Embed Size (px)

Citation preview

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 1

Financial & Managerial Financial & Managerial Accounting 2002eAccounting 2002e

Belverd E. Needles, Jr.Belverd E. Needles, Jr.

Marian PowersMarian Powers

Susan CrossonSusan Crosson- - - - - - - - - - -

Multimedia Slides by:

Harry HooperSante Fe Community College

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 2

Chapter 6Chapter 6Merchandising Merchandising

Operations and Operations and Internal ControlInternal Control

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 3

LEARNING OBJECTIVESLEARNING OBJECTIVES1. Identify the management issues related

to merchandising businesses.

2. Define and distinguish the terms of sale for merchandising transactions.

3. Prepare an income statement and record merchandising transactions under the perpetual inventory system.

4. Prepare an income statement and record merchandising transactions under the periodic inventory system.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 4

5. Define internal control, identify the five components of internal control, and explain seven examples of control activities.

6. Describe the inherent limitations of internal control.

7. Apply internal control activities to common merchandising transactions.

LEARNING OBJECTIVESLEARNING OBJECTIVES (continued)(continued)

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 5

Supplemental Objective Supplemental Objective

8. Apply sales and purchases discounts to merchandising transactions.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 6

Management Issues in Management Issues in Merchandising BusinessesMerchandising Businesses

OBJECTIVE 1 Identify the management issues

related to merchandising businesses.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 7

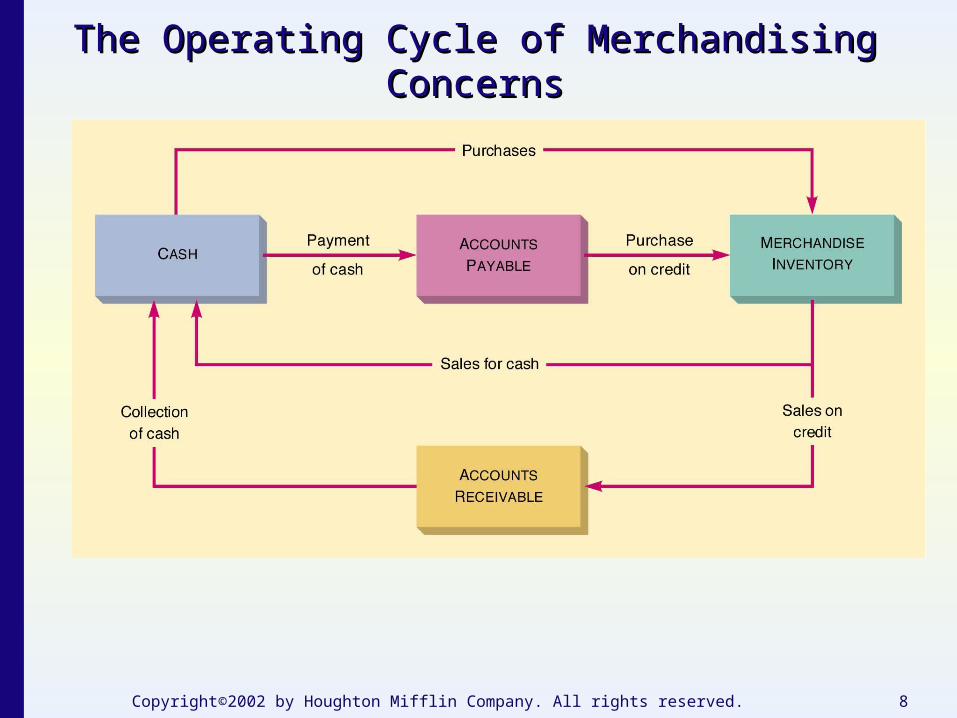

Merchandising businesses differ from service businesses in that they have goods on hand for sale to customers and engage in a series of transactions, listed below, called the operating cycle. Purchase of inventory for cash or credit Payment for purchases made on credit Sales of inventory for cash or credit Collection of cash from credit sales

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 8

The Operating Cycle of Merchandising ConcernsThe Operating Cycle of Merchandising Concerns

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 9

• Purchases of merchandise are usually made on credit. Suppliers of merchandise usually require payment before inventory is sold. The merchandiser must plan for cash flows from prior sales, additional stockholders’ investment, or from borrowing to finance the inventory until it is sold and resulting revenue is collected.

• Operators of a merchandising business must carefully manage cash flows or liquidity.

• If a company can’t pay its bills when due, it may be forced out of business.

Cash Flow ManagementCash Flow Management

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 10

• A company must sell its merchandise at a price that exceeds its cost by a sufficient margin to pay operating expenses and have enough left to provide sufficient net income or profitability.

• Profitability management includes: Setting appropriate prices for merchandise. Purchasing merchandise at favorable prices

and terms. Maintaining acceptable levels of operating

expenses.• An effective tool for controlling expenses is the

operating budget.

Profitability ManagementProfitability Management

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 11

Features of the Perpetual Features of the Perpetual Inventory SystemInventory System

• Continuous records are kept of the quantity and, usually, the cost of individual items as they are bought and sold.

• More effective for providing current, real time information about actual quantities and dollar amounts of inventory available for sale and sold.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 12

• Physically count inventory, usually at end of accounting period.

• No detailed records of the actual inventory available or sold are maintained during the accounting period.

• Less costly than perpetual inventory method, but provides less information.

Features of the Periodic Features of the Periodic Inventory SystemInventory System

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 13

Control of Merchandising Control of Merchandising OperationsOperations

• Principal transactions of merchandising businesses are vulnerable to theft and embezzlement. Cash and inventory are easy to steal. These asset accounts are usually involved in a

large number of transactions.• Management’s responsibility is to establish

an environment, accounting systems, and control procedures that will protect the company’s assets.

• These systems and procedures are called internal control.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 14

DiscussionDiscussion

Q.Q. What four issues must be faced by managers of merchandising businesses?

A.A. The four issues that must be faced by managers of merchandising businesses are (1) cash flow management, (2) profitability management, (3) choosing between the periodic and the perpetual inventory systems, and (4) establishing an internal control structure that protects the business’s assets.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 15

Terms of SaleTerms of Sale

OBJECTIVE 2 Define and distinguish the

terms of sale for merchandising transactions.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 16

• Trade discount. A reduction of the list price. Not shown in accounting records.

• Sales discount.Discount given for early payment.Taken if payment is made within the

terms of sale. For example, “2/10, n/30.”

Practice of giving sales discounts has been declining.

Sales TermsSales Terms

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 17

• FOB shipping point.Title passes at origin.Buyer pays the freight.

• FOB destination.Title passes at destination.Seller pays the freight.

Sales Terms Sales Terms (Continued)(Continued)

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 18

Perpetual Inventory SystemPerpetual Inventory System

OBJECTIVE 3 Prepare an income statement and record

merchandising transactions under the perpetual inventory system.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 19

Inventory and cost of Goods Sold are continually updated during the accounting period, as purchases, sales, and other inventory transactions take place.

Applying the Perpetual Inventory Applying the Perpetual Inventory SystemSystem

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 20

• Purchases of Merchandise on Credit The cost of merchandise purchased is placed in the

Merchandise Inventory account at the time of purchase.

• Transportation Costs on Purchases Accumulated in a Freight In / Transportation In account. In some cases, the seller pays the freight charges and

bills them to the buyer as a separate item on the invoice.

• Purchases Returns and Allowances Returned merchandise is removed from the Merchandise

Inventory account.

• Payments on Account Payments by cash (or checks) to suppliers.

Transactions Related to Purchases of Transactions Related to Purchases of MerchandiseMerchandise

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 21

• At the time of sale, the cost of merchandise is transferred from the Merchandise Inventory account to the Cost of Goods Sold account.

• In the case of a return, the cost of the merchandise is transferred from Cost of Goods Sold back to Merchandise Inventory.

Transactions Related to Sales of Transactions Related to Sales of MerchandiseMerchandise

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 22

• Sales of Merchandise on Credit Two entries are necessary

Record the sale as a debit to Accounts Receivable

Update the Cost of Goods sold by transferring from Merchandise Inventory

• Cash sales of Merchandise Debit Cash for the amount of the sale

• Payment of Delivery Costs Accumulated in the Freight Out Expense

account Shown as a selling expense on the income

statement

Transactions Related to Sales of Transactions Related to Sales of MerchandiseMerchandise

(continued)(continued)

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 23

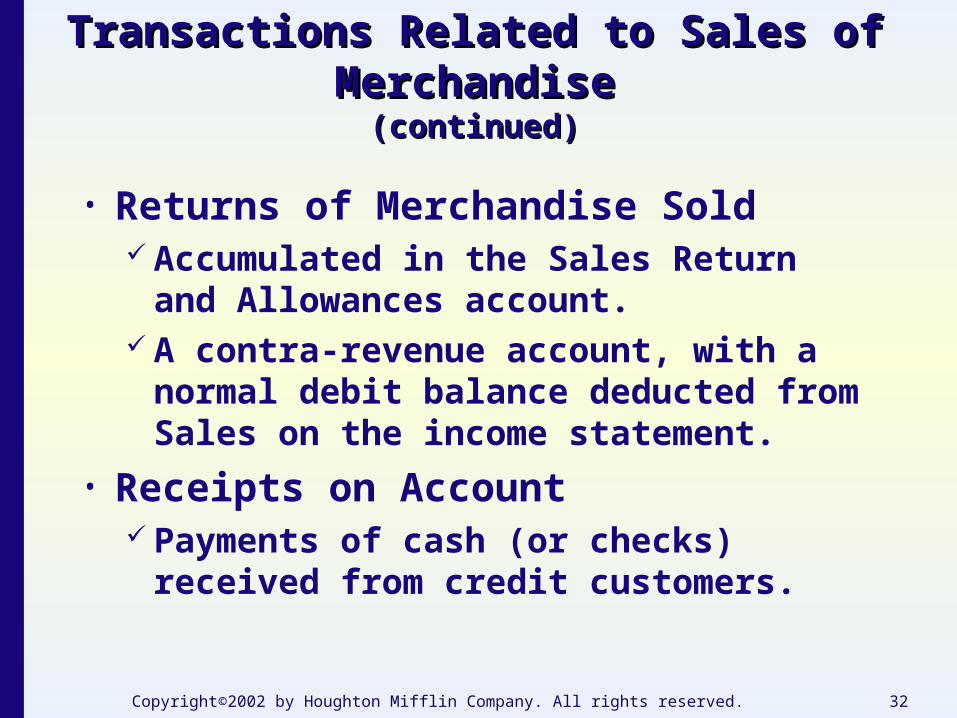

Transactions Related to Sales of Transactions Related to Sales of MerchandiseMerchandise

(continued)(continued)

• Returns of Merchandise Sold Accumulated in the Sales Return and

Allowances account, a contra-revenue account, with a normal debit balance, deducted from Sales in the income statement

The cost of merchandise must also be transferred from the COGS account back into the Merchandise Inventory account

• Receipts on Account Receipts of cash (or checks) from credit

customers recorded as credits to Accounts Receivable

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 24

DiscussionDiscussion

Q.Q. How are merchandising transactions recorded under the perpetual inventory system?

A.A. Merchandising transactions are recorded during the accounting periods, as purchases, sales, and other inventory transactions take place.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 25

Merchandising TransactionsMerchandising Transactions

OBJECTIVE 4 Prepare an income statement

and record merchandising transactions under the periodic inventory system.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 26

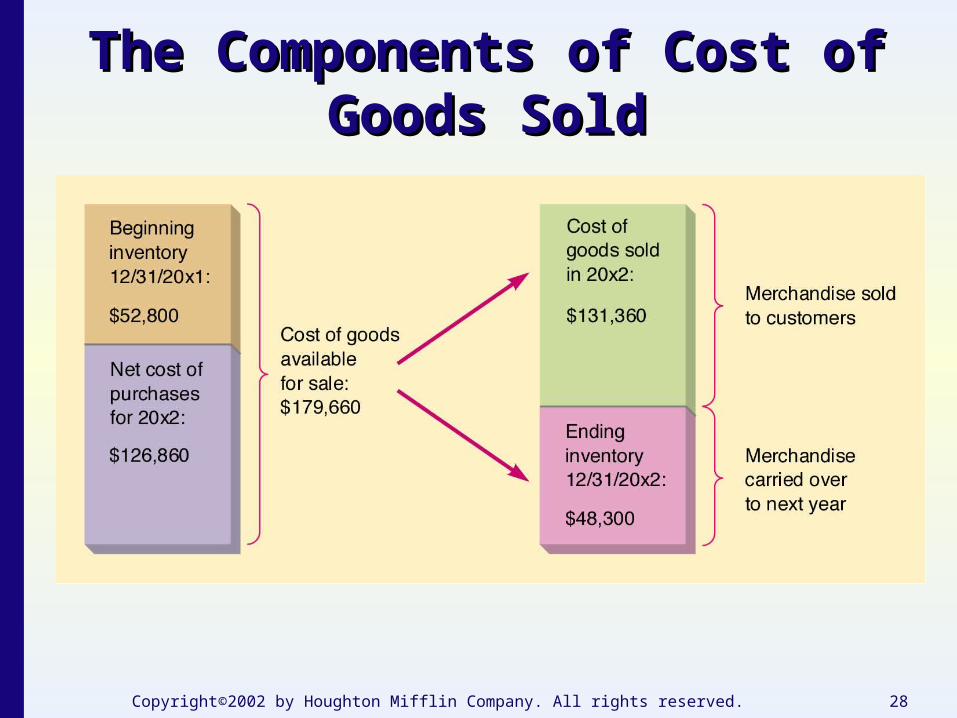

• Cost of Goods Sold must be computed, because it is not updated for purchases, sales and other transactions during the accounting period.

• To calculate cost of goods sold:1. Net purchases = (total purchases –

deductions)2. Net cost of purchases = (net purchases +

freight charges on the purchases 3. Goods available for sale = (net cost of

purchases + beginning purchases)4. Costs of Goods Sold = (Goods available for

sale – ending inventory)

Applying the Periodic Inventory Applying the Periodic Inventory SystemSystem

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 27

• Physical inventory is taken and recorded in the Merchandise Inventory account at the end of the period.

• A Purchases account is used to accumulate the purchases of merchandise during the accounting period.

• A Purchases Returns and Allowances account is used to accumulate returns of and allowances on purchases.

Transactions Related to Transactions Related to Purchases of MerchandisePurchases of Merchandise

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 28

The Components of Cost of Goods The Components of Cost of Goods SoldSold

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 29

• Purchases of Merchandise on Credit Purchases, a temporary account, used to

accumulate the total cost of merchandise purchased for resale during the accounting period.

It does not indicate whether merchandise has been sold or is still on hand.

• Transportation Costs on Purchases Usually accumulated in a Freight In account. In some cases, the seller pays the freight

charges and bills them to the buyer as a separate item on the invoice.

Transactions Related to Purchases Transactions Related to Purchases of Merchandiseof Merchandise

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 30

Transactions Related to Purchases of Transactions Related to Purchases of MerchandiseMerchandise

(continued)(continued)

• Purchases Returns and AllowancesRecorded in the Purchases

Returns and Allowances account. A contra-purchases account with a

normal credit balance, deducted form Purchases on the income statement.

• Payments on AccountPayments made to suppliers.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 31

• Sales of Merchandise on Credit Debit the Accounts Receivable

account for the amount of the sale.• Cash Sales of Merchandise

Debit Cash for the amount of the sale.

• Payment of Delivery Costs Accumulated in the Freight Out /

Delivery Expense account. Shown as a selling expense on the

income statement.

Transactions Related to Sales of Transactions Related to Sales of MerchandiseMerchandise

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 32

Transactions Related to Sales of Transactions Related to Sales of MerchandiseMerchandise

(continued)(continued)

• Returns of Merchandise Sold Accumulated in the Sales Return and

Allowances account. A contra-revenue account, with a

normal debit balance deducted from Sales on the income statement.

• Receipts on Account Payments of cash (or checks) received

from credit customers.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 33

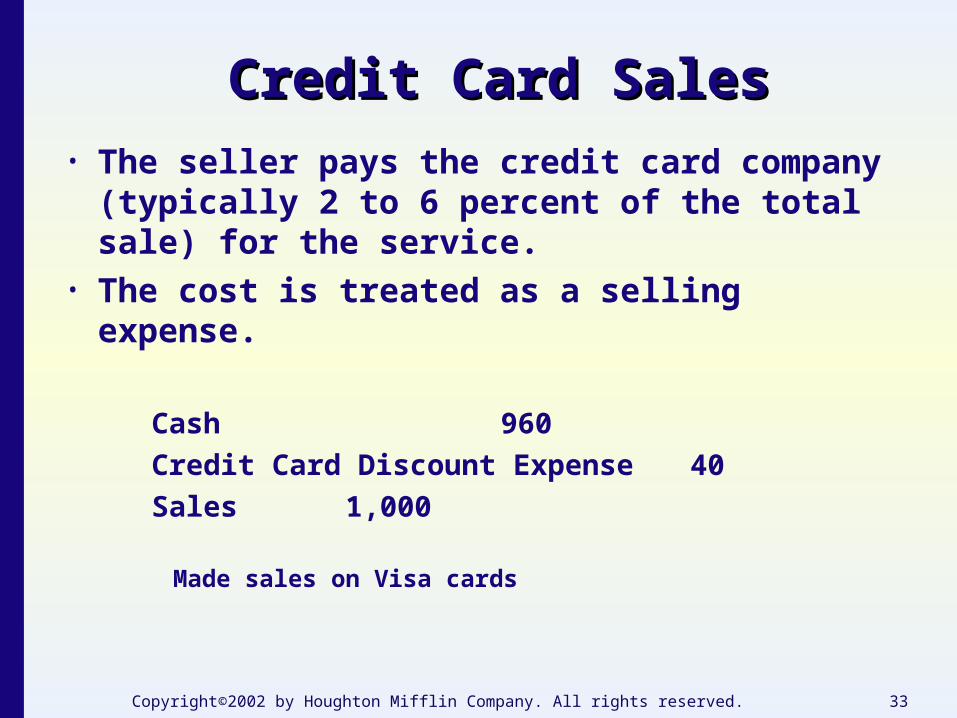

Credit Card SalesCredit Card Sales• The seller pays the credit card company

(typically 2 to 6 percent of the total sale) for the service.

• The cost is treated as a selling expense.

Cash 960

Credit Card Discount Expense 40

Sales 1,000

Made sales on Visa cards

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 34

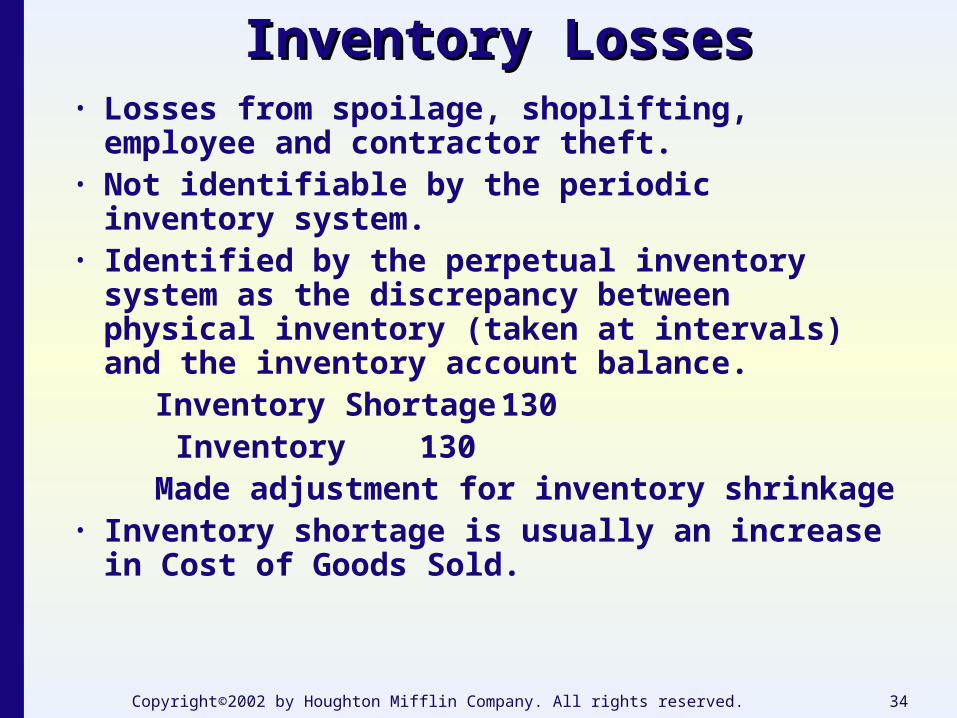

Inventory LossesInventory Losses• Losses from spoilage, shoplifting, employee

and contractor theft.• Not identifiable by the periodic inventory

system.• Identified by the perpetual inventory system as

the discrepancy between physical inventory (taken at intervals) and the inventory account balance.

Inventory Shortage 130Inventory 130

Made adjustment for inventory shrinkage• Inventory shortage is usually an increase in

Cost of Goods Sold.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 35

DiscussionDiscussion

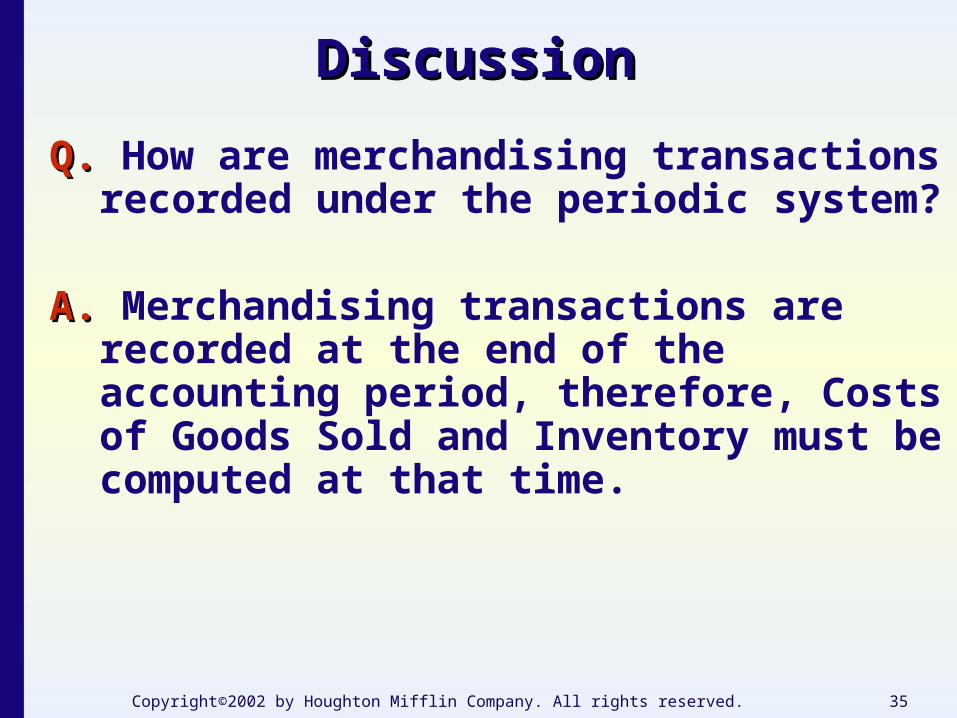

Q.Q. How are merchandising transactions recorded under the periodic system?

A.A. Merchandising transactions are recorded at the end of the accounting period, therefore, Costs of Goods Sold and Inventory must be computed at that time.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 36

Internal Control Structure:Internal Control Structure:Basic Elements and ProceduresBasic Elements and Procedures

OBJECTIVE 5 Define internal controlinternal control, , identify

the five components of internal control and explain seven examples of control activities.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 37

Internal Control DefinedInternal Control Defined

• Internal control is all the policies and procedures management uses to:Protect the firm’s assets and

ensure the accuracy and reliability of the accounting records.

Promote operating efficiency and encourage adherence to management’s policies.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 38

Components of Internal ControlComponents of Internal Control

• Internal control includes:1. The control environment.

2. Risk assessment.

3. Information and communication.

4. Control activities.

5. Monitoring.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 39

The Control EnvironmentThe Control Environment

• Created by the overall attitude, awareness, and actions of management.

• Influenced by: Management’s philosophy and operating

style. Organizational structure. Methods of assigning authority and

responsibility. Personnel policies and practices.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 40

Risk AssessmentRisk Assessment

The identification of areas where risks of loss of assets or inaccuracies in the accounting records are high so that adequate controls can be implemented.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 41

Information and Communication Information and Communication

Relates to the accounting systems established by management to identify, assemble, analyze, classify, record, and report a company’s transactions and to the clear communication of individual responsibilities in achieving these functions.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 42

Control Activities Control Activities

The policies and procedures management puts in place to see that its directives are carried out.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 43

Monitoring Monitoring

Involves management’s regular assessment of the quality of internal control including periodic review of actual compliance with all policies and procedures.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 44

Control ActivitiesControl Activities

1. Authorization2. Recording transactions3. Documents and records4. Physical controls5. Periodic checks6. Separation of duties7. Sound personnel procedures

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 45

DiscussionDiscussion

Q.Q. A good system of internal controls accomplishes what broad objectives?

A.A. It safeguards the company assets, produces reliable accounting records, promotes operating efficiency, and encourages adherence to management’s policies.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 46

Limitations of Internal ControlLimitations of Internal Control

OBJECTIVE 6 Describe the inherent

limitations of internal control.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 47

Limitations of Internal ControlLimitations of Internal Control

• Human error.• Misunderstandings.• Mistakes in judgment.• Carelessness.• Distraction.• Fatigue.• Collusion.• Dishonesty.• Changes in conditions.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 48

DiscussionDiscussion

Q.Q. Why is the separation of duties necessary to ensure sound internal control? What does this principle assume about the relationships of employees in a company and the possibility of two or more of them stealing from the company?

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 49

A. The separation of duties is important to sound internal control because a person who combines the responsibilities of keeping records, operating a department, and managing assets would be able to misappropriate assets without detection. The separation of duties assumes that two or more employees will not work together to overcome the controls.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 50

Internal Control over Internal Control over Merchandising TransactionsMerchandising Transactions

OBJECTIVE 7 Apply internal control

activities to common merchandising transactions.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 51

Internal Control and Internal Control and Management GoalsManagement Goals

• Key Goals for the success of a merchandising business.Prevent losses of cash or

inventory owing to theft or fraud.

Provide accurate records of merchandising transactions, and account balances.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 52

Goals for ManagementGoals for Management

Broader Goals:• Keep enough inventory on hand

to sell to customers without overstocking.

• Keep enough cash on hand to pay for purchases in time to receive discounts.

• Keep credit losses as low as possible by making credit sales only to customers who are likely to pay on time.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 53

Controls for Meeting Controls for Meeting Management’s GoalsManagement’s Goals

• Cash budget.• Separation of duties.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 54

Control of Cash Sales ReceiptsControl of Cash Sales Receipts• Cash is received either by mail or over the

counter. In either case: It should be recorded immediately in cash receipts

journal. It establishes a written record of cash receipts.

• Control of cash received through the mail. Encourage customers to pay by check. Handle by two or more employees. Make a list of receipts in triplicate.

• Control of cash received over the counter. Cash registers. Pre-numbered sales tickets.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 55

Control of Purchases and Cash Control of Purchases and Cash DisbursementsDisbursements

• Pay cash only based on specific authorization backed by proof of validity and amount of claim.

• Separate purchasing and payment duties.

• Document and verify by at least 2 people.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 56

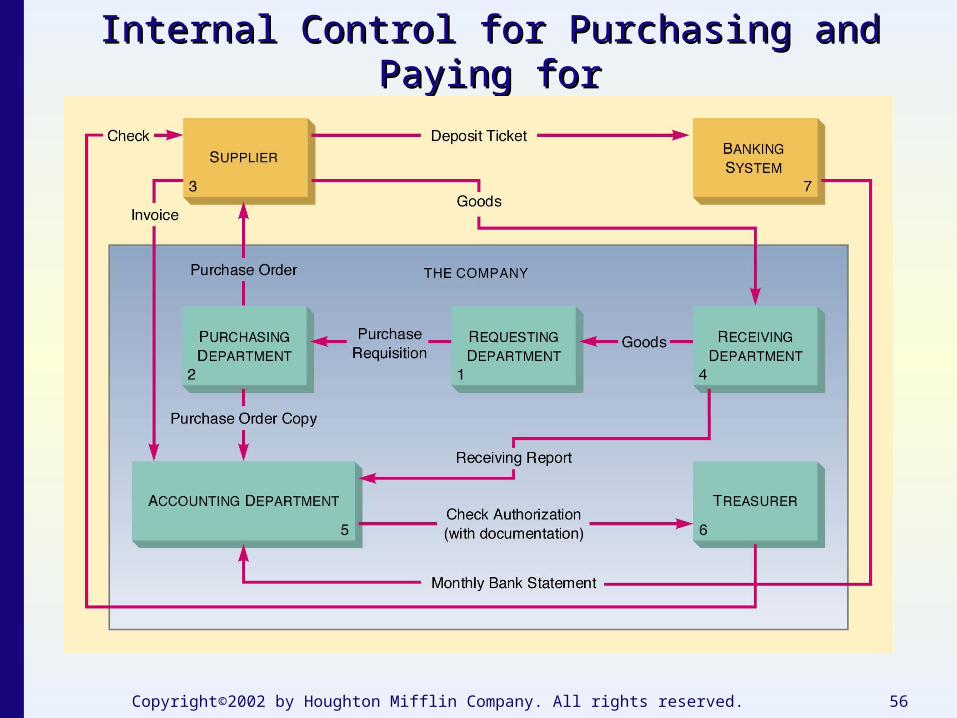

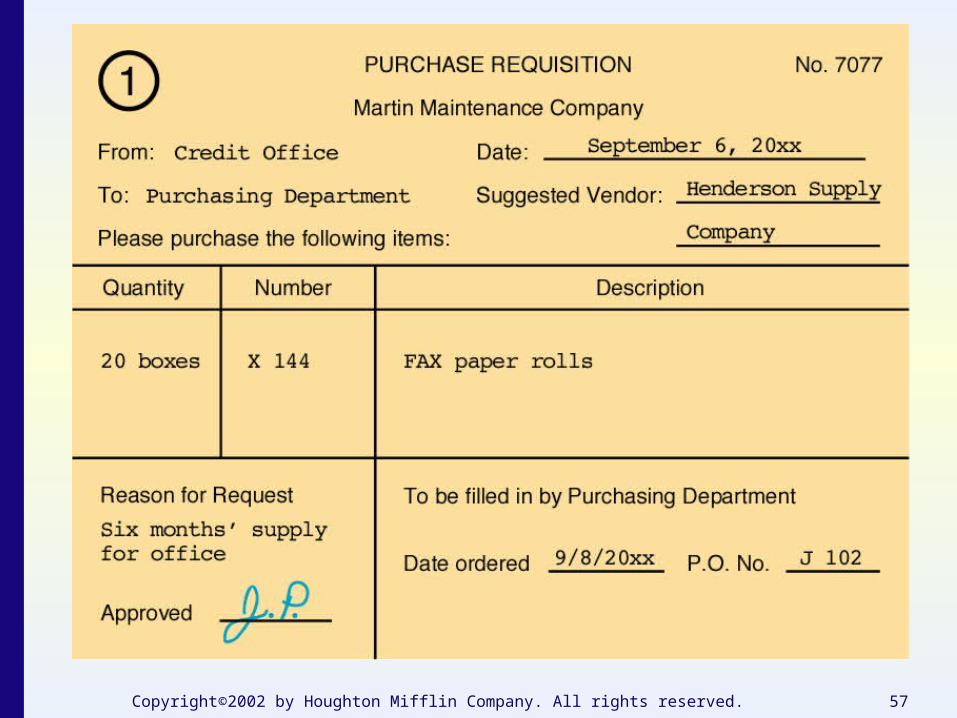

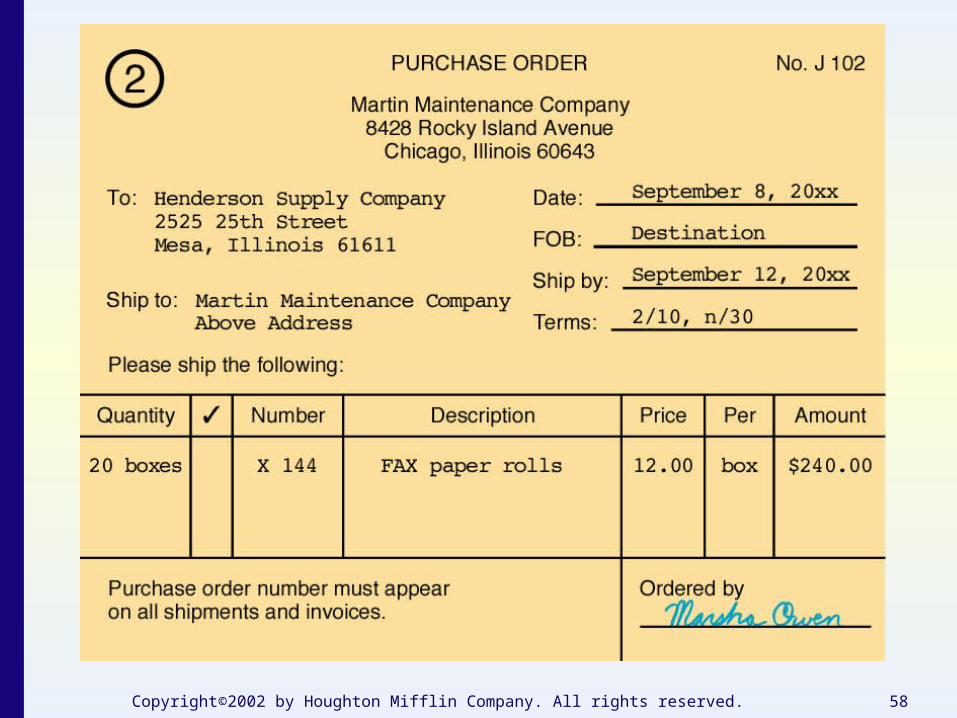

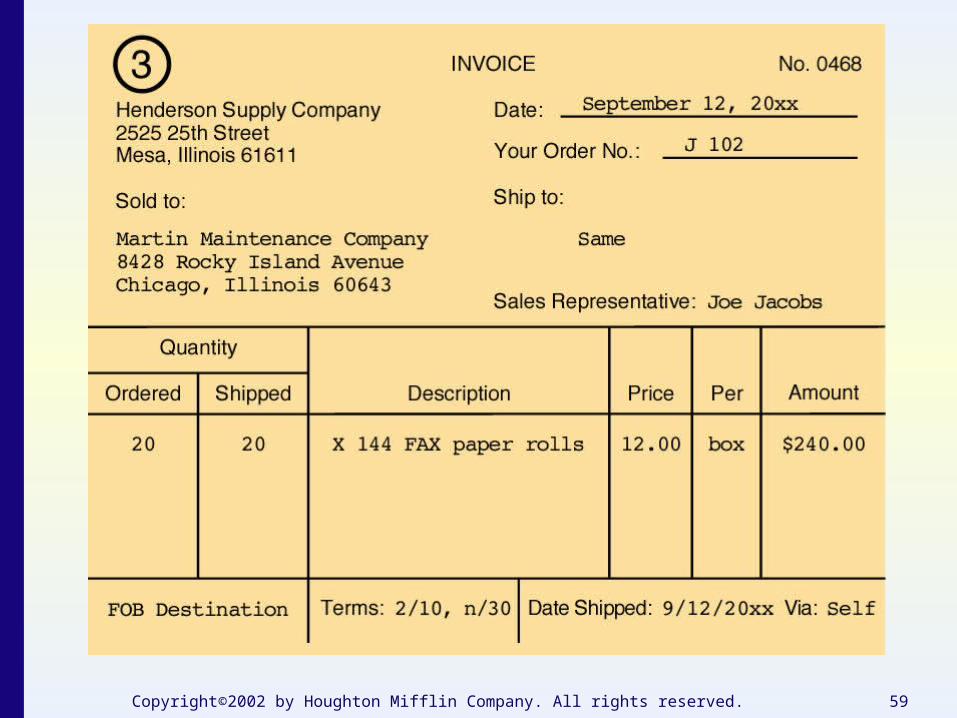

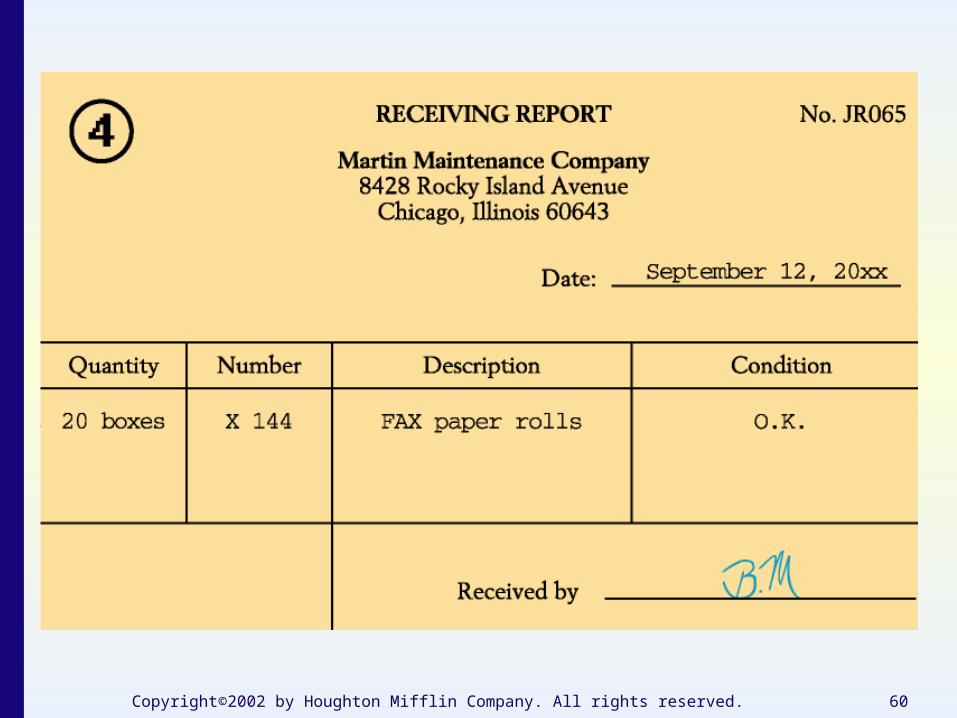

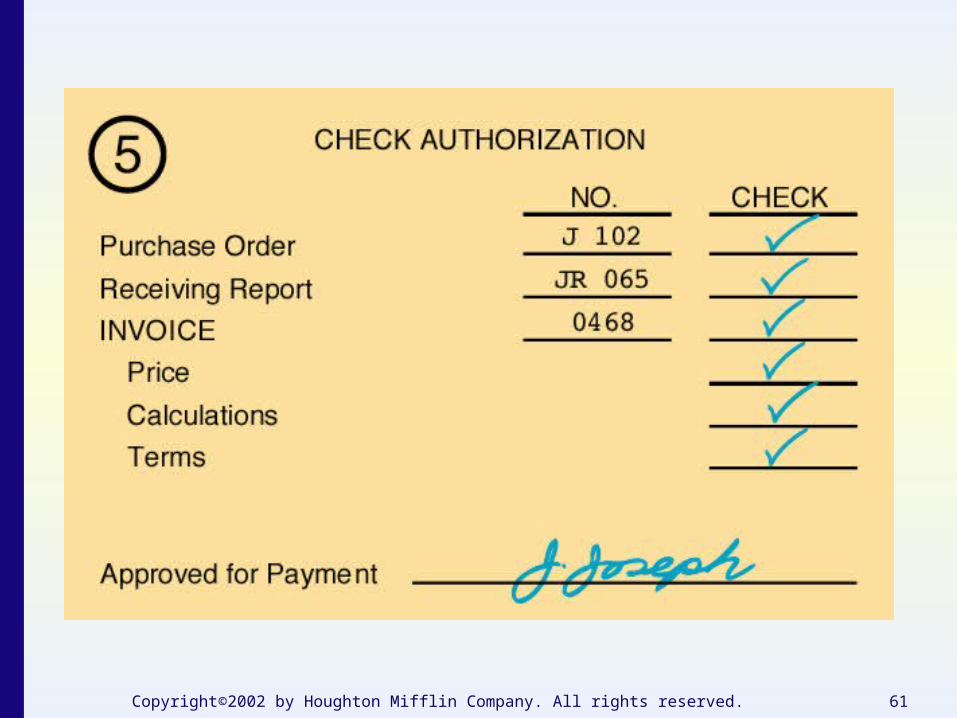

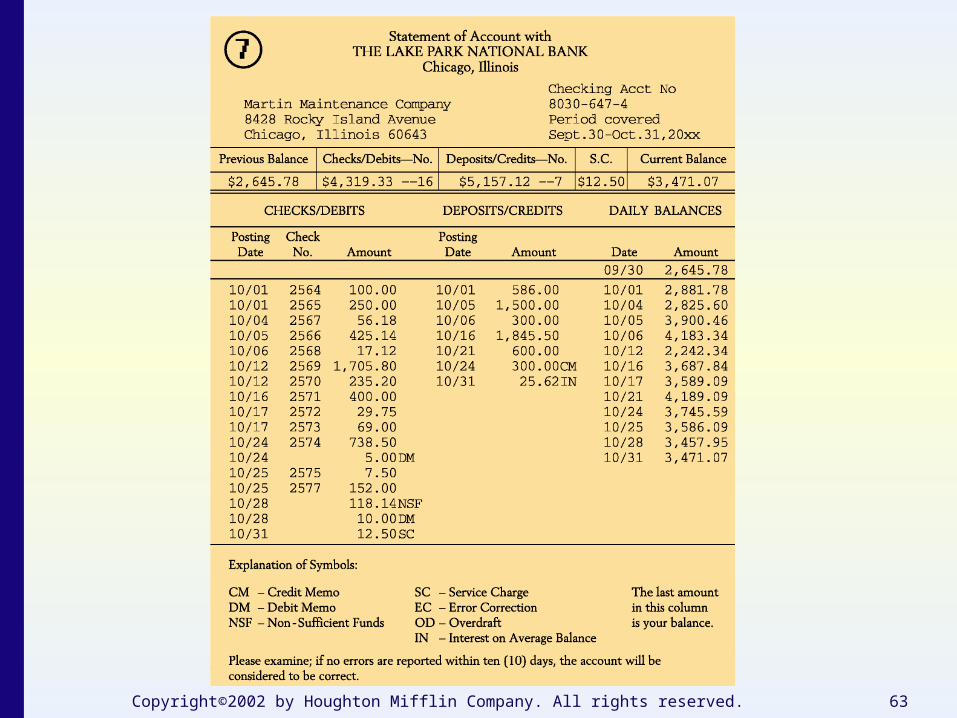

Internal Control for Purchasing and Paying forInternal Control for Purchasing and Paying forGoods and ServicesGoods and Services

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 57

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 58

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 59

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 60

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 61

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 62

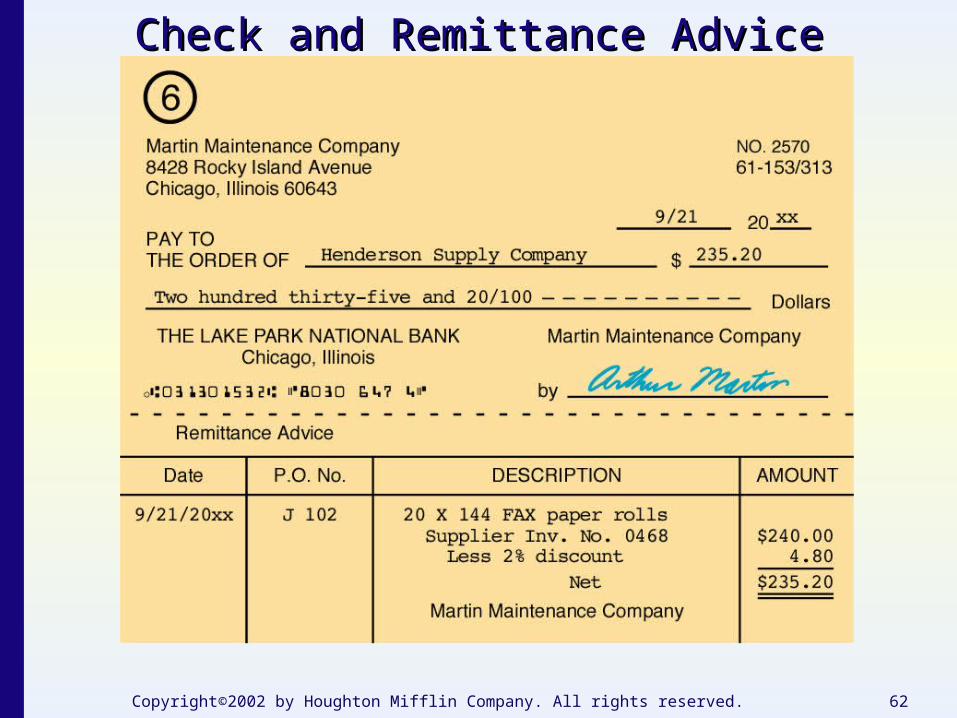

Check and Remittance AdviceCheck and Remittance Advice

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 63

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 64

DiscussionDiscussion

Q.Q. Name the documents needed for an internal control plan for purchases and cash disbursements.

A.A. Purchase requisition, purchase order, invoice, receiving report, check authorization, check with a remittance advice.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 65

Accounting for DiscountsAccounting for Discounts

SUPPLEMENTAL OBJECTIVE 8

Apply sales and purchases discounts to merchandising transactions.

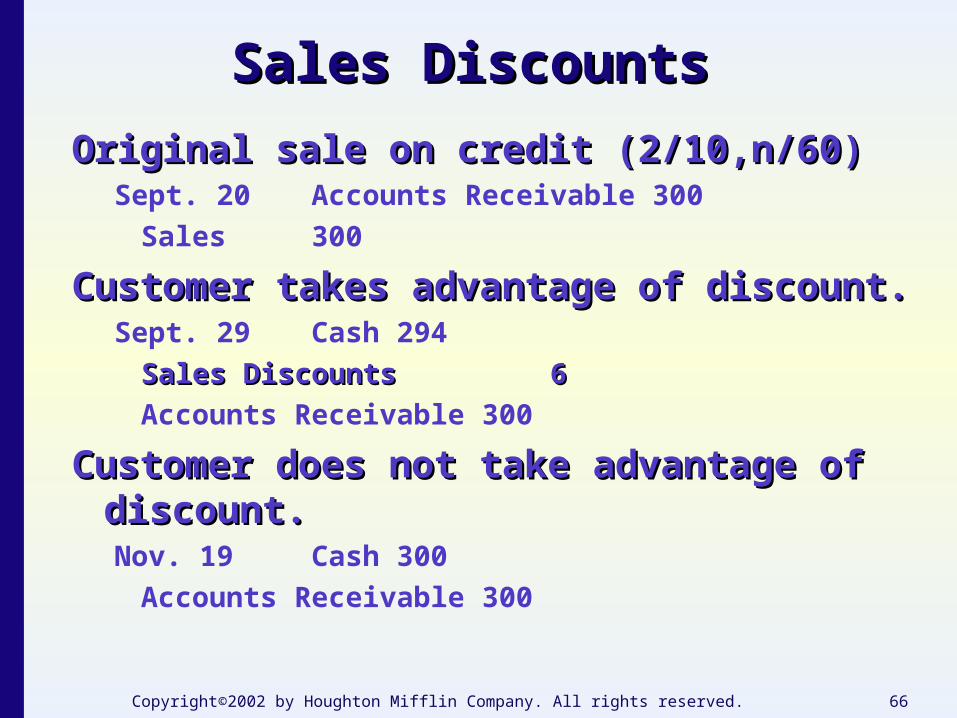

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 66

Original sale on credit (2/10,n/60)Original sale on credit (2/10,n/60)Sept. 20 Accounts Receivable 300

Sales 300

Customer takes advantage of discount.Customer takes advantage of discount.Sept. 29 Cash 294

Sales DiscountsSales Discounts 6 6

Accounts Receivable 300

Customer does not take advantage of discount.Customer does not take advantage of discount.Nov. 19 Cash 300

Accounts Receivable 300

Sales DiscountsSales Discounts

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 67

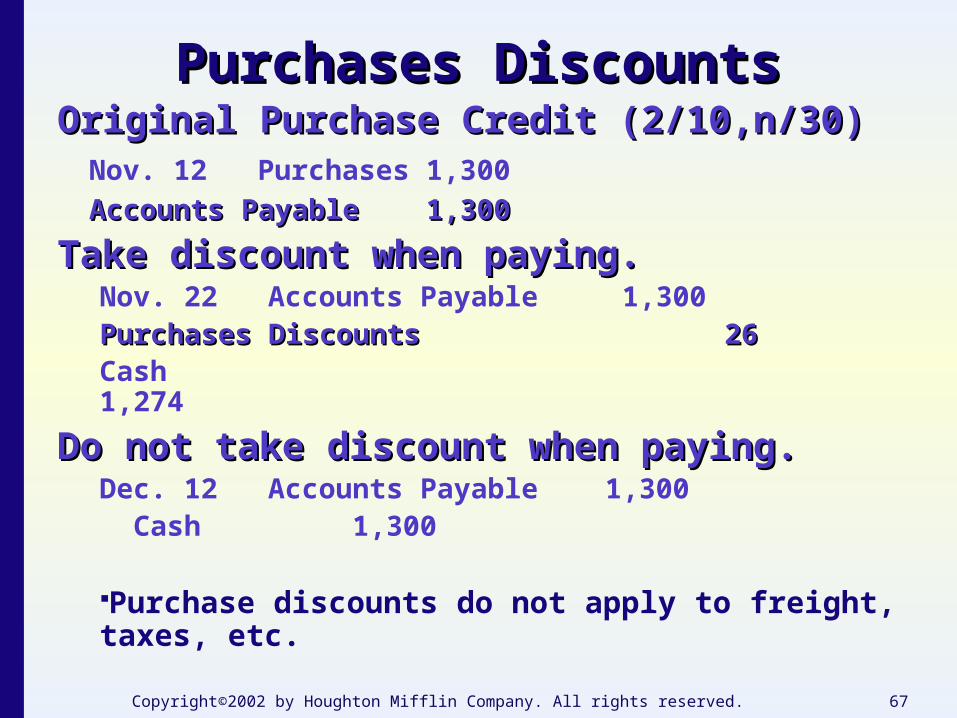

Original Purchase Credit (2/10,n/30)Original Purchase Credit (2/10,n/30)Nov. 12 Purchases 1,300

Accounts PayableAccounts Payable 1,3001,300

Take discount when paying.Take discount when paying.Nov. 22 Accounts Payable 1,300

Purchases Discounts 26Purchases Discounts 26Cash 1,274

Do not take discount when paying.Do not take discount when paying.Dec. 12 Accounts Payable 1,300

Cash 1,300

Purchase discounts do not apply to freight, taxes, etc.

Purchases DiscountsPurchases Discounts

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 68

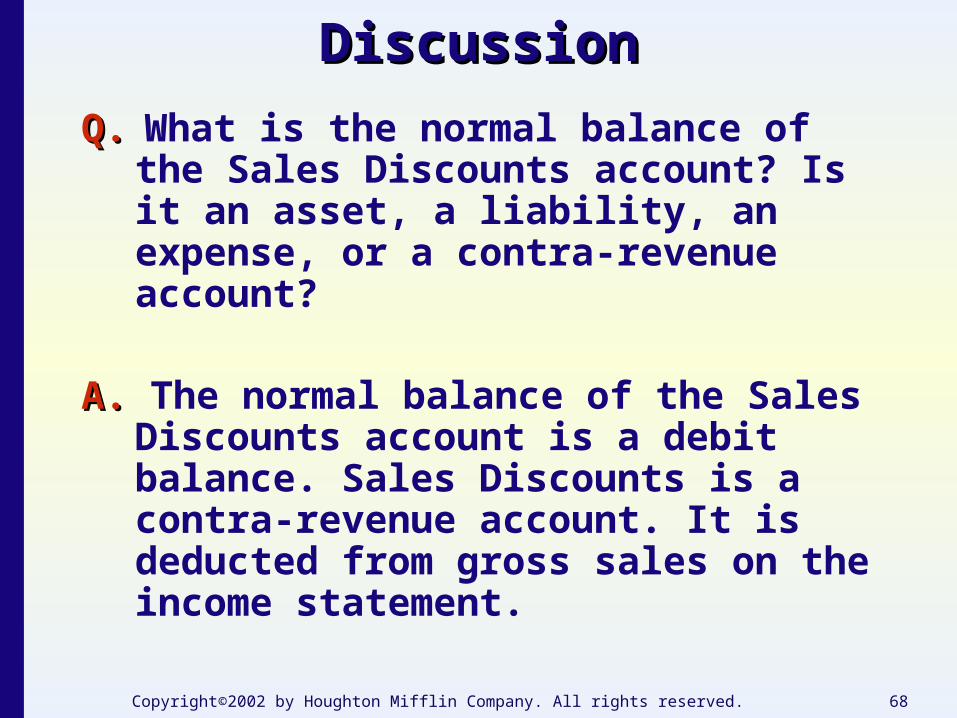

DiscussionDiscussion

Q.Q. What is the normal balance of the Sales Discounts account? Is it an asset, a liability, an expense, or a contra-revenue account?

A.A. The normal balance of the Sales Discounts account is a debit balance. Sales Discounts is a contra-revenue account. It is deducted from gross sales on the income statement.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 69

OKAY, LET’S REVIEW...OKAY, LET’S REVIEW...

1. Identify the management issues related to merchandising businesses.

2. Define and distinguish the terms of sale for merchandising transactions

3. Prepare an income statement and record merchandising transactions under the perpetual inventory system.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 70

CONTINUING OUR REVIEW...CONTINUING OUR REVIEW...

4. Prepare an income statement and record merchandising transactions under the periodic inventory system.

5. Define internal control, identify the five components of internal control, and explain seven examples of control activities.

Copyright©2002 by Houghton Mifflin Company. All rights reserved. 71

AND FINALLY...AND FINALLY...

6. Describe the inherent limitations of internal control.

7. Apply internal control activities to common merchandising transactions.

8. Apply sales and purchases discounts to merchandising transactions.