Embed Size (px)

Citation preview

Future Power Generation in Georgia

Georgia Climate Change SummitMay 6, 2008

Danny Herrin, Manager

Climate and Environmental Strategies

Southern Company

Historical Electricity GenerationUnited States, 1990-2006

0

500

1000

1500

2000

2500

3000

3500

4000

4500

1990 1992 1994 1996 1998 2000 2002 2004 2006

Mill

ion

MW

h .

OtherNatural gasPetroleumCoalOther RenewableHydroNuclear

Data Source: Energy Information Administration, US Department of Energy

1990 - 52%

2006 - 49%

Historical Electricity GenerationGeorgia, 1990-2006

0

20

40

60

80

100

120

140

160

1990 1992 1994 1996 1998 2000 2002 2004 2006

Milli

on M

Wh

.

OtherNatural gasPetroleumCoalOther RenewableHydroNuclear

Data Source: Energy Information Administration, US Department of Energy

1990 - 67%

2006 - 63%

Nuclear

Hydro

Other Renewable

Coal

Petroleum

Natural gas

Other

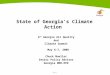

Current Electricity GenerationSelected southeastern states, 2006

Georgia

Alabama

South Carolina

Florida Alabama

63%39%

55%

51%23%

29%43%

23%

Data source: Energy Information Administration

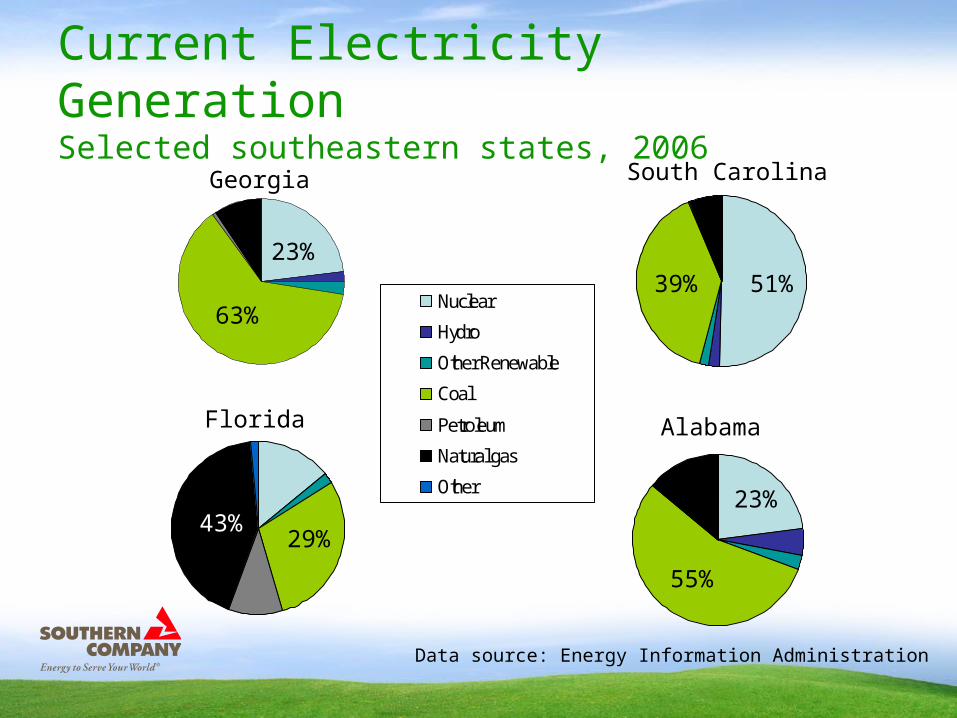

U.S. Electricity Generation by RegionHistory and projection, 1990-2030

0%

20%

40%

60%

80%

100%

120%

1990 1995 2000 2005 2010 2015 2020 2025 2030

Ch

ang

e fr

om

m 1

990

Southeast (SERC, FRCC: AL, AR, FL, GA, LA, W MO, MS, NC, SC, VA)

US

West (WECC: AZ, CA, CO, ID, MT, NV, NM, OR, UT, WA, WY)

Northeast (CT, DE, ME, MD, MA, NH, NJ, NY, PA, RI, VT)

Midwest (ECAR: IN, KY, MI, OH, WV)

Data Source: Energy Information Administration, US Department of Energy

ProjectionHistory

Projected growth

2008-2030

34%

25%34%

22%

11%

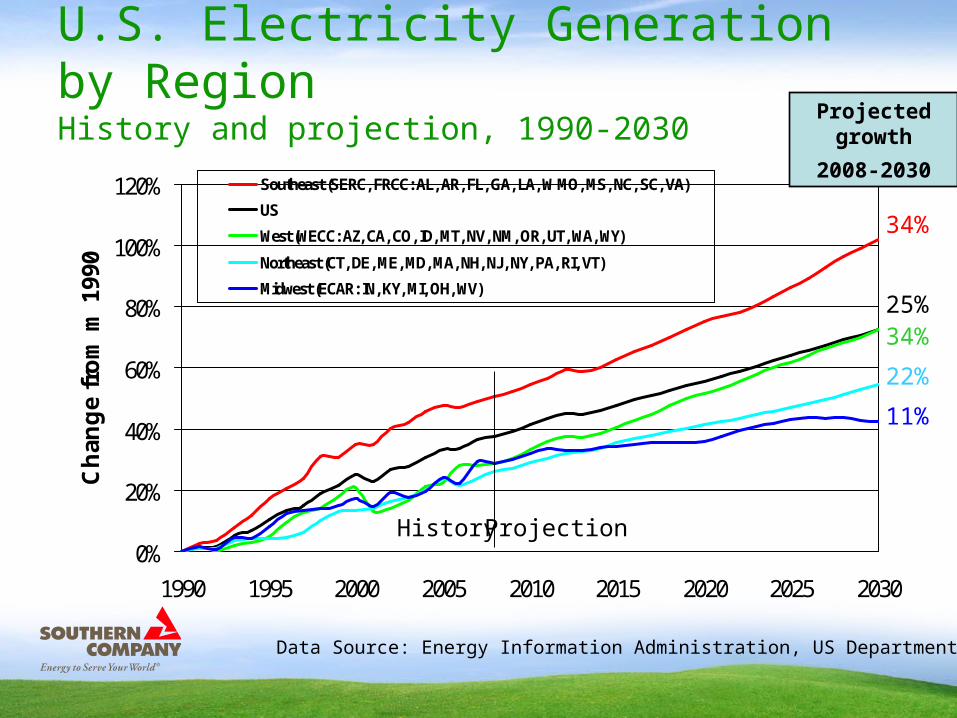

Projected Electricity GenerationSoutheast US, EIA Reference Case projection, 2008-2030

0

200

400

600

800

1000

1200

1400

1600

1800

2008 2012 2016 2020 2024 2028

Milli

on M

Wh

.

OtherNatural gasPetroleumCoalRenewableNuclear

Data Source: Energy Information Administration, Annual Energy Outlook 2007

2008 - 47%

2030 - 57%

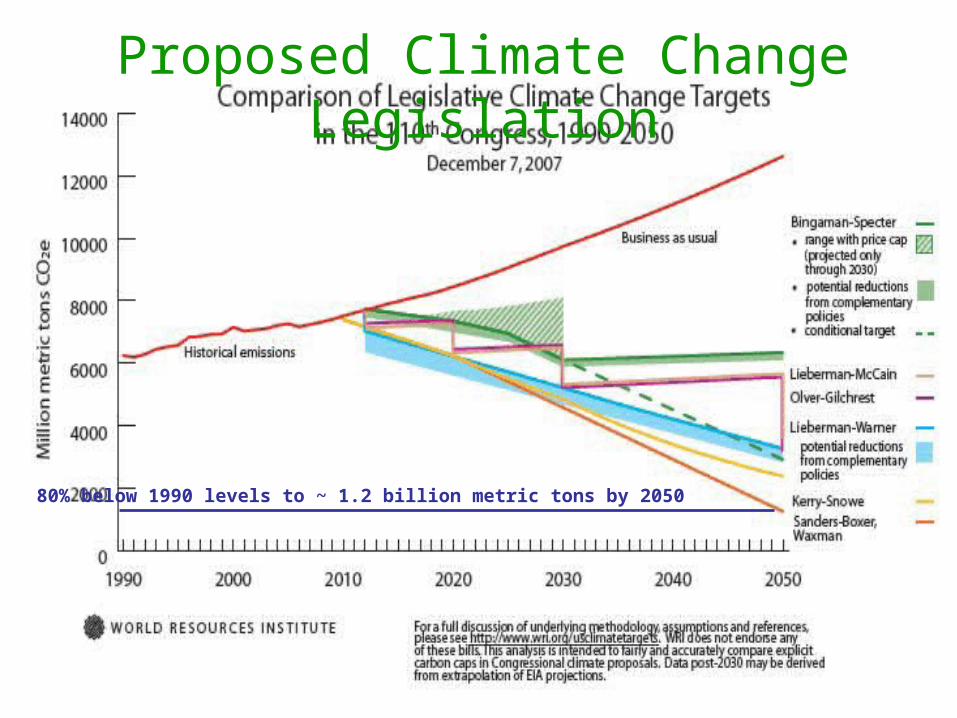

Proposed Climate Change Legislation

80% below 1990 levels to ~ 1.2 billion metric tons by 2050

The Real Cost of Tackling Climate Change• U.S. population is expected to be around 420 million by 2050.• To meet the 80% below 1990 levels by 2050 we would have to

reduce U.S. emissions to ~1 billion metric tons or go from ~20 tons per capita to ~2.5 tons per capita.

• France and Switzerland that generate almost all their electricity from non-fossil fuels are at about 6.5 tons per capita.

• Replacing every existing coal plant with a natural gas plant would still put us at twice the 2050 target.

• If everyone drove a Toyota Prius in 2050 the equivalent transportation target would be overshot by 40%.“The Real Cost of Tackling Climate Change” Steven F. Hayward Wall Street Journal - April 28, 2008

Generating Options

• Pulverized coal • Integrated gasification combined cycle• Natural gas combined cycle • Nuclear • Renewable energy• Carbon capture and sequestration

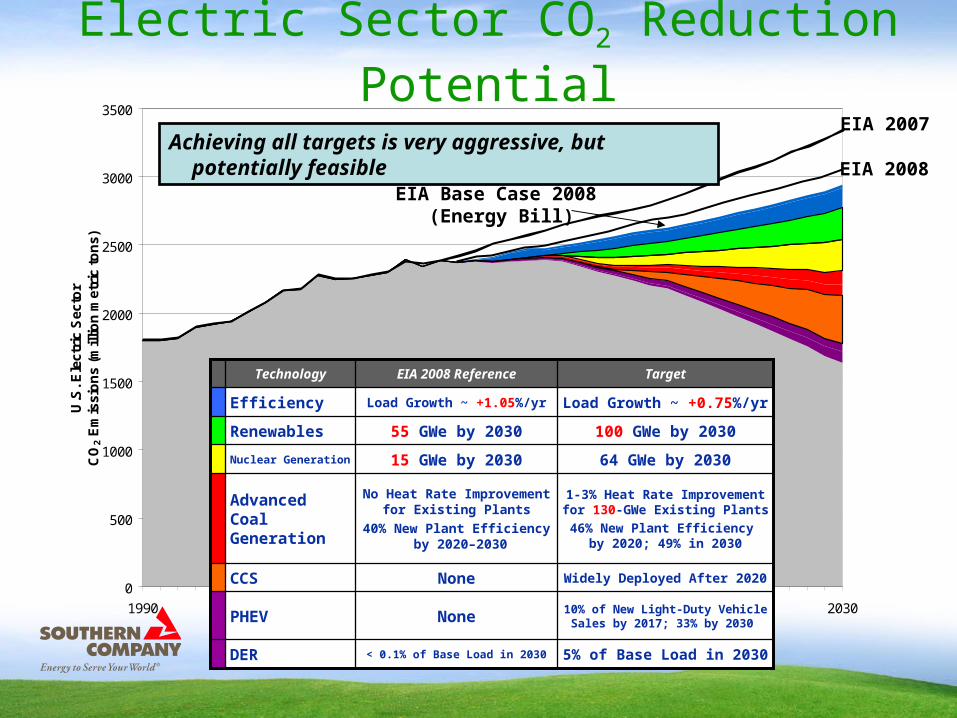

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2015 2020 2025 2030

U.S

. Ele

ctri

c S

ecto

rC

O2 E

mis

sio

ns

(mill

ion

met

ric

ton

s)

EIA 2008

1-3% Heat Rate Improvement for 130-GWe Existing Plants

46% New Plant Efficiency by 2020; 49% in 2030

No Heat Rate Improvement for Existing Plants

40% New Plant Efficiency by 2020–2030

Advanced Coal Generation

5% of Base Load in 2030< 0.1% of Base Load in 2030DER

10% of New Light-Duty Vehicle Sales by 2017; 33% by 2030

NonePHEV

Widely Deployed After 2020NoneCCS

64 GWe by 203015 GWe by 2030Nuclear Generation

100 GWe by 203055 GWe by 2030Renewables

Load Growth ~ +0.75%/yrLoad Growth ~ +1.05%/yrEfficiency

TargetEIA 2008 ReferenceTechnology

EIA Base Case 2008 (Energy Bill)

Electric Sector CO2 Reduction Potential

Achieving all targets is very aggressive, but potentially feasibleEIA 2007

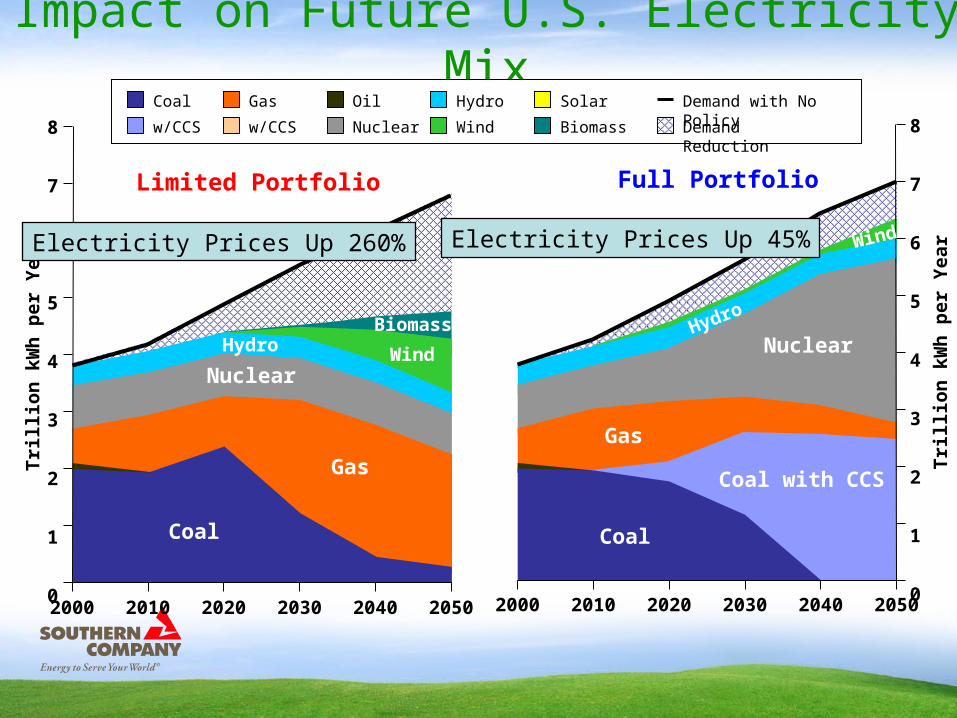

Full Portfolio

8

7

6

5

4

3

2

1

02000 2010 2020 2030 2040 2050

Trill

ion

kWh

per Y

ear

8

7

6

5

4

3

2

1

02000 2010 2020 2030 2040 2050

Trill

ion

kWh

per Y

ear

Limited Portfolio

Impact on Future U.S. Electricity MixCoal

w/CCS

Gas

w/CCS Nuclear

Hydro

Wind

SolarOil

Demand Reduction

Demand with No Policy

Biomass

Coal Coal

Coal with CCSGas

Gas

Nuclear

NuclearHydro

Hydro Wind

Biomass

WindElectricity Prices Up 260% Electricity Prices Up 45%

Climate Change Technology Development Timeline

2005 2010 2015 2020 2025

Renewables

IGCC Capture & Storage Demo Projects

New Nuclear

Retail and Generation Energy Conservation and Efficiency Improvements

Capture & Storage Commercial?

Insights from Recent EPRI Work• The technical potential exists for the U.S. electricity sector to

significantly reduce its CO2 emissions over the next several decades.

• No one technology will be a silver bullet – a portfolio of technologies will be needed.

• Much of the needed technology is not available yet – substantial R&D, demonstrations are required.

• A low-cost, low-carbon portfolio of electricity technologies can significantly reduce the costs of climate policy.

Key FindingsEIA Analysis of Lieberman-Warner S.2191

“The electric power sector accounts for the vast majority of the emissions reductions, with new nuclear, renewable, and fossil plants with CCS serving as the key compliance technologies in most cases. Manyexisting coal plants without CCS are projected to be retired early because retrofitting with CCS technology is generally impractical.”“If new nuclear, renewable, and fossil plants with CCS are not developed and deployed in a timeframe consistent with the emissions reduction requirements, covered entities are projected to turn to increasednatural gas use to offset reductions in coal generation, resulting in

markedly higher delivered prices of natural gas.”

Seeking Solutions - Some of Southern Company’s Notable Initiatives

• Developed, with KBR and DOE, TRIGTM advanced coal gasification technology • Leading a consortium that is researching:

• CO2 deep saline injection demonstration at Mississippi Power’s Plant Daniel • CO2 injection into unmineable coal seams in Alabama • Capacity of an Alabama oil field for CO2 storage

• Researching biomass co-firing • Evaluating conversion of selected coal plants to 100 percent biomass • Planting trees – 45 million, and counting • Winner of 2008 Excellence in ENERGY STAR® Promotion Award for Georgia Power’s compact fluorescent light bulb program• Evaluating significant new nuclear and IGCC generation

Southern Company’s Climate Change Policy Climate change is a challenging issue for our world and our nation. Southern Company is committed to a leadership role in finding solutions that make technological, environmental and economic sense. The focus of this effort must be on developing and deploying technologies that reduce greenhouse gases while making sure that electricity remains reliable and affordable. Southern Company believes that this is the most responsible approach to meeting the needs of the environment and its customers and shareholders.