Embed Size (px)

DESCRIPTION

Global Benchmark Report 2014

Citation preview

Including themes on global investment fl ows and Africa

The conditions for doing business in the global economy are con-stantly changing – presenting new challenges and opportunities.

For the tenth consecutive year, the Global Benchmark Report 2014 examines how the global challenge is met in the OECD countries. The assessment is based on 87 benchmarks across fi ve pillars com-prising Level of globalisation, Productivity and innovation, Qualifi ed labour, Public economy and Costs. Together these pillars constitute the foundation for creating open and prosperous nations capable of creating and sustaining growth and balance. The report highlights strengths and weaknesses of each OECD country in facing interna-tional competition, providing a picture of each country’s ability to de-velop attrac tive business environments and utilise opportunities pre-sented by globalisation.

For further information on the Global Benchmark Report see di.dk/gbr. The website provides a unique opportunity to download a PDF-version of the report where you can read more about how the in-dividual benchmarks are prepared and why they are relevant in inter-national competition. All graphs and fi gures are available for down-load intended for your own presentations and analyses.

DI – Confederation of Danish Industry H.C. Andersens Boulevard 18 1787 Copenhagen V Phone 3377 3377 [email protected] di.dk

GLO

BA

L BEN

CH

MA

RK

REP

OR

TR

eady for globalisation?D

I AN

ALY

SIS

DI ANALYSIS

Ready for globalisation?

GLOBALBENCHMARKREPORT

Ready for globalisation?

Global benchmark report 2014

READY FORGLOBALISATION

2 GLOBAL BENCHMARK REPORT 2014

Published by the Confederation of Danish Industry

Edited by Kathrine Klitskov, Mathias Secher, Marie Gad, Michael Meineche, Nanna Bøgesvang Olesen and Mads Dal Jørgensen

Printed by Zeuner Grafisk as

ISSN: 1901-6948

1000.3.14

3GLOBAL BENCHMARK REPORT 2014 – FOREWORD

FOREWORD

Businesses across the EU are beginning to see signs that a badly needed confidence is returning to the economy as an indication that the European economy could return to moderate growth in 2014. But the situation remains fragile. In order for Europe to emerge stronger from the financial crisis and restore long-term growth, we need to do much more to strengthen the fundamental determinants of competitiveness. We need a reduction of financial, trade and labour market imbalances in all the European countries in order to build a strong foundation for future growth. And we must be much better at combining national and European reforms so they become mutually reinforc-ing. A continued focus on fiscal consolidation and growth enhancing structural reforms is key to improving Europe’s international competitiveness, growth and employment prospects.

With its rich data and insightful assessments, DI’s Global Benchmark Report provides a useful overview of the national policies that ultimately determine Europe’s overall competitiveness. It can help each and every European member state to identify its strengths and weaknesses in facing international competition.

BUSINESSEUROPE strongly supports this continued effort to provide facts and figures for a fruitful dialogue on best practices. The DI Global Benchmark Report comple-ments our own annual European Reform Barometer. We hope both publications can inform and inspire policymakers to work on the difficult task of designing and imple-menting policies that will support businesses in their efforts to make the best of the op-portunities presented by global markets and help return the EU economy to stronger growth and full employment.

March 2014

Markus J. BeyrerDirector General, BUSINESSEUROPE

4 GLOBAL BENCHMARK REPORT 2014

5GLOBAL BENCHMARK REPORT 2014 – PREFACE

PREFACE

Economic recovery in the wake of the financial crisis is slow and uneven. Forecasts predict some acceleration of growth in 2014 and 2015, though still hesitant. However, we have yet to realise these expectations. In the current context, governments must avoid complacen-cy in preparing nations for the future economic landscape. Clear and credible strategies are needed to make the growth path irreversible and sustainable. These strategies require a strong commitment to long overdue structural reforms. It is DI’s intention that policy-makers and business leaders can make use of the Global Benchmark Report to identify strengths and weaknesses of their nations and apply these insights in the pursuit of creat-ing open and prosperous nations capable of creating and sustaining growing economies in balanced societies.

The Global Benchmark Report 2014 is the tenth in a series of reports presenting DI’s annu-al assessment of how the global challenge is met in the OECD member states. Across five pillars comprising level of globalisation, productivity and innovation, qualified labour, public economy and costs, each nation is benchmarked on the basis of 87 indicators that support the common aspiration for growth and prosperity. The report provides a snapshot of each country’s ability to develop attractive business environments and seize opportunities pre-sented by globalisation.

The conditions for doing business in the global economy are constantly changing – pre-senting new challenges and opportunities. Therefore, the two theme chapters of the Global Benchmark Report address how to make the most of these challenges and opportunities. The first theme chapter focuses on the struggle to attract foreign direct investment, an issue of growing concern in several OECD member states. Globalisation has increased foreign direct investment flows and new, viable destinations for investment have emerged putting pressure on the business and investment climates in several OECD countries. Foreign di-rect investment introduces new technologies and offers something unique in terms of inno-vation and productivity. It is vital to continually improve conditions that attract and retain foreign companies.

The second theme chapter highlights opportunities of tapping into the vast and growing African market and emphasises the major development results that can be achieved from combining aid and trade promotion.

March 2014

Karsten DybvadCEO, Confederation of Danish Industry (DI)

6 GLOBAL BENCHMARK REPORT 2014

7GLOBAL BENCHMARK REPORT 2014 – CONTENT

CONTENT

9 Performance in the global arena

18 Benchmarking

20 Level of globalisation

30 Productivity and innovation

46 Qualified labour

62 Public economy

70 Costs

78 Theme chapters

80 New trends in global investment flows

96 Africa: Open for business

123 Methodology,definitionsandsources

127 Descriptionofsources

131 Summaryofbenchmarks

137 Index to benchmarks

GROWTH

Seizingopportunitiespresentedbyglobalisation

Developinghighproductivityandinnovation

Havingaccesstoqualifiedandmotivatedlabour

Sustainingabalancedandefficientpublicsector

Maintaining a competitive cost level

Pilla

rs

9GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

For the tenth consecutive year, the Global Benchmark Report examines how the global challenge is met in the OECD member states. The report highlights strengths and weaknesses of each OECD member state in facing international competition and gives a picture of each country’s ability to develop attractive business environ-ments and utilise the opportunities presented by globalisation. The Global Bench-mark Report is an annually recurring publication intended as a benchmarking tool for business leaders and policymakers to identify obstacles and opportunities pre-sented in the global business arena.

This year, the report also includes two chapters on “New trends in global invest-ment flows” and "Africa: Open for business". The first theme chapter focuses on the struggle of attracting companies and their investment, an issue of growing con-cern in several OECD member states. Foreign investment introduces new technolo-gies and offers something unique in terms of innovation and productivity. The sec-ond chapter highlights opportunities of tapping into the vast and growing African market and emphasizes the major development results that can be achieved from combining aid and trade promotion.

International benchmarkingThe report compares the performance of 33 OECD member states and their busi-ness environments. When possible, data from Brazil, Russia, India and China is included. The report is based upon five fundamental pillars of competitiveness. To-gether these five pillars constitute the foundation for creating open and prosperous nations capable of creating and sustaining growing economies in balanced socie-ties. Thus, the comparison is based on 87 benchmarks divided into Level of globali-sation, Productivity and innovation, Qualified labour, Public economy and Costs.

PERFORMANCE IN THE GLOBAL ARENA

87 benchmarks

Productivityandinnovation

Qualifiedlabour

Public economy

CostsLevel of globalisation

10 GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

An agenda for growthOptimism is carefully returning to the global economy creating a slow recovery in business confidence and economic activity. However, the recovery remains precar-ious. Macroeconomic policies are under acute pressure in several OECD countries that still face many challenges including low growth, high fiscal deficits, high debt and high unemployment. For the OECD member states, success across the five pil-lars that form the basis of this report is a prerequisite for future growth and pros-perity.

Again, Chile excels as the OECD country with the highest average GDP growth in the period 2009-2013. The Eurozone has been especially challenged by economic decline over the past five years. Among the BRIC nations, China and India have re-corded remarkable growth in spite of the global crisis.

-6 -4 -2 0 2 4 6 8 10

RussiaBrazilIndia

China

GreeceSlovenia

ItalyPortugal

SpainIrelandIceland

HungaryFinland

NetherlandsDenmark

Czech RepublicUnited Kingdom

FranceBelgium

JapanAustriaEstonia

GermanyNorway

Slovak RepublicSwitzerland

United StatesSwedenCanada

New ZealandMexico

AustraliaPoland

South KoreaIsrael

TurkeyChile

GDP growth, 2009-2013 (average)

Per cent

OECDEUROZONE

SourceOECD Economic Outlook No. 94 and DI calculations

Behind the benchmark

11GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

The most prosperous members of the OECD continue to be Norway, United States and Switzerland. The Norwegian first place ranking is mainly due to the country's major oil production. Despite high growth for several years, the BRIC countries still have low per capita GDP.

0 10,000 20,000 30,000 40,000 50,000 60,000

IndiaChinaBrazil

Russia

TurkeyMexico

ChileHungary

PolandEstonia

PortugalGreece

Slovak RepublicCzech Republic

SloveniaItaly

SpainNew ZealandSouth Korea

IsraelFrance

FinlandJapan

United KingdomDenmark

BelgiumGermany

IcelandSwedenIreland

NetherlandsAustria

AustraliaCanada

SwitzerlandUnited States

Norway

GDP per capita, Purchasing power parity, 2013

USD

Source IMF, World Economic Outlook October 2013

OECDEUROZONE

Behind the benchmark

12 GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

Competitiveness index of the Global Benchmark Report 2014Based on a competitiveness index, the Global Benchmark Report provides an over-view of how the OECD countries are ranked in terms of competitiveness – and not only within the single pillars. This comprehensive index captures results from benchmarks divided across the five pillars of national competitiveness.

Switzerland tops the competitiveness index yet again Yet again, Switzerland wins the title as the most competitive OECD member state based on the benchmarks in the Global Benchmark Report. Sweden and South Ko-rea take the runner-up positions. Greece and Italy are placed at the bottom as the least competitive OECD member states.

0 5 10 15 20 25 30

ItalyGreeceMexicoTurkey

SloveniaFrance

SpainHungaryPortugalBelgium

Slovak RepublicPolandJapan

Czech RepublicAustriaIcelandNorway

IsraelGermany

New ZealandDenmark

FinlandUnited Kingdom

NetherlandsUnited States

EstoniaAustralia

ChileCanadaIreland

SwedenSouth KoreaSwitzerland

1 (1) 2 (2) 2 (3) 4 (8) 5 (4) 6 (7) 7 (5) 8 (13) 8 (9) 10 (6) 10 (15) 12 (12) 13 (10) 14 (17) 15 (11) 16 (19) 16 (18) 18 (14) 19 (16) 19 (21) 21 (20) 21 (23) 23 (22) 24 (26) 25 (24) 26 (28) 27 (24) 28 (30) 29 (28) 29 (27) 31 (31) 32 (32) 33 (33)

* All pillars have equal weights

Note The numbers in the brackets indicate the countries’ ranks in the competitiveness index for 2013. The coloured circle specifies if the country has either improved, worsened or kept its position.

Competitiveness index of the Global Benchmark Report, 2014Average rank of OECD countries across all five pillars* in the Global Benchmark Report

The overall average ranks of countries (1-33)

13GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

1. Level of globalisationSeveral OECD member states are still struggling with weak domestic demand. Im-proved access to major international export markets can help countries tap into global economic growth. The process of globalisation cultivates interaction be-tween countries and increases international sales. In this first pillar, a nation's level of globalisation is determined by the degree of global market involvement in terms of exports, foreign direct investment, global mindset among citizens and business-es, and the extent of cultural openness, to mention a few. The members of the OECD should strive to seize the opportunities offered by globalisation in order to create future growth. Ireland has the position as the OECD country with the highest Level of globalisa-tion. The Irish lead is based on several top rankings including the largest share of exports relative to GDP, highest freedom to trade internationally, efficient customs authorities, highest cultural openness, and a population with the most positive at-titude towards globalisation. Chile ranks second.

2.ProductivityandinnovationThe stage of development varies across the OECD, and so does the specific need for development in productivity and innovation. The most advanced countries strongly rely on the design and development of cutting-edge innovations in order to maintain their competitive advantage. Countries less advanced can still reap ben-efits from adopting existing technologies. This pillar measures a nation's level of productivity and innovation by addressing labour productivity, investment activity, the institutional environment and infrastructure. The goal is for each OECD country to develop high productivity and product quality.

Switzerland excels with the highest levels of Productivity and innovation. The coun-try has particularly strong university/industry research collaboration and is leading in both patent applications and innovation performance. Switzerland has been suc-cessful in attracting several businesses in sectors with high patent activity. Finally, Switzerland has the most widespread use of fixed broadband subscriptions and is one of the most energy efficient countries in the OECD. Sweden is the runner-up.

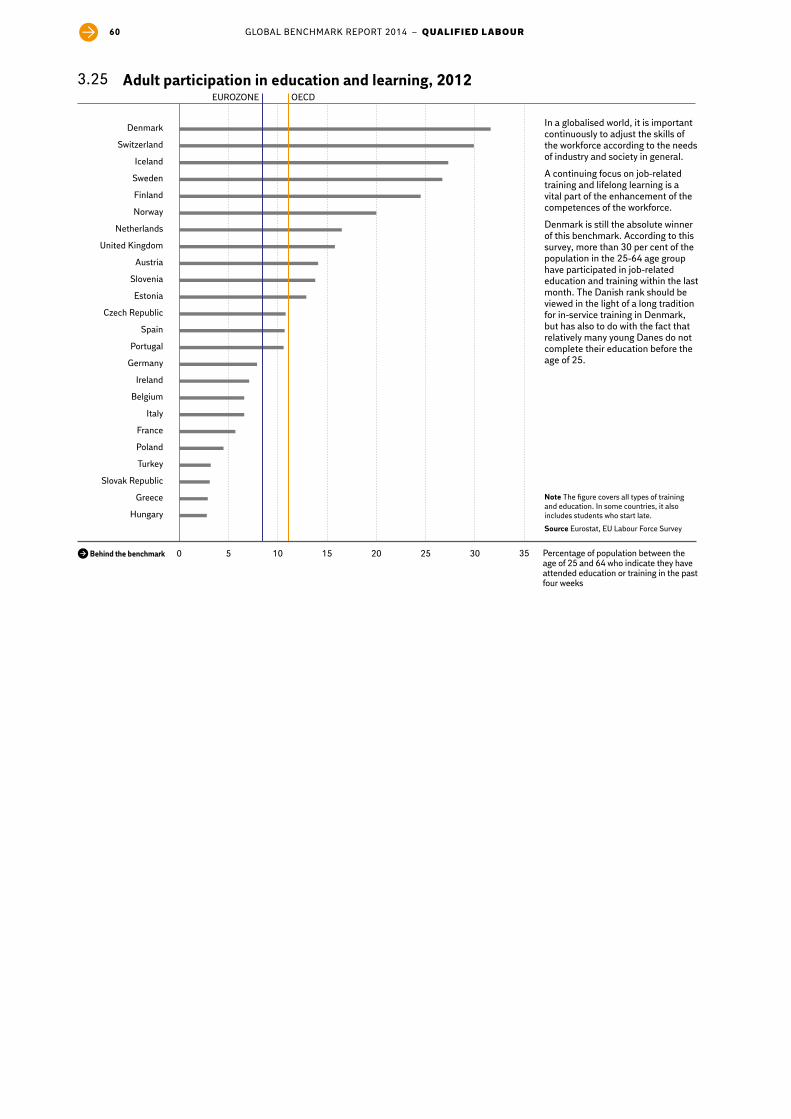

3.QualifiedlabourA well-educated workforce contributes significantly to a nation's economic value creation through productivity and business innovation. It is therefore of paramount importance that the business conditions of society support education and R&D and that businesses have access to employees with the desired competences. In this pillar, the availability of qualified labour in the OECD member states is determined by measuring investment in education, levels of educational attainment, business conditions provided by society, and labour market participation.

Canada tops the Qualified labour pillar with a highly educated population and strong focus on tertiary education. Furthermore, Canadian senior managers assess that the country's legislation on equal opportunities supports economic growth. Switzerland and South Korea together rank second with a series of solid perfor-mances.

Ireland no. 1 in Level of globalisation

Switzerland no. 1 in Productivity and innovation

Canada no. 1 in Qualified labour

14 GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

4.PubliceconomyAmong other lessons, the financial crisis and the following European debt crisis have taught the world the importance of monitoring the health of a country's pub-lic sector. A country's economic robustness is dependent not only on a strong and thriving private sector but also an efficient and balanced public sector. Therefore, among other indicators, this fourth pillar assesses budget balance, public debt, public expenditure, and corruption levels.

Switzerland excels as the OECD member with the best average ranking in Public economy. The country has the lowest public expenditure as a proportion of GDP. Additionally, Switzerland is one of the only OECD member states with a structural surplus on its public budgets, and the Swiss public sector is among the smallest in OECD. South Korea is the runner-up.

5. Costs The final pillar of the Global Benchmark Report is Costs. The competitiveness of businesses in a global economy depends on whether productivity and the quality of the product offset the costs of production. Production costs and taxes are therefore important indicators of competitiveness. In this pillar, the level of costs in the OECD countries is determined by benchmarks that measure taxes, consumer prices and compensation costs. Maintaining a competitive cost level is the fifth and final com-ponent of creating growth.

Switzerland is the most competitive country in terms of Costs. This rank is earned as a result of low marginal tax rates for especially medium wage earners and low inflation. Furthermore, Swiss businesses have easy access to capital markets, and this minimises financial costs and helps to stimulate economic growth. Chile holds second place.

Switzerland no. 1 in Public economy

Switzerland no. 1 in Costs

15GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

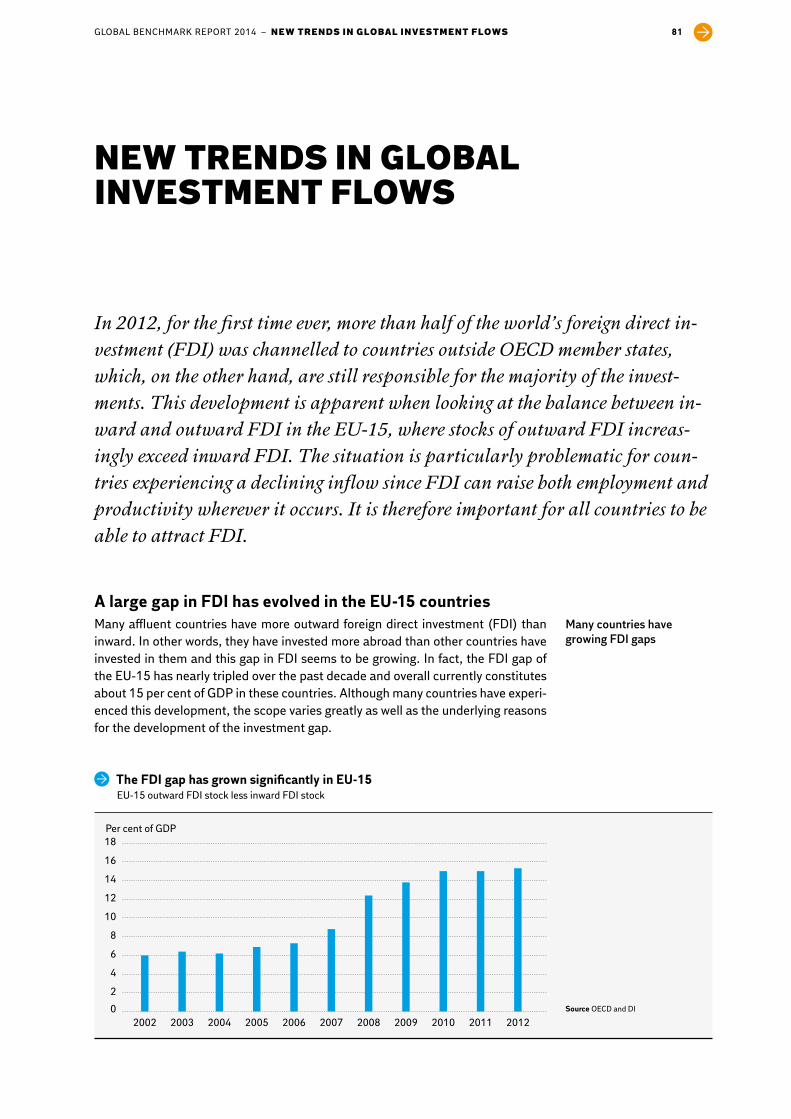

NewtrendsinglobalinvestmentflowsFor the first time ever, in 2012 less foreign direct investment (FDI) went to OECD member states than to the world’s other countries. The distinct shift is a natu-ral consequence of the fact that, for many years, an increasing proportion of the world’s FDI has sidestepped the OECD. Most of the capital, however, still comes from the OECD, and as a result, many OECD countries have developed a gap be-tween their outward and inward FDI with outbound FDI increasingly exceeding in-bound FDI.

The trend is particularly evident in EU-15, where the gap has nearly tripled in the past decade and currently constitutes 15 per cent of the countries’ overall GDP. Al-though many countries have experienced this development, the scope varies great-ly as well as the underlying reasons for the development of the investment gap. The situation is particularly problematic for countries experiencing a declining in-flow since FDI can raise both employment and productivity wherever it occurs. It is therefore important for all countries to be able to attract FDI.

In general, the pattern of the global FDI flows indicates that several affluent OECD member states have difficulties attracting and maintaining businesses and jobs. However, it is possible to reverse the trend and increase a country’s attractiveness as a FDI destination. This involves reducing administrative burdens, better interac-tion between private and public investment, and enhanced direct financial incen-tives to invest.

Many OECD member states have developed a gap in FDI

TheFDIgaphasgrownsignificantlyinEU-15EU-15 outward FDI stock less inward FDI stock

0

2

4

6

8

10

12

14

16

18

20122011201020092008200720062005200420032002

Per cent of GDP

Source OECD and DI

16 GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

Per cent0 1 2 3 4 5 6

G7*

Central and Eastern Europe

Middle East

Asia

Africa

Sub-Saharan Africa

AfricawillbeworldchampionineconomicgrowthinthenextfiveyearsExpected average annual GDP growth, 2013-2018

* G7 are Canada, France, Germany, Italy, Japan, UK and USA.

Note Africa includes Northern Africa

SourceIMF, World Economic Outlook, Database, October 2013

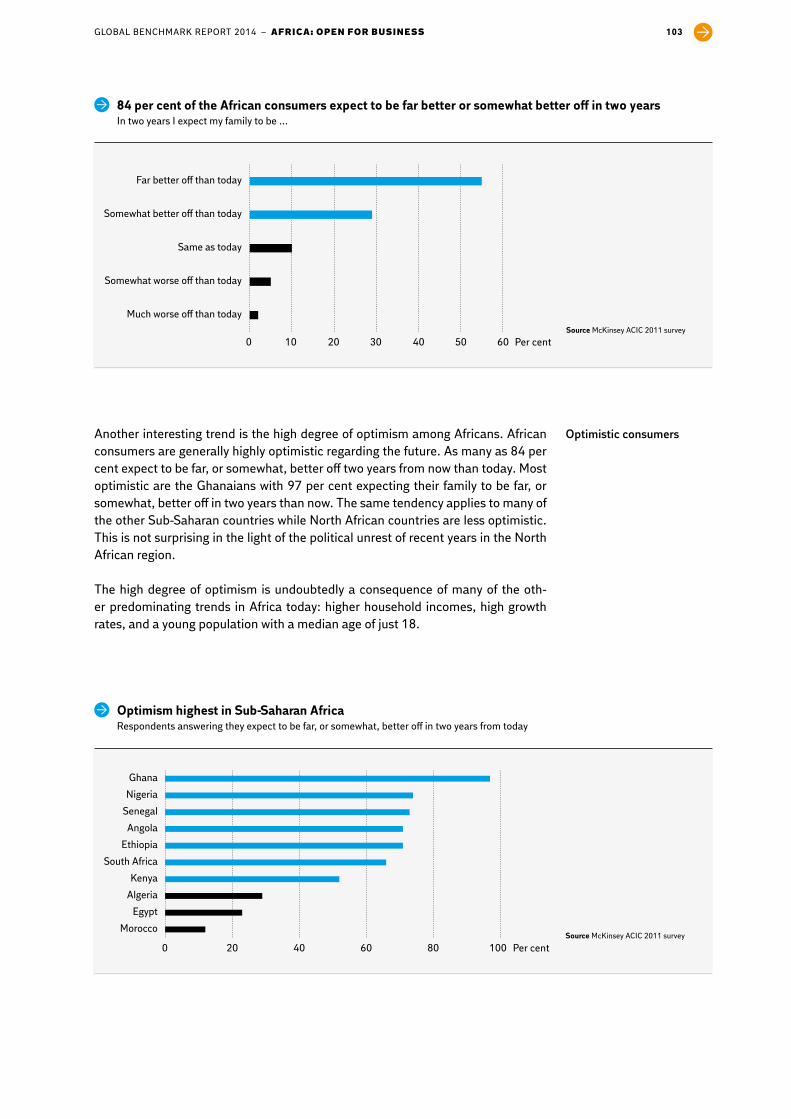

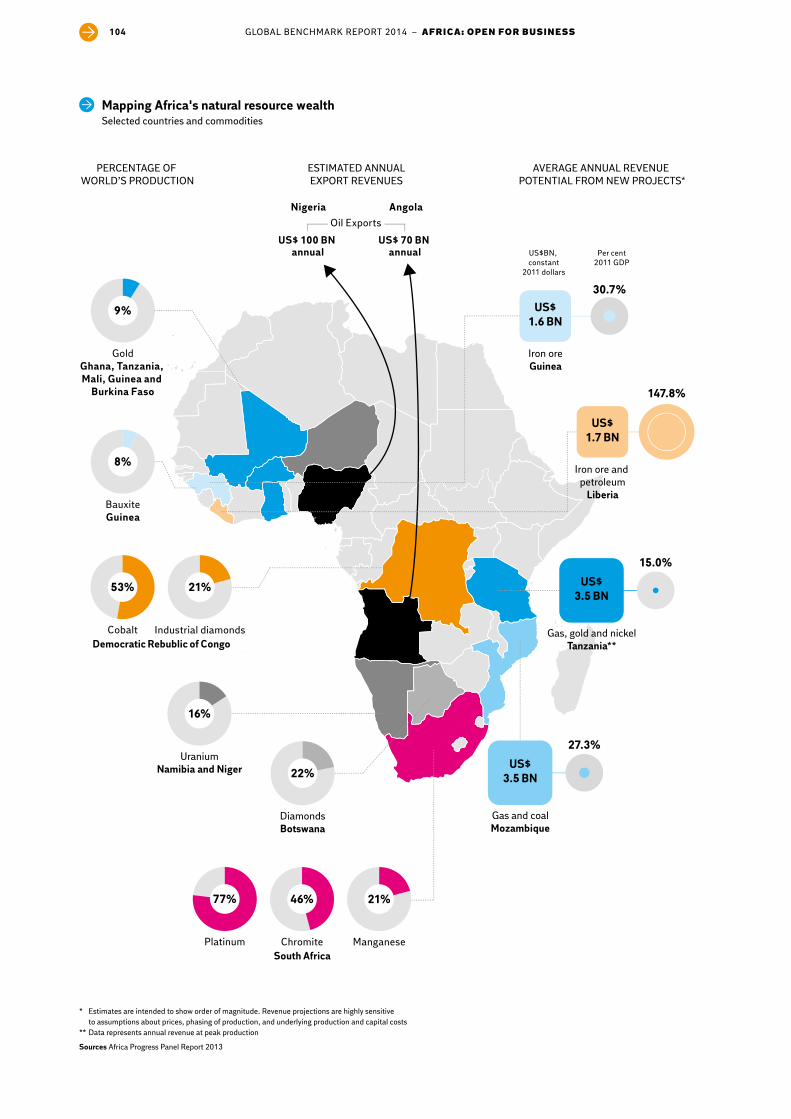

Africa:OpenforbusinessOver the past decade, Africa has developed from being an extremely poor conti-nent with dark prospects for the future to becoming the region with the highest growth rates in the world. This provides a potential for European companies, but also affects Europe’s involvement as an aid donor and trade partner for Africa.

The high African growth rates are thanks to a strong increase in inward foreign di-rect investment and major demand for African raw materials from growth countries such as China, India and Turkey.

Contributing directly to the growth and attracting FDI, the African consumer has become a significant player. African consumers demand a wealth of new products and services and often pay for them through their mobile telephones. This gener-ates business opportunities that many companies have gradually spotted.

Business conditions have also improved significantly in the African countries. Some countries are even competing to implement most business-friendly reforms in or-der to be attractive for FDI. It is, however, important to realise that there are major differences across the continent. Not all countries have been able to achieve sky-high growth rates, and a group of African countries are still dominating the bottom of all kinds of ranking from corruption to education.

Some European countries have had strong trade relations with Africa over many years, and the EU is still Africa’s greatest trading partner. There are, however, major differences as to how much the individual countries trade with Africa, and it is par-ticularly the EU-15 member states that have high trade with Africa while the new member states are lagging behind.

At the same time, several donor countries and African partner countries have spotted the advantages of co-thinking aid and trade cooperation and in this way achieved synergic effects between public development aid and private investment. Historically, as Africa’s largest donor, the EU has placed the highest priority on oth-

Potential for European companies in Africa

17GLOBAL BENCHMARK REPORT 2014 – PERFORMANCE IN THE GLOBAL ARENA

er types of aid that aid with focus on job creation and growth. There are signs, however, that in future the EU will place greater emphasis on industrialisation and private sector development with focus on job creation. The chapter ends with a number of recommendations for how the development aid can be structured so that it harmonises most efficiently with the activities of businesses with a view to optimising both development and business effects.

GLOBAL BENCHMARK REPORT 2014 – XXXX

Global Benchmark Report

GLOBAL BENCHMARK REPORT 2014 – XXX

The average ranks of countries in the Level of globalisation pillar

Level of globalisation1.00Average ranks of countries

1 (1) 2 (2) 3 (3) 4 (5) 5 (4) 6 (7) 7 (6) 8 (8) 9 (10) 10 (12) 11 (14) 11 (9) 13 (11) 14 (13) 15 (18) 16 (16) 17 (15) 18 (21) 19 (19) 19 (20) 21 (23) 22 (17) 23 (29) 23 (22) 25 (26) 26 (27) 27 (24) 28 (25) 29 (28) 30 (30) 31 (31) 32 (32) 33 (33)

0 5 10 15 20 25 30

GreeceItaly

JapanFrance

SloveniaSpain

PolandSlovak Republic

TurkeyNorway

Czech RepublicIcelandMexico

PortugalFinland

New ZealandCanada

United StatesHungary

GermanySouth Korea

DenmarkAustria

AustraliaBelgium

United KingdomIsrael

EstoniaNetherlands

SwedenSwitzerland

ChileIreland

Ireland tops the list in terms of average ranking in the benchmarks for Level of globalisation.

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION 21

Several OECD countries are still struggling with weak domestic demand. Improved access to major international export markets can help countries tap into global economic growth. The process of globalisation cultivates in-teraction between countries and increases international sales. In order to take advantage of the many new opportunities presented by globalisation, great demands are placed on the global outlook of citizens, companies and policy makers. A positive attitude towards globalisation and openness to-wards foreign ideas and cultures are prerequisites for success.

LEVEL OF GLOBALISATION

The top three countries in Level of globalisation, Ireland, Chile and Switzerland, have retained the same positions as last year.

Ireland is the OECD country with the highest rank in Level of globalisation. The Irish lead is based on several top rankings including the largest share of exports relative to GDP, highest degree of freedom to trade internationally, efficient customs authorities, highest degree of cultural openness and a population with the most positive attitude towards globalisation.

Chile is second with a series of solid performances. The country has the most positive image abroad and excels in terms of both attracting foreign investments and investing abroad.

Switzerland ranks third. The country has the highest share of upmarket exports to EU15, Swiss senior managers have the highest degree of international experience and, additionally, Switzerland is a major investor abroad.

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION22

Per cent of GDP

Exports as a percentage of GDP, 20131.02OECD EUROZONE

0 20 40 60 80 100 120

United StatesJapan

AustraliaTurkeyFrance

New ZealandGreece

CanadaItaly

United KingdomMexico

IsraelSpain

NorwayFinland

PortugalSwedenPoland

GermanySwitzerland

DenmarkSouth Korea

AustriaIceland

SloveniaCzech Republic

BelgiumNetherlands

EstoniaHungary

Slovak RepublicIreland

Average annual real growth in per cent

Growth in exports, 2009-2013 (average)1.01OECDEUROZONE

-4 -2 0 2 4 6 8 10

BrazilIndia

China

GreeceFinlandNorway

JapanDenmark

CanadaItaly

SloveniaSwedenAustria

BelgiumFrance

United KingdomSwitzerland

IrelandIsrael

NetherlandsNew Zealand

GermanyHungaryPortugal

United StatesSpain

IcelandCzech Republic

AustraliaPolandMexicoTurkey

Slovak RepublicSouth Korea

Estonia

A country’s export percentage indi-cates to which degree the country participates in the international divi-sion of labour. Small countries typ-ically have a higher export percent-age than large countries because the domestic market is too small to support a highly specialised pro-duction.

Ireland continues to be the coun-try with the largest export as a per-centage of GDP. Ireland is followed by the Slovak Republic and Hun-gary. Ireland has been able to attract international companies that sell a large proportion of their production outside the Irish domestic market.

Export growth is an expression of how successful countries are at converting international business opportunities into increased sales. As a consequence of the financial crisis, many countries have experi-enced major export setbacks, and this decline is only slowly recuper-ated.

Estonia, South Korea and the Slovak Republic top this benchmark.

SourceOECD Economic Outlook No. 94 and DI calculations

Note Exports should be viewed in relation to total production, but in international compar-isons it is often most practical to use GDP (production adjusted for product taxes and consumption in production).

Source OECD Economic Outlook No. 94 and DI calculations

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION 23

Per cent of total exports of goods to EU15

Upmarket exports to EU15, 2008-2012 (average)1.04OECDEUROZONE

0 10 20 30 40 50 60 70 80 90

RussiaChinaBrazilIndia

NorwayChile

IcelandPoland

SpainTurkey

FinlandFranceGreece

SloveniaBelgiumPortugal

ItalyNetherlands

GermanySlovak RepublicCzech Republic

HungaryNew Zealand

United KingdomEstonia

South KoreaSwedenMexicoAustria

DenmarkCanada

AustraliaIsrael

United StatesIrelandJapan

Switzerland

Export index divided by market index

Export performance, 2009-2013 (average)1.03OECDEUROZONE

-0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0

BrazilRussiaChinaIndia

JapanBelgiumFinlandNorwayCanada

ItalyFranceGreece

AustraliaNew Zealand

AustriaDenmark

ChileNetherlands

United KingdomSwedenIreland

United StatesSlovenia

SpainSwitzerland

Czech RepublicGermany

South KoreaPortugal

MexicoTurkey

HungaryEstoniaIceland

Slovak RepublicIsrael

Poland

Companies in high-cost countries often focus on upmarket products which, due to their quality, design or service concept, are able to earn a higher price than corresponding products from other countries.

85 per cent of Swiss exports to the EU15 are upmarket products, and this again earns Switzerland a clear first place, with Japan and Ireland taking the two following rankings.

Note Upmarket exports are defined as exported products that achieve a price at least 15 per cent higher than the average price for the product in the EU15 states.

Source Eurostat and DI calculations

Export performance indicates whether a country’s exports increase more or less than the general import growth on the export markets.

Positive values indicate that market shares are won abroad while nega-tive values mean loss of market shares. If exports are parallel with imports on the export markets, the country’s export performance will equal zero.

Poland is the top scorer this year with exports in the period 2009-2013 that have developed signifi-cantly faster than the imports of its export markets.

India and China stand out among the BRIC countries. For several years, they have both won market shares to a much higher degree than all the OECD countries.

Source OECD Economic Outlook No. 94 and DI calculations

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION24

Foreign direct investment holdings as a percentage of GDP, 20121.06OECD EUROZONE

0 50 100 150 200 250

ChinaIndia (2009)

RussiaBrazil

Japan (2011)South Korea

GreeceItaly

GermanyTurkey

United States (2011)Mexico

Israel (2011)Slovenia

Canada (2011)Finland (2010)

NorwayAustralia

AustriaFrance

Spain (2011)Poland

DenmarkNew Zealand

United KingdomPortugal

Slovak RepublicCzech Republic

SwedenNetherlands

ChileHungaryEstoniaIceland

SwitzerlandIreland

Belgium

Per cent of GDP

Per cent of total exports of goods

Exports to emerging markets (non-OECD countries), 20121.05OECDEUROZONE

0 10 20 30 40 50 60 70

NorwayIrelandMexico

CanadaSlovak RepublicCzech Republic

IcelandNetherlands

BelgiumDenmark

AustriaSwedenPoland

PortugalHungary

SpainGermany

SwitzerlandUnited Kingdom

FranceSlovenia

Italy (2011)Finland

IsraelUnited States

EstoniaGreece

New ZealandChile

TurkeyAustralia

JapanSouth Korea Several markets outside the OECD,

including the BRIC markets, have a high export potential due to the size of their populations, increasing middle classes and economic growth potential. A positive development is closely linked to the ability to reach these markets.

South Korea, Japan and Australia are once again at the top. This should be viewed in the light of their proximity to high-growth markets in Asia, particularly China.

Globalisation is characterised by in-creasing investment across nation-al borders. This development should be viewed in the light of a wish to strengthen ties with foreign custom-ers and benefit from favourable pro-duction conditions in other parts of the world.

The holdings of foreign direct invest-ment indicate the attractiveness of a country’s general business conditions such as taxes, access to raw materi-als, wages and level of education.

Belgium is the OECD country where FDI holdings take up the greatest share of the economy. Ireland and Switzerland come next.

Note Data only includes goods exports.

Source OECD.Stat and DI calculations

SourceUNCTAD

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION 25

Foreign direct investments, inflow 2008-2012 (average)OECD EUROZONE

0 5 10 15 20

ChinaIndia

BrazilRussia

JapanDenmark

ItalyFinlandGreece

GermanySouth Korea

SloveniaNetherlands

FranceUnited StatesNew Zealand

AustriaTurkeyMexico

SpainSlovak Republic

CanadaPortugal

PolandUnited KingdomCzech Republic

SwedenSwitzerland

NorwayAustralia

IsraelIceland

HungaryEstonia

ChileIreland

Belgium

Per cent of GDP

1.08

Direct investment holdings abroad as a percentage of GDP, 2012OECD EUROZONE

0 50 100 150 200 250

ChinaIndia

BrazilRussia

TurkeySlovak RepublicCzech Republic

New ZealandMexicoPoland

South KoreaGreece

SloveniaJapan

EstoniaAustraliaHungary

ItalyIsrael

United StatesPortugal

ChileCanadaNorway

GermanySpain

AustriaFinlandFrance

DenmarkUnited Kingdom

IcelandSweden

NetherlandsIreland

SwitzerlandBelgium

Per cent of GDP

1.07

Direct investment abroad is an indi-cation that the country is an active participant in the international divi-sion of labour. It can also, however, be an indication that businesses prefer to invest in countries other than their own.

Belgium takes the lead regarding investment abroad.

SourceUNCTAD

The ability to attract foreign invest-ment is central for domestic compa-nies in a globalised world economy and vital for economic growth in society. A high investment flow indi-cates that foreign investors antici-pate a major growth potential.

Belgium has clearly recorded the highest average inflow of FDI in the past 5 years corresponding to almost 18 per cent of GDP. Ireland and Chile take the following two places.

SourceUNCTAD

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION26

Direct investment holding in emerging markets, 2012OECDEUROZONE

0 20 40 60 80 100

IcelandFinlandSweden

FranceBelgium

Germany (2011)Netherlands

DenmarkNew Zealand

Slovak RepublicCzech Republic

ItalySpain

United KingdomPortugal

PolandIreland

Australia (2011)Canada

Israel (2011)United States

SwitzerlandAustriaNorway

JapanTurkey

HungaryKorea

GreeceEstonia

ChileSlovenia

Mexico (2011)

Per cent of total investments

1.10

Foreign direct investments, outflow 2008-2012 (average)OECD EUROZONE

-10 -5 0 5 10 15

BrazilIndia

ChinaRussia

IcelandNew Zealand

TurkeyGreece

SloveniaSlovak RepublicCzech Republic

PolandPortugal

MexicoAustralia

JapanItaly

SpainUnited States

EstoniaIsrael

GermanyDenmark

South KoreaFinland

HungaryFrance

CanadaUnited Kingdom

AustriaNorway

NetherlandsSweden

ChileIreland

SwitzerlandBelgium

Per cent of GDP

1.09

Outflow of direct investment is a sign that a country is an active participant in the international division of labour and aims to take part in growth found outside of the country. It can, however, also be a sign that companies prefer to invest abroad rather than in their own country.

Belgium has the largest outflow of direct investment followed by Switzerland and Ireland.

Source UNCTAD

An increasing share of direct invest-ments takes place in markets out-side the OECD. Such investments can be explained by low production costs, but another important goal is to get hold of a share of the high growth in several of these markets.

Mexico has the greatest share of its direct investment holding in emerg-ing markets. Slovenia and Chile are runners-up.

Note Emerging markets are markets outside the OECD.

Source OECD.Stat and DI calculations

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION 27

Index 0 -10

Efficient customs authorities, 20131.12OECD

0 1 2 3 4 5 6 7 8 9 10

BrazilRussia

IndiaChina

PolandSlovak Republic

GreeceMexico

ItalyTurkey

HungaryIceland

PortugalIsrael

Czech RepublicSpain

FranceSouth Korea

JapanSloveniaEstonia

ChileUnited States

CanadaBelgium

SwitzerlandAustralia

United KingdomGermany

NetherlandsAustria

DenmarkNorway

New ZealandFinlandIreland

Sweden

EUROZONE

Index 0 -10

Freedom to trade internationally, 20111.11OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaIndia

ChinaBrazil

IcelandMexicoJapan

SwitzerlandTurkey

NorwayPoland

SloveniaGreece

South KoreaCanada

AustraliaUnited States

Czech RepublicHungary

ItalySpain

AustriaGermany

IsraelFrance

SwedenSlovak Republic

PortugalBelgium

ChileDenmark

EstoniaFinland

NetherlandsNew Zealand

United KingdomIreland

EUROZONE

Cato’s index for international free-dom of trade measures the degree to which general business conditions in the country support internation-alisation and the export and import activities of companies. The index focuses on aspects such as cus-toms barriers and other trade bar-riers, as well as barriers to foreign investment.

Freedom to trade creates a broader sales potential for companies. In addition, the freedom to trade con-tributes to stimulating competitive-ness due to the presence of foreign goods and services.

Ireland takes first place closely fol-lowed by the United Kingdom and New Zealand.

Note High values indicate few barriers for international trade and FDI.

Source Cato Institute, Economic Freedom of the World, 2013

Efficient customs authorities ensure smooth trade across national borders and are a vital

precondition for international business activities. In a period of increasing digitalisation and growing numbers of IT-based reporting systems, it is important that these work optimally and do not constitute a barrier for imports and exports.

Sweden has conquered the top rank followed by Ireland and Finland.

Note High values indicate that local senior managers find the country’s customs author-ities efficient.

Source IMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION28

Index 0 -10

Cultural openness, 20131.14OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaIndia

BrazilChina

SloveniaFrance

HungaryJapan

EstoniaSlovak Republic

South KoreaCzech Republic

GreeceFinland

ItalyIceland

GermanyNorway

SwitzerlandSpain

AustriaTurkeyMexicoPoland

United StatesBelgium

DenmarkUnited Kingdom

New ZealandChile

PortugalAustralia

CanadaNetherlands

IsraelSwedenIreland

EUROZONE

Index 0 -10

Attitudes toward globalisation, 20131.13OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaBrazilChinaIndia

HungaryFrancePoland

SloveniaSpain

GreeceAustria

Slovak RepublicBelgium

New ZealandCzech Republic

EstoniaItaly

PortugalUnited States

JapanUnited Kingdom

CanadaIceland

GermanySwitzerland

NorwaySouth Korea

FinlandMexicoTurkey

AustraliaNetherlands

ChileDenmark

IsraelSwedenIreland

EUROZONE

A positive attitude to globalisation in society helps to promote the ability of businesses to benefit from the opportunities of globalisation and continuously adapt to the changes needed in international competition.

Ireland, Sweden and Israel hold the top 3 positions in that order.

Note This benchmark indicates the degree to which local senior managers assess that there is a positive attitude to globalisation in society.

Source IMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

Globalisation gives companies access to new partners across the globe. Therefore, adaptation and accept-ance of foreign ideas and cultures are important in order to take an active part in globalisation and exploit its benefits. This applies for instance to the ability to attract foreign invest-ment and highly skilled workers.

Ireland is once again in first place.

China, Brazil and India have a high degree of openness – at a level with the best OECD countries.

Note This benchmark indicates the degree to which local senior managers assess that society is open to foreign ideas.

SourceIMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – LEVEL OF GLOBALISATION 29

Index 0 -10

Image abroad, 20131.16OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaIndia

ChinaBrazil

HungaryGreecePoland

PortugalSpain

FranceMexico

ItalySloveniaBelgium

IsraelSlovak RepublicCzech Republic

IcelandTurkey

EstoniaUnited Kingdom

NorwayFinland

JapanUnited States

DenmarkNetherlands

New ZealandIreland

AustraliaAustriaCanada

SwitzerlandSouth Korea

SwedenGermany

Chile

EUROZONE

Index 0 -10

International experience for senior managers, 20131.15OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaChinaIndia

Brazil

JapanSpain

SloveniaPortugalEstoniaIceland

ItalySlovak Republic

New ZealandSouth Korea

FranceAustralia

Czech RepublicNorwayGreece

CanadaTurkey

United StatesChile

United KingdomHungary

IsraelDenmark

AustriaMexicoFinland

BelgiumGermany

IrelandNetherlands

PolandSweden

Switzerland

EUROZONE

A high degree of international expe-rience of senior managers is vital when strategic decisions have to be made on global issues, and when employees across national borders have to be managed as efficiently as possible.

Switzerland is still number one in this benchmark. The country is headquarters of many global corpo-rations and organisations, and is characterised by an attractive business environment, including a favourable tax system for highly educated people.

Note A high value indicates that senior managers generally have major international experience.

Source IMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

A positive image abroad can help to promote exports and international relations and contribute to attracting investment to the country. A coun-try's image abroad is affected by many different factors including sports performances, tourist attractions, major events, business strengths and the international commitment of the country.

Chile, Germany and Sweden top the benchmark this year.

Note This benchmark shows to which degree local senior managers assess that the image abroad of their country helps to promote international business developments.

Source IMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION30

The average ranks of countries in the Productivity and innovation pillar

Productivity and innovation2.00

0 5 10 15 20 25 30

GreeceMexico

ItalySlovak Republic

HungaryPoland

SloveniaChile

Czech RepublicSpain

PortugalIsrael

EstoniaFranceAustria

New ZealandBelgium

JapanNorway

South KoreaGermany

IcelandUnited Kingdom

CanadaIreland

AustraliaDenmark

FinlandUnited States

NetherlandsSweden

Switzerland

Average ranks of countries

1 (1) 2 (2) 3 (3) 3 (5) 5 (9) 6 (6) 7 (4) 8 (10) 9 (8) 10 (11) 11 (7) 12 (12) 13 (13) 14 (14) 15 (17) 16 (16) 17 (19) 18 (15) 19 (18) 20 (20) 21 (21) 22 (22) 23 (23) 24 (24) 25 (25) 25 (26) 27 (27) 28 (27) 29 (29) 30 (29) 31 (31) 32 (32) 33 (33)

Turkey

Switzerland is most successful in terms of average ranking in benchmarks for Productivity and innovation.

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 31

PRODUCTIVITY AND INNOVATION

The level of development varies across the OECD, and so does the specific need for development in the areas of productivity and innovation. The most advanced countries are strongly reliant on the design and development of cutting-edge innovations in order to maintain their competitive advantage. Countries less advanced can still reap benefits from adopting existing tech-nologies. Developing a country's level of productivity and innovation in-cludes prioritizing investment in research and development, taking out pat-ents and facilitating entrepreneurship.

Switzerland excels as the country with the highest levels of Productivity and innova-tion. The country has particularly strong university/industry research collaboration and is leading in both patent applications and innovation performance. Switzerland has been successful in attracting businesses in sectors with high patent activity. Final-ly, Switzerland has the most widespread use of fixed broadband subscriptions and is one of the most energy efficient countries in the OECD.

Sweden is the runner-up in Productivity and innovation, and good rankings include high patent activity including European patent applications and triadic patent fami-lies. The country also has a high level of innovation performance.

The Netherlands earns third place as a result of the high quality of infrastructure, effi-cient supply of electricity, and a large number of fixed broadband subscribers.

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION32

Per cent of GDP

Public sector investments as percentage of GDP, 20112.02OECD

0 1 2 3 4 5 6

Russia (2009)

Austria

Greece

Germany

Belgium

Israel

Iceland

Italy

Denmark

Switzerland

Slovak Republic

Finland

Ireland

Portugal

Spain

France

Hungary

Norway

Japan

Netherlands

Sweden

Slovenia

Czech Republic

Estonia

South Korea

Poland

EUROZONE

Per cent

Investments as a percentage of GDP, 20132.01OECDEUROZONE

0 10 20 30 40 50

BrazilRussia

IndiaChina

IrelandGreeceIceland

United KingdomPortugal

NetherlandsSloveniaHungary

DenmarkItaly

GermanySpain

Slovak RepublicIsrael

SwedenFinland

United StatesFranceTurkeyPoland

New ZealandJapan

SwitzerlandBelgium

AustriaCzech Republic

MexicoCanada

ChileNorway

South KoreaEstonia

Australia Investment is an important driving force behind productivity gains and growth. Many factors are involved in the level of investment in the various countries, including economic devel-opment, access to financing and gen-eral business conditions.

Investment in new equipment, means of transport, buildings and informa-tion technology makes production more efficient. Investment in research and innovation supports the develop-ment of new products while invest-ment in infrastructure and energy sup-ply provides more efficient conditions for businesses.

Australia takes the lead with invest-ments corresponding to almost a third of the country's GDP. Far ahead of both the OECD countries and the oth-er BRIC countries, China has an im-pressive investment share of almost 50 per cent of GDP.

Note Investment covers private sector invest-ment, public sector investment and housing investment.

SourceIMF, World Economic Outlook October 2013

Public sector investment can contribute to enhancing growth in the private sector. Investment in infrastructure and information tech-nology, for example, may contribute to increased mobility, flexibility and productivity.

Poland, South Korea and Estonia have the highest proportions of public investment in relation to GDP among the OECD countries.

Comparisons of public sector invest-ment across countries are influ-enced by the fact that some coun-tries have developed the public sector at a much earlier stage than others, and currently do not need investment at the same scale. Furthermore, the definition of public investment differs among the coun-tries suggesting cautious interpreta-tion of the figure.

Source IMF, World Economic Outlook October 2013

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 33

Average annual growth in GDP per working hour in per cent

Growth in labour productivity, 2009-2013 (average)2.04OECD

-3 -2 -1 0 1 2 3 4

Brazil

GreeceSlovenia

United KingdomNetherlands

IsraelCzech Republic

HungarySwitzerland

ItalyFinland

BelgiumTurkey

GermanyAustriaFrance

NorwayChile

CanadaSwedenPortugal

DenmarkIcelandMexico

United StatesAustralia

New ZealandSlovak Republic

JapanSpain

EstoniaSouth Korea

IrelandPoland

EUROZONE

USD per working hour (PPP)

Labour productivity, 20132.03OECD

0 10 20 30 40 50 60 70 80

Brazil

ChileMexicoTurkey

EstoniaHungary

PolandPortugal

Czech RepublicSouth Korea

GreeceSlovak Republic

IsraelSlovenia

New ZealandItaly

FinlandJapanSpain

SwitzerlandIcelandCanada

United KingdomDenmark

AustriaSweden

AustraliaIreland

GermanyFrance

NetherlandsBelgium

United StatesNorway

EUROZONE

Wealth creation in a society is close-ly connected with labour produc-tivity.

Norway tops the list with the highest productivity per working hour. Norway’s considerable production per working hour is particularly ascribed to oil and therefore less a reflection of labour productivity on the Norwegian mainland. The United States, Belgium and the Netherlands are runners-up with labour productivity significant-ly above the OECD average. This shows that these countries are capable of generating high pros-perity per working hour.

Countries with a low level of produc-tivity will often develop faster than countries with a high productivity lev-el because the aforementioned coun-tries can more easily improve their productivity through imports of mod-ern capital equipment and reorgani-sation of their production structure.

Poland, Ireland and South Korea win the three top ranks and, according-ly, have recorded the highest average growth in labour productivity over the past five years.

Source The Conference Board Total Economy Database, January 2014

SourceThe Conference Board Total Economy Database, January 2014

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION34

Per cent of GDP

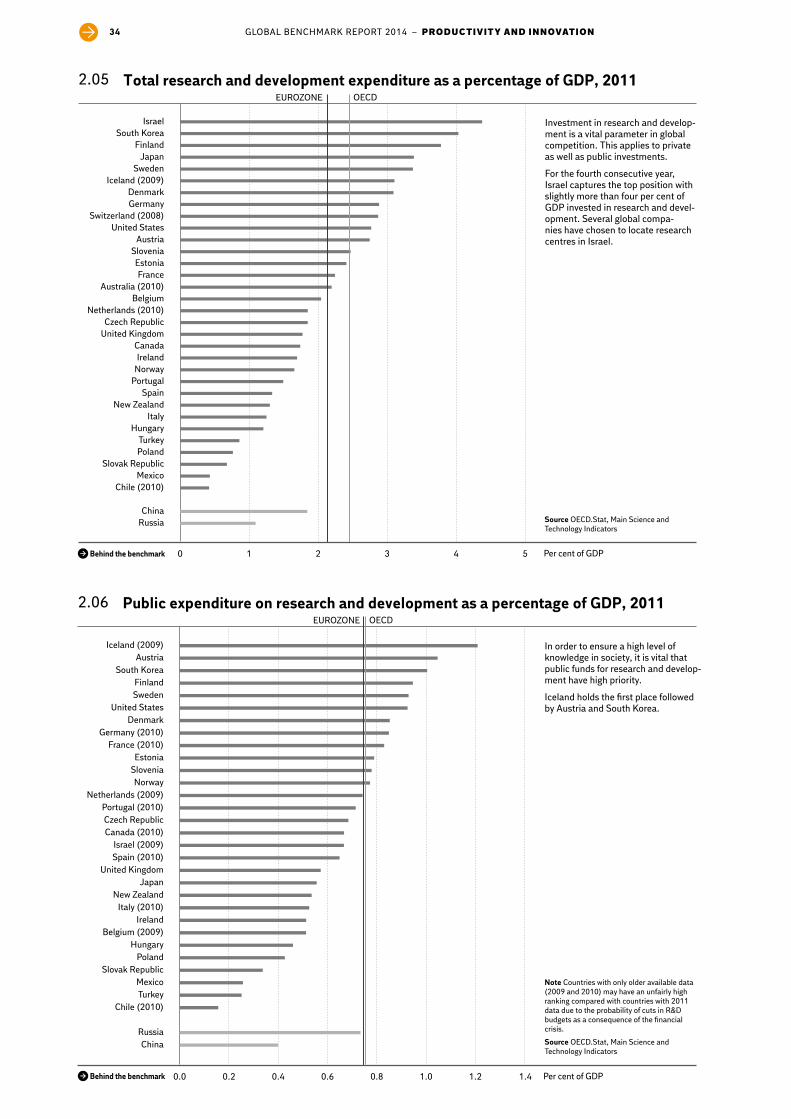

Public expenditure on research and development as a percentage of GDP, 20112.06OECD

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

ChinaRussia

Chile (2010)TurkeyMexico

Slovak RepublicPoland

HungaryBelgium (2009)

IrelandItaly (2010)

New ZealandJapan

United KingdomSpain (2010)Israel (2009)

Canada (2010)Czech Republic

Portugal (2010)Netherlands (2009)

NorwaySloveniaEstonia

France (2010)Germany (2010)

DenmarkUnited States

SwedenFinland

South KoreaAustria

Iceland (2009)

EUROZONE

Per cent of GDP

Total research and development expenditure as a percentage of GDP, 20112.05OECD

0 1 2 3 4 5

RussiaChina

Chile (2010)Mexico

Slovak RepublicPolandTurkey

HungaryItaly

New ZealandSpain

PortugalNorwayIreland

CanadaUnited KingdomCzech Republic

Netherlands (2010)Belgium

Australia (2010)France

EstoniaSlovenia

AustriaUnited States

Switzerland (2008)GermanyDenmark

Iceland (2009)Sweden

JapanFinland

South KoreaIsrael

EUROZONE

Investment in research and develop-ment is a vital parameter in global competition. This applies to private as well as public investments.

For the fourth consecutive year, Israel captures the top position with slightly more than four per cent of GDP invested in research and devel-opment. Several global compa-nies have chosen to locate research centres in Israel.

SourceOECD.Stat, Main Science and Technology Indicators

In order to ensure a high level of knowledge in society, it is vital that public funds for research and develop-ment have high priority.

Iceland holds the first place followed by Austria and South Korea.

Note Countries with only older available data (2009 and 2010) may have an unfairly high ranking compared with countries with 2011 data due to the probability of cuts in R&D budgets as a consequence of the financial crisis.

Source OECD.Stat, Main Science and Technology Indicators

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 35

Index 1-7

University/industry research collaboration, 2012-2013 (average)2.08OECD

1 2 3 4 5 6 7

RussiaBrazilIndia

China

GreeceSlovak Republic

PolandItaly

SloveniaTurkeySpain

MexicoHungary

ChileEstonia

Czech RepublicFrance

PortugalSouth Korea

IcelandAustria

DenmarkNew Zealand

CanadaJapan

AustraliaNorwayIreland

NetherlandsSweden

GermanyIsrael

BelgiumUnited Kingdom

United StatesFinland

Switzerland

EUROZONE

Index 1-7

Quality of scientific research institutions, 2012-2013 (average)2.07OECD

1 2 3 4 5 6 7

RussiaBrazilChinaIndia

GrækenlandSlovak Republic

TurkeyPolandMexico

ChileItaly

SpainSlovenia

IcelandCzech Republic

EstoniaSouth Korea

AustriaNorway

HungaryPortugal

New ZealandDenmark

CanadaSwedenIrelandFrance

FinlandJapan

AustraliaNetherlands

GermanyUnited States

BelgiumUnited Kingdom

SwitzerlandIsrael

EUROZONE

High quality in scientific institutions is central to a high level of research and makes it easier to attract foreign students and scientists as well as foreign investment in R&D.

Israel has the top rank this year. Israel’s position has to do with its massive investment in R&D in recent years.

Note High index values indicate that senior managers in the country assess that the local scientific research institutions are among the best in the world in their specific field.

Source WEF 2013-2014, survey

Strong research collaboration be-tween universities and industry is essential in order to guarantee rel-evant research for both businesses and society. It is also an important path for the transfer of new knowl-edge between businesses and uni-versities.

Switzerland takes the rank as num-ber one followed by Finland and the United States.

According to senior managers, these countries have the best research col-laboration between universities and industry.

Note High index values indicate that senior managers in the country assess that research collaboration between universities and industry is widespread.

Source WEF 2013-2014, survey

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION36

Patents per million inhabitants

Triadic patent families, 20112.10OECD

0 10 20 30 40 50 60 70 80 90 100 110

IndiaBrazil

RussiaChina

MexicoTurkeyPoland

ChileGreece

Slovak RepublicPortugal

Czech RepublicEstonia

HungarySlovenia

SpainIceland

New ZealandAustralia

ItalyCanadaIreland

NorwayUnited Kingdom

BelgiumFrance

South KoreaAustria

IsraelUnited States

DenmarkNetherlands

FinlandGermany

SwedenSwitzerland

Japan

EUROZONE

Applications per million inhabitants

European patent applications, 20122.09OECD

0 100 200 300 400 500 600 700 800 900

IndiaBrazil

RussiaChina

MexicoChile

TurkeySlovak Republic

GreecePortugal

PolandHungary

Czech RepublicNew Zealand

EstoniaSpain

AustraliaSlovenia

ItalyCanada

United KingdomNorway

United StatesSouth Korea

IrelandIsrael

IcelandFrance

BelgiumJapan

AustriaDenmark

NetherlandsGermany

FinlandSweden

Switzerland

EUROZONE

The number of European patent applications is an indicator of the degree to which companies in the country perceive the European coun-tries as key markets for their innova-tive products and processes.

Similar to previous years, Switzerland is in a superior position ahead of all other OECD countries with the high-est number of patent applications per million inhabitants. Switzerland has attracted many businesses in the most patent-active sectors, includ-ing the pharmaceutical industry. The appeal is mainly due to the combina-tion of low tax rates, researcher pro-grammes, corporate law, infrastruc-ture and location.

Note A European patent is achieved through application to the European Patent Office (EPO). Following submission of application, the patents must be designated in the indi-vidual country at the national patent author-ities. The figures here only indicate submis-sion of applications to EPO and do not say which EU member states were designated afterwards.

Source European Patent Office, IMF, and DI calculations

A triadic patent is a patent that is taken out at the same time in the United States, Japan and the EU. The triadic patents are taken out to ensure broad international protec-tion in three of the world’s major markets.

It should be noted that global com-panies increasingly also take out patents in one or several BRIC coun-tries and in other emerging markets.

Similar to preceding years, Japan, Switzerland and Sweden top the list of this type of patent. One of the reasons is that all three countries are knowledge societies with focus on sectors with frequent patenting such as the IT and telecom indus-try, the pharmaceutical industry and high technology in general.

Source OECD.Stat, IMF World Economic Outlook October 2013 and DI calculations

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 37

Per cent

Growth expectations among entrepreneurs, 20122.12OECD

0 10 20 30 40 50

BrazilChina

Russia

SpainAustriaGreece

SwitzerlandSweden

ItalyNorway

NetherlandsFinlandMexico

BelgiumIsrael

SloveniaFrance

GermanyPortugal

PolandUnited States

United KingdomDenmark

IrelandHungary

Slovak RepublicJapan

Iceland (2010)South Korea

EstoniaCzech Republic (2011)

Chile (2011)Australia (2011)

Turkey

EUROZONE

Index 0-1

Innovation performance, 20122.11OECD

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9

Turkey

Poland

Hungary

Slovak Republic

Greece

Czech Republic

Portugal

Spain

Italy

Norway

Estonia

Slovenia

France

Ireland

Austria

United Kingdom

Iceland

Belgium

Netherlands

Finland

Denmark

Germany

Sweden

Switzerland

EUROZONE

In a world of tough international competition, the continual innova-tion and development of products, processes and services are a precon-dition for creating growth and pros-perity in society.

The European Innovation Scoreboard tracks 25 socio-economic and company-specific factors that are central to the ability of compa-nies to be innovative. These factors include number of patents, innova-tion expenditure and the launch of new products and services by small companies.

Switzerland takes the innovation prize again this year.

Source European Innovation Scoreboard, Summary Innovation Index 2012

The most important job creation takes place among small and, in particular, newly established busi-nesses. It is vital that entrepreneurs are able to grow and develop their enterprises. The entrepreneurs’ own expectations for their growth are an indication of their future situation. Since growth expectations often work as a mental benchmark for the individual entrepreneur, there is often close correlation between expectations and reality.

Turkey holds first place with the highest growth expectations among the country's entrepreneurs.

Note The share of entrepreneurs who expect to take on at least five new employees in the next five years. Entrepreneurs are defined as people in the 18-64 age group who are either in the process of starting a business or are actually operating a newly established firm (maximum 3.5 years old). This data was also included in the Global Benchmark Report 2013. Additional information is provided in the section on methodology.

SourceGEM 2013

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION38

Per cent

Framework conditions for entrepreneurship, 20132.14OECD

0 10 20 30 40 50 60 70 80 90 100

BrazilIndia

ChinaRussia

SpainCzech Republic

AustriaJapan

GermanySlovak Republic

SwitzerlandPolandMexico

ItalyTurkey

ChileUnited Kingdom

GreeceIsrael

United StatesSouth Korea

EstoniaNorwayIcelandFrance

HungarySweden

DenmarkIrelandFinland

NetherlandsBelgiumSloveniaPortugalAustralia

CanadaNew Zealand

EUROZONE

Per cent

Entrepreneurial activity, 20122.13OECD

0 5 10 15 20 25

RussiaChinaBrazil

JapanItaly

FranceBelgium

GermanyDenmarkSlovenia

SpainSwitzerland

FinlandIreland

SwedenGreece

IsraelSouth Korea

NorwayCzech Republic (2011)

PortugalUnited Kingdom

HungaryPolandAustria

Slovak RepublicNetherlands

Australia (2011)Iceland (2010)

TurkeyUnited States

EstoniaChile

EUROZONE

In order to support the establish-ment of new businesses it is impor-tant that the structures and legis-lation of society provide good conditions for entrepreneurship.

Again this year, New Zealand wins most points and gets the maximum score (100 per cent). Canada and Australia are close to 100 per cent in second and third place.

Note This benchmark is an indicator of the scope of procedures, time and costs required for a small or medium-sized enterprise to get started and to function formally. New Zealand has the best business conditions for entrepre-neurship and is therefore assigned a score of 100 per cent. The other countries are bench-marked in relation to New Zealand.

Source World Bank, Doing Business 2014

Entrepreneurial activity is an impor-tant precondition for economic growth.

Chile ranks highest on the list again this year followed by Estonia and the United States as the countries with the greatest share of new entrepre-neurs in the OECD.

It is normal to distinguish between entrepreneurship driven by neces-sity and entrepreneurship driven by opportunity. Countries such as Chile and Estonia with a relatively low level of prosperity typically have a large share of entrepreneurs driven by necessity.

Note The share of the population in the 18-64 age group which is either in the process of starting a business or is actually operating a newly established firm (maximum 3.5 years old). This data was also included in the Global Benchmark Report 2013. Additional infor-mation is provided in the section on meth-odology.

Source GEM 2013

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 39

Per cent of GDP

Venture capital investments as a percentage of GDP, 2009-2012 (average)2.16

0.00 0.05 0.10 0.15 0.20 0.25 0.30 0.35 0.40 0.45

Poland

Greece

Czech Republic

Italy

Spain

Austria

Portugal

Germany

Netherlands

France

United Kingdom

Hungary

Belgium

Ireland

Norway

Finland

Sweden

Switzerland

Denmark

EUROZONE

Years

Average time to complete the procedure of closing a business, 20132.15OECD

0 1 2 3 4 5

IndiaBrazil

RussiaChina

Slovak RepublicGreeceTurkey

ChileSwitzerland

PolandEstonia

Czech RepublicSweden

SloveniaPortugal

IsraelHungary

FranceMexico

ItalyUnited States

SpainSouth Korea

New ZealandGermany

NetherlandsAustria

United KingdomIceland

DenmarkAustralia

NorwayFinland

BelgiumCanada

JapanIreland

EUROZONE

Entrepreneurs who start a new business after bankruptcy or clo-sure grow faster than other newly established businesses. This is why it should be easy to close the old business and get started again with a new one after bankruptcy.

In Ireland it takes less than six months to close a business and once again this puts Ireland in the top position in this indicator.

It is important to create a come-again-culture in society in order to encourage entrepreneurs to start again after a bankruptcy or closure.

The procedures of closing a busi-ness generally take longer in the BRIC countries. Particularly in India where it takes more than four years, on average, to complete the closing of a business.

Access to risk capital is essential for entrepreneurs in order to realise their ideas and start their own busi-ness. Venture capital is particularly important for entrepreneurs for whom return on investment lies rela-tively far into the future.

These enterprises are often based on technology and knowledge that it takes a long time to develop, but which, on the other hand, are vital for productivity. Therefore, access to venture capital is not only important for the individual entrepreneur, but also for the general improvement of productivity in society.

This year, Denmark is the country with the best access to risk capital as seen as an average over the period 2009-2012.

Note The estimated time it takes to handle a bankruptcy case and close/reorganise a bank-rupt company from presumed information about the company.

Source World Bank, Doing Business 2014

Note Data shows the level of seed and early stage investments.

Source Eurostat and DI calculations

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION40

Index 0-10

Mentality of society supporting competitiveness, 20132.18OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaBrazilChinaIndia

HungarySpain

PolandSlovenia

FranceItaly

PortugalCzech RepublicSlovak Republic

GreeceAustria

BelgiumJapan

MexicoTurkey

DenmarkIceland

South KoreaNorwayFinlandEstonia

NetherlandsUnited Kingdom

New ZealandGermany

ChileAustralia

CanadaSwedenIreland

IsraelSwitzerland

United States

EUROZONE

Share of enterprises with 10 or more employees, per cent

Gazelle enterprises, 20102.17

ManufacturingService

0.0 0.2 0.4 0.6 0.8 1.0 1.2

United States

Denmark*

Spain

Italy

New Zealand

Sweden

Slovenia (2009)

Hungary

Portugal

Israel

Canada (2009)

France

Estonia (2009)

Czech Republic

Strong competitiveness contributes to increasing the incentive to qualify further and achieve good results both individually and at company-level.

For the tenth consecutive year, the United States is the country assessed to have the most compet-itive mentality. American society is permeated by a strong compet-itive mentality that is cultivated already in the educational system with tracking and privileges for the best pupils. This continues onto the labour market where schemes such as “the employee of the month” help to promote competition among the employees of a company.

Gazelles are the subset of high-growth enterprises up to five years old with average annualised growth greater than 20 per cent over a three-year period and at least 10 employees.

Gazelles are an indication of how favourable the environment in which the enterprises operate is. Countries such as the Czech Republic and Esto-nia have a very low starting point, and therefore it is relatively easy for them to achieve a higher proportion of gazelles.

Note This indicator shows to which degree senior managers in the country assess the mentality of society to support competition.

Source IMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

* Data for Denmark is gleaned from Statistics Denmark and is based on market sectors while the OECD has cate-gorised data according to service and manufacturing. Data therefore is not directly comparable, but gives an indi-cation of levels. The ranking is based on manufacturing enterprises.

Source OECD, Entrepreneurship at a Glance, 2013 and Statistics Denmark

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 41

Broadband subscribers per 100 inhabitants

Fixed broadband subscribers, 20122.20OECD

0 5 10 15 20 25 30 35 40 45

TurkeyMexico

ChileSlovak Republic

PolandCzech Republic

HungaryItaly

PortugalIrelandGreece

SloveniaEstonia

SpainIsrael

AustriaAustralia

JapanNew Zealand

United StatesFinlandSwedenCanada

BelgiumGermany

United KingdomIcelandNorwayFrance

South KoreaDenmark

NetherlandsSwitzerland

EUROZONE

Index 0-10

Flexibility and adaptability, 20132.19OECD

0 1 2 3 4 5 6 7 8 9 10

RussiaChinaIndia

Brazil

SlovenienFrance

HungarySpainJapan

AustriaGermany

Czech RepublicChile

BelgiumFinland

ItalyNorwayGreece

Slovak RepublicEstonia

NetherlandsUnited Kingdom

South KoreaAustraliaPortugal

MexicoSwitzerland

CanadaNew Zealand

DenmarkIceland

United StatesSweden

TurkeyPoland

IsraelIreland

EUROZONE

Changing market conditions are companions of globalisation. This means that businesses must be flexible and adaptable if they are to succeed in global competition.

Ireland tops the list this year as the country with the greatest flexibility and adaptability.

Brazilian and Indian flexibility and adaptability are assessed to be over the level of the average performance in both the OECD countries and the Eurozone.

Note This benchmark shows to which degree senior managers in the country assess that the local population displays flexibility and adaptability in the face of challenge.

Source IMD World Competitiveness Yearbook 2013 (survey, scale 0-10)

The number of fixed broadband connections is an indicator of the degree to which the individual cit-izen has access to a good and fast Internet connection.

IT and high-speed connections in both the private and public sector help boost productivity and enhance international competitiveness. The spread of high-speed Internet in sparsely populated areas can reduce gaps between different parts of a country and enhance economic development.

In order to ensure this, the EU has prioritised the rollout of the extremely fast next-generation access network. The European Commission’s 2020-target aims at speeds of 30 megabit per second for all and 100 megabit per second for more than half of all households.

Switzerland, the Netherlands and Denmark take the top three posi-tions.

SourceOECD Broadband Statistics, 2012

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION42

Index 0-10

Economic freedom, 20112.22OECD

0 1 2 3 4 5 6 7 8 9

RussiaIndia

ChinaBrazil

SloveniaMexicoGreece

ItalyTurkeyPoland

Czech RepublicIsrael

PortugalBelgiumIcelandFrance

Slovak RepublicSouth Korea

JapanSpain

NorwayNetherlands

SwedenHungary

AustriaIreland

GermanyUnited States

EstoniaDenmark

United KingdomChile

AustraliaCanadaFinland

SwitzerlandNew Zealand

EUROZONE

Percentage of enterprises that have received orders online in the past year

E-commerce, 20122.21

0 5 10 15 20 25 30 35 40

Italy

Greece

Turkey (2010)

Poland

Hungary

France

Estonia

Austria

Slovak Republic

Spain

Slovenia

Portugal

Finland

United Kingdom

Netherlands

Germany

Ireland

Belgium

Czech Republic

Denmark

Sweden

Norway

Iceland

EUROZONE

E-commerce is a central element in modern, digital society. It minimises sales costs and makes everyday life easier for companies as well as for citizens. Online sales make it eas-ier to sell products across large dis-tances and across national borders. The share of companies that sell products online is therefore an indi-cator of the degree of digitalisation in a country, and suggests the com-petitiveness of the private sector.

Iceland tops the chart this year with 35 per cent of its companies selling products online.

Only 14.5 per cent of Internet users in the EU purchased products online from another EU member state in 2012.

Note Financial sector is not included. Enterprises with ten employees or more selling at least 1 per cent of turnover online

SourceEurostat

Economic freedom promotes dyna-mism and growth in society and creates the basis for an efficient use of the country’s resources.

Cato's index for economic freedom measures a number of socio-eco-nomic provisions that support the initiative, entrepreneurship and freedom of individuals.

For the fifth consecutive year, New Zealand takes top rank as the best provider of economic freedom. New Zealand excels with a well-func-tioning legal system, good access to capital and a low level of govern-ment regulation. Switzerland and Finland are followers-up.

Note High values indicate high economic freedom.

SourceCato Institute, Economic Freedom of the World 2013

Behind the benchmark

Behind the benchmark

GLOBAL BENCHMARK REPORT 2014 – PRODUCTIVITY AND INNOVATION 43

Index 1-7

Quality of infrastructure, 2012-2013 (average)2.24OECD

1 2 3 4 5 6 7

BrazilRussia

IndiaChina

PolandSlovak Republic

HungaryMexicoGreece

IsraelItaly

EstoniaSlovenia

TurkeyChile

Czech RepublicNorway

AustraliaIreland

New ZealandDenmark

AustriaPortugal

United KingdomSwedenCanada

United StatesBelgiumIceland*

South KoreaJapanSpain

GermanySwitzerland

FranceFinland

Netherlands

EUROZONE

Index 1-7

Burden of government regulation, 2012-2013 (average)2.23OECD

1 2 3 4 5 6 7

BrazilRussia

IndiaChina

ItalyGreece

HungarySlovak Republic

SloveniaCzech Republic

BelgiumPoland

PortugalFrance

AustraliaSpain

MexicoIsrael

DenmarkSouth Korea

AustriaJapan

United StatesTurkey

NorwayGermany

CanadaUnited Kingdom

IcelandIreland

NetherlandsChile

SwedenSwitzerland

New ZealandEstoniaFinland

EUROZONE

A reduction of the administrative bur-dens of industry presents a major potential for releasing resources and promoting competitiveness.

During the recession, governments around the world have become more aware of the benefits of rule simplifi-cation and have launched ambitious goals.

Finland, Estonia and New Zealand are assessed to have the least administra-tive hardship for industry. Among the BRIC countries, Brazil has the most widespread red tape.

Note High values indicate that senior managers in the country perceive that the government imposes major administrative burdens on businesses.

Source WEF 2013-2014, survey

High mobility is important for the competitiveness of a country. Good quality infrastructure increases pro-ductivity and attracts international investment. Well-developed infra-structure reduces the effects of large distances between regions, integrates the national market, and connects it to other countries and regions at low cost. A well-in-tegrated infrastructure network is a prerequisite for the access of less-developed municipalities to core economic activities, and can thereby contribute to reducing eco-nomic inequalities across commu-nities and stimulating economic growth.

The Netherlands takes the top posi-tion followed by Finland and France.

* Iceland is without assessment of railway infrastructure since there is less than 50 kilometres of railway in the country.