Embed Size (px)

DESCRIPTION

Conference German-Italian Cooperation for the Development of Renewable Energies in the Mediterranean DESERTEC EU-MENA Cooperation for Clean Energies from Deserts. Gerhard Knies The Club of Rome and TREC, Trans-Mediterranean Renewable Energy Cooperation [email protected]. - PowerPoint PPT Presentation

Citation preview

CONFERENCEGERMAN-ITALIAN COOPERATION FOR THE

DEVELOPMENT OF RENEWABLE ENERGIES IN THE

MEDITERRANEAN

DESERTEC EU-MENA Cooperation for Clean Energies from

DesertsGerhard Knies

The Club of Rome and TREC, Trans-Mediterranean Renewable Energy Cooperation

1Gerhard Knies, Berlin 2007-11-19

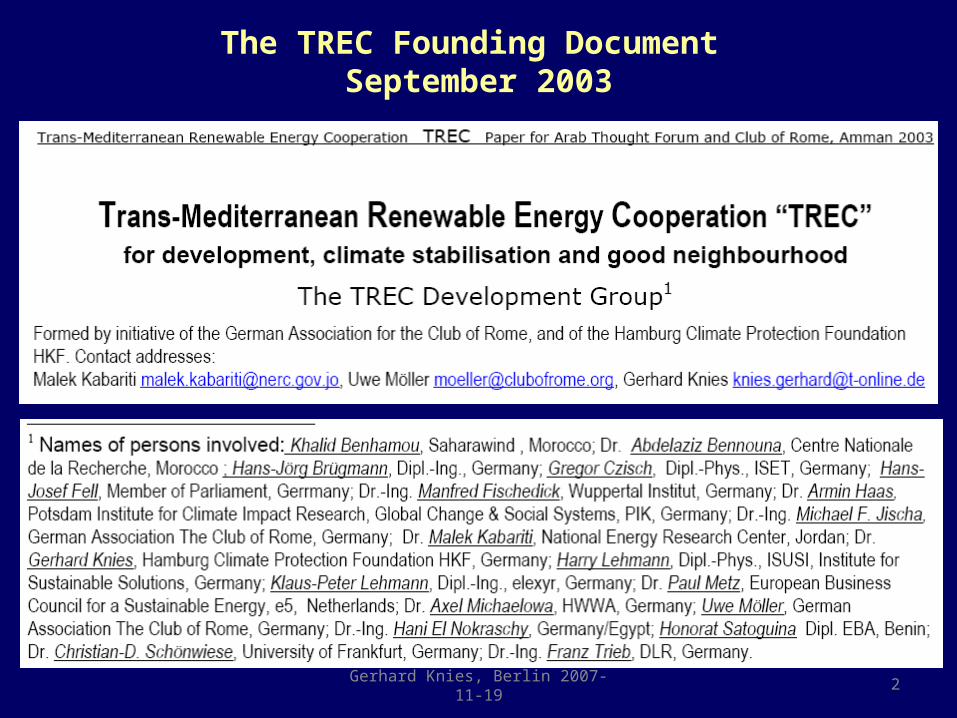

The TREC Founding Document September 2003

Gerhard Knies, Berlin 2007-11-19 2

Gerhard Knies, Berlin 2007-11-19 3

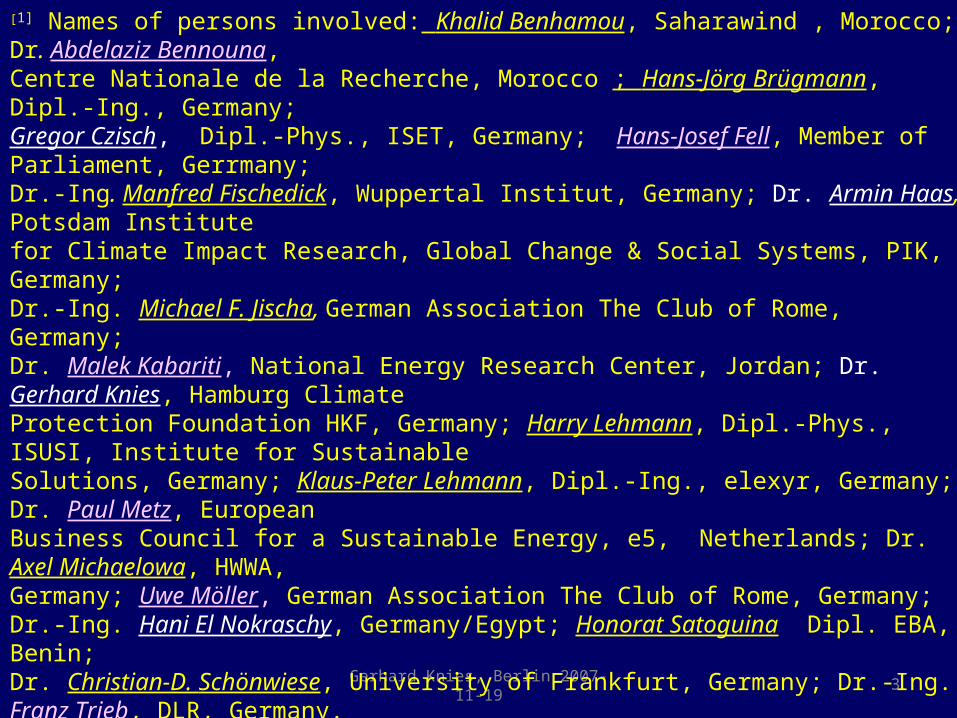

[1] Names of persons involved: Khalid Benhamou, Saharawind , Morocco; Dr. Abdelaziz Bennouna, Centre Nationale de la Recherche, Morocco ; Hans-Jörg Brügmann, Dipl.-Ing., Germany; Gregor Czisch, Dipl.-Phys., ISET, Germany; Hans-Josef Fell, Member of Parliament, Gerrmany; Dr.-Ing. Manfred Fischedick, Wuppertal Institut, Germany; Dr. Armin Haas, Potsdam Institute for Climate Impact Research, Global Change & Social Systems, PIK, Germany; Dr.-Ing. Michael F. Jischa, German Association The Club of Rome, Germany; Dr. Malek Kabariti, National Energy Research Center, Jordan; Dr. Gerhard Knies, Hamburg Climate Protection Foundation HKF, Germany; Harry Lehmann, Dipl.-Phys., ISUSI, Institute for Sustainable Solutions, Germany; Klaus-Peter Lehmann, Dipl.-Ing., elexyr, Germany; Dr. Paul Metz, European Business Council for a Sustainable Energy, e5, Netherlands; Dr. Axel Michaelowa, HWWA, Germany; Uwe Möller, German Association The Club of Rome, Germany; Dr.-Ing. Hani El Nokraschy, Germany/Egypt; Honorat Satoguina Dipl. EBA, Benin; Dr. Christian-D. Schönwiese, University of Frankfurt, Germany; Dr.-Ing. Franz Trieb, DLR, Germany.

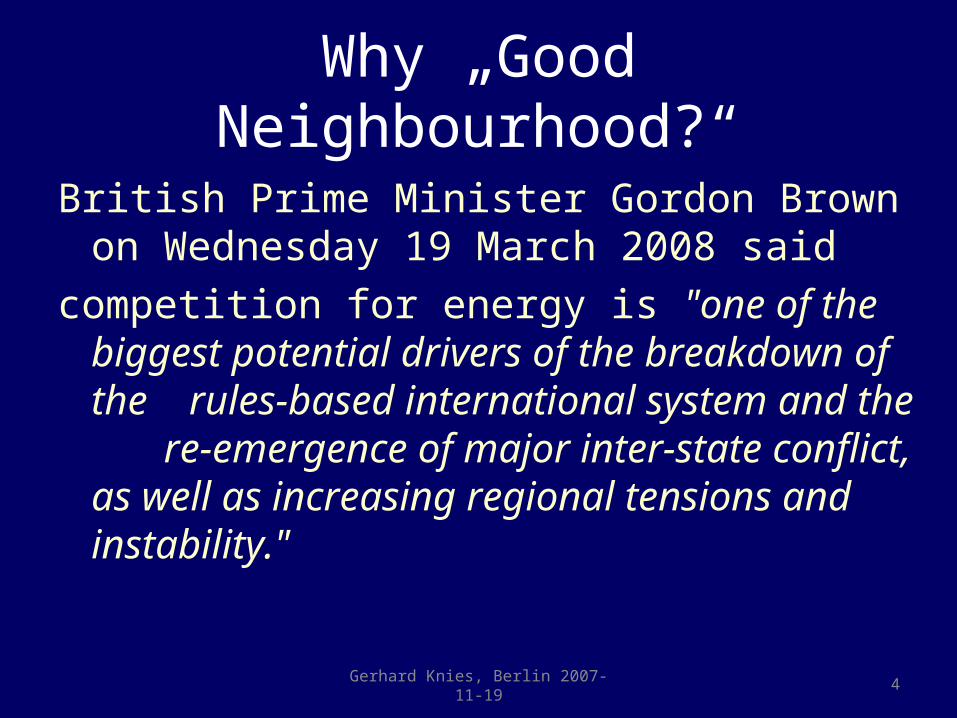

Why „Good Neighbourhood?“

British Prime Minister Gordon Brown on Wednesday 19 March 2008 said

competition for energy is "one of the biggest potential drivers of the breakdown of the rules-based international system and the re-emergence of major inter-state conflict, as well as increasing regional tensions and instability."

Gerhard Knies, Berlin 2007-11-19 4

Gerhard Knies, Berlin 2007-11-19 6

TRANS-CSPTRANS-CSP

3 “CSP” studies

Mediterranean PotentialsTrans-Mediterranean Interconnection

Sea Water Desalination -www.desertec.org-

7Gerhard Knies, Taipei e-parl. + WFC 2008-03-1/2

MED-CSPMED-CSP AQUA-CSPAQUA-CSP

Final Reports (2005,2006, 2007)by

German Aerospace Center (DLR)Institute of Technical Thermodynamics

Section Systems Analysis and Technology Assessment

Studies commissioned byFederal Ministry for the Environment,

Nature Conservation and Nuclear SafetyGermany

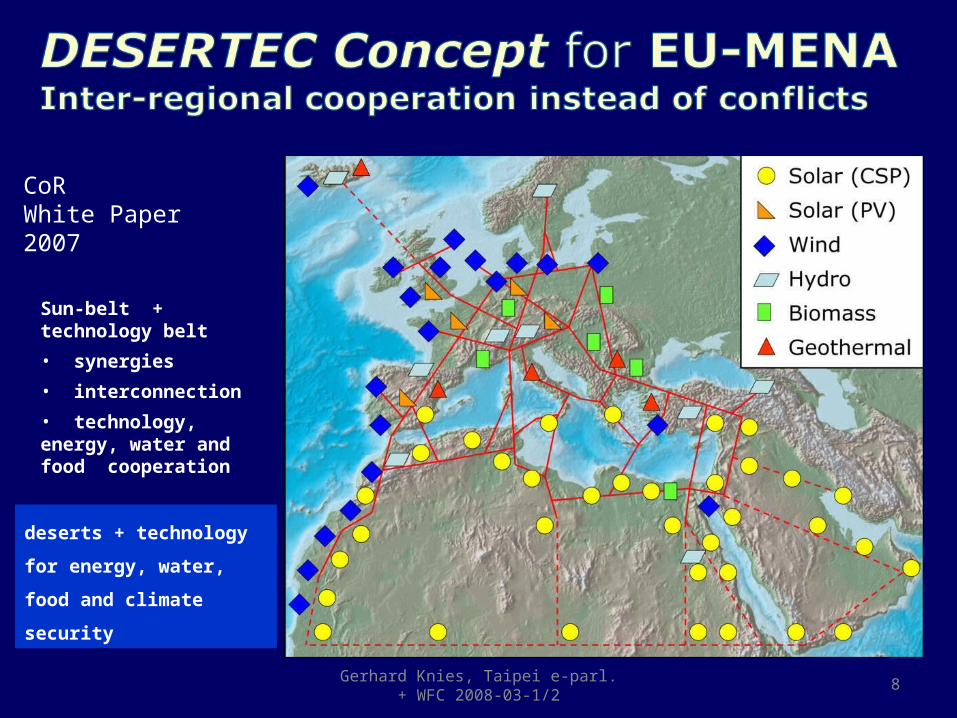

deserts + technology

for energy, water,

food and climate

security

Sun-belt + technology belt

• synergies

• interconnection

• technology, energy, water and food cooperation

8Gerhard Knies, Taipei e-parl. + WFC 2008-03-1/2

CoR White Paper 2007

Gerhard Knies, CSP 2008 Barcelona

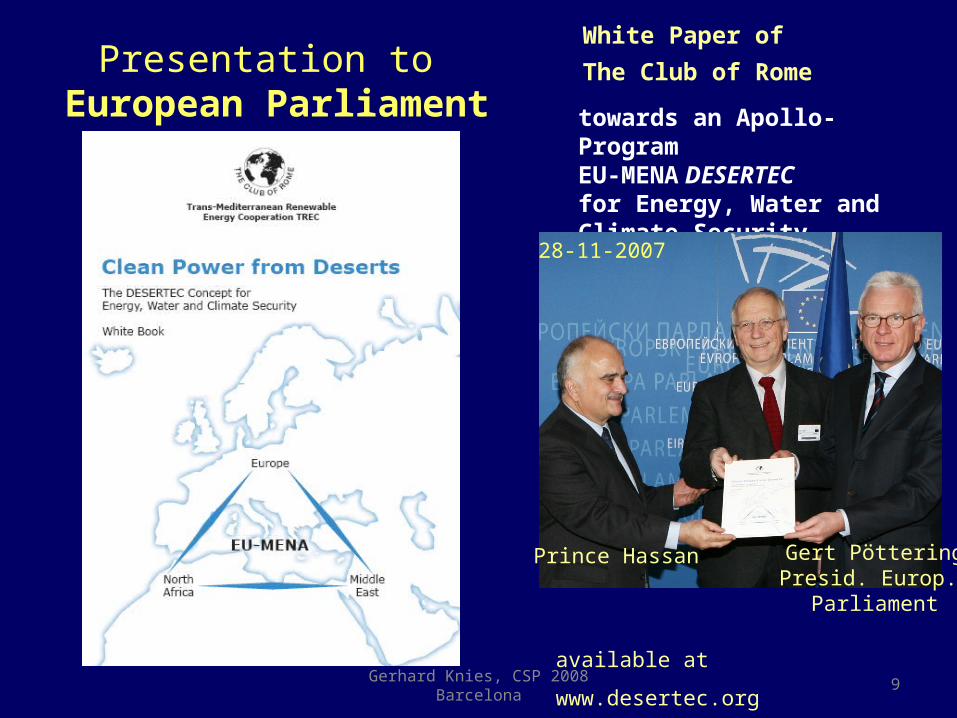

White Paper of

The Club of Rome

towards an Apollo-Program EU-MENA DESERTEC for Energy, Water and Climate Security

available at www.desertec.org9

Prince Hassan Gert PötteringPresid. Europ.

Parliament

Presentation to European Parliament

28-11-2007

Studies on potentials of renewable energies in EU-MENAInitiated by TREC, performed by DLR, financed by German gov’t, www.desertec.org

Biomass

Wind Energy

Geothermal Energy

Hydropower

(Typical Yield in GWhel/km²/y)

1700+ off

shore

1090

750

890

> 600 000

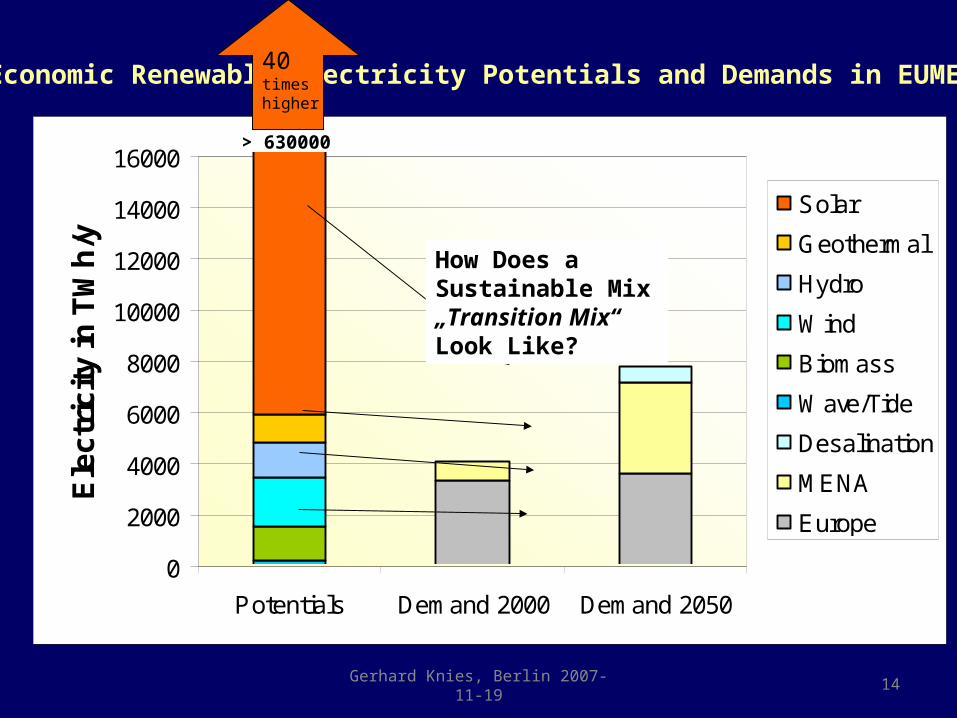

demand 7 500 TWh/y EU+MENA 2050 50 000 TWh/y world-wide 2050

Economic Potential TWhel/y.

(1)

(50)

(50)

Solar - CSP, PV

(1)

(250)

10Gerhard Knies, Taipei e-parl. + WFC 2008-03-1/2

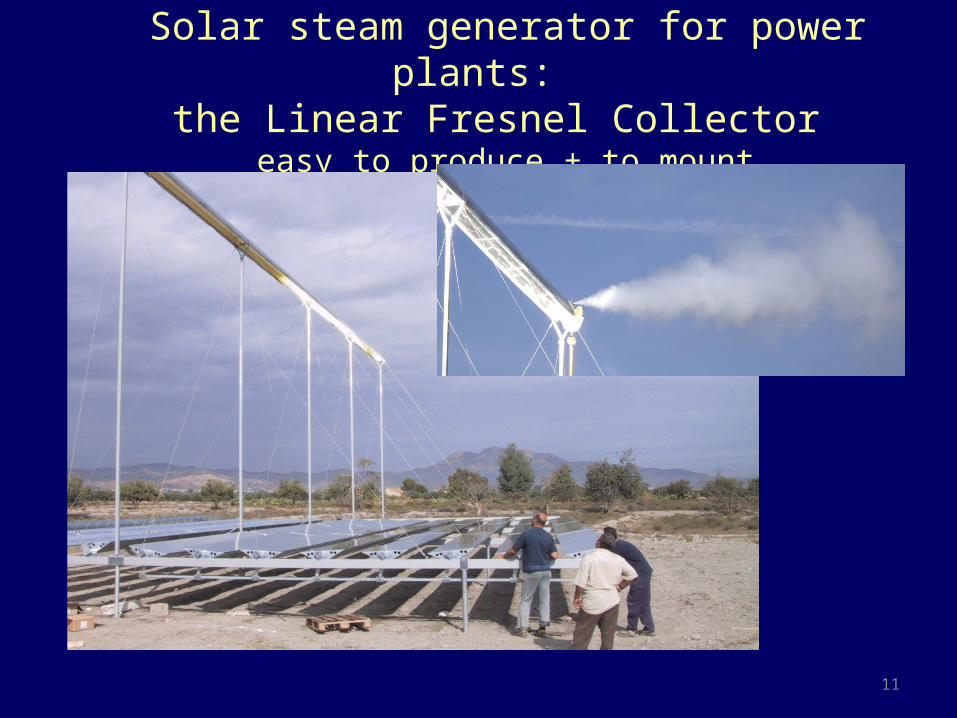

Solar steam generator for power plants: the Linear Fresnel Collector

easy to produce + to mount

11

Clean Power from Deserts for the World

Gerhard Knies, Taipei e-parl. + WFC 2008-03-1/2 12

WORLD EU-25 MENA

0

2000

4000

6000

8000

10000

12000

14000

16000

Potentials Demand 2000 Demand 2050

Ele

ctr

icit

y in

TW

h/y

Solar

Geothermal

Hydro

Wind

Biomass

Wave/Tide

Desalination

MENA

Europe

Economic Renewable Electricity Potentials and Demands in EUMENA

> 630000

How Does a Sustainable Mix„Transition Mix“Look Like?

14Gerhard Knies, Berlin 2007-11-19

40timeshigher

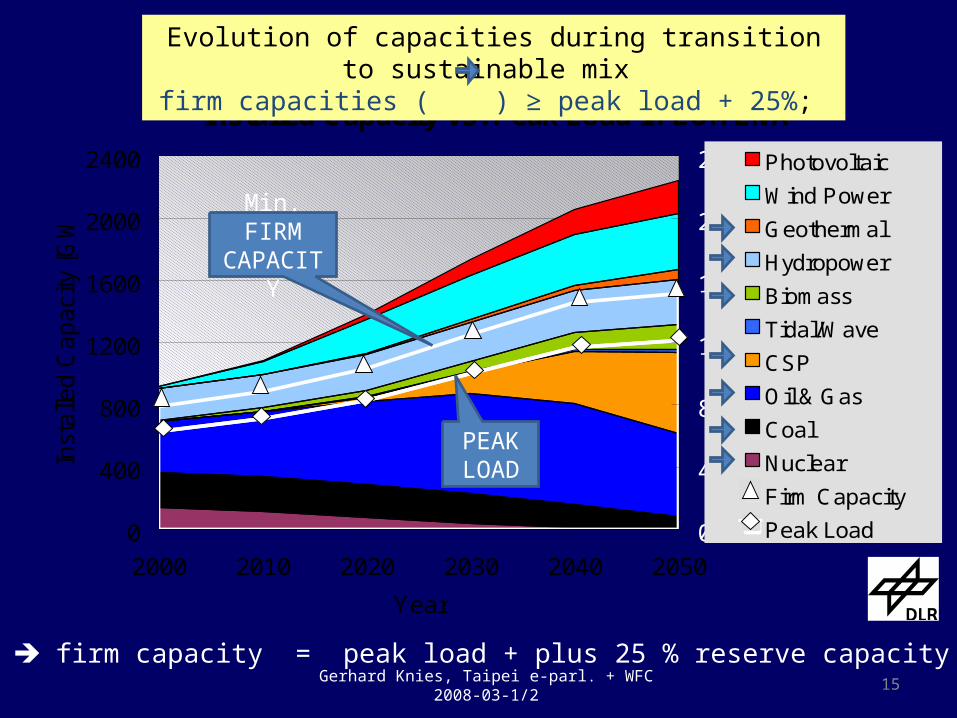

Installed Capacity vs. Peak Load in EUMENA

0

400

800

1200

1600

2000

2400

2000 2010 2020 2030 2040 2050

Year

Inst

alle

d C

ap

aci

ty [G

W]

0

400

800

1200

1600

2000

2400 Photovoltaic

Wind Power

Geothermal

Hydropower

Biomass

Tidal/Wave

CSP

Oil & Gas

Coal

Nuclear

Firm Capacity

Peak Load

Evolution of capacities during transition to sustainable mix firm capacities ( ) ≥ peak load + 25%;

firm capacity = peak load + plus 25 % reserve capacity

15Gerhard Knies, Taipei e-parl. + WFC 2008-03-1/2

Min. FIRM CAPACITY

PEAK LOAD

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2000 2010 2020 2030 2040 2050

Year

Ele

ctric

ity [

TW

h/y]

DesalinationExport SolarPhotovoltaicsWindGeothermalHydropowerBiomassWave / TidalCSP PlantsOil / GasCoalNuclear

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2000 2010 2020 2030 2040 2050

Year

Ele

ctric

ity [T

Wh/

y]

Import SolarPhotovoltaicsWindGeothermalHydropowerBiomassWave / TidalCSP PlantsOil GasCoalNuclear

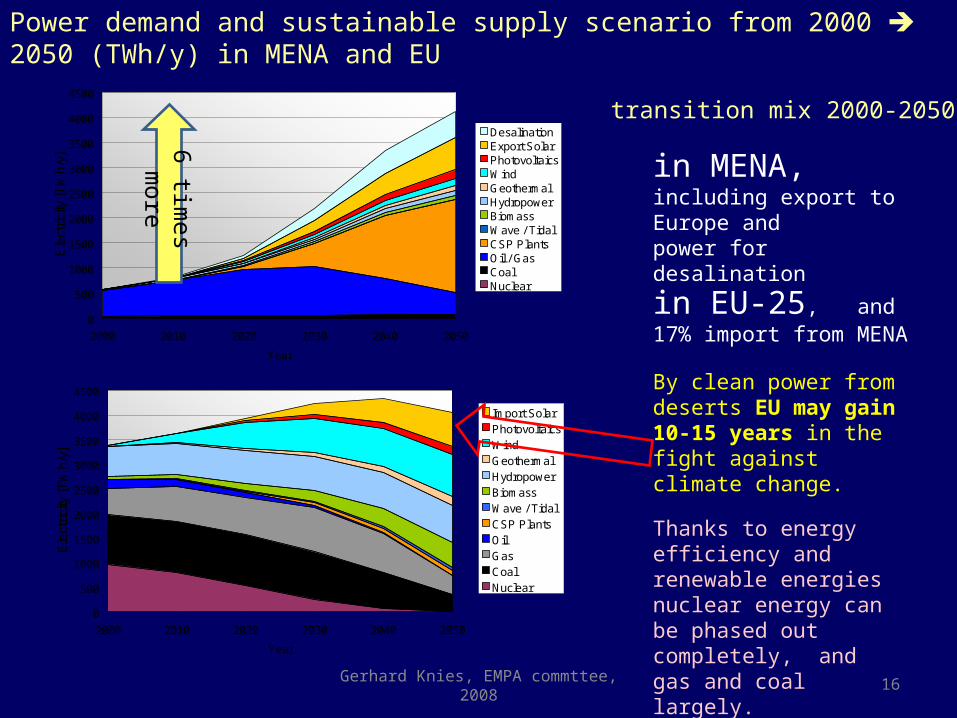

in MENA, including export to Europe and power for desalination

in EU-25, and17% import from MENA

By clean power from deserts EU may gain 10-15 years in the fight against climate change.

Thanks to energy efficiency and renewable energies nuclear energy can be phased out completely, andgas and coal largely.

Power demand and sustainable supply scenario from 2000 2050 (TWh/y) in MENA and EU

Gerhard Knies, EMPA commttee, 2008 16

transition mix 2000-2050

6 times m

ore

17

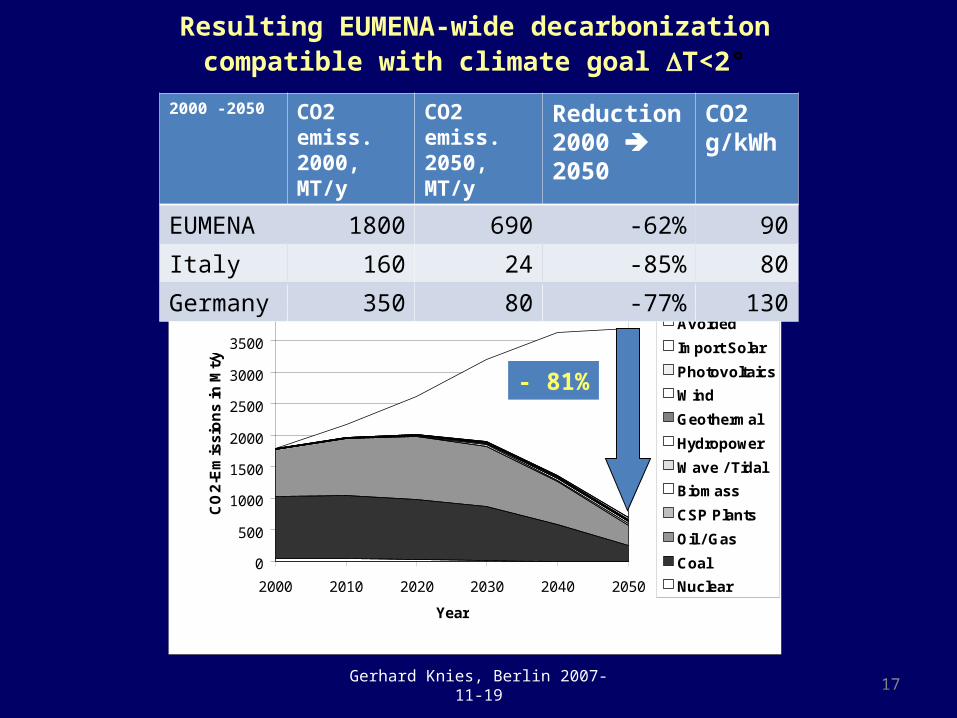

Resulting EUMENA-wide decarbonization compatible with climate goal T<2°

0

500

1000

1500

2000

2500

3000

3500

4000

2000 2010 2020 2030 2040 2050

Year

CO

2-E

mis

sio

ns

in

Mt/

y

Avoided

Import Solar

Photovoltaics

Wind

Geothermal

Hydropower

Wave / Tidal

Biomass

CSP Plants

Oil / Gas

Coal

Nuclear

- 81%

Gerhard Knies, Berlin 2007-11-19

2000 -2050 CO2 emiss.2000, MT/y

CO2 emiss.2050, MT/y

Reduction2000 2050

CO2 g/kWh

EUMENA 1800 690 -62% 90

Italy 160 24 -85% 80

Germany 350 80 -77% 130

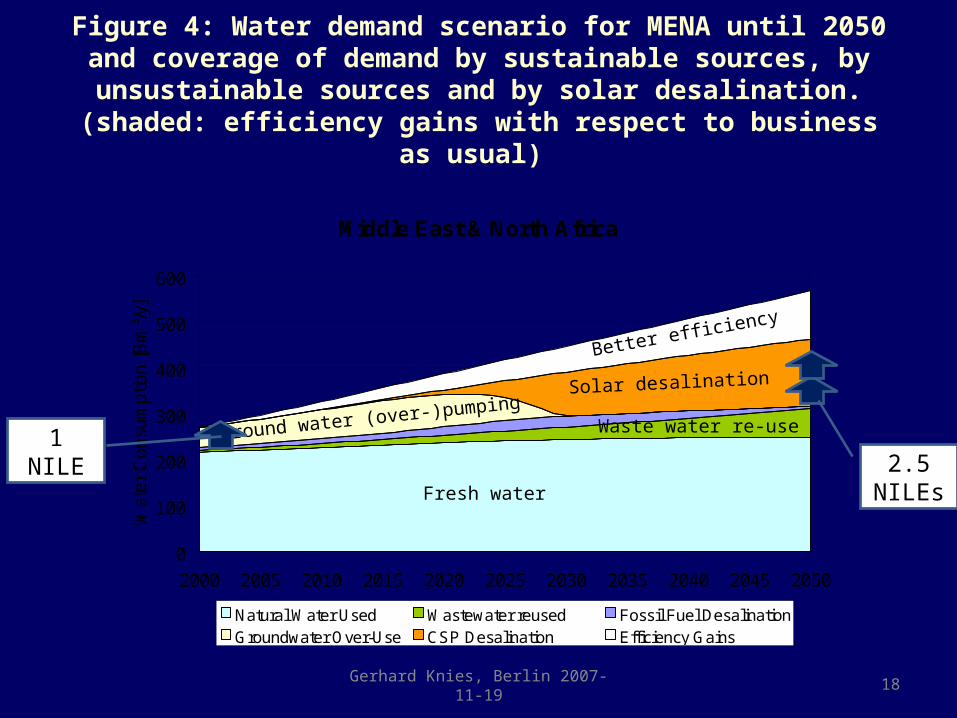

Figure 4: Water demand scenario for MENA until 2050 and coverage of demand by sustainable sources, by unsustainable sources and by solar

desalination. (shaded: efficiency gains with respect to business as usual)

Gerhard Knies, Berlin 2007-11-19 18

Middle East & North Africa

0

100

200

300

400

500

600

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

Wat

er C

onsu

mpt

ion

[Bm

³/y]

Natural Water Used Wastewater reused Fossil Fuel DesalinationGroundwater Over-Use CSP Desalination Efficiency Gains

Ground water (over-)pumpingSolar desalination

Waste water re-use

Fresh water

Better efficiency

2.5 NILEs

1 NILE

Gerhard Knies, CSP 2008 Barcelona 20

EU-MENA food+power symbiosis:Clean power export for virtual water import

Source: International Water Management Institute IWMI, January 2000, http://iwmi.org

Water scarcity:

red : physical scarcity

brown: economic scarcity

blue: little or no scarcity

Food insecurity: Striped countries have to import >10% of cerealsexport

clean power

importfood

(virtual water)

Mediterranean

Partnership

for

Energy & Food

Security

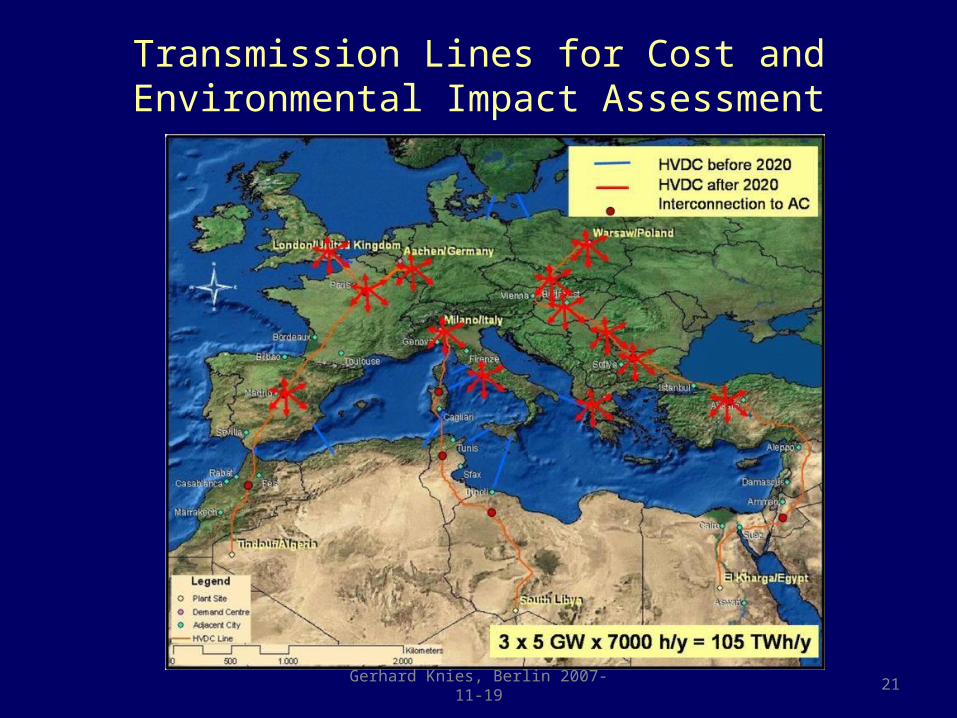

Transmission Lines for Cost and Environmental Impact Assessment

21Gerhard Knies, Berlin 2007-11-19

22

0.800.750.670.60Capacity Factor

350

45

245

31

143

20

42

5

Investment CSP

Billion € HVDC

0.040

0.010

0.040

0.010

0.045

0.010

0.050

0.014

Elec. Cost CSP

€/kWh HVDC

50 x 503600 x 1.0

40 x 403600 x 0.7

30 x 303600 x 0.4

15 x 153100 x 0.1

Land Area CSP

km x km HVDC

352412.53.8Turnover Billion €/y

70047023060Electricity Transfer TWh/y

20 x 514 x 58 x 52 x 5Transfer Capacity GW

2050204020302020Year

0.800.750.670.60Capacity Factor

350

45

245

31

143

20

42

5

Investment CSP

Billion € HVDC

0.040

0.010

0.040

0.010

0.045

0.010

0.050

0.014

Elec. Cost CSP

€/kWh HVDC

50 x 503600 x 1.0

40 x 403600 x 0.7

30 x 303600 x 0.4

15 x 153100 x 0.1

Land Area CSP

km x km HVDC

352412.53.8Turnover Billion €/y

70047023060Electricity Transfer TWh/y

20 x 514 x 58 x 52 x 5Transfer Capacity GW

2050204020302020Year

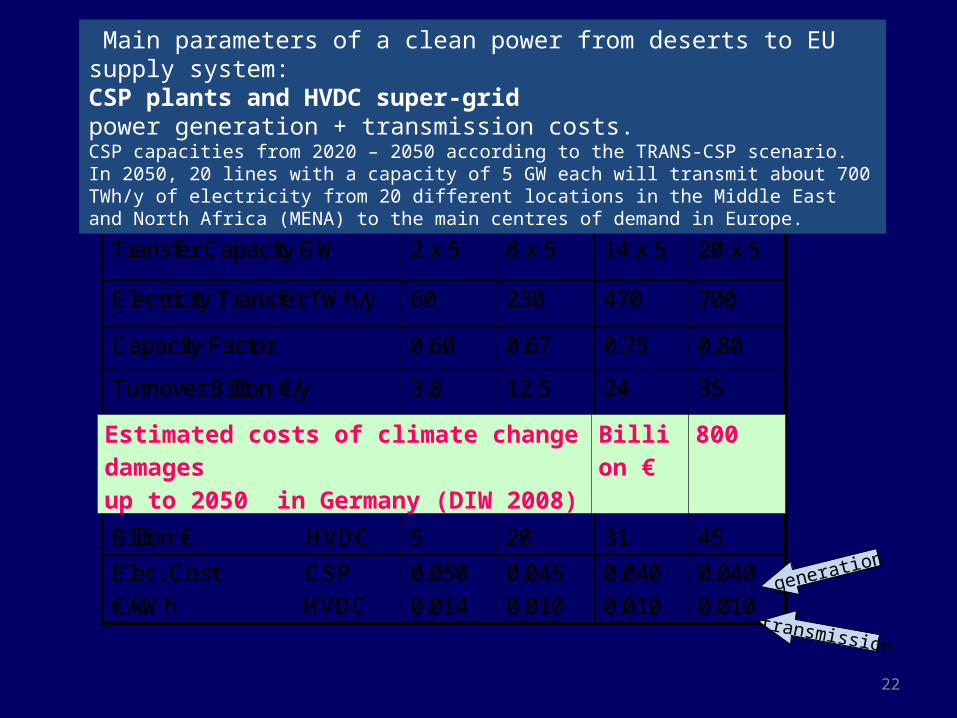

Main parameters of a clean power from deserts to EU supply system:CSP plants and HVDC super-grid power generation + transmission costs.CSP capacities from 2020 – 2050 according to the TRANS-CSP scenario. In 2050, 20 lines with a capacity of 5 GW each will transmit about 700 TWh/y of electricity from 20 different locations in the Middle East and North Africa (MENA) to the main centres of demand in Europe.

transmission

generation

Estimated costs of climate change damages up to 2050 in Germany (DIW 2008)

Billion € 800

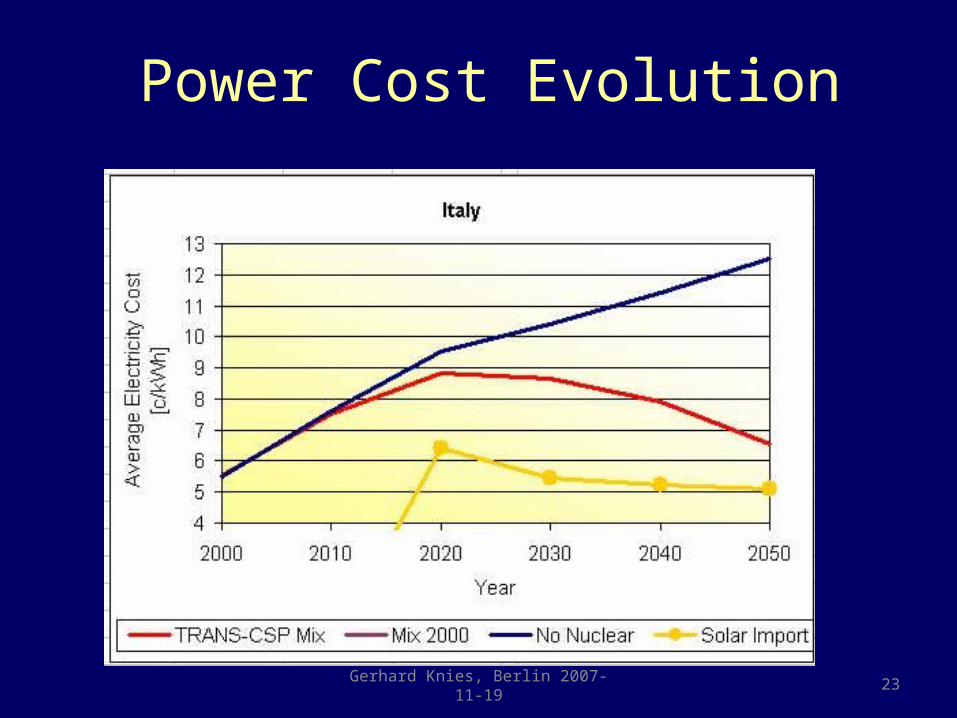

Power Cost Evolution

23Gerhard Knies, Berlin 2007-11-19

Gerhard Knies, EMPA commttee, 2008

Power Cost Development

24

Solar power from deserts can limit power cost escalation in Germany

Clean Power from Deserts for the World!

3000 km

Gerhard Knies, Taipei e-parl. + WFC 2008-03-1/2 25

More than 90% of world pop could be servedby clean power from deserts (DESERTEC) !

world electricity demand of

18,000 TWh/y (in 2005)

300 x 300 km²

=0.23% of all deserts

In 2050: ~50,000 TWh/y

500 x 500 km²

Gerhard Knies, CSP 2008 Barcelona

Forum1000 Solar Gigawatt

.

Forum10 000 Solar Gigawatt

At Hanover Industrial Fair,

23.-24. April 2008, Germany

Topics:

1.CSP Technology

2.DESERTEC: 10 000 Solar Gigawatt from deserts - how?

more: www.desertec.org 26

DESERTEC SUMMARY:• Deserts, with solar-thermal and wind power plants and with HVDC

transmission grids, can supply clean power to over 90% of world population.

• Up to 2050 the world’s power system can be largely decarbonized T < 2°) with the help of clean power from global deserts

• 2050: EU-MENA region with 1.5 bn people:

– Example for the global problem and how it can be solved

– Collectors for 1,500 Solar Gigawatts and 600 GW power capacity

– Power&water supply can be secured by “powerhouse desert”

• 2050: MENA supply to EU: – Union for the Mediterranean - the political facilitator for DESERTEC ?

– Solar: 100 GW and 700 TWh/y (17% of expected EU-consumption)– Investments: CSP=350 bn Euro, HVDC=45 bn Euro

– Wind : 120 GW and 360 TWh/y generation (coarse guess)– Investments: 100 bn Euro, HVDC=30 bn Euro (coarse guess)

• Cost of clean energy system ~ 1% of climate change damageGerhard Knies, Berlin 2007-11-19 27

Gerhard Knies, Berlin 2007-11-19 28

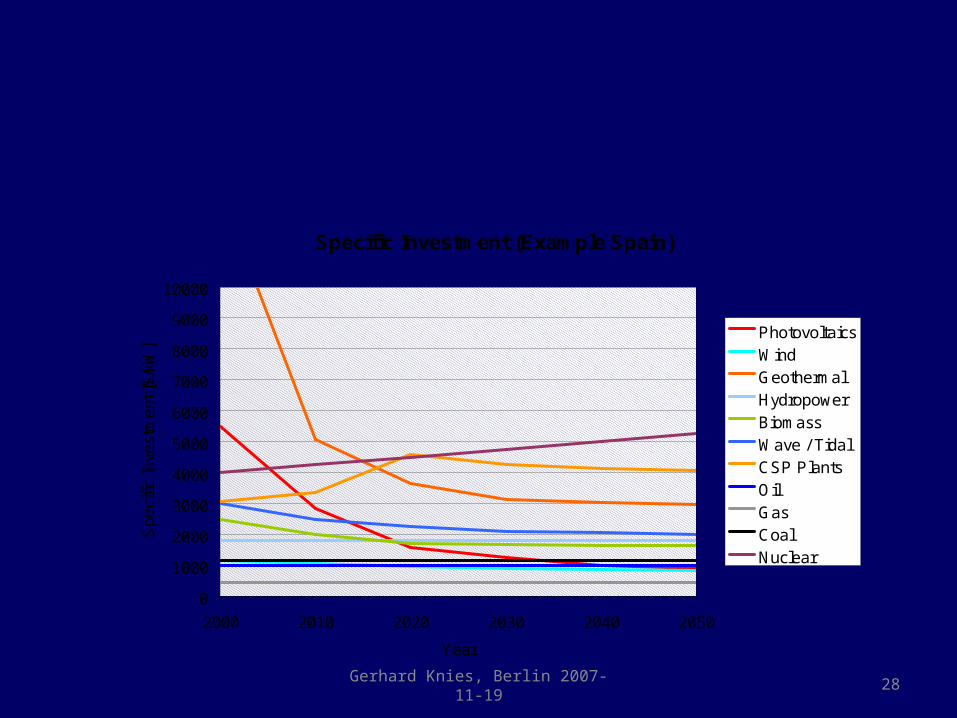

Specific Investment (Example Spain)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2000 2010 2020 2030 2040 2050

Year

Spe

cific

Inv

estm

ent [

$/kW

]

PhotovoltaicsWindGeothermalHydropowerBiomassWave / TidalCSP PlantsOil GasCoalNuclear

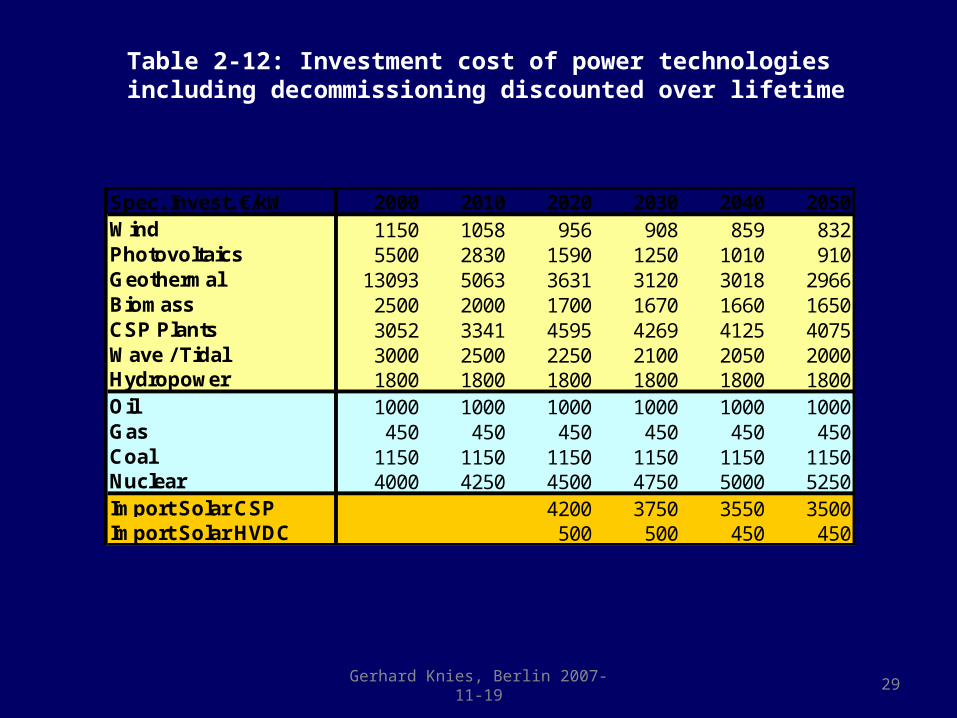

Table 2‑12: Investment cost of power technologies including decommissioning discounted over lifetime

Gerhard Knies, Berlin 2007-11-19 29

Spec. Invest. €/kW 2000 2010 2020 2030 2040 2050Wind 1150 1058 956 908 859 832Photovoltaics 5500 2830 1590 1250 1010 910Geothermal 13093 5063 3631 3120 3018 2966Biomass 2500 2000 1700 1670 1660 1650CSP Plants 3052 3341 4595 4269 4125 4075Wave / Tidal 3000 2500 2250 2100 2050 2000Hydropower 1800 1800 1800 1800 1800 1800Oil 1000 1000 1000 1000 1000 1000Gas 450 450 450 450 450 450Coal 1150 1150 1150 1150 1150 1150Nuclear 4000 4250 4500 4750 5000 5250Import Solar CSP 4200 3750 3550 3500Import Solar HVDC 500 500 450 450

Table 2‑13: Development of the electricity cost of new plants of different power technologies in the example of Spain on the basis of the investment cost development in Table 2‑12 and the different performance indicators representing each technology in each country following the TRANS-CSP scenario until 2050. From 2030 onwards, biomass, geothermal and CSP plants subsequently take over peaking duties, which is the reason for their cost elevation.

Gerhard Knies, Berlin 2007-11-19 30

Electricity Cost c/kWh 2000 2010 2020 2030 2040 2050Wind 7,7 6,8 6,1 5,8 5,4 5,2Photovoltaics 36,7 16,9 8,6 6,6 5,3 4,8Geothermal 17,5 6,8 4,8 4,8 5,5 5,9Biomass 6,1 4,9 4,3 4,2 4,7 5,2CSP Plants 17,6 12,2 7,5 6,7 6,2 6,6Wave / Tidal 8,3 6,9 6,2 5,8 5,6 5,5Hydropower 8,4 8,4 8,4 8,4 8,4 8,4Oil 8,1 12,2 15,0 16,4 17,8 19,6Gas 4,7 7,0 9,9 11,5 12,4 13,7Coal 3,3 4,0 5,6 5,7 5,8 6,0Nuclear 3,6 3,9 4,1 4,4 4,6 4,9Solar Import Electricity 5,4 4,8 4,6 4,9TRANS-CSP Average 4,8 5,9 6,9 6,7 6,8 6,6Electricity Mix 2000 4,8 5,7 6,8 7,2 7,6 8,0

Table 2 14: Technologies and range of required ‑revenues in the different electricity market segments

Gerhard Knies, Berlin 2007-11-19 31

Segment Source / Technology Min. Rev. Max. Rev.ct/kWh ct/kWh

Pump Hydro StorageFuel OilGas TurbineBiomassGeothermalCSPCoal Gas Combined CycleCSPBiomassGeothermalCoal LigniteNuclearRiver Run-OffGas Combined CycleCo-generationWindPhotovoltaicsCSPGeothermal

Base Load 3 6

10 25Peak Power

Intermediate Power

5 12