Embed Size (px)

Citation preview

FUNDAMENTALS VALUATION

NTPC Limited

29th

April 2011

ANALYTICAL CONTACT

Ms. Revati Kasture +91-22-6754 3465 [email protected]

BUSINESS DEVELOPMENT CONTACTS

MUMBAI

Mr. P. N. Satheeskumar +91-22-6754 3555 [email protected]

KOLKATA

Mr. Sukanta Nag +91-33- 2283 1800 [email protected]

CHENNAI

Mr. V Pradeep Kumar +91-44-2849 7812 [email protected]

AHMEDABAD

Mr. Mehul Pandya +91-79-40265656 [email protected]

NEW DELHI

Ms. Swati Agrawal +91- 11- 2331 8701 [email protected]

BANGALORE

Mr. G. Sundara Vathanan +91-80-2211 7140 [email protected]

HYDERABAD

Mr. Ashwini Kumar Jani +91-40-40102030 [email protected]

CARE EQUITY RESEARCH OFFERS

Independent Research of equities on fundamentals or valuations or both

IPO Grading

White Label Research

Valuation of companies for Institutional Investors, Asset Managers and Corporates

Sector Write-ups for Offer Documents of securities

NTPC LIMITED

1 www.careratings.com

EQUIGRADE

EQUIGRADE – Analytical Power for Investment Decisions

NTPC Limited Electric Utilities

Strong Fundamentals; Considerable Upside Potential CMP : Rs. 183.5 / CIV : Rs. 246 1

Sensex: 19,291

CARE Equity Research assigns 5/5 on fundamental grade to NTPC

CARE Equity Research assigns fundamental grade of 5/5 to NTPC. This

indicates ‘Strong Fundamentals’. The grade draws strength from NTPC’s

leadership position in India’s power generation sector, commendable

execution track record, revenue security through power purchase

agreements for existing as well as capacities planned over more than

coming two decades and fuel security through long term coal supply

agreements. Secured profitability of the company, being an efficient

player in the industry with regulated returns, further supports our grading

strength. Foray in forward and backward links like coal mining, power

trading and equipment manufacturing to some extent adds to the

strength of the company. ‘Maharatna’ status gives the highly experienced

board significant autonomy in its business decision-making. Low interest

costs, reasonable gearing levels, healthy cash balance, 100 per cent

realisation of power bills and healthy dividend payment track record

indicates strong financial position. With plans to double the power

generating capacity by FY17, NTPC would continue to ‘feed the power

hungry India’.

However, CARE Equity Research views the timely completion of

expansion projects, timely and continuous availability of fuel and timely

availability of equipment as key moniterable for the company.

Furthermore, minority stakeholders do not have significant say in

company’s affairs.

Valuation

CARE Research assigns valuation grade of 5/5 to NTPC based on the

Current Intrinsic Value (CIV) of Rs. 246 as against Current Market Price

(CMP) of 183.5. This indicates ‘Considerable Upside Potential’. CARE

Equity Research has used Discounted Cash Flow (DCF) to value the

power related business and EV per tonne for valuing its coal assets.

1 2 3 4 5

Fundamentals

Valuation

Market Capitalisation Rs. Bn. 1,509

Enterprise Value Rs. Bn. 1,790

52 Week High / Low Rs. 219 / 170

Diluted EPS (consolidated - FY10) Rs. 10.7

P/E (FY10) times 17.1

Beta times 0.7

Average Daily Volumes* Bn. 0.6

* BSE + NSE for last 52 weeks

Returns 1M 3M 6M I Yr

Absolute 5% -2% -9% -10%

Rel. to Sensex -1% -3% -3% -19%

Revati Kasture Head - Research +91-22-6754 3465

Dhimant Kothari Senior Manager +91-22-6754 3479

Hitesh Avachat Analyst +91-22-6754 3447

1 CMP: Current market Price; CIV; Current Intrinsic Value

ANALYTICAL CONTACTS

CARE EQUIGRADE GRID (CEG)

CEG is explained on the last page

KEY EQUISTATS

STOCK PERFORMANCE

SHARE HOLDING PATTERN

Financial Information Snapshot

(Rs. Billion) FY10 FY11 P FY12 P FY13 P

Operating Income 512 591 701 827

EBITDA 160 171 210 252

PAT (After minority interest) 88 91 105 117

Fully Diluted EPS* (Rs.) 10.7 11.1 12.7 14.1

Dividend Per Share (Rs.) 3.8 4.0 4.3 4.5

P/E (times) 17.1 16.5 14.4 12.9

EV/EBITDA (times) 11.2 10.4 8.5 7.1

* Calculated on Current Face Value of Rs. 10/- per share

29th

April2011

NTPC LIMITED

www.careratings.com 2

EQUIGRADE

Power: indispensable to power India growth story; execution a key

In a fast growing economy like India, there is an indispensible need for more and more power. Furthermore, with

current situation of power deficit, opportunity in the sector remains humungous. The total energy deficit and peak

deficit in FY10 stood at approximately 10.1 per cent and 12.7 per cent respectively. In the scenario of GDP

growing at 8 per cent, which according to CARE Equity Research seems realistic, the energy demand is likely to

increase from around 110 Giga Watts (GW) in FY11E to 160 GW in FY17 and 220 GW in FY22. This translates

into a compounded annual growth rate (CAGR) of more than 6 per cent through the above period. Accordingly,

from the current capacity of around 162 GW, the power generation capacity need to grow to around 230 GW by

FY17 and 310 GW by FY22 assuming similar PLF. The timely execution of such huge quantum of expansions

would remain a key for the sector, given the challenges relating to tying up of fuel / feedstock, acquisition of land,

timely delivery of capital equipments, achieving financial closure on time and at feasible terms, disposal of waste

(like ash in case of coal fuelled plant), etc.

NTPC has big plans to en-cash upon this opportunity

NTPC, with current capacity standing at around 34 GW or around 21 per cent of capacities in India that generates

close to 30 per cent of the power generated in India, plans to double its capacity by FY17 and further to 128 GW

by FY32 under its Long Term Corporate Plan. Accordingly, NTPC would account for more than 25 per cent of

power capacities in India by then. Thus, NTPC would continue to ‘feed the power hungry India’. Though NTPC

did not manage to win any of the four Ultra Mega Power Projects (UMPPs) announced by the Government

recently for cumulative capacity of 16 GW, CARE Equity Research feels that it is not of a major concern, as the

company has much bigger expansion plans chalked out for it. CARE Equity Research expects NTPC to surpass 50

GW of capacity by the end of FY15.

Details of UMPPs

Source: CARE Equity Research

FUNDAMENTAL GRADE Strong Fundamentals 5/5

UMPP State Lowest Bidder Bid Price

(Rs. / Kw h)

NTPC's Bid

(Rs. / Kw h)

Capacity

(MW)

Sasan Madhya Pradesh Reliance Power 1.19 2.12 3,960

Krishnapatanam Andhra Pradesh Reliance Power 2.33 n.a.1

3,960

Tilaiya Jharkhand Reliance Power 1.77 2.39 3,960

Mundra Gujarat Tata Power 2.26 n.a.1

4,000

1 NTPC did not submit any bid for these UMPPs

NTPC LIMITED

3 www.careratings.com

EQUIGRADE

NTPC’s projects under construction (Alphabetical order)

(a) Successfully synchronized on 07th

March 2011

(b) Successfully synchronized on 18th

February 2011

(1) Joint Venture with Haryana Power Generation Corporation Ltd. and Indraprastha Power Generation Co. Ltd.

(2) Joint Venture with Bihar State Electric Board

(3) Joint Venture with Railways

(4) Joint Venture with Tamil Nadu Electricity Board

Source: Company, CARE Equity Research

NTPC’ execution track record speaks for itself

NTPC’s capacity increased from 200 mega watts (MW) in FY82 or merely 0.6 per cent of the total installed

capacities in India then to 10 GW in FY91 or 15 per cent of the total installed capacities in India and further to 34

GW in FY 11 or 21 per cent of the total installed capacities in India now. Thus, NTPC’s track record speaks for

itself, highlighting its commendable ability to execute power projects. Though such capacity additions would have

faced various challenges, the capacity additions have been at a much faster rate than the industry. In the last three

years, which were dotted by the global economic crisis and subsequent recovery, India saw capacity additions of 19

GW. Of this, 7 GW or close to 37 per cent of the capacities were added by NTPC alone.

Project Fuel Capacity

(MW)

Cost (Rs.

Bn.)

Barh I Bihar Coal 1,980 105

Barh II Bihar Coal 1,320 70

Bongaigaon Assam Coal 750 33

Farakka VI (a) West Bengal Coal 500 26

Indira Gandhi STPP (1) Haryana Coal 1,000 53

Koldam - U1 Himachal Pradesh Hydel 800 37

Mauda I Maharashtra Coal 1,000 56

Muzaffarpur (2) Bihar Coal 390 20

Nabinagar (3) Bihar Coal 1,000 50

Rihand III Uttar Pradesh Coal 1,000 60

Simhadri II Andhra Pradesh Coal 1,000 49

Sipat – 1 (b) Chhattisgarh Coal 1,980 90

Tapovan Vishnugad Uttaranchal Hydel 520 27

Vallur I (4) Tamil Nadu Coal 1,500 76

Vindhyachal IV Madhya Pradesh Coal 1,000 57

Total 15,740 809

NTPC LIMITED

www.careratings.com 4

EQUIGRADE

NTPC: Capacity addition track record

Source: Company, CARE Equity Research

Real-time project monitoring helps smooth project execution and removal of bottle-necks at a faster pace

NTPC has state-of-the art Project Monitoring Centre (PMC) comprising of IT-based real-time monitoring of

various new and on-going projects. The PMC, which forms part of management information system, is equipped

with high resolution remote controlled cameras and video conferencing facilities. The system at PMC captures and

reports more than 2,000 critical parameters of the project online and helps management take a much faster

decision, including that on the bottle-necks affecting the project. The access of PMC is made available to the

Ministry of Power, which renders complete visibility of the progress of the projects.

‘Maharatna’ status enhances the NTPC board’s autonomy

NTPC was awarded ‘Navratna’ status way back in 1997 that gave the Board of Directors autonomy to take

company’s capital expenditure of any quantum and investment decisions to some extent. The decision for equity

investment in joint ventures (JV) or special purpose vehicles (SPV) or for acquisition of stakes by the board

without any approvals was restricted to Rs. 1,000 crore per acquisition / investment. With the prestigious

‘Maharatna’ status accorded in 2010, the scope of autonomy was widened with the upper cap on investments

enhanced to Rs. 5,000 crore per acquisition / investment without any approvals. This would enable NTPC to

acquire coal mines / stake in coal mines and / or invest in power projects of much higher capacities with much

more strategic decision making flexibility. The board is also empowered to create and to wind up all below the

board level posts, which gives operational flexibility.

Power Purchase Agreements in place for 3 times the current capacity

Power is transacted in India largely through the long term power purchase agreements (PPAs). NTPC already has

PPAs in place for more than 100 GW. Thus, not only the off-take is secured for current capacity of 34 GW, but

also for capacities much beyond those planned till FY17. As mentioned, NTPC plans to double its capacity by

FY17. Thus, the revenue visibility is very high for the company.

0

50

100

150

200

FY82 FY91 FY11E

NTPC Rest of India

CAGR 6%

CAGR 19%G

W

NTPC LIMITED

5 www.careratings.com

EQUIGRADE

NTPC: Power Purchase Agreements

Source: Company

Fuel security also appreciable

Tying up fuel is a big challenge in the Indian power generation industry. However, NTPC has secured its coal

requirements Long Term Model Coal Supply Agreement (CSA) with Coal India Limited (CIL), the largest coal

miner in India, and its subsidiaries for supply of coal to its various power stations for 20 years. The reliance on

coal sold through e-auction and imported coal is significantly low. The agreement for supply of imported coal is

also made with MMTC. This ensures fuel security and in turn revenue security for the company.

Furthermore, NTPC has also ventured into coal mining. It has already been allocated five coal blocks by the

Government. These blocks have total mineable reserves of close to 2 billion tones and the company expects to

have mining capacity of 65 - 70 million tonnes per annum (mtpa) by FY17. The output from the captive mines is

expected to meet close to one-fifth of NTPC’s coal requirement by the end of FY17 on higher capacities.

However, the timely development of coal blocks remain a key moniterable, as NTPC has been issued show-cause

notices in relation to delay in developing coal blocks. NTPC has appointed Thiess Minecs India Private Limited

as mine developer-cum-operator for Pakri Barwadih Coal Mining Project for a period of 27 years. The peak

production from this mine is expected to be 15 mtpa.

Besides, NTPC is also part of a JV christened International Coal Ventures Private Limited (ICVPL) that involves

other big companies like SAIL, Rashtriya Ispat Nigam Limited, Coal India Limited and NMDC for buying coal

mines abroad. NTPC holds 14.3 per cent stake in ICVPL.

Similarly, NTPC has formed two separate 50:50 JVs with Singareni Coalieries Company Limited (SCCL) and

Coal India Limited (CIL) christened NTPC SCCL Global Ventures Private Limited and CIL NTPC Urja Private

Limited (CNUPL) respectively to jointly acquire, develop and operate coal blocks in India and overseas. CNUPL

has been allotted two coal blocks – Brahmini and Chichro Patsimal with total mineable reserves of around 1

billion tonnes.

Description GW

For capacities already commissioned 33

For capacities under construction 16

For capacities under bidding 14

For New Projects 37

Total 100

NTPC LIMITED

www.careratings.com 6

EQUIGRADE

NTPC: Coal Blocks

# Estimates; *CNUPL JV

Source: CARE Equity Research

However, the dispute with Reliance Industries regarding gas supply at $ 2.53 per million metric british thermal

units (mmbtu) is not yet resolved.

Foray in forward and backward links adds to the strength of NTPC

Besides coal mining, NTPC’s foray in backward link of equipment manufacturing and forward link of power

trading adds to its strengths.

It has entered into two JVs, namely NTPC BHEL Power Projects Private Limited (50 per cent stake) with BHEL

and BF NTPC Energy Systems Limited (49 per cent stake) with Bharat Forge and has acquired 44.6 per cent stake

in Transformers and Electricals Kerala Limited. These investments relate to the business of manufacturing capital

equipments for power plants. The business of manufacturing power equipments is new for NTPC. Nevertheless,

NTPC’s rich domain knowledge of the power sector and experience of the JV partner would be advantageous.

Block State Mineable Reserves#

(mn tonnes)

Pakri-Barwadih Jharkhand 700

Talaipali Jharkhand 600

Kerandari Jharkhand 140

Chatti-Baritu Jharkhand 310

Dulanga Orissa 200

Brahmani* Orissa 1,000

Chichro-Patsimal* Orissa 160

Total 8 Blocks 3,110

NTPC LIMITED

7 www.careratings.com

EQUIGRADE

NTPC: Investments relating to equipment manufacturing

Source: CERC

NTPC also has a 100 per cent subsidiary NTPC Vidyut Vyapar Nigam Limited (NVVN) engaged in the business

of power trading and 16.67 per cent stake in National Power Exchange Limited (NPEX). NVVN has been

designated as the Nodal Agency for the purchase of up to 1,000 MW of solar power under the National Solar

Mission. However, a major portion of power is sold in India through long term PPAs and small portion is

transacted through other modes, including power exchanges. Nevertheless, investment made in power trading and

power exchange is a good attempt to make NTPC a holistic player in the power industry.

Challenges inevitable for the company

CARE Equity Research acknowledges the capabilities of NTPC with respect to both project execution and plant

operations, given its large size, better negotiating power, historical track record, revenue visibility through PPAs

fuel security and experienced management. Nevertheless, the challenges are inevitable for the company. NTPC

may face challenges with respect to:

• Timely and continuous availability of fuel: Any situation of non-availability of feedstock or disruption in

supplies can affect the expansion plans or running operations of the company. To illustrate, NTPC’s gas

based power projects at Kawas and Gandhar are facing challenges of fuel supplies, as the dispute with

Reliance Industries regarding gas supply at $ 2.53 per million metric british thermal units (mmbtu) is not yet

resolved. Though NTPC has made an attempt for Liquefied Natural Gas (LNG) supplies from Nigeria, it has

not been successful yet.

• Timely availability of equipments: NTPC is largely dependent on BHEL, the only sub-critical component

manufacturer in India. There is shortage in the power equipment sector and the fate depends on the capital

expansion plans of BHEL, which are currently under-way. Nevertheless, imported equipments remain an

option, with NTPC importing super-critical equipments from Russian and Korean companies.

• Securing land and waste disposal: Securing of land and arranging for waste disposal is also very critical for the

company for timely execution of expansions and smooth operations of its plants. The company largely has

coal based power capacities, which leads to generation of ash. Though the company attempts to dispose the

Company Stake Objective

NTPC BHEL Power Projects

Private Limited 50.0%

To explore, secure and execute EPC contracts for power

plants and to engage in manufacturing and supply of

equipments for power plants

BF NTPC Energy Systems

Limited 49.0%

To manufacture castings, forgings, fittings and high Pressure

piping required for power and other industries, Balance of

Plant (BOP) equipment for the power sector etc.

Transformers and Electricals

Kerala Limited 44.6% For Manufacturing and repair of Transformers

NTPC LIMITED

www.careratings.com 8

EQUIGRADE

same in environmental friendly manner, disposal of huge quantum remains a challenge. India has seen

instances of power projects facing opposition over concerns relating to environment or relocation of

population or adverse impact to local agriculture.

NTPC had planned to add 21 - 22 GW of capacities in the Eleventh Five Year Plan (FYP) from FY07 to FY12.

But it is expected to add only 12 GW, a slippage of around 10 GW. The slippages can be attributed to contracting

disputes in three projects, resolution whereof is underway. Getting clearance from various Government

departments also remains a bottle-neck for capacity expansions. However, CARE Equity Research is of the

opinion that challenges relating to financial closure are minimal on the back of healthy financial position and

strong cash accruals. The company is rated ‘AAA’ by CARE Ratings which means highest safety for timely

servicing of debt obligations and minimal credit risk.

Majority stake with Government leads to minority stake holder having limited say

Despite the recent dilution of 5 per cent in last quarter of FY10, the Government of India, through the President

of India holds 84.5 per cent stake in the company. Thus structurally, minority stakeholders do not have significant

say in the affairs of the company. Despite the good corporate governance practices, healthy internal control

systems and accountability, the minority is exposed to the risk of influence by the Government decisions, which

may many a times be in the interest of nation at large, thereby placing the minority shareholders at

disadvantageous position.

Healthy Corporate Governance practices

NTPC’s board currently comprises of nineteen directors, which include Chairman and Managing Director (CMD)

and six whole time functional directors (Finance, Commercial, Projects, Technical, HR and Operations) all having

rich experience of 25 – 35 years. Two directors are nominees of Government of India, while nine are independent

non-official part time directors and one as Chief Vigilance Officer (CVO) of the company.

NTPC has constituted ten committees which include Audit Committee, Shareholders/ Investors Grievance

Committee, Remuneration Committee, Committee on Management Controls, Contracts Sub- Committee, Project

Sub-Committee, Investment/Contribution Sub-Committee, Committee of the Board for allotment and post

allotment activities of NTPC’s Securities, Committee for Further Public Offering of NTPC’s Securities and

Enterprise Risk Management Committee. The company also has its own internal audit department and CVO as

mentioned.

NTPC was adjudged as one of the best governed company of India by a jury headed by Former Chief Justice of

India. It was conferred ‘ICSI National Award for Excellence in Corporate Governance – 2009’ by the Institute of

Company Secretaries of India. NTPC has also bagged ‘Golden Peacock Global Award for Excellence in

Corporate Governance for the year 2009’.

NTPC LIMITED

9 www.careratings.com

EQUIGRADE

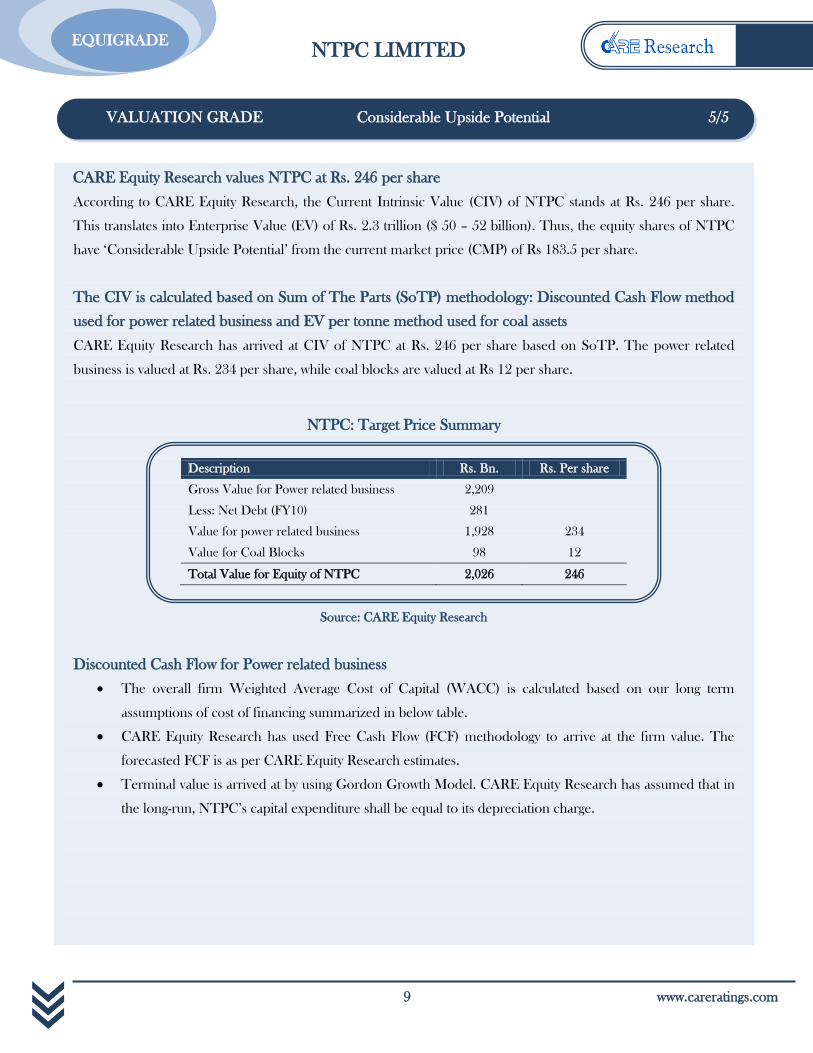

CARE Equity Research values NTPC at Rs. 246 per share

According to CARE Equity Research, the Current Intrinsic Value (CIV) of NTPC stands at Rs. 246 per share.

This translates into Enterprise Value (EV) of Rs. 2.3 trillion ($ 50 – 52 billion). Thus, the equity shares of NTPC

have ‘Considerable Upside Potential’ from the current market price (CMP) of Rs 183.5 per share.

The CIV is calculated based on Sum of The Parts (SoTP) methodology: Discounted Cash Flow method

used for power related business and EV per tonne method used for coal assets

CARE Equity Research has arrived at CIV of NTPC at Rs. 246 per share based on SoTP. The power related

business is valued at Rs. 234 per share, while coal blocks are valued at Rs 12 per share.

NTPC: Target Price Summary

Source: CARE Equity Research

Discounted Cash Flow for Power related business

The overall firm Weighted Average Cost of Capital (WACC) is calculated based on our long term

assumptions of cost of financing summarized in below table.

CARE Equity Research has used Free Cash Flow (FCF) methodology to arrive at the firm value. The

forecasted FCF is as per CARE Equity Research estimates.

Terminal value is arrived at by using Gordon Growth Model. CARE Equity Research has assumed that in

the long-run, NTPC’s capital expenditure shall be equal to its depreciation charge.

VALUATION GRADE Considerable Upside Potential 5/5

Description Rs. Bn. Rs. Per share

Gross Value for Power related business 2,209

Less: Net Debt (FY10) 281

Value for power related business 1,928 234

Value for Coal Blocks 98 12

Total Value for Equity of NTPC 2,026 246

NTPC LIMITED

www.careratings.com 10

EQUIGRADE

NTPC: Valuation of Equity

Source: CARE Equity Research

Enterprise Value per tonne for coal blocks

The average Enterprise Value (EV) of coal miners usually ranges from $ 1.5 to $ 2.5 per tonne depending

on the quality of reserves, mining capacities and capacity ramp up plans.

The EV of Coal India Limited (CIL), the largest coal miner in India stands at Rs. 80 per tonne, based on

market price of Rs. 300 per share and mineable reserves of 19 billion tonnes.

Though the market price of CIL’s share is dynamic, EV of Rs. 80 per tonne ($1.8 per tonne) appears

reasonable.

Item Value Basis

Risk Free Rate 8.25% 10 year G-Sec yields

Equity Risk Premium 6.00% Average inflation

Beta 0.6 One year stock performance vis-a-vis Sensex

Cost of Equity 11.85%

Cost of Debt 6.00% Long term cost of debt

Tax Rate 25.00% Long term tax rate

Debt/Equity Ratio 1.00 Long term target D/E ratio

WACC 8.18%

Terminal growth rate 3.00%

(Rs billion except per share data)

2010-11 2011-12 2012-13 2013-14 2014-15

PAT 91 105 117 128 143

Deferred tax Liability 17 21 24 26 30

Depreciation 24 30 40 49 57

Interest (1-Tax Rate) 19 28 40 52 61

Capital Expenditure -207 -249 -264 -241 -279

Increase in Working Capital -12 -22 -37 -49 -62

Free Cash Flow (FCF) -68 -87 -81 -35 -50

Discount Rate 1.00 0.92 0.85 0.79 0.73

PV of FCF -68 -80 -69 -28 -37

PV of Terminal Value 2,491

Total Discounted Value of Firm 2,209

Less: Net Debt (FY10) 281

Sub Total 1,928

Add: Value of coal mines 98

Present Value of equity 2,026

No of Equity Shares (billion) 8

CIV 246

NTPC LIMITED

11 www.careratings.com

EQUIGRADE

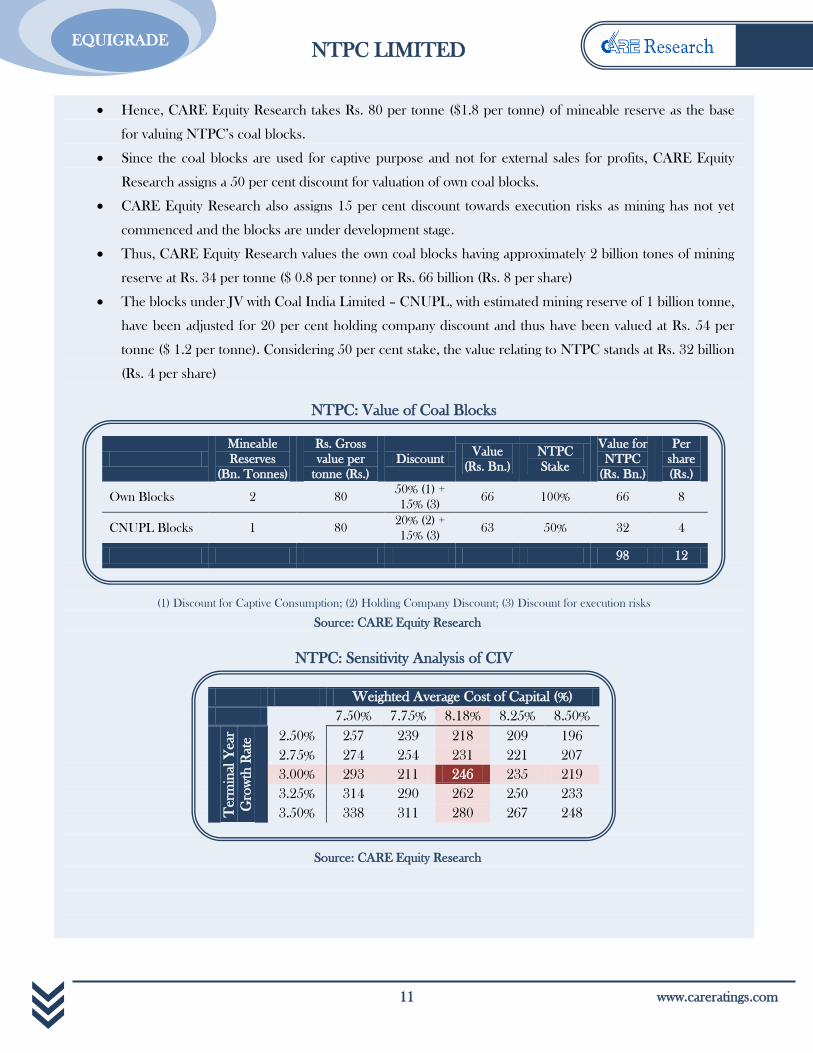

Hence, CARE Equity Research takes Rs. 80 per tonne ($1.8 per tonne) of mineable reserve as the base

for valuing NTPC’s coal blocks.

Since the coal blocks are used for captive purpose and not for external sales for profits, CARE Equity

Research assigns a 50 per cent discount for valuation of own coal blocks.

CARE Equity Research also assigns 15 per cent discount towards execution risks as mining has not yet

commenced and the blocks are under development stage.

Thus, CARE Equity Research values the own coal blocks having approximately 2 billion tones of mining

reserve at Rs. 34 per tonne ($ 0.8 per tonne) or Rs. 66 billion (Rs. 8 per share)

The blocks under JV with Coal India Limited – CNUPL, with estimated mining reserve of 1 billion tonne,

have been adjusted for 20 per cent holding company discount and thus have been valued at Rs. 54 per

tonne ($ 1.2 per tonne). Considering 50 per cent stake, the value relating to NTPC stands at Rs. 32 billion

(Rs. 4 per share)

NTPC: Value of Coal Blocks

(1) Discount for Captive Consumption; (2) Holding Company Discount; (3) Discount for execution risks

Source: CARE Equity Research

NTPC: Sensitivity Analysis of CIV

Source: CARE Equity Research

Weighted Average Cost of Capital (%)

7.50% 7.75% 8.18% 8.25% 8.50%

Term

inal

Year

Gro

wth

Rat

e 2.50% 257 239 218 209 196

2.75% 274 254 231 221 207

3.00% 293 211 246 235 219

3.25% 314 290 262 250 233

3.50% 338 311 280 267 248

Mineable

Reserves

(Bn. Tonnes)

Rs. Gross

value per

tonne (Rs.)

Discount Value

(Rs. Bn.)

NTPC

Stake

Value for

NTPC

(Rs. Bn.)

Per

share

(Rs.)

Own Blocks 2 80 50% (1) +

15% (3) 66 100% 66 8

CNUPL Blocks 1 80 20% (2) +

15% (3) 63 50% 32 4

98 12

NTPC LIMITED

www.careratings.com 12

EQUIGRADE

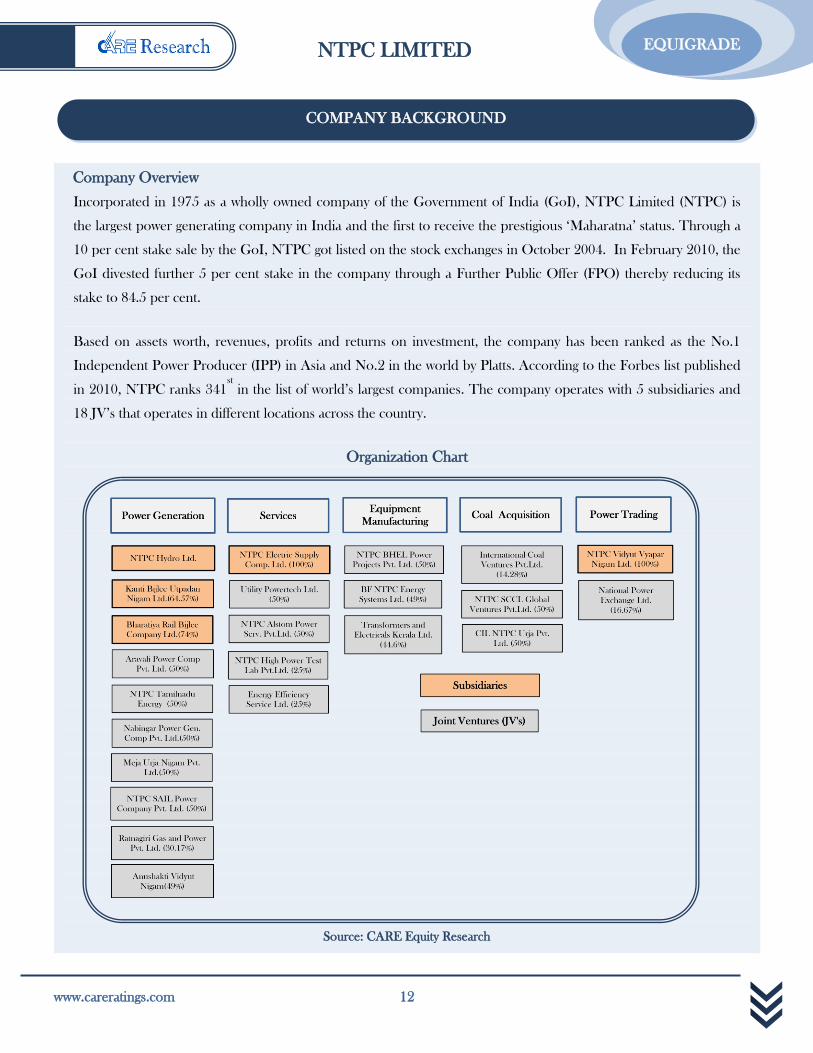

Company Overview

Incorporated in 1975 as a wholly owned company of the Government of India (GoI), NTPC Limited (NTPC) is

the largest power generating company in India and the first to receive the prestigious ‘Maharatna’ status. Through a

10 per cent stake sale by the GoI, NTPC got listed on the stock exchanges in October 2004. In February 2010, the

GoI divested further 5 per cent stake in the company through a Further Public Offer (FPO) thereby reducing its

stake to 84.5 per cent.

Based on assets worth, revenues, profits and returns on investment, the company has been ranked as the No.1

Independent Power Producer (IPP) in Asia and No.2 in the world by Platts. According to the Forbes list published

in 2010, NTPC ranks 341st in the list of world’s largest companies. The company operates with 5 subsidiaries and

18 JV’s that operates in different locations across the country.

Organization Chart

Source: CARE Equity Research

COMPANY BACKGROUND

NTPC LIMITED

13 www.careratings.com

EQUIGRADE

Business Overview

With a total current installed capacity of 34 GW (including Joint Ventures), NTPC is primarily engaged in the

business of power generation. During FY10, NTPC’s power generation plants accounted for around 18 per cent

and 29 per cent of the overall country’s power generating capacity and actual power generation respectively. The

power generation division accounts for almost the entire share of the company’s revenue. NTPC is also venturing

into new business activities like power trading, power equipment manufacturing, coal mining and consultancy. The

company plans in becoming an Integrated Power Major by diversifying itself through backward, forward and lateral

integration.

NTPC’s contribution to domestic power sector

*Excluding JVs

Source: CARE Equity Research

As on 31st

March, 2010, excluding JV’s, NTPC’s current power generation capacity comprises of fifteen coal based

power plants and seven gas / liquid based power plants. The coal based power plants account for about 86 per cent

of the overall capacity. During FY10, the coal based power plants of the company operated at a Plant Load Factor

(PLF) of 90.8 per cent as against the national average of 77.5 per cent.

Other Business activities and Subsidiaries

Power Trading

NTPC Vidyut Vyapar Nigam Ltd. (NVVN), a wholly owned subsidiary was created for trading power leading to

optimal utilization of NTPC’s assets. It is the second largest power trading company in the country. In order to

facilitate power trading in the country, ‘National Power Exchange Ltd.’, a JV between NTPC, NHPC, PFC and

TCS has been formed for operating a Power Exchange.

Coal Mining

The backward integration move to create fuel security, NTPC has ventured into coal mining business. The GoI has

NTPC*

18%

Others

82%

All India Capacity share as on 31st

March 2010 (MW)

NTPC*

28%

Others

72%

All India Generation Share as on 31st

March 2010 (MW)

NTPC LIMITED

www.careratings.com 14

EQUIGRADE

so far allotted 7 coal blocks to NTPC, including 2 blocks to be developed through JV route.

Hydro Power

NTPC has entered into the hydro power business with the 800 MW Koldam hydro project in Himachal Pradesh.

One more project, Tapovan Vishnugad, is been taken up in Uttarakhand for 520 MW. A wholly owned subsidiary,

NTPC Hydro Limited, is also setting up hydro projects of capacities up to 250 MW.

Power Distribution

NTPC Electric Supply Company Ltd (NESCL), a wholly owned subsidiary of NTPC, was set up for distribution of

power. NESCL is actively engaged in ‘Rajiv Gandhi Gramin Vidyutikaran Yojana’ programme for rural

electrification and also working as 'Advisor cum Consultant' for Ministry of Power for implementation of

Restructured Accelerated Power Development and Reforms Programme (RAPDRP) launched by the GOI.

Equipment Manufacturing

NTPC has formed a JV with BHEL and Bharat Forge Ltd. for power plant equipment manufacturing. NTPC has

also acquired stake in Transformers and Electricals Kerela Ltd. (TELK) for manufacturing and repair of

transformers.

Ash Business

NTPC has focused on the utilization of ash generated by its power stations to convert the challenge of ash disposal

into an opportunity. Ash is being used as a raw material input for cement companies and brick manufacturers.

NVVN is engaged in the business of Fly Ash export and sale to domestic customers. JV’s with cement companies

are being planned to set up cement grinding units in the vicinity of NTPC stations.

Key Management Personnel: Functional Directors

Source: Company

Name Designation Education Experience

Shri Arup Roy

Choudhury

Chairman & Managing

Director B.E. (Civil), BIT 32 years

Shri A. K. Singhal Director (Finance) C.A. 29 years

Shri. I.J.Kapoor Director (Commercial) B.E ( Mechanical), MBA

(Marketing) 32 years

Shri B.P. Singh Director(Projects) B.E. (Mining) 36 years

Shri D.K. Jain Director (Technical) B.E (Mechanical) - IIT -

Kharagapur 35 years

Shri S. P. Singh Director (HR) B.E (Electricals) 25 years

Shri N. N. Misra Director (Operations) B.E (Electricals) 33 years

NTPC LIMITED

15 www.careratings.com

EQUIGRADE

Deficit situation in power

India is the world’s sixth largest energy consumer, relying on coal as the primary energy source for over half of its

total energy needs. In FY10, India’s power generating capacities stood at around 159 GW, with close to 64 per cent

accounted by coal based plants. The plant load factor, that measures utilisation of capacities, stood at mere 77.5 per

cent. However, India has been facing deficit scenario, with total energy deficit and peak deficit at approximately

10.1 per cent and 12.7 per cent respectively in FY10. In the scenario of GDP growing at 8 per cent, which

according to CARE Equity Research seems realistic, the energy demand is likely to increase from around 110 Giga

Watts (GW) in FY11E to 160 GW in FY17 and 220 GW in FY22. This translates into a compounded annual

growth rate (CAGR) of more than 6 per cent through the above period. Accordingly, from the current capacity of

around 162 GW, the power generation capacities need to grow to around 230 GW by FY17 and 310 GW by FY22

assuming similar PLF. The timely execution of such huge quantum of expansions would remain a key for the

sector.

Trend in power deficit

Source: NTPC Presentation

A regulated sector with cap on the earnings

The power sector is regulated under the Electricity Act and Central Electricity Regulatory Commission (CERC) is

constituted as the regulator of the industry. CERC approves tariff for every five year plans. The new tariff norms

(2009-14) mandates 15.5 per cent return, with additional incentive of 0.5 per cent on timely completion, with

further income from Unscheduled Interchange (UI), incentive for higher availability and better operating

parameters.

SNAPSHOT OF THE INDUSTRY

13.011.8 12.2 11.2 11.7

12.3

13.816.6

11.912.7

7.8 7.58.8

7.1 7.38.4

9.6 9.8

11.110.1

6

9

12

15

18

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

Peak Deficit (%) Energy Deficit (%)

NTPC LIMITED

www.careratings.com 16

EQUIGRADE

Consolidated Income Statement

(Rs Billion) FY08 FY09 FY10 FY11 P FY12 P FY13 P

Operating Income 416 460 512 591 701 827

EBITDA 144 139 160 171 210 252

Depreciation and amortisation 22 25 29 24 30 40

EBIT 122 114 131 148 180 212

Interest 19 21 21 26 38 53

PBT 104 93 110 122 142 160

Ordinary PAT (After minority interest) 75 81 88 91 105 117

PAT (After minority interest) 75 81 88 91 105 117

Fully Diluted Earnings Per Share* (Rs.) 9.1 9.8 10.7 11.1 12.7 14.1

Dividend, including tax 34 35 37 38 41 43

* Calculated based on ordinary PAT on Current Face Value of Rs. 10/- per share

Consolidated Balance Sheet

(Rs Billion) FY08 FY09 FY10 FY11 P FY12 P FY13 P

Net worth (incl. Minority Interest) 544 601 645 698 762 835

Debt 303 388 441 594 781 979

Deferred Liabilities / (Assets) 3 -9 -1 0 0 0

Capital Employed 849 980 1,086 1,292 1,543 1,814

Net Fixed Assets, incl. Capital WIP 538 659 765 949 1,167 1,391

Investments 134 117 118 128 138 148

Loans and Advances 41 70 57 66 78 92

Inventory 28 34 35 40 48 57

Receivables 32 38 71 78 88 100

Cash and Cash Equivalents 154 173 161 167 185 217

Current Assets, Loans and Advances 263 325 332 361 411 479

Less: Current Liabilities and Provisions 86 120 129 146 173 204

Total Assets 849 980 1,086 1,292 1,543 1,814

FINANCIAL STATISTICS

NTPC LIMITED

17 www.careratings.com

EQUIGRADE

Ratios based on Consolidated Financials

FY08 FY09 FY10 FY11 P FY12 P FY13 P

Growth in Operating Income 13.6% 10.6% 11.2% 15.3% 18.7% 17.9%

Growth in EBITDA 11.3% -3.4% 15.1% 6.9% 22.8% 19.9%

Growth in PAT 8.3% 8.3% 9.2% 3.3% 15.1% 10.9%

Growth in EPS 8.2% 8.3% 9.3% 3.3% 15.1% 10.9%

EBITDA Margin 34.6% 30.2% 31.3% 29.0% 30.0% 30.5%

PAT Margin 17.9% 17.6% 17.3% 15.5% 15.0% 14.1%

RoCE 15.1% 12.5% 12.7% 12.4% 12.7% 12.7%

RoE 14.4% 14.1% 14.2% 13.6% 14.4% 14.6%

Net Debt-Equity (times) 0.3 0.4 0.4 0.6 0.8 0.9

Interest Coverage (times) 7.8 6.6 7.7 6.6 5.6 4.8

Current Ratio (times) 3.1 2.7 2.6 2.5 2.4 2.3

Inventory Days 24 27 25 25 25 25

Receivable Days 28 30 50 48 46 44

Price / Earnings (P/E) Ratio 17.1 16.5 14.4 12.9

Price / Book Value(P/BV) Ratio

2.3 2.2 2.0 1.8

Enterprise Value (EV)/EBITDA 11.2 10.4 8.5 7.1

Source: Company, CARE Equity Research

NTPC LIMITED

www.careratings.com 18

EQUIGRADE

CARE Equigrade Grid (CEG)

Through CEG, CARE Equity Research addresses two critical factors considered by an investor while investing in a

particular company’s equity shares:

1. Fundamentals: Whether the company is fundamentally sound with respect to its business, its financial position, its

management and its prospects.

2. Valuation: What is the Current Intrinsic Value (CIV) of the stock and how it compares vis-a-vis its Current

Market Price (CMP)

These factors are answered assigning quantitative grades to both these parameters. CEG is the snapshot of

‘Fundamental Grade’ and ‘Valuation Grade’ assigned by CARE Equity Research.

Fundamental Grade

This grade represents how sound the company is fundamentally, vis-à-vis other listed companies in India. This grade

captures:

1. Business Fundamentals and Prospects

2. Financial Soundness

3. Management Quality

4. Corporate Governance Practices

The grade is assigned on a five-point scale as under:

CARE Fundamental Grade Evaluation

5/5 Strong Fundamentals

4/5 Very Good Fundamentals

3/5 Good Fundamentals

2/5 Modest Fundamentals

1/5 Weak Fundamentals

Valuation Grade

This grade represents the potential value in the company’s equity share for the investor over a 1 year period. The

Current Intrinsic Value (CIV) or the price arrived by CARE Equity Research on fundamental basis is compared with

the current market price (CMP) of the stock and the grade is assigned based on the gap between CIV and CMP of the

stock.

EXPLANATION OF GRADES

NTPC LIMITED

19 www.careratings.com

EQUIGRADE

The grade is assigned on a five-point scale as under:

CARE Valuation Grade Evaluation

5/5 Considerable Upside Potential

(>25% from CMP)

4/5 Moderate Upside Potential

(10-25% from CMP)

3/5 Fairly Priced

(+/- 10% from CMP)

2/5 Moderate Downside Potential

(Negative 10-25 from CMP)

1/5 Considerable Downside Potential

(<25% from CMP)

Grading determination is a matter of experienced and holistic judgment, based on relevant quantitative and qualitative factors of

the company in relation to other listed companies.

DISCLOSURES

Each member of the team involved in the preparation of this grading report, hereby affirms that there exists no conflict of

interest that can bias the grading recommendation of the company.

This report has been sponsored by the company.

DISLCLAIMER

This report is prepared by CARE Research, a division of Credit Analysis & REsearch Limited [CARE]. CARE Research has taken

utmost care to ensure accuracy and objectivity while developing this report based on information available in public domain or from

sources considered reliable. However, neither the accuracy nor completeness of information contained in this report is guaranteed.

CARE Research operates independently of ratings division and this report does not contain any confidential information obtained by

ratings division, which they may have obtained in the regular course of operations. Opinions expressed herein are our current

opinions as on the date of this report.

CARE’s valaution of the security is mainly based on company specific fundamental factors. Equity prices are affected by both

fundamental factors as well as market factors such as – liquidity, sentiment, broad market direction etc. The impact of market factors

can distort the price of the security thereby deviating from the intrinsic value for extended period of time. This report should not be

construed as recommendation to buy, sell or hold a security or any advice or any solicitation, whatsoever. It is also not a comment on

the suitability of the investment to the reader. The subscriber / user assumes the entire risk of any use made of this report or data

herein. CARE specifically states that it or any of its divisions or employees have no financial liabilities whatsoever to the subscribers /

users of this report. This report is for personal information only of the authorised recipient in India only. This report or part of it

should not be reproduced or redistributed or communicated directly or indirectly in any form to any other person, especially outside

India or published or copied for any purpose.

Published by Credit Analysis & REsearch Ltd., 4th Floor Godrej Coliseum, Off Eastern Express Highway, Somaiya

Hospital Road, Sion East, Mumbai – 400 022.

CARE Research is not responsible for any errors or omissions in analysis/inferences/views or for results obtained from the use of

information contained in this report and especially states that CARE (including all divisions) has no financial liability whatsoever to

the user of this product. This report is for the information of the intended recipients only and no part of this report may be published

or reproduced in any form or manner without prior written permission of CARE Research.

NTPC LIMITED

www.careratings.com 20

EQUIGRADE

Credit Analysis & REsearch Ltd. (CARE) is a full service rating company that offers a wide range of rating and grading services

across sectors. CARE has an unparallel depth of expertise. CARE Ratings methodologies are in line with the best international

practices.

CARE Research

CARE Research is an independent research division of CARE Ratings, a full service rating company. CARE Research is

involved in preparing detailed industry research reports with 5 year demand and 2 year profitability outlook on the industry

besides providing comprehensive trend analysis and the current state of the industry. CARE Research also offers research that

is customised to client requirements. CARE Research currently offers reports on more than 21 industries that include Cement,

Steel, Aluminium, Construction, Shipping, Ship-building, Commercial Vehicles, Two-Wheelers, Tyres, Auto Components,

Pipes, Natural Gas, Retail, Sugar, etc. CARE Research now offers independent research of equities through its product

‘EQUIGRADE’.

CREDIT ANALYSIS & RESEARCH LTD

HEAD OFFICE |Mr. P. N. Satheeskumar | Cell: +91-9820416004 | Tel: +91-22-6754 3555 | E-mail:

4th Floor, Godrej Coliseum, Somaiya Hospital Road, Off Eastern Express Highway, Sion (East), Mumbai - 400 022 |

Tel: +91-022- 6754 3456 | E-mail: [email protected] | Fax: +91-022- 6754 3457

KOLKATA | Mr. Sukanta Nag | Cell: +91-98311 70075 | Tel: +91-33- 2283 1800/ 1803, 2280 8472 |

E- mail: [email protected] | 3rd Flr., Prasad Chambers (Shagun Mall Bldg), 10A, Shakespeare Sarani, Kolkata -700 071

CHENNAI | Mr. V Pradeep Kumar | Cell: +91 9840754521 | Tel: +91-44-2849 7812/2849 0811 | Fax: +91-44-2849 0876 |

Email: [email protected] | Unit No. O-509/C, Spencer Plaza, 5th Floor, No. 769, Anna Salai, Chennai - 600 002

AHMEDABAD | Mr. Mehul Pandya | Cell: +91-98242 56265 | Tel: +91-79-40265656 | Fax: +91-79-40265657 |

E-mail:[email protected] | 32, Titanium, Prahaladnagar Corporate Road, Satellite, Ahmedabad - 380 015.

NEW DELHI | Ms. Swati Agrawal | Cell: +91-98117 45677 | Tel: +91- 11- 2331 8701/ 2371 6199 |

E-mail: [email protected] | 710 Surya Kiran,19 K.G. Road, New Delhi - 110 001.

BANGALORE | Mr. G. Sundara Vathanan | Cell: +91 98860 24430 | Tel:+91-80-2211 7140 |

E-mail: [email protected] | Unit No. 8, I floor, Commander's Place, No. 6, Raja Ram Mohan Roy Road,

(Opp. P F Office), Richmond Circle, Bangalore - 560 025.

HYDERABAD | Mr. Ashwini Kumar Jani | Cell: +91-91766 47599 | Tel: +91-40-40102030 |

E-mail: [email protected] | 401, Ashoka Scintilla | 3-6-520, Himayat Nagar | Hyderabad - 500 029

ABOUT CARE