Embed Size (px)

Citation preview

PAYMENT PROCESS UNDER GST REGIME

Model Law GST

SEPTEMBER’2016

GSTPANACEA.COM CONSULTANCY PRIVATE LIMITED

New Delhi

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

1 | P a g e

To get regular updates please share your details on 7503031378

PAYMENT PROCESS UNDER GST REGIME

1. Broad Features .......................................................................................................................................... 2

2. Tax Types & Modes of Payment ............................................................................................................. 4

3. Stakeholders .............................................................................................................................................. 6

4. Basic Features ........................................................................................................................................... 7

5. MODE –I: e-Payment made through Auhtorised Bank’s Internet Banking, CC/DC ....................... 8

5.1. Issues with Payment through Credit Card ................................................................................... 9

6. MODE –II: Over the Counter (OTC) Payments.................................................................................... 10

6.1. Issues with Payment through OTC .............................................................................................. 12

7. MODE -III: NEFT/RTGS from Any Bank ............................................................................................... 12

8. Challan Correction Mechanism ............................................................................................................ 14

9. Features of Accounting Process .......................................................................................................... 14

10. Proposed Accounting System .......................................................................................................... 15

11. Banking Arrangements ...................................................................................................................... 16

11.1. e-kuber ............................................................................................................................................... 16

12. Reconciliation of Receipts ................................................................................................................ 17

13. Grievance Redressal .......................................................................................................................... 17

14. Source of this Article .......................................................................................................................... 18

15. DISCLAIMER ........................................................................................................................................ 18

16. Other Articles ....................................................................................................................................... 18

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

2 | P a g e

To get regular updates please share your details on 7503031378

PROPOSED PAYMENT PROCESS UNDER GST REGIME

n modern day taxation regime, every transaction of the tax payer with the tax administration

should be transparent, responsive and simple. It has been experience of tax administrations

that more the system and procedures are made electronic more is the efficiency of tax

administration and greater is the satisfaction of taxpayer. In this context, payment system of GST

should also be based on Information Technology which can handle both the receipt and payment

processes. [Extracts from Report of Joint committee On Business Processes for GST]

1. Broad Features

Broad features of the new payment process proposed under GST Regime is:

It is noted that under GST regime, some taxes and duties may remain outside the

purview of GST and will continue to be collected in the manner prescribed under

existing accounting procedures/rules/manuals, etc. This means that two types of

Electronic payment

Single point interface for challan generation

Ease of payment

Common challan form with auto-population features

Use of single challan and single payment instrument

Common set of authorized banks

Payment through any bank

Common Accounting Codes

I

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

3 | P a g e

To get regular updates please share your details on 7503031378

challans (one for GST and other for non-GST) will be used and accounted for by the

respective Pay and Accounts Offices (PAOs)/State AGs.

The payment processes under proposed GST regime should have the following

features:

a) Electronically generated challan from GSTN Common Portal in all modes of

payment and no use of manually prepared challan;

b) Facilitation for the taxpayer by providing hassle free, anytime, anywhere mode of

payment of tax;

c) Convenience of making payment online;

d) Logical tax collection data in electronic format;

e) Faster remittance of tax revenue to the Government Account;

f) Paperless transactions;

g) Speedy Accounting and reporting;

h) Electronic reconciliation of all receipts;

i) Simplified procedure for banks;

j) Warehousing of Digital Challan.

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

4 | P a g e

To get regular updates please share your details on 7503031378

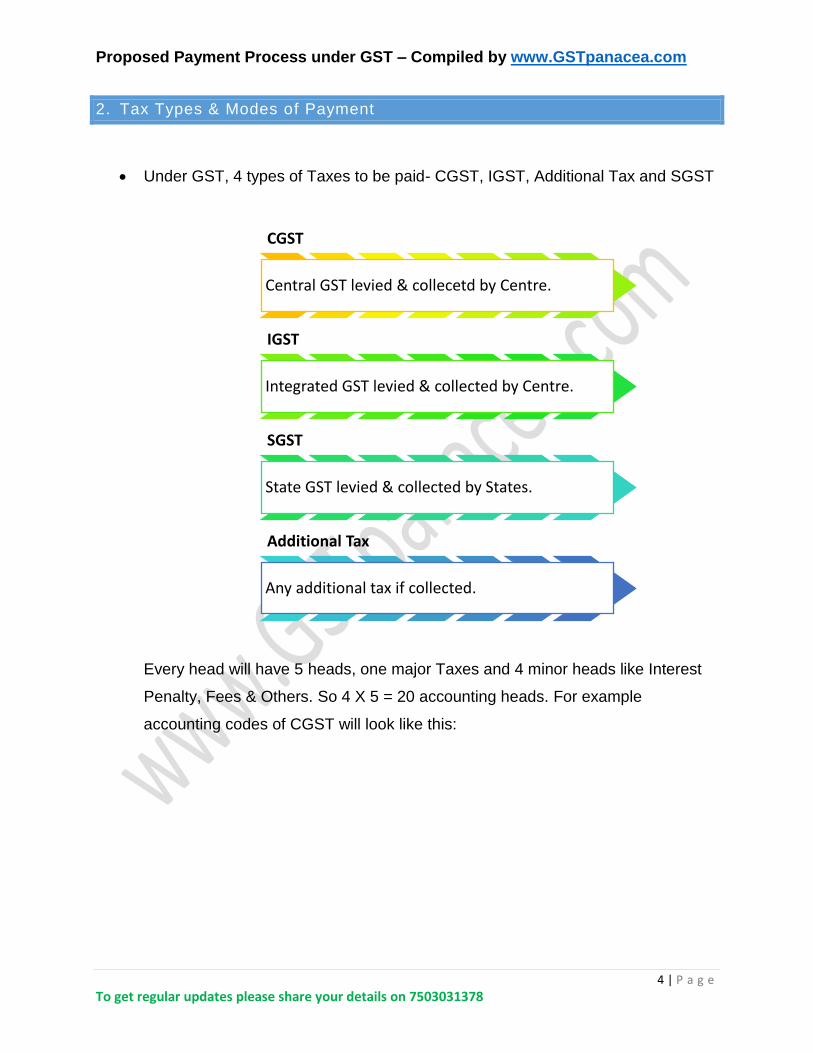

2. Tax Types & Modes of Payment

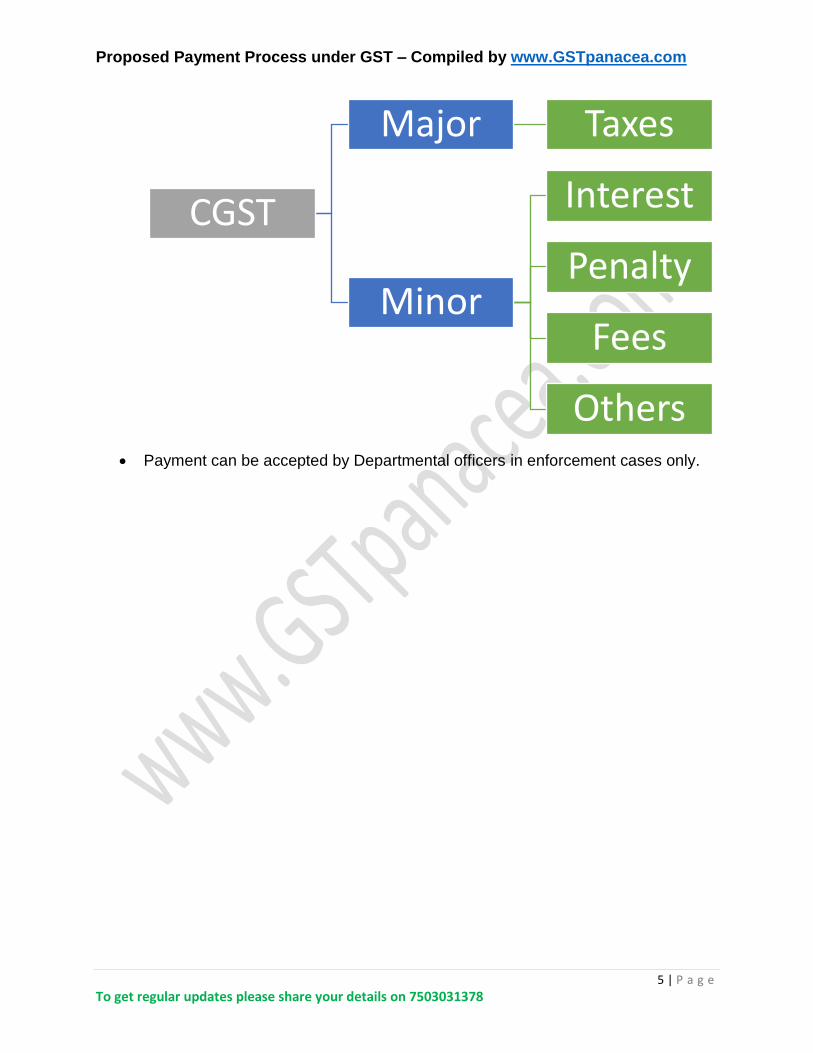

Under GST, 4 types of Taxes to be paid- CGST, IGST, Additional Tax and SGST

Every head will have 5 heads, one major Taxes and 4 minor heads like Interest

Penalty, Fees & Others. So 4 X 5 = 20 accounting heads. For example

accounting codes of CGST will look like this:

CGST

Central GST levied & collecetd by Centre.

IGST

Integrated GST levied & collected by Centre.

SGST

State GST levied & collected by States.

Additional Tax

Any additional tax if collected.

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

5 | P a g e

To get regular updates please share your details on 7503031378

Payment can be accepted by Departmental officers in enforcement cases only.

CGST

Major Taxes

Minor

Interest

Penalty

Fees

Others

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

6 | P a g e

To get regular updates please share your details on 7503031378

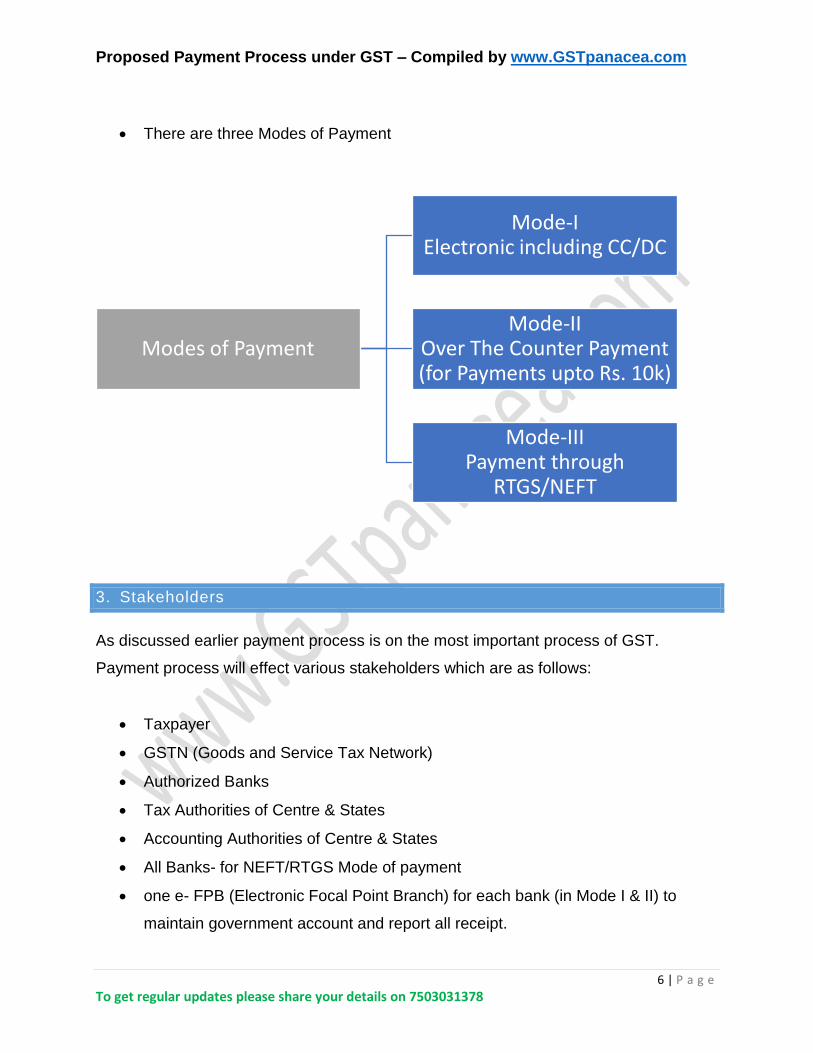

There are three Modes of Payment

3. Stakeholders

As discussed earlier payment process is on the most important process of GST.

Payment process will effect various stakeholders which are as follows:

Taxpayer

GSTN (Goods and Service Tax Network)

Authorized Banks

Tax Authorities of Centre & States

Accounting Authorities of Centre & States

All Banks- for NEFT/RTGS Mode of payment

one e- FPB (Electronic Focal Point Branch) for each bank (in Mode I & II) to

maintain government account and report all receipt.

Modes of Payment

Mode-IElectronic including CC/DC

Mode-IIOver The Counter Payment (for Payments upto Rs. 10k)

Mode-IIIPayment through

RTGS/NEFT

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

7 | P a g e

To get regular updates please share your details on 7503031378

all branches for receiving Over the Counter Payments

one or more front end service branch

Reserve Bank of India

o e- FPB (in Mode III)

o Aggregator for Accountal & Reconciliation of receipts

4. Basic Features

Electronically generated Challan from GSTN for all 3 modes containing a unique

14-digit Common Portal Identification Number (CPIN) for each challan.

o 4 digit ‘yymm’

o 10 digit unique CPIN

Challan once generated to be valid for 7 days.

Challan can be generated by

o Taxpayer

o His authorized representative

Departmental officers

o Any other person paying on behalf of taxpayer

Certain key details like name, address, email, GSTIN of payer to be auto-

populated.

Jurisdictional Location not to be mentioned in challan. Challan will be matched with

Master received from Tax Authorities.

Payment Period will not be mentioned in the Challan like current Service Tax

procedure.

Single challan / instrument for payment of all four types of taxes.

Time of payment: from 0000 hrs. to 2000 hrs. (Time IST)

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

8 | P a g e

To get regular updates please share your details on 7503031378

Proposed workflow of RBI’s e-Kuber model to be followed for payment, accounting

and reconciliation

Accounting Authorities to interact directly with RBI & not with Authorized banks

in case of discrepancies found during reconciliation

System of electronic Personal Ledger Account (cash ledger) on GSTN for each

taxpayer (20 pages)

One e-FPB per Authorized Bank (in Mode I & II) / RBI (in Mode –III)

GSTN to be anchor in payment process with responsibility for information flow to

various agencies

RBI to act as aggregator and anchor of flow of fund and information about receipts

5. MODE –I: E-PAYMENT MADE THROUGH AUHTORISED BANK’S

INTERNET BANKING, CC/DC

Generation of e-Challan at GSTN

Tax payer to select e-payment mode

o Net Banking

o Credit/Debit Card of any bank

o Tax Payer to choose Authorized bank in case of Net Banking

o Payment gateway of authorized bank (or their SPVs) in case of CC/DC

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

9 | P a g e

To get regular updates please share your details on 7503031378

Credit Card proposed to be used by taxpayer to be registered at GSTN - as an

additional safety check to eliminate the issue of charge back

GSTN to direct the taxpayer to the website of selected bank/payment gateway

Alongside, GSTN to forward an electronic string to the selected bank carrying

specified details of challan on real time basis

Taxpayer to make payment using the USER ID & Password provided by his bank

On successful completion of transaction, e-FPB of bank to forward a confirmation

electronic string (CIN) to GSTN on real time basis.

In case of payments through this mode a unique 17 digit number containing 14-

digit CPIN as generated by GSTN for a particular challan & unique 3 digit Bank

Code (MICR based which will be communicated by RBI to GSTN).

GSTN to credit the Taxpayer’s ledger

Copy of paid Challan to be available on GSTN for taxpayer

(downloadable/printable)

5.1. ISSUES WITH PAYMENT THROUGH CREDIT CARD

There are few issues we would like to attract attention of our readers:

a. Pre-registration of Card?

Page 10 of Report on GST Payments: The taxpayer would be required to pre-

register his credit card, from which the tax payment is intended, with the GSTN

system.

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

10 | P a g e

To get regular updates please share your details on 7503031378

Author’s view: Such pre-registration of card will slow down the process. This requirement

should be relaxed as there might be a case where CA of assesse might be making payments

on last date and registering Credit Card at that time would be time consuming as payments

made till 20.00 IST will b be reflected.

b. Delay in credit of payments from Credit Card?

Page 10 & 11 of Report on GST Payments: In respect of Credit Card payments,

presently the acquiring bank is permitted to transfer the amount to the merchant

on T+3 basis. Thus there may arise some situations where the taxpayers account

has been debited on T+0 whereas Government’s account in authorized bank

would be credited on T+3 basis.

Author’s view: Government through RBI should reduce the time by suitable negotiations

with payment gateways. Because Credit Card might be reduced as last option by assesse

when he doesn’t have sufficient money in ba-nk account and in this case credit would be

reflected after 3 days then there would be last payment interest, penalties etc. And so this

will in itself defeat the purpose of making payments through Credit Card. Or this could

also be understood that Credit Card payments should be made 4 days before last date and

thus this method reduces the payment due date which is hardship to assesse.

6. MODE –II: OVER THE COUNTER (OTC) PAYMENTS

For small taxpayers for making payment upto Rs.10,000/- per challan - by cash /

DD / cheque drawn on same bank or on another bank in the same city. No

outstation cheques are to be accepted except those which are payable at par all

branches of bank having presence at that location.

Tax payer to tender only one instrument to pay one or more type of tax.

For cheque payment, Name of authorized bank & its location to be mandatorily

filled in challan

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

11 | P a g e

To get regular updates please share your details on 7503031378

On real time basis, GSTN to share challan details with Core Banking System

(CBS) of the selected authorized Bank

Taxpayer to approach the branch of the authorized bank for payment of taxes

along with the instrument or cash

In case of cash / same bank instrument a unique transaction number (BTR/BRN)

will be generated immediately by the authorized bank’s system and given to

taxpayer

Authorized bank to send receipt information (CIN) to GSTN on real time basis

In case of instruments drawn on another bank in the same city, payment would

not be realized immediately.

Authorized Bank to inform GSTN on real time basis in two stages

when an instrument is given OTC – to send an electronic string to GSTN

containing specified details

second acknowledgement - after the cheque is realizedwith 3 additional

details

Similarly, bank to issue acknowledgement to taxpayer in two steps

Acknowledgment of cheque immediately

Upon realization of cheque, issuance of BTR / BTN

GSTN to credit the Taxpayer’s Ledger

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

12 | P a g e

To get regular updates please share your details on 7503031378

6.1. ISSUES WITH PAYMENT THROUGH OTC

There are few issues we would like to attract attention of our readers:

a. Limit of 10k for cash payments?

Only Rs. 10,000/- can be deposited over the counter in cash.

Author’s view: Current Banking Regulations allows a person to deposit upto Rs. 50,000/- in cash

without PAN Card and above than that with production of PAN Card. As this payment is to

Government for taxes either the limit should be scrapped or with production of PAN Card or at

least limit should be enhanced to Rs. 50,000/- as Rs. 10,000/- is very small amount and might not

suffice the purpose of payments of tax.

b. Limit of 10k for Cheque payments?

Only Rs. 10,000/- can be deposited over the counter in Cheque.

Author’s view: Payments through regular banking channels such as Cheques should not have any

limit. They should be limitless as there is no issue in current banking system why such limit is

prescribed for tax payments. We agree that over the period of time & considering dynamic real

time transactions recording NEFT/RTGS are more preferred method but we should not ignore old

time tested methods like Cheque Payments. Small Assesse also might not have access to Internet

Banking facilities or they might not be comfortable with Internet Banking and in this case

responsibility of payment come on shoulder of professional.

7. MODE -III: NEFT/RTGS FROM ANY BANK

To be made operational after a pilot run by RBI

For taxpayers

o not having a bank account in any of the Authorized Banks

o having a bank account in any of the Authorized Banks

No limit on amount to be paid through this mode

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

13 | P a g e

To get regular updates please share your details on 7503031378

Payments to be collected by RBI directly

RBI to perform the role of e-FPB also

Challan and NEFT/RTGS mandate form generated on GSTN NEFT/RTGS

mandate form to have validity period of CPIN printed on it

In challan, the field for name of Authorized Bank to be auto-populated as RBI

NEFT/RTGS mandate form will have certain information auto-populated

o CPIN in “Account Name” field

o ‘GST Payment’ in “Sender to Receiver Information” field

Taxpayer to print a copy of Challan and NEFT/RTGS mandate form from GSTN

& approach his bank for payment

Amount indicated for remittance to be transferred by bank to the designated

account of the government in RBI along with challan details and a Unique

Transaction Reference (UTR) Number

RBI to validate payments against each challan with UTR received from remitter

bank

RBI to report receipt of payment to GSTN (CIN) on real time basis through an

electronic string with specified details

GSTN to credit the Taxpayer’s ledger

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

14 | P a g e

To get regular updates please share your details on 7503031378

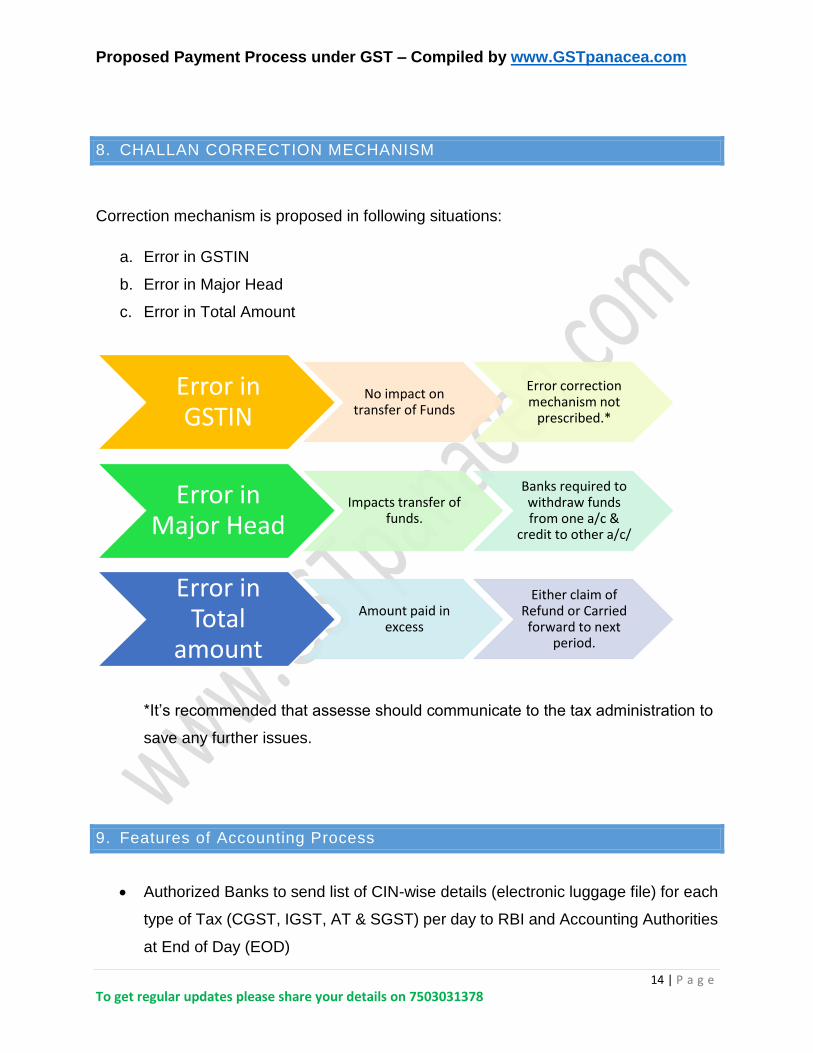

8. CHALLAN CORRECTION MECHANISM

Correction mechanism is proposed in following situations:

a. Error in GSTIN

b. Error in Major Head

c. Error in Total Amount

*It’s recommended that assesse should communicate to the tax administration to

save any further issues.

9. Features of Accounting Process

Authorized Banks to send list of CIN-wise details (electronic luggage file) for each

type of Tax (CGST, IGST, AT & SGST) per day to RBI and Accounting Authorities

at End of Day (EOD)

Error in GSTIN

No impact on transfer of Funds

Error correction mechanism not

prescribed.*

Error in Major Head

Impacts transfer of funds.

Banks required to withdraw funds from one a/c &

credit to other a/c/

Error in Total

amount

Amount paid in excess

Either claim of Refund or Carried forward to next

period.

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

15 | P a g e

To get regular updates please share your details on 7503031378

RBI through its e-kuber system to consolidate the lists received from all authorized

banks, debit their accounts and correspondingly credit Tax accounts of GOI /

respective State Governments

RBI to send digitally signed one e-scroll for each type of Tax (CGST, IGST, AT &

SGST) per day (39) to Accounting Authorities of Central Government and State

Governments & GSTN on T+1 basis

GSTN to send reconciled data (challan data from Authorized Banks and e-scroll

from RBI) to Accounting Authorities at EOD

For any discrepancy noticed, accounting authority to generate a Memorandum of

Error (MOE) & send to RBI

RBI to resolve the discrepancy in consultation with the Authorized Bank

RBI to report the corrected data to respective Accounting Authority & GSTN

Taxpayers Master data to be provided by Tax Authorities to Accounting Authorities

for mapping of payment details jurisdiction wise

10. Proposed Accounting System

Four different Major Heads of accounts to be opened for each tax along with

underlying Minor Heads to account for various taxes & other receipts like interest,

penalty, fees & others

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

16 | P a g e

To get regular updates please share your details on 7503031378

Standardized uniform Accounting Codes for all taxes under GST regime among

Centre, State & UTs to facilitate settlement of IGST on the basis of centralized

reporting

Common Accounting Codes for Centre & States.

GSTN will receive 39 e-scrolls from RBI (one each for CGST, IGST and Additional

Tax and one each for SGST for each State/UG).

11. Banking Arrangements

Common set of Authorized Banks comprising existing authorized banks of the

Central Government & all State Governments/UTs (presently 26)

Certain minimum standards to be met by banks to become authorized banks

A system of penalty/incentive proposed for reporting of error free data

Payments through non-authorized banks permitted (NEFT/RTGS)

11.1. E-KUBER

e-Kuber is “Core Banking System” (CBS) of RBI. RBI will consolidate luggage files received from all authorized banks, debit their accounts and correspondingly credit the CGST, IGST and Additional Tax accounts of Government of India and SGST accounts of each State/UT Government maintained in RBI(39 accounts). RBI would send consolidated, digitally signed e-scrolls, along with all the challan details, for each type of Tax (one each for CGST, IGST and Additional Tax for Government of India, and separate e-scrolls of SGST for each State/UT Governments) per day (including NIL payment day) after including the amount collected by it in Mode – III to Accounting Authority of Centre (e-PAO) / each State (e-Treasury) and GSTN simultaneously.

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

17 | P a g e

To get regular updates please share your details on 7503031378

If any discrepancy is reported by Accounting Authority or GSTN, it would carry out the correction mechanism with the authorized bank and thereafter report the corrected data to respective Accounting Authority and GSTN. RBI will consolidate Datewise Monthly Statements (DMS) received from the banks for each tax and government, validate the consolidated statements (39) with reference to its own data of e-scrolls reported during the report month, have a systemic review of unresolved discrepancies and communicate the statements to the respective accounting authorities within 3 days from end of the report month.

12. Reconciliation of Receipts

Use of only system generated challans – no re-digitization by any actor in the entire

work flow

CPIN to be generated by GSTN -- to be used as a key identifier up till receipt of

payment by Bank

CIN (actual indicator of receipt of payment) to be generated by collecting Bank --

to be used as a key identifier thereafter for accounting, reconciliation, etc.

Accounting Authorities to play a paramount role in reconciliation –

Accounting on the basis of RBI data

Reconciliation on the basis of GSTN and bank data

13. Grievance Redressal

In OTC mode if cash ledger of taxpayer not credited within three days- approach

bank where instrument presented

In RTGS/NEFT mode if cash ledger of taxpayer not credited within three days-

approach bank where taxpayer’s account is

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

18 | P a g e

To get regular updates please share your details on 7503031378

Each e-FPB required to have front end service branch to resolve payment related

issues

14. Source of this Article

Report of the Joint Committee on Business Process for GST on GST Payment

Process (April’15)

PPT on Proposed Payment Process (Oct’15)

Model Law GST

15. DISCLAIMER

This document is for information only. All care has been taken for laws but in

case something has been missed request our readers to update us. This

should not be taken as any advice from our concern. We shall not be liable

for any loss if occurred for laws stated in this document.

16. Other Articles

Opportunities for Professionals under GST Regime

http://gstpanacea.com/services/opportunities-professionals-gst-regime/

Registration Process under GST Regime

http://gstpanacea.com/services/registration-process-goods-service-tax-gst-regime/

Returns proposed under GST Regime

Proposed Payment Process under GST – Compiled by www.GSTpanacea.com

19 | P a g e

To get regular updates please share your details on 7503031378

http://gstpanacea.com/services/returns-proposed-goods-service-tax-gst-laws/

Model Law GST - Law & Practice (Part-1)

http://gstpanacea.com/services/model-law-gst-law-practice-part-1/

Thanks & Regards Team GSTpanacea.com 7503031378