Embed Size (px)

Citation preview

Accelerating Adoption of the Industrial Internet of Things !

Growing from Big to Strong !!

A Pragmatic Assessment of Challenges and Opportunities in Chinese Industrial Automation !

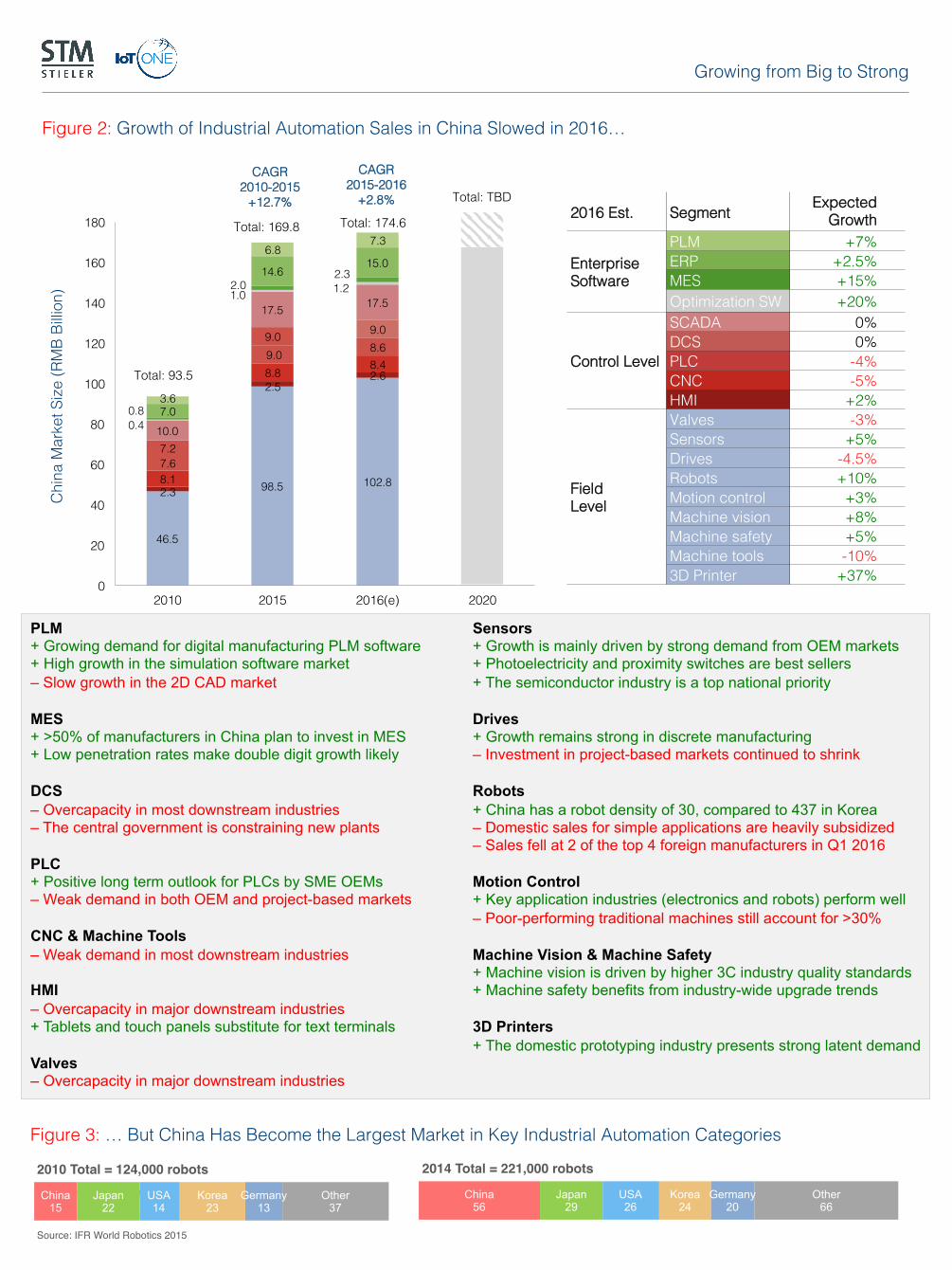

The total market for industrial IoT solutions in China grew by 82 percent between 2010 and 2015. This equates to an average compound annual growth of 12.7 percent, which compared favorability to the compound annual growth of 10.7 percent of China’s GDP. Industrial IoT in China – Where is the growth? Theoretically, the outlook for the industry should be bright. A compelling of strong, sustained growth is easy to imagine. • China is the leading manufacturing location for

more industries than any other country. Established supply chains within the country make an exodus to cheaper countries difficult.

• China’s manufacturing sector needs automation and digitization to remain competitive.

• Adoption of industrial automation technologies forms an essential parts of the government’s “Made in China 2025” and “Internet Plus” strategies and is heavily encouraged in state owned enterprises (SOEs).

• China is at an automation level from which other Asian countries automatized rapidly. Japan automated rapidly in the 1980s, followed by South Korea and Taiwan in the 1990s.

We are seeing a great divide between strong political will to upgrade industrial capabilities and a risk adverse private sector that has yet to supply the expected market demand in 2016:

• Enterprise software adoption has slowed due to

hesitant adoption by domestic companies.

• Demand for all control level segments except for Human Machine Interfaces is shrinking.

• On the field level, we are seeing slower than expected growth in most segments. Sales of valves, drives and machine tools are declining.

Growing from Big to Strong !

0! 100! 200! 300! 400! 500! 600! 700!

Manufacturing!

Public Services!

Resource Extraction!

Construction!

Retail / Wholesale!

Transportation!

Utilities!

Financial Services!

Healthcare!

Low Estimate!High Estimate!

Incremental GDP Growth ($USD Billions)!

Source: Accenture (2015)

Figure 1: Estimated Impact of the Industrial IoT on Chinese Growth, by Industry (2020)!

Will industrial policy be used to mobilize China’s private sector or entrench national champions? The Chinese miracle of the past 30 years was largely driven by tens of thousands of small and medium manufacturers. However, the first iteration of the Made in China 2025 policy released in 2015 focused on financing investment in a handful of state-owned ‘national champions’. This strategy is unlikely to be an effective growth driver as it neglects the most dynamic segment of Chinese manufacturers (SMEs). In the second half of 2015, Siemens and other providers reported an influx of orders by SOEs. Orders were often remarked to be large and urgent but poorly defined, indicating that they were made with the intent of meeting national objectives rather than well defined business needs. The Made in China 2025 policy is under review and we are hopeful that an updated version in 2016 will increase focus on the private sector. This period of review has coincided with a decline in investment, indicating that the financing of investment by SOEs is being re-assessed. Accenture provided a range of estimates for incremental GDP growth due to IoT adoption. Achieving the high estimate will likely require a refocusing of financing away from national champions and towards the dynamic private sector.

46.5!

98.5! 102.8!2.3!

2.5!2.6!

8.1!

8.8!8.4!

7.6!

9.0 ! 8.6!

7.2!

9.0! 9.0!

10.0!

17.5! 17.5!

0.4!

1.0! 1.2!

0.8!

2.0!2.3!

7.0!

14.6!15.0!

3.6!

6.8!7.3!

0!

20!

40!

60!

80!

100!

120!

140!

160!

180!

2010! 2015! 2016(e)! 2020!

Chi

na M

arke

t Siz

e (R

MB

Billio

n)!

CAGR!2010-2015!

+12.7%!

Total: 93.5!

Total: 169.8! Total: 174.6!

CAGR!2015-2016!

+2.8%! Total: TBD!2016 Est.! Segment! Expected

Growth!

Enterprise!Software!

PLM! +7%!ERP! +2.5%!MES! +15%!Optimization SW! +20%!

Control Level!

SCADA! 0%!DCS! 0%!PLC! -4%!CNC! -5%!HMI! +2%!

Field !Level!

Valves! -3%!Sensors! +5%!Drives! -4.5%!Robots! +10%!Motion control ! +3%!Machine vision! +8%!Machine safety! +5%!Machine tools! -10%!3D Printer! +37%!

Growing from Big to Strong !

Figure 2: Growth of Industrial Automation Sales in China Slowed in 2016…!

Source: STM Stieler

PLM + Growing demand for digital manufacturing PLM software + High growth in the simulation software market – Slow growth in the 2D CAD market MES + >50% of manufacturers in China plan to invest in MES + Low penetration rates make double digit growth likely DCS – Overcapacity in most downstream industries – The central government is constraining new plants PLC + Positive long term outlook for PLCs by SME OEMs – Weak demand in both OEM and project-based markets CNC & Machine Tools – Weak demand in most downstream industries HMI – Overcapacity in major downstream industries + Tablets and touch panels substitute for text terminals Valves – Overcapacity in major downstream industries

Sensors + Growth is mainly driven by strong demand from OEM markets + Photoelectricity and proximity switches are best sellers + The semiconductor industry is a top national priority Drives + Growth remains strong in discrete manufacturing – Investment in project-based markets continued to shrink Robots + China has a robot density of 30, compared to 437 in Korea – Domestic sales for simple applications are heavily subsidized – Sales fell at 2 of the top 4 foreign manufacturers in Q1 2016 Motion Control + Key application industries (electronics and robots) perform well – Poor-performing traditional machines still account for >30% Machine Vision & Machine Safety + Machine vision is driven by higher 3C industry quality standards + Machine safety benefits from industry-wide upgrade trends 3D Printers + The domestic prototyping industry presents strong latent demand

Figure 3: … But China Has Become the Largest Market in Key Industrial Automation Categories!

China 15

Japan 22

USA 14

Korea 23

Germany 13

Other 37

Source: IFR World Robotics 2015

2010 Total = 124,000 robots

China 56

Japan 29

USA 26

Korea 24

Germany 20

Other 66

2014 Total = 221,000 robots

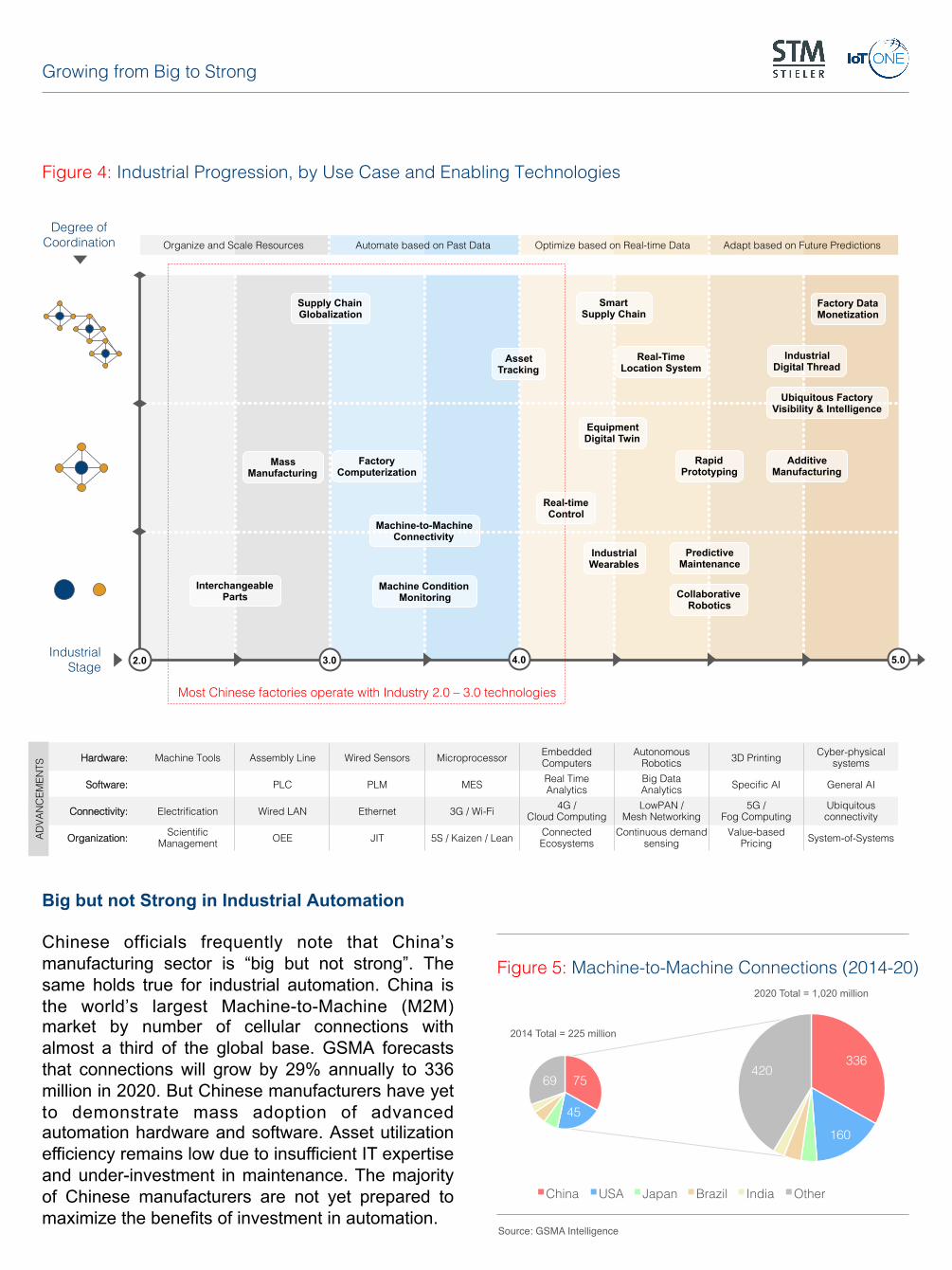

Degree of Coordination!

2.0 3.0 4.0 5.0

Organize and Scale Resources! Automate based on Past Data! Optimize based on Real-time Data! Adapt based on Future Predictions!

Industrial !Stage!

Machine Tools! Assembly Line! Wired Sensors! Microprocessor! Embedded Computers!

Autonomous Robotics! 3D Printing! Cyber-physical

systems!

PLC ! PLM ! MES! Real Time !Analytics!

Big Data !Analytics! Specific AI! General AI!

Electrification! Wired LAN! Ethernet! 3G / Wi-Fi! 4G / !Cloud Computing!

LowPAN / !Mesh Networking!

5G /!Fog Computing!

Ubiquitous connectivity !

Scientific Management ! OEE! JIT! 5S / Kaizen / Lean ! Connected

Ecosystems!Continuous demand

sensing!Value-based !

Pricing! System-of-Systems!

Hardware:!

Software:!

Connectivity: !

Organization:!ADVA

NC

EMEN

TS!

Asset Tracking

Industrial Wearables

Smart Supply Chain

Collaborative Robotics

Predictive Maintenance

Ubiquitous Factory Visibility & Intelligence

Industrial Digital Thread

Machine Condition Monitoring

Rapid Prototyping

Real-Time Location System

Machine-to-Machine Connectivity

Factory Data Monetization

Mass Manufacturing

Factory Computerization

Interchangeable Parts

Supply Chain Globalization

Equipment Digital Twin

Additive Manufacturing

Real-time Control

Most Chinese factories operate with Industry 2.0 – 3.0 technologies!

Figure 4: Industrial Progression, by Use Case and Enabling Technologies!

Growing from Big to Strong !

China! USA! Japan! Brazil! India! Other!

Big but not Strong in Industrial Automation Chinese officials frequently note that China’s manufacturing sector is “big but not strong”. The same holds true for industrial automation. China is the world’s largest Machine-to-Machine (M2M) market by number of cellular connections with almost a third of the global base. GSMA forecasts that connections will grow by 29% annually to 336 million in 2020. But Chinese manufacturers have yet to demonstrate mass adoption of advanced automation hardware and software. Asset utilization efficiency remains low due to insufficient IT expertise and under-investment in maintenance. The majority of Chinese manufacturers are not yet prepared to maximize the benefits of investment in automation.

75!

45!

69!336!

160!

420!

2014 Total = 225 million

2020 Total = 1,020 million

Figure 5: Machine-to-Machine Connections (2014-20)!

Source: GSMA Intelligence

Challenges Solutions

Lack of experience + short-term investment horizons = risk-reward imbalance

• On the supply side, there is a shortage of qualified system integrators to support the education and implementation of automation and digitization projects.

• The demand side is dominated by buyers with limited experience and short investment horizons, resulting in a sense of high right and insufficient reward.

Accept the role of system integrator and invest in the required talent and partnerships • Bosch operates as an engineering consultancy

in only one market – China. They have taken on the task of educating their sales partners and customers in order to create a market.

• Apply simple use cases that take into consideration the tight financial situation among manufacturers in China. Use cases should offer short payback periods (<2 years) that can be understood by Chinese customers.

Customers demand substantial knowledge transfer and relationship development • Potential Chinese automation customers expect

a considerable amount of intermediate support, during which they tap vendor knowledge and tie up personal resources.

• Often, buyers invite several companies into a bidding process with the intention of gaining insight, potentially without awarding a project.

Find ways to commit your Chinese clients to a joint project early. Know when to say “No” • Learn from M&A and create tiered processes –

do not progress to a further state of knowledge transfer without meeting a project milestone.

• Prioritize your proprietary know-how and share generously but selectively.

• Trust your gut and walk away when appropriate. • Attack market niches by using ‘ambassador’

customers to create trust and buy-in.

Growing from Big to Strong !

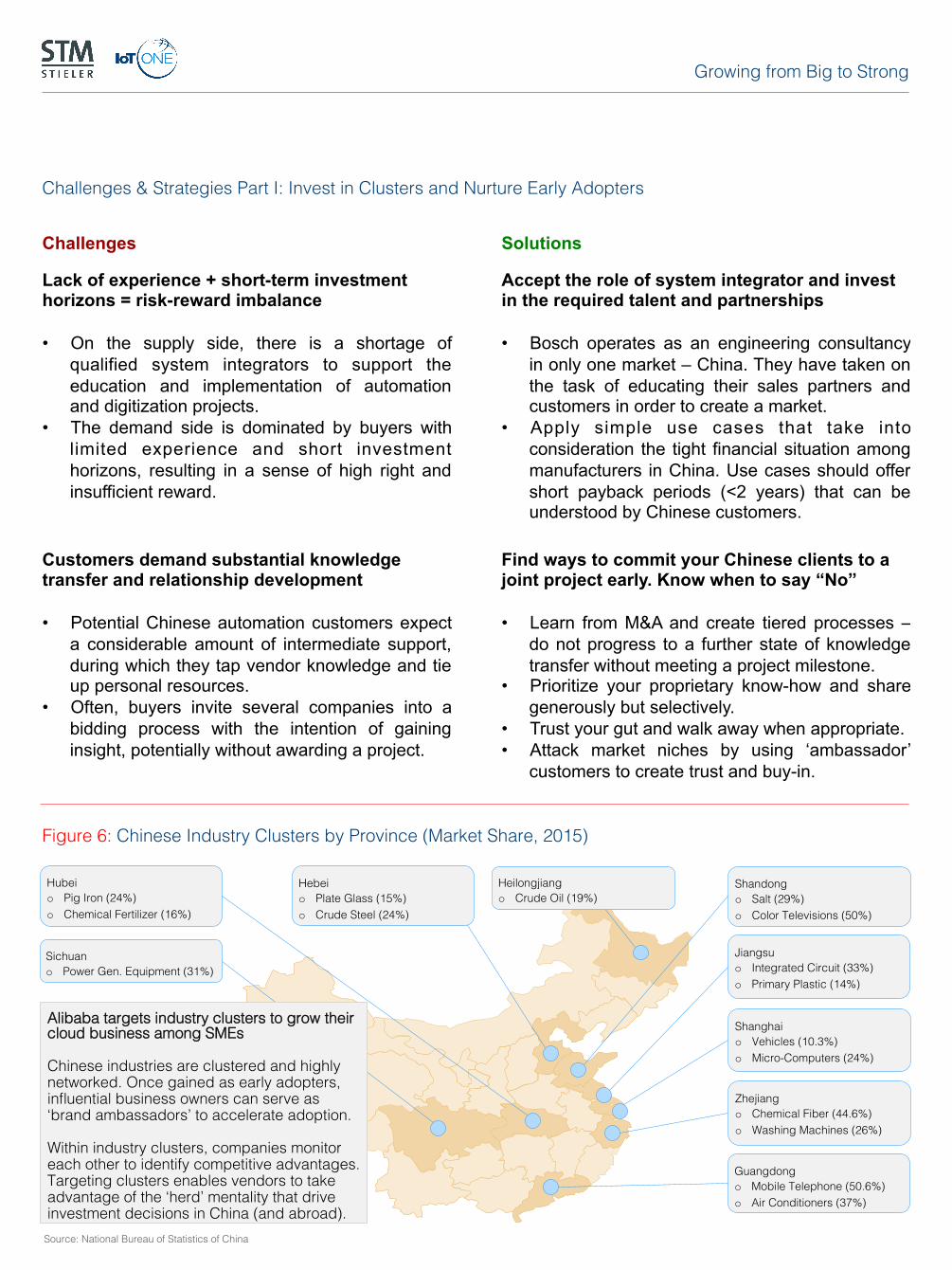

Challenges & Strategies Part I: Invest in Clusters and Nurture Early Adopters!

Zhejiang!o Chemical Fiber (44.6%)!o Washing Machines (26%)!

Shandong !o Salt (29%)!o Color Televisions (50%)!!

Shanghai !o Vehicles (10.3%)!o Micro-Computers (24%)!

Guangdong!o Mobile Telephone (50.6%)!o Air Conditioners (37%)!

Jiangsu !o Integrated Circuit (33%)!o Primary Plastic (14%)!

Hubei !o Pig Iron (24%)!o Chemical Fertilizer (16%)!

Sichuan !o Power Gen. Equipment (31%)!

Hebei !o Plate Glass (15%)!o Crude Steel (24%)!

Heilongjiang !o Crude Oil (19%)!

Alibaba targets industry clusters to grow their cloud business among SMEs!

Chinese industries are clustered and highly networked. Once gained as early adopters, influential business owners can serve as ‘brand ambassadors’ to accelerate adoption.!

Within industry clusters, companies monitor each other to identify competitive advantages. Targeting clusters enables vendors to take advantage of the ‘herd’ mentality that drive investment decisions in China (and abroad).!

Source: National Bureau of Statistics of China!

Figure 6: Chinese Industry Clusters by Province (Market Share, 2015)!

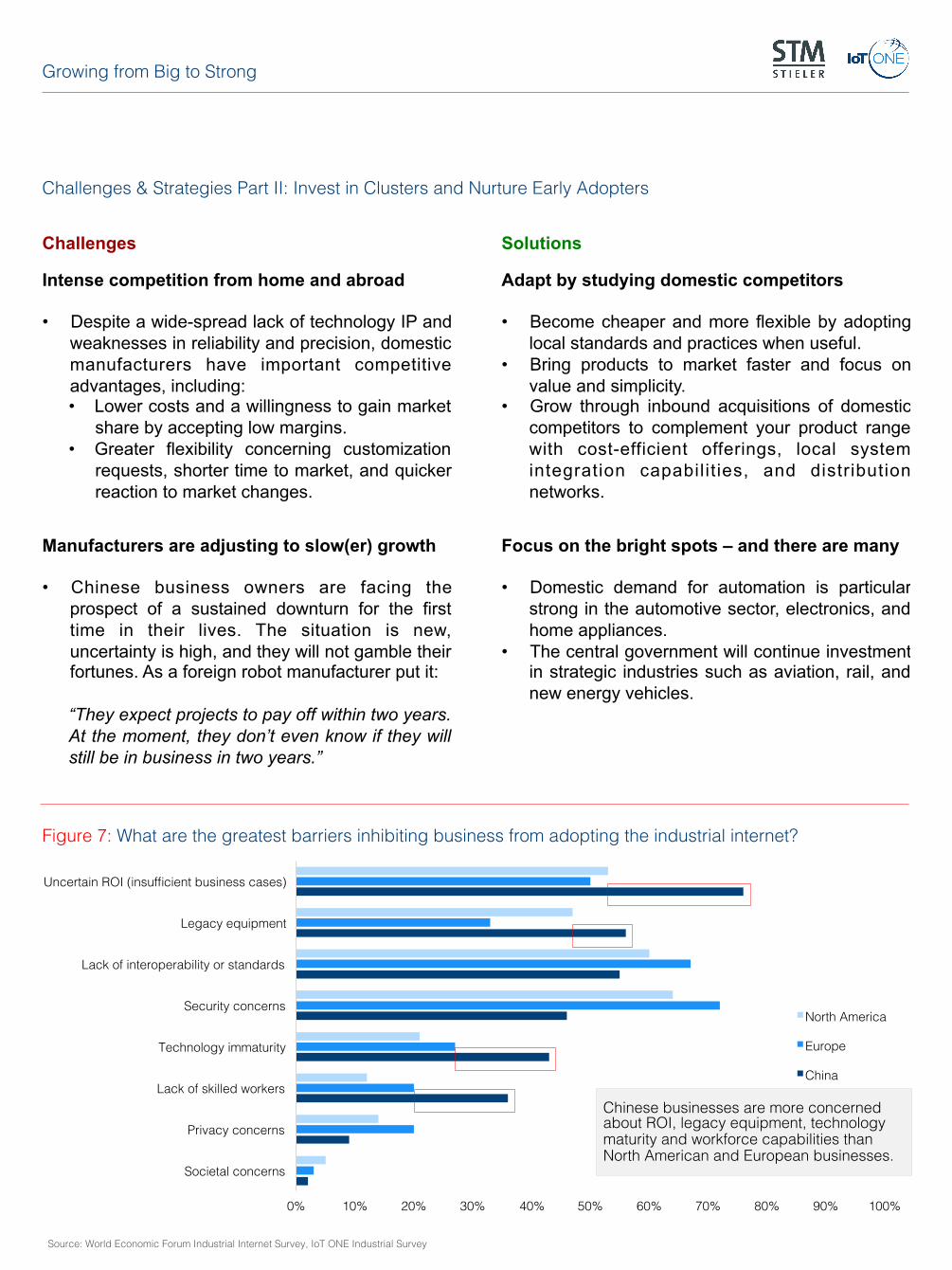

0%! 10%! 20%! 30%! 40%! 50%! 60%! 70%! 80%! 90%! 100%!

Uncertain ROI (insufficient business cases)!

Legacy equipment!

Lack of interoperability or standards!

Security concerns!

Technology immaturity!

Lack of skilled workers!

Privacy concerns!

Societal concerns!

North America!

Europe!

China!

Chinese businesses are more concerned about ROI, legacy equipment, technology maturity and workforce capabilities than North American and European businesses.!

Source: World Economic Forum Industrial Internet Survey, IoT ONE Industrial Survey!

Challenges Solutions

Intense competition from home and abroad • Despite a wide-spread lack of technology IP and

weaknesses in reliability and precision, domestic manufacturers have important competitive advantages, including: • Lower costs and a willingness to gain market

share by accepting low margins. • Greater flexibility concerning customization

requests, shorter time to market, and quicker reaction to market changes.

Adapt by studying domestic competitors • Become cheaper and more flexible by adopting

local standards and practices when useful. • Bring products to market faster and focus on

value and simplicity. • Grow through inbound acquisitions of domestic

competitors to complement your product range with cost-efficient offerings, local system integration capabilit ies, and distribution networks.

Manufacturers are adjusting to slow(er) growth • Chinese business owners are facing the

prospect of a sustained downturn for the first time in their lives. The situation is new, uncertainty is high, and they will not gamble their fortunes. As a foreign robot manufacturer put it: “They expect projects to pay off within two years. At the moment, they don’t even know if they will still be in business in two years.”

Focus on the bright spots – and there are many • Domestic demand for automation is particular

strong in the automotive sector, electronics, and home appliances.

• The central government will continue investment in strategic industries such as aviation, rail, and new energy vehicles.

Challenges & Strategies Part II: Invest in Clusters and Nurture Early Adopters!

Figure 7: What are the greatest barriers inhibiting business from adopting the industrial internet?!

Growing from Big to Strong !

Growing from Big to Strong !

Predictions for China’s Industrial Automation Market from 2016 through 2018!

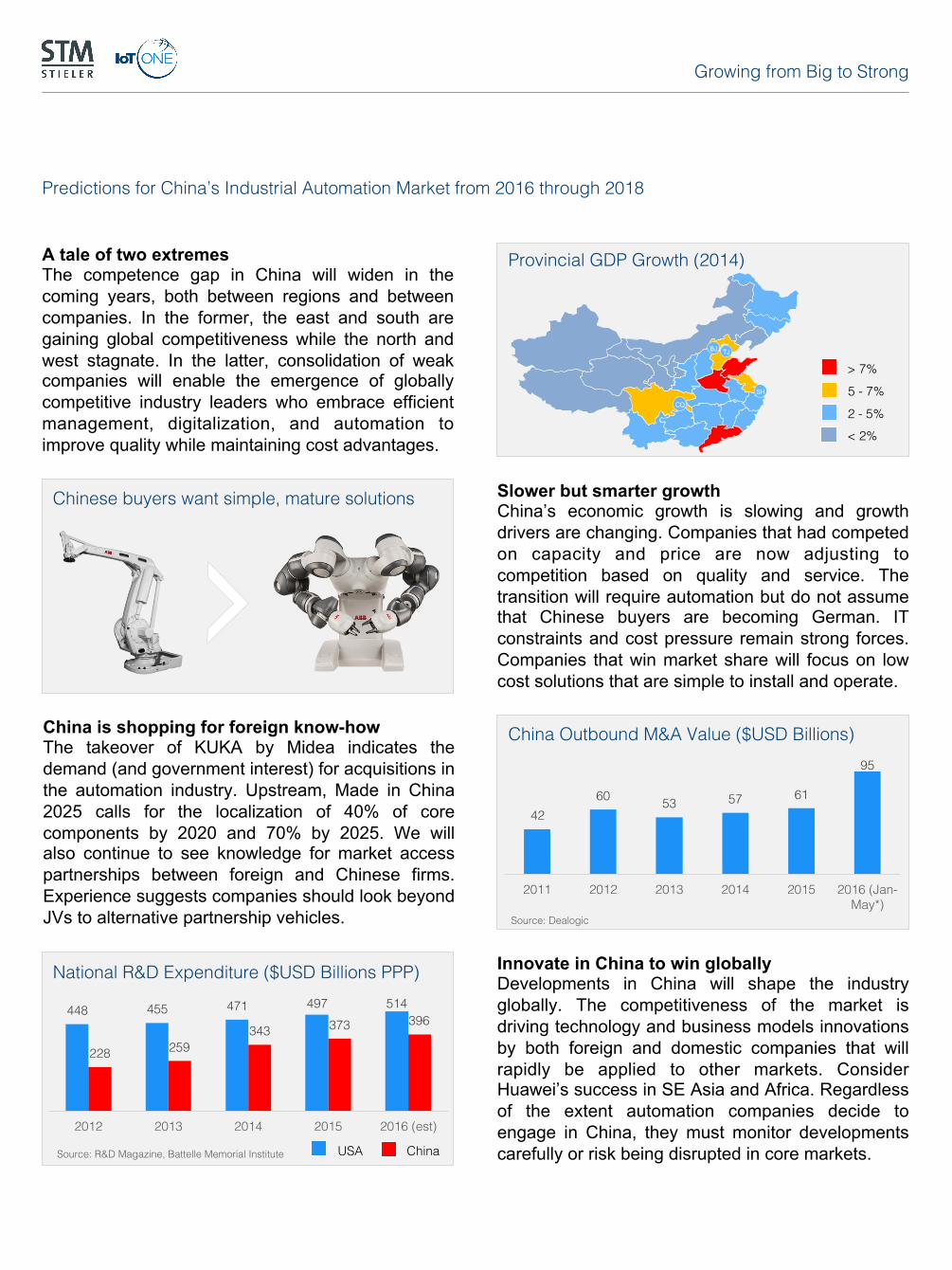

A tale of two extremes The competence gap in China will widen in the coming years, both between regions and between companies. In the former, the east and south are gaining global competitiveness while the north and west stagnate. In the latter, consolidation of weak companies will enable the emergence of globally competitive industry leaders who embrace efficient management, digitalization, and automation to improve quality while maintaining cost advantages.

Slower but smarter growth China’s economic growth is slowing and growth drivers are changing. Companies that had competed on capacity and price are now adjusting to competition based on quality and service. The transition will require automation but do not assume that Chinese buyers are becoming German. IT constraints and cost pressure remain strong forces. Companies that win market share will focus on low cost solutions that are simple to install and operate.

China is shopping for foreign know-how The takeover of KUKA by Midea indicates the demand (and government interest) for acquisitions in the automation industry. Upstream, Made in China 2025 calls for the localization of 40% of core components by 2020 and 70% by 2025. We will also continue to see knowledge for market access partnerships between foreign and Chinese firms. Experience suggests companies should look beyond JVs to alternative partnership vehicles.

Innovate in China to win globally Developments in China will shape the industry globally. The competitiveness of the market is driving technology and business models innovations by both foreign and domestic companies that will rapidly be applied to other markets. Consider Huawei’s success in SE Asia and Africa. Regardless of the extent automation companies decide to engage in China, they must monitor developments carefully or risk being disrupted in core markets.

BJ!

SH!

TJ!

CQ!

Provincial GDP Growth (2014)!

> 7%!5 - 7%!2 - 5%!< 2%!

Chinese buyers want simple, mature solutions!

42!60! 53! 57! 61!

95!

2011! 2012! 2013! 2014! 2015! 2016 (Jan-May*)!

China Outbound M&A Value ($USD Billions)!

Source: Dealogic!

448! 455! 471! 497! 514!

228! 259!343! 373! 396!

2012! 2013! 2014! 2015! 2016 (est)!

Source: R&D Magazine, Battelle Memorial Institute!

National R&D Expenditure ($USD Billions PPP)!

China!USA!

Accelerating Adoption of the Industrial Internet of Things !

Georg Stieler | !Managing Director China | !P: + 86 21 2218 3015!M (CHN): + 86 186 2167 4356!M (DE): + 49 175 207 1423 !E: [email protected]!I: www.stieler.co!

STM is a German consulting firm providing market research and business development services for technology companies. We have an extensive know-how about the following customer industries:!!• Mechanical engineering and plant

automation!• Mobile working machines!• Pharmaceuticals and medical devices!• Environmental and energy technology!

Erik Walenza-Slabe | !CEO | !P: + 86 21 6010 5058!M (CHN): + 86 156 0183 9705!!E: [email protected]!I: www.iotone.com!

IoT ONE is an information platform dedicated to mapping the Industrial IoT ecosystem. We help companies achieve transformative business results with Internet of Things technologies. !!End users and systems integrators use IoT ONE to identify new use cases, technologies, and technology providers. IoT vendors use the platform to enhance market awareness and connect with customers and partners.!!

Growing from Big to Strong !!

A Pragmatic Assessment of Challenges and Opportunities in Chinese Industrial Automation !