Embed Size (px)

Citation preview

1

GST ON BANKING SECTOR

Compiled by

CA Atul Kumar Gupta B.Com (H), FCA, FCMA, LLB,

MIMA, CIQA, PGDEMM

Mobile: 9810103611

Email: [email protected]

2

3

Preface

The indirect taxation in our country has underwent a paradigm shift from

various taxes to one and single tax i.e. Goods and Services Tax. It has

subsumed more than 16 Central and State Taxes, thus providing various

advantages to economy. The changes in the process of taxation led to changes

in procedures and compliances across all sectors.

The Banking industry’s contribution towards GDP is continuously increasing

year by year. Implementation of GST has become imperative for the auditors

to check and examine each and every banking activity to ensure Goods and

service tax compliance not only on the revenue side but also on expenditure

side. The nature and varieties of transactions which banking industries have

been undertaking, the assignment of auditing of banking industries has

become peculiarly important.

In this book GST- Banking Sector, we have endeavored to incorporate all the

provisions of the GST which are relevant from the perspective of an audit of

a Banking Sector. Provisions are duly updated upto 20th March, 2018. We

have also incorporated the checklist along with the clarification to allow the

auditors to conduct the audit in lucid manner. CA Kanika Agarwal & Kartika

Jain under the guidance of CA Vishal Gill supported me in gathering the

provisions related to banking sector and preparation of checklist to make

these efforts really valuable.

I hope the book will support the readers in their upcoming bank audits on

GST.

New Delhi Atul Kumar Gupta

March 2018

4

5

Index

Chapter

No. Chapter Name Page No.

1. Taxability of Incomes Earned By Banks 7 – 18

2. Expense Incurred By Banks 19 – 23

3. Input Tax Credit 24 – 28

4. Procedural compliances under GST 29 – 31

5. Summarised Checklist for GST Audit of

Banks 32 – 43

6

7

Chapter 1

Taxability of Incomes Earned By Banks

During the last 30 years since nationalization tremendous changes have taken place in the

financial markets as well as in the banking industry. The growth in the Indian Banking

Industry has been more qualitative than quantitative and it is expected to remain the same

in the coming years. Banks have been given greater freedom to frame their own policies.

The banks have shed their traditional functions and have been innovating, improving and

coming out with new types of services to cater emerging needs of their Customer.

In pre-GST regime, service tax was applicable on most of the services provided by banks

however interest was outside the ambit of service tax. With introduction of GST, these

services are subject to GST at the rate of 18% instead of 15% service tax rate that was

being charged earlier. Further, with the introduction of GST, the states are empowered to

levy SGST on services. Accordingly, on the same activity, there is two levies, namely

Central GST(CGST) and State GST(SGST), levied and administered by the Central

Government and State Government respectively.

Banks provide different types of services to its customers for which it earns variety of

incomes. There are two broad sources of bank income or revenues i.e. Interest Income or

Fund Based Income and Non-Interest Income or Non-fund Based Income. All such

incomes are recorded in the books of accounts under various heads which we have to

analyse and decide taxability on the same. Some incomes so earned and their taxability are

as under:

1. Interest income

Taking deposits and lending money is the most basic function of a bank. Under pre-GST

regime, income earned by way of interest was excluded from service tax by way of entry

(n) of the negative list. On similar line, in GST regime, income earned by way of interest

income is excluded by way of entry 27(a) of Notification No. 12/2017-Central tax (Rate)

and entry 28 of Notification No. 09/2017-Integrated Tax (Rate). According to the aforesaid

notifications interest or discount earned by way of extending deposits, loans or advances

is exempt from GST. However, interest income earned by way of issuing or maintaining

credit cards are not included in the said exemption notification, so GST is levied on such

interest income.

For the purpose of this exemption, “interest” means interest payable in any manner in

respect of any moneys borrowed or debt incurred (including a deposit, claim or other

similar right or obligation) but does not include any service fee or other charge in respect

of the moneys borrowed or debt incurred or in respect of any credit facility which has not

been utilized.

Therefore, for the auditor it is essential to check whether the income is rightly characterized

as ‘interest’ to enjoy the exclusion from GST. Special focus should be given on interest

involved in credit card services leviable to GST.

8

2. Commission income

Banks earns commission income from its various contractual arrangements for distribution

of products and solutions including agreements obtained in co-ordination between banks.

GST would be leviable on the commission income received by them and some examples

are discussed here by way of illustration:

(a) M/s. A Ltd. wants to invest in fixed securities / bonds. HDFC bank has exclusive

rights for subscribing these securities therefore HDFC bank gets 2% commission on

the amounts so subscribed by Mr. A. For the period 2017-18, the bank earns 15 crores

of commission from such subscription which is recorded as ‘Other Incomes’. The

auditor has to check whether GST is appropriately disbursed on the said amount. If

the tax is not discharged then appropriate disclosure would be required. Discrepancy

in the returns filed and liability as determined may be disclosed. Interest being

mandatory may be suitably included in the disclosure. Suitable disclosure whether

any contingency exists in respect of applicable penalty may also be appropriate.

(b) ABC bank gets 1% commission from private companies for providing them

investment exposure in foreign markets. The same is liable for payment of GST and

appropriate tax treatment should be followed and suggested. Disclosures as discussed

above may be considered, if any tax liability is found to be unpaid.

In general trade practice, investment related activities are performed by another group

company. On the other hand, banking company provides leads to such investment company

for which they get some percent as commission. Further, this transaction is executed

between related parties therefore auditor should also check valuation of the transaction.

GST will apply even of this transaction is executed at nil value.

3. Brokerage income

A brokerage fee is charged to facilitate trading or to administer investment or other

accounts. In general trade practice, such income is either earned by security section of the

bank or by a group company. In case, this income is earned by group company, banking

company receive referral commission for referral of leads to security company. In this

scenario, auditor should also check taxability of services provided free of cost and

valuation of supply. Taxability has to be determined and appropriate tax should be

disbursed as the same is liable for payment of GST.

4. Agency charges

Banks also performs certain agency functions for and on behalf of their customers. Such

agency services are of immense value to the people at large. Under such arrangements,

banks act as a facilitator/collection center, and in lieu of provision of such services banks

collects certain fees or charges. Under GST, such charges or fees collected are taxable. The

various agency services rendered by the banks are as: Collection and payment of Credit

instruments, Collection of dividends on shares, Execution of standing orders etc.

9

The auditor needs to analyse the relevant agreements entered and has to study the flow of

consideration and thereafter decide taxability and the amount on which GST would be

applicable.

5. Portfolio management service:

Generally, the said services are being provided by different entities within the banking

sector. Due to stiff competition and one-stop window for priority customer’s (i.e. customers

who are depositing amount beyond a certain limits) only one person provides all such

services and thereafter relevant commissions are split between entities or costs are shared.

Under such situations, such commission splitting has to be analysed in great details and

appropriate tax treatment adopted be reviewed for compliance with applicable provisions.

In addition to decide taxability, auditor should also check provisions related to valuation.

6. Account maintenance charges:

It is a common practice that in most of the banks certain charges are recovered towards

account maintenance. These charges are generally charged in case customer fails to

maintain minimum average balance. These charges are nominal but the same is liable for

payment of GST. Accordingly, auditor should do well to check on this aspect of taxability

and ensure compliance.

7. Credit/Debit card charges:

Income earned by banks by way of issuance and maintenance of debit or credit card is

subject to GST. Also, GST is chargeable on the interest income involved in credit card

services, as the same is excluded by entry no. entry 27(a) of Notification No. 12/2017-

Central tax (Rate) and entry 28 of Notification No. 09/2017-Integrated Tax (Rate).

Auditor should carefully examine such transactions and appropriate disclosures be made

in case of non- compliance with relevant tax provisions.

8. Locker charges

Rental charges earned by banks for providing locker facility to its customers on annual

basis are subject to GST. There can be different modes of arrangement for availing such

income but such incomes are liable for payment of GST.

For e.g: Mr A wants to open a locker at ABC bank wherein the bank has an option for

opening a locker:

a) Make an FD of Rs. 50,000/- and pay an annual charge of Rs. 5000/-.

b) Make an FD of Rs. 75,000/- and pay an annual charge of Rs. 2500/-.

c) Make an FD of Rs. 2,00,000/- and do not pay any annual charge.

In each case, the auditor has to analyse the tax position and thereafter decide taxability on

the same i.e. under all the options whether GST is payable on FD interest + annual charge

or only annual charge or there is some different mechanism of determining taxability for

the said transactions.

10

9. Demand draft charges

Banks charges certain charges from its customers for preparation of demand drafts

including online requests. There is no standard charges for making a demand draft and the

charges usually varies from bank to bank and also vary with the value of the demand draft.

GST will be chargeable on such charges. Further, some banks have a policy, where such

charges are waived for issue of Demand Draft to all salary account holder. GST is also

applicable in case of free supply of service to related parties.

10. Digital payment facilities

Banks charges some convenience fees from the person who accepts payment through debit

card, credit card or through other some other card service. The charges earned by the bank

are chargeable to GST.

Further, accordingly to the entry no. 34 of Notification No. 12/2017-Central tax (Rate) and

entry no. 35 of Notification no 9/2017-Integrated Tax (Rate), No GST will be payable in

respect to services provided by bank, to any person in relation to settlement of an amount

up to Rs. 2000 in a single transaction transacted through credit card, debit card or charge

card or other payment card service.

11. Sale and purchase of foreign currency

Banking companies receiving consideration for providing services by way of securities and

foreign exchange broking and purchase or sale of foreign currency, including money

changing is chargeable to GST. However, exemption from payment of GST has been

provided when banks does inter-bank transactions of sale or purchase of foreign currency

or transactions with authorized dealers of money changing. Such exemption is provided

under entry no 27(b) of Notification No. 12/2017-Central tax (Rate) and entry 28(b) of

Notification No. 09/2017-Integrated Tax (Rate)

The Auditor shall carefully bifurcate the services provided by banks to other banks or

authorized dealers and to other customers, so that GST liability can be calculated on the

services provided to customers (other than banks and authorized dealers of money

changing) and exemption can be claimed on transaction between other banking companies

and authorized money changers.

12. Activities covered under Schedule I of CGST Act

Earlier under service tax laws, no tax was required to be paid for the service provided

without consideration. However, under GST, there are some exceptions to the requirement

of “Consideration” as a pre-condition for a supply to be known as supply under GST.

Schedule I of the CGST Act, 2017, provides the activities that shall be treated as supply of

goods/services even if made without consideration. Some of the supplies which are relevant

with respect to the banking sector are explained as under:

i. Permanent transfer or disposal of business assets where input tax credit has been

availed on such assets.

11

ii. Inter Unit Supply: Supply of goods/ services or both between related persons or

between distinct persons as specified in section 25, when made in the course or

furtherance of business.

However, now any supply of goods or services or both supplied or received by one branch

bank to another or by Head office bank to branch bank or vice versa without consideration,

shall be considered as supply under GST for payment of tax. Similarly, the activity

performed by employer to employee without consideration will be taxable under GST,

except where the value such supply does not exceed Rs. 50,000 in a financial year.

This such cases, for the purpose of payment of tax, value will be arrived by following the

Section 15 of the CGST, Act. (i.e. Rule 28 of the valuation rules)

Transactions without consideration are very difficult to track as these are generally not

captured in books of accounts therefore auditor should apply substantial audit procedure to

check compliances w.r.t. valuation and payment of GST thereon.

13. Other incomes

PROVISIONS OF PLACE OF SUPPLY APPLICABLE IN CASE OF

BANKING SERVICES

GST is a destination based tax i.e. consumption tax, which means that tax will be levied

where goods and services are consumed and would accrue to that State. There are three

levels to taxes under GST, i.e. IGST, SGST, CGST based on the place of ‘supply’, so

determined. Integrated Goods and Service Tax (IGST) is levied where transaction is inter-

state, and CGST & SGST is levied where the transaction is intra-state. The need for

determination of Place of Supply of goods or services is very important as it would

determine the nature of tax to be paid.

In banking industry, most of the banks have a pan-India presence which means they are

required to register in ALL the states. In addition to this, banks provide services to their

own branches and also to other banks. The transactions between the branches are also

taxable under GST.

Nature of income Taxability

Penalty for non-maintenance of Monthly average

balance

GST chargeable

Issuance of cheque book either for current/ saving

account

GST chargeable

Fees charged for Issuance of duplicate passbook GST chargeable

Bank Guarantees fees GST chargeable

NEFT/RTGS charges through net banking/Mobile

banking

GST chargeable

ATM charges GST chargeable

Fees charged for issuance Interest Certificates for all

segments

GST chargeable

12

It is interesting to know the place of business under banking sector. In order to determine

the GST on banking services, it would be necessary to determine the place of supply of

services. As per the GST law, even though the place of supply can be tracked it will be

cumbersome tasks and add significantly to the compliance cost.

Need as to why an accurate determination of place of supply is important under GST

• Where wrong taxes have been paid on the basis of the wrong classification, refund will

have to be claimed by the taxpayer

• The taxpayer will have to pay the correct tax along with interest for delay on the basis

of revised/correct classification

• Also, correct determination of place of supply will help us in knowing the incidence of

tax. As if place of supply is determined as a place outside India, then tax will not have

to be paid on that transaction.

Under GST, provisions for place of supply is governed by the Section 12 & 13 of the IGST

Act, 2017.

Place of Supply of services, where location of supplier and the location of recipient is

in India

In case, where the location of the banks and location of the recipient of service is in India,

section 12(12) of the IGST Act, 2017, provides for the place of supply of services.

According to the said section, the place of supply of services shall be the location of service

receiver on the records of banks and where location of receiver is not mentioned on the

records of the banks, the place of supply shall be the location of the banks.

According to Section 12(12) of IGST Act,2017, the place of supply of banking and other

financial services including stock broking services to any person shall be the location of

the recipient of services on the records of the supplier of services. However, in case the

location of the recipient of services is not on the records of the supplier, the place of supply

shall be location of the supplier of services. “

For example, Delhi branch of M/s ABC Bank provides the following services to the

following persons. Determine the place of supply of the services.

As far as place of supply of ‘other income’ earned by banks are concerned place of

provision of service depend on nature of services and auditor should determine the place

of provision on case to case basis e.g. place of provision of renting of immovable property

service is location of immovable property ir-respective of location of recipient of service.

For services not specified under section 12(3) to 12(14) of the IGST Act, 2017 e.g.

commission income, place of supply of service is determined as under:

a) Services made to a registered person shall be the location of such person;

b) Services made to any person other than a registered person shall be-

a. the location of the recipient where the address on record exists; and

b. the location of the supplier of services in other cases.

Place of Supply of services, where location of supplier or the location of recipient is

outside India (i.e. Cross border supply of services)

13

In case, where the location of the banks or location of the recipient of service is outside

India, section 13(8) of the IGST Act, 2017, provides for the place of supply of services.

According to the said section, the place of supply of services shall be the location of service

provider.

For example: ABC Inc. operates an NRO account with SBI, Mumbai and avail services of

cheque clearing, loan processing, NEFT clearing charges and so on. The place of supply

of services in respect of this service shall be location of services provider i.e. the location

of the banking institution SBI (Mumbai) which is in the taxable territory. Hence IGST will

be chargeable on these transactions.

As far as place of supply of ‘other income’ earned by banks are concerned place of

provision of service depend on nature of services and auditor should determine the place

of provision on case to case basis e.g. place of provision of renting of immovable property

service is location of immovable property ir-respective of location of recipient of service.

Further, place of supply of intermediary services i.e. commission income is location of

service provider i.e. location of bank.

For services not specified under section 13(3) to 13(13) of the IGST Act, 2017 e.g.

commission income, place of supply of service is the location of the recipient of service.

Where, the location of the recipient of services is not available in the ordinary course of

business, the place of supply shall be the location of the supplier of services.

Name of service Place of supply Comments

Cheque Clearing charges

from Mr. X, an accountholder

located in Delhi

Delhi;

CGST and

SGST

shall be charged

Since the location of

recipient is available with

the bank, the place of

supply will be the location

of the service receiver.

Demand draft charges from a

customer who does not have

an account with the bank

Delhi;

CGST and

SGST

shall be charged

Since the location of the

recipient is not available

with the bank, the place of

supply will be the location

of service provider

Loan processing fees charged

from a borrower based in

Haryana and the location of

the borrower is

available with the bank

Haryana;

IGST will be

charged on such

supply

Since the location of

recipient is available with

the bank, the place of

supply will be the location

of the service receiver.

14

Under certain circumstances, it is possible that even though the person is having an bank

account in a single location, he can do the transactions across the globe through internet

banking. It is also possible that the actual recipient of such services may be different

offices/ plants of the customer situated in different States and therefore, there could be a

doubt as to whether each time, the bank would be required to capture the location of the

recipient of service for each transaction. For this purpose, it is crucial to determine the

location of recipient of service.

Section 2(14) of IGST Act, 2017 defines location of recipient of services as:—

a) where a supply is received at a place of business for which the registration has been

obtained, the location of such place of business;

b) where a supply is received at a place other than the place of business for which

registration has been obtained, that is to say, a fixed establishment elsewhere, the

location of such fixed establishment;

c) where a supply is received at more than one establishment, whether the place of

business or fixed establishment, the location of the establishment most directly

concerned with the receipt of the supply; and

d) in absence of such places, the location of the usual place of residence of the recipient

PROVISIONS OF TIME OF SUPPLY OF SERVICES APPLICABLE IN CASE OF

BANKING SERVICES

The time of supply of services in case of banks and financial services shall be earlier of the

following events:

• Date of issue of invoice or on the last date on which invoice is required to be issued.

• Date on which bank receives payment with respect to such supply.

VALUATION OF SERVICES

In GST also, ax payable on ad-valorem basis, i.e. percentage of value of the supply of

goods or services. Section 15 of the CGST Act and Determination of Value of Supply,

CGST Rules, 2017contans the provisions related to valuation of supply made in different

circumstances and to different persons.

Under GST law, taxable value is the transaction value i.e. price actually paid or payable,

provided the supplier & the recipient are not related and price is the sole consideration. In

most of the cases of regular normal trade, the invoice value will be the taxable value. For

the purpose of calculating the transaction value certain inclusions and exclusions has to be

done.

Section 15(2) of the CGST Act, 2017, provides for the following inclusions in the value of

supply:

i. Any taxes, fees, charges levied under any law other than CGST Act, SGST Act,

UTGST Act and the GST(Compensation to States) Act, 2017, if charged separately by

the supplier.

ii. expenses incurred by the recipient on behalf of the supplier

iii. incidental expenses like commission & packing incurred by the supplier

15

iv. interest or late fees or penalty for delayed payment of any consideration for any supply

and

v. direct subsidies (except government subsidies) are required to be added to the price (if

not already added) to arrive at the taxable value.

Exclusions of discounts

Discounts like trade discount, quantity discount etc. are part of the normal trade and

commerce. Therefore, pre-supply discounts i.e. discounts recorded in the invoice have been

allowed to be excluded while determining the taxable value.

Discounts provided after the supply can also be excluded while determining the taxable

value, provided two conditions are met, namely:

a) discount is established in terms of a pre supply agreement between the supplier & the

recipient and such discount is linked to relevant invoices

b) input tax credit attributable to the discounts is reversed by the recipient

However, to determine value of certain specific transactions, Determination of Value of

Supply rules have been prescribed in CGST Rules, 2017.

Determination of value in respect of few specific supplies

A. Special provisions related to determination of value of service of purchase and

sale of foreign currency including money changing

Since banking sector also provides services of purchase and sale of foreign currency to its

customers, which is chargeable to GST, the need for valuation of the same arises. However,

The Rule 32(2) of the CGST Rules provides the special provisions for valuation of the said

services in the following manner:

Option 1

Case 1: Transaction where one of the currencies exchanged is Indian Rupees

Taxable value is difference between buying rate or selling rate of currency and RBI

reference rate for that currency at the time of exchange multiplied by total units of foreign

currency.

However, if RBI reference rate for a currency is not available then taxable value is 1% of

the gross amount of Indian Rupees provided/ received by the person changing the money.

For example, on 1st November,2017, Mr. A converted USD 100 into INR 6,200 (INR 62

per USD) through ICICI Bank. RBI’s reference rate for buying and selling was Rs. 61/61.5

respectively on such date. Now the value of supply will be: (62-61)*100 = INR 100

Thus the value of supply for ICICI Bank will be INR 100 and GST will be levied on this

amount.

16

In above example, if the reference rate is not available then 1% of INR 6,200 i.e INR 62

will be the value of supply of service.

Case 2: Transaction where neither of the currencies exchanged is Indian Rupees Taxable

value will be 1% of the lesser of the two amounts the person changing the money would

have received by converting (at RBI reference rate) any of the two currencies in Indian

Rupees.

For example, in case USD is converted against EURO, as per the above rule, both these

currencies will be converted into INR terms and the value of supply will be 1% of the lesser

amount.

Option 2

The banking companies providing the said services may also exercise the following option

to ascertain the taxable value i.e.:

• One percent of the gross amount of currency exchanged for an amount upto one lakh

rupees, subject to minimum amount of two hundred and fifty rupees

• One thousand rupees and half of a percent of the gross amount of currency exchanged

for an amount exceeding one lakh rupees and up to ten lakh rupees

• Five thousand rupees and one tenth of a percent of the gross amount of currency

exchanged for an amount exceeding ten lakhs rupees subject to a maximum amount of

sixty thousand rupees

However, the option once opted, the banks cannot withdraw it during the remaining part of

the financial year. Auditor should check valuation method opted by bank and accordingly

payment of tax.

B. Valuation of services between the distinct and related persons (excluding agents)

Generally, banks would have lot of common/ shared services being supported from Head

Office such as call centre, security software etc. Further, many times one branch would

internally provide service to other branches for example: resolving issue of a customer

having PAN India accounts, providing local information etc. to other branches etc.

Under pre-GST regime, transactions between branches were not subjected to any taxes

however, under GST regime this is taxable. Transactions between two branches of the same

bank attract GST. In such cases, according to Rule 28 of the CGST Rules, 2017, for the

purpose of valuation, following values have to be taken sequentially:

i. Open Market Value

ii. Value of supply of like kind and quality.

iii. Value of supply based on cost i.e. cost of supply plus 10% mark-up. (Rule 30 of the

CGST Rules)

iv. Value of supply determined by using reasonable means consistent with principles &

general provisions of GST law. (Best Judgement method as per Rule 31 of the Rules)

However, if the recipient is eligible for full input tax credit, the invoice value will be

accepted as taxable value. It has also been provided that where the goods being supplied

17

are intended for further supply as such be the recipient, the value shall, at the option of the

supplier, be an amount equivalent to 90% of the price charged for the supply of goods of

like kind and quality by the recipient to his unrelated customer.

EXEMPTIONS AVAILABLE TO BANKING INDUSTRY

The Central Government vide Notification No. 12/2017-Central Tax (Rate) and

Notification on the recommendation of the GST Council has exempted certain intra-state

supply of services from the payment of GST. The list of such services relevant for Banking

industry are as under:

1. Services by the Reserve Bank of India. [Entry no 26]

2. Services by way of—

a. extending deposits, loans or advances in so far as the consideration is represented

by way of interest or discount (other than interest involved in credit card

services);

b. inter se sale or purchase of foreign currency amongst banks or authorised dealers

of foreign exchange or amongst banks and such dealers. [Entry no. 27]

3. Services by an acquiring bank, to any person in relation to settlement of an amount

upto Rs. 2000 in a single transaction transacted through credit card, debit card, charge

card or other payment card service. [Entry no. 34]

“Acquiring bank” means any banking company, financial institution including non-

banking financial company or any other person, who makes the payment to any person

who accepts such card.

4. Services by way of collection of contribution under the Atal Pension Yojana. [Entry

no. 37]

5. Services by way of collection of contribution under any pension scheme of the State

Governments. [Entry no. 38]

6. Services by the following persons in respective capacities – (a) business facilitator or

a business correspondent to a banking company with respect to accounts in its rural

area branch; (b) any person as an intermediary to a business facilitator or a business

correspondent with respect to services mentioned in entry (a); or (c) business

facilitator or a business correspondent to an insurance company in a rural area. [Entry

No. 39]

7. Services provided to the Central Government, State Government, Union territory

under any insurance scheme for which total premium is paid by the Central

Government, State Government, Union territory. [Entry No. 40]

8. Services by an intermediary of financial services located in a multi services SEZ with

International Financial Services Centre (IFSC) status to a customer located outside

India for international financial services in currencies other than Indian rupees (INR).

[Entry no. 39A]

Explanation.- For the purposes of this entry, the intermediary of financial services in

IFSC is a person,-

(i) who is permitted or recognised as such by the Government of India or any

Regulator appointed for regulation of IFSC; or

(ii) who is treated as a person resident outside India under the Foreign Exchange

Management (International Financial Services Centre) Regulations, 2015; or

18

(iii) who is registered under the Insurance Regulatory and Development Authority of

India (International Financial Service Centre) Guidelines, 2015 as IFSC

Insurance Office; or (iv) who is permitted as such by Securities and Exchange

Board of India (SEBI) under the Securities and Exchange Board of India

(International Financial Services Centres) Guidelines, 2015.

ADDITIONAL EXEMPTIONS UNDER IGST

• The Central Government vide Enty No. 42 of the Notification No. 09/2017-Integrated

Tax(rate) provided that, No IGST is required to be payable by the Reserve Bank of

India under reverse charge mechanism, where services are received from outside India

in relation to management of foreign reserves.

• Also, according to Notification No. 18/2017-Integrated Tax(rate), services imported by

a unit or a developer in the Special Economic Zone for authorised operations, shall be

exempted from payment of IGST.

19

Chapter-2

Expense Incurred By Banks

There are various expenses incurred by the banks and some expenses are also in the form

of foreign payments for various reasons like import of services. In respect of certain

goods/services, banks are required to pay GST under reverse charge basis. Under GST,

there are two types of reverse charge scenarios. First is dependent on the nature of supply

and/or nature of supplier covered under section 9(3) of CGST Act and 5(3) of the IGST

Act. Second scenario is covered by section 9(4) of the CGST and 5(4) of the IGST Act,

which covers taxable supplies by any unregistered person to a registered person.

A. Supplies of services under Reverse charge mechanism (Scenario-1)

The list of goods on which tax will be paid under reverse charge has been notified under

Notification No. 4/2017-Central Tax(rate) and Notification No. 4/2017-Integrated

Tax(rate).

The list of services on which tax will be paid under reverse charge has been notified by the

Central Government on the recommendation of the Council vide Notification No. 13/2017-

Central Tax (Rate) and 10/2017-Integrated Tax (Rate).

Some of the services which are relevant with respect to the banking sector are explained in

detailed below:

1. Services provided by recovery agent:

Many banks sell their loans to third party agents to initiate recovery on their behalf. Under

this situation third party agent are hired to initiate recovery on behalf of the banks which

is purely a service transaction and liable for payment of GST.

Further, RCM is applicable on such transactions and therefore the banks who hire such

third party agents are liable for payment of GST on the fees so paid to these recovery

agents/third party agents (entry no. 8 of Notification No. 13/2017- Central Tax(rate) and

entry no.9 of 10/2017-Integrated Tax (rate)).

Banks also provide infrastructure, phone facilities and such other benefits to these third

party agents in order to perform their services. Even such value is required to be taken into

consideration while determining the value of service for the purpose of payment of GST.

2. Services provided by goods transport agency service:

If any services are provided by any goods transport agency wherein the bank pays any

freight, then GST is payable on the same by the banks. (entry no 1 of the NN. 13/2017-

CT(rate) and entry no. 2 of NN. 10/2017-IT(rate)).

20

3. Services provided by advocates:

If any services of advocates are availed by the banks, then GST is payable on the same.

Further, banks are liable to pay GST on such services received under reverse charge

mechanism.

Further banks are also liable to pay GST under RCM on services provided by senior

advocates by way of representational services before any court, tribunal or authority

directly or indirectly, even if contract for provision of such service has been entered

through another advocate, or by a firm of advocates, by way of legal services. (Entry no. 2

of NN. 13/2017-CT (rate) and entry no. 3 of NN. 10/2017-IT(rate)).

4. Services provided by arbitral tribunal:

Services availed from arbitral tribunal are covered under reverse charge mechanism

therefore banks are liable to pay GST on such services received under reverse charge

mechanism. (Entry no. 3 of NN. 13/2017-CT (rate) and entry no. 4 of NN. 10/2017-

IT(rate)).

5. Sponsorship services

Sponsorship services provided by any person are subjected to GST. Further, services

provided by way of sponsorship to any body corporate or firm is covered under reverse

charge mechanism. Thus, bank is liable to pay GST under reverse charge on sponsorship

services received from any person. Auditor should examine business promotion and other

related expenses to check compliance of reverse charge mechanism w.r.t. sponsorship

services. (Entry no. 4 of NN. 13/2017-CT (rate) and entry no. 5 of NN. 10/2017-IT(rate)).

6. Services by Directors

Under GST regime, if any service is provided by an employee to the employer in the course

of or in relation to his employment, such transactions shall not be treated as supply of

services and hence no GST is payable. Sometimes, bank receives certain services from its

directors, such services provided are chargeable to GST, provided the services provided

are not in course of or in relation to his employment. However, services provided by the

working director is considered to be the services provided in the course or in relation to the

employment not chargeable to GST, whereas services provided by the executive directors

shall be taxed under GST.

Further as per the entry no 6 of NN. 13/2017-CT(rate) and entry no. 7 of NN. 10/2017-

IT(rate), GST in respect of services provided by directors to the banks (on which GST is

applicable) shall be payable by the banks under RCM.

7. Services by Government or local authority

Services supplied by the Central Government, State Government, Union territory or local

authority to a bank excluding, -

21

(i) services by the Department of Posts by way of speed post, express parcel post, life

insurance, and agency services provided to a person other than Central Government,

State Government or Union territory or local authority;

(ii) services in relation to an aircraft or a vessel, inside or outside the precincts of a port

or an airport;

(iii) transport of goods or passengers

are covered under reverse charge mechanism therefore bank is liable to pay GST on

services received from Government or local authorities except services mentioned above

and exempted services.

8. Service provided by way of import of services:

Many banks do spend a lot of funds on procuring services from abroad. GST on such

imported services shall be payable by the receiving banks unless the services received are

exempted under any notification.

1. Bond floating expenditure:

Generally, bond floating expenditure is an expenditure which though appropriately

recorded in the books of accounts, skips the attention and the applicable taxes are not

discharged often in respect of the same. Therefore, the concerned auditor should

thoroughly inspect the books of accounts and identify all payments in foreign currency for

compliance with these provisions.

2. Underwriting charges:

If underwriting charges are paid in foreign currency to an underwriter who is located

outside India, then GST is imminent on such transactions. Appropriate ledgers, contracts

etc should be scrutinised in great detail and thereafter relevant disclosures should be made

regarding taxability on the same.

3. I.T infrastructure cost:

Generally, I.T infrastructure is a common cost which the banks bears on a all-India basis

and executes one common contract for the same. If the vendor is based outside India or the

technicians are outside India and payment is being disbursed in foreign currency then such

transactions attract GST. Such GST shall be payable by the banks located in India. The

auditor has to scrutinise the same in detail and determine tax compliance.

B. Services received form unregistered persons (Scenario-2)

Under GST regime, section 9(4) of CGST Act and 5(4) of the IGST act, provides that the

tax in respect of the supply of taxable goods or services or both by a supplier, who is not

registered, to a registered person shall be paid by such person on reverse charge basis as

the recipient and all the provisions of this Act shall apply to such recipient as if he is the

person liable for paying the tax in relation to the supply of such goods or services or both.

However, vide NN. 08/2017-Central Tax(rate), Government has exempted intra-State

supplies of goods or services or both received by a registered person from any unregistered

22

supplier subject to the condition that aggregate value of such supplies of goods or service

or both does not exceeds five thousand rupees in a day. With effect from 13.10.2017 till

31.03.2018, scope of this exemption has been extended, vide NN. 38/2017-Central

Tax(rate), to every situation by removing limit of five thousand rupees in a day meaning

thereby benefit of exemption is available ir-respective amount of expenditure per day.

Therefore, no CGST and SGST or UTGST has to be paid by the banks under reverse charge

mechanism when receiving goods and/or services from the un-registered person from 13th

October, 2017 till 31st March, 2018 however for the period 1st July, 2017 to 12th October,

2017, auditor should check payment of GST under reverse charge mechanism keeping in

mind the daily expenditure limit of Rs. 5,000.

Recently, GST Council in its 26th GST Council Meet concluded on 10th March, 2018 has

recommended to defer the liability to pay tax on reverse charge basis in cases of supplies

intra-state supplies made by un-registered persons to registered persons till 30th June,

2018. But, no notification has been issued yet in respect of such deferment by CBEC.

Time of Supply of goods/services under reverse charge mechanism

The time of supply is the point when the supply is liable to GST. In reverse charge, the

time of supply is different from that under forward charge. In case of supply of goods, time

of supply shall be the earliest of:

a. date of receipt of goods; or

b. date of payment as per books of account or date of debit in bank account, whichever

is earlier; or

c. the date immediately following 30 days from the date of issue of invoice or similar

other document.

In case of supply of services, time of supply shall be earliest of:

• Date immediately following 60 days of issuance of invoice or other supporting

documents issued by the service provider.

• Date of payment as entered in the books of account of the recipient or the date on

which the payment is debited in his bank account whichever is earlier.

Further, in case the time of supply cannot be determined as per aforesaid provisions, the

time of supply shall be the date of entry in the books of accounts of the recipient.

Other compliances in respect of supplies under reverse charge

1. Any amount payable under reverse charge shall be paid by debiting the electronic cash

ledger. In other words, reverse charge liability cannot be discharged by using input

tax credit. However, after discharging reverse charge liability, credit of the same can

be taken by the recipient, if bank is otherwise eligible

2. Advance paid for reverse charge supplies is also leviable to GST.

3. In case of purchase from unregistered dealer covered under reverse charge

mechanism, bank was required to issue invoice and payment voucher.

23

4. Invoice level information in respect of all supplies attracting reverse charge, rate wise,

are to be furnished separately in the table 4B of GSTR-1.

5. Every registered person is required to keep and maintain records of all supplies

attracting payment of tax on reverse charge.

6. For the purpose of payment of tax under reverse charge mechanism, bank is required

to determine place of supply of service.

24

Chapter 3

Input Tax Credit

Under GST, the provisions in relation to input tax credit on inputs, capital goods and input

services are governed by sections 16 to 20 of the CGST Act, 2017 read with Rule 36 to 45

of the CGST Rules, 2017. The Banking companies are eligible to claim input tax credit in

respect of inputs, input services and capital goods.

Some of the technical aspects of the scheme of Input Tax Credit are as under:

A. Any registered person can avail credit of tax paid on the inward supply of goods or

services or both, which is used or intended to be used in the course or furtherance of

business

B. The pre-requisites for availing credit by registered person are:

a) Possession of tax invoice or any other specified tax paying document.

b) The goods or services has been received by the person. “Bill to ship” scenarios

also included.

c) Tax is actually paid by the supplier.

d) Return has been furnished by bank under Section 39.

e) If the inputs are received in lots, the credit will be eligible only when the last lot

of the inputs is received.

f) Payment has been made for the value of the goods or services along with the tax

within 180 days from the date of issue of invoice, failing which the amount of

credit availed by the recipient would be added to his output tax liability, with

interest. However, once the amount is paid, the recipient will be entitled to avail

the credit again. In case part payment has been made, proportionate credit would

be allowed.

C. Documents on the basis of which credit can be availed are:

a) Invoice issued by a supplier of goods or services or both

b) Invoice issued by recipient along with proof of payment of tax

c) A debit note issued by supplier

d) Bill of entry or similar document prescribed under Customs Act

e) Revised invoice

f) Document issued by Input Service Distributor

D. No ITC beyond September of the following FY to which invoice pertains or date of

filing of annual return, whichever is earlier.

E. ITC is not available in some cases as mentioned in section 17(5) of CGST Act, 2017.

(Blocked credit). Some of them are as follows:

a) motor vehicles and other conveyances except under certain circumstances.

b) goods and/or services provided in relation to:

(i) Food and beverages, outdoor catering, beauty treatment, health services,

cosmetic and plastic surgery, except under specified circumstances;

(ii) Membership of a club, health and fitness center;

(iii) Rent-a-cab, life insurance, health insurance except where it is obligatory for

an employer under any law;

25

(iv) Travel benefits extended to employees on vacation such as leave or home

travel concession;

c) Works contract services when supplied for construction of immovable property,

other than plant & machinery, except where it is an input service for further

supply of works contract;

d) Goods or services received by a taxable person for construction of immovable

property on his own account, other than plant & machinery, even when used in

course or furtherance of business;

e) Goods and/or services on which tax has been paid under composition scheme;

f) Goods and/or services used for private or personal consumption, to the extent

they are so consumed;

g) Goods lost, stolen, destroyed, written off, gifted, or free samples;

h) Any tax paid due to short payment on account of fraud, suppression, mis-

declaration, seizure, detention.

Apportionment of Credits

1. Credit admissibility if goods and/or services are used for providing both business

as well as non-business purpose (Section 17(1))

Proportionate credit shall be available if goods or services are used partly for non-

business purpose and partly for business purposes.

2. Credit admissibility if goods and/or services are used for providing both taxable

as well as exempted supplies (Section 17(2))

In such cases, the amount of credit shall be restricted to so much of the input tax credit

as is attributable to the taxable supplies.

Special Credit provisions for Banking Companies

As per GST Act, where banking sector engaged in supplying services by way of accepting

deposits, extending loans or advances is receiving goods and/or services partly for effecting

taxable supplies including zero –rated supplies and partly for effecting exempted supplies,

then it shall have two options for the reversal of their credit. One option is given under

section 17(4) read with Rule 38 of the CGST Rules, 2017 and another is general procedure

given in section 17(2) read Rule 42 of the CGST Rules, 2017.

As per section 17(4) read with Rule 38 of the CGST Rules, 2017, the banking sector has to

avail for every month, an amount of 50% of the eligible input tax credit on the inputs,

capital goods and input services in that month and the remaining 50% input tax credit shall

be lapsed.

The option once exercised by the banking companies shall not be withdrawn during the

remaining part of the financial year. Further, restriction of 50% shall not be applicable to

the tax paid on supplies made by bank to any another registered person having the same

PAN.

As per section 17(2) read with Rule 42 , the credit reversal shall be as under:

Eligible ITC: ITC directly related to taxable supplies including zero rated supplies (T4)

26

• Proportionate common ITC related to taxable supplies including zero rated supplies (C3)

Whereas proportionate common ITC (C3) related to taxable supplies shall be calculated

as:

Common ITC (C2 Refer Note-1) - ITC attributable to exempted supply (D1 Refer Note-2)

and the amount of credit attributable to non-business purposes (D2 Refer Note-3)

Note-1

Common ITC (C2) =Total ITC (T) - ITC directly related to non-business purpose (T1) ITC

directly related to exempted supply(T2)-ineligible ITC under Section 17 (5) of CGST Act

like outdoor catering, health services, rent a cab etc. (T3)- ITC directly related to taxable

supplies including zero rated supplies (T4)

Note-2

* where the registered person does not have any turnover during the said tax period or the

aggregate value of exempted and total turnover are not available, such values shall be taken

from previous to the month.

Note-3

The amount of credit attributable to non-business purposes (D2) = Common ITC (C2) *

5%

Note-4:

The input tax credit determined as per above provisions (1) shall be calculated finally for

the financial year before the due date for filing the return for the month of September

following the end of the financial year to which such credit relates and where final value

of ‘D1’ and ‘D2’ exceeds the aggregate of the amounts of D1 and D2 determined earlier

then, such excess shall be added to the output tax liability of the registered person for a

month not later than the month of September following the end of the financial year to

which such credit relates. However, in opposite case, such excess amount shall be claimed

as credit by the registered person in his return for a month not later than the month of

September following the end of the financial year to which such credit relates.

Note-5:

ITC

attributable

to exempted

supply (D1)

= Common

ITC (C2) x

aggregate value of exempt

supplies during the tax period*

total turnover of the registered

person during the tax period

27

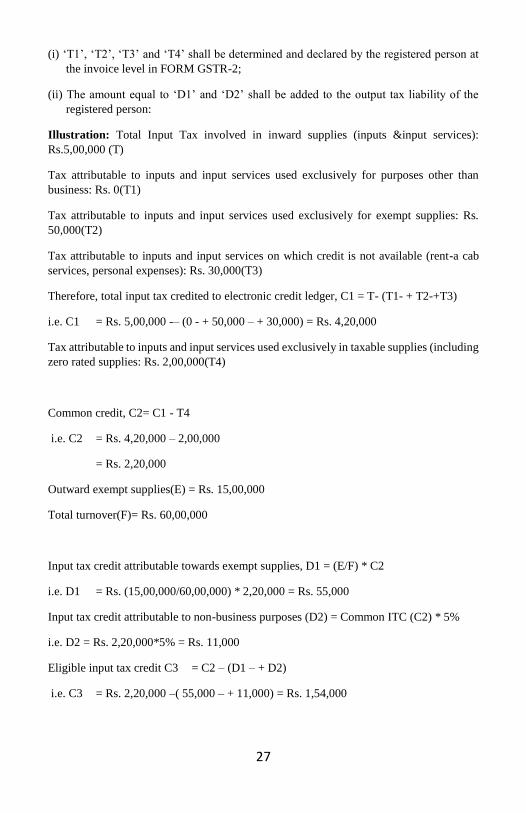

(i) ‘T1’, ‘T2’, ‘T3’ and ‘T4’ shall be determined and declared by the registered person at

the invoice level in FORM GSTR-2;

(ii) The amount equal to ‘D1’ and ‘D2’ shall be added to the output tax liability of the

registered person:

Illustration: Total Input Tax involved in inward supplies (inputs &input services):

Rs.5,00,000 (T)

Tax attributable to inputs and input services used exclusively for purposes other than

business: Rs. 0(T1)

Tax attributable to inputs and input services used exclusively for exempt supplies: Rs.

50,000(T2)

Tax attributable to inputs and input services on which credit is not available (rent-a cab

services, personal expenses): Rs. 30,000(T3)

Therefore, total input tax credited to electronic credit ledger, C1 = T- (T1- + T2-+T3)

i.e. C1 = Rs. 5,00,000 -– (0 - + 50,000 – + 30,000) = Rs. 4,20,000

Tax attributable to inputs and input services used exclusively in taxable supplies (including

zero rated supplies: Rs. 2,00,000(T4)

Common credit, C2= C1 - T4

i.e. C2 = Rs. 4,20,000 – 2,00,000

= Rs. 2,20,000

Outward exempt supplies(E) = Rs. 15,00,000

Total turnover(F)= Rs. 60,00,000

Input tax credit attributable towards exempt supplies, D1 = (E/F) * C2

i.e. D1 = Rs. (15,00,000/60,00,000) * 2,20,000 = Rs. 55,000

Input tax credit attributable to non-business purposes (D2) = Common ITC (C2) * 5%

i.e. D2 = Rs. 2,20,000*5% = Rs. 11,000

Eligible input tax credit C3 = C2 – (D1 – + D2)

i.e. C3 = Rs. 2,20,000 –( 55,000 – + 11,000) = Rs. 1,54,000

28

Total eligible credit = Rs. 2,00,000(t4) + 1,54,000(C3) = Rs. 3,54,000

Also, Option once opted cannot be changed during the financial year.

Being an auditor, we can check whether, concerned branch is reversing the Input Tax Credit

in compliance to the above Rule. If Input Tax Credit is not reversed in compliance to the

above Rules, it shall be treated as Input Tax Credit wrongly taken and the same will be

recovered along with the interest under Section 50 of the CGST Act, 2017.

29

Chapter 4

Procedural compliances under GST

A. Registration

Earlier, most of the banks have a centralized registration under the Service Tax Laws for

all its branches located in multiple States and Union Territories. Under GST regime, banks

having branches in multiple States and Union Territories will be required to obtain

registrations in each such state and Union territory.

Further, within a State, banks with different branches will have to take single registration,

and is required to declare one place as principal place of business and other branches as

additional places of business in the registration form.

Auditor has to check that bank has declared all offices/branches except principal place of

business in the state as additional place of business.

However, separate registration for different business verticals within a State/UT may also

be obtained. In such cases, separate registration application need to be filed for each

business vertical. The meaning of business vertical has been defined under section 2(18)

of the CGST Act, 2017.

Moreover, under GST, accounting, administration, financial records etc are required to be

maintained by the banks for each state-wise separately.

B. Invoicing

Under GST, every registered person is required to issue an invoice for every supply of

goods or services. Further, it is not only necessary that only a person supplying goods or

services need to issue an invoice, but also any registered person buying goods or services

from an unregistered person need to issue a payment voucher as well as tax invoice. A tax

invoice is an important document, as it not only evidences the supply of goods or services,

but is also an essential for availing Input Tax Credit.

For banking industry, special provisions for invoicing are provided under GST Act i.e.

a. Time limitation for issuance of invoice (Rule 47 of the CGST, Rules)

- Invoice shall be issued before or after the provision of service, but within 45 days

from the date of supply of services.

- In case, taxable services are provided to the distinct persons as specified in section

25, then banks may issue the invoice before or at the time such supplier bank records

the same in its books of accounts or before the expiry of the quarter during which

the supply was made.

b. Issuance of document in lieu of invoice (Rule 54 of the CGST, Rules)

The banking companies have the option to issue a consolidated tax invoice or any

other document in lieu of tax invoice for the supply of services made during a month,

at the end of the month, either in physical form or electronically.

c. Manner of issuing invoice

30

For supplying of service, two copies of invoice are required to be issued

• Original Copy – for the recipient

• Duplicate Copy – for the supplier

d. Certain other relaxations

Banking companies may issue tax invoice or any other document, whether serially

numbered or not and issuing the invoice even without containing the address of the

recipient of service but contains the other information as provided by Rule 46 of the CGST,

Rules.

C. Payment:

• FORM GST PMT-6 Challan for deposit of GST – valid for 15 days from the date of

generation of challan.

• For delayed payment, rate of interest to be paid @ 18% p.a.

• For undue/excess claim of ITC/excess reduction in output tax liability-rate of interest

@ 24% is to be paid.

D. Returns

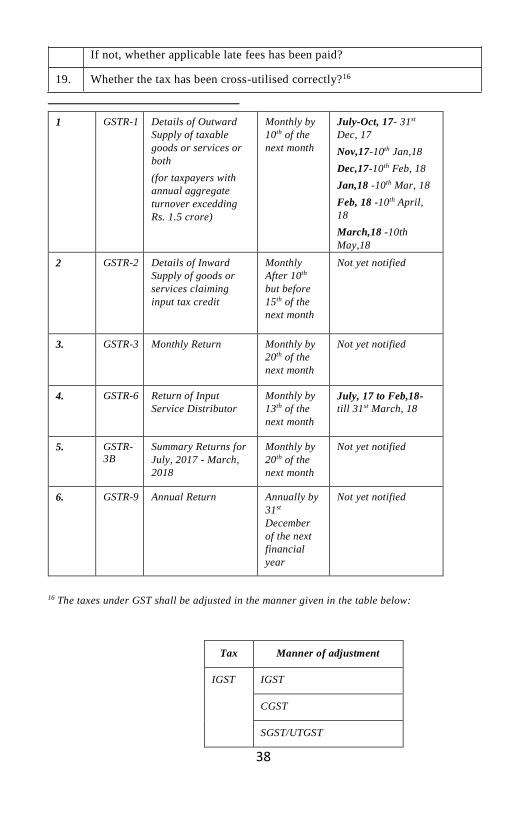

Every banking company is liable to file the following returns:

Sr.

No

Form Details to be furnished Due Date Extended date by the

Central Government

1 GSTR-1 Details of Outward

Supply of taxable

goods or services or

both

(for taxpayers with

annual aggregate

turnover excedding

Rs. 1.5 crore)

Monthly by

10th of the

next month

July-Oct, 17- 31st Dec,

17

Nov,17-10th Jan,18

Dec,17-10th Feb, 18

Jan,18 -10th Mar, 18

Feb, 18 -10th April, 18

March,18 -10th May,18

2 GSTR-2 Details of Inward

Supply of goods or

services claiming

input tax credit

Monthly

After 10th

but before

15th of the

next month

Not yet notified

3. GSTR-3 Monthly Return Monthly by

20th of the

next month

Not yet notified

4. GSTR-6 Return of Input

Service Distributor

Monthly by

13th of the

next month

July, 17 to Feb,18- till

31st March, 18

31

E. Accounts and Records

Under GST, according to section 35 read with Rule 56 of the CGST Rules, 2017, every

registered person shall keep and maintain all records at its principal place of business.

Therefore, every bank is required to keep and maintain records in respect of Inward and

outward supply of goods and/or services, Input tax credit availed, Output tax payable and

paid and other particulars as prescribed under Rule 56 of the CGST Rules. In addition to

this, banks are also required to keep and maintain true and correct account of goods or

services imported or exported or of supplies attracting payment of tax under reverse charge

along with relevant documents such as, invoices, credit notes, debit notes, receipt vouchers,

payment vouchers and refund vouchers.

Banks may keep and maintain the required accounts and other particulars in electronic

form. For maintenance of records in electronic form following requirements must be

fulfilled i.e.

• Proper electronic back-ups of records

• Produce, on demand, the relevant records or documents, duly authenticated in hard

copy or in any electronically readable format.

Further, as per Section 36 of the CGST Act, banks are required to retain such records until

the expiry of 72 months from the due date of filing of annual return for the year pertaining

to such accounts and records. The last date of filing the Annual Return is 31st December

of the following year.

Penalty for not maintaining of accounts/ records- Under GST, penalty of Rs. 10,000 is

to be paid, in case there is a failure to maintain or retain the accounts/ documents as required

by the CGST Rules.

5. GSTR-3B Summary Returns for

July, 2017 - March,

2018

Monthly by

20th of the

next month

Not yet notified

6. GSTR-9 Annual Return Annually by

31st

December of

the next

financial

year

Not yet notified

32

Chapter 5

Summarised Checklist for GST Audit of Banks

PART A: Basic Details of Assessee

1. Whether all the additional place of business has been added in the

registration form, if separate registration has not been taken for them1.

2. Whether separate registration has been taken on the basis of multiple

business verticals?2

3. If the branch is distributing the credits to distinct entity, whether separate

registration of ISD has been taken?

4. Is there any change in the information furnished in registration certificate?

Whether the registration certificate has been amended on the basis of the

same?3

1 As per Section 22 of the CGST Act, 2017, every supplier is liable to take registration from each

and every state from where it is making taxable supplies.

Assessee needs to get the registration of principal place of business from where it is making

taxable supply, further it shall mention all the additional place of business in that particular

state in the registration certificate

With reference to the checklist, an auditor should check, whether the concerned branch is

registered with the department registration certificate has been obtained or not? To check

registration details we may log in into gst.gov.in by using client’s user id and password.

2 As per section 25(2) of the CGST Act, 2017, a person seeking registration under this Act

shall be granted a single registration in a State or Union territory.

However, if a person having multiple business verticals in a State or Union territory may be

granted a separate registration for each business vertical, separately

Being an auditor, we can check that whether the branch has taken two or more registrations in

a single state on the basis of different business verticals? And if yes, does it actually form

separate business vertical?

3 As per Rule 19 of the CGST Rules, 2017, in case of any changes furnished in the registration

application, then within 15 days submit an application in FORM GST REG-14 along with the

documents relating to such documents.

An auditor can check whether FORM REG-14 has been filled on time and other provisions of

Rule 19 of the CGST Rules, 2017 has been complied accordingly?

33

5. (a) Whether prescribed accounts and records have been maintained at

principal place of business?4

(b) If the assessee is having additional place of business, whether the

accounts related to that place has been kept at such place?

PART B: EXEMPTION AVAILED

6. (a) Whether any activity in the nature of “Transaction in Money” has

been claimed as outside the definition of “Service” as per section 2(102) of

the CGST Act, 20175

(b) If yes, whether any separate consideration is charged and GST being

paid on the same.

7. (a) Whether the company is engaged in providing services related to

securities/ derivatives which does not fall under definition of services as per

4 As per section 35 of the CGST Act, 2017, every assessee shall maintain at its principal place

of business a true and correct account of:

a. production or manufacture of goods;

b. inward and outward supply of goods or services or both;

c. stock of goods; d. input tax credit availed;

e. output tax payable and paid; and

f. such other particulars as may be prescribed (Refer Rule No. 56 & 58 of the CGST Rules, 2017)

Where assessee has additional place of business then each place shall have kept accounts

related to it. An auditor can check whether all the books prescribed has been maintained at

principal place of business. Also, in case of additional place of business, accounts related to it

has been kept at such place.

5 Money has been excluded from the definition of service under section 2(102) as well as from

the definition of goods under section 2(52) of the CGST Act, 2017. Hence GST liab ility will not

apply on transaction in money. However, it is also provided that if any separate consideration

is charged by the service provider, then the same will be taxable and GST shall be payable on

such separate consideration.

For eg. A is carrying 40$ and wants to convert it in to INR. A approaches to a bank and get an

amount of Rs. 40*60=Rs.2400. In this case, no separate consideration is charged by the bank

and the transaction is merely a transaction in money. However, if the bank recovers an

additional amount say Rs. 100 for the same, it will be liable to GST payment.

34

Section 2(102) of the CGST Act, 2017.6

(b) If yes, whether any service charges collected, during the relevant

period and GST is being paid on the same. Please provide the details thereof.

8. In case, any service charges or administrative charges or entry charges are

recovered in addition to interest on a loan, advance or a deposit such as

locker rent, folio charges, loan processing fee, late payment fee, lease

management fee, rent, management fee etc. Whether GST is being paid on

the same.7

9. (a) Whether the Bank is trading in Commercial paper /Certificates of

deposits?

(b) If yes, whether any separate charges are collected and GST being paid

6 Securities /Derivatives has been excluded from the definition of goods as well as from the

definition of services under the CGST Act, 2017. Transaction in instruments are not taxabl e

however, any sort of service charge collected by the service provider for such transaction shall

be liable for the payment of tax.

Being an auditor, we can check whether GST is paid by the concerned branch on amount

recovered as an additional consideration.

7 Any services by way of extending deposits, loans or advances in so far as the consideration is

represented by way of interest or discounts is exempt. However, if any additional amount is

charged over and above interest or discounts the same would represent taxable consideration.

Services covered under this exemption category are-

Fixed deposits or saving deposits or any other such deposits in a bank or a financial

institution for which return is received by way of interest.

Providing a loan or overdraft facility or a credit limit facility in consideration for

payment of interest.

Mortgages or loans with a collateral security to the extent that the consideration for

advancing such loans or advances are represented by way of interest.

Corporate deposits to the extent that the consideration for advancing such loans and

advances are represented by way of interest or discount.

Being an auditor, we can check whether any additional amount is recovered by the concerned

branch/head office and the same is accounted for separately instead of treating it as a component

of interest/ advance.

35

on the same and provide details thereon.

10. Whether the late fees have been charged for the services supplied by bank?

If yes, whether late fees have been made part of transaction value?8

11. Whether GST is charged on interest received from credit card holders?9

12. a. Whether business assets have been transferred permanently on which

ITC has been availed without consideration?10

8 As per section 15(2)(d) of the CGST Act, 2017, any interest or late fees or penalty for delayed

payment of any consideration will be included in the value of supply.

For e.g.: If any late fees has been charged by bank for not making the payment of bank charges

then tax will be charged on late fees amount along with bank charges.

Being an auditor, we can check whether bank has charged GST on any interest or late fees

charged from customer for delayed payment. If the same has not charged then, tax shall be paid

on the same along with interest @ 18%.

9 Any services by way of extending deposits, loans or advances in so far as the consideration is

represented by way of interest or discounts is exempt under GST, but the interest received from

credit card holders have been made taxable. Since, charges received in case of credit card are

in the nature of consideration for the services rendered for using the convenience of services by

way of a credit card and hence taxable.

Being an auditor, we can check whether such late payment charges recovered by the concerned

branch are not shown as interest. These charges are taxable and GST shall be levied on the

same.

10 As per Schedule I of the CGST Act, 2017 following activities shall be treated as supply even if

made without consideration:

1. Permanent transfer or disposal of business assets where input tax credit has been availed

on such assets. 2. Supply of goods or services or both between related persons or between distinct persons

as specified in section 25, when made in the course or furtherance of business

Provided that gifts not exceeding fifty thousand rupees in value in a financial year by an

employer to an employee shall not be treated as supply of goods or services or both.

3. Supply of goods—

a. by a principal to his agent where the agent undertakes to supply such goods on behalf of the principal; or

b. by an agent to his principal where the agent undertakes to receive such goods on

behalf of the principal. 4. Import of services by a taxable person from a related person or from any of his other

establishments outside India, in the course or furtherance of business.

Even if no consideration has been charged for the above-mentioned supplies then also they will

be treated as supplies under GST. For eg: if the bank has given an old car worth Rs. 100000, to

36

b. Whether the services have been supplied to related or distinct person

without consideration?

c. Whether the gifts exceeding Rs. 50,000 has been provided to

employees?

13. Whether the assessee has the option of discharging its liability under Rule

32 of the CGST Rules, 2017. For branches dealing in purchase or sale of

foreign currency and money changing.11

If yes, whether GST liability has been discharged in manner prescribed under

the provisions.

14. Whether branches having separate registration has been treated as distinct

person?12

If yes, its valuation has been done according to the Rule 29 of the CGST

Rules, 2017?

15. Whether any services has been provided to group entities?

If yes, whether its valuation has been done according to Rule 29 of the CGST

its employees without any consideration then GST will be charged on such supplies. Therefore,

being an auditor, we can check whether any supplies mentioned in Schedule I has been made by

banks. If yes, whether the GST has been charged on the same?

11 A service provider dealing in the sale or purchase of foreign currency has the option to pay

GST in a manner as mentioned under Rule 32 of the CGST Rules, 2017 instead of discharging

its GST liability at the rate general rate.

12 As per section 25 of the CGST Act, 2017 where a person who has obtained or is required to

obtain registration in a State or Union territory in respect of an establishment, has an

establishment in another State or Union territory, then such establishments shall be treated as

establishments of distinct persons for the purposes of this Act.

Further, if any supplies have been made between the group entities of the bank, then such group

entity will be treated as related party to the assessee.

Valuation of the supplies made to distinct and related person has been treated separately. As

per Rule 28 of the CGST Rules, 2017, the value of supply shall be:

a. Open market value

b. Value of goods and services of like kind and quality, if a not available

c. Value shall be 110% of the cost, if a and b not available d. Reasonable means, if all the above points cannot be applied.

However, where the goods are intended to be supplied as such then value may be amount

equivalent to 90% of the price charged from the customers.

Being an auditor, we can check whether the transactions between distinct and related person

have been valued as per Rule 28 of the CGST Rules, 2017.

37

Rules, 2017?

16. Whether reverse charge has been paid for supplies taken from unregistered

person exceeding Rs. 5000 in a day from any or all of them. 13

(However this provision has been postponed till 31.03.2018 from 13 th

October, 2017

17. a. Is Provisions of Reverse charge as provided under section 9(3) and 9(4)

of the CGST Act, 2017 followed? 14

b. if the answer (d) is No, Specify the head of expenditure and corresponding

details ?

PART D: PAYMENT OF TAX & RETURNS

18. Whether all the returns under GST have been filled on time?15

13 As per section 9(4) of the CGST Act, 2017 if any supplies have been taken from unregistered

person then the registered taking supplies has to pay the under reverse charge. However, as per

NN 8/2017- CT(R) if the supplies do not exceed Rs. 5000 in a day from any or all suppliers, then

the tax is not to be paid under reverse charge.

Further as per NN 38/2017-CT(R) reverse charge on unregistered supplies has been deferred

till 31st March, 2018. Also, in the 26th council meeting held on 10 th March it is recommended to

defer it till 1st July, 2018.

Therefore, Auditor can check whether the reverse charge has been paid till 13 th October, 2017

for the supplies received from unregistered supplier exceeding Rs. 5000 in a day.

14 A service receiver is liable to pay tax under reverse charge for the services received under

Section 9(3) of the CGST Act 2017 read with NN 13/2017-CT(R) and under section 5(3) of the CGST Act, 2017 read with NN 10/2017-IT(R). In order to identify the amount of tax payable by

the service recipient, it is important to clearly define the nature of services received. This

point requires auditors to check the nature and description of services received by the concerned branch/head office.

15 As per GST Act, various returns have to be filled by the assesee at different deadlines. If the

same has not been filed on time then it will attract the late fees provisions. Auditor needs to

check whether the returns have been filed on time? If not, whether the correct late fees has been

paid on the same?

Various returns that are to be filed are:

Sr.No Form Details to be furnished Due Date Extended date by the

Central Government

38

If not, whether applicable late fees has been paid?

19. Whether the tax has been cross-utilised correctly?16

1 GSTR-1 Details of Outward

Supply of taxable

goods or services or

both

(for taxpayers with

annual aggregate

turnover excedding

Rs. 1.5 crore)

Monthly by