Embed Size (px)

Citation preview

Getting Up To Speed: The Academic Response to the Challenge of Change

Belverd E. Needles, Jr.

Vice-President Education-Elect

American Accounting Association

DePaul University

Disclaimer

The views expressed in this presentation are solely those of the author and do not represent the views of the AAA or any other organization.

Objective

To summarize efforts of the AAA and other organizations to address emerging developments in accounting

To assess the readiness of accounting educators to address the issues of International Financial Reporting Standards (IFRS)

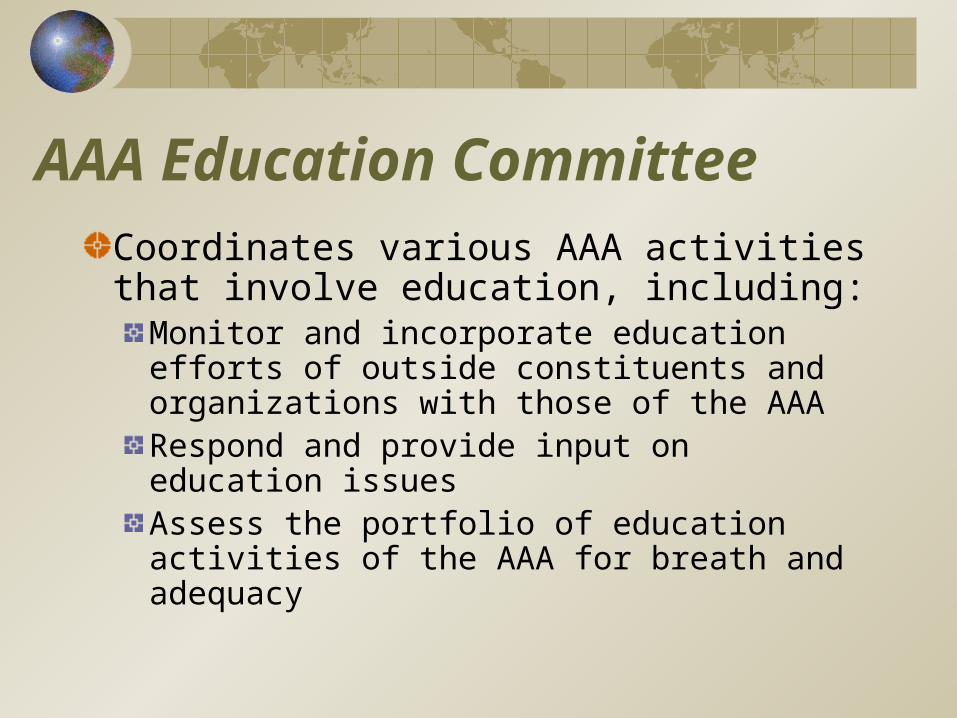

AAA Education Committee

Coordinates various AAA activities that involve education, including:

Monitor and incorporate education efforts of outside constituents and organizations with those of the AAARespond and provide input on education issuesAssess the portfolio of education activities of the AAA for breath and adequacy

AAA Activities

The AAA has long played a critical role in transforming accounting curriculum.

Treasury ACAP Committee (Gary Previts, President of AAA)

AACSB-Ethics throughout the curriculum equivalent to a course

AICPA-The CPA Profession: Opportunities, Responsibilities, and Services

Fair Value Accounting Education Report

AICPA IFRS Roundtable

Challenges Facing Accounting Educators

Fair value accounting

Forensic accounting

Ethics and professional responsibilities

International Financial Reporting Standards (IFRS)

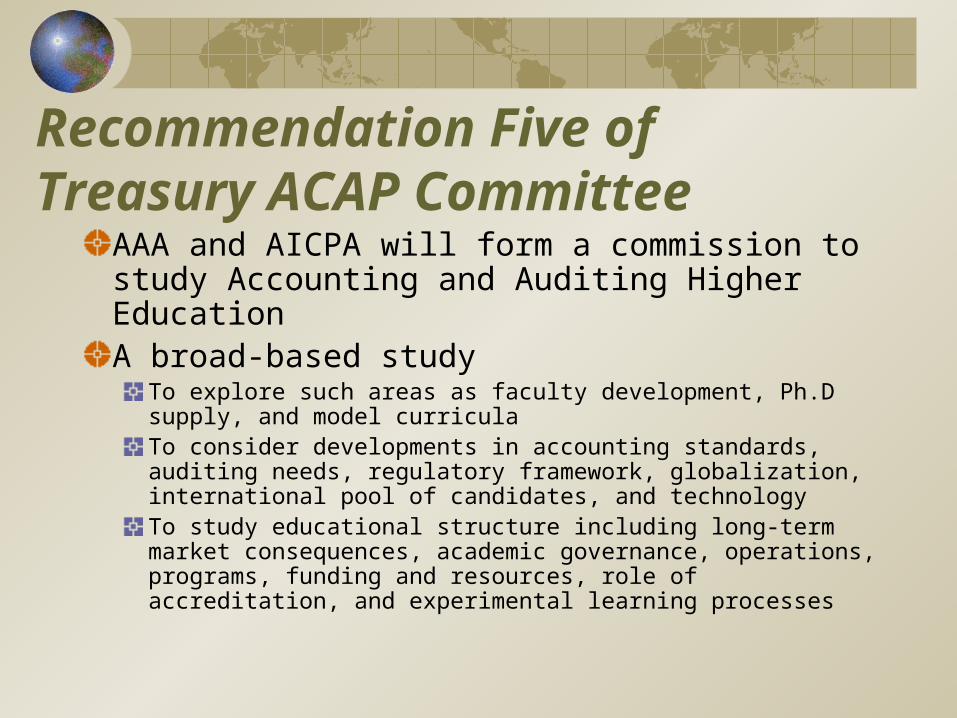

Recommendation Five of Treasury ACAP Committee

AAA and AICPA will form a commission to study Accounting and Auditing Higher EducationA broad-based study

To explore such areas as faculty development, Ph.D supply, and model curriculaTo consider developments in accounting standards, auditing needs, regulatory framework, globalization, international pool of candidates, and technologyTo study educational structure including long-term market consequences, academic governance, operations, programs, funding and resources, role of accreditation, and experimental learning processes

Accounting Educator Response

Accounting Educators have shown an ability to respond quickly to important changes in the profession

Sarbanes-Oxley was passed in 2002

By 2004-2005 the effects of this law were fully incorporated into the textbooks and the curriculum

Who Should Teach Ethics Courses?

Hurtt and Thomas (2008) report a mixed model in Texas:57% say the course should be housed in Accounting Dept. (48% are currently outside of Accounting Dept.)60% favor both a separate and an integrated approachNo school used an instrument such as DIT to measure effects of teaching ethicsFaculty teaching the courses have little training in ethics (39% either did not answer or selected the option that they had zero hours of training)

9

Who Should Teach Ethics Courses?

The preference seems to be toward joint teaching:

Accounting faculty in Blanthorne, et al. (2007) rated themselves as the most appropriate faculty to teach ethics

Over 72% of faculty, students and professionals in Abdolmohammadi (2008) indicated that ethics courses should be taught jointly by accounting and philosophy professors • Only 3.5% said philosophy professors only• Only 24.2% said accounting professors only :

– This indicates a staffing problem: “Few, if any [faculty], are trained for this in our doctoral programs. (AAA Education Committee response to NASBA, 2006 proposal).

What Should Be The Content Of Ethics

Courses? Jennings (2004) provides a reading list and a discussion of seminal and other important works.Thomas (2004) presents a list of texts and reference works, commercial books, academic and professional articles, and electronic resources such as film and Internet Web sites for teaching ethics in a stand-alone or an integrated ethics training program.In addition to covering integrity, objectivity, and independence, NASBA proposes ethical reasoning.

What Should Be The Content Of Ethics Courses?

Hurtt and Thomas (2008) report that in Texas: 85% incorporate a mixed-model approach (ethical theory, decision making, codes of conduct)Top content issues are:• Components of codes of conduct [of AICPA and TSBPA]

such as integrity, honesty, independence, objectivity, impartiality, confidentiality

• Ethical reasoning• Making correct choices under pressure • Moral exemplars

What Should Be The Content Of Ethics Courses?

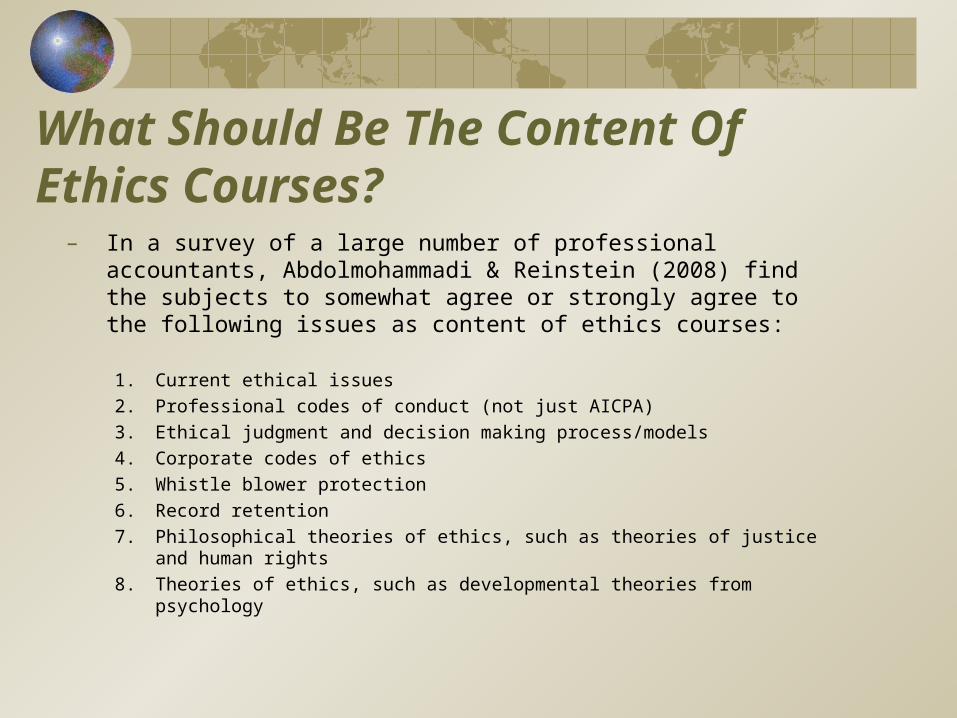

– In a survey of a large number of professional accountants, Abdolmohammadi & Reinstein (2008) find the subjects to somewhat agree or strongly agree to the following issues as content of ethics courses: 1. Current ethical issues

2. Professional codes of conduct (not just AICPA)

3. Ethical judgment and decision making process/models

4. Corporate codes of ethics

5. Whistle blower protection

6. Record retention

7. Philosophical theories of ethics, such as theories of justice and human rights

8. Theories of ethics, such as developmental theories from psychology

What Can Be Done Outside the Classroom?

Create an ethical culture in the business school and Department/School of Accounting

Develop Student Honor Codes and/or Codes of Ethics

Teach students about plagiarism and classroom cheating; enforce rules

Invite college/school-wide guest speakers to talk about ethical leadership

Help faculty learn to teach ethics (e.g., AACSB holds ethics seminars)

IFRS Timetable2005 European Union Adopted IFRS followed by Japan, Canada, Israel, and Australia2007 SEC allows foreign registrants in the U.S. use IFRS2008 SEC issues a Roadmap for public comment2011 Decision as to go forwardIt’s not a done deal.

SEC Proposal

Part I allows a small number of U.S. public companies to early adopt IFRS (110 companies-14% of U.S. capitalization) in 2009: Must reconcile to U.S. GAAP

Part II identifies four milestones to be evaluated in 2011, at which time a further time table will be set

Milestones

Continued development of IFRS and convergence with U.S. GAAP

Revenue recognition

Financial statement presentation

Lessee accounting

Post-retirement benefits

Consolidation

De-recognition

Fair value

Milestones

Progress on accountability and stability including (regulatory) oversight body and stable fundingContinued development of IFRS XBRL consistent with SEC TaxonomyProgress on IFRS related education, including integration of IFRS into accounting curriculum

KPMG/AAA Education Committee Faculty Survey

530 faculty responses

Summary conclusion: Overall faculty expectations are quite encouraging and very much in line with the SEC timetable.

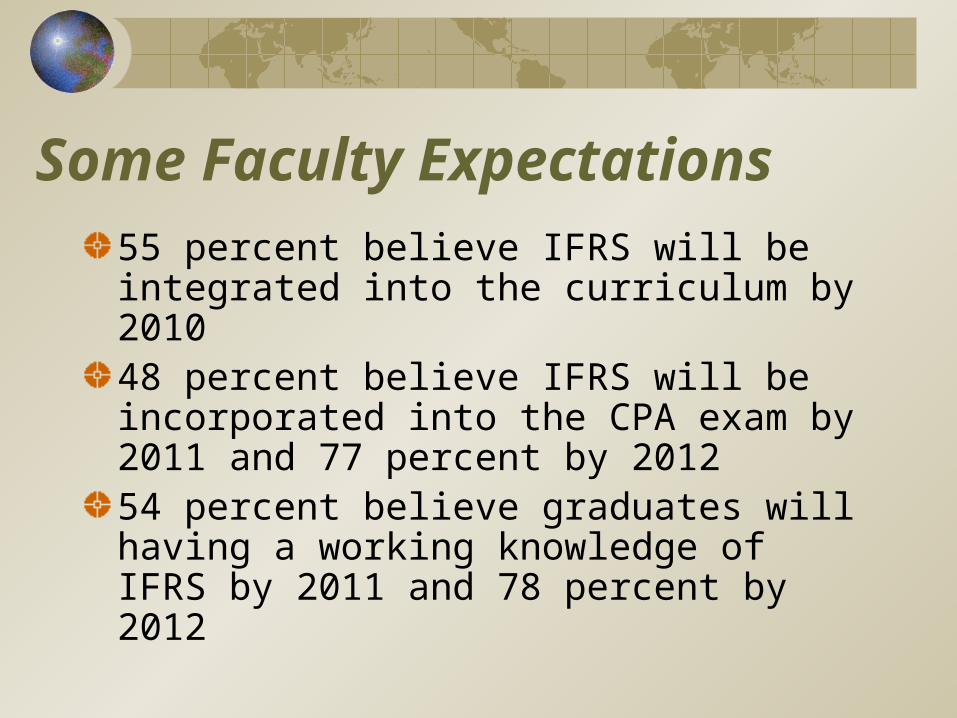

Some Faculty Expectations55 percent believe IFRS will be integrated into the curriculum by 201048 percent believe IFRS will be incorporated into the CPA exam by 2011 and 77 percent by 201254 percent believe graduates will having a working knowledge of IFRS by 2011 and 78 percent by 2012

How Will IFRS Be Incorporated in the Curriculum?

89 percent believe textbooks will be the main source of IFRS in the curriculum74 percent believe this will be accomplished by 2011 and 94 percent by 2012Most believe IFRS will be taught with a compare and contrast approach with U.S. GAAP

How Will Faculty Come Up to Speed?Most believe it is the existing individual faculty members’ responsibility to come up to speed on IFRSAccounting faculty have met these challenges before:

Sarbanes-Oxley and the PCAOBModern managerial accounting topics such as balanced scorecard, value chain, activity-based costing, etc.

Textbooks will play a major role in changing the curriculum

Role of AAA in Incorporating IFRS into the Accounting Curriculum

A special issue of Issues in Accounting Education prepared in conjunction with the International Accounting Section of the AAA (November, 2007) addressed the issue of IFRS educationJoint Project with Grant Thornton developing IFRS casesAt its Annual Meeting in August, which had the highest attendance in its history, more than 20 sessions were devoted to IFRS

AAA IFRS CPE Sessions

IFRS – U.S. GAAP Comparison

FASB/IASB Update – Part 1

FASB/IASB Update – Part 2

Incorporating International Financial Reporting Standards (IFRS) in Intermediate Financial Accounting — How to Proceed

IFRS Main Sessions and PanelsIFRS Is Here, and What To Do About ItThe IFRS of the Academic WorldAcademic Open Forum: The FASB-IASB Conceptual Framework ProjectIncorporating IFRS in Intermediate AccountingChallenges of Regulators and Practitioners if IFRS is Adopted for Domestic IssuersHow to Successfully Integrate IFRS into the UG Accounting CurriculumA Globally Converged Conceptual Framework

More IFRS SessionsSEC Update--Regulators Discussion of IFRS IssuesThe Expanding Role of IFRS--Research IssuesIFRS IIFRS IIIFRS IIIIFRS IVIncorporating IFRS in the Financial Accounting CurriculumIntegrating an IFRS Module into the Master’s CurriculumFASB-IASB UpdateSEC IFRS Reporting ISSUES

IAAER Role

Promotes Excellence in accounting education

Maximize the contribution of academics to the development and maintenance of high quality, globally recognized standards of accounting practice

IAAER Promotes IFRS

IAAER Members (including students) receive access to eIFRSUniversity members enable access by all faculty: forty universities currentlyFifty-one academic and professional association members around the worldCongresses, conferences, and globalization roundtables

Other Organizations

Other organizations are making extensive efforts to bring faculty up to speed, including

The major accounting firms

AICPA

IASB

SEC

IMA

Other professional organizations

Conclusion

Accounting educators will meet the challenge of change

They will do this in multiple ways

Many organizations, including the AAA, will work together to achieve this objective