Embed Size (px)

Citation preview

Getting started in payroll in Canada

Module 1

Agenda Country Overview

Business Culture

Glossary of Abbreviations

Employer Obligations

Reporting

Employment Law

Canada Labour Code

Build up to Gross Pay

Pay Elements

National Minimum Wage

First Nation Employees

Country Overview

Country OverviewFacts about Canada

The Dominion of Canada came into being on July 1, 1867. Dominion indicated Canada was a self-governing colony of the British Empire.

On the day Canada came into being, New Brunswick, Nova Scotia, Ontario and Quebec became its first provinces.

Further provinces and territories were added over the years, with the most recent territory – Nunavut – forming in 1999.

Country Overview

Canada is the world's second largest country by area, behind Russia

Canada's total area is 9,984,670 km2 (3,855,103 mi2)

Freshwater lakes account for 8.9% of Canada's size - that's 891,163 km2 (344,080 mi2) of lakes

Canada’s total land area is 9,093,507 km2 (3,511,023 mi2)

Canada is federal country. Each of its provinces and territories has its own capital city and government

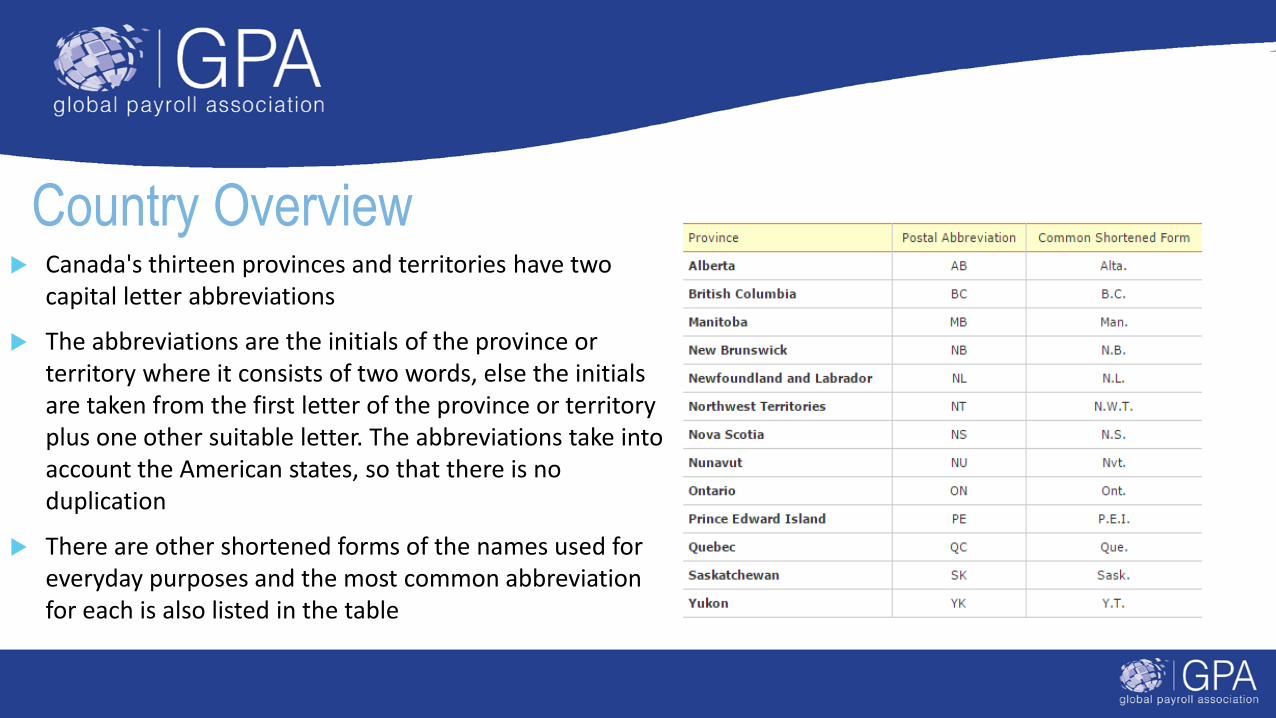

Country Overview Canada's thirteen provinces and territories have two

capital letter abbreviations

The abbreviations are the initials of the province or territory where it consists of two words, else the initials are taken from the first letter of the province or territory plus one other suitable letter. The abbreviations take into account the American states, so that there is no duplication

There are other shortened forms of the names used for everyday purposes and the most common abbreviation for each is also listed in the table

Business Culture

Business Culture Although Canada is the second largest country in the world almost 90% of the population live within

200km of the border with the US. This means that vast tracts of Canada are uninhabited wilderness and that, if you are doing business in Canada, you are never likely to be, geographically speaking, too far from the States

This close proximity is defining for Canadian business as the largest trade relationship of any two countries in the world is the one between the US and Canada

It is important to note that although close to the USA geographically, there are definitely differences in the general approach to business between the USA and Canada; Canadians are sometimes known to take exception to any assumption being made on this matter

Canada is a large, vibrant economy with a number of global companies and an extremely successful export industry

Business Culture There is no norm in terms of business structure as many organisations are opting for flatter, leaner

structures than it’s more traditional hierarchical structures

Managers are not expected to manage in an authoritarian manner but to be decisive. The management style is informal and friendly, and managers prefer to be seen as 'one of the guys' rather than as a superior figure

Managers will consult widely for decision-making, however, the final decision still remains firmly with them and quick decision-making is respected.

Failure to consult widely could lead to a feeling of dissatisfaction amongst team members who will feel that their manger is being dictatorial

Managers are is not necessarily expected to be the highly technically skilled; interpersonal and people management skills are considered of vital importance

Business Culture Meetings are relatively formal, punctuality is expected and often start with some polite small talk

Body language tends to be quite reserved with few visible shows of emotion or anger

Etiquette for meetings follows the Anglo-Saxon approach of one person speaking at a time and interruptions are generally frowned upon and considered to be rude

Meetings are democratic, with everyone being able to have their say and for opinions to be respected, regardless of their position or seniority

Aggressive or heated meetings are rare, they are usually calm and civil, and carried out with courtesy and politeness

Attendees are expected to be well prepared as decisions tend to be taken on the basis of empirical facts rather than on gut reactions. Inability to provide the relevant level of detail could be viewed as suspicious and potentially evasive behaviour

Business Culture People expect to be valued as team members based on the skills they bring to the team; the leader or

manager needs to reflect this in their approach

Teams need to have a clear idea of vision and objectives, each member needs to understand what contribution they personally will be making

People prefer to be given outline guides and general instructions rather than to be micro-managed. Micro-managing might be seen as interference or a lack of trust

Business Culture Canada is officially bilingual and this needs to be recognised in your dealings with the country

Canadian communication patterns are usually low key. Reserve, understatement, diplomacy and tact are the key attributes of communication, however Canadians are still direct and say what they mean

Canadians do not use overtly coded language. 'Yes' means 'yes' and 'no' means 'no'. They see coded language as suspicious and prefer problems to be put on the table for discussion

Like most organisations much of the intra-company communication is email based with phones used 'in an emergency'

Please bear in mind that many international organisations will have their own culture

Glossary of Terms and Abbreviations

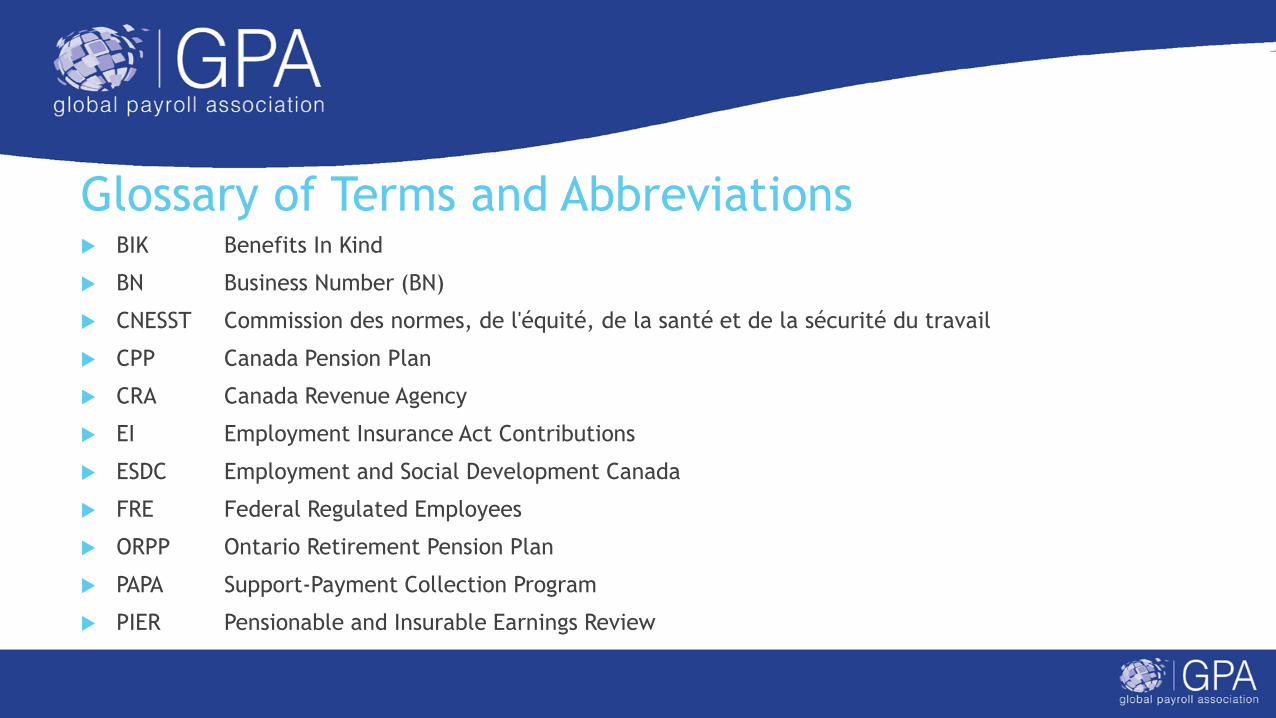

Glossary of Terms and Abbreviations BIK Benefits In Kind

BN Business Number (BN)

CNESST Commission des normes, de l'équité, de la santé et de la sécurité du travail

CPP Canada Pension Plan

CRA Canada Revenue Agency

EI Employment Insurance Act Contributions

ESDC Employment and Social Development Canada

FRE Federal Regulated Employees

ORPP Ontario Retirement Pension Plan

PAPA Support-Payment Collection Program

PIER Pensionable and Insurable Earnings Review

Glossary of Terms and Abbreviations PRPP Pooled Registered Pension Plan

QPIP Québec Parental Insurance Plan

QPP Quebec Pension Plan

RCA Retirement Compensation Arrangement

RoE Record of Employment

RPP Registered Pension Plan

RRSP Registered Retirement Savings Plan

SAT Secure Automated Transfer

SIN Social Insurance Number

TC Taxation Centres

TSO Tax Service Offices

WSDRF Workforce Skills Development & Recognition Fund

Employer Obligations

Tax Authority The Canada Revenue Agency (CRA) is responsible for administration of certain tax

programmes at federal level, and some provincial/territory taxes

The CRA may also undertake tax collection of non harmonised taxes for provinces/territories on a cost recovery basis

The CRA administers benefits and related programmes

And promotes compliance with all relevant Canadian tax legislation

Website at www.cra-arc.gc.ca

CRA Structure

The CRA is divided into 5 regions: Atlantic, Quebec, Ontario, Prairie and Pacific

Within each region there are several Tax Service Offices (TSO) for audit and collection work

There are 7 Taxation Centres (TC) used for processing and reviewing filed tax returns

Revenue QuebecAgence du Revenue Quebec

Collects income tax and consumption taxes and ensures that each person pays a fair share of the financing of public services

Administers the support-payment collection program (PAPA) in order to ensure that the support children and custodial parents are entitled to is received on a regular basis

Administers taxation-related social programs, as well as any other tax-collection and redistribution program entrusted to it by the government

Revenue QuebecAgence du Revenue Quebec

Ensures provisional administration of unclaimed property and liquidation of that property in order pay out the value to assigns (persons in whom a property right is vested), or, failing that, to the Minister of Finance

Keeps a public register of the businesses that carry on activities in Québec and administers the system governing the existence of legal persons in Québec in order to protect the public and businesses

Makes recommendations to the government concerning fiscal policy and programs

Website at www.revenuquebec.ca/en

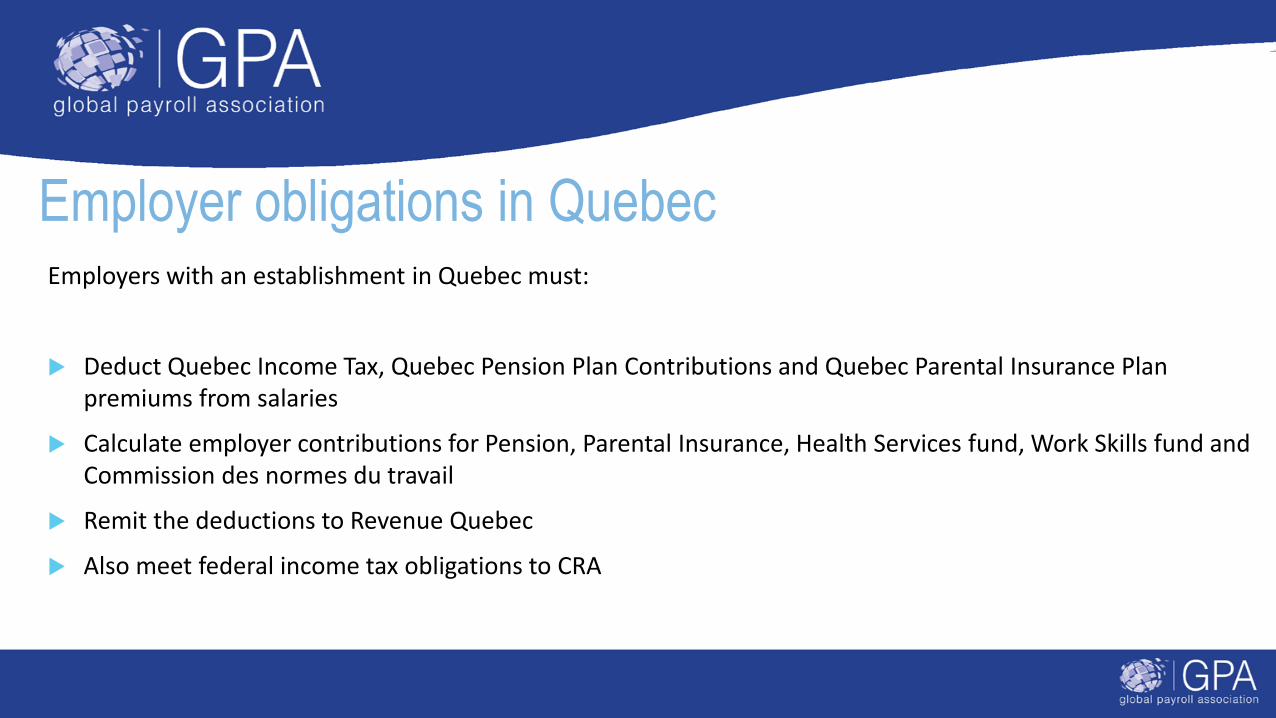

Employer obligations in QuebecEmployers with an establishment in Quebec must:

If an employers pays or plans to pay a salary, wages or remuneration to an employee or beneficiary who meets at least one of the basic conditions for making source deductions and paying contributions, they must register for source deductions and obtain an employer identification number

This is done using the Registering for Revenu Québec Files online service; file the Application for Registration (form LM-1-V)

Note: Even if the employer identification number has not been received/applied for the employer must remit source deductions and pay the employer contributions and make the remittance by the deadline

An account will be opened in the employer’s name and and a form sent to the employer to use for the following remittance

Employer obligations in QuebecEmployers with an establishment in Quebec must:

Deduct Quebec Income Tax, Quebec Pension Plan Contributions and Quebec Parental Insurance Plan premiums from salaries

Calculate employer contributions for Pension, Parental Insurance, Health Services fund, Work Skills fund and Commission des normes du travail

Remit the deductions to Revenue Quebec

Also meet federal income tax obligations to CRA

Operating Payroll

What is a Payroll Program AccountA payroll program account is an account number assigned to either an employer, a trustee or a payer

to identify themselves when dealing with the Canada Revenue Agency

This 15-character account number contains the 9-digit business number (BN)

This is a unique federal government number that identifies the business and the accounts maintained

The payroll account number consists of:

9-digit BN

2 letters for the type of account (for payroll program the letters are "RP”) and

4 numbers for the specific account reference

When to open an account

Employers have to register for a payroll program account before the first remittance, which is the 15th day of the month following the month in which they began withholding deductions from employee's pay.

Penalties are imposed of $1,000 to $25,000 for missing the deadline and there is a potential prison sentence for a term of up to 12 months

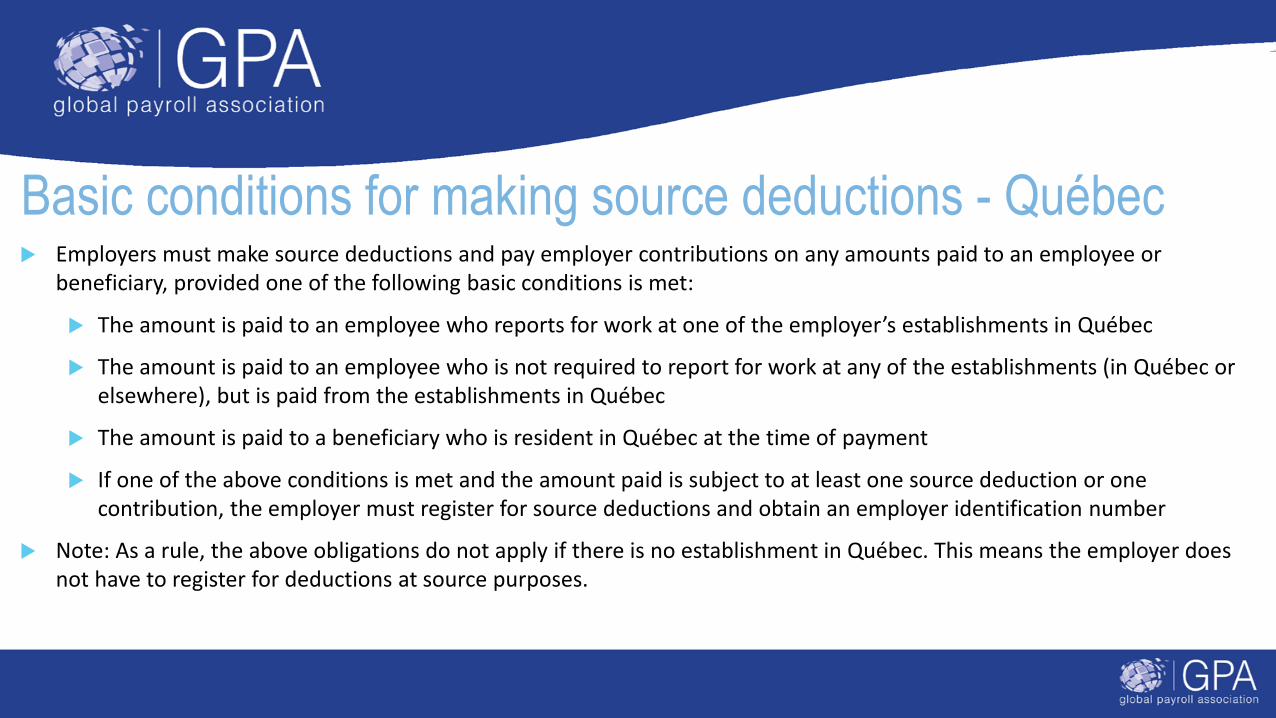

Basic conditions for making source deductions - Québec Employers must make source deductions and pay employer contributions on any amounts paid to an employee or

beneficiary, provided one of the following basic conditions is met:

The amount is paid to an employee who reports for work at one of the employer’s establishments in Québec

The amount is paid to an employee who is not required to report for work at any of the establishments (in Québec or elsewhere), but is paid from the establishments in Québec

The amount is paid to a beneficiary who is resident in Québec at the time of payment

If one of the above conditions is met and the amount paid is subject to at least one source deduction or one contribution, the employer must register for source deductions and obtain an employer identification number

Note: As a rule, the above obligations do not apply if there is no establishment in Québec. This means the employer does not have to register for deductions at source purposes.

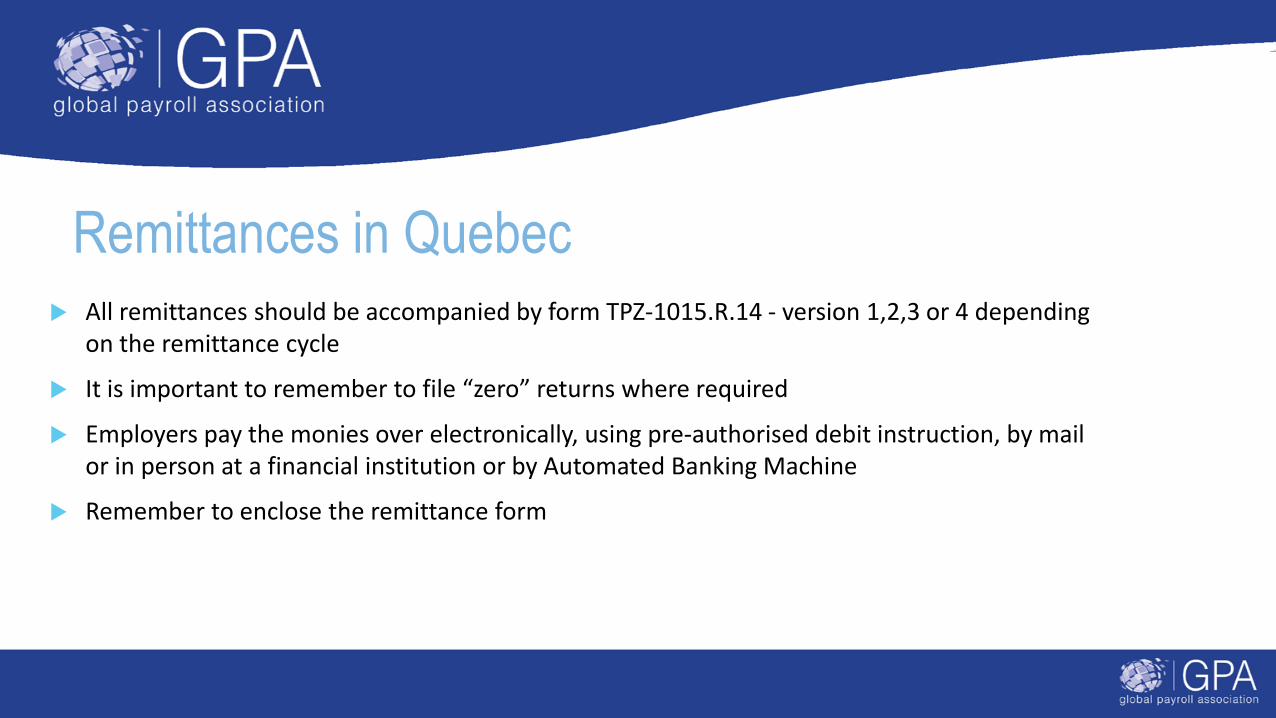

Remittances in Quebec All remittances should be accompanied by form TPZ-1015.R.14 - version 1,2,3 or 4 depending

on the remittance cycle

It is important to remember to file “zero” returns where required

Employers pay the monies over electronically, using pre-authorised debit instruction, by mail or in person at a financial institution or by Automated Banking Machine

Remember to enclose the remittance form

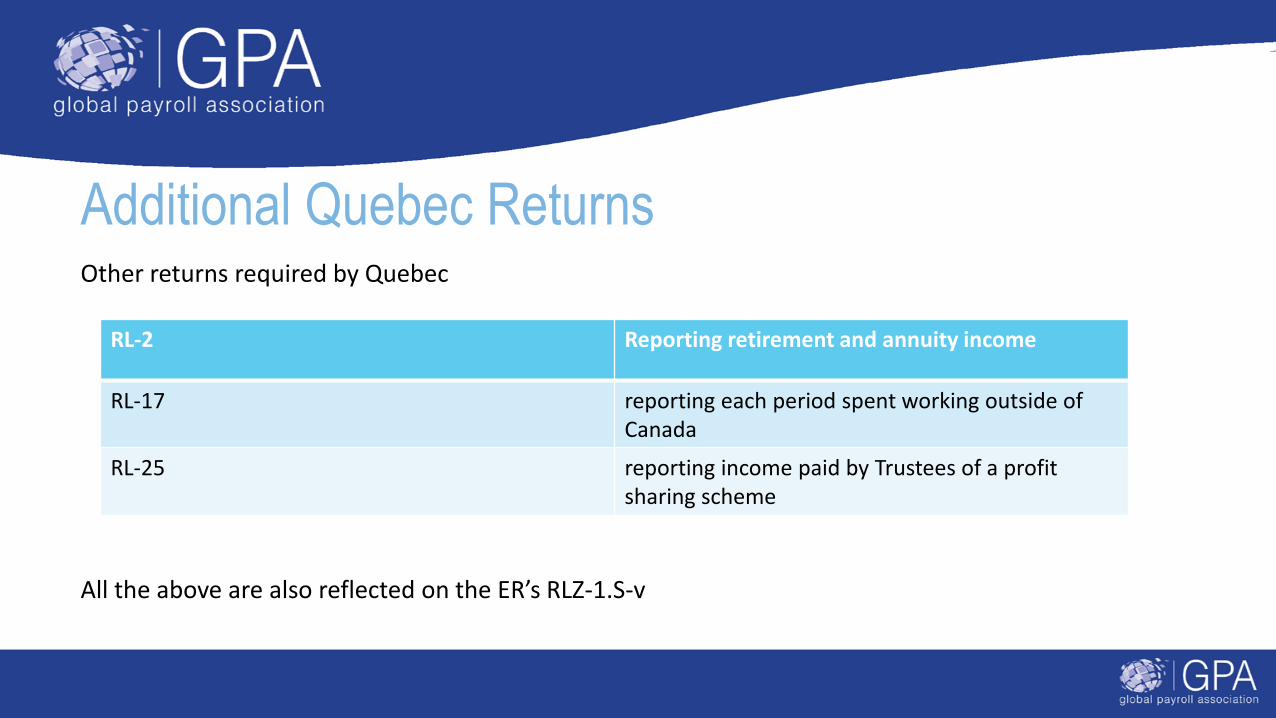

Additional Quebec ReturnsOther returns required by Quebec

All the above are also reflected on the ER’s RLZ-1.S-v

RL-2 Reporting retirement and annuity income

RL-17 reporting each period spent working outside of Canada

RL-25 reporting income paid by Trustees of a profit sharing scheme

Payroll Remittances to CRA As an employer, you have to remit the CPP contributions, the EI premiums, and income tax

deducted from your employees' income, along with your share of CPP contributions and EI premiums

Remittances are deemed to have been made on the day on which it is received by the Receiver General – not the date you sent it

These deductions, along with the remittance form, must be received on or before the remittance due dates. The due dates vary depending on the type of remitter

If the remittance due date is a Saturday, a Sunday or a public holiday, the remittance is due on the next business day.

If a business goes bankrupt or stops operating, deductions must be remitted to the tax centre within 7 days following the closure/bankruptcy of the business

Payroll Remittances to CRAWhen to pay over deductions of tax, CPP and EI

The timetable depends upon when the employee is paid, rather than the pay period

New remitters or those with average monthly remittances remit by the 15th of the month following when the deduction was taken

Small employers with average monthly remittances of $3,000 or less may pay CRA quarterly

Accelerated RemittancesThere are two different groupings for these

Threshold 1

Those whose payroll had average monthly remittances two years ago of $25,000 - $99,999.99

Remittances on remuneration paid up to and including the 15th of the month need to be received by 25th of that month

Remuneration paid from 16th onwards by the 10th of following month

Accelerated Remittances Threshold 2

An average monthly remittance of over $100,000 two years ago

Deductions must be remitted 3 working days after the end of the following periods when pay day falls:

1st to 7th

8th to 14th

15th to 21st

22nd to end of month

Paying Remittances Payments should be made via a financial institution

All payments received at least one day before they are due are deemed to have met the deadline

Payments made on the deadline but not at a financial institution are subject to a 3% penalty

Payments after the deadline are subject to a further, graduated penalty

If a remittance is due on a weekend/public holiday the date falls back rather than forward, effectively bringing the deadline forward to an earlier date

Penalties for late remittance 3% 1-3 days late

5% 4-5 days late

7% 6-7 days late

10% - 8 days plus

Penalties are applied if the value outstanding is $500 or more

A second offence in year attracts an automatic 20% penalty

5% interest will be charged in addition to the penalty

How to pay Threshold 2 remitters must pay:

electronically or

in person at a Canadian financial institution

Non Resident employers with no Canadian account

by wire transfer to the CRA account at the Bank of Nova Scotia, King Street West, Toronto

Post

a cheque or money order to CRA

Pay at a Canadian financial institution using the remittance form

Remittance FormForm PD7A should accompany the remittance

There is a different version of the form for threshold 1-2 remitters (PD7A (RB))

Forms are usually sent electronically to CRA

Form includes gross payroll value rounded to the nearest dollar

It must state:

the number of employees

the end date of the remitting period

Total tax, CPP and EI being remitted

Nil RemittanceIf there is a nil remittance then to avoid a penalty being levied advise the CRA

PD7A can be:

Mailed to the CRA

Filed electronically showing “nil”

Advised via telephone on the TeleReply service offered by CRA

Remittances in Quebec

Remittances of Quebec Income Tax, QPP and QPIP

Schedules can be found at: http://www.revenuquebec.ca/en/entreprises/ras/payerras/cot_empl/default.aspx

Revenue Quebec may authorise employers to remit the source deductions, employer Québec Pension Plan (QPP) contributions, employer Québec parental insurance plan (QPIP) premiums and the employer contribution to the health services fund for 2017:

Annually, if the total of the source deductions and employer contributions for 2016 did not exceed $2,400

Quarterly, if the average monthly remittance for 2015 or 2016 did not exceed $3,000 and the employer has fulfilled all fiscal obligations over the last 12 months

Remittances in Quebec Where the conditions are not meet remittances must be made:

Monthly, if the average monthly remittance for 2015 was less than $25,000

Twice-monthly, if the average monthly remittance for 2015 was at least $25,000 but less than $100,000

Weekly, if the average monthly remittance for 2015 was $100,000 or more

Remittances should be accompanied by form TPZ-1015.R.14- version 1,2,3 or 4 depending on the remittance cycle

File “Zero” returns where required

Pay electronically, by pre-authorised debit instruction, by mail or in person at a financial institution or by Automated Banking Machine and be sure to enclose the remittance form

Employment Law

Working Time Standard hours of work are 40 hours per week and 8 hours per day.

Employees who work more than the standard hours they must be paid at the overtime wage rate.

Employees are also entitled to an unpaid 30 minute break after 5 hours of consecutive work.

Working TimeThere are exceptions to standard hours of work, which include:

Areas of the construction industry

The landscaping business

Companies with collective (union) agreements that specify different hours

Companies with an Averaging Permit from Employment Standards

Employees who have an Individual Flextime Agreement with their employer

Election officials, enumerators and any other temporary person appointed under The Elections Act.

Working Time QuebecThe Act respecting labour standards contains provisions concerning an employee’s presence at work that protect the majority of Québec workers, whether they are full or part time.

An employee is deemed to be at work and must be paid:

When he is at his employer’s disposal on the worksite and he is required to wait for work to be assigned

During breaks granted by the employer

During the time of any travel required by the employer

During any trial period or training required by the employer.

The employer must reimburse the employee for the reasonable expenses that the employee must pay when, at the employer’s request, he must travel or take training.

Working Time Quebec An employer is under no obligation to offer coffee breaks, but when a coffee break is

granted, it must be paid and included in the calculation of the hours worked.

After a period of work of 5 consecutive hours, the employee is entitled to a 30-minute period, without pay, for his meal. He must be paid for this period if he is unable to leave his work station.

An employee who reports to work at the express request of his employer or in the normal course of his employment and who does not work or works fewer than 3 consecutive hours is entitled to an indemnity equal to 3 hours of pay at his regular wage.

Each week, an employee is entitled to a rest period of at least 32 consecutive hours. In the case of a farm worker, his day of rest may be postponed to the following week if he is in agreement.

Canada Labour Code

Canada Labour CodeThe Labour Code covers 12,000 businesses and 820,000 employees in:

Banking

Marine shipping, ferry and port services

Air transportation (including airports, aerodromes and airlines)

Railway and road transportation that involves crossing provincial or international borders

Canals, pipelines, tunnels and bridges (crossing provincial borders)

Telephone, telegraph and cable systems

Radio and television broadcasting

Grain elevators, feed and seed mills

Canada Labour Code Uranium mining and processing

Businesses dealing with the protection of fisheries as a natural resource

Many First Nation activities

Most federal Crown corporations

Private businesses necessary to the operation of a federal act

The Labour Code can be viewed at http://laws-lois.justice.gc.ca/eng/acts/L-2/index.html

Those in other industries have employment standards regulated by Provincial/Territorial Ministry of Labour

Employment Types and ContractsIn Canada an Employment Contract is a contract which can be either written or verbal. The contract sets out the terms and conditions for employment between an employee and an employer. Typically the contract will include the following items:

the job role being offered and accepted

the term of employment

details of holiday, sickness, and grievance policies

the compensation that will be provided to the employee

the responsibilities of the employee and employer

Employment Types and ContractsCanada also uses Service Agreements to engage resource.

Service Agreements are used to hire service providers or independent contractors, not employees. A Service Agreement is limited to a specific project or time period. Employment Contracts are used to hire employees.

Employment Types and Contracts Quebec Individual contracts of employment are generally governed by the Civil Code of Québec.

A contract of employment can be oral or in writing, it is defined as a contract by which the employee undertakes to do work for remuneration, according to the instructions and under the direction or control of the employer.

It is to be distinguished from a contract of services, under which the contractor or provider of services (often a consultant) is free to choose the means of performing the contract and under which no relationship of subordination exists between the contractor or the provider of services and the client.

Service Agreements are used to hire service providers or independent contractors, not employees. A Service Agreement is limited to a specific project or time period.

Employment Types and Contracts QuebecAn employer cannot give an employee who is subject to the Act respecting labour standards conditions of employment that are less advantageous than those of other employees doing the same work in the same establishment due to his hiring date. These conditions of employment notably deal with:

wages

length of work

paid statutory holidays

annual vacation

rest periods

absences and leaves for family or parental reasons

notice of termination of employment

StartersWhen hiring an employee, the employer has to obtain:

The employee's social insurance number (SIN); and

A completed Form TD1, Personal Tax Credits Return (this is completed by the employee)

For Quebec a Federal TD1 is required, but for the Provincial deductions its form TP-1015.3-V.

If the employer get the SIN or Form TD1, they are still responsible for calculating and withholding payroll deductions from day one

Social Insurance NumbersSocial Insurance Numbers are a key piece of employee identification

Employee will provide a SIN card or letter

Employers must inform Service Canada within 6 days of commencement of employment if the employee fails to present a SIN and must commence deductions whether they have received one or not

The SIN is a 9 digit number

Numbers commencing with a “9” have been issued to non Canadians or permanent residents of Canada. They should be checked in conjunction with the relevant immigration document as they expire at the end of the individual’s legitimate time in Canada

Personal Tax Credits ReturnA TD1 Must be submitted for individuals who:

Have a new employer or payer;

Want to change amounts from those previously claimed;

Want to claim the deduction for living in a prescribed zone; or

Want to voluntarily increase the amount of tax deducted at source (because they have some income untaxed at source)

The form should be submitted to the employer no later than 7 days of the relevant change occurring

There is no need to re-submit a TD1 each year where employment is on-going and no changes occur

Forms are retained by the employer and not sent to the CRA

Canadian Tax ReturnsThe Canadian tax year runs for a calendar year, 1st January to 31st December

All Canadians must submit an annual tax return

This is completed for individuals on form T1

It can be done by paper or on-line using Netfile – specific software available through tax professionals or purchased from software providers – the web access code can be obtained: https://apps.cra-arc.gc.ca/ebci/leb0/wacretrieve/pub/entry-e.do

Employers must file the returns by the last day in February for the previous tax year i.e. by 28th

February 2017 for the year 2016.

Where an employer has more than employees this must be done electronically

Quebec – Form TP-1015.3-VThis form is to be submitted by the employee to the employer on the first day of employment

It is similar to the TD1

It can be used to claim the various allowances – the headings are similar (but not identical) to TD1

This form can be used to voluntarily pay more tax as with the TD1

It can be used to claim exemption from withholding if income is below the prescribed threshold

The form can be used to claim exemption from the Quebec health contribution in certain circumstances

LeaversWhen someone leaves the employers must:

Prepare a T4 summarising earnings and deductions for the Year To Date, this is given to the employee

Send the T4 to CRA electronically with the others for the business at year end

Complete a RoE and give it to the employee within 5 days of leaving

In Quebec If one of your employees leaves his or her employment before the end of the year, you can prepare the RL-1 slip at that time and give the employee copy 2. If the version of the RL-1 slip for the year in question is not yet available, use the previous year's version (simply cross out the year that appears on the slip and enter the year in question).File copy 1 of that RL-1 slip at the same time as the RL-1 slips for your other employees and your RL-1 summary for the year in question.

Work PermitIf you send an employee to work in Canada

You usually need a work permit to work in Canada.

However in some cases, employees can work without a permit.

Each instance should be individually looked at to see if a visa is required

Rules for Quebec require the employer to obtain the authorizations for the employee to work temporarily in Québec

Under the Quebec temporary Foreign Worker Program, positions offered are classified according to the median hourly wage in Québec. To find out about the procedure to follow, select the job category that corresponds to your situation.

Build up to Gross Pay

Pay Elements The following chart will help you determine whether or not to deduct Canada Pension

Plan (CPP) contributions, employment insurance (EI) premiums, and income tax on the

special payments you make to your employees or recipients.

Pay ElementsPayments

CPP

contributionsEI premiums

Tax

deductions

Advances Yes Yes Yes

Benefits under the Employment Insurance Act No No Yes

Bonuses and retroactive pay increases or irregular amounts Yes Yes Yes

Casual employment if it is for a purpose other than your usual

trade or business (even if there is a contract of employment)No No No

Compassionate care benefits – amounts paid to cover the waiting

period or to increase the benefitYes Yes/No Yes

Corporate employee who controls more than 40% of the

corporation's voting shares receiving salary, wages or other

remuneration

Yes No Yes

Directors' fees paid to residents of Canada or non-residents – Fee

onlyYes No Yes

Directors' fees paid to residents of Canada or non-residents – Fee

in addition to salaryYes/No Yes/No Yes

Pay ElementsEmployees profit sharing plan (EPSP) No No No

Employment in Canada by a foreign government or an

international organizationYes/No Yes/No Yes

Employment in Canada of a non-resident person if the

unemployment insurance laws of any foreign country require

someone to pay premiums for that employment

Yes/No No Yes

Employment in Canada under an exchange program if the

employer paying the remuneration is not resident in CanadaYes/No No Yes

Employment of your child or a person that you maintain if no

cash remuneration is paidNo No No

Employment that is an exchange of work or service (even if

there is a contract of service)Yes/No No Yes/No

Employment under the "Self-employment assistance" or "Job

creation partnerships" benefit program established under

section 59 of the Employment Insurance Act, or under a similar

benefit program that a provincial government or other

organization provides and is part of an agreement under

section 63 of the Employment Insurance Act.

Yes/No No Yes/No

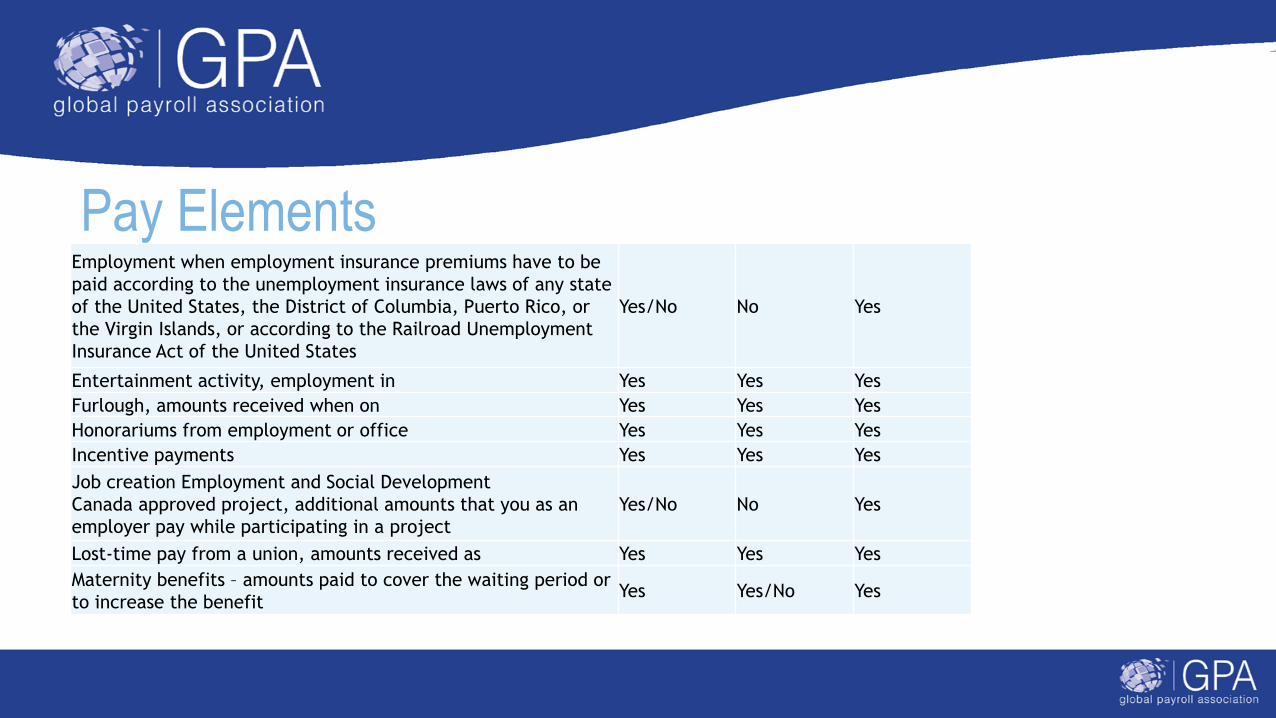

Pay ElementsEmployment when employment insurance premiums have to be

paid according to the unemployment insurance laws of any state

of the United States, the District of Columbia, Puerto Rico, or

the Virgin Islands, or according to the Railroad Unemployment

Insurance Act of the United States

Yes/No No Yes

Entertainment activity, employment in Yes Yes Yes

Furlough, amounts received when on Yes Yes Yes

Honorariums from employment or office Yes Yes Yes

Incentive payments Yes Yes Yes

Job creation Employment and Social Development

Canada approved project, additional amounts that you as an

employer pay while participating in a project

Yes/No No Yes

Lost-time pay from a union, amounts received as Yes Yes Yes

Maternity benefits – amounts paid to cover the waiting period or

to increase the benefitYes Yes/No Yes

Pay ElementsOvertime pay, including banked overtime pay Yes Yes Yes

Parental care benefits – amounts paid to cover the waiting

period or to increase the benefitYes Yes/No Yes

Payments under Part 2 of the Canadian Forces Members and

Veterans Re-establishment and Compensation Act – amounts

received on account of an earnings loss benefit, supplementary

retirement benefit or permanent impairment allowance payable

to the taxpayer

No No Yes

Qualifying retroactive lump-sum payments Yes Yes Yes

Retirement compensation arrangements (RCA) No No Yes

Retiring allowances (also called severance pay) No No Yes

Sabbatical, remuneration received while on Yes Yes Yes

Salary Yes Yes Yes

Salary deferral – non-prescribed plans or arrangements – on

amounts earnedYes Yes Yes

Pay ElementsSalary deferral – prescribed plans or arrangements – on amounts

receivedYes/No Yes/No Yes

Sick leave, amounts received while on sick leave, sick leave

credits, payments forYes Yes Yes

Spouse or common-law partner, employment of, if you cannot

deduct the remuneration paid as an expense under the Income

Tax Act

No Yes/No Yes

Teacher on exchange from a foreign country, employment of No Yes/No Yes/No

Tips and gratuities (controlled by employer) Yes Yes Yes

Tips and gratuities (direct tips or gratuities – not controlled by

the employer)No No No

Vacation pay and public holidays, and lump-sum vacation

paymentYes Yes Yes

Vow of poverty – employment of a member of a religious order

who has taken a vow of poverty. This applies whether the

remuneration is paid directly to the order or the member pays it

to the order.

No No Yes/No

Pay ElementsWages Yes Yes Yes

Wages in lieu of termination notice Yes Yes Yes

Wage-loss replacement plans – Paid by the employer Yes Yes Yes

Wage-loss replacement plans – Paid by third party/trustee and

the employer:

-funds any part of the plan; and

-exercises a degree of control over the plan; and

-directly or indirectly determines the eligibility for benefits

Yes Yes Yes

Workers' compensation claims – Employee's salary paid before or

after a workers' compensation board claim is decidedYes Yes Yes

Workers' compensation claims – Advances or loans equal to the

workers' compensation benefits awardedNo No No

Workers' compensation claims – Amount paid in addition to an

advance or loan before the claim is acceptedYes Yes Yes

Pay ElementsWorkers' compensation claims – Top-up amounts paid after the

claim is acceptedYes No Yes

Workers' compensation claims – Top-up amounts paid as sick

leave after the claim is acceptedYes No Yes

Pay Elements - Quebec Income is defined as consisting of amounts such as:

salaries and wages, remuneration, commission, fees, interest, dividends, annuities

As a rule, income is derived from:

Employment, a business, an office, property

However, an amount received in the form of capital does not constitute income. For example, if you make a one-year term deposit of $1,000 (capital) at a bank, at 5% interest, the bank will remit $1,050 ($1,000 in capital + $50 in interest) to you when the investment matures. Only the $50 in interest is considered income. Consequently, you will receive an RL slip from the bank indicating $50 in interest income.

Payrolling of Benefits All emoluments paid under the contract of employment are included for gross pay

purposes this includes all Benefits In Kind (BIK)

National Minimum Wage Canada’s Minimum Wage, the minimum hourly pay rate employers can pay their workers,

varies across the ten provinces and three territories

Each province and territory in Canada has a distinct set of minimum wage laws specifying the minimum wage, exemptions to the minimum wage, and other labour-law issues

There is no national legislation regulating the minimum wage, and all power rests with the provinces and territories

More information available at http://www.minimum-wage.ca/

National Minimum Wage 2017 Canada

National Minimum Wage 2017 Quebec

The majority of workers are entitled to the minimum wage rates, which are set by the Government of Québec

First Nation Employees

First Nations Employees

Guidance still refers to First Nations employees as Indians due to the term having legal meaning under the

Indian Act in Canada

They are not people who originated from the Indian sub-continent

In certain circumstances Indians are exempt from tax and CPP deductions

Form TD1-IN has been designed to assist employers in determining whether or not a First Nations employee is exempt from tax and/or CPP

End of Session

![JD Edwards EnterpriseOne Applications Canadian Payroll ... · [1]JD Edwards EnterpriseOne Applications Canadian Payroll Implementation Guide Release 9.1 E15127-05 July 2019](https://img.pdfslide.us/doc/110x75/5f7a45016ccd8f3ab16c47d7/jd-edwards-enterpriseone-applications-canadian-payroll-1jd-edwards-enterpriseone.jpg)