Embed Size (px)

Citation preview

Sean GowranPresident and Country ManagerEricsson Philippines

Commercial in confidence, © Ericsson AB 2016

Global OPERATORinvestment and bandwidth management

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 2

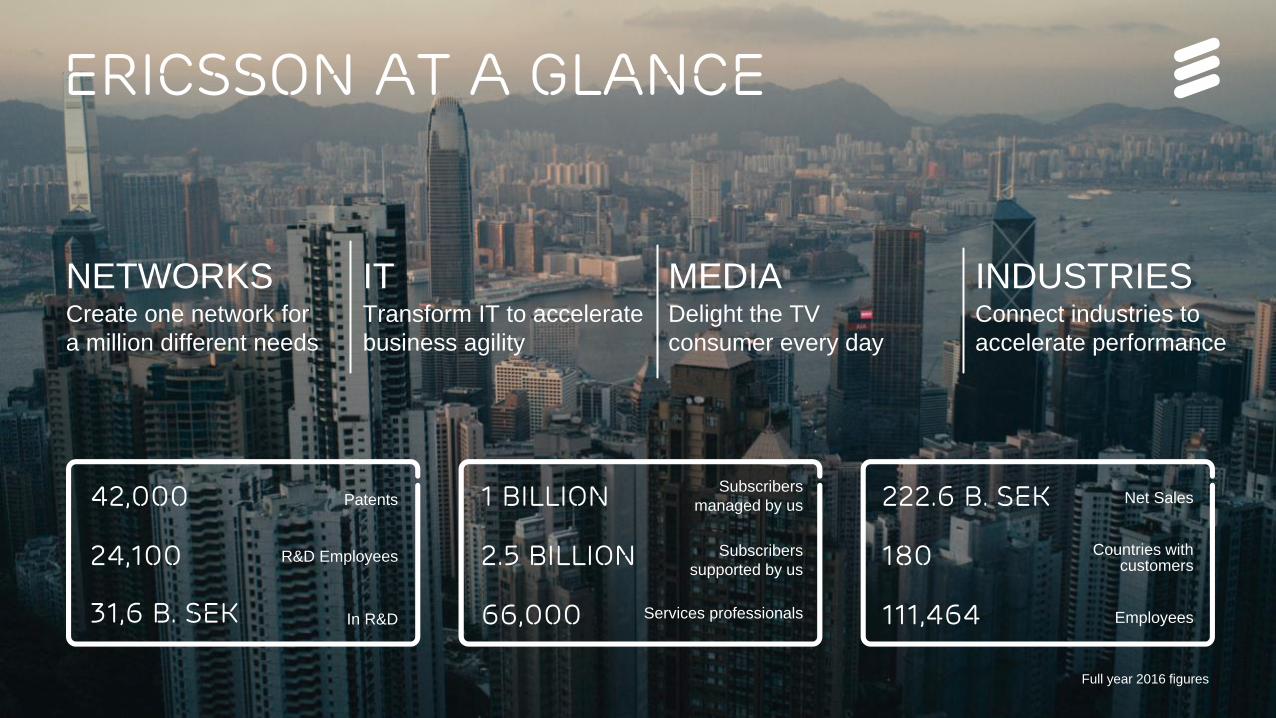

Ericsson at a glance

42,000

24,100

66,000

2.5 billion

1 billion

180

111,464

Subscribers

managed by us

Subscribers

supported by us

Services professionals Employees

Countries with customers

R&D Employees

Patents

In R&D

222.6 B. SEK Net Sales

31,6 B. SEK

NETWORKSCreate one network for

a million different needs

ITTransform IT to accelerate

business agility

MEDIADelight the TV

consumer every day

INDUSTRIESConnect industries to

accelerate performance

Full year 2016 figures

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 3

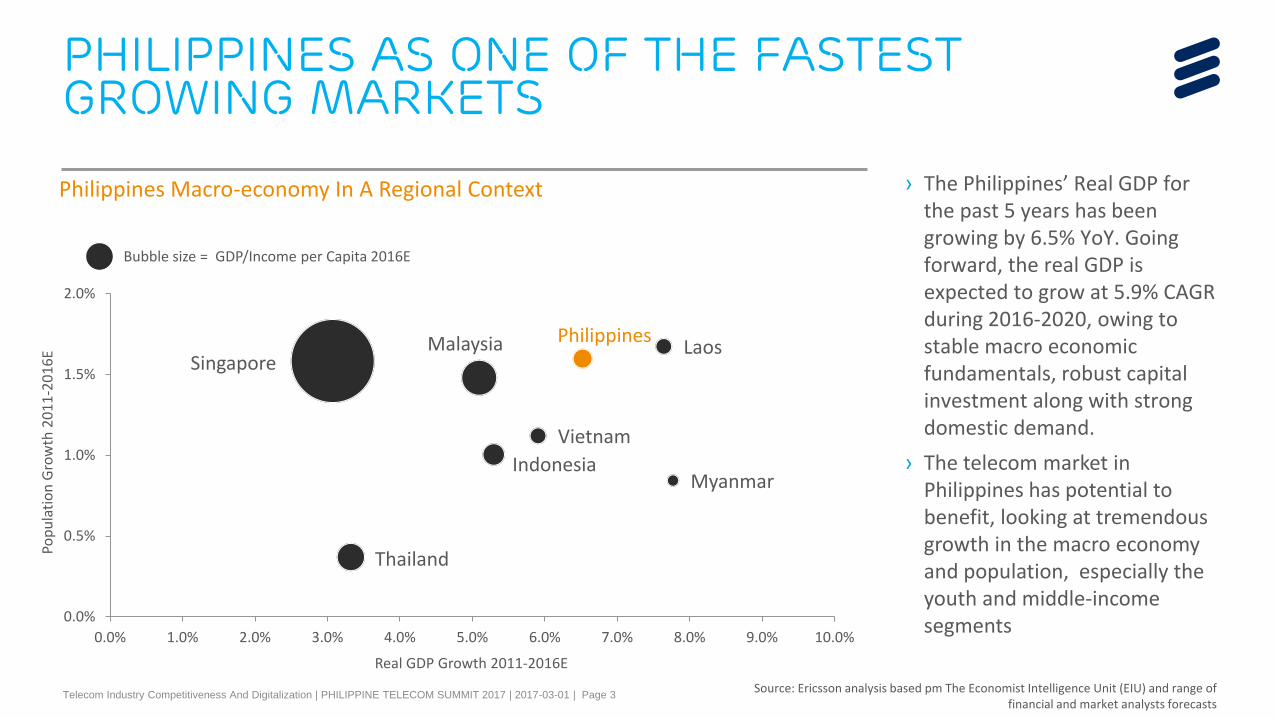

Philippines as ONE OF THE FASTEST GROWING MARKETS

Source: Ericsson analysis based pm The Economist Intelligence Unit (EIU) and range of financial and market analysts forecasts

Indonesia

LaosMalaysia

Myanmar

Philippines

Singapore

Thailand

Vietnam

0.0%

0.5%

1.0%

1.5%

2.0%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0%

Philippines Macro-economy In A Regional Context

Real GDP Growth 2011-2016E

Pop

ula

tio

n G

row

th 2

01

1-2

01

6E

Bubble size = GDP/Income per Capita 2016E

› The Philippines’ Real GDP for the past 5 years has been growing by 6.5% YoY. Going forward, the real GDP is expected to grow at 5.9% CAGR during 2016-2020, owing to stable macro economic fundamentals, robust capital investment along with strong domestic demand.

› The telecom market in Philippines has potential to benefit, looking at tremendous growth in the macro economy and population, especially the youth and middle-income segments

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 4

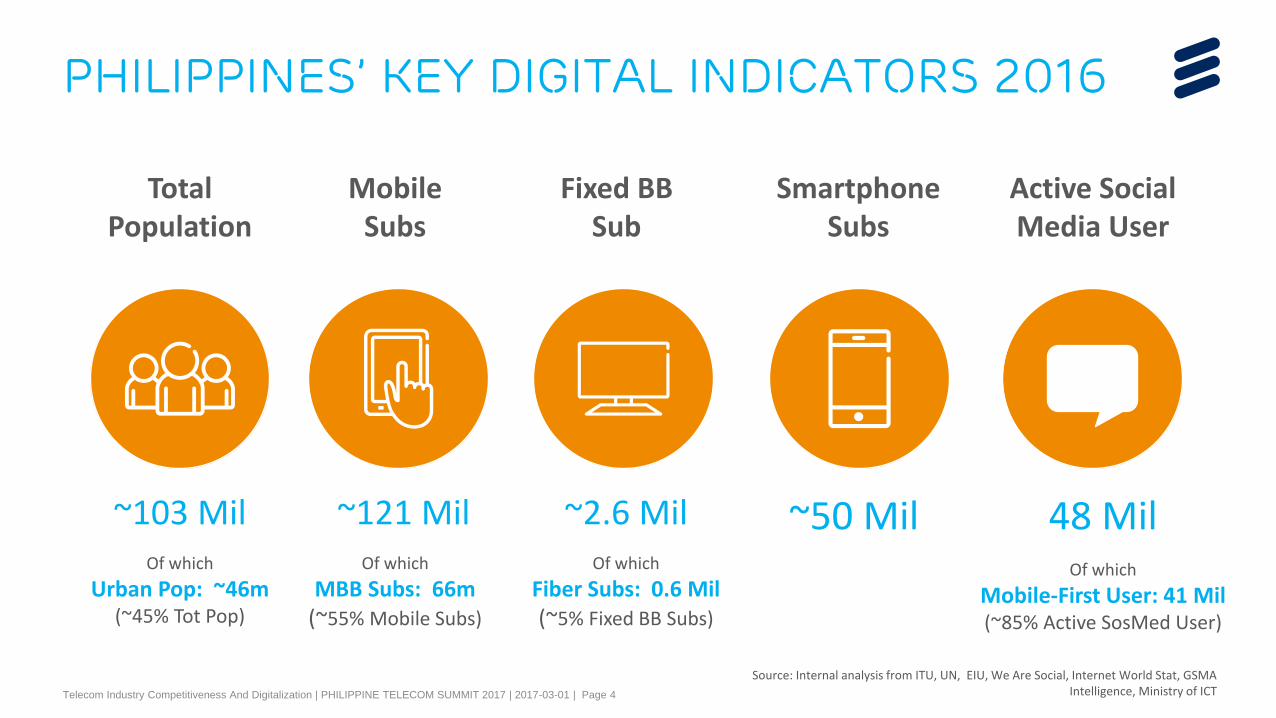

Philippines’ KEY DIGITAL INDICATORS 2016

Smartphone Subs

~50 Mil

Mobile Subs

~121 MilOf which

MBB Subs: 66m(~55% Mobile Subs)

Active Social Media User

48 MilOf which

Mobile-First User: 41 Mil(~85% Active SosMed User)

Source: Internal analysis from ITU, UN, EIU, We Are Social, Internet World Stat, GSMA Intelligence, Ministry of ICT

Total Population

~103 MilOf which

Urban Pop: ~46m(~45% Tot Pop)

Fixed BBSub

~2.6 MilOf which

Fiber Subs: 0.6 Mil(~5% Fixed BB Subs)

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 5

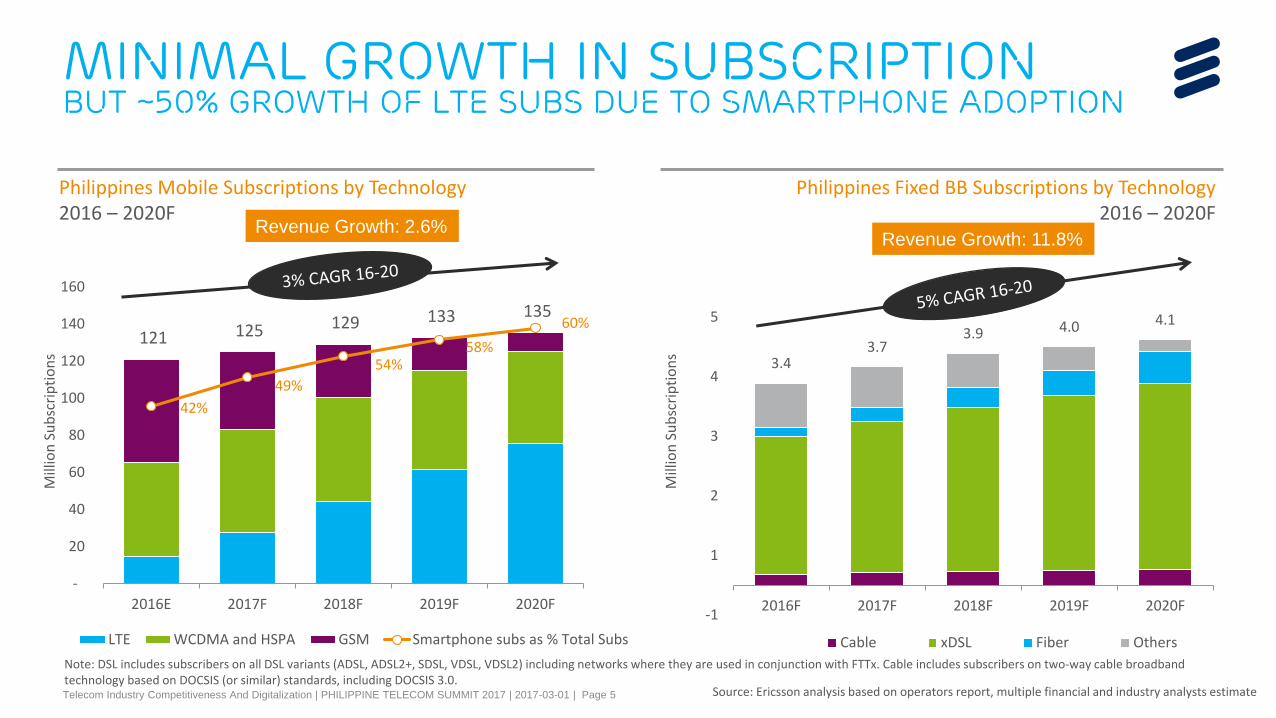

Philippines Mobile Subscriptions by Technology 2016 – 2020F

Philippines Fixed BB Subscriptions by Technology2016 – 2020F

121 125 129 133 135

42%

49%

54%58%

60%

0%

10%

20%

30%

40%

50%

60%

70%

-

20

40

60

80

100

120

140

160

2016E 2017F 2018F 2019F 2020F

LTE WCDMA and HSPA GSM Smartphone subs as % Total Subs

Mill

ion

Su

bsc

rip

tio

ns

Mill

ion

Su

bsc

rip

tio

ns

Source: Ericsson analysis based on operators report, multiple financial and industry analysts estimate

3.43.7

3.9 4.0 4.1

-1

1

2

3

4

5

2016F 2017F 2018F 2019F 2020F

Cable xDSL Fiber Others

Note: DSL includes subscribers on all DSL variants (ADSL, ADSL2+, SDSL, VDSL, VDSL2) including networks where they are used in conjunction with FTTx. Cable includes subscribers on two-way cable broadband technology based on DOCSIS (or similar) standards, including DOCSIS 3.0.

Minimal growth in subscriptionbut ~50% growth of lte subs due to smartphone adoption

Revenue Growth: 2.6%Revenue Growth: 11.8%

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 6

-

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

PC/Router/Tablet Smartphone

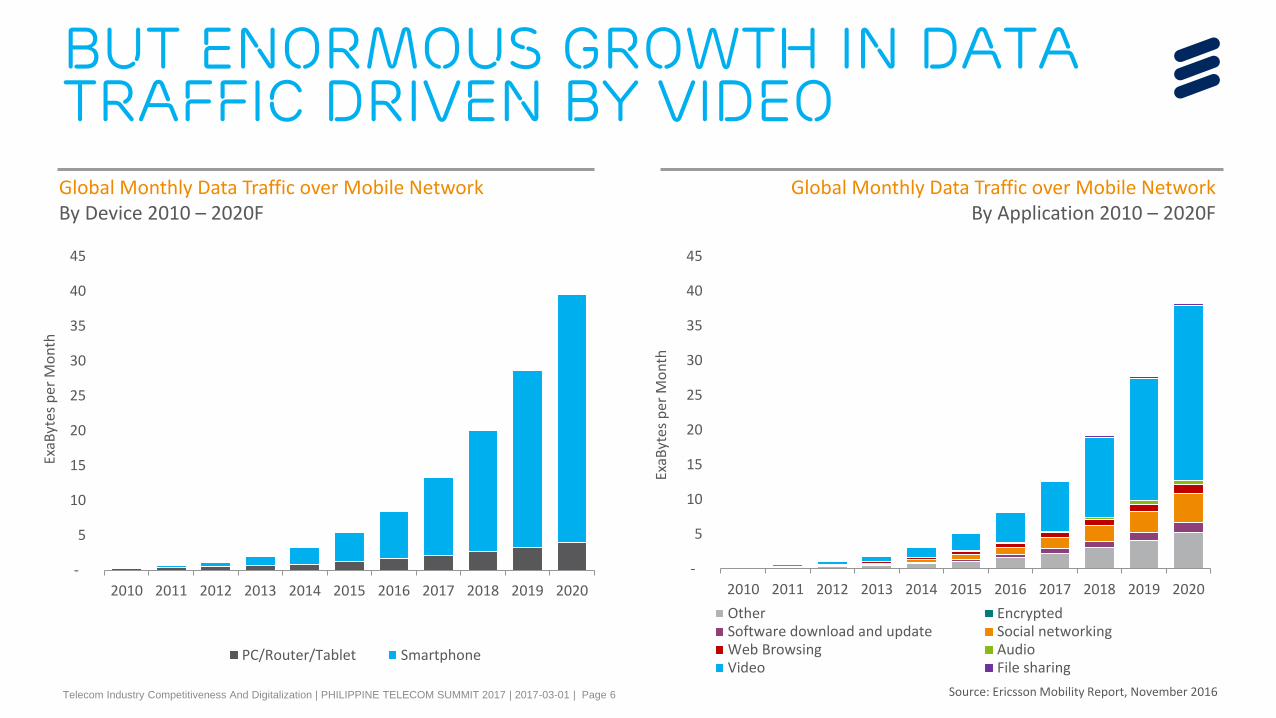

Global Monthly Data Traffic over Mobile NetworkBy Device 2010 – 2020F

ExaB

ytes

per

Mo

nth

Global Monthly Data Traffic over Mobile NetworkBy Application 2010 – 2020F

-

5

10

15

20

25

30

35

40

45

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Other EncryptedSoftware download and update Social networkingWeb Browsing AudioVideo File sharing

Source: Ericsson Mobility Report, November 2016

ExaB

ytes

per

Mo

nth

but enormous growth in data traffic driven by video

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 7

GROWING MOBILE data USAGE, BUT..MOBILE INTERNET = MOBILE NETWORK?

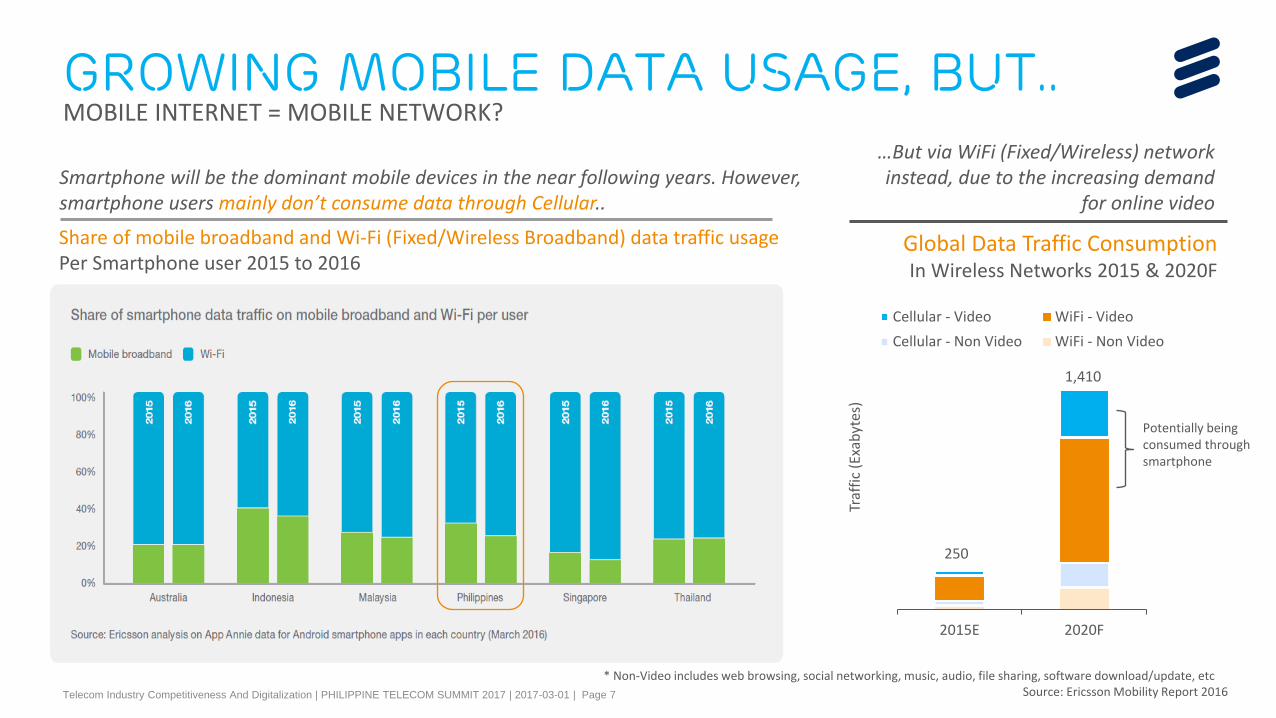

Share of mobile broadband and Wi-Fi (Fixed/Wireless Broadband) data traffic usage Per Smartphone user 2015 to 2016

Source: Ericsson Mobility Report 2016* Non-Video includes web browsing, social networking, music, audio, file sharing, software download/update, etc

Global Data Traffic Consumption In Wireless Networks 2015 & 2020F

250

1,410

2015E 2020F

Cellular - Video WiFi - Video

Cellular - Non Video WiFi - Non Video

Potentially being consumed through smartphone

…But via WiFi (Fixed/Wireless) network instead, due to the increasing demand

for online video

Traf

fic

(Exa

byt

es)

Smartphone will be the dominant mobile devices in the near following years. However, smartphone users mainly don’t consume data through Cellular..

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 8

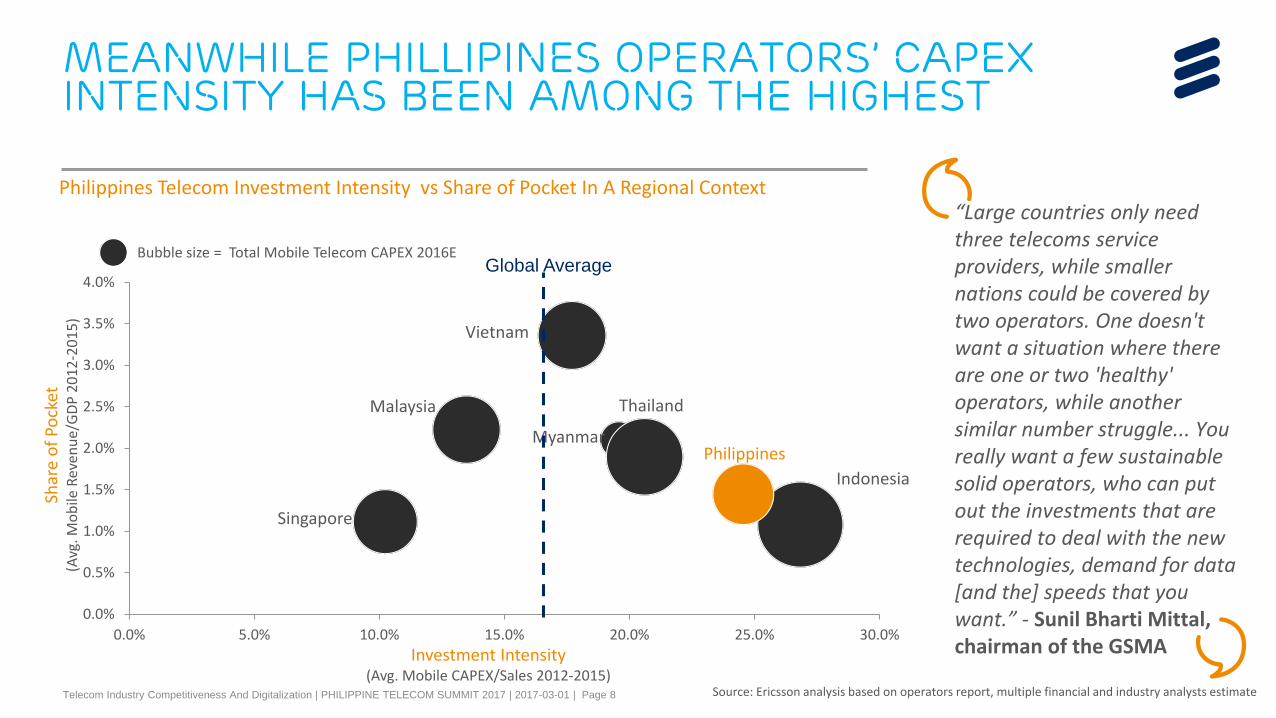

MEANWHILE PHILLIPINES OPERATORS’ CAPEX INTENSITY HAS BEEN AMONG THE HIGHEST

Indonesia

Malaysia

MyanmarPhilippines

Singapore

Thailand

Vietnam

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0%

Philippines Telecom Investment Intensity vs Share of Pocket In A Regional Context

Investment Intensity (Avg. Mobile CAPEX/Sales 2012-2015)

Shar

e o

f Po

cket

(A

vg. M

ob

ile R

even

ue

/GD

P 2

01

2-2

01

5)

Bubble size = Total Mobile Telecom CAPEX 2016E

“Large countries only need three telecoms service providers, while smaller nations could be covered by two operators. One doesn't want a situation where there are one or two 'healthy' operators, while another similar number struggle... You really want a few sustainable solid operators, who can put out the investments that are required to deal with the new technologies, demand for data [and the] speeds that you want.” - Sunil Bharti Mittal, chairman of the GSMA

Source: Ericsson analysis based on operators report, multiple financial and industry analysts estimate

Global Average

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 9

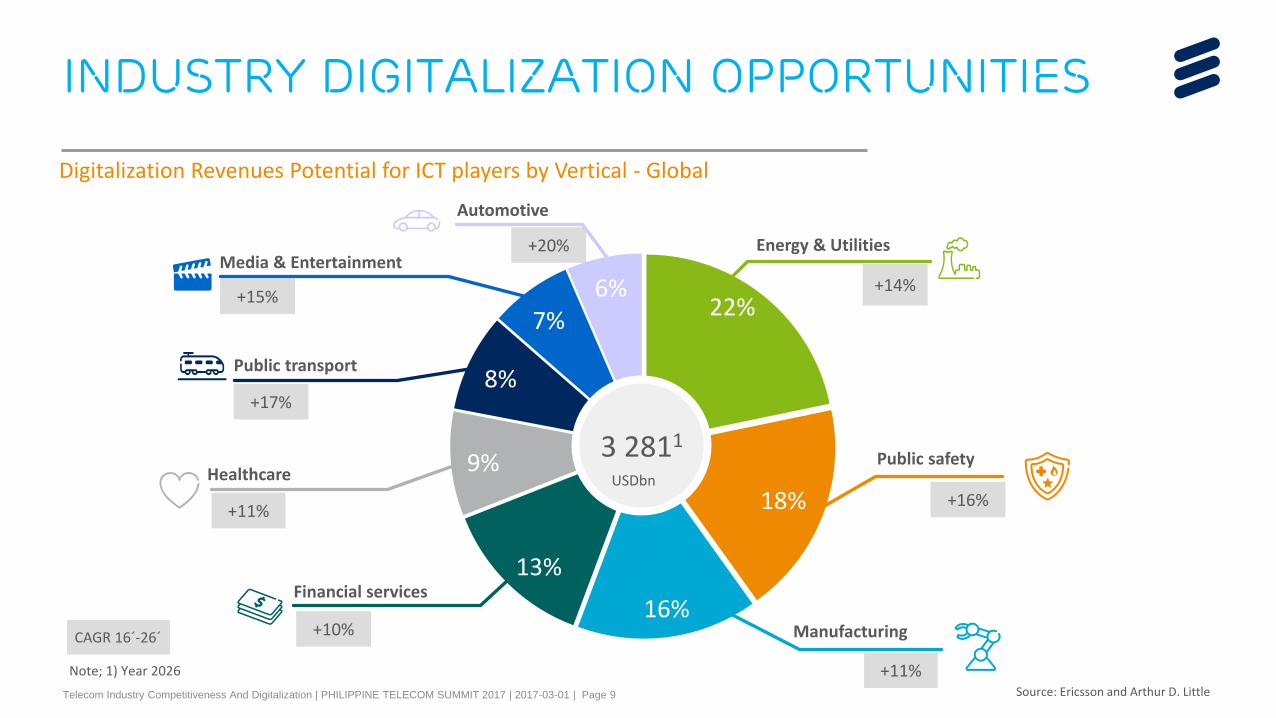

Industry digitalization opportunities

Note; 1) Year 2026

Energy & Utilities

Automotive

Media & Entertainment

Public transport

Healthcare

Financial services

Public safety

+16%

+10%

+14%

+20%

+15%

+17%

+11%

3 2811

CAGR 16´-26´

USDbn

Manufacturing

+11%

22%

8%

7%6%

18%

9%

13%

16%

Source: Ericsson and Arthur D. Little

Digitalization Revenues Potential for ICT players by Vertical - Global

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 10

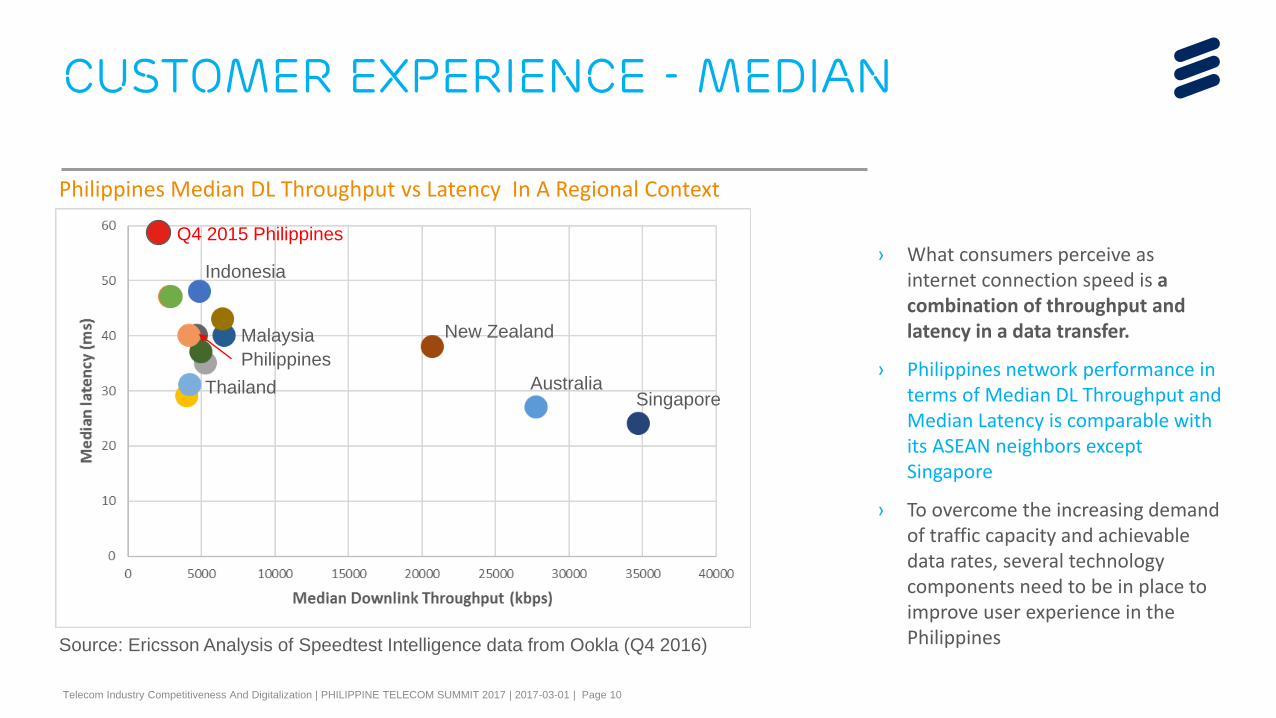

Philippines Median DL Throughput vs Latency In A Regional Context

› What consumers perceive as internet connection speed is a combination of throughput and latency in a data transfer.

› Philippines network performance in terms of Median DL Throughput and Median Latency is comparable with its ASEAN neighbors except Singapore

› To overcome the increasing demand of traffic capacity and achievable data rates, several technology components need to be in place to improve user experience in the Philippines Source: Ericsson Analysis of Speedtest Intelligence data from Ookla (Q4 2016)

AustraliaSingapore

New Zealand

Philippines

Indonesia

Thailand

Malaysia

Customer experience - median

Q4 2015 Philippines

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 11

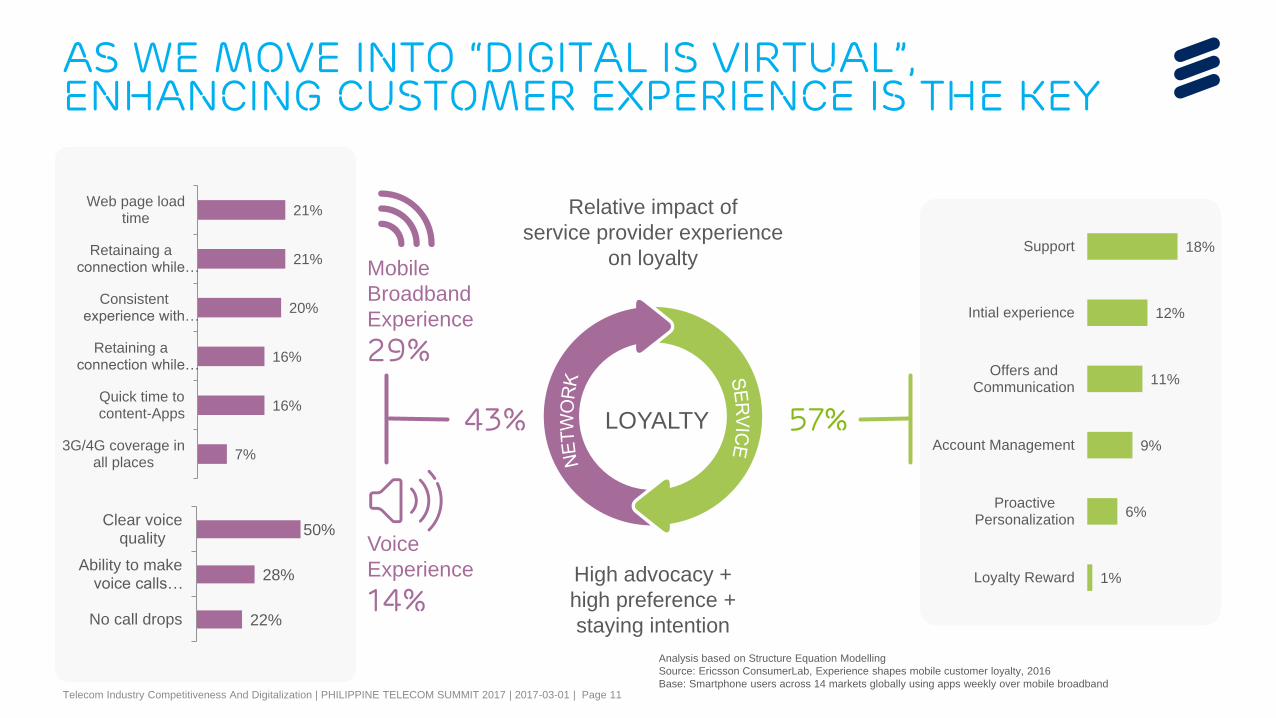

As we move into “digital is virtual”, enhancing CUSTOMER experience is THE key

18%

12%

11%

9%

6%

1%

Support

Intial experience

Offers andCommunication

Account Management

ProactivePersonalization

Loyalty Reward

21%

21%

20%

16%

16%

7%

Web page loadtime

Retainaing aconnection while…

Consistentexperience with…

Retaining aconnection while…

Quick time tocontent-Apps

3G/4G coverage inall places

50%

28%

22%

Clear voicequality

Ability to makevoice calls…

No call drops

LOYALTY

Relative impact of

service provider experience

on loyalty

High advocacy +

high preference +

staying intention

Mobile

Broadband

Experience

29%

Voice

Experience

14%

43% 57%

Analysis based on Structure Equation Modelling

Source: Ericsson ConsumerLab, Experience shapes mobile customer loyalty, 2016

Base: Smartphone users across 14 markets globally using apps weekly over mobile broadband

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 12

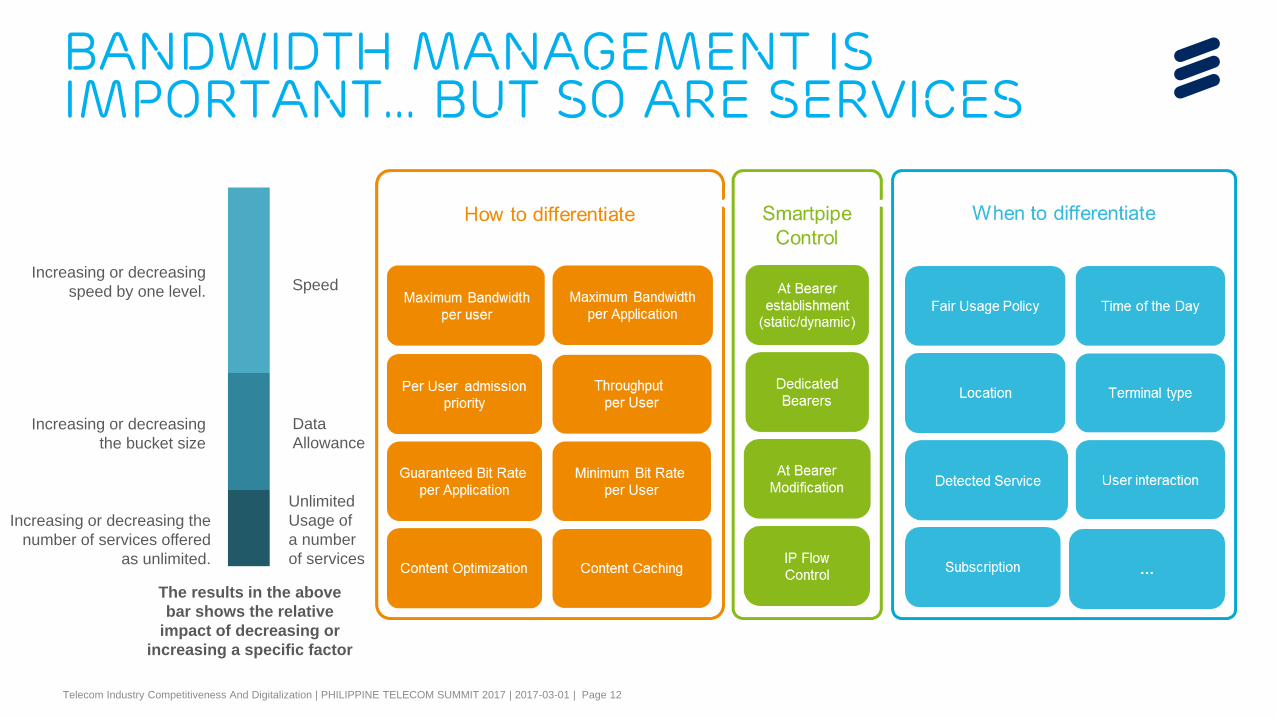

Bandwidth management is important... but so are services

Speed

Data

Allowance

Unlimited

Usage of

a number

of services

Increasing or decreasing

speed by one level.

Increasing or decreasing

the bucket size

Increasing or decreasing the

number of services offered

as unlimited.

The results in the above

bar shows the relative

impact of decreasing or

increasing a specific factor

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 13

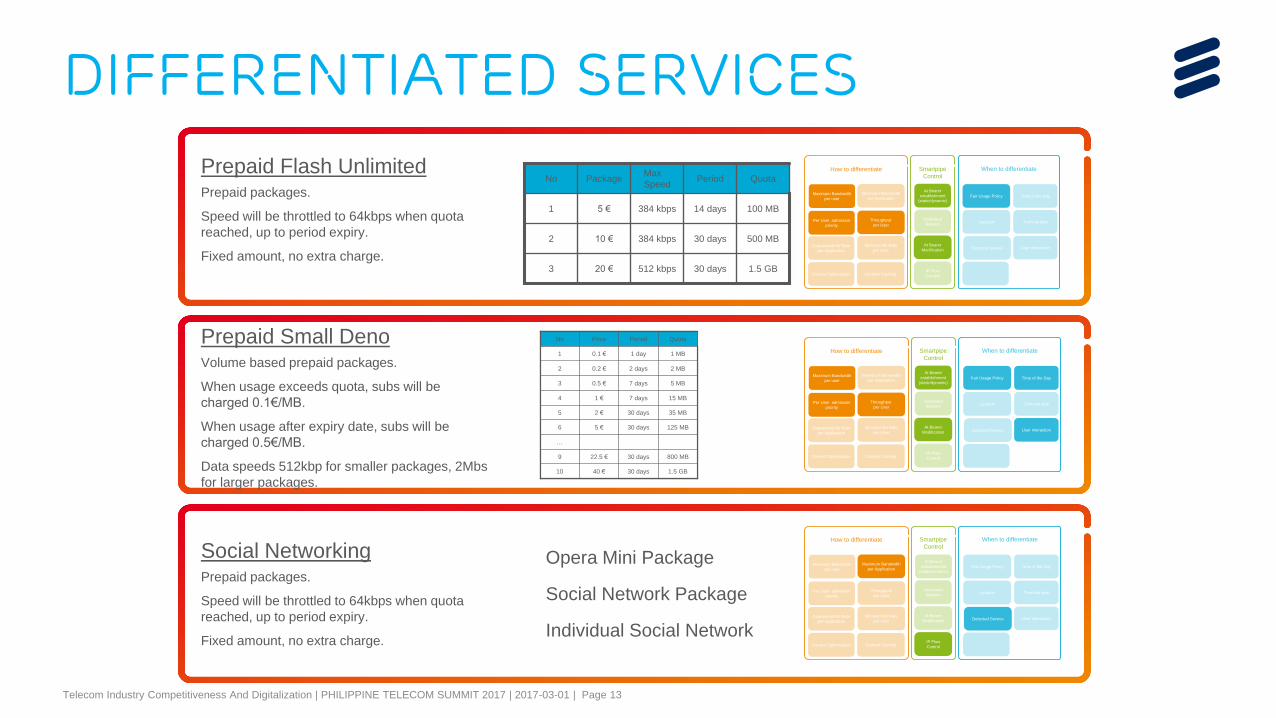

differentiated Services

1.5 GB

500 MB

100 MB

Quota

30 days512 kbps20 €3

30 days384 kbps10 €2

14 days384 kbps 5 €1

PeriodMax

SpeedPackageNo

Prepaid packages.

Speed will be throttled to 64kbps when quota

reached, up to period expiry.

Fixed amount, no extra charge.

Prepaid Flash Unlimited

Volume based prepaid packages.

When usage exceeds quota, subs will be

charged 0.1€/MB.

When usage after expiry date, subs will be

charged 0.5€/MB.

Data speeds 512kbp for smaller packages, 2Mbs

for larger packages.

Prepaid Small Deno

Prepaid packages.

Speed will be throttled to 64kbps when quota

reached, up to period expiry.

Fixed amount, no extra charge.

Social Networking

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

…

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

1.5 GB30 days40 €10

800 MB30 days22.5 €9

…

125 MB30 days5 €6

35 MB30 days2 €5

15 MB7 days1 €4

5 MB

2 MB

1 MB

Quota

7 days0.5 €3

2 days0.2 €2

1 day0.1 €1

PeriodPriceNo

1.5 GB30 days40 €10

800 MB30 days22.5 €9

…

125 MB30 days5 €6

35 MB30 days2 €5

15 MB7 days1 €4

5 MB

2 MB

1 MB

Quota

7 days0.5 €3

2 days0.2 €2

1 day0.1 €1

PeriodPriceNo

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

…

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

Opera Mini Package

Social Network Package

Individual Social Network

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

…

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 14

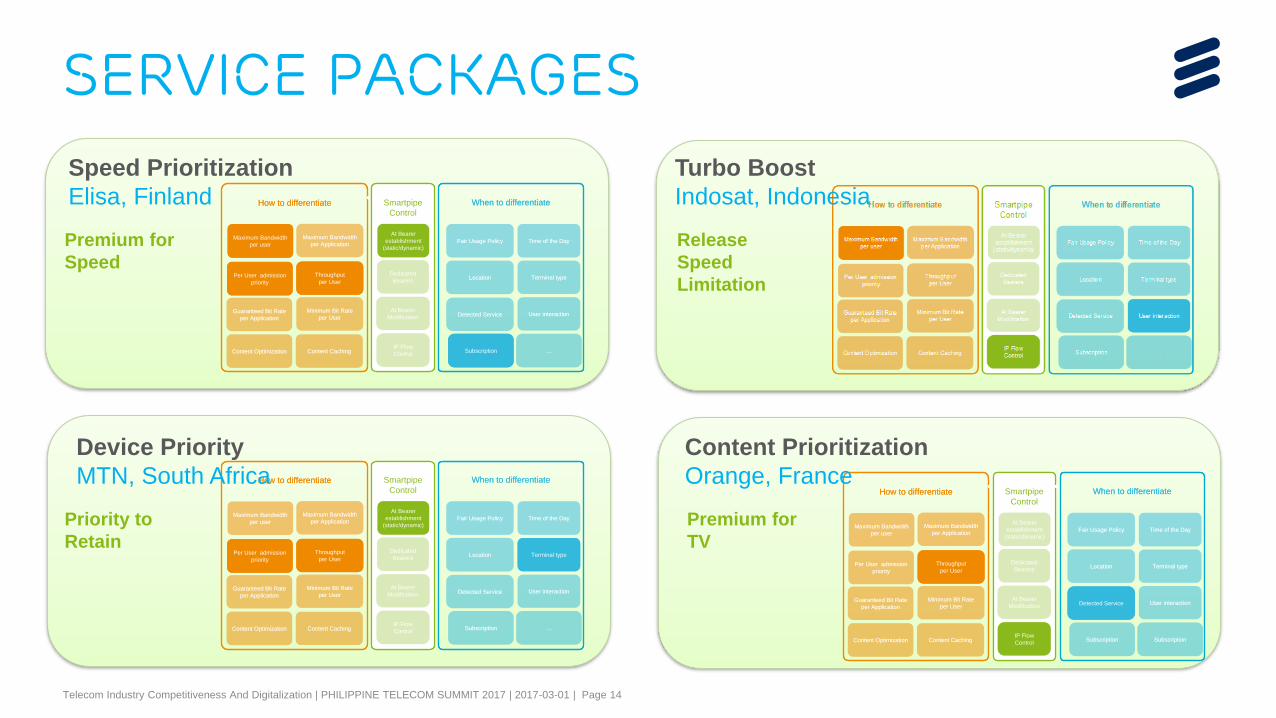

Service packages

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

Subscription

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

…

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

Subscription

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

…

Speed Prioritization

Elisa, Finland

Turbo Boost

Indosat, Indonesia

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

Subscription

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

…

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

Subscription

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

…

Device Priority

MTN, South AfricaWhen to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

Subscription

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

Subscription

When to differentiateHow to differentiate Smartpipe

Control

Maximum Bandwidth

per user

Per User admission

priority

Throughput

per User

Content Caching

Guaranteed Bit Rate

per Application

Content Optimization

Minimum Bit Rate

per User

Fair Usage Policy Time of the Day

Location Terminal type

User interaction

Subscription

At Bearer

Modification

At Bearer

establishment

(static/dynamic)

Dedicated

Bearers

IP Flow

Control

Maximum Bandwidth

per Application

Detected Service

Subscription

Content Prioritization

Orange, France

Premium for

Speed

Release

Speed

Limitation

Priority to

Retain

Premium for

TV

Telecom Industry Competitiveness And Digitalization | PHILIPPINE TELECOM SUMMIT 2017 | 2017-03-01 | Page 15Commercial in confidence, © Ericsson AB 2016

• Minimal growth in subscription and forecasted mobile revenues but enormous

growth in data traffic driven by video and adoption of smartphones

• Migration to newer technology, e.g., LTE, is key to provide efficient network and better

customer experience

• Service providers must capitalize on Industries’ Digitalization revenue opportunities

• Philippines’ telecom services providers are investing on network infrastructure

above global average in terms of CAPEX/Revenue

• Bandwidth Management is necessary but so are services

Key takeaways