Embed Size (px)

Citation preview

Presented by Bobbi Leahy

Gluten-free: Long-term trend or short-term fad

2

Gluten Free Insights

Today’s presentation:

• Celiac disease and GS/GI statistics

• Labeling and certification

• Market drivers

• Market, segment, and channel performance

• Product innovation

• Recap of what is helping and hurting the market

3

Gluten Free Insights

Methodology Basis for today’s presentation: Gluten-free Food, January 2012 report

Consumer survey

• Conducted online, Oct. 13-20, 2011

• 3,000 adults 18+, proportionally-balanced to adult U.S. population

• 299 adults (10%) were identified as gluten-free food users

Mintel’s Global New Products Database (GNPD)

• Captures global new product launches

• Includes claims and positioning (Kosher, gluten-free) • GF data period: January 2007 – December 2011

Sales data

• SPINS-based; FDMx and natural/specialty markets scan data (excluding Walmart, Whole Foods, Trader Joe’s, store brands, PLU)

• Calendar years 2009-11, with Mintel forecast through 2013

• Includes inherently GF

4

Gluten Free Insights

Celiac and gluten intolerance are on the rise

5

Gluten Free Insights

Why A Rise in Incidence? Over consumption of wheat

The wheat of today is not your grandmothers wheat

6

Gluten Free Insights

And young adults are most aware, meaning longer lifespan for trend

Fully 8% of respondents say they are gluten intolerant/sensitive, lending additional evidence to the notion of widespread under-diagnosis of the ailment.

Respondents aged 25-44 are more likely than other respondents to say they are gluten intolerant/sensitive and to be gluten-free food users.

0

5

10

15

Total 18-24 25-34 35-44 45-54 55-64 65+

#

Health and gluten-free food usage, by age, October 2011

Gluten intolerant/sensitive (net)

Gluten intolerant/sensitive and gluten-free food user (net)

Gluten-free food user for other reasons (net)

Base: 3,000 internet users aged 18+ Source: Mintel

7

Gluten Free Insights

Label confusion now, but certification may help

8

Gluten Free Insights

Product label claims for gluten vary, confuse consumers

Gluten-free labeling varies tremendously and is akin to early organic label claims (i.e., all over the map)

“Gluten-free” with no other mentions of certifiers, etc. is

common among brands.

Some labels are confusing and have consumers

wondering if there is a risk of cross contamination.

49% say a gluten-

free claim clearly

marked on FOP

influences purchase decision

9

Gluten Free Insights

Product label claims for gluten vary, confuse consumers

Dedicated facility claims help.

Others have certified some ingredients (fair trade), but not gluten, but also claim

to make products in dedicated GF facility.

Ultimately, a lack of third-party certification is common on labels from some of the biggest food brands down to smaller natural brands.

35% say a

“dedicated facility” claim

influences purchase decision

Retailers and manufacturers are occasionally utilizing

this claim.

10

Gluten Free Insights

Current regulatory environment

No current FDA regulation or enforcement of gluten-free labeling

January 2007 - FDA proposed 20 ppm.

Most manufacturers who label foods "gluten-free" are following the FDA's recommendation.

11

Gluten Free Insights

International Gluten Standards

Europe In 2008 the standard was reduced from 200 ppm to 20 ppm, 21-100ppm for low gluten New Zealand & Australia No detectable gluten allowed <3ppm Canada 20 ppm

12

Gluten Free Insights

Brand websites serve a variety of functions Hain directs consumers to its dedicated GF website: In addition, for example, its Garden of Eatin’ brand website provides an FAQ page to speak to gluten concerns.

…while also providing logos for consumers to look for and a GF guarantee.

General Mills has created a multi-tiered approach: Its Gluten Free Chex cereal aren’t certified as such (at least this isn’t specified on labels), but GMI does sponsor the Celiac Disease Foundation.

In May 2011, the company launched Glutenfreely.com; selling 400+ GF products from its own roster of brands, and others as well.

13

Gluten Free Insights

Social media key to making GI/GS/celiacs feel like they aren’t alone

Facebook and Twitter are primary sources for

consumers to learn, follow, nab recipes, and add

content.

Brand recognition

Udi’s

613K “likes”

GlutenFreely (GMI)

106K “likes”

Individuals

GlutenFreeville 46K “likes”

Organizations

Celiac Central 14K “likes”

Data points are based on review conducted February 2012 Source: Mintel

Individuals

Elizabeth Hasselback

241K followers

Diana J Herrington 22K

followers

Brand recognition

Rudi’s

2K followers

Gluten Free Works!

22K followers

14

Gluten Free Insights

Apps now readily available…and sometimes free

Is That Gluten Free?: large database of brands, products, and ingredients. $7.99

Find Me Gluten Free: restaurant directory, reviews. “Share photos, ratings, and reviews with other gluten-free diners.” FREE

So Simple Gluten Free Recipes: 75 GF recipes, created by Gluten Free Classes. $2.99

15

Gluten Free Insights

Gluten Free Certification in the US

Quality Assurance International (QAI)/National Foundation of Celiac Awareness, introduced its

“Certified Gluten-Free” label in June 2011. Certification tests to insure that the product 10 ppm

gluten or less.

Gluten Free Certification Organization: Certification requires that the product

contains less than 10 ppm gluten.

Celiac Sprue Association (CSA) tests for gluten in conjunction with the Univ. of Nebraska, and

has a lower limit of quantification of 5 ppm.

15% say third-party gluten-free claims, certification logos, etc. influence purchase decision

16

Gluten Free Insights

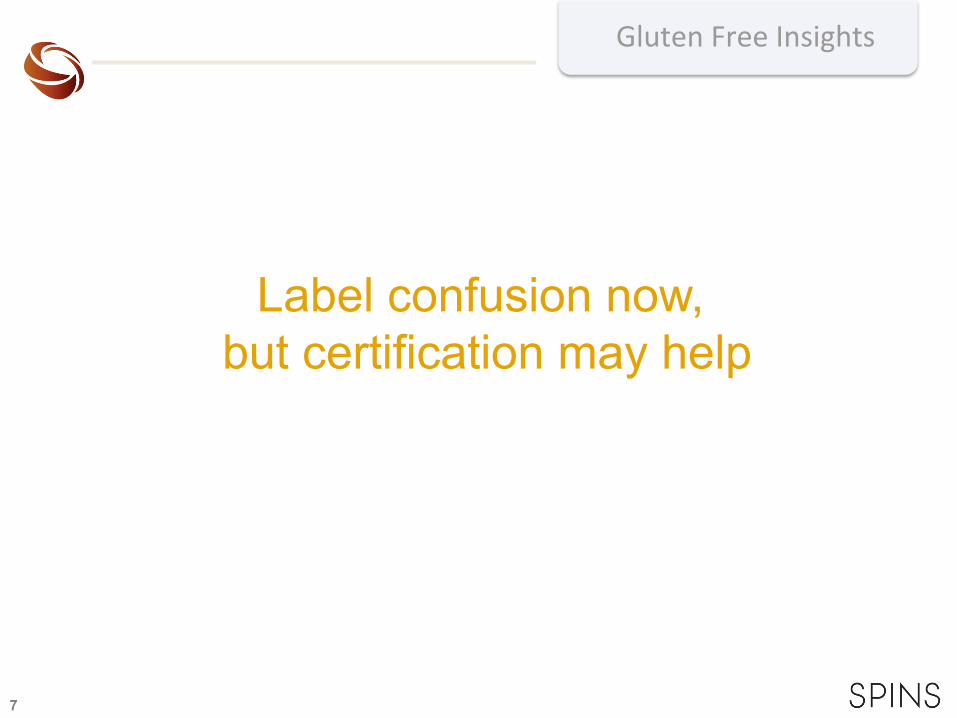

Total GF labeled and/or certified

SPINSscan Natural (excludes Whole foods), SPINSscan Food/Drug/Mass +AOC (includes Wal-mart) 52 weeks ending 9/1/2012 and YA

TOTAL Gluten Free Categories: YE 9-1-2012 vs Year Ago

Bread & BakedGoods

Chips, Pretze ls,Snacks

Cookies & SnackBars

Crackers &Crispbreads

YE Sept 2011 YE Sept 2012

$ Sales

17

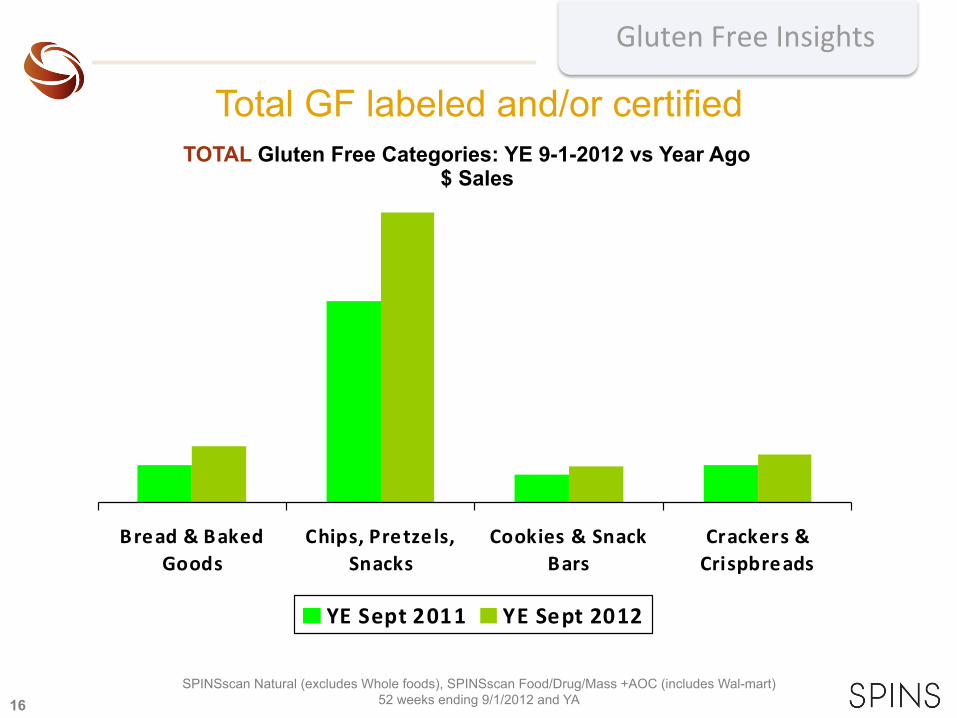

Gluten Free Insights

Purpose To gauge reactions of a variety of participants when introduced to GF foods and to find out whether they could tell the difference between a gluten-free food and its traditional counterpart.

Categories tested:

• Bread

• Pretzels

• Cookies

• Chips

Salty snacks have the greatest acceptance and appeal. Bread and cookies are less acceptable currently. Inconsistencies may

hurt the sector’s growth.

“Average Joe” and “Jody” can tell which products are GF

18

Gluten Free Insights

Snyder’s of Hanover Gluten-Free Pretzel Sticks, 10-oz $3.19

Glutino Gluten Free Pretzel Twists,

14.1-oz, $7.79

Urge Premium Pretzel Sticks, 12-oz, $1.79

Price disparity will certainly slow usage, especially among GS’s…

.32 oz.

.55 oz.

.15 oz.

26% say GF products are too expensive to buy as often

as they’d like to

19

Gluten Free Insights

Natural & Organic Consumer Gluten Free food and beverage products, in general tend to fit a natural lifestyle

SPINSscan Natural, SPINSscan Specialty Gourmet 52 weeks ending 12/24/11

*Organic includes products with at least 70% organic content.

SPINS Natural Supermarkets Labeled GF Food & Beverage $ Sales

SPINS Specialty Gourmet Supermarkets Labeled GF Food & Beverage $ Sales

20

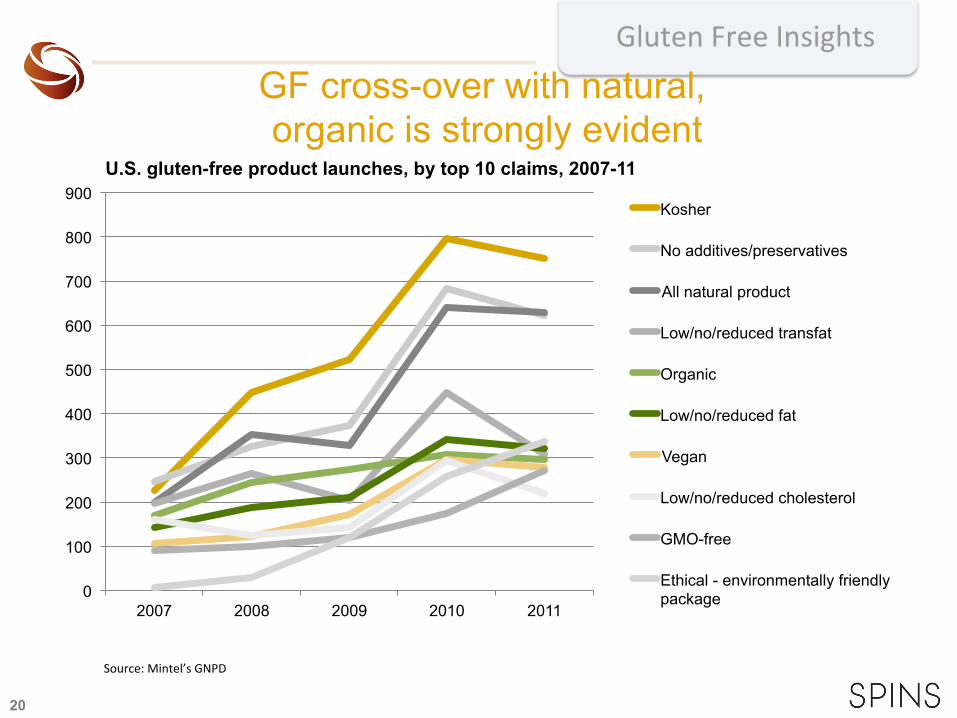

Gluten Free Insights

GF cross-over with natural, organic is strongly evident

U.S. gluten-free product launches, by top 10 claims, 2007-11

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011

Kosher

No additives/preservatives

All natural product

Low/no/reduced transfat

Organic

Low/no/reduced fat

Vegan

Low/no/reduced cholesterol

GMO-free

Ethical - environmentally friendly package

Source: Mintel’s GNPD

21

Gluten Free Insights

Sales are on continual upward swing; market not yet mature

22

Gluten Free Insights

Sales of Gluten Free products continues to grow: +19%

Labeled and/or certified GF Billions

$7.97

$9.49

YE Sept 2011 YE Sept 2012

SPINSscan Natural (excludes Whole foods), SPINSscan Food/Drug/Mass +AOC (includes Wal-mart) 52 weeks ending 9/1/2012 and YA

23

Gluten Free Insights Strong channel performance belies

unmet consumer need

The FDMx channel was responsible for more than 80% of segment sales during 2009-11.

FDMx’s market share

slightly declined (1.2%), while natural food and specialty retailers slightly increased their market share from 2009-11.

3,910

4,901

821 1,116

0

1,000

2,000

3,000

4,000

5,000

6,000

2009* 2011* $

mill

ions

FDMx Natural and specialty food retailers

* 52 weeks ending Oct. 31, 2009 and Oct. 29, 2011 Sales in FDMx, natural, and specialty markets only Source: Mintel/SPINS/Nielsen

Total sales of gluten-free food and beverages, by channel, 2009 and 2011

46% say they wish there were more GF items to pick

from in stores

24

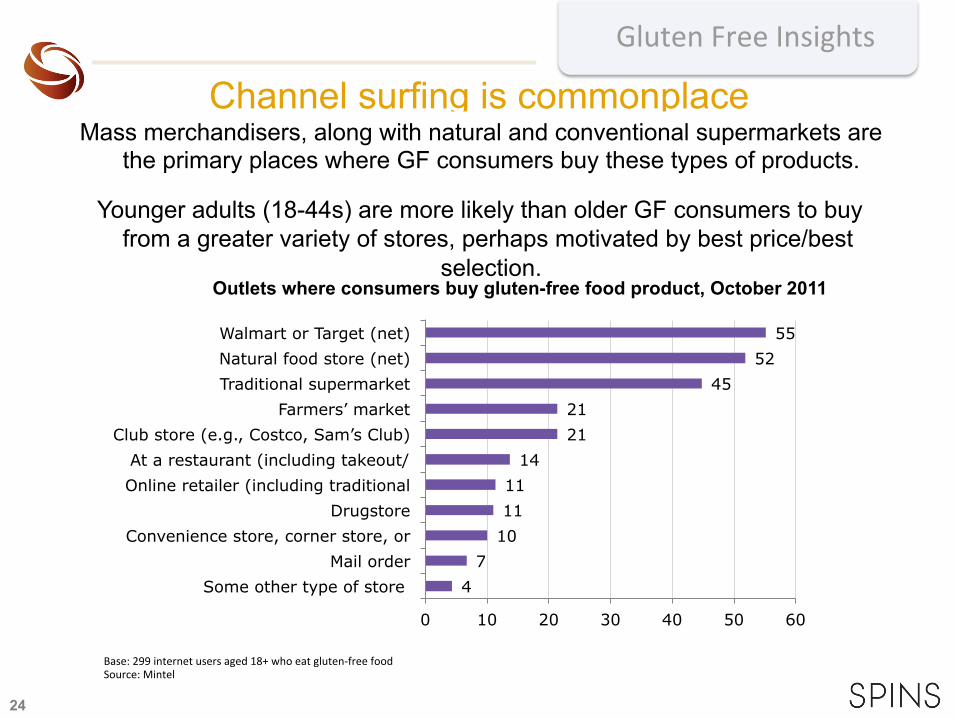

Gluten Free Insights

Channel surfing is commonplace

4 7

10 11 11

14 21 21

45 52

55

0 10 20 30 40 50 60

Some other type of store Mail order

Convenience store, corner store, or Drugstore

Online retailer (including traditional At a restaurant (including takeout/

Club store (e.g., Costco, Sam’s Club) Farmers’ market

Traditional supermarket Natural food store (net) Walmart or Target (net)

Outlets where consumers buy gluten-free food product, October 2011

Base: 299 internet users aged 18+ who eat gluten-‐free food Source: Mintel

Mass merchandisers, along with natural and conventional supermarkets are the primary places where GF consumers buy these types of products.

Younger adults (18-44s) are more likely than older GF consumers to buy from a greater variety of stores, perhaps motivated by best price/best

selection.

25

Gluten Free Insights

Segment leaders

Leading company/brand performance

Chips: Pirate Brands, $58mm, up 23%

Cold cereal: General Mills, $132mm, up 37%

Fz Entrées: Amy’s Kitchen, $105mm, up 18%

Bread: Udi’s Gluten Free Foods, $47mm, up 247%

* 52 weeks ending Oct. 29, 2011 Sales in FDMx, natural, and specialty markets only Source: Mintel/SPINS/Nielsen

Emerging players

Chips: Popchips, $46mm, up 106%

Cold cereal: Nature’s Path, $22mm, up 13%

Fz Entrées: John Soules Foods, $11mm, up 40%

Bread: Food for Life, $12mm, up 10%

26

Gluten Free Insights

Product innovation on upswing since 2010, and expanding

beyond food

27

Gluten Free Insights

New GF innovations expanded dramatically in recent years

The total number of innovations with GF claims jumped from roughly 600 in 2007 to more than 1,600 in 2011. Much of this shift has come

from larger manufacturers now labeling inherently GF items (e.g., tomato sauce) with these claims.

0

200

400

600

800

1000

1200

1400

1600

1800

2007 2008 2009 2010 2011

U.S. gluten-free product launches, 2007-11

Source: Mintel’s GNPD

28

Gluten Free Insights

New gluten free items continue to launch in record numbers

Number of New ‘Labeled Gluten Free’ Products Entering the Market as Captured by SPINS

2009-2011 February 2009-2012 All-time high!

Source: SPINS Product Library across channels

208 224

394 404

0

50

100

150

200

250

300

350

400

450

Feb-09 Feb-10 Feb-11 Feb-12

3582

5305 5364

0

1000

2000

3000

4000

5000

6000

2009 2010 2011

29

Gluten Free Insights

Non-food sector also exploding Consumers can now find a variety of pet and health products that are GF. Beauty care offerings are relatively new but make

great sense considering absorption.

97

224

296 238 239

105

27

81

80

36

35

0

50

100

150

200

250

300

350

400

2007 2008 2009 2010 2011

# o

f in

nova

tions

Health & Hygiene Beauty & Personal Care Pet

Source: Mintel’s GNPD

U.S. gluten-free product launches (non-food), 2007-11

30

Gluten Free Insights Gluten Free Opportunity: Whole Grain/ Ancient Grain

Amaranth Buckwheat Corn (including cornmeal and popcorn) Millet Rice (including brown and colored) Sorghum (a.k.a milo) Wild Rice Ancient Grains: Quinoa, Teff, Amaranth

Wheat (varieties Spelt, Emmer, Farro, Kamut, Durum, forms such as Bulgur, cracked wheat and wheat berries) Barley Rye Oats (including oatmeal) [may be GF] Triticale (a rye-wheat hybrid) Ancient Grains: Einkorn, Freekeh

GLU

TE

N

GLU

TE

N-F

RE

E

"Whole grains are an important part of eating a nutritionally balanced diet and the Whole Grains Council is encouraged to see so many of our members striving to include whole grains in gluten-free products for the consumer." -Karen Mansur , Program Manager Oldways / Whole Grains Council

SPINSscan Natural (excludes Whole foods), SPINSscan Food/Drug/Mass +AOC (includes Wal-mart) 52 weeks ending 9/1/2012 and YA

YES there are Gluten Free Whole Grains!

Certified Whole Grain GF products grew 24% last year!

31

Gluten Free Insights

Looking ahead & opportunities

32

Gluten Free Insights

What’s helping the market

• Celiac/GS/GI audience is growing

• Certification may lead to more consistency and consumer confidence

• Sales are expected to continue on growth path

• Innovations have spiked since 2010, including menu items

• Piggybacking on natural/organic sector’s success

33

Gluten Free Insights

What’s hurting the GF market

• Gluten sensitivity not widely understood/hard to diagnose

• Price disparity between GF and “regular” items

• Taste/texture/appearance inconsistencies between products and between categories

• Lack of widespread availability in mainstream market (retailers still in “wait and see” mode)

• Inconsistent label/signage in retail

34

Gluten Free Insights

THANK YOU Bobbi Leahy, SPINS LLC