are met. The concept of reasonable assurance recognizes that: (1) the cost of a control should not exceed the benefits likely to be derived; and (2) the evaluation of costs and benefits requires estimates and judgments by management. We believe the Board’s internal accounting controls adequately safeguard assets and provide reasonable assurance of proper recording of financial transactions.

- x -

As a recipient of federal, state and county financial assistance, the district also is responsible for ensuring that adequate internal controls are in place to ensure compliance with applicable laws and regulations related to those programs. The internal controls are subject to periodic evaluation by management and the external auditor for the district. The program administrators for school accounting monitor the activity funds of the individual schools for compliance with applicable federal, state, and local laws/regulations/policies/procedures. As a part of the district’s single audit, tests are made to determine the adequacy of the internal controls, including that portion related to state and federal financial assistance programs, as well as to determine that the district has complied with applicable laws and regulations. The district’s single audit for the fiscal year ended June 30, 2010 resulted in no instances of material weaknesses in internal controls, material violations of applicable laws and regulations or questioned costs. INDEPENDENT AUDIT North Carolina General Statutes require an annual audit by independent certified public accountants. The financial records and transactions of the Guilford County Board of Education for the year ended June 30, 2010 have been audited by Dixon Hughes PLLC, a firm of independent certified public accountants. Their audit of the basic financial statements and accompanying combining and individual fund statements and schedules was performed in accordance with generally accepted auditing standards and, accordingly, included a review of the Board’s system of budgetary and accounting controls. In addition to meeting the requirements set forth by the statutes, the audit also was designed to meet the single audit requirements. Guilford County Schools received an unqualified opinion on the basic financial statements. The auditors’ report on the basic financial statements and the combining and individual fund statements and schedules are included in the financial section of this Report. FINANCIAL REPORTING The Guilford County Board of Education has prepared the Comprehensive Annual Financial Report in conformance with Governmental Accounting Standards Board (GASB) Statement No. 34, Basic Financial Statements – and Management’s Discussion and Analysis–- for State and Local Governments. GASB Statement 34 is an all encompassing and sweeping change to financial reporting requirements for governments. The timing of GASB Statement 34 implementation depends upon the reporting entity’s total revenues. Public school districts with annual revenues of $100 million or more were subject to the provisions of GASB Statement 34 starting with fiscal years ending June 30, 2002. GASB 34 creates the following financial statements that had not previously been published: Statement of net assets to report all assets and liabilities of the district as a whole; Statement of activities to report all revenues and expenses of the district as a whole, and Budgetary comparison statements to inform readers of changes in the budget during the fiscal year as well as

compare year-end results with the final budget.

Management’s Discussion and Analysis provides an overview of the school district’s financial activities and condition for the fiscal year ended June 30, 2009. The analysis focuses on school district financial performance as a whole. Please read it in conjunction with this transmittal letter and the school district’s financial statements.

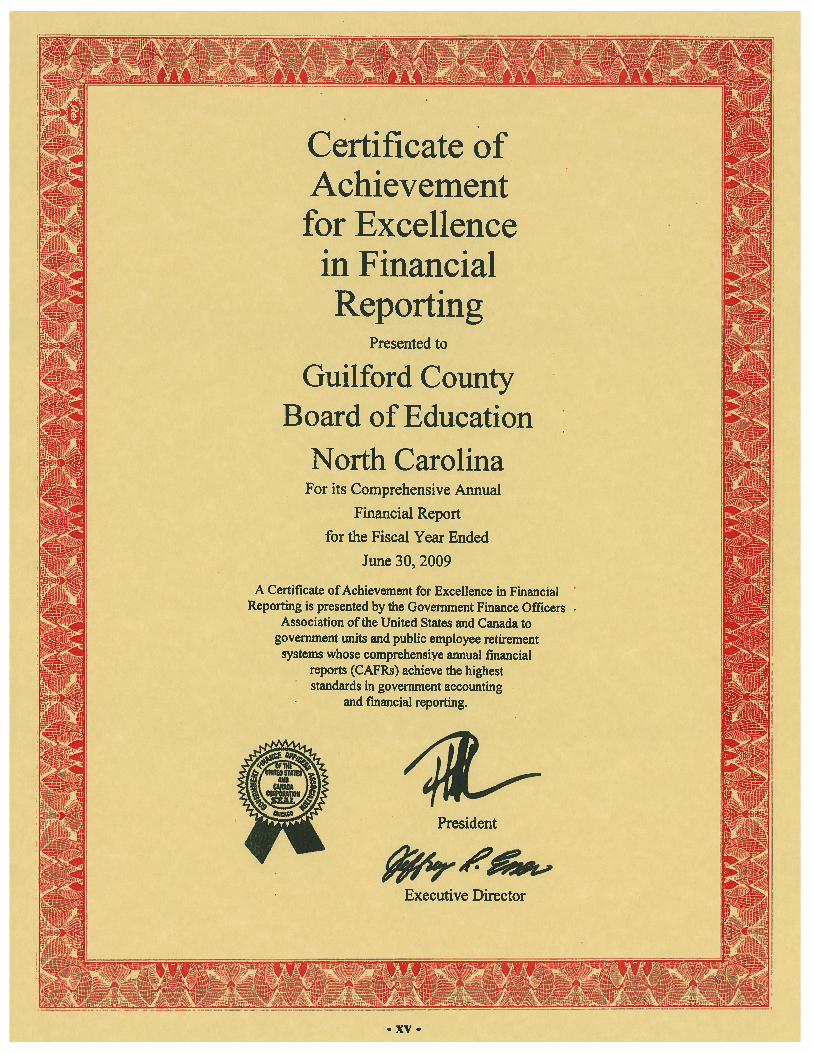

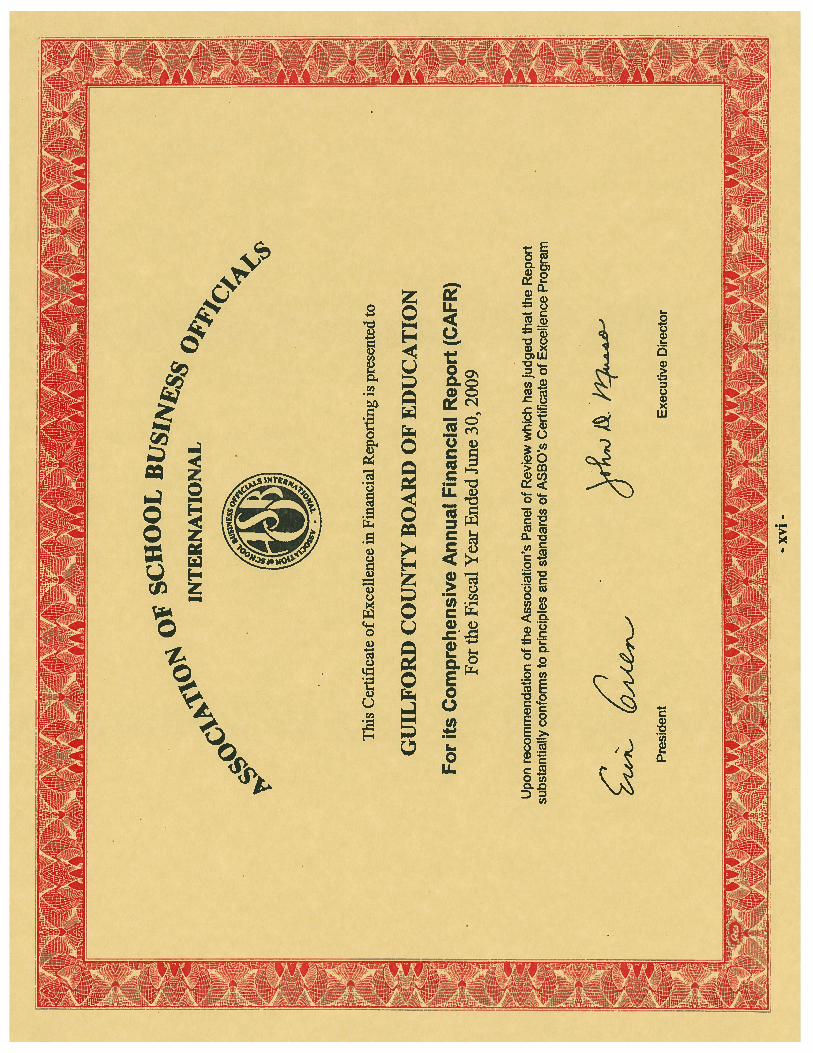

AWARDS The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting and the Association of School Business Officials International (ASBO) awarded a Certificate of Excellence in Financial Reporting to the Guilford County Board of Education for its comprehensive annual financial report for the fiscal year ended June 30, 2009. These are prestigious awards recognizing conformance with the highest standards for preparation of state and local government financial reports.

- xi -

These awards are made only to governmental units that publish a comprehensive annual financial report that is easily readable, efficiently organized, and conforms to program standards as well as satisfies generally accepted accounting principles and applicable legal requirements. The awards are valid for a period of one year only. We believe the accompanying Report continues to conform to GFOA and ASBO program requirements; therefore, we will submit it to these respective organizations for consideration of renewed certificate eligibility and award. In addition, the GFOA presented a Distinguished Budget Presentation Award to the Guilford County Board of Education for its annual budget document for the fiscal year beginning July 1, 2009. The Board has received this award for nine consecutive years. In order to receive this award, the district must publish a budget document that meets program criteria as a policy document, as an operations guide, as a financial plan, and as a communications device. ACKNOWLEDGEMENTS The preparation of this Report could not have been accomplished without the efforts and dedication of the Financial Services staff of Guilford County Schools and the independent audit firm. We would like to express our appreciation to all of the employees who contributed in the development of this Report and to the Guilford County government for providing statistical data. Also, we would like to thank members of the Guilford County Board of Education for supporting the financial operation of the school system in a dedicated and responsible manner. Respectfully submitted, Maurice O. Green Sharon S. Ozment Superintendent Chief Financial Officer

xii

THIS PAGE LEFT INTENTIONALLY BLANK.

- xiii -

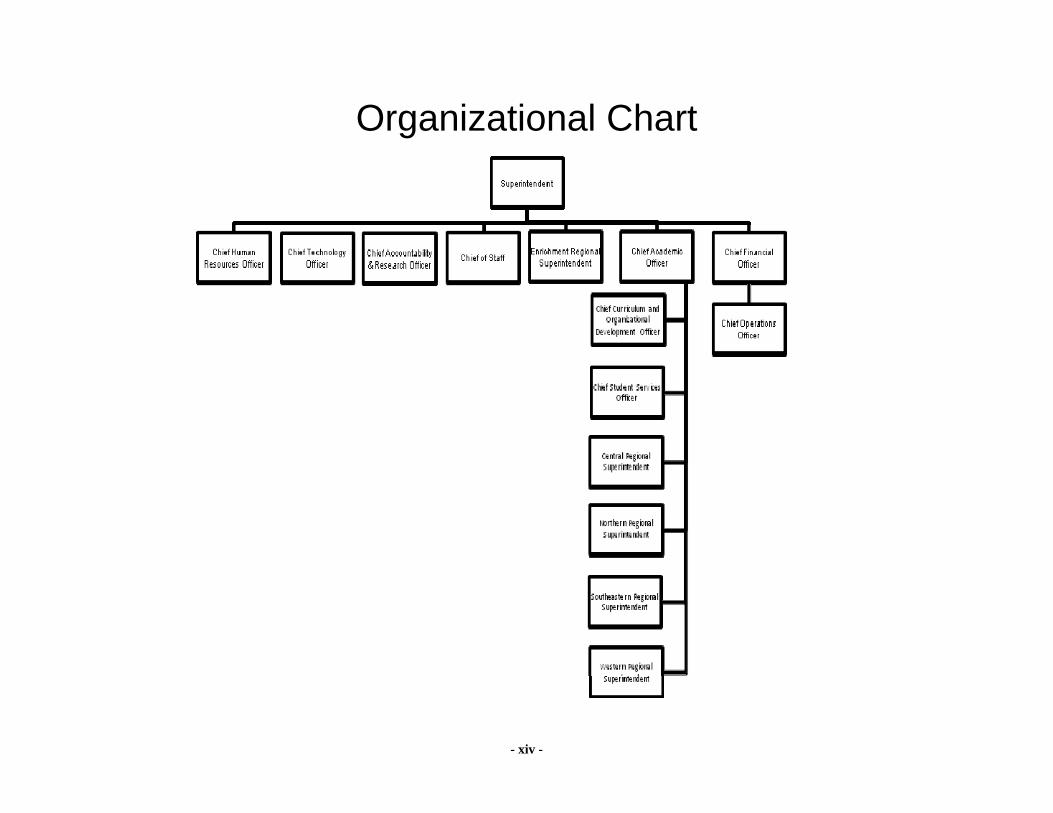

GUILFORD COUNTY SCHOOL SYSTEM

BOARD MEMBERS AND

PRINCIPAL OFFICIALS

BOARD OF EDUCATION

Alan W. Duncan, Chairperson Amos Quick, III, Vice Chairperson

Dr. Sandra Alexander Jeff Belton

Kris B. Cooke Paul Daniels

Carlvena Foster Darlene Garrett Deena A. Hayes

Garth Hébert Dr. Nancy R. Routh

SUPERINTENDENT

Maurice O. Green

SUPERINTENDENT’S CABINET

Nora Carr, Chief of Staff Dr. Lewis D. Ferebee, Enrichment Regional Superintendent

Dr. Beth Folger, Chief Academic Officer Angelo Kidd, Western Regional Superintendent

Dr. Phyllis W. Martin, Southeastern Regional Superintendent John W. Modest, Northern Regional Superintendent

Dr. Shirley D. Morrison, Chief Human Resources Officer Sharon S. Ozment, Chief Financial Officer

Gwen Willis, Chief Student Services Officer Dr. Terry W. Worrell, Central Regional Superintendent

Dr. Terrence O. Young, Chief Technology Officer Dr. Gongshu Zhang, Chief Accountability and Research Officer

Dr. Barbara H. Zwadyk, Chief Curriculum and Organizational Development Officer

- xiv -

Organizational Chart

FINANCIAL SECTION

THIS PAGE LEFT INTENTIONALLY BLANK.

- 1 -

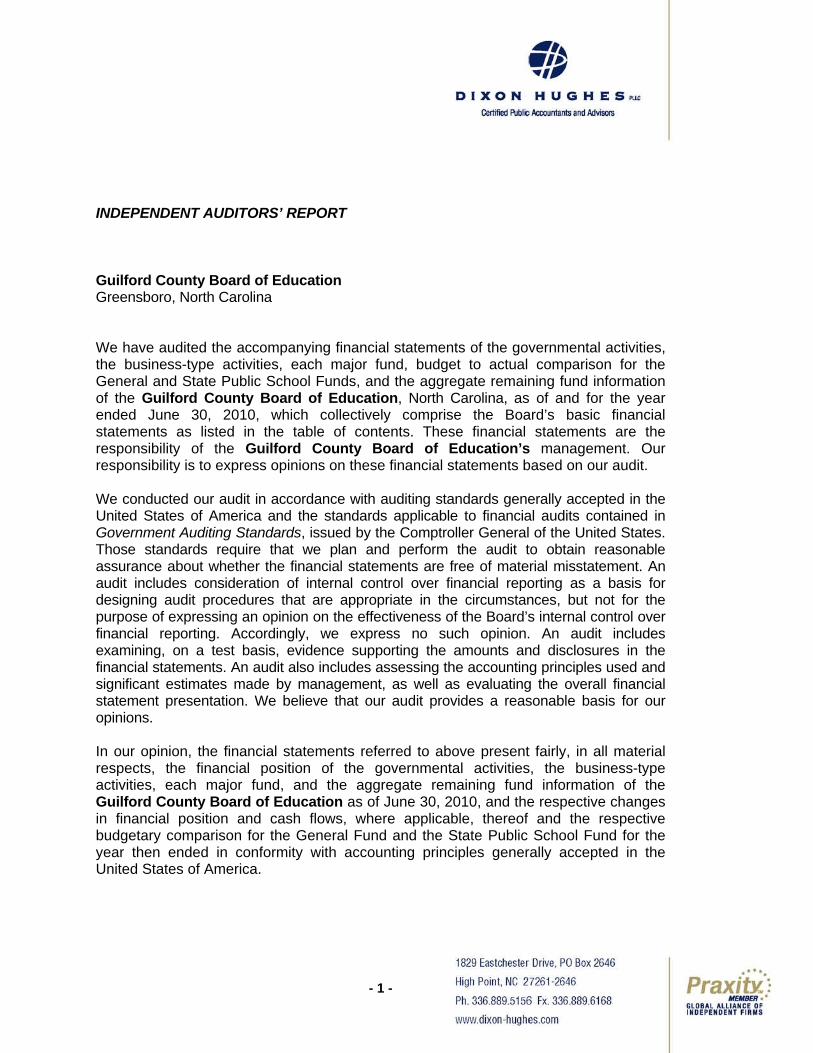

INDEPENDENT AUDITORS’ REPORT Guilford County Board of Education Greensboro, North Carolina We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, budget to actual comparison for the General and State Public School Funds, and the aggregate remaining fund information of the Guilford County Board of Education, North Carolina, as of and for the year ended June 30, 2010, which collectively comprise the Board’s basic financial statements as listed in the table of contents. These financial statements are the responsibility of the Guilford County Board of Education’s management. Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Board’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our opinions. In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the Guilford County Board of Education as of June 30, 2010, and the respective changes in financial position and cash flows, where applicable, thereof and the respective budgetary comparison for the General Fund and the State Public School Fund for the year then ended in conformity with accounting principles generally accepted in the United States of America.

- 2 -

In accordance with Government Auditing Standards, we have also issued our report dated December 18, 2010 on our consideration of the Guilford County Board of Education’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. Accordingly, we express no such opinion. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit. Management’s Discussion and Analysis on pages 3 through 15 is not a required part of the basic financial statements but is supplementary information required by accounting principals generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it. Our audit was conducted for the purpose of forming an opinion on the financial statements that collectively comprise the basic financial statements of the Guilford County Board of Education. The combining and individual nonmajor fund financial statements and schedules, as well as the accompanying schedule of expenditures of federal and state awards as required by U. S. Office of Management and Budget Circular A-133, Audits of States, Local Governments and Non-Profit Organizations, and the State Single Audit Implementation Act, and other schedules listed in the table of contents are presented for purposes of additional analysis and are not a required part of the basic financial statements. Such information has been subjected to the auditing procedures applied in our audit of the basic financial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financial statements taken as a whole. The introductory and statistical sections listed in the table of contents have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we express no opinion on them.

December 18, 2010

- 3 -

Management’s Discussion and Analysis This section of the Guilford County Board of Education’s (the Board) financial report represents our discussion and analysis of the financial performance of the Board for the year ended June 30, 2010. This information should be read in conjunction with the audited financial statements included in this report. Financial Highlights The district’s average daily membership (ADM) decreased by 258 students (or .4%) from the previous year.

[ADM is calculated by dividing the number of students enrolled each school day (whether in attendance or not) by the number of school days.] In the past decade our student enrollment has increased by more than 8,800 students.

The Board’s total net assets increased 3.3% during the year due primarily because of the increase in capital assets in the governmental activities due to new school construction and/or major renovation projects associated with the district’s Capital Improvement Plan (CIP). The CIP was designed to create permanent classroom seats to accommodate growing student enrollment; to provide technology for the education program; to air-condition schools where air-conditioning was lacking; and to make efficient utilization of all facilities.

Total fund balance in the district’s General Fund increased from $11.7 million at June 30, 2009 to $14.2 million at June 30, 2010. Undesignated fund balance remained at zero as of June 30, 2010. The increase in the total fund balance is due to the Board of Education’s decision to set aside $3 million in the 2009-10 budget to fund a possible state budget cut or spending freeze. Fortunately, it was not necessary to draw on the $3 million in 2009-10 so those dollars are included in the total fund balance of the General Fund at June 30, 2010. The Board did designate those dollars to be included in the 2010-11 budget.

The American Recovery and Reinvestment Act of 2009 (ARRA), signed into law by President Obama on February 17, 2009, provides approximately $100 billion for education. The ARRA expenditures included in this report total approximately $31.8 million. Of that amount, nearly $31.2 million or 98.2%, is comprised of the following three components of ARRA education funding: the State Fiscal Stabilization Fund (SFSF), Title I, Part A of the Elementary and Secondary Education Act (Title I), and Title VI, Part B of the Individuals with Disabilities Education Act (IDEA).

GCS was able to save 964 jobs, or approximately 750-full-time equivalent positions, as a result of having access to ARRA funds in 2009-10: 836-school-based custodians, school treasurers, NC WISE data managers, office support

(guidance/attendance/registrar), etc, jobs were funded with SFSF dollars; 30 positions were funded with ARRA Title I funds; and 98 positions serving children with special needs were funded ARRA Title VI-B funds.

Four principles guide the distribution and use of ARRA funds:

(a) Spend funds quickly to save and create jobs

(b) Improve student achievement through school improvement and reform ARRA funds should be used to close the achievement gap, help students from all backgrounds

achieve high standards, and address four specific areas that are authorized under bipartisan

- 4 -

education legislation – including the Elementary and Secondary Education Act and the America Competes Act of 2007:

1. Making progress toward rigorous college- and career-ready standards and high-quality assessments that are valid and reliable for all students, including English language learners and students with disabilities;

2. Establishing pre-K-to college and career data systems that track progress and foster continuous improvement;

3. Making improvements in teacher effectiveness and in the equitable distribution of qualified teachers for all students, particularly students who are most in need; and

4. Providing intensive support and effective interventions for the lowest-performing schools.

(c) Ensure transparency, reporting and accountability To prevent fraud and abuse, support the most effective uses of ARRA funds, and accurately

measure and track results, recipients must publicly report on how funds are used. Due to the unprecedented scope and importance of this investment, ARRA funds are subject to additional and more rigorous reporting requirements than normally apply to grant recipients.

(d) Invest one-time ARRA funds thoughtfully to minimize the "funding cliff"

ARRA represents a historic infusion of funds that is expected to be temporary. Depending on the program, these funds are available for only two to three years (2008-09 through 2010-11). These funds should be invested in ways that do not result in unsustainable continuing commitments after the funding expires.

The 2009-10 county appropriation to the capital outlay fund was $4 million - $3 million less than was

appropriated in the previous fiscal year. Therefore, on July 23, 2009, the Board of Education approved utilizing $1,169,189 in local red light camera citation proceeds to fund the following 2009-10 capital outlay items: $759,189 for school-based instructional equipment allotments $60,000 for replacement of band uniforms/instruments $50,000 for district-wide equipment/furniture replacement (primarily school-based) $300,000 for the district’s school technology plan

Per NCGS 115C-102.6, each local school district is required to submit an updated technology plan to the North Carolina Department of Public Instruction that is written to support and enhance the following defined priorities: globally competitive students 21st Century professionals healthy and responsible students leadership that will guide innovation 21st Century systems

Subsequently, on August 20, 2009, the county commissioners approved a Board of Education request to

amend/increase the Board’s 2009-10 capital outlay budget by the $1,169,189 in local red light camera citation proceeds. This report reflects the transfer of $1,169,189 to the Capital Outlay Fund from the General Fund.

In 2009-10 Guilford County Schools established a special revenue fund to account for reimbursements,

including fees for actual costs, gifts and grants restricted as to use, trust funds, federal appropriations made

- 5 -

directly to local school administrative units, funds received for prekindergarten programs, and special programs.

On May 6 2008, Guilford County residents also approved an additional $412 million in school bonds. The package contains 27 projects, which include five new schools and 6,571 new student seats. Thirteen schools will receive major renovations and additions. Projects included in the bond are prioritized with 93.5 percent of the request relieving overcrowding, 3.5 percent targeting repairs and renovations and 3 percent improving heating and air conditioning systems district wide. Projects included in the May 2008 $412 million school bonds are:

Jamestown Middle School - Funding for new 1,112 student replacement school on new site (site

has been purchased) Ragsdale High School - Combine existing Jamestown MS with Ragsdale HS and add new gym and

media center Ragsdale Autism Wing - Autism wing at Ragsdale High School for 48 students Special Education Center West - Additional funding to be added to current funding Southeast High School - New classrooms, media center and gymnasium addition Alamance Elementary School - Addition, demolition and renovations to convert to 700 student

elementary school Summerfield Elementary School - New classrooms and media center addition including expansion

of the dining room Southwest High School - New classrooms, media center and gymnasium addition Southeast Area Elementary School - New 700 student school in Southeast area Southeast Area Autism Wing - Autism Wing at Southeast Area Elementary School for 48 students Allen Middle School - New classrooms and auxiliary gym addition Southeast Middle School - New media center, auxiliary gym and dining room expansion. Convert

existing media center to classrooms North Greensboro Area Elementary School - New 700 student school to help relieve Jesse

Wharton and Brightwood areas Grimsley High School - New cafeteria addition, renovate main gym and Jameson Stadium; convert

existing cafeteria to classrooms Airport Area High School - New high school facilities in airport area for 1,200 students Airport Area Autism Wing - Autism wing at Airport Area High School for 48 students Airport Middle School Land - Purchase land for future airport area middle school Northwest Middle School - New auxiliary gym and classrooms addition Allen Jay Middle School - Renovation of existing facility for use as a small middle school Dudley High School - Renovation of existing English building for use as additional classrooms Dudley High School (athletics) - Funding to improve athletic facilities including football stadium Mobile Classrooms - Relocation costs for mobile classrooms at construction projects High Point Central High School - Lighting system/technology upgrades and renovations to main

gym McLeansville Elementary School - Classrooms addition and media center expansion Northwest High School (site & athletics) - Site improvements for traffic control and

improvements to athletic facilities Simeon Stadium - Funding to improve athletic facilities including new lighting Tracks - Systemwide improvements to high school running tracks Tennis Courts - Systemwide improvements and additions to high school tennis courts HVAC - Systemwide improvements to heating and air conditioning systems Page HS (athletics) - Funding to improve athletic facilities

- 6 -

It is important to note that the Board of Education has no tax levying authority; therefore, bond debt is issued and reported by Guilford County while the capital assets and associated depreciation are reported by the Guilford County Board of Education.

Overview of the Financial Section The audited financial statements of the Guilford County Board of Education consist of four components. They are as follows: Independent Auditors’ Report; Management's Discussion and Analysis (required supplementary information); Basic Financial Statements; and Supplemental section that presents combining and budgetary statements for non-major governmental

funds and budgetary statements for major governmental and enterprise funds. The Basic Financial Statements include two types of statements that present different views of the Board’s finances. The first is the government-wide statements. The government-wide statements are presented on the full accrual basis of accounting and include the statement of net assets and the statement of activities. The Statement of Net Assets includes all of the Board’s assets and liabilities. Assets and liabilities are classified in the order of relative liquidity for assets and due date for liabilities. This statement provides a summary of the Board's investment in assets and obligations to creditors. Liquidity and financial flexibility can be evaluated using the information contained in this statement. The Statement of Activities summarizes the Board’s revenues and expenses for the current year. A net (expense) revenue format is used to indicate to what extent each function is self-sufficient. The second set of statements included in the basic financial statements is the fund financial statements, which is presented for the Board’s governmental funds, proprietary funds, and fiduciary funds. These statements present the governmental funds on the modified accrual basis of accounting, measuring the near term inflows and outflows of financial resources and what is available at year end to spend in the next fiscal year. The proprietary and fiduciary funds are presented on the full accrual basis of accounting. The fund financial statements focus on the Board’s most significant funds. Because a different basis of accounting is used in the government wide statements, reconciliation from the governmental fund financial statements to the government-wide statements is required. The government-wide statements provide information about the Board as an economic unit while the fund financial statements provide information on the financial resources of each of the Board’s major funds. Government-Wide Statements The government-wide statements report information about the unit as a whole using accounting methods similar to those used by private-sector companies. The Statement of Net Assets includes all of the Board’s assets and liabilities, except for fiduciary fund assets and liabilities. All of the current year’s revenues and expenses are accounted for in the statement of activities regardless of when cash is received or paid. The two government-wide statements report the Board’s net assets and how they have changed. Net assets – the difference between the board’s assets and liabilities – is one way to measure the unit’s financial health or position. Over time, increases or decreases in the Board’s net assets are an indicator of whether its financial

position is improving or deteriorating. To assess the district’s overall health, factors such as the condition of its school buildings and other

physical assets must also be considered. The unit’s activities are divided into two categories in the government-wide statements:

- 7 -

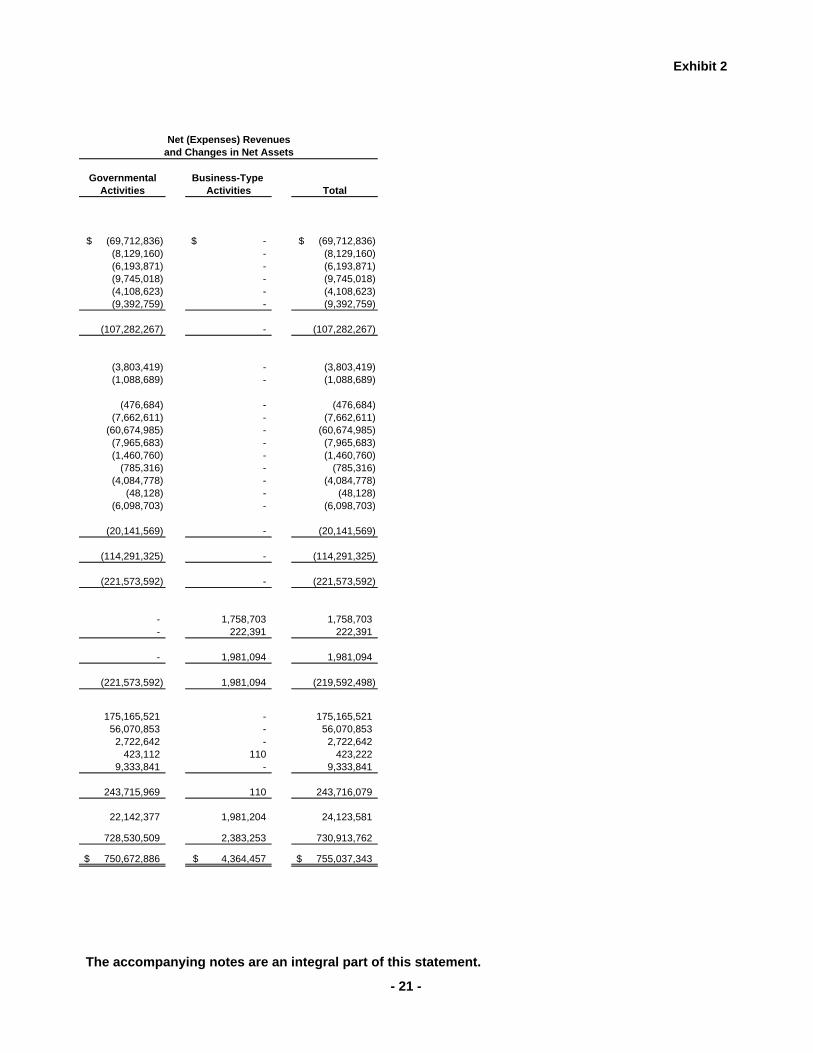

Governmental activities: Most of the Board’s basic services are included here, such as regular and special education, transportation, and administration. County funding and state and federal aid finance most of these activities.

Business-type activities: The Board charges fees to help it cover the costs of certain services it provides. School Food Service and After-School Care Enrichment Services are included here.

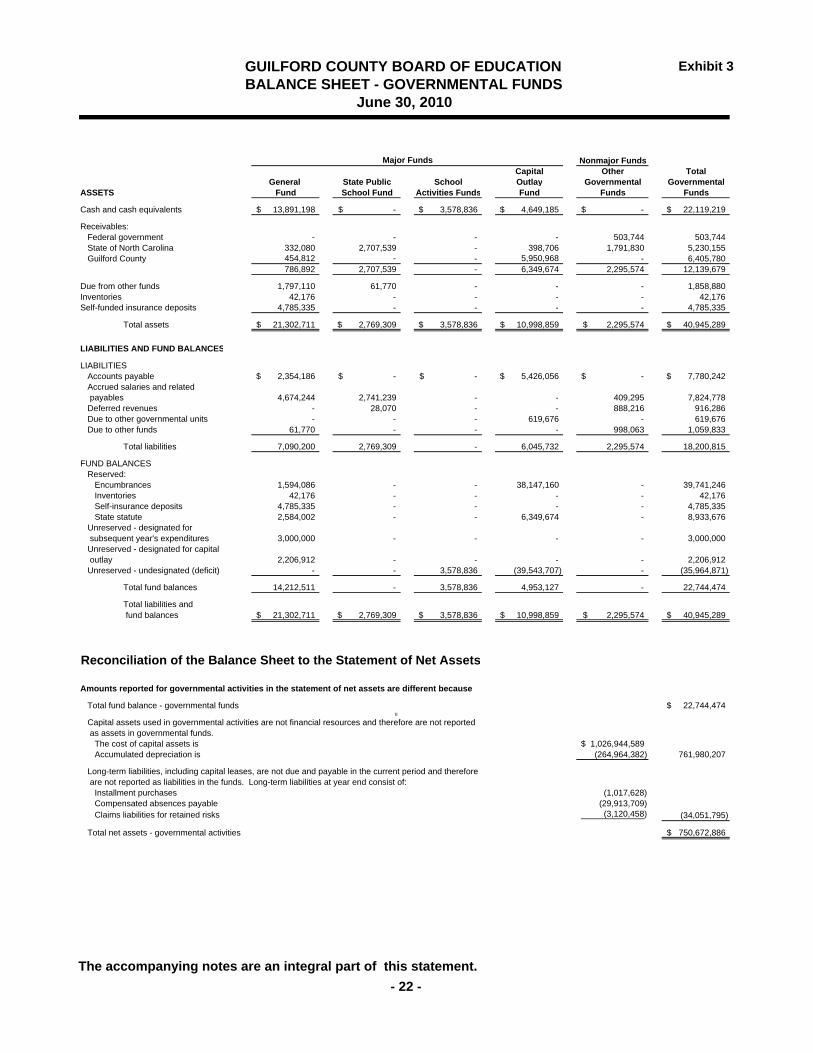

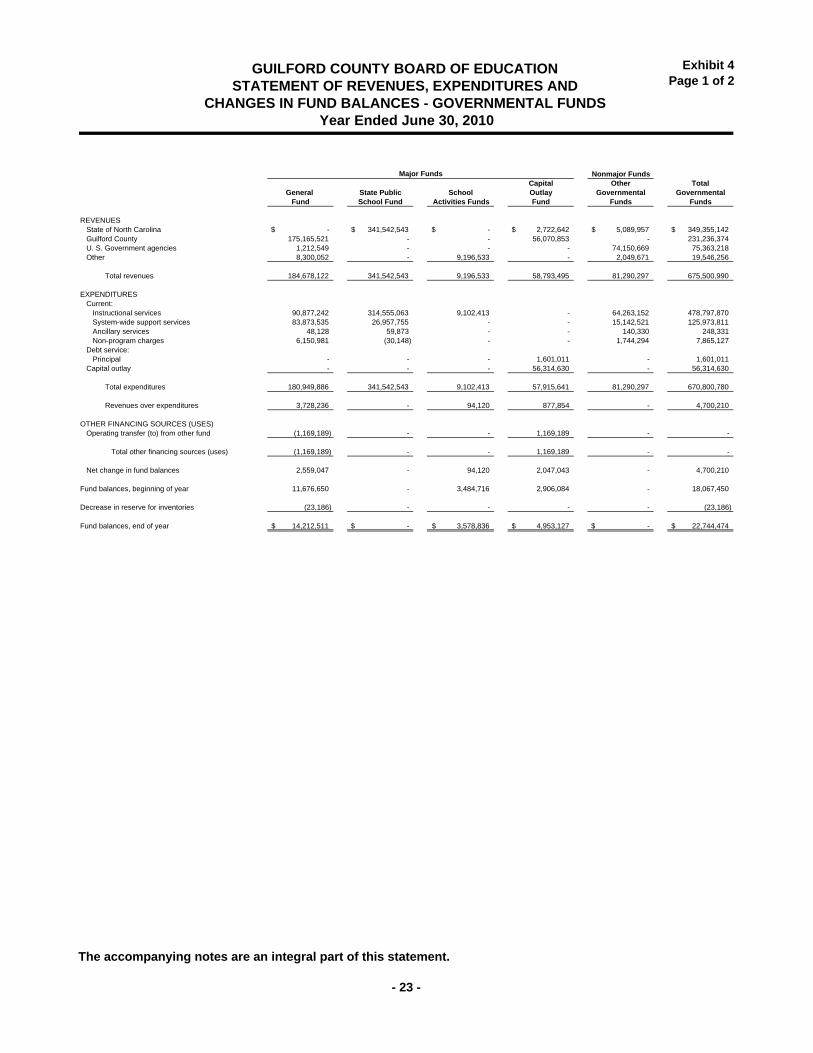

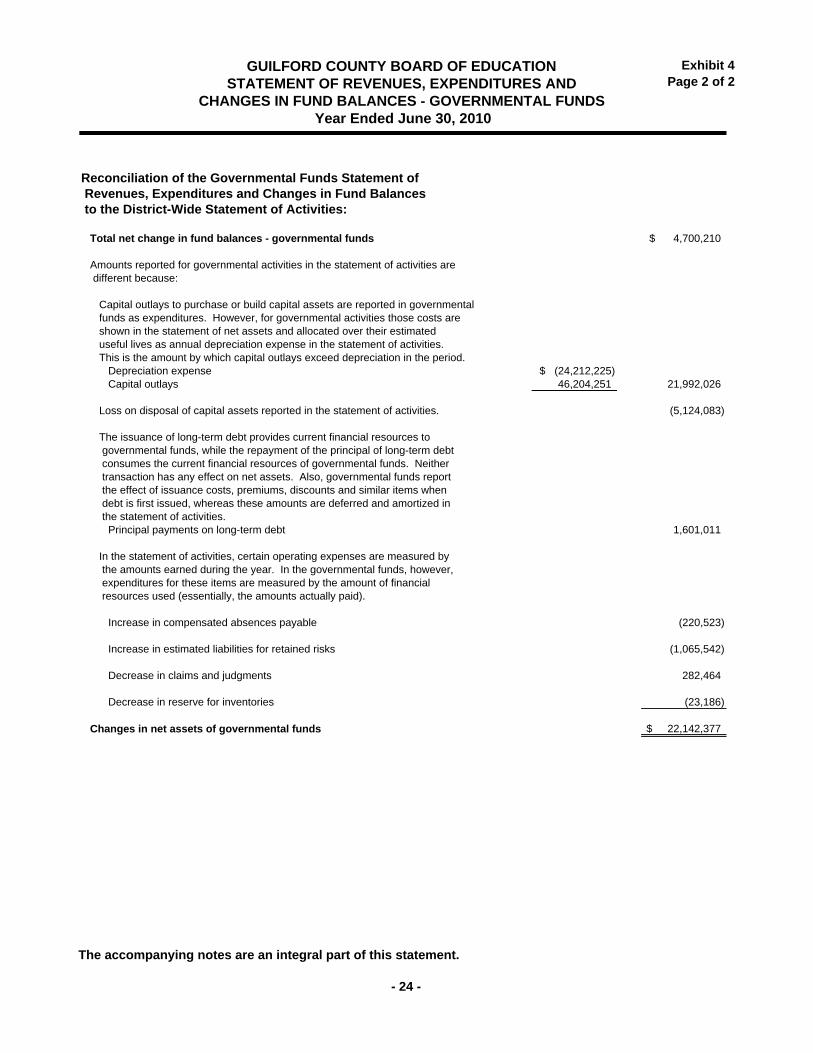

The government-wide statements are shown as Exhibits 1 and 2 of this report. Fund Financial Statements The fund financial statements provide more detailed information about the Board’s funds, focusing on its most significant or “major” funds – not the unit as a whole. Funds are accounting devices the Board uses to keep track of specific sources of funding and spending on particular programs. Some funds are required by State law, such as the State Public School Fund. The Board has established other funds to control and manage money for a particular purpose or to show

that it is properly using certain revenues, such as in the Federal Grants fund. Guilford County Board of Education has three types of funds: governmental funds, proprietary funds, and fiduciary funds. Governmental funds: Most of the Board’s basic services are included in the governmental funds, which generally focus on two things – how cash and other assets can readily be converted to cash flow in and out, and the balances left at year end that are available for spending. As a result of this focus, the governmental funds statements provide a detailed short-term view that helps the reader determine whether there are more or fewer financial resources that can be spent in the coming year to finance the Board’s programs. Because this information does not encompass the additional long-term focus of the government-wide statements, additional information at the bottom of the governmental funds statements, in the form of a reconciliation, explains the relationship (or differences) between the government-side and the fund financial statements. The district has several governmental funds: the General Fund, the State Public School Fund, the Capital Outlay Fund, the Federal Grants Fund, the Special Revenue Fund, and the School Activity Fund. The governmental fund statements are shown as Exhibits 3, 4 and 5 of this report. Proprietary funds: Services for which the Board charges a fee are generally reported in the proprietary funds. The proprietary fund statements are reported on the same full accrual basis of accounting as the government-wide statements. Guilford County Board of Education has two proprietary funds – both enterprise funds – the School Food Service Fund and the After School Care Enrichment Services Fund. The proprietary fund statements are shown as Exhibits 6, 7, and 8 of this report. Fiduciary funds: Fiduciary funds are used to account for resources held for the benefit of parties outside the government. The Board serves as a trustee, or fiduciary, for ten scholarships. All of the Board’s fiduciary activities are reported in a separate Statement of Fiduciary Net Assets and a separate Statement of Changes in Fiduciary Net Assets. We exclude these activities from the Board’s other financial statements because the Board cannot use these assets to finance its operations. The Board is responsible for ensuring that the assets reported in these funds are used for their intended purposes and by those to whom the assets belong. This is accounted for as a private purpose trust fund. The fiduciary fund statements are shown as Exhibits 9 and 10 of this report.

- 8 -

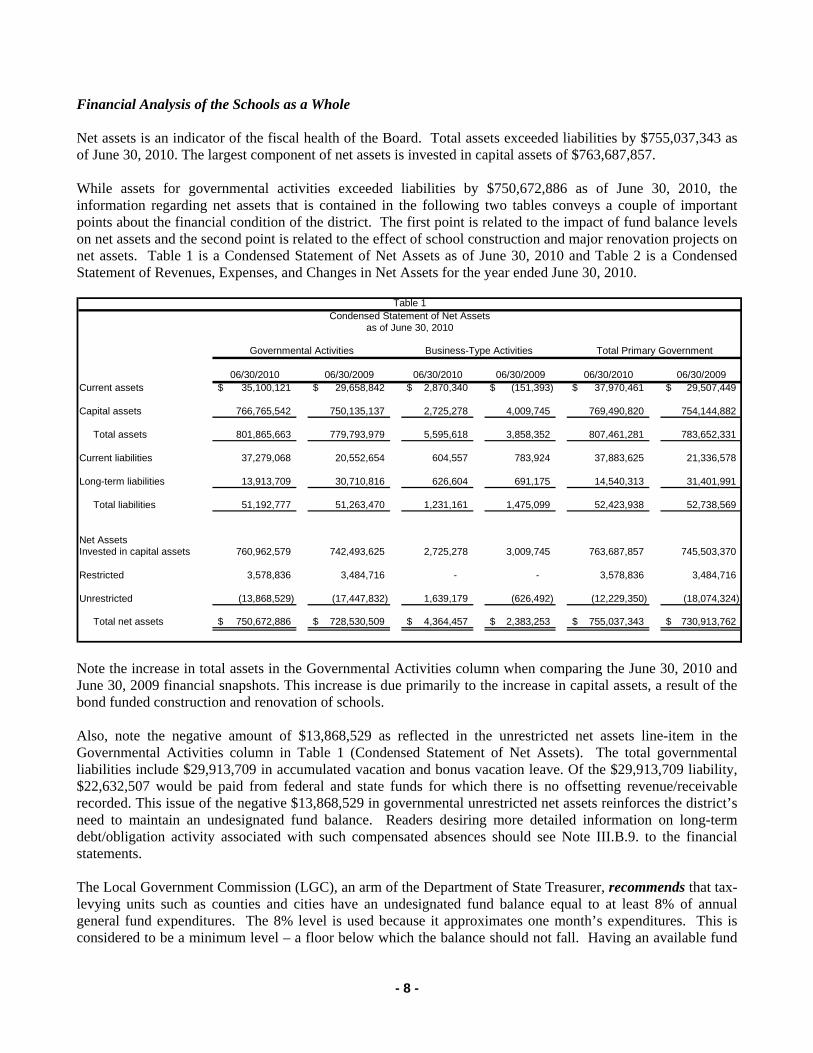

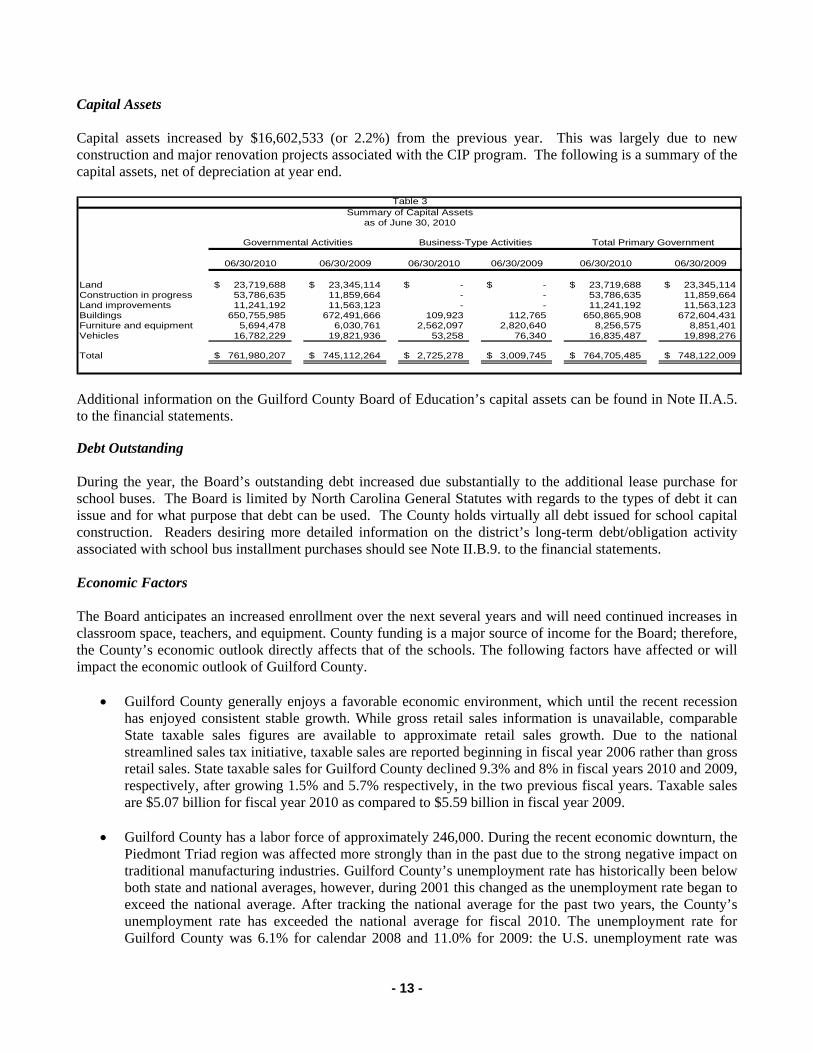

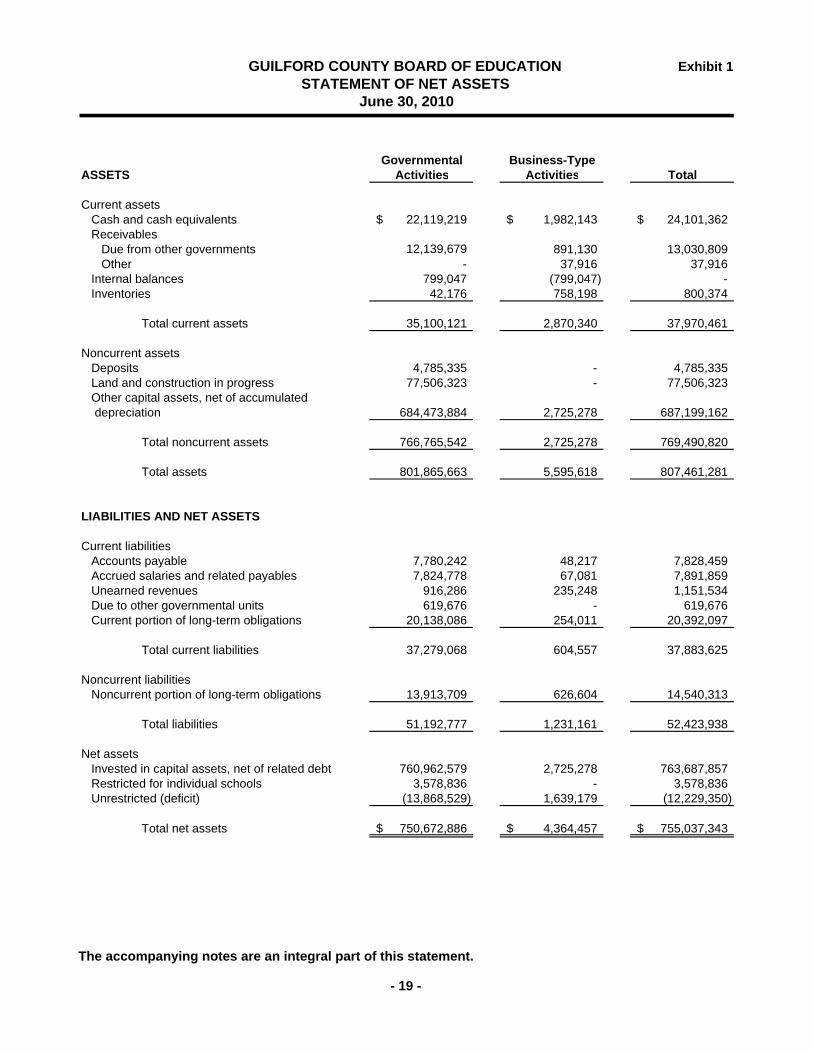

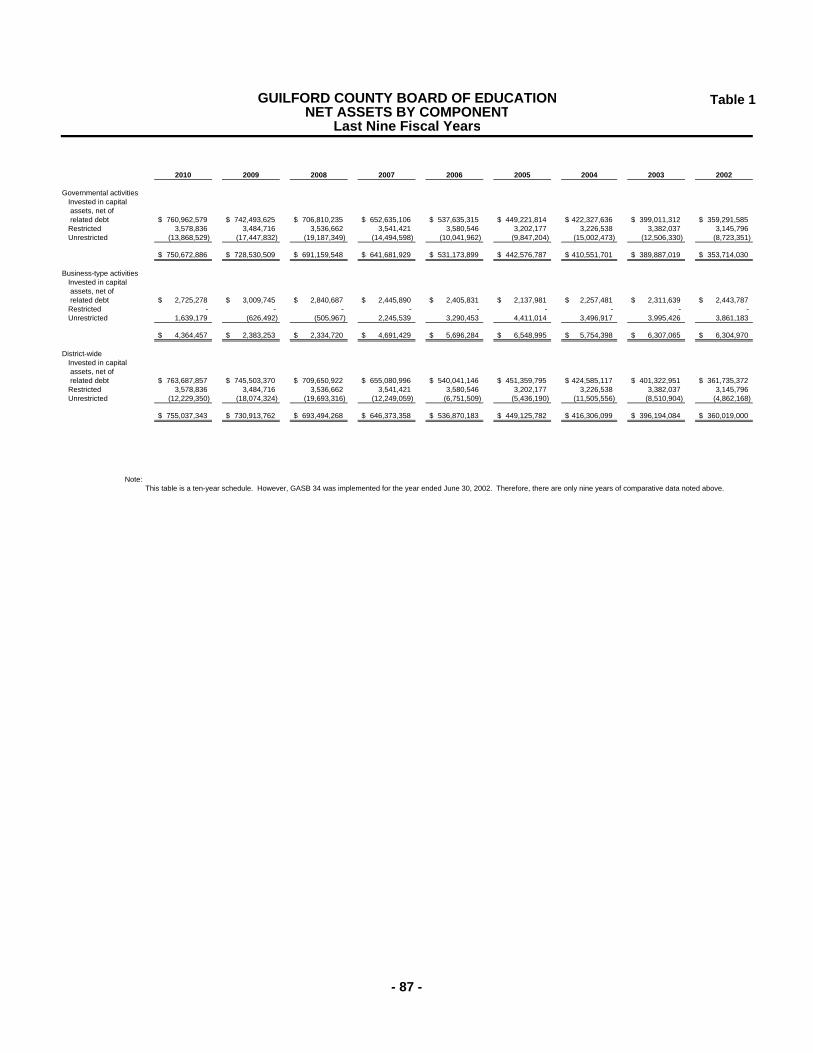

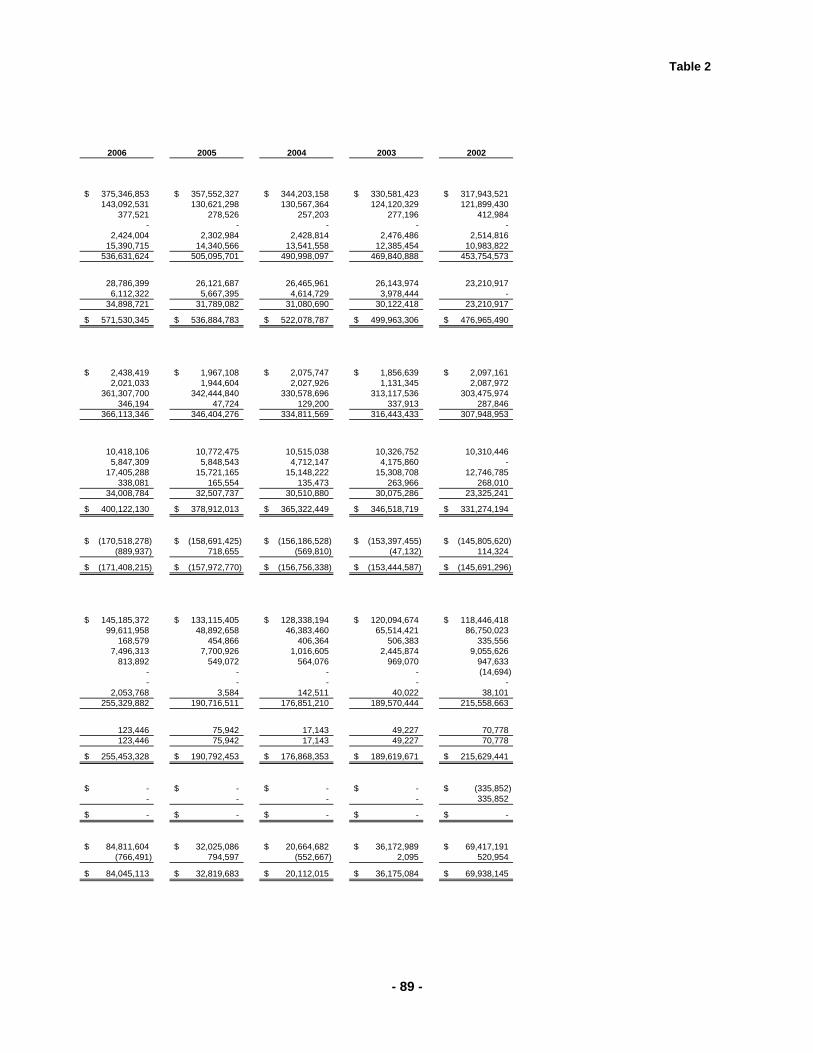

Financial Analysis of the Schools as a Whole Net assets is an indicator of the fiscal health of the Board. Total assets exceeded liabilities by $755,037,343 as of June 30, 2010. The largest component of net assets is invested in capital assets of $763,687,857. While assets for governmental activities exceeded liabilities by $750,672,886 as of June 30, 2010, the information regarding net assets that is contained in the following two tables conveys a couple of important points about the financial condition of the district. The first point is related to the impact of fund balance levels on net assets and the second point is related to the effect of school construction and major renovation projects on net assets. Table 1 is a Condensed Statement of Net Assets as of June 30, 2010 and Table 2 is a Condensed Statement of Revenues, Expenses, and Changes in Net Assets for the year ended June 30, 2010.

06/30/2010 06/30/2009 06/30/2010 06/30/2009 06/30/2010 06/30/2009Current assets 35,100,121$ 29,658,842$ 2,870,340$ (151,393)$ 37,970,461$ 29,507,449$

Capital assets 766,765,542 750,135,137 2,725,278 4,009,745 769,490,820 754,144,882

Total assets 801,865,663 779,793,979 5,595,618 3,858,352 807,461,281 783,652,331

Current liabilities 37,279,068 20,552,654 604,557 783,924 37,883,625 21,336,578

Long-term liabilities 13,913,709 30,710,816 626,604 691,175 14,540,313 31,401,991

Total liabilities 51,192,777 51,263,470 1,231,161 1,475,099 52,423,938 52,738,569

Net AssetsInvested in capital assets 760,962,579 742,493,625 2,725,278 3,009,745 763,687,857 745,503,370

Restricted 3,578,836 3,484,716 - - 3,578,836 3,484,716

Unrestricted (13,868,529) (17,447,832) 1,639,179 (626,492) (12,229,350) (18,074,324)

Total net assets 750,672,886$ 728,530,509$ 4,364,457$ 2,383,253$ 755,037,343$ 730,913,762$

Table 1Condensed Statement of Net Assets

as of June 30, 2010

Total Primary GovernmentBusiness-Type ActivitiesGovernmental Activities

Note the increase in total assets in the Governmental Activities column when comparing the June 30, 2010 and June 30, 2009 financial snapshots. This increase is due primarily to the increase in capital assets, a result of the bond funded construction and renovation of schools. Also, note the negative amount of $13,868,529 as reflected in the unrestricted net assets line-item in the Governmental Activities column in Table 1 (Condensed Statement of Net Assets). The total governmental liabilities include $29,913,709 in accumulated vacation and bonus vacation leave. Of the $29,913,709 liability, $22,632,507 would be paid from federal and state funds for which there is no offsetting revenue/receivable recorded. This issue of the negative $13,868,529 in governmental unrestricted net assets reinforces the district’s need to maintain an undesignated fund balance. Readers desiring more detailed information on long-term debt/obligation activity associated with such compensated absences should see Note III.B.9. to the financial statements. The Local Government Commission (LGC), an arm of the Department of State Treasurer, recommends that tax-levying units such as counties and cities have an undesignated fund balance equal to at least 8% of annual general fund expenditures. The 8% level is used because it approximates one month’s expenditures. This is considered to be a minimum level – a floor below which the balance should not fall. Having an available fund

- 9 -

balance that is less than the recommended minimum for tax-levying units could have an adverse impact on a unit’s credit rating, causing it to pay more in interest when issuing bonds. For units such as school districts which do not levy taxes, the LGC makes no recommendation(s) with respect to undesignated fund balance levels. The Budgeting section of the North Carolina Department of State Treasurer Policies Manual indicates that “the appropriate level of fund balance for non tax levying units is likely to be dependent upon the frequency and amount of funding received from State, federal and other sources”. In an article entitled “Fund Balance in Local Government Budgeting and Finance” authored by Lee Carter and A. John Vogt that appeared in the Winter 1989 edition of Popular Government, Carter and Vogt write that “school systems do not need available operating fund balances as large as those of counties and cities for several reasons. First, school systems receive most of their operating revenues in monthly installments or as needed to match cash disbursements and therefore do not need large balances to cover cash-flow shortfalls. Second, if a school system confronts an unexpected need requiring expenditures in excess of its available balance, it can turn for additional funds to the county, which is responsible for providing them if the need is legitimate. Third, because counties, not school systems, issue bonds for school capital improvement projects, the bond rating agencies do not rate the school systems”. At the time the article was published, Carter was the assistant director of the Fiscal Management Section, State and Local Government Finance Division, North Carolina Department of State Treasurer and Vogt was a faculty member of the Institute of Government at the University of North Carolina at Chapel Hill specializing in budgeting and finance. While we do not dispute the reasoning cited above regarding counties and cities needing sufficient levels of fund balance in order to maintain favorable credit/bond ratings, the fiscal reality in Guilford County is such that the second reason cited above for schools to maintain a lesser amount of fund balance (turning to the county for additional funds) is problematic if not impossible. Previous fiscal policy decisions and financial/economic conditions such as those that existed in recent history and those with which we are currently faced have rendered available county fund balance figures that hover within a percentage point or two of the LGC’s recommended minimums. Per the Letter of Transmittal in the Comprehensive Annual Financial Report of Guilford County, North Carolina for the year ended June 30, 2008, the unreserved, undesignated fund balance of the County’s general fund at fiscal year end stood at only 8.6% of the subsequent year’s budget. Therefore, if circumstances such as war in the middle east and/or soaring fuel/gas prices cause the district to need a substantial amount of additional funding for heating and/or transportation purposes, the minimum undesignated fund balance level of 8% as established by the Guilford County Board of County Commissioners in concert with the LGC guideline would, in all likelihood, prohibit the appropriation of any such additional funds despite the legitimacy of the request. A small fund balance limits the ability of a school system to meet emergency or unforeseen needs; limits investment earnings on available funds thus forcing increased reliance on county tax dollars; and increases the probability of a school system reducing services due to revenue shortfalls such as cuts in state and/or federal funding.

- 10 -

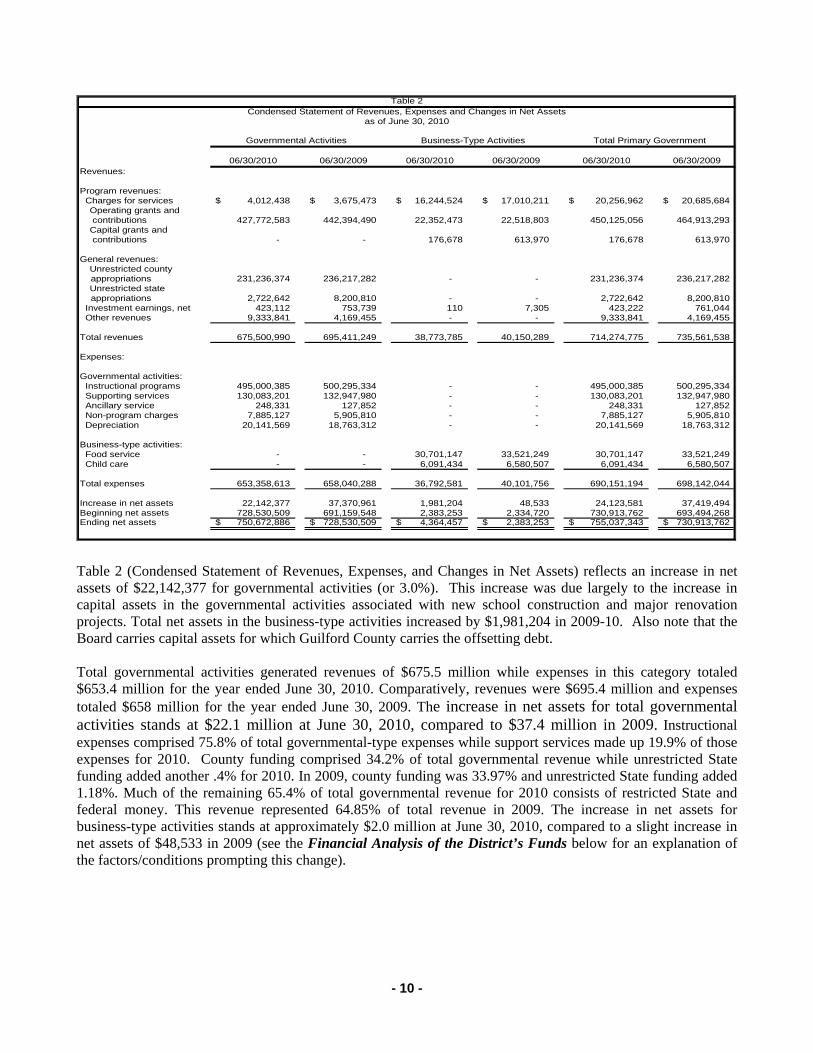

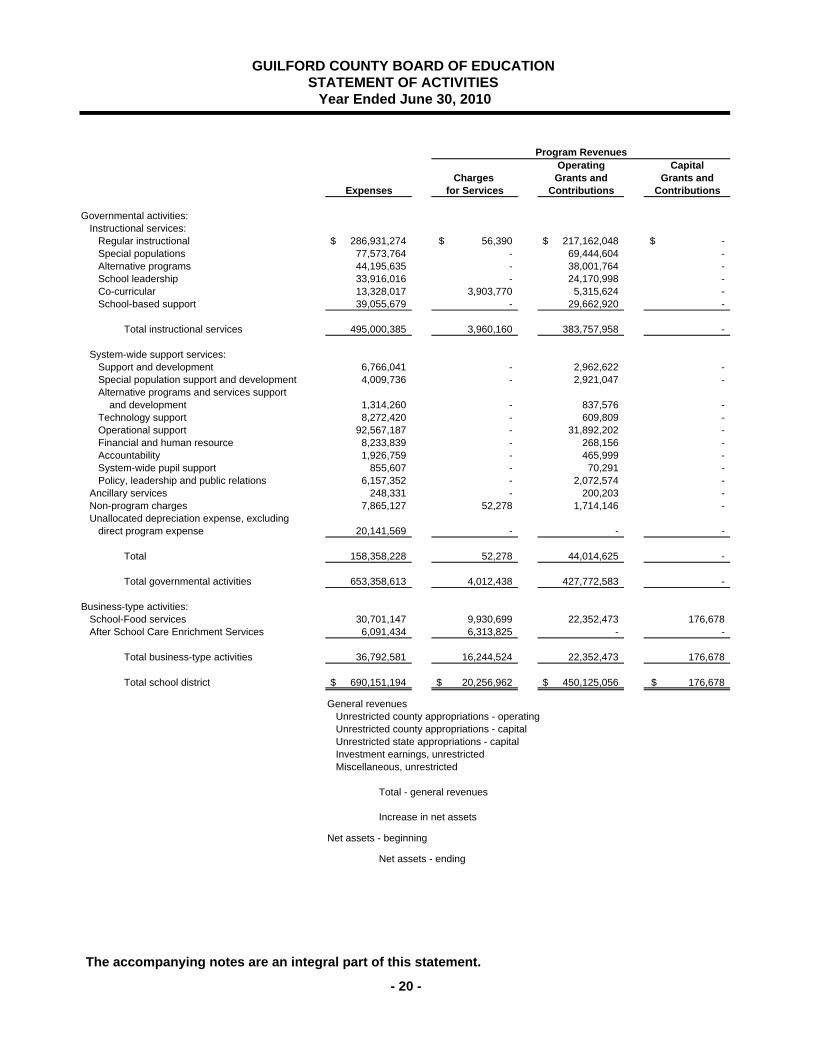

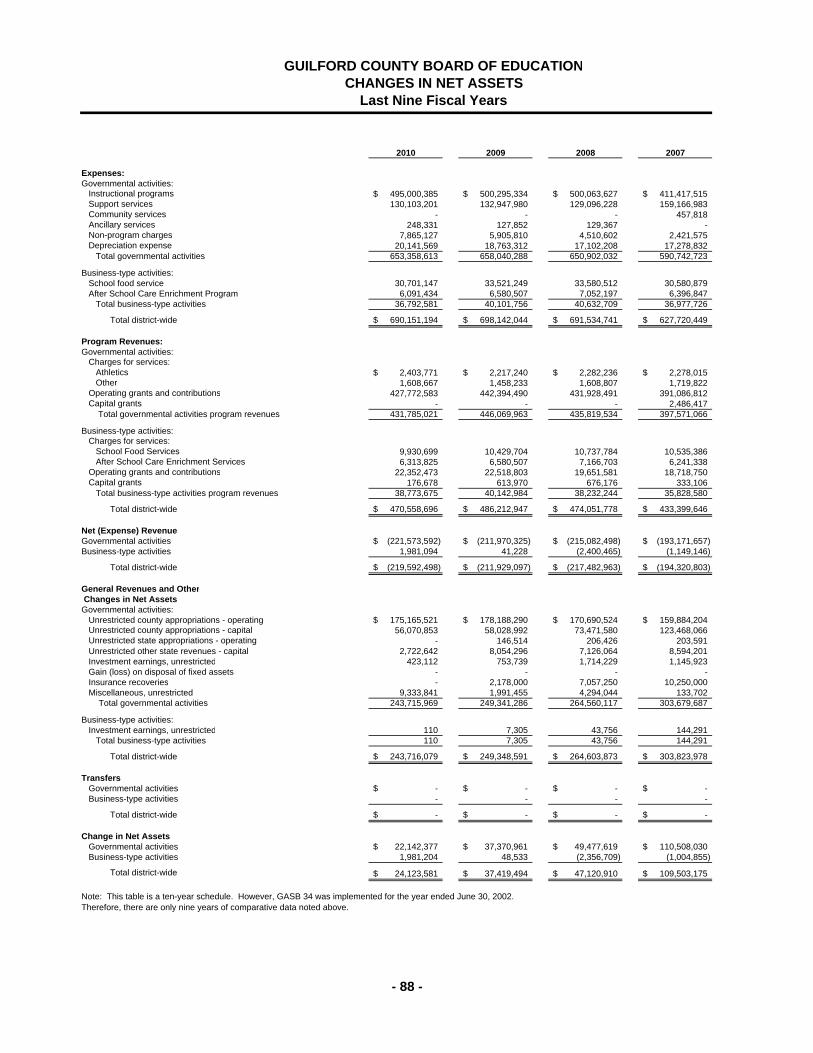

06/30/2010 06/30/2009 06/30/2010 06/30/2009 06/30/2010 06/30/2009Revenues:

Program revenues: Charges for services 4,012,438$ 3,675,473$ 16,244,524$ 17,010,211$ 20,256,962$ 20,685,684$

Operating grants and contributions 427,772,583 442,394,490 22,352,473 22,518,803 450,125,056 464,913,293 Capital grants and contributions - - 176,678 613,970 176,678 613,970

General revenues:Unrestricted county

appropriations 231,236,374 236,217,282 - - 231,236,374 236,217,282 Unrestricted state

appropriations 2,722,642 8,200,810 - - 2,722,642 8,200,810 Investment earnings, net 423,112 753,739 110 7,305 423,222 761,044 Other revenues 9,333,841 4,169,455 - - 9,333,841 4,169,455

Total revenues 675,500,990 695,411,249 38,773,785 40,150,289 714,274,775 735,561,538

Expenses:

Governmental activities: Instructional programs 495,000,385 500,295,334 - - 495,000,385 500,295,334 Supporting services 130,083,201 132,947,980 - - 130,083,201 132,947,980 Ancillary service 248,331 127,852 - - 248,331 127,852 Non-program charges 7,885,127 5,905,810 - - 7,885,127 5,905,810 Depreciation 20,141,569 18,763,312 - - 20,141,569 18,763,312

Business-type activities: Food service - - 30,701,147 33,521,249 30,701,147 33,521,249 Child care - - 6,091,434 6,580,507 6,091,434 6,580,507

Total expenses 653,358,613 658,040,288 36,792,581 40,101,756 690,151,194 698,142,044

Increase in net assets 22,142,377 37,370,961 1,981,204 48,533 24,123,581 37,419,494 Beginning net assets 728,530,509 691,159,548 2,383,253 2,334,720 730,913,762 693,494,268 Ending net assets 750,672,886$ 728,530,509$ 4,364,457$ 2,383,253$ 755,037,343$ 730,913,762$

Table 2Condensed Statement of Revenues, Expenses and Changes in Net Assets

as of June 30, 2010

Total Primary GovernmentBusiness-Type ActivitiesGovernmental Activities

Table 2 (Condensed Statement of Revenues, Expenses, and Changes in Net Assets) reflects an increase in net assets of $22,142,377 for governmental activities (or 3.0%). This increase was due largely to the increase in capital assets in the governmental activities associated with new school construction and major renovation projects. Total net assets in the business-type activities increased by $1,981,204 in 2009-10. Also note that the Board carries capital assets for which Guilford County carries the offsetting debt. Total governmental activities generated revenues of $675.5 million while expenses in this category totaled $653.4 million for the year ended June 30, 2010. Comparatively, revenues were $695.4 million and expenses totaled $658 million for the year ended June 30, 2009. The increase in net assets for total governmental activities stands at $22.1 million at June 30, 2010, compared to $37.4 million in 2009. Instructional expenses comprised 75.8% of total governmental-type expenses while support services made up 19.9% of those expenses for 2010. County funding comprised 34.2% of total governmental revenue while unrestricted State funding added another .4% for 2010. In 2009, county funding was 33.97% and unrestricted State funding added 1.18%. Much of the remaining 65.4% of total governmental revenue for 2010 consists of restricted State and federal money. This revenue represented 64.85% of total revenue in 2009. The increase in net assets for business-type activities stands at approximately $2.0 million at June 30, 2010, compared to a slight increase in net assets of $48,533 in 2009 (see the Financial Analysis of the District’s Funds below for an explanation of the factors/conditions prompting this change).

- 11 -

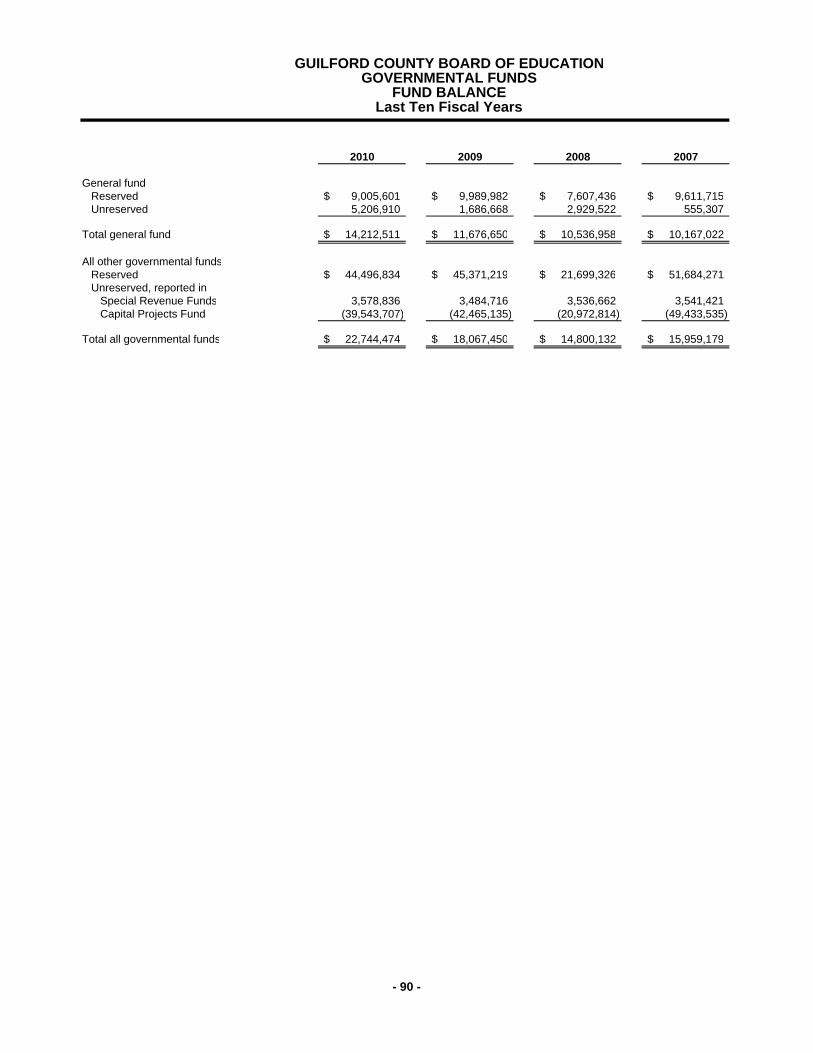

Financial Analysis of the District’s Funds Governmental Funds: The focus of the Board’s governmental funds is to provide information on near-term inflows, outflows, and balances of usable resources. Such information is useful in assessing the Board’s financing requirements. The Board’s governmental funds (general, state, federal, capital outlay and individual school funds) reported a combined fund balance of $22.7 million, an increase of approximately $4.7 million from last year. This increase was created primarily by a $2.5 million increase in the fund balance of the General Fund along with a $2.0 million increase in the fund balance of the Capital Outlay Fund. The increase in the General Fund fund balance is due to the Board of Education’s decision to set aside $3 million in the 2009-10 budget to fund a possible state budget cut or spending freeze. Fortunately, it was not necessary to draw on the $3 million in 2009-10 so those dollars are included in the total fund balance of the General Fund at June 30, 2010. The increase in the Capital Outlay Fund fund balance is due to unspent dollars from the county appropriation and transfer from the general fund. Of the $2 million carryover, more than $715,000 was encumbered at June 30, 2010 and the remaining amount will be spent in FY2011. Proprietary Funds: As mentioned previously, the Board has two proprietary funds – both enterprise funds – the School Food Service Fund and the After School Care Enrichment Services Fund. The activity in these two funds is categorized as business-type activity because the district charges fees to help it cover the costs of services provided.

For the year ended June 30, 2010, revenues exceeded expenses in the School Food Service Fund by $1.8 million. The primary reason for this increase was Board approval of the following recommendations from staff in order for the 2009-10 School Food Service Fund operation to generate sufficient revenues to cover expenses including the assessment of indirect cost:

reduce menu/food choices (i.e., offer two versus four entrees, use 25% less whole grain products); reduce amount of processing supplies purchased (i.e., reduce use of cups for serving individual

portions); reduce or eliminate breaks in serving time schedules where appropriate/possible; reduce number of serving lines where appropriate/possible (determine number of lines based on

participation); defer computer equipment replacement at elementary schools; limit other computer equipment replacement to that deemed mission critical/emergency; allow replacement only of small wares (i.e., serving utensils, food thermometers, pans); purchase uniforms for new employees only (i.e., postpone purchasing additional set of uniforms for

existing employees); and increase lunch prices by fifty cents at elementary (increase from $1.80 to $2.30) and by thirty cents at

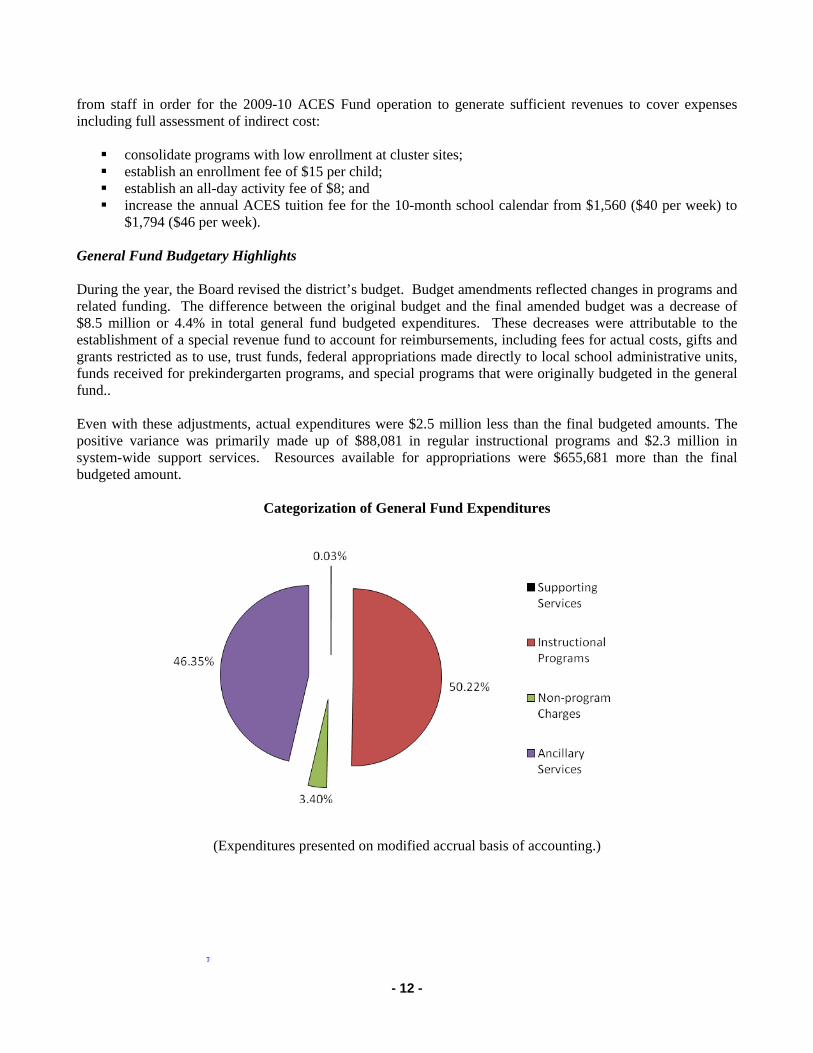

middle and high school (increase from $2.10 to $2.40 at middle school and from $2.20 to $2.50 at high school).