Embed Size (px)

Citation preview

Group 6: Xi Liu, Shulei Yuan, Cian Shalloe, Kevin

McSweeney & Ciara Ronayne

“In theory, hedging should help companies protect themselves against unexpected moves in exchange rates….In practice, however, results vary depending on the design, execution and timeliness of hedging strategies.”

Didier Cossin and Dinos Constantinou“Hedging your bets to protect against risk”Ft.com (April 6, 2006)

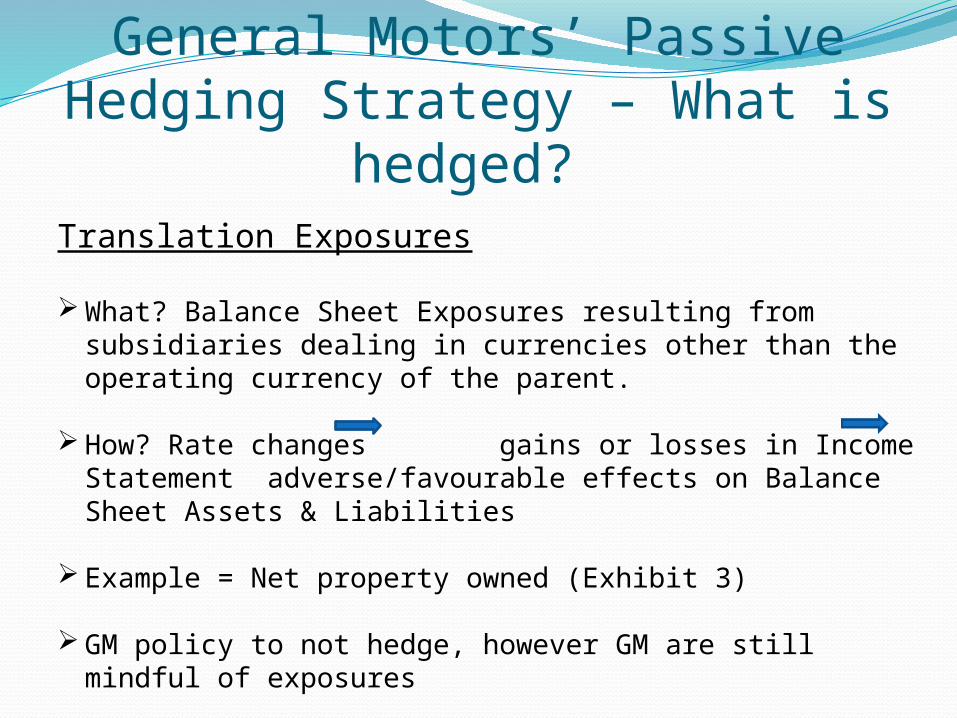

General Motors’ Passive Hedging Strategy – What is hedged?

Translation Exposures

What? Balance Sheet Exposures resulting from subsidiaries dealing in currencies other than the operating currency of the parent.

How? Rate changes gains or losses in Income Statement adverse/favourable effects on Balance Sheet Assets & Liabilities

Example = Net property owned (Exhibit 3)

GM policy to not hedge, however GM are still mindful of exposures

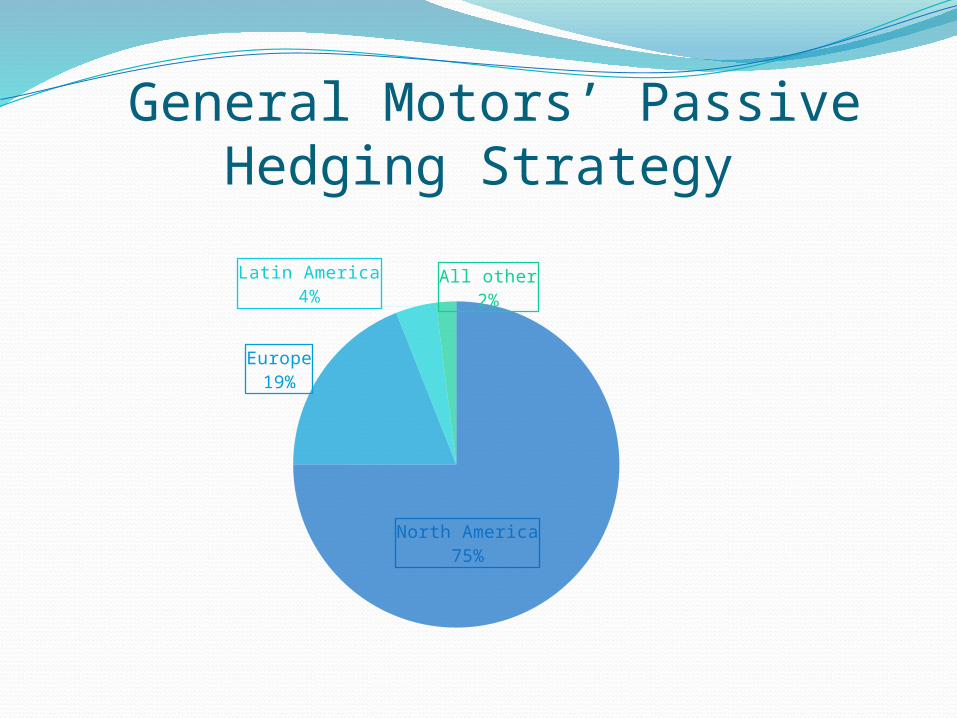

General Motors’ Passive Hedging Strategy

North America75%

Europe19%

Latin America4%

All other2%

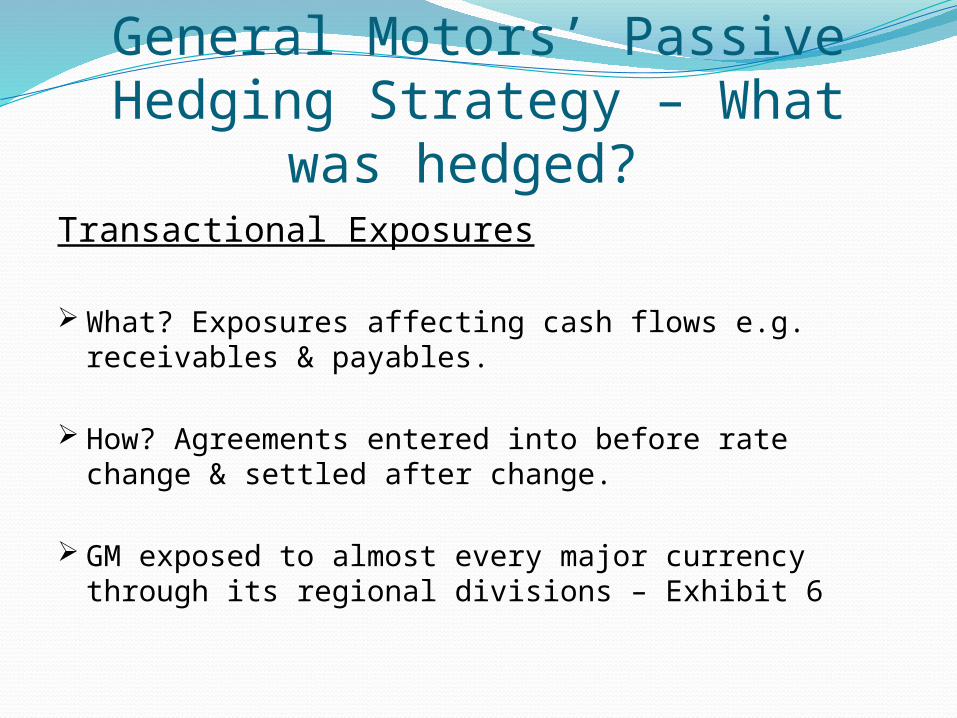

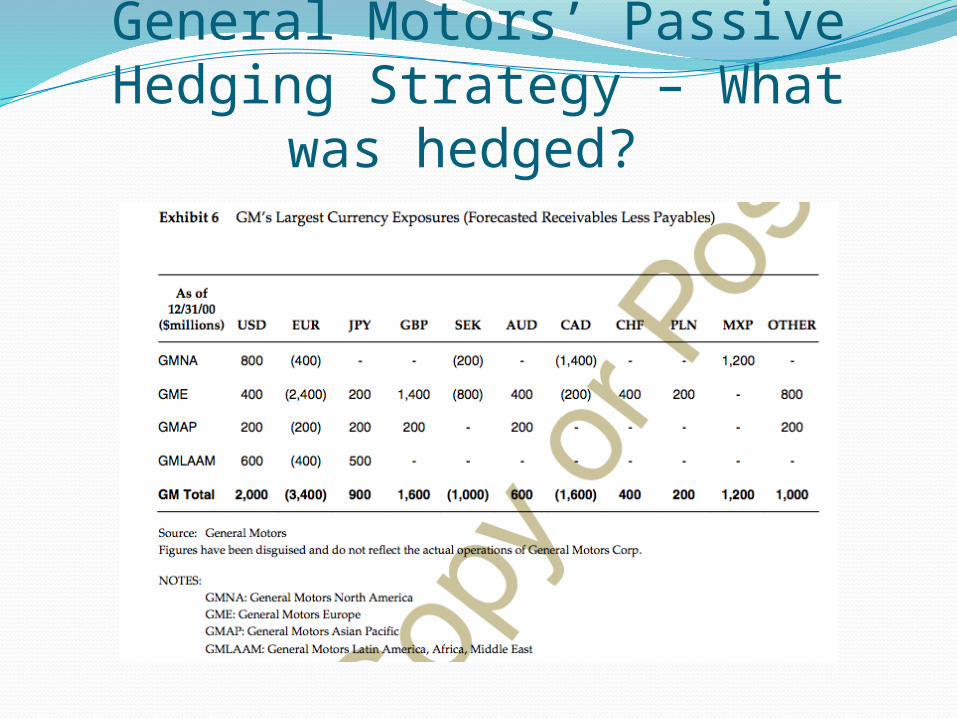

General Motors’ Passive Hedging Strategy – What was hedged?

Transactional Exposures

What? Exposures affecting cash flows e.g. receivables & payables.

How? Agreements entered into before rate change & settled after change.

GM exposed to almost every major currency through its regional divisions – Exhibit 6

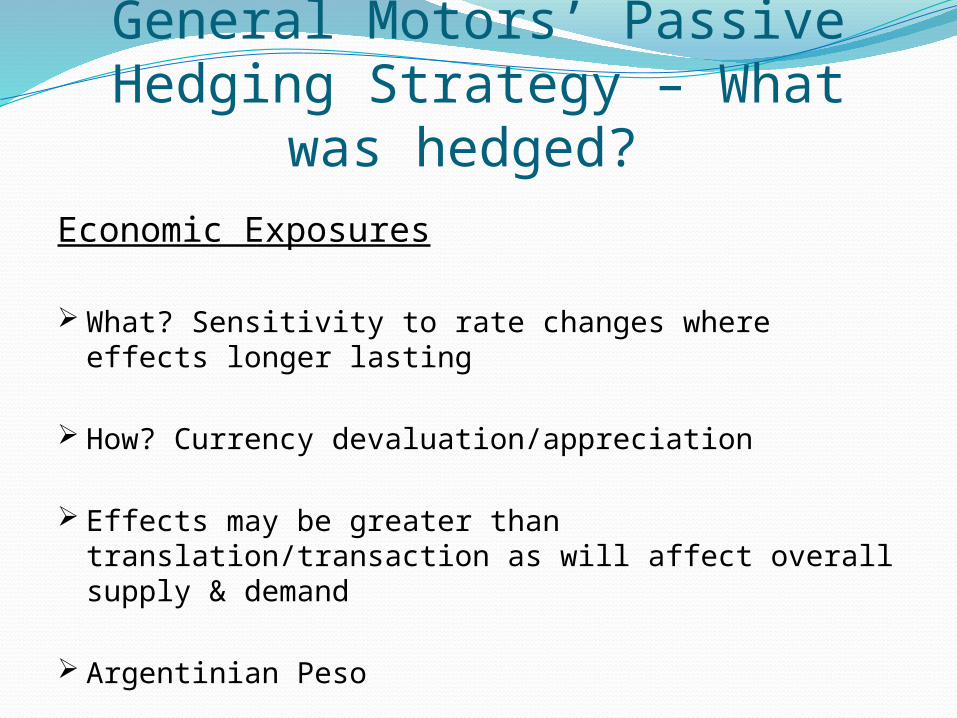

General Motors’ Passive Hedging Strategy – What was hedged?

General Motors’ Passive Hedging Strategy – What was hedged?

Economic Exposures

What? Sensitivity to rate changes where effects longer lasting

How? Currency devaluation/appreciation

Effects may be greater than translation/transaction as will affect overall supply & demand

Argentinian Peso

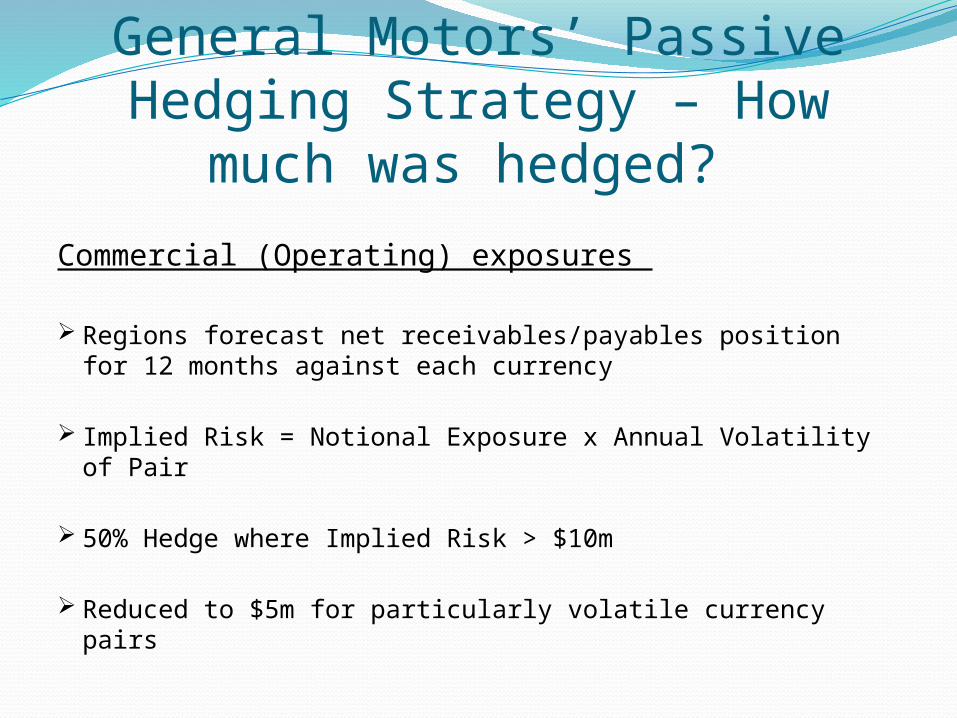

General Motors’ Passive Hedging Strategy – How much was hedged?

Commercial (Operating) exposures

Regions forecast net receivables/payables position for 12 months against each currency

Implied Risk = Notional Exposure x Annual Volatility of Pair

50% Hedge where Implied Risk > $10m

Reduced to $5m for particularly volatile currency pairs

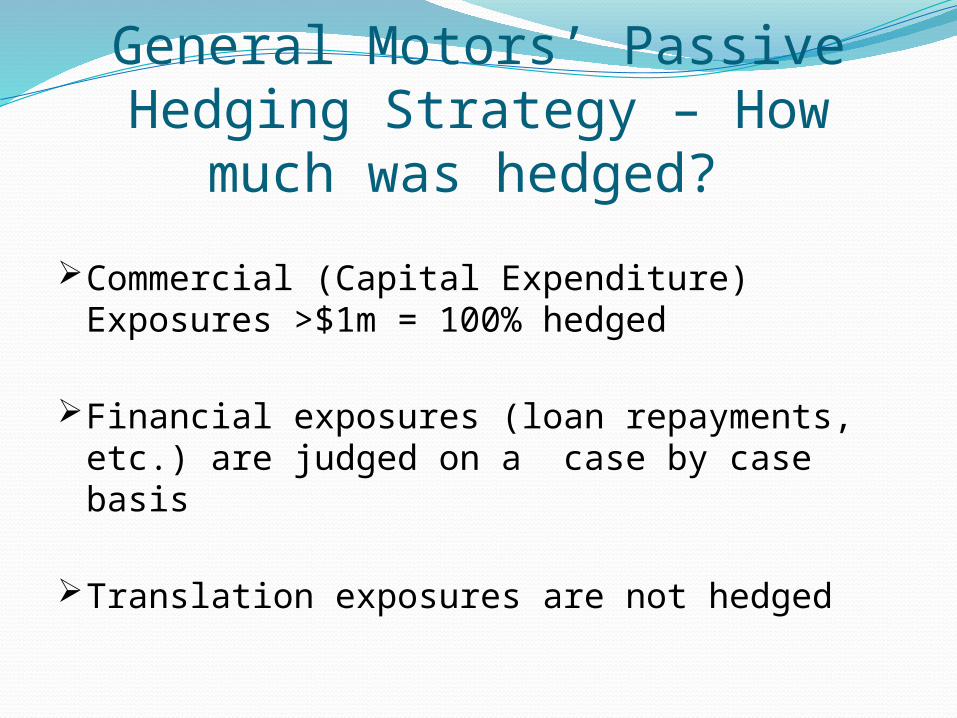

General Motors’ Passive Hedging Strategy – How much was hedged?

Commercial (Capital Expenditure) Exposures >$1m = 100% hedged

Financial exposures (loan repayments, etc.) are judged on a case by case basis

Translation exposures are not hedged

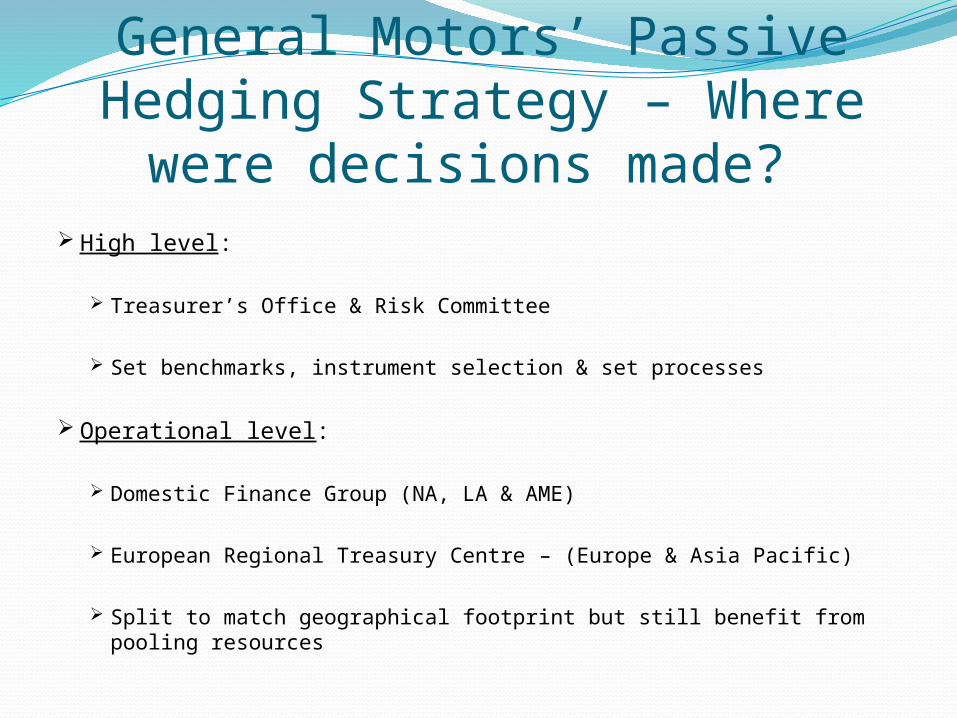

General Motors’ Passive Hedging Strategy – Where were decisions made? High level:

Treasurer’s Office & Risk Committee

Set benchmarks, instrument selection & set processes

Operational level:

Domestic Finance Group (NA, LA & AME)

European Regional Treasury Centre – (Europe & Asia Pacific)

Split to match geographical footprint but still benefit from pooling resources

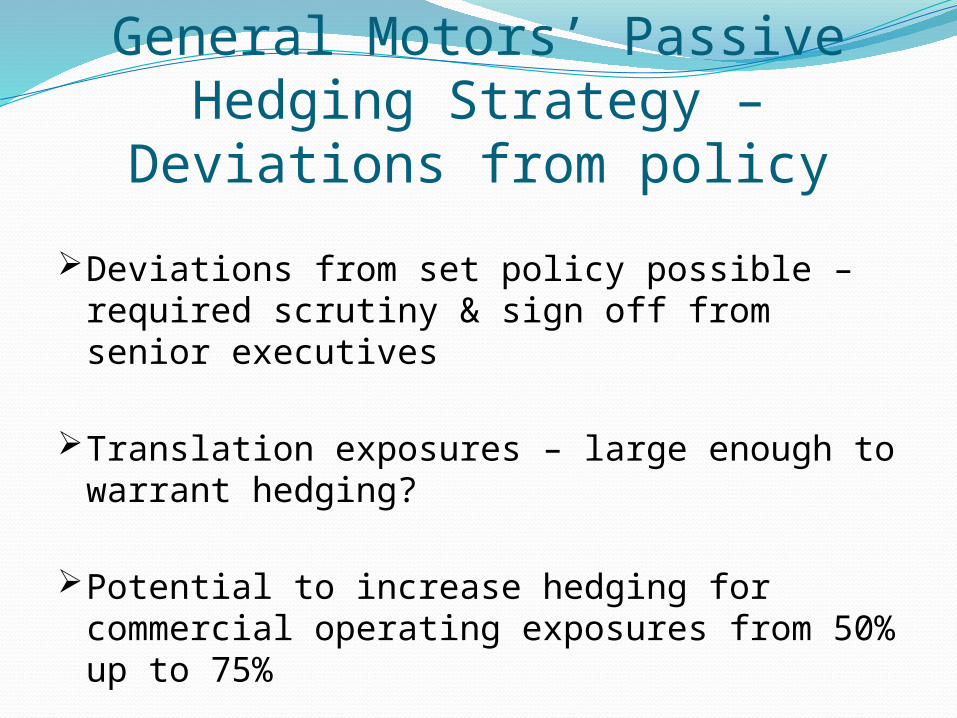

General Motors’ Passive Hedging Strategy – Deviations from policy

Deviations from set policy possible – required scrutiny & sign off from senior executives

Translation exposures – large enough to warrant hedging?

Potential to increase hedging for commercial operating exposures from 50% up to 75%

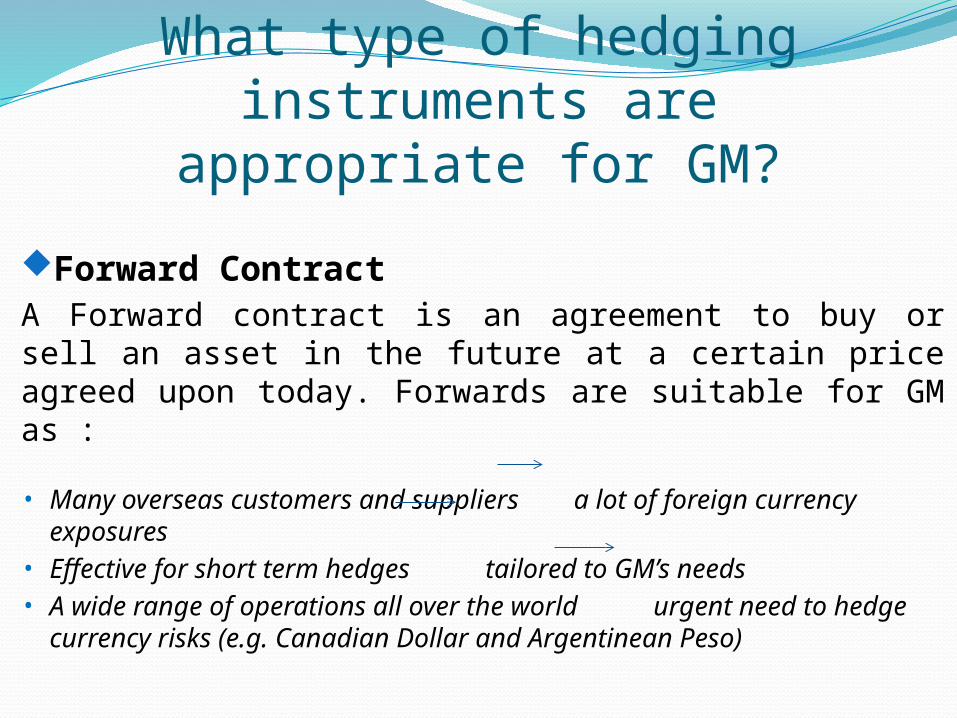

What type of hedging instruments are appropriate for GM?

Forward ContractA Forward contract is an agreement to buy or sell an asset in the future at a certain price agreed upon today. Forwards are suitable for GM as :

• Many overseas customers and suppliers a lot of foreign currency exposures

• Effective for short term hedges tailored to GM’s needs• A wide range of operations all over the world urgent need

to hedge currency risks (e.g. Canadian Dollar and Argentinean Peso)

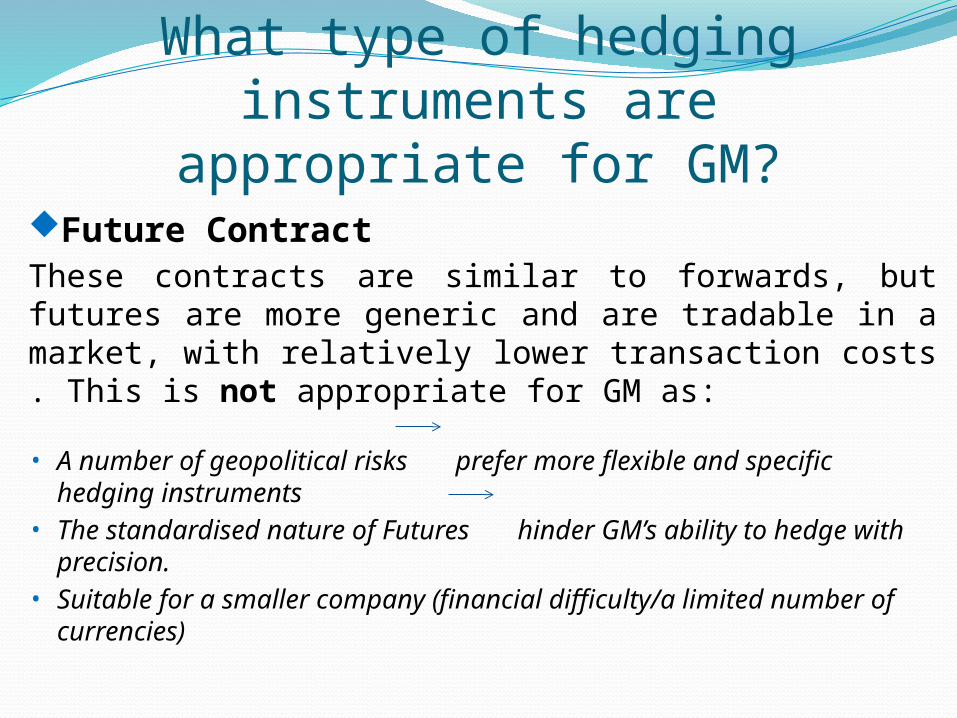

What type of hedging instruments are appropriate for GM?

Future ContractThese contracts are similar to forwards, but futures are more generic and are tradable in a market, with relatively lower transaction costs . This is not appropriate for GM as:

• A number of geopolitical risks prefer more flexible and specific hedging instruments

• The standardised nature of Futures hinder GM’s ability to hedge with precision.

• Suitable for a smaller company (financial difficulty/a limited number of currencies)

What type of hedging instruments are appropriate for GM?

Option ContractThis type of contract gives the holder the right, but not the obligation, to buy (call) or sell (put) a given quantity of an asset in the future, at prices agreed upon today. This type of Instrument is suitable for GM as :

• GM can choose whether to buy: -A tailor-made currency option specific needs, more expensive. -A standard option exercise the option at any point/sell the option• A great deal of uncertainty about future spot rates foreign

currency receipts and payments more flexibility around long term hedging strategies.

What type of hedging instruments are appropriate for GM?

Swap ContractThis is a formal agreement whereby two organisations contractually agree to exchange payments on different terms. This can possibly be another appropriate instrument for GM to use as:

• Can provide hedging for longer periods than the forward market• Easy to arrange and flexible • Transaction costs are low (only legal fees, no commission or

premium)• Obtain the currency they require , with avoiding uncertainties • Unfortunately, a high degree of counterparty risk can be present

Should the same instruments be used in all situations?

Not all of these strategies are suitable to use for the same situation

Factors that need to be considered for choosing a suitable hedging strategy include :• The cost of implementing a hedge, • The degree of flexibility• The duration of the hedge

Different strategies are suitable for different conditions (Prudence)

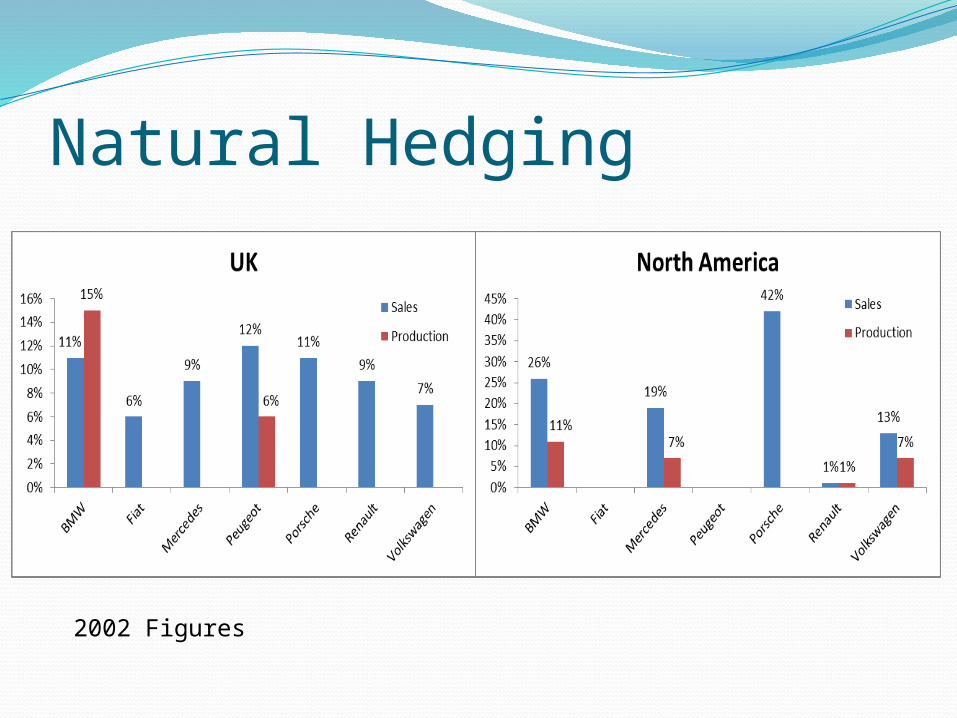

Natural Hedging

2002 Figures

Natural Hedging

DaimlerForeign Exchange Committee manages

exchange rate risk

80% exposure hedged

Mixture of forwards & options

Assessment of market conditions.

Porsche‘92/93 – 38% drop in sales

Aggressive hedging strategy

100% exposure hedged

Rolling put options

BMW

GM’s Exposure to the Canadian Dollar

What is the extent of GM’s exposure to the CAD?

C$1.682bn negative cash flow exposure resulting from Canadian Operations

C$2.143bn net liability exposure on GM-Canada’s Balance Sheet

GM are concerned that the CAD will appreciate

How much is at risk?Using the Implied Risk Function;

Implied Risk = Regional Notional Exposure x Annual Volatility of Relevant Currency Pair

Annual Intraday USD/CAD Volatility of 0.53% for 2001CAD$1.682bn x 0.53% Annual Average Intraday Volatility for 2001 =

C$89,146,000

Low volatility due to high interdependence between USA and Canada

GM feels that a higher amount than this needed to be hedged

What Hedging Instruments are available to GM in this case?

Forwards and Options currently usedForwards for short term hedgingOptions for longer term hedging

Cost differences and volatility are major factors

Forwards and Options give more flexibility than Futures

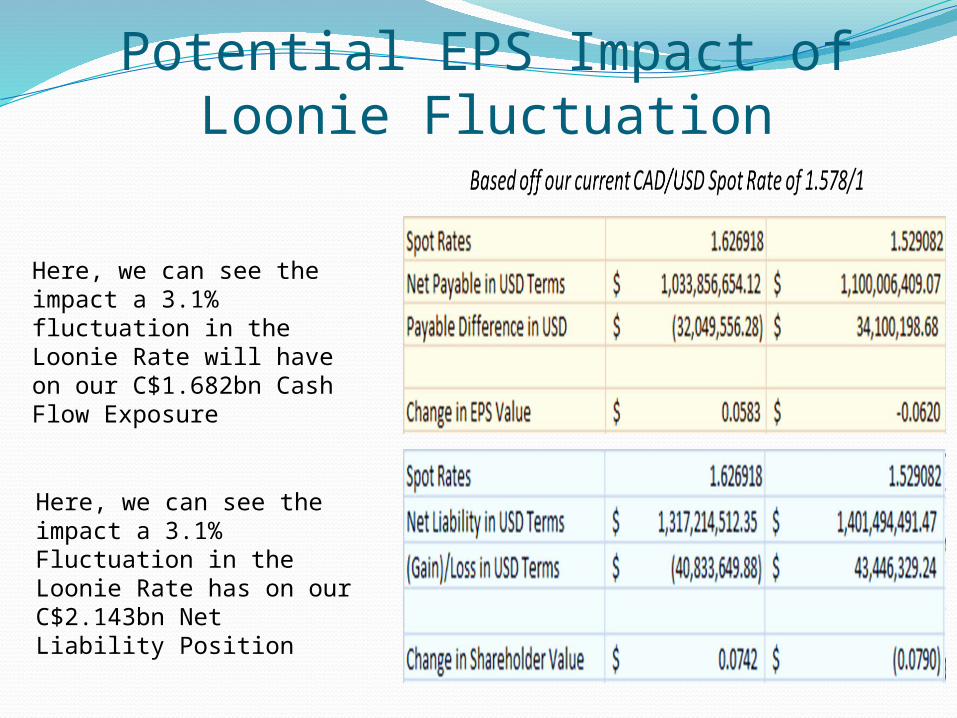

Potential EPS Impact of Loonie Fluctuation

Here, we can see the impact a 3.1% fluctuation in the Loonie Rate will have on our C$1.682bn Cash Flow Exposure

Here, we can see the impact a 3.1% Fluctuation in the Loonie Rate has on our C$2.143bn Net Liability Position

How much should be hedged?

External Factors must be considered

Reduced Earnings Volatility a goal of Treasury Department

75% Hedging Strategy compliments this goal

Prudent in the face of increased macroeconomic risks

What should GM do?

Options create more value than Forwards if a depreciation occurs

Forwards create more value than Options if appreciation occurs

75% Hedge Strategy reduces volatility

In Reality, a mixture of both may be best course of action

Close analysis of factors surrounding rate fluctuations is essential

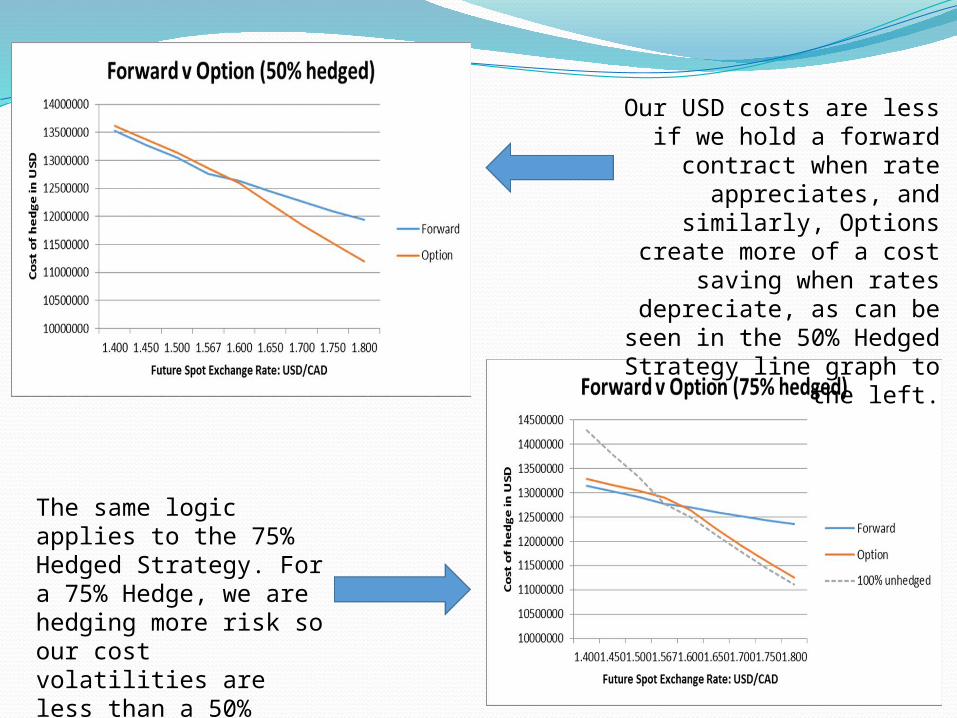

Our USD costs are less if we hold a forward contract when rate appreciates, and

similarly, Options create more of a cost saving when rates depreciate, as can be

seen in the 50% Hedged Strategy line graph to the

left.

The same logic applies to the 75% Hedged Strategy. For a 75% Hedge, we are hedging more risk so our cost volatilities are less than a 50% Hedge.

Questions?