Embed Size (px)

Citation preview

Future directions for foreign banks in China 2014

01. Foreword: EY’s insights on the report findings 4

02. Findings at a glance 6

03. Overview of the current landscape 14

04. The regulatory framework 36

05. Digital developments 48

06. Performance and growth 52

07. Product and segment developments 62

08. Human resource developments 70

09. Research methodology 76

10. Appendices 78

Contents

4 I Future directions for foreign banks in China 2014

Future directions for foreign banks in China 2014 I 5

01. The world continues to watch China with interest, looking to this important Asia hub as a source of growth and development. For non-Chinese companies, ambition to share in the success of this booming market and tap into the benefits of its vast population and increasing middle class is driving more investments.

While the size of prize is significant, gaining traction is not without its challenges. At the end of 2013, market share of foreign banks in mainland China was just 1.73%, which is not reflective of what foreign banks have committed to the China market.

In this, the second annual EY Future directions for foreign banks in China report, we examine the challenges facing players as they push to improve their footprint in China. We look at the trends and regulatory reform that is shaping the market and offer insights into ways of driving growth – now and in the future.

For example, consumer banking continues to be a challenging space for the foreign banks in two key areas. Firstly, the difficulties of limited physical distribution channels put them at a distinct disadvantage to the local banks. While online and mobile banking offer a way of working around this and attracting the attention of the younger, upwardly mobile financial consumer segment, the prevalence of non-banks, such as Alibaba and WeChat, highlight the second key challenge faced by foreign banks in the retail space. These groups, which typically operate outside of the regulatory net, offer arguably more attractive alternatives to consumers and contribute to the challenge of achieving a profitable retail banking operation. In March 2014, the regulators approved the set-up for five new privately-owned banks, a move that will further increase competition. Arguably, foreign players with a focus on retail banking would need to ask themselves if this will continue to be a primary focus in the future.

The regulatory landscape continues to confront foreign players with respondents this year ranking it their second most significant challenge. The move towards renminbi internationalization and interest rate liberalization topped this list of concerns followed by the creation of the Shanghai Free Trade Zone. It is clear that to be successful in China, it is critical that the foreign players keep on top of regulatory change. Indeed, as this report went to press, China’s Legislative Affairs Office of the State Council issued draft regulations to introduce for the first time a bank insurance deposit scheme covering deposits up to a maximum of RMB500,000, expected to take effect from early 2015. Deposit insurance is considered a precondition for liberalizing deposit interest rates and the final step required in achieving interest rate liberalization. This change will have widespread impacts for both domestic and foreign financial institutions; however, foreign financial institutions will likely be better positioned to respond swiftly to this change when formalized.

Finally, partnerships with domestic players as a means to achieving market penetration and growth continues to evolve slowly. The 20% investment ceiling to restrict the shareholdings of foreign banks in domestic operations no doubt contributes to the appetite of foreign banks to explore this as a means to expanding their operations in China. Notably, respondents indicated the investment ceiling as the fifth most significant regulatory challenge they face. Given the relative influence a holding of that size provides, foreign banks should consider both the financial and strategic benefits of such an arrangement in their decision making.

The challenges for foreign banks are real, but not insurmountable, and the potential for rewards for those who drive growth in this market remain unparalleled.

EY would like to thank the CEOs and senior executives of the 41 foreign banks operating in mainland China who have contributed to this report. We would also like to thank the report’s co-author, Dr. Brian Metcalfe.

Foreword: EY’s insights on the report findings

Jack Chan Managing Partner, EY Greater China Financial Services

6 I Future directions for foreign banks in China 2014

Future directions for foreign banks in China 2014 I 7

02. This report examines the future directions that foreign banks may take in mainland China. The interviews with CEOs and senior bank executives of foreign banks were conducted as China wrestles with the many issues surrounding financial reform and economic uncertainty.

It is now a year since the launch of the Shanghai Free Trade Zone (SFTZ) and while many foreign banks have set-up operations in the SFTZ, they have not yet been able to leverage its potential. Interest rate liberalization and renminbi (RMB) internationalization remain poised for further advancement.

Recent evidence suggests progress will continue in 2015. On 30 November 2014, a broad outline for a deposit insurance scheme was announced. Shortly thereafter, on 21 December 2014, rules governing RMB licenses for foreign banks were eased and the non-callable allocation of operating capital of no less than RMB 100 million or an equivalent amount in convertible currencies from the parent bank for set-up of a new branch was removed, both to be effective as of 1 January 2015.

A “big bang” moment was never anticipated. However, there is continued optimism that new opportunities may be just around the corner. Such opportunities will not only add new momentum to the foreign banks’ operations within China, but lead to an upswing in offshore businesses if, and when, controls on the RMB are finally relaxed.

Findings at a glance

Foreign banks are represented by over 400 different financial institutions in mainland China. This figure includes locally-incorporated foreign banks, branches, and subsidiaries. Foreign banks are present in 69 cities and 27 provinces in China.

In 2013, these banks had total assets of RMB2.56 trillion and after tax profits of RMB14.03 billion.

However, growth in the total assets of the foreign banks slowed to 7.66% in 2013 from 10.66% in 2012.

Foreign banks have made great efforts to build their presence in China. Based on China Banking Regulatory Commission (CBRC) Annual Report 2013, 42 foreign banks have established locally-incorporated units since 2007, and there are now 92 foreign bank branches. These banks hope to benefit from new opportunities inside China as a result of domestic financial reforms, but also increasingly, from opportunities that arise as Chinese corporates expand internationally across their global networks.

It is unlikely that many new foreign banking entities will enter the mainland China market over the next five years, with the exception of Taiwanese banks and banks from other parts of Asia.

Market shareThere has been significant discussions over the last few years on the market share of foreign financial institutions in China. Both foreign banks and foreign insurance companies have found it difficult to expand their respective market shares. If total assets are used as the metric, then the foreign banks have clearly failed to gain traction within the expanding Chinese banking industry.

At the end of 2013, foreign banks’ market share was just 1.73%, which was below the market share of 1.84% in 2004. However, market share in terms of total assets does not tell the whole story. Several participants mentioned that if onshore and offshore assets are included, the market share of foreign banks is around 4.9%. It also suggested that foreign banks’ share of the derivatives market is much higher, at around one-third.

02. Findings at a glance

Niche strategiesMost, if not all foreign bank entrants, have found the market challenging. As a result, most have adopted niche strategies focusing on areas where they have a particular expertise or competitive advantage.

For example, Spanish banks have attempted to leverage their strong position in Latin America, Japanese and Korean banks have serviced the needs of their home country corporates, and Australian and Canadian banks have tapped their resource sector skills and connections. Some foreign banks have attempted to cover both retail and wholesale banking while others have focused on very narrow market segments.

It is fair to say that at this stage of these foreign banks’ evolution and development in the world’s second largest economy, they would have hoped to have achieved more.

What is driving change?Against this background, it is important to consider the different drivers of change in the China marketplace. Participants in this survey readily identified a number of fundamental drivers that have the potential to change the financial market radically, and open new markets for foreign banks.

8 I Future directions for foreign banks in China 2014

Future directions for foreign banks in China 2014 I 9

Regulatory changeThe financial reform agenda, which picked-up momentum after the Third Plenum in November 2013, promises to herald a new era and launch a raft of opportunities for foreign banks. This includes further interest rate liberalization, increased RMB internationalization, and the establishment of the Shanghai Free Trade Zone.

E-finance revolutionIn addition to regulatory reform, there is also the e-finance revolution and the new financial environment resulting from the digitalization of financial services. The e-finance revolution is driving changes in consumer behavior and also, being impacted by such changes.

Mobile bankingMobile banking and the power of social media are already creating new opportunities as well as threats for foreign banks that have entered the retail banking arena. The difficulties of limited physical distribution channels may be offset by the opportunity afforded by online and mobile banking. Strong global brands, state of the art technology, innovative, well-designed products, and excellent service may win the attention and interest of younger, upwardly mobile financial consumers.

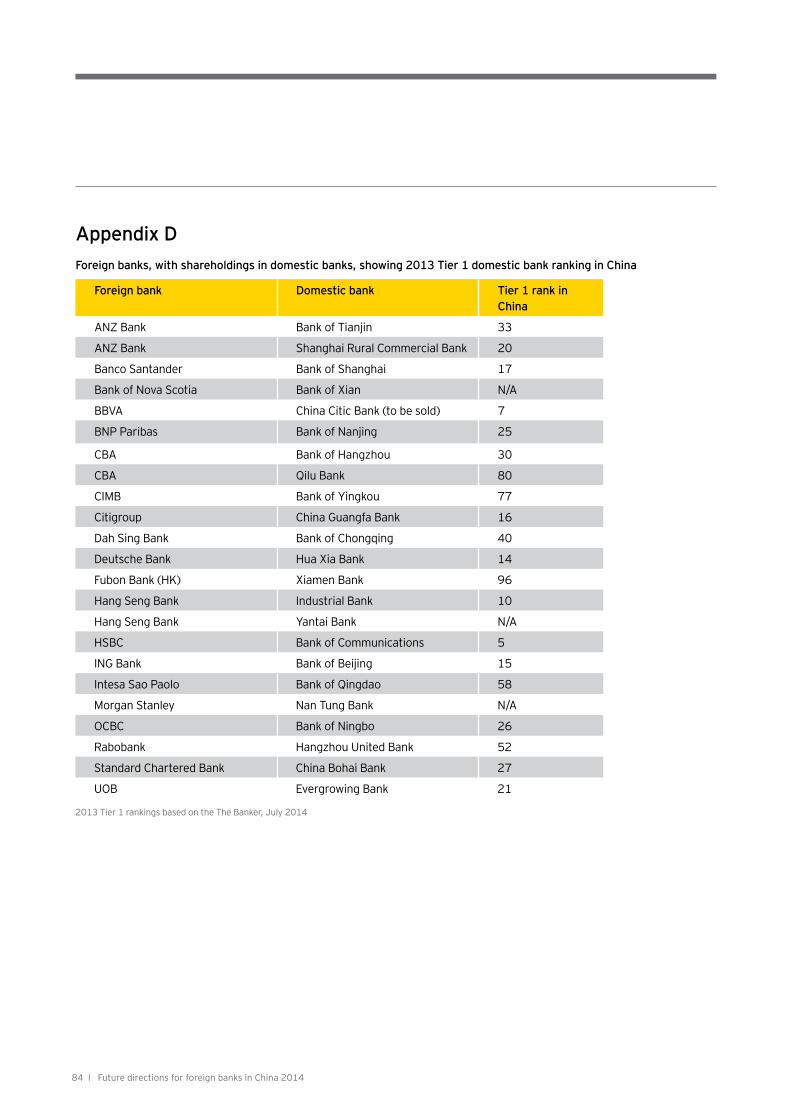

Ownership in domestic banksThe slowdown in China’s economy may also persuade its regulators to adopt a more lenient approach towards foreign banks. At least 20 foreign banks have shareholdings in domestic banks, and are subject to the 20% investment ceiling (see Appendix D, page 84). While this report concludes that foreign banks’ interest in investing in domestic banks has receded, an economic downturn might provide an impetus for government to change the current restrictions which could revive foreign banks’ interest.

Less restrictive ownership regulations, under which a foreign bank was permitted to acquire more than a 50% shareholding in a mid-sized bank, might attract interest from foreign banks that have, to date, struggled to grow their branch networks. Domestic policy may also need to be amended if Chinese banks accelerate their acquisitions of foreign financial institutions in offshore markets. As Chinese banks service their clients in international markets, they will want to grow in size and scope. Acquisitions of banks overseas will facilitate this process. Demands for reciprocal treatment will inevitably follow.

This report finds that while the underlying drivers are in place, it is not clear when change is likely to occur or what its scope might be.

The challengesCurrent challenges facing foreign banks can be sub-divided into three categories: regulatory challenges, market growth challenges, and operational challenges.

Regulatory challengesThe most difficult regulatory challenge identified by survey participants in 2014, was access to the bond market followed by the myriad of rules and regulations, and capital and liquidity constraints. As China’s economy evolves, the foreign banks believe it is critical that the capital markets open up and that the foreign banks participate more fully in the bond market.

Rules and regulations continue to frustrate foreign banks. A large foreign bank, with a retail presence, commented that it now provides more than 6,000 different regulatory reports. Additionally, capital and liquidity constraints also impede the foreign banks’ efforts to expand.

Growth challengesThe three most important market growth challenges were attracting and retaining retail customers, margin compression, and competition from domestic banks. The retail-oriented foreign banks must find new ways to cement their relationships with clients. Domestic banks are formidable competitors. In March 2014, regulators approved the set-up of five new privately-owned banks. The entrance of new and innovative privately-owned banks will increase the level of competition. Three foreign banks now have proprietary credit cards, but mobile banking and payments may leapfrog traditional service offerings.

Operational challengesThe perennial operational challenge of recruiting and retaining personnel remains important. Although this year’s report finds increased levels of staff retention and a slowdown in salary growth, many domestic banks offer attractive packages to foreign bank personnel.

The legal environment and good governance in client companies are also challenging. Participants cited the market shock resulting from the Qingdao commodity fraud, which reportedly caused 25 international and local lenders to lose up to US$4.5 billion, as a result of traders reusing copper collateral many times.1 Several participants in this report are listed as plaintiffs, and media reports suggest they have made provision for hundreds of millions of dollars for potential losses.

1 Wall Street Journal, 3 July 2014

10 I Future directions for foreign banks in China 2014

SFTZThe SFTZ has been heralded as a critical step in the financial reform process, and as a test laboratory for RMB products. Many of the larger, locally-incorporated foreign banks moved expeditiously to set-up inside the SFTZ. During the interviews, participants in this report predict that 20-25 foreign banks will set-up operations. As of 30 September 2014, twenty-three foreigh banks have registered in the SFTZ.

Three points summarize the views expressed by foreign banks on the SFTZ.

1. UncertaintyApproximately one year after the launch of the SFTZ, there remains uncertainty on the financial products that can be offered and to whom.

2. The cost/benefit of entryRegulators require a stand-alone accounting system for banking activity inside the SFTZ. Participants in this report say that the cost of such a system can range from US$2 million to US$10 million. They believe it is impossible to make a viable business case to head office, given the costs and resulting benefits.

3. Why move now?Smaller foreign banks, in particular, argue that if the objective is to rollout the SFTZ to other locations and perhaps also embrace all of Shanghai’s Lujiazui district, then why rush into the SFTZ?

The counter argument to these viewpoints suggests that first movers into the zone will be rewarded for their commitment, while latecomers may be restricted from future product offerings.

Top products in the SFTZAlthough the list of products that can be offered in the SFTZ remains unclear, participants frequently referred to opportunities associated with “cash pooling.” Those surveyed also mentioned opportunities related to trade finance and cross-border loans.

Participants also made reference to offshore Chinese renminbi (CNH) funding, mergers and acquisitions, and derivatives, including commodity and foreign exchange hedging.

Commitment from parent banksAgainst this background of predicted opportunity, tinged with market uncertainty, participants indicated that commitment from parent banks continues to grow. Only three participants said that support had declined over the last year, while 23 banks said support had increased. Parent banks remain fully committed to their China ventures. This suggests that if reform takes hold and new product and market opportunities unfold, then the foreign banks will respond with further investment in China.

Impact of shadow banksThe participants are divided regarding the impact of a potential deterioration in the shadow banking sector. Twenty banks believe it will have no impact on foreign banks while 15 banks believe there may be collateral damage. An October 2014 International Monetary Fund (IMF) report1

found that shadow banking financing amounted to 35% of China’s gross domestic product (GDP). The report also concluded that shadow banking is already stressing the domestic financial system, and will impact foreign banks through their cross-border bank lending.

Loan portfolios of domestic banksEighty percent of participants believed that the health of the domestic banks’ corporate loan portfolios had deteriorated in the last year. The stability of consumer loans was more balanced, 58% of foreign banks believe it has declined while 42% contend it remains the same. Interestingly, the majority of foreign banks believe market risk for the domestic banks remains the same, while half believe operational risk has increased.

Loan portfolios of foreign banksIn contrast to the assessment of the domestic banks, the foreign banks believe that corporate and consumer credit remains much the same as last year and there has been minimal deterioration. The China Banking Regulatory Commission (CBRC) non-performing loan ratio for foreign banks at the end of 2013, was 0.49% versus 0.52% in 2012.

02. Findings at a glance

1 Wall Street Journal, 3 July 2014

Future directions for foreign banks in China 2014 I 11

Most difficult regulatory issuesAccording to participants, the top five regulatory issues in 2014 are:

1. Removing the foreign debt quota

2. Removing the foreign guarantee quota

3. Insufficient coordination by regulators (for example, People’s Bank of China (PBOC), CBRC, and State Administration of Foreign Exchange (SAFE) all have roles in the emerging SFTZ)

4. Access to bond underwriting on the same basis as domestic banks

5. Removal of the withholding tax on offshore funding

Deposit insuranceOne of the key stepping stones in the liberalization of deposit rates is the introduction of a deposit insurance scheme. In late 2013, the Economist predicted it would be launched within months. The foreign banks believe it will not happen until 2015 and this view was supported by a PBOC announcement on 30 November 2014. Such a move is seen as a precursor to deposit rate liberalization in the short term, it will probably cause increased volatility and market uncertainty.

In general, foreign banks surveyed do not believe a deposit insurance scheme will have a direct impact on their business. However, it is expected to suppress margins further, and will be most directly felt by retail banks.

Liquidity pressuresDespite the more stable interest rate environment in 2014, foreign banks still expressed concern about liquidity management. Eighteen banks hold serious concerns. Closely related to liquidity concerns are funding sources. Thirty banks provided a breakdown of their funding sources for 2014 and 2017, and revealed a heavy dependence on the parent bank’s funding and corporate deposits.

The opening-up of the capital market envisaged in the financial reform process would greatly improve access to funding and ameliorate liquidity concerns.

Mobile bankingFinancial services in China are already impacted by the rapid growth in mobile banking. The domestic banks have been subjected to new mobile banking entrants, such as Alipay and WeChat.

Alipay is the market leader but Tencent’s social networking app, WeChat, may, in the medium term, be the more formidable competitor. It has the ability to act as an intermediary between customers and merchants.

As a result, traditional domestic banks may in time be relegated to the back-end of the transaction process. Back- end payments will continue to be provided by credit and debit cards offered by the domestic banks.

Presently, three foreign banks offer proprietary bank cards. Before the entrance of players such as Alipay and WeChat, they may have viewed the credit card or debit card as a key component in building their retail brand. New payment innovations in the mobile space will make this process more challenging.

The disruptive forces already developing in retail banking will have an impact on retail-oriented foreign banks. This report discusses the liberalization of deposit rates in the banking market, but most participants address this change in the context of corporate banking. Demand deposits in the domestic banks are already under threat by innovators such as Alibaba’s internal money market fund, Yu’ E Bao. Deposit rate liberalization will cause further disruption, when it occurs.

In September 2014, Alibaba’s financial unit was reported to be in talks with the Hong Kong Monetary Authority (HKMA) regarding a Hong Kong version of its Yu’ E Bao money market fund. Yu’ E Bao accumulated assets of RMB574 billion (US$94 billion) in the first year of operation to June 2014.2 Yu’ E Bao is managed by Tianhong Asset Management. Tencent’s WeChat app permits users to transfer money into a fund managed by the mutual fund giant, China Asset Management.

Although it is still early days, foreign banks do not appear to have addressed the fast moving changes in the mobile banking space. Only nine participants commented on a question relating to how they planned to introduce e-finance, mobile banking, and data analysis initiatives.

2 Financial Times, 28 September 2014

12 I Future directions for foreign banks in China 2014

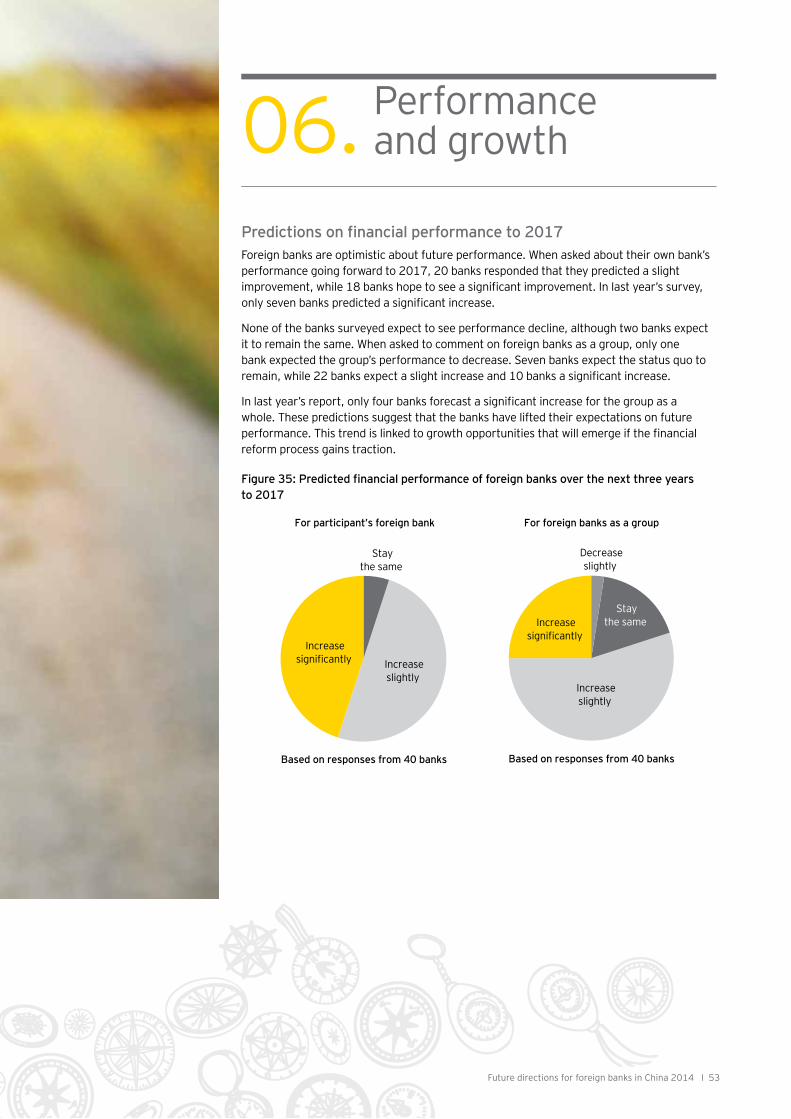

Performance and growthAlthough profitability for the foreign banks dipped in 2013, survey responses projecting forward to 2017 were positive. Twenty banks expect performance to increase slightly while 18 banks expect a significant improvement.

Participants looking back over the last 12 months reported that the three areas experiencing strongest revenue growth were trade finance, corporate lending, and treasury.

The retail banking environment is challenging. Over the last year, growth in mortgages and credit cards has been difficult, although personal loans appear to be performing well.

Thirty-four banks provided forecasts on their return on equity (ROE) in 2015, and on their ROE in three to five years.

Only two banks predict an ROE below 10% in both time periods. At the top end of the scale, three banks expect 19%–21% returns while four banks expect returns of 19%–21% in three to five years.

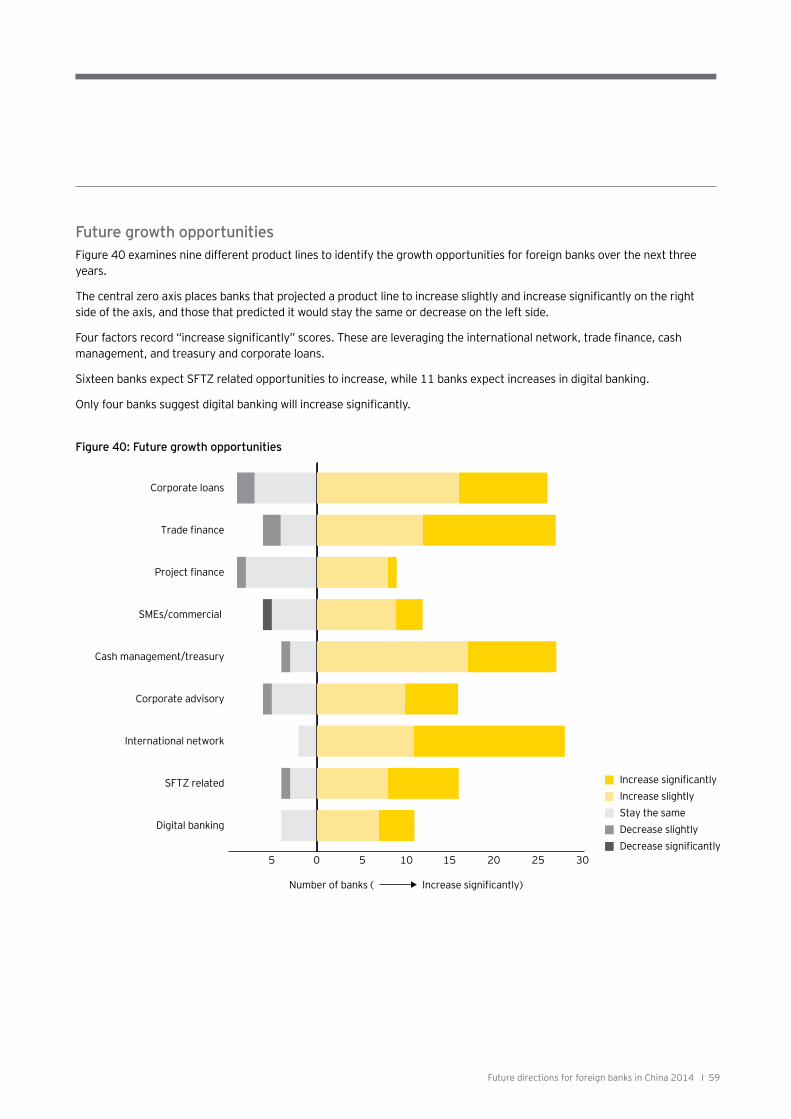

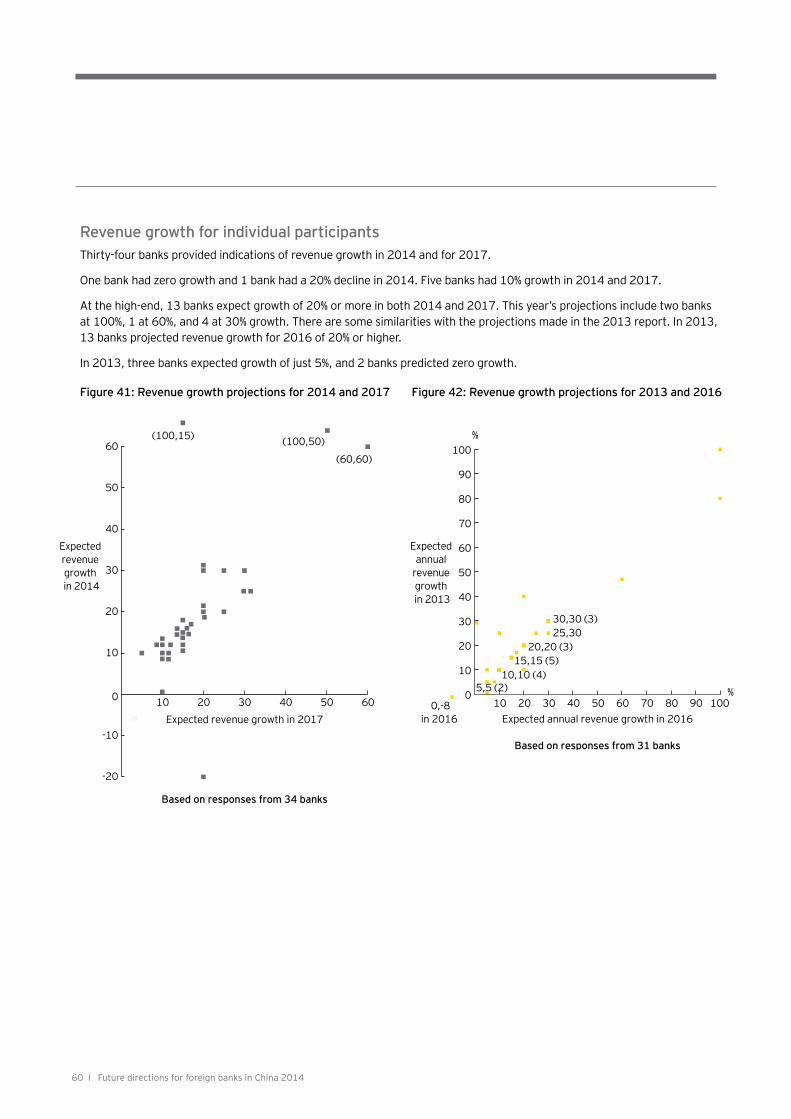

Future growthFour areas of opportunity for future growth are expected to increase significantly. These are leveraging the banks’ international networks, trade finance, cash management, and corporate lending. Thirty-four banks provided revenue growth projections for 2014 and 2017. Many banks are clustered in the 8% to 15% for both 2014 and 2017, but 13 banks expect 20% or more revenue growth in both 2014 and 2017.

Margin squeezeWithin a group of 35 respondents, only one contrarian believed margins were not being squeezed. Thirteen banks said margin compression was already moderate, while five banks reported extensive compression.

Key segments The foreign banks attribute different degrees of importance to six market segments, these are state-owned enterprises (SOEs), privately-owned enterprises (POEs), small- and medium-sized enterprises (SMEs), financial institutions, global corporates, and high-net-worth individuals (HNWIs). Participants ranked these markets from 1 to 10, 1 being least important and 10 being most important. The rankings given by each participant reflect their own market focus.

Many participants attributed high scores to both the SOEs and POEs in 2014. Scores for the SMEs sector have increased over 2013. Eighteen banks scored financial institutions between eight and 10. Nine banks scored the maximum score of 10 for global corporates. Reflecting the narrower appeal of marketing to HNWIs, only eight out of 20 respondents scored this segment 8 to 10.

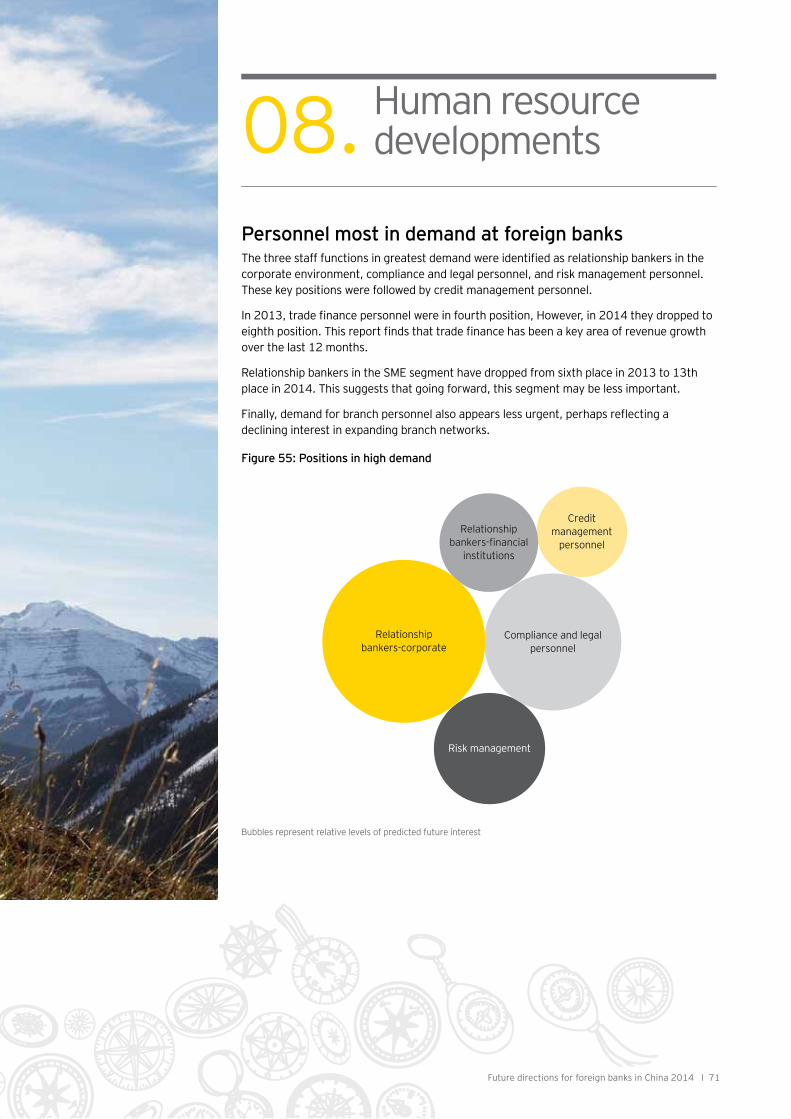

Hiring prioritiesA comparison of the top hiring positions between 2013 and 2014 revealed that the order and importance of the top three remain unchanged. They are relationship bankers in the corporate area, compliance and legal personnel, and risk management personnel.

A notable difference in 2014 was the priority given to relationship bankers dealing with financial institutions. This group move up from 13th position to 4th.

This reflects an increased involvement in the interbank market, which may be driven by concerns regarding liquidity management.

Future directions for foreign banks in China 2014 I 13

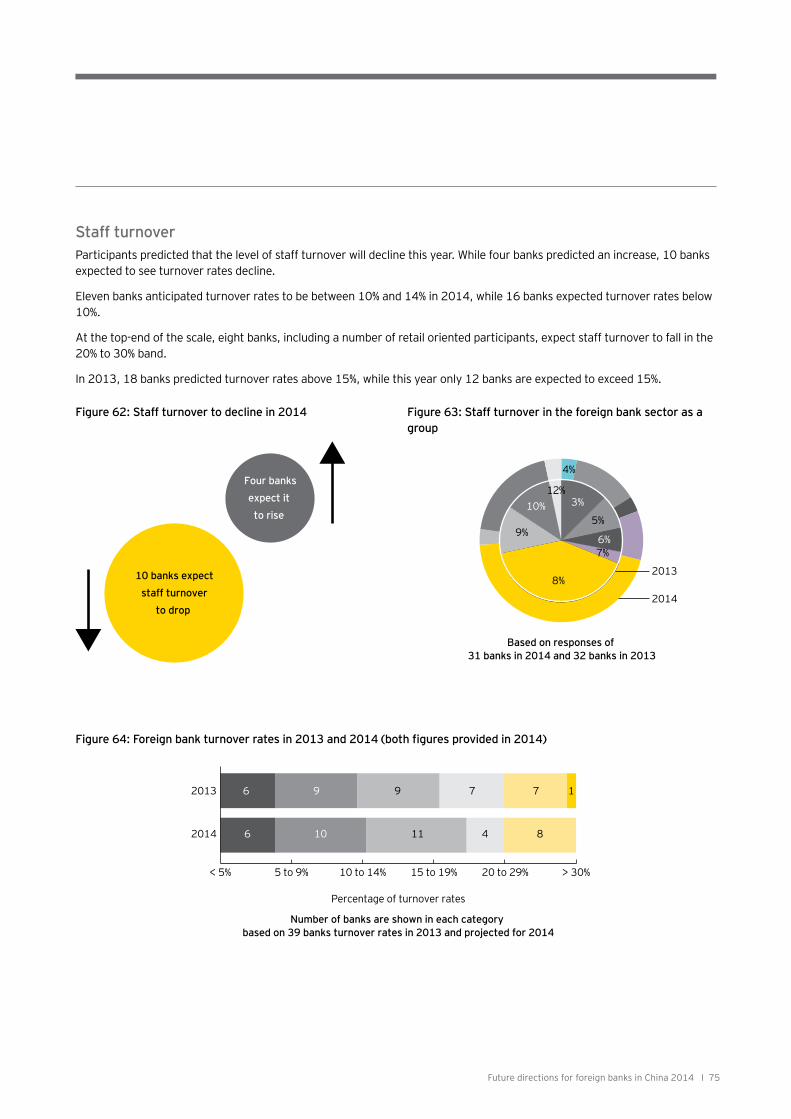

Hints of a reduction of staff turnoverTen banks predicted a decline in staff turnover in 2014. Sixteen banks expected rates below 10%, and a further 11 predicted turnover in the 10% to 14% range. A group of mostly retail-based banks envisage higher rates, but the general trend suggests that there is less movement between banks.

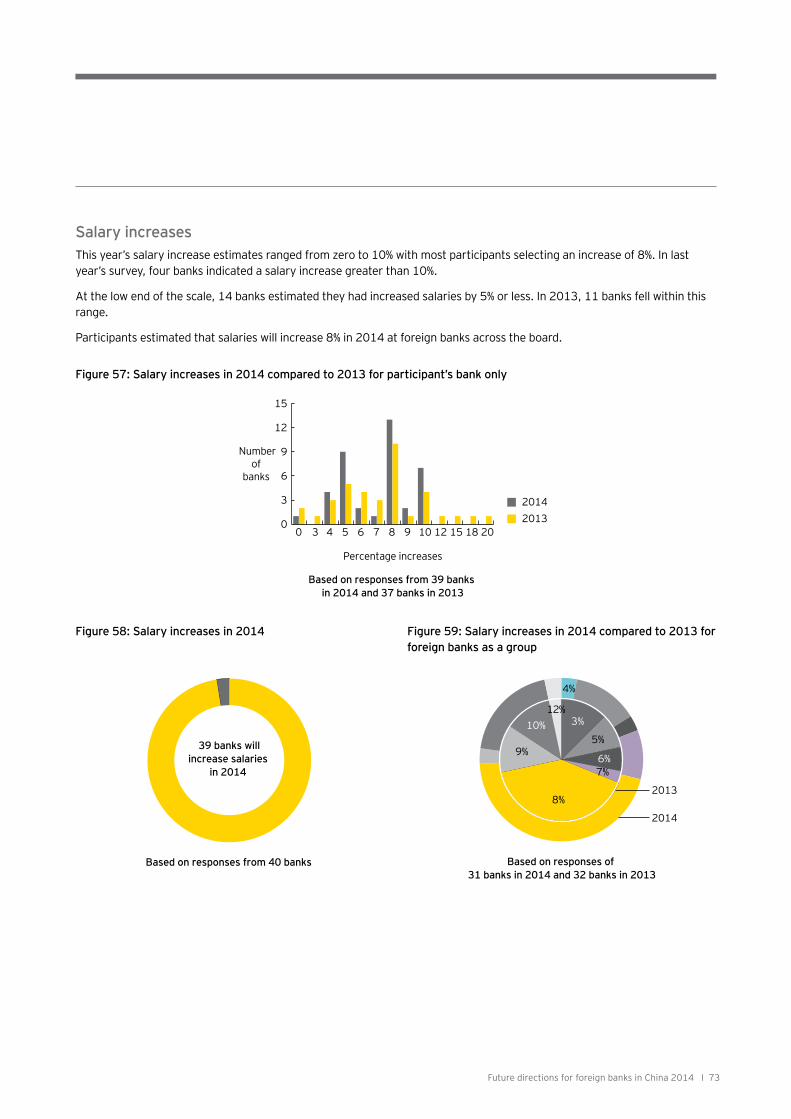

Salaries are expected to increase by around 8% in 2014. No foreign banks expect increases above 10%, which contrasts with last year.

As in 2013, foreign banks believe that their salaries remained above the domestic banks. However, many contend that salaries are comparable at the middle management and support levels.

Many respondents pointed out that domestic bank employees enjoy a range of fringe benefits. Media reports in September 2014, suggested that the heads of domestic banks and SOEs may see their salaries capped at around US$100,000.

Future directions for foreign banks in China 2014 I 13

14 I Future directions for foreign banks in China 2014

Future directions for foreign banks in China 2014 I 15

03. Overview of the current landscape

Foreign bank presenceForty-two locally-incorporated foreign banks, 92 branches, and 187 representative offices operated in China at the end of 2013, based on CBRC Annual Report 2013. (Refer to Appendix A for a list of locally-incorporated foreign banks.)

Within this group of foreign banks:

• 30 locally-incorporated foreign banks and 27 branches were permitted to offer derivatives.

• Six locally-incorporated foreign banks were authorized to issue RMB financial bonds.

• Three locally-incorporated banks were approved to issue proprietary credit cards.

The CBRC reports that foreign banks were present across 69 cities in 27 provinces. The map at Figure 11 shows the distribution of branches and outlets of the “Big Six” retail foreign banks (by branch network). In its 2012 report, the CBRC indicated that foreign banks had a presence in 59 cities.

Foreign banks

Wholly foreign-owned banks

Joint-venture banks

Wholly foreign-owned finance companies Total

Locally-incorporated institutions (LII)

39 2 1 42

LII branches and subsidiaries

282 3 285

Foreign bank branches

92 92

Branches 9 509 10 528

Total 101 830 15 1 947

Figure 1: Foreign banking establishments in China as of 31 December 2013

Source: CBRC Annual Report 2013

16 I Future directions for foreign banks in China 2014

Total assets of foreign banks and market share in 2013Although the total assets of foreign banks grew by 7.66% in 2013 to RMB2.56 trillion, their market share measured in total assets dropped to 1.73% in 2013. This market share figure is below the level recorded nine years ago in 2004.

As a group, the foreign banks had total assets of RMB2.56 trillion and generated after tax profits of RMB14.03 billion. This was below the 2012 figure of RMB16.34 billion.

Item/year 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Number of institutions*

188 207 224 274 311 338 360 387 412 413

Assets** 5,823 7,155 9,279 12,525 13,448 13,492 17,423 21,535 23,804 25,628

As % of the total banking assets in China

1.84 1.91 2.11 2.38 2.16 1.71 1.85 1.93 1.82 1.73

* Including headquarters, branches and subsidiaries** RMB100 millionSource: CBRC Annual Report 2013

Figure 2: Foreign banking institutions in China, 2004 to 2013

Figure 3: Foreign bank ratios, 2013

Liquidity ratio 72.42%

Nonperforming loans (NPL) ratio 0.49%

Deposit growth in 2013 4.72%

Loan growth in 2013 6.47%

CBRC provide a number of ratios pertaining to the foreign banks as a group. At the end of 2013, CBRC noted that the foreign banks liquidity ratio increased modestly from 68.77% in 2012 to 72.42%.

The non-performing loans percentage for foreign banks dropped from 0.52% in 2012 to 0.49% in 2013.

Deposits for all foreign banks in China grew by 4.72% in 2013, while total loans grew by 6.47%. Source: CBRC Annual Report 2013

Future directions for foreign banks in China 2014 I 17

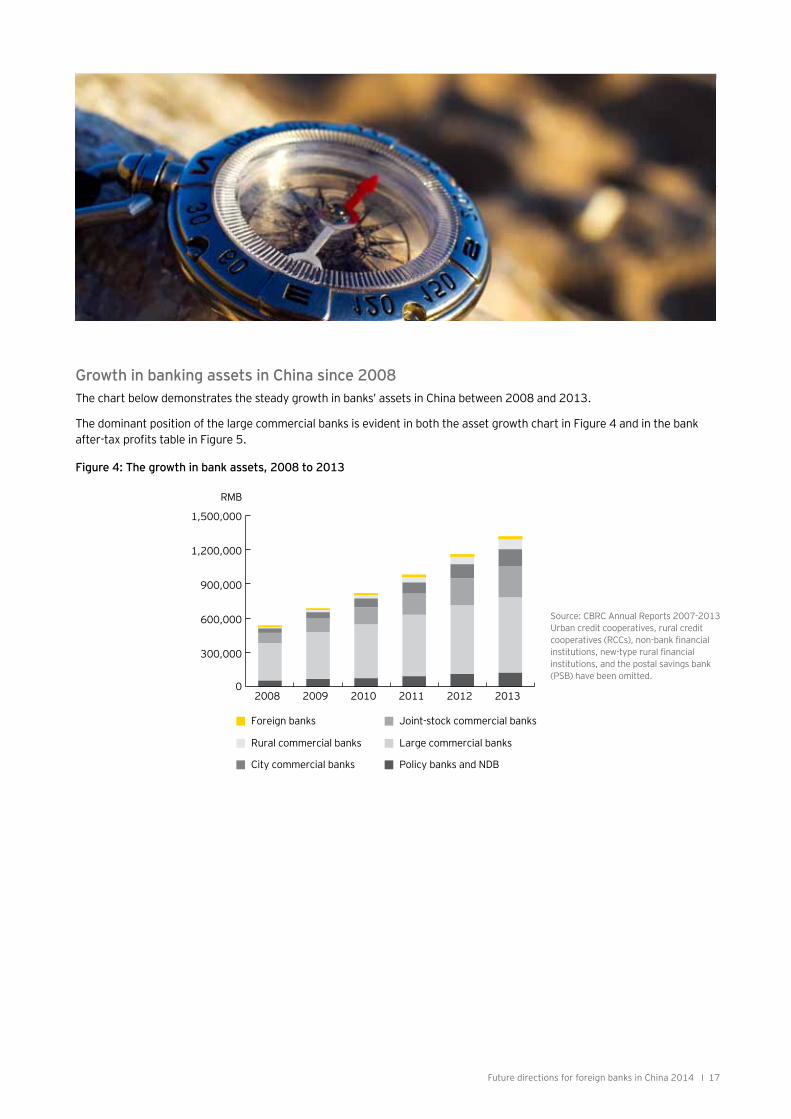

Growth in banking assets in China since 2008The chart below demonstrates the steady growth in banks’ assets in China between 2008 and 2013.

The dominant position of the large commercial banks is evident in both the asset growth chart in Figure 4 and in the bank after-tax profits table in Figure 5.

Source: CBRC Annual Reports 2007-2013Urban credit cooperatives, rural credit cooperatives (RCCs), non-bank financial institutions, new-type rural financial institutions, and the postal savings bank (PSB) have been omitted.

Figure 4: The growth in bank assets, 2008 to 2013

300,000

0

600,000

900,000

1,200,000

1,500,000

Foreign banks

Rural commercial banks

City commercial banks

Joint-stock commercial banks

Large commercial banks

Policy banks and NDB

201320122011201020092008

RMB

18 I Future directions for foreign banks in China 2014

Figure 6: After-tax profits of all banks, 2007 to 2013 (in RMB100 million)

2007 2008 2009 2010 2011 2012 2013All banking financial institutions (Fls)

4,467.3 5,833.6 6,684.2 8,990.9 12,518.7 15,115.5 17,444.6

Policy banks and National Development Bank

489.3 229.8 352.5 415.2 536.7 736.3 922.1

Large commercial banks 2,466.0 3,542.2 4,001.2 5,151.2 6,646.6 7,545.8 8,382.3

Joint-stock commercial banks 564.4 841.4 925.0 1,358.0 2,005.0 2,526.3 2,945.4

City commercial banks 248.1 407.9 496.5 769.8 1,080.9 1,367.6 1,641.4

Rural commercial bank 42.8 73.2 149.0 279.9 512.2 782.8 1,070.1

Rural cooperative banks 54.5 103.6 134.9 179.0 181.9 172.2 162.1

Urban credit cooperatives 7.7 6.2 1.9 0.1 0.2

RCCs 139.4 219.1 227.9 232.9 531.2 654.0 729.2

Non-bank financial institutions 333.8 284.5 298.7 408.0 598.8 825.5 1,059.7

Foreign banks 60.8 119.2 64.5 77.8 167.3 163.4 140.3

New rural FIs and PSB 6.5 6.5 32.2 119.0 257.9 340.7 390.3

After tax profits of banks in 2013While the after tax profits of the large commercial banks and the city commercial banks have grown steadily from 2007, the foreign banks have experienced fluctuations in profits.

Profitability in both 2011 and 2012 exceeded the figure for 2013.

Figure 5: After-tax profits of banks in 2013 (in RMB100 million)

Rural commercial bank1,070

Non-bank financial institutions1,060

Large commercial banks8,382

Joint-stock commercial banks2,945

City commercial banks1,641

New rural FIs and PSB390

Policy banks and NDB922

Rural coop banks 162

RCCs729

Foreignbanks 140

Source: CBRC Annual Reports, 2008 to 2013

Source: CBRC Annual Report 2013

Future directions for foreign banks in China 2014 I 19

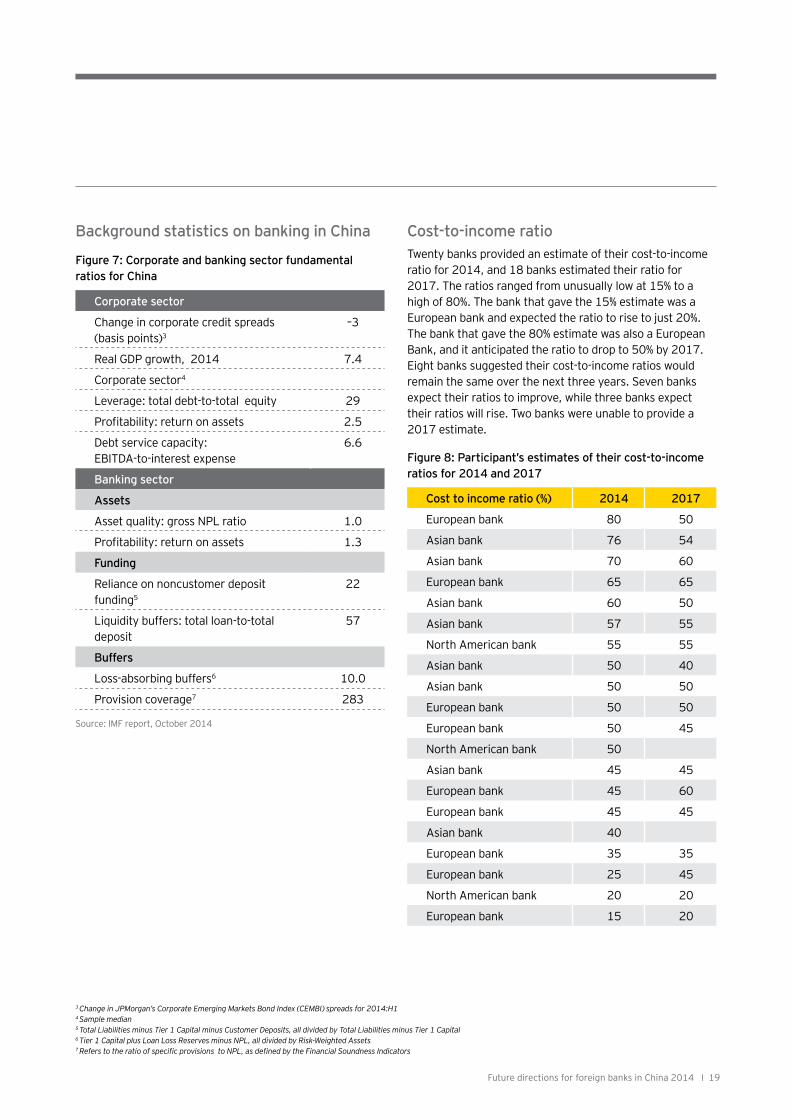

Background statistics on banking in China Cost-to-income ratioTwenty banks provided an estimate of their cost-to-income ratio for 2014, and 18 banks estimated their ratio for 2017. The ratios ranged from unusually low at 15% to a high of 80%. The bank that gave the 15% estimate was a European bank and expected the ratio to rise to just 20%. The bank that gave the 80% estimate was also a European Bank, and it anticipated the ratio to drop to 50% by 2017. Eight banks suggested their cost-to-income ratios would remain the same over the next three years. Seven banks expect their ratios to improve, while three banks expect their ratios will rise. Two banks were unable to provide a 2017 estimate.

Figure 7: Corporate and banking sector fundamental ratios for China

Figure 8: Participant’s estimates of their cost-to-income ratios for 2014 and 2017

Corporate sector

Change in corporate credit spreads (basis points)3

–3

Real GDP growth, 2014 7.4

Corporate sector4

Leverage: total debt-to-total equity 29

Profitability: return on assets 2.5

Debt service capacity: EBITDA-to-interest expense

6.6

Banking sector

Assets

Asset quality: gross NPL ratio 1.0

Profitability: return on assets 1.3

Funding

Reliance on noncustomer deposit funding5

22

Liquidity buffers: total loan-to-total deposit

57

Buffers

Loss-absorbing buffers6 10.0

Provision coverage7 283

Source: IMF report, October 2014

3 Change in JPMorgan’s Corporate Emerging Markets Bond Index (CEMBI) spreads for 2014:H14 Sample median5 Total Liabilities minus Tier 1 Capital minus Customer Deposits, all divided by Total Liabilities minus Tier 1 Capital6 Tier 1 Capital plus Loan Loss Reserves minus NPL, all divided by Risk-Weighted Assets7 Refers to the ratio of specific provisions to NPL, as defined by the Financial Soundness Indicators

Cost to income ratio (%) 2014 2017

European bank 80 50

Asian bank 76 54

Asian bank 70 60

European bank 65 65

Asian bank 60 50

Asian bank 57 55

North American bank 55 55

Asian bank 50 40

Asian bank 50 50

European bank 50 50

European bank 50 45

North American bank 50

Asian bank 45 45

European bank 45 60

European bank 45 45

Asian bank 40

European bank 35 35

European bank 25 45

North American bank 20 20

European bank 15 20

20 I Future directions for foreign banks in China 2014

Expectations around increasing market shareThe majority of banks expect market share over the next three years in both tier 1 cities and beyond tier 1 cities to remain the same. Eleven banks believe it may increase in both tier 1 cities and beyond. In 2013, 16 banks predicted an increase in tier 1 cities and beyond. Participants in 2014 appear less optimistic that they will be able to gain market share from the domestic banks.

Figure 9: Market share, 2003 to 2013 Figure 10: Market share in tier 1 cities and beyond

0.0

0.5

1.0

1.5

2.0

2.5

20132012

20112010

20092008

20072006

20052004

2003

Marketshare

%

DecreaseStay the sameIncrease

23 banks expecttier 1 to remain

the same

21 banks expectbeyond tier 1 to

remain the same

Based on responses from 40 banks

Based on responses from 40 banks

Source: CBRC Annual Reports 2003-2013

Future directions for foreign banks in China 2014 I 21

Figure 11: Big six retail bank networks in 2014

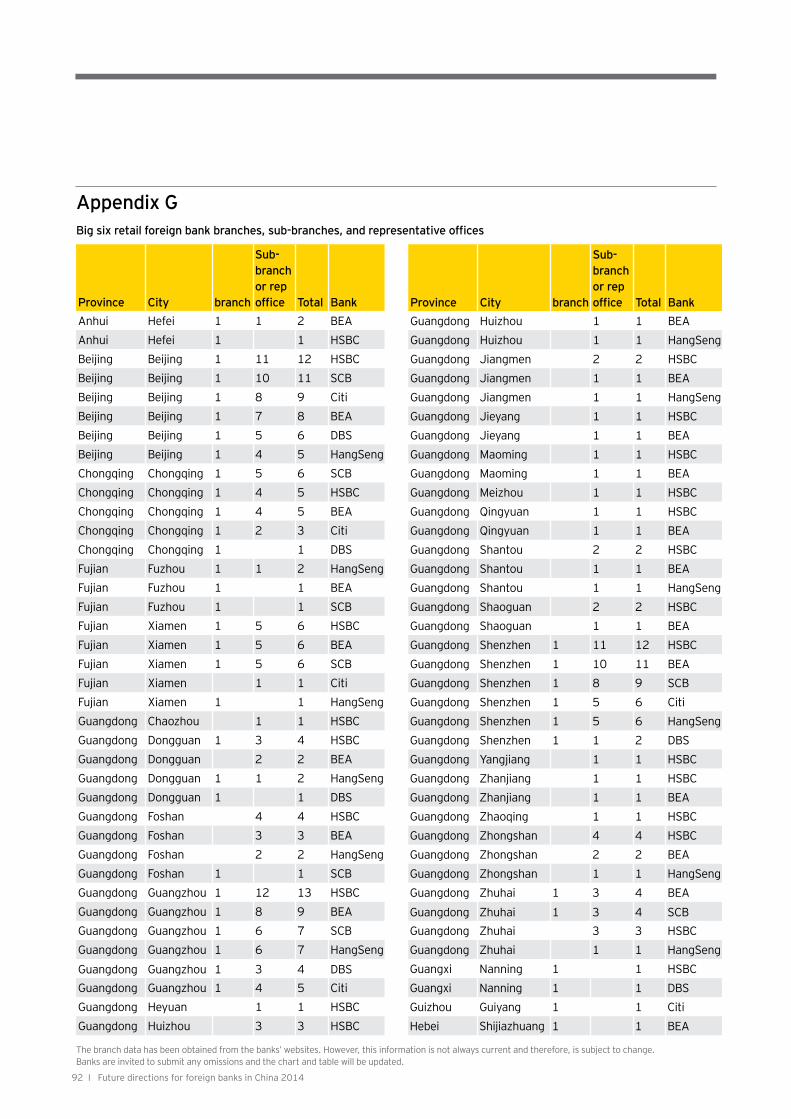

Geographic expansion continuesThe branch networks of the “Big Six” retail banks, Bank of East Asia, Citibank, DBS, Hang Seng Bank, HSBC, and Standard Chartered Bank, are shown in the map below.

Source: Individual bank websites, information consolidated by Dr. Brian Metcalfe In addition to the branches shown above are Xinjiang BEA 2, Nei Menggu SCB 1, and Heilongjiang HSBC 1 and BEA 1. Data shown as of 2014 has been obtained from the websites of the six largest foreign retail banks based on network size. Please note data may not be kept up to date by the banks; consequently, some deviation may exist.

22 I Future directions for foreign banks in China 2014

Expectations surrounding the SFTZThe SFTZ was formally announced over a year ago. Participants were asked to express their opinion on whether or not expectations surrounding the launch had been fulfilled.

Over 80% of participants concluded that to date, expectations had not been achieved.

A European bank and a North American bank commented that they never expected the pace of introduction to be fast. A seasoned European banker observed that he “had seen it all before.”

An Asian bank contended that preliminary regulations had been set-up, but there was now a need for much greater clarity.

Several participants mentioned the overlapping responsibilities of various regulators, including the PBOC, CBRC, SAFE, and the China Securities Regulatory Commission (CSRC).

How many foreign banks will enter the SFTZ?Twenty-five banks provided an estimate of the number of foreign banks expected to enter the SFTZ.

The chart suggests that around 20 to 25 foreign banks will set-up operations inside the SFTZ. As of 30 September 2014, 23 foreign banks have already registered in the SFTZ. This figure does not suggest that all of the locally-incorporated foreign banks will enter. It also confirms the uncertainty that continues to exist in the foreign banking community concerning the benefits of entry and the difficulty in making a robust business case.

Figure 12: Have the opportunity expectations been fulfilled?

Figure 13: Number of foreign banks expected in SFTZ in three years

0

1

2

3

4

5

6

7

8

403530252015

Numberof

responses

Estimated number of banks in SFTZ by 2017Based on responses from 25 banks

Banks

31 banksbelieve expectations

have not beenfulfilled

Based on responses from 38 banks

Future directions for foreign banks in China 2014 I 23

Figure 14: SFTZ entry decision by foreign banks

Decisions around entry to the SFTZThirty-five banks provided insight on whether they have already entered the SFTZ or had plans to do so in the next three years.

Figure 14 shows that approximately one-third have already entered or have plans to do so. However, nine banks indicated that the decision to enter was still under review, while 13 banks said that they had made a decision not to set-up presence inside the SFTZ.

Decided notto enter

Already set-upa branch

Plan to enterin the next year

Under reviewno decision taken

Based on responses from 35 banks

13 banks decided not to

enter

Future directions for foreign banks in China 2014 I 23

24 I Future directions for foreign banks in China 2014

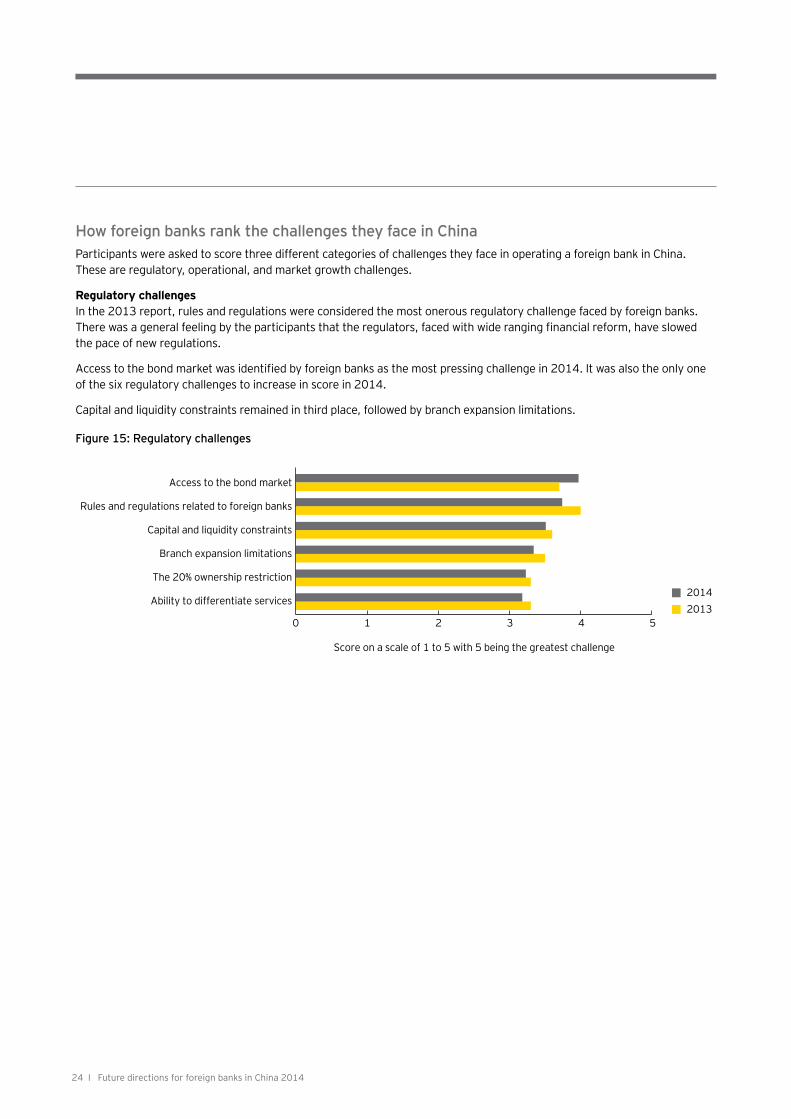

Figure 15: Regulatory challenges

How foreign banks rank the challenges they face in ChinaParticipants were asked to score three different categories of challenges they face in operating a foreign bank in China. These are regulatory, operational, and market growth challenges.

Regulatory challengesIn the 2013 report, rules and regulations were considered the most onerous regulatory challenge faced by foreign banks. There was a general feeling by the participants that the regulators, faced with wide ranging financial reform, have slowed the pace of new regulations.

Access to the bond market was identified by foreign banks as the most pressing challenge in 2014. It was also the only one of the six regulatory challenges to increase in score in 2014.

Capital and liquidity constraints remained in third place, followed by branch expansion limitations.

0 1 2 3 4 5

The 20% ownership restriction

Ability to differentiate services

Branch expansion limitations

Capital and liquidity constraints

Rules and regulations related to foreign banks

Access to the bond market

Score on a scale of 1 to 5 with 5 being the greatest challenge

20142013

Future directions for foreign banks in China 2014 I 25

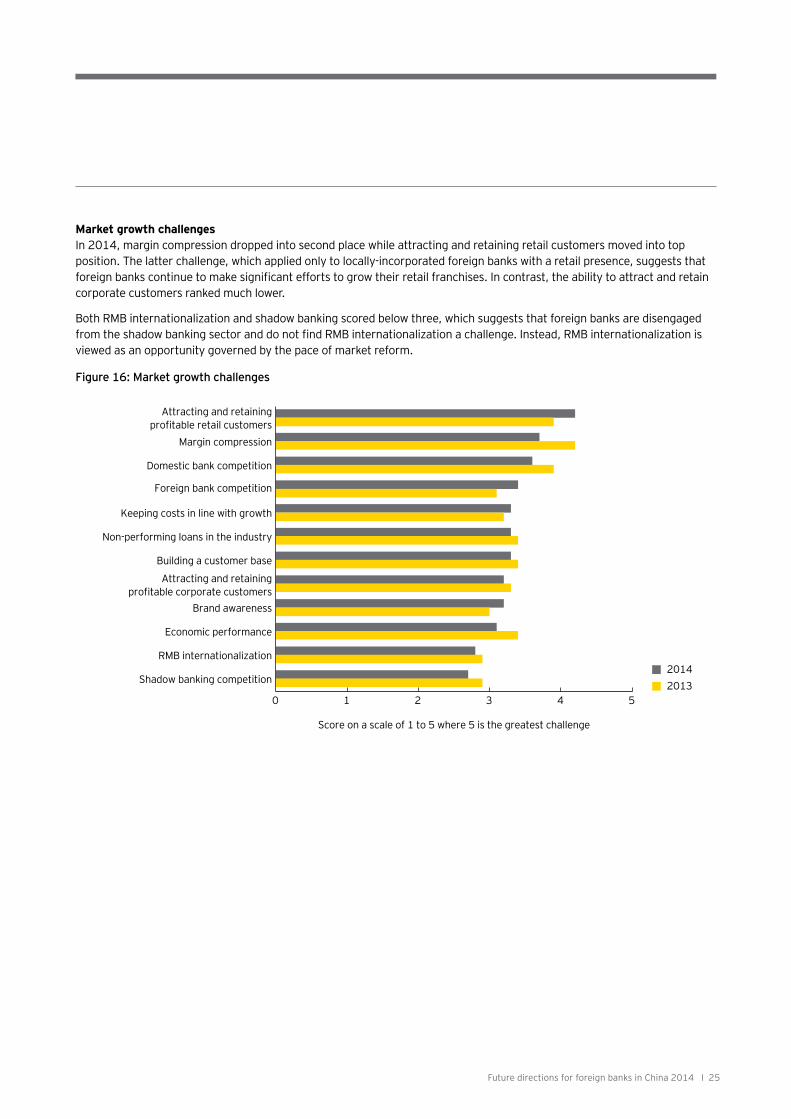

Market growth challengesIn 2014, margin compression dropped into second place while attracting and retaining retail customers moved into top position. The latter challenge, which applied only to locally-incorporated foreign banks with a retail presence, suggests that foreign banks continue to make significant efforts to grow their retail franchises. In contrast, the ability to attract and retain corporate customers ranked much lower.

Both RMB internationalization and shadow banking scored below three, which suggests that foreign banks are disengaged from the shadow banking sector and do not find RMB internationalization a challenge. Instead, RMB internationalization is viewed as an opportunity governed by the pace of market reform.

Figure 16: Market growth challenges

Score on a scale of 1 to 5 where 5 is the greatest challenge

0 1 2 3 4 5

Shadow banking competition

RMB internationalization

Economic performance

Brand awareness

Attracting and retainingprofitable corporate customers

Building a customer base

Non-performing loans in the industry

Keeping costs in line with growth

Foreign bank competition

Domestic bank competition

Margin compression

Attracting and retainingprofitable retail customers

20142013

26 I Future directions for foreign banks in China 2014

Operational challengesAttracting and retaining skilled personnel remains the primary operational challenge. This is unchanged from last year’s report. As noted further on, the economic slowdown has reduced the level of employee movement between banks. In spite of this, human resources remain a major challenge.

The biggest three challenges, after attraction and retention of skilled personnel, are the legal environment, client company governance issues, and the tax environment. Although profits for foreign banks as a group dropped in 2013, profitability also fell in importance from third to fifth place in this year’s survey. A number of participants commented that performance during the first half of 2014 has been positive, and this may have influenced this score.

Figure 17: Operational challenges

Score on a scale of 1 to 5 where 5 is the greatest challenge

0 1 2 3 4 5Accounting environment

Risk management

New technologies

Data quality and ability to leverage it

Keeping costs under control

Tax environment

Profitability

Good governance in client companies

Legal environment

Attracting and retaining skilled personnel

20142013

Future directions for foreign banks in China 2014 I 27

Setting-up in the SFTZSurvey participants believe that around 20-25 foreign banks will set-up operations in the SFTZ. Estimates ranged from just 15 foreign banks up to 38 foreign banks entering the zone.

Some of the smaller foreign banks argued that if the goal is to roll out the zone’s liberalized financial environment to other locations, and ultimately nationwide, then it would be better to wait for these broader changes rather than incur the expense of setting-up inside the zone. Those participants already committed to the zone countered this opinion by stressing the competitive advantage in being one of the first to set-up in the zone. Some also suggested that their readiness to enter the zone may be rewarded by the regulatory authorities.

Significant debate centered on the cost of setting-up inside the zone. Participants emphasized that they are required to set-up a separate accounting system. Estimated set-up costs for such a system ranged from US$1 to US$2 million, up to around US$10 million. The expense of the system reflects the size and scope of business to be undertaken.

A number of participants who indicated that they do not plan to enter the SFTZ said that they could not make a business case to their parent bank, given the uncertainty surrounding products that could be offered in the SFTZ. These banks have adopted a wait and see approach. One of these banks said that foreign banks with large dealing rooms may be able to make a business case to enter the SFTZ if they arbitraged offshore and onshore RMB. For example, hypothetically a spread of 2% (onshore RMB at 5% versus offshore RMB at 3%) on US$1 billion, would generate US$20 million and justify the business case.

Top products to be offered by the foreign banks in the SFTZSeveral participants commented that transaction banking and payment services would be the cornerstone of business in the zone.

The top product mentioned at this early stage of the SFTZ’s development was cash pooling. Cash pooling, for example, may allow companies to unlock liquidity trapped on the Chinese Mainland or permit surplus funds from overseas to assist in Chinese Mainland operations.

Trade finance was the second most commonly mentioned product area, followed by cross-border loans. In addition to these terms, participants also made specific reference to:

• CNH funding in the zone

• Mergers and acquisition services

• Providing domestic companies in the zone with banking services, participants referenced trading manufacturing and logistics companies

• Derivatives, including commodity

• Foreign exchange hedging

Internationalization of the RMBThe RMB has evolved from being used to settle international trade payments to providing investment and lending opportunities in international financial markets. Increases in trade flows have resulted in a growing pool of offshore RMB funds.

China’s government has facilitated the creation of RMB backflow channels, to foster further internationalization of the currency.

Chinese companies are now able to settle global transactions for goods and services in RMB. These cross-border transactions limit exchange rate exposure, reduce conversion costs, and make payments easier.

Backflow channels have also embraced RMB denominated foreign loans, as Chinese companies engage in more offshore funding and RMB denominated bonds.

The SFTZ is already participating in an expansion of the RMB backflow channel, and foreign banks anticipate that this will continue to grow.

At the same time, domestic companies located in the SFTZ are able to incur RMB denominated foreign debt, while multinationals can benefit from cross-border cash pooling assisted by foreign banks.

28 I Future directions for foreign banks in China 2014

Source: MarketWatch, 15 October 2014

Citi launches automated RMB cross-border sweeping from China to London

Building on its global RMB cash-pooling solutions, Citi has today announced the implementation of its first RMB Cross- Border Auto Sweeping structure from China to London. The latest development allows Citi to offer live automated RMB cross-border sweeping in China, Hong Kong, Singapore and London.

Citi’s global concentration engine allows clients to sweep true end-of-day balances into London without any loss of value. This platform also comes with tracking and reconciliation of intercompany loan positions, automated mechanisms to control lending positions, as well as reporting to meet local regulatory and reporting requirements.

Rajesh Mehta, EMEA Head of Citi’s Treasury and Trade solutions said: “Automated RMB sweeping to London is an important addition to Citi’s RMB footprint, given that London has traditionally been the center for managing currency risk. We have a number of clients already manually concentrating their RMB into London as part of multi-currency pools to leverage RMB liquidity and centralize management of FX exposures; our new automation capability makes this process even more efficient for clients.”

Sandip Patil, Asia-Pacific Head of Liquidity Management added: “With our local depth and global concentration platform, Citi enables our clients to integrate RMB effectively into their treasury and liquidity structures, irrespective of location, truly paving the way for the RMB’s development as an international currency. Our success in replicating our G10 expertise and capabilities into the RMB space is playing a critical role for our clients.”

The structure has been put in place for Swiss-based Pentair – a global water, fluid, thermal management and equipment protection partner – and was implemented using Pentair’s registered entity in the SFTZ (SFTZ), thus enabling the company to integrate its daily working capital RMB balances into its global cash pool. Benefits will include improvements in the company’s liquidity management, capital utilization efficiency, reduced cost in cross-border transactions, as well as intragroup financing and foreign exchange benefits.

Terri Scherber, Senior Treasury Director at Pentair, said: “Pentair was keen to take advantage of the newly deregulated SFTZ policies and connect our domestic RMB funding structures to our global liquidity pool. Citi’s automated sweeping solution now provides us a much more efficient way of managing this process.”

Amit Agarwal, EMEA Head of Liquidity Management Services at Citi, said: “Citi has one of the most extensive geographic and currency footprints, supporting some of the most sophisticated treasury management structures. The incorporation of RMB into London-based cash pools will be of significant benefit to both Chinese and multinational companies in the SFTZ, allowing them to capitalize on interest increases, effectively offset overdrafts in low-yield, hard currencies, as well as achieve greater visibility and improved risk management.”

Future directions for foreign banks in China 2014 I 29

Source: HSBC Global Connections, 20 March 2014

HSBC pioneers two-way cross-border RMB cash pooling business

On 21st February 2014, HSBC China launched a centralized renminbi (“RMB”) cross-border transaction management solution for its corporate clients in the China (Shanghai) Pilot Free Trade Zone (“Shanghai FTZ”) by delivering the new service to Saint-Gobain via its subsidiary in the pilot zone. This innovative cash management solution covers functions including pay-on-behalf and receive-on-behalf (“POBO/ROBO”) and netting.

Saint-Gobain, the world leader in the habitat and construction markets, designs, manufactures and distributes high performance building materials, providing innovative solutions to the challenges of growth, energy efficiency and environmental protection. Since entering China in 1985, Saint-Gobain has invested over EUR2 billion in the market and grown the business rapidly. Via its subsidiary in the Shanghai FTZ, it is able to centralise payments and collections for merchandise and services trade settlement, along with other current account items, and subsequently improve the efficient use of RMB settlement within the group. This solution thus also enhances the cash management efficiency for its Asia Treasury Centre located in Shanghai.

Centralized payments and collections is an efficient cash management solution for multinational companies’ need to manage intra-group account payables and receivables. The newly-launched scheme in the Shanghai FTZ now applies to RMB cross-border settlement, enabling corporates to consolidate and offset account payables and receivables through a single transaction.

Centralized RMB cross-border payments and collections will bring significant benefits to our clients by simplifying their payment processes, reducing the number of transactions and unlocking additional liquidity. It therefore helps improve the efficiency of funding management and settlement, reducing funding cost and foreign exchange risk.

Currently, market demand for cross-border RMB cash management comes from three sources. The first of these is the need for cross-border capital flow, including investing surplus corporate capital in offshore markets, and Chinese businesses seeking to capitalize on overseas opportunities for financing. The second source concerns corporate demand for centralized and automated cross-border trade settlement. The third one is the need for full convertibility of the RMB. Although some Chinese businesses have developed onshore pooling services in the past, there is still pressing demand for further expansion of these services into a platform for regular cross-border cash management. It’s equally imperative is to develop, based on actual needs, a cross-border investment and financing mechanism. When both are done, a two-way cash pool will be in place.

Cross-border RMB pooling is an experimental effort for HSBC and provides an effective solution for MNCs to channel funds across Chinese borders. This will help corporates to sweep and integrate working capital for their Chinese and international business and even link it up with global pools automatically. Cross-border RMB pooling represents an opportunity to make corporate treasury much more convenient and transparent, allowing businesses to better manage their liquidity.

In the long term, innovative policies developed for the SFTZ will link up China with global funding channels, a development with strategic implications. Currently, MNCs tend to establish a network of treasury centres (cash pools) around the world, with Asia-Pacific operations overseen from Hong Kong or Singapore.

Two-way cross-border RMB cash pooling, as launched by HSBC, will become one of the major factors attracting MNCs to set up their Asia-Pacific headquarters in the SFTZ; the city currently hosts 200 such regional headquarters. The service will also open up a new gateway for corporates to globalize their cash management.

30 I Future directions for foreign banks in China 2014

Source: www.sonepar.ca, 16 June 2014

Sonepar and RBS completes the first RMB Cross-border cash pooling in Shanghai FTZ

Sonepar has become the first French company to implement two-way RMB Cross-border Cash Pooling in the SFTZ (FTZ). Sonepar is an independent family-owned company with global market leadership in B-to-B distribution of electrical products and related solutions. Founded in 1969, Sonepar employs 36,000 associates at 190 entities in 38 countries. The Royal Bank of Scotland (RBS) recently launched this innovative financial solution for multinational companies (MNCs) registered in the Shanghai FTZ.

The RMB Cross-border Cash Pooling is an extension of the service RBS provides to Sonepar’s regional treasury center in Hong Kong, supporting their operations in nine markets across Asia.

Sonepar has identified Asia is a key growth driver for the group with China contributing the largest share. “We are excited to be the first French company to have the ability to conduct two-way cross-border RMB sweeping through our subsidiary in the FTZ. The RBS facility means our regional treasury center in Hong Kong is able to integrate with our China entities’ onshore RMB cash pools. This not only brings greater transparency to our operations in the Mainland, but equally important is that it enables us to deploy RMB liquidity between our onshore and offshore affiliates effectively,” said Mathieu Raffestin, Senior Vice President of Finance, Sonepar Asia-Pacific.

“With liquidity management being more important than ever, especially for a company with a global reach like ours, we were looking for solutions that would not only improve our performance in Asia, but also act as the springboard for our expansion plans in the region. Adding the RMB two-way cross-border sweeping to our regional cash management capability, will be a tremendous support to our ambitious growth strategy in China.”

Commenting on the successful implementation, Manfred Schmoelz, Head of Global Transaction Services, Asia Pacific said: “We are delighted that through this innovative financial solution, RBS is able to help Sonepar in driving greater efficiency in its regional treasury management. This is also an exciting development in conjunction with the Chinese government’s continuing efforts to liberalize the use of RMB for international transactions.”

Future directions for foreign banks in China 2014 I 31

The most important developments according to the foreign banksThe two most important developments occurring in the Mainland China banking market, from the perspective of foreign banks, are RMB internationalization and liberalization of interest rates.

Both factors are mentioned on an equal basis by most of the survey’s participants. In third position is the SFTZ. Many participants believe that the Chinese Government is genuine in its desire to reform the financial system. However, they caution that the pace of reform is subject to a myriad of different and often unpredictable forces.

A North American bank commented that reforms were occurring at a fast pace, and that China should be viewed as an “emerging financial market.”

Other important developments mentioned by participants can be summarized under the following headings:

• Cross-border movement of funds

• Shadow banking and its future regulation

• Disintermediation of Chinese banks by large Chinese corporates

• Changes related to RMB loan quotas

• The loan to deposit ratio (LDR) and future changes

• Chinese corporates expanding internationally

• Interest rate and foreign exchange reform is expected to take place in measured stages

• Fast-paced change is not anticipated

Threats in the marketsSome of the drivers of change mentioned in the previous section, overlap with perceived threats, that may create shocks in the market in both the short and medium term.

A list of such threats raised by participants is listed below. The order in which these threats are listed does not reflect any priority or enhanced importance.

• Economic uncertainty

• Slowdown in government spending

• Liquidity fluctuations

• Non-performing loans in domestic banks

• Shadow banking

• Trade finance fraud

• Consumer complaints on wealth management products

• Interventions by CBRC, PBOC, and SAFE

• E-finance and its impact on traditional channels

• Surplus capacity (over investment by SOEs and POEs) in certain industrial sectors, such as steel

Immediate issuesThe participants were asked to identify the critical issues they faced in the banking market. Four issues were mentioned repeatedly. Liquidity was considered a very important issue, and a number of banks mentioned the need to monitor closely and match requirements on a quarterly basis.

Participants also mentioned a lack of access to capital, and a number commented on the difficulty faced in growing their loan portfolio when capital is in short supply.

Interest rate liberalization, and how it will continue to evolve, also adds market uncertainty and requires careful monitoring. Credit quality, not for foreign banks but in the wider market, is also a concern.

In addition, participants raised the following issues:

• Regulatory transparency

• The shadow banking sector

• A lack of scalability given their current business models

• The threat of an economic downturn

• Future developments in the real estate market

32 I Future directions for foreign banks in China 2014

What is driving change?Participants had little hesitation in suggesting a series of different factors driving change.

These include the regulatory reforms, the move towards RMB internationalization and interest rate liberalization. There are a number of different technology drivers, which are occurring in both the retail and wholesale markets. The e-finance revolution is only beginning, but it will play a major role, albeit subject to regulatory responses.

Changes in customer behavior was frequently cited as a driver. Retail consumer behavior is changing, with younger customers enthusiastically embracing the transition to mobile banking.

The move by Chinese corporates to expand internationally is forcing the domestic banks to internationalize, and simultaneously providing the global networks of foreign banks with new opportunities.

Economic drivers will also cause change in financial markets. Foreign banks noted how an economic slowdown may cause a rise in NPLs and possibly a shake out of non-bank financial institutions and some mid-sized banks.

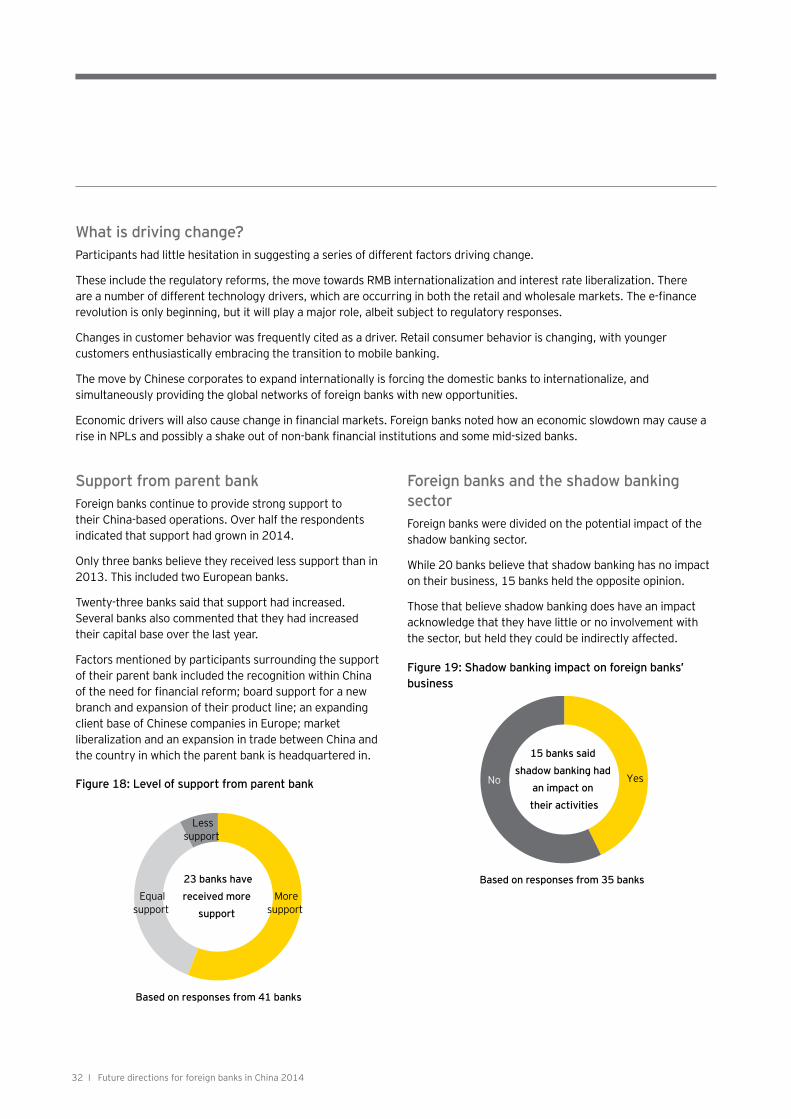

Foreign banks and the shadow banking sectorForeign banks were divided on the potential impact of the shadow banking sector.

While 20 banks believe that shadow banking has no impact on their business, 15 banks held the opposite opinion.

Those that believe shadow banking does have an impact acknowledge that they have little or no involvement with the sector, but held they could be indirectly affected.

Support from parent bankForeign banks continue to provide strong support to their China-based operations. Over half the respondents indicated that support had grown in 2014.

Only three banks believe they received less support than in 2013. This included two European banks.

Twenty-three banks said that support had increased. Several banks also commented that they had increased their capital base over the last year.

Factors mentioned by participants surrounding the support of their parent bank included the recognition within China of the need for financial reform; board support for a new branch and expansion of their product line; an expanding client base of Chinese companies in Europe; market liberalization and an expansion in trade between China and the country in which the parent bank is headquartered in.

Figure 18: Level of support from parent bank

Moresupport

Equalsupport

Lesssupport

Based on responses from 41 banks

23 banks havereceived more

support

Figure 19: Shadow banking impact on foreign banks’ business

No Yes

15 banks said shadow banking had

an impact on their activities

Based on responses from 35 banks

Future directions for foreign banks in China 2014 I 33

34 I Future directions for foreign banks in China 2014

Insights on the health of credit and risk in the corporate and retail marketsSurvey participants provided their views on the current health of a number of markets, from both domestic bank and foreign bank perspectives.

Domestic banksAlmost 80% of the foreign banks believed that corporate credit provided by the domestic banks has deteriorated since 2013. Forty-eight percent of participants believe that the health of consumer credit has declined and 52% believe it remains the same.

Only one-third believe that market risk has deteriorated while 58% think it remains the same.

Finally almost half the group believe that operational risk has worsened.

Figure 20: Foreign banks’ perception of domestic banks’ credit and risk assessment in 2014

Figure 21: Foreign banks’ perception of domestic banks’ credit, 2014 compared to 2013

0 20 40 60 80 100

Operational risk(37)

Market risk(36)

Consumer credit(21)

Corporate credit(37)

Number of participant responses shown in parentheses

WorseSameBetter

Corporate credit

2013

2014

WorseSameBetter

Consumer credit

2013

2014

WorseSameBetter

Based on responses from 37 banks in 2014 and 36 banks in 2013

Based on responses from 21 banks in 2014 and 22 banks in 2013

Future directions for foreign banks in China 2014 I 35

Foreign banksParticipants believe the status of loans looks much better for foreign banks. Only 11% of the 35 respondents think the health of corporate credit provided by them, has declined in the last year. Eighty-three percent think that consumer credit in the foreign banks remains the same as last year. Seventeen percent think it has deteriorated.

From a foreign banks’ perspective, 3% think it is worse while 17% think it has improved and 80% believe the status quo remains. Seventy-eight percent believe operational risk is the same as in 2013 and only 8% think it has declined.

A comparison with the opinions provided in the 2013 survey shows a continued decline in corporate credit’s health at the domestic banks, and a more dramatic decline in consumer credit this year.

From a foreign bank’s perspective, corporate credit appears to have marginally improved, while there has been a slight decline in consumer credit.

Figure 22: Perceptions of foreign banks’ own credit and risk assessment, 2014 compared to 2013

Figure 23: Perceptions of foreign banks’ credit, 2014 compared to 2013

Foreign banks’ corporate credit

2013

2014

WorseSameBetter

Foreign banks’ consumer credit

2013

2014

WorseSameBetter

0 20 40 60 80 100

Operational risk(36)

Market risk(35)

Consumer credit(12)

Corporate credit(35)

Number of participant responses shown in parentheses

WorseSameBetter

Based on responses from 35 banks in 2014 and 36 banks in 2013

Based on responses from 12 banks in 2014 and 11 banks in 2013

36 I Future directions for foreign banks in China 2014

Future directions for foreign banks in China 2014 I 37

04. The regulatory framework

The most important regulatory issues in 2014The top five regulatory issues facing foreign banks in 2014, according to survey participants, are:

1. Removal of the foreign debt quota

2. Removal of the foreign guarantee quota

3. Coordination between regulators

4. Equal access/rights as domestic banks to the bond underwriting market

5. The 10% withholding tax on offshore funding

Survey participants were asked to score regulatory issues on a scale of 1 to 10, with 1 being the least important and 10 being the most important. Scores for the first four issues have increased over last year’s ratings.

Figure 24: The top five regulatory issues in 2014 compared to 2013

0

2

4

6

8

10

Equal

acce

ss/rig

hts as

domes

tic ba

nks t

o the

bond

unde

rwrit

ing m

arket

Waive t

he 10% w

ithho

lding

tax o

n offs

hore

fundin

g

Level

of co

ordin

ation

by re

gulat

ors,

(PBOC, C

BRC, etc.

)

Remov

al for

eign g

uaran

tee qu

ota

Remov

al for

eign d

ebt q

uota

Score

20142013

Foreign debt quotaIn April 2014, SAFE lifted the total amount of short-term foreign debt banks and companies can borrow to US$43.392 billion, which according to Reuters is a 16% increase from 2013. Within this total, US$13.9 billion is allocated to domestic banks, while US$16.54 billion is allocated to foreign banks.8 SAFE awards different quotas to foreign banks based on decisions related to bank size and the loan’s purpose. As a result, some participants are unhappy with their allocation, while others believe it was a non-issue.

Changes in the loan to deposit ratioAnother regulation mentioned by participants, but not ranked in the top five was the loan to deposit ratio, which was redefined on 30 June 2014. This change seeks to stimulate bank lending in the real economy. The new formula excluded agro-related and SMEs financial debts as loans. Locally-incorporated foreign banks were permitted to include funding from their parent bank, provided the maturity exceeds one year.

8 Reuters, 8 April 2014

38 I Future directions for foreign banks in China 2014

Future directions for foreign banks in China 2014 I 39

Copyright: China Banking Regulatory Commission ADDR:Jia N0.15 Financial Street, Xicheng District, Beijing, 100140

The CBRC Releases Notice on Adjusting Loan-to-Deposit Calculation Rules for Commercial Banks

Loan-to-deposit (LTD) ratio is a statutory regulatory indicator provided in the Commercial Bank Law. To adapt to a more diversified banking balance sheet structure and improve the regulatory framework, the CBRC, building on previous work, recently further improved the measures for improving LTD regulation. The Notice on Adjusting Loan-to-Deposit Calculation Rules for Commercial Banks was released, effective on 1 July 2014.

Experiences from at home and abroad demonstrate that LTD ratio has contributed a lot to managing liquidity risk, curbing rapid credit growth and stabilizing the banking sector. However, as commercial banks’ balance sheet structure and operation model are changing and financial market keeps evolving, the LTD regulation becomes limited in coverage and not sensitive enough to risks, and does not fully accommodate that banking assets, with different funding sources and investment, enjoy different duration and stability, thus unable to fully reflect the liquidity risks of banking sector.

The CBRC highly emphasizes the improvement of LTD ratio regulation. On one hand, it has been actively promoting the revision of Commercial Bank Law; on the other hand, it’s been constantly improving the calculation method of LTD ratio. For example, agro-related and MSE financial debts will not be considered loans into the calculation of LTD ratio. Since 2011, the CBRC has begun implementing monthly average daily LTD ratio. These measures have delivered results in promoting commercial banks to support the real economy and reducing deposit fluctuations. The LTD ratio of Chinese commercial banks was 65.9 percent by the end of March, down 0.18 percentage point compared with year beginning, well below the regulatory ceiling of 75 percent.

To improve the regulation of LTD ratio, the CBRC made the following changes to the calculation.

First, the previous calculation counted deposits and loans in both local and foreign currencies. But now it will only involve deposits and loans denominated in yuan. Deposits and loans in other currencies will be used as a monitoring indicator. This adjustment conforms to current laws and regulations and requirements for managing major currency liquidity risks set forth in Basel III and Rules on Liquidity Risk Management of Commercial Banks (Provisional). Meanwhile, regulatory arbitrage through currency conversion can be prevented by monitoring the LTD both in foreign and local currencies.

Second, the calculation no longer consider agro-related and MSE financial debts as loans. On top of that, there are three additional deductions. First, bonds issued by commercial banks with a remaining maturity period of no less than one year and no early redemption. Second, MSE loans. Third, loans extended by some commercial banks by using funds from international financial organizations or overseas governments. All the above-mentioned loans enjoy clear and stable funding sources, therefore no need for matching deposit.

Third, the calculation of deposits will incorporate two more items: first, negotiable certificates of deposits issued by banks to enterprises and individuals; second, foreign banks’ net deposits from their overseas parent banks with a maturity of over one year. The first category is a stable source of funding for banks. A considerable amount of capital of incorporated foreign banks comes from their parent banks, among which the net capital with over one year maturity will be counted as deposit, so as to help foreign banks to fully utilize this stable source of funding to expand their business and support the real economy in China.

This adjustment plan does not change the basic calculation method for LTD ratio and is easy to be implemented. The quantitative result demonstrates that the plan can help commercial banks devote more credit to supporting the real economy. The CBRC will monitor the impact of the changing LTD ratio calculation on banks’ business and the financial market. It will take prompt measures to prevent regulatory arbitrage against banks with big swings in their loan-to-deposit ratio. Meanwhile, according to the Rules on Liquidity Risk Management of Commercial Banks (Provisional), the CBRC will employ loan-to-deposit ratio, liquidity ratio, liquidity coverage ratio and multi-dimensional risk monitoring index to track and analyze banking liquidity risks and safeguard the soundness of the banking sector. In the mid to long term, the CBRC will actively promote the revision of the Commercial Bank Law by working with legislative authorities.

40 I Future directions for foreign banks in China 2014

Rankings of regulatory issues highlighted by the European Chamber of Commerce in ChinaFigure 25 records a list of issues raised by the European Union Chamber of Commerce in China in its annual position paper, and shows the number of participants in the 2014 survey who ranked the issue.

For example, the foreign debt quota was highlighted by 30 banks and scored 9.17 out of 10. The three-year waiting period for an RMB license was a problem for 17 banks.

On 21 December 2014, the government announced that the three-year wait period for a new RMB license would be reduced to just one year, and removed the requirement that foreign banks applying for a license be profitable for two years before their application.

The adjacent table shows that 17 participants scored the three-year wait period at 7.71 in the survey and this change of policy will be well received by the foreign banks.

Many banks awarded a lower score to VAT reform, because they viewed it as a normal, if onerous, part of doing business.

The score for branch expansion was similar to 2013, while the score for ownership and scope for foreign banks versus domestic banks dropped from 7.1 in 2013 to 6.65 in 2014.

Figure 25: Participants’ scores for the regulatory issues raised by the EU Chamber

Issues raised by EU Chamber of Commerce in China

Score out of

10 Removal foreign debt quota (30) 9.17

Removal foreign guarantee quota (10) 8.70

Level of coordination by regulators, (PBOC, CBRC, etc.) (31)

8.42

Equal access/rights as domestic banks to the bond underwriting market (30)

8.40

Waive the 10% withholding tax on offshore funding (22)

8.05

Waive the 5% business tax on onshore and offshore lending (21)

7.90

Further review the LDR calculation (following recent changes) (17)

7.76

The three-year wait period for RMB (17) 7.71

Abolish the cost-based income taxation of rep offices (14)

7.36

VAT reform (20) 7.35

License approval process (29) 7.34Better communication of loan loss provisioning ratio (CBRC, MOF) (18)

7.28

Easier branch/outlet expansion (21) 6.86

Greater ownership and scope for foreign vs. domestic (23)

6.65

Source: European Union Chamber of Commerce in China in its annual position paper. Participants scored each factor on a scale of 1 to 10, 10 being the most important.

Future directions for foreign banks in China 2014 I 41

American Chamber of Commerce (AmCham) in China’s regulatory scorecard, April 2014Figure 26 outlines the progress made on key regulatory issues, as identified by AmCham in 2014.

It comments on the 20% investment ceiling for domestic banks, access to the bond market, and in the context of RMB internationalization, the China International Payments System. Further details on the AmCham review of the financial sector can be found in the appendices.

Figure 26: AmCham’s assessment of progress on key issues 2013

2013 recommendation 2014 recommendation

Commercial banking Raise and eventually eliminate the ceiling of ownership of foreign investors in local Chinese banks.

Low progress Raise the 20% investment ceiling imposed on foreign banks when investing in local Chinese banks, to incentivize foreign banks to transfer more of their expertise and best practices to their Chinese partners.

Credit rating N/A N/A Follow prevailing international practices, such as the IOSCO Code, and remove mandatory ratings requirements from relevant financial sector rules.

Interbank markets Further lift interbank limitations over foreign firms from the People’s Bank of China (PBOC) and the National Association of Financial Market Institutional Investors (NAFMII).

Low progress Further lift interbank limitations over foreign firms from the PBOC and the NAFMII.

Liquidity management N/A N/A Allow foreign banks to access the bond and certificate deposits (CD) markets for diversified sources of stable funding.

Private equity Keep the international “see-through” income taxes practice to avoid double taxation.

Moderate progress

Use “domestic in nature” treatment for foreign GP controlled RMB funds.

RMB internationalization

N/A N/A Release further information on the establishment of the China International Payment System.

Securities and bonds Grant SJVs business licenses related to innovative products more flexibly; shorten the grace period for securities JVs to get new licenses.

Moderate progress

More flexibly grant SJVs business licenses related to innovative products, and shorten the grace period for securities JVs to get new licenses.

Source: AmCham China 2014 White Paper Priority Recommendations Scorecard, April 2014

42 I Future directions for foreign banks in China 2014

A deposit insurance scheme for ChinaIn the first half of 2014, various media reports suggested that the Chinese government planned to set-up a deposit insurance scheme during the year. It is widely expected that a deposit scheme will be launched before the PBOC dismantles the ceiling on deposit rates.

At the time of writing this report, it is thought that the scheme will be introduced in 2015. Whilst removal of the deposit rate cap is a key part of financial reform, it is understood that it will introduce uncertainty and volatility into the financial markets.

China remains the only significant world economy without deposit insurance. At the end of 2013, 112 countries out of 189 surveyed by the World Bank have explicit deposit insurance schemes.9

Expected impact of deposit insurance on foreign banksTen participants said a deposit insurance scheme would have a significant impact and two banks indicated it would have a very significant impact. In contrast, 24 banks suggested it would have an insignificant or no impact.

It is clear that those most impacted by a deposit insurance scheme will be foreign banks with a retail focus. A number of participants believe a deposit insurance scheme could be implemented before the end of 2014, but others felt it will be another one to two years before implementation.