Embed Size (px)

Citation preview

Global Transaction Services

Rob van Paridon, SEVP - Global Head of Global Transaction Services BU

20 November, 2002

0 2

Overview Our four transaction businesses (Cash and Payments, Global Trade and

Advisory, Global Custody and Clearing and Execution Services) currently

occupy strong market positions

Significant consolidation and improvements to our operating environment

have been accomplished to date, and a lot of opportunities remain to

continue improving our efficiency

We are shifting our transaction business from an operational focus to value-

added working capital solutions

Our emerging working capital proposition combines our strength in

transaction annuity flows with our strong foreign exchange and debt

products and will allow us to leverage our client base across the bank

Our working capital business is believed to be the best platform for future

competitive advantage and hence profitable growth

0 3

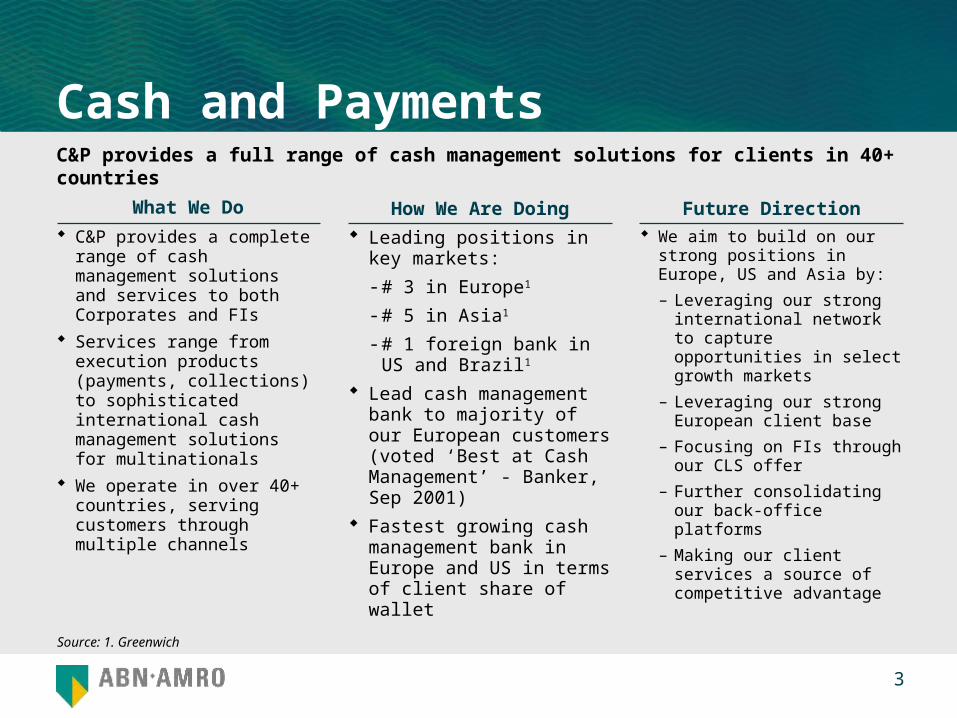

Cash and Payments

C&P provides a full range of cash management solutions for clients in 40+ countries

C&P provides a complete range of cash management solutions and services to both Corporates and FIs

Services range from execution products (payments, collections) to sophisticated international cash management solutions for multinationals

We operate in over 40+ countries, serving customers through multiple channels

We aim to build on our strong positions in Europe, US and Asia by:

– Leveraging our strong international network to capture opportunities in select growth markets

– Leveraging our strong European client base

– Focusing on FIs through our CLS offer

– Further consolidating our back-office platforms

– Making our client services a source of competitive advantage

Leading positions in key markets:

- # 3 in Europe1

- # 5 in Asia1

- # 1 foreign bank in US and Brazil1

Lead cash management bank to majority of our European customers (voted ‘Best at Cash Management’ - Banker, Sep 2001)

Fastest growing cash management bank in Europe and US in terms of client share of wallet

Source: 1. Greenwich

Future DirectionHow We Are DoingWhat We Do

0 4

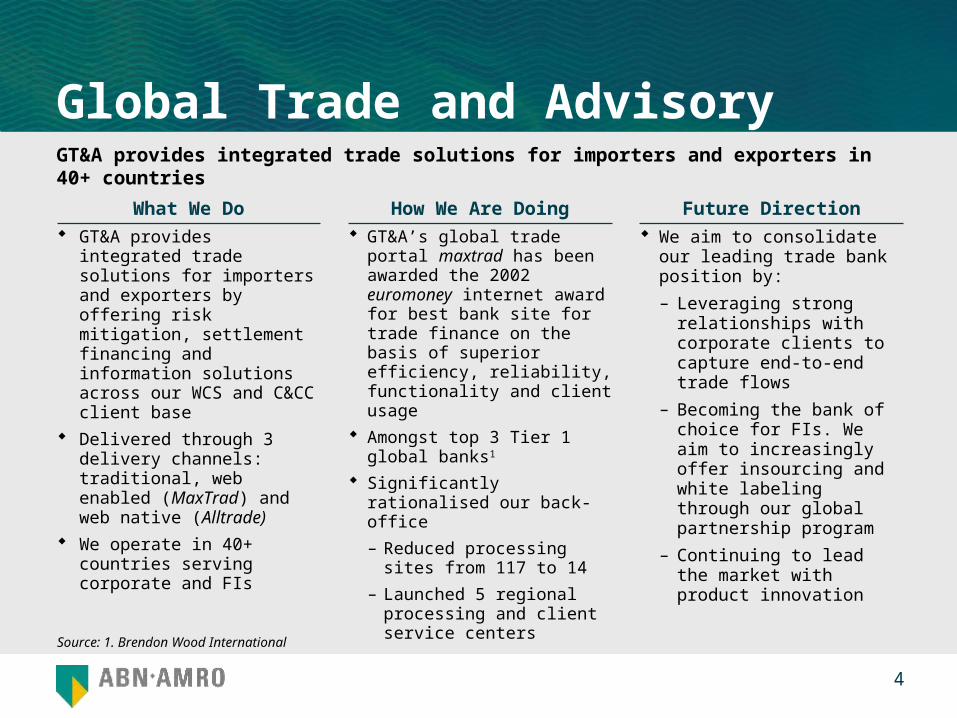

Global Trade and Advisory

We aim to consolidate our leading trade bank position by:

– Leveraging strong relationships with corporate clients to capture end-to-end trade flows

– Becoming the bank of choice for FIs. We aim to increasingly offer insourcing and white labeling through our global partnership program

– Continuing to lead the market with product innovation

GT&A’s global trade portal maxtrad has been awarded the 2002 euromoney internet award for best bank site for trade finance on the basis of superior efficiency, reliability, functionality and client usage

Amongst top 3 Tier 1 global banks1

Significantly rationalised our back-office

– Reduced processing sites from 117 to 14

– Launched 5 regional processing and client service centers

GT&A provides integrated trade solutions for importers and exporters by offering risk mitigation, settlement financing and information solutions across our WCS and C&CC client base

Delivered through 3 delivery channels: traditional, web enabled (MaxTrad) and web native (Alltrade)

We operate in 40+ countries serving corporate and FIs

GT&A provides integrated trade solutions for importers and exporters in 40+ countries

Source: 1. Brendon Wood International

Future DirectionHow We Are DoingWhat We Do

0 5

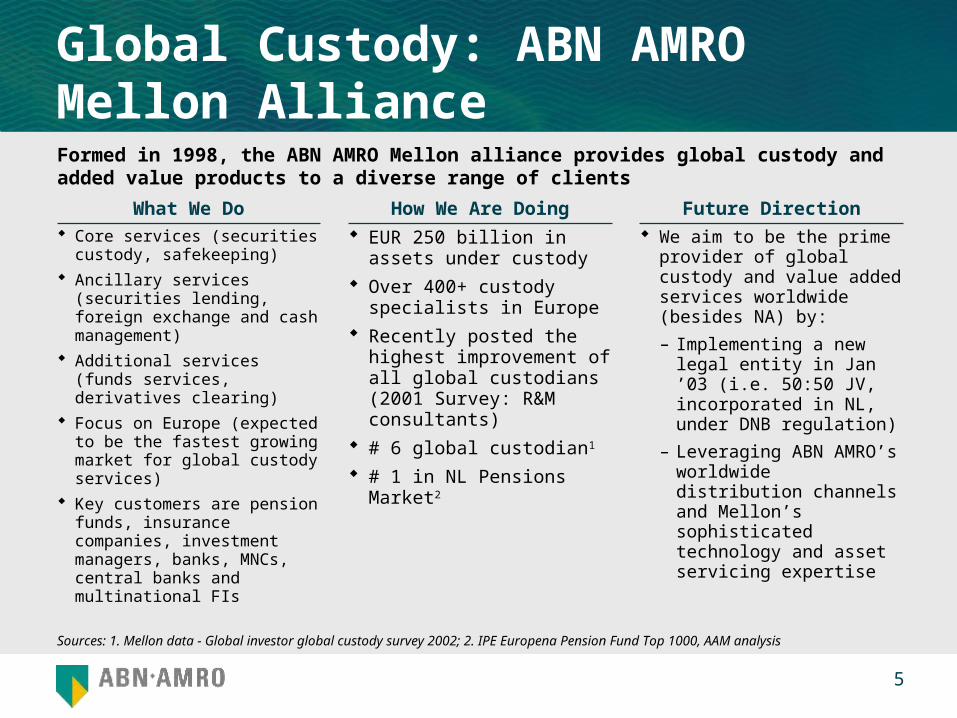

Global Custody: ABN AMRO Mellon Alliance

We aim to be the prime provider of global custody and value added services worldwide (besides NA) by:

– Implementing a new legal entity in Jan ’03 (i.e. 50:50 JV, incorporated in NL, under DNB regulation)

– Leveraging ABN AMRO’s worldwide distribution channels and Mellon’s sophisticated technology and asset servicing expertise

EUR 250 billion in assets under custody

Over 400+ custody specialists in Europe

Recently posted the highest improvement of all global custodians (2001 Survey: R&M consultants)

# 6 global custodian1

# 1 in NL Pensions Market2

Core services (securities custody, safekeeping)

Ancillary services (securities lending, foreign exchange and cash management)

Additional services (funds services, derivatives clearing)

Focus on Europe (expected to be the fastest growing market for global custody services)

Key customers are pension funds, insurance companies, investment managers, banks, MNCs, central banks and multinational FIs

Formed in 1998, the ABN AMRO Mellon alliance provides global custody and added value products to a diverse range of clients

Sources: 1. Mellon data - Global investor global custody survey 2002; 2. IPE Europena Pension Fund Top 1000, AAM analysis

Future DirectionHow We Are DoingWhat We Do

0 6

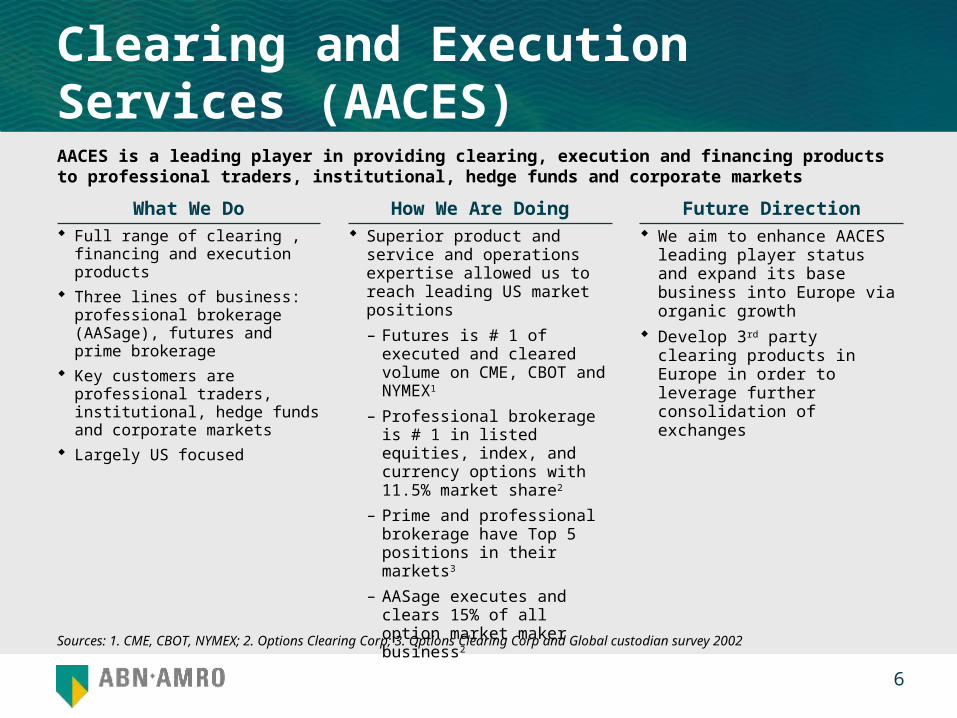

Clearing and Execution Services (AACES)

We aim to enhance AACES leading player status and expand its base business into Europe via organic growth

Develop 3rd party clearing products in Europe in order to leverage further consolidation of exchanges

Superior product and service and operations expertise allowed us to reach leading US market positions

– Futures is # 1 of executed and cleared volume on CME, CBOT and NYMEX1

– Professional brokerage is # 1 in listed equities, index, and currency options with 11.5% market share2

– Prime and professional brokerage have Top 5 positions in their markets3

– AASage executes and clears 15% of all option market maker business2

Full range of clearing , financing and execution products

Three lines of business: professional brokerage (AASage), futures and prime brokerage

Key customers are professional traders, institutional, hedge funds and corporate markets

Largely US focused

AACES is a leading player in providing clearing, execution and financing products to professional traders, institutional, hedge funds and corporate markets

Sources: 1. CME, CBOT, NYMEX; 2. Options Clearing Corp; 3. Options Clearing Corp and Global custodian survey 2002

Future DirectionHow We Are DoingWhat We Do

0 7

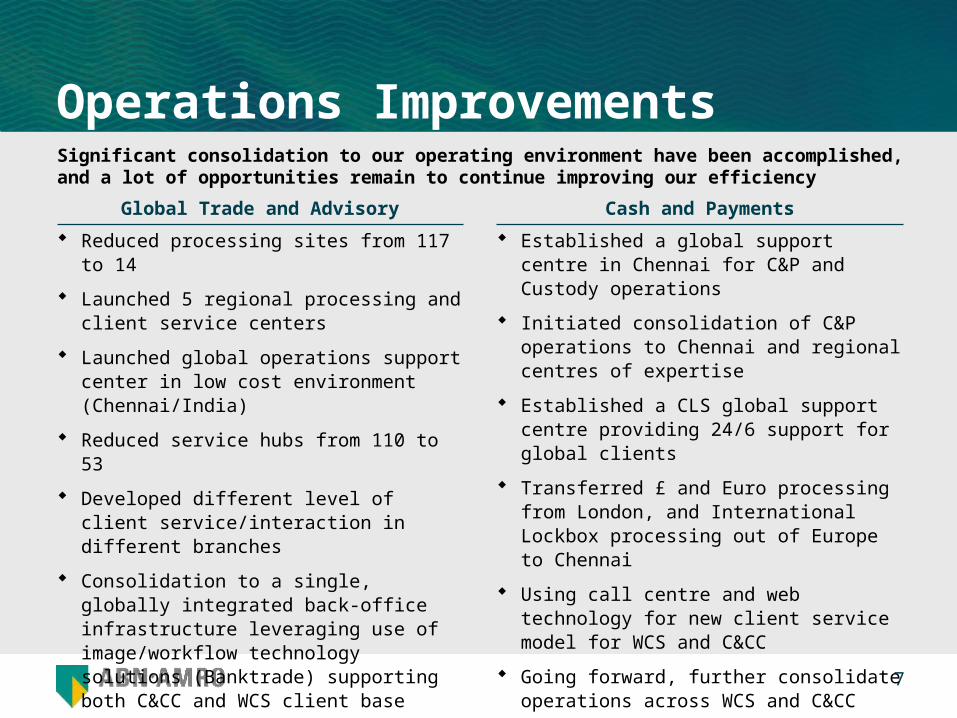

Operations Improvements

Reduced processing sites from 117 to 14

Launched 5 regional processing and client service centers

Launched global operations support center in low cost environment (Chennai/India)

Reduced service hubs from 110 to 53

Developed different level of client service/interaction in different branches

Consolidation to a single, globally integrated back-office infrastructure leveraging use of image/workflow technology solutions (Banktrade) supporting both C&CC and WCS client base

Established a global support centre in Chennai for C&P and Custody operations

Initiated consolidation of C&P operations to Chennai and regional centres of expertise

Established a CLS global support centre providing 24/6 support for global clients

Transferred £ and Euro processing from London, and International Lockbox processing out of Europe to Chennai

Using call centre and web technology for new client service model for WCS and C&CC

Going forward, further consolidate operations across WCS and C&CC

Global Trade and Advisory Cash and Payments

Significant consolidation to our operating environment have been accomplished, and a lot of opportunities remain to continue improving our efficiency

0 8

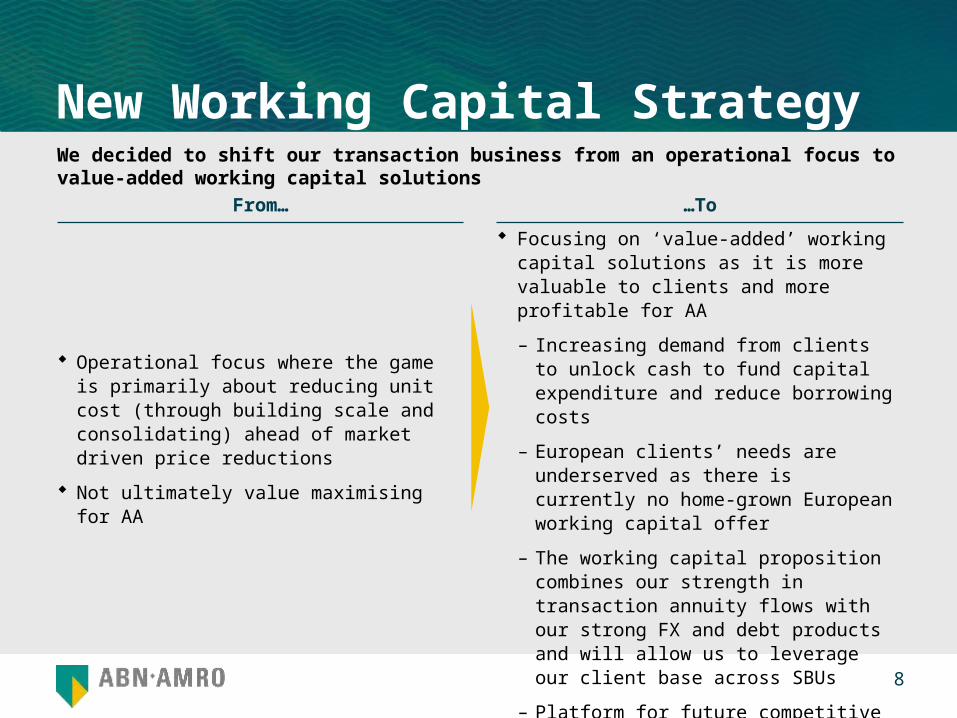

New Working Capital Strategy

Operational focus where the game is primarily about reducing unit cost (through building scale and consolidating) ahead of market driven price reductions

Not ultimately value maximising for AA

Focusing on ‘value-added’ working capital solutions as it is more valuable to clients and more profitable for AA

– Increasing demand from clients to unlock cash to fund capital expenditure and reduce borrowing costs

– European clients’ needs are underserved as there is currently no home-grown European working capital offer

– The working capital proposition combines our strength in transaction annuity flows with our strong FX and debt products and will allow us to leverage our client base across SBUs

– Platform for future competitive advantage and hence profitable growth

From… …To

We decided to shift our transaction business from an operational focus to value-added working capital solutions

0 9

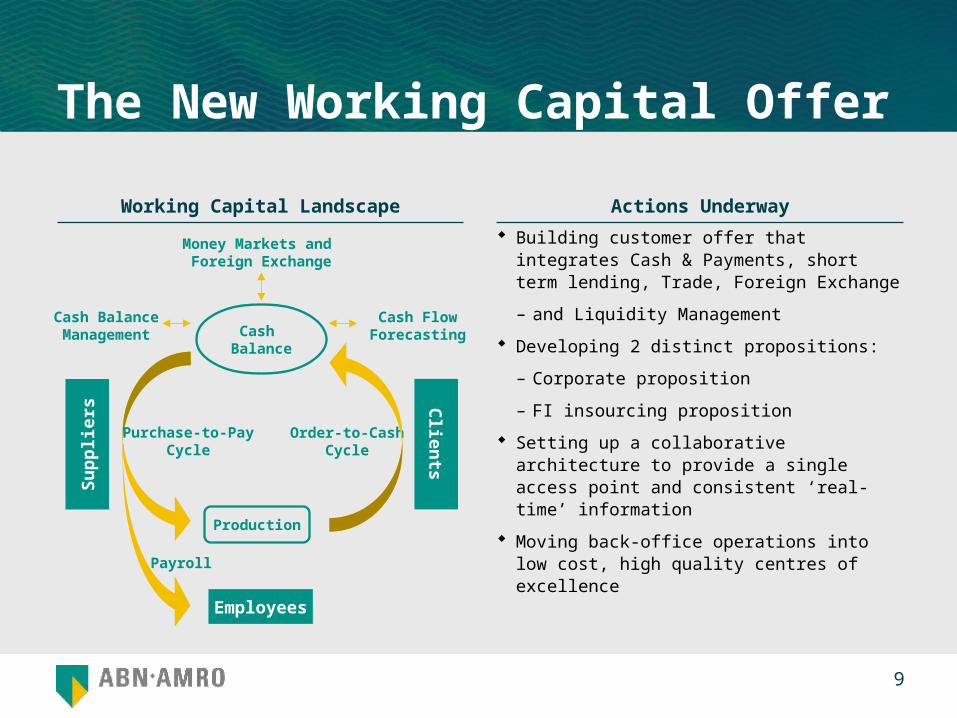

The New Working Capital Offer

Money Markets and Foreign Exchange

Order-to-CashCycle

Payroll

Cash Flow ForecastingCash

Balance

Employees

Clien

tsProduction

Cash Balance Management

Su

pp

liers

Purchase-to-PayCycle

Building customer offer that integrates Cash & Payments, short term lending, Trade, Foreign Exchange

– and Liquidity Management

Developing 2 distinct propositions:

– Corporate proposition

– FI insourcing proposition

Setting up a collaborative architecture to provide a single access point and consistent ‘real-time’ information

Moving back-office operations into low cost, high quality centres of excellence

Working Capital Landscape Actions Underway

20 November, 2002

Corporate Finance

Nigel Turner, SEVP - Global Head of Corporate

Finance

0 11

Restructuring Update YTD September revenues of €246 million in 2002, only 6% lower

than 2001 YTD September actuals

Direct operating costs have been reduced by 23% (year 2001

compared to forecast year 2002)

Headcount within Corporate Finance Business Unit (CF) has been

reduced from its peak in October 2001 by over 35% to 695

(professionals and support)

New York office closed; principal concentration of resources in

Europe (> 70%) with majority located in Amsterdam (approx. 100

professionals), with approx. 80 professionals located in London

On track to deliver positive net results in year 2003

0 12

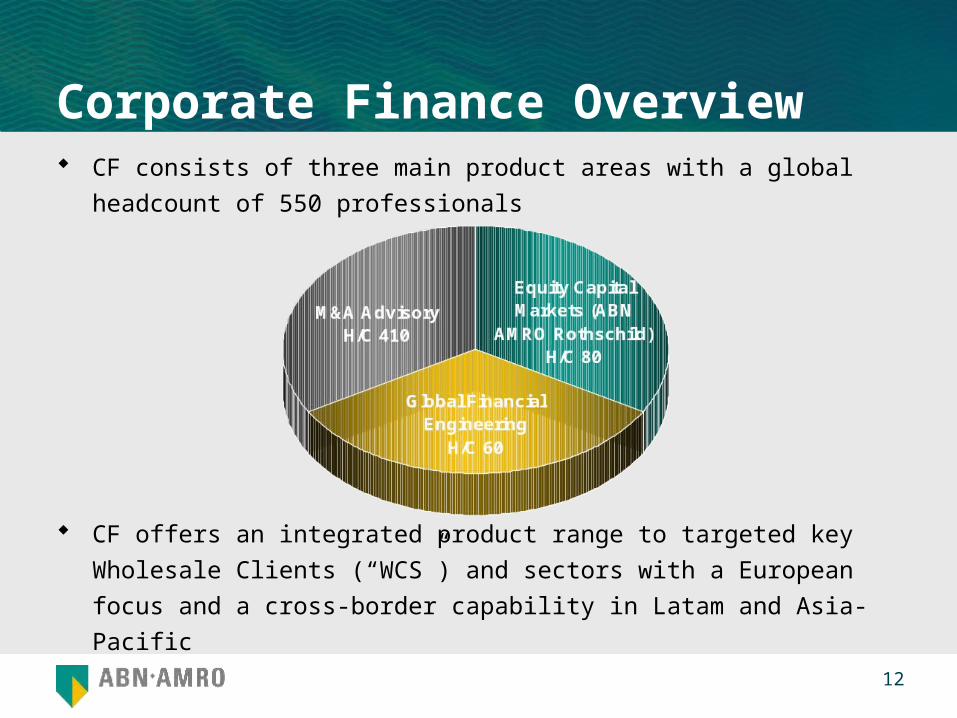

Corporate Finance Overview CF consists of three main product areas with a global headcount of

550 professionals

CF offers an integrated product range to targeted key Wholesale

Clients (“WCS”) and sectors with a European focus and a cross-

border capability in Latam and Asia-Pacific

0 13

Corporate Finance Overview Operating strategy includes improved productivity through higher

leveraged revenues & tight cost control. Headcount based around

regional hubs principally in Amsterdam, London & Stockholm but

also Hong Kong, Sydney & Brazil

Marketing differentiated product with strong execution capability.

Recognised leading brands in Netherlands, Nordic (Alfred Berg), UK

(Hoare Govett), European Emerging markets & Asia-Pacific

Strong CF capability links with strengths in other AA SBU’s - e.g.

private clients in France & BAPV in Italy

AA Rothschild (“AAR”), our Equity Capital Markets (“ECM”) joint

venture, is a recognised leading brand in the market place

0 14

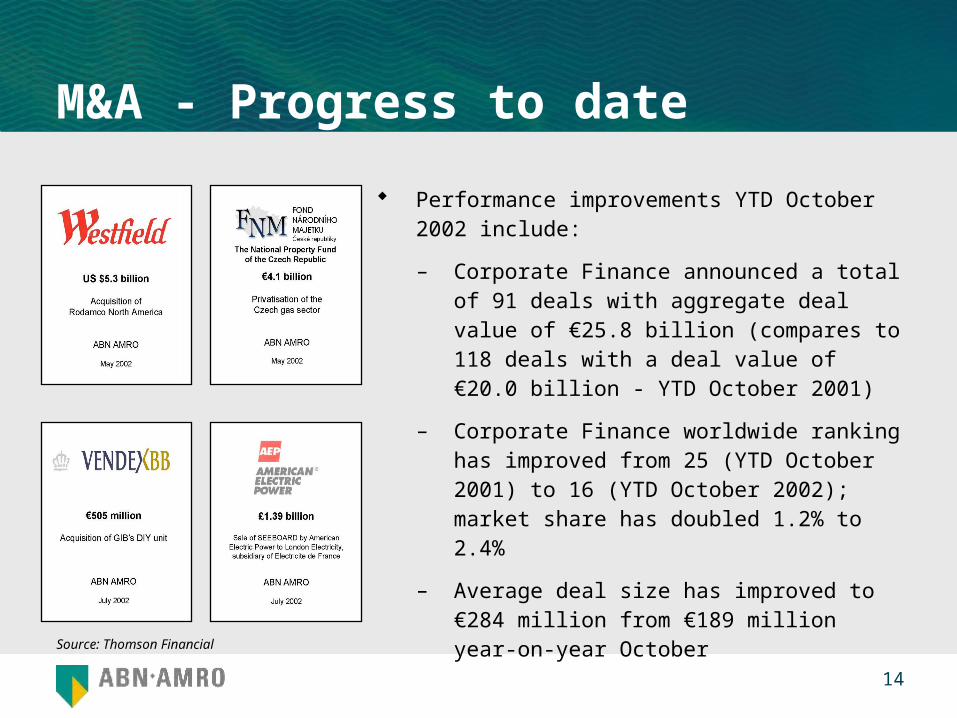

M&A - Progress to date

Performance improvements YTD October 2002 include:

– Corporate Finance announced a total of 91 deals with aggregate deal value of €25.8 billion (compares to 118 deals with a deal value of €20.0 billion - YTD October 2001)

– Corporate Finance worldwide ranking has improved from 25 (YTD October 2001) to 16 (YTD October 2002); market share has doubled 1.2% to 2.4%

– Average deal size has improved to €284 million from €189 million year-on-year October

Source: Thomson Financial

0 15

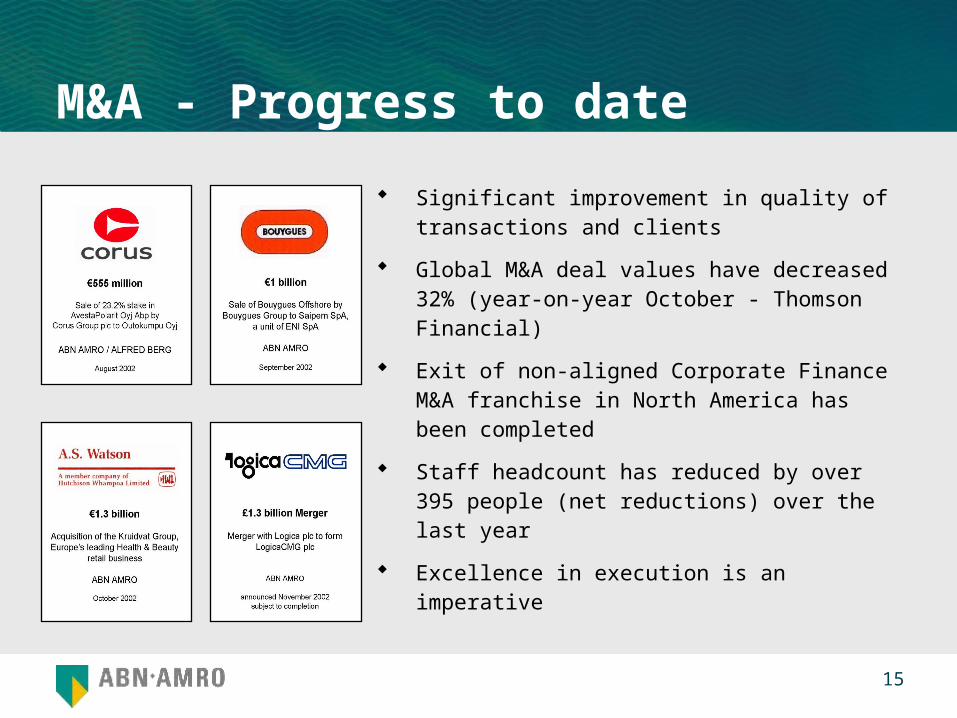

M&A - Progress to date

Significant improvement in quality of transactions and clients

Global M&A deal values have decreased 32% (year-on-year October - Thomson Financial)

Exit of non-aligned Corporate Finance M&A franchise in North America has been completed

Staff headcount has reduced by over 395 people (net reductions) over the last year

Excellence in execution is an imperative

0 16

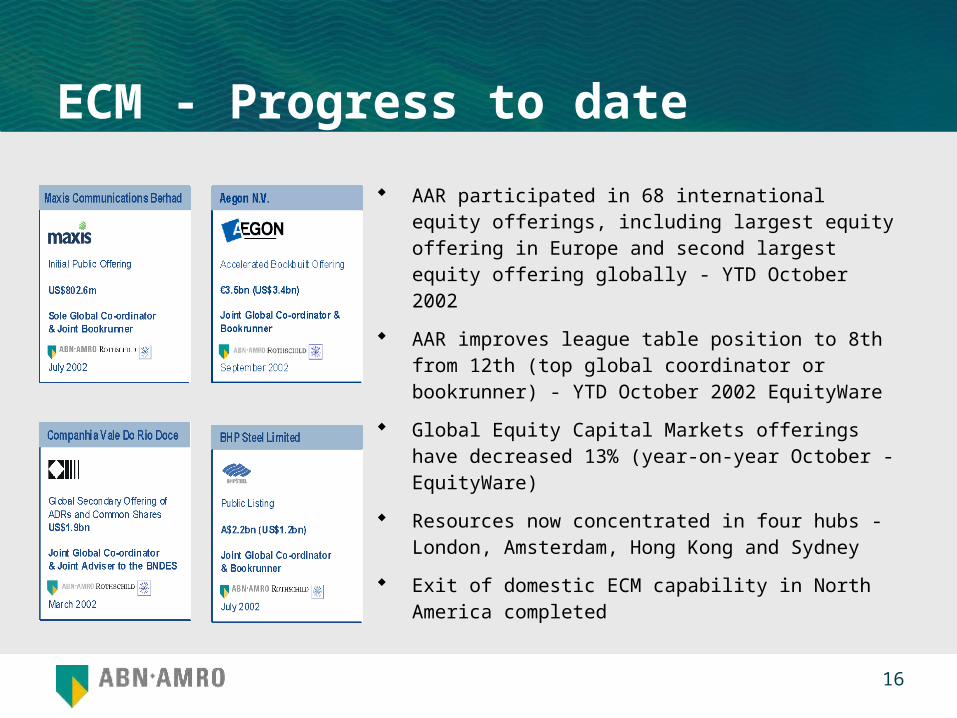

ECM - Progress to date

AAR participated in 68 international equity offerings, including largest equity offering in Europe and second largest equity offering globally - YTD October 2002

AAR improves league table position to 8th from 12th (top global coordinator or bookrunner) - YTD October 2002 EquityWare

Global Equity Capital Markets offerings have decreased 13% (year-on-year October - EquityWare)

Resources now concentrated in four hubs - London, Amsterdam, Hong Kong and Sydney

Exit of domestic ECM capability in North America completed

0 17

Improved Alignment For year 2002 - 75% of revenues delivered from Priority and Key

WCS clients (2001: 35% of revenues)

Successfully established a Corporate Finance M&A advisory joint

venture with C&CC in Brazil which will be the hub for our Latam

activities and also provide access to a large client base within Banco

Real

Interactive, intranet based global work-in-progress (launched

November 2001) used to measure director performance against

stated “Target Client Action Plans” (TCAP’s) targets

0 18

Critical Factors for Success Greater front-end delivery and client penetration required by client

coverage and corporate finance through continuous upgrade of staff (“self funded”)

Greater concentration on improving Primary revenues from existing client base

Continue to leverage our competitive advantages including:– European strength and geographic footprint– sector expertise– large client base– strategic use of balance sheet– professional team work and integrity

Maintain tight control of costs as we drive for bigger ticket revenues

Believe in ourselves and the benefits of AA’s partnership culture

20 November, 2002

Equities Nigel Turner, SEVP - Global Head of Equities BU

0 20

Restructuring Update Restructuring within Equities is now substantially complete with front

office restructuring costs already included within tight 2002 cost

targets

European research and trading to be focused into three hubs by

year end - Amsterdam, London and Stockholm

Research to be targeted and aligned to critical sectors and clients by

year end

Operating costs have been reduced by 32% (year 2001 compared

to forecast year 2002)

0 21

Restructuring Update Headcount has been reduced by approximately 35% during the year

(approximately 50% over the two year period - 2001/2002) to 1350

at year end

TOPS has delivered a “step change” in operating costs charged to

Equities

European market share is being maintained or increasing with peer

group suffering from larger percentage falls in revenue

0 22

Equities Overview Overall Equities goal of a top 5 to 7 position in both Pan-European

Secondary Equities - Research, Sales and Execution and Pan Asian Equities

Global distribution reach and capability with offices throughout Asia and in the US

– A comprehensive Pan-Asia/Australian product with sector and country based coverage providing full Research, Execution and Trading capabilities

Equity Derivatives - A core component of our Wholesale Clients strategy and skill base which is actively marketed to the full range of WCS client sectors. Distribution through C&CC retail network is of increasing significance

0 23

Research Research is an integral part of our Equity offering

We are building a Pan-European research franchise in core secondary market sectors

Our research franchise is closely aligned with the competitive advantages of AA

– Maintaining our existing competitive geographic advantages (UK, Netherlands, Nordic, Pan-European, Mid/Small Cap)

– Focusing on other sectors where we have, within AA, existing or potential competitive advantage - Financial Institutions, Technology, Media, Telecommunications, Healthcare, Integrated Energy, Consumer

0 24

Research Analysts are based in key hubs (London, Amsterdam, Stockholm,

Hong Kong and Sydney) with hires already made in some targeted research areas - Media, Support Services, Banking, Real Estate

A clear determination to produce value-added research

Maintain integrity of research

Improvements to recommendations process will give greater transparency and accountability

Examples of recent successes (Pan-European Thomson Extel 2002)

– 5th most improved research service; 3rd position in AQ Pan European Accuracy survey; 3 AA analysts in top 20 in Rising Star category

0 25

Sales Three European home markets (Netherlands, UK, Nordic) give

unusually strong platform

Focus on clients and a flexible distribution platform to meet their needs. Linkage with other WCS products through FIPS client coverage to be improved

Global distribution network (US, Asia/Australia); European Sales Team is 150 strong and continues to be upgraded

Examples of recent successes (Pan-European Thomson Extel 2002 survey) include

– 7th, Pan-European brokerage sales; 5th, market knowledge “and feel”

– 4th, most improved firm for sales service; 3rd, independent ideas

0 26

Sales Trading and Trading A programme to introduce more automated order execution

functionality

To capture internal liquidity to improve trading efficiency

Aim to boost the role of program trading

Aim to widen our client base by offering new, advanced execution

products

Employ high calibre, motivated traders and sales traders (180

professionals in Europe)

Short term goal to be in a top 5 to 7 position in European execution,

providing an effective, cost efficient service to clients

0 27

Derivatives A core component of strategy for WCS, no longer seen as just a

niche product. Key product in deriving further synergies and

increased linkages with C&CC and its retail distribution network

Improving our ability to cross-sell retail derivative products into key

markets (e.g. Germany, Italy, the Netherlands and US) with

improved linkages to C&CC retail distribution network

A greater synergy between cash and derivative groups to meet the

changing needs of clients and improve our trading capabilities

Increased investment in trading systems

0 28

Equity Capital Markets Full range of Equity Capital Market (“ECM”)

services are offered through leading recognised brand ABN AMRO Rothschild (“AAR”)

– AA provides full suite of investment banking products, capital strength and global distribution power while Rothschild provide additional relationships and skills in key markets

AAR consistently ranked in the top 5 in Europe; also improved to 8th from 12th on a global basis (top global co-ordinator or bookrunner - YTD October 2002 EquityWare)

For the market as a whole global ECM offerings have decreased 13% (year-on-year October - EquityWare)

0 29

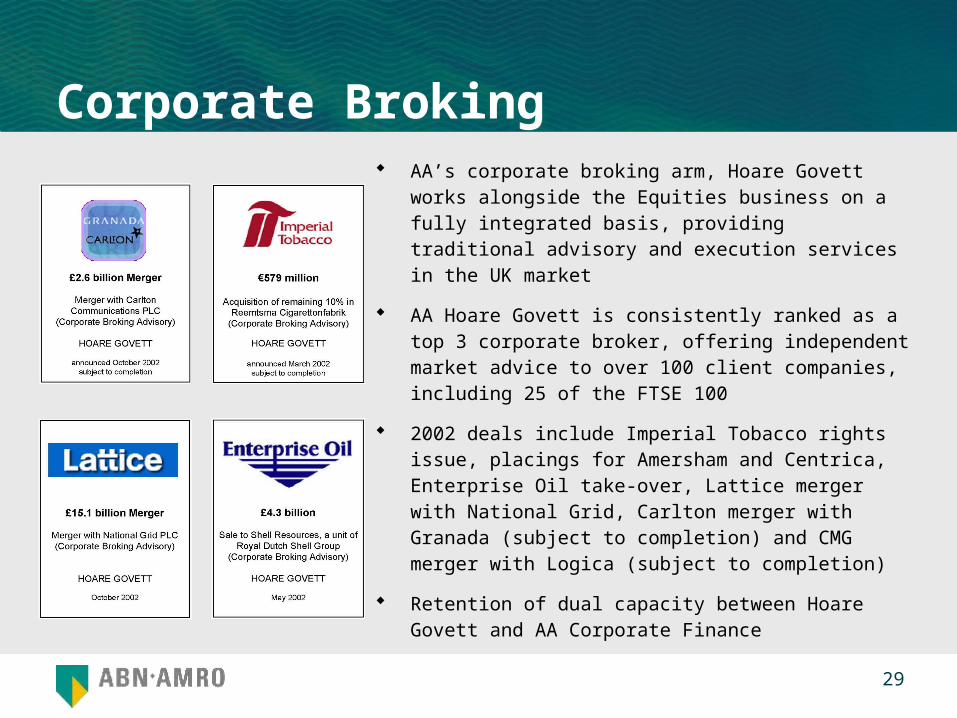

Corporate Broking AA’s corporate broking arm, Hoare Govett works

alongside the Equities business on a fully integrated basis, providing traditional advisory and execution services in the UK market

AA Hoare Govett is consistently ranked as a top 3 corporate broker, offering independent market advice to over 100 client companies, including 25 of the FTSE 100

2002 deals include Imperial Tobacco rights issue, placings for Amersham and Centrica, Enterprise Oil take-over, Lattice merger with National Grid, Carlton merger with Granada (subject to completion) and CMG merger with Logica (subject to completion)

Retention of dual capacity between Hoare Govett and AA Corporate Finance

0 30

Critical Factors for Success Drivers of future revenue growth within Equities will include pension

reforms particularly in continental Europe, venture capital,

corporates demanding a full product range and hedge funds

Continued structured investment in key research sectors to improve

rankings for our European and Asian products in order to generate

increased allocation of revenue from target clients

Higher quality execution and service penetration of Priority client

base at all levels

Equity markets have now fallen to a cyclical low. AA’s Equities

business will be in good shape to benefit from any improvement in

underlying markets

Technology, Operations and Property Services (TOPS)

Ron Teerlink, SEVP - Global Head of TOPS BU and WCS COO

20 November, 2002

0 32

TOPS have established a simple agenda to help focus decision making

Clients’ Perception of Services

Our People

Economic Value Operational risk

Contribute to value creation primarily through lowering the cost of support service

provision

Minimise operational losses and allow WCS to maximise

capital efficiency through advanced level compliance

Lead by example, seek best people, address performance issues and foster a

performance culture

Be a partner with clients, respond to feedback, be accountable and

transparent

Strategic agenda

0 33

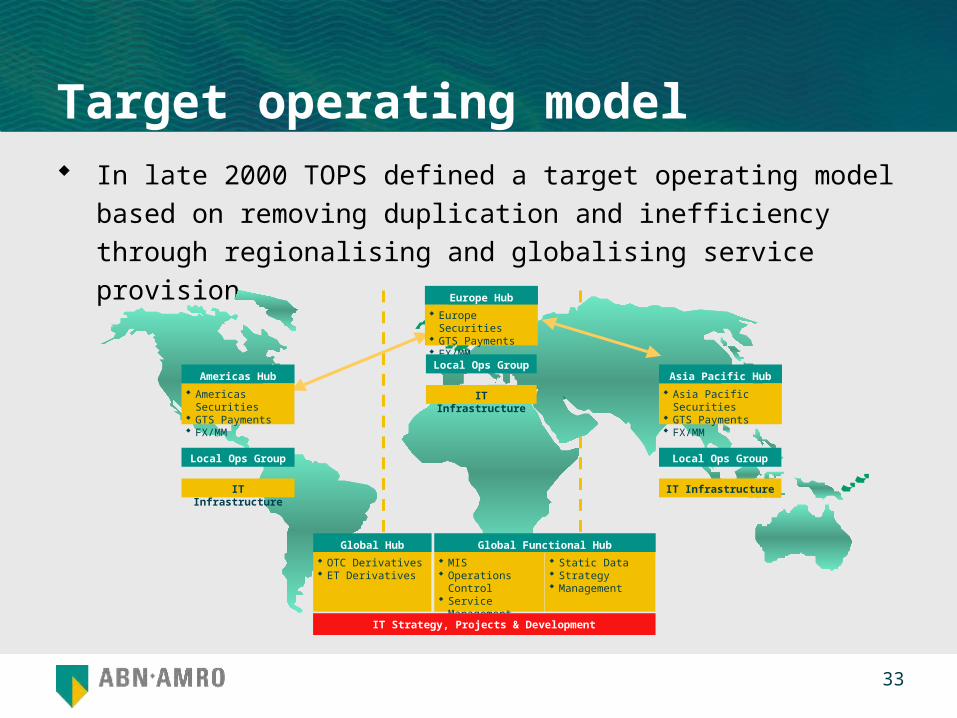

Target operating model In late 2000 TOPS defined a target operating model based on

removing duplication and inefficiency through regionalising and

globalising service provision …

Americas Hub

Americas Securities GTS Payments FX/MM

Local Ops Group

IT Infrastructure

Europe Hub

Europe Securities GTS Payments FX/MM

Local Ops Group

IT Infrastructure

Asia Pacific Hub

Asia Pacific Securities GTS Payments FX/MM

Local Ops Group

IT Infrastructure

Global Hub

OTC Derivatives ET Derivatives

Global Functional Hub

MIS Operations Control Service

Management

IT Strategy, Projects & Development

Static Data Strategy Management

0 34

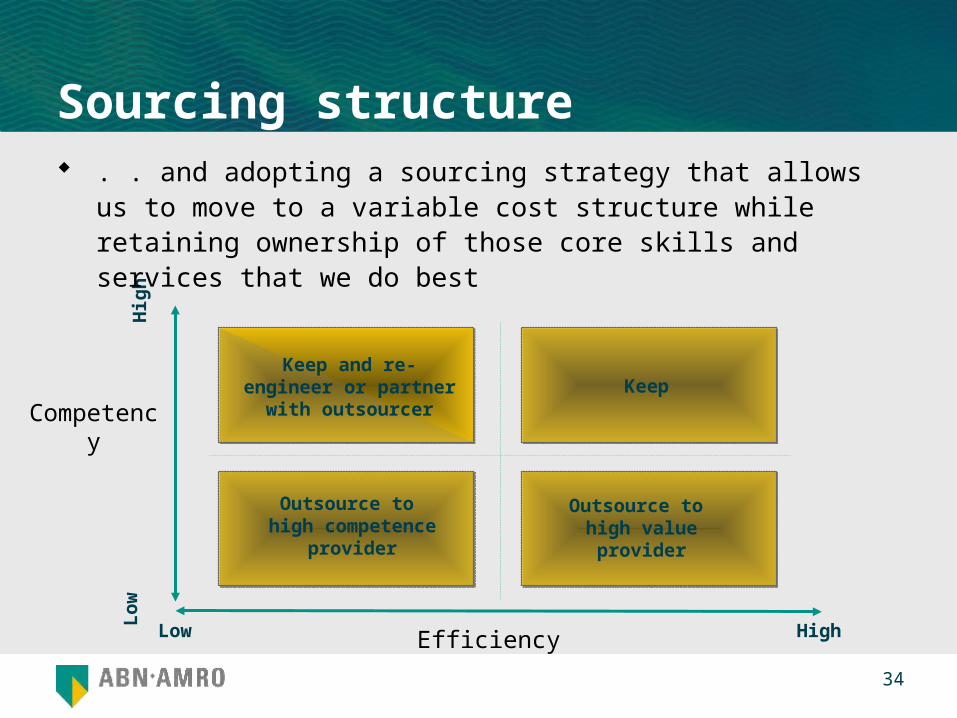

- Potential Sourcing Model -

Competitive Advantage

Outsource to high value provider

Keep

Outsource to high competence

provider

Keep and re-engineer or partner with outsourcer

Current Capability Level

Hig

hL

ow

Low High

Sourcing structure . . and adopting a sourcing strategy that allows us to move to a

variable cost structure while retaining ownership of those core skills and services that we do best

Efficiency

Competency

0 35

High profile programmesWe have successfully implemented a number of high profile

programmes over the past 24 months which have enabled us to

dramatically lower our cost base and headcount

Hubbing of European Capital Markets Operations in London and

closure of units in Amsterdam, Paris, Frankfurt, Zurich, Milan

Hubbing of Derivatives Operations in London

Hubbing of European Treasury Operations in Amsterdam and closure of units in Stockholm, London, Paris and Frankfurt

Hubbing of AsiaPac & EMEA Nostro Reconciliations in London

Hubbing in US and Asia

0 36

High profile programmes (cont’d) Consolidation of European Technology Infrastructure in Amsterdam

and London and reduction of application duplication

More efficient use of office space, improved transparency of occupancy across all major locations, moves to lower cost locations in major financial centres including New York, Frankfurt & Singapore

Renegotiated contract pricing and other procurement initiatives

We will leverage these experiences for the group by consolidating Procurement, Real Estate Portfolio Management and Sourcing Strategy in Corporate Centre

0 37

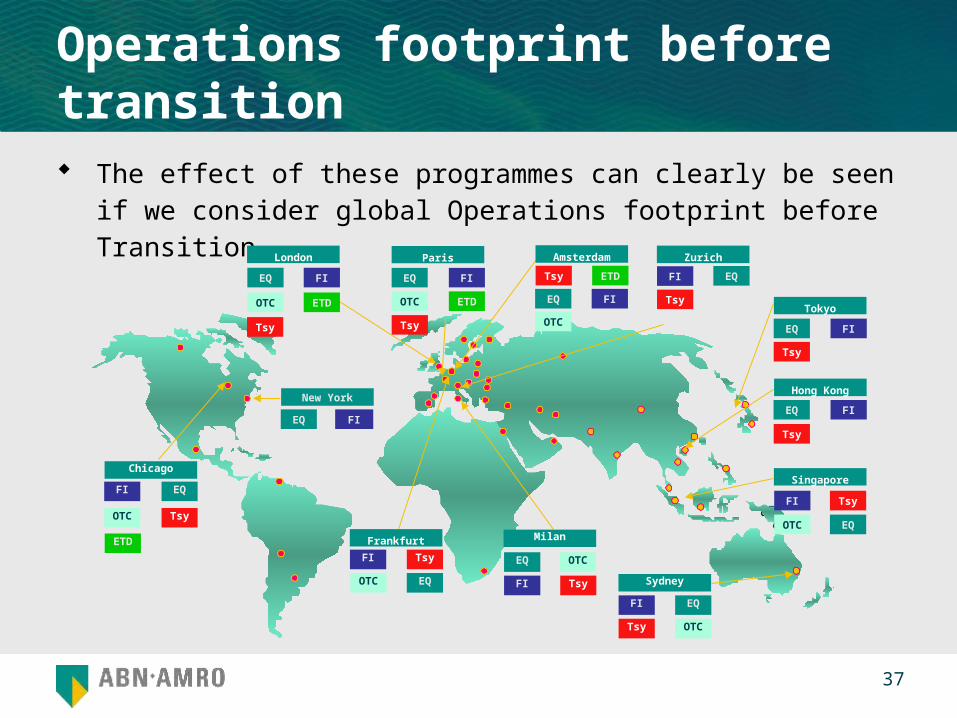

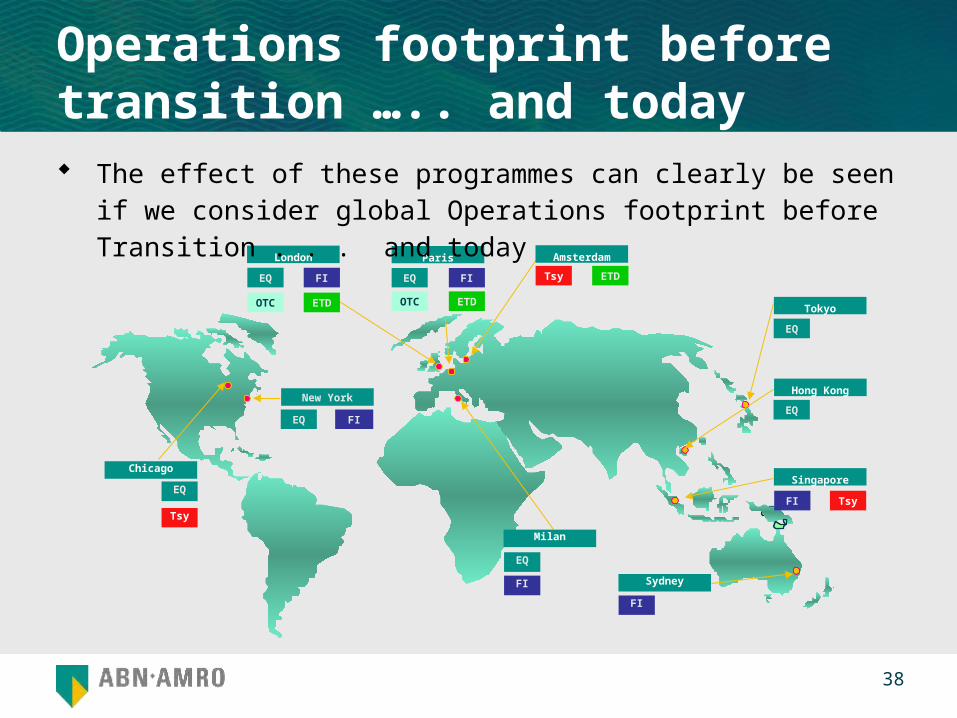

Operations footprint before transition The effect of these programmes can clearly be seen if we consider

global Operations footprint before Transition

Tsy

Tokyo

Hong Kong

Singapore

ParisLondon

EQ FI

OTC ETD

Tsy

EQ FI

OTC

Zurich

FI EQ

Tsy

EQ FI

Tsy

Frankfurt

FI Tsy

OTC

Sydney

EQFI

Tsy OTC

FI Tsy

OTC

Milan

EQ OTC

FI Tsy

Chicago

FI EQ

OTC Tsy

ETD

ETD

EQ

New York

EQ FI

Tsy

Amsterdam

EQ FI

OTC

ETD

EQ

Tsy

EQ

FI

0 38

Tokyo

Hong Kong

Singapore

ParisLondon

EQ FI

OTC ETD

EQ FI

OTC

EQ

FI Tsy

Sydney

FI

Milan

EQ

FI

Chicago

EQ

Tsy

ETD

New York

EQ FI

Tsy

Amsterdam

ETD

EQ

Operations footprint before transition ….. and today The effect of these programmes can clearly be seen if we consider

global Operations footprint before Transition . . . and today

0 39

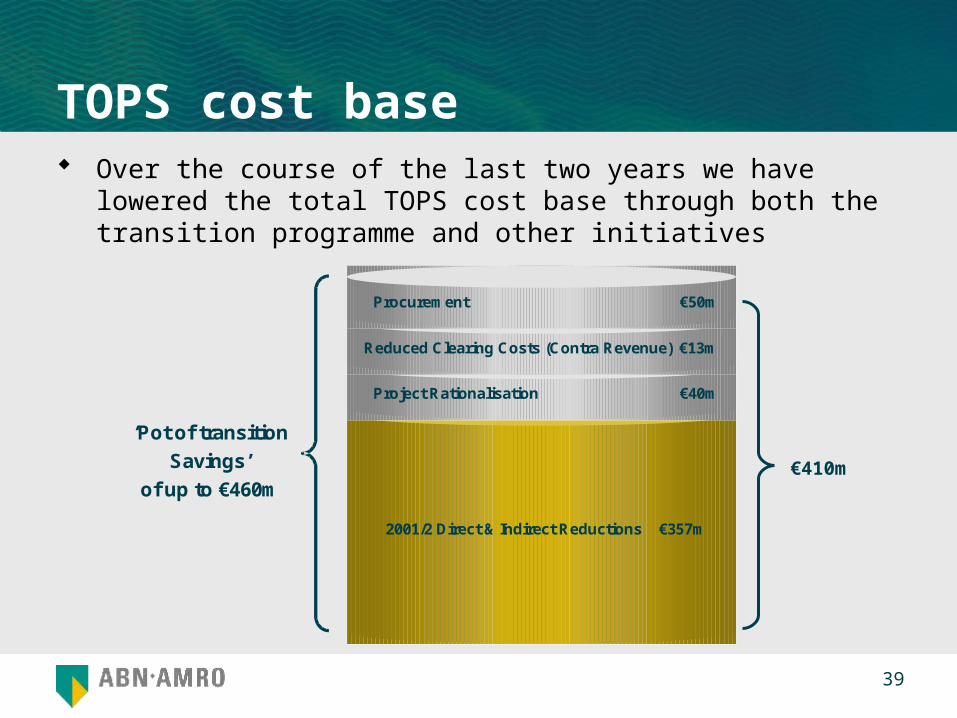

TOPS cost base Over the course of the last two years we have lowered the total

TOPS cost base through both the transition programme and other initiatives

€410m

2001/2 Direct & Indirect Reductions €357m

‘Pot of transition

Savings’

of up to €460m

Project Rationalisation €40m

Reduced Clearing Costs (Contra Revenue) €13m

Procurement €50m

0 40

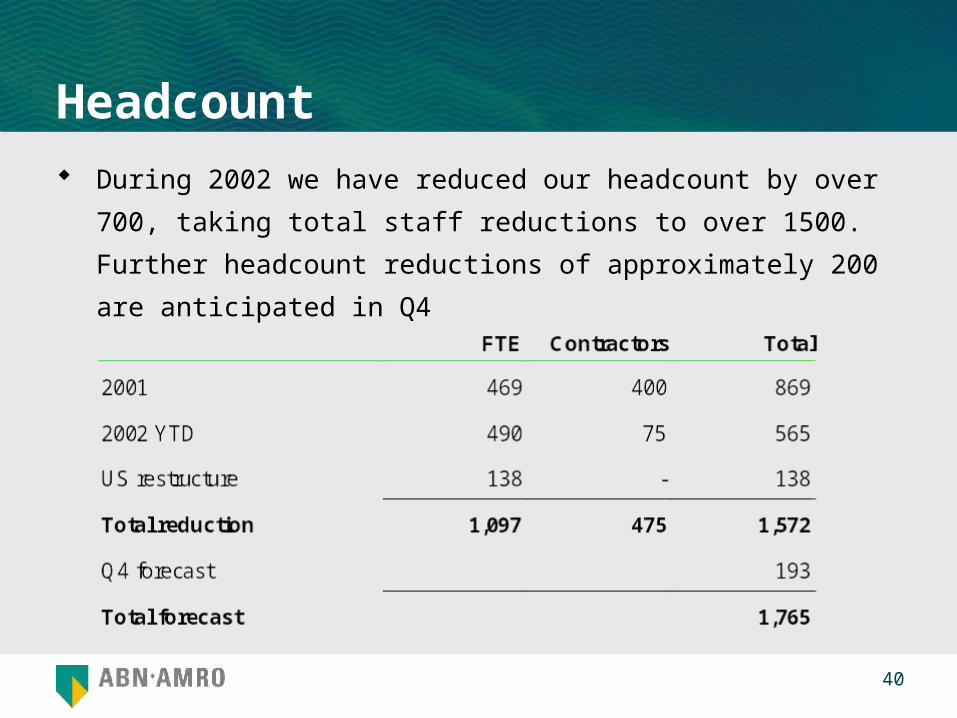

Headcount During 2002 we have reduced our headcount by over 700, taking

total staff reductions to over 1500. Further headcount reductions of

approximately 200 are anticipated in Q4

0 41

Cost Cost reductionFlexibility Flexible cost baseControl Strong governance and greater transparencyProductivity Continuous improvement of productivityQuality Deliver industry best practice processes

Closing with EDS expected before the end of 2002Transfer of 1000+ staff in NL, UK, US, Germany, Singapore, Hong KongSavings to materialise starting 2004 (0 impact in 2003)

5 Key objectives

Outsourcing to EDS Through outsourcing large components of technology to EDS we

plan to make a step change in the cost and quality of service

provision

0 42

Summary TOPS has established a simple strategic agenda to help focus

decision making; Clients, Value, People, Risk

In late 2000 TOPS defined a target operating model based on

removing duplication and inefficiency through regionalising and

globalising service provision

. . and adopting a sourcing strategy that allows us to move to a

variable cost structure while retaining ownership of those core skills

and services that we do best

We have successfully implemented a number of high profile

programmes over the past 24 months which have enabled us to

dramatically lower our cost base and headcount

0 43

Summary (cont’d) When taken together the ‘total pot’ of transition savings delivered by

TOPS this year is in excess of €460m

This compares favourably with our commitments at the start of the

Programme to deliver €408m of savings to the P&L by the end of

2002

During 2002 we have reduced our headcount by over 700, taking

total staff reductions to over 1500. Further headcount reductions of

approximately 200 are anticipated in Q4

We will continue to focus on managing down our costs and

headcount in Q4 and into 2003