Embed Size (px)

Citation preview

Copyright © 2017 IQVIA. All rights reserved.

Prepared for CIB

28th February 2018

Patrick Bervelt, Sales Director

Patrick Van Dooren, Services Director

Global, European and

Belgian pharmaceutical

market trends

1

Agenda

Patrick Van Dooren, Principal, Director Commercial & Technology Services IQVIA

Patrick Bervelt, Sales Director, Sales, BEL & LUX, IQVIA

Global and European pharmaceutical market trends

Belgian pharmaceutical market trends

2© IQVIA 2017. All rights reserved.

3© IQVIA 2017. All rights reserved.

4© IQVIA 2017. All rights reserved.

5© IQVIA 2017. All rights reserved.

6© IQVIA 2017. All rights reserved.

Table of

Contents

7

+ Global and European pharmaceutical market trends

+ Belgian pharmaceutical market trends

Global and European pharmaceutical market trends

9

1.072 1.109

1.135 1.166

1.221

1.287

1.361

0%

2%

4%

6%

8%

10%

12%

14%

0

200

400

600

800

1.000

1.200

1.400

2015 (a) 2016 (a) 2017 (f) 2018 (f) 2019 (f) 2020 (f) 2021 (f)

An

nu

al g

row

th

Sa

les (

$U

S b

n)

Global sales Global growth US growth Europe growth

IQVIA Health Market Prognosis Q3 2017

Global sales are expected to return to more vigorous growth led by the US market

+4.2%

Forecasted annual

growth 2016-2021

+4.4%

+3.6%

10IQVIA Health Market Prognosis Q3 2017

In Europe, Belgium market growth is expected to trail that of the rest of the region

+3.6%

Forecasted annual

growth 2016-2021

+2.4%

214 224

232 241

249 258

267

0%

2%

4%

6%

8%

10%

0

50

100

150

200

250

300

2015 (a) 2016 (a) 2017 (f) 2018 (f) 2019 (f) 2020 (f) 2021 (f)

An

nu

al g

row

th

Sa

les (

US

$ b

n)

Europe sales Europe growth Belgium growth

11IQVIA Health Market Prognosis Q3 2017

Globally, the greatest contribution to sales will come from North America but emerging markets play a significant role

Contribution to Global Sales by Region

(2016-2021)

+4.4% +3.5% +8.2% +3.7% +5.5% +4.1% -0.1%

12

Developed and pharmerging markets CAGR 2016-2021

US 4.4%

EU5 2.8%

Germany 3.4%

France 1.8%

Italy 3.0%

Spain 2.4%

UK 3.9%

China 6.3%

Brazil 6.9%

Russia 8.2%

India 9.2%

Developed 3.4%

At par with region CAGR

Lower than region CAGR

Higher than region CAGR

Pharmerging 7.0%

Developed Markets

CAGR 2016-2021Pharmerging Markets

CAGR 2016-2021

IQVIA Health Market Prognosis Q3 2017

Belgium 2.4%

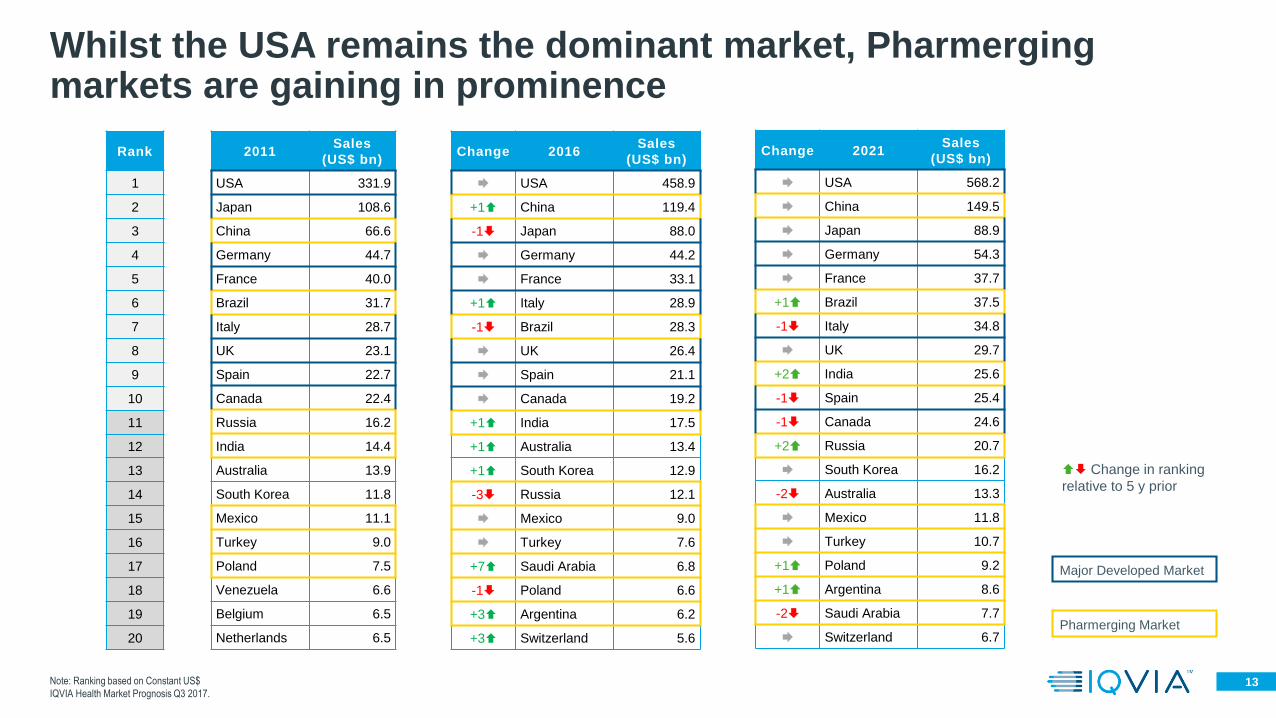

13Note: Ranking based on Constant US$

IQVIA Health Market Prognosis Q3 2017.

Whilst the USA remains the dominant market, Pharmerging markets are gaining in prominence

Rank

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

2011Sales

(US$ bn)

USA 331.9

Japan 108.6

China 66.6

Germany 44.7

France 40.0

Brazil 31.7

Italy 28.7

UK 23.1

Spain 22.7

Canada 22.4

Russia 16.2

India 14.4

Australia 13.9

South Korea 11.8

Mexico 11.1

Turkey 9.0

Poland 7.5

Venezuela 6.6

Belgium 6.5

Netherlands 6.5

Change 2021Sales

(US$ bn)

USA 568.2

China 149.5

Japan 88.9

Germany 54.3

France 37.7

+1 Brazil 37.5

-1 Italy 34.8

UK 29.7

+2 India 25.6

-1 Spain 25.4

-1 Canada 24.6

+2 Russia 20.7

South Korea 16.2

-2 Australia 13.3

Mexico 11.8

Turkey 10.7

+1 Poland 9.2

+1 Argentina 8.6

-2 Saudi Arabia 7.7

Switzerland 6.7

Change 2016Sales

(US$ bn)

USA 458.9

+1 China 119.4

-1 Japan 88.0

Germany 44.2

France 33.1

+1 Italy 28.9

-1 Brazil 28.3

UK 26.4

Spain 21.1

Canada 19.2

+1 India 17.5

+1 Australia 13.4

+1 South Korea 12.9

-3 Russia 12.1

Mexico 9.0

Turkey 7.6

+7 Saudi Arabia 6.8

-1 Poland 6.6

+3 Argentina 6.2

+3 Switzerland 5.6

Major Developed Market

Pharmerging Market

Change in ranking

relative to 5 y prior

14

Pharmerging market growth is fueled by spending on products other than the original from the inventors or marketers of a medicine

69%

14%

12%

5%

Developed MarketsSpending 2021

22%

42%

14%

22%

Pharmerging MarketsSpending 2021

3-6%Original Brands

Non-Original Brands

Unbranded

Other Products

13-16%

1-4%

0-3%

4-7%Original Brands

Non-Original Brands

Unbranded

Other Products

7-10%

8-11%

5-8%

Forecasted annual growth

2016-2021

Forecasted annual growth

2016-2021

IQVIA Global Outlook 2021

15

By 2021, these are projected to make up close to half of medicine spending

Specialty medicines have come to account for a third of medicine spending globally

Source: IQVIA MIDAS

77% 67%

23%

33%

2012 2017

US

$ (

Bn

)

Global Sales (MNF US$ (Bn); MAT11/2012-11/2017)

Traditional Specialty

$921bn

$1,361bn

+0.9%

CAGR

+11.1%

CAGR

16

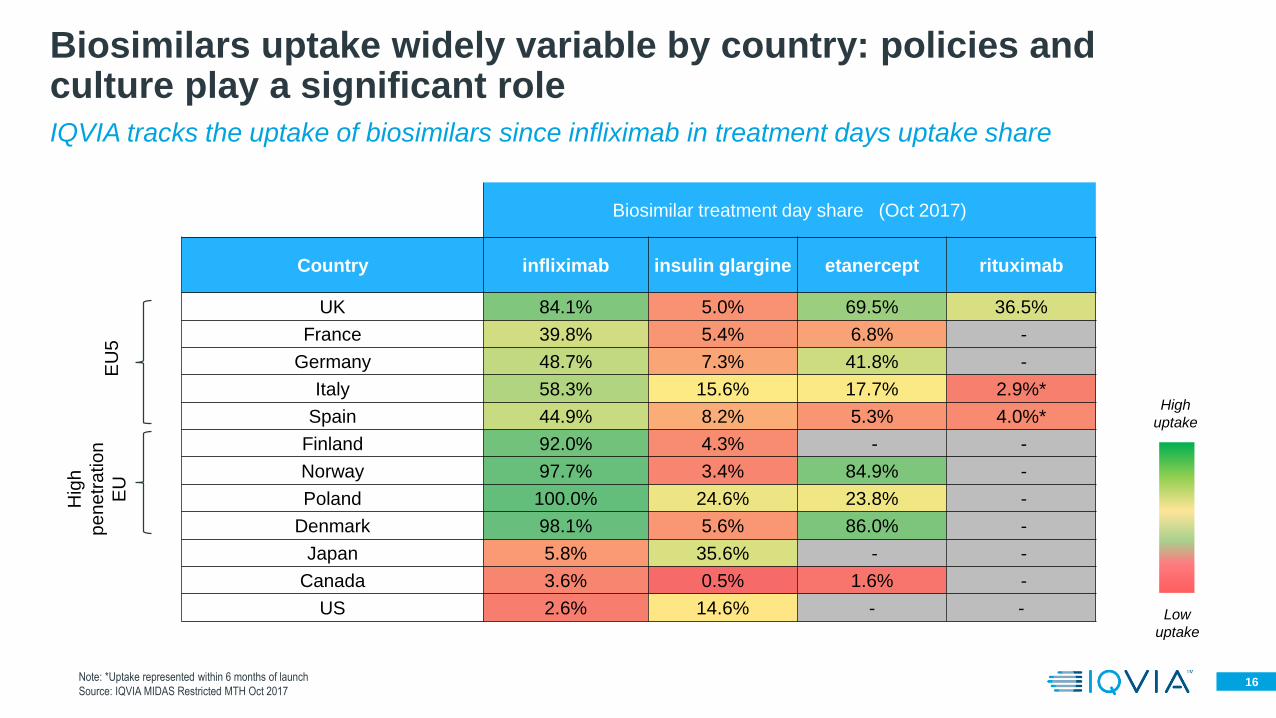

IQVIA tracks the uptake of biosimilars since infliximab in treatment days uptake share

Biosimilars uptake widely variable by country: policies and culture play a significant role

EU

5

Hig

h

pe

ne

tra

tio

n

EU

High

uptake

Low

uptake

Biosimilar treatment day share (Oct 2017)

Country infliximab insulin glargine etanercept rituximab

UK 84.1% 5.0% 69.5% 36.5%

France 39.8% 5.4% 6.8% -

Germany 48.7% 7.3% 41.8% -

Italy 58.3% 15.6% 17.7% 2.9%*

Spain 44.9% 8.2% 5.3% 4.0%*

Finland 92.0% 4.3% - -

Norway 97.7% 3.4% 84.9% -

Poland 100.0% 24.6% 23.8% -

Denmark 98.1% 5.6% 86.0% -

Japan 5.8% 35.6% - -

Canada 3.6% 0.5% 1.6% -

US 2.6% 14.6% - -

Note: *Uptake represented within 6 months of launch

Source: IQVIA MIDAS Restricted MTH Oct 2017

17

$22bn

$24bn

$25bn

$27bn

$28bn

$30bn

$34bn

$37bn

$38bn

$43bn

$46bn

$64bn

$69bn

$92bn

$103bn

Lipid regulators

Viral hepatitis

Other cardiovasculars

Nervous system disorders

Multiple sclerosis

Antivirals

Mental Health

Anticoagulants

Antibacterials

Antihypertensives

Respiratory Agents

Pain

Autoimmune Diseases

Antidiabetics

Oncologics

Source: IQVIA MIDAS

By therapy area, oncology and antidiabetics products dominate the global market

Top 15 Therapy area ranked by sales

(Global sales, $US bn MAT 11/2017) 5 year CAGR

-9%

27%

2%

5%

13%

9%

-6%

6%

-2%

-6%

2%

1%

18%

11%

9%

18IQVIA Market Analytics and ReSearch

The current drug pipeline reflects this emphasis on oncology

336

262281

158 18959 144 102 110 84

0

2000

4000

6000

8000

10000

Num

be

r o

f M

ole

cu

les in D

eve

lop

me

nt

Top 10 Therapy Areas by Molecule Count

Discovery Clinical Phase 1 Clinical Phase 2 Clinical Phase 3 Clinical

19

Budget caps and pharma

payback schemes

Portugal and Italy reviewing payback

mechanisms for budget overspend

French HCV spending cap

UK PPRS scheme

Increasing emphasis on drug cost-

value

NHS England Cancer Drugs Fund being

included under NICE QALY assessment

NICE QALY threshold being reviewed

French and Italian MoH reviewing current drug

reimbursement systems

Post launch payer led RWE scrutiny

France NOAC re-assessment based in part on

own RWE

Italy and France Avastin reimbursement for

use in AMD

Infliximab switching NOR-SWITCH

Recent changes in spending control mechanisms in Europe

Price negotiation collaboration and net price

transparency

Netherlands and Belgium announced pilot collaborative

Price negotiation for orphan drugs

Greek and Portuguese health ministers call

for increasing payer collaboratives

Controlling

costs

IQVIA Global outlook 2021

Belgian pharmaceutical market trends

21

Recent measures impacting the Belgium market

2015 - Signature of the Pact of the Future

2016 - Agreement to boost uptake of biosimilars

- Introduction of patent cliff system for

medicines in cat A, B, C, Cs,and Cx

- Reduction of the security margine

- Application of patent cliff

- Implementation of the “180 + 1” measure

- Variable Care

- Hospital Networks

- BeNeLuxA – inititaitive to facilitate

information sharing and streamline Health

Technology Assessments

2017

…

Source: Market Prognosis 2016-2021 Belgium, Pharma.be, EMA, Pharmaexec.com

22Source: IQVIA MIDAS

The hospital channel has made the strongest contribution to Belgian pharmaceutical market growth

Total Pharmaceutical Market €5.056m

Total Pharmaceutical market – Belgium

(MNF Euro value; MAT November 2017)

Delta Absolute growth €306m 1yr growth+6.5% 5yr CAGR 2.3%

Hospital €1.951m

Retail €3.106m

+€271m abs value

16.1% 1y growth

7.6% 5y CAGR

+€37m abs value

1.2% 1y growth

-0.3% 5y CAGR

39%

61%

Rx sales €2.642m

1.3% 1y growth

Non Rx €463m

0.4% 1y growth

85%15%

23

Hospital sales growth is led by original products, whilst in the retail channel generics are performing best

Total Pharmaceutical Market €5.056m

Total Pharmaceutical market – Belgium

(MNF Euro value; MAT November 2017)

Hospital €1.951m

Retail €3.106m

Generic €95m5%

95%

Original €1.851m

+8% 1yr growth

+16% 1yr growth

17%

83%

Generic €457m

Original €2.171m

+3% 1yr growth

+1% 1yr growth

86%

14%

58%

42%

Protected

Unprotected

Protected

Unprotected

Source: IQVIA MIDAS

24

302,108

206,346

168,351

140,267

137,739

67,609

52,633

51,377

51,027

35,621

Immunosuppressants (L04)

Antithrombotics (B01)

Antihistamines and COPD products(R03)

Antidiabetics (A10)

Systematic antivirals (J05)

Urologicals (G04)

Antiinflammatory and antirheumaticproducts (M01)

Antiepileptics (N03)

Vaccines (J07)

Endocrine therapy (L02)

167,919

157,049

146,632

123,995

98,973

98,810

98,021

76,749

59,786

53,505

Psycholeptics (N05)

Lipid modifying agents (C10)

Analgesics (N02)

Renin-Angiotensin agents (C09)

Other nervous system drugs(N07)

Drugs for acid-related disorders(A02)

Psychoanaleptics (N06)

Sex hormones and modulators ofthe genital system (G03)

Systematic antibacterals (J01)

Cough medications (R05)

Top 10 ATC2 classes in values with growing and declining – Retail

(MNF Euro Value (thousands); MAT November 2017)

In retail, immunotherapy and haematology are the best performing categories, whilst angiotensin products have seen the greatest decline

+11,5%

+10,8%

+2,4%

+4,9%

+6,0%

+1,4%

+5,0%

+5,4%

+4,3%

+6,5%

-0,2%

-3,5%

-1,8%

-9,5%

-0,6%

-8,9%

-3,7%

-0,7%

-3,0%

-1,2%

Retail

Source: IQVIA Retail Audit

25

Top 20 companies performances and growth – Retail

(MNF Euro Value (thousands) ; MAT December 2017)

The top 20 companies account for 66% of the market share and display variable performances over the last year

217,638

177,794

138,494

129,142

125,178

122,612

122,058

119,120

108,263

106,863

104,746

94,793

70,441

68,382

62,253

61,450

56,383

48,138

47,362

46,928

EUROGENERICS

PFIZER

ASTRAZENECA

ABBVIE

NOVARTIS PHARMA

GLAXOSMITHKL.PHARM

MSD BELGIUM

SANDOZ

BAYER PHARMACEUTIC

BRISTOL-M. SQUIBB

SANOFI BELGIUM

JANSSEN-CILAG

BOEHRINGER INGEL.

TAKEDA BELGIUM

GILEAD SCIENCES

TEVA PHARM.BELGIUM

J&J CONS.

VIIV HEALTHCARE

NOVO-NORDISK

LILLY

Source: IQVIA Retail Audit

+2

-3

-1

+5

+1

+1

-1

+1

-1

+1

-1

+1

-1

+1

3,2%

-1,6%

12,7%

2,9%

-5,7%

9,4%

-19,6%

3,2%

4,0%

1,1%

9,7%

-6,1%

7,4%

-3,3%

3,6%

-0,5%

7,9%

-7,5%

-4,5%

-0,5%

Retail

26

Together, the top 10 retail companies are declining while smallercompanies are doing relatively better

17%26%

44%

66%

78%

91%99%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top 3 Top 5 Top 10 Top 20 Top 30 Top 50 Top 100

-4%

-2%

-0,1%

-0,1%

0,2%

-0,1%

0.2%

Top manufacturers ranking according to revenues – Retail

(in Mio absolute sales and sales growth in MNF Value; MAT December 2017)

Source: IQVIA Retail Audit

Retail

27

Top 10 ATC2 classes in values with growing and declining – Hospital

(MNF Euro Value (thousands); MAT November 2017)

On the hospital market, Antineoplastic drugs lead in sales and growth, adding €138m additional sales for the period

580,166

186,538

107,430

85,710

73,844

71,579

70,168

64,566

63,913

61,488

Antineoplastic agents (L01)

Immunosuppressants (L04)

Systematic antivirals (J05)

Antihemorrhagics (B02)

Ophthalmologicals (S01)

Immunoglobulins (J06)

Antianemics (B03)

Other nervous system drugs (N07)

Imaging diagnostics (T01)

Systematic antibacterials (J01)

+31,3%

+8,7%

+10,4%

+8,2%

+1,7%

+28,9%

+18,9%

+22,9%

+5,9%

+10,1%

34,187

20,932

18,187

17,542

14,822

11,807

11,329

9,034

8,252

8,130

Immunostimulants (L03)

Systematic antimycotics (J02)

Analgesics (N02)

Psycholeptics (N05)

Antiinflammatory andantirheumatic products (M01)

Bone disease drugs (M05)

Antiparkinson drugs (N04)

Antiemetics and antinauseants(A04)

Systematic corticosteroids (H02)

Pituitary and hypothalamichormones and analogues (H01)

-9,6%

-3,8%

-11,2%

-2,5%

-5,3%

-3,4%

-5,0%

-3,1%

-7,4%

-14,2%

Source: IQVIA Hospital Audit

Hospital

28

• Top 20 hospital companies sales and growth

(MNF Euro Values (thousands) ; MAT December 2017)

Source: IQVIA Hospital Audit

The leaders on the hospital market remain consistent compared to last period

25,560

26,775

27,385

29,006

36,203

41,951

42,212

46,899

48,394

55,291

57,709

64,003

71,429

82,850

87,742

102,494

130,372

132,254

150,529

203,359

SHIRE

ASTRAZENECA

NOVO-NORDISK

PFIZER PFE BELGIUM

ASTELLAS

CSL BEHRING

BAXTER

ABBVIE

TAKEDA BELGIUM

FRESENIUS KABI

BAYER PHARMACEUTICALS

GILEAD SCIENCES

SANOFI BELGIUM

CELGENE

AMGEN

JANSSEN-CILAG

MSD BELGIUM

BMS

NOVARTIS PHARMA

ROCHE 1%

12%

21%

136%

14%

7%

19%

3%

35%

22%

7%

52%

-15%

7%

-0,4%

11%

30%

61%

22%

9%

+5

-1

+5

+2

-2

+3

-1

-1

-1

+2

-2

Hospital

-1

-1

+1

+4

-3

29

For 15 out of the 20 top manufacturers serving hospitals, more than 80% of the total sales are made in 2 categories only

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

SHIRE PHARMACEUT.

ASTRAZENECA

NOVO-NORDISK

PFIZER PFE BELGIUM

ASTELLAS

CSL BEHRING

BAXTER

ABBVIE

TAKEDA BELGIUM

FRESENIUS KABI

BAYER PHARMACEUTICALS

GILEAD SCIENCES

SANOFI BELGIUM

CELGENE

AMGEN

JANSSEN-CILAG

MSD BELGIUM

BRISTOL-M. SQUIBB

NOVARTIS PHARMA

ROCHE

ATC Share for Top 20 Manufacturers(by MNF Euro Values; MAT December 2017)

Antineoplastic & Immuno Anti-infectives Haemato Digestive & Metabolic Nervous Syst. Hospital Solutions Others

Hospital

Source: IQVIA Hospital Audit

30

For 12 out of the 20 top manufacturers serving hospitals, around 80% of the total sales are made in 1 category only

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

SHIRE PHARMACEUT.

ASTRAZENECA

NOVO-NORDISK

PFIZER PFE BELGIUM

ASTELLAS

CSL BEHRING

BAXTER

ABBVIE

TAKEDA BELGIUM

FRESENIUS KABI

BAYER PHARMACEUTICALS

GILEAD SCIENCES

SANOFI BELGIUM

CELGENE

AMGEN

JANSSEN-CILAG

MSD BELGIUM

BRISTOL-M. SQUIBB

NOVARTIS PHARMA

ROCHE

ATC Share for Top 20 Manufacturers(by MNF Euro Values; MAT December 2017)

Antineoplastic & Immuno Anti-infectives Haemato Digestive & Metabolic Nervous Syst. Hospital Solutions Others

Hospital

Source: IQVIA Hospital Audit

31

For 12 out of the 20 top manufacturers serving hospitals, around 80% of the total sales are made in 1 category only

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

SHIRE PHARMACEUT.

ASTRAZENECA

NOVO-NORDISK

PFIZER PFE BELGIUM

ASTELLAS

CSL BEHRING

BAXTER

ABBVIE

TAKEDA BELGIUM

FRESENIUS KABI

BAYER PHARMACEUTICALS

GILEAD SCIENCES

SANOFI BELGIUM

CELGENE

AMGEN

JANSSEN-CILAG

MSD BELGIUM

BRISTOL-M. SQUIBB

NOVARTIS PHARMA

ROCHE

ATC Share for Top 20 Manufacturers(by MNF Euro Values; MAT December 2017)

Antineoplastic & Immuno Anti-infectives Haemato Digestive & Metabolic Nervous Syst. Hospital Solutions Others

Hospital

Source: IQVIA Hospital Audit

32Source: IQVIA Xponent

General practitioners remain the main player on the market but specialists contributed more to growth

60% 59%

40%41%

0

500

1.000

1.500

2.000

2.500

3.000

3.500

MAT December 2016 MAT December 2017

Rx S

ale

s (

€m

)

Primary and Secondary Care Evolution

(MNF Euro; MAT December 2016 and 2017)

General Practitioners Specialists

43% 43%

57%57%

0

500

1.000

1.500

2.000

2.500

3.000

3.500

MAT December 2016 MAT December 2017

Rx S

ale

s (

€m

)

Geographic Distribution of Sales

(MNF Euro; MAT December 2016 and 2017)

South North

Retail

33

607

338

249186

13899

6333 9 1

35%

20%

14%

11%8%

6%4%

2%0,05% 0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

100

200

300

400

500

600

700

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Ma

rket sh

are

Pre

scrip

tio

n v

alu

e (

mill

ion

s)

Amongst the General Practitioners, 4,305 of them are responsiblefor almost 70% of the market share

Decile analysis

(Active GPs and Occupational GP prescription value (millions) ; MAT December 2017)

14,358 Physicians

Prescription

Source: IQVIA Xponent

34

607

338

249186

13899

6333 9 10

100

200

300

400

500

600

700

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Pre

scrip

tio

n v

alu

e (

mill

ion

s)

Amongst the General Practitioners, 4,305 of them are responsiblefor almost 70% of the market share

Decile analysis

(Active GPs and Occupational GP prescription value (millions) ; MAT December 2017)

14,358 Physicians

Prescription

Source: IQVIA Xponent

35Source: IQVIA Xponent

607

338

249186

13899

6333 9 1

35%

20%

14%

11%8%

6%4%

2%0,05% 0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

100

200

300

400

500

600

700

D1 D2 D3 D4 D5 D6 D7 D8 D9 D10

Ma

rket sh

are

Pre

scrip

tio

n v

alu

e (

mill

ion

s)

Amongst the General Practitioners, 4,305 of them are responsiblefor almost 70% of the market share

Decile analysis

(Active GPs and Occupational GP prescription value (millions) ; MAT December 2017)

14,358 Physicians

Prescription

423 236 173 130 96 69 44 23 7 1AVERAGE prescription

value per doctor per year (in

thousands euro)

36

In the future, the pressure of visits from patients on the younger generationof GPs will increase

Source: IQVIA Doctor Universe 2018

11%

8%

7%

9% 9%10%

18%

17%

8%

26-30 31-35 36-40 41-45 46-50 51-55 56-60 61-65 66-70

% A

ctive

GP

s p

er

age

ra

nge

Age range

Active GPs age range profile53%

37Source: IQVIA Consumer Health Services

The Consumer Health market grew by 1.5% in the past year, driven by the performance of the patient care category

Total Consumer Health Market €1,973m

Consumer Health market – Belgium

(PUB Euro value; MAT December 2017)

Delta Absolute growth €29m 1yr growth (+1.5%) 5yr growth (+1.9%)

OTC €1,327m

PEC €353m

PAC + NTR €293m

0.8% 1y growth

1.5% 5y CAGR

0.3% 1y growth

2.9% 5y CAGR

6.1% 1y growth

2.7% 5y CAGR

67%

18%

15%

Registered €817m

-0.9% 1y growth

70% free sales 30% Rx sales

Non registered €510m

+3.7% 1y growth

83% free sales 17% Rx sales

Consumer

HealthConsumer Health

38Source: IQVIA Consumer Health Services

Most of the biggest Consumer Health classes are OTC but are experiencing mixed performances

269

242

192

187

118

88

87

81

62

62

02 PAIN RELIEF

01 COUGH COLD/OTH RESP REMS

04 VIT/MINERALS/NUTRIT.SUPPL

03 DIGESTIVE/OTH INTEST REMS

82 BEAUTY PRODUCT FOR WOMEN

06 SKIN TREATMENT

10 CIRCULATORY PRODUCTS

83 UNISEX BEAUTY PRODUCTS

35 BABY FOODS

07 EYE CARE

Top 10 Consumer Health Classes

(PUB Euro (millions); MAT December 2018)

-1%

-2%

2%

4%

-1%

-2%

-3%

2%

3%

1%

Growth vs

MAT/12/2017

Consumer Health

39Source: IQVIA Consumer Health Services

Johnson & Johnson retains its leadership in Belgium Consumer Health but the top 10 have overall seen negative performance

-1%

7%

3%

13%

0%

5%

3%

6%

-1%

-3%

-2%

4%

-3%

-7%

-5%

-6%

-4%

-3%

-4%

1%

Growth since last MAT

Market growth

1.5%0 10 20 30 40 50 60 70 80 90 100

VICHY

NESTLE BELGILUX

LOUIS WIDMER

METAGENICS

QUALIPHAR

LA ROCHE POSAY

EUROGENERICS

TILMAN

NUTRICIA

MELISANA

MEDA PHARMA

SMB LABORATOIRE

MERCK CONS.HLTH

TAKEDA BELGIUM

RECKITT BENCKISER

SANOFI CHC

BRISTOL-M. SQUIBB

OMEGA PHARMA

GLAXOSMITHKL.CHLT

J&J CONS.

€m

Top 20 Consumer Health Companies Ranked by Sales(PUB Prices €m, MAT December 2017)

OTC PEC NTR PAC

90.0

80.6

71.2

67.9

64.8

59.1

59.0

56.2

47.2

47.2

45.4

44.0

38.5

38.5

38.3

38.2

33.7

30.6

29.2

27.0

-1

+1

+2

-1

-1

+3

-3

-1

+1

Consumer Health

40Source: IQVIA Consumer Health Services

Market growth is principally coming from smaller players

-1.8%

-3.0%

-3.0%

-1.0%

-0.5%

+0.4%

+0.9%

+1.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top 3 (>€70m) Top 5 (>€60m) Top 10 (>€45m) Top 20 (>€25m) Top 30 (>€15m) Top 50 (>€9m) Top 100 (>€3.75m) All (1147)

Co

ntr

ibu

tio

n t

o t

ota

l mar

ket

Top manufacturers ranking according to Consumer Health revenues(PUB value; MAT December 2017)

Consumer Health

![VESA Holes 4 - M8 116 - LG Electronics · 2020. 1. 30. · [75xs2e dimension] - applied model: 75xs2e - unit: mm 116 11.8 11.8 11.8 11.8 1675.2 953.6 600 400 vesa holes 4 - m8 600](https://img.pdfslide.us/doc/110x75/60afd7d1a1ba645bf236e933/vesa-holes-4-m8-116-lg-electronics-2020-1-30-75xs2e-dimension-applied.jpg)