Embed Size (px)

Citation preview

110 North Wacker DriveChicago, Illinois 60606(312) 960-5000

www.generalgrowth.com

places∑reat∑a¬h∏rin∑

Financial Highlights liftCompany Profile liftShareholders Letter 2Retail Portfolio 13Following Portfolio Form 10-K Directors/Officers Corporate Information

con¸nts

2005 annual reportGeneral Growth Properties

2005 annual reportG

enera

l Gro

wth

Pro

perties

shop,...plac∏s ¬Ω

play,∏xp∏rıence!and

Financial Highlights liftCompany Profile liftShareholders Letter 2Retail Portfolio 13Following Portfolio Form 10-K Directors/Officers Corporate Information

con¸nts

designed by Conyers Design, Inc. illustrations by Tom Rosborough

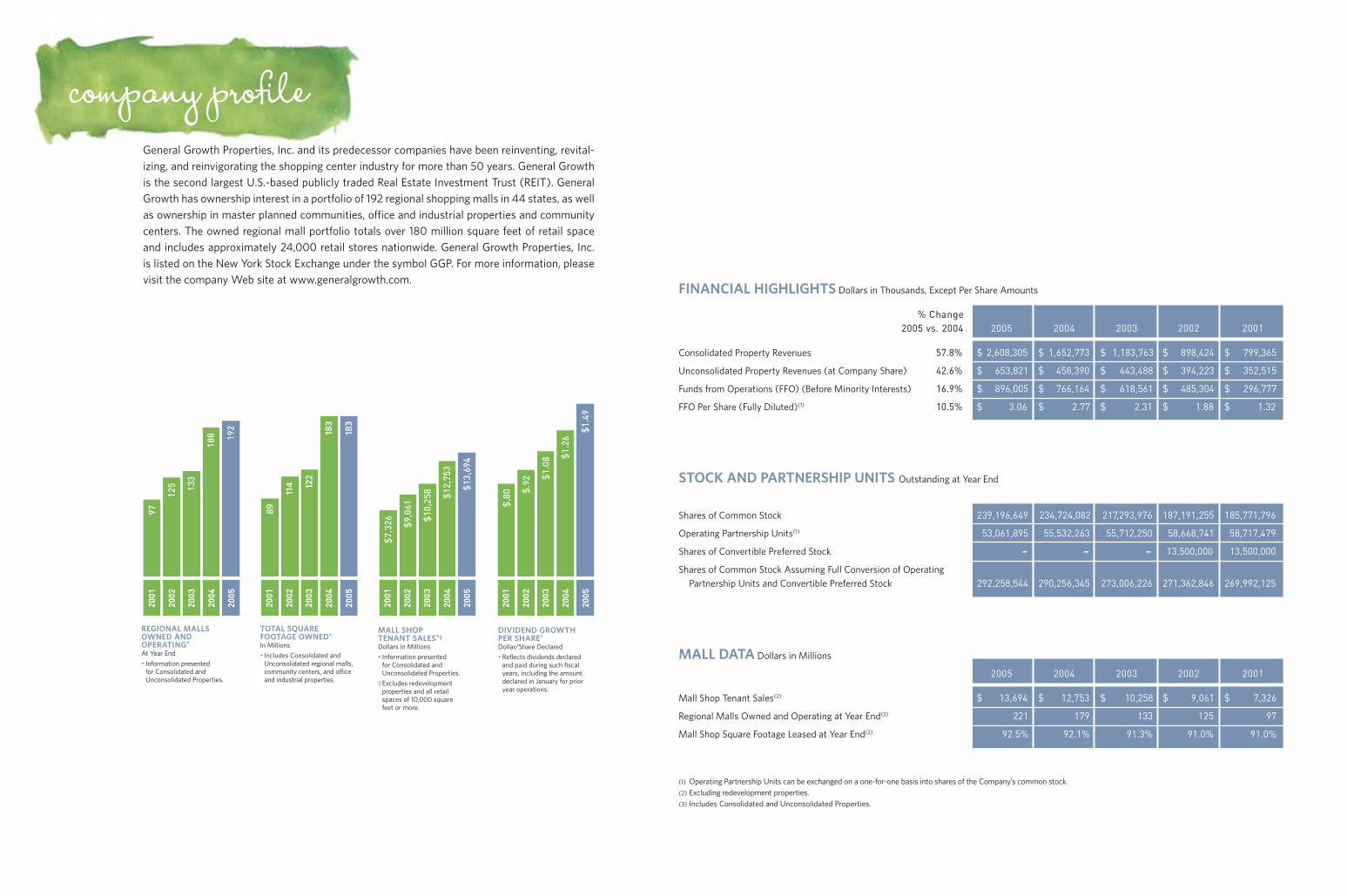

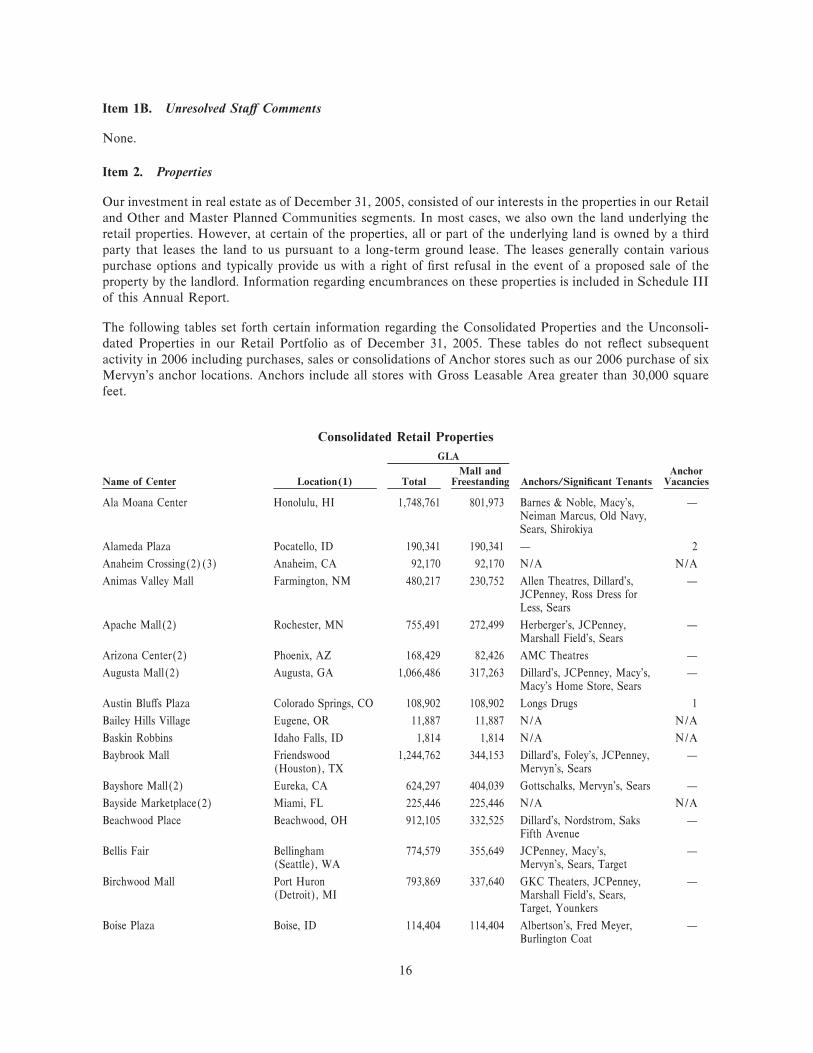

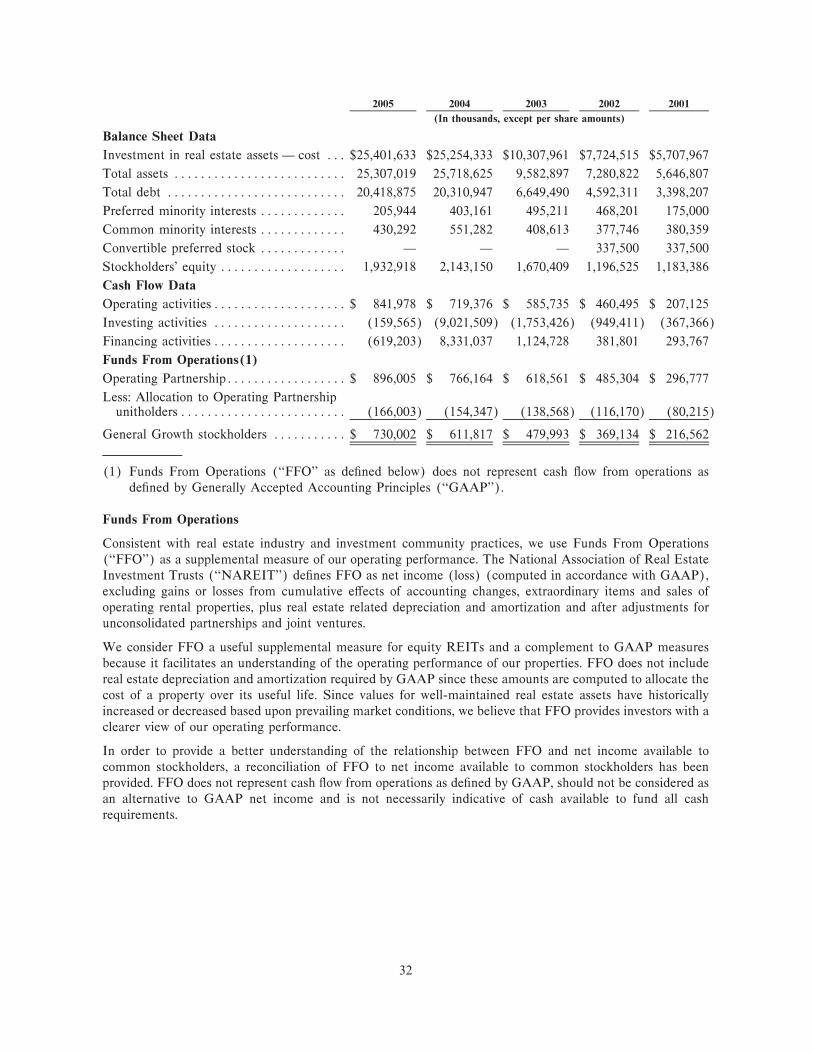

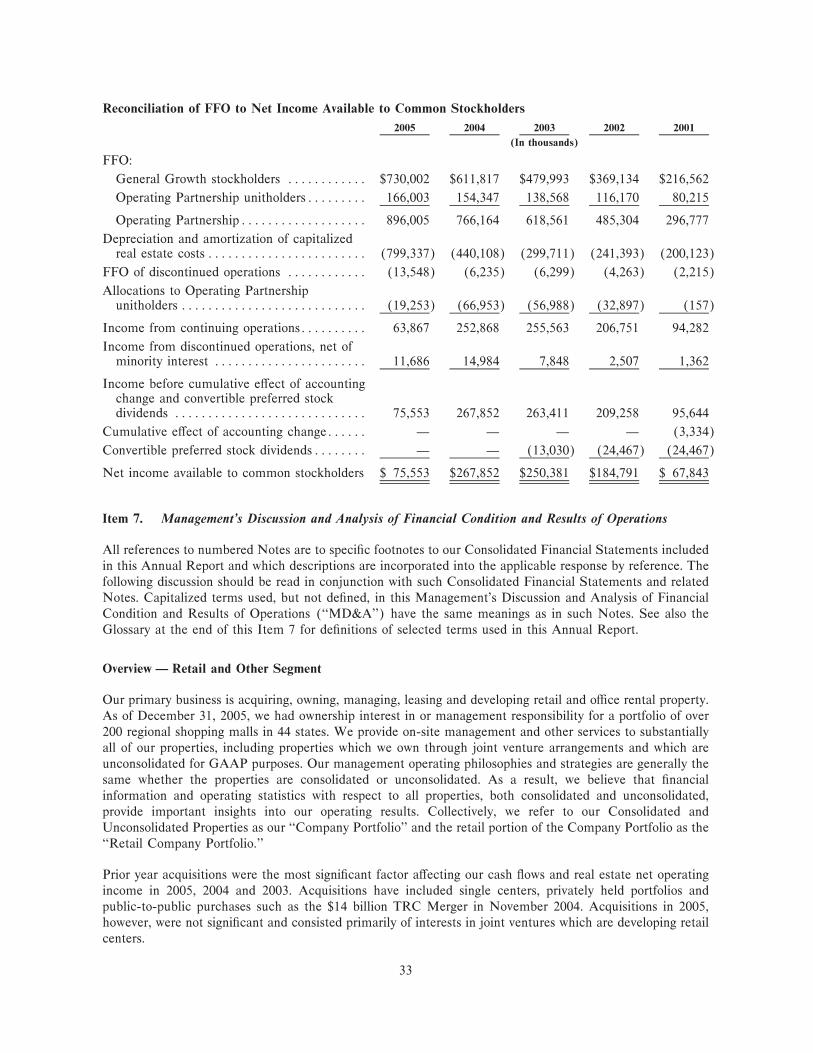

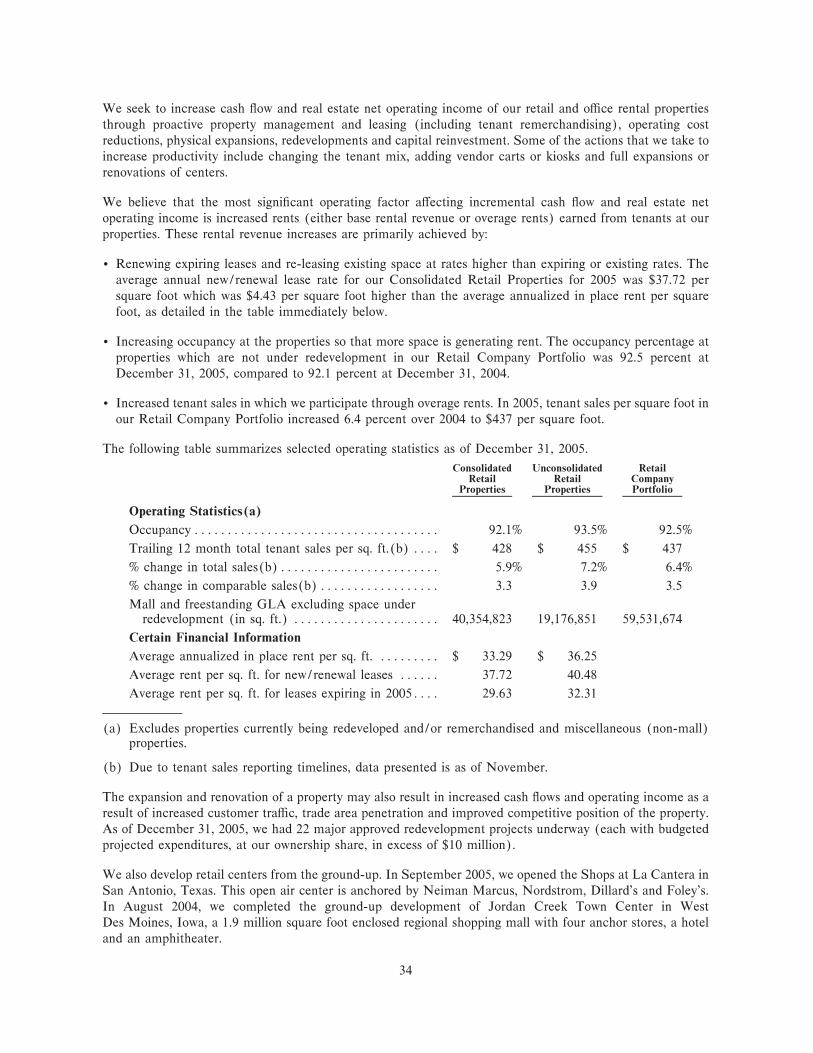

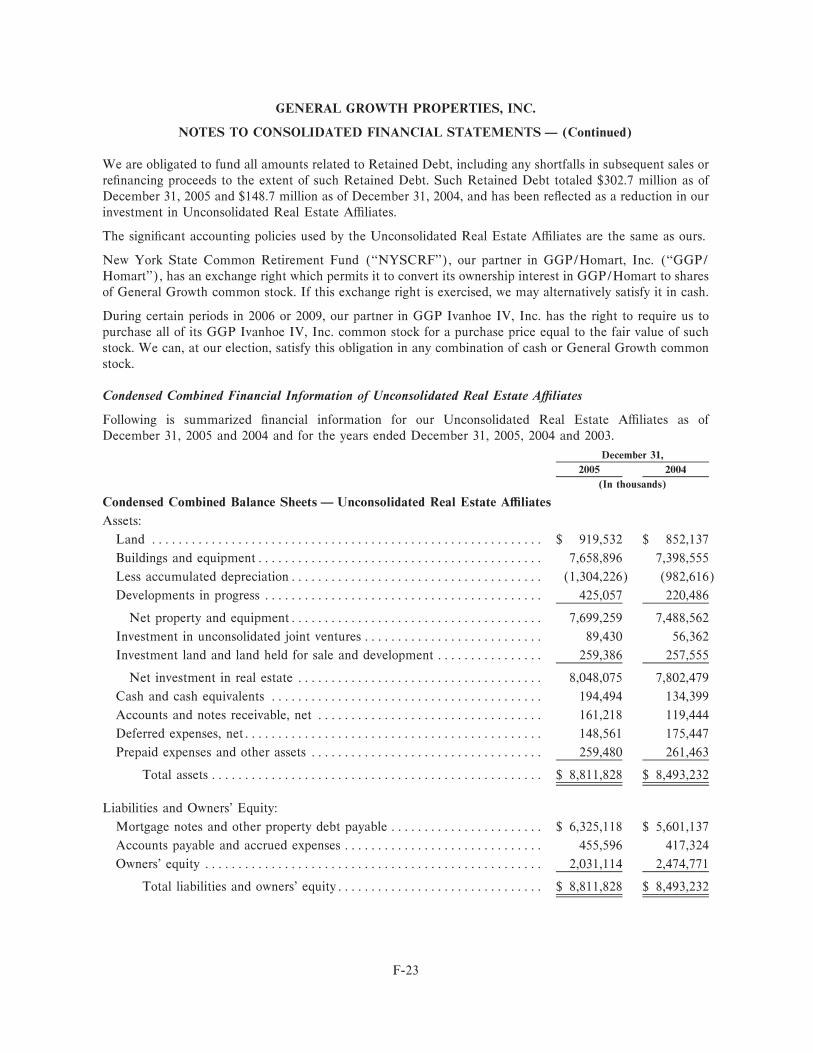

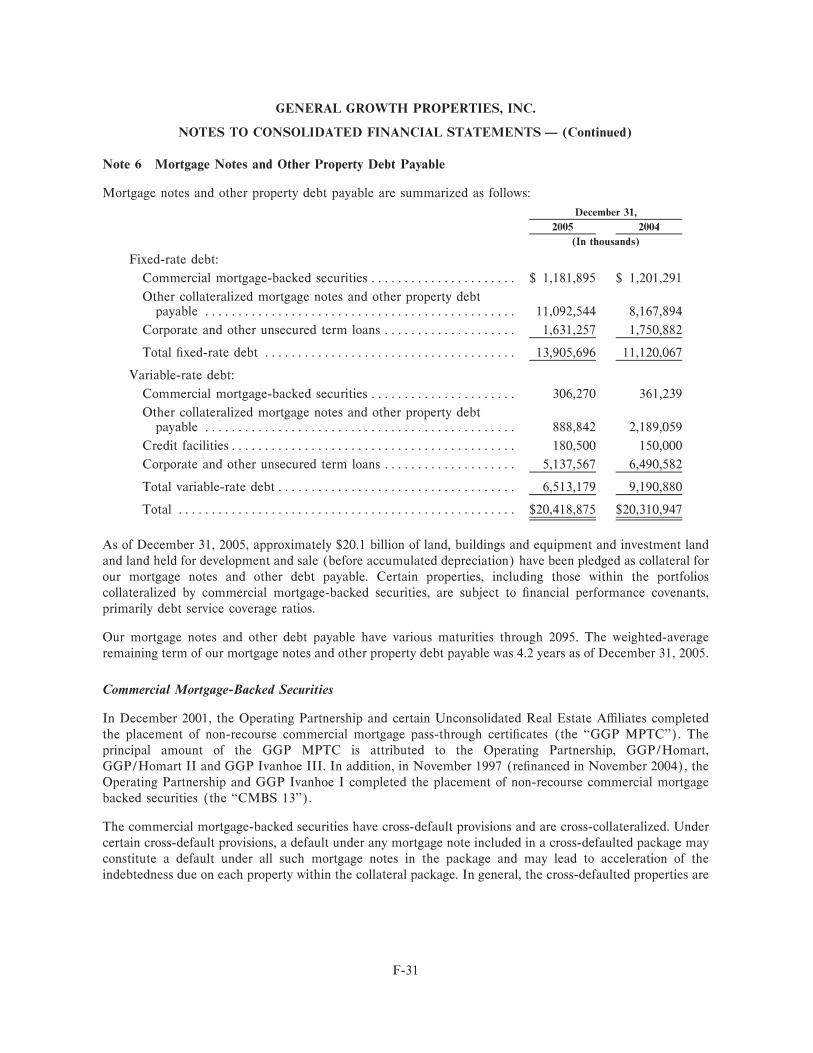

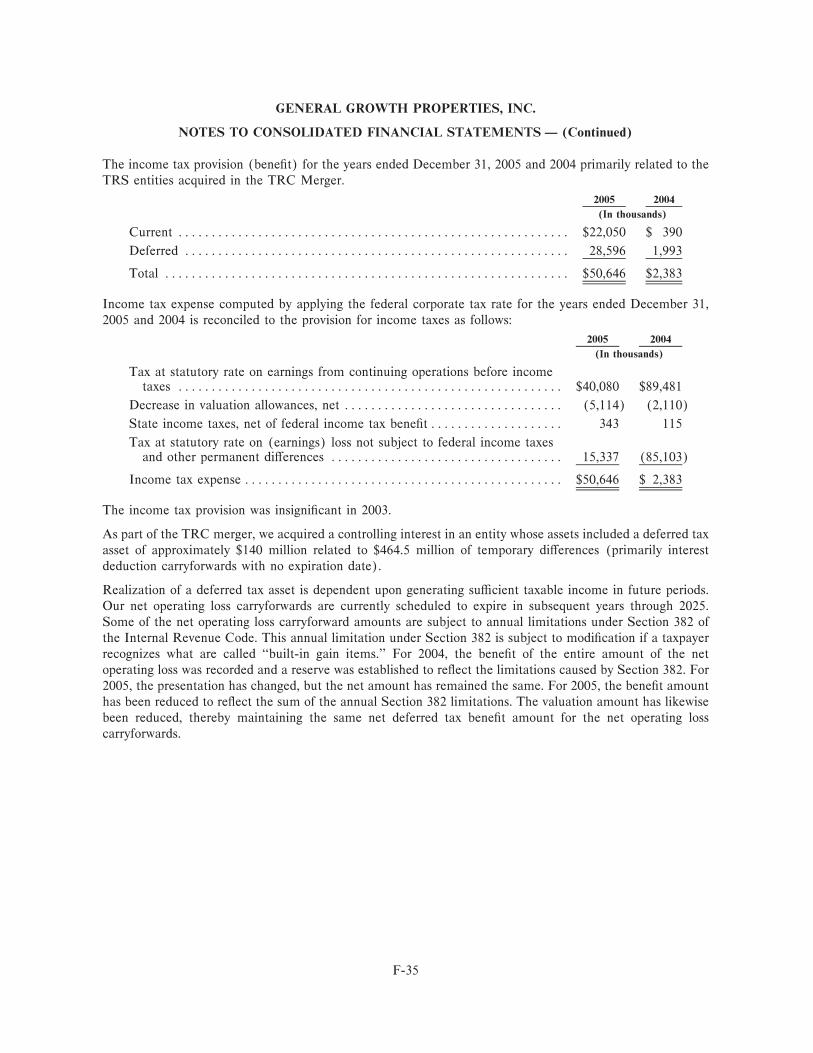

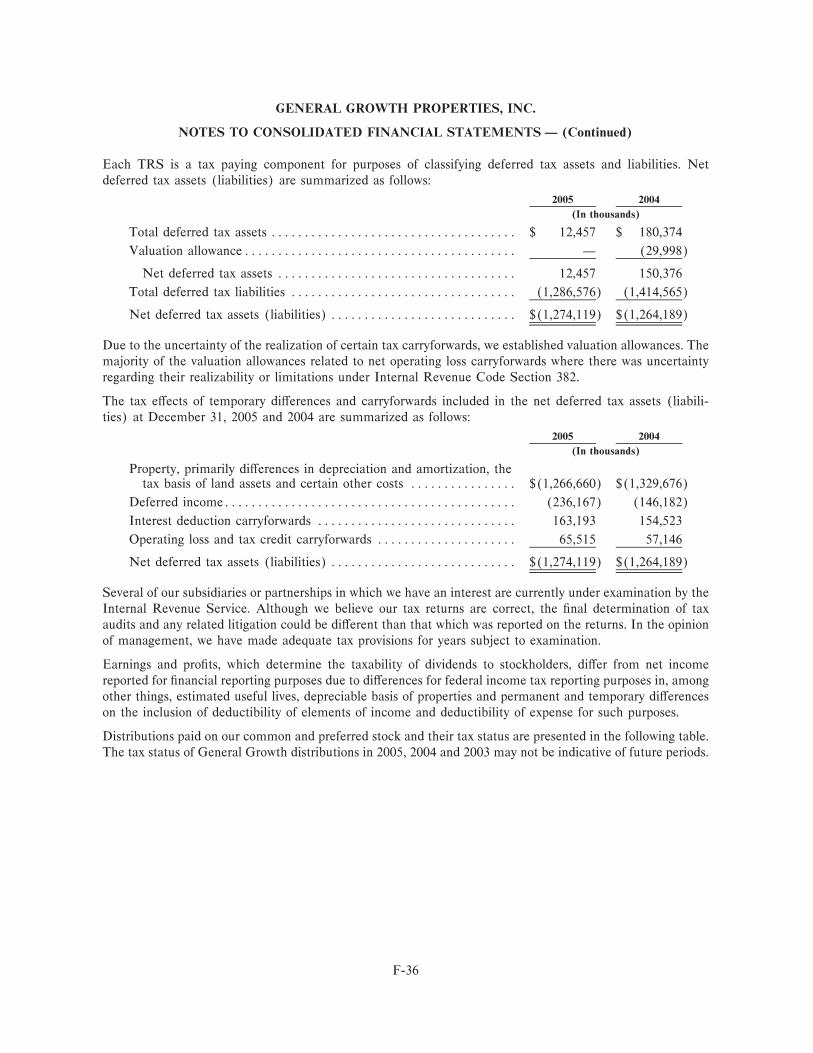

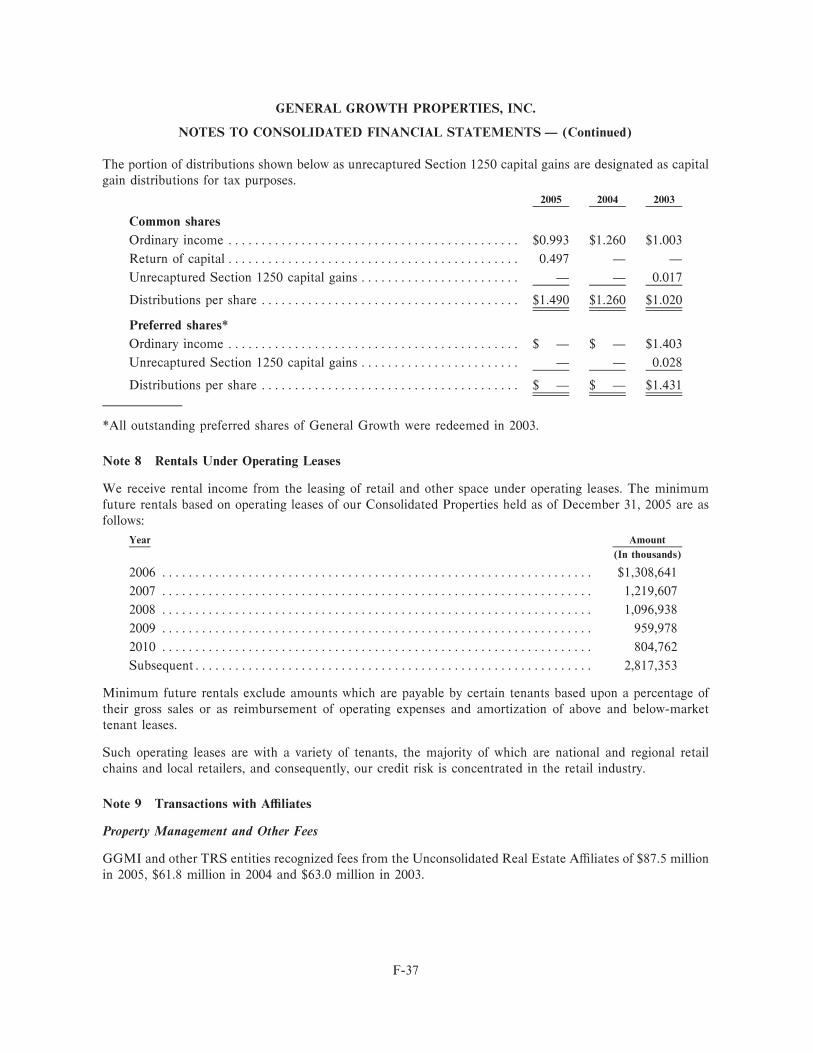

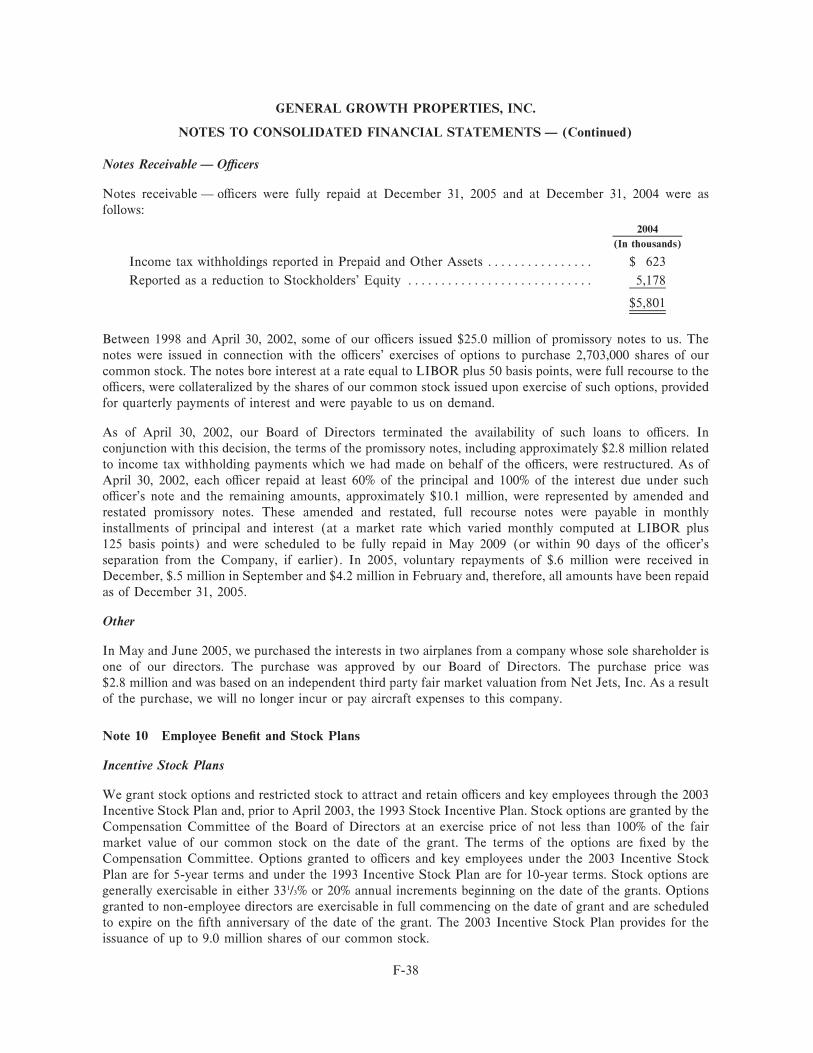

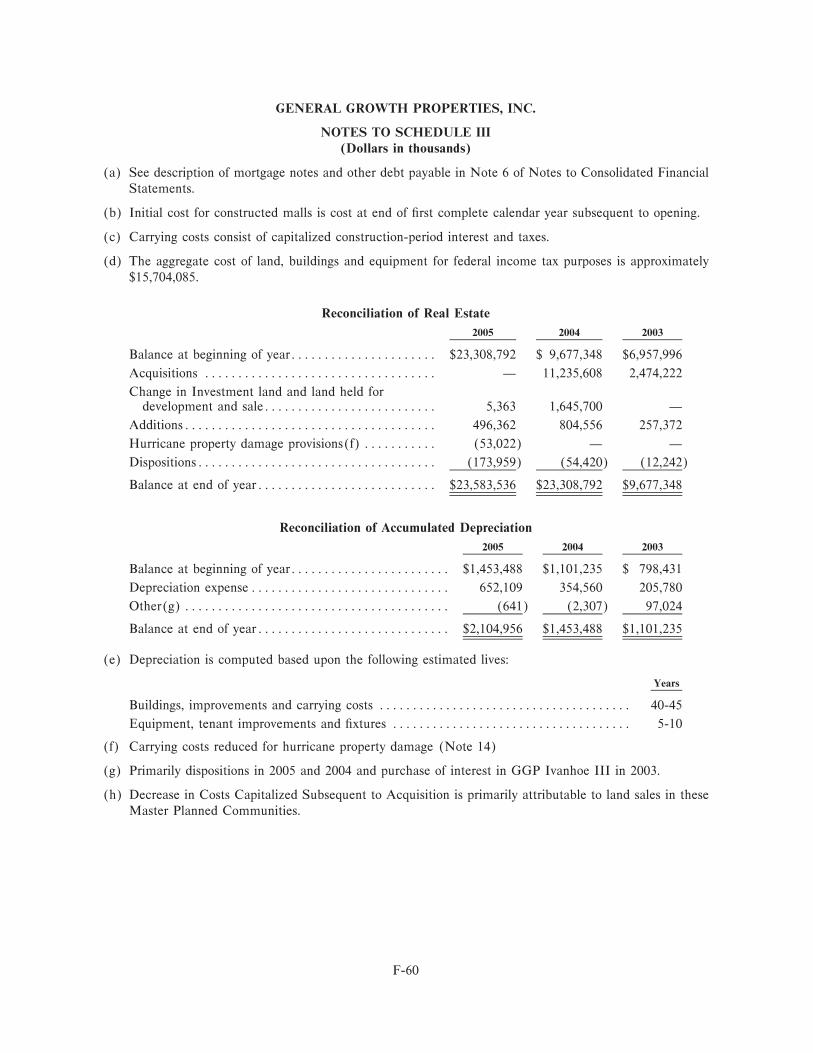

FINANCIAL HIGHLIGHTS Dollars in Thousands, Except Per Share Amounts

% Change 2005 vs. 2004 2005 2004 2003 2002 2001

Consolidated Property Revenues 57.8% $ 2,608,305 $ 1,652,773 $ 1,183,763 $ 898,424 $ 799,365

Unconsolidated Property Revenues (at Company Share) 42.6% $ 653,821 $ 458,390 $ 443,488 $ 394,223 $ 352,515

Funds from Operations (FFO) (Before Minority Interests) 16.9% $ 896,005 $ 766,164 $ 618,561 $ 485,304 $ 296,777

FFO Per Share (Fully Diluted)(1) 10.5% $ 3.06 $ 2.77 $ 2.31 $ 1.88 $ 1.32

STOCK AND PARTNERSHIP UNITS Outstanding at Year End

Shares of Common Stock 239,196,649 234,724,082 217,293,976 187,191,255 185,771,796

Operating Partnership Units(1) 53,061,895 55,532,263 55,712,250 58,668,741 58,717,479

Shares of Convertible Preferred Stock – – – 13,500,000 13,500,000

Shares of Common Stock Assuming Full Conversion of Operating Partnership Units and Convertible Preferred Stock 292,258,544 290,256,345 273,006,226 271,362,846 269,992,125

MALL DATA Dollars in Millions

2005 2004 2003 2002 2001

Mall Shop Tenant Sales(2) $ 13,694 $ 12,753 $ 10,258 $ 9,061 $ 7,326

Regional Malls Owned and Operating at Year End(3) 221 179 133 125 97

Mall Shop Square Footage Leased at Year End(2) 92.5% 92.1% 91.3% 91.0% 91.0%

(1) Operating Partnership Units can be exchanged on a one-for-one basis into shares of the Company’s common stock.(2) Excluding redevelopment properties.(3) Includes Consolidated and Unconsolidated Properties.

company profileGeneral Growth Properties, Inc. and its predecessor companies have been reinventing, revital-izing, and reinvigorating the shopping center industry for more than 50 years. General Growth is the second largest U.S.-based publicly traded Real Estate Investment Trust (REIT). General Growth has ownership interest in a portfolio of 192 regional shopping malls in 44 states, as well as ownership in master planned communities, office and industrial properties and community centers. The owned regional mall portfolio totals over 180 million square feet of retail space and includes approximately 24,000 retail stores nationwide. General Growth Properties, Inc. is listed on the New York Stock Exchange under the symbol GGP. For more information, please visit the company Web site at www.generalgrowth.com.

2001

2002

2003

2004

2005

97

125 133

188 192

2001

2002

2003

2004

2005

89

114 12

2

183

183

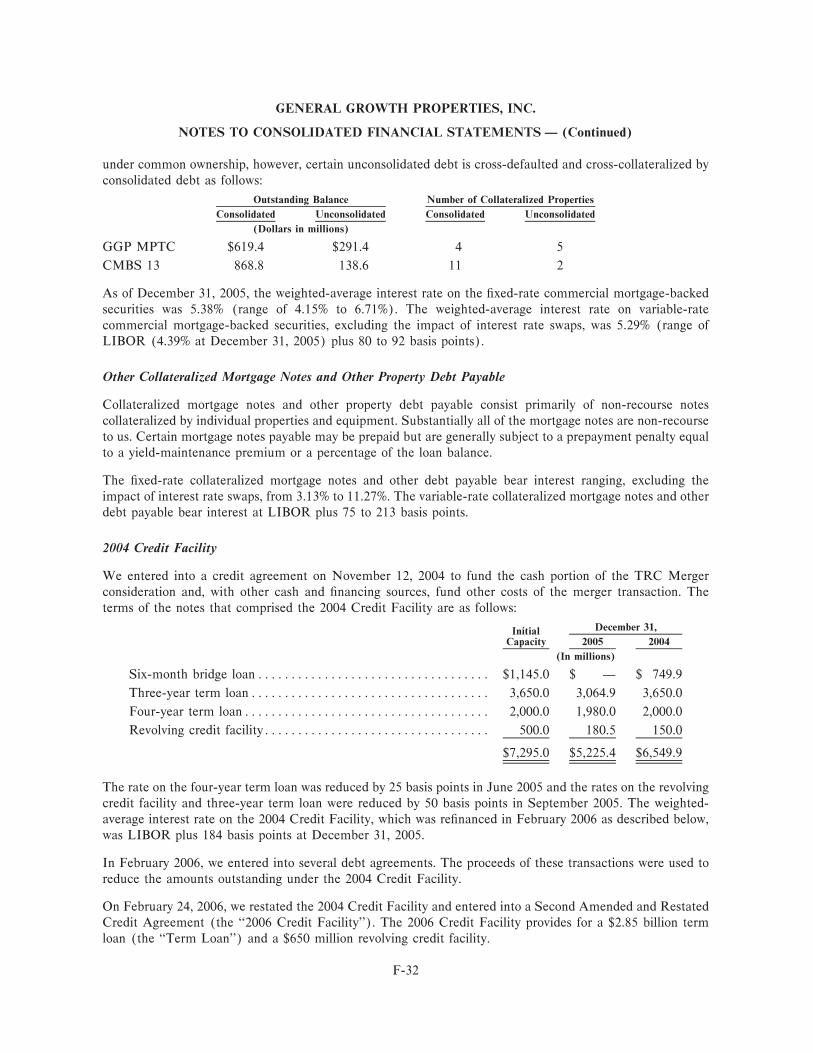

REGIONAL MALLS OWNED AND OPERATING* At Year End

* Information presented for Consolidated and Unconsolidated Properties.

TOTAL SQUARE FOOTAGE OWNED* In Millions

* Includes Consolidated and Unconsolidated regional malls, community centers, and office and industrial properties.

2001

2002

2003

2004

2005

2001

2002

2003

2004

2005

$7,326

$9,061

$10,258 $12,753

$13,694

$.80 $.92 $1.08

$1.26

$1.49

MALL SHOP TENANT SALES*† Dollars in Millions

* Information presented for Consolidated and Unconsolidated Properties.

† Excludes redevelopment properties and all retail spaces of 10,000 square feet or more.

DIVIDEND GROWTH PER SHARE* Dollar/Share Declared

* Reflects dividends declared and paid during such fiscal years, including the amount declared in January for prior year operations.

that we have created at GGP. Are we happy with our decision to acquire the Rouse Company?

Absolutely. Our enthusiasm for this transaction grows with each passing day. Our excitement

builds because we see many opportunities to improve the Rouse portfolio of retail centers,

and we see our existing GGP malls improving as well. We are creating even Greater Gathering

Places in malls such as Water Tower Place, Chicago, Illinois, Fashion Show Mall, Las Vegas,

Nevada, Faneuil Hall, Boston, Massachusetts and Ala Moana Center, Honolulu, Hawaii.

GGP is a strong and unified company. The addition of the Rouse people and properties make us

even better. We are a team at General Growth. We share the same goals, objectives and values to

make this a better company for all concerned. Yes, we have an outstanding collection of assets,

but first and foremost we are a company. The properties comprise a part of the company but they

do not make up the whole. The REIT industry has historically relied on net asset value (NAV) as

being the primary metric for establishing the value of a publicly traded real estate company. Why

are real estate companies not valued on earnings per share growth, cash flow growth or dividend

growth? Is real estate that different from other industries? We believe that as GGP continues to

grow and continues to operate as a consistently stable and

profitable company, living up in every way to our reputation

as a blue-chip real estate company, that the marketplace will

revisit how we should be valued.

2005 was another exceptionally profitable year for our

shareholders. We delivered a 35.2% total return versus

the Morgan Stanley REIT Index, which appreciated 12.1%,

the S&P 500, which increased 4.9%, the NASDAQ which

appreciated 2.2% and the DJIA, which appreciated 1.7%,

all on a total return basis. Over the last 12 years (since its

initial public offering (IPO) in April 1993), GGP’s per-share

growth in FFO has increased at a 16% rate compounded

GGP has produced superior returns ranking us within the top three among all during periods covering the last three, five and ten years.

General Growth Properties, Inc. 3

Dear Shareholders: Great Gathering Places: these are what we create. Special Places and

Experiences are the focus of our vision. A CUSTOMer-built Company giving our Consumers,

Owners, Retailers and Employees (C.O.R.E.) what they want, when they want it and where they

want it is our mission. These three things define and drive us as we strive to create value for

you. To be successful it is imperative for a company to have vision, a mission and goals. It has

been demonstrated and documented that companies that adhere to these traits are better

financial performers over extended periods of time. It is not “dumb luck” that General Growth

Properties, Inc. (GGP) has produced superior returns, ranking us within the top three among all

Real Estate Investment Trusts (REITs) during periods covering the last three, five and ten years.

We have accomplished this because GGP is anchored solidly to our core foundation of ethics,

integrity, timeless fundamentals and consistent profitability. Good reputations are not made

overnight, nor is recurring profitability; it takes time and it takes hard work. That is what we are

here doing for you. We have made, and we continue to make, a lasting contribution in the

marketplace. Beginning in 1954, this company was Built To Last and we are continuing to Build

To Last as we move forward in the 21st century.

2005 was a year of integration for GGP. Following the 2004 acquisition of The Rouse Company,

which consisted of ownership interests in 37 regional malls, 4 community centers, 6 mixed-use

projects and the master planned communities of Columbia, Maryland, Summerlin, (Las Vegas)

Nevada, The Bridgelands, (Houston) Texas and

a 52.5% interest in The Woodlands, (Houston)

Texas; we had to integrate all of the properties

into our company. With these properties came

approximately an additional 1100 people that

needed to understand and embrace the culture

2 General Growth Properties, Inc.

to our shareholders

General Growth Properties, Inc. 54 General Growth Properties, Inc.

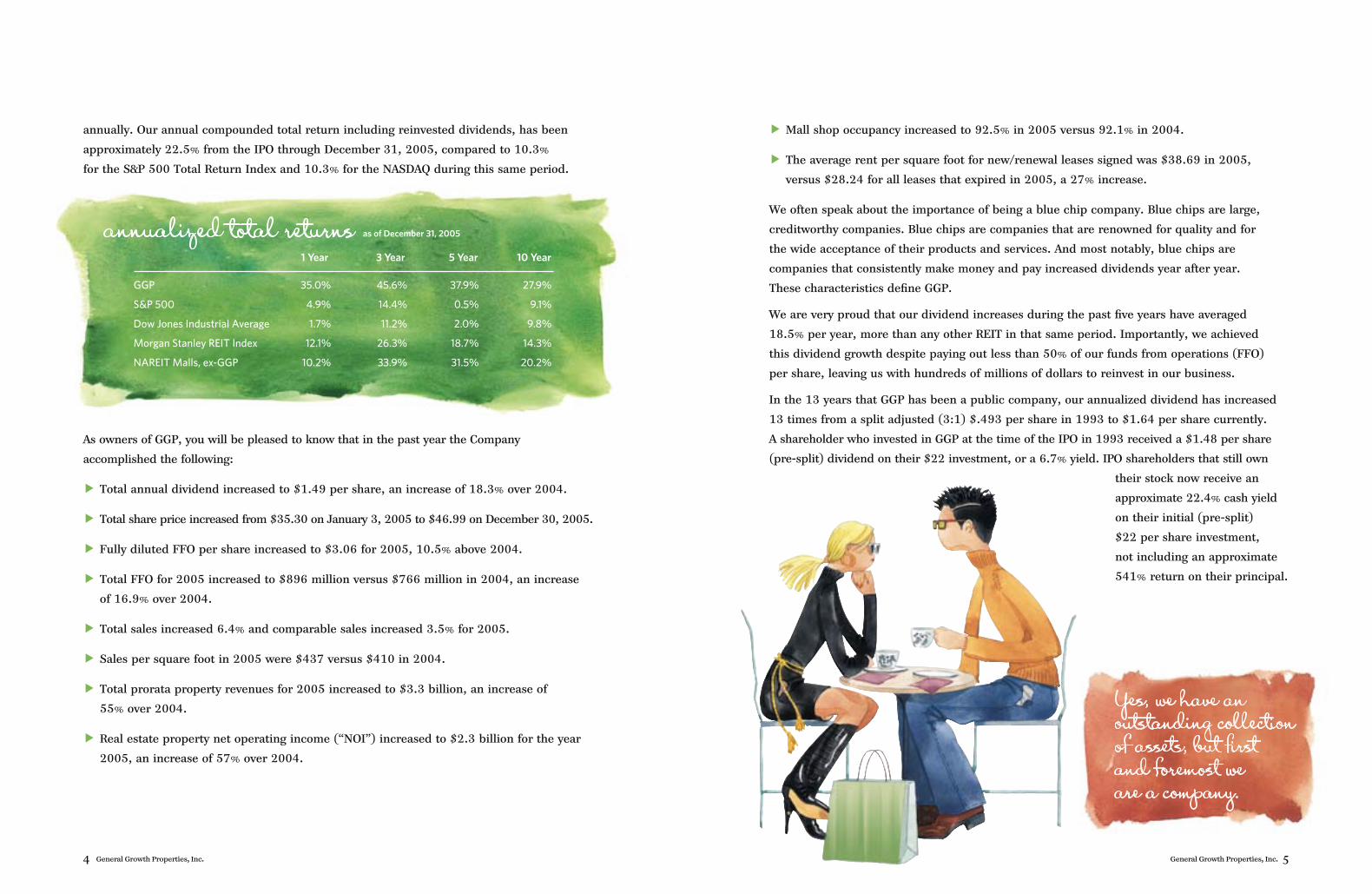

1 Year 3 Year 5 Year 10 Year

GGP 35.0% 45.6% 37.9% 27.9%

S&P 500 4.9% 14.4% 0.5% 9.1%

Dow Jones Industrial Average 1.7% 11.2% 2.0% 9.8%

Morgan Stanley REIT Index 12.1% 26.3% 18.7% 14.3%

NAREIT Malls, ex-GGP 10.2% 33.9% 31.5% 20.2%

annualized total returns as of December 31, 2005

Yes, we have an outstanding collection of assets, but first and foremost we are a company.

annually. Our annual compounded total return including reinvested dividends, has been

approximately 22.5% from the IPO through December 31, 2005, compared to 10.3%

for the S&P 500 Total Return Index and 10.3% for the NASDAQ during this same period.

As owners of GGP, you will be pleased to know that in the past year the Company

accomplished the following:

1 Total annual dividend increased to $1.49 per share, an increase of 18.3% over 2004.

1 Total share price increased from $35.30 on January 3, 2005 to $46.99 on December 30, 2005.

1 Fully diluted FFO per share increased to $3.06 for 2005, 10.5% above 2004.

1 Total FFO for 2005 increased to $896 million versus $766 million in 2004, an increase

of 16.9% over 2004.

1 Total sales increased 6.4% and comparable sales increased 3.5% for 2005.

1 Sales per square foot in 2005 were $437 versus $410 in 2004.

1 Total prorata property revenues for 2005 increased to $3.3 billion, an increase of

55% over 2004.

1 Real estate property net operating income (“NOI”) increased to $2.3 billion for the year

2005, an increase of 57% over 2004.

1 Mall shop occupancy increased to 92.5% in 2005 versus 92.1% in 2004.

1 The average rent per square foot for new/renewal leases signed was $38.69 in 2005,

versus $28.24 for all leases that expired in 2005, a 27% increase.

We often speak about the importance of being a blue chip company. Blue chips are large,

creditworthy companies. Blue chips are companies that are renowned for quality and for

the wide acceptance of their products and services. And most notably, blue chips are

companies that consistently make money and pay increased dividends year after year.

These characteristics define GGP.

We are very proud that our dividend increases during the past five years have averaged

18.5% per year, more than any other REIT in that same period. Importantly, we achieved

this dividend growth despite paying out less than 50% of our funds from operations (FFO)

per share, leaving us with hundreds of millions of dollars to reinvest in our business.

In the 13 years that GGP has been a public company, our annualized dividend has increased

13 times from a split adjusted (3:1) $.493 per share in 1993 to $1.64 per share currently.

A shareholder who invested in GGP at the time of the IPO in 1993 received a $1.48 per share

(pre-split) dividend on their $22 investment, or a 6.7% yield. IPO shareholders that still own

their stock now receive an

approximate 22.4% cash yield

on their initial (pre-split)

$22 per share investment,

not including an approximate

541% return on their principal.

The question we ask ourselves daily is where do we go from here? How do we maintain and

grow the terrific business we have? Guidance can oftentimes come from looking back into

history. It was during 500 BC that The Greek Agora at the foot of the Acropolis in ancient

Athens became one of the first urban marketplaces, with a central square surrounded by

buildings. In 100 BC, the Republican Forum at the base of Capitoline Hill was the commercial

and government center in Rome. By 1174 AD, the Market-Place developed in the city of Brussels

with buildings constructed by guilds and crafts corporations along a rectangular square. Similar

market squares would appear during the Middle Ages in other European cities. In 1288, the

Piazza del Campo in Venice, Italy was an open space surrounded by the cathedral and buildings,

with eleven shop-lined streets converging on the center. Sturbridge Fair opened in 1400 near

Cambridge, England and was one of the largest medieval fairs that were market centers for

merchants and in 1500 the London Bridge was lined with shops across the Thames River in

London, England. Markets are as old as history. They have been incessantly reinvented—

merchants bring new ideas and innovations which result in new marketplaces. We believe the

single most exciting area, the one which affords us the best opportunity to create enormous

value going forward, is reinventing, remerchandising and reinvesting in our existing properties,

just as investors, owners and developers have been doing for hundreds and hundreds of years.

The department stores at our malls are an example of this opportunity. We frequently meet

with all department store chains during the year as we strive to improve performance for

both our centers and the department stores themselves. As these stores experience continual

change, we are excited about the

opportunities for GGP created by

these changes. GGP continues to

take what was once department

General Growth Properties, Inc. 76 General Growth Properties, Inc.

Learning is critically important to improving. We learn new things every day.

1. Maintain a clear focus on what we do best: create value and profit by

acquiring, developing, renovating, and managing retail properties throughout

the United States.

2. Make decisions with your money that we would make with our own. When

we act, we are acting with our own money side by side with yours. We are

partners with our shareholders. The management and approximately 4,700

employees of General Growth own approximately 30% of the company.

3. Avoid actions based solely on our current stock price or for short-term

results. We are in a long-term business. Our goal is to maximize and

increase shareholder value.

4. Use conservative reporting methods and disclose supplemental

financial data that accurately and meaningfully reflect the operating

results of our company.

5. Distribute less than 50 percent of Funds From Operations (FFO).

Undistributed FFO represents our least expensive form of capital. The

need to continuously improve requires that we have sufficient funds

available for reinvestment to keep our properties interesting, appealing,

and attractive to customers.

6. Keep sight of the reasons our community of shareholders and business

partners are invested in us: performance, security, and liquidity. We will be

candid in our reporting to you. We will be honest in telling you what is good

in our business and what the challenges are. In a business that counts on the

successful handling of details, we will work hard to keep your confidence as

we tend to the details at hand.

GGP was founded on the following principles, which guide our daily business. This is why we strive to:

op∏ratıng principles

levels are high, and retailers are rolling out unprecedented levels of new branding concepts.

Spend time in our malls. Monitor the pulse of our business. You will see from firsthand

observation that GGP’s pulse is strong.

Densification. This will define our properties for many, many years into the future and gives

us the ability to bring more square footage onto our existing properties. Our malls are in the

enviable position of being situated on sites typically ranging in size from 100 to 120 acres

of land. As we witness changing demographics, changing commuting patterns and the desire

of people to live, work, play and learn in convenient environments, we have the ability and the

responsibility to provide this to them. Our properties lend themselves to change. Our centers

are constantly evolving. We have continually brought new ideas and innovations to our land.

As previously mentioned, recaptured department store space can be reincarnated into “village”

retail environments, entertainment areas, big box retail formats, residential units, hotels

and/or office complexes. The array of choices we have is large. We treat each and every market

individually, giving us alternatives that are completely unique in the real estate industry.

Learning is critically important to improving. We learn new things every day. One area of our

business that is a continual source of new lessons is the master planned community business.

GGP is expanding from being the creator of special places and experiences through retail

alone, to being the creator of special places and experiences for living, working, playing and

General Growth Properties, Inc. 9

left to right: John Bucksbaum,

Matthew Bucksbaum, Robert Michaels,

Bernard Freibaum, Jean Schlemmer

store space and create additional mall shop space, big box retail space, restaurant space,

theatres, outdoor retail villages, residential components, office space, hotels or simply replace

one department store with another to enhance the image and productivity of the property.

All of these alternatives benefit GGP and increase the long-term viability of our malls.

Alternative uses with potentially greater density of space are cash flow generators available

to us that will contribute to our future growth.

A good example can be found in the recently announced Federated department store closings.

On average, the announced closings occurring in GGP centers are at properties that have sales

of approximately $500 per square foot – more than 14% higher than our average center and

more than 35% higher than the industry average. The trade area populations in these locations

are estimated to be growing at 8.4% between now and 2009 versus 4.8% nationally, a difference

of 75%. On average, these same trade areas show household incomes approximately 11% higher

than the national average. This is just one of many reasons we remain excited about the future

of our properties.

Touring our properties reinforces the strength and solidity of our business. When we visit our

malls we see first hand how our customers embrace what we are doing. The redevelopments

and village components that we add to our existing centers are desired by our shoppers and

our retailers. The consumers want the restaurants and retail concepts that are located in our

properties. Because of the viability and

strength of our centers, the retailers are

introducing almost 100% of their new

concepts in the mall, creating centers that

are fresh and innovative. They are at the

forefront of retail and consumer desirability.

We believe GGP must give the consumer and

the retailer what they want, when they want

it and where they want it. Conditions for the

consumer and retailer are close to ideal. The

consumer continues to motor along, fueled

by positive job growth and ample disposable

income from home equity increases and a

willingness to acquire more debt. Mall space

supply remains in equilibrium and is not

outpacing retail tenant demand. Occupancy

8 General Growth Properties, Inc.

learning in master planned communities. The special places we

now strive to create include destinations where residential, office,

hospitality, retail and civic uses can find effective expressions. This

allows GGP to benefit from extending the experience we create in retail

to other asset classes as well. Instead of deriving financial returns from

retail alone, we now benefit from the economic potential of effective

development of other uses. We now capture the value of “place and

experience” over thousands of acres, instead of hundreds—and what

we learn from the thousands of acres we apply to the hundreds.

Jim Rouse envisioned Columbia, Maryland as “a place to grow people.”

His vision for Columbia has succeeded. Because of his success,

Columbia today is a thriving community of nearly 100,000 residents.

But today, Columbia is much different in its needs and its desires than it was 37 years ago as

it was being planned. Today, the “town center” of Columbia comprises approximately 500

acres and this land is vastly under-utilized. There is a demand for high-rise office and living

spaces, learning centers, hospitality and village retail. People want a more urbane expression

and vitality in their town centers as they densify. The community has the opportunity to become

“bright lights, little city.”

The Woodlands has been developed as a “city in the forest.” The Woodlands took a “village”

approach to living over 32 years ago and today the villages of the Woodlands form a community

of unparalleled living. Much like Columbia, we envision the Woodlands taking on a much more

urbane expression while remaining dedicated and nestled in the splendor and glory of its

natural environment.

Summerlin, (Las Vegas) Nevada is also a community of beautiful neighborhoods in natural

surroundings. Summerlin is fast approaching a population of 100,000 people and is quickly

emerging as an active, vibrant suburban community. As the community has grown, we have

recognized the importance of growing with the community and we are establishing the first phases

of Summerlin Town Center. We are planning and developing more extensive retail, office, multi-

family and hospitality uses. We continue to redefine the “experience” as the scale of the community

becomes more apparent and we are not viewing the mall as an isolated microcosm but as the

heart of the shopping, entertainment, business and residential fabric of the Town Center.

Columbia, The Woodlands, and Summerlin are leaders in advancing the practice of

sustainable development. By designing with nature, they demonstrate that community

10 General Growth Properties, Inc.

building can meet market opportunities better when the planning process includes thoughtful

stewardship of our natural resources. These developments have won international acclaim

by achieving our core human aspiration to be in harmony with nature while also enjoying

the rewarding experience of participating in vibrant, special gathering places. We are excited

about the prospect of applying these lessons to our newest community, Bridgelands, as well

as to the communities of merchants at our malls.

In addition, GGP is actively taking steps to adopt high performance, green design building and

operational practices in our existing, redevelopment and new development projects. GGP is

exploring new technologies and practices to help ensure an efficient use of resources, promote

the health and comfort of our building users and reduce negative impact on the environment,

while reducing energy and operating costs. We believe these efforts are both environmentally

responsible and sound business practices that will benefit our shoppers, retailers, employees

and investors.

We hope this letter gives you a better understanding of how we look for ways to change and

improve GGP. These improvements touch all aspects of our business—not just the obvious

ones. We are improving as a company, and we have the best and most talented people in

the mall industry. We are improving as managers of our employees, and our employees are

in turn improving the assets in each and every community in which we operate. People are

the foundation of GGP.

In 513 BC, Heraclitus of Greece observed, “There is nothing permanent except change.”

GGP continues to change. We make certain that as we change, we live our vision and our

mission each and every day. People Creating Special Places and Experiences—this is our

vision, and this is what we are accomplishing. Enjoy our Great Gathering Places.

our valuesrespecthonestyintegritypassionurgencyteamworkloyaltyhumilityfairness

General Growth Properties, Inc. 11

Bernard Freibaum

Executive Vice President

and Chief Financial Officer

Matthew BucksbaumFounder and Chairman of the Board

Jean Schlemmer

Chief Development Officer

John BucksbaumChief Executive Officer

Robert Michaels

President and

Chief Operating Officer

General Growth Properties, Inc. 13

CaliforniaBayshore Mall Eureka

Burbank Town Center 4Burbank

Chico Mall Chico

Chula Vista CenterChula Vista

Eastridge San Jose

Fallbrook Center West Hills (Los Angeles)

Galleria at Tyler Riverside (Los Angeles)

Glendale Galleria Glendale (Los Angeles)

Montclair Plaza Montclair (San Bernardino)

Moreno Valley MallMoreno Valley (Riverside)

NewPark Mall Newark (San Francisco)

Northridge Fashion CenterNorthridge

Redlands MallRedlands

The Shops at Tanforan 44San Bruno

Southbay Pavilion 4 Carson

Southland Mall Hayward

Stonestown San Francisco

Valley Plaza MallBakersfield

Visalia Mall Visalia

West Valley Mall Tracy (San Francisco)

ColoradoChapel Hills Mall Colorado Springs

Foothills Mall Fort Collins

Park Meadows Littleton (Denver)

Southwest Plaza Littleton (Denver)

ConnecticutBrass Mill Center Waterbury

The Shoppes at Buckland HillsManchester

DelawareChristiana Mall Newark

FloridaAltamonte MallAltamonte Springs

The Avenue Viera 44Viera

Bayside MarketplaceMiami

Coastland Center Naples

Eagle Ridge Mall Lake Wales (Orlando)

Festival Bay Mall 4 Orlando

Governor’s SquareTallahassee

Lakeland Square MallLakeland (Orlando)

Mizner Park Boca Raton

The Oaks MallGainesville

Oviedo MarketplaceOrlando

Pembroke Lakes Mall Pembroke Pines

Regency Square MallJacksonville

Village of Merrick ParkCoral Gables

West Oaks Mall Ocoee

GeorgiaAugusta Mall Augusta

Cumberland Mall Atlanta

North Point MallAlpharetta

Oglethorpe Mall Savannah

Peachtree Mall Columbus

Perimeter Mall Atlanta

Southlake MallMorrow (Atlanta)

HawaiiAla Moana CenterHonolulu

Kings’ Shop 4 Waikoloa

Prince Kuhio PlazaHilo

Queen Ka’ahumanu Center 4Kahului

Queens Marketplace 4 Waikoloa Beach Resort

Ward CentersHonolulu

12 General Growth Properties, Inc.

4 Managed only; no ownership interest

4 Leasing only

from the top: Jordan Creek Town Center West Des Moines (Des Moines), Iowa

Alderwood Lynnwood (Seattle), Washington

retail portfolioAlabamaCentury PlazaBirmingham

Riverchase GalleriaBirmingham

Arizona Arizona Center Phoenix

Arrowhead Town CenterGlendale

The Mall at Sierra VistaSierra Vista

Park Place Tucson

Superstition Springs CenterEast Mesa (Phoenix)

Tucson MallTucson

ArkansasThe PinesPine Bluff

General Growth Properties, Inc. 15

Lakeside Mall Sterling Heights (Detroit)

Lakeview Square Mall Battle Creek

Lansing Mall Lansing

RiverTown CrossingsGrandville (Grand Rapids)

Southland Center Taylor (Detroit)

Westwood Mall Jackson

MinnesotaApache Mall Rochester

Crossroads CenterSt. Cloud

Eden Prairie CenterEden Prairie (Minneapolis)

Knollwood Mall St. Louis Park (Minneapolis)

Ridgedale CenterMinneapolis

River Hills Mall Mankato

MississippiEdgewood Mall 44 McComb

Metrocenter Mall 4 Jackson

MissouriCapital Mall Jefferson City

Columbia Mall Columbia

Jamestown Mall 4 Florissant

Saint Louis GalleriaSt. Louis

14 General Growth Properties, Inc.

Whalers Village Lahaina

Windward Mall 4 Kaneohe

IdahoBoise Towne SquareBoise

Grand Teton Mall Idaho Falls

Pine Ridge Mall Pocatello

Silver Lake Mall Coeur d’Alene

IllinoisFord City Mall 4 Chicago

Golf Mill Shopping Center 4Niles (Chicago)

Lincolnshire Commons Lincolnshire (Chicago)

Main Street at Seven Bridges 4 Woodridge

Market Place Shopping CenterChampaign

Northbrook Court Northbrook (Chicago)

Oakbrook Center Oak Brook (Chicago)

Sandburg Mall 4 Galesburg

Spring Hill Mall West Dundee (Chicago)

Water Tower PlaceChicago

IndianaGlenbrook Square Fort Wayne

River Falls MallClarksville

IowaCoral Ridge MallCoralville (Iowa City)

Jordan Creek Town CenterWest Des Moines

Mall of the Bluffs Council Bluffs (Omaha, NE)

KentuckyFlorence Mall Florence

Greenwood MallGreenwood

Mall St. Matthews Louisville

Oxmoor Center Louisville

LouisianaAlexandria Mall 4Alexandria

Mall of Louisiana Baton Rouge

Mall St. VincentShreveport

Oakwood Center Gretna (New Orleans)

Pecanland Mall Monroe

Pierre Bossier MallBossier City (Shreveport)

Riverwalk MarketplaceNew Orleans

MaineThe Maine MallSouth Portland

MarylandThe Gallery at HarborplaceBaltimore

Harborplace Baltimore

Laurel Mall 4 Laurel (Baltimore)

The Mall in ColumbiaColumbia (Baltimore)

Mondawmin Mall Baltimore

Owings Mills Baltimore

Towson Town CenterBaltimore

The Village of Cross KeysBaltimore

White Marsh Mall Baltimore

MassachusettsFaneuil Hall MarketplaceBoston

Natick Mall Natick (Boston)

Silver City GalleriaTaunton

Swansea Mall 4 Swansea

MichiganAdrian Mall 4 Adrian

Bay City Mall Bay City

Birchwood Mall Port Huron (Detroit)

Centerpointe 4 Grand Rapids

The Crossroads Portage (Kalamazoo)

Grand Traverse MallTraverse City

4 Managed only; no ownership interest

4 Leasing only

clockwise from left: Water Tower Place Chicago, Illinois

Mizner Park Boca Raton, Florida

Faneuil Hall Marketplace Boston, Massachusetts

General Growth Properties, Inc. 17

NebraskaOak View MallOmaha

Westroads MallOmaha

NevadaThe Boulevard MallLas Vegas

Fashion Show Las Vegas

The Grand Canal Shoppes at The Venetian Las Vegas

Meadows Mall Las Vegas

New HampshireSteeplegate MallConcord

New JerseyBridgewater CommonsBridgewater

Paramus Park Paramus

Willowbrook Mall Wayne

Woodbridge CenterWoodbridge

New MexicoAnimas Valley MallFarmington

Coronado CenterAlbuquerque

North Plains Mall Clovis

Rio West Mall Gallup

New YorkLockport Mall Lockport

South Street SeaportNew York

St. Lawrence Centre 4Messina

Staten Island Mall Staten Island

North CarolinaCarolina Place Pineville (Charlotte)

Four Seasons Town CentreGreensboro

The Streets at SouthpointDurham

Valley Hills Mall Hickory

OhioBeachwood Place Cleveland

Colony Square MallZanesville

Kenwood Towne CentreKenwood (Cincinnati)

OklahomaQuail Springs Mall Oklahoma City

Sooner Mall Norman

Washington Park MallBartlesville

OregonClackamas Town CenterPortland

Gateway MallSpringfield

Pioneer Place Portland

Rogue Valley Mall Medford

Salem Center Salem

PennsylvaniaLebanon Valley 4Lebanon

The Mall at Steamtown 4 Scranton

Neshaminy Mall Bensalem (Philadelphia)

Park City Center Lancaster (Philadelphia)

Rhode IslandGarden City Shopping Center 4Cranston

Providence PlaceProvidence

South CarolinaColumbiana CentreColumbia

Rock Hill Galleria 4 Rock Hill

TennesseeNorthgate MallChattanooga

Stones River Mall 4Murfreesboro (Nashville)

TexasBassett Center 44 El Paso

Baybrook MallFriendswood (Houston)

Collin Creek Plano

Deerbrook Mall Humble (Houston)

16 General Growth Properties, Inc.

4 Managed only; no ownership interest

4 Leasing only

clockwise from above: Market Place Shopping Center Champaign, Illinois

The Woodlands Mall The Woodlands, Texas

Oakbrook Center Oak Brook (Chicago), Illinois

Perimeter Mall Atlanta, Georgia

directors and officers

Directors

Matthew Bucksbaum Founder and Chairman

John Bucksbaum Chief Executive Officer

Alan S. Cohen Senior Director of Marketing, Wireless Networking Business Unit Cisco Systems, Inc. San Jose, CA

Anthony Downs Senior Fellow, The Brookings Institution Washington, D.C.

Bernard Freibaum Executive Vice President and Chief Financial Officer

Adam S. Metz Co-founding Partner, Polaris Capital LLC Northbrook, IL

Robert Michaels President and Chief Operating Officer

Thomas H. Nolan President and Chief Financial Officer, Loreto Bay Company Scottsdale, AZ

John T. Riordan Ex-officio Trustee of the International Council of Shopping Centers Cotuit, MA

Beth Stewart Chief Executive Officer, Storetrax.com Rockville, MD

Officers

Matthew Bucksbaum Founder and Chairman

John Bucksbaum Chief Executive Officer

Robert Michaels President and Chief Operating Officer

Bernard Freibaum Executive Vice President and Chief Financial Officer

Jean Schlemmer Chief Development Officer

Joel Bayer Senior Vice President and Chief Investment Officer

Alex Berman Senior Vice President, GGP Ventures

Thomas D’Alesandro Senior Vice President, Development

Marshall E. Eisenberg Secretary

Ronald L. Gern Senior Vice President and Assistant Secretary

Melinda Holland Senior Vice President, Business Development

General Growth Properties, Inc.

Edmund Hoyt Senior Vice President and Chief Accounting Officer

Chuck Lhotka Chief Administrative Officer

Sharon Polonia Senior Vice President, Asset Management

Daniel Sheridan Executive Vice President, Asset Management

Warren Wilson Executive Vice President, Development

Rob Wyant Senior Vice President, Asset Management

18 General Growth Properties, Inc.

The Woodlands (Houston)

UtahCache Valley Mall Logan

Cottonwood Mall Holladay (Salt Lake City)

Fashion Place Salt Lake City

Newgate Mall Ogden (Salt Lake City)

Provo Towne CentreProvo

Red Cliffs Mall St. George

VermontBurlington Town CenterBurlington

VirginiaLandmark Mall Alexandria (Washington, D.C.)

Lynnhaven Mall Virginia Beach

Piedmont Mall Danville

Tysons Galleria McLean (Washington, D.C.)

WashingtonAlderwoodLynnwood (Seattle)

Bellis FairBellingham

NorthTown Mall Spokane

SouthShore Mall Aberdeen

Spokane Valley MallSpokane

Three Rivers Mall Kelso

Westlake Center Seattle

WisconsinFox River Mall Appleton

Mayfair Wauwatosa (Milwaukee)

Oakwood Mall Eau Claire

WyomingEastridge Mall Casper

White Mountain MallRock Springs

4 Managed only; no ownership interest

4 Leasing only

master planned communitiesTHE WOODLANDS

Houston, Texas

COLUMBIA

Columbia, Maryland

BRIDGELANDS

Houston Texas

FAIRWOOD

Fairwood, Maryland

EMERSON

Emerson, Maryland

STONE LAKE

Stone Lake, Maryland

SUMMERLIN

Las Vegas, Nevada

First Colony Mall Sugar Land (Houston)

Galleria Dallas 4 Dallas

Highland Mall Austin

Hulen Mall Fort Worth

North Star Mall San Antonio

The Parks at ArlingtonArlington

The Shops at La Cantera San Antonio

Sikes Senter Wichita Falls

Stonebriar Centre Frisco (Dallas)

Town East Mall Mesquite (Dallas)

Vista Ridge Mall Lewisville (Dallas)

Willowbrook Mall Houston

The Woodlands Mall

110 North Wacker DriveChicago, Illinois 60606(312) 960-5000

www.generalgrowth.com

corporate informationCorporate Office110 North Wacker Drive Chicago, Illinois 60606 (312) 960-5000

Employees4,700

Registrar and Transfer Agent and Shareowner Services Department

Mellon Investor Services, LLC 480 Washington Blvd Jersey City, NJ 07310

You may contact the Administrator at (888) 395-8037 or www.melloninvestor.com/isd TDD for Hearing Impaired: (800) 231-5469 Foreign Shareholders: (201) 680-6610 TDD for Foreign Shareholders: (201) 680-6578

Information about the Dividend Reinvestment and Stock Purchase Plan may also be obtained from Mellon.

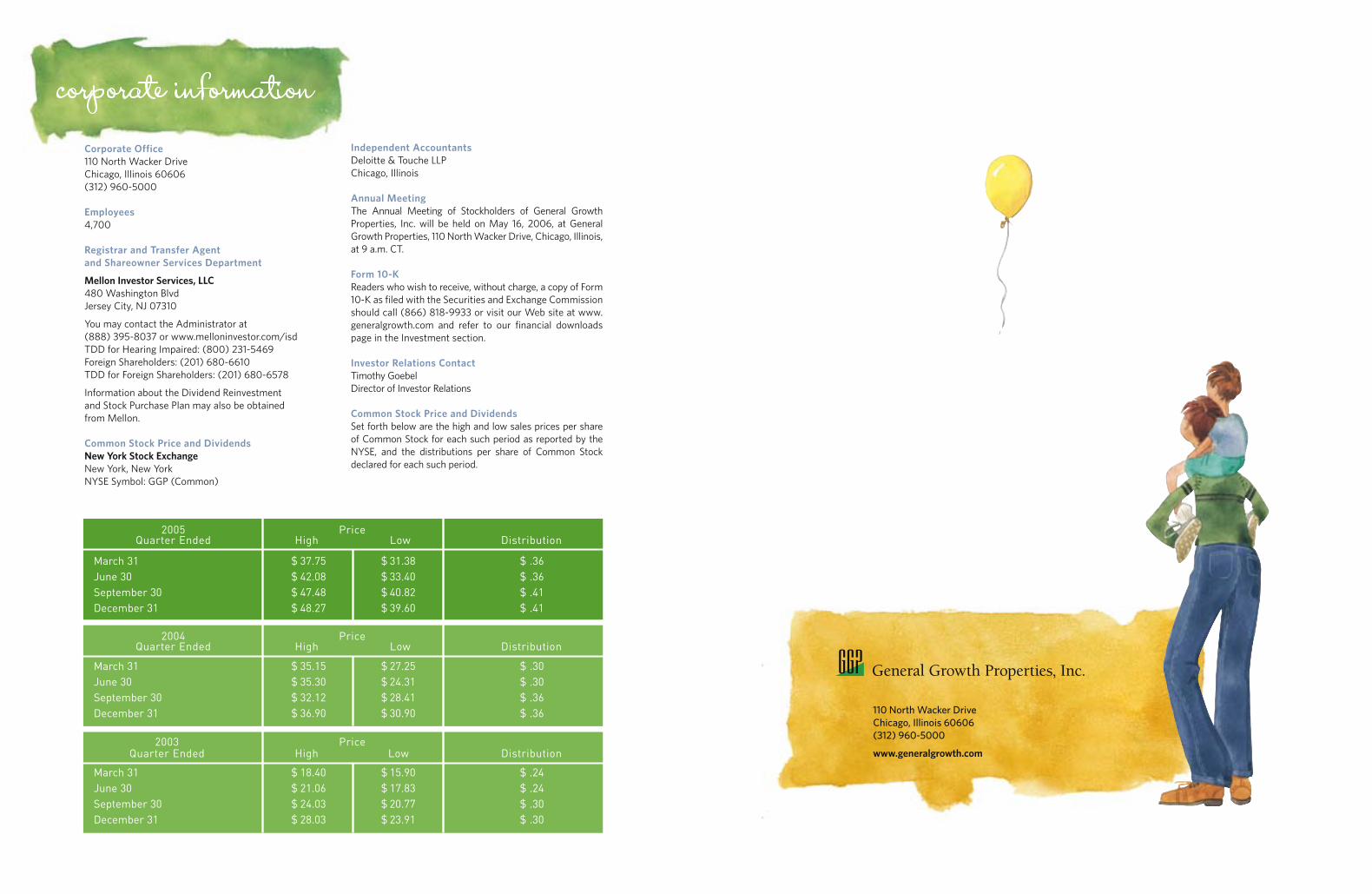

Common Stock Price and DividendsNew York Stock Exchange New York, New York NYSE Symbol: GGP (Common)

Independent AccountantsDeloitte & Touche LLP Chicago, Illinois

Annual MeetingThe Annual Meeting of Stockholders of General Growth Properties, Inc. will be held on May 16, 2006, at General Growth Properties, 110 North Wacker Drive, Chicago, Illinois, at 9 a.m. CT.

Form 10-KReaders who wish to receive, without charge, a copy of Form 10-K as filed with the Securities and Exchange Commission should call (866) 818-9933 or visit our Web site at www.generalgrowth.com and refer to our financial downloads page in the Investment section.

Investor Relations ContactTimothy Goebel Director of Investor Relations

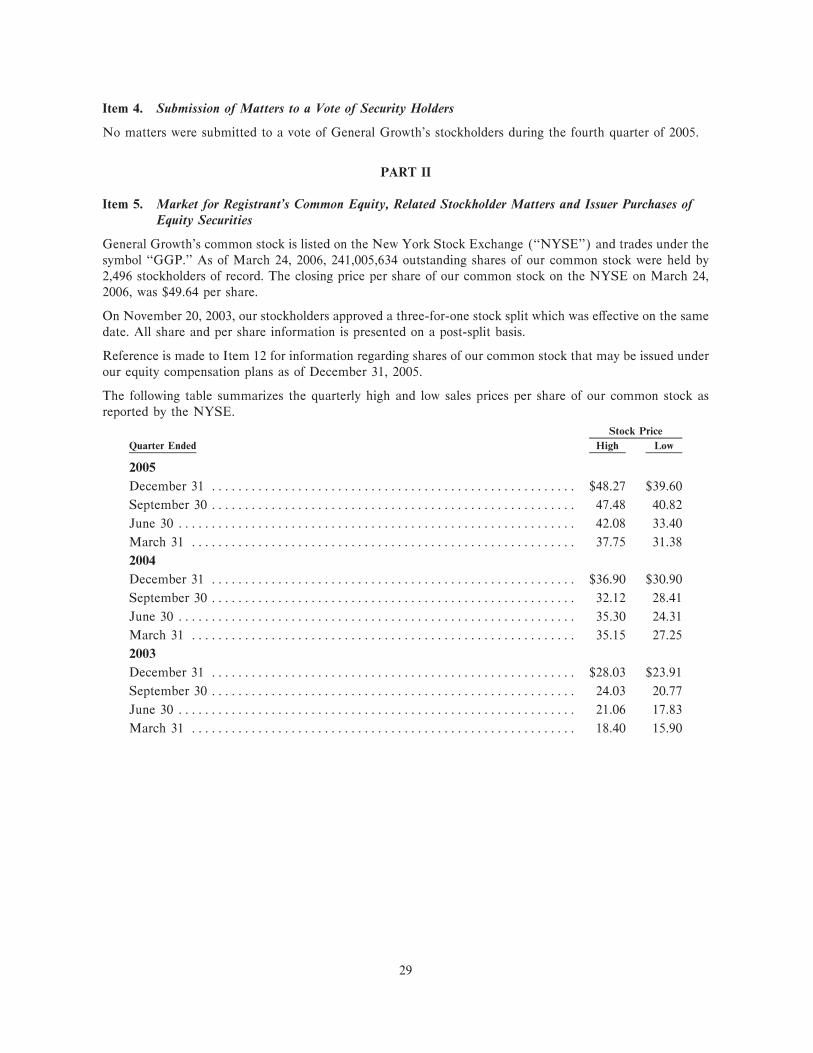

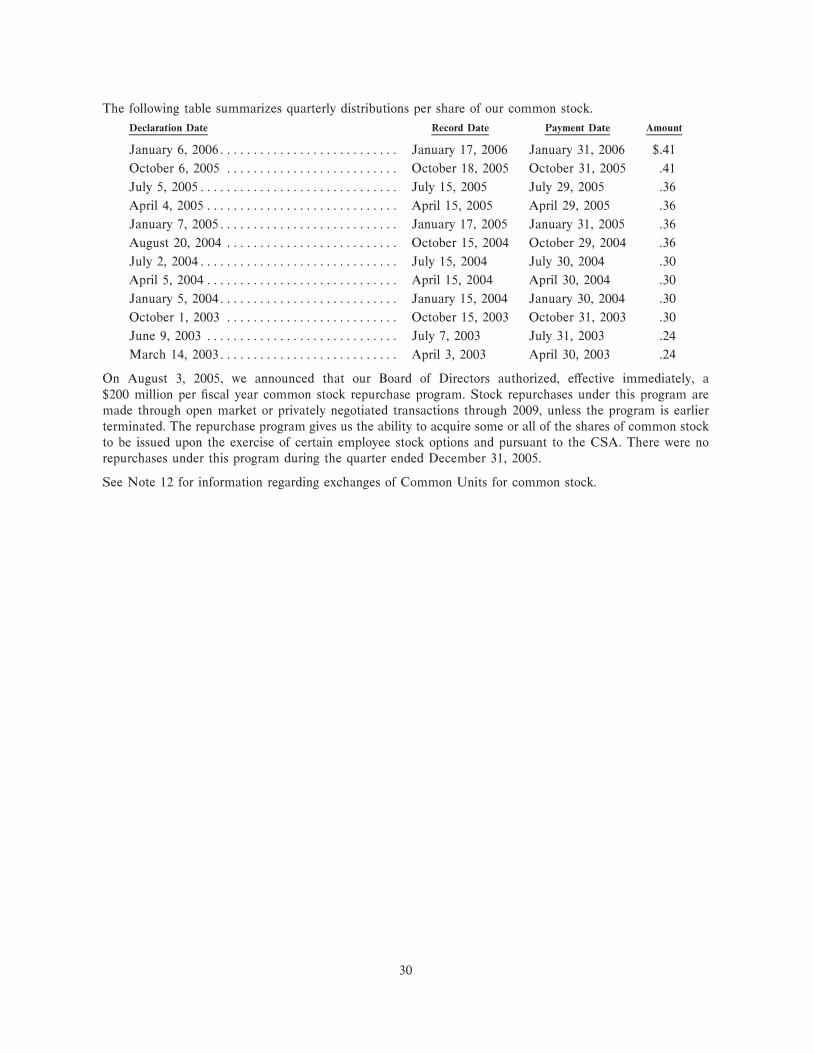

Common Stock Price and DividendsSet forth below are the high and low sales prices per share of Common Stock for each such period as reported by the NYSE, and the distributions per share of Common Stock declared for each such period.

2005 Price Quarter Ended High Low Distribution

March 31 $ 37.75 $ 31.38 $ .36 June 30 $ 42.08 $ 33.40 $ .36 September 30 $ 47.48 $ 40.82 $ .41 December 31 $ 48.27 $ 39.60 $ .41

2004 Price Quarter Ended High Low Distribution

March 31 $ 35.15 $ 27.25 $ .30 June 30 $ 35.30 $ 24.31 $ .30 September 30 $ 32.12 $ 28.41 $ .36 December 31 $ 36.90 $ 30.90 $ .36

2003 Price Quarter Ended High Low Distribution

March 31 $ 18.40 $ 15.90 $ .24 June 30 $ 21.06 $ 17.83 $ .24 September 30 $ 24.03 $ 20.77 $ .30 December 31 $ 28.03 $ 23.91 $ .30

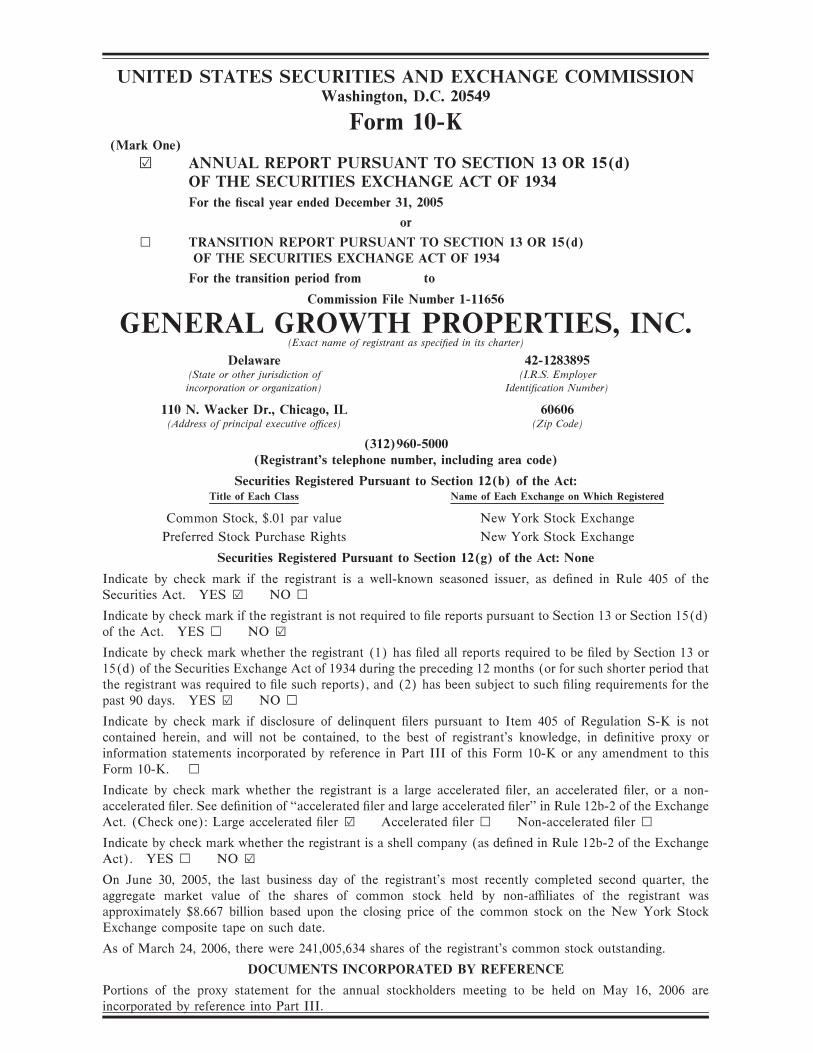

UNITED STATES SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

Form 10-K(Mark One)

¥ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)OF THE SECURITIES EXCHANGE ACT OF 1934

For the Ñscal year ended December 31, 2005

or

n TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 1-11656

GENERAL GROWTH PROPERTIES, INC.(Exact name of registrant as speciÑed in its charter)

Delaware 42-1283895(State or other jurisdiction of (I.R.S. Employerincorporation or organization) IdentiÑcation Number)

110 N. Wacker Dr., Chicago, IL 60606(Address of principal executive oÇces) (Zip Code)

(312)960-5000(Registrant's telephone number, including area code)

Securities Registered Pursuant to Section 12(b) of the Act:Title of Each Class Name of Each Exchange on Which Registered

Common Stock, $.01 par value New York Stock Exchange

Preferred Stock Purchase Rights New York Stock Exchange

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as deÑned in Rule 405 of theSecurities Act. YES ¥ NO n

Indicate by check mark if the registrant is not required to Ñle reports pursuant to Section 13 or Section 15(d)of the Act. YES n NO ¥

Indicate by check mark whether the registrant (1) has Ñled all reports required to be Ñled by Section 13 or15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period thatthe registrant was required to Ñle such reports), and (2) has been subject to such Ñling requirements for thepast 90 days. YES ¥ NO n

Indicate by check mark if disclosure of delinquent Ñlers pursuant to Item 405 of Regulation S-K is notcontained herein, and will not be contained, to the best of registrant's knowledge, in deÑnitive proxy orinformation statements incorporated by reference in Part III of this Form 10-K or any amendment to thisForm 10-K. n

Indicate by check mark whether the registrant is a large accelerated Ñler, an accelerated Ñler, or a non-accelerated Ñler. See deÑnition of ""accelerated Ñler and large accelerated Ñler'' in Rule 12b-2 of the ExchangeAct. (Check one): Large accelerated Ñler ¥ Accelerated Ñler n Non-accelerated Ñler n

Indicate by check mark whether the registrant is a shell company (as deÑned in Rule 12b-2 of the ExchangeAct). YES n NO ¥

On June 30, 2005, the last business day of the registrant's most recently completed second quarter, theaggregate market value of the shares of common stock held by non-aÇliates of the registrant wasapproximately $8.667 billion based upon the closing price of the common stock on the New York StockExchange composite tape on such date.

As of March 24, 2006, there were 241,005,634 shares of the registrant's common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the proxy statement for the annual stockholders meeting to be held on May 16, 2006 areincorporated by reference into Part III.

GENERAL GROWTH PROPERTIES, INC.

Annual Report on Form 10-KDecember 31, 2005

TABLE OF CONTENTS

Item No. Page Number

Part I

1. Business ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 1

1A. Risk Factors ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 7

1B. Unresolved StaÅ Comments ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 16

2. PropertiesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 16

3. Legal ProceedingsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 28

4. Submission of Matters to a Vote of Security Holders ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 29

Part II

5. Market for Registrant's Common Equity, Related Stockholder Matters and IssuerPurchases of Equity Securities ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 29

6. Selected Financial Data ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 31

7. Management's Discussion and Analysis of Financial Condition and Results ofOperations ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 33

7A. Quantitative and Qualitative Disclosures About Market RiskÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 50

8. Financial Statements and Supplementary DataÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 50

9. Changes in and Disagreements with Accountants on Accounting and FinancialDisclosure ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 51

9A. Controls and Procedures ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 51

9B. Other InformationÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 55

Part III

10. Directors and Executive OÇcers of the RegistrantÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 55

11. Executive Compensation ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 55

12. Security Ownership of Certain BeneÑcial Owners and Management and RelatedStockholder Matters ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 55

13. Certain Relationships and Related TransactionsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 56

14. Principal Accounting Fees and Services ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 56

Part IV

15. Exhibits and Financial Statement SchedulesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 57

Signatures ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 58

Consolidated Financial Statements ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ F-1

Consolidated Financial Statement ScheduleÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ F-55

Exhibit Index ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ S-1

i

PART I

Item 1. Business

All references to numbered Notes are to speciÑc footnotes to the Consolidated Financial Statements ofGeneral Growth Properties, Inc. (""General Growth'' or the ""Company'') as included in this Annual Reporton Form 10-K (""Annual Report''). The descriptions included in such Notes are incorporated into theapplicable Item response by reference. The following discussion should be read in conjunction with suchConsolidated Financial Statements and related Notes. The terms ""we,'' ""us'' and ""our'' may also be used torefer to General Growth and its subsidiaries. See also the Glossary at the end of Item 7, Management'sDiscussion and Analysis of Financial Condition and Results of Operations, for deÑnitions of selected termsused in this Annual Report.

Overview

General Growth is a self-administered and self-managed real estate investment trust, referred to as a ""REIT.''General Growth is a Delaware corporation and was organized in 1986.

Our business is focused in two main areas:

‚ Retail and Other. Through this segment of our business, we own, operate, manage, lease, acquire, develop,expand and Ñnance rental properties. These properties, which are located primarily throughout the UnitedStates, include retail centers, oÇce and industrial buildings and mixed-use and other properties. As ofDecember 31, 2005, we had ownership interest in and/or management responsibility for a portfolio of over200 regional shopping malls in 44 states. We also have ownership interest in certain joint ventures whichown four retail properties (one under construction) in Brazil and one retail property under construction inCosta Rica.

‚ Master Planned Communities. Through this segment of our business, we develop and sell land in andaround Columbia, Maryland; Summerlin, Nevada; and Houston, Texas for residential, commercial andother uses primarily in master planned communities. As of December 31, 2005, these communities,including land previously sold or not saleable, total over 70,000 acres.

Substantially all of our business is conducted through GGP Limited Partnership (the ""Operating Partnership''or ""GGPLP''). As of December 31, 2005, ownership of the Operating Partnership was as follows:

82% ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ General Growth, as sole general partner

Limited partners that indirectly include familymembers of the original stockholders of theCompany. Represented by common units oflimited partnership interest (the ""Common

16ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Units'')

Limited partners that include subsequentcontributors of properties to the OperatingPartnership which are also represented by

2ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Common Units.

100%

The Operating Partnership also has preferred units of limited partnership interest (the ""Preferred Units'')outstanding. Under certain circumstances, the Preferred Units are convertible into Common Units which areredeemable for shares of General Growth common stock on a one-for-one basis.

Many of our properties are owned entirely by us, or through entities in which we own a majority or controllinginterest. As a result, these properties are consolidated under generally accepted accounting principles(""GAAP''), and we refer to them as the ""Consolidated Properties.'' Some properties are held through jointventure entities in which we own a non-controlling interest (""Unconsolidated Real Estate AÇliates'') and we

1

refer to those properties as the ""Unconsolidated Properties.'' Collectively, we refer to the ConsolidatedProperties and Unconsolidated Properties as our ""Company Portfolio.''

We make all key strategic decisions for our properties. However, in connection with the UnconsolidatedProperties, such strategic decisions are made with the respective stockholders, members or joint venturepartners of such properties. We are also the asset manager of most of the properties in the Company Portfolio,executing the strategic decisions and overseeing the day-to-day property management functions, includingleasing, construction management, data processing, maintenance, accounting, marketing, promotional servicesand security oversight. With respect to jointly owned properties, we generally conduct the managementactivities through one of our taxable REIT subsidiaries (""TRS''). As of December 31, 2005, we managed theproperties for 21 of our unconsolidated joint ventures and seven of our consolidated joint ventures. Our jointventure partners managed the properties for 12 of our unconsolidated joint ventures and four of ourconsolidated joint ventures.

General Development of Business

In recent years, acquisitions have been a key contributor to our growth. In 2004, for example, acquisitionstotaled over $16 billion, largely due to the $14 billion acquisition of The Rouse Company in November (the""TRC Merger''). In 2005, however, acquisitions were minimal and our operational focus was on the following:

‚ Integrating and maximizing the operations of The Rouse Company LP (""TRCLP,'' successor to The RouseCompany (""TRC'')) through proactive property management and leasing and through operating costreductions. SpeciÑc actions to increase productivity of the TRCLP properties as well as our previouslyexisting properties have included changing the tenant mix and adding vendor carts and kiosks. As the TRCMerger was primarily funded with new acquisition debt, an additional focus has been the management andreÑnancing of our current debt.

‚ Development activities, including ground-up development and redevelopment and expansion of existingproperties. For example, we substantially completed the ground-up development of The Shops at LaCanterain San Antonio, Texas in September 2005, and the renovation of Eastridge Mall in San Jose, California inNovember 2005. The expansion and renovation of a property may result in increased cash Öows and netincome as a result of increased customer traÇc, trade area penetration and improved competitive position ofthe property.

‚ Growing our specialty leasing and alternative revenue business, which involves, among other things, thetemporary leasing of carts, kiosks and available space to generate additional alternative rental revenue.

Financial Information About Industry Segments

Information regarding our segments is incorporated herein by reference to Note 16.

Narrative Description of Business

Retail and Other Segment

Our Retail and Other segment consists of retail centers, oÇce and industrial buildings and mixed-use andother properties.

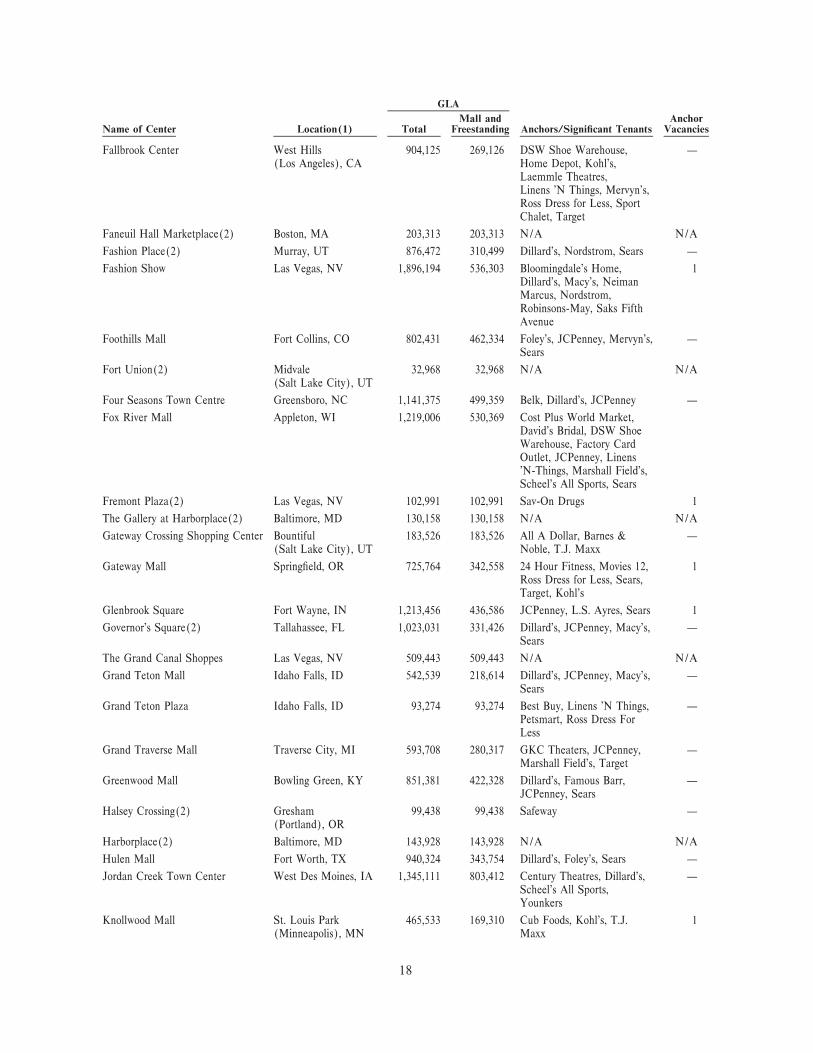

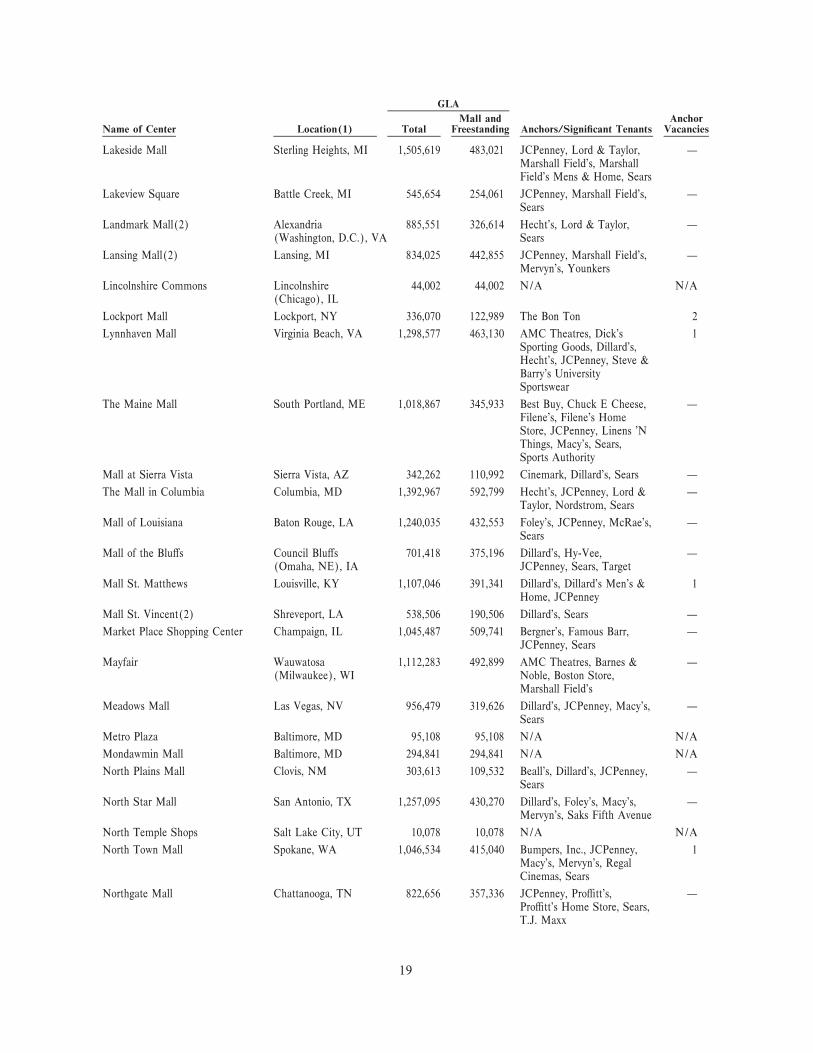

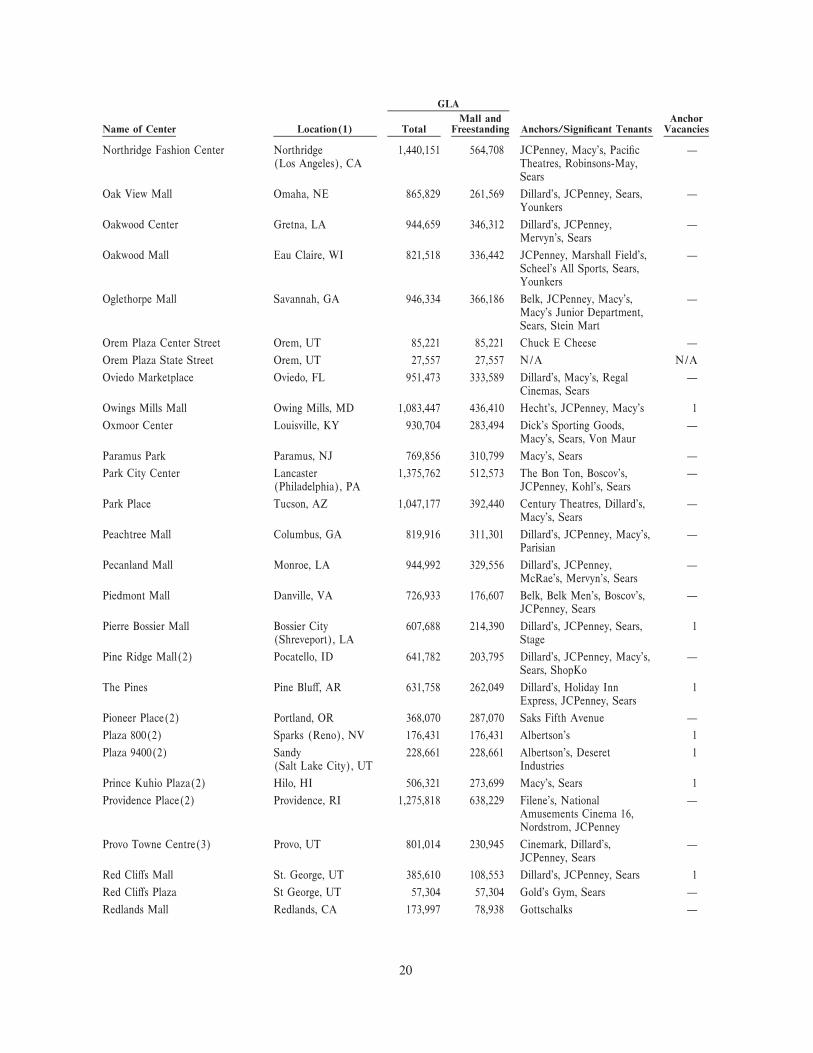

Retail Portfolio

The Retail Portfolio is comprised primarily of regional shopping centers, but also includes festival marketplaces, urban mixed-use centers and strip/community centers. Most of our shopping centers are strategicallylocated in major and middle markets where they have strong competitive positions. Most of these propertiescontain at least one major department store as an Anchor. We believe the Retail Portfolio's geographicdiversiÑcation should mitigate the eÅects of regional economic conditions and local factors.

A detailed listing of the principal properties in our Retail Portfolio is included in Item 2 of this Annual Report.

2

The majority of the income from the properties in the Retail Portfolio is derived from rents received throughlong-term leases with retail tenants. These long-term leases generally require the tenants to pay base rentwhich is a Ñxed amount speciÑed in the lease. The base rent is often subject to scheduled increases during theterm of the lease. Another component of income is overage rent. Overage rent is paid by a tenant generally ifits sales exceed an agreed upon minimum amount. Overage rent is calculated by multiplying the sales inexcess of the minimum amount by a percentage deÑned in the lease, the majority of which is earned in thefourth quarter. In addition, our long-term leases generally contain provisions for us to bill to tenants amountsto recover certain expenses incurred in the day-to-day operations of the respective properties, includingcommon area maintenance and real estate taxes. The recovery amount is generally related to the tenant's pro-rata share of space in the property.

The following table reÖects retail tenant representation by category for the Consolidated Properties as ofDecember 31, 2005. In general, similar percentages existed for the Unconsolidated Properties.

Category % of Square Feet Representative Tenants

Specialty (includes personal services)ÏÏÏÏÏ 22% Regis, Lenscrafters, Dollar Tree, Petland

Family Apparel (includes unisex) ÏÏÏÏÏÏÏÏ 14 Gap, Old Navy, J Crew, Express, AnchorBlue, Banana Republic, Bachrach

Women's Apparel ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 14 Limited, Talbot's, Chico's, Lane Bryant,Ann Taylor, Coldwater Creek, Victoria'sSecret

Teen Apparel ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 9 PacSun, Charlotte Russe, Forever 21,d.e.m.o., Hollister & Co., Aeropostale,Abercrombie & Fitch

ShoesÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 8 FootLocker, Journeys, Champ's, FinishLine, Payless Shoesource

RestaurantsÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 7 Ruby Tuesday, Applebee's, Bennigan's,Cheesecake Factory, Panera Bread, PFChang's China Bistro

Home Entertainment and Electronics ÏÏÏÏÏ 5 RadioShack, Ritz Camera, FYE, SamGoody, Apple Computer

Home Furnishings ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 4 William-Sonoma, Select Comfort,Z Gallerie, Pottery Barn, Crate & Barrel

Sporting Goods ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 3 Scheel's All Sports, MC Sports, Dick'sSporting Goods, Big 5 Sports

Gifts (includes stationery, cards, gifts and 3 Papyrus, Hallmark, Yankee Candle, Thingsnovelty)ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Remembered, Spencer Gifts

Fast Food/Food Court ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 3 Arby's, Sbarro, McDonald's, AuntieAnne's, Chick-Fil-A, Subway, Sonic

Jewelry ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 3 Zales Jewelers, Kay Jewelers, PiercingPagoda, Helzberg Diamonds

Children's MerchandiseÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 2 Gymboree, Club Libby Lu, Build-A-Bear,The Children's Place, GapKids/BabyGap

Personal Care ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 2 L'Occitane, Sephora, Trade Secret, Bath &Body Works

Specialty Food (includes health, candy and 1 GNC, Vitamin World, Starbuck's, GodivacoÅee)ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Chocolatier, Harry & David

TOTAL ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ 100%

As of December 31, 2005, our largest tenant (based on common parent ownership) accounted for less than 4%of consolidated rents.

3

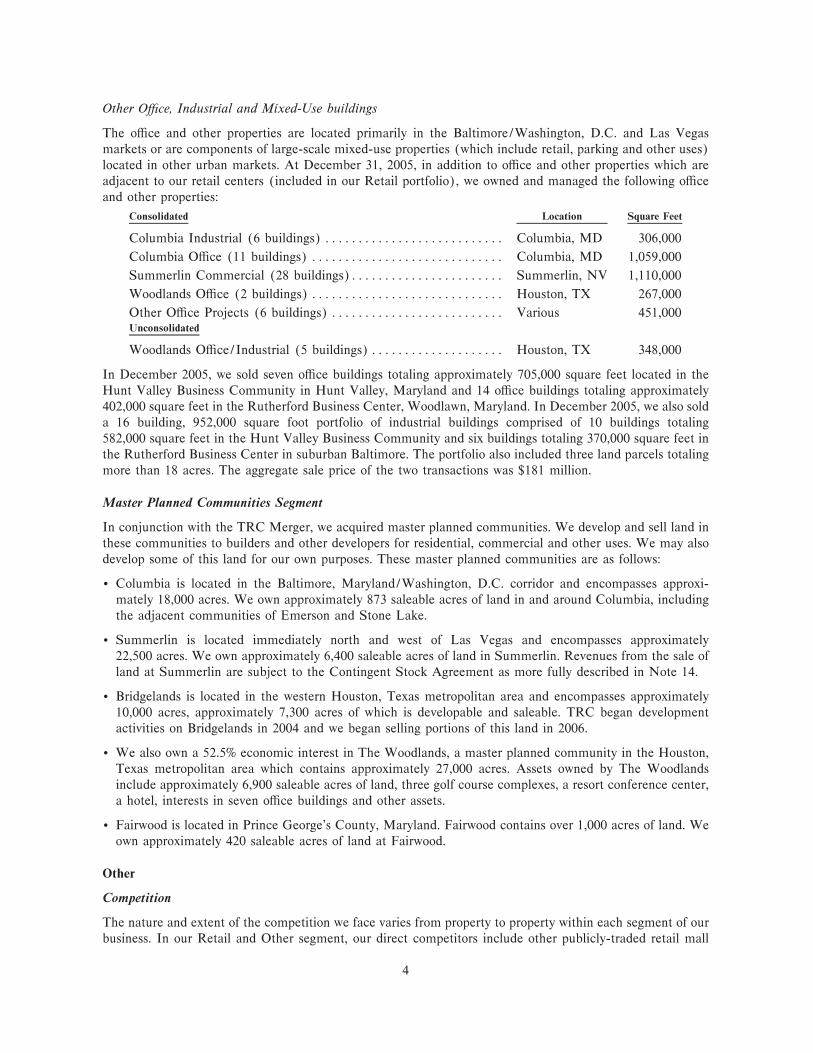

Other OÇce, Industrial and Mixed-Use buildings

The oÇce and other properties are located primarily in the Baltimore/Washington, D.C. and Las Vegasmarkets or are components of large-scale mixed-use properties (which include retail, parking and other uses)located in other urban markets. At December 31, 2005, in addition to oÇce and other properties which areadjacent to our retail centers (included in our Retail portfolio), we owned and managed the following oÇceand other properties:

Consolidated Location Square Feet

Columbia Industrial (6 buildings) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Columbia, MD 306,000

Columbia OÇce (11 buildings) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Columbia, MD 1,059,000

Summerlin Commercial (28 buildings)ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Summerlin, NV 1,110,000

Woodlands OÇce (2 buildings) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Houston, TX 267,000

Other OÇce Projects (6 buildings) ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Various 451,000Unconsolidated

Woodlands OÇce/Industrial (5 buildings)ÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏÏ Houston, TX 348,000

In December 2005, we sold seven oÇce buildings totaling approximately 705,000 square feet located in theHunt Valley Business Community in Hunt Valley, Maryland and 14 oÇce buildings totaling approximately402,000 square feet in the Rutherford Business Center, Woodlawn, Maryland. In December 2005, we also solda 16 building, 952,000 square foot portfolio of industrial buildings comprised of 10 buildings totaling582,000 square feet in the Hunt Valley Business Community and six buildings totaling 370,000 square feet inthe Rutherford Business Center in suburban Baltimore. The portfolio also included three land parcels totalingmore than 18 acres. The aggregate sale price of the two transactions was $181 million.

Master Planned Communities Segment

In conjunction with the TRC Merger, we acquired master planned communities. We develop and sell land inthese communities to builders and other developers for residential, commercial and other uses. We may alsodevelop some of this land for our own purposes. These master planned communities are as follows:

‚ Columbia is located in the Baltimore, Maryland/Washington, D.C. corridor and encompasses approxi-mately 18,000 acres. We own approximately 873 saleable acres of land in and around Columbia, includingthe adjacent communities of Emerson and Stone Lake.

‚ Summerlin is located immediately north and west of Las Vegas and encompasses approximately22,500 acres. We own approximately 6,400 saleable acres of land in Summerlin. Revenues from the sale ofland at Summerlin are subject to the Contingent Stock Agreement as more fully described in Note 14.

‚ Bridgelands is located in the western Houston, Texas metropolitan area and encompasses approximately10,000 acres, approximately 7,300 acres of which is developable and saleable. TRC began developmentactivities on Bridgelands in 2004 and we began selling portions of this land in 2006.

‚ We also own a 52.5% economic interest in The Woodlands, a master planned community in the Houston,Texas metropolitan area which contains approximately 27,000 acres. Assets owned by The Woodlandsinclude approximately 6,900 saleable acres of land, three golf course complexes, a resort conference center,a hotel, interests in seven oÇce buildings and other assets.

‚ Fairwood is located in Prince George's County, Maryland. Fairwood contains over 1,000 acres of land. Weown approximately 420 saleable acres of land at Fairwood.

Other

Competition

The nature and extent of the competition we face varies from property to property within each segment of ourbusiness. In our Retail and Other segment, our direct competitors include other publicly-traded retail mall

4

development and operating companies, retail real estate companies, commercial property developers and otherowners of retail real estate that engage in similar businesses.

Within our Retail Portfolio, we compete to acquire land for new site development and to acquire existing retailproperties. We believe that we have a competitive advantage with respect to acquisitions for the followingreasons:

‚ Subject to certain limitations, the funds necessary for cash acquisitions are available to us from acombination of sources, including mortgage or unsecured Ñnancing or the issuance of public or private debtor equity.

‚ We have the Öexibility to pay for an acquisition with a combination of cash, General Growth equitysecurities or common or preferred units of limited partnership interest in the Operating Partnership. Thislast approach may create the opportunity for a tax-advantaged transaction for the seller.

‚ Our expertise allows us to evaluate proposed acquisitions of existing retail properties for their increasedproÑt potential through expansion, remodeling, re-merchandising and more eÇcient management of theproperty.

We also compete for retail tenants. We believe the principal factors that retailers consider in making theirleasing decision include:

‚ Consumer demographics

‚ Quality, design and location of properties

‚ Total number and geographic distribution of properties

‚ Diversity of retailers and anchor tenants at shopping center locations

‚ Management and operational expertise

‚ Rental rates

Based on these criteria, we believe that the size and scope of our property portfolio, as well as the overallquality and attractiveness of our individual properties, enable us to compete eÅectively for retail tenants in ourlocal markets. Because our revenue potential is linked to the success of our retailers, we indirectly shareexposure to the same competitive factors that our retail tenants experience in their respective markets whentrying to attract individual shoppers. These dynamics include general competition from other regionalshopping centers, including outlet malls and other discount shopping centers, as well as competition withdiscount shopping clubs, catalog companies, internet sales and telemarketing.

With respect to our oÇce and other properties, we experience competition in the development andmanagement of our properties similar to that of our Retail Portfolio. Prospective tenants generally considerquality and appearance, amenities, location relative to other commercial activity and price in determining theattractiveness of our properties. Based on the quality and location of our properties, which are generally inurban markets or are concentrated in the commercial centers of our master planned communities, we believethat our properties are viewed favorably among prospective tenants.

In our Master Planned Communities segment, we compete with other landholders and residential andcommercial property developers in the development of properties within the Baltimore/Washington, D.C., LasVegas, and Houston markets. SigniÑcant factors aÅecting our competition in this business include:

‚ The size and scope of our master planned communities

‚ The recreational and cultural amenities available within the communities

‚ The commercial centers in the communities

‚ The relationships of the developer with homebuilders

‚ The proximity to major metropolitan areas

5

We believe our projects oÅer signiÑcant advantages when viewed against these criteria.

Environmental Matters

Under various federal, state and local laws and regulations, an owner of real estate is liable for the costs ofremoval or remediation of certain hazardous or toxic substances on such real estate. These laws often imposesuch liability without regard to whether the owner knew of, or was responsible for, the presence of suchhazardous or toxic substances. The costs of remediation or removal of such substances may be substantial, andthe presence of such substances, or the failure to promptly remediate such substances, may adversely aÅectthe owner's ability to sell such real estate or to borrow using such real estate as collateral. In connection withour ownership and operation of our properties, we, or the relevant property venture through which the propertyis owned, may be potentially liable for such costs.

Substantially all of our properties have been subject to environmental assessments, which are intended todiscover information regarding, and to evaluate the environmental condition of, the surveyed and surroundingproperties.

The Phase I environmental assessments included a historical review, a public records review, a preliminaryinvestigation of the site and surrounding properties, screening for the presence of asbestos, polychlorinatedbiphenyls (""PCBs'') and underground storage tanks and the preparation and issuance of a written report, butdo not include soil sampling or subsurface investigations. A Phase II assessment, when necessary, wasconducted to further investigate any issues raised by the Phase I assessment. In each case where Phase Iand/or Phase II assessments resulted in speciÑc recommendations for remedial actions required by law,management has either taken or scheduled the recommended action.

Neither the Phase I nor the Phase II assessments have revealed any environmental liability that we believewould have a material eÅect on our overall business, Ñnancial condition or results of operations. Nevertheless,it is possible that these assessments do not reveal all environmental liabilities or that there are materialenvironmental liabilities of which we are unaware. Moreover, no assurances can be given that future laws,ordinances or regulations will not impose any material environmental liability or the current environmentalcondition of our properties will not be adversely aÅected by tenants and occupants of the properties, by thecondition of properties in the vicinity of our properties (such as the presence on such properties ofunderground storage tanks) or by third parties unrelated to us.

Future development opportunities may require additional capital and other expenditures in order to complywith Federal, state and local statutes and regulations relating to the protection of the environment. It isimpossible at this time to predict with any certainty the magnitude of any such expenditures or the long-rangeeÅect, if any, on our operations. Compliance with such laws has had no material adverse eÅect on ouroperating results or competitive position in the past.

Employees

As of March 1, 2006, we had approximately 4,700 employees.

QualiÑcation as a Real Estate Investment Trust and Taxability of Distributions

General Growth currently qualiÑes as a real estate investment trust pursuant to the requirements contained inSections 856-858 of the Internal Revenue Code of 1986, as amended (the ""Code''). If, as we contemplate,such qualiÑcation continues, General Growth will not be taxed on its real estate investment trust taxableincome. During 2005, General Growth distributed (or was deemed to have distributed) 100% of its taxableincome to its preferred and common stockholders (Note 7).

Available Information

Our Internet website address is www.generalgrowth.com. Our Annual Reports on Form 10-K, QuarterlyReports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are available and maybe accessed free of charge through the Investment section of our Internet website under the Shareholder Info

6

subsection, as soon as reasonably practicable after those documents are Ñled with, or furnished to, the SEC.Our Internet website and information contained therein or connected thereto are not intended to beincorporated into this Annual Report.

Item 1A. Risk Factors

Risks Related to Real Estate Investments

We invest primarily in regional mall shopping centers and other retail properties, which are subject to anumber of signiÑcant risks which are beyond our control

Real property investments are subject to varying degrees of risk that may aÅect the ability of our retailproperties to generate suÇcient revenues. A number of factors may decrease the income generated by a retailproperty, including:

‚ the regional and local economy, which may be negatively impacted by plant closings, industry slowdowns,adverse weather conditions, natural disasters and other factors;

‚ local real estate conditions, such as an oversupply of, or a reduction in demand for, retail space or retailgoods, and the availability and creditworthiness of current and prospective tenants;

‚ perceptions by retailers or shoppers of the safety, convenience and attractiveness of the retail property;

‚ the convenience and quality of competing retail properties and other retailing options such as the Internet;

‚ changes in laws and regulations applicable to real property, including tax and zoning laws; and

‚ changes in interest rate levels and the availability and cost of Ñnancing.

If we are unable to generate suÇcient revenue from our retail properties, including those held by jointventures, we will be unable to meet operating and other expenses, including debt service, lease payments,capital expenditures and tenant improvements, and to make distributions from our joint ventures and then, inturn, to our stockholders.

We depend on leasing space to tenants on economically favorable terms and collecting rent from thesetenants, who may not be able to pay

Our results of operations will depend on our ability to continue to lease space in our properties on economicallyfavorable terms. If the sales of stores operating in our centers decline suÇciently, tenants might be unable topay their existing minimum rents or expense recovery charges, since these rents and charges would represent ahigher percentage of their sales. If our tenants' sales decline, new tenants would be less likely to be willing topay minimum rents as high as they would otherwise pay. In addition, as substantially all of our income isderived from rentals of real property, our income and cash available for distribution to our stockholders wouldbe adversely aÅected if a signiÑcant number of tenants were unable to meet their obligations to us. Duringtimes of economic recession, these risks will increase.

Bankruptcy or store closures of tenants may decrease our revenues and available cash

A number of companies in the retail industry, including some of our tenants, have declared bankruptcy orvoluntarily closed certain of their stores in recent years. The bankruptcy or closure of a major tenant,particularly an Anchor tenant, may have a material adverse eÅect on the retail properties aÅected and theincome produced by these properties and may make it substantially more diÇcult to lease the remainder of theaÅected retail properties. Our leases generally do not contain provisions designed to ensure the creditworthi-ness of the tenant. As a result, the bankruptcy or closure of a major tenant could result in a lower level ofrevenues and cash available for distribution to our stockholders.

7

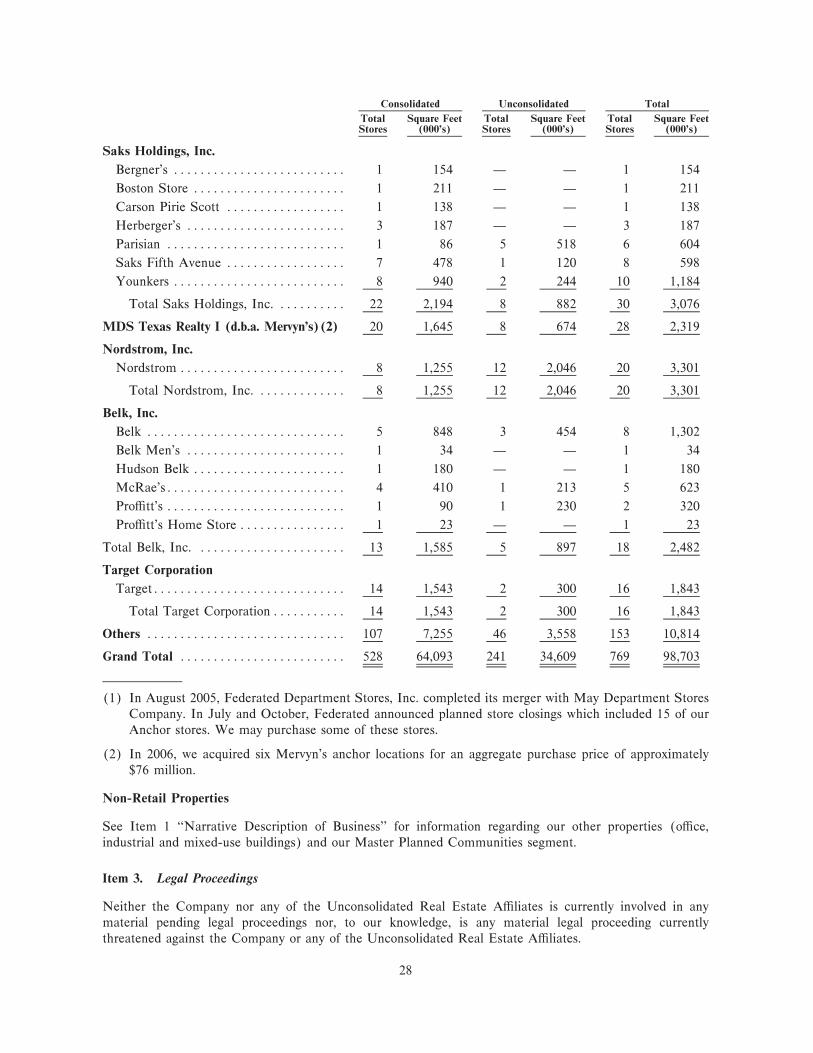

We may be negatively impacted by department store consolidations

Department store consolidations, such as K-Mart's acquisition of Sears and Federated's acquisition of MayDepartment Stores, are resulting in the closure of existing department stores and we may be unable to re-leasethis area or to re-lease it on comparable or more favorable terms. Other tenants may be entitled to modify theterms of their existing leases, including those pertaining to rent payment, in the event of such closures.Additionally, department store closures could result in decreased customer traÇc which could lead todecreased sales at other stores. Consolidations may also negatively aÅect current and future development andredevelopment projects.

It may be diÇcult to buy and sell real estate quickly, and transfer restrictions apply to some of ourproperties

Equity real estate investments are relatively illiquid, and this characteristic tends to limit our ability to vary ourportfolio promptly in response to changes in economic or other conditions. In addition, signiÑcant expendituresassociated with each equity investment, such as mortgage payments, real estate taxes and maintenance costs,are generally not reduced when circumstances cause a reduction in income from the investment. If incomefrom a property declines while the related expenses do not decline, our income and cash available fordistribution to our stockholders would be adversely aÅected. A signiÑcant portion of our properties aremortgaged to secure payment of indebtedness, and if we were unable to meet our mortgage payments, wecould lose money as a result of foreclosure on the properties by the various mortgagees. In addition, if itbecomes necessary or desirable for us to dispose of one or more of the mortgaged properties, we might not beable to obtain a release of the lien on the mortgaged property without payment of the associated debt. Theforeclosure of a mortgage on a property or inability to sell a property could adversely aÅect the level of cashavailable for distribution to our stockholders. In certain transactions, if persons selling properties to us wish todefer the payment of taxes on the sales proceeds, we are likely to pay them in units of limited partnershipinterest in the Operating Partnership. In transactions of this kind, we may also agree, subject to certainexceptions, not to sell the acquired properties for signiÑcant periods of time.

Risks Related to our Business

We develop and expand properties, and this activity is subject to various risks

We intend to continue to pursue development and expansion activities as opportunities arise. In connectionwith any development or expansion, we will be subject to various risks, including the following:

‚ we may abandon development or expansion activities, which may result in additional cost recognition;

‚ construction costs of a project may exceed original estimates or available Ñnancing, possibly making theproject unfeasible or unproÑtable;

‚ we may not be able to obtain Ñnancing or to reÑnance construction loans, which generally have full recourseto us;

‚ we may not be able to obtain zoning, occupancy or other required governmental permits and authorizations;

‚ occupancy rates and rents at a completed project may not meet projections and, therefore, the project maynot be proÑtable; and

‚ we may need Anchor, mortgage lender and property partner approvals, if applicable, for expansion orredevelopment activities.

If a development project is unsuccessful, our loss could exceed our investment in the project.

If we are unable to manage our growth eÅectively, our Ñnancial condition and results of operations may beadversely aÅected

We have experienced rapid growth in recent years, increasing our total consolidated assets from less than$2 billion at December 31, 1996 to over $25 billion at December 31, 2005. We may not be able to manage our

8

growth eÅectively or to maintain a similar rate of growth in the future, and the failure to do so may have amaterial adverse eÅect on our Ñnancial condition and results of operations.

We may incur costs to comply with environmental laws

Under various federal, state or local laws, ordinances and regulations, a current or previous owner or operatorof real estate may be required to investigate and clean up hazardous or toxic substances released at a property,and may be held liable to a governmental entity or to third parties for property damage or personal injuries andfor investigation and clean-up costs incurred by the parties in connection with the contamination. These lawsoften impose liability without regard to whether the owner or operator knew of, or was responsible for, therelease of the hazardous or toxic substances. The presence of contamination or the failure to remediatecontamination may adversely aÅect the owner's ability to sell or lease real estate or to borrow using the realestate as collateral. Other federal, state and local laws, ordinances and regulations require abatement orremoval of asbestos-containing materials in the event of demolition or certain renovations or remodeling andalso govern emissions of and exposure to asbestos Ñbers in the air. Federal and state laws also regulate theoperation and removal of underground storage tanks. In connection with the ownership, operation andmanagement of our properties, we could be held liable for the costs of remedial action with respect to theseregulated substances or tanks or related claims.

Each of our properties has been subjected to varying degrees of environmental assessment at various times.However, the identiÑcation of new areas of contamination, a change in the extent or known scope ofcontamination or changes in cleanup requirements could result in signiÑcant costs to us.

We are in a competitive business

There are numerous shopping facilities that compete with our properties in attracting retailers to lease space.In addition, retailers at our properties face continued competition from discount shopping centers, lifestylecenters, outlet malls, wholesale and discount shopping clubs, direct mail, telemarketing, television shoppingnetworks and shopping via the Internet. Competition of this type could adversely aÅect our revenues and cashavailable for distribution to our stockholders.

We compete with other major real estate investors with signiÑcant capital for attractive investmentopportunities. These competitors include other REITs, investment banking Ñrms and private institutionalinvestors. This competition has increased prices for commercial properties and may impair our ability to makesuitable property acquisitions on favorable terms in the future.

We may not be able to obtain capital to make investments

We depend primarily on external Ñnancing to fund the growth of our business. This is because one of therequirements of the Internal Revenue Code of 1986, as amended, which we refer to as the ""Code,'' for a REITgenerally is that it distribute 90% of its taxable income, excluding net capital gains, to its stockholders. Ouraccess to debt or equity Ñnancing depends on banks' willingness to lend to us and on conditions in the capitalmarkets in general. We and other companies in the real estate industry have experienced less favorable termsfor bank loans and capital markets Ñnancing from time to time. Although we believe, based on current marketconditions, that we will be able to Ñnance investments we wish to make in the foreseeable future, Ñnancingmight not be available on acceptable terms or may be aÅected by the amount of debt we have outstanding as aresult of the TRC Merger.

Some of our properties are subject to potential natural or other disasters

A number of our properties are located in areas which are subject to natural disasters. For example, two of ourproperties, located in the New Orleans area, suÅered major damage in 2005. It is uncertain as to whether theNew Orleans area will recover to its prior economic strength.

We carry comprehensive liability, Ñre, Öood, earthquake, terrorism, extended coverage and rental lossinsurance on all of our properties. We believe the policy speciÑcations and insured limits of these policies are

9

adequate and appropriate. There are, however, some types of losses, including lease and other contract claims,which generally are not insured. If an uninsured loss or a loss in excess of insured limits occurs, we could loseall or a portion of the capital we have invested in a property, as well as the anticipated future revenue from theproperty. If this happens, we might nevertheless remain obligated for any mortgage debt or other Ñnancialobligations related to the property.

If the Terrorism Risk Insurance Extension Act is not extended beyond 2007, we may incur higher insurancecosts and greater diÇculty in obtaining insurance which covers terrorist-related damages. Our tenants mayalso experience similar diÇculties.

We are subject to risks that aÅect the general retail environment