Embed Size (px)

Citation preview

Find our up-to-date analysis here:

http://election2017.ifs.org.uk

@theifs #ge2017

Institute for Fiscal Studies

General election analysis 2017

The outlook for the public finances

© Institute for Fiscal Studies The outlook for the public finances

Carl Emmerson

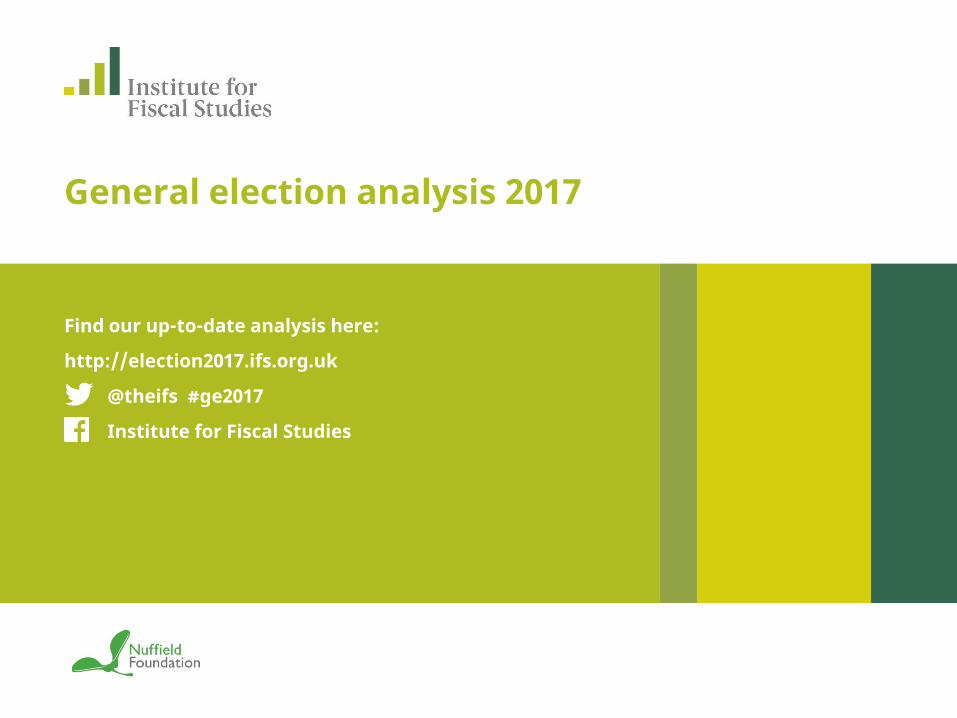

Taxes: Conservatives

Measures in the pipeline boost revenues by £5bn in 2021–22

• includes increase in dividend tax and council tax rise for social care

New tax rises: none though stated intent to reduce avoidance

New tax cuts

• increase in personal allowance and higher-rate threshold would reduce revenues by £2bn

© Institute for Fiscal Studies The outlook for the public finances

Taxes: Labour

Measures in the pipeline boost revenues by £5bn in 2021–22

No significant tax cuts

New tax rises which Labour score at £49bn (£52bn less a £3bn margin for additional behaviour change and uncertainty)

We drop £11bn of the £52bn due to • error by Labour in costing of avoidance package • central estimate of revenues from excessive pay levy and offshore

company property levy close to £0bn • lower central estimate of revenue from income tax rise

Even then £41bn very generous given downside risk of other policies • tax avoidance programme, extension of stamp duty to derivatives, and

review of corporate tax reliefs would still need to deliver £13bn • increased rate of corporation tax might raise £19bn in 2021–22 but won’t

raise that much in the long-run © Institute for Fiscal Studies The outlook for the public finances

25

30

35

40

45 19

50–5

1

1955

–56

1960

–61

1965

–66

1970

–71

1975

–76

1980

–81

1985

–86

1990

–91

1995

–96

2000

–01

2005

–06

2010

–11

2015

–16

2020

–21

Per

cent

of n

atio

nal i

ncom

e

© Institute for Fiscal Studies

National accounts taxes

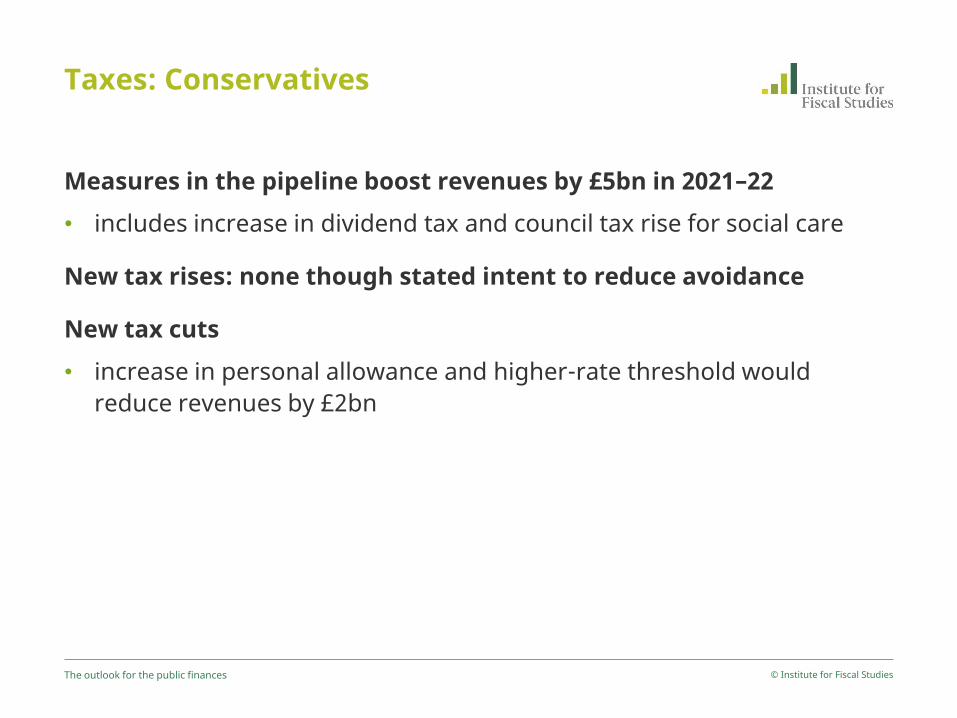

Tax receipts to climb under both Conservatives and Labour

The outlook for the public finances

Current receipts

Highest since 1969–70

Highest since 1986–87

Highest since 1949–50

Highest since 1984–85

Note: Assumes Labour’s tax measures boost revenues by £41bn and additional infrastructure spending temporarily boosts the size of the economy. Sources: Office for Budget Responsibility; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

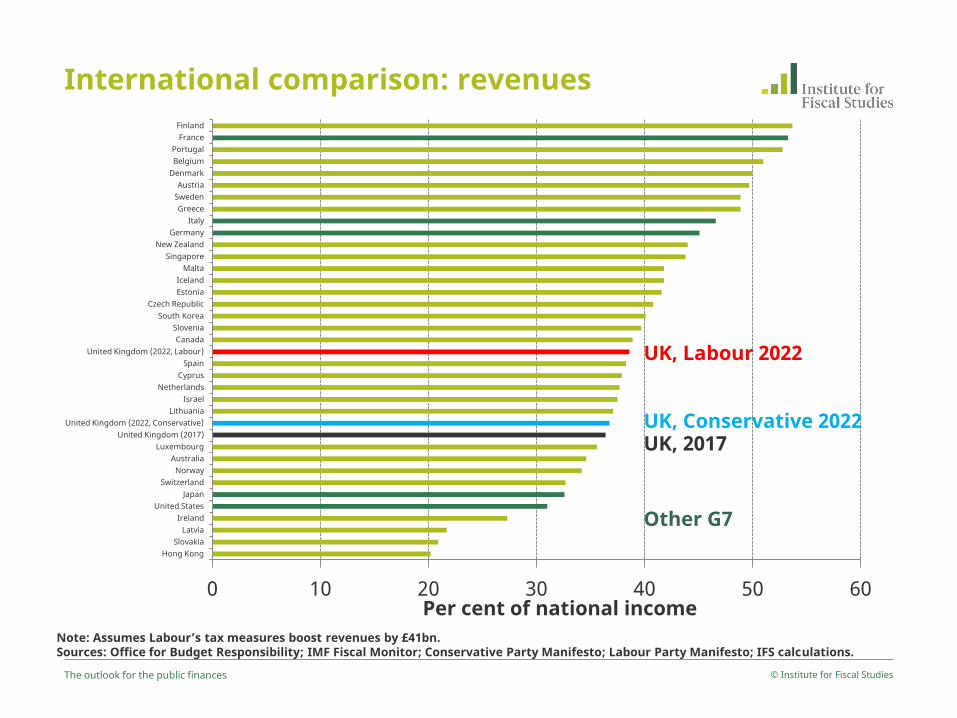

International comparison: revenues

© Institute for Fiscal Studies The outlook for the public finances

0 10 20 30 40 50 60

Hong Kong Slovakia

Latvia Ireland

United States Japan

Switzerland Norway

Australia Luxembourg

United Kingdom (2017) United Kingdom (2022, Conservative)

Lithuania Israel

Netherlands Cyprus

Spain United Kingdom (2022, Labour)

Canada Slovenia

South Korea Czech Republic

Estonia Iceland

Malta Singapore

New Zealand Germany

Italy Greece

Sweden Austria

Denmark Belgium Portugal

France Finland

Per cent of national income Note: Assumes Labour’s tax measures boost revenues by £41bn. Sources: Office for Budget Responsibility; IMF Fiscal Monitor; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

UK, Conservative 2022

UK, Labour 2022

UK, 2017

Other G7

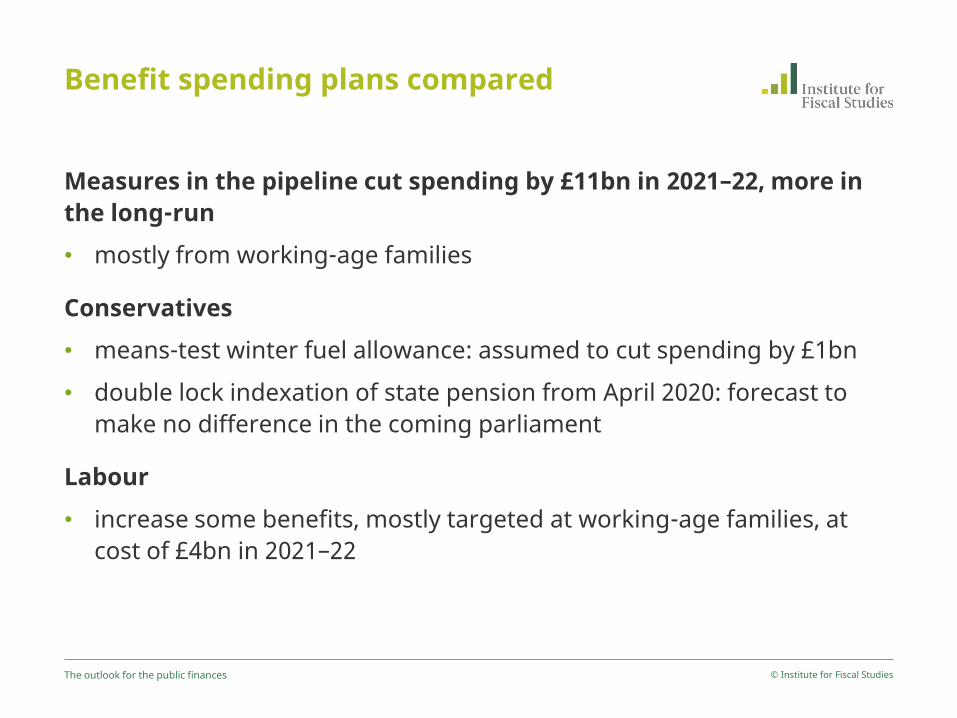

Benefit spending plans compared

Measures in the pipeline cut spending by £11bn in 2021–22, more in the long-run

• mostly from working-age families

Conservatives

• means-test winter fuel allowance: assumed to cut spending by £1bn

• double lock indexation of state pension from April 2020: forecast to make no difference in the coming parliament

Labour

• increase some benefits, mostly targeted at working-age families, at cost of £4bn in 2021–22

© Institute for Fiscal Studies The outlook for the public finances

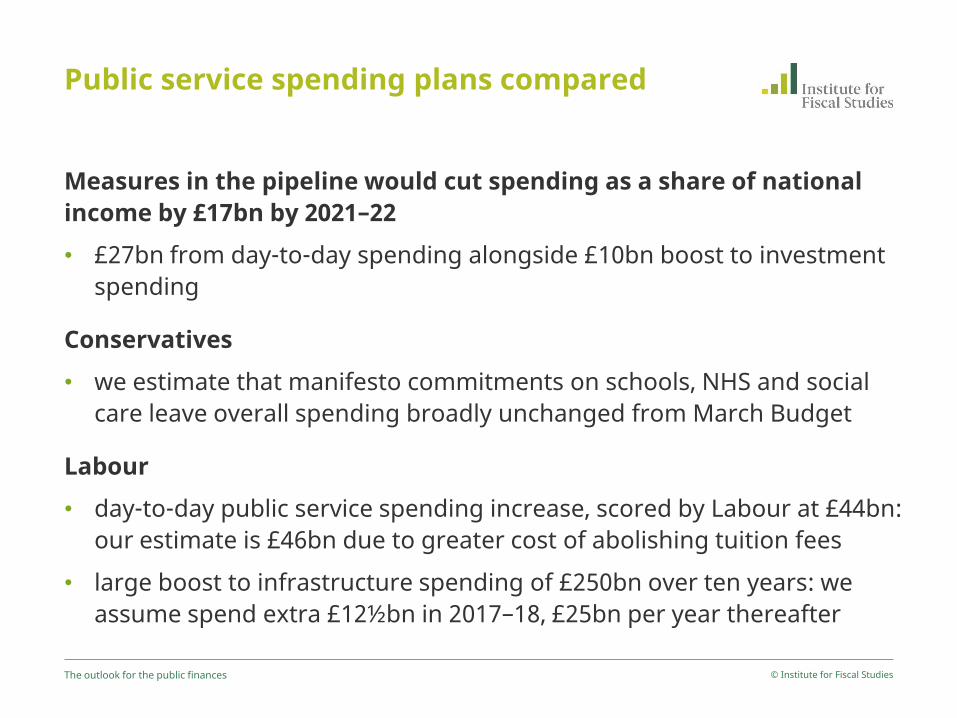

Public service spending plans compared

Measures in the pipeline would cut spending as a share of national income by £17bn by 2021–22

• £27bn from day-to-day spending alongside £10bn boost to investment spending

Conservatives

• we estimate that manifesto commitments on schools, NHS and social care leave overall spending broadly unchanged from March Budget

Labour

• day-to-day public service spending increase, scored by Labour at £44bn: our estimate is £46bn due to greater cost of abolishing tuition fees

• large boost to infrastructure spending of £250bn over ten years: we assume spend extra £12½bn in 2017–18, £25bn per year thereafter

© Institute for Fiscal Studies The outlook for the public finances

30

35

40

45

50 19

50–5

1

1955

–56

1960

–61

1965

–66

1970

–71

1975

–76

1980

–81

1985

–86

1990

–91

1995

–96

2000

–01

2005

–06

2010

–11

2015

–16

2020

–21

Per

cent

of n

atio

nal i

ncom

e

© Institute for Fiscal Studies

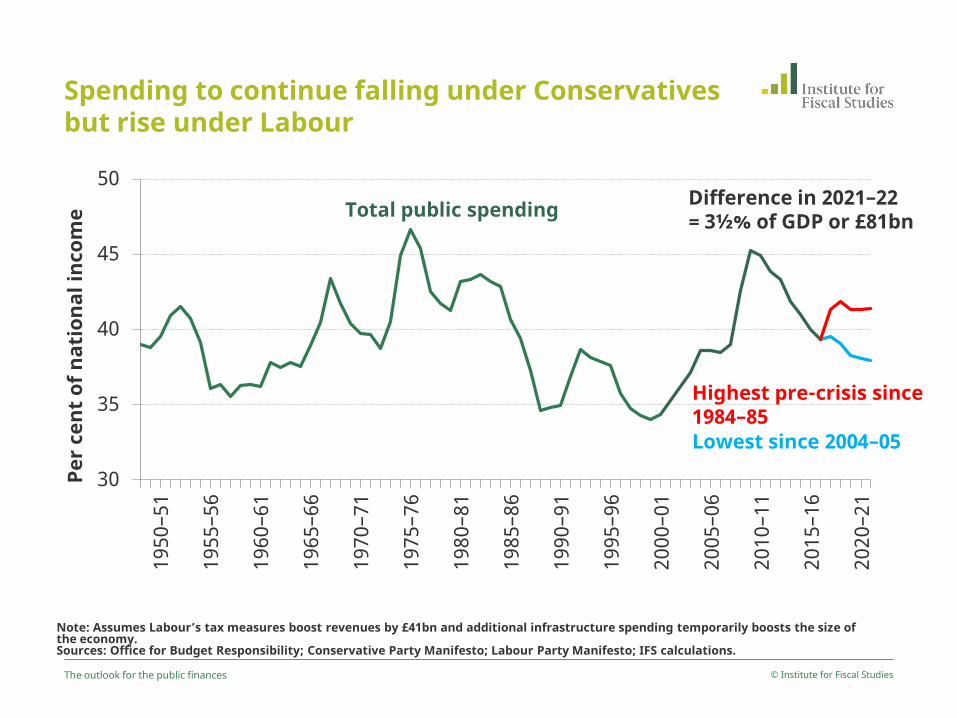

Total public spending

Spending to continue falling under Conservatives but rise under Labour

The outlook for the public finances

Lowest since 2004–05

Highest pre-crisis since 1984–85

Difference in 2021–22 = 3½% of GDP or £81bn

Note: Assumes Labour’s tax measures boost revenues by £41bn and additional infrastructure spending temporarily boosts the size of the economy. Sources: Office for Budget Responsibility; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

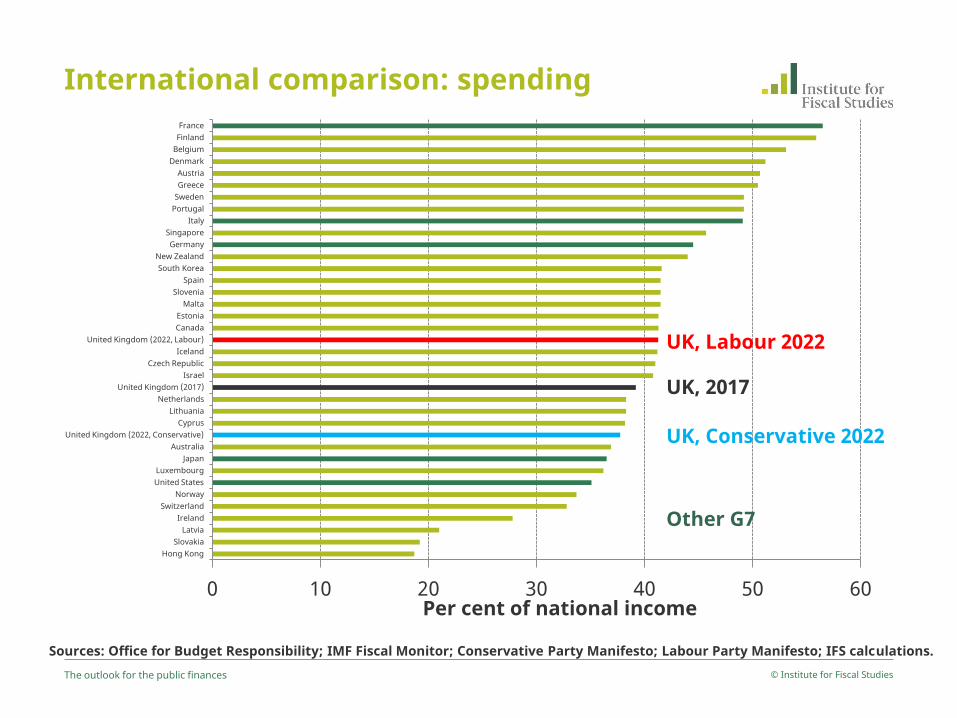

International comparison: spending

© Institute for Fiscal Studies The outlook for the public finances

0 10 20 30 40 50 60

Hong Kong Slovakia

Latvia Ireland

Switzerland Norway

United States Luxembourg

Japan Australia

United Kingdom (2022, Conservative) Cyprus

Lithuania Netherlands

United Kingdom (2017) Israel

Czech Republic Iceland

United Kingdom (2022, Labour) Canada Estonia

Malta Slovenia

Spain South Korea

New Zealand Germany

Singapore Italy

Portugal Sweden Greece Austria

Denmark Belgium Finland France

Per cent of national income

Sources: Office for Budget Responsibility; IMF Fiscal Monitor; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

UK, Conservative 2022

UK, Labour 2022

UK, 2017

Other G7

Impact on the economy

Demand

• we use the OBR’s multiplier to allow Labour’s additional infrastructure spending to boost GDP – and therefore tax receipts – in the near-term

Supply

• Labour’s significant increase in infrastructure spending, if spent well, would increase the productive capacity of the UK economy

• Labour’s increased labour market regulations such as higher minimum wage would have the opposite effect …

© Institute for Fiscal Studies The outlook for the public finances

© Institute for Fiscal Studies

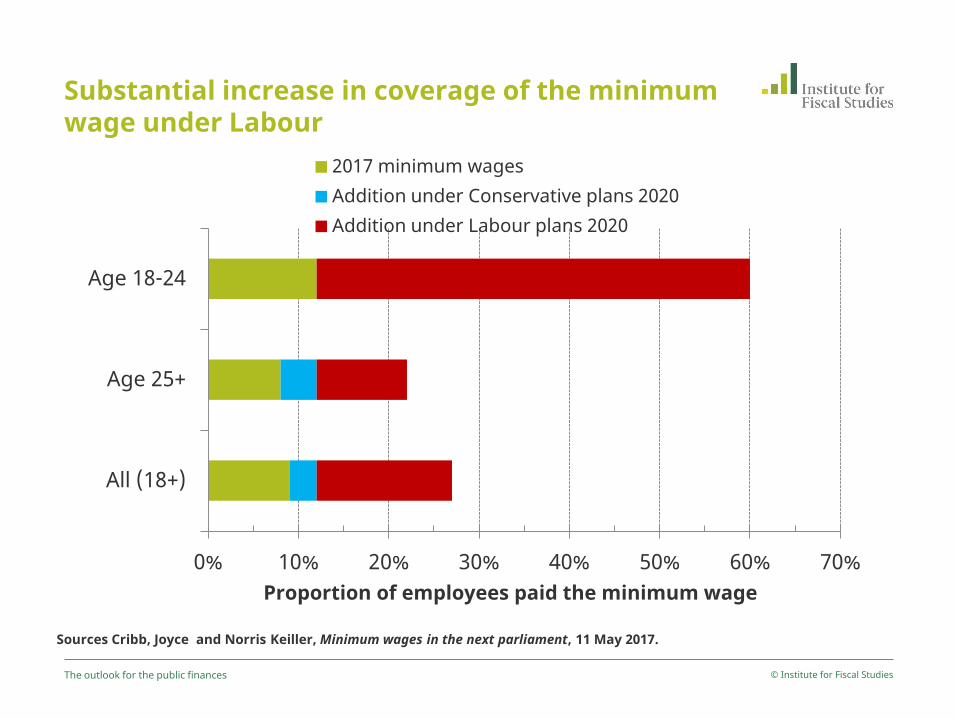

Substantial increase in coverage of the minimum wage under Labour

Sources Cribb, Joyce and Norris Keiller, Minimum wages in the next parliament, 11 May 2017.

The outlook for the public finances

0% 10% 20% 30% 40% 50% 60% 70%

All (18+)

Age 25+

Age 18-24

Proportion of employees paid the minimum wage

2017 minimum wages Addition under Conservative plans 2020 Addition under Labour plans 2020

Impact on the economy

Demand • we use the OBR’s multiplier to allow Labour’s additional infrastructure

spending to boost GDP – and therefore tax receipts – in the near-term

Supply • Labour’s significant increase in infrastructure spending, if spent well,

would increase the productive capacity of the UK economy • Labour’s increased labour market regulations such as higher minimum

wage would have the opposite effect … • … as would four additional bank holidays and Labour’s higher rate of

corporation tax • Conservatives’ commitment to reduce net immigration would, if delivered,

also weaken growth and the public finances

Despite this we assume no overall impact on productive capacity of the economy under either party’s policies

© Institute for Fiscal Studies The outlook for the public finances

Targets for borrowing

Current Government

• had committed to eliminate deficit by 2018–19

• pushed back to “as soon as possible in the next parliament”

• Budget forecasts implied further fiscal action required to achieve this

Conservatives: “balanced budget by the middle of the next decade”

• target date pushed back further

• 15 years of austerity from 2010 to 2025?

Labour: eliminate “deficit on day-to-day spending within five years”

• forward-looking target for current budget has much to commend it

• recommended in successive IFS Green Budgets, adopted by George Osborne in 2010 and Ed Balls in 2015

© Institute for Fiscal Studies The outlook for the public finances

-1

0

1

2

3

4

5

2016

–17

2017

–18

2018

–19

2019

–20

2020

–21

2021

–22

Per

cent

of n

atio

nal i

ncom

e

© Institute for Fiscal Studies

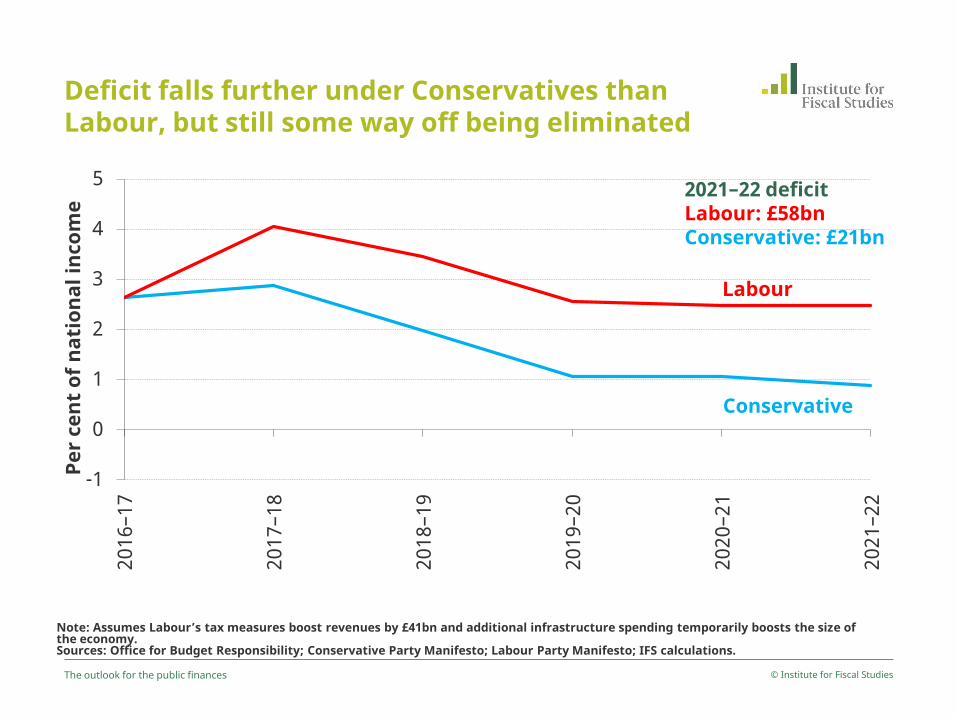

Deficit falls further under Conservatives than Labour, but still some way off being eliminated

The outlook for the public finances

2021–22 deficit Labour: £58bn Conservative: £21bn

Labour

Conservative

Note: Assumes Labour’s tax measures boost revenues by £41bn and additional infrastructure spending temporarily boosts the size of the economy. Sources: Office for Budget Responsibility; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2016

–17

2017

–18

2018

–19

2019

–20

2020

–21

2021

–22

Per

cent

of n

atio

nal i

ncom

e

© Institute for Fiscal Studies

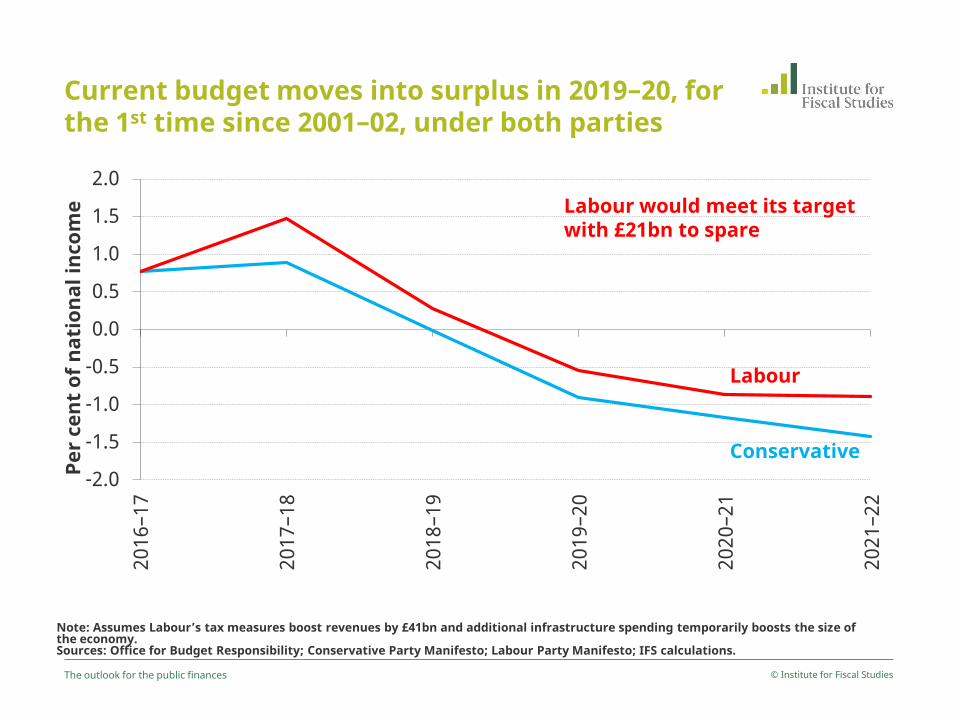

Current budget moves into surplus in 2019–20, for the 1st time since 2001–02, under both parties

The outlook for the public finances

Labour

Conservative

Labour would meet its target with £21bn to spare

Note: Assumes Labour’s tax measures boost revenues by £41bn and additional infrastructure spending temporarily boosts the size of the economy. Sources: Office for Budget Responsibility; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

Targets for debt

Current Government

• had committed to debt falling as a share of GDP in every year

• target missed and revised to debt falling as a share of GDP in 2020–21

• Budget forecast this being met with room to spare

Conservatives: no debt target specified in manifesto

Labour: ensure that, as a share of national income, “national debt is lower at the end of the next Parliament than it is today”

• good reasons to want this to fall over the longer-term, less clear that it has to be lower in 2021–22 than in 2016–17

© Institute for Fiscal Studies The outlook for the public finances

70

75

80

85

90

95

2016

–17

2017

–18

2018

–19

2019

–20

2020

–21

2021

–22

Per

cent

of n

atio

nal i

ncom

e

© Institute for Fiscal Studies

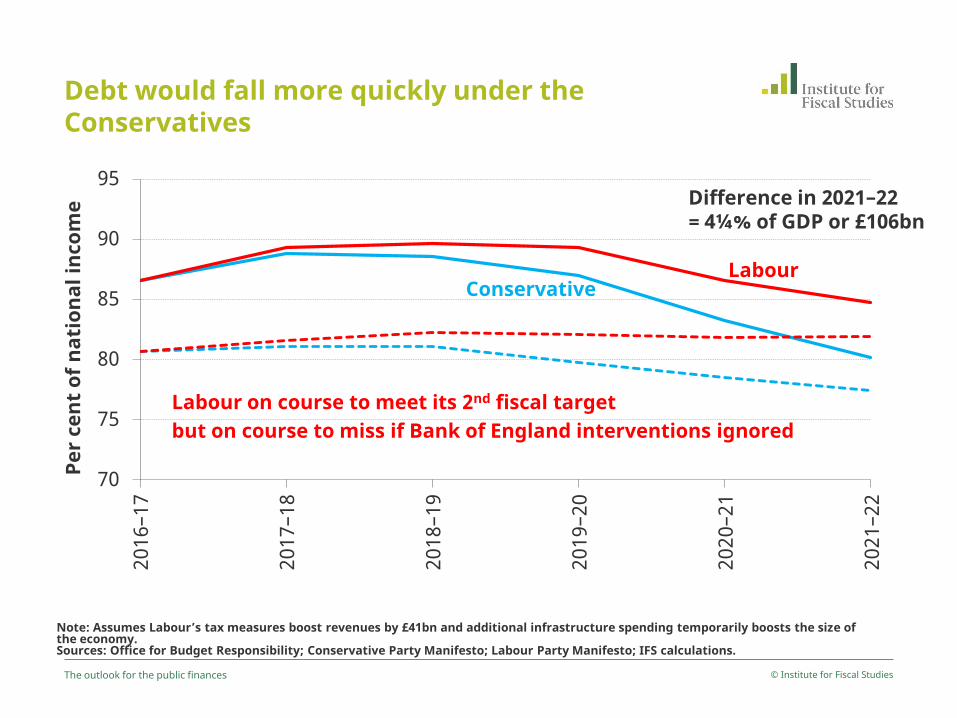

Debt would fall more quickly under the Conservatives

The outlook for the public finances

Labour Conservative

Difference in 2021–22 = 4¼% of GDP or £106bn

Labour on course to meet its 2nd fiscal target

Note: Assumes Labour’s tax measures boost revenues by £41bn and additional infrastructure spending temporarily boosts the size of the economy. Sources: Office for Budget Responsibility; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

but on course to miss if Bank of England interventions ignored

Would Labour really reduce debt as a share of national income?

Substantial increase in outlook for borrowing could still be consistent with debt falling as a share of national income

• day-to-day spending increases & extra £25bn a year on infrastructure, combined with £30bn of tax rises, could be consistent with this

But Labour’s manifesto proposes nationalisation of Royal Mail and publicly owned companies operating in rail, energy and water

• these would add to public sector net debt

Depending on scale and timing nationalisation programme could lead to Labour breaching its fiscal target

• of course higher debt would be associated with greater assets too

• what matters is whether assets would be better managed by the public or the private sector

© Institute for Fiscal Studies The outlook for the public finances

© Institute for Fiscal Studies

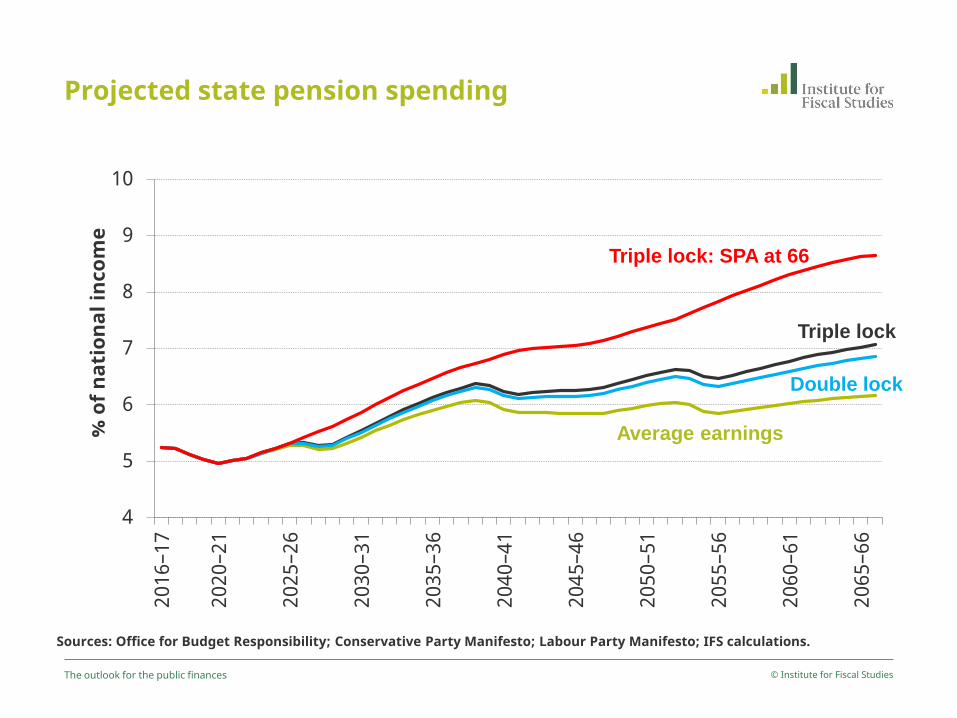

Projected state pension spending

The outlook for the public finances

4

5

6

7

8

9

10 20

16–1

7

2020

–21

2025

–26

2030

–31

2035

–36

2040

–41

2045

–46

2050

–51

2055

–56

2060

–61

2065

–66

% o

f nat

iona

l inc

ome

Triple lock: SPA at 66

Triple lock

Double lock

Average earnings

Sources: Office for Budget Responsibility; Conservative Party Manifesto; Labour Party Manifesto; IFS calculations.

Conclusions

Conservatives: modest changes relative to current Government policy

• tax burden rising and day-to-day spending being cut

• eliminating deficit pushed into parliament after next and the long-run public finance challenge would remain significant

• meeting immigration target would weaken growth and the public finances

Labour: big increase in the size and shape of the state

• very large increase in tax and borrowing maintained at current level financing a very large increase in spending, in particular on infrastructure

Particularly big downside risks with Labour’s plan

• tax measures unlikely to raise anything like the £49bn Labour wants, particularly over the longer-term

• despite increased infrastructure spending, productive capacity of economy could be harmed by proposals such as substantially increased national minimum wage

• not raising state pension age beyond 66 would make long-run public finance challenge even harder to meet

© Institute for Fiscal Studies The outlook for the public finances