Embed Size (px)

Citation preview

Strategic Management JournalStrat. Mgmt. J., 33: 252–276 (2012)

Published online EarlyView in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/smj.954

Received 15 July 2009; Final revision received 27 July 2011

GROWING PAINS: PRE-ENTRY EXPERIENCE AND THECHALLENGE OF TRANSITION TO INCUMBENCY†

PAO-LIEN CHEN,1 CHARLES WILLIAMS,2 and RAJSHREE AGARWAL3*1 Institute of Technology Management, National Tsing Hua University, Hsinchu,Taiwan2 Bocconi University, Milan, Italy3 Robert H. Smith School of Business, University of Maryland, College Park, Maryland,U.S.A.

We examine how entrepreneurial entry by diversifying and de novo firms in new industries leads todifferent levels of performance. We propose that these types of firms differ in dynamic capabilities,which help them overcome growth impediments and transition to incumbency in the industry.Growth impediments arise at larger size, older tenure levels in industry, and after technologicaldiscontinuities. Because of their prior experience, diversifying firms are better equipped to handlethe challenges of impediments to growth. Meanwhile, de novo firms, ostensibly tailor-made forthe targeted industry, are more likely to stumble over these growth challenges, and eventuallylag behind diversifying firms. We find support for our hypotheses using a near census of firms inthe U.S. wireless telecommunications industry over the 1983–2004 period. Copyright 2011John Wiley & Sons, Ltd.

INTRODUCTION

Studies of industry evolution largely sort firmsalong separate dimensions of incumbency andexperience. Some studies focus on the survivalof incumbents and entrants, extolling the virtuesof entrepreneurial firms that displace incumbents(Christensen and Rosenbloom, 1995; Cooper andSchendel, 1976; Gort and Klepper, 1982; Hen-derson and Clark, 1990; Tushman and Anderson,1986; Utterback, 1994). Other studies compare theperformance of diversifying (pre existing firms inother industries) and de novo (new firms created inthe focal industry context) entrants in a new indus-try (Bayus and Agarwal, 2007; Carroll et al., 1996;

Keywords: growth; evolution; entrepreneurship; dynamiccapabilities; reconfiguration.*Correspondence to: Rajshree Agarwal, Robert H. Smith Schoolof Business, Department of Management and Organization, Uni-versity of Maryland, 4512 Van Munching Hall, College Park,MD 20742, U.S.A. E-mail: [email protected]† All authors contributed equally to the study and the names arelisted in random order.

Ganco and Agarwal, 2009; Helfat and Lieberman,2002; Holbrook et al., 2000; Klepper and Simons,2000; Lane, 1989; Mitchell, 1991). Left unstudied,however, is the question of how pre-entry experi-ence impacts diversifying and de novo entrants asthey evolve and become incumbents.

Prior studies examining the static effects of pre-entry experience on survival have generally founda survival advantage for firms with pre-entry expe-rience, though there are conflicting approaches andfindings (Ganco and Agarwal, 2009). To the extentthat researchers have considered dynamic pat-terns, the dominant models in economics (Klepper,2002b) and organization studies (Carroll and Han-nan, 2004) predict gradual convergence betweendiversifying and de novo firms. Convergenceremains the dominant model, despite little empiri-cal validation (Carroll et al., 1996) and even in theface of contradictory evidence (Bayus and Agar-wal, 2007; Holbrook et al., 2000; Klepper, 2002a;Klepper and Simons, 2000).

Clearly the dynamic pattern of advantagebetween experienced and de novo firms merits

Copyright 2011 John Wiley & Sons, Ltd.

Growing Pains 253

more focused exploration. To study this dynamic,we examine how diversifying and de novo firmsconfront impediments to growth as they tran-sition to incumbency in the industry. Harkingback to an earlier tradition (Penrose, 1959), wetreat growth as a primary challenge for firmsas they evolve in the context of a focal indus-try (Caves, 1998; Sutton, 1997). Prior literaturehas identified three particular characteristics ofincumbents (Acs and Audretsch, 1990; Gort andKlepper, 1982; Helfat and Lieberman, 2002; Tush-man and Anderson, 1986)1 that represent a seriousimpediment to growth: size (Penrose, 1959; Sut-ton, 1997), tenure in industry (Stinchcombe, 1965;Tripsas, 2009), and changing technology regime(Dowell and Swaminathan, 2006; Tushman andAnderson, 1986). Firms that successfully over-come these impediments—rising to incumbency inthe new industry—must reconfigure existing oper-ations (Karim, 2006) in order to plan and executegrowth (Penrose, 1959).

We propose that de novo firms will have fewerintegrative capabilities (Helfat and Raubitschek,2000) and less transformational experience (Kingand Tucci, 2002) to draw upon than diversifyingfirms when they must integrate new resources toface these impediments. We test this prediction inthe empirical context of the U.S. wireless telecom-munications industry in 1983–2004, when a mixof de novo and diversifying firms raced to establishand grow service networks through a tumultuousperiod of growth and change. We find that size,tenure in industry, and technology regime changedid, in fact, slow the growth of de novo firms morethan they slowed comparable diversifying firms.Our results are consistent with the proposition thatde novo entrants may be able to overcome infe-rior resources initially because their core knowl-edge better fits the new industry’s needs (Helfatand Lieberman, 2002; Helfat and Raubitschek,2000; Teece, 1986). However, de novo firms haveless general experience (Teece, 1986), developedroutines (Nelson and Winter, 1982), and integra-tive or transformational experience (Helfat andRaubitschek, 2000; King and Tucci, 2002) thandiversifying firms, and this gap appears to exact a‘growth penalty’ as they transition to incumbency.

1 This is also consistent with entrepreneurship literature, wherethe entrepreneurial or established firm distinction is based onsize, firm tenure, and technological shocks (e.g., Agarwal,Ganco, and Ziedonis, 2009).

By undertaking a study of growth of firmsas they face the challenges of incumbency, weintegrate firm and industry evolution and extendthe literature in research streams in entrepreneur-ship, strategy, and organizational theory. In entre-preneurship, we highlight once again thatestablished firms can be an important source ofentrepreneurial activity when they enter new mar-kets and compete in technology-intensive indus-tries. Our analysis and findings stand in starkcontrast to most theories of industry evolution,entrepreneurship, and strategy, which predict aninitial advantage for diversifying firms that erodesover time (Carroll et al., 1996; Klepper, 2002a).Instead, the results are consistent with thewidespread but little studied notion that growthis a particular challenge for entrepreneurial or denovo firms. In particular, the pattern of slow-ing growth in the face of impediments suggeststhat the capability to renew and reconfigure oper-ations is one of the key deficits that de novofirms face in competition with firms that possessprior experience. This finding suggests that pre-entry experience helps diversifying firms developsuperior dynamic capabilities (Carroll et al., 1996;Eisenhardt and Martin, 2000; Ganco and Agarwal,2009; Teece, Pisano, and Shuen, 1997), engagein strategic renewal (Agarwal and Helfat, 2009),and successfully transition to incumbency. One ofthe essential tasks for future research, then, is tounderstand how firms transform experience intothis ability, and whether the process can be accel-erated through effective knowledge management.

THEORETICAL FRAMEWORK ANDHYPOTHESES

Since the seminal work of Penrose (1959) and Nel-son and Winter (1982), a rich line of researchhas focused on the importance of routines andpath dependence in the persistence of heteroge-neous firm capabilities and performance. Broadly,de novo and diversifying firms2 differ in two

2 We note that this definition relies on pre-entry experience atthe firm level of analysis, rather than pre-entry experience ofindividuals/teams of individuals who found a firm or representits top management team. Since founder pre-entry experience isan important determinant of heterogeneous capabilities and per-formance (Klepper, 2002a; Phillips, 2002; Agarwal et al., 2004),such spin-out firms could also be classified as possessing pre-entry experience, or at least a hybrid organization between the

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

254 P.-L. Chen, C. Williams, and R. Agarwal

important dimensions: access to core knowledgespecific to the industry (Helfat and Lieberman,2002; Teece, 1986), and development of inte-grative knowledge (Hannan and Freeman, 1984;Helfat and Lieberman, 2002; Helfat andRaubitschek, 2000). While both types of knowl-edge have performance consequences, the lattertype of knowledge is particularly important interms of capabilities that help overcome impedi-ments to growth, the focal issue examined in ourpaper.

We begin with a brief review of extant literatureon the differences between de novo and diversi-fying firms and the anticipated impact of thosetraits on firm performance. We then develop ourcore theoretical proposition comparing the abilityof de novo and diversifying firms when confrontedwith impediments to growth as they transition fromentrants to incumbents. This leads us to hypothe-size about how pre-entry experience interacts withsize, tenure in industry, and change in technologyregime leading to different patterns of growth.

Initial capabilities and performance after entry

Popular wisdom frequently credits de novo firmswith being more focused and nimble, suggestingthat they will outmaneuver their more experiencedrivals and grow more quickly in new industries.De novo firms, by definition, start with a ‘cleanslate’ and enter by configuring their resources tomatch the focal industry’s competitive environ-ment. Given their singular focus on this indus-try context, de novo firms can better cater to thedemands of customers, suppliers, and other insti-tutional players. Their core knowledge (Helfat andRaubitschek, 2000) is more likely to be suited tothe technology and state of the market in the indus-try at time of entry. De novo firms can also lever-age their flexibility to generate higher rates of newproduct innovations (Khessina and Carroll, 2008)and to avoid the myopic learning (Levinthal andMarch, 1993) and competency traps (Levitt andMarch, 1988) inherent to more established firms.Anecdotally, in the context of the semiconductor

two (Qian, Agarwal, and Hoetker, forthcoming). While acknowl-edging this issue, we retain the distinction at the firm-level unitof analysis since our interest is in examining the evolution offirm-level routines, capabilities and growth trajectories. As astand-alone firm, spin-outs lack the experience of functioningin a competitive environment and producing goods and services(Helfat and Lieberman, 2002).

industry, Holbrook et al. (2000) describe how denovo firms Shockley and Fairchild Semiconductor,unfettered by past electrochemical technologicaland manufacturing traditions, chose entirely newtechnologies and experimented with alternativematerials and processes. In the process, FairchildSemiconductor coinvented and mastered the dom-inant design of the monolithic integrated circuit,in which all components are manufactured on asingle piece of silicon.

Theory also suggests that diversifying firmsmight be more constrained and less flexible thande novo firms upon entering a new market. Whilediversifying firms often enjoy better resourceendowments than de novo firms because they canleverage existing firm resources (Farjoun, 1998;Markides and Williamson, 1994; Miller, 2006;Teece et al., 1994), they typically must negotiateresource gaps because the new market requiresa specific capability they lack, or because somepre-entry resources and capabilities are dysfunc-tional in the focal market (Helfat and Lieberman,2002). This initial lack of fit to the focal indus-try context requires significantly more adaptationthan de novo firms, which do not have to negoti-ate internal sources of inertia or have long-standingcommitments to established value networks (Hilland Rothaermel, 2003). For example, while diver-sifying firms Sprague and Motorola brought relatedexperience from electrochemistry into semicon-ductor manufacturing, they faced serious chal-lenges as they developed hybrid circuits that couldbe used in conjunction with electrochemical tran-sistors. In addition to the challenges of reconfig-uring technological capabilities, both firms had tobalance conflicting needs of existing and new cus-tomer segments and address managerial cognitivebiases and coordination problems that arose dueto differences in geographic locations of R&D andproduction (Holbrook et al., 2000).

Nonetheless, diversifying firms possess supe-rior resource endowments from other markets, andhave better access to financing, managers, technol-ogy, and relationships, (Carroll et al., 1996; Helfatand Lieberman, 2002; Klepper and Simons, 2000;Lane, 1989). Further, early diversifying firms canalso influence the competitive landscape to bet-ter fit their own resources and capabilities (Carrollet al., 1996; Helfat and Lieberman, 2002; Klepperand Simons, 2000; Mitchell, 1991; Tripsas, 1997).For instance, IBM followed Apple and other denovo firms into the PC industry, but leveraged

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 255

its extensive core and complementary resourcesto ensure that DOS-based PCs became the domi-nant standard (Bayus and Agarwal, 2007; Steffens,1994).

Empirical studies of diversifying and de novofirm advantages find patterns of performance andsurvival that match each of these theoretical sto-ries. Ganco and Agarwal’s (2009) literature reviewdocuments evidence for a diversifying firm advan-tage (Barnett and Freeman, 2001; Klepper andSimons, 2000), a de novo advantage (Agarwalet al., 2004; Khessina and Carroll, 2008), and acombination of the two (Bayus and Agarwal, 2007;Carroll et al., 1996; Hannan et al., 1998; Khessina,2006; Klepper, 2002a). With these contrary expec-tations in mind, we make no prediction for therelative growth rates of the two types of firms whenthey are new entrants in the focal industry, and inthe absence of impediments to growth. However,as both types of firm transition into incumbency,differences in their ability to undertake strategicrenewal may result in performance differentials,an issue we now turn to.

Renewal ability of de novo and diversifyingfirms

The above attribution of potential diversifyingfirms’ advantage to superior resource endowmentsignores the potential value of a diversifying firm’sintegrative knowledge—its ability to reconfigurefirm resources for new challenges or, as definedby Helfat and Raubitschek (2000), the knowledgeof how to integrate different activities, capabilities,and products in one or more vertical chains. Inte-grating knowledge and activities across the firm isessential for strategic renewal.

To understand whether diversifying firms orde novo firms will be more capable of strategicrenewal, we need to examine how their resourcesand capabilities enable or constrain integrativeknowledge. In navigating the change to a newenvironment before or immediately after entry,diversifying firms amass integrative knowledge.They learn to scout and evaluate new marketopportunities, for example, to integrate demandand technology signals and to restructure exist-ing resources to enter a new market (Gancoand Agarwal, 2009; Helfat and Lieberman, 2002;Mitchell, 1989). By recombining firm resources tofit new problems and opportunities in the focalmarket, diversifying firms engage in bricolage

(Baker and Nelson, 2005; Levi-Strauss, 1967).Thus, diversifying firms are more likely to pos-sess ‘transformational experience’ developed dur-ing their reorganization and redirection of effort tonew markets (King and Tucci, 2002).

Carroll et al. (1996) assume that de novo firmshave greater structural flexibility than diversify-ing firms, even though diversifying firms overcomeinertial tendencies to enter a new industry. In con-trast, we posit that superior integrative knowledgeand transformational experience provides diversi-fying firms with a better ability to deal with theimpediments to growth. In this sense, diversifyingfirms possess both structural and strategic flexi-bility (Volberda, 1996). Volberda (1996) definedstructural flexibility as managerial capabilities foradapting an organization’s structure and its deci-sion and communication processes to suit evolu-tionary changes, and strategic flexibility as man-agerial capabilities that allow modification of goalsin light of disruptive changes.

Holbrook et al. (2000) document the differencesbetween the two types of firms when navigat-ing changes in the semiconductor industry. Denovo firms Shockley and Fairchild were able toleverage their initial fit for an early competitiveadvantage, but were less successful when changesrendered their core information advantage obso-lete. At Shockley, for example, top management’sfocus on research and treatment of production as asubordinate turned into a disadvantage when man-aging the growing importance and complexity ofproduction. Similar problems plagued Fairchild,which could not keep up with new competitionand new technologies (Malone, 1985). In contrast,diversifying entrant Motorola’s skillful manage-ment and coordination of R&D, production, andmarketing enabled successful adaptation to mar-ket changes. Similarly, while de novo Fairchildinitially led the way in the development of the inte-grated circuit dominant design, diversifying firmTexas Instruments—credited with coinventing theintegrated circuit—ultimately outpaced Fairchild.

In sum, we believe that prior experience over-coming impediments to growth in other mar-kets, and the transformative experience of entryinto the focal industry, provides diversifying firmswith more effective integrative knowledge. Thisintegrative knowledge enables strategic renewal,and thus helps diversifying firms navigate thetransition to incumbency in the focal industrybetter than de novo firms. In contrast to the

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

256 P.-L. Chen, C. Williams, and R. Agarwal

mixed predictions for performance immediatelyafter entry into the industry, this theory suggestsan unequivocal advantage for diversifying firmsas they face situations requiring strategic renewal,and particularly as they face the impediments togrowth that arise in the transition to incumbency.This represents the foundational proposition of thepaper.

Proposition: Diversifying firms are more capa-ble of strategic renewal than de novo firms.

Transition to incumbency and impediments togrowth

Separate from the research on de novo and diversi-fying firms, a rich literature on incumbent-entrantdynamics examines the challenges of incumbencyin the face of ‘creative destruction’ represented byentrants (Agarwal and Gort, 1996; Christensen andRosenbloom, 1995; Cooper and Schendel, 1976;Gort and Klepper, 1982; Henderson and Clark,1990; Tushman and Anderson, 1986; Utterback,1994). Notwithstanding a few exceptions (Bayusand Agarwal, 2007; Ganco and Agarwal, 2009;Methe, Swaminathan, and Mitchell, 1996; Sosa,2006), this research stream largely lumps togetherboth diversifying and de novo firms that enterthe industry (Cooper and Schendel, 1976; Gortand Klepper, 1982; Henderson and Clark, 1990).No research, however, has examined how the twotypes of firms transition to the status of incumbentafter entry.

While entrants are easily classified by appear-ance at a point in time, the status of incumbent isless distinct. In precise usage, incumbents are theestablished firms that exist when a new firm enters.In practice, when firms enter a market continu-ously, it is less clear which firms are ‘establishedincumbents’ at the time of entry since some exist-ing firms will be other recent entrants. Theoreti-cally, the concept of incumbency is closely relatedto the concepts of market power, resources, andlegitimacy. Firms are accorded legitimacy, garnerresources, and gain power as they spend moretime in the industry, as they grow in size, andas they survive major transitions in the industry.Accordingly, incumbency status has been linkedto three characteristics across literature streams inentrepreneurship, organizational demography, andindustry evolution: firm size (Acs and Audretsch,1990; Agarwal et al., 2009; Caves, 1998; Sutton,

1997) tenure in industry (Agarwal et al., 2009;Stinchcombe, 1965; Tripsas, 2009), and expe-rience with prior technological regime (Dowelland Swaminathan, 2006; Tushman and Anderson,1986).

These three characteristics of incumbents—size,tenure, and technological experience—also repre-sent impediments to growth. Growth stresses theold system by threatening it with information over-load or inconsistent activities. To accommodatethe coordination and decision-making demands ofgrowth, firms must socialize new members, extendroutines, and reassign decision making to main-tain consistency while still limiting the informa-tion and decision-making demands on existingmanagers (Penrose, 1959). Size, age, and technol-ogy regime experience amplify these challengesbecause they require reconfiguration of the firm’sexisting resource base (Karim, 2006; Karim andMitchell, 2000; Penrose, 1959; Puranam, Singh,and Chaudhuri, 2009). As a result, diversifyingand de novo firms negotiating the transition toincumbency must face impediments to growth bypurposefully modifying their resource base. In thefollowing sections, we explain why each char-acteristic of incumbency represents an impedi-ment to growth, and we hypothesize that de novofirms—which have a relative disadvantage in theability to renew the firm and modify their resourcebase—will grow more slowly than diversifyingfirms as they face the impediments.

The impediment of size

The effect of size on growth has occupiedresearchers since Gibrat proposed his ‘law’ thatfirms will grow at the same rate no matter theirsize (Gibrat, 1931). Penrose’s seminal work (1959)argued that growth would peak for mid-sized firmsand then fall for large firms. Since then, manystudies have compared the growth rates of smalland large firms. While the topic is still debated(Geroski, 1995; Sutton, 1997), studies that includeprivate firms (Dunne, Roberts, and Samuelson,1988, 1989; Evans, 1987a, 1987b) and that accountfor selection bias (Hall, 1987) generally find thatsmall firms grow more quickly than large firms(Caves, 1998).

Large firms need well-developed systems fordecentralized decision making to sustain creativityand entrepreneurship while reducing the demandson top management. Concurrently, these firms

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 257

must provide information, incentives, and infor-mal organization that ensure decisions do notclash across different functions, units, or levelsof the company. Thus, size increases the chal-lenge of growth because new techniques and prac-tices are required to maintain the managementsystem in the face of larger scale. Specific bureau-cratic challenges arise for large firms in terms ofadding additional resources and people. Top exec-utives necessarily sacrifice the depth of informa-tion they can obtain about firm activities whenthe activities’ breadth is large (Williamson, 1967).The administrative intensity of organizations isalso higher for large firms, as they must devoteproportionally more resources to monitoring andcoordination (Caplow, 1957; Sutherland, 1980).The higher administrative intensity and controlsin the firm will generally dampen incentives forentrepreneurial behavior. As a result of these chal-lenges, new roles, structures, and practices mustbe created to maintain the coherent managementsystem (Chandler, 1962; Stinchcombe, 1990).

In response to higher bureaucratic challenges,firms must reconfigure activities to maintain effec-tive administration in the face of noisier infor-mation, weaker incentives, and rising complexity.Large firms must deploy integrative knowledge torecombine skills and knowledge held by the dis-parate members of the organization (Grant, 1996).The nature of administration across small and largefirms becomes so radically different ‘that in manyways it is hard to see that the two species are ofthe same genus’ (Penrose, 1959: 19). The growthof the firm at larger sizes demands reconfigurationof firm resources to match the increased adminis-trative challenges. Our core proposition that diver-sifying firms possess more developed capabilitiesfor renewal then suggests:

Hypothesis 1: At larger sizes, de novo firmswill face a larger growth penalty compared todiversifying firms.

The impediment of tenure in industry

While size represents an impediment to growthbecause of the bureaucratic costs of growth,increased tenure or age in industry represents animpediment because of the challenge of inertia.3

3 As noted above, we define firm tenure to be ‘time in focalindustry’ to maintain consistency across diversifying and de novo

Tenure in the industry represents a growth chal-lenge because historic industry-specific practicesaccumulate in an interdependent activity system;these practices create overlapping relationshipswithin the firm that are difficult to alter. Oncefirms acquire the capital and social resources tolaunch operations, they tend to imprint powerfullywith particular demands and structure of the extantenvironment (Stinchcombe, 1965). Organizationshold an imprint because the external environmentdemands consistent and reliable execution of thefirm’s mission, while internal organizational forcesdemand strong commitments to the firm’s mis-sion, core technology, and structure (Hannan andFreeman, 1984). For instance, firms that enter anindustry before a dominant design emerges aresignificantly less likely to embrace that design(Dowell and Swaminathan, 2006). In addition, asfirm tenure in the industry increases, their mem-bers increase their commitment to cultural scriptsthat dictate beliefs and actions concerning ways ofdoing things and the firm’s mission (Harrison andCarroll, 2006). For example, Tripsas (2009) dis-cusses the challenges faced by de novo firms overtime as they navigate through identity and iner-tial pressures both within and outside firm bound-aries. Evolutionary theories of organization sug-gest that these accumulated automatic behaviors,connections, and inertia have both benefits andcosts (Nelson and Winter, 1982). In the context ofgrowth, however, a firm’s historic commitmentsand operations tend to increase the challenge ofincorporating new resources and people.

These commitments increase the challenge ofincorporating new resources because they rep-resent an interdependent system of connectionsbetween activities and knowledge in the firm(Argote and Ingram, 2000). This interdependencemakes it more costly and difficult to adopt new,complementary systems of production, such as thesystem of flexible manufacturing practices thatarose in the 1980s and 90s (Milgrom and Roberts,1990). In addition, the interdependence of activi-ties makes knowledge transfer more costly withinthe firm (Rivkin, 2000) and between partners(Williams, 2007). These overlapping commitments

firms. Our arguments for time as an impediment to growth relateto focal industry environmental conditions and the accumulationof routines and commitments within the industry. Diversifyingfirms’ efforts at altering existing capabilities to enter the focalindustry implies a ‘restarting of their clock’ for a better fit withthe focal industry conditions (Helfat and Lieberman, 2002).

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

258 P.-L. Chen, C. Williams, and R. Agarwal

and connections mean that incorporating new peo-ple and resources in one area of the firm requireschanges to other areas. Empirical studies also pro-vide strong evidence that firm growth slows withage and tenure in an industry (Dunne et al., 1988,1989; Evans, 1987a, 1987b; Sutton, 1997).

Beyond the focal industry context, it is truethat diversifying firms are older and have exist-ing commitments and activities from other indus-tries. These prior commitments, however, willaffect diversifiers’ growth rate at entry. Withincreased industry tenure and concomitant transi-tion to incumbency, we predict that de novo firmswill struggle more with growth challenges eventhough they are younger in absolute terms thandiversifying firms, because they possess less devel-oped integrative knowledge. Specifically, diversi-fying firms have valuable prior experience manag-ing interdependence, which is likely to make themmore proficient at modularizing activities (Bald-win and Clark, 2000; Henderson and Clark, 1990)and are more likely to have administrative sys-tems that can cope with increased complexity. Fac-ing impediments from increasing age in the focalindustry, we believe diversifying firms can deploythis integrative knowledge to manage interdepen-dence more effectively than de novo firms. Thisleads us to hypothesize:

Hypothesis 2: At greater levels of industrytenure, de novo firms will face a larger growthpenalty compared to diversifying firms.

The impediment of technology regime

A change in technology regime represents a dis-continuous shock to the industry that demandsnew configurations of organizational and manage-rial resources. This is also a key context withinwhich the dynamics between entrants and incum-bents have been studied. Technological shifts causenew entrant information to become more important(Gort and Klepper, 1982), require incorporation ofnew resources that conflict with accepted routinesin the industry (Abernathy and Utterback, 1978),and devalue the existing resources of the incum-bent firm (Tushman and Anderson, 1986). Firmsmay have a hard time perceiving that reconfigura-tion is necessary (Henderson and Clark, 1990), andeven if they do so, face the innovator’s dilemma

given existing technological and demand commit-ments (Christensen, 1997). The critical impedi-ment to growth in the face of a changing technicalenvironment is the need to reconfigure the exist-ing managerial system while incorporating novelresources and practices. Given that technologicalregime changes are often competence destroying(Tushman and Anderson, 1986), firms need totake stock of which competences to divest, andwhich ones still retain value. This is particularlyhard if the external change renders core capabil-ities of the firm obsolete. Even seemingly smallchanges may require reconfiguration of embeddedpractices in ways that are difficult to perceive andreact to (Henderson and Clark, 1990). Agarwaland Helfat (2009) document, in the case of thedigital technology shock in the camera industry,that once dominant firms Konica and Minolta hadto exit the industry. Even though Kodak survivedthe regime change, it faced significant hurdles inregaining part of its earlier market position. Simi-larly, Dowell and Swaminathan (2006) found thatentrants to the bicycle industry were constrainedby early technological choices: those that enteredbefore the dominant design emerged had a hardtime transitioning to the new design. Often thetechnological change is accompanied by changesin customer demand (Adner, 2002; Agarwal et al.,2004; Tripsas, 2009), requiring firms to under-take strategic renewal along multiple dimensions:business model, technological base, organizationalstructure, and organizational mindset (Agarwal andHelfat, 2009).

Within this context, diversifying firms can usetheir experience and integrative knowledge to reactto the need for novel configurations when mar-kets go through technology regime changes. Theirtransition from entrant to incumbency status whenconfronted with the impediment of a changingtechnological regime is enabled by their priorexperience in negotiating such transformations inorder to enter the industry, an experience that islacking among de novo firms that are facing sucha transition perhaps for the first time. In differentindustries, Bayus and Agarwal (2007) and Dowelland Swaminathan (2006) show that diversifyingfirms are better able to switch technologies after adominant design is established than de novo firms.Accordingly, we argue that diversifying firms willbetter weather the discontinuous change relative tode novo firms. Thus,

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 259

Hypothesis 3: After a shift to a new technologyregime, de novo firms will face a larger growthpenalty than diversifying firms.

In summary, we argue that size, tenure in indus-try, and change in technology regime representimportant impediments to growth. As firms transi-tion from entrants in the focal industry to becomemore established incumbents, their growth in theface of these impediments requires that they recon-figure management systems and informal organiza-tion so that they can maintain coherent and reliablebehavior in the face of these changing demands(Nelson and Winter, 1982; Penrose, 1959). Diver-sifying firms possess more developed renewalcapabilities through their experience in other mar-kets and the experience of entering the focal mar-ket, so we hypothesize that de novo firms willincur a larger growth penalty in the face of theseimpediments.

It is important to distinguish this predictedadvantage for diversifying firms from an overallgrowth advantage. All firms face limits to growthin any period (Penrose, 1959). We make no com-parative prediction about the baseline growth ratesof the two types of firms immediately after entry.Theory suggests many alternative endowments thatdiversifying firms possess that might give them auniform advantage over de novo firms. Theory alsosuggests, however, that de novo firms are able tomatch their core operations more closely to thedemands of the industry at the time of entry. Thus,we leave open the possibility that de novo firmswill grow faster than diversifying firms when thefirms do not face these impediments, that is, whenthe two types of firms are small, young in theindustry, and founded in the current technologyregime. Faster growth rates for de novo firms couldarise in the absence of impediments to growthif de novo firms possess a flexibility advantagethat allows them to match their core operationsmore closely to the competitive demands of theenvironment. The focus of our predictions, how-ever, is that when both firms face impedimentsto growth, diversifying firms will face a smallergrowth penalty than de novo firms.

Finally, size, tenure in industry, and chang-ing technology regime are naturally highly corre-lated. Size and tenure tend to increase together,especially in an evolving industry with growingdemand. In addition, increased tenure in industrywill expose firms to more chances for a change in

technology regime, so exposure to this change islikely to rise with tenure. Since we believe theseare three specific instances of the more fundamen-tal concept of an impediment to growth, we testfor the effect of each separately, and then examinetheir joint effect.

EMPIRICAL CONTEXT ANDMETHODOLOGY

Industry context

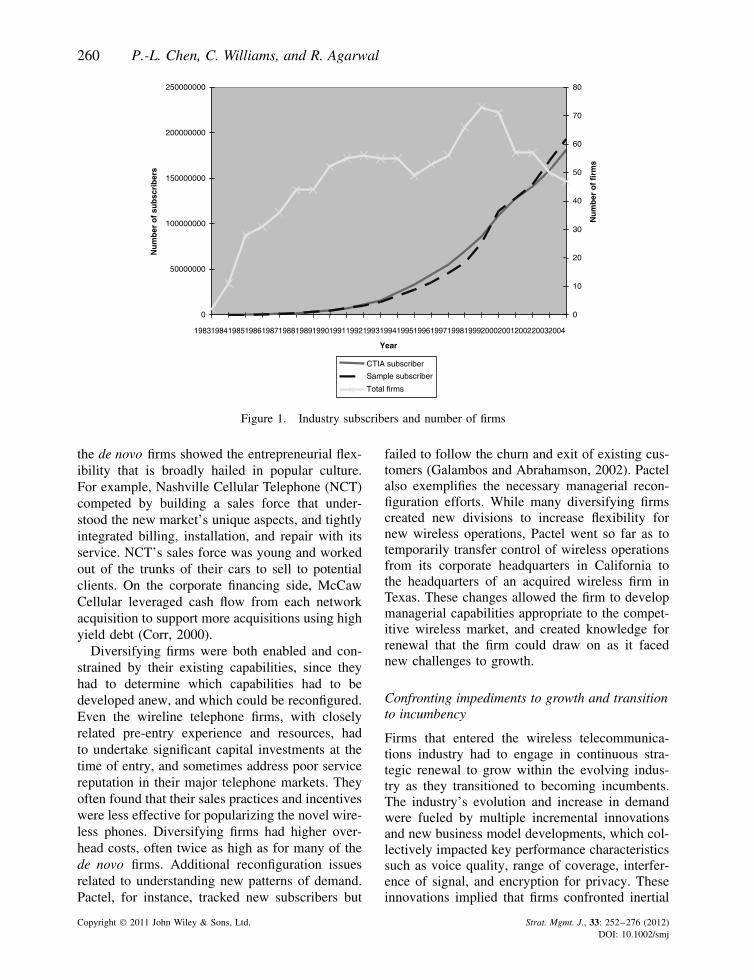

We test our hypotheses using data from the U.S.wireless telecommunications industry from 1983to 2004. Firms provide wireless radio communi-cations services based on regional licenses fromthe Federal Communications Commission (FCC).The industry emerged in 1983, when AmeritechMobile Communications launched the first com-mercial wireless telecommunications in Chicago.Fueled by the FCC granting hundreds of newlicenses, the industry experienced significant entryand rapid growth in sales (number of cellular sub-scribers). Figure 1 depicts the number of wire-less telecommunications firms in the industry andthe total number of subscribers in each year. Weinclude both composite data from the CellularTechnology Industry Association (CTIA) and theaggregate statistics for the firms in our sample. Thetrends conform to patterns documented in priorindustry evolution studies (Agarwal and Bayus,2002; Gort and Klepper, 1982). Additionally, theindustry experienced a major discontinuous tech-nological regime change from analog to digitaltransmission, which first entered the market in1991 and took off around 1993.

Development and reconfiguration of capabilitiesfor entry in the analog era of wirelesscommunications

The 1984 FCC lottery selection process resultedin significant variation in the types of firms thatentered the wireless communications industry. Inaddition to de novo firms, firms from relatedindustries such as television, broadcasting, paging,and landline-telephones also offered wireless ser-vices. De novo firms developed their capabilitiesfrom scratch, investing in technical and operationalcapabilities, and several also engaged in allianceswith firms related in the value chain. Many of

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

260 P.-L. Chen, C. Williams, and R. Agarwal

0

50000000

100000000

150000000

200000000

250000000

19831984 19851986198719881989199019911992199319941995199619971998199920002001200220032004

Year

Nu

mb

er o

f su

bsc

rib

ers

0

10

20

30

40

50

60

70

80

Nu

mb

er o

f fi

rms

CTIA subscriber

Sample subscriber

Total firms

Figure 1. Industry subscribers and number of firms

the de novo firms showed the entrepreneurial flex-ibility that is broadly hailed in popular culture.For example, Nashville Cellular Telephone (NCT)competed by building a sales force that under-stood the new market’s unique aspects, and tightlyintegrated billing, installation, and repair with itsservice. NCT’s sales force was young and workedout of the trunks of their cars to sell to potentialclients. On the corporate financing side, McCawCellular leveraged cash flow from each networkacquisition to support more acquisitions using highyield debt (Corr, 2000).

Diversifying firms were both enabled and con-strained by their existing capabilities, since theyhad to determine which capabilities had to bedeveloped anew, and which could be reconfigured.Even the wireline telephone firms, with closelyrelated pre-entry experience and resources, hadto undertake significant capital investments at thetime of entry, and sometimes address poor servicereputation in their major telephone markets. Theyoften found that their sales practices and incentiveswere less effective for popularizing the novel wire-less phones. Diversifying firms had higher over-head costs, often twice as high as for many of thede novo firms. Additional reconfiguration issuesrelated to understanding new patterns of demand.Pactel, for instance, tracked new subscribers but

failed to follow the churn and exit of existing cus-tomers (Galambos and Abrahamson, 2002). Pactelalso exemplifies the necessary managerial recon-figuration efforts. While many diversifying firmscreated new divisions to increase flexibility fornew wireless operations, Pactel went so far as totemporarily transfer control of wireless operationsfrom its corporate headquarters in California tothe headquarters of an acquired wireless firm inTexas. These changes allowed the firm to developmanagerial capabilities appropriate to the compet-itive wireless market, and created knowledge forrenewal that the firm could draw on as it facednew challenges to growth.

Confronting impediments to growth and transitionto incumbency

Firms that entered the wireless telecommunica-tions industry had to engage in continuous stra-tegic renewal to grow within the evolving indus-try as they transitioned to becoming incumbents.The industry’s evolution and increase in demandwere fueled by multiple incremental innovationsand new business model developments, which col-lectively impacted key performance characteristicssuch as voice quality, range of coverage, interfer-ence of signal, and encryption for privacy. Theseinnovations implied that firms confronted inertial

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 261

pressures of the technology that they entered with,and had to engage in strategic renewal to stayabreast of the evolving technology.

Firms also engaged in other strategic renewalefforts as they exploited opportunities for increas-ing their customer base and coped with increas-ing competition. For instance, roaming agreementswere key to increasing geographic scope and callernetwork base while staying price competitive. Toenable subscribers to receive calls while travel-ing, firms needed to address the technical chal-lenges of how to connect subscribers’ handsetswhen they were in a partner’s territory. Firmsalso needed to develop systems to record andappropriately bill/share revenues for such roam-ing calls. Other incremental innovations related toserving customer needs cost effectively, sometimesthrough the development of outsourcing agree-ments. Larger firms had to invest disproportion-ately in developing capabilities related to theirsubscriber base: some coordinated with externalbilling companies to handle the increased volumeof subscribers, while others developed better inter-nal capabilities related to automatic billing andcredit checking systems. Indeed, as the wirelesstelecommunications industry matured, key suc-cess factors shifted away from reliability, tech-nology, and interoperability and toward brand,reputation, and service. As a result, successfuloperators shifted from a business configuration inwhich technology and operations dominated deci-sion making to one in which marketing and cus-tomer service dominated.

Transformation and reconfiguration of capabilitiesdue to regime change to digital technology

The industry transition from analog to digital wire-less telecommunications represented a major dis-ruption that required firms to undertake significantreconfiguration and, thus, was an additional imped-iment to growth. Unlike the continuous signal ofanalog service, digital service converted speechinto binary bits that improved performance charac-teristics and enabled more efficient use of the radiospectrum. Moreover, digital technology increasedthe scope of potential services from voice aloneto images, music, and data (Calhoun, 1988; PRNewswire; Gruber, 2005).

Multiple challenges were encountered in thetransformation to digital transmission. First, the

industry was confronted with a ‘war’ where sev-eral standards (e.g., NAMPS, IS-45 TDMA, IS-136 TDMA, GSM, IS-95 CDMA) competed fordominance. Further, existing internal and externalvalue chains had to be significantly restructured.Internal value chain restructuring required firms toalter equipment, reconfigure wireless transmissionsites for optimal space allocation, develop rules forefficient and effective digital conversion, migratecustomers from analog to digital service, educatesales force and reshape front-line operations tomeet increasing demands for customer service. Forexample, the introduction of personal communi-cation systems (PCS) digital technology requiredinternal collaboration between a firm’s assets man-agement department and technical department toreconfigure radio sites due to the reduction ofthe size of transmission equipment. While analogtechnology required significantly more real estateto set up giant towers, higher-density PCS cellsites required significantly less space and could beplaced inside a building. There was also signifi-cant variation in the rules used by firms for digitalconversion. Bell Atlantic Mobile systems openeda new, $5-million regional operations center andswitching facility in the University Research Parknear Charlotte, North Carolina, and quadrupled callprocessing capability when converting to digitaltechnology. Meanwhile, U.S. Cellular relied on analliance with Numerex for expertise in migratingcustomers from analog to a digital network. Inthe context of front-line sales and customer ser-vice, AT&T Wireless introduced new retail outletsoffering cellular phone and telephone service whenconverting to digital technology, and Ameritechopened 21 new ‘One-Stop Communications Cen-ters’ in several states while rebranding its remain-ing 99 retail outlets as Ameritech Cellular Centers.

The technological regime change also causedsignificant changes in the external value chain ofthe industry, causing disruptions in existing part-nerships and supply chain relationships as theyrelated to technology sourcing, complementaryproducts, and distribution channels. For example,to attract new subscribers and evolve its exist-ing network, Vanguard Cellular Systems switchedpartners to work closely with Nortel and BNRfor the switch and radio units that provided theflexibility of operations in both analog and digitalmode. Firms often switched to new suppliers whenexisting suppliers were reluctant to move to digitaltechnology, endorsed a different digital standard,

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

262 P.-L. Chen, C. Williams, and R. Agarwal

or had lower digital technological capabilities. Forinstance, in spite of a long-standing relationshipwith Motorola, Nynex Mobile and Ameritech Cor-poration switched to Qualcomm (Business Week,1990). Some firms forged new partnerships to offerproducts and services enabled by the digital tech-nology, as when AT&T Wireless collaborated withBloomberg Financial Markets to offer financialnews for users of its PocketNet digital phone. Mar-keting agreements between Bell Atlantic Mobileand Comverge Technologies offered utility com-panies automated meter reading, environmentalmonitoring, energy management, and distributedgeneration monitoring services.

Thus, we believe the history of the wirelesstelecommunications industry makes it an ideal set-ting for our study: there was significant variationin the pre-entry experience of firms, a variety ofincremental changes in both supply and demandcharacteristics representing opportunities and chal-lenges for firm growth, and a major technologicalregime shift that required firms to undertake dis-continuous transformation to survive and grow.

Data description

To obtain a comprehensive list of wireless telecom-munications firms in the United States in each yearfrom 1983 to 2004, we collected data from multi-ple sources, including annual directoriespublished by Phillips Publishing, the FCC’s Uni-versal Licensing System (ULS), and industrialmagazines and publications such as Cellular Busi-ness, Cellular Radio: Birth of an Industry (1983),Cellular Marketplace (1984) and The Status of theCellular Industry (1986–1992). Additionally, weobtained relevant information on license ownershipand licensees’ activities from LexisNexis, com-pany annual reports and 10Ks, and Donaldson,Lufkin and Jenrette Inc.’s Cellular Communica-tions Industry Report (1985, New York).

To be included in our sample, we defined wire-less telecommunications firms as firms that main-tained majority ownership in a cellular phonelicense, purchased inputs such as communicationequipment, and actually provided wireless commu-nications service. This allowed us to rule out firmsor individuals entering the industry solely to real-ize short-term gains from arbitrage, particularly asthis occurred early in the industry when sales werevery low. Our final dataset consists of an almost-census of the 77 wireless telecommunications firms

for a total of 506 firm-year observations from 1983to 2004. As depicted in Figure 1, the annual trendin subscribers attributable to sample firms closelymatches the trend reported by CTIA.

Model specification and estimation

We test our hypotheses in an empirical growthmodel, which examines effects of explanatory vari-ables on the annual growth of a firm’s subscribers.Following the standard approach to growth models(c.f. Geroski, 2005), we define the natural loga-rithm of the growth rate (r) as

Ln(rit ) = ln(

subscribersit

subscribersit−1

)

= ln(subscribersit ) − ln(subscribersit−1)

= α + γ ln(subscribersit−1) + βXit−1 + ε

where i denotes the firm of interest and t denotesthe year, α is an intercept, X is a vector of otherexplanatory and control variables, β is a vec-tor of estimated parameter values for those vari-ables, and ε is an error term. To consider whethersize affects the growth rate, our right-hand sideequation includes lagged size, ln(subscribersit−1),with a parameter effect of γ . We consolidate thelagged variables on the right-hand side, thus ourfinal growth model becomes the following:

ln(subscribersit ) = α + ln(subscribersit−1) + γ

ln(subscribersit−1) + βXit−1 + ε

Gathering the lagged size terms together givesus:

ln(subscribersit ) = α + (1 + γ )

ln(subscribersit−1) + βXit−1 + ε

The coefficient of the lagged size variable, (1 +γ ), is thus benchmarked at 1. For no effect ofsize(γ = 0), the coefficient is 1; if larger firmsgrow faster than smaller firms(γ > 0), the coef-ficient is greater than 1, and if vice versa, thecoefficient is less than 1.

We estimate this model using a panel regres-sion estimator with random effects to account forunobserved heterogeneity among the firms andHuber-White heteroskedasticity-consistent errors,clustered by firm (Table 2). To ensure robustness

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 263

of results, we also analyze the effect of our vari-ables of interest on the likelihood of exit (Table 3).For this model we use a panel complementary log-log estimator, as recommended by Allison (1982).

Dependent variables

Firm growth: Our central dependent variable, firmgrowth, is the increase in firm size, measured intotal subscribers, over two consecutive periods.As described above in the model specificationsection, the dependent variable of firm growthis transformed into the logarithm of subscribersin a given year, with the lagged values of thevariable collected on the right- hand side. Thus, thedependent variable in the analysis of firm growthis the natural logarithm of subscribers for firm i inyear t , or ln(subscribersit ).

Firm exit : As a robustness check, and given thewidespread use of firm exit in studies that exam-ine the relationship between pre-entry experienceand performance (Bayus and Agarwal, 2007; Car-roll et al., 1996; Klepper and Simons, 2000), weexamine firm exit as an additional dependent vari-able. If a firm ceases independent operations inyear t , the variable firm exit is coded as 1 thatyear, and 0 in the years between firm entry andyear t . We note that firms rarely liquidate assetssince the FCC licenses, along with other assetsthat they may have developed, retain value to theindustry when bundled with operations. Accord-ingly, the chief mode of exit is by acquisition byanother firm.

Key explanatory variables

The explanatory variables in our study relate topre-entry experience, firm size, tenure in the wire-less telecommunications industry, and technologi-cal regime.

De novo

Following prior literature, we define a firm as a denovo firm if it was founded in the wireless telecom-munications industry, and as a diversifying firmif it operated in another industry prior to enter-ing wireless telecommunications. Accordingly, thevariable de novo is coded as 1 if the firm was a denovo and 0 otherwise. Among all the entrants, 25percent were de novo firms.

Firm size

The growth model includes lagged size as anexplanatory variable. This variable is computed asthe natural logarithm of subscribers for the focalfirm i in year t − 1 . Please refer to the section onmodel specification above for details regarding theinterpretation of the coefficient.

Tenure in industry

Firm tenure in industry is measured as the years afirm has been in operation in the wireless telecom-munications industry, and equals the differencebetween time t and entry year.

Entered in prior technology regime

This variable captures changes in the industry envi-ronment due to the discontinuous regime changefrom analog to digital. The variable ‘entered inprior technology regime’ is coded as 1 if the firmentered the industry before 1991 and the year ofobservation is later than 1991 and zero otherwise;that is, it is coded as 1 if the firm entered duringthe analog era and is currently operating in the dig-ital era and 0 if the firm operates under the sametechnology regime in use when it entered (analogor digital). The analog regime is defined as endingin 1991 when the first digital service is introduced.In robustness analysis we found little substantivedifference in the results if we coded the transitionas occurring in 1996, when service began in a newset of licenses issued by the FCC for digital servicein a new part of the radio spectrum.

Control variables

We include several firm- and industry- level con-trols to account for both fixed- and time-varyingeffects. Our firm-level controls include firm yearof entry to capture effects of imprinting at time ofentry. Further, scholars in the industry evolutionliterature have identified evolutionary changes oftwo types: industry life cycle changes as they relateto increased standardization and development ofthe industry (captured by number of firms, indus-try sales, and growth), and disruptive technologicalchange (as captured by technology s-curves andregime changes). While the latter is an explanatoryvariable of interest, we control for the effects ofcontinual life cycle changes over time (and shifts

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

264 P.-L. Chen, C. Williams, and R. Agarwal

of key success factors from reliability, technologyand interoperability toward brand, reputation, andservice) by including variables used in prior liter-ature. These include the linear and quadratic termsfor total number of firms in the prior year, thenatural logarithm of all industry subscribers in theprior year (industry size), and the natural log ofnew industry subscribers added in the prior year(industry growth).

RESULTS

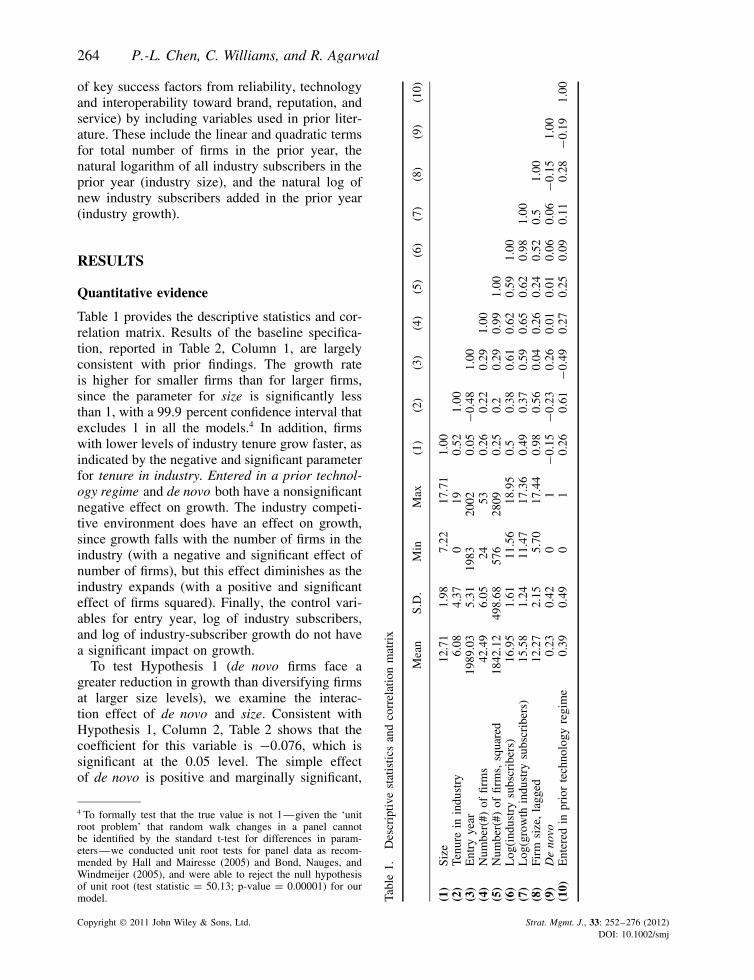

Quantitative evidence

Table 1 provides the descriptive statistics and cor-relation matrix. Results of the baseline specifica-tion, reported in Table 2, Column 1, are largelyconsistent with prior findings. The growth rateis higher for smaller firms than for larger firms,since the parameter for size is significantly lessthan 1, with a 99.9 percent confidence interval thatexcludes 1 in all the models.4 In addition, firmswith lower levels of industry tenure grow faster, asindicated by the negative and significant parameterfor tenure in industry. Entered in a prior technol-ogy regime and de novo both have a nonsignificantnegative effect on growth. The industry competi-tive environment does have an effect on growth,since growth falls with the number of firms in theindustry (with a negative and significant effect ofnumber of firms), but this effect diminishes as theindustry expands (with a positive and significanteffect of firms squared). Finally, the control vari-ables for entry year, log of industry subscribers,and log of industry-subscriber growth do not havea significant impact on growth.

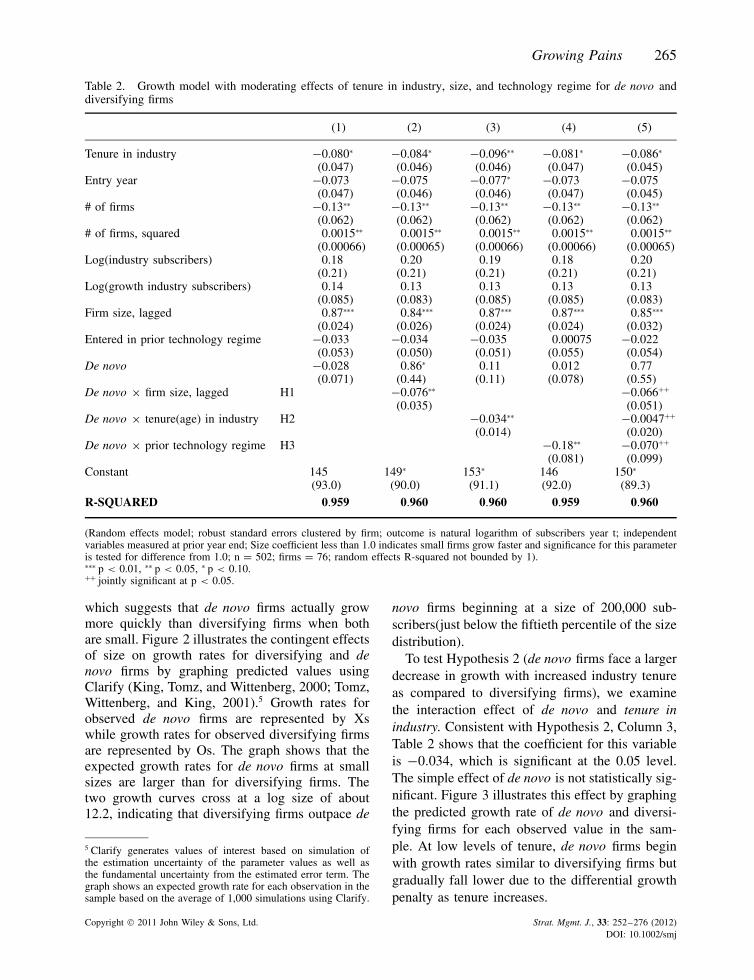

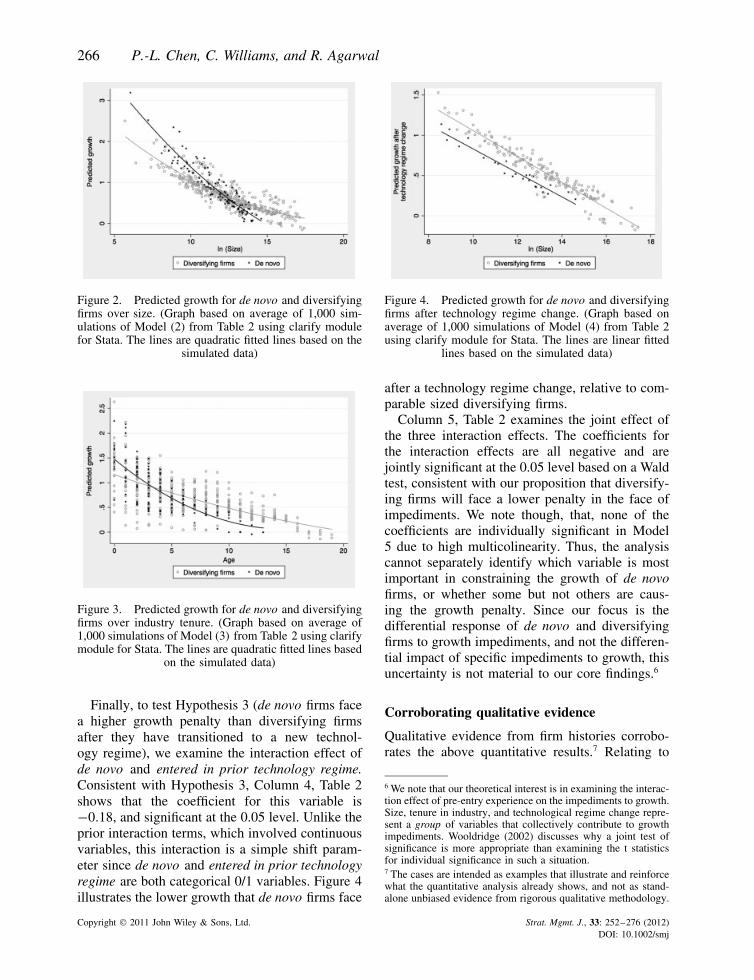

To test Hypothesis 1 (de novo firms face agreater reduction in growth than diversifying firmsat larger size levels), we examine the interac-tion effect of de novo and size. Consistent withHypothesis 1, Column 2, Table 2 shows that thecoefficient for this variable is −0.076, which issignificant at the 0.05 level. The simple effectof de novo is positive and marginally significant,

4 To formally test that the true value is not 1—given the ‘unitroot problem’ that random walk changes in a panel cannotbe identified by the standard t-test for differences in param-eters—we conducted unit root tests for panel data as recom-mended by Hall and Mairesse (2005) and Bond, Nauges, andWindmeijer (2005), and were able to reject the null hypothesisof unit root (test statistic = 50.13; p-value = 0.00001) for ourmodel. Ta

ble

1.D

escr

iptiv

est

atis

tics

and

corr

elat

ion

mat

rix

Mea

nS.

D.

Min

Max

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(1)

Size

12.7

11.

987.

2217

.71

1.00

(2)

Tenu

rein

indu

stry

6.08

4.37

019

0.52

1.00

(3)

Ent

ryye

ar19

89.0

35.

3119

8320

020.

05−0

.48

1.00

(4)

Num

ber(

#)of

firm

s42

.49

6.05

2453

0.26

0.22

0.29

1.00

(5)

Num

ber(

#)of

firm

s,sq

uare

d18

42.1

249

8.68

576

2809

0.25

0.2

0.29

0.99

1.00

(6)

Log

(ind

ustr

ysu

bscr

iber

s)16

.95

1.61

11.5

618

.95

0.5

0.38

0.61

0.62

0.59

1.00

(7)

Log

(gro

wth

indu

stry

subs

crib

ers)

15.5

81.

2411

.47

17.3

60.

490.

370.

590.

650.

620.

981.

00(8

)Fi

rmsi

ze,

lagg

ed12

.27

2.15

5.70

17.4

40.

980.

560.

040.

260.

240.

520.

51.

00(9

)D

eno

vo0.

230.

420

1−0

.15

−0.2

30.

260.

010.

010.

060.

06−0

.15

1.00

(10)

Ent

ered

inpr

ior

tech

nolo

gyre

gim

e0.

390.

490

10.

260.

61−0

.49

0.27

0.25

0.09

0.11

0.28

−0.1

91.

00

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 265

Table 2. Growth model with moderating effects of tenure in industry, size, and technology regime for de novo anddiversifying firms

(1) (2) (3) (4) (5)

Tenure in industry −0.080∗ −0.084∗ −0.096∗∗ −0.081∗ −0.086∗

(0.047) (0.046) (0.046) (0.047) (0.045)Entry year −0.073 −0.075 −0.077∗ −0.073 −0.075

(0.047) (0.046) (0.046) (0.047) (0.045)# of firms −0.13∗∗ −0.13∗∗ −0.13∗∗ −0.13∗∗ −0.13∗∗

(0.062) (0.062) (0.062) (0.062) (0.062)# of firms, squared 0.0015∗∗ 0.0015∗∗ 0.0015∗∗ 0.0015∗∗ 0.0015∗∗

(0.00066) (0.00065) (0.00066) (0.00066) (0.00065)Log(industry subscribers) 0.18 0.20 0.19 0.18 0.20

(0.21) (0.21) (0.21) (0.21) (0.21)Log(growth industry subscribers) 0.14 0.13 0.13 0.13 0.13

(0.085) (0.083) (0.085) (0.085) (0.083)Firm size, lagged 0.87∗∗∗ 0.84∗∗∗ 0.87∗∗∗ 0.87∗∗∗ 0.85∗∗∗

(0.024) (0.026) (0.024) (0.024) (0.032)Entered in prior technology regime −0.033 −0.034 −0.035 0.00075 −0.022

(0.053) (0.050) (0.051) (0.055) (0.054)De novo −0.028 0.86∗ 0.11 0.012 0.77

(0.071) (0.44) (0.11) (0.078) (0.55)De novo × firm size, lagged H1 −0.076∗∗ −0.066++

(0.035) (0.051)De novo × tenure(age) in industry H2 −0.034∗∗ −0.0047++

(0.014) (0.020)De novo × prior technology regime H3 −0.18∗∗ −0.070++

(0.081) (0.099)Constant 145 149∗ 153∗ 146 150∗

(93.0) (90.0) (91.1) (92.0) (89.3)

R-SQUARED 0.959 0.960 0.960 0.959 0.960

(Random effects model; robust standard errors clustered by firm; outcome is natural logarithm of subscribers year t; independentvariables measured at prior year end; Size coefficient less than 1.0 indicates small firms grow faster and significance for this parameteris tested for difference from 1.0; n = 502; firms = 76; random effects R-squared not bounded by 1).∗∗∗ p < 0.01, ∗∗ p < 0.05, ∗ p < 0.10.++ jointly significant at p < 0.05.

which suggests that de novo firms actually growmore quickly than diversifying firms when bothare small. Figure 2 illustrates the contingent effectsof size on growth rates for diversifying and denovo firms by graphing predicted values usingClarify (King, Tomz, and Wittenberg, 2000; Tomz,Wittenberg, and King, 2001).5 Growth rates forobserved de novo firms are represented by Xswhile growth rates for observed diversifying firmsare represented by Os. The graph shows that theexpected growth rates for de novo firms at smallsizes are larger than for diversifying firms. Thetwo growth curves cross at a log size of about12.2, indicating that diversifying firms outpace de

5 Clarify generates values of interest based on simulation ofthe estimation uncertainty of the parameter values as well asthe fundamental uncertainty from the estimated error term. Thegraph shows an expected growth rate for each observation in thesample based on the average of 1,000 simulations using Clarify.

novo firms beginning at a size of 200,000 sub-scribers(just below the fiftieth percentile of the sizedistribution).

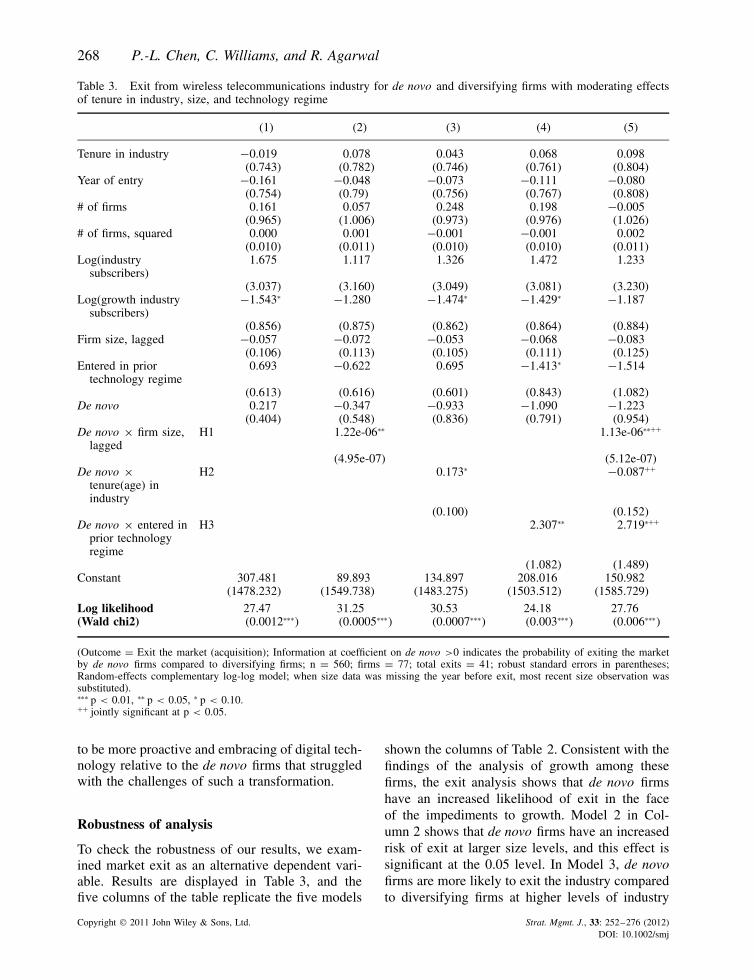

To test Hypothesis 2 (de novo firms face a largerdecrease in growth with increased industry tenureas compared to diversifying firms), we examinethe interaction effect of de novo and tenure inindustry. Consistent with Hypothesis 2, Column 3,Table 2 shows that the coefficient for this variableis −0.034, which is significant at the 0.05 level.The simple effect of de novo is not statistically sig-nificant. Figure 3 illustrates this effect by graphingthe predicted growth rate of de novo and diversi-fying firms for each observed value in the sam-ple. At low levels of tenure, de novo firms beginwith growth rates similar to diversifying firms butgradually fall lower due to the differential growthpenalty as tenure increases.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

266 P.-L. Chen, C. Williams, and R. Agarwal

Figure 2. Predicted growth for de novo and diversifyingfirms over size. (Graph based on average of 1,000 sim-ulations of Model (2) from Table 2 using clarify modulefor Stata. The lines are quadratic fitted lines based on the

simulated data)

Figure 3. Predicted growth for de novo and diversifyingfirms over industry tenure. (Graph based on average of1,000 simulations of Model (3) from Table 2 using clarifymodule for Stata. The lines are quadratic fitted lines based

on the simulated data)

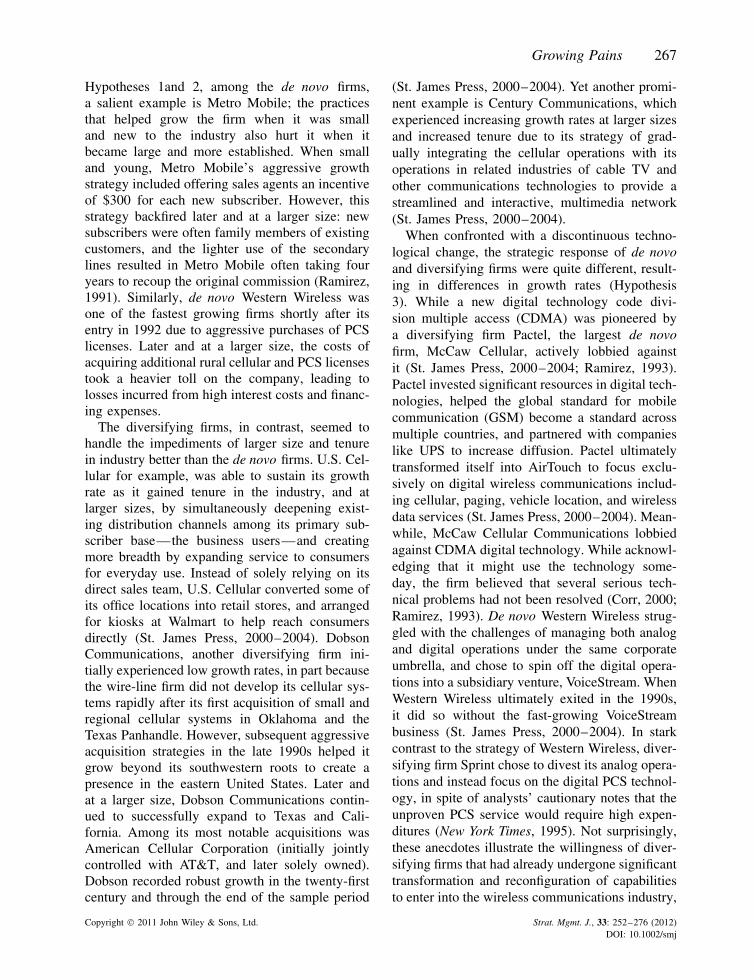

Finally, to test Hypothesis 3 (de novo firms facea higher growth penalty than diversifying firmsafter they have transitioned to a new technol-ogy regime), we examine the interaction effect ofde novo and entered in prior technology regime.Consistent with Hypothesis 3, Column 4, Table 2shows that the coefficient for this variable is−0.18, and significant at the 0.05 level. Unlike theprior interaction terms, which involved continuousvariables, this interaction is a simple shift param-eter since de novo and entered in prior technologyregime are both categorical 0/1 variables. Figure 4illustrates the lower growth that de novo firms face

Figure 4. Predicted growth for de novo and diversifyingfirms after technology regime change. (Graph based onaverage of 1,000 simulations of Model (4) from Table 2using clarify module for Stata. The lines are linear fitted

lines based on the simulated data)

after a technology regime change, relative to com-parable sized diversifying firms.

Column 5, Table 2 examines the joint effect ofthe three interaction effects. The coefficients forthe interaction effects are all negative and arejointly significant at the 0.05 level based on a Waldtest, consistent with our proposition that diversify-ing firms will face a lower penalty in the face ofimpediments. We note though, that, none of thecoefficients are individually significant in Model5 due to high multicolinearity. Thus, the analysiscannot separately identify which variable is mostimportant in constraining the growth of de novofirms, or whether some but not others are caus-ing the growth penalty. Since our focus is thedifferential response of de novo and diversifyingfirms to growth impediments, and not the differen-tial impact of specific impediments to growth, thisuncertainty is not material to our core findings.6

Corroborating qualitative evidence

Qualitative evidence from firm histories corrobo-rates the above quantitative results.7 Relating to

6 We note that our theoretical interest is in examining the interac-tion effect of pre-entry experience on the impediments to growth.Size, tenure in industry, and technological regime change repre-sent a group of variables that collectively contribute to growthimpediments. Wooldridge (2002) discusses why a joint test ofsignificance is more appropriate than examining the t statisticsfor individual significance in such a situation.7 The cases are intended as examples that illustrate and reinforcewhat the quantitative analysis already shows, and not as stand-alone unbiased evidence from rigorous qualitative methodology.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 267

Hypotheses 1and 2, among the de novo firms,a salient example is Metro Mobile; the practicesthat helped grow the firm when it was smalland new to the industry also hurt it when itbecame large and more established. When smalland young, Metro Mobile’s aggressive growthstrategy included offering sales agents an incentiveof $300 for each new subscriber. However, thisstrategy backfired later and at a larger size: newsubscribers were often family members of existingcustomers, and the lighter use of the secondarylines resulted in Metro Mobile often taking fouryears to recoup the original commission (Ramirez,1991). Similarly, de novo Western Wireless wasone of the fastest growing firms shortly after itsentry in 1992 due to aggressive purchases of PCSlicenses. Later and at a larger size, the costs ofacquiring additional rural cellular and PCS licensestook a heavier toll on the company, leading tolosses incurred from high interest costs and financ-ing expenses.

The diversifying firms, in contrast, seemed tohandle the impediments of larger size and tenurein industry better than the de novo firms. U.S. Cel-lular for example, was able to sustain its growthrate as it gained tenure in the industry, and atlarger sizes, by simultaneously deepening exist-ing distribution channels among its primary sub-scriber base—the business users—and creatingmore breadth by expanding service to consumersfor everyday use. Instead of solely relying on itsdirect sales team, U.S. Cellular converted some ofits office locations into retail stores, and arrangedfor kiosks at Walmart to help reach consumersdirectly (St. James Press, 2000–2004). DobsonCommunications, another diversifying firm ini-tially experienced low growth rates, in part becausethe wire-line firm did not develop its cellular sys-tems rapidly after its first acquisition of small andregional cellular systems in Oklahoma and theTexas Panhandle. However, subsequent aggressiveacquisition strategies in the late 1990s helped itgrow beyond its southwestern roots to create apresence in the eastern United States. Later andat a larger size, Dobson Communications contin-ued to successfully expand to Texas and Cali-fornia. Among its most notable acquisitions wasAmerican Cellular Corporation (initially jointlycontrolled with AT&T, and later solely owned).Dobson recorded robust growth in the twenty-firstcentury and through the end of the sample period

(St. James Press, 2000–2004). Yet another promi-nent example is Century Communications, whichexperienced increasing growth rates at larger sizesand increased tenure due to its strategy of grad-ually integrating the cellular operations with itsoperations in related industries of cable TV andother communications technologies to provide astreamlined and interactive, multimedia network(St. James Press, 2000–2004).

When confronted with a discontinuous techno-logical change, the strategic response of de novoand diversifying firms were quite different, result-ing in differences in growth rates (Hypothesis3). While a new digital technology code divi-sion multiple access (CDMA) was pioneered bya diversifying firm Pactel, the largest de novofirm, McCaw Cellular, actively lobbied againstit (St. James Press, 2000–2004; Ramirez, 1993).Pactel invested significant resources in digital tech-nologies, helped the global standard for mobilecommunication (GSM) become a standard acrossmultiple countries, and partnered with companieslike UPS to increase diffusion. Pactel ultimatelytransformed itself into AirTouch to focus exclu-sively on digital wireless communications includ-ing cellular, paging, vehicle location, and wirelessdata services (St. James Press, 2000–2004). Mean-while, McCaw Cellular Communications lobbiedagainst CDMA digital technology. While acknowl-edging that it might use the technology some-day, the firm believed that several serious tech-nical problems had not been resolved (Corr, 2000;Ramirez, 1993). De novo Western Wireless strug-gled with the challenges of managing both analogand digital operations under the same corporateumbrella, and chose to spin off the digital opera-tions into a subsidiary venture, VoiceStream. WhenWestern Wireless ultimately exited in the 1990s,it did so without the fast-growing VoiceStreambusiness (St. James Press, 2000–2004). In starkcontrast to the strategy of Western Wireless, diver-sifying firm Sprint chose to divest its analog opera-tions and instead focus on the digital PCS technol-ogy, in spite of analysts’ cautionary notes that theunproven PCS service would require high expen-ditures (New York Times, 1995). Not surprisingly,these anecdotes illustrate the willingness of diver-sifying firms that had already undergone significanttransformation and reconfiguration of capabilitiesto enter into the wireless communications industry,

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

268 P.-L. Chen, C. Williams, and R. Agarwal

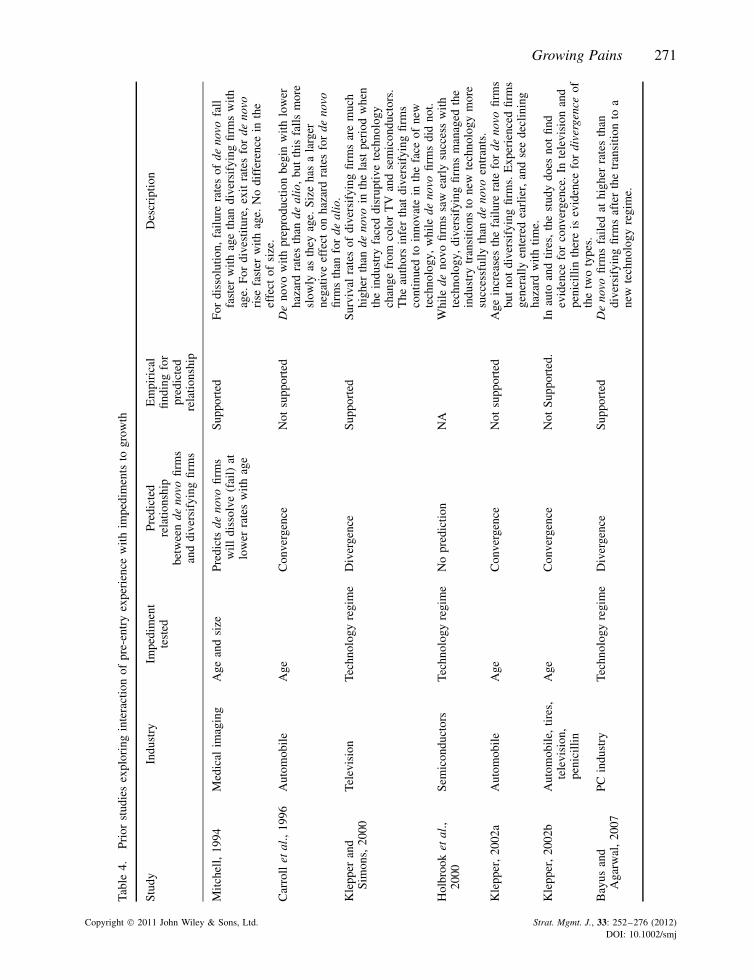

Table 3. Exit from wireless telecommunications industry for de novo and diversifying firms with moderating effectsof tenure in industry, size, and technology regime

(1) (2) (3) (4) (5)

Tenure in industry −0.019 0.078 0.043 0.068 0.098(0.743) (0.782) (0.746) (0.761) (0.804)

Year of entry −0.161 −0.048 −0.073 −0.111 −0.080(0.754) (0.79) (0.756) (0.767) (0.808)

# of firms 0.161 0.057 0.248 0.198 −0.005(0.965) (1.006) (0.973) (0.976) (1.026)

# of firms, squared 0.000 0.001 −0.001 −0.001 0.002(0.010) (0.011) (0.010) (0.010) (0.011)

Log(industrysubscribers)

1.675 1.117 1.326 1.472 1.233

(3.037) (3.160) (3.049) (3.081) (3.230)Log(growth industry

subscribers)−1.543∗ −1.280 −1.474∗ −1.429∗ −1.187

(0.856) (0.875) (0.862) (0.864) (0.884)Firm size, lagged −0.057 −0.072 −0.053 −0.068 −0.083

(0.106) (0.113) (0.105) (0.111) (0.125)Entered in prior

technology regime0.693 −0.622 0.695 −1.413∗ −1.514

(0.613) (0.616) (0.601) (0.843) (1.082)De novo 0.217 −0.347 −0.933 −1.090 −1.223

(0.404) (0.548) (0.836) (0.791) (0.954)De novo × firm size,

laggedH1 1.22e-06∗∗ 1.13e-06∗∗++

(4.95e-07) (5.12e-07)De novo ×

tenure(age) inindustry

H2 0.173∗ −0.087++

(0.100) (0.152)De novo × entered in

prior technologyregime

H3 2.307∗∗ 2.719∗++

(1.082) (1.489)Constant 307.481 89.893 134.897 208.016 150.982

(1478.232) (1549.738) (1483.275) (1503.512) (1585.729)

Log likelihood 27.47 31.25 30.53 24.18 27.76(Wald chi2) (0.0012∗∗∗) (0.0005∗∗∗) (0.0007∗∗∗) (0.003∗∗∗) (0.006∗∗∗)

(Outcome = Exit the market (acquisition); Information at coefficient on de novo >0 indicates the probability of exiting the marketby de novo firms compared to diversifying firms; n = 560; firms = 77; total exits = 41; robust standard errors in parentheses;Random-effects complementary log-log model; when size data was missing the year before exit, most recent size observation wassubstituted).∗∗∗ p < 0.01, ∗∗ p < 0.05, ∗ p < 0.10.++ jointly significant at p < 0.05.

to be more proactive and embracing of digital tech-nology relative to the de novo firms that struggledwith the challenges of such a transformation.

Robustness of analysis

To check the robustness of our results, we exam-ined market exit as an alternative dependent vari-able. Results are displayed in Table 3, and thefive columns of the table replicate the five models

shown the columns of Table 2. Consistent with thefindings of the analysis of growth among thesefirms, the exit analysis shows that de novo firmshave an increased likelihood of exit in the faceof the impediments to growth. Model 2 in Col-umn 2 shows that de novo firms have an increasedrisk of exit at larger size levels, and this effect issignificant at the 0.05 level. In Model 3, de novofirms are more likely to exit the industry comparedto diversifying firms at higher levels of industry

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

Growing Pains 269

tenure, though this effect is marginally significantat the 0.10 level. In Model 4, de novo firms are sig-nificantly more likely to exit the industry after theyhave experienced the industry shift from analog todigital technology standards. In addition, the threeeffects are jointly significant at the 0.05 level inModel 5, and the effects of size and change in tech-nology regime remain individually significant aswell. Tenure in industry appears to have a weakereffect on exit than the other two impediments,because the parameter estimate becomes negative,though nonsignificant, in the joint model. Over-all, however, the impact of impediments on exitvery closely matches the pattern of their effects ongrowth and is, if anything, more significant in theexit analysis.

We also conducted various checks to examinesensitivity of our analysis and rule out potentialalternative explanations. The following robustnessanalyses are not reported in tables due to spaceconstraints, but are available upon request fromthe authors. A significant robustness check of ourgrowth model was to estimate it using the gen-eralized method of moments (GMM) system esti-mators for panel models (Arellano, 2003; Blundelland Bond, 2000; Bond, 2002). While the approachis not without limitations,8 it is useful in regres-sions that include a lagged value of the depen-dent variable, since any firm-level heterogeneitywill bias the ordinary least squares estimate of thelagged value upward.9 The estimates of the inter-action of de novo with instrumented values for thesize variable remain negative and significant at the0.05 level. We also test the sensitivity of our resultsfor alternative values of the dummy variable forentered in a prior technological regime. It couldbe argued that when digital technology was firstintroduced in 1991, the industry did not immedi-ately switch to digital. The results are substantivelysimilar for alternative coding of the transition yearthrough 1996, which marks the new set of digital

8 This approach uses further lags of the dependent and indepen-dent variables in the regression to instrument for current values.Shortcomings of the approach include the following: The laggedinstruments have no prior theoretical justification for why theyshould be uncorrelated with the error that is presumed in therelationship between the values at t and t − 1. In addition,instrumental variable GMM estimators are known to have poorfinite-sample estimation properties with large numbers of instru-ments, as in the case of some specifications of this estimator forour model, which involved over 200 instruments.9 We note that this biases the effect of size in Table 2 toward 1,in the opposite direction of our predicted relationship, implyingthat our test is conservative.

licenses issued by the FCC for a new part of theradio spectrum.

An important alternative explanation relates tothe ‘resource-richness’ of diversifying firms.Resource advantages, particularly related to deepfinancial pockets, may cause differentials in growthand exit rates, rather than the integrative knowl-edge that helps in strategic renewal. First, wenote that resource richness should cause a uni-form growth advantage or growth advantages atsmaller levels of size and tenure in industry,rather than one that increases with these factors.Thus, our findings for the opposite effect run con-trary to resource richness being the main driver.Second, we explicitly test for whether resource-rich diversifying firms grow faster because ofinvestments made to acquire other firms and gain-ing ready-made subscribers. In robustness checks,we removed subscribers that were added throughacquisitions. The results for this analysis werealmost identical to the results reported in Table 2.Thus, we conclude that acquisitions are not the pri-mary factor in higher growth rates for diversifyingfirms in our sample.

It is also possible that the results are drivenby mode of entry choices by the diversifyingfirms coming into the market. That is, outsidefirms enter the market as a coherent organizationalentrant—thus appearing as diversifying firms inour study—when they anticipate slower initialgrowth requiring more sustaining resources fromthe parent, and they enter as a spin-out formed bydeparting executives from the related firm—thusappearing as de novo firms in our study—whenthey anticipate rapid initial growth that will notrequire resources from the parent. As a robust-ness check, we exclude six spin-out firms—denovo firms with founding executives from a relatedindustry—from the analysis and the results arenot substantively different from those reported inTable 2. As an additional check, we exclude twospin-off firms—those divested from diversifyingfirms—from the analysis and find no differencein the results. Finally, we note that our controlvariables capture much of the general effects ofindustry evolution and competition, since the num-ber of firms, industry sales, growth in sales, andyear of entry dummies are all included in the anal-ysis. Consistent with prior literature, we do findthat increased competition results in lower overallgrowth rates, but the other variables do not have amain or interaction effect on growth rates.

Copyright 2011 John Wiley & Sons, Ltd. Strat. Mgmt. J., 33: 252–276 (2012)DOI: 10.1002/smj

270 P.-L. Chen, C. Williams, and R. Agarwal

DISCUSSION AND CONCLUSIONS