Embed Size (px)

Citation preview

1

Gamuda Berhad

PTMP – Nearing the Finishing Line

Q3 2015 INVESTORS’ BRIEFING 23 June 2015

2

(RMmil) 9 mths to Apr ’15 9 mths to Apr ’14 Change (%)

Revenue 1,776.6 1,637.6 +8Profit from operations (EBIT) 467.2 369.0 +27

Finance Costs (80.2) (55.7) +44

Share of JVs (net of tax) 130.5 132.3 -1

Share of associates (net of tax) 150.1 170.2 -12

Profit before tax 667.7 615.9 +8Tax (97.2) (93.4) +4

Minority Interests (42.0) (9.0) +>100

Net profit attributable to equity holders 528.5 513.5 +3Fully diluted EPS (sen) 22.2 21.9

Dividend per share (sen) 12.0 12.0

EBIT margins (%) 26.3 22.5

PBT margins (%) 37.6 37.6

INCOME STATEMENT SUMMARY

3

FRS – 11 JOINT ARRANGEMENTS

• FRS 11 adopted since Q114 statements• Joint ventures (incorporated) now treated using equity method

(share of JVs), reported net of tax• Joint ventures (unincorporated) treated as previously, using

proportionate consolidation, reported gross of tax• Share of associates reported as previously, net of tax• Key impacts

- substantial group revenue is `lost’ as significant amount of activities are carried out by incorporated JVs

- group and divisional margins are distorted by the mixing up of pretax and net profits above the `Group PBT’ line

- no impact on net profit, but generally understates PBT- performance analyses’ becomes more difficult and tricky

4

INCOME STATEMENT (before FRS 11)(RMmil) 9 mths to Apr ’15 9 mths to Apr ’14 Change (%)

Revenue 3,439.8 3,813.9 -10

Profit from operations (EBIT) 643.7 565.8 +14

Finance Costs (86.9) (63.7) +36

Share of JVs (net of tax) - - -

Share of associates (net of tax) 150.1 170.2 -12

Profit before tax 706.9 672.4 +5

Tax (136.4) (149.9) -9

Minority Interests (42.0) (9.0) +>100

Net profit attributable to equity holders 528.5 513.5 +3

Fully diluted EPS (sen) 22.2 21.9

Dividend per share (sen) 12.0 12.0

EBIT margins (%) 18.7 14.8

PBT margins (%) 20.6 17.6

5

BALANCE SHEET SUMMARY(RMmil) As at 30 Apr ’15 As at 31 Jan ’15

Current Assets 6,385.3 6,874.4Current Liabilities 1,632.6 2,040.7

Current Ratio 3.9x 3.4x

Total borrowings 3,503.8 3,559.1

Cash and marketable securities 1,285.2 1,649.9

Net cash (2,218.6) (1,902.2)

Share capital 2,373.2 2,348.3

Reserves 3,744.7 3,623.1

Equity attributable to equity holders 6,117.9 5,971.5

Net gearing (overall) 36% 32%Net assets per share (RM) 2.58 2.54

6

QUARTERLY SEGMENTAL PROFITS (before FRS 11, one-offs)

(RMmil) Q314 Q414 Q115 Q215 Q3 `15 Q3 `14 +/-Construction & Eng 89.5 53.3 53.7 75.0 63.2 89.5 -29Properties 83.6 75.0 81.7 64.8 81.8 83.6 -2Concessions 67.2 114.6 111.0 97.2 78.6 67.2 +17

Group Pretax Profit 240.3 242.9 246.4 237.0 223.5 240.3 -7Group Net Profit 177.9 198.8 185.8 182.2 160.4 177.9 -10

% 9M `15 9M `14Construction 8.6 8.2

Properties 25.7 26.3

Concessions n.m. n.m.

Group PBT 20.6 17.6

YTD PBT Margins (RMmil) 9M `15 9M `14 +/-Construction 191.8 228.4 -16

Properties 228.3 238.2 -4

Concessions 286.8 205.8 +39

Group PBT 706.9 672.4 +5

YTD Segmental PBT

7

KEY HIGHLIGHTS• Earnings slowdown continues in Q3 – ytd, revenue fell 10%, PBT rose 5% and net

profit rose a marginal 3%; slowing earnings growth a reflection of rapidly-completing civil works on KVMRT1, and 2-year property slowdown

• KVMRT2 roll-out making good progress – public display completing without issues; PDP signing likely in 2 months; preQ for civil works ongoing; tender-calling by end 2015, major civil awards from mid-2016 onwards, line completion in 2022

• KVMRT2 mostly similar to KVMRT1 – dual roles for Gamuda JVs – PDP for elevated works and only local contractor fully qualified to tender for underground works

• Penang Transport Master Plan (PTMP) – making good progress; PDP outcome expected soon; significant financial impact if successful

• Splash negotiations to resume soon – awaiting resolution of master agreement between Federal and State; negotiations will resume thereafter

• Property sector likely bottomed out – looking for gradual recovery in 2016, well-positioned to ride upturn, on track for RM1.2bn presales target for FY15

8

KEY CORPORATE UPDATES• KVMRT2 – prequalification of civil contractors ongoing with fast-track option; key targeted milestones – tender calling (Q4

2015), major civil packages awards (from mid-2016), line completion (2022); PDP agreement signing in 2 months

• KVMRT1 - cumulative financial progress on underground works at 68% (+7%) and PDP scope 55% (+5%) respectively at end Q3; on track to meeting cost and time KPIs

• PDP progress – foundations (100%), pier construction (98%); elevated guideways (92%); SBG production (100%), track-laying (60%), train testing underway, other systems, M&E works progressing at full momentum

• Penang Transport Master Plan (PTMP) – 2 groups shortlisted; intensive negotiations ongoing, PDP terms, scope being fine-tuned; PDP outcome expected soon, with appointment shortly thereafter; another long-term income stream if successful

• New land parcel acquired – 18-acre leasehold parcel for Bukit Bantayan project in Kota Kinabalu, Sabah for RM100m

• Three upcoming property launches in FY16 (total RM1.7bn GDV) – HighPark Suites (Kelana Jaya), Chapel Street (Melbourne), Bukit Bantayan (Sabah)

• Celadon City project now wholly-owned – purchased 40% stake from Sacomreal for USD46.5m (RM168m); buyout will facilitate more aggressive marketing, stronger branding, and improved sales

• New Singapore project likely – cycle now appears favourable; a 50% Gamuda-led JV emerges highest bidder for SGD650m Toa Payoh project; SGD345.9m bid price translates into SGD755 psf; matured neighbourhood with strong demand for private residences; excellent location

• Property presales – RM810m in 9 months (-46% y-o-y); RM280m in Q3 (-44% y-o-y); RM1.3bn unbilled sales at end Q3; full year projections maintained at RM1.2bn; growing evidence that sector has bottomed-out

9

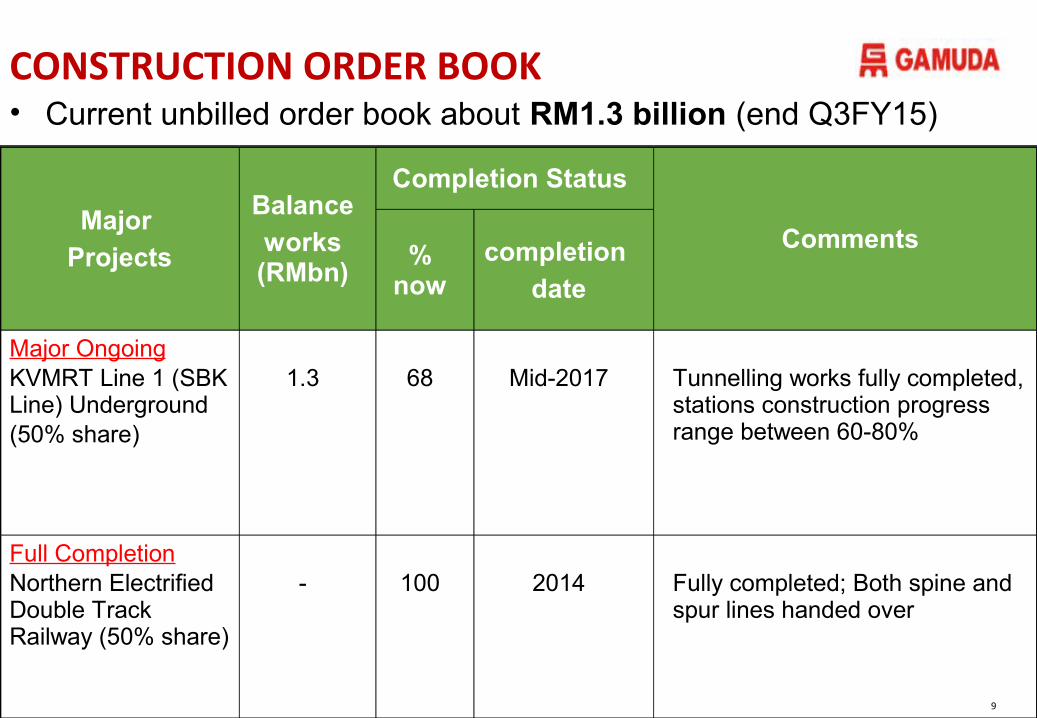

CONSTRUCTION ORDER BOOK

Major Projects

Balance works (RMbn)

Completion Status

Comments% now

completion date

Major OngoingKVMRT Line 1 (SBK Line) Underground(50% share)

1.3 68 Mid-2017 Tunnelling works fully completed, stations construction progress range between 60-80%

Full CompletionNorthern Electrified Double Track Railway (50% share)

- 100 2014 Fully completed; Both spine and spur lines handed over

• Current unbilled order book about RM1.3 billion (end Q3FY15)

10

CONSTRUCTION OUTLOOK• Slightly slower Q3 billings as pace of civil works start to taper off; ytd,

revenues decline 20% to RM2.24bn whilst PBT fell 16% to RM192m y-o-y; unbilled order book at RM1.3bn

• PBT margin holds steady at 9.2% in Q3 compared to 9.4% in Q2

• KVMRT1 – tunnelling works fully completed; tracks, systems, electrification, signalling, train testing works are all progressing on schedule

• KVMRT2 – all progressing smoothly; public display completing soon; civil tenders to be called in Q4 2015; major civil awards by mid-2016; PDP agreement expected to be signed within 2 months;

• Penang Transport Master Plan (PTMP) – in final shortlist; PDP outcome expected within 2 months; PDP appointment shortly thereafter; significant long-term financial impact if successful

• New project opportunities – Gemas-JB double track, Pan Borneo Highway

11

PROPERTIES OUTLOOK• Steady Q3 performance; ytd, revenue slipped 2% to RM887m whilst PBT

slipped 4% to RM228m; PBT margin remained stable at 26%• Group achieved new presales of RM810m (-46%) ytd; unbilled sales stands

at RM1.3bn; Q3 presales came in at RM280m (-44%)• Market appears to have bottomed-out; recovery may be more evident from

2016 onwards; group now well-positioned for the next upcycle• Acquired a 19-acre leasehold parcel in Kota Kinabalu for RM100m (Bukit

Bantayan); plan to develop 1500 apartments; RM710m GDV over 8 years; launch in 2016

• Equity stake in Celadon City increased to 100% after buyout of 40% stake from Sacomreal for USD46.5m (RM168m)

• A 50% Gamuda-led JV emerged the highest bidder for a 12,154 sq m piece of leasehold land in Toa Payoh, Singapore; very tight bids with the top 5 bidders’ prices within a 4% range

12

BUKIT BANTAYAN – KEY HIGHLIGHTS

• Size: 18 acres• Purchase price: RM100m or RM125psf• GDV: RM710m over 8 years• Tenure: Leasehold • Location: 7km east of Kota Kinabalu, Sabah• Road access: Jalan Bantayan-Minintod, Inanam• No of units: 1,500 - with average built-ups of 1,000 sq ft each• Features: Likely among the earliest earthquake-resistant

developments in Sabah

13

KK19 SITE

Inanam Town

Sabah Golf & Country

Club

Sayfol Int. School

Sabah Int. School

Jalan

Lint

as

Jalan

Dut

a

Jalan

Tun R

azak

Jalan Penampang

Jalan

Ban

tayan

-Mini

ntod

Jalan

Tun F

uad S

tephe

n

Jalan kiansom

Kota Kinabalu Airport

SJK(C) Yik Nam

Queen Elizabeth

HospKK

Specialist Center

Town Center

Sutera Harbor Resort City Mall

5KM

Rad

ius

10KM

Rad

ius

10KM Radius

5KM Radius

Jalan

Tuara

n By

pass

Jalan

Tuara

n

Jalan Tu

aran

Jalan Kolam

View A

View B

View CTshung Tshin

School

Kian Kok School

View A: View towards Likas Town

View B: View towards Likas Town with ridge at background

View C: View towards project site

BUKIT BANTAYAN –SITE LOCATION MAPSite Location

14

CHAPEL STREET – KEY HIGHLIGHTS• Size: 1435 square metres (0.35 acres)• Purchase price: AUD 40 million or AUD27,875 psm• GDV: RM400m (AUD130m) over 3 years• Tenure: Freehold• Land status: Mixed-use development land• Location: In South Yarra, Melbourne, about 4 km from

CBD• Accessibility: Highways, Train, Tram• Target Market: Business Executives, Professionals, Investors,

Inter-state and International Migrants, Urban families

15

THE SITE

SOUTHKENSINGTON

MACAULAY

NORTHMELBOURNE

SOUTHERNCROSS FLINDERS ST

RICHMOND

EAST RICHMOND BURNLEY

HAWTHORN GLENFERRIEAUBURN

SOUTH YARRA

HAWKSBURN

TOORAK

MELBOURNE CBD

SOUTHBANK

DOCKLANDS

SOUTHMELBOURNE

FAWKNERPARK

VICTORIAHARBOUR

UNIVERSITY OFMELBOURNE

BURNLEYGOLF

TOALAMEIN, LILYDALE

& BELGRAVE

TOFRANKSTON,

STONY POINT,CRANBOURNE,

PAKENHAM

HEYINGTON

KOOYONG

TOORONGA

TOGLEN

WAVERLY

OLYMPICPARK

CARLTONGARDENS

FITZROYGARDENS

ROYAL BOTANICGARDEN

MELBOURNE

COMOPARK

ORRONGPARK

CITIZENPARK

YARRA BENDPARKVICTORIA

PARK

VICTORIAGARDENS

VICTORIAPARK

CENTRALPARK

ST JAMESPARK

ABERDEEN STPARK

TOUPFIELD

TOSUNBURY,WERIBEE,

WILLIAMSTOWN

TOCRAIGIEBURN

ST VINCENTGARDENS

EDWARDSPARK

LAGOONRESERVE

GASWORK ARTPARK

ALBERTPARK LAKE

RICHMOND

COLLINGWOODCARLTON

NORTHMELBOURNE

WESTMELBOURNE

SOUTH YARRA

HAWTHORN

KEW

ABBOTFORD

TOORAK

PARKVILLE

WINDSOR

ARMADALE

PORTMELBOURNE

HAWTHORN EAST

CAMBERWELL

FITZROY

BURNLEY

YARRA RIVER

CHAPEL STREET - LOCATION MAP

16

CONCESSIONS OUTLOOK• Stable concession earnings in Q3

• Kesas now a 70%-subsidiary and is fully consolidated;

• Water restructuring – awaiting resolution of master agreement between Federal and State governments

• Splash disposal negotiations expected to resume after water restructuring issues resolved

17

Thank You

![RESORT LIFESTYLE | SMART LIVING · 2020. 6. 18. · pemaju: gamuda land (t12) sdn bhd [199401024746(310424-m)] • gamuda cove experience gallery, persiaran cove sentral, bandar gamuda](https://img.pdfslide.us/doc/110x75/60c53faa48bd340d8b3381a2/resort-lifestyle-smart-living-2020-6-18-pemaju-gamuda-land-t12-sdn-bhd.jpg)