Embed Size (px)

Citation preview

i

Government of Karnataka

Report:

FISCAL INDICATORS OF ‘BRICS’ NATIONS: A

COMPARATIVE ANALYSIS

Center for Financial Accountability and Decentralization

Fiscal Policy Institute

Kengeri, Bengaluru-60

October, 2017

ii

iii

TABLE OF CONTENTS

Abstract iii

Executive Summary iv

List of Chapters vi

List of Tables vi

List of Illustrations vi

List of Abbreviations vii

iv

Abstract

This report analyses and compares the fiscal policies/indicators of BRICS economies for last two

decades and in particular, post crisis period comprehensively. With the emergence financial crisis

in 2008, favourable fiscal balances of BRICS economies turned into deficits. Consequently the

debt level started peaking up. India has highest fiscal deficits and debt and also lowest revenues

and expenditure as proportion to GDP amongst the BRICS economies. China has the least deficits

and debt when compared to other BRICS nations. In 2014-15, due to global economic slowdown

there was a crisis again in the fiscal balance of Brazil and Russia. The Russian economy is highly

dependent on oil exports for revenue. The oil price fluctuations determine Russia’s fiscal balances.

It was also found that vertical fiscal imbalance is a major problem for China and South Africa, as

the Center has more revenue raising powers whereas lower level of governments have higher

spending responsibilities.

Fiscal rules have played very important role in keeping fiscal variables under control. Amongst

the BRICS, Brazil is the first country to enact a Fiscal Responsibility Legislation in the year 2000.

Brazil’s Fiscal Responsibility Law (FRL) is very strict and it even specifies penalties and

sometimes imprisonment for mismanagement of government funds. Both India and Russia follow

numerical fiscal rules. South Africa and China do not follow any legislated budget constraints.

However, Medium Term Fiscal Plan was adopted by both the nations. In recent episodes, Chinese

Government is stressing on the fiscal transparency aspect.

Fiscal indicators of BRICS economies were under control before the onset of 2008 global financial

crisis. However, after the crisis, it started deteriorating for all BRICS economies with exception of

China. A well-controlled fiscal situation was observed for China even in the crisis period. To an

extent, numerical fiscal rules has worked for Brazil and India. In the recent years all the BRICS

economies are giving greater prominence to procedural rules and fiscal transparency.

v

Executive Summary

Brazil, Russia, India, China and South Africa (BRICS) are grouped as emerging economies and

these countries are fastest growing in the world. There was tremendous improvements in output

growth and per capita income growth for these nations over the last two decades. The recent 2008

financial crisis adversely affected many economies in the world and the BRICS countries are not

an exception.

This report analyses and compares the developments in fiscal policies/indicators for last two

decades and in particular, post crisis period comprehensively. It was found that favourable fiscal

balances (surpluses and smaller deficits) has turned out to be huge deficits after the 2008 crisis.

Consequently the debt level started peaking up. India has highest fiscal deficits and debt and also

lowest revenues and expenditure as proportion to GDP amongst the BRICS economies. China has

the least deficits and debt when compared to other BRICS nations. In 2014-15, due to global

economic slowdown there was a crisis again in the fiscal balance of Brazil and Russia. The Russian

economy is highly dependent on oil exports for revenue. The oil price fluctuations determine

Russia’s fiscal balances. It was also found that vertical fiscal imbalance is a major problem for

China and South Africa, as the Center has more revenue raising powers whereas lower level of

governments have higher spending responsibilities.

Fiscal rules have played very important role in keeping fiscal variables under control. Amongst

the BRICS, Brazil is the first country to enact a Fiscal Responsibility Legislation in the year 2000.

This rule applies to all levels of government. Brazil’s Fiscal Responsibility Law (FRL) is very

strict and it even specifies penalties and sometimes imprisonment for mismanagement of

government funds.

India enacted FRBM Act in 2003 and at subnational level, State Governments have enacted their

own FRLs. Framing of FRLs at subnational level was incentivized and promoted by the Central

Government through several schemes like Debt Swap Scheme, Fiscal Reform Facility and Debt

Consolidation & Relief Facility. With the help of FRLs and favourable economic condition both

Centre and State Governments in India could reduce their deficits below threshold of 3% of GDP.

The State Governments efforts in reducing fiscal deficits are remarkable. 14th Finance Commission

has incentivized the states’ fiscal efforts by providing a flexibility in fiscal deficit target by 0.5%

vi

of GSDP if state’s debt to GSDP ratio is below 25% and interest payments to revenue receipts

ratio is below 10% in the preceding year.

Russian Government has framed Balanced Budget Rule (BBR) in 2007-08. Government has

adopted non-oil fiscal balance as target fiscal indicator. However BBR was removed in 2012 owing

to 2008 financial crisis. Since 2013 Russian Government is following ‘Expenditure Rule’. South

Africa and China do not follow any legislated budget constraints. However, Medium Term Fiscal

Plan was adopted by both the nations. In recent episodes, Chinese Government is stressing on the

fiscal transparency aspect.

Overall, this study finds that fiscal position of BRICS nation was in good shape before 2008 crisis.

Aftermath the crisis, these indicators turned out to be negative. China’s fiscal performance even

in crisis period was remarkable. Numerical fiscal rules has worked to an extent for Brazil and

India. All the BRICS nations presently emphasizes on procedural rules and fiscal transparency

implying their path towards sustainable fiscal balance.

vii

List of Chapters

Chapter-1:

Economic Profile of BRICS Nations 1 - 5

Chapter-2:

Fiscal Indicators of BRICS Economies 6 - 12

Chapter-3:

Fiscal Rules in BRICS Economies 13 - 28

Chapter-4:

Conclusion 29 - 30

Bibliography 31 – 32

List of Tables

1.1 Per-Capita GDP (in current US$) 04

1.2 Sector-wise Distribution of GDP 04

2.1 General Government Revenue & Expenditure 06

2.2 Cyclical Component of GENERAL Government Balance (% of GDP) 10

List of Illustrations

1.1 Real GDP growth of BRICS Nations 02

2.1 General Government Balance (% of GDP) 07

2.2 General Government Cyclically adjusted Balance (% of GDP) 09

2.3 General Government Primary Balance (% of GDP) 10

2.4 General Government Debt (% of GDP) 11

viii

List of Abbreviations

BBR: Balanced Budget Rule

BRICS: Brazil, Russia, India, China & South Africa

DSS: Debt Swap Scheme

FRBM: Fiscal Responsibility and Budget Management

FRF: Fiscal Reforms Facility

FRL: Fiscal Responsibility Law

GDP: Gross Domestic Product

GEAR: Growth, Employment and Redistribution

IMF: International Monetary Fund

MTBPS: Medium Term Budget Policy Statement

MTFP: Medium Term Fiscal Plan

MTFRP: Medium Term Fiscal Reforms Program

NDB: New Development Bank

OECD: Organization for Economic Cooperation and Development

PCI: Per Capita Income

RDP: Reconstruction and Development Program

SARS: South African Revenue Service

1

Fiscal Indicators of ‘BRICS’ Nations: A Comparative Analysis

The acronym ‘BRIC’ was first coined by Jim O’ Neill in Goldman Sachs’ research paper ‘Building

Better Global Economic BRICs” in the year 2001 (Neill, 2001). BRIC represents emerging nations

namely Brazil. Russia, India & China. Formal grouping of BRIC was happened in the year 2006.

It was agreed to expand BRIC into BRICS (Brazil, Russia, India, China & South Africa) with the

inclusion of South Africa at the BRIC foreign ministers meeting in New York in 2010. These five

emerging economies comprises 43% of world’s population, 30% of world Gross Domestic Product

(GDP) and 17% share in global trade (GoI, 2017).

Eight BRICS summit were held till now. The agenda of BRICS meetings has considerably widened

over the years. BRICS cooperation has two pillars namely consultations on issues of mutual

interest through meeting of leaders as well as minsters of different ministries and practical

cooperation in number of areas through meetings of working group and senior officials.

In the 6th BRICS summit held at Fortaleza, Brazil in 2014 an agreement was signed among BRICS

nations to establish a multilateral development bank and it was named as New Development Bank

(NDB). The purpose of NDB is to mobilize resources for infrastructure and sustainable

development projects in BRICS and other emerging and developing economies while

complementing efforts of other multilateral and regional financial institutions (NDB, 2017).

This report basically examines the fiscal situation of BRICS nations in terms of its revenue,

expenditure and debt. The 2008 financial crisis severely affected many countries in the world,

especially the advanced ones. Its adverse effect was also observed on emerging nations in terms

of slow growth. This report concentrates mainly on fiscal indicators behavior aftermath the crisis

and also examines the fiscal developments (fiscal rules in particular) took place in BRICS Nations

in the last two decades.

This report comprises of four chapters. First chapter provides brief economic profile of all the

BRICS Nations in terms of economic growth, per capita income etc. Second chapter comparatively

analyzes the trend and patterns of fiscal indicators of BRICS economies. Third chapter provides a

discussion on fiscal developments took place in BRICS Nations, particularly in terms of fiscal

rules in the last two decades. Last chapter concludes the report.

2

Chapter-1

Economic Profile of BRICS Nations

Higher GDP growth implies increase in country’s productive capacity. Simon Kuznets in his Noble

Prize lecture defines economic growth as a long term rise in capacity to supply increasingly diverse

economic goods to its population, this growing capacity is based on advanced technology and the

institutional and ideological adjustments that it demands (Nobleprize.org, 2017). Figure-1.1

depicts real GDP growth of BRICS Nations since 1991 to 2015.

Figure-1.1

Real GDP Growth of BRICS Nations

Source: World Development Indicators, The World Bank (2017)

Note: growth figures are in annual % growth rate of GDP at Market Price based on constant local

currency

In 1991, GDP growth of India and Brazil was as low as 2%, whereas it was negative for South

Africa and Russia. Political turmoil, collapse of Soviet Union, plummeting foreign trade, drastic

fall in state revenues, decline in oil prices etc resulted in negative growth in early 90s for Russia

(Aslund, 1999). The macroeconomics of fiscal policy in Russia is mainly dominated by oil

revenues. It is the main export earner and largest source of government revenue. The financial

indiscipline with massive implicit subsidies amounting to about 10% of GDP has resulted in

-20

-15

-10

-5

0

5

10

15

20

GR

OW

TH (

IN %

)

YEAR

Brazil Russia India China South Africa

3

declining tax collections, rising government debt, higher interest rates and poor growth

performance in 1998. These factors reinforced each other, contributing to the general financial and

currency crisis in 1998 (Bogetic, 2010). Sharp reduction in Russia’s GDP growth can be observed

from Figure-1.1. South Africa’s growth rate has picked up after the end of apartheid era in 1994.

India’s growth was very low in 1991. In the same year India has faced severe Balance of Payments

crisis, high inflation and higher budget deficits. However, liberalization reforms of 1991-92 by

opening up of economy for private investments has resulted in higher growth rate in subsequent

years. More importantly, massive growth in service sector through revolution in information

technology sector and other service sectors is the prime reason for better growth rates. The upward

trend in growth rate continued for all the countries until 2007 and the growth rate was 8% for India

and Russia, around 5% for Brazil and South Africa. After a recovery from 2008 financial crisis,

Brazilian economy once again entered into recession in 2014. The situation further worsened in

2015. The factors which lead to Brazilian recession in 2014 are structural weakness of Brazilian

economy, negative terms of trade, strong capital inflows which fueled currency appreciation,

higher fiscal and current account deficits, decline in commodity prices and consequent decline in

export earnings etc (ECB, 2016). China since 1991 has maintained comparatively higher growth

rate among the BRICS nations. This trend was mainly owing to China’s large investments in

infrastructure, which boosted the growth. Productivity gains in terms of increased economic

efficiency is another reason for higher growth (Morrison, 2015). India is a strong service provider

with a rising manufacturing base, while China is seen as the manufacturing work shop of the world

with a highly skilled workforce and relatively low wage costs (GoI, 2012).

Availability of natural resources also contributes for the growth and also revenue to the

Government. Russia, China and South Africa are resource rich states. For instance, South Africa

generates 45% of Africa’s electricity and the South Africa power supplier provides the 4th cheapest

electricity in the world (GoI, 2012). Russia accounts 20% of world oil reserves, while China has

about 12% of world’s mineral resources. Among the BRICS India and Brazil are relatively more

domestic demand driven economies whereas China and Russia has significant outward linkage

(GoI, 2012).

With 2008 economic recession, there was a drastic decline in the growth rates for all the five

countries. However this decline is minimal for India and China. Immediate recovery of these two

4

countries and consistent growth performance is impressive. The decline is highest for Russia

followed by South Africa and Brazil in 2009.

Sustained economic reforms and improved macroeconomic fundamentals along with a buoyant

macroeconomic environment contributed to the improved growth performance of BRICS in the

present and last decade.

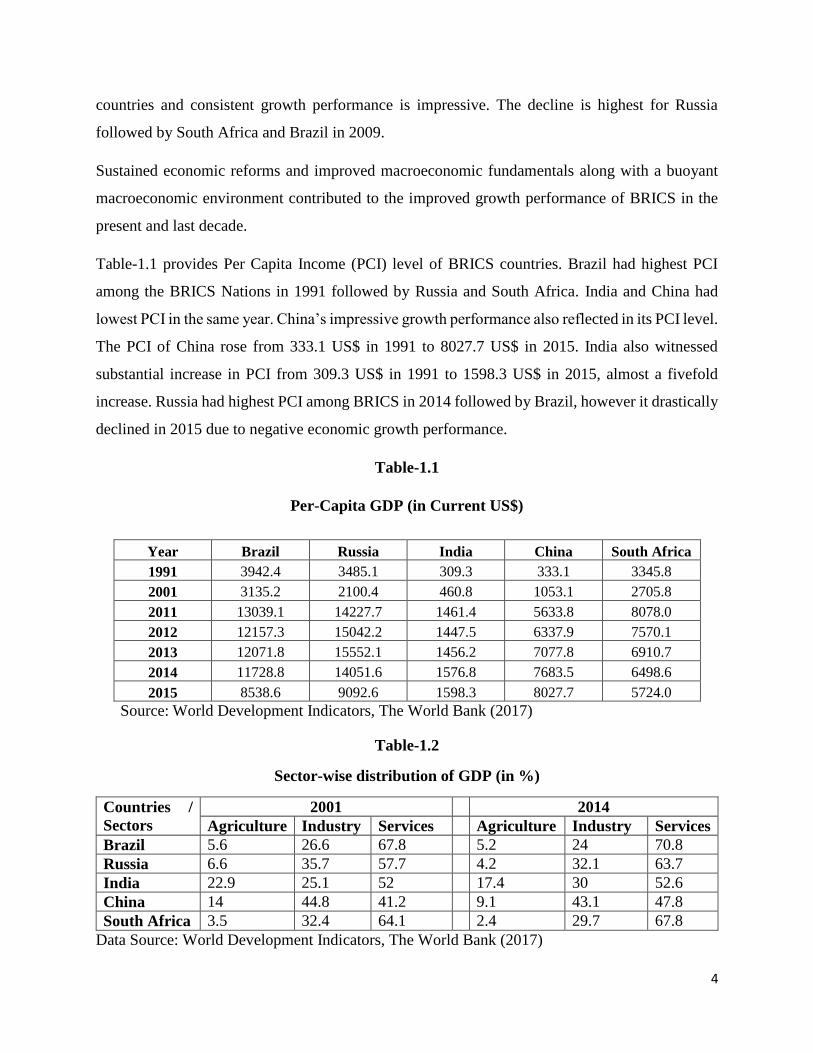

Table-1.1 provides Per Capita Income (PCI) level of BRICS countries. Brazil had highest PCI

among the BRICS Nations in 1991 followed by Russia and South Africa. India and China had

lowest PCI in the same year. China’s impressive growth performance also reflected in its PCI level.

The PCI of China rose from 333.1 US$ in 1991 to 8027.7 US$ in 2015. India also witnessed

substantial increase in PCI from 309.3 US$ in 1991 to 1598.3 US$ in 2015, almost a fivefold

increase. Russia had highest PCI among BRICS in 2014 followed by Brazil, however it drastically

declined in 2015 due to negative economic growth performance.

Table-1.1

Per-Capita GDP (in Current US$)

Year Brazil Russia India China South Africa

1991 3942.4 3485.1 309.3 333.1 3345.8

2001 3135.2 2100.4 460.8 1053.1 2705.8

2011 13039.1 14227.7 1461.4 5633.8 8078.0

2012 12157.3 15042.2 1447.5 6337.9 7570.1

2013 12071.8 15552.1 1456.2 7077.8 6910.7

2014 11728.8 14051.6 1576.8 7683.5 6498.6

2015 8538.6 9092.6 1598.3 8027.7 5724.0

Source: World Development Indicators, The World Bank (2017)

Table-1.2

Sector-wise distribution of GDP (in %)

Countries /

Sectors

2001 2014

Agriculture Industry Services Agriculture Industry Services

Brazil 5.6 26.6 67.8 5.2 24 70.8

Russia 6.6 35.7 57.7 4.2 32.1 63.7

India 22.9 25.1 52 17.4 30 52.6

China 14 44.8 41.2 9.1 43.1 47.8

South Africa 3.5 32.4 64.1 2.4 29.7 67.8

Data Source: World Development Indicators, The World Bank (2017)

5

Table-1.2 provides sector wise distribution of GDP in BRICS countries. Value added from

agricultural sector is highest for India followed by China. For all the BRICS countries value added

from agriculture has declined over the years. Industrial contribution to GDP is highest for China

accounting nearly 45% followed by Russia and South Africa. China maintains top position even

in 2014 in terms of gross value added from industrial sector. Service sector is the major contributor

towards national output in all the BRICS countries in 2014.

Higher economic growth, substantial increase in PCI, high value added from services etc implies

BRICS countries are growing as emerging global players. These factors also have fiscal

implications in terms of higher revenue collection and spending by the Governments. Next chapter

reviews the fiscal position of BRICS nations and further elaborates the trends and patterns of fiscal

indicators.

6

Chapter-2

Fiscal Indicators of BRICS Economies

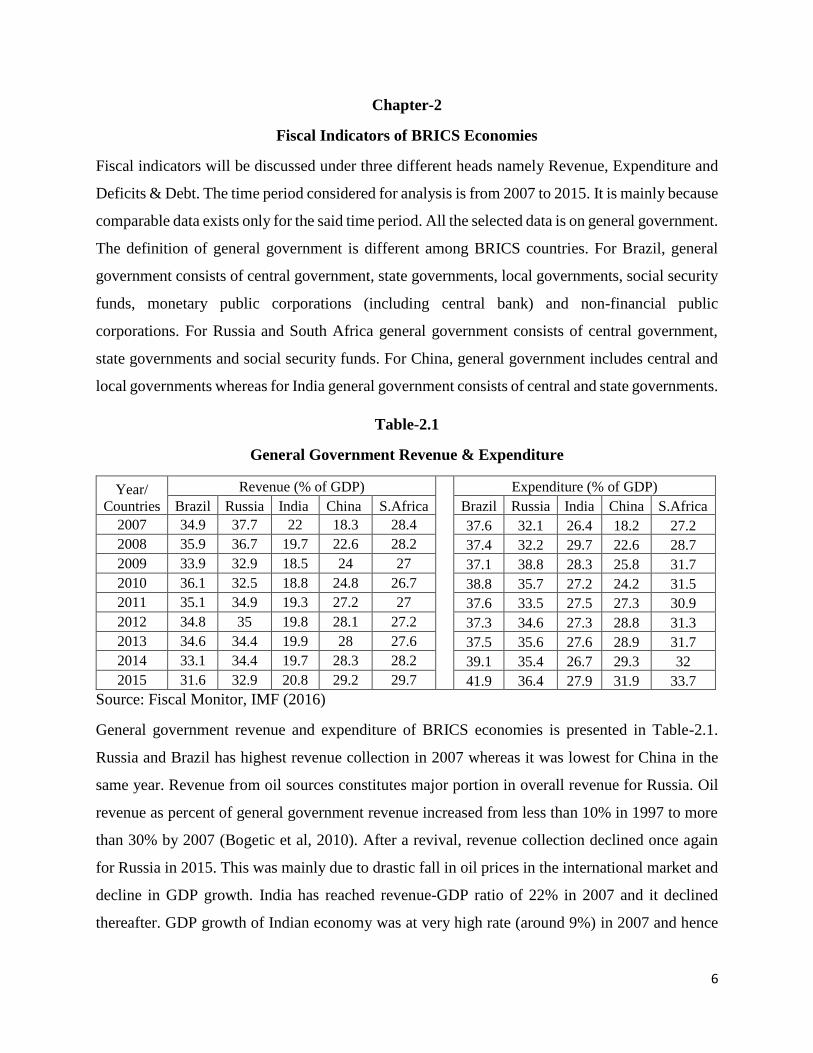

Fiscal indicators will be discussed under three different heads namely Revenue, Expenditure and

Deficits & Debt. The time period considered for analysis is from 2007 to 2015. It is mainly because

comparable data exists only for the said time period. All the selected data is on general government.

The definition of general government is different among BRICS countries. For Brazil, general

government consists of central government, state governments, local governments, social security

funds, monetary public corporations (including central bank) and non-financial public

corporations. For Russia and South Africa general government consists of central government,

state governments and social security funds. For China, general government includes central and

local governments whereas for India general government consists of central and state governments.

Table-2.1

General Government Revenue & Expenditure

Year/

Countries

Revenue (% of GDP)

Expenditure (% of GDP)

Brazil Russia India China S.Africa Brazil Russia India China S.Africa

2007 34.9 37.7 22 18.3 28.4 37.6 32.1 26.4 18.2 27.2

2008 35.9 36.7 19.7 22.6 28.2 37.4 32.2 29.7 22.6 28.7

2009 33.9 32.9 18.5 24 27 37.1 38.8 28.3 25.8 31.7

2010 36.1 32.5 18.8 24.8 26.7 38.8 35.7 27.2 24.2 31.5

2011 35.1 34.9 19.3 27.2 27 37.6 33.5 27.5 27.3 30.9

2012 34.8 35 19.8 28.1 27.2 37.3 34.6 27.3 28.8 31.3

2013 34.6 34.4 19.9 28 27.6 37.5 35.6 27.6 28.9 31.7

2014 33.1 34.4 19.7 28.3 28.2 39.1 35.4 26.7 29.3 32

2015 31.6 32.9 20.8 29.2 29.7 41.9 36.4 27.9 31.9 33.7

Source: Fiscal Monitor, IMF (2016)

General government revenue and expenditure of BRICS economies is presented in Table-2.1.

Russia and Brazil has highest revenue collection in 2007 whereas it was lowest for China in the

same year. Revenue from oil sources constitutes major portion in overall revenue for Russia. Oil

revenue as percent of general government revenue increased from less than 10% in 1997 to more

than 30% by 2007 (Bogetic et al, 2010). After a revival, revenue collection declined once again

for Russia in 2015. This was mainly due to drastic fall in oil prices in the international market and

decline in GDP growth. India has reached revenue-GDP ratio of 22% in 2007 and it declined

thereafter. GDP growth of Indian economy was at very high rate (around 9%) in 2007 and hence

7

the revenue collection was also highest in that year. Revenue collection declined until the year

2010 and it started raising thereon.

2008 financial crisis turned around the positive trend. Revenue collection as percent to GDP

declined for all the countries except China. Interestingly China’s revenue collection improved over

the years from 18.3% in 2007 to 29.2% in 2015. Even in the crisis period China has maintained

better economic growth rate. However its export was severely affected. In order to offset the

negative impacts of export decline on GDP growth and employment, China increased fixed assets

investment (Zhang, 2012). Among the BRICS countries, India has the lowest revenue-GDP ratio

as on 2015.

Expenditure as percent to GDP has increased for all BRICS economies between 2007 and 2015.

Increase was almost 4% of GDP for Brazil and Russia and 6% of GDP for South Africa. There

was a drastic rise in government expenditure for China from 18.2% in 2007 to 31.9% in 2015. The

2008 recession adversely affected the Chinese economy. Its foreign trade and GDP growth

declined. Millions of Chinese workers reportedly lost their job. The Chinese Government

responded by implementing a $586 billion economic package (Morrison, 2015). Indian

Government also provided a stimulus package to revive the economy from recession. The fiscal

stimulus provided by Government of India in the 2009-10 union budget was around 3.5% of GDP

amounting INR 1,86,000 crore (GoI, 2009).

Figure-2.1

General Government Balance (% of GDP)

Source: Fiscal Monitor, IMF (2016)

-12

-10

-8

-6

-4

-2

0

2

4

6

8

2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5

% O

F G

DP

YEARBrazil Russia India China S.Africa

8

Higher expenditure and decline in revenue aftermath the crisis resulted in higher deficits. Figure-

2.1 depicts general government balance of BRICS economies starting from 2007 to 2015. In the

year 2007, only Brazil and India had deficit in the Government account where as other two

countries namely Russia and South Africa were well positioned with a fiscal surplus. China’s

Government account was balanced in 2007. However, by the year 2009, fiscal surplus of Russia,

South Africa and China has turned into deficits. The fiscal situation in countries like India and

Brazil, which were already in deficits even before the 2008 financial crisis has worsened further.

India’s fiscal deficit was as high as 9.8% of GDP in 2009. There was a sharp reduction (almost

10% of GDP) in fiscal balance for Russia from a fiscal surplus of 4.6% of GDP in 2008 to a deficit

of 5.9% of GDP in 2009. Russia’s budget, exports and the structure of its economy is highly

dependent on the oil and gas sector. Large shocks and volatility will continue to define Russia’s

economic environment (Bogetic et al, 2010). With the emergence of 2008 financial crisis, on the

one hand oil revenue base has shrunk dramatically and even non-oil revenue declined with

economic activity and on the other hand social spending pressure has increased resulting in a huge

fiscal deficit for the Government.

China has comparatively better fiscal position then other BRICS economies. China has achieved

fiscal surplus in 2010 and there was a small reduction in fiscal balance by 0.7% of GDP in the

subsequent year. South Africa is facing fiscal deficit since 2009, which was about 4.9% of GDP

and it got reduced to 4% of GDP in 2015.

Brazil’s fiscal position was better than India and South Africa until 2013. However there was a

drastic fall in fiscal balance. Fiscal deficit which was at 3% of GDP in 2013 moved up drastically

to 10.3% of GDP. Brazilian economy has faced severe recession in 2014. Subsidized public sector

lending coupled with a rise in tax exemptions to revive business confidence, sharply increased

fiscal deficits (ECB, 2016). Weaker economic activities and fall in revenues has resulted in higher

deficits.

9

Figure-2.2

General Government Cyclically Adjusted Balance (% of GDP)

Source: Fiscal Monitor, IMF (2016)

International Monetary Fund (IMF) also publishes cyclically adjusted balance every year along

with general government balance data. Cyclically adjusted balance mean structural balance. It

provide a measure of the fiscal position that is net of the impact of macroeconomic developments

on the budget. It involves an estimation of what revenues and cyclically adjusted expenditure

would be if the economy were at its potential. Figure-2.2 depicts general government cyclically

adjusted balance. Cyclically adjusted balance almost follow similar trend of overall fiscal balance

as depicted in Figure-2.1. The difference between the overall fiscal balance and cyclically adjusted

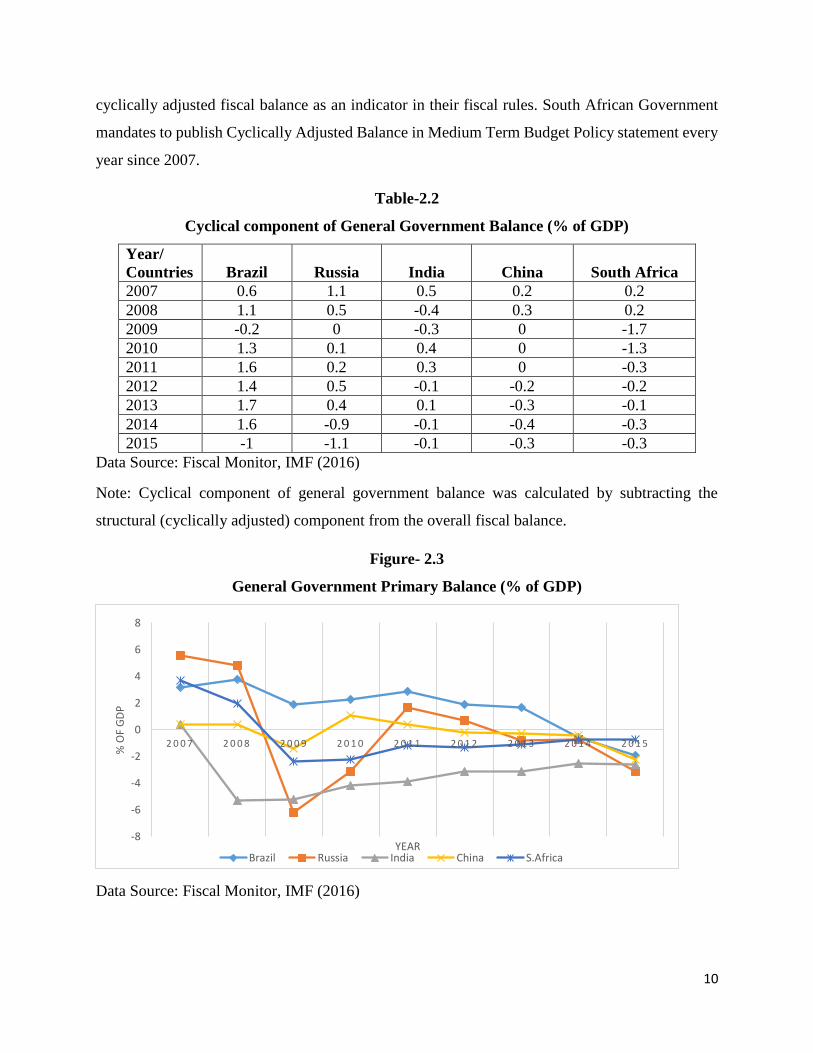

(structural) balance indicate the deficits/surplus aroused due to cyclical factors. Table-2.2 provides

the deficit/surplus aroused due to cyclical factors.

Table-2.2 clearly shows that cyclical component was the major factor which resulted in higher

deficits in 2009. Global economic slowdown in 2014 and 2015 can also be observed from Table-

2.2. It also clearly indicate that fiscal imbalance in India and China is more of structural in nature

than the cyclical one. Rao (2009) argue that deficit problem in India is structural in nature and not

attributable to cyclical factors. He further mentions that stimulus package provided by Indian

Government in 2009 through increased subsidies, rural development outlay, pay revisions etc were

mainly because of 2009 general election. Cyclical component was highest for Brazil followed by

Russia and South Africa. Some of the developed countries like Australia and Germany follow

-12

-10

-8

-6

-4

-2

0

2

4

6

2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5

% O

F G

DP

YEARBrazil Russia India China S.Africa

10

cyclically adjusted fiscal balance as an indicator in their fiscal rules. South African Government

mandates to publish Cyclically Adjusted Balance in Medium Term Budget Policy statement every

year since 2007.

Table-2.2

Cyclical component of General Government Balance (% of GDP)

Year/

Countries Brazil Russia India China South Africa

2007 0.6 1.1 0.5 0.2 0.2

2008 1.1 0.5 -0.4 0.3 0.2

2009 -0.2 0 -0.3 0 -1.7

2010 1.3 0.1 0.4 0 -1.3

2011 1.6 0.2 0.3 0 -0.3

2012 1.4 0.5 -0.1 -0.2 -0.2

2013 1.7 0.4 0.1 -0.3 -0.1

2014 1.6 -0.9 -0.1 -0.4 -0.3

2015 -1 -1.1 -0.1 -0.3 -0.3

Data Source: Fiscal Monitor, IMF (2016)

Note: Cyclical component of general government balance was calculated by subtracting the

structural (cyclically adjusted) component from the overall fiscal balance.

Figure- 2.3

General Government Primary Balance (% of GDP)

Data Source: Fiscal Monitor, IMF (2016)

-8

-6

-4

-2

0

2

4

6

8

2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5

% O

F G

DP

YEARBrazil Russia India China S.Africa

11

General Government primary balance of BRICS Nations is depicted in Figure-2.3. In the year 2007

all the BRICS economies have achieved primary surplus in the account. For all the BRICS

economies except Brazil primary surplus turned into deficits in 2009, following financial crisis.

Even though in deficit, there is an improvement in reducing primary deficit for India and South

Africa. The primary deficit of Russia and China has turned into surplus by 2011. However, in 2015

once again, primary balance has turned out as deficits for all the BRICS economies.

Figure-2.4

General Government Debt (% of GDP)

Data Source: Fiscal Monitor, IMF (2016)

Figure-2.4 depicts the general government debt level of BRICS economies from 2000 to 2015.

India has highest debt-GDP ratio among the BRICS economies. Debt level for India crossed 80%

of GDP in 2003. With the enactment of Fiscal Responsibility and Budget Management Act by

Central Government in 2003 and also by the State Governments in subsequent years enabled the

Indian government to reduce the debt level to an extent. Brazilian debt level closely follows India

in its trend and in the year 2015, Brazilian debt level surpassed India and reached almost 74% of

GDP. China and South Africa’s debt was below 30% and 40% of GDP respectively until 2008.

After the 2008 financial crisis, debt situation of both China and South Africa started worsening

and it reached almost 43% of GDP for China and 50% of GDP for South Africa. Russia has

witnessed considerable improvement in debt situation. Debt-GDP ratio which was at 55% of GDP

in 2000 has declined to around 16% of GDP for Russia in 2015.

0

10

20

30

40

50

60

70

80

90

2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 0 2 0 1 1 2 0 1 2 2 0 1 3 2 0 1 4 2 0 1 5

% O

F G

DP

YEARBrazil Russia India China S.Africa

12

When the debt situation of BRICS economies are compared with some of the advanced economies

like USA and Japan, BRICS nations have much better fiscal situation (in terms of debt). For

instance, the debt level of USA was 105.8% of GDP and for Japan debt level was as high as 248%

of GDP in 2015. However, one interesting difference between Japan and other emerging nations

are, Japanese Government holds large assets as well as debt and the debt is denominated in home

currency and the interest rates are very minimal. Wakatabe (2015) argue that the key to understand

Japan’s fiscal situation is the net debt as opposed to gross debt. The Japanese Government holds

large amount of assets, therefore the net debt relative to GDP ratio goes down to 132% as on June

2014 and the gross debt in that year was 245% of GDP. Bank of Japan holds large amount of

Japanese Government bonds. He further adds that, since the Central Bank could, in principle

forever hold its current stock of Japan Government bonds, the government need not to worry about

how it is going to repay these bonds. In this case net debt relative to GDP ratio goes even further

down to 80% of GDP.

Few BRICS economies have enacted and following rule based fiscal correction mechanism. Others

have initiated ‘fiscal rules’ to bring back fiscal situation under control after the 2008 crisis. Next

chapter discusses fiscal rules followed by the BRICS economies in detail and also compares the

existing rules amongst the BRICS nations.

13

Chapter-3

Fiscal Rules in BRICS Economies

Governments appear to be interested in FRLs for two related reasons: for an individual government

to control its impulses to run excessive deficits and for a group of governments in the same country

to make and enforce a mutual agreement that each of them would avoid running excessive deficits

(Webb, 2004). Liu & Webb (2011) lists out possible reasons for Governments to be interested in

drawing fiscal responsibility legislations. They are:

Short time-horizons of policymakers. A government may wish to institutionalize its commitment

to control its impulses to run excessive deficits, in order to resist temptation in more pressing times

that may come in the future.

Free riders: A group of governments in the same country may wish to make and enforce a mutual

agreement that each of them would avoid running excessive deficits. Individual governments’

interests would diverge from the common interest, however, in that factors such as electoral

pressures would motivate them to follow fiscal behavior that is risky or unsustainable.

Principal-agent and moral hazard problems: When citizens or a higher level of government (the

principal) entrusts a subnational government (agent) with resources and the responsibility to carry

out a task, then there is the principal-agent problem in assuring that the agent government will

maintain the requisite fiscal stability to carry out the task, without default or bailout. Sub-national

borrowers as agents have an incentive not to repay their lenders as principals because they perceive

that they will be bailed-out by the central government in case of default, resulting in moral hazard.

Demonstrating commitment to be creditworthy: Borrowers, including sub national governments,

have an incentive not to reveal negative characteristics about themselves to lenders, which results

in adverse selection. Lenders will therefore charge a risk premium above what is directly justified

by the revealed information, even for a borrower who is not risky. So the asymmetrical information

can lead to mispricing of risks. To improve its terms of borrowing, a government needs to show

creditors that it is fiscally responsible. It can demonstrate this commitment by constraining itself

with a FRL, its own or from the national level.

Rule based fiscal correction mechanism saw a momentum in 1990s. European Union counties

signed Maastricht Treaty in 1992 and agreed up on to maintain the fiscal deficit below 3% of GDP.

Since the 1990s many governments have intensified the search for mechanisms to escape from

14

fiscal populism that had been used as a strategy for winning elections and retaining public office.

National governments have tried various ways to avert these problems. One way has been to pass

a fiscal responsibility laws that prescribes proper fiscal behavior for sub national governments,

provides guidelines for parameters of sub national governments fiscal legislation, or sets incentives

and rewards for success or sanctions for failure in following the rules (Liu & Webb, 2011). A

‘Fiscal Rule’ imposes a long lasting constraint on fiscal policy through numerical limits on

budgetary aggregates. Fiscal rules typically aims at correcting distorted incentives and containing

pressures to overspend, particularly in good time, so as to ensure fiscal responsibility and debt

sustainability (Schaechter et al, 2012). As per Organization for Economic Cooperation and

Development (OECD) fiscal consolidation is a policy aimed at reducing government deficits and

debt accumulation.

This chapter briefly discusses the fiscal rules which exists in BRICS economies.

Brazil:

Brazil is a federal presidential constitution consisting of Federal Government, 26 States, one

Federal District and Municipalities. The municipalities are relatively autonomous. Municipalities

can enact their own constitution and is allowed to collect taxes and fees and also to maintain a

municipal police force. Goldfanj & Guardia (2003) observe that debt agreement signed by Federal

Government with State and local governments and introduction of Fiscal Responsibility Law in

2000 were the two most important changes in the Brazilian fiscal regime.

Debt agreement:

25 out of 27 States have signed debt restructuring agreements. As per the agreement, States have

refinanced their debts for 30 years with a fixed real interest rate of 6%. The Federal Government

has issued federal securities to redeem the existing State debts and became creditor to the States.

This bailout was followed by an explicit obligation for the States to commit themselves to an

agreed upon fiscal adjustment program, including an accorded path for the State debt. To receive

the benefits of the debt restructuring agreement, the States has to offer their own revenue and legal

revenue transfers from the Federal Government as a guarantee (Goldfanj & Guardia, 2003). In

case of a default, the contracts authorize the Federal Government to retain legal transfers or to

withdraw the amount due from the State’s own bank account. Furthermore, States failing to

15

comply will be denied of Federal Guarantee on new state borrowing and can incur interest penalties

on the rescheduled debt.

As per the agreement, minimum debt payment to Federal Government is equivalent to 13% of

states’ net revenue. Federal Government also restructured local government debt incurred before

May 2000. Federal Government took municipalities own revenue as a guarantee and required a

monthly payment equivalent to 13% of municipality’s net current revenue.

Fiscal Responsibility Law, 2000

Fiscal Responsibility Law (FRL), 2000 has set a general framework for budgetary planning,

execution and reporting for the three levels of Government. The law calls for sustaining the

structural adjustment of public finances and constraining public indebtedness. It comprises 3 types

of fiscal rules: general targets & limits for selected fiscal indicators; corrective institutional

mechanisms in case of non-compliance and institutional sanctions for non-compliance (Goldfanj

& Guardia, 2003).

Budget Guideline Law, as prescribed under FRL, 2000 is applicable to all three levels of

government and sets the rules and guidelines for budget preparation. According to FRL, the Budget

Guideline Law should fix a target for the primary surplus for the upcoming year and a reference

for the next two years. Primary surplus must be consistent with the debt caps fixed by a senate

resolution.

Brazil follows debt rule and expenditure rule. It covers general government and is statutory in

nature. In general Brazil’s FRL includes three types of fiscal rules (IMF, 2001). They are:

1. General targets and limits for selected fiscal indicators

2. Corrective institutional mechanisms in the case on non-compliance

3. Institutional sanctions for non-compliance

The FRL requires the preparation and dissemination of transparent fiscal reports. Presentation of

a fiscal policy annexure to the Government’s multi-year plan with multi-year fiscal targets.

Presentation of a fiscal targets annex to the Annual Budget Guidelines law with targets for primary

balance and projections for revenue, expenditure, nominal balance and the public debt for the

following three years. It should also require to include an annexure describing fiscal risks with an

assessment of contingent fiscal liabilities (IMF, 2001).

16

On the Revenues, the FRA mandates the withholding of discretionary federal transfers to States

and municipalities that do not collect effectively their own taxes.

On Expenditure, it requires that permanent spending mandates not to be created without

corresponding increases in permanent revenues or cuts in other permanent spending items and

bans new spending commitments that cannot be extended before the end of the incumbent’s terms

in office, as well as the recording of these as unspent commitments in the two quarters prior to end

incumbents’ terms in office, unless there are sufficient cash balances to cover them at end of fiscal

year. It also prohibits credit or rescheduling operations among the various levels of Government

to avoid the risk of intragovernmental bailouts (IMF, 2001).

Goldfanj & Guardia, 2000 notes that FRL, 2000 is based on two fundamental issues. The design

of a new fiscal federalism, aiming at maintaining fiscal discipline at subnational level and

prohibiting future bailouts. The maintenance of public sector solvency through the definition of a

legal target for the primary surplus consistent with debt sustainability.

Major rules prescribed under FRL are as follows (Bova et al, 2015 & Goldfanj & Guardia, 2000):

1. Personnel expenditure is limited to 50% of net current revenue for the federal Government

and 60% for States & municipalities.

2. Permanent spending mandates cannot be created without permanent revenue increase or

spending cuts.

3. Senate sets debt limits for all levels of Government. However, there was never an

agreement reached on the limit for Central Government; thus the only limits currently in

place are for States & municipalities.

4. The Government sets numerical multiyear targets for the budget balance (for the current

year & indicative targets for next two years), expenditure & debt.

5. The case on non-compliance, corrective measures need to be taken and can result in

sanctions (the fiscal crimes law details penalties for mismanagement ranging from fines to

loss of job)

6. Escape clauses exist for exceptional economic conditions and natural disaster but can only

be invoked with congressional approval.

7. There is also the ‘golden rule’ principle set in the Constitution (new borrowings should be

at must equal to public investment).

17

8. Public finance institutions at all levels of government are not allowed to lend to their main

shareholders.

9. Spending commitments that exceed one budgetary period during the last year of a political

term of office are prohibited.

10. Tax benefits should be included in the annual budget together with the instruments to offset

their impact on the budget for two consecutive years.

11. Changes in monetary or exchange rate policy affecting fiscal performance will trigger an

extension in time limit for debt adjustment.

12. Sanctions for misbehavior range from withholding federal voluntary transfers to denial of

credit guarantees or banning of new debt.

13. Personal responsibility applies to all public officials. A fiscal crime law details penalties

for mismanagement, ranging from fines to loss of job and ineligibility for public office for

a maximum of 5 years, to imprisonment.

FRL also enshrines fiscal transparency as a key component of new framework. Proposals, laws

and accounts are to be widely distributed. FRL also requires all levels of Governments to publish

a quarterly fiscal management report that contains the major fiscal variables and indicates

compliance with fiscal targets.

One of the distinguished and unusual feature of Brazil’s FRL is ‘Fiscal Crime Law’. It is a

companion law to FRL which specifies criminal penalties like fines and even jail for officials who

violate the rules. The fiscal crime law applies to public officials of all branches of government at

all levels. Among other provisions, the fiscal crime law provides for detention of up to four years

for a public official who engages in credit operations without prior legislative authorization, incurs

unauthorized expenditure commitments (including any in the last two quarters in office that cannot

be repaid during the present term of office), extends loan guarantees without collateral of equal or

higher value, increases personnel expenditures during the final 180 days of the term of office, or

issues unregistered public debt (Liu & Webb, 2011). An example of this nature in recent past is

impeachment of Dilma Rousseff, former President, Brazil. Leahy (2016) claims that contrary to

popular perception, Ms. Rousseff was on trial not for a vast corruption scandal at Petrobras, the

state-run oil company she once led, or for the country’s terrible economy, which shrunk by 3.8 per

cent in 2015. Instead, she was under scrutiny over arcane fiscal maneuvers her government

18

allegedly used to pump up the economy and disguise a deficit in the public accounts. This creative

accounting, known as “pedaladas” Portuguese for pedalling has allegedly helped her to win the

2014 elections by disguising the true state of the economy.

With the FRL in place, Brazil could achieve better economic growth, reduced fiscal deficits and

debt. However, year 2009, 2014 and 2015 are the exceptions to the trend of healthy fiscal behavior.

India:

Indian economy was under severe economic imbalance in terms of low economic growth, high

inflation, worsening balance of payments and escalating fiscal deficits. Government of India

initiated economic reforms in 1991 by opening up of the economy for private investments and

significant structural changes in the economy has been taken place. Despite many reforms, fiscal

deficits were at very high level. Political inconsistency, pay revision, military spending due to

Kargila War in 2000 etc lead to higher fiscal deficits both for Central and State Governments in

late 90s and also in early 2000.

A high level committee to frame ‘Fiscal Responsibility Legislation’ was set up by the then Finance

Minister, GoI, under the chairmanship of Dr. E A S Sarma, then Secretary, Economic Affairs

Department. The Committee submitted its report to the Finance Minister on 4th July 2000. The

Committee observed that the wide spread deterioration in the fiscal position with its associated

impact on fiscal sustainability, macroeconomic vulnerability and economic growth has led to an

emerging consensus about the urgent need for imposing statutory ceiling on Central Government’s

borrowings, debt and deficits. Thus, after several years of deliberations, the Government of India

introduced rule based fiscal mechanism called the Fiscal Responsibility and Budget Management

Bill in December 2000. After series of discussions FRBM Act was passed in the year 2003 and

implemented from the year 2004.

FRBM Act, 2003 prescribes the following:

1. Central Government shall lay in each financial year before both the Houses of Parliament

the following statements of fiscal policy:

a. The Medium Term Fiscal Policy Statement

b. The Fiscal Policy Strategy Statement

c. The Macroeconomic framework Statement

19

2. Medium term fiscal policy statement shall set forth three-year rolling targets for prescribed

fiscal indicators namely fiscal deficit, revenue deficit and liabilities. The statement shall

include assessment of sustainability relating to balance between revenue receipts and

revenue expenditure and the use of capital receipts including market borrowings for

generating productive assets.

3. Fiscal Policy strategy statement shall include policies of Central Government for ensuing

financial year relating to taxation, expenditure, market borrowings and other liabilities,

lending and investments, pricing of administered goods and services etc. Strategic priorities

for ensuing year, rationale for any major deviation from key fiscal measures pertaining to

taxation, subsidies, administered pricing and subsidies.

4. Macroeconomic policy statement shall contain an assessment of GDP growth, fiscal

balance of Union Government as reflected in revenue balance and gross fiscal balance and

external sector balance as reflected in current account balance of the balance of payments.

5. Reduce fiscal deficit to be 3% of GDP and revenue deficit to be nil by 31st March 2008 and

build revenue surplus thereafter. The target date was postponed later to 31st March 2009.

6. Central Government should specify annual targets for assuming contingent liabilities in the

form of guarantees and the total liabilities as % of GDP.

7. Central Government shall not borrow from Reserve Bank of India except by way of

advances to temporarily meet cash imbalances.

8. Central Government should take measure to ensure greater transparency in fiscal

operations and minimize secrecy.

9. Deficit target may exceed in exceptional cases like on the grounds of natural calamity,

national security and other cases as may specified by the Central Government.

Following the Central Government, many state governments enacted fiscal responsibility laws.

Karnataka was the first state to enact fiscal responsibility act, even before the Central Government.

There are few schemes which incentivized and also obliged the state governments to enact fiscal

responsibility legislations. They are:

1. Fiscal Reforms Facility: Pursuant to the recommendations of the Eleventh Finance

Commission, Government of India created a Fiscal Reforms Facility (FRF) for

incentivizing the states to undertake Medium Term Fiscal Reforms Program (MTFRP) for

20

fiscal consolidation. The state governments were asked to draw up MTFRP incorporating

time-bound action points on fiscal objectives and reforms, power sector reforms, public

sector restructuring and budgetary reforms. FRF envisaged that if the state on an average

achieves a five percentage point reduction in revenue deficit as percentage of revenue

receipts consistently each year, by the year 2005-06 the sector as whole would come into

revenue balance. An incentive fund was created and release of it was based on single

monitorable fiscal objective as mentioned above.

2. Debt Swap Scheme: Government of India formulated a Debt Swap Scheme (DSS) realizing

the mounting burden of interest payments on the states and supplement their effort towards

fiscal management. The scheme was in operation from 2003-03 to 2004-05. The scheme

capitalized on the current low interest regime, to enable states to prepay expensive loans

contracted from Government of India, with low coupon bearing small savings and open

market loans. This scheme covered outstanding high cost loans with interest rate of 13%

and above.

3. Debt Consolidation and Relief Facility: The general debt relief with reschedule and lower

interest rate shall be available to States with effect from the year they enact FRBM

legislation which shall contain some core elements as recommended by Twelfth Finance

Commission. The Twelfth Finance Commission has also framed a scheme of debt waiver

based on fiscal performance linked to the reduction of revenue deficit and control of fiscal

deficit of the states. The quantum of debt write-off of the repayment was linked to absolute

amount by which the revenue deficit has reduced in each successive years during the award

period. If the revenue deficit brought down to zero, the entire repayment during the award

period of Twelfth Finance Commission will be written off.

All these measures by the Central Government incentivized the state governments to enact the

fiscal responsibility laws. Combined fiscal deficit of center and state government (general

government fiscal balance) got reduced from as high as 9% of GDP in early 2000s to around 4%

of GDP in 2007-08. There was a pause to FRBM roadmap after the 2008 financial crisis and it

resumed after few years. Presently, Central Government has a target to bring back fiscal deficit to

less than or equal to 3% of GDP by end of March 2018. 14th Finance Commission has incentivized

the states’ fiscal efforts by providing a flexibility in fiscal deficit target by 0.5% of GSDP if state’s

21

debt to GSDP ratio is below 25% and interest payments to revenue receipts ratio is below 10% in

the preceding year.

China:

China is one of the fastest growing nations in the world. As elaborated in Chapter-1, China’s

economic growth and per-capita income has grown tremendously in last two and half decade.

China is also forefront in balancing fiscal indicators. It has very low fiscal deficits and debt when

compared to many developed nations and also amongst the BRICS economies. China has not

formally enacted any Fiscal Rule. However, there are several developments which contributed to

better fiscal situation of China and in recent years Chinese Government have taken a step towards

fiscal responsibility.

Constitution of China mentions three levels of administrative structure namely provincial, county

and townships. However broad classification specifies five levels of administrative structure and

they are as follows:

1. Provincial level: It includes provinces, autonomous regions, municipalities and special

administrative regions.

2. Prefectural level: It consist prefectural level cities, autonomous prefectures and leagues.

3. County level: It includes counties, districts and autonomous counties.

4. Township level: it includes towns, townships, sub districts etc.

5. Village level

Hou (2016) explains China’s fiscal reforms under three stages. First stage is from 1979 to 1993.

Second stage is from 1994 to 2008 and third stage starts after 2008. In the first stage there were

structural readjustments taken place to promote growth and development. The reform was to

decentralize revenue and outlays from center to provinces. Another important reform was to

relieve individuals from grip of the state so that laborers could make their own living and can work

hard with their skills. In urban areas, the reforms gave rise to family businesses and in rural areas

22

farmers grew crops they wanted. But these reforms resulted in serious problems. Revenues for the

government started shrinking and reform also caused income disparities and regional disparities.

Second stage was innovation towards new fiscal system. In the second stage, policy innovations

were introduced to build a new fiscal system in accord with the generic principles of public finance,

thereby solving the problems that occurred in the first stage. The goal of the new fiscal structure

was to finance the opportunity for equal access to basic public services for every citizen regardless

of their location of residence or type of household registration (Hou, 2016). A separate central

versus local tax system was introduced. Centre collected a larger share of taxes including value

added tax and personal income tax. Remaining taxes were distributed among the provinces and

local governments. New fiscal transfers system particularly for basic services has been introduced.

In the initial stage, this system has demonstrated substantial impact on transfers related to

education, public health, social security etc.

However, this system created serious problem more than what has been faced in the first stage.

Tax revenue was heavy at center but responsibilities are more for the local governments. Revenue

and responsibilities did not match between different levels of government. Hou (2016) further adds

that local officials are incentivized to fulfil all tasks set by their superior levels, because they are

appointed by their bosses – thus “career considerations have driven most top local officials to

resort to informal, even illegal means of financing for infrastructure and development, including

selling the use right of state land for cash and borrowing huge sums via local financing vehicles”.

The hidden borrowing, has piled up long-term liabilities that in some cases are multiple times over

annual local revenue.

There are two additional reforms took place in the second stage and they are: framing of Budget

Law of China in 1995 and 1999 Budget Reforms. Budget Law of 1995 forbids sub-national

governments from borrowing in financial markets without approval of State Council. However

this measure, as mentioned earlier lead to more off-budget borrowings. Liu (2010) argue that the

off-budget borrowings has supported large-scale urban infrastructure in China. He further adds

that the off-budget financing has not only expanded the financial resources, but also facilitated the

development of competitive land and housing markets.

The 1999 Budget Reform consists of three components. They are:

a. Departmental Budget Reform: As per this reform, budget will be compiled on a

departmental basis. The government budget was previously divided along functional lines,

23

such as education and agricultural sectors etc. A number of government departments

performing similar functions formed an appropriation cohort; budget compilation was

based on the needs of this cohort rather than individual departments. Under the new

arrangement, the budget is organized on a departmental basis whereby individual

government departments submit their budget requests in the form of a simple table to the

budget agency (Wu, 2014). The budget agency will decide upon the request. It was

expected that budgeting on a departmental basis can improve the “accountability within

the bureaucracy” and enhance allocative and operational efficiency in public finance. Zero

based budgeting was incorporated in place of incremental budgeting. This reform was also

aimed at reducing non-budgetary financing.

b. Treasury Management Reform: only a single treasury account system is allowed to operate

at each level of governments. Individual department cannot hide their revenues and

expenditures from the budget agency.

c. Government Procurement Reform: Aiming at corruption control and increasing operational

efficiency, a centralized procurement system was introduced.

Third stage of China’s reforms is towards achieving efficiency and accountability. New Budget

Law of China was passed in 2014 and became effective on 2015. The 2015 Budget Law of China

revised old law in five major areas and they are:

1. Transparency: 2015 Budget Law stipulates the government that all revenues and outlays

must be included in the government budget. The official report and account schedules on

all the budgeted items, adjustments, final approved amounts and details on implementation

of budget, arrangements for transfers and debt use should be made public by Finance

Ministry within 20 days of approval of People’s Congress (Hou, 2016).

2. Budget Stabilization Fund: In boom years when current revenue exceeds the budget, extra

amount should be placed in the stabilization fund. It is applicable to all levels of

government.

3. Local Government Debt: Old law require local governments to achieve annual balance and

does not allow localities to incur any deficits. The new law allows the local governments

to borrow by imposing following restrictions:

a. Only provincial governments, with prior approval by the State Council, can incur debt.

24

b. Government debt can be used only for capital outlay that produces public

goods/services.

c. The amount of debt for each province should be submitted by the State Council to the

National People’s Congress or its Standing Committee for approval. Each province can

only borrow within the approved limit with the approval of the standing committee of

the provincial people’s congress.

d. The method of borrowing can be only via issuing local government bonds, not any

other means or venues.

e. To control risk related to and rising from local government borrowing, any issue of

provincial government bonds should have a matching debt service plan and stable

source of revenue for debt retirement. The State Council shall set up a risk evaluation

and warning mechanism of local government debt, an emergency management

mechanism, and accountability system.

4. Central-Local Fiscal Transfers: Law intends to promote equalization between regions.

Transfers will consist of equalization grants and special purpose transfers. Higher level of

Governments should notify the lower levels their estimates of transfers ahead of local

governments’ budget preparation. All the local governments should include these estimates

in their budget.

5. Hard Budget Constraint: Governments should not seek any revenue reduction policies or

measures in middle of the fiscal year.

Chinese Government has announced adoption of Medium Term Fiscal Plan (MTFP). The MTFP

should consists of:

a. Forecasts of major economic indicators and socio-economic status in the next three years

considering domestic and international economic scenario. Based on economic forecasts,

estimates of the mid-term revenues and outlays in accord with current macroeconomic

policies should be presented in the document.

b. Analyze the issues with existing policies on revenue sources and outlay priorities

c. Compose reform plans on revenue and outlay: (1) Regarding revenues, the Ministry of

Finance shall consult with the Tax, Customs, and Development Ministries to propose

routes and timelines for tax reform, major revenue adjustments, regulation of fees/charges,

25

with clear policy goals and implementation schedule. These ministries should also evaluate

the impact of the proposed policies on the economy, related industries, and tax burden of

individuals. (2) Regarding outlays, the Ministry of Finance shall consult relevant agencies

to outline major reforms within the MTFP period, policies and projects of outlays, specify

policy goals, list annual tasks and deadlines, with clarifications on performance measures.

(3) Regarding governmental debt, the Ministry of Finance shall, based on revenue and

outlay and debt risk forecasts, determine appropriate scope of deficits and debt limits as

risk control target. Classify debts and place them into the budget. Establish debt risk

warning and emergency management mechanisms.

d. Estimate revenues and outlays in the next three years after implementing the proposed

reforms, and conduct overall balance.

China has lowest fiscal deficits among the BRICS economies as on 2015. Even the debt level is

less, amounting 40% of GDP in 2015.

South Africa:

Fiscal reforms in independent South Africa has been articulated through two most important

macroeconomic programs namely the Reconstruction and Development Program (RDP) in 1994

and the Growth, Employment And Redistribution (GEAR) strategy in 1996. The fiscal reform was

consistent over time covering three broad areas that are: budget and financial management reform,

creation of the intergovernmental fiscal system and tax policy and administration reforms (Ajam

& Aron, 2007). These initiatives was supported by Public Finance Management Act of 1999. This

Act formally established the ‘National Treasury’ by amalgamating the former Departments of

Finance and State Expenditure. This Act emphasized regular financial reporting, sound internal

expenditure controls, independent audit and supervision of control systems, improved accounting

standards and training of financial managers and greater emphasis on outputs and performance

monitoring.

Budget and Financial Management Reforms: Fiscal data need to be regularly published in the

Budget Review and Intergovernmental Fiscal Reviews. The Medium Term Budget Policy

Statement (MTBPS) was introduced in 1997 and is being regularly published every year. The

MTBPS is a government policy document that communicates the Parliament and the country the

26

economic context in which the forthcoming budget will be presented along with fiscal policy

objectives and spending priorities over the three year expenditure period. It need to be tabled at

least three months before the national budget is presented (SAG, 2016). MTBPS should include

the following:

1. A revised fiscal framework for the current financial year and the proposed fiscal framework

for the next three years.

2. An explanation of the macroeconomic and fiscal policy position and macroeconomic

projections and assumptions underpinning the fiscal framework.

3. Spending priorities of the government for next three years.

4. Proposed division of revenue between national, provincial and local governments.

5. A review of spending by each national department and each provincial government

between 1st April and 30th September of the current financial year.

A new budget and reporting formats was introduced in 2004, aligned with international Public

Sector Accounting Standards.

Intergovernmental Fiscal Relations: Creation of the Budget Council in 1996 is a landmark step to

strengthen intergovernmental fiscal relations. Other important steps were establishing formula

based revenue sharing based on recommendations of Financial and Fiscal Commission and

promulgation of Intergovernmental Fiscal Relations Act, 1997 which introduced predictability and

transparency into the intergovernmental budget process (Ajam & Arom, 2007).

Tax Policy and Administration Reforms: It has greatly contributed to broadening the tax base and

enhancing the revenue collection efficiency. An autonomous revenue service known as South

African Revenue Service (SARS), combining Inland Revenue and Customs and Excise

Department was created (Ajam & Arom, 2007). It raised audit capacity through introduction of

computerized systems, enhanced capacity to investigate and prosecute tax evaders and improved

debt recovery procedures.

The South African Government has not formally enacted legislative constraints on fiscal variables.

In mid and late 90s, authorities have maintained tight fiscal position, despite political pressure.

However, in 1994 South African Government announced a targeted reduction in budget deficit to

2.5% of GDP over five years, cuts in non-interest expenditure and constant revenue of 25% as a

27

share of GDP. Introduction of GEAR, SARS and framing of Public Finance Management Act in

1999 have together contributed to reduction in fiscal deficit to as low as 1.1% of GDP in 2002-03

(Ajam & Arom, 2007). Expenditure cuts continued to focus on the wage bill, with cuts in civil

service employment.

These reforms also had several negative impact on fiscal sharing. Revenue rising power in South

Africa is highly centralized in nature, whereas provincial governments have higher spending

responsibilities. This resulted in vertical imbalance. The provincial governments face significant

expenditure mandates and have restricted own financial resources. After deducting interest

obligations and statutory payments from total revenue collected, the balance will be equitably split

up among the three spheres of government (Ajam & Arom, 2007).

South Africa’s fiscal balance is at favorable position. Its primary deficit is lowest among the

BRICS economies. Its debt was less than 40% of GDP between 2000 and 2008. There is an

increase in the debt and fiscal imbalance after the 2008 financial crisis. Despite not having any

legislated numerical fiscal rule South Africa’s fiscal situation is well under control.

Russia:

Russia is an oil rich nation. Its budget, exports and structure of the economy is highly dependent

on the oil and gas sector. Since late 90s to 2007, Russia enjoyed prudent fiscal balance with

surpluses, declining debt and rising reserves accumulated in the Stabilization Fund. Russia in the

same period, introduced many fiscal management innovations like treasury management of the

budget, a Medium Term Fiscal Framework (three year targets), oil revenue management fund etc.

the oil stabilization fund was split into the Reserve Fund and a National Welfare Fund which will

accumulate oil revenues beyond the Reserve Fund maximum of 10% of GDP (Bogetic et al, 2010).

Oil revenue as percent to general government revenue has increased from less than 10% in 1997

to more than 30% in 2007.

The Balance Budget Rule was framed in 2007-08. Russia’s legal fiscal framework relies mainly

on non-oil balance as a key fiscal indicator. The budget included non-oil fiscal deficit target of

4.7% of GDP. This was suspended in April 2009 as a result of 2008 financial crisis and formally

abolished in 2011 (Bova et al, 2015).

28

Since 2013, Russian Government is following the Expenditure Rule. Russian Parliament adopted

a new-oil price based fiscal rule in December 2012. The rule sets a ceiling on expenditures. Oil

revenues above the ‘base’ oil price need to be saved in the Reserve Fund until it reaches 7% of

GDP. Once the Reserve Fund reaches the threshold, at least half of the oil revenues should go to

National Wealth Fund and remaining revenues would be channeled to the budget to finance

infrastructure and other priority projects. This rule uses a five year backward looking average of

oil prices as a base, which will be gradually increased to 10 years by 2018 in order to avoid abruptly

moving to a very low base oil price (Bova et al, 2015).

The multiyear framework was suspended in 2015. The Government aims to resume it in 2017

budget. To adjust to the new reality of lower oil prices, Russian Government is considering a broad

range of fiscal consolidation measures including pension reform, improving capital budgeting,

cutting subsidies and improving tax collections (IMF, 2016). The IMF country report-16/229 says

that Government is considering to reintroduce the fiscal rule once the fiscal adjustment is

completed based on fixed oil price of US$40 or US$50 per barrel depending on the authorities

assessment of long-term average oil prices to smooth the impact of oil price cycles on public

finances, domestic demand and real exchange rate. The IMF country report also noted that a more

flexible oil price rule, which sets an oil benchmark that incorporates future oil prices in its

calculation. This would help to avoid suspending the fiscal rule when faced with pressures of

drastic oil price fluctuations (IMF, 2016).

Fiscal Rules in BRICS Economies: A comparison

India, Brazil and Russia follow legislated numerical fiscal rules. In India, targets are fixed on fiscal

and revenue deficits and liabilities. In Brazil, ceilings have been imposed on the expenditures,

particularly the personnel expenditure. Non-oil fiscal balance is the target fiscal variable in Russia.

Brazilian Fiscal Responsibility Law applies to the general government. Brazil’s FRL is peculiar in

several aspects like fiscal crimes law. In India, Center and State Governments have separate FRLs.

The FRLs in Brazil and India has significantly contributed in reducing deficits and debt. The fiscal

rules in India and Brazil are based on ‘Golden Rule’ which suggests to use the borrowings only

for capital formation.

China and South Africa do not follow any numerical fiscal rules and instead they follow procedural

rules. In recent years Chinese Government is stressing the transparency aspect of fiscal rule (which

29

already exists among other BRICS economies). The Budget and Financial Management reforms

have helped to strengthen the South Africa’s fiscal condition. All the BRICS nations presents and

also follows Medium Term Fiscal Plans.

Chapter-4

Conclusion

Brazil, Russia, India, China and South Africa (BRICS) are grouped as emerging economies and

these countries are fastest growing in the world. There was tremendous improvements in output

growth and per capita income growth for these nations over the last two decades. The recent 2008

financial crisis adversely affected many economies in the world and the BRICS countries are not

an exception.

This study has analyzed and compared the developments in fiscal policies/indicators for last two

decades and in particular, post crisis period comprehensively. It was found that favourable fiscal

balances (surpluses and smaller deficits) has turned out to be huge deficits after the 2008 crisis.

Consequently the debt level started peaking up. India has highest fiscal deficits and debt and also

lowest revenues and expenditure as proportion to GDP amongst the BRICS economies. There

should be efforts by Indian Government to rise the revenue-GDP ratio. The expected rollout of

Goods and Service Tax in July 2016 may help in raising the revenue ratio in the coming years.

China has the least deficits and debt when compared to other BRICS nations. In 2014-15, due to

global economic slowdown there was a crisis again in the fiscal balance of Brazil and Russia. The

Russian economy is highly dependent on oil for revenue as well as exports. The oil price

fluctuations determine Russia’s fiscal balances. It was also found that vertical fiscal imbalance is

a major problem for China and South Africa, as the Center has more revenue raising powers

whereas lower level of governments have higher spending responsibilities.

Fiscal rules have played very important role in keeping fiscal variables under control. Amongst

the BRICS, Brazil is the first country to enact a Fiscal Responsibility Legislation in the year 2000.

This rule applies to all levels of government. Brazil’s Fiscal Responsibility Law (FRL) is very

strict and it even specifies penalties and sometimes imprisonment for mismanagement of

government funds.

30

India enacted FRBM Act in 2003 and at subnational level, State Governments have enacted their

own FRLs. Framing of FRLs at subnational level was incentivized and promoted by the Central

Government through several schemes like Debt Swap Scheme, Fiscal Reform Facility and Debt

Consolidation & Relief Facility. With the help of FRLs and favourable economic condition both

Centre and State Governments in India could reduce their deficits below threshold of 3% of GDP.

The State Governments efforts in reducing fiscal deficits are remarkable.

Russian Government has framed Balanced Budget Rule (BBR) in 2007-08. Government has

adopted non-oil fiscal balance as target fiscal indicator. However BBR was removed in 2012 owing

to 2008 financial crisis. Since 2013 Russian Government is following ‘Expenditure Rule’. South

Africa and China do not follow any legislated budget constraints. However, Medium Term Fiscal

Plan was adopted by both the nations. In recent episodes, Chinese Government is stressing on the

fiscal transparency aspect.

Overall, this study finds that fiscal position of BRICS nation was in good shape before 2008 crisis.

Aftermath the crisis, these indicators turned out to be negative. China’s fiscal performance even

in crisis period was remarkable. Numerical fiscal rules has worked to an extent for Brazil and

India. All the BRICS nations presently emphasizes on procedural rules and fiscal transparency

implying their path towards sustainable fiscal balance.

31

Bibliography:

Ajam, T., & Janine, A. (2007). Fiscal Renaissance in a Democratic South Africa. Journal of

African Economies, 16(5), 745-781.

Aslund, A. (1999). Why has Russia's Economic Transformation been so Arduous. Annual World

Bank Conference on Development Economics, Washington D C. Washington D C: The

World Bank. Retrieved March 30, 2017, from

http://siteresources.worldbank.org/DEC/Resources/84797-1251813753820/6415739-

1251814010799/aslund.pdf

Bogetic, Z., Smits, K., Bubina, N., & Wijnbergen, S. V. (2010). Long Term Fiscal Risks and

Sustainability in an Oil-rich Country- The Case of Russia. World Bank Policy Research

Working Paper-5240.

Bova, E., Kinda, T., Muthoora, P., & Toscani, F. (2015). Fiscal Rules at a Glance. Washington D

C: International Monetary Fund.

ECB. (2016). Economic Bulletin- Issue 1. Franfurt: European Central Bank.

GoI. (2009). Union Budget 2009-10 Budget Speech. New Delhi: Ministry of Finance, Government

of India.

GoI. (2012). The BRICS Report. New Delhi: Oxford University Press.

GoI. (2017, March 28). BRICS India 2016. Retrieved from brics2016.gov.in:

http://brics2016.gov.in/content/innerpage/about-usphp.php

Hou, Y. (2016, April 27). Interpreting China's Fiscal Reforms and the 13th Five year Plan Targets.

Retrieved from US-China Economic and Security Review Division:

https://www.uscc.gov/sites/default/files/Yilin%20Hou_Written%20Testimony%2004271

6.pdf

IMF. (2001). Brazil: Report on Observance of Standards and Codes (ROSC)- Fiscal Transparency

Module. Washington D C: International Monetary Fund.

IMF. (2016). Fiscal Monitor: Acting Now, Acting Together. Washington D C: International

Monetary Fund.

IMF. (2016). Russian Federation- IMF Country Report- 16/229. Washington D C: International

Monetary Fund.

Liu, L. (2010). Strengthening Subnational Debt Financing and Managing Risks. Beijing: Review

of Economic Research, Ministry of Finance, Government of China.

32

Liu, L., & Webb, S. B. (2011). Laws for Fiscal Responsibility for Subnational Discipline-

International Experience. World Bank Policy Research Working Paper-5587.

MGI. (2015). Debt and (not much) Deleveraging. McKinsey Global Institute.

Morrison, W. M. (2015). China's Economic Rise: History, Trends, Challenges and Implications

for UNited States. Washington D C: Congressional Research Service. Retrieved March 31,

2017, from https://fas.org/sgp/crs/row/RL33534.pdf