Embed Size (px)

Citation preview

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

GLOBAL INTEREST

RATES: DISLOCATIONS

AND OPPORTUNITIES

MAY // 2 // 2017

Francesco Tonin, Bloomberg

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

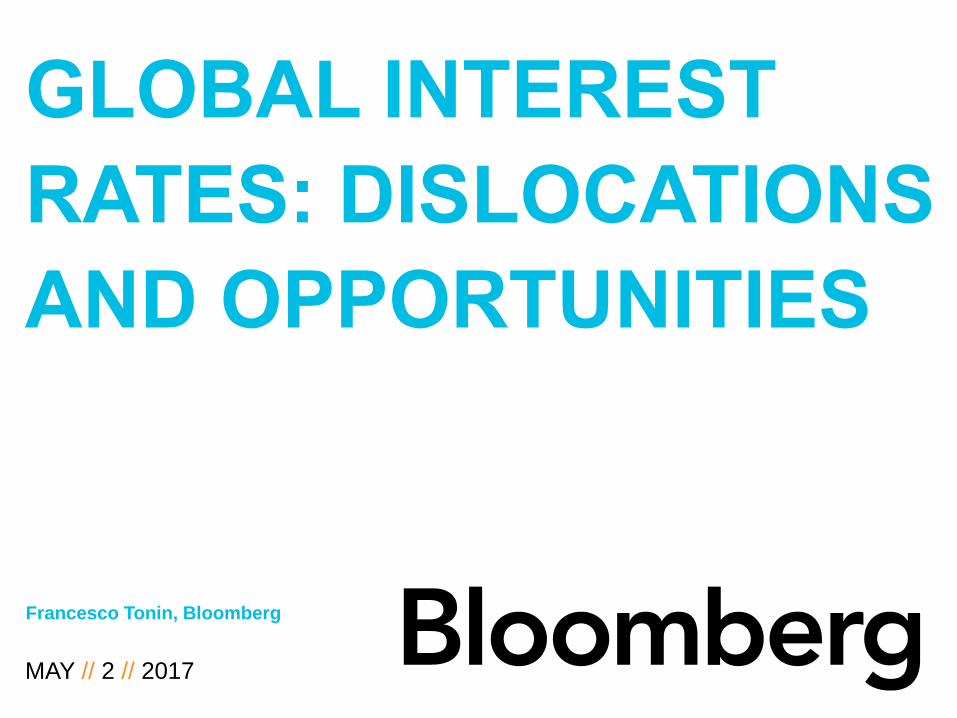

JAPANIFICATION OF TREASURIES2

Dislocations in the relation between US rates and Japanese rates has

eliminated the appeal for Japanese investors willing to purchase US debt and

synthetically turn it into Japanese cash flows

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

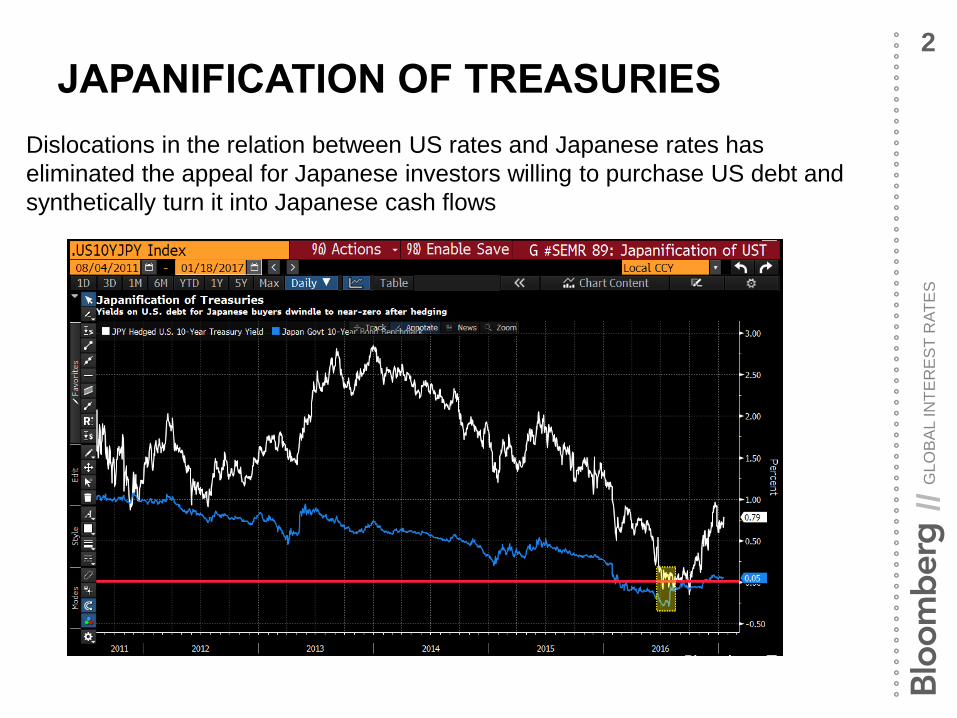

TO A US INVESTOR, JAPANESE T-BILLS YIELD MORE THAN US T-BILLS

3

A US investor can purchase Japanese T-Bills and swap all the cash flows into

dollar cash flows, thus achieving a yield of 1.22% which is higher than US T-

Bills

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

TO A EUR INVESTOR, ANY YIELD PICK UP IS BETTER THAN NOTHING

4

Euro investors starved for yield have turned to USD debt but of recent the yield

pick up has dwindled to zero

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

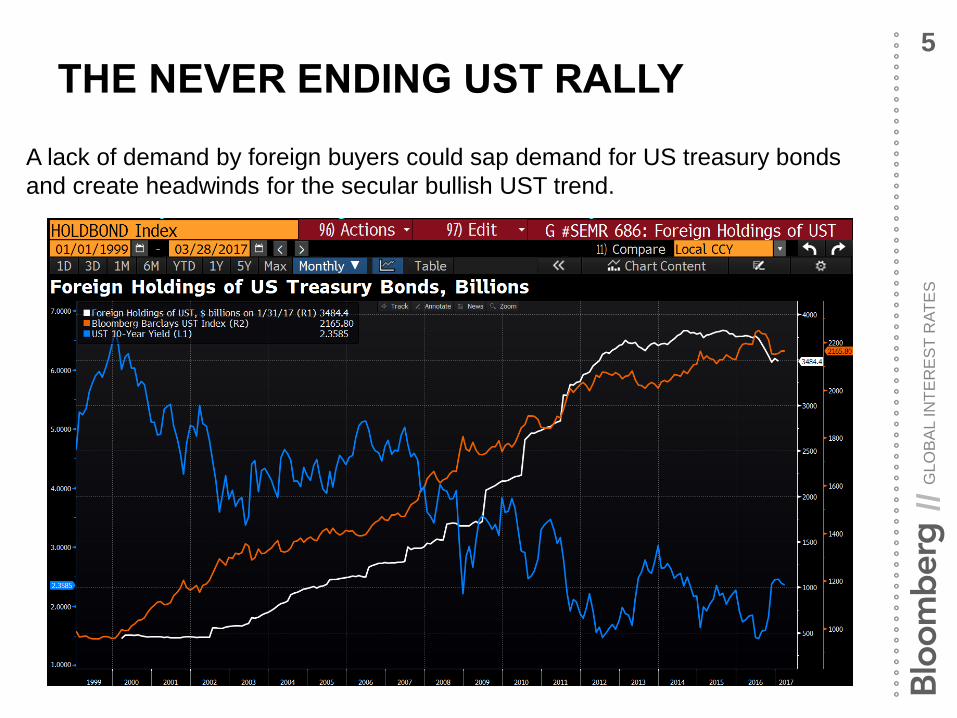

THE NEVER ENDING UST RALLY5

A lack of demand by foreign buyers could sap demand for US treasury bonds

and create headwinds for the secular bullish UST trend.

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

THE NEVER ENDING UST RALLY6

Here we show the impact of the Trump trade.

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

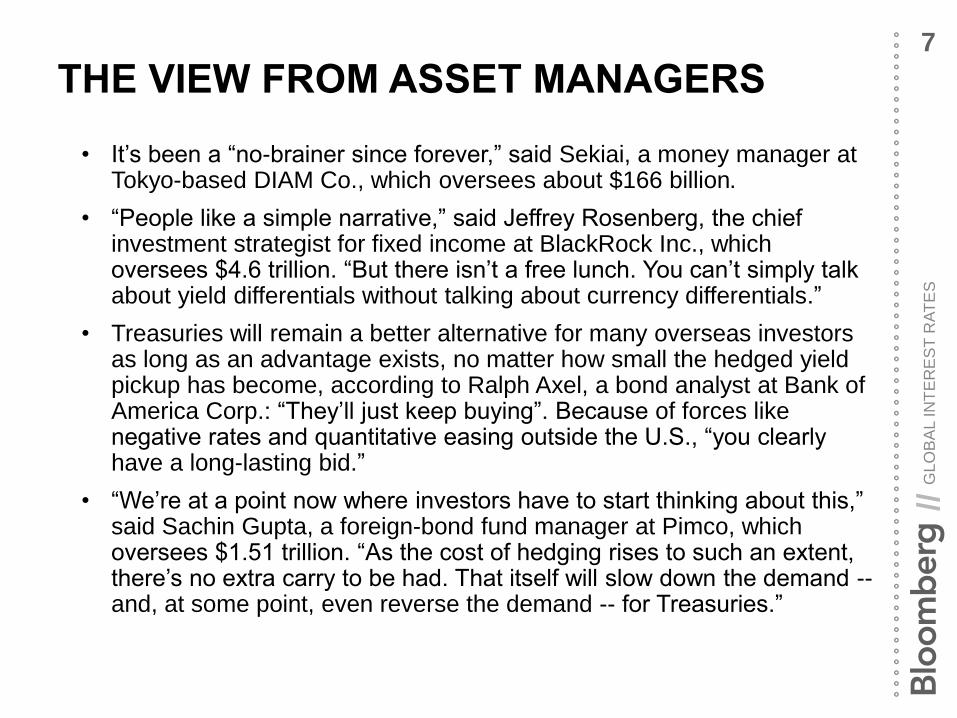

THE VIEW FROM ASSET MANAGERS7

• It’s been a “no-brainer since forever,” said Sekiai, a money manager at Tokyo-based DIAM Co., which oversees about $166 billion.

• “People like a simple narrative,” said Jeffrey Rosenberg, the chief investment strategist for fixed income at BlackRock Inc., which oversees $4.6 trillion. “But there isn’t a free lunch. You can’t simply talk about yield differentials without talking about currency differentials.”

• Treasuries will remain a better alternative for many overseas investors as long as an advantage exists, no matter how small the hedged yield pickup has become, according to Ralph Axel, a bond analyst at Bank of America Corp.: “They’ll just keep buying”. Because of forces like negative rates and quantitative easing outside the U.S., “you clearly have a long-lasting bid.”

• “We’re at a point now where investors have to start thinking about this,” said Sachin Gupta, a foreign-bond fund manager at Pimco, which oversees $1.51 trillion. “As the cost of hedging rises to such an extent, there’s no extra carry to be had. That itself will slow down the demand --and, at some point, even reverse the demand -- for Treasuries.”

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

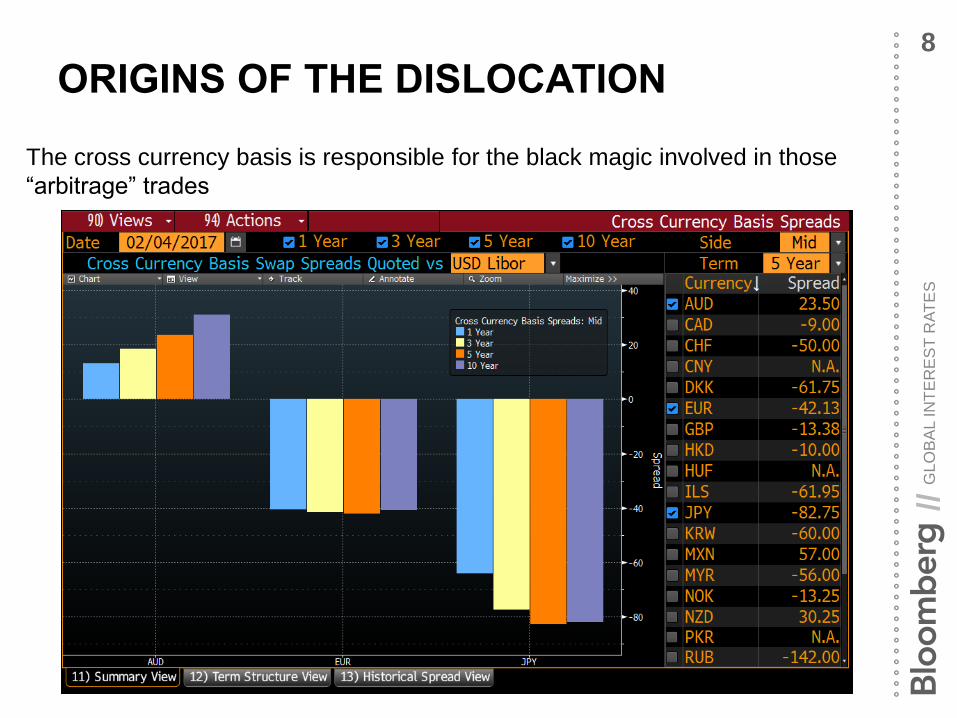

ORIGINS OF THE DISLOCATION8

The cross currency basis is responsible for the black magic involved in those

“arbitrage” trades

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

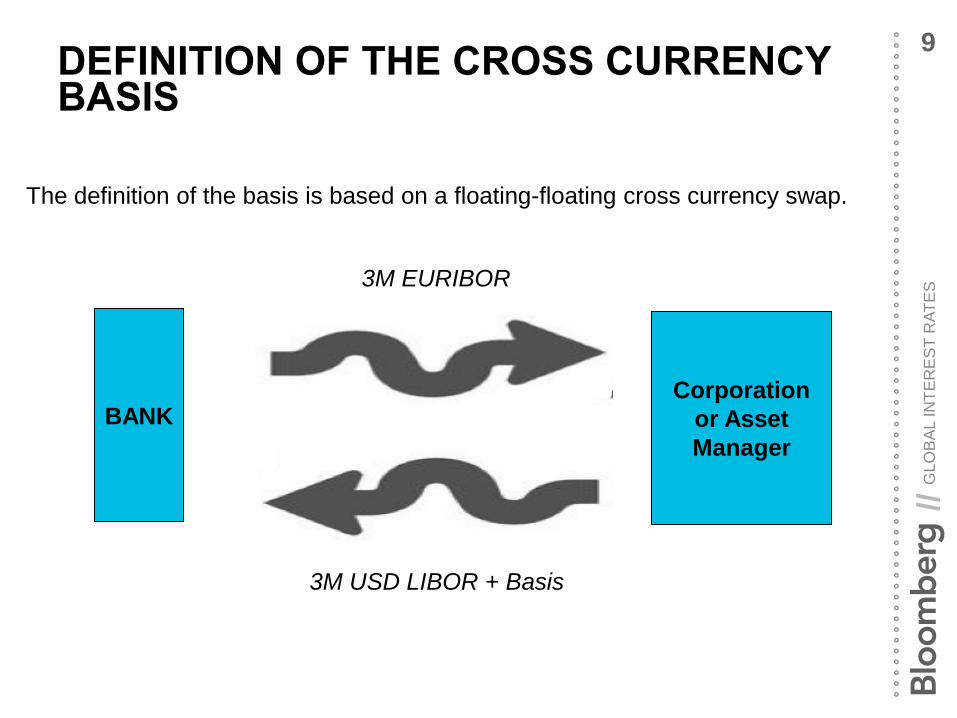

DEFINITION OF THE CROSS CURRENCY BASIS

9

The definition of the basis is based on a floating-floating cross currency swap.

BANKCorporation

or Asset

Manager

3M EURIBOR

3M USD LIBOR + Basis

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

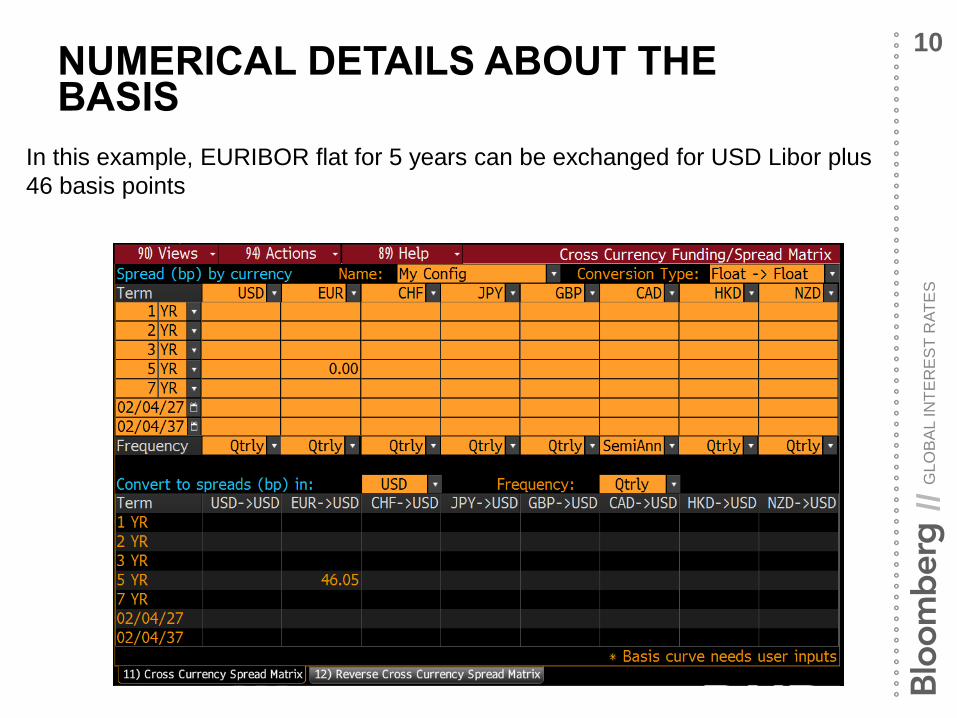

NUMERICAL DETAILS ABOUT THE BASIS

10

In this example, EURIBOR flat for 5 years can be exchanged for USD Libor plus

46 basis points

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

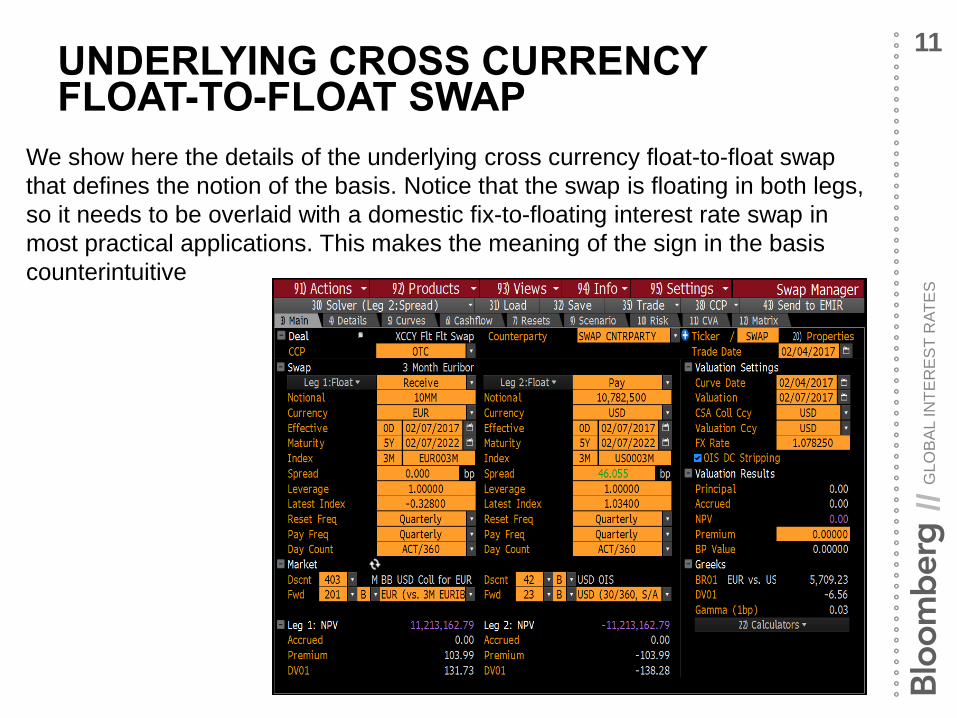

UNDERLYING CROSS CURRENCY FLOAT-TO-FLOAT SWAP

11

We show here the details of the underlying cross currency float-to-float swap

that defines the notion of the basis. Notice that the swap is floating in both legs,

so it needs to be overlaid with a domestic fix-to-floating interest rate swap in

most practical applications. This makes the meaning of the sign in the basis

counterintuitive

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

UNDERLYING CROSS CURRENCY FLOAT-TO-FLOAT SWAP

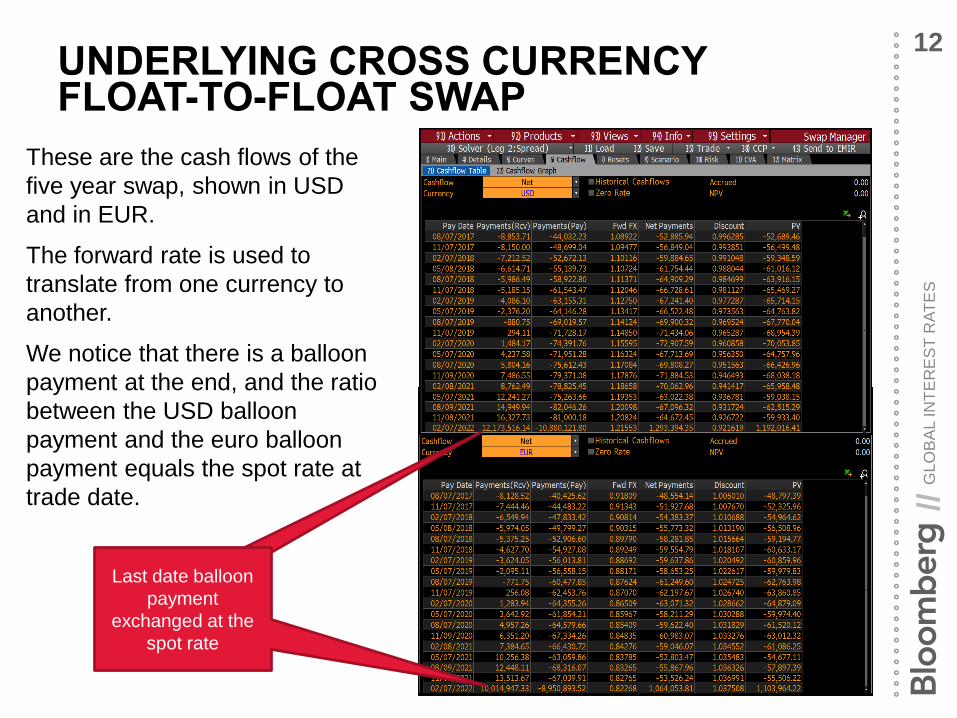

12

These are the cash flows of the

five year swap, shown in USD

and in EUR.

The forward rate is used to

translate from one currency to

another.

We notice that there is a balloon

payment at the end, and the ratio

between the USD balloon

payment and the euro balloon

payment equals the spot rate at

trade date.

Last date balloon

payment

exchanged at the

spot rate

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

MEASURES OF STRESS IN THE FINANCIAL SECTOR

13

The LIBOR-OIS spread, or LOIS, is a measure of fragility in the banking sector

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

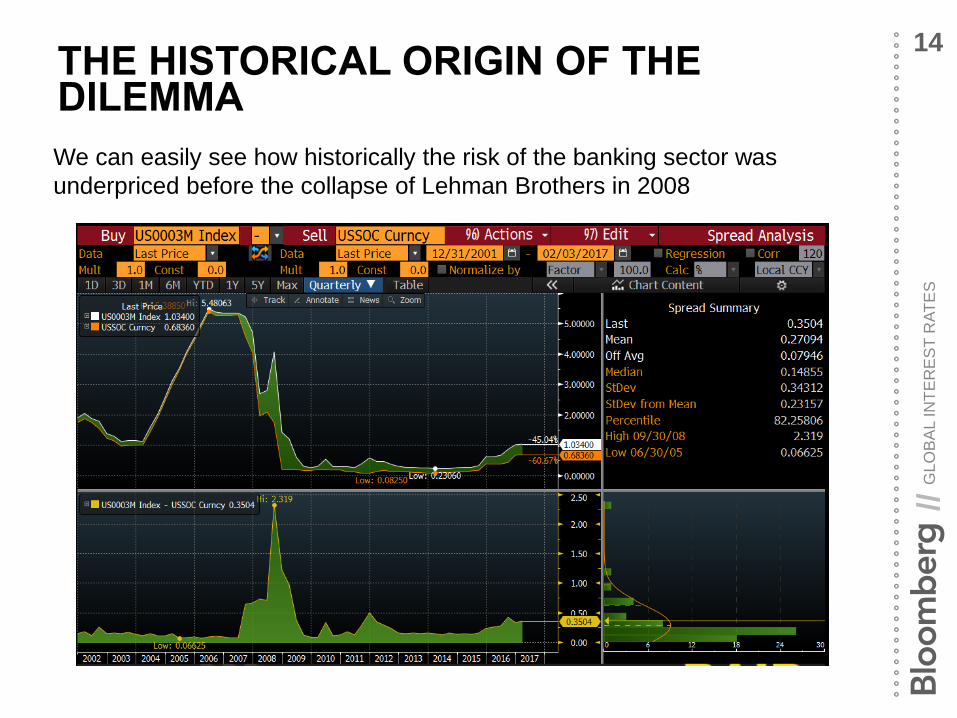

THE HISTORICAL ORIGIN OF THE DILEMMA

14

We can easily see how historically the risk of the banking sector was

underpriced before the collapse of Lehman Brothers in 2008

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

MAIN CHART THAT TELLS THE WHOLE STORY

15

Here is the chart of the EURUSD 1y (EURBS1 Curncy) and USDJPY 1y

(JYBS1 Curncy) cross currency basis. Note the basis is a negative number.

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

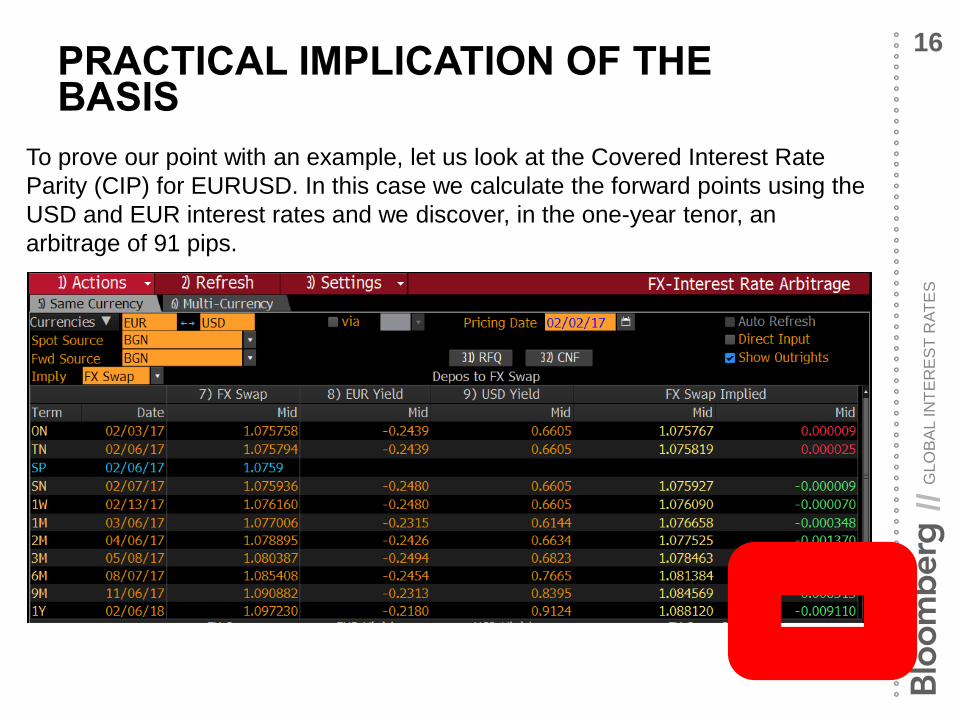

PRACTICAL IMPLICATION OF THE BASIS

16

To prove our point with an example, let us look at the Covered Interest Rate

Parity (CIP) for EURUSD. In this case we calculate the forward points using the

USD and EUR interest rates and we discover, in the one-year tenor, an

arbitrage of 91 pips.

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

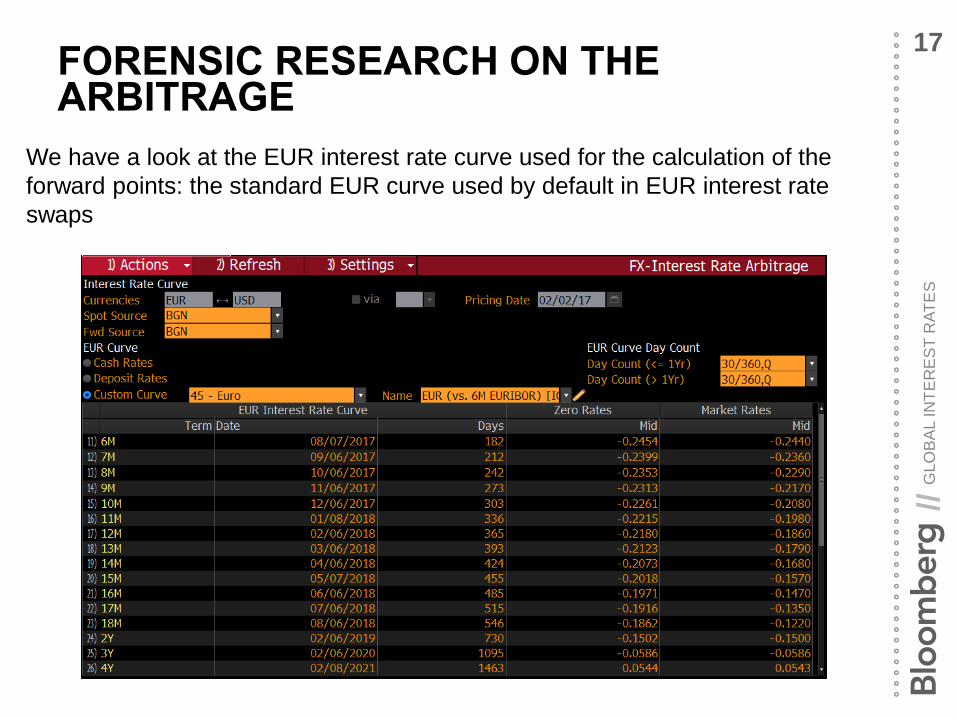

FORENSIC RESEARCH ON THE ARBITRAGE

17

We have a look at the EUR interest rate curve used for the calculation of the

forward points: the standard EUR curve used by default in EUR interest rate

swaps

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

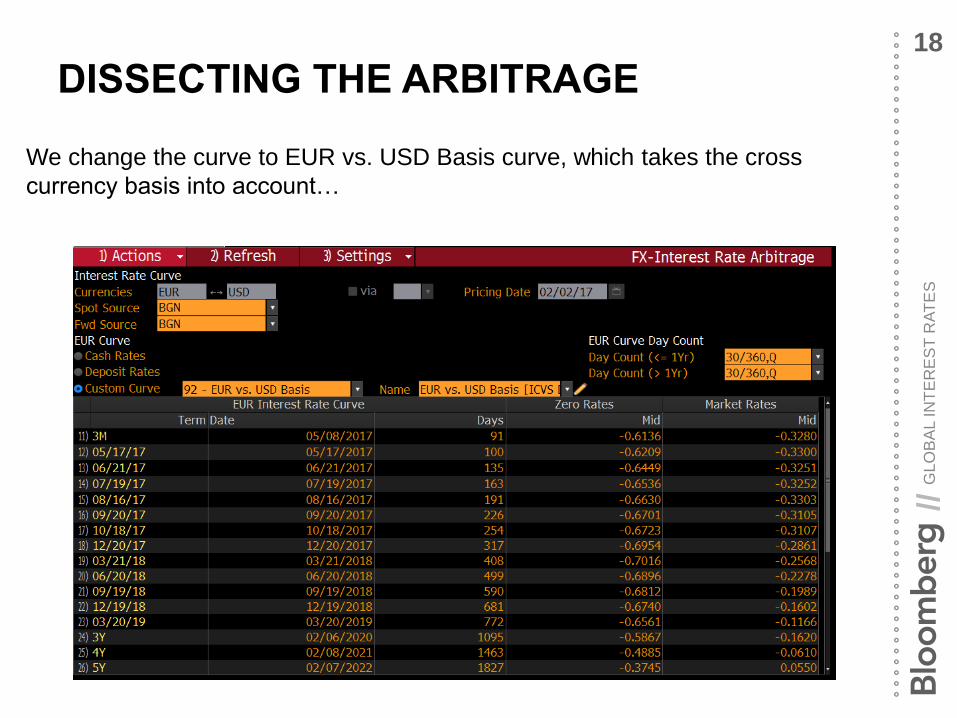

DISSECTING THE ARBITRAGE18

We change the curve to EUR vs. USD Basis curve, which takes the cross

currency basis into account…

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

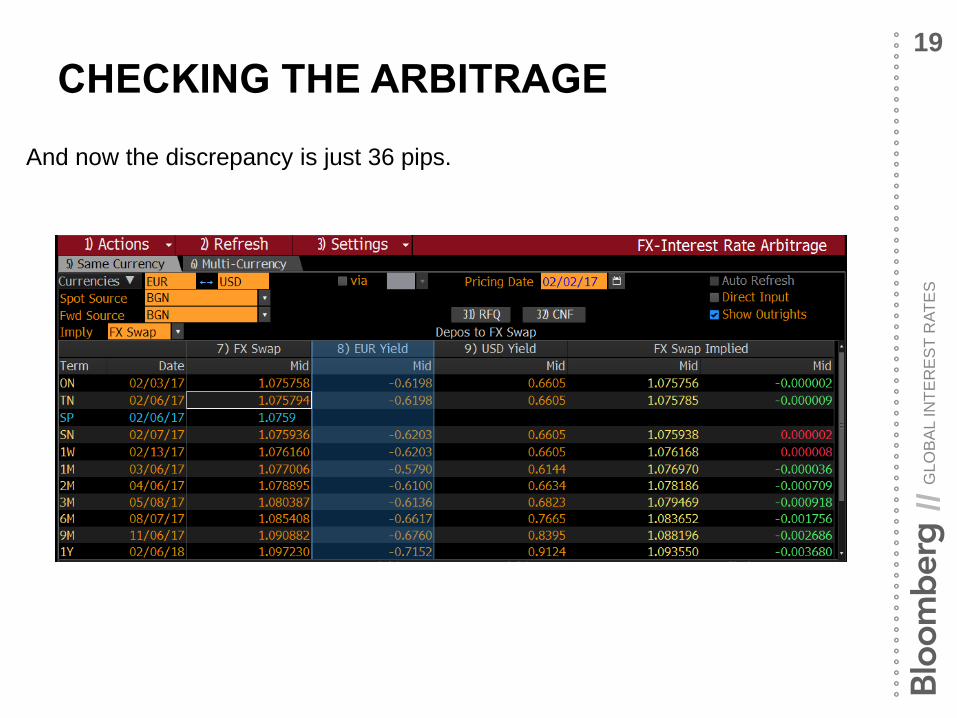

CHECKING THE ARBITRAGE19

And now the discrepancy is just 36 pips.

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

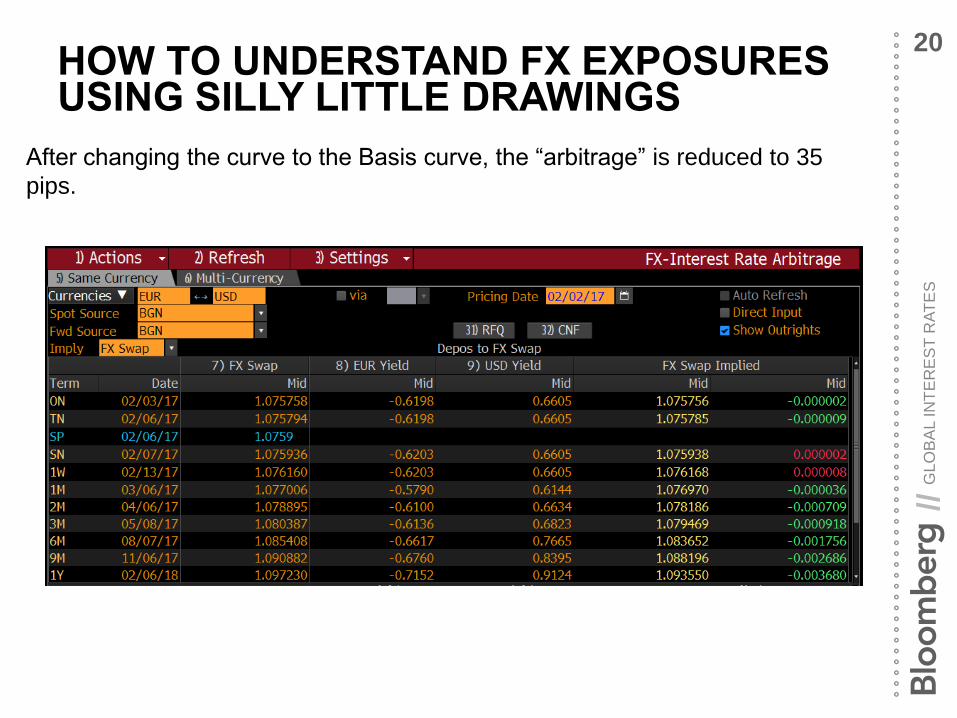

HOW TO UNDERSTAND FX EXPOSURES USING SILLY LITTLE DRAWINGS

20

After changing the curve to the Basis curve, the “arbitrage” is reduced to 35

pips.

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

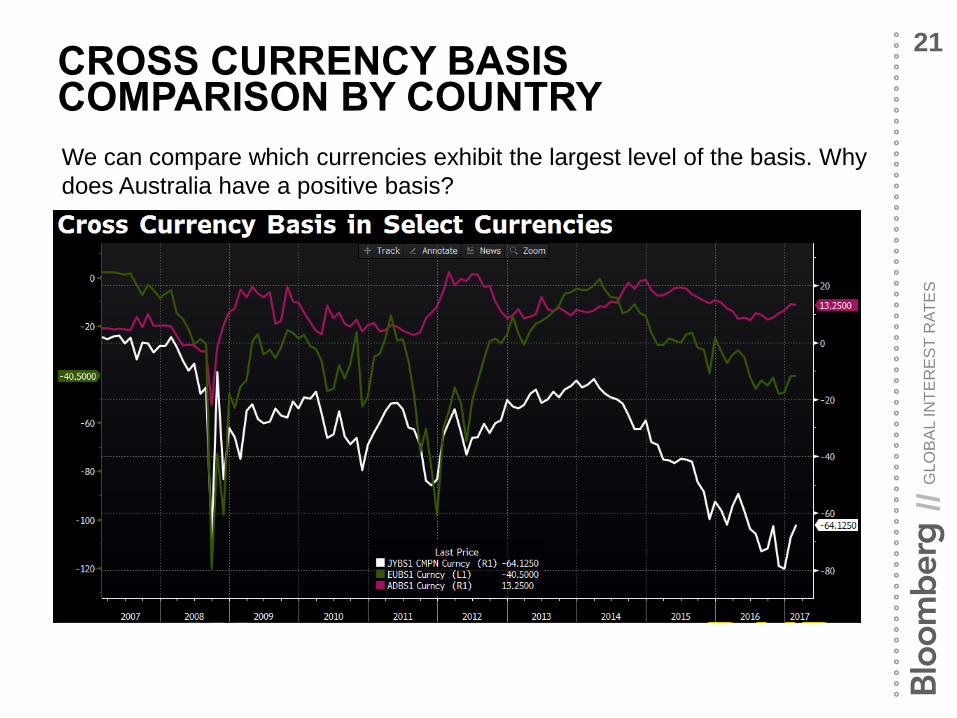

CROSS CURRENCY BASIS COMPARISON BY COUNTRY

21

We can compare which currencies exhibit the largest level of the basis. Why

does Australia have a positive basis?

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

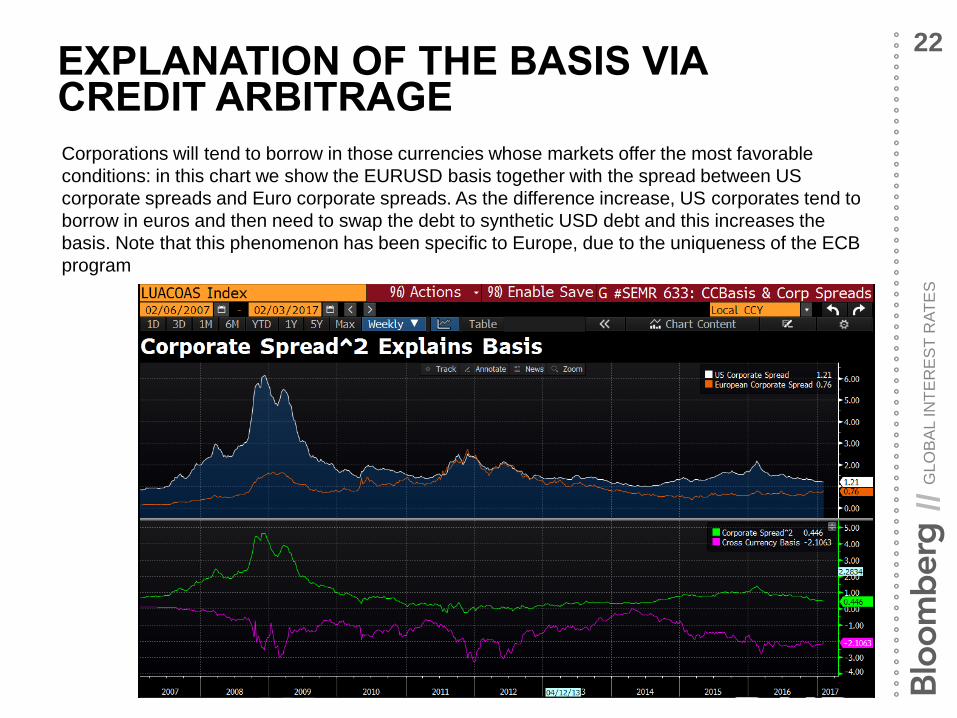

EXPLANATION OF THE BASIS VIA CREDIT ARBITRAGE

22

Corporations will tend to borrow in those currencies whose markets offer the most favorable

conditions: in this chart we show the EURUSD basis together with the spread between US

corporate spreads and Euro corporate spreads. As the difference increase, US corporates tend to

borrow in euros and then need to swap the debt to synthetic USD debt and this increases the

basis. Note that this phenomenon has been specific to Europe, due to the uniqueness of the ECB

program

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

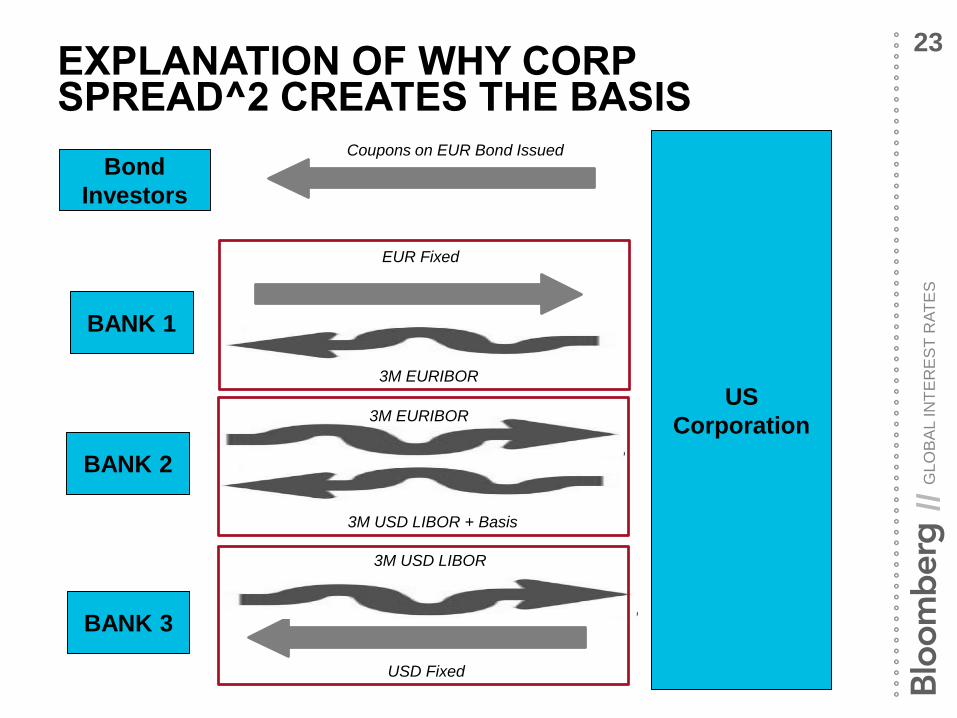

EXPLANATION OF WHY CORPSPREAD^2 CREATES THE BASIS

23

Bond

Investors

US

Corporation

3M EURIBOR

3M USD LIBOR + Basis

3M EURIBOR

3M USD LIBOR

USD Fixed

EUR Fixed

Coupons on EUR Bond Issued

BANK 1

BANK 2

BANK 3

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

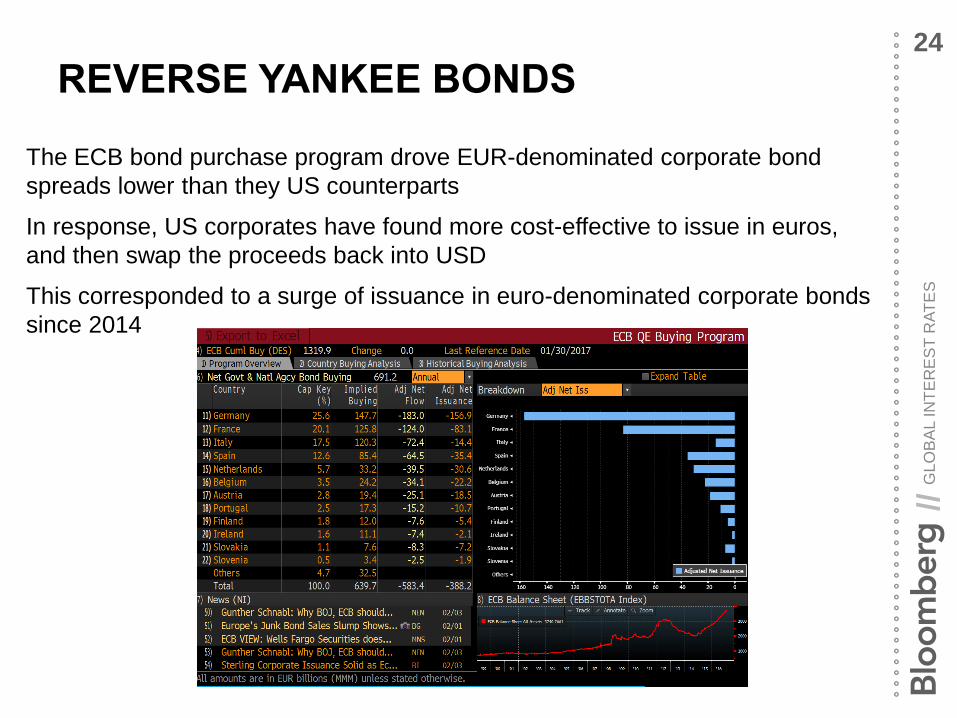

REVERSE YANKEE BONDS24

The ECB bond purchase program drove EUR-denominated corporate bond

spreads lower than they US counterparts

In response, US corporates have found more cost-effective to issue in euros,

and then swap the proceeds back into USD

This corresponded to a surge of issuance in euro-denominated corporate bonds

since 2014

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

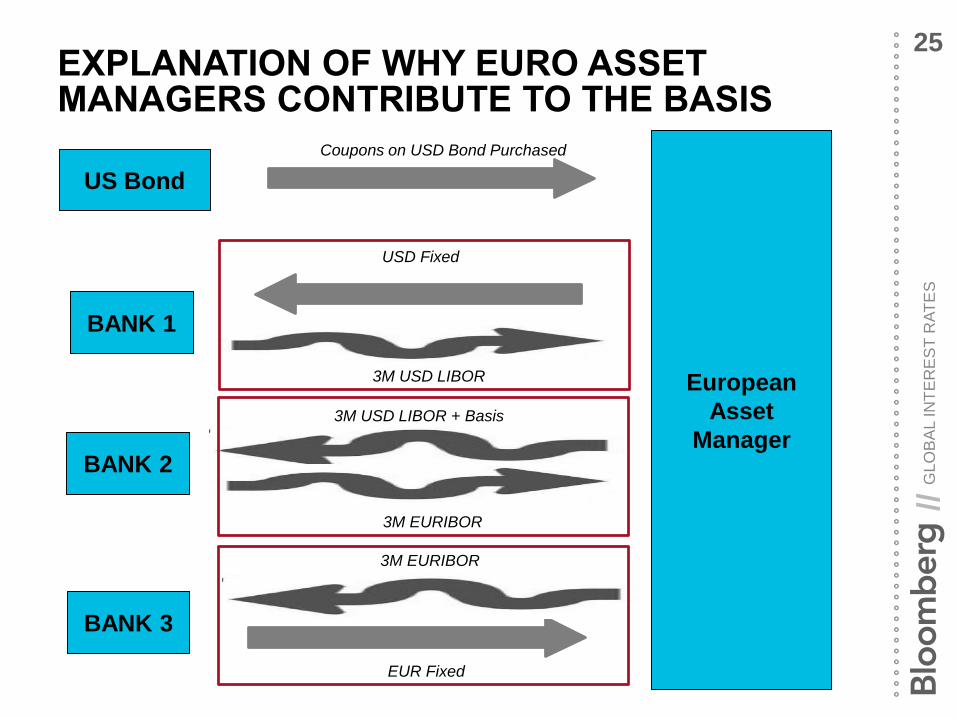

EXPLANATION OF WHY EURO ASSET MANAGERS CONTRIBUTE TO THE BASIS

25

US Bond

European

Asset

Manager

3M USD LIBOR

3M EURIBOR

3M USD LIBOR + Basis

3M EURIBOR

EUR Fixed

USD Fixed

Coupons on USD Bond Purchased

BANK 1

BANK 2

BANK 3

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

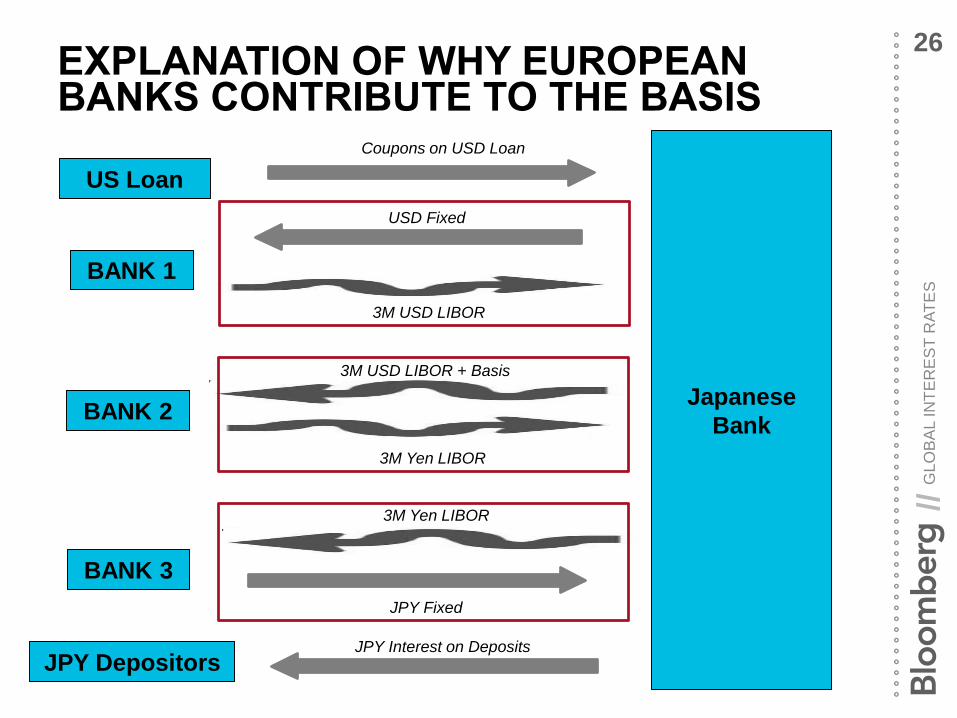

EXPLANATION OF WHY EUROPEANBANKS CONTRIBUTE TO THE BASIS

26

US Loan

Japanese

Bank

3M USD LIBOR

3M Yen LIBOR

3M USD LIBOR + Basis

3M Yen LIBOR

JPY Fixed

USD Fixed

Coupons on USD Loan

BANK 1

BANK 2

BANK 3

JPY Interest on Deposits

JPY Depositors

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

PLACEHOLDER27

Charts of issuance of EUR-denominated corporate bonds over time

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

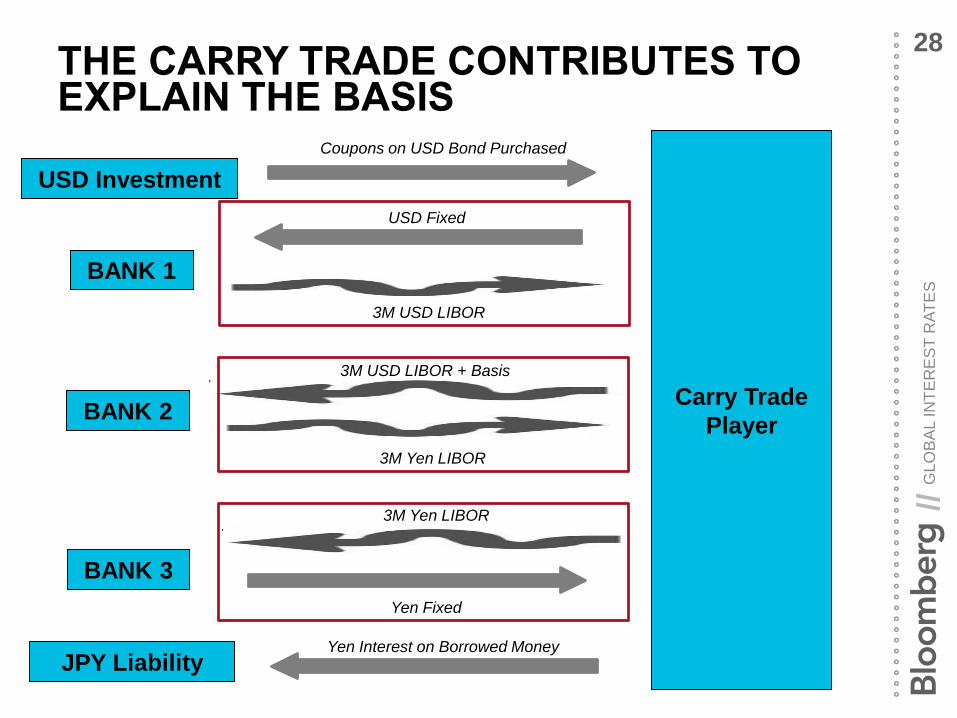

THE CARRY TRADE CONTRIBUTES TO EXPLAIN THE BASIS

28

USD Investment

Carry Trade

Player

3M USD LIBOR

3M Yen LIBOR

3M USD LIBOR + Basis

3M Yen LIBOR

Yen Fixed

USD Fixed

Coupons on USD Bond Purchased

BANK 1

BANK 2

BANK 3

Yen Interest on Borrowed Money

JPY Liability

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

WHERE ARE THE ARBITRAGEURS?29

• Hedge funds, CTA’s and all sorts of investors should be able to take

advantage of the cross currency basis and should be able to make it

disappear

• But time goes by and the financial crisis recedes more and more in the

past and the basis does not show signs of closing

• This is due to the very reason the basis came to be in the first place: the

great financial crisis

• In order to arbitrage the basis, people have to be able to rent balance

sheet from their bank counterparties, the very activity that recent

legislation has made so expensive

• Credit charges, more discriminating Prime Brokerages, margin

requirements… all conjure to keep the basis alive

GL

OB

AL IN

TE

RE

ST

RA

TE

S//

Q&A>>>>>>>>>>>>>