Embed Size (px)

Citation preview

• TheGamblingDataCoreEstimate:Using the German revenues of online market leader Bwin.Party Digital Entertainment, and having confirmed with sources a rough estimate of its current market share, GamblingData estimates the German grey market to be currently worth between €760m and €960m in annual gaming revenues.

• TheInterstateGamblingTreaty:The Interstate Gambling Treaty introduced a blanket ban on online gambling on January 1, 2008, but will expire at the end of 2011. The new draft treaty, agreed on by 15 of Germany’s 16 federal states, proposes to regulate online sports betting with 20 licences and a 5 percent turnover tax as well as maintaining a ban on online poker and casino.

• Schleswig-Holstein:Meanwhile, Schleswig-Holstein is

pushing forward its own bill to regulate online sports betting, poker and casino games with a 20 percent tax on gross profits. Unless a compromise is reached between Schleswig-Holstein and the remaining 15 federal states the alternative legislation is due to be enacted on January 1, 2012, with licences to be issued from March 1, 2012.

• TheGreyMarket:Although reduced significantly from the

orginally proposed 16.7 percent turnover tax, analysts suggest the 5 percent rate remains commercially unattractive for online operators. We estimate that, under this system, licensed online sportsbooks would operate with a gross win margin of around 15 percent, putting them at a competitive disadvantage to offshore operators with margins of around 7.5 percent.

The Ifo Institute for Economic Research estimates that online gaming generated 8.9 percent (€850m) of total gaming revenues of €9.57bn in 2009, up from 3.4 percent (€300m) in 2005. Analyst consensus dictates that the German online market is currently split 50:30:20 between sports betting, poker and casino.

• TheLand-basedSituation:According to the German Centre

for Addiction Issues, the regulated land-based gaming sector generated turnover of €24bn, down 14.0 percent on the €27.9bn recorded in 2007, prior to the imposition of the Interstate Treaty.

Suite 704, 91 Waterloo Road,London, SE1 8RTTel: +44 207 921 [email protected]

Scott Longley+44(0)207 921 [email protected]

GermanGamblingMarketReportDecember2011

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

1

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

2

Contents

3

4

5

7

9

11

11

11

11

15

18

19

WhereWeAre

2012 Interstate Gambling Treaty

StateLotterySector

CasinoSector

AWPMachineSector

OnlineSector

GamblingData Core Estimate

Online Product Split

The Tax Issue

Analyst View: Online Market Potential

AboutGamblingData

Disclaimer

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

3

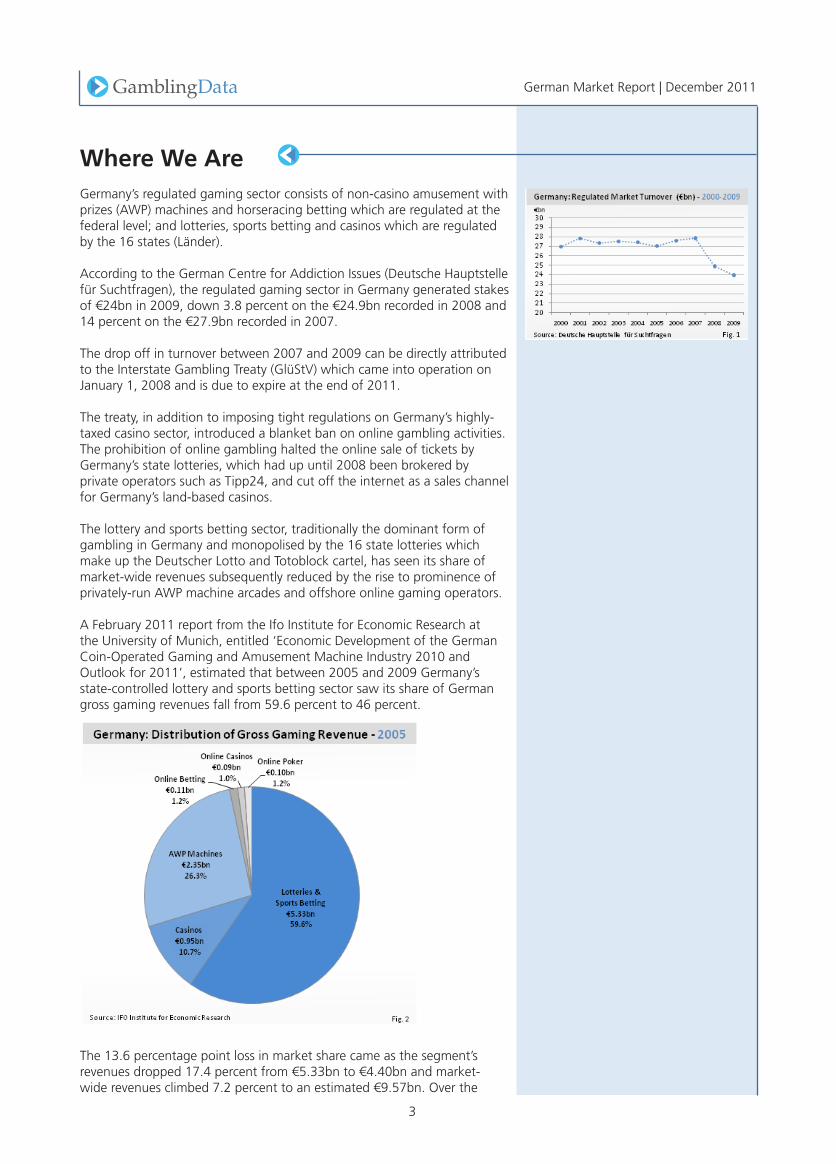

WhereWeAreGermany’s regulated gaming sector consists of non-casino amusement with prizes (AWP) machines and horseracing betting which are regulated at the federal level; and lotteries, sports betting and casinos which are regulated by the 16 states (Länder).

According to the German Centre for Addiction Issues (Deutsche Hauptstelle für Suchtfragen), the regulated gaming sector in Germany generated stakes of €24bn in 2009, down 3.8 percent on the €24.9bn recorded in 2008 and 14 percent on the €27.9bn recorded in 2007.

The drop off in turnover between 2007 and 2009 can be directly attributed to the Interstate Gambling Treaty (GlüStV) which came into operation on January 1, 2008 and is due to expire at the end of 2011.

The treaty, in addition to imposing tight regulations on Germany’s highly-taxed casino sector, introduced a blanket ban on online gambling activities. The prohibition of online gambling halted the online sale of tickets by Germany’s state lotteries, which had up until 2008 been brokered by private operators such as Tipp24, and cut off the internet as a sales channel for Germany’s land-based casinos.

The lottery and sports betting sector, traditionally the dominant form of gambling in Germany and monopolised by the 16 state lotteries which make up the Deutscher Lotto and Totoblock cartel, has seen its share of market-wide revenues subsequently reduced by the rise to prominence of privately-run AWP machine arcades and offshore online gaming operators.

A February 2011 report from the Ifo Institute for Economic Research at the University of Munich, entitled ‘Economic Development of the German Coin-Operated Gaming and Amusement Machine Industry 2010 and Outlook for 2011’, estimated that between 2005 and 2009 Germany’s state-controlled lottery and sports betting sector saw its share of German gross gaming revenues fall from 59.6 percent to 46 percent.

The 13.6 percentage point loss in market share came as the segment’s revenues dropped 17.4 percent from €5.33bn to €4.40bn and market-wide revenues climbed 7.2 percent to an estimated €9.57bn. Over the

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

4

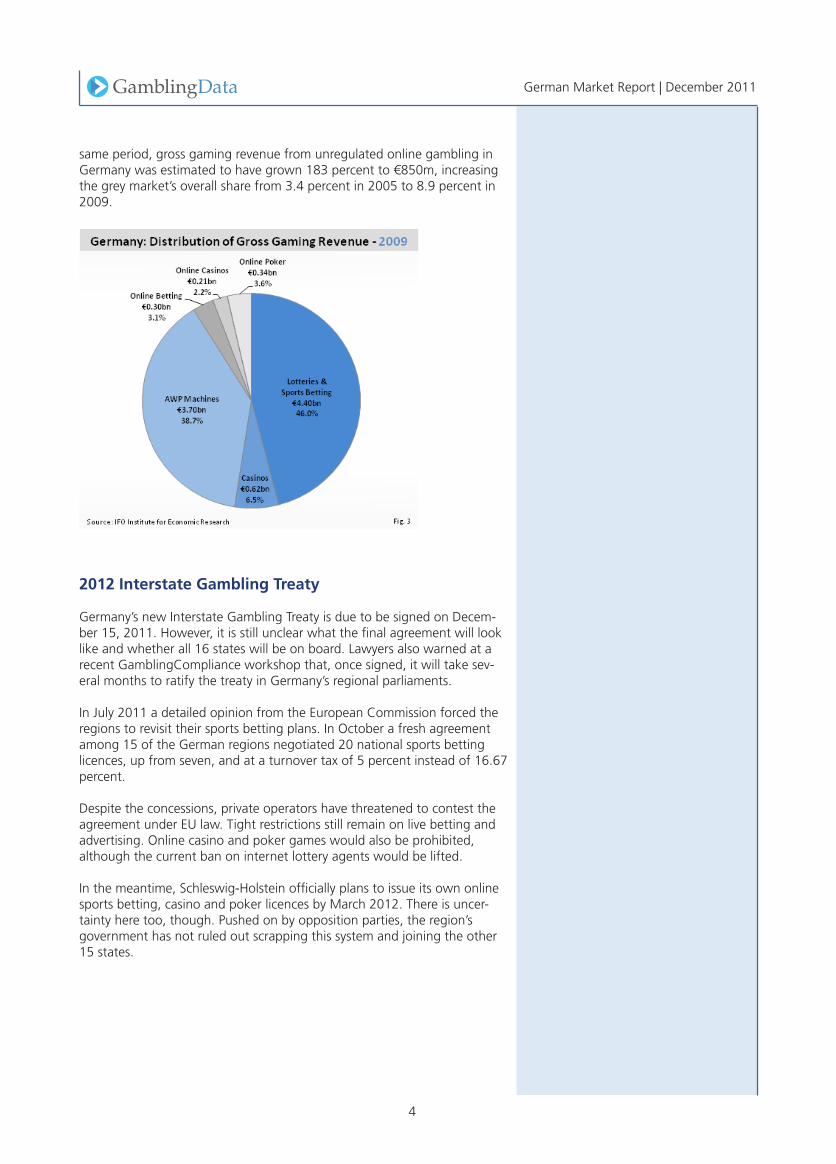

same period, gross gaming revenue from unregulated online gambling in Germany was estimated to have grown 183 percent to €850m, increasing the grey market’s overall share from 3.4 percent in 2005 to 8.9 percent in 2009.

2012InterstateGamblingTreaty

Germany’s new Interstate Gambling Treaty is due to be signed on Decem-ber 15, 2011. However, it is still unclear what the final agreement will look like and whether all 16 states will be on board. Lawyers also warned at a recent GamblingCompliance workshop that, once signed, it will take sev-eral months to ratify the treaty in Germany’s regional parliaments.

In July 2011 a detailed opinion from the European Commission forced the regions to revisit their sports betting plans. In October a fresh agreement among 15 of the German regions negotiated 20 national sports betting licences, up from seven, and at a turnover tax of 5 percent instead of 16.67 percent.

Despite the concessions, private operators have threatened to contest the agreement under EU law. Tight restrictions still remain on live betting and advertising. Online casino and poker games would also be prohibited, although the current ban on internet lottery agents would be lifted.

In the meantime, Schleswig-Holstein officially plans to issue its own online sports betting, casino and poker licences by March 2012. There is uncer-tainty here too, though. Pushed on by opposition parties, the region’s government has not ruled out scrapping this system and joining the other 15 states.

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

5

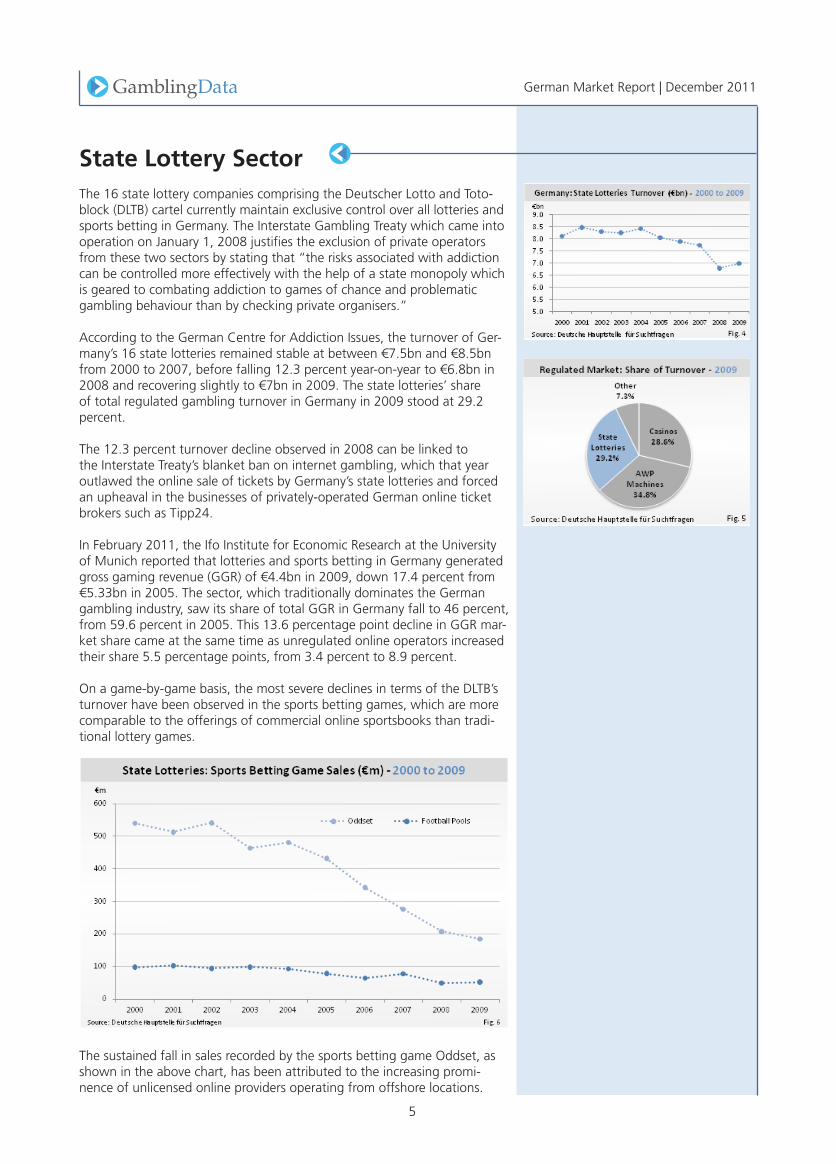

StateLotterySectorThe 16 state lottery companies comprising the Deutscher Lotto and Toto-block (DLTB) cartel currently maintain exclusive control over all lotteries and sports betting in Germany. The Interstate Gambling Treaty which came into operation on January 1, 2008 justifies the exclusion of private operators from these two sectors by stating that “the risks associated with addiction can be controlled more effectively with the help of a state monopoly which is geared to combating addiction to games of chance and problematic gambling behaviour than by checking private organisers.”

According to the German Centre for Addiction Issues, the turnover of Ger-many’s 16 state lotteries remained stable at between €7.5bn and €8.5bn from 2000 to 2007, before falling 12.3 percent year-on-year to €6.8bn in 2008 and recovering slightly to €7bn in 2009. The state lotteries’ share of total regulated gambling turnover in Germany in 2009 stood at 29.2 percent.

The 12.3 percent turnover decline observed in 2008 can be linked to the Interstate Treaty’s blanket ban on internet gambling, which that year outlawed the online sale of tickets by Germany’s state lotteries and forced an upheaval in the businesses of privately-operated German online ticket brokers such as Tipp24.

In February 2011, the Ifo Institute for Economic Research at the University of Munich reported that lotteries and sports betting in Germany generated gross gaming revenue (GGR) of €4.4bn in 2009, down 17.4 percent from €5.33bn in 2005. The sector, which traditionally dominates the German gambling industry, saw its share of total GGR in Germany fall to 46 percent, from 59.6 percent in 2005. This 13.6 percentage point decline in GGR mar-ket share came at the same time as unregulated online operators increased their share 5.5 percentage points, from 3.4 percent to 8.9 percent.

On a game-by-game basis, the most severe declines in terms of the DLTB’s turnover have been observed in the sports betting games, which are more comparable to the offerings of commercial online sportsbooks than tradi-tional lottery games.

The sustained fall in sales recorded by the sports betting game Oddset, as shown in the above chart, has been attributed to the increasing promi-nence of unlicensed online providers operating from offshore locations.

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

6

Oddset sales turnover fell from €481.5m in 2004 to €184.5m in 2009, with a compund annual growth rate (CAGR) of -17.5 percent representing a far more intense decline than the -2.96 percent CAGR recorded by the DLTB’s non-sports betting games. Sales in the football pools (Toto) game fell from €93.2m in 2004 to €52.3m in 2009, a CAGR of -10.9 percent.

In its February 2011 report the Ifo Institute estimated that Oddset’s sales turnover of €184.5m in 2009 represented just 2 to 3 percent of the total sports betting market in Germany, with the market share of unlicensed operators well above 95 percent.

The Ifo Institute wrote: “The provisions of the Interstate Treaty entered into force on January 1, 2008 resulted in a decline of state and state-licensed gambling and at the same time created free room for unregulated gam-bling.

“Unregulated gambling, especially cross-border offers from the internet gained importance in Germany over the last few years, affecting the full state and state-licensed product range… While foreign operators conquer the German gambling market, the states signing the Interstate Treaty on gambling have agreed on terminating their activity on the Internet. In recent years state-run betting operators have been marginalised as a result of this competition.”

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

7

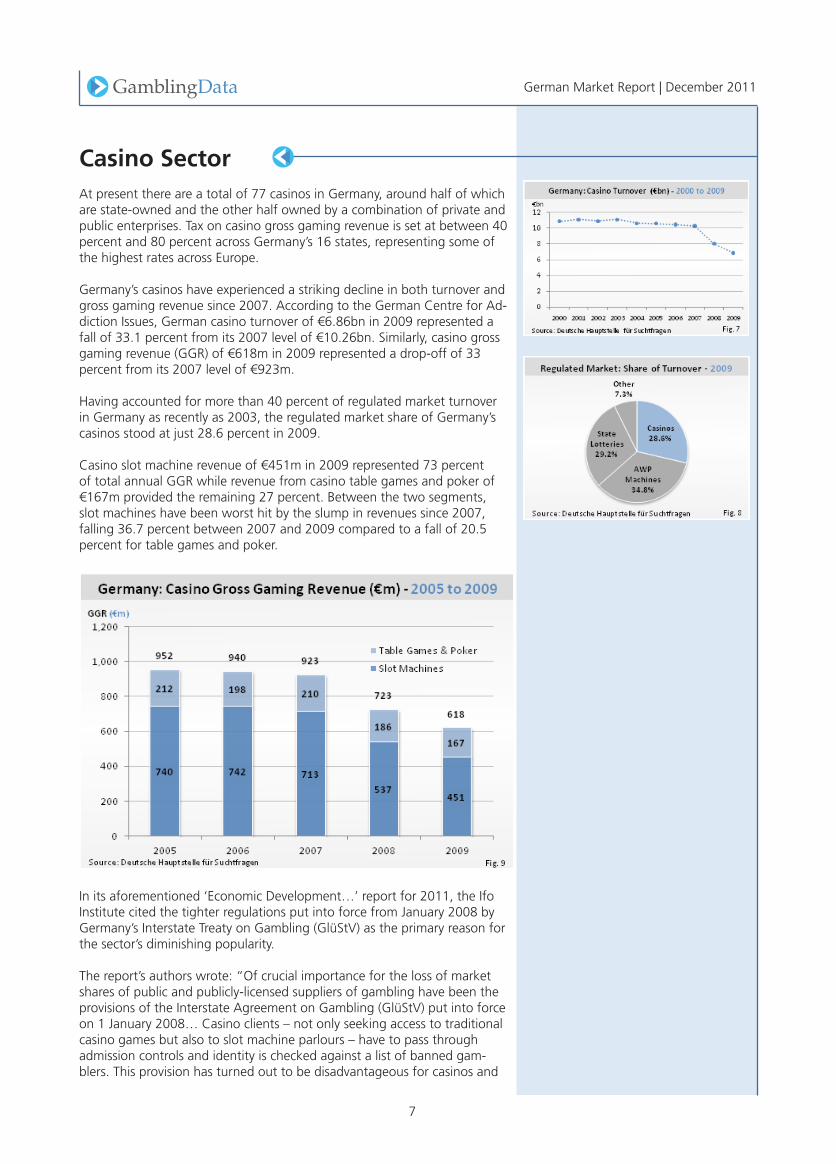

CasinoSectorAt present there are a total of 77 casinos in Germany, around half of which are state-owned and the other half owned by a combination of private and public enterprises. Tax on casino gross gaming revenue is set at between 40 percent and 80 percent across Germany’s 16 states, representing some of the highest rates across Europe.

Germany’s casinos have experienced a striking decline in both turnover and gross gaming revenue since 2007. According to the German Centre for Ad-diction Issues, German casino turnover of €6.86bn in 2009 represented a fall of 33.1 percent from its 2007 level of €10.26bn. Similarly, casino gross gaming revenue (GGR) of €618m in 2009 represented a drop-off of 33 percent from its 2007 level of €923m.

Having accounted for more than 40 percent of regulated market turnover in Germany as recently as 2003, the regulated market share of Germany’s casinos stood at just 28.6 percent in 2009.

Casino slot machine revenue of €451m in 2009 represented 73 percent of total annual GGR while revenue from casino table games and poker of €167m provided the remaining 27 percent. Between the two segments, slot machines have been worst hit by the slump in revenues since 2007, falling 36.7 percent between 2007 and 2009 compared to a fall of 20.5 percent for table games and poker.

In its aforementioned ‘Economic Development…’ report for 2011, the Ifo Institute cited the tighter regulations put into force from January 2008 by Germany’s Interstate Treaty on Gambling (GlüStV) as the primary reason for the sector’s diminishing popularity.

The report’s authors wrote: “Of crucial importance for the loss of market shares of public and publicly-licensed suppliers of gambling have been the provisions of the Interstate Agreement on Gambling (GlüStV) put into force on 1 January 2008… Casino clients – not only seeking access to traditional casino games but also to slot machine parlours – have to pass through admission controls and identity is checked against a list of banned gam-blers. This provision has turned out to be disadvantageous for casinos and

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

8

has contributed considerably to their losses in market shares. Many gamblers who are refused entry to casinos turn to the internet or even illegal betting gambling offers.”

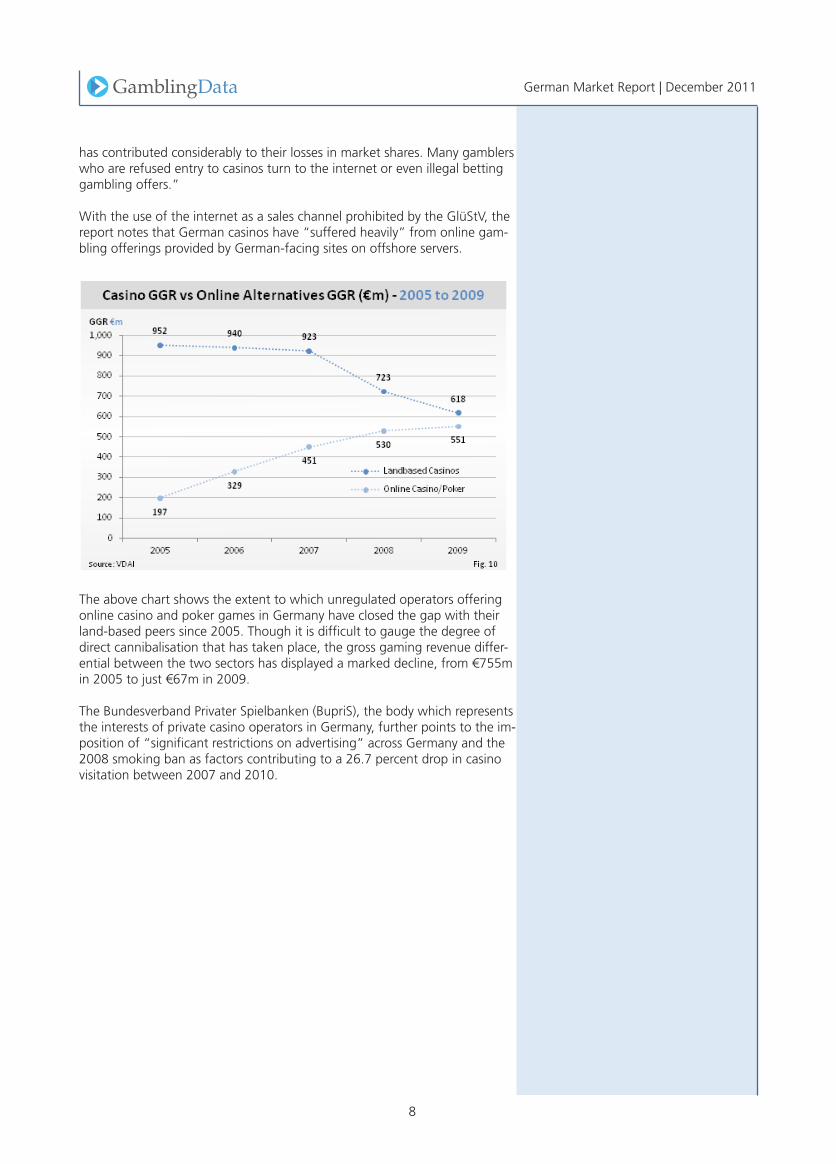

With the use of the internet as a sales channel prohibited by the GlüStV, the report notes that German casinos have “suffered heavily” from online gam-bling offerings provided by German-facing sites on offshore servers.

The above chart shows the extent to which unregulated operators offering online casino and poker games in Germany have closed the gap with their land-based peers since 2005. Though it is difficult to gauge the degree of direct cannibalisation that has taken place, the gross gaming revenue differ-ential between the two sectors has displayed a marked decline, from €755m in 2005 to just €67m in 2009.

The Bundesverband Privater Spielbanken (BupriS), the body which represents the interests of private casino operators in Germany, further points to the im-position of “significant restrictions on advertising” across Germany and the 2008 smoking ban as factors contributing to a 26.7 percent drop in casino visitation between 2007 and 2010.

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

9

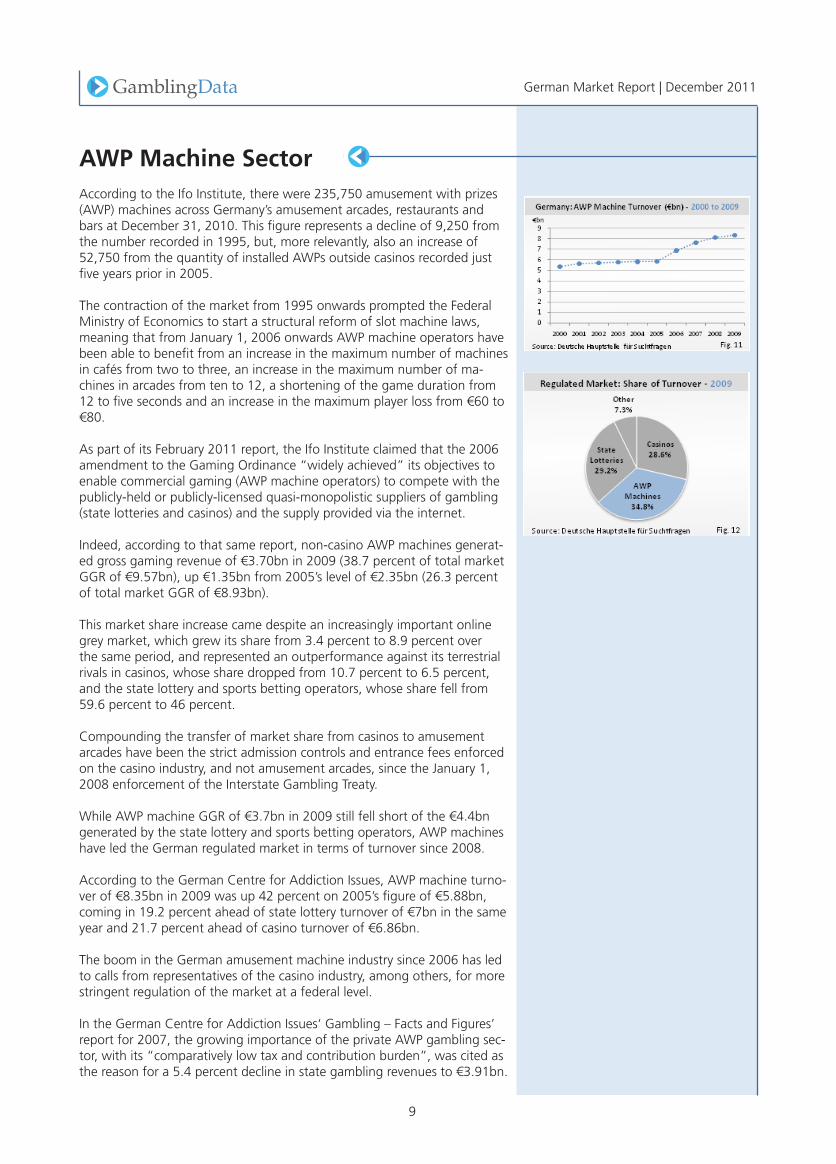

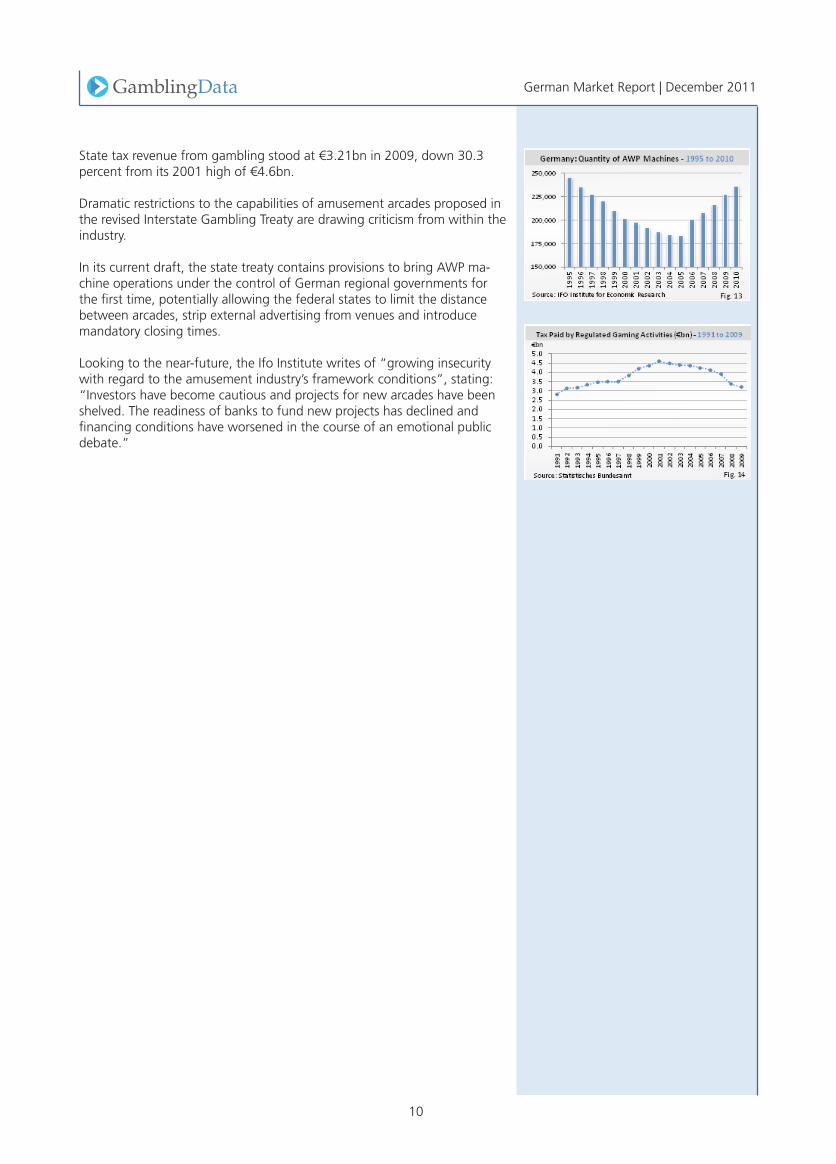

AWPMachineSectorAccording to the Ifo Institute, there were 235,750 amusement with prizes (AWP) machines across Germany’s amusement arcades, restaurants and bars at December 31, 2010. This figure represents a decline of 9,250 from the number recorded in 1995, but, more relevantly, also an increase of 52,750 from the quantity of installed AWPs outside casinos recorded just five years prior in 2005.

The contraction of the market from 1995 onwards prompted the Federal Ministry of Economics to start a structural reform of slot machine laws, meaning that from January 1, 2006 onwards AWP machine operators have been able to benefit from an increase in the maximum number of machines in cafés from two to three, an increase in the maximum number of ma-chines in arcades from ten to 12, a shortening of the game duration from 12 to five seconds and an increase in the maximum player loss from €60 to €80.

As part of its February 2011 report, the Ifo Institute claimed that the 2006 amendment to the Gaming Ordinance “widely achieved” its objectives to enable commercial gaming (AWP machine operators) to compete with the publicly-held or publicly-licensed quasi-monopolistic suppliers of gambling (state lotteries and casinos) and the supply provided via the internet.

Indeed, according to that same report, non-casino AWP machines generat-ed gross gaming revenue of €3.70bn in 2009 (38.7 percent of total market GGR of €9.57bn), up €1.35bn from 2005’s level of €2.35bn (26.3 percent of total market GGR of €8.93bn).

This market share increase came despite an increasingly important online grey market, which grew its share from 3.4 percent to 8.9 percent over the same period, and represented an outperformance against its terrestrial rivals in casinos, whose share dropped from 10.7 percent to 6.5 percent, and the state lottery and sports betting operators, whose share fell from 59.6 percent to 46 percent.

Compounding the transfer of market share from casinos to amusement arcades have been the strict admission controls and entrance fees enforced on the casino industry, and not amusement arcades, since the January 1, 2008 enforcement of the Interstate Gambling Treaty.

While AWP machine GGR of €3.7bn in 2009 still fell short of the €4.4bn generated by the state lottery and sports betting operators, AWP machines have led the German regulated market in terms of turnover since 2008.

According to the German Centre for Addiction Issues, AWP machine turno-ver of €8.35bn in 2009 was up 42 percent on 2005’s figure of €5.88bn, coming in 19.2 percent ahead of state lottery turnover of €7bn in the same year and 21.7 percent ahead of casino turnover of €6.86bn.

The boom in the German amusement machine industry since 2006 has led to calls from representatives of the casino industry, among others, for more stringent regulation of the market at a federal level.

In the German Centre for Addiction Issues‘ Gambling – Facts and Figures’ report for 2007, the growing importance of the private AWP gambling sec-tor, with its “comparatively low tax and contribution burden”, was cited as the reason for a 5.4 percent decline in state gambling revenues to €3.91bn.

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

10

State tax revenue from gambling stood at €3.21bn in 2009, down 30.3 percent from its 2001 high of €4.6bn.

Dramatic restrictions to the capabilities of amusement arcades proposed in the revised Interstate Gambling Treaty are drawing criticism from within the industry.

In its current draft, the state treaty contains provisions to bring AWP ma-chine operations under the control of German regional governments for the first time, potentially allowing the federal states to limit the distance between arcades, strip external advertising from venues and introduce mandatory closing times.

Looking to the near-future, the Ifo Institute writes of “growing insecurity with regard to the amusement industry’s framework conditions”, stating: “Investors have become cautious and projects for new arcades have been shelved. The readiness of banks to fund new projects has declined and financing conditions have worsened in the course of an emotional public debate.”

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

11

OnlineSector

GamblingDataCoreEstimate

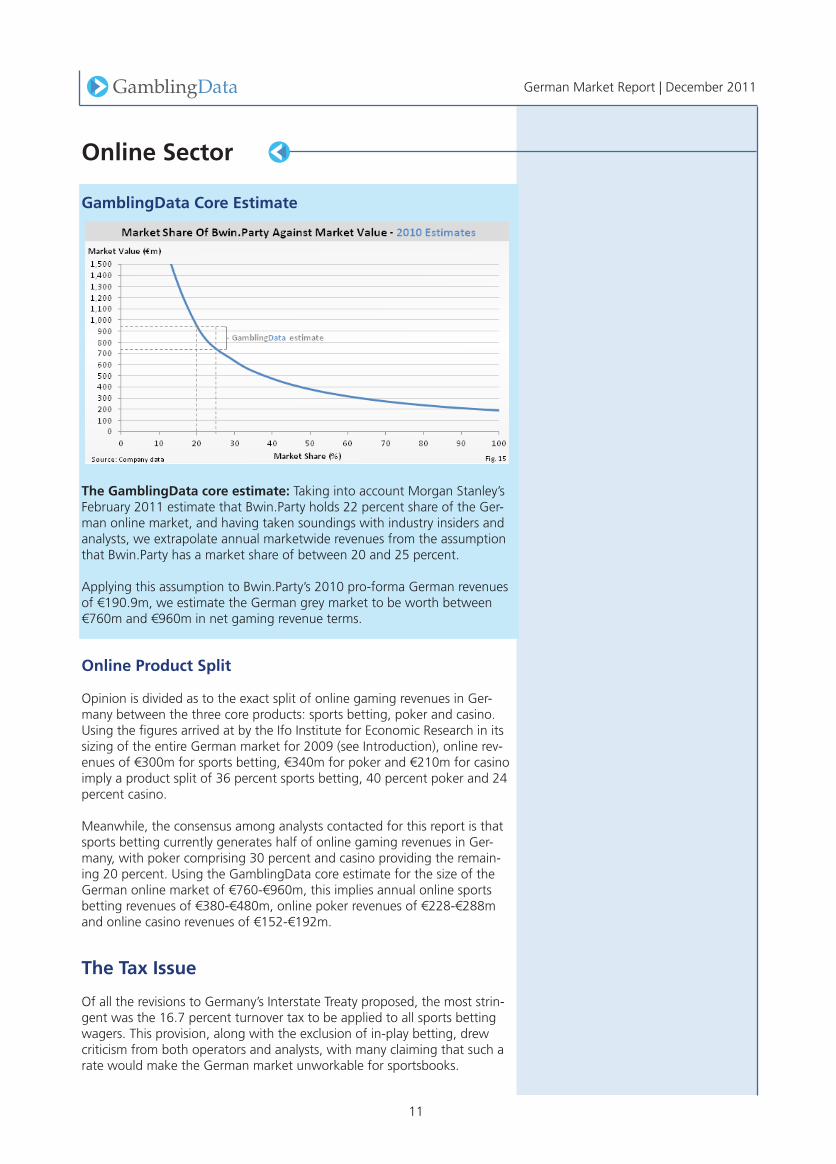

TheGamblingDatacoreestimate: Taking into account Morgan Stanley’s February 2011 estimate that Bwin.Party holds 22 percent share of the Ger-man online market, and having taken soundings with industry insiders and analysts, we extrapolate annual marketwide revenues from the assumption that Bwin.Party has a market share of between 20 and 25 percent.

Applying this assumption to Bwin.Party’s 2010 pro-forma German revenues of €190.9m, we estimate the German grey market to be worth between €760m and €960m in net gaming revenue terms.

OnlineProductSplit

Opinion is divided as to the exact split of online gaming revenues in Ger-many between the three core products: sports betting, poker and casino. Using the figures arrived at by the Ifo Institute for Economic Research in its sizing of the entire German market for 2009 (see Introduction), online rev-enues of €300m for sports betting, €340m for poker and €210m for casino imply a product split of 36 percent sports betting, 40 percent poker and 24 percent casino.

Meanwhile, the consensus among analysts contacted for this report is that sports betting currently generates half of online gaming revenues in Ger-many, with poker comprising 30 percent and casino providing the remain-ing 20 percent. Using the GamblingData core estimate for the size of the German online market of €760-€960m, this implies annual online sports betting revenues of €380-€480m, online poker revenues of €228-€288m and online casino revenues of €152-€192m.

TheTaxIssue

Of all the revisions to Germany’s Interstate Treaty proposed, the most strin-gent was the 16.7 percent turnover tax to be applied to all sports betting wagers. This provision, along with the exclusion of in-play betting, drew criticism from both operators and analysts, with many claiming that such a rate would make the German market unworkable for sportsbooks.

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

12

Following April’s announcement, Nick Batram of Peel Hunt questioned the viability of the tax rate for operators, stating in a note to investors: “Such a structure would make it very difficult for operators to make money, and in reality the market would remain dominated by unlicensed operators.”

A detailed note from analysts at UBS explored the potential motives behind the turnover tax, stating: “Germany appears to be proposing the highest tax rate across all regulated markets. France carries a turnover tax of 8.5 percent on sports, and this is generally considered to be unworkable given gross win margins are typically less than 10 percent. Operators are forced to raise gross win margins to the point where their offering becomes unattrac-tive and customers move offshore.”

The analyst team at Morgan Stanley, meanwhile, wrote: “The proposals as they stand are not viable for a risk-taking bookmaker, unless it passed on the 17 percent fee to customers. With freely available access to other bet-ting options on the Internet that would not levy this charge, that option is not possible.”

Federer Nadal Total

OffshoreModel

Odds 1.85 1.85

Bets €50 €50 €100

Payout €0 €92.50 €92.50

Gross Win - - €7.50

Gross Win Margin - - 7.5%

OnshoreModel

Odds 1.40 1.40

Bets €50 €50 €100

Payout €0 €70 €70

Gross Win - - €30

Gross Win Margin - - 30%

Taxes - - -€17

Net Win - - €13

Fig. 15

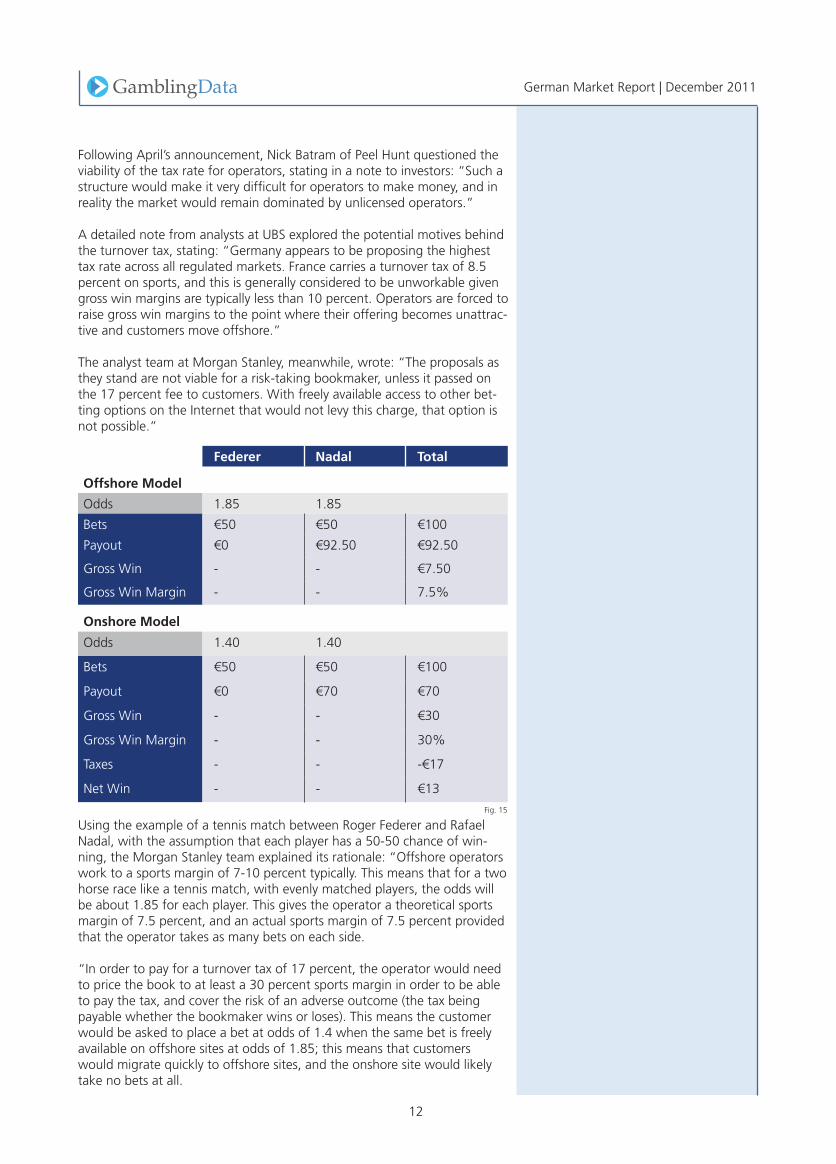

Using the example of a tennis match between Roger Federer and Rafael Nadal, with the assumption that each player has a 50-50 chance of win-ning, the Morgan Stanley team explained its rationale: “Offshore operators work to a sports margin of 7-10 percent typically. This means that for a two horse race like a tennis match, with evenly matched players, the odds will be about 1.85 for each player. This gives the operator a theoretical sports margin of 7.5 percent, and an actual sports margin of 7.5 percent provided that the operator takes as many bets on each side.

“In order to pay for a turnover tax of 17 percent, the operator would need to price the book to at least a 30 percent sports margin in order to be able to pay the tax, and cover the risk of an adverse outcome (the tax being payable whether the bookmaker wins or loses). This means the customer would be asked to place a bet at odds of 1.4 when the same bet is freely available on offshore sites at odds of 1.85; this means that customers would migrate quickly to offshore sites, and the onshore site would likely take no bets at all.

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

13

“As a direct result, the rules would generate almost no tax and offer no customer protections, as most customers would remain offshore.”

On October 28, a revised draft of the 2012 Interstate Treaty was agreed upon by 15 of the 16 German Länder, with Schleswig-Holstein once again abstaining. The new draft proposals, in addition to increasing the number of sports betting licences from seven to 20, contain a decrease in turnover tax from 16.7 percent to 5 percent.

A follow-up note to investors from Investec’s Paul Leyland stated: “[The latest draft] would seem positive, however, with maximum bets per month limited to €1000 and restrictions on in-play, we doubt this would be profit-able, especially given that the ban on casino and poker is to remain.“

Analysts at Deutsche Bank, meanwhile, said of the revised proposals: “If this was to be the final outcome then we think this would make the Ger-man online gaming market commercially unattractive for the majority of online gaming operators.“

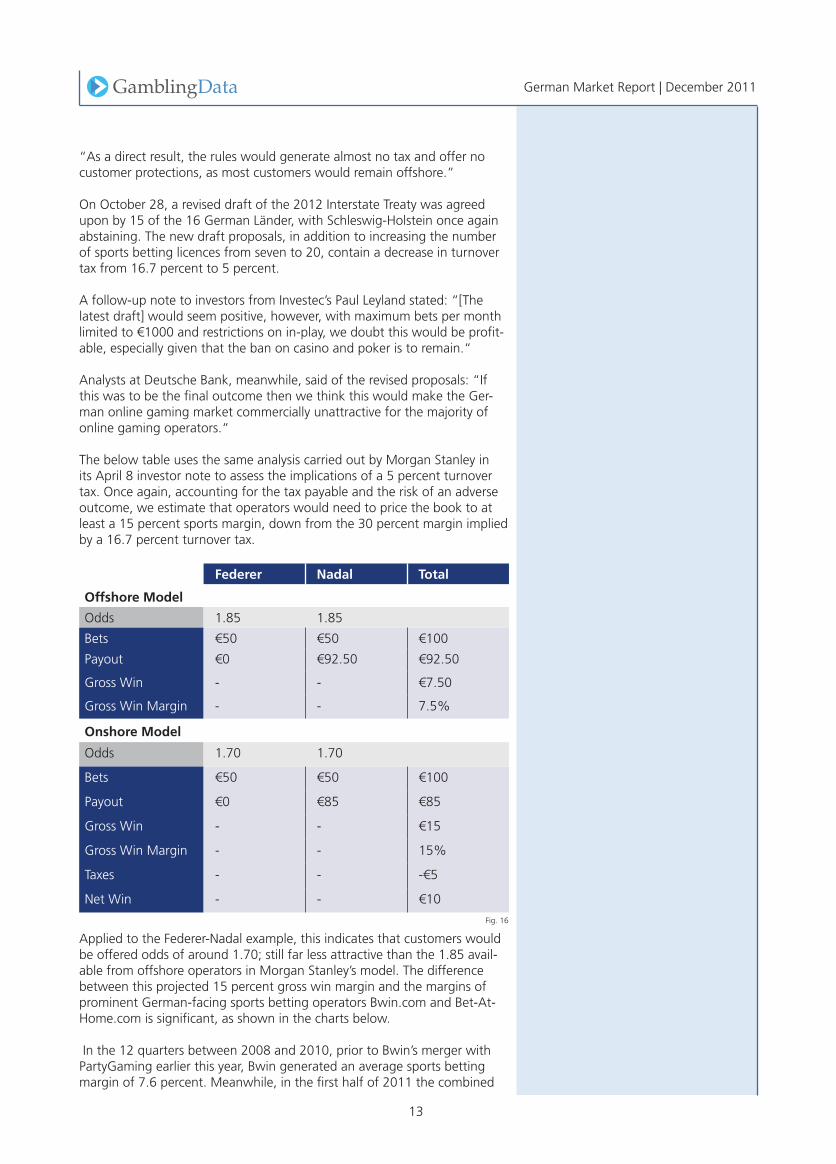

The below table uses the same analysis carried out by Morgan Stanley in its April 8 investor note to assess the implications of a 5 percent turnover tax. Once again, accounting for the tax payable and the risk of an adverse outcome, we estimate that operators would need to price the book to at least a 15 percent sports margin, down from the 30 percent margin implied by a 16.7 percent turnover tax.

Federer Nadal Total

OffshoreModel

Odds 1.85 1.85

Bets €50 €50 €100

Payout €0 €92.50 €92.50

Gross Win - - €7.50

Gross Win Margin - - 7.5%

OnshoreModel

Odds 1.70 1.70

Bets €50 €50 €100

Payout €0 €85 €85

Gross Win - - €15

Gross Win Margin - - 15%

Taxes - - -€5

Net Win - - €10

Fig. 16

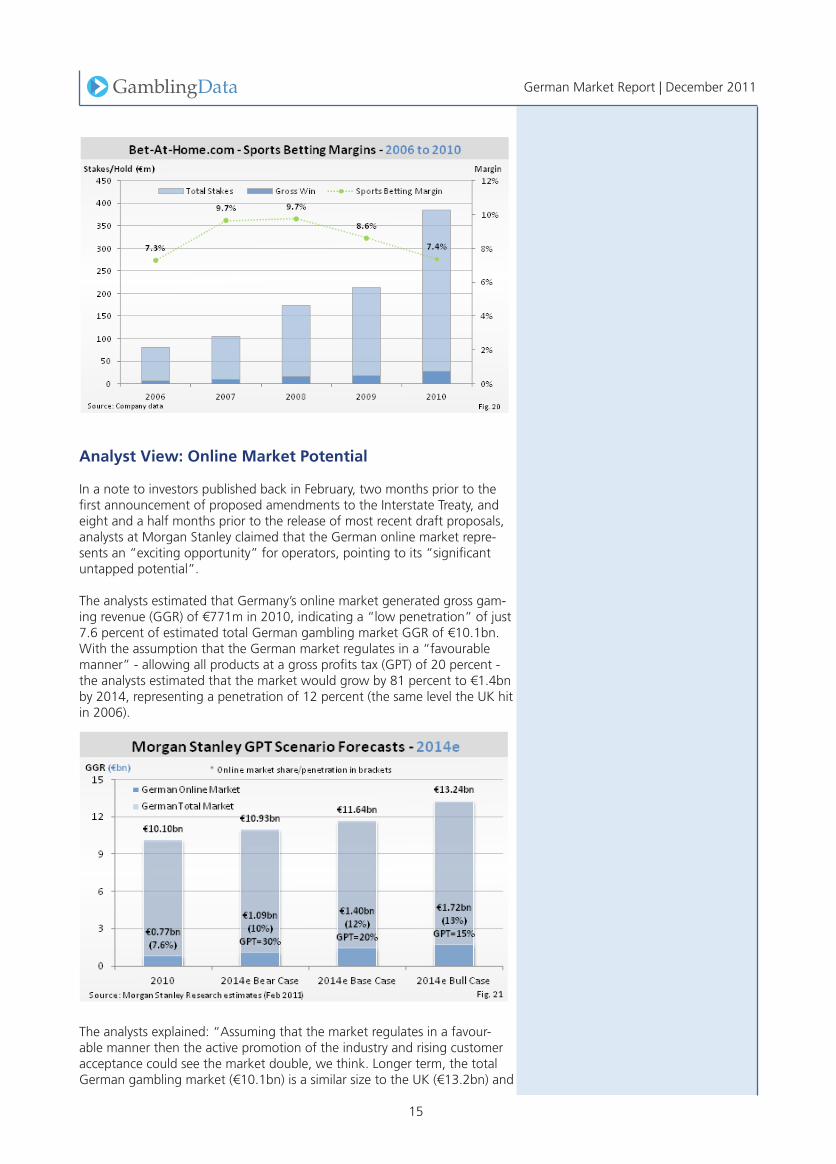

Applied to the Federer-Nadal example, this indicates that customers would be offered odds of around 1.70; still far less attractive than the 1.85 avail-able from offshore operators in Morgan Stanley’s model. The difference between this projected 15 percent gross win margin and the margins of prominent German-facing sports betting operators Bwin.com and Bet-At-Home.com is significant, as shown in the charts below.

In the 12 quarters between 2008 and 2010, prior to Bwin’s merger with PartyGaming earlier this year, Bwin generated an average sports betting margin of 7.6 percent. Meanwhile, in the first half of 2011 the combined

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

14

entity Bwin.Party Digital Entertainment generated a pro forma sports bet-ting margin of 7.5 percent.

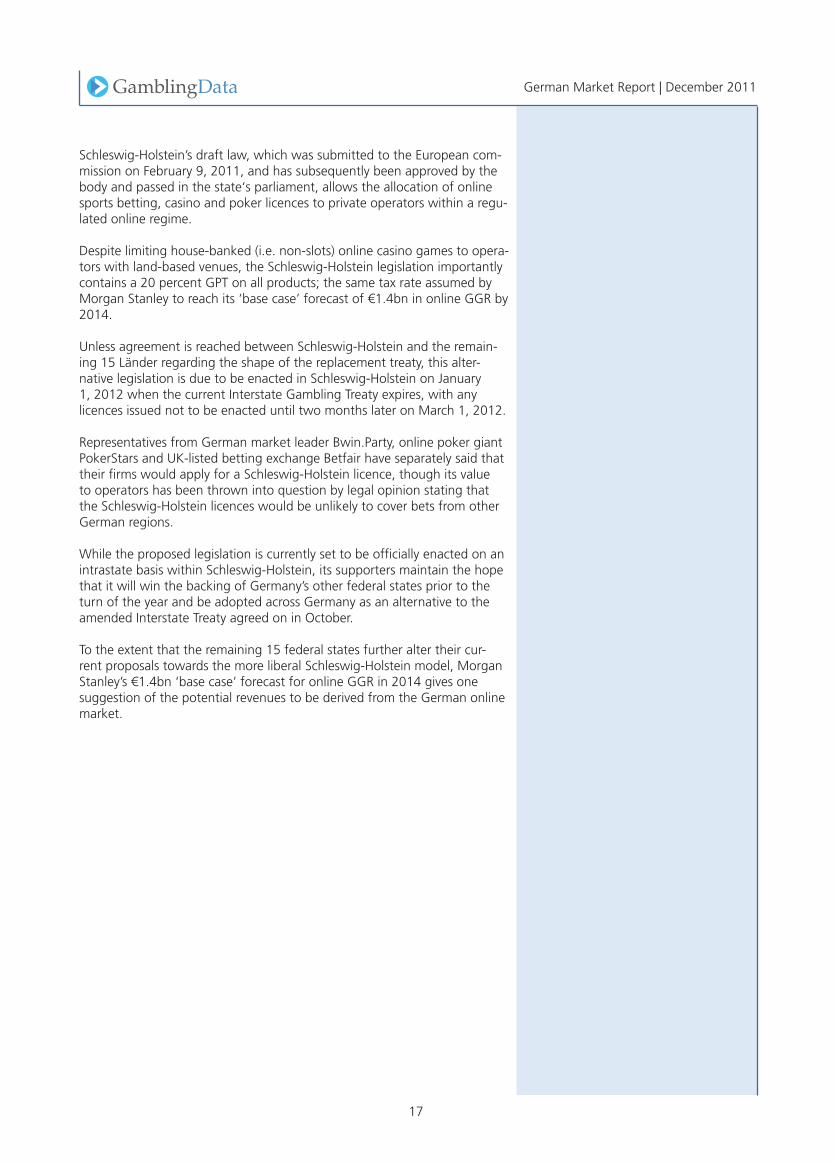

Mangas Group-owned online operator Bet-At-Home.com similarly gener-ates sports betting revenues within Morgan Stanley’s suggested 7-10 per-cent range. In the five years between 2006 and 2010 the firm’s sportsbook achieved an average margin of 8.5 percent.

Though both of these two websites attract a geographically diverse set of punters, each offering their services in more than 20 European languages, their sports betting margins can be said to offer a reasonable proxy for those of the German online market as a whole.

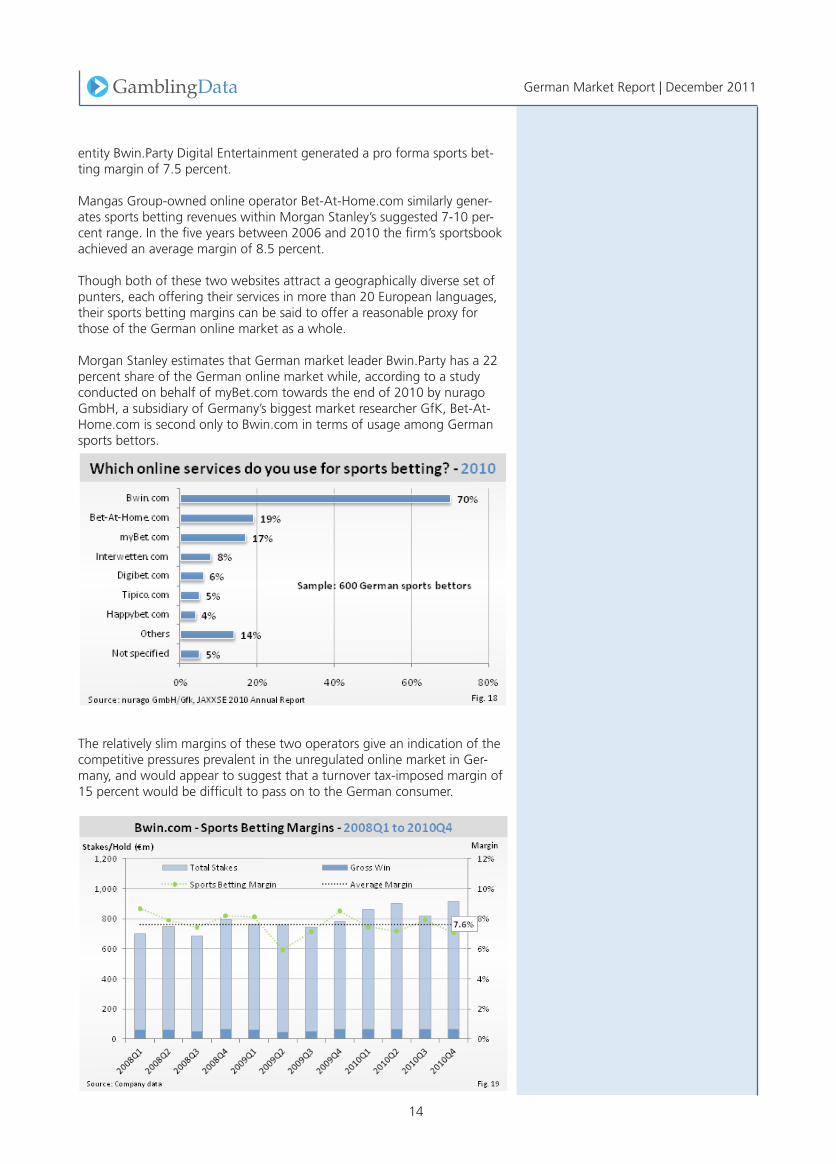

Morgan Stanley estimates that German market leader Bwin.Party has a 22 percent share of the German online market while, according to a study conducted on behalf of myBet.com towards the end of 2010 by nurago GmbH, a subsidiary of Germany’s biggest market researcher GfK, Bet-At-Home.com is second only to Bwin.com in terms of usage among German sports bettors.

The relatively slim margins of these two operators give an indication of the competitive pressures prevalent in the unregulated online market in Ger-many, and would appear to suggest that a turnover tax-imposed margin of 15 percent would be difficult to pass on to the German consumer.

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

15

AnalystView:OnlineMarketPotential

In a note to investors published back in February, two months prior to the first announcement of proposed amendments to the Interstate Treaty, and eight and a half months prior to the release of most recent draft proposals, analysts at Morgan Stanley claimed that the German online market repre-sents an “exciting opportunity” for operators, pointing to its “significant untapped potential”.

The analysts estimated that Germany’s online market generated gross gam-ing revenue (GGR) of €771m in 2010, indicating a “low penetration” of just 7.6 percent of estimated total German gambling market GGR of €10.1bn. With the assumption that the German market regulates in a “favourable manner” - allowing all products at a gross profits tax (GPT) of 20 percent - the analysts estimated that the market would grow by 81 percent to €1.4bn by 2014, representing a penetration of 12 percent (the same level the UK hit in 2006).

The analysts explained: “Assuming that the market regulates in a favour-able manner then the active promotion of the industry and rising customer acceptance could see the market double, we think. Longer term, the total German gambling market (€10.1bn) is a similar size to the UK (€13.2bn) and

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

16

even if the German online gambling market doubles from today’s level of €0.8bn, there would be substantial catch-up potential to the UK level of €2.6bn.”

Morgan Stanley’s ‘base case’ forecast of 81 percent growth in German online GGR between 2010 and 2014 placed Germany’s potential market size in 2014 at a similar level to that of the ‘base case’ forecasts for newly-regulated France and soon-to-regulate Spain, with each market projected to reach around €1.4bn in online GGR.

Positing the theory that all newly-regulated markets in Europe will grow by more than 50 percent over their first four years of existence, the ana-lysts wrote: “The drivers for growth in regulating markets are clear to us. The ability to advertise and promote the products creates new interest in gaming. The wider range of products and more interesting content drives market share gains from offline gambling. The natural demographic factors drive more betting and gambling online, as younger demographics spend more time on the internet.

“50-100 percent market growth may sound aggressive over four years, but the UK has doubled since 2006, and in 2006 online gambling was already seen as a mass-market product and accounted for 11 percent of all gam-bling.”

Morgan Stanley’s assumptions, and therefore its German online GGR fore-cast of €1.40bn by 2014, would appear to have been subsequently blown out of the water by the announcement on April 6 of the passing of the First State Treaty amending the GlüStV.

Instead of the 20 percent GPT on gambling assumed by Morgan Stanley, 15 of Germany’s 16 federal states passed plans to tax all products at a more restrictive 16.7 percent of turnover, with online casino and poker limited to one land-based casino operator per federal state and sports betting restrict-ed to seven licensees.

Nevertheless, in light of a separate draft law passed in September of this year by Schleswig-Holstein, a small northern German state close to the Dan-ish border which abstained from joining its 15 fellow Länder in voting for April’s draft proposals, Morgan Stanley’s prior ‘base case’ forecast can still be said to hold near-term relevance.

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

17

Schleswig-Holstein’s draft law, which was submitted to the European com-mission on February 9, 2011, and has subsequently been approved by the body and passed in the state‘s parliament, allows the allocation of online sports betting, casino and poker licences to private operators within a regu-lated online regime.

Despite limiting house-banked (i.e. non-slots) online casino games to opera-tors with land-based venues, the Schleswig-Holstein legislation importantly contains a 20 percent GPT on all products; the same tax rate assumed by Morgan Stanley to reach its ‘base case’ forecast of €1.4bn in online GGR by 2014.

Unless agreement is reached between Schleswig-Holstein and the remain-ing 15 Länder regarding the shape of the replacement treaty, this alter-native legislation is due to be enacted in Schleswig-Holstein on January 1, 2012 when the current Interstate Gambling Treaty expires, with any licences issued not to be enacted until two months later on March 1, 2012.

Representatives from German market leader Bwin.Party, online poker giant PokerStars and UK-listed betting exchange Betfair have separately said that their firms would apply for a Schleswig-Holstein licence, though its value to operators has been thrown into question by legal opinion stating that the Schleswig-Holstein licences would be unlikely to cover bets from other German regions.

While the proposed legislation is currently set to be officially enacted on an intrastate basis within Schleswig-Holstein, its supporters maintain the hope that it will win the backing of Germany’s other federal states prior to the turn of the year and be adopted across Germany as an alternative to the amended Interstate Treaty agreed on in October.

To the extent that the remaining 15 federal states further alter their cur-rent proposals towards the more liberal Schleswig-Holstein model, Morgan Stanley’s €1.4bn ‘base case’ forecast for online GGR in 2014 gives one suggestion of the potential revenues to be derived from the German online market.

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

18

AboutGamblingData The global gaming industry is changing fast. With many jurisdictions in transition between pre- and post-regulation, never has it been so important to have access to reliable data information about the market.

GamblingData provides clients with essential country, sector and com-pany analytics to help achieve the best possible understanding of the underlying facts, figures and trends in support of their business, com-petitor, product and market research activities.

GamblingData provides the facts, intelligence and analysis gaming businesses need to make the most of the opportunities in a volatile business environment.

We have a team of four dedicated business analysts researching, compil-ing and analyzing relevant gambling data points from over 150 jurisdic-tions.

We are able to provide tailored data research services specific to your company requirements and/or access to an online database with histori-cal data going back over 30 years.

Our database is updated in real time so you can be sure you are accessing the latest available research and has some market leading functionality allowing very focused intelligence gathering.

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

German Market Report | December 2011Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

19

Suite 704, 91 Waterloo Road,London, SE1 8RTTel: +44 207 921 [email protected]

Scott Longley+44(0)207 921 [email protected]

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’

DisclaimerIn preparing this report GamblingCompliance Ltd. has made every effort to ensure the accuracy of the contents of this report. However, no representa-tion or warranty (express or implied) is given as to the accuracy or com-pleteness of the information contained in this report.

Any reader, or their associated corporate entity, that relies on any informa-tion contained in this report does so entirely at their own risk. Gambling-Compliance Ltd. and its employees do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this report or any decision based on it.

© Copyright 2011 GamblingCompliance Ltd. All rights reserved.

The intended use of this report is for purchasers only. No part of this report may be (i) copied, photocopied or duplicated in any form by any means or (ii) redistributed or republished without the prior written consent of Gam-blingCompliance Ltd.

Font: Palatino RomanBlue: From gamblingdata.com, current live websiteRed: from gamblingcompliance.com, current live website

Logo revisions/options

This set shows the logos with the connecting ‘g’