Embed Size (px)

Citation preview

Guide to International Financial Reporting Standards in Canada

IAS 36 Impairment of AssetsIrene Wiecek, FCPA, FCA

Martha Dunlop, FCPA, FCA

Jane Bowen, FCPA, FCA

primary editor: Alex Fisher, CPA, CA

June 2013

FINANCIAL REPORTING

CANADIAN SERIES

Guide to International Financial Reporting Standards in Canada

IAS 36 Impairment of AssetsIrene Wiecek, FCPA, FCA

Martha Dunlop, FCPA, FCA

Jane Bowen, FCPA, FCA

primary editor: Alex Fisher, CPA, CA

June 2013

CANADIAN SERIES

iiiIAS 36 Impairment of Assets

June 2013

Table of ContentsPreface 1

Introduction to IAS 36 5

Standards Update 5

Key Standards Referred to in This Publication 6

IAS 36 Definitions 7

Overview of Key Requirements 8

Analysis of Relevant Issues 10

Identifying an Asset That May Be Impaired 11

Indicators of Impairment 11

Measuring Recoverable Amount 13

Determining Recoverable Amount at the Level of the Individual Asset or CGU 15

Relief for Determination of Recoverable Amount — Certain Intangible Assets and Goodwill 18

FVLCD 20

VIU 21

CGUs and Goodwill 28

Identifying an Asset’s CGU 28

Carrying Amount 30

Goodwill 31

Corporate Assets 36

Impairment Loss for a CGU 37

Interim Financial Reporting 39

Reversing an Impairment Loss 39

Recognition, Measurement and Presentation of Impairment Loss Reversals 40

Disclosure 41

Using Present Value Techniques to Measure VIU 45

iv Guide to International Financial Reporting in Canada

Impairment Testing CGUs with Goodwill and NCIs 46

NCIs Measured as Proportionate Interest 47

Accounting Policy Choices 48

Significant Judgments and Estimates 48

APPENDIX A — Acronyms Used 50

List of ExtractsExtract 1 — Excerpt from Nexen Inc. 2012 Financial Statements Note 5B — Indicators of Impairment 12

Extract 2 — Excerpt from Suncor Energy Inc. 2012 Financial Statements Note 9 — Indicators of Impairment 12

Extract 3 — Excerpt from Royal Bank of Canada 2012 Financial Statements Note 11 — Calculation of Recoverable Amount 14

Extract 4 — Excerpt from Pizza Pizza Royalty Corp. 2012 Financial Statements Note 4 — Calculation of Recoverable Amount 14

Extract 5 — Excerpt from Metro Inc. 2012 Financial Statements Note 16 — Calculation of Recoverable Amount 18

Extract 6 — Excerpt from Air Canada 2012 Notes to Financial Statements Note 5 — Relief from Calculating Recoverable Amount 20

Extract 7 — Excerpt from Corby Distilleries Limited 2012 Notes to Financial Statements Note 12 — Inputs Used to Determine Discount Rates 25

Extract 8 — Excerpt from Air Canada 2012 Financial Statements Note 5 — Calculating VIU 26

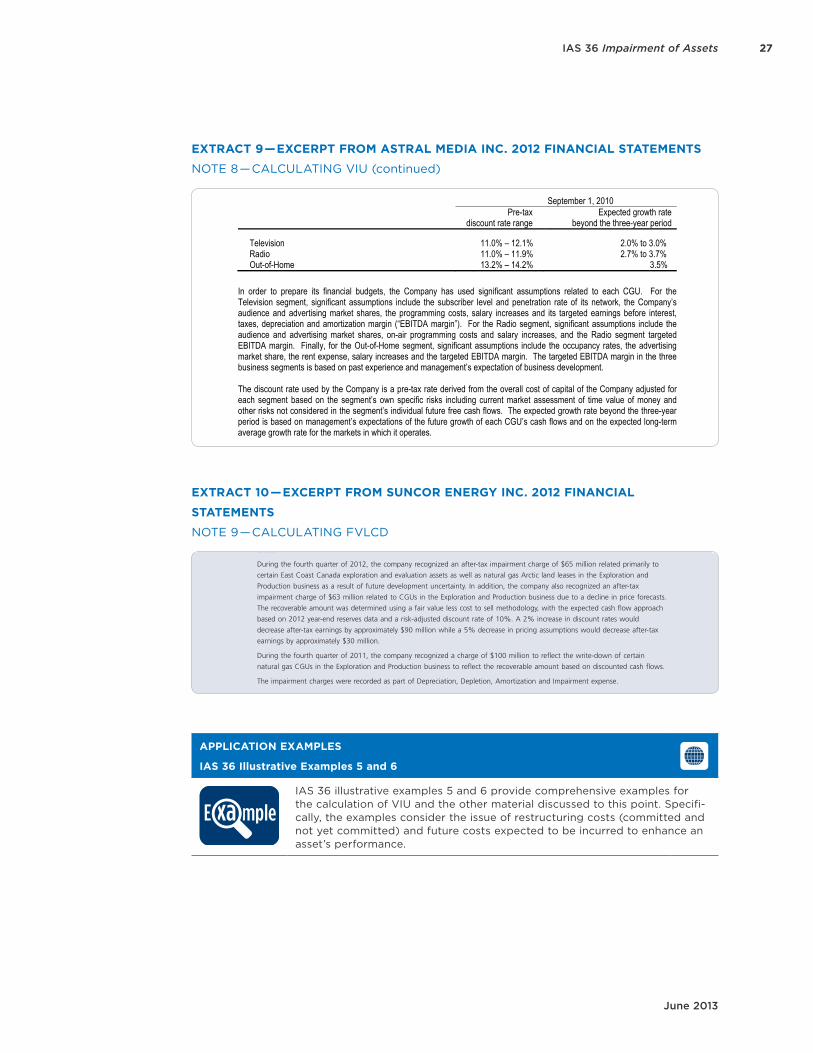

Extract 9 — Excerpt from Astral Media Inc. 2012 Financial Statements Note 8 — Calculating VIU 26

Extract 10 — Excerpt from Suncor Energy Inc. 2012 Financial Statements Note 9 — Calculating FVLCD 27

Extract 11 — Excerpt from Rona Inc. 2012 Financial Statements Note 14 — CGU Groupings 31

v

June 2013

Table of Contents

Extract 12 — Excerpt from Astral Media Inc. 2012 Financial Statements Note 8 — CGU at Lower Level Than Operating Segment 33

Extract 13 — Excerpt from Maple Leaf Foods Inc. 2012 Financial Statements Note 3 — Corporate Assets 37

Extract 14 — Excerpt from Astral Media Inc. 2012 Financial Statements Note 8 — Reversal of Impairment Loss 41

Extract 15 — Excerpt from Sherritt International Corporation 2012 Financial Statements Note 2.13 — Accounting Policy Note As It Relates to Impairments 43

Extract 16 — Excerpt from Bombardier Inc. 2012 Financial Statements Note 4 — Critical Accounting Estimates and Judgments As They Relate to Impairment Regarding Aerospace Program Tooling 44

Extract 17 — Excerpt from Bombardier Inc. 2012 Financial Statements Note 4 — Sensitivity Disclosures As They Relate to Aerospace Program Tooling 45

List of IllustrationsIllustration 1 — Some Indicators of Impairment As Noted in IAS 36 11

Illustration 2 — Decision Tree — Recoverable Amount 13

Illustration 3 — Level of Impairment Testing 17

Illustration 4 — Relief Regarding Calculation of Recoverable Amount for Indefinite-Lived Intangibles and Goodwill 19

Illustration 5 — The Difference between FVLCD and VIU 21

Illustration 6 — Calculating VIU — Cash Flows 22

Illustration 7 — Recognition and Presentation of Impairment Losses 38

Illustration 8 — Indicators of Impairment Reversal As Noted in IAS 36 39

Illustration 9 — Types of Disclosures Required by IAS 36 42

Illustration 10 — Two Approaches to Computing Present Value 45

Illustration 11 — Some Significant Judgments and Sources of Estimation Uncertainty under IAS 36 48

1

June 2013

IAS 36 Impairment of Assets

PrefaceThis publication is part of the Guide to International Financial Reporting Stan-dards in Canada series published by the Chartered Professional Accountants of Canada (CPA Canada) to support its members.

The objective of this publication, IAS 36 Impairment of Assets, is to help you understand IAS 36 and the IASB material that accompanies the standard. The publication begins with an introduction and standards update and then includes definitions, an overview chart, an analysis section, a section on accounting policies and one on significant judgments and estimates.

Every attempt has been made to use plain language and to avoid mere restatement of the IFRS standards although, where deemed necessary, specific wording from the standards is referred to.

This publication has been carefully prepared, but it necessarily contains infor-mation in summarized form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment.

The overview section takes a high-level look at the key requirements of the standard in a chart format (the Overview chart). Specific “touchstone” refer-ences to IAS 36 are included in the Overview chart to help you navigate the standard. These are not meant to be comprehensive references, rather

2 Guide to International Financial Reporting in Canada

a starting point for your research. The analysis section analyzes the more com-plex areas of the standard in more depth. Note that, where parts of the stan-dard are more straightforward, they are included in the Overview chart only as it is felt that this coverage is at a sufficient level.

Illustrations, examples and extracts have been used to explain a particular concept and/or provide insight into how the standard is applied. Financial statement note extracts have been selected to illustrate a particular point but do not necessarily represent best practices.

Several features have been included to enhance understanding as follows:

1. Illustrations, including the following:• charts• decision trees• summaries

These illustrations add value by summarizing, grouping, highlighting simi-larities/differences and working through decision processes in applying the standard.

2. Examples, including the following:• IASB Illustrative Examples excerpts — nine deal with impairments• IASB examples excerpted from the IAS 36 standard — seven are included

within IAS 36• other examples

These examples add value by showing how a particular part of the standard might be applied in a specific situation.

3. Extracts from the IASB standards, including the following:• definitions• select quotes

Even though every attempt has been made to use plain language, in some cases it has been important to use the specific wording in the standard to get a point across.

4. Extracts from financial statements — financial statements of prominent Canadian companies have been selected, including those that were recipients of the CPA Corporate Reporting Awards. The report on the Corporate Reporting Awards, including a list of winners, may be found at www.cpacanada.ca.

The extracts included illustrate a particular aspect. It may be useful to review the complete note, which may be found at www.sedar.com.

3IAS 36 Impairment of Assets

June 2013

5. Non-IFRS Interpretations Committee insights — Items discussed but not taken to the IASB agenda, referred to as NIFRICs (non-IFRICs), have been included because in some cases, they provide insights into the standard setting decision processes.

6. IFRS Discussion Group (IDG) insights — The IDG was established by the Canadian Accounting Standards Board (AcSB) in 2009. Its aim is to provide a public forum for the discussion of issues relating to IFRSs and to collect the views of Canadians experiencing issues in implementing IFRSs. These discussions are not meant to provide authoritative guidance; however, they do help clarify issues and allow interested parties to learn how others are working through their financial reporting issues and applying judgment in the application of IFRSs. These have been drawn from the publically avail-able reports of the IDG meetings. IDG meetings are recorded and audio webcasts are archived on the AcSB website (www.frascanada.ca). Discus-sants include preparers, practitioners, regulators and users of financial statements.

7. References to relevant other CPA Canada material.

8. This publication is part of a series with various publication dates. The dates have been noted on each publication.

Where necessary, icons have been used throughout the publication to refer to many of these features so the reader can easily distinguish the sources of the information.

Insight

Application insights explain, discuss and/or debate a particular IFRS application issue.

Application insights include:• Items discussed but never incorporated into the IASB

agenda are referred to as NIFRICs (non-IFRICs)• IFRS Discussion Group reports

Viewpoints

Viewpoints refer to the Viewpoints: Applying IFRSs in the Min-ing Industry or the Viewpoints: Applying IFRSs in the Oil and Gas Industry — a series of papers that addresses specific IFRS application issues.

E xa mpleExamples illustrate how a particular part of an IFRS might be applied in a specific situation.

4 Guide to International Financial Reporting in Canada

Statistics Statistics on particular IFRS application practices highlight common practices and/or application approaches.

Resources Resources include references to relevant other CPA Canada material.

DisclaimerThe authors, publisher and/or CPA Canada accept no responsibility for loss occasioned to any person acting, or refraining from acting, as a result of any material in this publication. In addition, neither the authors nor CPA Canada accept any responsibility or liability that might occur directly or indirectly as a consequence of the use, application or reliance on this material.

5IAS 36 Impairment of Assets

June 2013

Introduction to IAS 36IAS 36 seeks to ensure that an entity’s assets are not carried at more than their recoverable amount. The standard provides guidance as to when to assess impairment, how to determine the recoverable amount and when to recognize an impairment loss. It also provides guidance on reversal of impairment losses.

An asset is impaired when its carrying amount exceeds its recoverable amount. When this happens, the carrying amount of the asset is reduced to its recover-able amount. Impairment losses, other than goodwill impairment losses, may be reduced or reversed in future periods if there is a change in the estimate of the asset’s recoverable amount.

IAS 36 includes a substantial Basis for Conclusions document and nine Illustra-tive Examples. IFRIC 10 Interim Financial Reporting and Impairment deals with interim reporting and impairment.

This publication is based on the requirements of IFRS standards and inter-pretations for annual periods beginning January 1, 2013. Where appropriate for illustration purposes, certain note-disclosure examples are presented from financial statements with annual periods ending before January 1, 2013.

Standards UpdateIn May 2013, the IASB published Recoverable Amount Disclosures for Non-Financial Assets (Amendments to IAS 36). These narrow-scope amendments to IAS 36 address the disclosure of information about the recoverable amount of impaired assets if that amount is based on fair value less costs of disposal.

In developing IFRS 13, the IASB decided to amend IAS 36 to require the disclo-sure of information about the recoverable amount of impaired assets, particu-larly if that amount is based on fair value less costs of disposal. However, it came to the IASB’s attention that some of the amendments made to IAS 36 resulted in the requirement being more broadly applied than the IASB had intended. In particular, instead of requiring an entity to disclose the recoverable amount of an asset (including goodwill) or a cash-generating unit for which a material impairment loss was recognized or reversed during the reporting period, the amendment to IAS 36 requires an entity to disclose the recover-able amount of each cash-generating unit for which the carrying amount of goodwill or intangible assets with indefinite useful lives allocated to that unit is significant in comparison with the entity’s total carrying amount of goodwill or of intangible assets with indefinite useful lives.

6 Guide to International Financial Reporting in Canada

The amendments published in May 2013 clarify the IASB’s original intention: the scope of those disclosures is limited to the recoverable amount of impaired assets that is based on fair value less costs of disposal.

The amendments are to be applied retrospectively for annual periods begin-ning on or after January 1, 2014. Earlier application is permitted for periods when the entity has already applied IFRS 13.

Key Standards Referred to in This PublicationThe following is a list of standards mentioned in this publication. Names of the standards have been included for the sake of clarity. The standards have been separated into two groups for purposes of this list — primary and secondary. The primary standards are the main standards that deal with the topic under discussion (in this publication — impairment). The secondary standards are those referred to in this publication but not discussed in depth.

Primary standards:

IAS 36 Impairment of assetsIFRIC 10 Interim financial reporting and impairment

Secondary standards:

IFRS 3 Business combinationsIFRS 4 Insurance contractsIFRS 5 Non-current assets held for sale and discontinued operationsIFRS 8 Operating segmentsIFRS 9 Financial instrumentsIFRS 10 Consolidated financial statementsIFRS 11 Joint arrangementsIFRS 13 Fair value measurementIAS 12 Income taxesIAS 16 Property, plant and equipmentIAS 34 Interim financial reportingIAS 37 Provisions, contingent liabilities and contingent assetsIAS 38 Intangible assetsIAS 39 Financial instruments: recognition and measurement

Subsequently, only the standard number will be referenced, not the name (e.g., IAS 16).

7IAS 36 Impairment of Assets

June 2013

IAS 36 Definitions[IAS 36.6]

These definitions were taken directly from IAS 36.

Carrying amount Carrying amount is the amount at which an asset is recog-nised after deducting any accumulated depreciation (amorti-sation) and accumulated impairment losses thereon.

Cash-generating unit A cash-generating unit is the smallest identifiable group of assets that generates cash inflows that are largely indepen-dent of the cash inflows from other assets or groups of assets.

Corporate assets Corporate assets are assets other than goodwill that contrib-ute to the future cash flows of both the cash-generating unit under review and other cash-generating units.

Costs of disposal Costs of disposal are incremental costs directly attributable to the disposal of an asset or cash-generating unit, excluding finance costs and income tax expense.

Depreciable amount Depreciable amount is the cost of an asset, or other amount substituted for cost in the financial statements, less its residual value.

Depreciation (Amortisation) Depreciation (Amortisation) is the systematic allocation of the depreciable amount of an asset over its useful life.

Fair value Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. (See IFRS 13 Fair Value Measurement.)

Impairment loss An impairment loss is the amount by which the carrying amount of an asset or a cash-generating unit exceeds its recoverable amount.

Recoverable amount The recoverable amount of an asset or a cash-generating unit is the higher of its fair value less costs of disposal and its value in use.

Useful life Useful life is either:1. the period of time over which an asset is expected to be

used by the entity; or2. the number of production or similar units expected to be

obtained from the asset by the entity.

Value in use Value in use is the present value of the future cash flows expected to be derived from an asset or cash-generating unit.

8 Guide to International Financial Reporting in Canada

Overview of Key RequirementsThe following chart provides a high-level overview of the key requirements of IAS 36 and accompanying IASB support materials. The intent is not to repeat the standard but to walk through the main requirements in the standard and identify the areas where detailed guidance is given and where complexity in application exists. Areas of greater complexity will be covered in more detail under the Analysis section of this publication.

As mentioned in the Preface, specific “touchstone” references to IAS 36 have been inserted to help the reader navigate the standard. The referencing is not meant to be all-inclusive but rather to give a starting point for further research in the standard itself.

KEY REQUIREMENTS OF IAS 36

Scope — IAS 36.2-5

Assets included within the Scope of IAS 36:• property, plant and equipment, including

assets carried at a revalued amount• intangible assets, including assets carried

at a revalued amount• goodwill• investment property carried at cost less

accumulated depreciation• biological assets measured at cost less

accumulated depreciation• subsidiaries• associates• joint ventures as defined in IFRS 11• exploration and evaluation assets

(with exceptions noted in IFRS 6)

Assets excluded from the Scope of IAS 36:• inventories• assets arising from construction contracts• deferred-tax assets• assets arising from employee benefits• financial assets within the scope of IAS 39

(or IFRS 9)• investment property measured at fair value• biological assets related to agricultural

activity that are measured at fair value less costs of disposal

• deferred acquisition costs and intangible assets arising from an insurer’s contrac-tual rights under insurance contracts within the scope of IFRS 4

• non-current assets (or disposal groups) classified as held for sale in accordance with IFRS 5

Identifying an asset that may be impaired — IAS 36.7–.17

IAS 36.9 requires an entity to assess at the end of each reporting period whether there is any indication that an asset may be impaired. If there is such indication, the asset is tested for impairment. IAS 36.12–.14 list external and internal impairment indicators and note that the guidance is not exhaustive and that other indicators may exist. The test for impairment involves estimating the recoverable amount and comparing it to the carrying amount at the end of the reporting period. Where the carrying amount exceeds the recoverable amount, an impairment loss exists and is recognized. Depreciation (amortization) calculations and policies for the asset (i.e., useful life, residual value and/or depreciation method) would be revisited in this case.

In addition, the following assets are tested for impairment at least annually, regardless of whether there is any indication of impairment:• indefinite-life intangible assets;• intangible assets not yet available for use; and• goodwill.

9IAS 36 Impairment of Assets

June 2013

KEY REQUIREMENTS OF IAS 36

Identifying an asset that may be impaired — IAS 36.7–.17 (continued)

The testing for these assets may be done anytime during the year as long as it is done at the same time each year. For these assets, where the recoverable value from previous esti-mates is significantly greater than the carrying amount, it is not necessary to re-estimate the recoverable amount as long as no events have occurred in the intervening periods that would eliminate the difference (IAS 36.15). Specific conditions are given for indefinite-lived intangible assets (IAS 36.24) and goodwill (IAS 36.99).

Increases in market or other interest rates are not necessarily indicators of impairment.

Measuring recoverable amount — IAS 36.18–.57

IAS 36 requires that assets be tested for impairment at the lowest level for which cash inflows are largely independent of those from other assets or groups of assets. This means that assets are tested for impairment at the level of the individual assets, unless the assets do not gener-ate independent cash inflows. In this case, they will be tested for impairment at the level of the cash-generating unit (CGU) to which they belong, unless certain conditions exist (e.g., the fair value less costs of disposal (FVLCD) exceeds the carrying amount or the value in use (VIU) is close to the FVLCD — for instance in the case of an asset soon to be sold).

In accordance with IAS 36.6, the recoverable amount of an asset or CGU is the higher of its FVLCD and its VIU. Even though this suggests that both FVLCD and VIU must be calculated, it is not always necessary to do so. If either FVLCD or VIU exceeds the asset’s carrying amount, the asset is not impaired and it is not necessary to estimate the other amount. For intangible assets with an indefinite life, the most recent calculation of the recoverable amount made in a prior period may be used in the current period calculation of the recoverable amount if certain conditions are met, as noted in IAS 36.24.

Guidance is given on how to measure FVLCD and VIU, including which cash flows to include and discount rates (IAS 36.28–.57). IFRS Illustrative Example 2 deals with the calculation of VIU and recognition of an impairment loss. IFRS Illustrative Examples 5 and 6 deal with future restructuring and future costs.

Recognizing and measuring an impairment loss — IAS 36.58–.64

IAS 36.6 defines impairment loss as the amount by which the carrying amount of an asset or CGU exceeds its recoverable amount. This could result in a liability being recognized where the loss is greater than the carrying amount, but only if recognition is required by another standard (e.g., if a constructive obligation, as defined by IAS 37, arose as a result of the asset being impaired). The impairment loss is recognized in net income, unless the asset is revalued in accordance with another standard (e.g., using the revaluation method according to IAS 16, in which case a decrease in an asset’s carrying value would be booked to other comprehensive income to the extent that a credit balance exists relating to prior revaluations).

CGUs and goodwill — IAS 36.65-.108

As noted above, the recoverable amount is estimated for an individual asset. Where this is not possible, the recoverable amount is estimated for the CGU to which the asset belongs. Guidance is given for situations where it is not possible to determine the recoverable amount of an individual asset (IAS 36.67). Guidance is also given on how to determine a CGU and to which CGU an asset belongs (IAS 36.68–.71). It may be necessary to consider some recognized liabilities when determining the recoverable amount of a CGU (IAS 36.78). Consistency from period to period in determining the CGU is required unless a change is justifiable. The stan-dard provides a number of examples. These will be referred to in the Analysis section below. IFRS Illustrative Example 1 deals with identification of CGUs, including a retail store chain, a manufacturing plant, a single-product entity, magazine titles and a rental building.

10 Guide to International Financial Reporting in Canada

KEY REQUIREMENTS OF IAS 36

CGUs and goodwill — IAS 36.65-.108

Goodwill must be allocated at the acquisition date (i.e., the date of a business combination) to a CGU or group of CGUs, depending on certain criteria. Goodwill is tested for impairment at this level by comparing the CGU or group’s carrying amount (including allocated goodwill) with the recoverable amount. Depreciation (amortization) calculations and policies for indi-vidual assets within a CGU (i.e., useful life, residual value and/or depreciation method) may have to be revisited even if no impairment is recognized in a CGU (IAS 36.17 and 107). Guid-ance is given regarding disposals of operations within a CGU (IAS 36.86) and reorganizations (IAS 36.87).

Different CGUs may be tested for impairment at different times, provided the timing is consis-tent from year to year. Relief is given regarding detailed calculations of recoverable amounts where certain conditions are met (IAS 36.99). Guidance is given for allocating corporate assets to CGUs (IAS 36.100–.103). IFRS Illustrative Example 8 deals with corporate assets. Where impairment exists, the impairment loss is allocated first to goodwill and then to the other assets in the unit on a pro rata basis (IAS 36.104). There is a limit on how much of the loss can be allocated to each asset (IAS 36.105). Any remaining loss after the allocation would only be recognized as a liability if such recognition is required by another IFRS (IAS 36.108). IFRS Illustrative Example 3 deals with recognition and measurement of related deferred-tax effects.

Reversing an impairment loss — IAS 36.109–.125

At the end of each reporting period, the entity must determine whether the impairment still exists. An impairment loss is reversed if there has been a (favourable) change in the estimates used to determine the recoverable amount of the asset or CGU. Guidance is given in IAS 36.111 and .112 regarding sources of evidence and how to allocate a reversal to the assets of a CGU. Goodwill impairments are not reversed. IFRS Illustrative Example 4 deals with impairment loss reversals.

Disclosure — IAS 36.126–.137

Disclosure requirements for impaired assets are significant and include information about estimates used. IFRS Illustrative Example 9 deals with disclosures. The disclosures required by IFRS 13 are not required for assets for which the recoverable amount is fair value less costs of disposal in accordance with IAS 36 (IFRS 13.07). General disclosure requirements under IAS 1 must also be met, including those related to significant judgments and sources of estimation uncertainty.

Using present value techniques to measure VIU — IAS 36 Appendix A

Appendix A to IAS 36 notes the components of present value measurements and discusses the traditional and expected cash flow approaches to estimate present value.

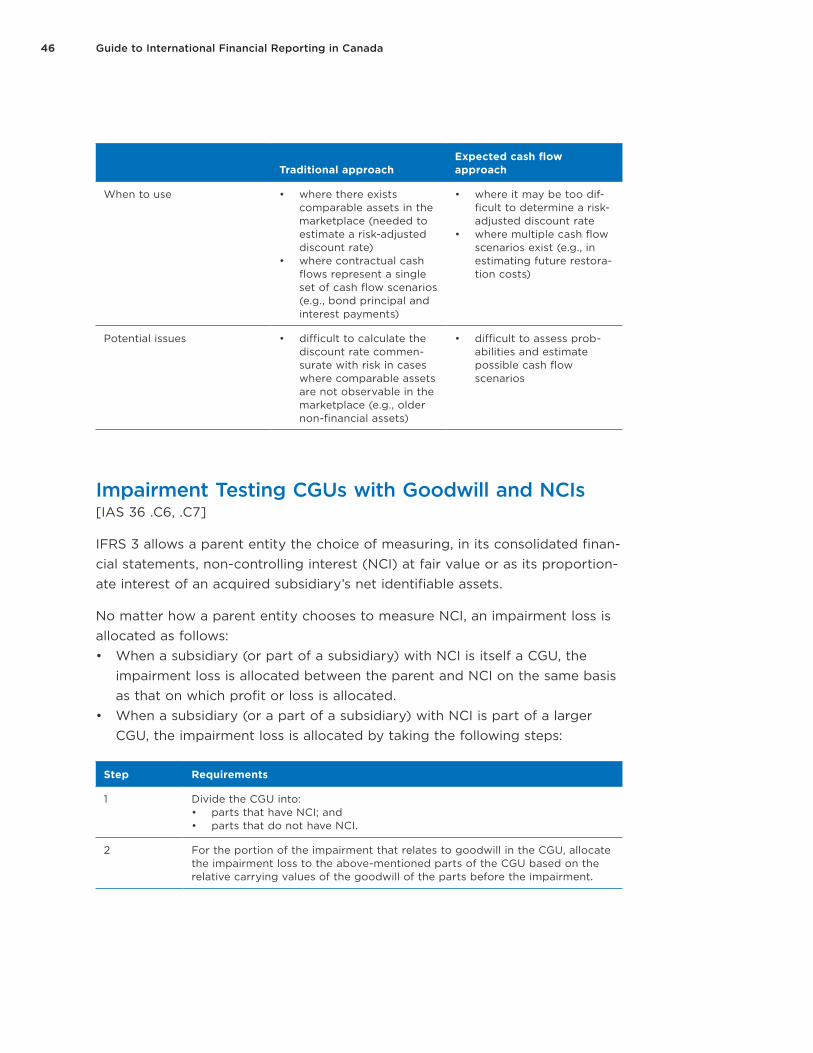

Impairment testing CGUs with goodwill and non-controlling interests — IAS 36 Appendix C

Appendix C to IAS 36 discusses accounting where non-controlling interests (NCI) exist. IFRS Illustrative Example 7 deals with CGUs and goodwill where there are NCIs.

Analysis of Relevant IssuesThis section expands on certain areas of greater complexity and/or areas requiring significant judgment.

11IAS 36 Impairment of Assets

June 2013

Identifying an Asset That May Be Impaired

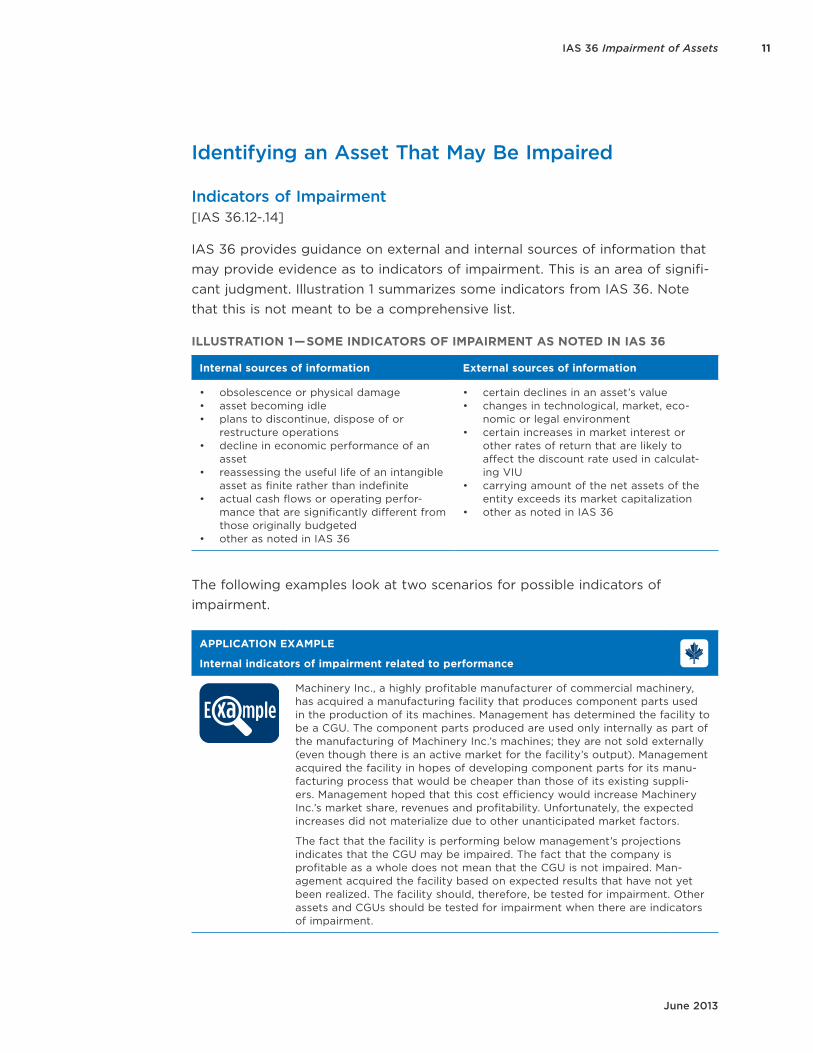

Indicators of Impairment[IAS 36.12-.14]

IAS 36 provides guidance on external and internal sources of information that may provide evidence as to indicators of impairment. This is an area of signifi-cant judgment. Illustration 1 summarizes some indicators from IAS 36. Note that this is not meant to be a comprehensive list.

ILLUSTRATION 1 — SOME INDICATORS OF IMPAIRMENT AS NOTED IN IAS 36

Internal sources of information External sources of information

• obsolescence or physical damage• asset becoming idle• plans to discontinue, dispose of or

restructure operations• decline in economic performance of an

asset• reassessing the useful life of an intangible

asset as finite rather than indefinite• actual cash flows or operating perfor-

mance that are significantly different from those originally budgeted

• other as noted in IAS 36

• certain declines in an asset’s value• changes in technological, market, eco-

nomic or legal environment• certain increases in market interest or

other rates of return that are likely to affect the discount rate used in calculat-ing VIU

• carrying amount of the net assets of the entity exceeds its market capitalization

• other as noted in IAS 36

The following examples look at two scenarios for possible indicators of impairment.

APPLICATION EXAMPLE

Internal indicators of impairment related to performance

E xa mpleMachinery Inc., a highly profitable manufacturer of commercial machinery, has acquired a manufacturing facility that produces component parts used in the production of its machines. Management has determined the facility to be a CGU. The component parts produced are used only internally as part of the manufacturing of Machinery Inc.’s machines; they are not sold externally (even though there is an active market for the facility’s output). Management acquired the facility in hopes of developing component parts for its manu-facturing process that would be cheaper than those of its existing suppli-ers. Management hoped that this cost efficiency would increase Machinery Inc.’s market share, revenues and profitability. Unfortunately, the expected increases did not materialize due to other unanticipated market factors.

The fact that the facility is performing below management’s projections indicates that the CGU may be impaired. The fact that the company is profitable as a whole does not mean that the CGU is not impaired. Man-agement acquired the facility based on expected results that have not yet been realized. The facility should, therefore, be tested for impairment. Other assets and CGUs should be tested for impairment when there are indicators of impairment.

12 Guide to International Financial Reporting in Canada

APPLICATION EXAMPLE

Internal indicators of impairment — adverse change of use — idle asset

E xa mpleProducer Co. uses Machine J to manufacture Product A; however, Machine J has recently been idle due to a change in consumer needs.

In this case, management should review Machine J for impairment because the change in the extent to which Machine J is used has had a negative impact on the cash flows directly attributable to it. If a change in the way an asset is used has an adverse effect on the entity, that is an indicator of impairment.

The following extract represents an excerpt from the financial statements of Nexen Inc. showing indicators of impairment. The decrease in gas prices and increase in future abandonment charges are external indicators.

EXTRACT 1 — EXCERPT FROM NEXEN INC. 2012 FINANCIAL STATEMENTS

NOTE 5B — INDICATORS OF IMPAIRMENT

23

(B) IMPAIRMENT In the fourth quarter of 2012, lower estimated future North American natural gas prices and increases in future abandonment costs resulted in a $237 million non-cash impairment charge for natural gas properties in North America. These assets are included in our Conventional North America segment.

DD&A expense for 2011 includes non-cash impairment charges of $322 million for our oil and gas properties in our Conventional North America segment. Canadian natural gas assets were impaired $234 million in the second half of 2011 due to lower estimated future natural gas prices and performance-related negative reserve revisions. In the fourth quarter of 2011, lower estimated future natural gas prices and higher estimated future abandonment costs resulted in an $88 million impairment of mature Gulf of Mexico properties.

The properties were written down to the higher amount of value-in-use and estimated fair value less costs to sell. We estimated fair value based on discounted future net cash flows using estimated future prices, a discount rate of 9% and management’s estimate of future production, capital and operating expenditures.

(C) ASSET DERECOGNITIONS Nexen’s original strategy for future oil sands development was to build duplicates of the existing Long Lake SAGD facilities and upgrader. In 2011, we revised our strategy to focus on smaller, phased, SAGD-only projects. As a result, previously capitalized design and engineering costs of $253 million on the future phases were expensed in 2011.

6. GOODWILL

(A) CARRYING AMOUNT OF GOODWILL Goodwill As at December 31, 2010 286 Effect of Changes in Exchange Rate 7 Dispositions (2) As at December 31, 2011 291 Effect of Changes in Exchange Rate (6) As at December 31, 2012 285

December 31 December 31 2012 2011 UK Conventional 277 284 Corporate and Other 8 7 Total 285 291

(B) IMPAIRMENT TESTING OF GOODWILL Goodwill is attributable to our UK Conventional and Corporate and Other segments which have been allocated for impairment testing purposes to the cash-generating units that reflect the lowest level at which goodwill is attributable.

UK Conventional The recoverable amount of the UK group was based on cash flow projections discounted at a rate of 9%. The significant assumptions used in the cash flow projections are:

Commodity prices: these assumptions are based on estimated market-based future prices, the global supply-demand balance for each commodity, other macroeconomic factors, historical trends and variability.

Discount rates: the rates used in the calculation are based on an industry-specific discount rate, adjusted to take into consideration country and project risks specific to the cash-generating unit.

The following extract represents an excerpt from the financial statements of Suncor Energy Inc. showing indicators of impairment. The political unrest is an external indicator, but the decision to suspend operations is an internal indicator.

EXTRACT 2 — EXCERPT FROM SUNCOR ENERGY INC. 2012 FINANCIAL STATEMENTS

NOTE 9 — INDICATORS OF IMPAIRMENT

7. OTHER INCOME

Other Income consists of the following:

($ millions) 2012 2011

Energy trading activitiesChange in fair value of contracts 246 301Unrealized losses on inventory valuation (13) (19)

Risk management activities 1 (22)Investment and interest income 80 141Renewable energy grants 59 64Other 35 (12)

408 453

8. OPERATING, SELLING AND GENERAL

Operating, Selling and General expense consists of the following:

($ millions) 2012 2011

Contract services 4 069 4 107Employee benefit costs (1) 2 697 2 062Materials 725 882Energy 613 712Equipment rentals and leases 330 363Travel, marketing and other 514 298

8 948 8 424

(1) The company incurred $3.2 billion of employee benefit costs for the year ended December 31, 2012 (2011 – $2.5 billion), of which$2.7 billion (2011 – $2.1 billion) was recorded as employee benefits in Operating, Selling and General expense. Employee benefits expenseincludes salaries, benefits and share-based compensation.

9. ASSET IMPAIRMENT

Oil Sands

During the fourth quarter of 2012, the company recognized after-tax impairment charges of $1.487 billion related to the

Voyageur upgrader project in its Oil Sands business. As a result of the challenging economic outlook for the Voyageur upgrader

project, an impairment test was performed at December 31, 2012, using a fair value less cost to sell methodology. The company

used an expected future cash flow approach, with a risk-adjusted discount rate of 10% to perform the calculation. As at

December 31, 2012, the company’s carrying value for assets relating to the Voyageur upgrader project was approximately

$345 million.

The impairment charges were recorded as part of Depreciation, Depletion, Amortization and Impairment expense.

Syria

In December 2011, the company declared force majeure under its contractual obligations, suspended its operations and ceased

recording production due to political unrest and international sanctions affecting that country. An impairment test was

performed at that time, which determined that the assets were not impaired.

As there had been no resolution of the political situation at the end of the second quarter of 2012, another impairment test

was performed on the company’s Syrian assets. As a result, the company recognized after-tax impairment charges and write-

downs of $694 million. The impairment losses were recorded as part of Depreciation, Depletion, Amortization and Impairment

expense and charged against Property, Plant and Equipment ($604 million) and other current assets ($23 million). The company

also wrote off the remainder of its Syrian receivables ($67 million). A write-down of receivables of $64 million was previously

recorded at December 31, 2011.

During the fourth quarter of 2012, the company received $300 million of risk mitigation proceeds related to its Syrian

operations. The proceeds are subject to a provisional repayment should the company resume operations in Syria and therefore,

have been recorded as a non-current provision at December 31, 2012.

After receipt of the risk mitigation proceeds, an impairment test was performed at December 31, 2012, using a value-in-use

methodology. The company used an expected cash flow approach based on 2011 year-end reserves data updated for the

SUNCOR ENERGY INC. ANNUAL REPORT102 2012

13IAS 36 Impairment of Assets

June 2013

company’s best estimate of price realizations and remaining reserves, with three scenarios representing i) resumption of

operations in one year, ii) resumption of operations in five years, and iii) total loss. The two scenarios where the company

resumes operations incorporated repayment of the risk mitigation proceeds in accordance with the terms of the agreement.

These scenarios were equally weighted based on the company’s best estimates, and present valued using a risk-adjusted discount

rate of 19%. Based on this assessment, the company recognized an impairment reversal of $177 million related to Syrian assets

in its Exploration and Production business.

The impairment reversal of $177 million was recorded in the fourth quarter of 2012 as part of Depreciation, Depletion,

Amortization and Impairment expense. A 2% change in discount rates and a 5% change in pricing assumptions would each

have an impact on after-tax earnings of approximately $20 million.

The resulting carrying value of the company’s Property, Plant, and Equipment in Syria, net of the risk mitigation provision, at

December 31, 2012 was approximately $130 million.

Libya

In the second quarter of 2011, the company recognized after-tax impairment charges of $514 million related to Libyan assets in

its Exploration and Production business. At that time, production had been shut in due to political violence in Libya. The

impairment losses were recorded as part of Depreciation, Depletion, Amortization and Impairment expense, and charged against

Property, Plant and Equipment ($259 million), Exploration and Evaluation assets ($211 million), and Inventories ($44 million).

During the fourth quarter of 2011, the company reversed $11 million of the impairment charge that related to crude oil

inventories. The reversal was the result of lifting certain political sanctions, and the joint venture partner confirming the existence

of previously written off crude oil.

Production payments resumed in January 2012 with production in all major fields restarted in the first quarter of 2012. As a

result, a valuation assessment was performed. The company used an expected cash flow approach based on 2012 year-end

reserves data with a risk-adjusted discount rate of 17% to reflect uncertainty related to continued political unrest in the region,

current production levels and the timing and success of future exploration drilling commitments. No reversal of impairment was

recorded at December 31, 2012. A 2% change in discount rates would impact after-tax earnings by approximately $90 million

while a 5% change in pricing assumptions would impact after-tax earnings by approximately $70 million.

The carrying value of Suncor’s net assets in Libya as at December 31, 2012, net of asset impairment and write-offs, was

approximately $650 million.

Other

During the fourth quarter of 2012, the company recognized an after-tax impairment charge of $65 million related primarily to

certain East Coast Canada exploration and evaluation assets as well as natural gas Arctic land leases in the Exploration and

Production business as a result of future development uncertainty. In addition, the company also recognized an after-tax

impairment charge of $63 million related to CGUs in the Exploration and Production business due to a decline in price forecasts.

The recoverable amount was determined using a fair value less cost to sell methodology, with the expected cash flow approach

based on 2012 year-end reserves data and a risk-adjusted discount rate of 10%. A 2% increase in discount rates would

decrease after-tax earnings by approximately $90 million while a 5% decrease in pricing assumptions would decrease after-tax

earnings by approximately $30 million.

During the fourth quarter of 2011, the company recognized a charge of $100 million to reflect the write-down of certain

natural gas CGUs in the Exploration and Production business to reflect the recoverable amount based on discounted cash flows.

The impairment charges were recorded as part of Depreciation, Depletion, Amortization and Impairment expense.

SUNCOR ENERGY INC. ANNUAL REPORT2012 103

Measuring Recoverable Amount[IAS 36.18, .19]

Illustration 2 shows the basic steps for measuring the recoverable amount.

ILLUSTRATION 2 — DECISION TREE — RECOVERABLE AMOUNT

Carryingvalue

Fair value less costsof disposal

Value in use

Compared with

Recoverable amount

Higher of

14 Guide to International Financial Reporting in Canada

Recall that it may not be necessary to calculate both the VIU and the FVLCD where either the VIU or FVLCD exceeds the carrying amount.

The following extracts represent excerpts from the financial statements of Royal Bank of Canada and Pizza Pizza Royalty Corp. showing whether VIU or FVLCD were used in measuring the recoverable amount.

EXTRACT 3 — EXCERPT FROM ROYAL BANK OF CANADA 2012 FINANCIAL

STATEMENTS

NOTE 11 — CALCULATION OF RECOVERABLE AMOUNT

(Millions of Canadian dollars) Land BuildingsComputer

equipment

Furniture,fixtures

and otherequipment

Leaseholdimprovements

Work inprocess Total

CostBalance at November 1, 2010 $ 216 $ 934 $ 1,954 $ 1,467 $ 1,641 $ 293 $ 6,505Assets from discontinued operations (105) (269) (38) (154) (81) (12) (659)Additions (1) 6 40 77 56 34 612 825Acquisitions through business combinations – – – – – – –Transfers from work in process 1 66 95 53 156 (371) –Disposals – (5) (34) (54) (23) – (116)Foreign exchange translation (2) 7 (20) (17) (24) (1) (57)Other – 28 (219) 2 (19) 11 (197)

Balance at October 31, 2011 $ 116 $ 801 $ 1,815 $ 1,353 $ 1,684 $ 532 $ 6,301

Accumulated depreciationBalance at November 1, 2010 $ – $ 498 $ 1,511 $ 993 $ 1,002 $ – $ 4,004Assets from discontinued operations – (108) (31) (111) (46) – (296)Depreciation – 18 165 76 128 – 387Impairment loss (reversal) – – – – – – –Disposals – (3) (34) (49) (20) – (106)Foreign exchange translation – 3 (11) (5) (12) – (25)Other – 19 (168) 3 (7) – (153)

Balance at October 31, 2011 $ – $ 427 $ 1,432 $ 907 $ 1,045 $ – $ 3,811

Net carrying amount at October 31, 2011 $ 116 $ 374 $ 383 $ 446 $ 639 $ 532 $ 2,490

(1) At October 31, 2012, we had total contractual commitments of $96 million to acquire premises and equipment (October 31, 2011 – $154 million; November 1, 2010 – $72 million).

Note 11 Goodwill and other intangibles

GoodwillThe following table presents changes in the carrying amount of goodwill by CGU for the years ended October 31, 2012 and 2011.

(Millions of Canadian dollars)Canadian

BankingCaribbean

Banking

CanadianWealth

ManagementGlobal AssetManagement

U.S. WealthManagement

InternationalWealth

Management InsuranceInvestorServices

Investor &Treasury

Services (1)Capital

Markets Total

At November 1, 2010 $ 1,931 $ 1,492 $ 545 $ 765 $ 528 $ 119 $ 126 $ 146 $ – $ 901 $ 6,553Acquisitions 11 – – 1,099 – – – – – 2 1,112Currency translations – (41) (3) 17 (12) (1) (8) (2) – (16) (66)Other changes 11 – – – – – – – – – 11At October 31, 2011 $ 1,953 $ 1,451 $ 542 $ 1,881 $ 516 $ 118 $ 118 $ 144 $ – $ 887 $ 7,610Acquisitions – – – – – 8 – – – – 8Transfers – – – – – – – – 52 (52) –Impairment losses (2) – – – – – – – (142) – – (142)Currency translations – – – 8 1 – – (2) – 2 9Other changes (2) – 1 – – 1 – – – – –At October 31, 2012 $ 1,951 $ 1,451 $ 543 $ 1,889 $ 517 $ 127 $ 118 $ – $ 52 $ 837 $ 7,485

(1) Effective October 31, 2012, Investor & Treasury Services is a newly created CGU that includes our former Investor Services CGU and certain related businesses that were part of our CapitalMarkets CGU. The transfer of goodwill was based on the relative fair value of the transferred businesses. See Note 30 for further details on our business segments.

(2) During the second quarter of 2012, we recorded an impairment loss of $142 million in our Investor Services CGU related to our acquisition of the remaining 50% interest in RBC Dexia. SeeNote 12 for further details.

Key inputs and assumptionsWe perform our annual impairment test by comparing the carrying amount of each CGU to its recoverable amount. The recoverable amount of aCGU is represented by its value in use, except in circumstances where the carrying amount of a CGU exceeds its value in use. In such cases, wedetermine the CGU’s fair value less costs to sell and its recoverable amount is the greater of its value in use and fair value less costs to sell.

In our annual impairment tests performed as at August 1, 2012 and August 1, 2011 and our goodwill impairment test performed ontransition to IFRS as at November 1, 2010, the recoverable amounts of our CGUs were based on value in use, except for Caribbean Banking as atAugust 1, 2012 and 2011, which was based on fair value less costs to sell.

We calculate value in use using the discounted cash flow (DCF) method that projects future cash flows, which are discounted to their present value. Future cash flows are based on financial plans agreed by management for a five-year period, estimated based on forecast results, business initiatives, planned capital investments and returns to shareholders. Cash flow projections beyond the initial five-year period are assumed to increase at a constant rate using a nominal long-term growth rate (terminal growth rate).

The estimation of value in use involves significant judgment in the determination of inputs to the model and is most sensitive to changes infuture cash flows, discount rates and terminal growth rates applied to cash flows beyond the forecast period. These key inputs and assumptionsused to determine the recoverable amount of each CGU using value in use were tested for sensitivity by applying a reasonably possible changeto those assumptions. The discount rates were increased by 1%, terminal growth rates were decreased by 0.5%, and future cash flows werereduced by 10%. As at August 1, 2012, no change in an individual key input or assumption as described, would result in a CGU’s carrying valueexceeding its recoverable amount.

Consolidated Financial Statements Royal Bank of Canada: Annual Report 2012 145

EXTRACT 4 — EXCERPT FROM PIZZA PIZZA ROYALTY CORP. 2012 FINANCIAL

STATEMENTS

NOTE 4 — CALCULATION OF RECOVERABLE AMOUNT

Pizza Pizza Royalty Corp. Notes to the Consolidated Financial Statements For the years ended December 31, 2012 and 2011 (Expressed in thousands of Canadian dollars except number of shares and per share amounts)

12

Annually, on January 1 (the Adjustment Date), the Royalty Pool is adjusted to include the forecasted system sales from new Pizza Pizza restaurants opened on or before December 31 of the prior year, less system sales from any Pizza Pizza restaurants that have been permanently closed during the year. Similarly, on the Adjustment Date, the Royalty Pool is adjusted to include the forecasted system sales from new Pizza 73 restaurants opened on or before September 1 of the prior year, less any Pizza 73 restaurants permanently closed during the calendar year.

In return for adding net additional royalty revenue, PPL receives the right to indirectly acquire additional shares of the Company through an adjustment to the Class B and Class D Exchange Multiplier (see note 7).

As a result of adding new restaurants to the Royalty Pool, as described in note 7, the Rights and Marks increased by $111 for the year ended December 31, 2012 (December 31, 2011 – $921), resulting in a corresponding increase in exchangeable units.

Impairment test of the Rights and Marks

The Company performed impairment tests for both the Pizza Pizza and Pizza 73 Rights and Marks at December, 31, 2012 and December 31, 2011 in accordance with the accounting policy as described in note 2. The recoverable amount of each cash generating unit (CGU) was determined based on value-in-use calculations. These calculations used cash flow projections based on financial budgets approved by management covering a one year period and extrapolated for five years. Cash flows beyond the one year period are extrapolated using the estimated growth rates stated below.

The key assumptions used for the value-in-use calculation at December 31, 2012 were as follows:

Growth ratePre-tax

discount ratePizza Pizza CGU 3.5% 11.6%Pizza 73 CGU 3.5% 12.8%

The key assumptions used for the value-in-use calculation at December 31, 2011 were as follows:

Growth ratePre-tax

discount ratePizza Pizza CGU 3.5% 11.6%Pizza 73 CGU 3.5% 12.8%

The impairment tests performed resulted in no impairment of the Rights and Marks at December 31, 2012 or 2011.

5. Trade and Other Payables

December 31, 2012

$

December 31, 2011

$

Accruals 174 70Other payables 291 273Total trade and other payables 465 343

15IAS 36 Impairment of Assets

June 2013

APPLICATION STATISTIC

Survey of Selected Accounting Policies of Junior Oil and Gas Entities — January 2013

StatisticsThis survey of selected junior oil and gas company financial statements showed that, where an impairment loss or reversal existed, in calculat-ing recoverable amount, 65% used FVLCD, 17% used VIU and 17% did not disclose.

In practice, it is not uncommon for FVLCD to result in a higher recoverable amount than VIU because a FVLCD calculation is typically less limiting than VIU, supporting the inclusion of factors a market participant may take into consideration such as possible reserves or future internal synergies (e.g., uncommitted restructurings).

The publication is available online at www.cica.ca/ifrs

Determining Recoverable Amount at the Level of the Individual Asset or CGU[IAS 36.19 and 22]

The recoverable amount is determined at the individual asset level unless the asset does not generate cash inflows that are largely independent of those of other assets or groups of assets. Notwithstanding this, according to IAS 36.22, impairment may still be tested at the level of the individual asset if either:• the asset’s FVLCD is greater than its carrying amount (as mentioned ear-

lier — in which case, the asset is not impaired); or• the asset’s VIU can be estimated to be close to its FVLCD (e.g., the values

essentially do not differ) and FVLCD can be determined.

When it is not possible to isolate an asset’s cash inflows, and its recoverable amount cannot be determined through either of the above-mentioned alter-natives, impairment is tested at the level of that asset’s CGU. The example in IAS 36.107 looks at this issue.

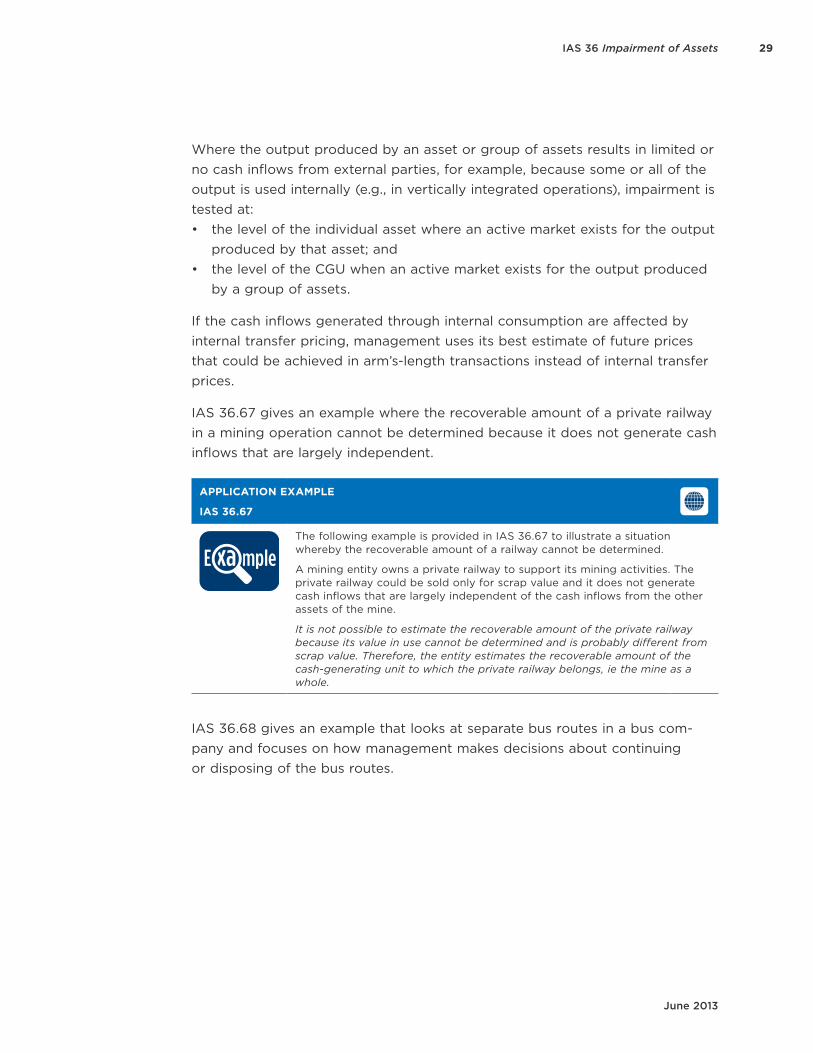

APPLICATION EXAMPLE

IAS 36.107 — Impairment testing at individual asset level

E xa mpleThe following example is provided in IAS 36 to illustrate a situation where the impairment test is done at the individual asset level because the asset’s VIU is close to its FVLCD. Assumption 2 in the example illustrates this.

A machine has suffered physical damage but is still working, although not as well as before it was damaged. The machine’s fair value less costs of disposal is less than its carrying amount. The machine does not generate independent cash inflows. The smallest identifiable group of assets that includes the machine and generates cash inflows that are largely indepen-dent of the cash inflows from other assets is the production line to which the machine belongs. The recoverable amount of the production line shows that the production line taken as a whole is not impaired.

16 Guide to International Financial Reporting in Canada

APPLICATION EXAMPLE

IAS 36.107 — Impairment testing at individual asset level

Assumption 1: budgets/forecasts approved by management reflect no com-mitment of management to replace the machine.

The recoverable amount of the machine alone cannot be estimated because the machine’s value in use:1. may differ from its fair value less costs of disposal; and2. can be determined only for the cash-generating unit to which the

machine belongs (the production line).

The production line is not impaired. Therefore, no impairment loss is rec-ognised for the machine. Nevertheless, the entity may need to reassess the depreciation period or the depreciation method for the machine. Perhaps a shorter depreciation period or a faster depreciation method is required to reflect the expected remaining useful life of the machine or the pattern in which economic benefits are expected to be consumed by the entity.

Assumption 2: budgets/forecasts approved by management reflect a com-mitment of management to replace the machine and sell it in the near future. Cash flows from continuing use of the machine until its disposal are esti-mated to be negligible.

The machine’s value in use can be estimated to be close to its fair value less costs of disposal. Therefore, the recoverable amount of the machine can be determined and no consideration is given to the cash-generating unit to which the machine belongs (ie the production line). Because the machine’s fair value less costs of disposal is less than its carrying amount, an impair-ment loss is recognised for the machine.

The identification of a CGU involves significant judgment in terms of the level of asset aggregation. The following should be kept in mind when applying the definition of a CGU:• The smallest identifiable group of assets that generates cash inflows is a

matter of fact.• The determination of what “largely independent” means is a matter of

judgment.• The sole determinant of a CGU is the cash inflows.• Practically, this means that entities will have to identify CGUs by looking at

the smallest group of assets. This group of assets constitutes a CGU unless its cash inflows depend on other assets.

17IAS 36 Impairment of Assets

June 2013

Examples of a CGU may include:• an individual retail store or hotel, which would usually generate cash inflows

that are largely independent of the others in a group even though they might share common services such as marketing and finance;

• a factory with a single production line where there is an external market for the product at an intermediate stage; and

• a service route provided by a transport business where the assets deployed to each route, as well as the route’s cash flows, can be separately identified.

Illustration 3 summarizes the level of impairment testing under IFRSs. It has been assumed that it may be better to start testing by trying to determine FVLCD as a first step. If FVLCD can be determined and it exceeds the carrying amount, or certain other conditions apply, it may not be necessary to calcu-late VIU. Having said that, you could also start by trying to measure VIU first, although this may be more difficult since it is necessary to determine cash flows.

ILLUSTRATION 3 — LEVEL OF IMPAIRMENT TESTING

[IAS 36.19-.22]

Does the FVLCD exceed carrying

amount?Not impaired

Can the asset’s VIU be estimated to be close to its FVLCD?

The asset’s recov-erable value is not determinable and impairment is as-sessed at the level

of the CGU.

Does the asset gen-erate cash fl ows that

are largely inde-pendent of those

from other assets or groups of assets?

The asset’s recover-able amount is de-terminable and im-

pairment is assessed at the level of the individual asset.

Is FVLCDmeasurable?

YES YES

YES

YESNO

NO

NO

NO

Extract 5 represents an excerpt from the 2012 financial statements of Metro Inc. showing the level at which the assets were tested for impairment.

18 Guide to International Financial Reporting in Canada

EXTRACT 5 — EXCERPT FROM METRO INC. 2012 FINANCIAL STATEMENTS

NOTE 16 — CALCULATION OF RECOVERABLE AMOUNTNotes to consolidated financial statementsSeptember 29, 2012 and September 24, 2011(Millions of dollars, unless otherwise indicated)

- 85 -

Intangible assets with indefinite useful lives were as follows:

Banners Private labels Loyalty programs Total

Balance as at September 26, 2010 53.3 33.1 22.1 108.5Transfers 1.4 1.4

Balance as at September 24, 2011 53.3 33.1 23.5 109.9Acquisitions through business

combinations (note 6) 57.0 6.4 63.4

Balance as at September 29, 2012 110.3 39.5 23.5 173.3

Net additions of intangible assets excluded from the consolidated statement of cash flows amounted to $6.5 in 2012 ($11.0 in 2011).

For impairment testing, the carrying amount of certain private labels was allocated to the unique operating segment. The recoverable amount was determined based on its value in use which was calculated using pre-tax cash flow forecasts from the management-approved budgets. The forecasts reflected past experience. A pre-tax discount rate of 14.4% was used without considering a growth rate.

Impairment testing of loyalty programs was conducted at the level of the asset itself. The recoverable amount was determined based on its fair value less costs to sell, which was calculated using the capitalized excess EBIT method. The estimated EBIT directly allocated to the programs, after deduction of the return on contributory assets, was based on historical data reflecting past experience. The earnings multiple used was 6.9 considering a growth rate of 2.0% corresponding to the consumer price index.

Impairment testing of banners and certain private labels were conducted at the level of the asset itself. The recoverable amount was determined based on its fair value less costs to sell, which was calculated using the royalty-free licence method. The estimated royalty rate was based on information from external sources and historical data reflecting past experience. For the banners, the earnings multiples used were 7.5 et 10.0 considering growth rates of 2.0% and 3.0% corresponding to the consumer price index and banners' growth. For certain private labels, the earnings multiple used was 11.1 considering a growth rate of 3.0% corresponding to the consumer price index and the growth of these private labels.

No reasonably possible change of any of the previously mentioned key assumptions would result in a carrying amount higher than the recoverable amount.

Relief for Determination of Recoverable Amount — Certain Intangible Assets and Goodwill[IAS 36.15, .24, .99]

Because the requirement to test certain intangible assets and goodwill for impairment annually may be onerous, relief has been provided for the determi-nation of the recoverable amount. IAS 36.15 provides some general guidance for indefinite-lived intangibles assets, intangible assets not yet available for use and goodwill by noting that the recoverable amount might not need to be estimated, for instance where:• the previous estimate of recoverable amount exceeds carrying amount by

a significant amount; and• no events have occurred which would eliminate that difference.

IAS 36.24 and .99 give more explicit guidance for indefinite-lived intangible assets and goodwill.

19IAS 36 Impairment of Assets

June 2013

Illustration 4 shows a decision tree that helps determine whether a prior mea-sure of recoverable amount for an indefinite-lived intangible asset and/or goodwill may be used in impairment testing.

ILLUSTRATION 4 — RELIEF REGARDING CALCULATION OF RECOVERABLE AMOUNT

FOR INDEFINITE-LIVED INTANGIBLES AND GOODWILL

Intangible assets — indefi nite life and/or

goodwill

Where intangible asset and/orgoodwill tested for impairment

as part of a CGU

Where intangible asset tested forimpairment at individual asset level

Most recent calculation of recov-erable amount exceeds carrying

amount by a substantial margin and there is only a remote chance that the current recoverable amount would be less than the carrying

amount?[IAS 36.24]

YES

Use most recent calculation of recov-

erable amount

Must calculate new recoverable amount

Use most recent calculation of recov-

erable amount

NO YES

Most recent calculation of recov-erable amount exceeds carrying

amount by a substantial margin and there is only a remote chance that the current recoverable amount would be less than the carrying

amount and the assets and liabilities of the CGU have not changed

signifi cantly?[IAS 36.24 and .99]

Extract 6 represents an excerpt from the 2012 Air Canada financial statement showing an instance whereby the company utilized the prior-year calculation of recoverable amount in the current-year impairment test.

20 Guide to International Financial Reporting in Canada

EXTRACT 6 — EXCERPT FROM AIR CANADA 2012 NOTES TO FINANCIAL

STATEMENTS

NOTE 5 — RELIEF FROM CALCULATING RECOVERABLE AMOUNT

2012 Consolidated Financial Statements and Notes

22

For the annual 2012 impairment review, the most recent calculations from the preceding period were carried forward as the calculation of the recoverable amount exceeded the carrying amount by a substantial margin, the assets and liabilities making up the CGU had not changed significantly and no events had occurred or circumstances had changed which would indicate that the likelihood of the recoverable asset not exceeding the carrying value was remote.

Key assumptions used for the value in use calculations in fiscal 2011 were as follows:

2011

Pre-tax discount rate 15.6%

Long-term growth rate 2.5%

Jet fuel price range per barrel $125 – $135

The recoverable amount of both cash-generating units based on value in use exceeded their respective carrying values by approximately $1,400. If the discount rate were increased by 380 basis points, the excess of recoverable amount over carrying value would be reduced to nil.

FVLCD[IAS 36.6, .20, .21, .28, .53A]

Fair value is the price that would be received to sell an asset (or paid to trans-fer a liability) in an orderly transaction between market participants at the measurement date (IAS 36.06). Fair value reflects assumptions that market participants would make when pricing an asset. The fair value of an asset is determined in accordance with IFRS 13. If there is no active market for the asset being valued, the entity must calculate the fair value using a valuation technique. The entity should select the technique (e.g., discounted cash flows) that is most appropriate for the asset being valued. For instance, it might make sense to value an operating hotel using a discounted cash flow method. More than one model may be used. In the case of the hotel previously mentioned, the entity may choose to value the hotel by looking at market-comparable prices for similar hotels in the geographical area. Maximum use of externally observable inputs is optimal and the fair value hierarchy should be used to classify inputs. An entity is not required to provide the disclosures required by IFRS 13.

In accordance with IFRS 13, fair value measurement considers utilization of the asset at its highest and best use (i.e., the use that would provide maximum economic benefit to a market participant).

Costs of disposal are incremental costs directly attributable to the disposal of an asset, such as legal costs and similar transaction fees, costs of removing the asset and direct incremental costs to bring an asset into condition for its sale (excluding finance costs and income tax expense).

21IAS 36 Impairment of Assets

June 2013

If it is not possible to measure FVLCD because there is no basis for making a reliable estimate of the price to sell the asset in an orderly transaction, the entity would use VIU to determine the recoverable amount.

VIU[IAS 36.6, .20, .21, .30– 57, .69, .70, .A15–.A21]

VIU is the present value of the future cash flows expected to be derived from an asset or CGU (IAS 36.6). VIU reflects factors specific to an entity (e.g., value from asset grouping, synergies between assets, legal rights or restrictions, tax benefits or burdens). It is therefore different from a fair value measure, which is a market-based measure calculated according to IFRS 13. Some of the differ-ences are highlighted in Illustration 5.

ILLUSTRATION 5 — THE DIFFERENCE BETWEEN FVLCD AND VIU

FVLCD [IFRS 13]

VIU [IAS 36.53A]

• measured in accordance with IFRS 13 guidance

• includes only those factors that a market participant would include in valuing the asset (market participant perspective)

• may be measured using market prices or a valuation technique used for estimating market prices

• considers highest and best use of a non-financial asset (which may be different from actual use by the entity, although the entity’s current use of a non-financial asset may be assumed to be the highest and best use unless there is evidence to the contrary)

• measured in accordance with IAS 36 guidance

• includes those factors that an entity would include in valuing the asset (entity-specific)

• examples of factors include: o additional value derived from a group

of assets o synergies between the asset being

measured and other entity-owned assets

o legal rights or restrictions relating to the asset that are specific to the entity

VIU requires the discounting of future cash flows to be derived from the asset’s continuing use and from its ultimate disposal. Judgment is required to make realistic estimates of future cash flows and to determine appropriate discount rates to calculate the present value of those future cash flows.

Estimates of future cash flows must be based on reasonable and support-able assumptions that represent management’s best estimate of the range of economic conditions that will exist over the asset’s remaining useful life. Greater weight must be given to external evidence. Management must assess the reasonableness of its assumptions by examining the causes of differences between past cash flow projections and actual cash flows.

22 Guide to International Financial Reporting in Canada

As a starting point, estimates of future cash flows are based on the most recent financial budgets/forecasts approved by management. There is a rebut-table presumption that it is not possible to make detailed, explicit and reli-able financial budgets/forecasts of future cash flows for periods longer than five years. Therefore, projections based on budgets/forecasts must cover a maximum period of five years, unless management can demonstrate its abil-ity (based on past experience) to forecast cash flows accurately over a longer period. Projections beyond the period covered by the most recent budgets/forecasts are estimated by extrapolating the projections based on the bud-gets/forecasts using a steady or declining growth rate for subsequent years, unless an increasing rate can be justified. This growth rate must not exceed the long-term average growth rate for the products, industries, country or countries in which the entity operates, or for the market in which the assets are used, unless a higher rate can be justified.

A chart showing items to be included in, and excluded from, cash flows is shown in Illustration 6.

ILLUSTRATION 6 — CALCULATING VIU — CASH FLOWS

Items to include in cash flows [IAS 36.39-.42, .47, .49, .52, .53]

Items to exclude from cash flows [IAS 36.43-.45, .48, .50]

• general inflation where this is not included in the discount rate

• projections of cash inflows from continu-ing use of the asset

• projections of cash outflows that are necessarily incurred to generate the above cash inflows and can be directly attributed, or allocated on a reasonable and consistent basis, to the asset

• projections for cash outflows include: o those for day-to-day servicing of the

asset o those for future overheads that can

be attributed directly, or allocated on a reasonable and consistent basis, to the use of the asset

o those expected to be incurred before an asset is ready for use or sale

• net cash flows to be received or paid for the disposal of the asset at the end of its useful life

• net cash flows relating to a restructuring where the entity has committed to the restructuring, as defined by IAS 36.46

• cash flows from assets that generate cash flows that are largely independent of the asset under review

• cash outflows related to obligations recognized as liabilities (e.g., payables, pensions or provisions)

• future cash outflows or related cost sav-ings or benefits expected to arise from a future restructuring to which an entity has not committed

• future cash outflows that will improve or enhance the performance of the asset, or the related cash inflows that are expected to arise from such outflows

• cash inflows or outflows from financing activities

• income tax receipts or payments

23IAS 36 Impairment of Assets

June 2013

The following insight looks at the issue of what to include in cash flows. Note the date of the NIFRIC. Even though some of the NIFRICs are older, they may still provide some insight into how the standards are interpreted by the stan-dard setters.

APPLICATION INSIGHTS

Calculation of value in use

Source NIFRIC

Meeting Date November 2010

Insight

The following insights were obtained from “IFRIC — items not taken onto the agenda” report.

Calculation of value in use

The Committee received a request for clarification on whether esti-mated future cash flows expected to arise from dividends, that are calculated using dividend discount models (DDMs), are an appropriate cash flow projection when determin-ing the calculation of value in use of a cash generating unit (CGU) in accordance with paragraph 33 of IAS 36.

The Committee noted that para-graphs 30 – 57 and paragraphs 74 – 79 of IAS 36 provide guidance on the principles to be applied in calcuating value in use of a CGU. The Committee observed that cal-culations using a DDM which values shares at the discounted value of future dividend payments, may be appropriate when calculating value in use of a single asset, for example when an entity applies IAS 36 in determining whether an investment is impaired in the separate financial statements of an entity. The Com-mittee understands that some DDMs may focus on future cash flows that are expected to be available for distribution to shareholders, rather than future cash flows from divi-dends. Such a DDM could be used to calculate value in use of a CGU in consolidated financial statements, if it is consistent with the principles and requirements in IAS 36.

The committee noted that the cur-rent principles in IAS 36 relating to the calculation of value in use of a CGU are sufficient and that any guidance that it could provide would be in the nature of application guid-ance. Consequently, the Committee decided not to add the issue to its agenda.

Details of the issues that have been considered by the IFRIC but not added to its agenda are available online at www.ifrs.org/.

24 Guide to International Financial Reporting in Canada

The example in IAS 36.78 looks at the calculation of cash flows for the VIU measurement where there are restoration costs.

APPLICATION EXAMPLE

IAS 36.78 — Calculation of cash flows where restoration costs exist

E xa mpleThe following example is provided in IAS 36.78 to illustrate calculation of cash flows where restoration costs exist.

A company operates a mine in a country where legislation requires that the owner must restore the site on completion of its mining operations. The cost of restoration includes the replacement of the overburden, which must be removed before mining operations commence. A provision for the costs to replace the overburden was recognised as soon as the overburden was removed. The amount provided was recognised as part of the cost of the mine and is being depreciated over the mine’s useful life. The carrying amount of the provision for restoration costs is CU500, which is equal to the present value of the restoration costs.

The entity is testing the mine for impairment. The cash-generating unit for the mine is the mine as a whole. The entity has received various offers to buy the mine at a price of around CU800. This price reflects the fact that the buyer will assume the obligation to restore the overburden. Disposal costs for the mine are negligible. The value in use of the mine is approximately CU1,200, excluding restoration costs. The carrying amount of the mine is CU1,000.

The cash-generating unit’s fair value less costs of disposal is CU800. This amount considers restoration costs that have already been provided for. As a consequence, the value in use for the cash-generating unit is determined after consideration of the restoration costs and is estimated to be CU700 (CU1,200 less CU500). The carrying amount of the cash-generating unit is CU500, which is the carrying amount of the mine (CU1,000) less the carrying amount of the provision for restoration costs (CU500). Therefore, the recov-erable amount of the cash-generating unit exceeds its carrying amount.

This calculation must reflect the following elements, either as adjustments to the future cash flows or as adjustments to the discount rate:• expectations about possible variations in the amount or timing of future

cash flows;• the premium for bearing the uncertainty inherent in the asset; and• other factors that market participants would reflect in pricing the future

cash flows.

The discount rate used must be a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the future cash flow estimates have not been adjusted. This represents the return investors would require if they were to choose an investment that would generate cash flows of the same amounts, timing and risk profile as those the entity expects from the asset. The discount rate is, therefore, inde-pendent of the way the asset is financed.

25IAS 36 Impairment of Assets

June 2013

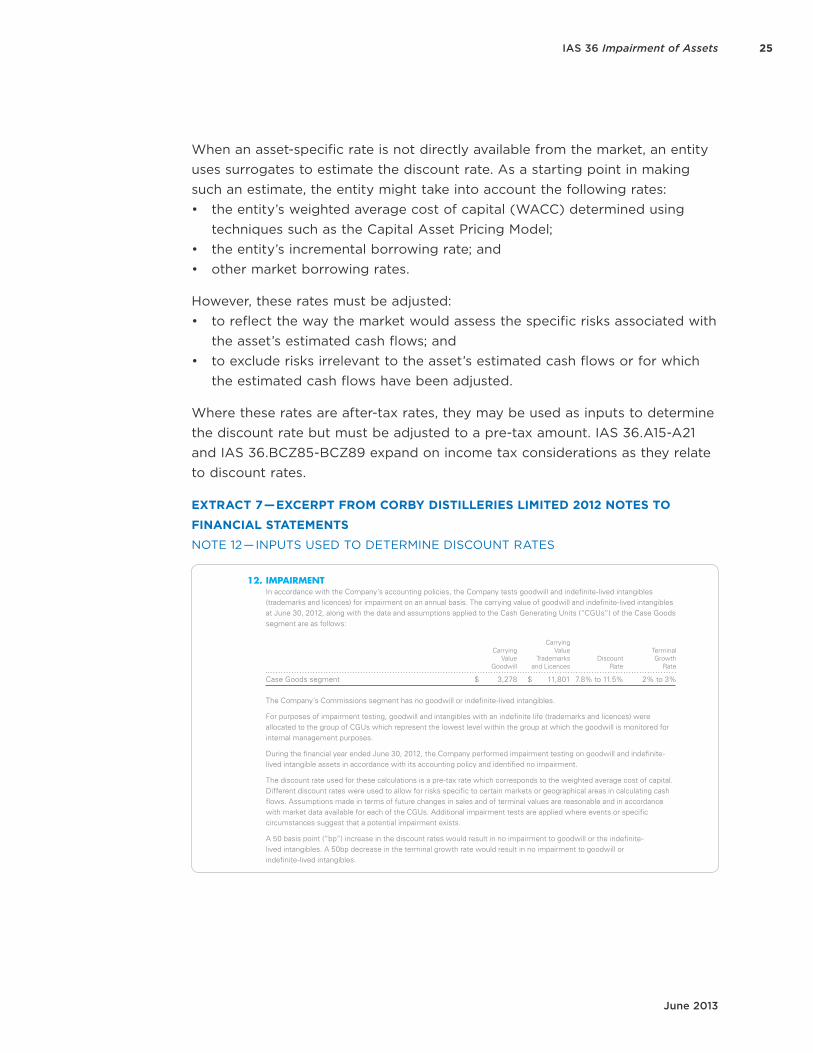

When an asset-specific rate is not directly available from the market, an entity uses surrogates to estimate the discount rate. As a starting point in making such an estimate, the entity might take into account the following rates:• the entity’s weighted average cost of capital (WACC) determined using

techniques such as the Capital Asset Pricing Model;• the entity’s incremental borrowing rate; and• other market borrowing rates.

However, these rates must be adjusted:• to reflect the way the market would assess the specific risks associated with

the asset’s estimated cash flows; and• to exclude risks irrelevant to the asset’s estimated cash flows or for which

the estimated cash flows have been adjusted.

Where these rates are after-tax rates, they may be used as inputs to determine the discount rate but must be adjusted to a pre-tax amount. IAS 36.A15-A21 and IAS 36.BCZ85-BCZ89 expand on income tax considerations as they relate to discount rates.

EXTRACT 7 — EXCERPT FROM CORBY DISTILLERIES LIMITED 2012 NOTES TO

FINANCIAL STATEMENTS

NOTE 12 — INPUTS USED TO DETERMINE DISCOUNT RATES

Corby Distilleries limiteD | AnnuAl report 2012 63

notes to the consolidated financial stateMents

12. iMPairMentin accordance with the Company’s accounting policies, the Company tests goodwill and indefinite-lived intangibles (trademarks and licences) for impairment on an annual basis. the carrying value of goodwill and indefinite-lived intangibles at June 30, 2012, along with the data and assumptions applied to the Cash Generating units (“CGus”) of the Case Goods segment are as follows:

Carrying Carrying Value terminal

Value trademarks Discount Growth Goodwill and licences rate rate

Case Goods segment $ 3,278 $ 11,801 7.8% to 11.5% 2% to 3%

the Company’s Commissions segment has no goodwill or indefinite-lived intangibles.

For purposes of impairment testing, goodwill and intangibles with an indefinite life (trademarks and licences) were allocated to the group of CGus which represent the lowest level within the group at which the goodwill is monitored for internal management purposes.

During the financial year ended June 30, 2012, the Company performed impairment testing on goodwill and indefinite-lived intangible assets in accordance with its accounting policy and identified no impairment.