Embed Size (px)

Citation preview

Gijs Jeuken, CEO of Fidem LifePension System in the Netherlands. European Experience.

Kyiv, October 20th, 2011

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

What Does Dutch Pension System Look Like?

1. A 3-pillar system (partially based on pay-as-you-go + partially capital funded)

2. After 40 years of paid work, workers are eligible for pension – 70% of the last earned or average income)

Pillar 1: 1. Basic old age pension (all residents of the

Netherlands at 65 get a flat-rate pension benefit, which guarantees 70% of the net minimum wage)

2. In comparison to other EU countries, it’s only a limited part of the total old age pension system

3. Pay-as-you-go system: today’s contributors finance the pension payments made to the pensioners of today.

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

What Does Dutch Pension System Look Like?

Pillar 2: 1. Pillar 2 consists of supplementary pensions - part of

people’s terms of employment. It’s the largest pillar in terms of the overall Dutch financial system.

Pillar 3:1. Pillar 3 – supplementary personal pensions, which anyone

can buy from insurance companies.

Concentrated sector:• The largest fund (investment capital of over €200 billion)

represents 37% of the total assets• The largest 5 funds share 57% of the total assets• All these funds are being supervised by the Dutch

National Bank DNB• The Dutch have saved more than the GDP for their old

age.

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

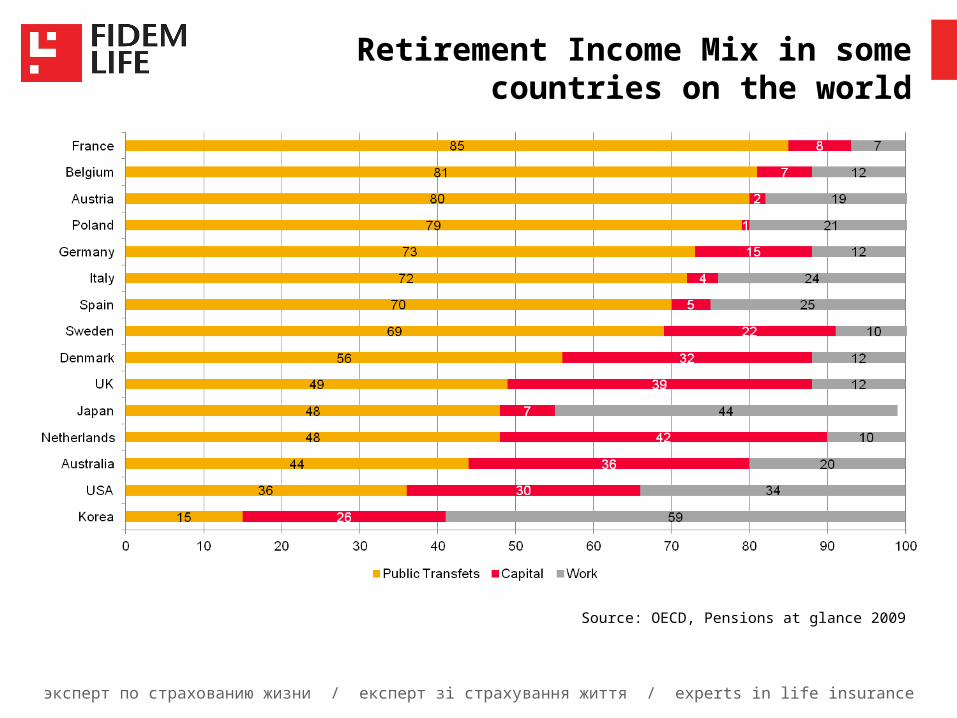

Retirement Income Mix in some countries on the world

Source: OECD, Pensions at glance 2009

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

Pension Legislation and the role of Tax Incentives

Tax:1. Tax legislation fosters development of the Dutch

pension system2. Defines reasonable pensions, fiscal exemption limits3. Pension contributions from the employer and employee

are tax-deductible4. Pension benefits received are taxed as income.

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

Pension Law requirements

1. Pension commitments have to be financed on the basis of capital funding

2. The pension reserves must be placed outside the employer’s company• either by joining an industry-wide pension fund • or by establishing a company pension fund • or by entering into an agreement with an insurance

provider.3. The PL lays down the institutional framework of a

pension scheme:• conditions concerning statute and rules• the constitution of the Governing/Executive Boards• representation of workers/pensioners• supervision on schemes and pension providers • Information given to participants by pension funds

and insurance providers.

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

Pension Participation/Pension Funds

1. The vast majority of employed in the Netherlands (over 90%) participate in a supplementary Pillar 2 scheme – despite obligation for both employers and employees

2. The average employer contribution amounts to approx. 78% of all contributions

Financial position of pension funds:1. Pillar 2 of the Dutch pension system is characterized by

the legal obligation of full funding for the liabilities of pension funds

2. In order to compensate the higher risks, the DNB requires a Dutch pension fund to hold additional reserves (buffers)

3. These requirements resulted in an excess of Dutch pension capital over pension commitments by about 35% in 2001

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

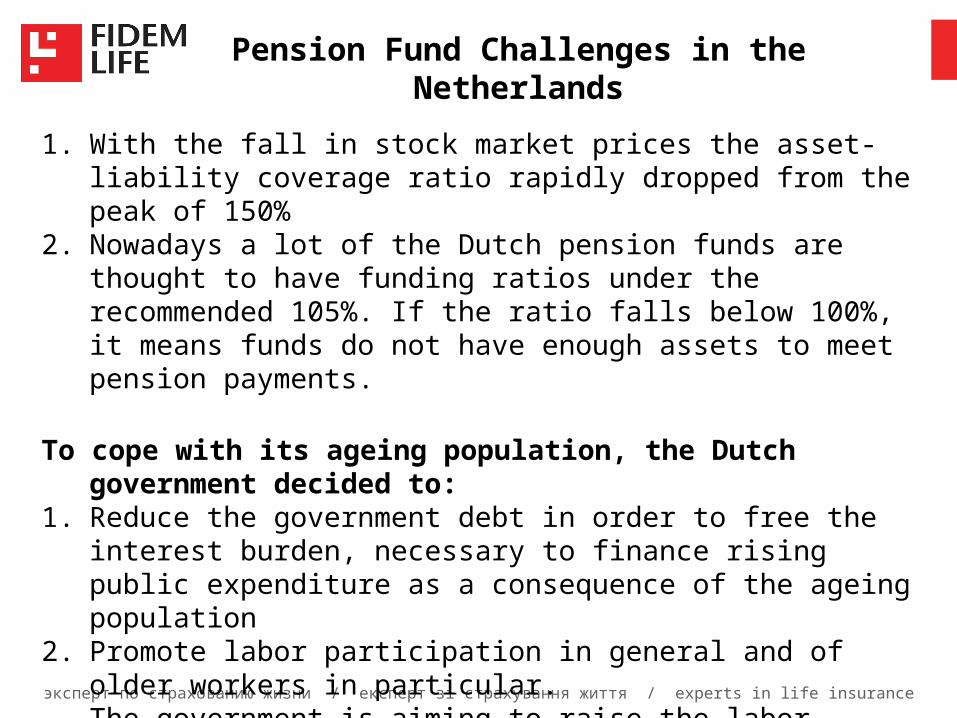

Pension Fund Challenges in the Netherlands

1. With the fall in stock market prices the asset-liability coverage ratio rapidly dropped from the peak of 150%

2. Nowadays a lot of the Dutch pension funds are thought to have funding ratios under the recommended 105%. If the ratio falls below 100%, it means funds do not have enough assets to meet pension payments.

To cope with its ageing population, the Dutch government decided to:

1. Reduce the government debt in order to free the interest burden, necessary to finance rising public expenditure as a consequence of the ageing population

2. Promote labor participation in general and of older workers in particular.The government is aiming to raise the labor participation of 55 – 65-year-old workers to 40% in 2010 and to 50% in 2020.

Fiscal facilities for early retirement are already reduced.

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

Ukraine is heading in the right direction

1. Sense of urgency driven by needed reforms in Public Finance

2. Increasing of pension age (the most fair way to spread responsibility for future pension provision between generations)

3. Awareness that participating parties should have minimum standards

4. Balanced budget

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

Dutch Pension System. Things Ukraine could take into account

1. Clear fiscal incentives both for employers and employees (Pillar 2 and 3)

2. Transparent regulation on participation and quality3. Quality assurance by regular reporting and

measuring of key indicators by independent regulator

4. Supported by Pillar 3 programs, which do not discriminate between offering parties (Pension Funds, Life Insurance), also based on fiscal incentives

5. Every working person realizes Pillar 1 (State Pension), alone will not suffice

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

Caveats of Pension Reform

1. Guarantee funds to cover failure of regulation/quality management (for asset management and Life Insurance)

2. Discrepancy between fiscal and regulatory treatment of Pension Funds and Life Insurance Companies on participation and role

Keys to Successful Reform: 1. Fiscal framework on Income Tax, ISW (Social

Security Tax) and exemption periods to be set for Pillar 3

2. Level playing field for participants that are of good standing and quality

3. Regulator to move the sector transparently into the right direction

эксперт по страхованию жизни / експерт зі страхування життя / experts in life insuranceэксперт по страхованию жизни / експерт зі страхування життя / experts in life insurance

www.fidem.ua

Thank you for attention!

Gjis Jeuken, CEO of Fidem Life