Embed Size (px)

Citation preview

Grafton Group plc

Investor Day

London

Thursday, 7 November 2013

Gavin Slark

Chief Executive Officer

Cautionary Statement

Certain statements made in this presentation are forward-looking statements. Such statements arebased on current expectations and are subject to a number of risks and uncertainties that couldcause actual events or results to differ materially from those expressed or implied by these forwardlooking statements. They appear in a number of places throughout this presentation and includestatements regarding the intentions, beliefs or current expectations of Directors and seniormanagement concerning, amongst other things, the results of operations, financial condition,liquidity, prospects, growth, strategies and the businesses operated by the Group. The Directorsand senior management do not undertake any obligation to update or revise any forward-lookingstatements, whether as a result of new information, future developments or otherwise.

Agenda

• Welcome and Overview

• Strategic Financial Overview

• Irish Merchanting

• Selco

• Development Strategy

• Summary

• Questions and Answers

Lunch with Management Team

Gavin Slark, Group CEO

David Arnold, Group CFO

Eddie Kelly, CEO Grafton Merchanting ROI

Chris Cunliffe, CEO Selco

Video presentation

Joe Sowton, Group Strategic Development Director

Gavin Slark

Gavin Slark, David Arnold

Executive Management Team

Peter Kearney CEO Grafton

Merchanting NI

Gavin SlarkCEO

David ArnoldGroup CFO

Charles RinnGroup Financial

Controller/ Secretary

Jonathan JenningsGroup Property

Director

Eddie Kelly CEO Grafton

Merchanting ROI

Mark Kelly CEO Grafton

Merchanting GB

Chris CunliffeChief Executive

Selco

Declan RonayneChief ExecutiveWoodie’s DIY

Jolyon InghamGroup IT Director

Joe SowtonGroup StrategicDevelopment

Director

Management Team in attendance

Steve ThompstoneManaging DirectorBuildbase

Andy WilliamsManaging DirectorPlumbase

Kate TinsleyFinance DirectorGrafton Merchanting GB

Peter KearneyChief ExecutiveGrafton Merchanting NI

Declan RonayneChief ExecutiveWoodie’s DIY

Charles RinnGroup Financial Controller / Secretary

Chris CunliffeChief ExecutiveSelco

Joe SowtonGroup Strategic

Development Director

Eddie Kelly CEO Grafton Merchanting ROI

Larry DaleChief ExecutiveEuroMix

1909 - 2013

• 1909 Established in Dublin

• 1965 PLC - Listed on Dublin Stock exchange

• 1985 Michael Chadwick appointed Executive Chairman

• 1990 Northern Ireland – Builders Merchanting

• 1994 England – Plumbers Merchanting

• 1995 England – Builders Merchanting

• 1998 British Dredging plc

• 2003 Jacksons

• 2005 Heiton Group plc

• 2006 Online retail - Plumbworld

• 2009 Belgium – Joint Venture

• 2011 Appointment of Gavin Slark as CEO

• 2013 Change of Listing Arrangements and Reporting Currency

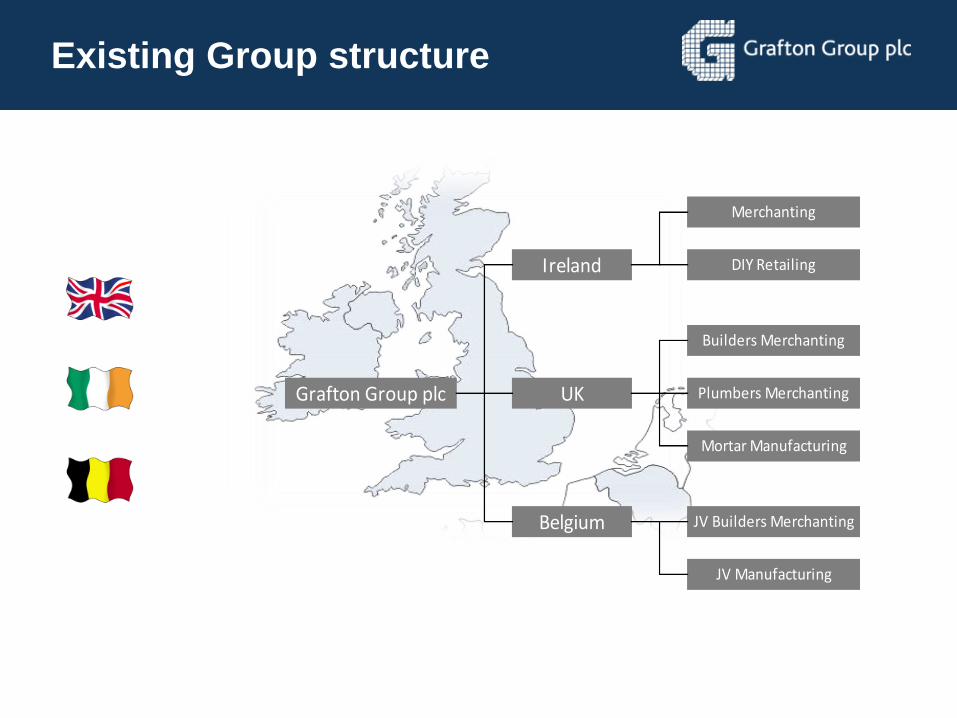

Existing Group structure

Grafton Group plc

Ireland

UK

Belgium JV Builders Merchanting

JV Manufacturing

Merchanting

DIY Retailing

Builders Merchanting

Plumbers Merchanting

Mortar Manufacturing

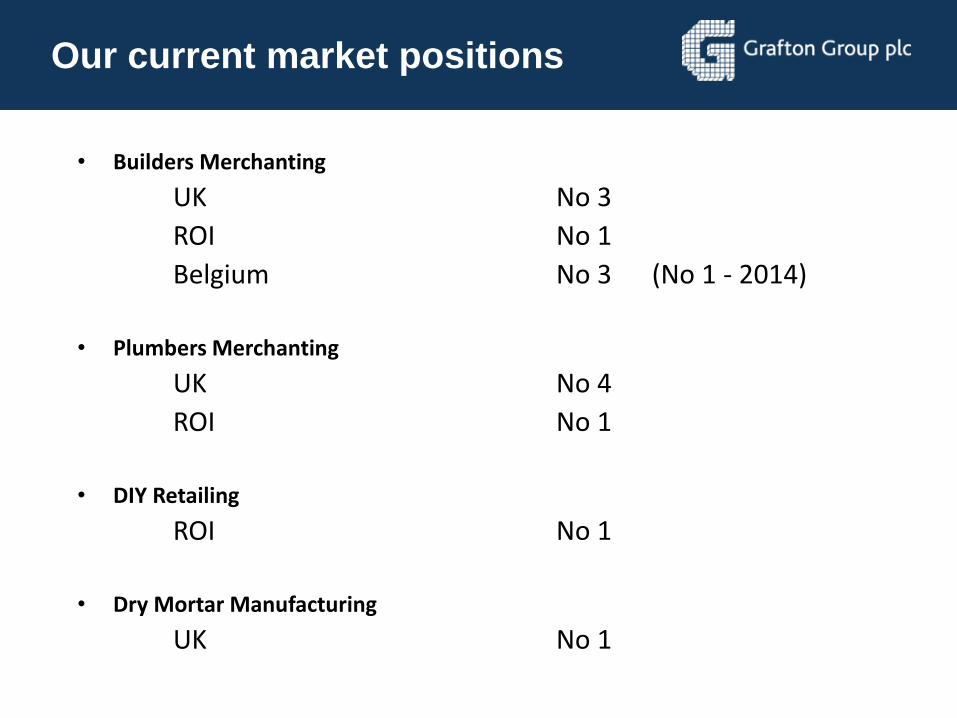

Our current market positions

• Builders Merchanting

UK No 3

ROI No 1

Belgium No 3 (No 1 - 2014)

• Plumbers Merchanting

UK No 4

ROI No 1

• DIY Retailing

ROI No 1

• Dry Mortar Manufacturing

UK No 1

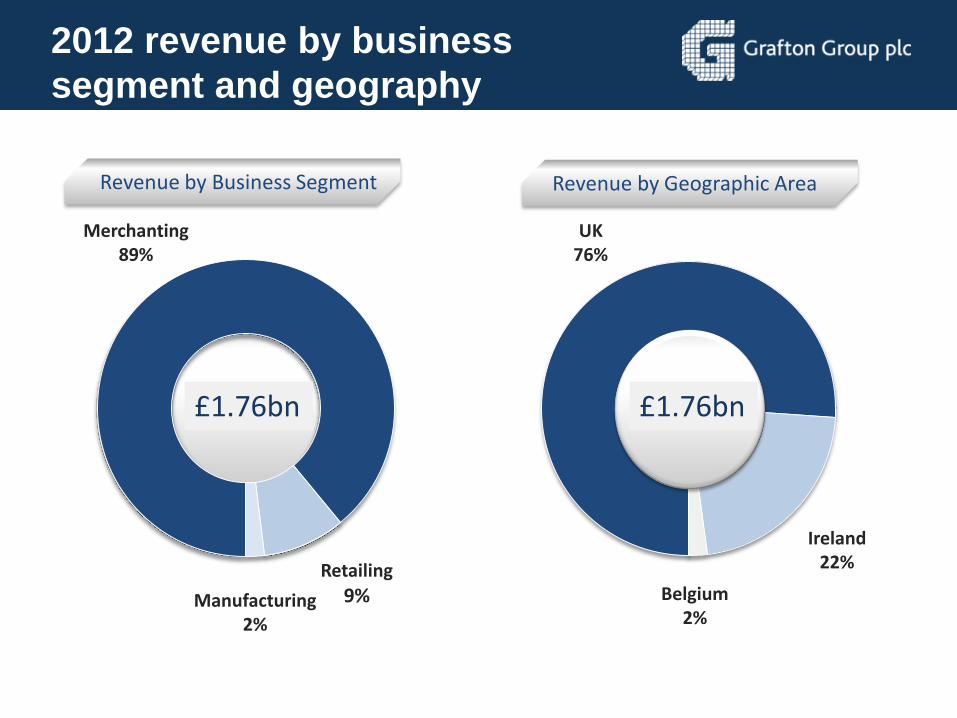

2012 revenue by business

segment and geography

Revenue by Geographic Area Revenue by Business Segment

€2.17bn €2.17bn

Manufacturing2%

Retailing

9%

UK76%

Ireland 22%

Belgium2%

Merchanting 89%

£1.76bn £1.76bn

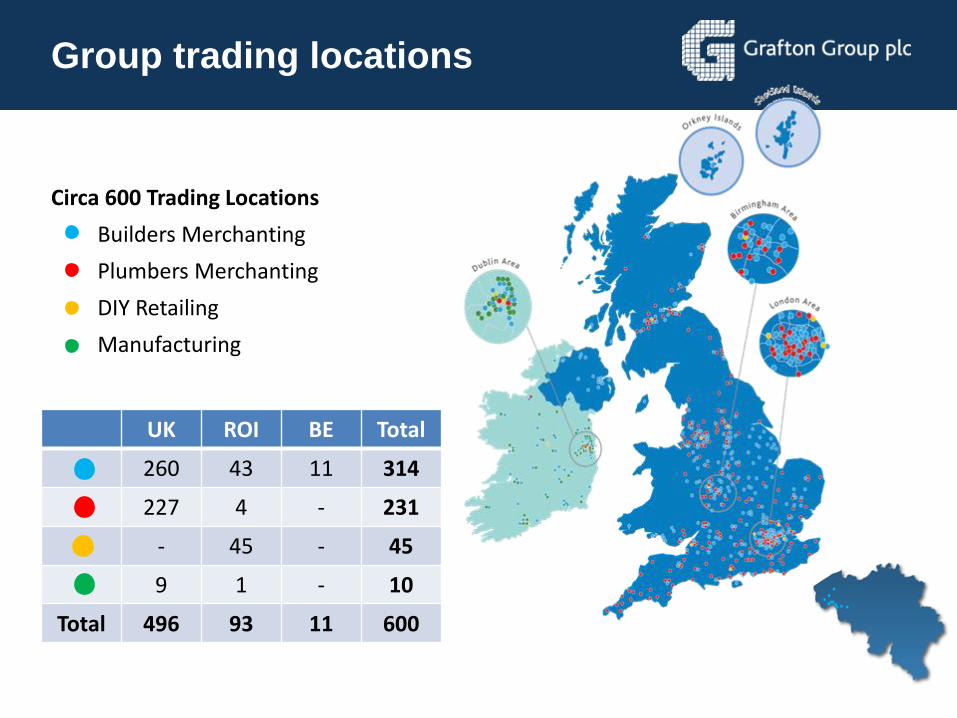

Group trading locations

UK ROI BE Total

260 43 11 314

227 4 - 231

- 45 - 45

9 1 - 10

Total 496 93 11 600

Circa 600 Trading Locations

Builders Merchanting

Plumbers Merchanting

DIY Retailing

Manufacturing

David Arnold

Chief Financial Officer

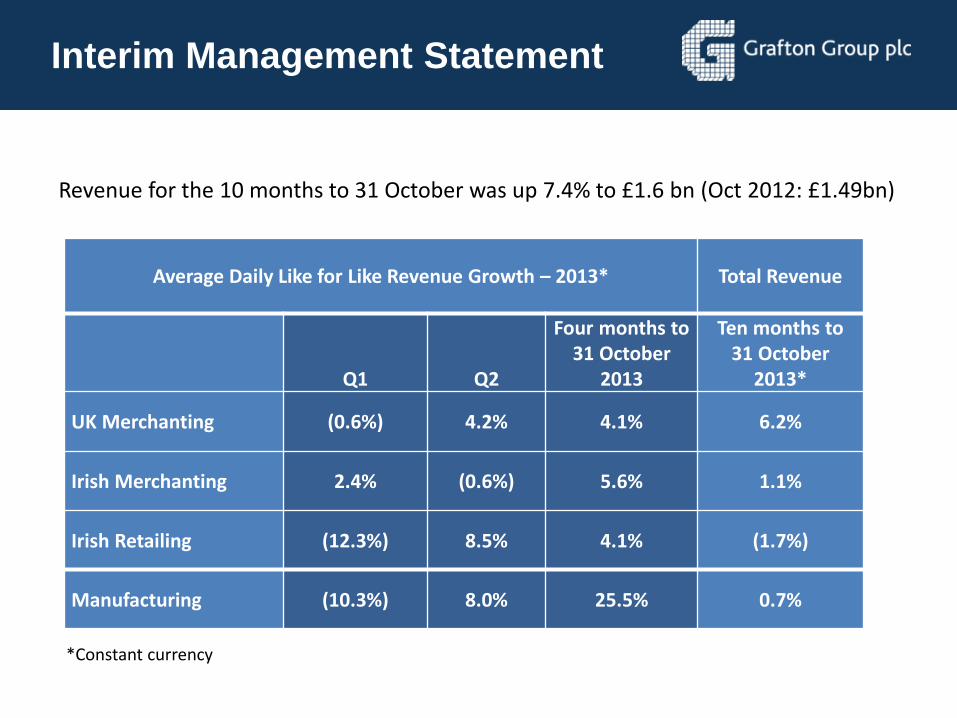

Interim Management Statement

*Constant currency

Average Daily Like for Like Revenue Growth – 2013* Total Revenue

Q1 Q2

Four months to 31 October

2013

Ten months to 31 October

2013*

UK Merchanting (0.6%) 4.2% 4.1% 6.2%

Irish Merchanting 2.4% (0.6%) 5.6% 1.1%

Irish Retailing (12.3%) 8.5% 4.1% (1.7%)

Manufacturing (10.3%) 8.0% 25.5% 0.7%

Revenue for the 10 months to 31 October was up 7.4% to £1.6 bn (Oct 2012: £1.49bn)

UK

• Housing market is benefitting from Government backed initiatives

• Confidence slowly but surely returning

• Positive, though lagged, effect on Grafton as housing transactions and household spending on RMI increases

Ireland

• Consumer confidence has improved and the Merchanting and DIY markets have stabilised at very low levels of activity

Interim Management Statement

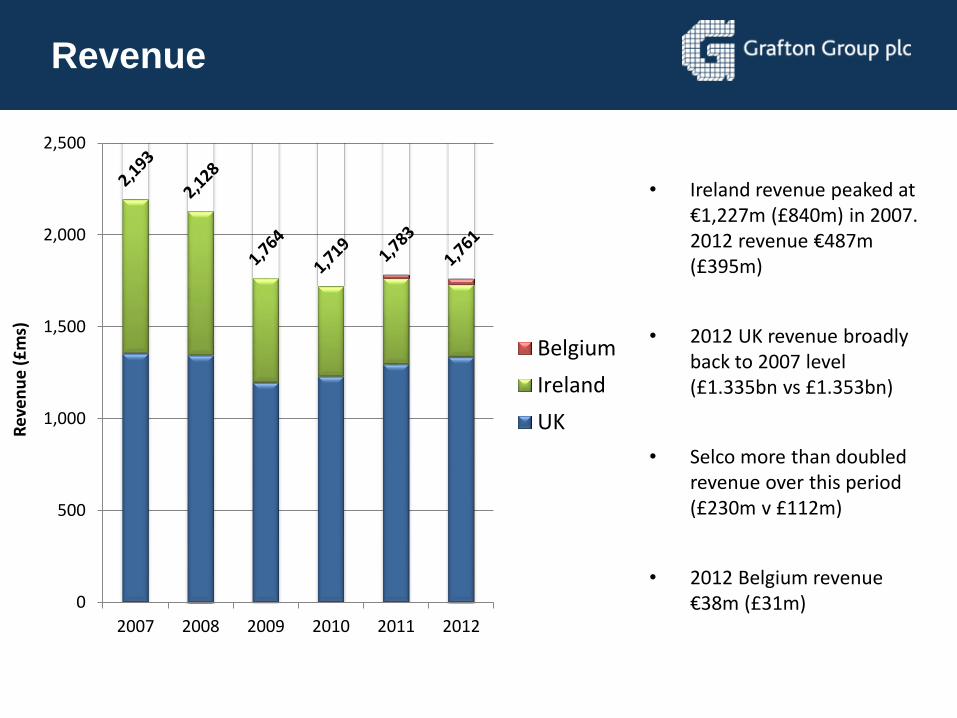

Revenue

0

500

1,000

1,500

2,000

2,500

2007 2008 2009 2010 2011 2012

Rev

en

ue

(£

ms)

Belgium

Ireland

UK

• Ireland revenue peaked at €1,227m (£840m) in 2007. 2012 revenue €487m (£395m)

• 2012 UK revenue broadly back to 2007 level (£1.335bn vs £1.353bn)

• Selco more than doubled revenue over this period (£230m v £112m)

• 2012 Belgium revenue €38m (£31m)

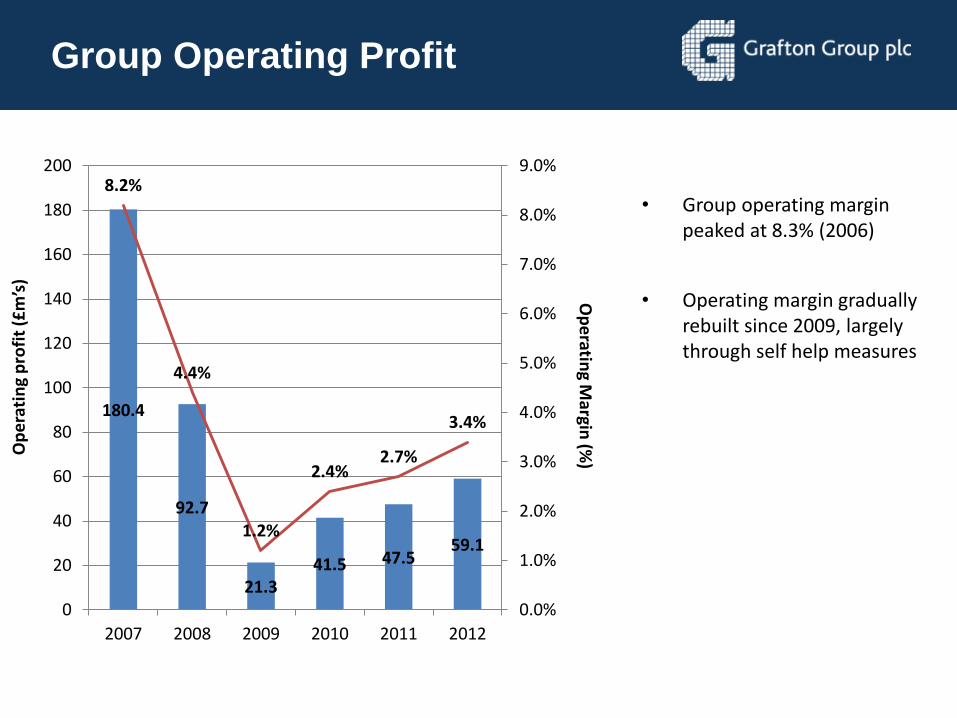

Group Operating Profit

180.4

92.7

21.341.5 47.5

59.1

8.2%

4.4%

1.2%

2.4%2.7%

3.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0

20

40

60

80

100

120

140

160

180

200

2007 2008 2009 2010 2011 2012

Op

eratin

g Margin

(%)O

pe

rati

ng

pro

fit

(£m

’s)

• Group operating margin peaked at 8.3% (2006)

• Operating margin gradually rebuilt since 2009, largely through self help measures

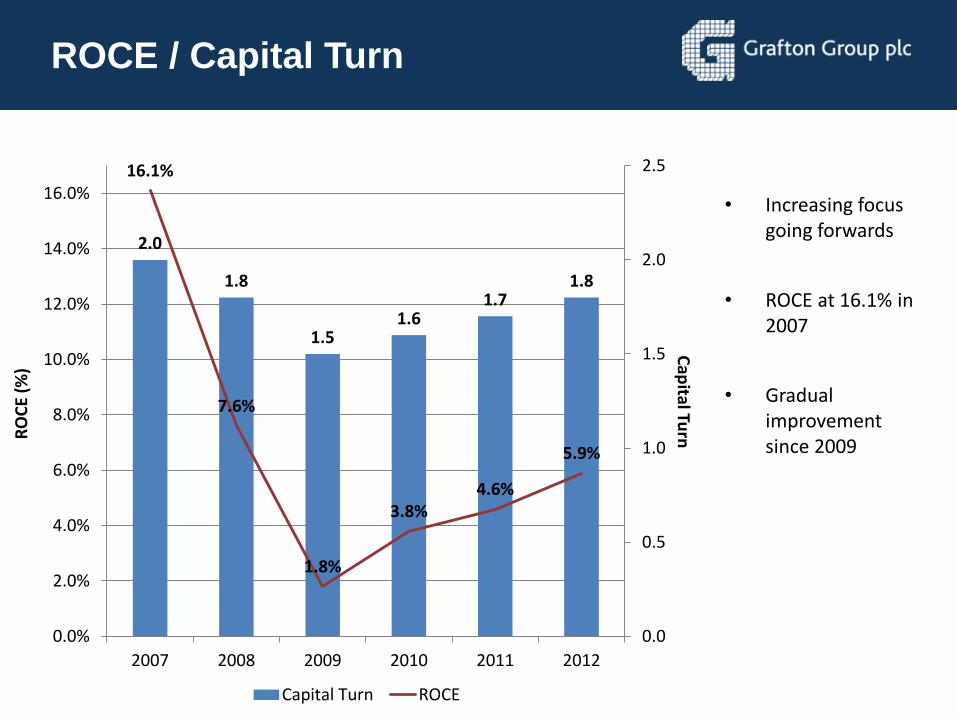

ROCE / Capital Turn

2.0

1.8

1.51.6

1.71.8

16.1%

7.6%

1.8%

3.8%4.6%

5.9%

0.0

0.5

1.0

1.5

2.0

2.5

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2007 2008 2009 2010 2011 2012

Cap

ital TurnR

OC

E (%

)

Capital Turn ROCE

• Increasing focus going forwards

• ROCE at 16.1% in 2007

• Gradual improvement since 2009

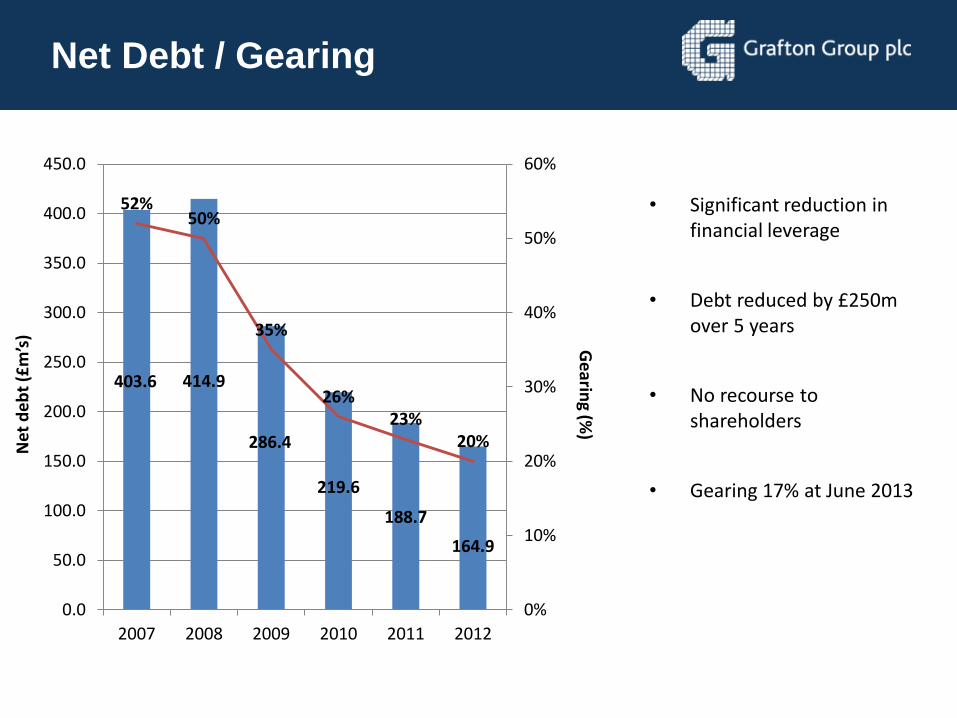

Net Debt / Gearing

403.6 414.9

286.4

219.6

188.7

164.9

52%50%

35%

26%23%

20%

0%

10%

20%

30%

40%

50%

60%

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

2007 2008 2009 2010 2011 2012

Ge

aring (%

)

Net

de

bt

(£m

’s)

• Significant reduction in financial leverage

• Debt reduced by £250m over 5 years

• No recourse to shareholders

• Gearing 17% at June 2013

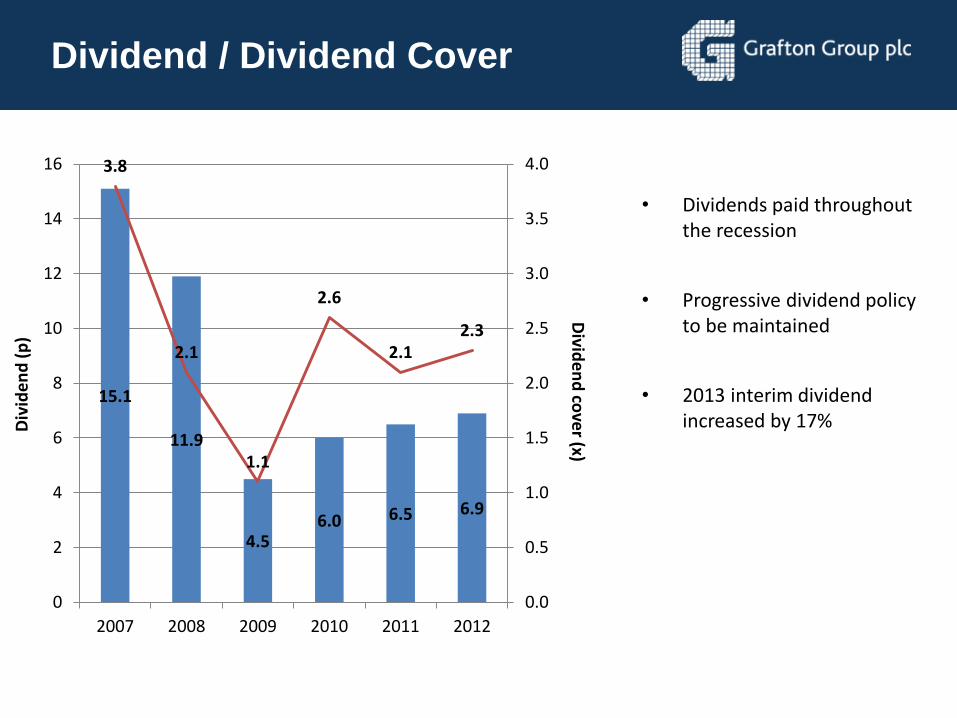

Dividend / Dividend Cover

15.1

11.9

4.56.0 6.5 6.9

3.8

2.1

1.1

2.6

2.12.3

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0

2

4

6

8

10

12

14

16

2007 2008 2009 2010 2011 2012

Divid

en

d co

ver (x)

Div

ide

nd

(p

)

• Dividends paid throughout the recession

• Progressive dividend policy to be maintained

• 2013 interim dividend increased by 17%

Strategic Pillars

Economic Growth

Organic Growth

RevenueOperating

MarginCapital

Turn

Grafton’s Strategic Pillars

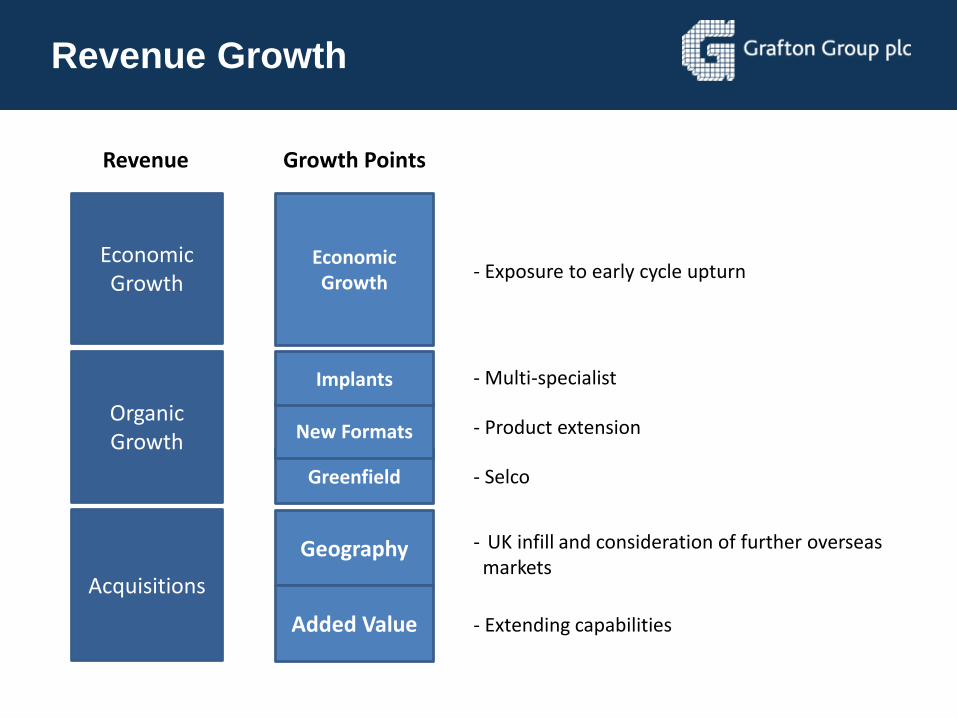

Revenue Growth

Economic Growth

Organic Growth

Acquisitions

Revenue

Greenfield

New Formats

Implants

Geography

Added Value

- Exposure to early cycle upturn

- Multi-specialist

- Product extension

- Selco

- UK infill and consideration of further overseas markets

- Extending capabilities

EconomicGrowth

Growth Points

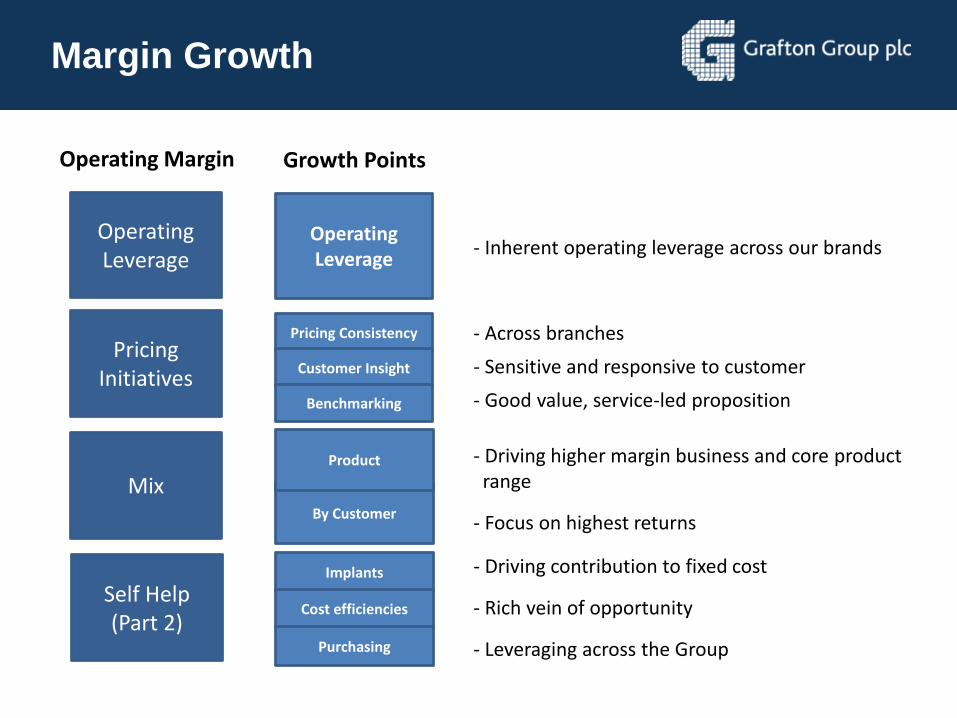

Margin Growth

Operating Leverage

Operating Margin

Pricing Initiatives

Mix

Self Help (Part 2)

Pricing Consistency

Customer Insight

Benchmarking

By Customer

Product

Implants

Cost efficiencies

Purchasing

- Across branches

- Sensitive and responsive to customer

- Good value, service-led proposition

- Driving higher margin business and core product range

- Focus on highest returns

- Driving contribution to fixed cost

- Rich vein of opportunity

- Leveraging across the Group

OperatingLeverage

Growth Points

- Inherent operating leverage across our brands

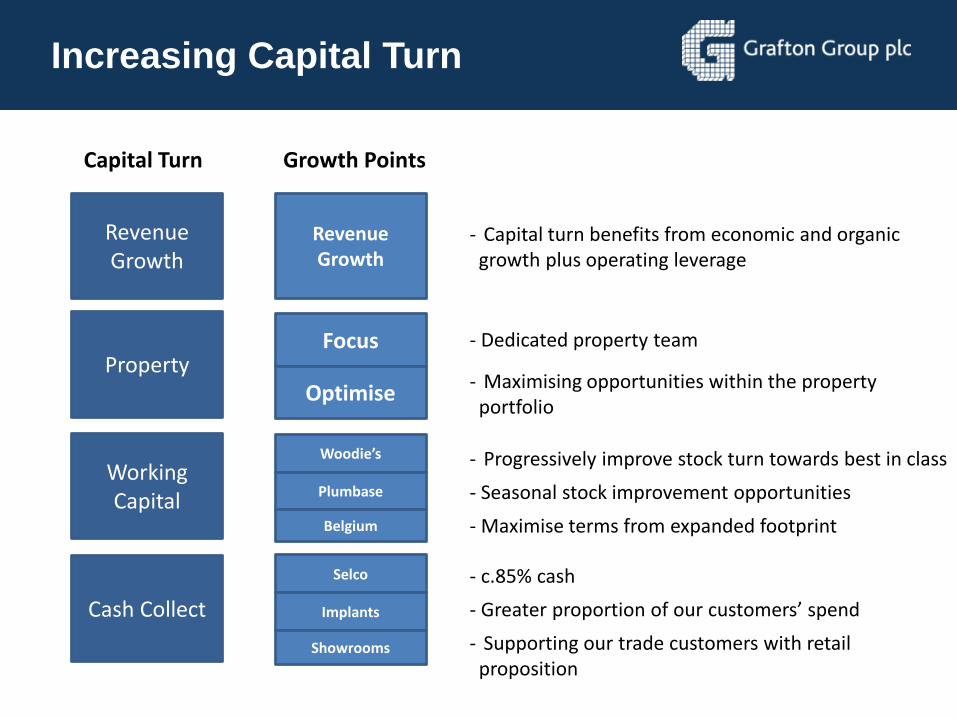

Increasing Capital Turn

Capital Turn

Revenue Growth

Property

Working Capital

Cash Collect

Focus

Optimise

Woodie’s

Plumbase

Belgium

Selco

Implants

Showrooms

- Capital turn benefits from economic and organic growth plus operating leverage

- Dedicated property team

- Maximising opportunities within the property portfolio

- Progressively improve stock turn towards best in class

- Seasonal stock improvement opportunities

- Maximise terms from expanded footprint

- c.85% cash

- Greater proportion of our customers’ spend

- Supporting our trade customers with retail proposition

RevenueGrowth

Growth Points

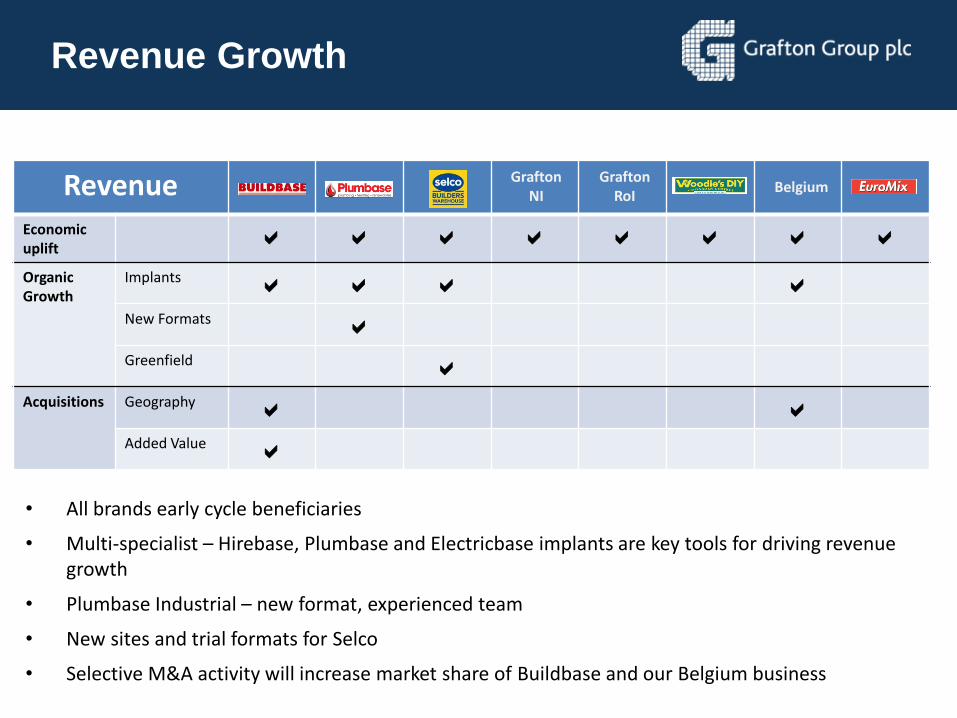

Revenue Growth

RevenueEconomic uplift

a a a a a a a a

Organic Growth

Implants a a a aNew Formats aGreenfield a

Acquisitions Geography a aAdded Value a

Grafton NI

Grafton RoI

Belgium

• All brands early cycle beneficiaries

• Multi-specialist – Hirebase, Plumbase and Electricbase implants are key tools for driving revenue growth

• Plumbase Industrial – new format, experienced team

• New sites and trial formats for Selco

• Selective M&A activity will increase market share of Buildbase and our Belgium business

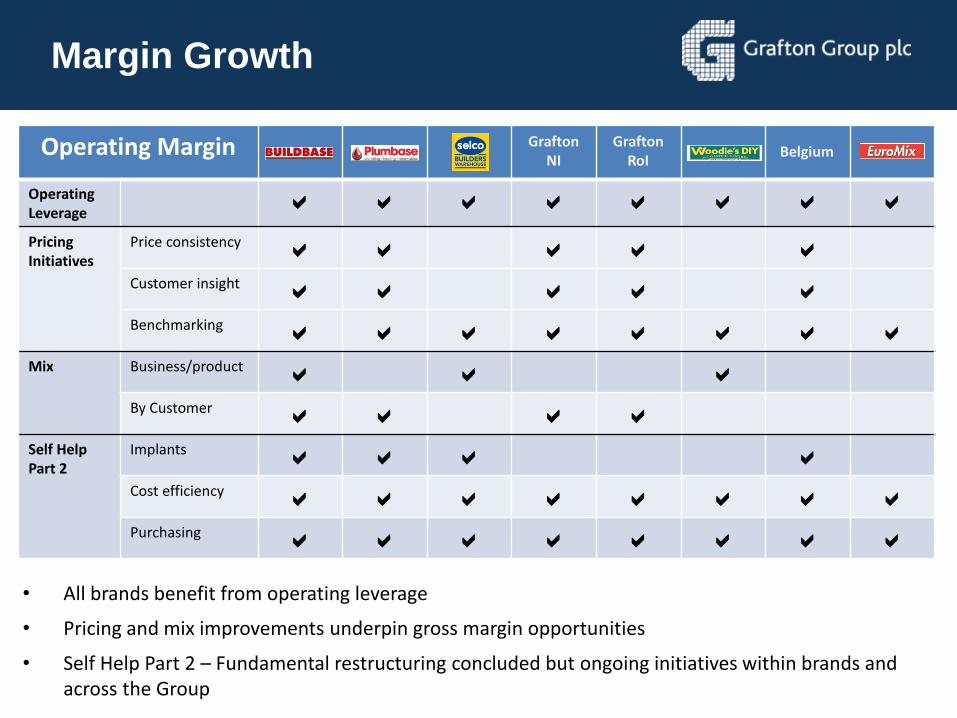

Margin Growth

Operating Margin

Operating Leverage

a a a a a a a a

Pricing Initiatives

Price consistency a a a a aCustomer insight a a a a aBenchmarking a a a a a a a a

Mix Business/product a a aBy Customer a a a a

Self Help Part 2

Implants a a a aCost efficiency a a a a a a a aPurchasing a a a a a a a a

Grafton NI

Grafton RoI

Belgium

• All brands benefit from operating leverage

• Pricing and mix improvements underpin gross margin opportunities

• Self Help Part 2 – Fundamental restructuring concluded but ongoing initiatives within brands and across the Group

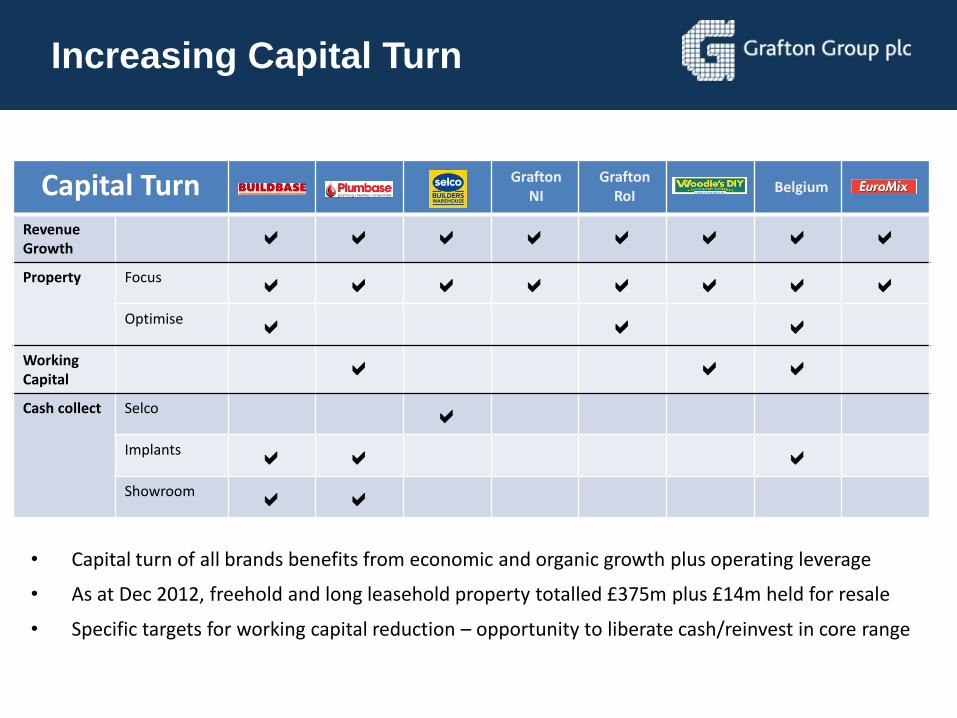

Increasing Capital Turn

Capital TurnRevenue Growth

a a a a a a a a

Property Focus a a a a a a a aOptimise a a a

Working Capital

a a a

Cash collect Selco aImplants a a aShowroom a a

Grafton NI

Grafton RoI

Belgium

• Capital turn of all brands benefits from economic and organic growth plus operating leverage

• As at Dec 2012, freehold and long leasehold property totalled £375m plus £14m held for resale

• Specific targets for working capital reduction – opportunity to liberate cash/reinvest in core range

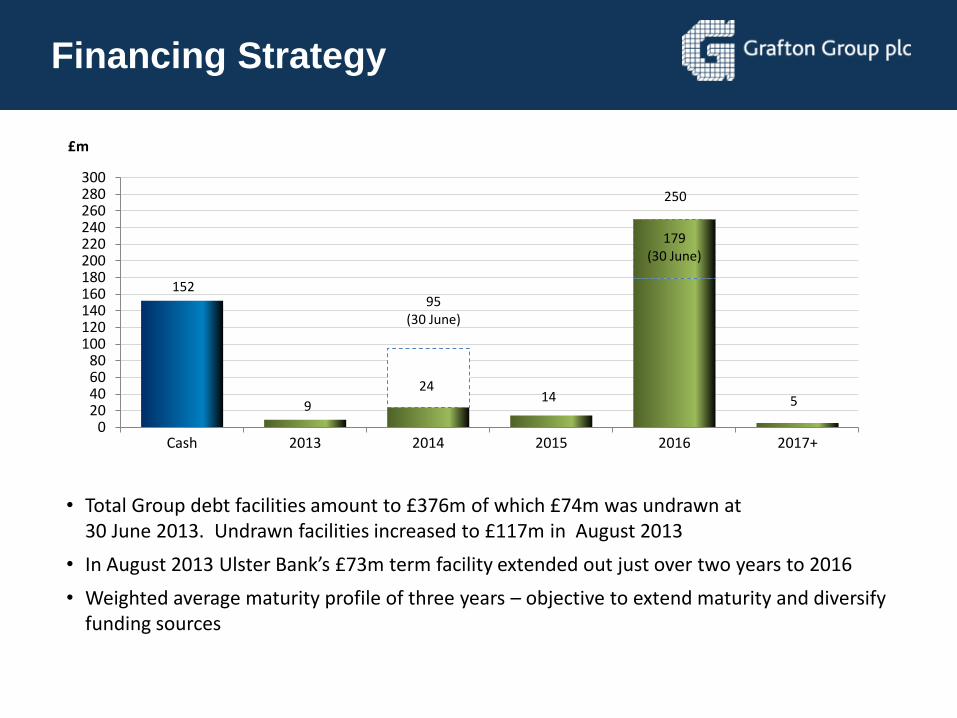

Financing Strategy

15295

(30 June)

9

24

179(30 June)

250

020406080

100120140160180200220240260280300

Cash 2013 2014 2015 2016 2017+

£m

14 5

• Total Group debt facilities amount to £376m of which £74m was undrawn at 30 June 2013. Undrawn facilities increased to £117m in August 2013

• In August 2013 Ulster Bank’s £73m term facility extended out just over two years to 2016

• Weighted average maturity profile of three years – objective to extend maturity and diversify funding sources

Eddie Kelly

CEO

Grafton Merchanting, RoI

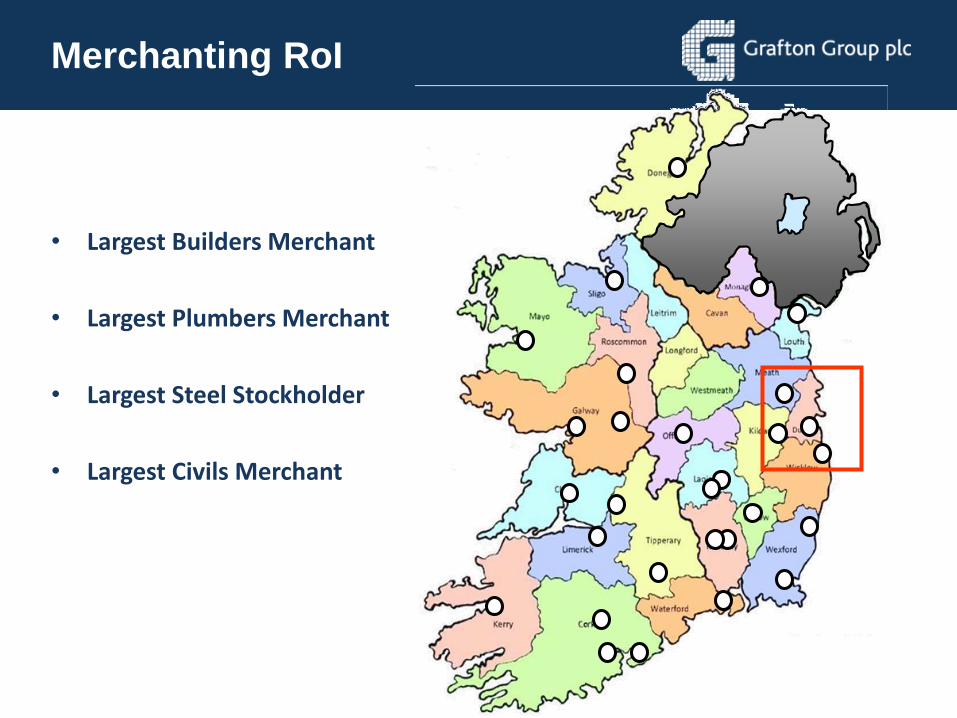

Merchanting RoI

• Largest Builders Merchant

• Largest Plumbers Merchant

• Largest Steel Stockholder

• Largest Civils Merchant

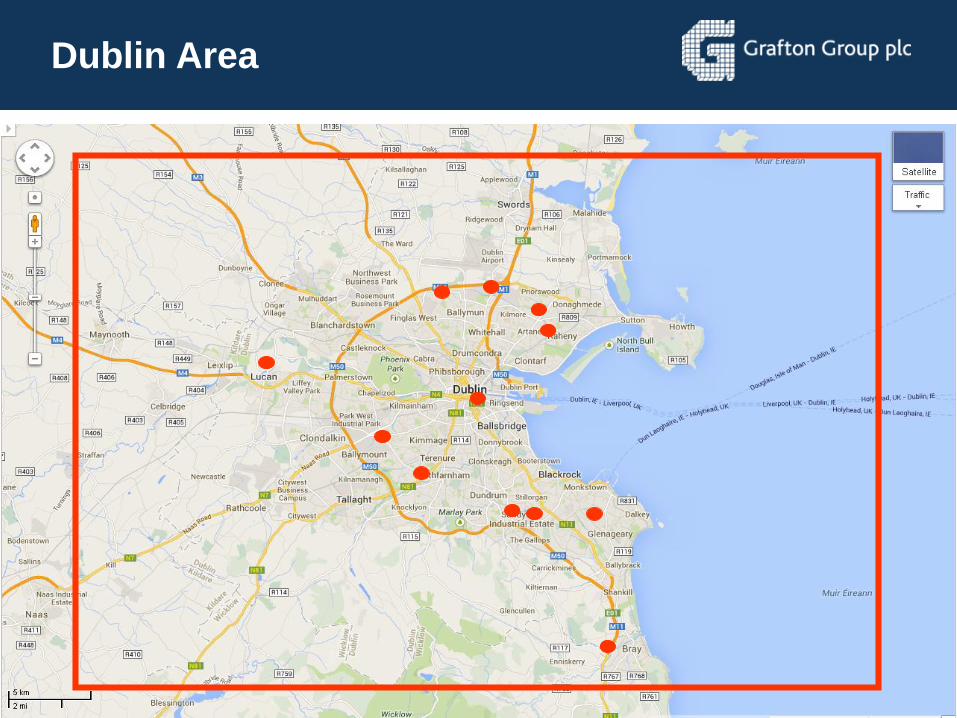

Dublin Area

Chadwicks Clonmel

Chadwicks Naas

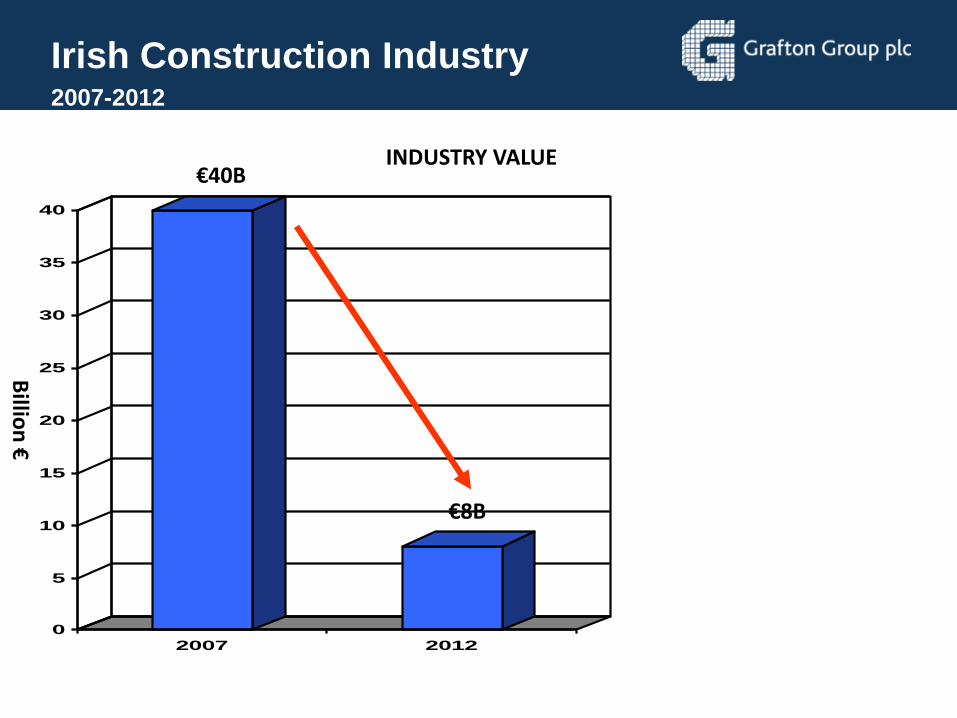

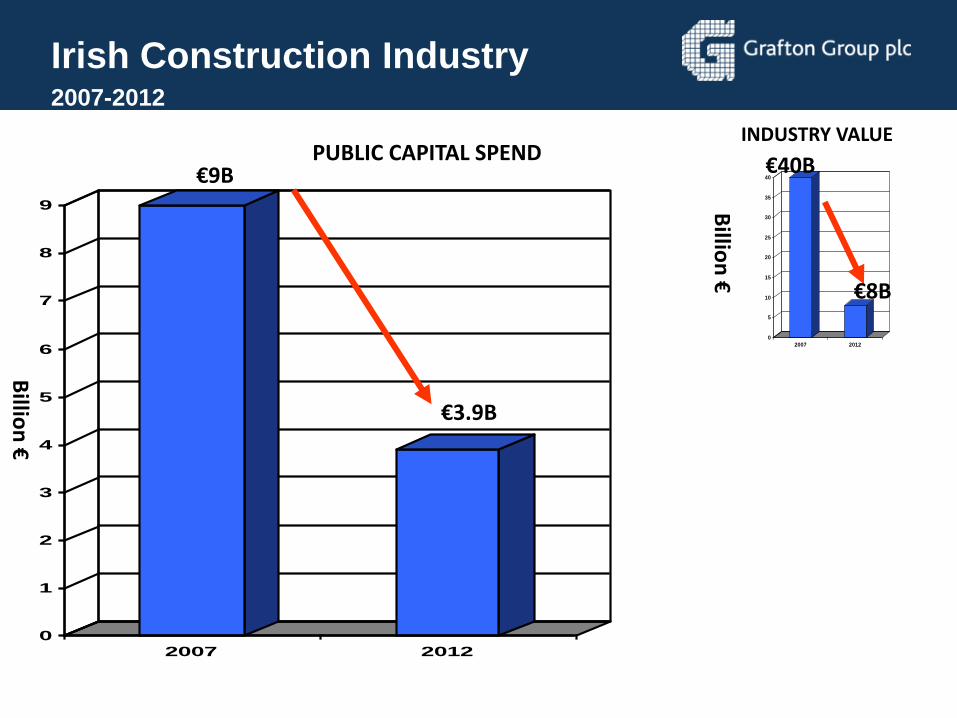

Irish Construction Industry2007-2012

0

5

10

15

20

25

30

35

40

2007 2012

Billio

n €

INDUSTRY VALUE€40B

€8B

Irish Construction Industry2007-2012

INDUSTRY VALUE

0

5

10

15

20

25

30

35

40

2007 2012

Billio

n €

€40B

€8B

0

1

2

3

4

5

6

7

8

9

2007 2012

Billio

n €

PUBLIC CAPITAL SPEND€9B

€3.9B

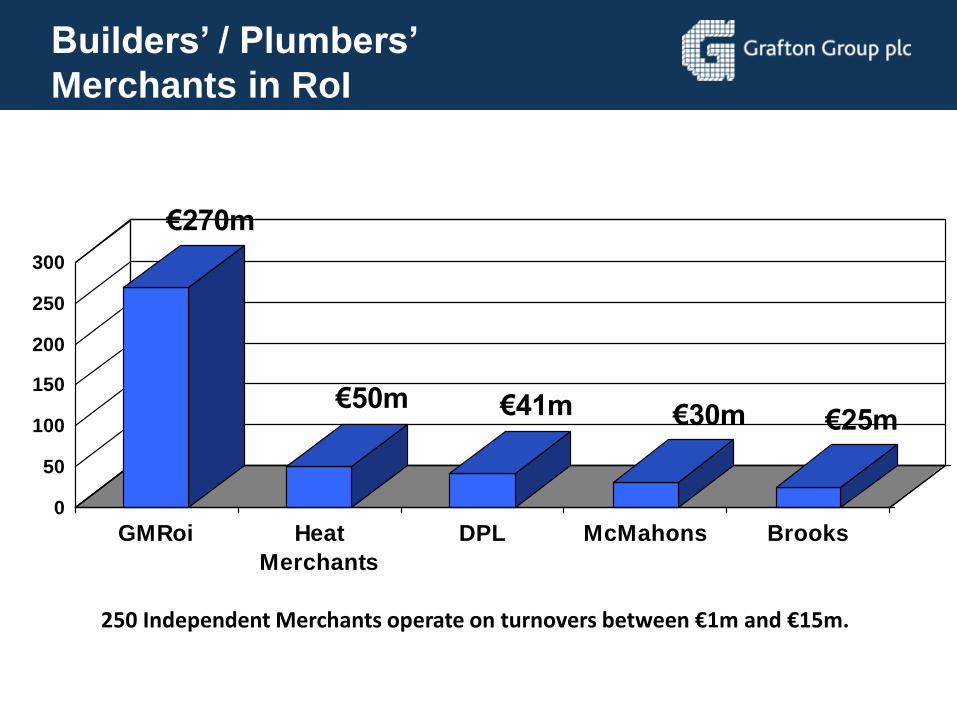

Builders’ / Plumbers’

Merchants in RoI

€270m

€25m€30m€41m€50m

0

50

100

150

200

250

300

GMRoi Heat

Merchants

DPL McMahons Brooks

250 Independent Merchants operate on turnovers between €1m and €15m.

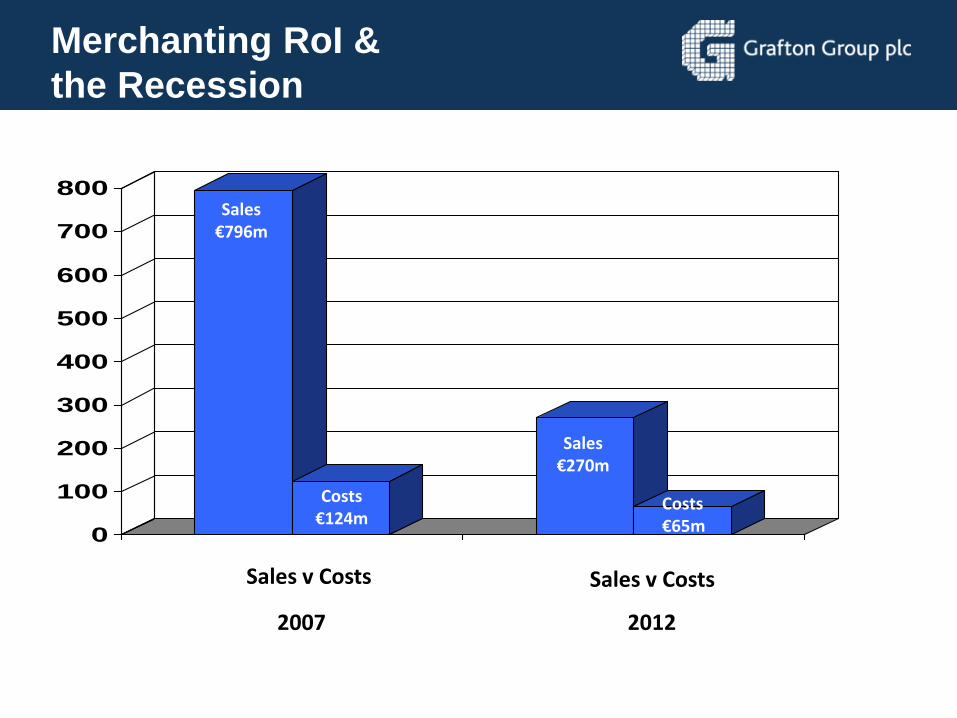

Merchanting RoI &

the Recession

2007 2012

0

100

200

300

400

500

600

700

800Sales

€796m

Sales€270m

Costs€124m

Costs€65m

Sales v Costs Sales v Costs

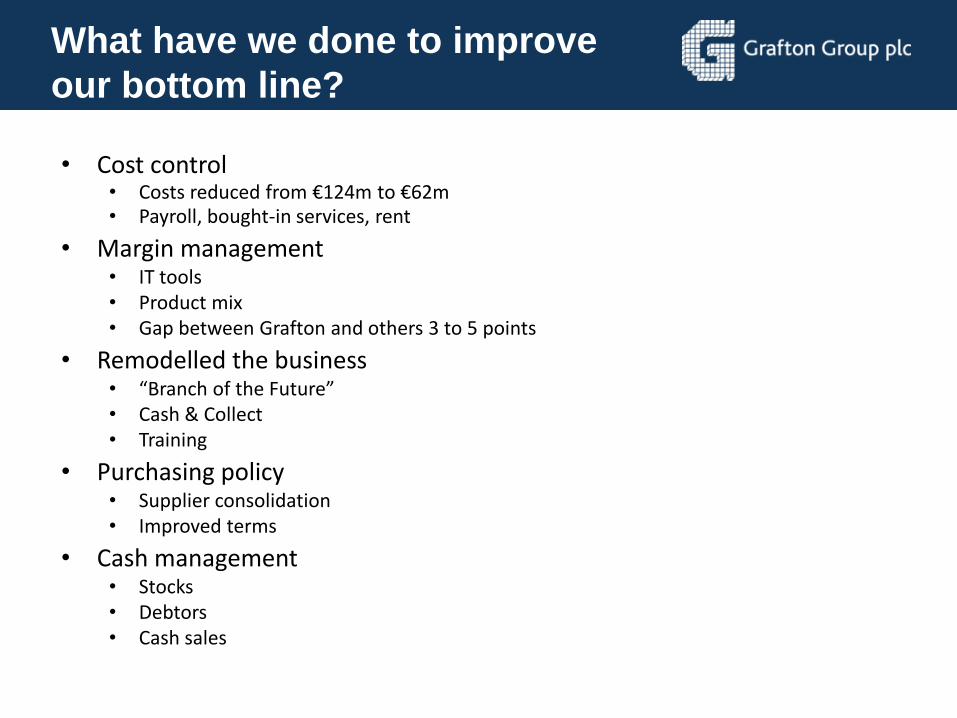

What have we done to improve

our bottom line?

• Cost control• Costs reduced from €124m to €62m• Payroll, bought-in services, rent

• Margin management• IT tools• Product mix• Gap between Grafton and others 3 to 5 points

• Remodelled the business• “Branch of the Future”• Cash & Collect• Training

• Purchasing policy• Supplier consolidation• Improved terms

• Cash management• Stocks• Debtors• Cash sales

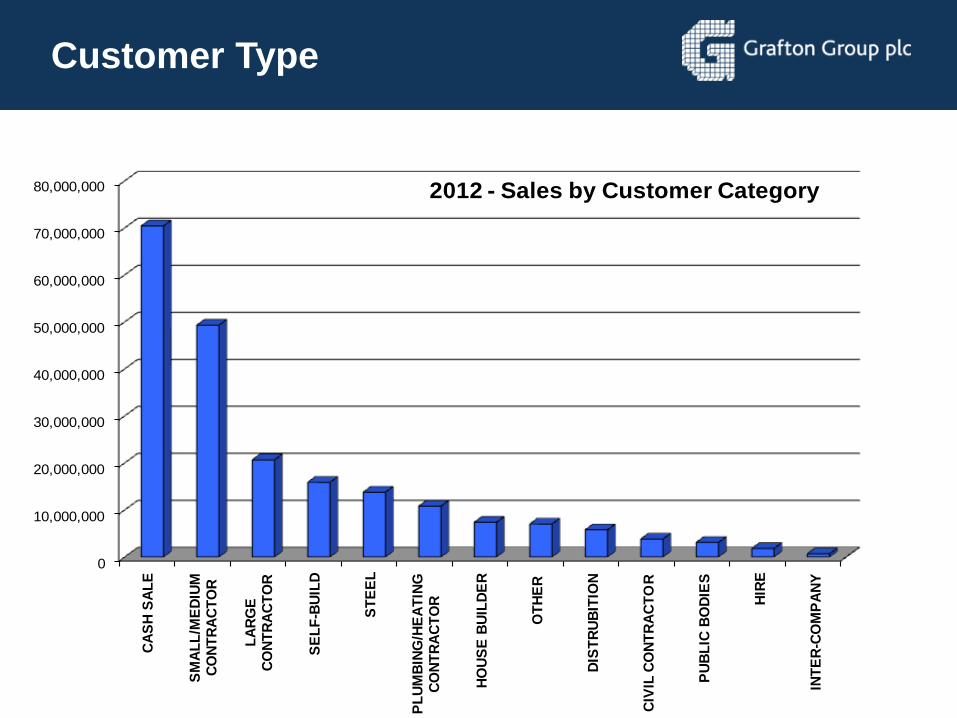

Customer Type

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

CA

SH

SA

LE

SM

AL

L/M

ED

IUM

C

ON

TR

AC

TO

R

LA

RG

E

CO

NT

RA

CT

OR

SE

LF

-BU

ILD

ST

EE

L

PL

UM

BIN

G/H

EA

TIN

G

CO

NT

RA

CT

OR

HO

US

E B

UIL

DE

R

OT

HE

R

DIS

TR

UB

ITIO

N

CIV

IL C

ON

TR

AC

TO

R

PU

BL

IC B

OD

IES

HIR

E

INT

ER

-CO

MP

AN

Y

2012 - Sales by Customer Category

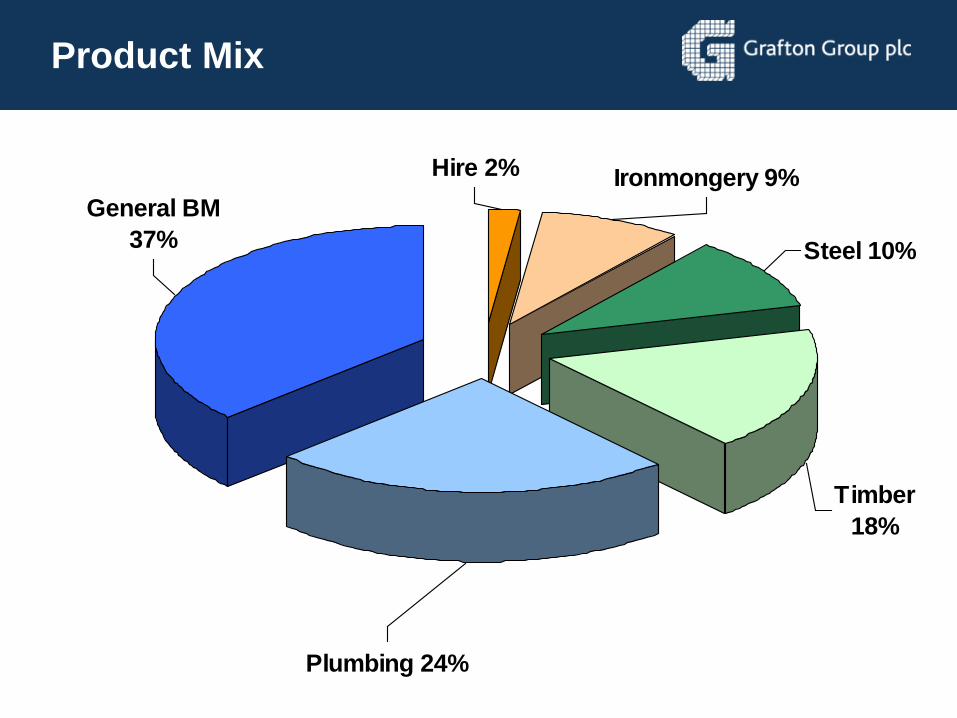

Product Mix

Ironmongery 9%Hire 2%

Timber

18%

Steel 10%

Plumbing 24%

General BM

37%

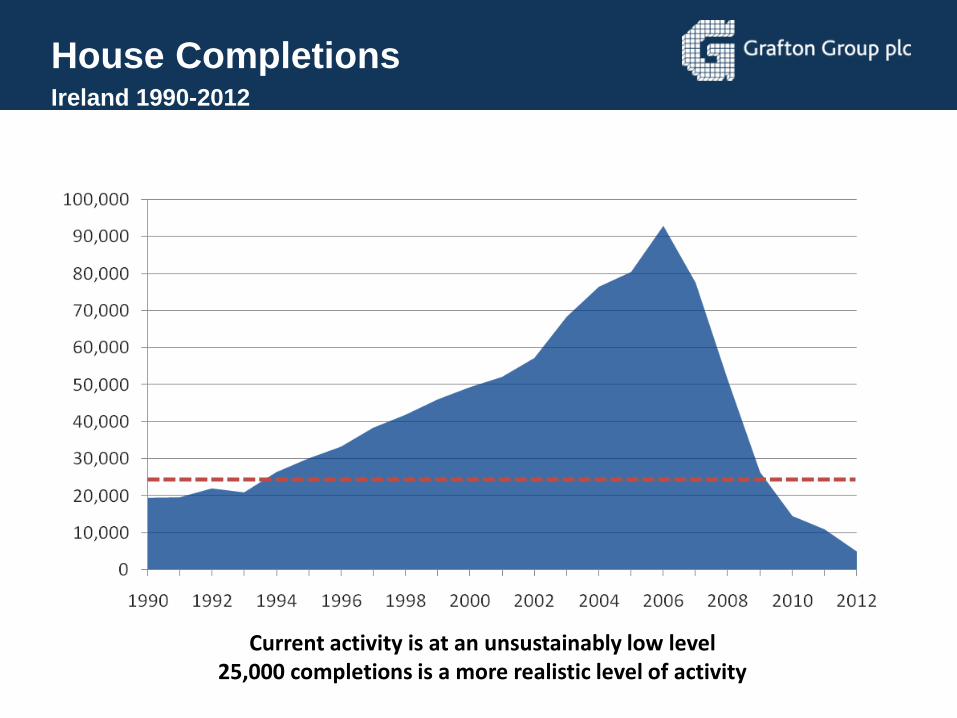

House CompletionsIreland 1990-2012

Current activity is at an unsustainably low level25,000 completions is a more realistic level of activity

Outlook for Irish economy

• Recovering Market Conditions• Housing

• RMI• Demographics

• Min 25,000 units needed per annum

• Young population• Government Stimulus

• RMI

• New business start-ups• Foreign Investment

• Hotels

• Incomplete projects• Food / Agri

• CAP changes in 2015

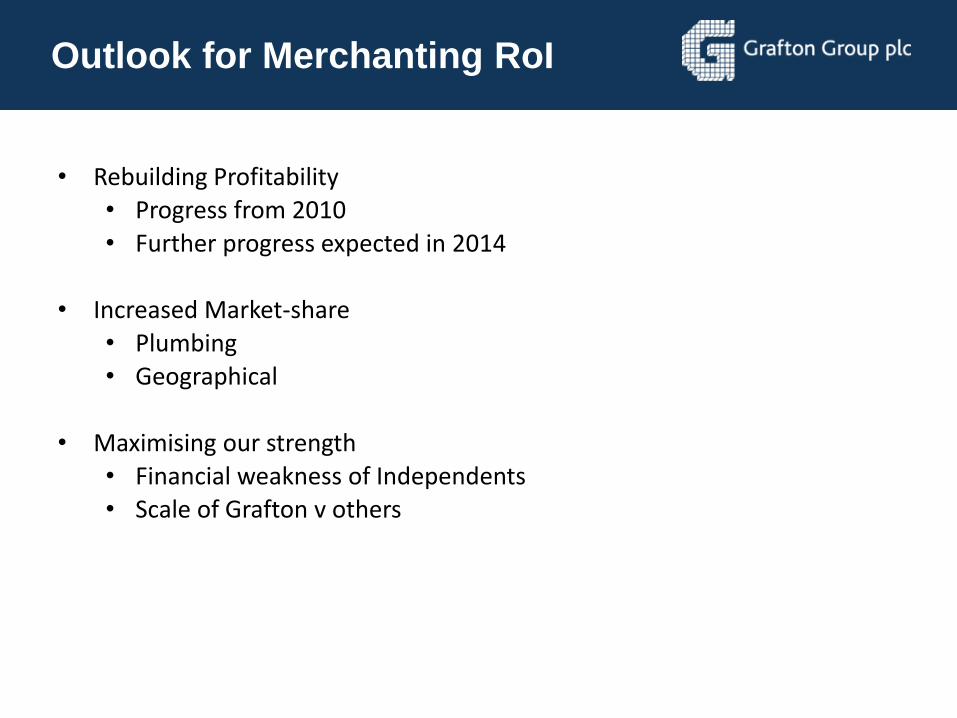

Outlook for Merchanting RoI

• Rebuilding Profitability• Progress from 2010

• Further progress expected in 2014

• Increased Market-share

• Plumbing• Geographical

• Maximising our strength• Financial weakness of Independents• Scale of Grafton v others

Selco video presentation

Joe Sowton

Group Strategic

Development Director

Our Strategy

• A focussed supplier of construction materials

• Active in the UK, Ireland and Belgium

• Our reputation is built on service

• Market leading positions

• To expand both organically and into new markets

What sets Grafton apart?

• We aim to lead not follow the market

• ‘Multi specialist’ stores

• Market leader in Ireland

• Selco – unique model

• Strong local management

• Group structure and disciplines

• High service levels

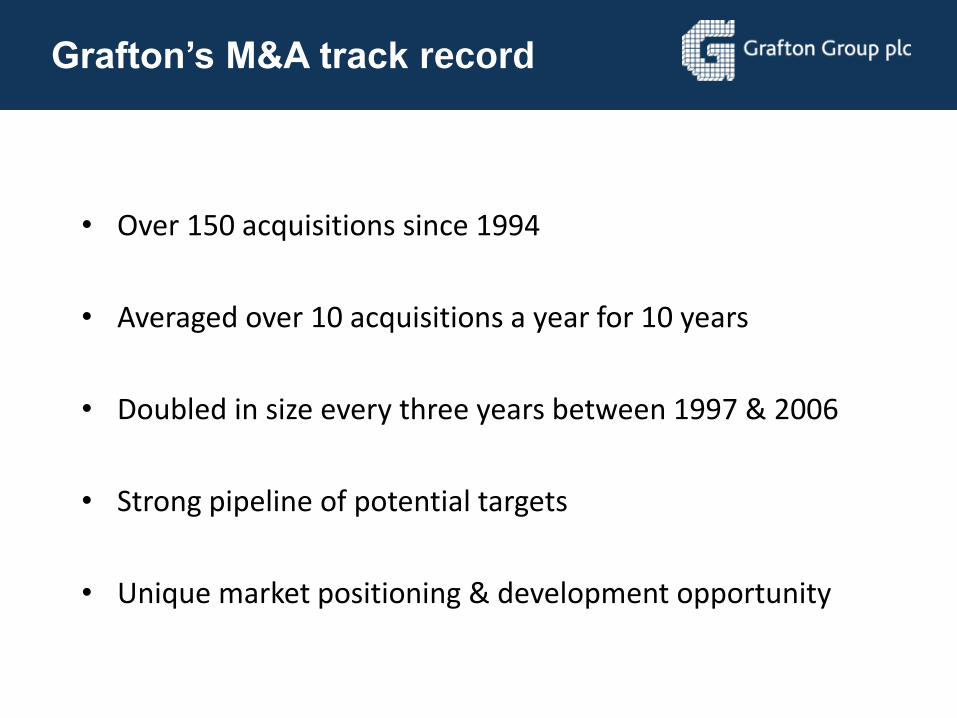

Grafton’s M&A track record

• Over 150 acquisitions since 1994

• Averaged over 10 acquisitions a year for 10 years

• Doubled in size every three years between 1997 & 2006

• Strong pipeline of potential targets

• Unique market positioning & development opportunity

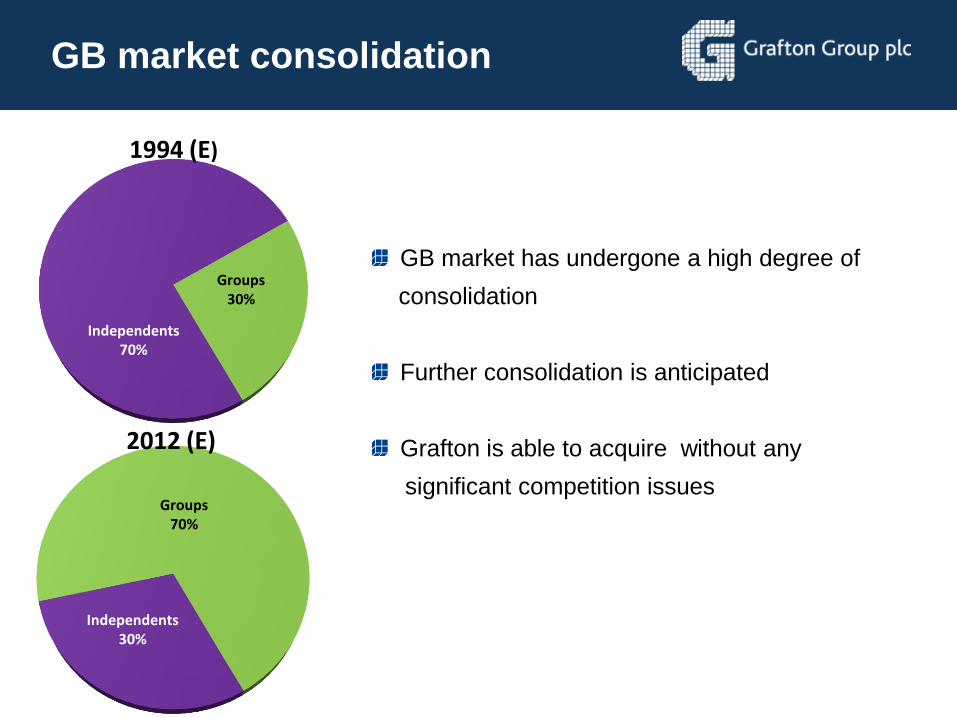

GB market consolidation

Independents70%

Groups30%

Independents30%

Groups70%

1994 (E)

2012 (E)

GB market has undergone a high degree of

consolidation

Further consolidation is anticipated

Grafton is able to acquire without any

significant competition issues

Effect of consolidation

• Rapid growth of largest Groups

• Modern efficient outlets

• IT transforms efficiency and communication

• Wider range of products and services

• Retail custom encouraged

• Industry professionalised

• Buying groups evolved

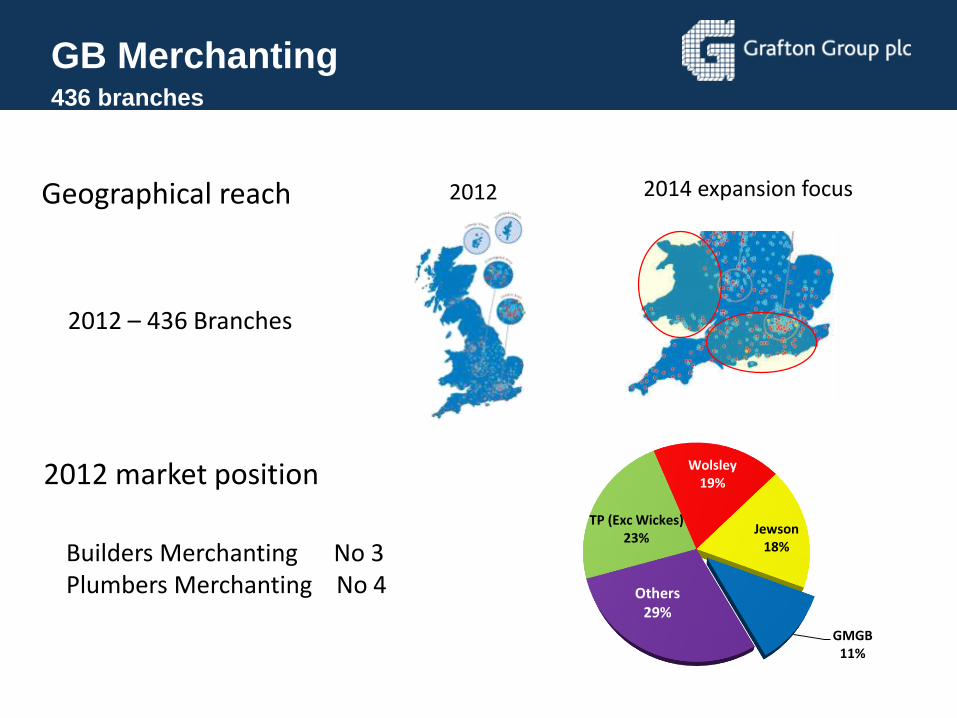

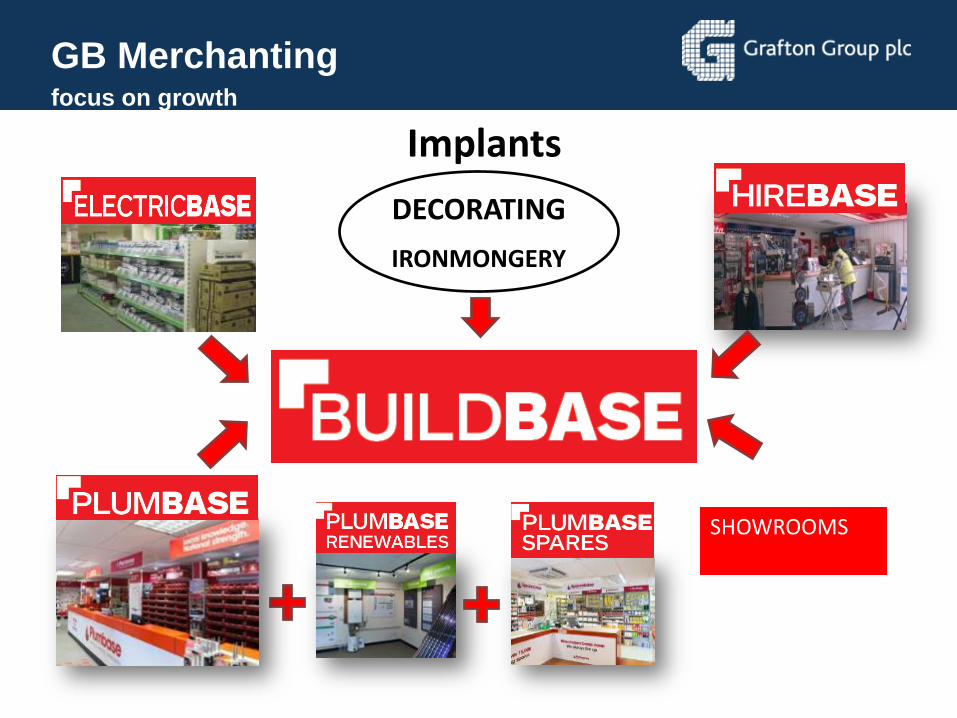

GB Merchanting436 branches

Geographical reach

2012 market position

TP (Exc Wickes)23%

Wolsley19%

Jewson18%

GMGB11%

Others29%

2012 2014 expansion focus

Builders Merchanting No 3Plumbers Merchanting No 4

2012 – 436 Branches

Source: Management data

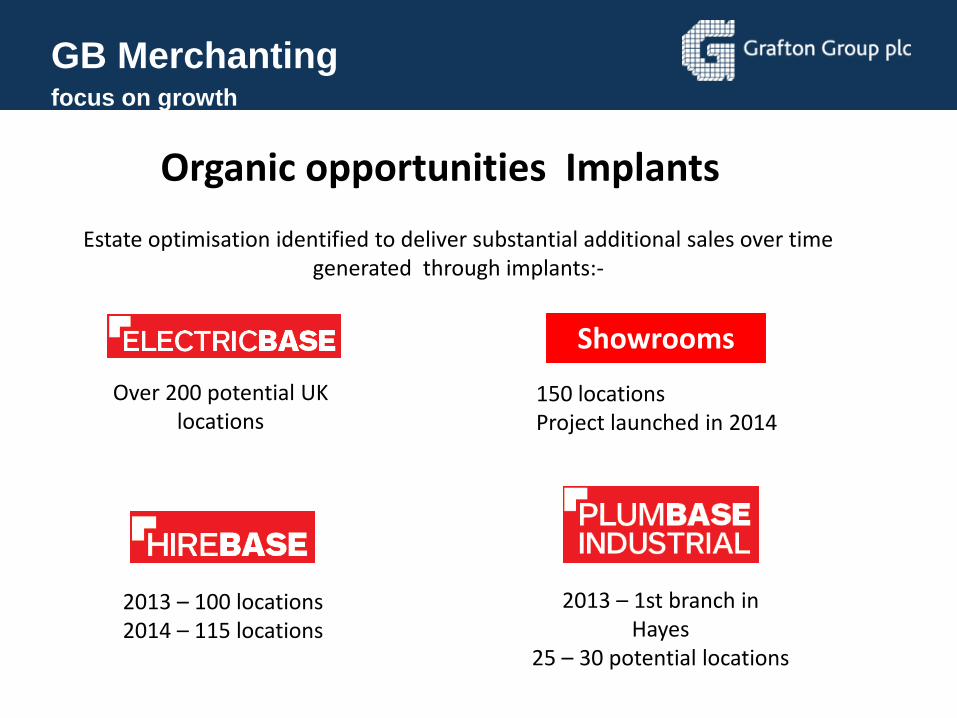

GB Merchantingfocus on growth

Organic opportunities Implants

Over 200 potential UK locations

150 locationsProject launched in 2014

Estate optimisation identified to deliver substantial additional sales over time generated through implants:-

2013 – 100 locations2014 – 115 locations

Showrooms

2013 – 1st branch in Hayes

25 – 30 potential locations

GB Merchantingfocus on growth

Implants

DECORATING

IRONMONGERY

SHOWROOMS

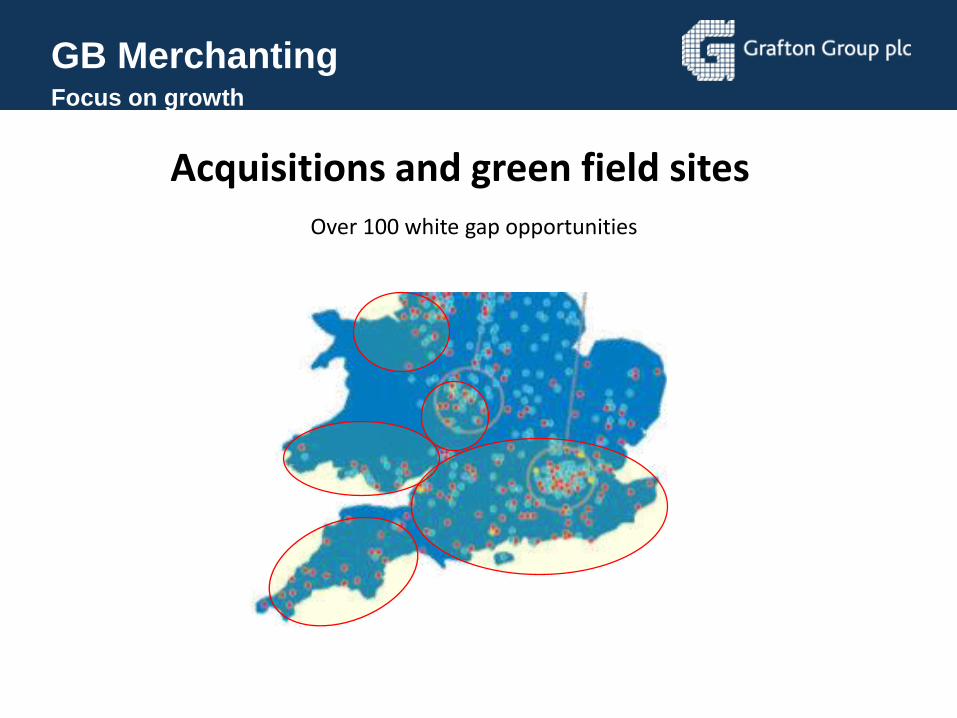

GB MerchantingFocus on growth

Over 100 white gap opportunities

Acquisitions and green field sites

Trade cash & carry - 36 stores

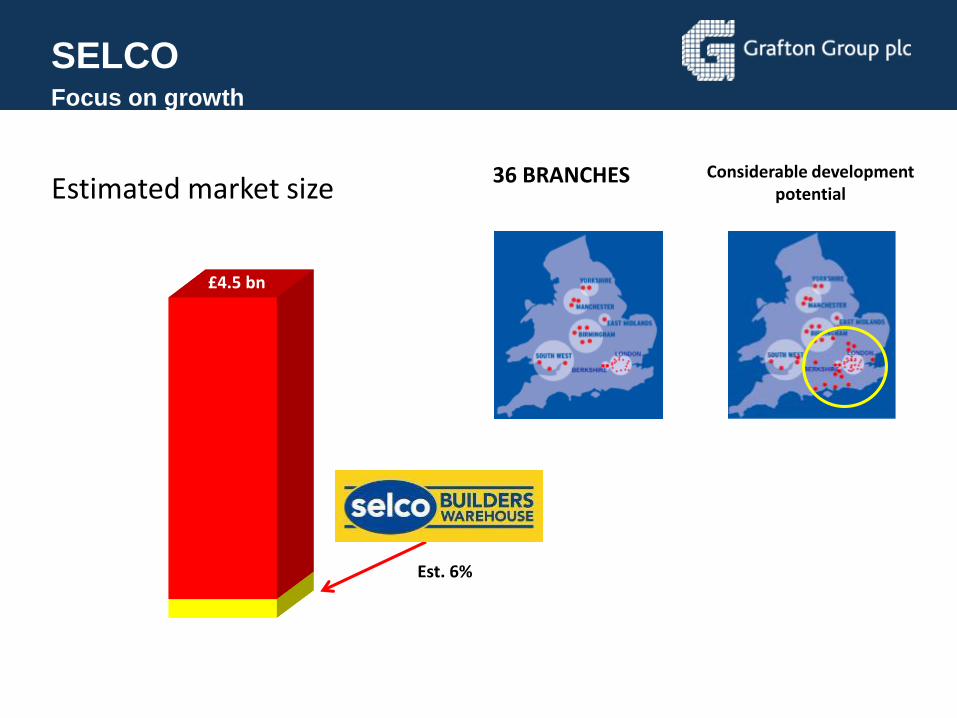

SELCOFocus on growth

36 BRANCHES Considerable development potential

£4.5 bn

Est. 6%

Estimated market size

Source: Management estimate

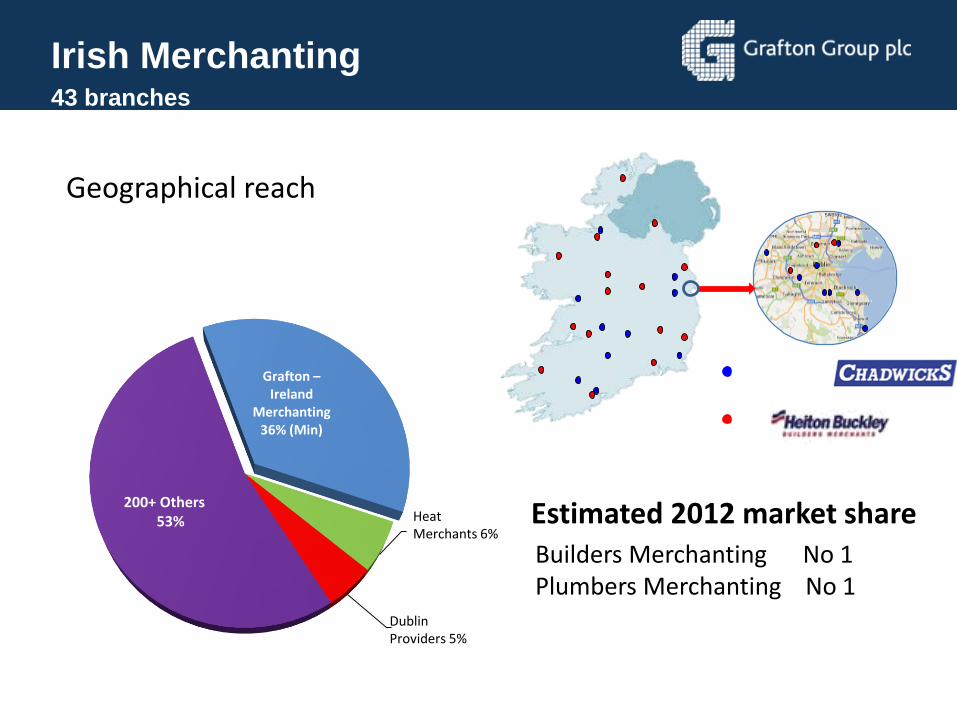

Irish Merchanting43 branches

Estimated 2012 market shareHeat Merchants 6%

Dublin Providers 5%

Grafton –Ireland

Merchanting36% (Min)

200+ Others53% Heat

Merchants 6%

Geographical reach

Builders Merchanting No 1Plumbers Merchanting No 1

DublinProviders 5%

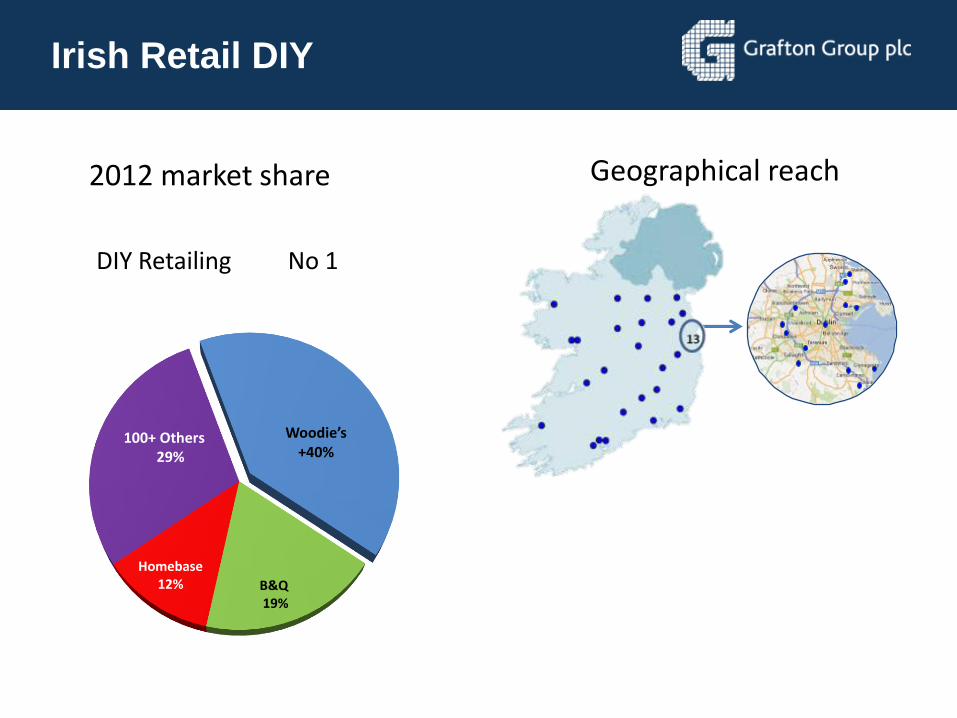

Irish Retail DIY45 stores

Irish Retail DIY

2012 market share

Woodie’s+40%

B&Q19%

Homebase12%

100+ Others29%

Geographical reach

DIY Retailing No 1

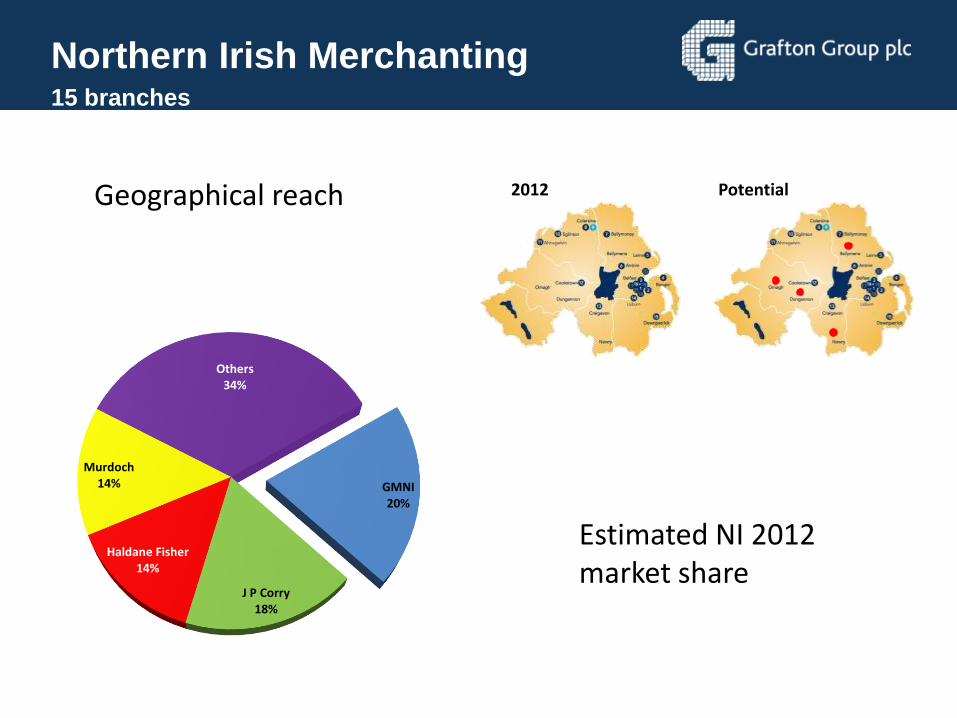

Northern Irish Merchanting15 branches

Estimated NI 2012 market share

GMNI20%

J P Corry18%

Haldane Fisher14%

Murdoch14%

Others34%

2012 PotentialGeographical reach

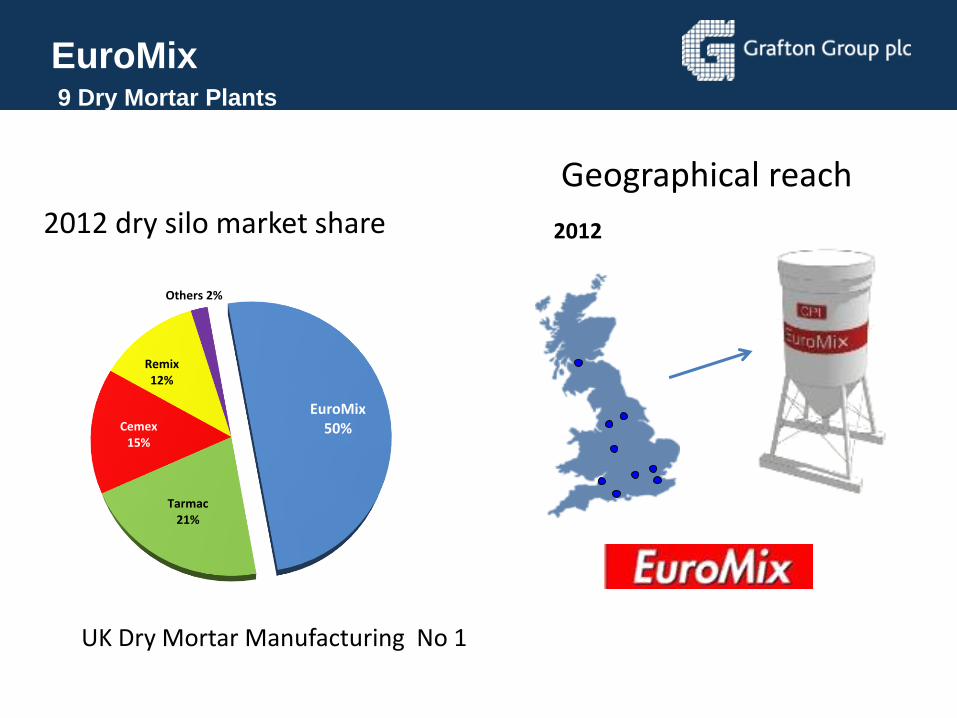

EuroMix Dry Mortar

EuroMix9 Dry Mortar Plants

2012 dry silo market share

EuroMix50%

Tarmac21%

Cemex 15%

Remix12%

Others 2%

2012

Geographical reach

UK Dry Mortar Manufacturing No 1

Where can we add value?

• Transferable skills & knowhow

• Synergies

• Experience of growth

Considerations and tests

Ability to deliver shareholder value

Construction output

Market size: RMI housing & non-housing / commercial

GDP per capita & CAGR

Housing starts

Age of housing stock

Population trends

Unemployment trends

Ease of doing business

Risk analysis

Expansion into Belgium

GRAFTON’S JOINT VENTURE WITH ROUSSEL NV - 2009

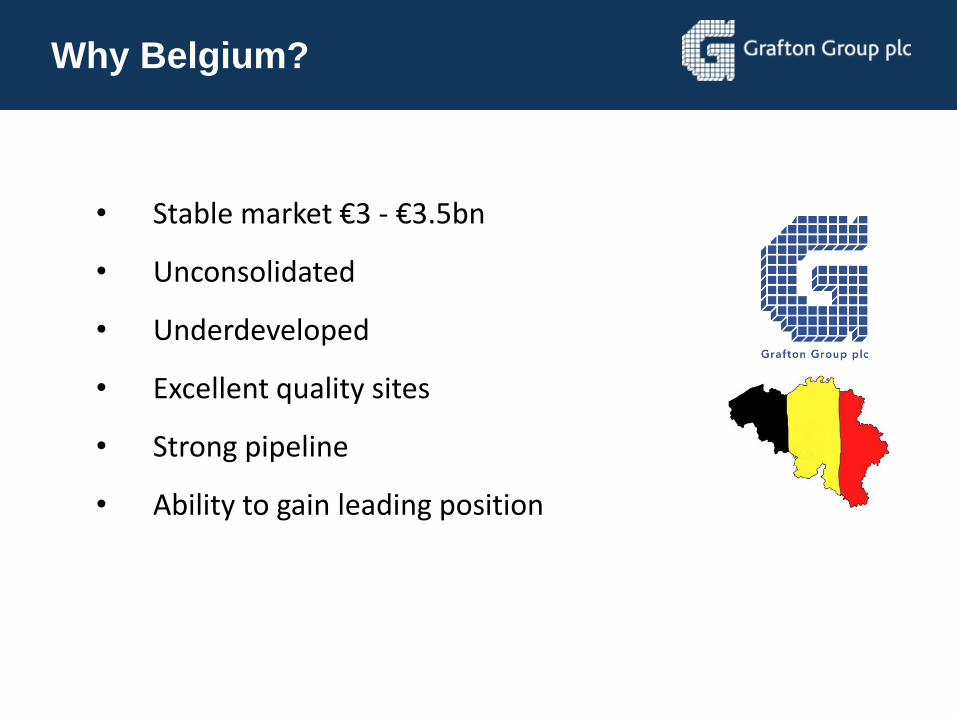

Why Belgium?

• Stable market €3 - €3.5bn

• Unconsolidated

• Underdeveloped

• Excellent quality sites

• Strong pipeline

• Ability to gain leading position

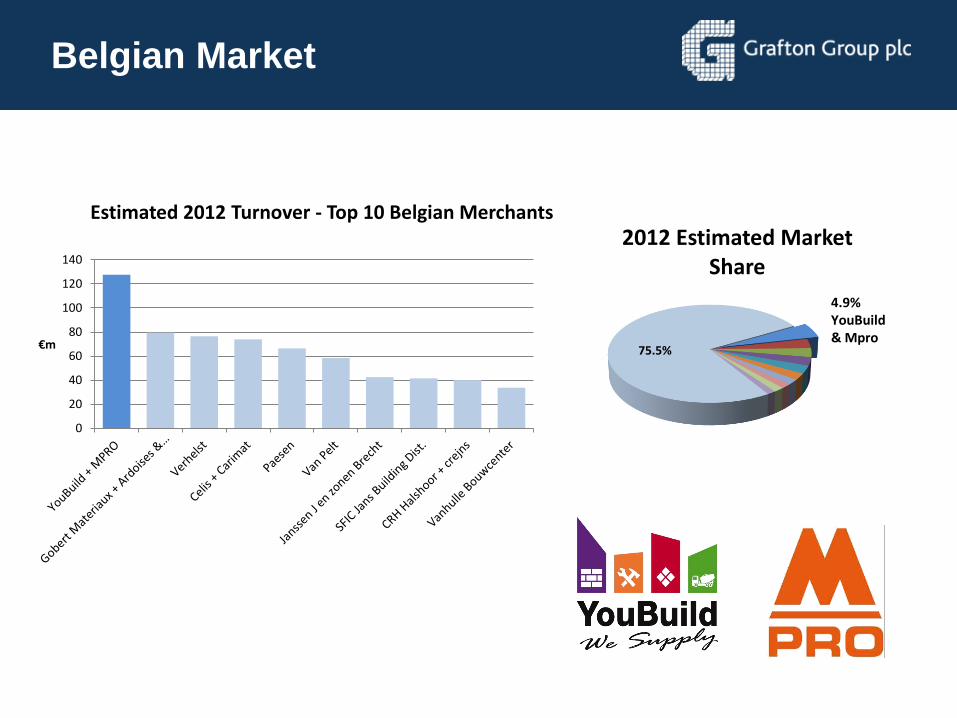

Belgian Market

0

20

40

60

80

100

120

140

€m

Estimated 2012 Turnover - Top 10 Belgian Merchants

75.5%

2012 Estimated Market Share

4.9%YouBuild & Mpro

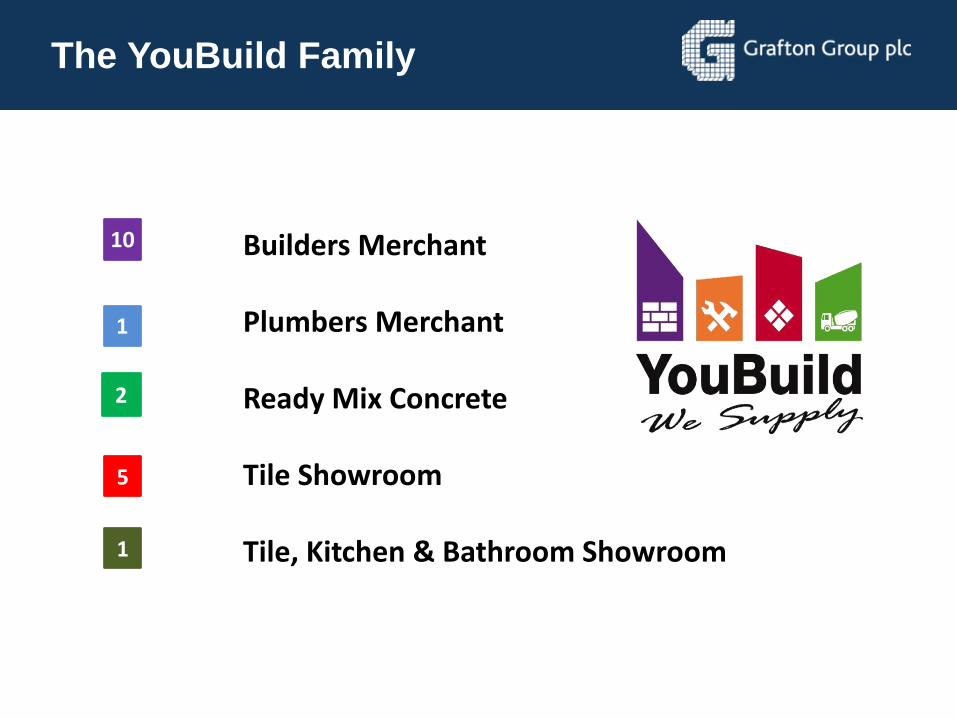

The YouBuild Family

10

2

5

1

1

Builders Merchant

Plumbers Merchant

Ready Mix Concrete

Tile Showroom

Tile, Kitchen & Bathroom Showroom

• JV successfully repositioned in 2012

• Grafton now has control

• JV area redefined mainly within an area of West Flanders

• Family shareholders no longer operational management

• Supplier renegotiations successfully completed following exit from buying group

• 2013 – introduced uniform IT platform across group

• Grafton at liberty to develop outside of the JV in Belgium

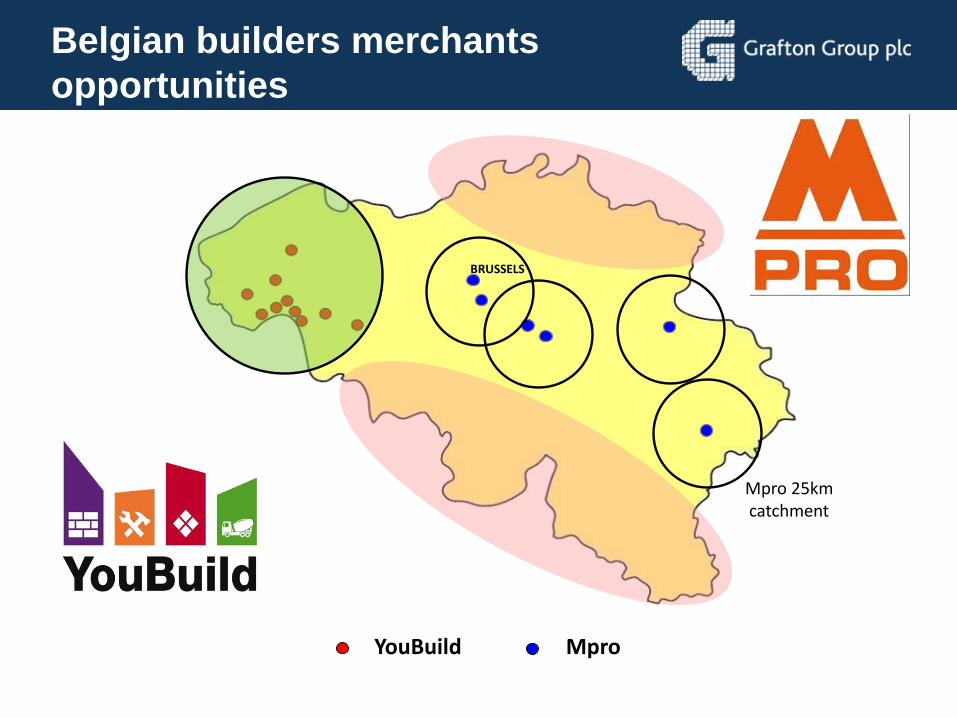

Belgian builders merchants

opportunities

YouBuild Mpro

Mpro 25kmcatchment

BRUSSELS

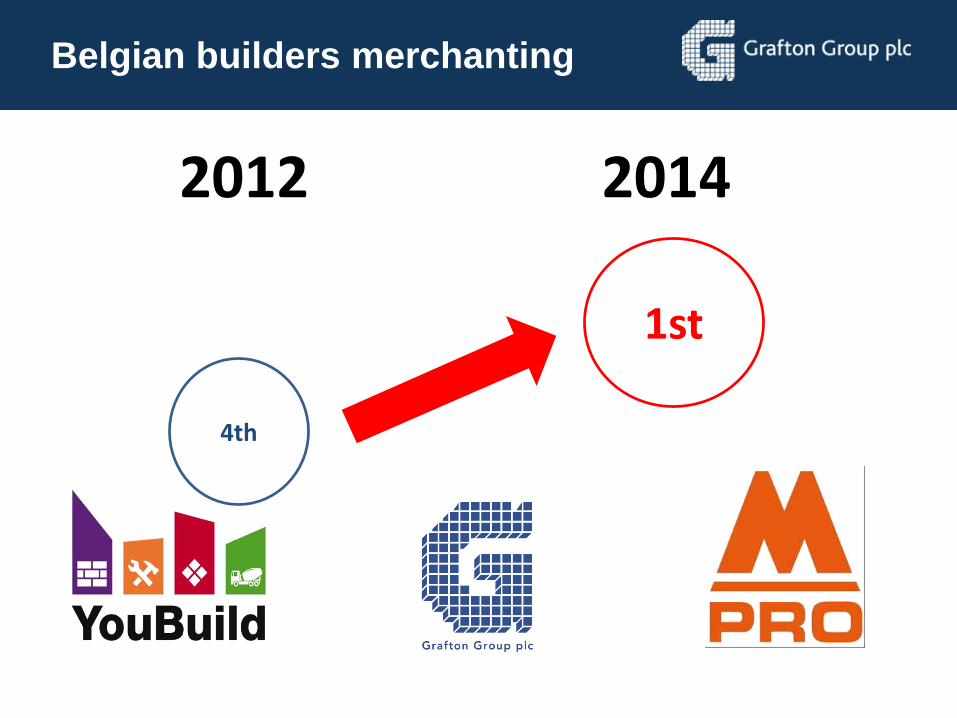

Belgian builders merchanting

1st

4th

2012 2014

Summary

• Key focus on UK growth

• Well positioned in Ireland

• Significant progress in Belgium

• Potential to develop internationally

Gavin Slark

Chief Executive Officer

Outlook and Summary

Outlook - UK

• Economy growing at moderate rate as recovery takes hold

• Clear signs that the housing market has strengthened

• Improving trend in housing transactions and mortgage approvals

• Economic and housing market backdrop supportive of increase in RMI volumes in merchanting market

• Internal developments also providing a platform for growth

• Government help to buy measures will benefit the Group but we anticipate a time delay

Outlook - Ireland

• Domestic economy starting to stabilise – after contracting for five years

• Downturn in housing construction bottoming out

• House price stabilisation expected to become more broadly based geographically

• Housing transactions and mortgage approvals coming off a low base

Summary

• Grafton has managed the recession well

• Experienced Executive management team now in place

• Significant potential for organic growth

• UK acquisition opportunities

• Scope for further international development

Thank you for listening

Questions and answers