Embed Size (px)

DESCRIPTION

Ceri Presentation 2015 Petrochemical conf

Citation preview

What Are We Going To Do With All

These NGLs ?

Presented to

The CERI 2015 Petrochemical ConferenceKananaskis, Alberta

June 8, 2015 Gas Processing Management Inc. 1

Gerry Goobie, P.Eng.

Dave Tulk, P.Eng.

Gas Processing Management Inc.

Just What The *&#% Is Going On

With Propane ?

Presented to

The CERI 2015 Petrochemical ConferenceKananaskis, Alberta

June 8, 2015 Gas Processing Management Inc. 2

Gerry Goobie, P.Eng.

Dave Tulk, P.Eng.

Gas Processing Management Inc.

Just What The *&#% Is Going On With Propane?

• Edmonton propane has been priced at

less than shrinkage value since the

beginning of 2015 !

• Edmonton propane prices have been

negative for the last several weeks !

• Are we swimming in propane ?

• Is there a Petrochemical opportunity ?

• What about West Coast exports ?

• How serious is this ?

June 8, 2015 Gas Processing Management Inc. 3

Presentation Outline

• GPMi Introduction

• Canadian and U.S. NGL Production

• Recent Prices and Margins

• How Bad Is It?

• What Will Happen Next?

• Disposition Options

• Petrochemical Opportunity

• Conclusion

June 8, 2015 Gas Processing Management Inc. 4

Presentation Outline

• GPMi Introduction

• Canadian and U.S. NGL Production

• Recent Prices and Margins

• How Bad Is It?

• What Will Happen Next?

• Disposition Options

• Petrochemical Opportunity

• Conclusion

June 8, 2015 Gas Processing Management Inc. 5

Gas Processing Management Inc.

• For 15 years, GPMi has been delivering industry leading

solutions to the Business of Energy Infrastructure – Worldwide!

• Over 400 man years of hands-on front line Senior Management

and Executive Level Experience in the Natural Gas, NGL and

Petrochemical industries

• Areas of Expertise

• www.gasprocessing.com

June 8, 2015 Gas Processing Management Inc. 6

NGLs Petrochemical Gas & LNG Other

• Supply

• Demand

• Markets

• Pricing

outlooks

• Netbacks

• Infrastructure

Development

• Regulatory

• Feedstock

• Ethylene business

development &

infrastructure

• New plant economics

• “Alberta Advantage”

• Processing Fees &

negotiation

• Gas plant operations

• Unconventional gas

infrastructure

development

• Sour gas processing

• JV agreement

development, negotiation

& related services

• Strategic planning for natural gas, LNG

and NGL infrastructure

• Acquisitions & divestitures

• Mediation, arbitration & expert witness

testimony

• Knowledge transfer & mentoring

• Facility evaluation & economic analysis

• Infrastructure development &

project/commercial management

• Contract negotiation

Who Is GPMi ?

June 8, 2015 Gas Processing Management Inc. 7

A bunch of cranky old guys who have spent their

careers in the gas, NGL and petrochemical

industries but don’t want to retire!

Presentation Outline

• GPMi Introduction

• Canadian and U.S. NGL Production

• Recent Prices and Margins

• How Bad Is It?

• What Will Happen Next?

• Disposition Options

• Petrochemical Opportunity

• Conclusion

June 8, 2015 Gas Processing Management Inc. 8

Current Situation

• The development of

unconventional petroleum

resources has glutted North

American natural gas and NGL

markets

• Price relationships have

changed

• The situation has deteriorated

sharply in recent months

• North American gas and NGL

markets are demand

constrained

June 8, 2015 Gas Processing Management Inc. 9

U.S. NGL Production

• U.S. NGL production

growth is driven by rich

gas developments in the

Marcellus, Utica, Eagle

Ford and other plays

• Total C2, C3 & C4

production has increased

by about 1.5 million bpd

since 2009

• Ethane production

growth has been

constrained awaiting new

petchem demand

– Up to 500 kbpd is being

rejected

June 8, 2015 Gas Processing Management Inc. 10

Source: US EIA

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

kbpd U.S. NGL Production

Ethane Propane n-Butane i-Butane

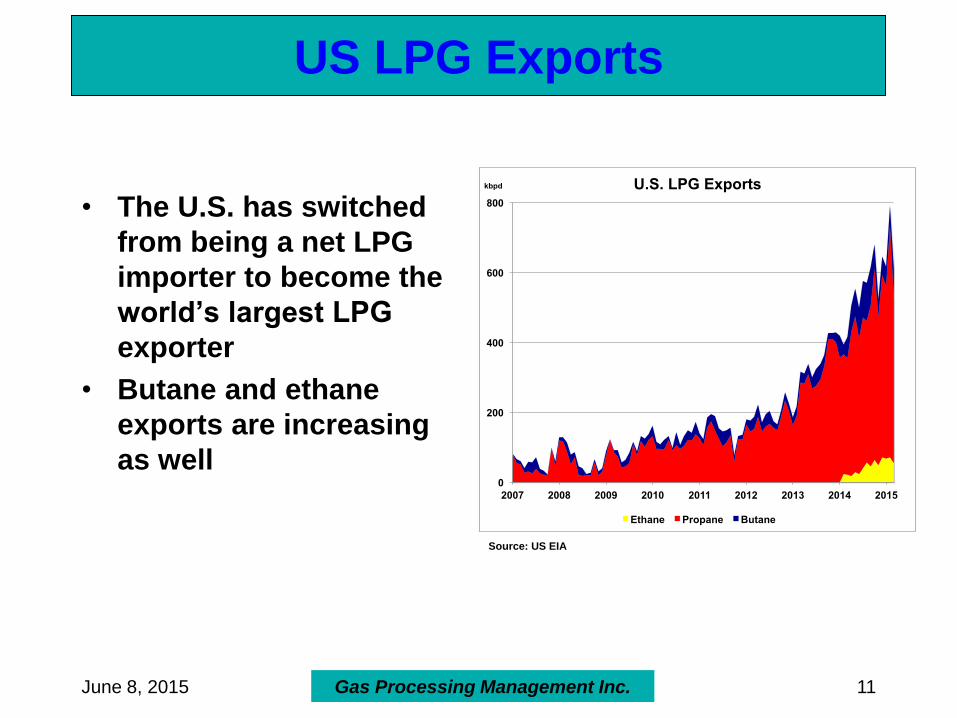

US LPG Exports

June 8, 2015 Gas Processing Management Inc. 11

• The U.S. has switched

from being a net LPG

importer to become the

world’s largest LPG

exporter

• Butane and ethane

exports are increasing

as well

Source: US EIA

0

200

400

600

800

2007 2008 2009 2010 2011 2012 2013 2014 2015

kbpd U.S. LPG Exports

Ethane Propane Butane

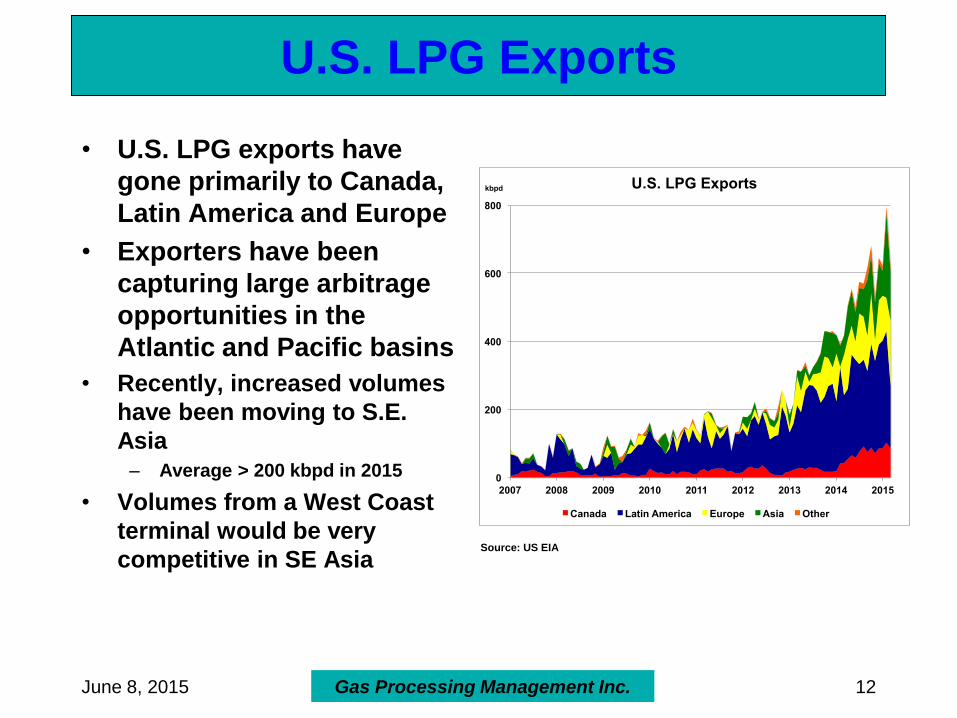

U.S. LPG Exports

• U.S. LPG exports have

gone primarily to Canada,

Latin America and Europe

• Exporters have been

capturing large arbitrage

opportunities in the

Atlantic and Pacific basins

• Recently, increased volumes

have been moving to S.E.

Asia– Average > 200 kbpd in 2015

• Volumes from a West Coast

terminal would be very

competitive in SE Asia

June 8, 2015 Gas Processing Management Inc. 12

Source: US EIA

0

200

400

600

800

2007 2008 2009 2010 2011 2012 2013 2014 2015

kbpd U.S. LPG Exports

Canada Latin America Europe Asia Other

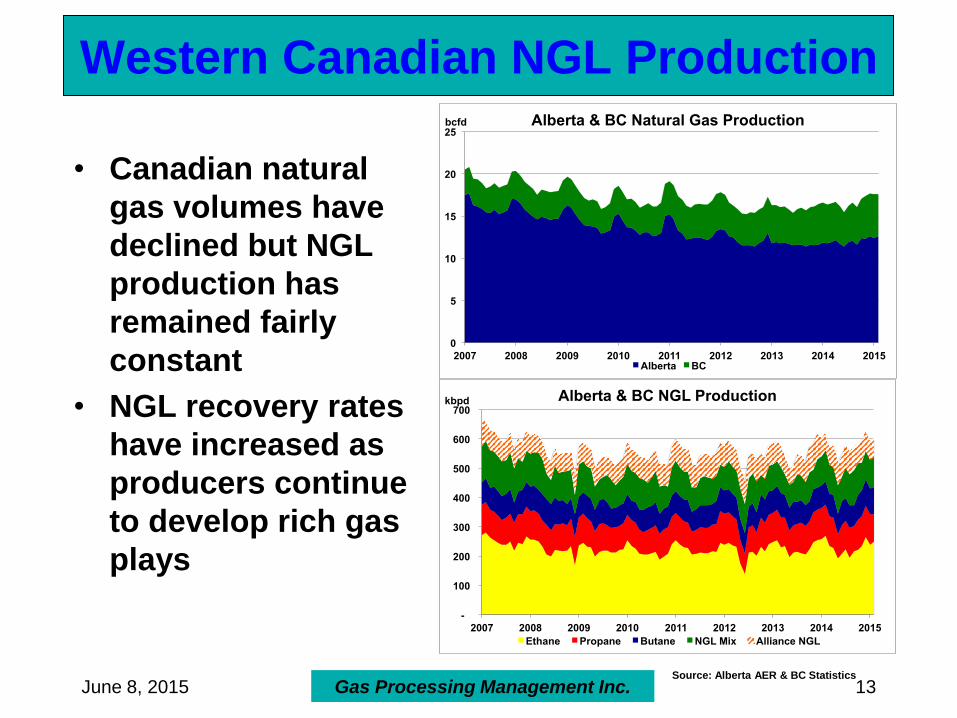

Western Canadian NGL Production

• Canadian natural

gas volumes have

declined but NGL

production has

remained fairly

constant

• NGL recovery rates

have increased as

producers continue

to develop rich gas

plays

June 8, 2015 Gas Processing Management Inc. 13Source: Alberta AER & BC Statistics

-

100

200

300

400

500

600

700

2007 2008 2009 2010 2011 2012 2013 2014 2015

kbpd Alberta & BC NGL Production

Ethane Propane Butane NGL Mix Alliance NGL

0

5

10

15

20

25

2007 2008 2009 2010 2011 2012 2013 2014 2015

bcfd Alberta & BC Natural Gas Production

Alberta BC

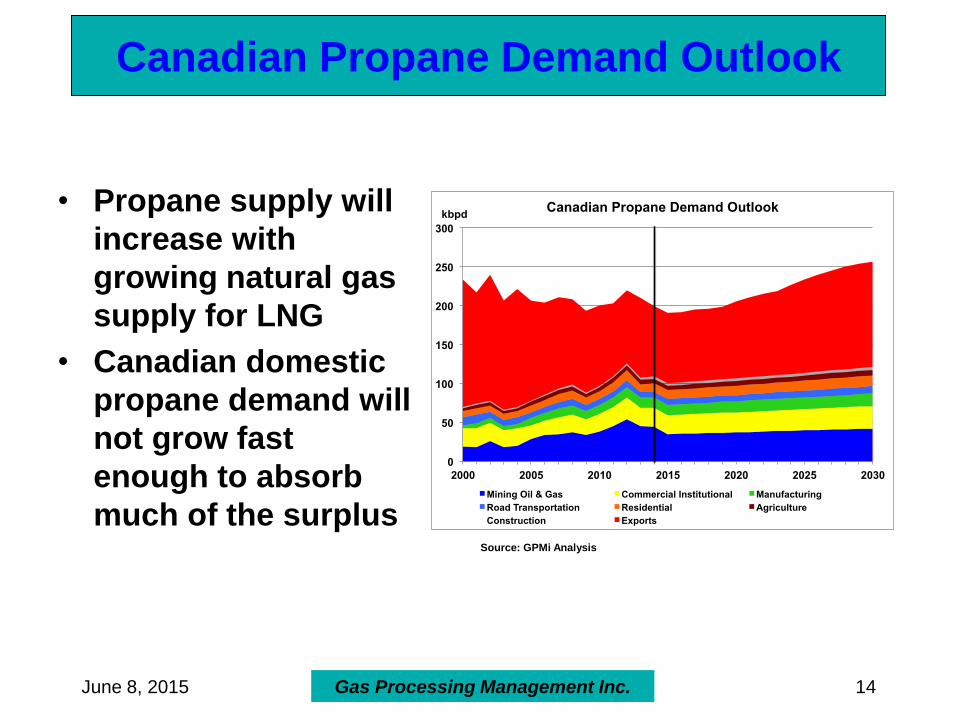

Canadian Propane Demand Outlook

June 8, 2015 Gas Processing Management Inc. 14

• Propane supply will

increase with

growing natural gas

supply for LNG

• Canadian domestic

propane demand will

not grow fast

enough to absorb

much of the surplus

0

50

100

150

200

250

300

2000 2005 2010 2015 2020 2025 2030

kbpd Canadian Propane Demand Outlook

Mining Oil & Gas Commercial Institutional Manufacturing

Road Transportation Residential Agriculture

Construction Exports

Source: GPMi Analysis

Canadian Propane Exports

June 8, 2015 Gas Processing Management Inc. 15

• Propane exports are

declining while

production rises

• Revenue will decline

further with the price

impact in 2015

• Continuing to push

product into a well

supplied market is

not a recipe for

success

• We need new

markets for our

propane

Source: National Energy Board

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

0

2

4

6

8

10

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MM m3/yr $C Billions Canadian Propane Exports

(Volume & Revenue)

• Most export volumes are

moving by rail

Presentation Outline

• GPMi Introduction

• Canadian and U.S. NGL Production

• Recent Prices and Margins

• How Bad Is It?

• What Will Happen Next?

• Disposition Options

• Petrochemical Opportunity

• Conclusion

June 8, 2015 Gas Processing Management Inc. 16

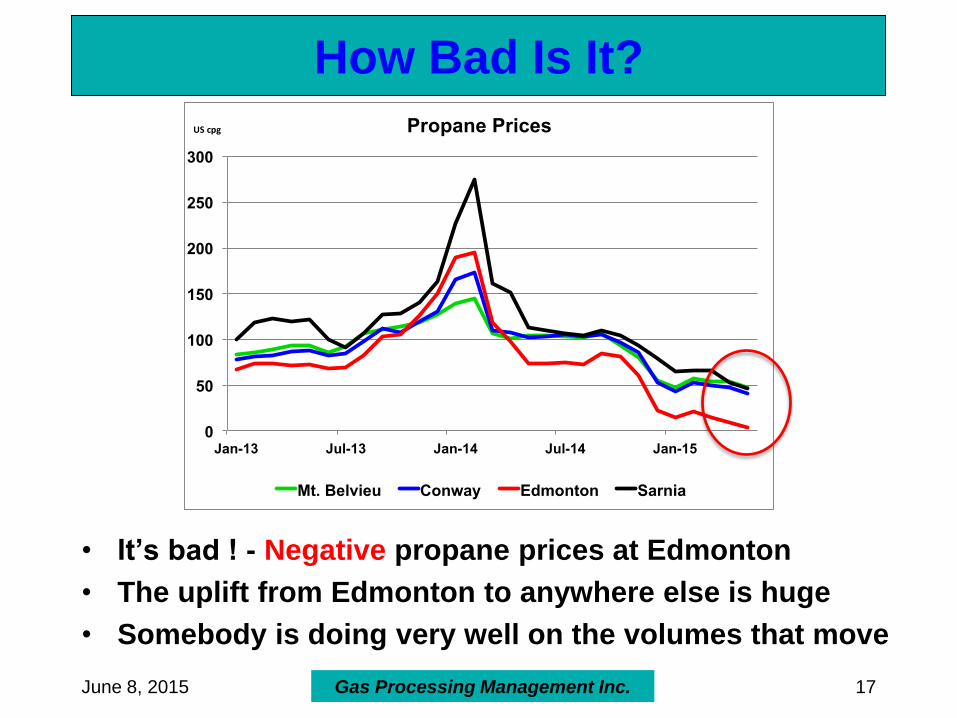

How Bad Is It?

• It’s bad ! - Negative propane prices at Edmonton

• The uplift from Edmonton to anywhere else is huge

• Somebody is doing very well on the volumes that move

June 8, 2015 Gas Processing Management Inc. 17

0

50

100

150

200

250

300

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

UScpg Propane Prices

Mt. Belvieu Conway Edmonton Sarnia

How Bad Is It?

• It’s bad ! – producers are losing ~ $5/GJ on propane

• The propane margin probably won’t become positive

for the balance of this year

June 8, 2015 Gas Processing Management Inc. 18

Source: GPMi Monthly NGL Report

-$6

-$4

-$2

$0

$2

$4

$6

$8

$10

$12

$14

$16

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

$Cdn/GJ

Edm - Chi Edmonton Chicago

Propane Available Netback over Shrinkage

-$1

$0

$1

$2

$3

$4

$5

$6

-$1

$0

$1

$2

$3

$4

$5

$6

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

WCSB Extraction - Component Op Income

Gas Ethane Propane Butane Pentanes + Total Margin

$/GJ $/GJ

$0

$1

$2

$3

$4

$5

$6

Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

WCSB Extraction - Component Revenue

Gas Ethane Propane Butane Pentanes +

$/GJ

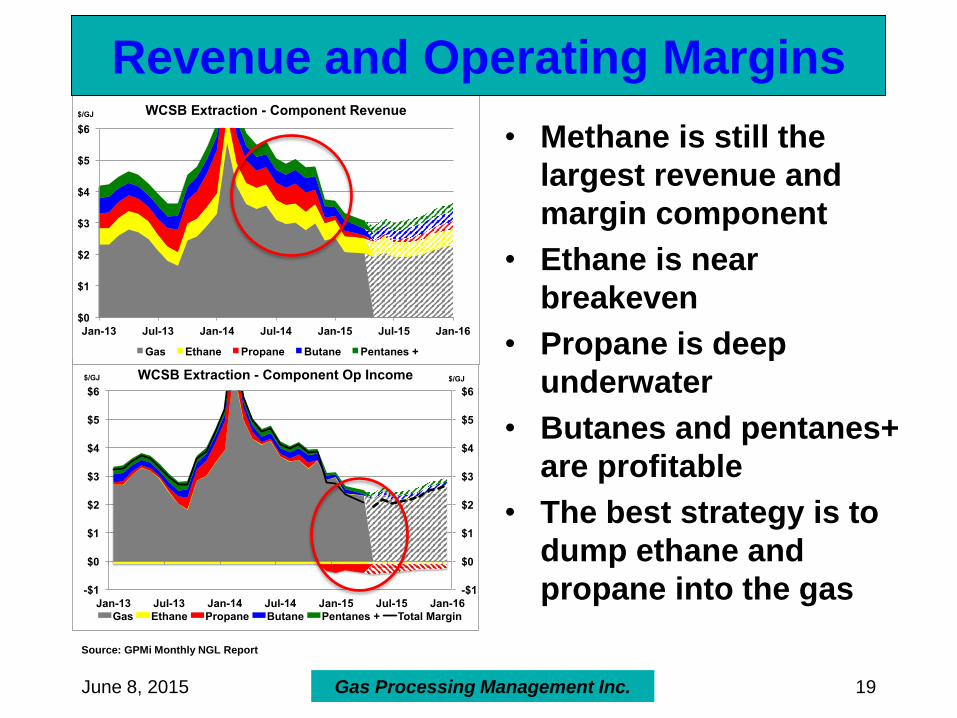

Revenue and Operating Margins

June 8, 2015 Gas Processing Management Inc. 19

• Methane is still the

largest revenue and

margin component

• Ethane is near

breakeven

• Propane is deep

underwater

• Butanes and pentanes+

are profitable

• The best strategy is to

dump ethane and

propane into the gas

Source: GPMi Monthly NGL Report

Presentation Outline

• GPMi Introduction

• Canadian and U.S. NGL Production

• Recent Prices and Margins

• How Bad Is It?

• What Will Happen Next?

• Disposition Options

• Petrochemical Opportunity

• Conclusion

June 8, 2015 Gas Processing Management Inc. 20

How Long Will The Glut Last?

• The reality is that

the US no longer

needs Canadian

gas and NGLs

– It is fixing its own

surplus

• This is a

fundamental,

permanent shift

• The glut will last

until we develop

alternative marketsJune 8, 2015 Gas Processing Management Inc. 21

What Will Happen Next? – Option 1

• We muddle along

• The NIMBYs and

BANANAs slow

everything down

• We miss the boat for

LNG and LPG exports

• Canadian natural gas

and NGL industry

declines

• The probability of this

option is way too high

!June 8, 2015 Gas Processing Management Inc. 22

What Will Happen Next? – Option 2

• Waterborne LPG

exports increase

– Petrogas at Ferndale

– Pembina at Portland

– Others – Prince Rupert?

• We capture a share of

the S.E. Asia market

• This option is difficult

but doable

• Canada desperately

needs this option

June 8, 2015 Gas Processing Management Inc. 23

What Will Happen Next? – Option 3

• Hot LNG

• Ethane & propane

streamed to the west

coast with C4 & C5’s

to Alberta

– Potential risk to

existing ethane supply

for petchems

• Canada needs the

LNG option to save

the gas industry from

irreversible declineJune 8, 2015 Gas Processing Management Inc. 24

What Will Happen Next? – Option 4

• Petchem demand

increases

• Petchems maximize

propane cracking

• They consider adding

C3 cracker capacity

• PDH and

polypropylene plants

get built

• This probability of this

option is uncertain

June 8, 2015 Gas Processing Management Inc. 25

What Will Happen Next? – Option 5• A Deus Ex Machina

saves the day

• Geopolitical events

drive prices back to

high levels

• The NIMBYs finally

understand

economics

• We implement

supportive

government policy

• Stranger things have

happenedJune 8, 2015 Gas Processing Management Inc. 26

Petrochemical Option

• The Petrochemical

Industry needs a

healthy producing

sector

– Without it, there is no

feedstock and no

Petrochemical Industry

• It is a buyer’s market

and a good time to

lock up long term

supply

• Is there a role for

government?

– Son of IEEP perhaps ?

June 8, 2015 Gas Processing Management Inc. 27

Presentation Outline

• GPMi Introduction

• Canadian and U.S. NGL Production

• Recent Prices and Margins

• How Bad Is It?

• What Will Happen Next?

• Disposition Options

• Petrochemical Opportunity

• Conclusion

June 8, 2015 Gas Processing Management Inc. 28

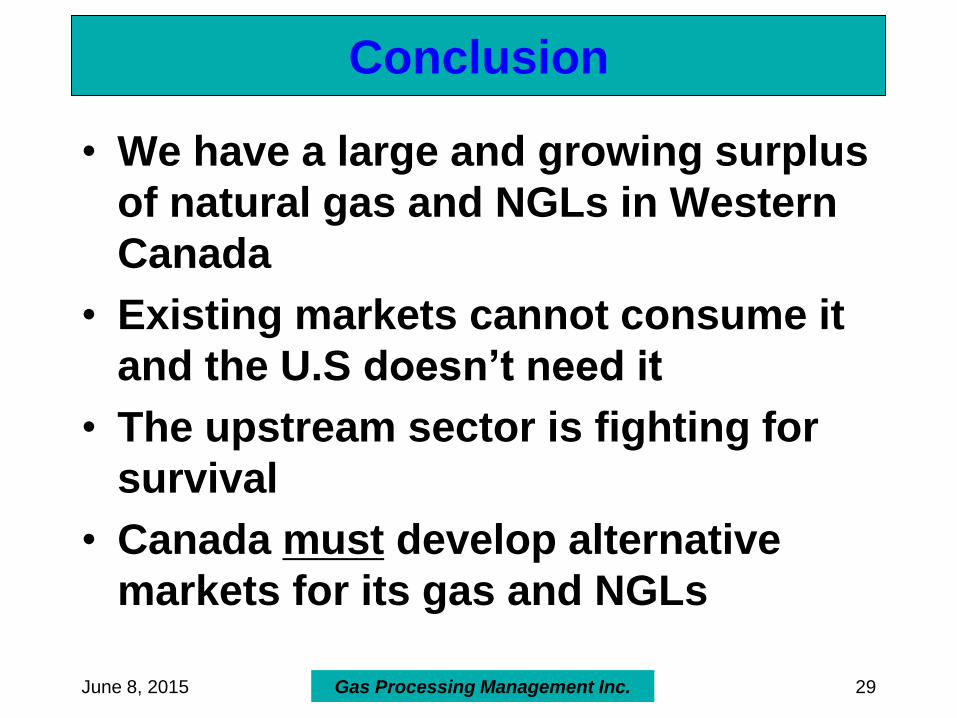

Conclusion

• We have a large and growing surplus

of natural gas and NGLs in Western

Canada

• Existing markets cannot consume it

and the U.S doesn’t need it

• The upstream sector is fighting for

survival

• Canada must develop alternative

markets for its gas and NGLs

June 8, 2015 Gas Processing Management Inc. 29

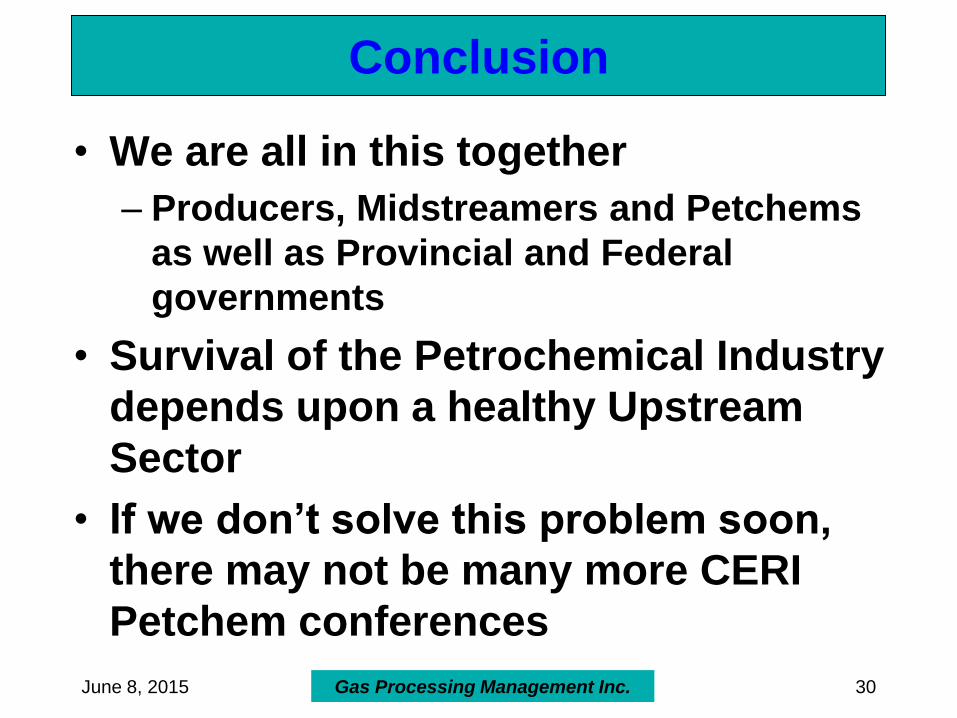

Conclusion

• We are all in this together

– Producers, Midstreamers and Petchems

as well as Provincial and Federal

governments

• Survival of the Petrochemical Industry

depends upon a healthy Upstream

Sector

• If we don’t solve this problem soon,

there may not be many more CERI

Petchem conferences

June 8, 2015 Gas Processing Management Inc. 30

Gas Processing Management Inc.

June 8, 2015 Gas Processing Management Inc. 31

Gerry Goobie, P.Eng.

403-680-9110

Dave Tulk. P. Eng.

tulk @gasprocessing.com

403-813-0254

www.gasprocessing.com

Disclaimer

Gas Processing Management Inc. 32

This presentation has been prepared for the sole benefit of attendees atthe CERI 2015 Petrochemical Conference. This presentation or any partof it shall not be provided to third parties without the express writtenconsent of Gas Processing Management Inc.

Gas Processing Management Inc. conducted the analysis herein utilizingreasonable professional skill, expertise, diligence and care consistentwith normal industry practice. All results are based on informationavailable at the time the analysis was conducted. Changes in factorsupon which the analysis is based could affect the results. Forecasts areinherently uncertain and Gas Processing Management Inc. accepts noliability with respect to the Client’s or any other third party’s conclusionsor decisions which are based on the analysis or forecasts herein.

Some of the information on which this analysis is based has beenprovided by others. Gas Processing Management Inc. has utilized suchinformation without verification unless specifically noted otherwise. GasProcessing Management Inc. accepts no liability for errors orinaccuracies in information provided by others.

June 8, 2015

Other GPMi Areas Of Expertise

• Just What The *&#% Is Going On With

– Ethane ?

– Natural Gas ?

– Other NGLs ?

– Gas Processing ?

– Petrochemicals ?

June 8, 2015 Gas Processing Management Inc. 33