Embed Size (px)

DESCRIPTION

Fund News issue 107 provides you with regulatory updates from Belgium, Ireland, Switzerland and UK.

Citation preview

FUND NEWS

Financial Services / Regulatory and Tax / Issue 107

Developments in September 2013 Investment Fund Regulatoryand Tax developments in selected jurisdictions

2 / Fund News / Issue 107 / Developments in September 2013

Regulatory Content

European Union 3 Proposed EU Regulation on Money Market Funds 4 AIFM reporting guidelines published 4 Shadow Banking Communication 5 EMIR indicative timeline 5 Proposed Regulation on financial benchmarks

Ireland 6 CBI Publishes Prospectus Handbook 6 CBI Consultation Paper on Investment

Intermediaries 6 AIMA submission on CBI’s Loan Origination DP 6 CBI Feedback on Fitness & Probity 6 Key Dates Reminder

Switzerland 7 FINMA Circular 2013/9 “Distribution of collective

investment schemes” enters into force

UK 8 FCA’s proposals for implementing AIFMD

Remuneration Code 11 FCA consults on minor changes to the platform

rules and proposes guidance on when cash rebates may continue for legacy business

12 FCA makes amendments to COLL reflecting the formal adoption of ESMA guidelines (ESMA 2012/832)

12 FCA defers the implementation date for the provision of fund information to investors who hold units in funds via nominees

Contents

Tax Content

The Netherlands 13 Dutch REITs: ancillary activities allowed

Fund News / Issue 107 / Developments in September 2013 / 3

Regulatory News

European Union

Eligible assets

The proposed regulation narrows the list of eligible assets of MMFs to:

• money market instruments

• deposits with credit institutions

• financial derivative instruments for hedging interest rate and currency risk

• reverse repurchase agreements

No (in)direct exposure to equities or commodities is permitted and investments in Asset Backed Commercial Paper (ABCP) would be strictly limited to those whose underlying assets are short-term debt issued by corporate entities.

Operations such as entering into securities lending/borrowing agreements, repurchase agreements, short selling and borrowing/lending cash would be prohibited.

Risk Management

The proposal provides a clear framework for risk management of MMF. It defines diversification and concentration restrictions, requires internal assessment procedures including an internal rating system, requires a KYC policy to understand potential redemption flows and clearly defines stress testing for MMFs.

Proposed EU Regulation on Money Market Funds

The European Commission issued a proposal on 4 September 2013 for a Regulation on Money Market Funds (MMF). The proposed regulation is a “Product” regulation that takes certain principles in existing CESR/ESMA guidelines and makes them into law.

The proposal defines a MMF as a “Collective investment undertaking that requires authorisation as UCITS under Directive 2009/65/EC or is an AIF under Directive 2011/61/EU, invests in short term assets and has as distinct or cumulative objectives offering returns in line with money market rates or preserving the value of the investment.”

The proposal will impact MMFs set up as UCITS, and those that qualify as AIFs, and would apply in addition to the existing UCITS and AIFMD frameworks. Furthermore, the proposed regulation would apply to MMFs established, managed or marketed in the Union.

The proposal introduces an authorisation procedure for all MMFs. It relies on the existing authorisation procedures for UCITS and introduces a new harmonised authorisation procedure for AIFs which mirrors the UCITS rules.

The proposed regulation lays down rules concerning the financial instruments eligible for investment by a MMF, its portfolio and valuation, and reporting requirements.

Fund Valuation

The proposed regulation authorises two types of valuations for units and shares of MMFs, either a floating NAV per share valuation or a constant NAV (“CNAV”) per share valuation.

Both types must fully comply with the regulation but CNAV MMFs will have to comply with the following additional requirements:

• A NAV Buffer representing at least 3% of the fund’s assets must be set aside by the Sponsor/Manager and serve as an absorbing mechanism for maintaining the CNAV;

• Procedures must be in place to verify the difference between CNAV/share and NAV/share on a daily basis and negative differences above 15bps must be escalated to the authorities;

• The CNAV MMF must have the possibility to turn into a variable NAV MMF at all times.

Portfolio valuation

The regulation distinguishes three possible valuation methods for the assets of an MMF: mark-to-market, mark-to-model and the amortised cost method.

Mark-to-market valuation method would have to be used for the valuation of an MMF’s assets whenever possible. Where mark-to-market would not be possible or market data would not be of sufficient quality, an asset of a MMF shall be valued conservatively by using mark-to-model. Mark-to-model is defined as any valuation

4 / Fund News / Issue 107 / Developments in September 2013

which has to be benchmarked, extrapolated or otherwise calculated from one or more market input.

The proposed regulation strictly restricts the use of the amortised cost accounting to CNAV MMFs for the purpose of the constant NAV calculation.

Reporting:

The proposed regulation would require a very detailed reporting on the fund’s portfolio to be made to the competent authorities at least on a quarterly basis.

According to the European Commission, the new MMF rules are likely to be agreed in the course of 2014. It should be noted that the Commission’s proposal is only a draft and will have to be approved by the EU Council and the European Parliament.

The Regulation contains Delegated Acts (meaning that additional detailed rules will be issued on certain aspects e.g. internal credit rating system requirements and reporting requirements).

The Regulation will be reviewed after 3 years.

The full text can be found via the following link:

http://ec.europa.eu/internal_market/investment/money-market-funds/index_en.htm

AIFM reporting guidelines published

On 1 October 2013 the European Securities and Markets Authority (ESMA) published the final guidelines on the reporting obligations for alternative investment fund managers (AIFMs). These guidelines provide clarification on the information that AIFMs should report to the authorities as well as indications as to the timing of reporting. ESMA also published some technical supporting material (a consolidated reporting template, detailed IT guidance for filing of the XML and the XSD schema) that will facilitate the reporting by AIFMs to regulators.

In addition to the guidelines ESMA published an Opinion providing details on a set of supplementary information that, in its view, the national authorities should require of AIFMs for the monitoring of systemic risk. This includes information on the number of transactions and their values carried out using high frequency algorithmic trading and information on the VaR of the AIFs.

The relevant ESMA documents are available at the following link:

http://www.esma.europa.eu/page/Investment-management-0

European Commission Shadow Banking Communication

Following the release of a Green Paper in March 2012 (see Fund News Issue 90), the European Commission on 4 September 2013 published a Communication on Shadow Banking describing the issues at stake in relation to the shadow banking system. The Communication describes the key measures already taken to deal with the risks related to shadow banking and also sets out a roadmap for the future. This roadmap includes increasing transparency of the shadow banking sector, improving the framework for certain investment funds, reducing the risks associated with securities financing transactions, strengthening the prudential banking framework in order to limit contagion and arbitrage risks, and establishing more effective supervision of the shadow baking sector.

The first measure taken under the roadmap is a Proposal for a Regulation on Money Market Funds (see our article on page 1). Other initiatives will focus on improving data collection and exchange, developing central repositories for derivatives with the EMIR framework, implementing the Legal Entity Identifier (LEI) project, the establishment of a central data repository for repurchase transactions, strengthening the UCITS framework and requiring banks to report on exposures to unregulated entities.

The full text of the Communication is available via the following web link:

http://eur-lex.europa.eu/LexUriServ/ LexUriServ.do?uri=CELEX:52013 DC0614:EN:NOT

Regulatory News

Fund News / Issue 107 / Developments in September 2013 / 5

EMIR indicative timeline – ESMA update

ESMA has published an updated version of its EMIR implementation timetable. Key changes in the implementation timeline relate to the registration of the first Trade Repositories which is expected not before 7 November 2013. Consequently, the transaction reporting to trade repositories has been delayed and will not start before 12 February 2014.

The revised timeline is available via the following web link:

http://www.esma.europa.eu/news/Trade-Repository-registration-approval-not-expected-7-November-reporting-begin-February-2014

Proposed EU Regulation on financial benchmarks

The European Commission issued a proposal on 19 September 2013 for a Regulation on financial benchmarks strengthening the rules of those used in financial instruments and financial contracts in the EU.

The main objective of this proposal is to improve benchmark’s market integrity and fairness in order to restore confidence in financial markets and ensure the protection of consumers and investors.

The proposal targets all published indices used to reference the price of a financial instrument or contract, or measure the performance of an investment fund.

Regulatory News

The scope of this proposal covers the activities performed by benchmark administrators producing these benchmarks. The proposal defines a benchmark administrator as any natural or legal person that has control over the provision of a financial benchmark.

Under the proposed new arrangements:

• National competent authorities would supervise administrators of benchmarks under the coordination of ESMA. In the scenario of a benchmark having a systemic impact on the financial stability, or the orderly functioning of markets, or consumers, or the real economy of one or more Member States (“critical benchmark”), the supervision would be carried out by a college of national supervisors.

• Benchmark calculators and contributors would be required to ensure robust governance with adequate management systems and effective controls, in particular to prevent conflicts of interest when possible. The disclosure of existing conflicts of interest would be mandatory.

• The proposal requires full transparency on benchmark methodology, underlying data, process and purpose. Such data and information would have to be publicly available in order to allow investors or regulators to replicate the benchmark. Delayed or partial transparency of underlying data would be allowed when justified.

• The proposal requires the use of transaction data if available and reliable, otherwise well founded and verifiable discretion should be used. For critical benchmarks lacking of data, regulators would have the power to mandate contributions to ensure the continuity of such benchmarks.

• Regulated entities entering into any financial contracts (e.g. loan, mortgage), where the payments are referenced by a benchmark, would have to assess the suitability of the benchmark, and would have to warn the client if the benchmark is unsuitable.

According to the European Commission, the new financial benchmark rules are likely to be agreed in the course of 2015. It should be noted that the Commission’s proposal is only a draft and will have to be approved by the EU Council and the European Parliament.

The Regulation will be reviewed three years after the entry into force of the legislative measure.

The full text can be found via the following link:

http://ec.europa.eu/internal_market/securities/benchmarks/index_en.htm

6 / Fund News / Issue 107 / Developments in September 2013

CBI Publishes Prospectus Handbook

The Central Bank has published a Prospectus Handbook (A Guide to Prospectus Approvals in Ireland). The handbook addresses prospectus review, approval and publication and provides an overview of the structure and content of prospectuses and is available via the following link:

http://www.centralbank.ie/regulation/securities-markets/prospectus/pages/new-prospectushandbook.aspx

CBI Consultation Paper on Investment Intermediaries

The Central Bank has issued Consultation Paper CP72 reviewing the Handbook of Prudential Requirements for Authorised Advisors and Intermediaries, which are investment intermediaries under the Investment Intermediaries Act 1995.

The Central Bank is proposing to significantly change the supervision of firms designated as “low impact” under its PRISM regime and is proposing that:

• Intermediary types be reclassified into a single grouping of “Investment Product Intermediaries” (“IPI”);

• IPIs must be able to demonstrate solvency with positive net assets at all times;

• Minimum regulatory capital requirements will be abolished, although a €50,000 minimum requirement will remain for Product Producers;

• Professional Indemnity Insurance requirements will be harmonised with the requirements of the Insurance Mediation Regulations applicable to insurance brokers.

Comments are invited by 29 November 2013. The Central Bank will issue the feedback document and the revised Handbook in 2014.

AIMA submission on CBI’s Loan Origination Discussion Paper

We previously reported on the Central Bank’s discussion paper on loan origination in Issue 105.

The Alternative Investment Management Association (“AIMA”) have submitted a response to the Central Bank’s discussion paper stating its view that the risks associated with loan origination by investment funds should be able to be adequately monitored and mitigated by the regulatory framework of AIFMD and that further regulatory measures should not be necessary. The full response can be obtained from AIMA.

CBI Feedback on Fitness & Probity

The report gives details of the Central Bank’s performance against the service standards for the processing of Individual Questionnaires for PCFs from January to June.

Key Dates Reminder

30 September 2013: Deadline for filing Section 891(c) returns to the Revenue Commissioners for the year 2012. (See Issue 106 regarding the Return of Values (Investment Undertakings) Regulations, 2013 SI 245/2013.)

11 October 2013: Deadline for responses to the Central Bank’s consultation on types of AIF under AIFMD including Unit Trusts, Exempt Unit Trusts, REITs, SPVs (CP68).

28 October 2013: Deadline for responses to the Central Bank’s consultation on the authorisation of regulated firms, funds and intermediaries, process improvements and service standards (CP67).

31 October 2013: Deadline for responses to the Central Bank’s consultation on client assets requirements (CP71).

Regulatory News

Ireland

Fund News / Issue 107 / Developments in September 2013 / 7

FINMA Circular 2013/9 “Distribution of collective investment schemes” enters into force

The Swiss Financial Market Supervisory Authority (FINMA) has fully revised its Circular “Public advertising – collective investment schemes”. The main aim of this revision is to provide a detailed definition of the term “distribution of collective investment schemes”. The Circular has thus been adapted to match the terms of the revised Collective Investment Schemes Act and Collective

Switzerland

Regulatory News

Investment Schemes Ordinance, which became law on 1 March 2013. It enters into force on 1 October 2013 and completely replaces the existing Circular (FINMA-Circ. 2008/8).

KPMG has published an unofficial English translation of the circular which is available via the following link:

http://www.kpmg.com/CH/en/Library/Legislative-Texts/Pages/finma-circular-2013-09-collective-investment-schemes.aspx

8 / Fund News / Issue 107 / Developments in September 2013

FCA’s proposals for implementing the AIFMD’s Remuneration Code

On 6 September the Financial Conduct Authority (“FCA”) published its quarterly consultation paper (“CP 13/9”) which includes, in Chapter 14, its proposals and draft guidance setting out how it intends to amend the FCA’s AIFM Remuneration Code (SYSC 19B) to implement key elements of the European Securities and Markets Authority (“ESMA”) final guidelines on AIFM remuneration. In particular, the FCA sets out proposals for the proportionality regime they might adopt. This could enable certain fund managers to disapply some of the more onerous requirements (e.g. deferral, risk adjustment and the payment in instruments of variable remuneration).

The AIFM Remuneration Code is applicable to “AIFM Remuneration Code Staff” (“Code Staff”) whose activities have a material impact on the risk profile of the AIFM or the AIFs it manages, and to certain delegate entity staff. It will apply to the first full performance period following the AIFM’s authorisation. The consultation period ends on 6 November 2013. The FCA intends to issue final remuneration guidance in early 2014.

Proportionality regime for AIFMs

An AIFM may elect to disapply the deferral, performance adjustment, payment in instruments and post-vesting retention of instruments provisions applicable to variable remuneration (defined in the FCA guidance as the “Pay-out Process Rules” ) following a proportionality assessment by the AIFM.

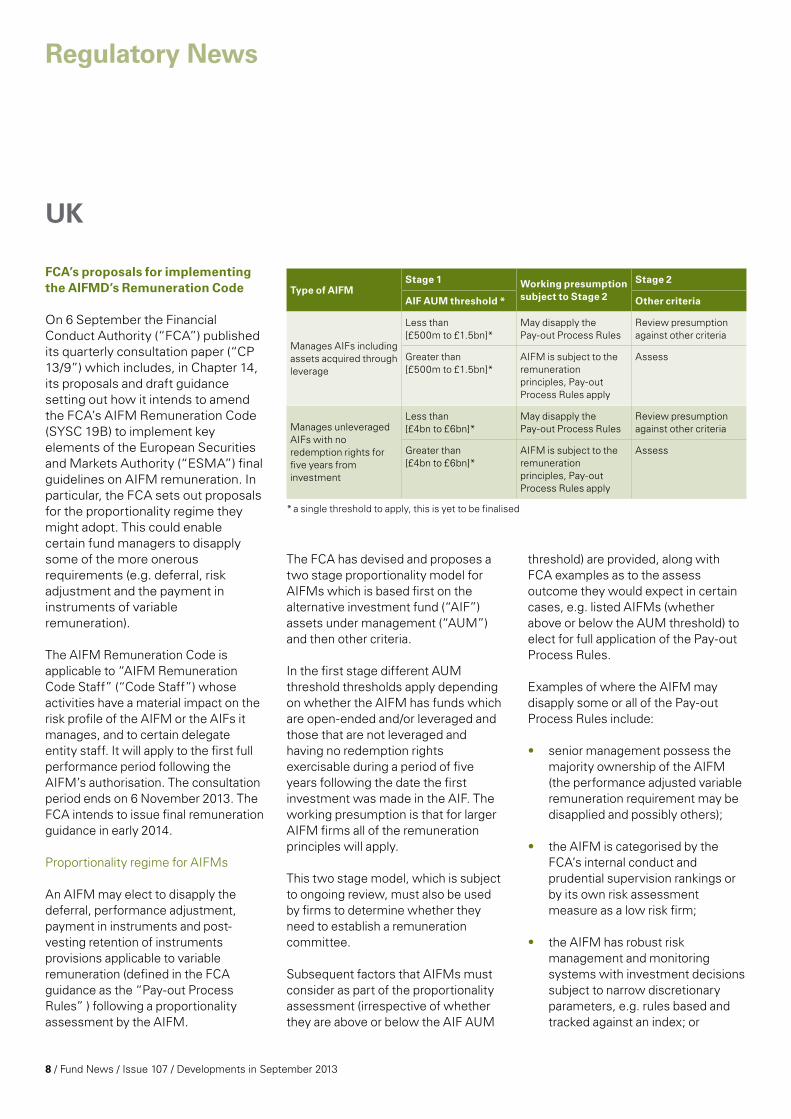

The FCA has devised and proposes a two stage proportionality model for AIFMs which is based first on the alternative investment fund (“AIF”) assets under management (“AUM”) and then other criteria.

In the first stage different AUM threshold thresholds apply depending on whether the AIFM has funds which are open-ended and/or leveraged and those that are not leveraged and having no redemption rights exercisable during a period of five years following the date the first investment was made in the AIF. The working presumption is that for larger AIFM firms all of the remuneration principles will apply.

This two stage model, which is subject to ongoing review, must also be used by firms to determine whether they need to establish a remuneration committee.

Subsequent factors that AIFMs must consider as part of the proportionality assessment (irrespective of whether they are above or below the AIF AUM

threshold) are provided, along with FCA examples as to the assess outcome they would expect in certain cases, e.g. listed AIFMs (whether above or below the AUM threshold) to elect for full application of the Pay-out Process Rules.

Examples of where the AIFM may disapply some or all of the Pay-out Process Rules include:

• senior management possess the majority ownership of the AIFM (the performance adjusted variable remuneration requirement may be disapplied and possibly others);

• the AIFM is categorised by the FCA’s internal conduct and prudential supervision rankings or by its own risk assessment measure as a low risk firm;

• the AIFM has robust risk management and monitoring systems with investment decisions subject to narrow discretionary parameters, e.g. rules based and tracked against an index; or

UK

Regulatory News

Type of AIFMStage 1 Working presumption

subject to Stage 2

Stage 2

AIF AUM threshold * Other criteria

Manages AIFs including assets acquired through leverage

Less than [£500m to £1.5bn]*

May disapply the Pay-out Process Rules

Review presumption against other criteria

Greater than [£500m to £1.5bn]*

AIFM is subject to the remuneration principles, Pay-out Process Rules apply

Assess

Manages unleveraged AIFs with no redemption rights for five years from investment

Less than [£4bn to £6bn]*

May disapply the Pay-out Process Rules

Review presumption against other criteria

Greater than [£4bn to £6bn]*

AIFM is subject to the remuneration principles, Pay-out Process Rules apply

Assess

* a single threshold to apply, this is yet to be finalised

Fund News / Issue 107 / Developments in September 2013 / 9

• fee structures are in place (e.g. carried interest) which align the Code Staff interests with investors and discourage inappropriate risk-taking by being paid out towards the end of the fund life-cycle and having been negotiated with prospective investors in advance.

Whilst the application of proportionality is based on a self-assessment process, the FCA has the authority to provide an AIFM with individual guidance as to how they should take proportionality into account.

AIFM Remuneration Code Staff

De minimis principle

Code Staff with total remuneration of no more than £500,000 and with variable remuneration no more than 33% of their total remuneration, can disapply the following provisions:

• guaranteed variable remuneration;

• payment in instruments;

• deferral; and

• performance adjustment.

Implementing the delegation provision

The final ESMA guidelines extend the reach of the remuneration provisions to delegates of AIFMs performing risk or portfolio management services if they are not already subject to provisions “equally as effective” as the AIFMD remuneration provisions.

The FCA have confirmed that if the delegate entity is subject to the Capital Requirements Directive (“CRD”)

Regulatory News

remuneration rules, they will be deemed to be “equally as effective” and the AIFMD remuneration provisions need not apply. However, if the delegate entity is not already subject to the CRD requirements or provisions which are deemed by the regulator to be “equally as effective” then the AIFM would need to put in place contractual arrangements with the delegate entity.

Overlapping remuneration regulation

Given AIFMs are permitted to perform non-AIFMD business (e.g. manage UCITS funds and carry out limited MiFID business activities), the FCA have stated that the Pay-out Process Rules may be disapplied in respect of Code Staff who only perform non-AIFMD business.

For Code Staff who perform non-AIFMD business in addition to AIFMD activities, the AIFM will need to apportion their remuneration appropriately according to that which falls under the AIFMD, UCITS Directive or MiFID. The guidance states: “A firm may apportion an individual’s remuneration based on time, funds under management or another benchmark taking into account any risks created in each case”.

Key developments for Partners or members of an LLP

Bifurcation process

If the AIFM has individual partners or members of an LLP and their activities have an impact on the risk profile of the AIFM or AIFs it manages (i.e. they are

10 / Fund News / Issue 107 / Developments in September 2013

Code Staff or working for a delegate entity and caught by the delegation provision) any payments they receive in exchange for professional services provided to the AIFM will be within the scope of the AIFM Remuneration Code.

Payments in the form of a profit allocation will need to be bifurcated into the portion considered to be the return on equity in the firm and the portion that is payment for their services to the AIFM. With regard to the latter portion, a second bifurcation process will need to be employed to divide the amount into fixed and variable components. Firms must ensure that the fixed and variable amounts are “appropriately balanced”.

The FCA have suggested that for founding or senior partners in an existing firm any amount of “additional profit share” may be considered to be their out-of-scope equity return with any “discretionary profit share distributed to all partners” forming the portion deemed to be variable remuneration under the AIFM Code. Likewise, any drawing made in advance of the profit allocation is fixed remuneration for the purposes of the Code. Subject to ESMA’s anti-circumvention rule, this recommendation is seemingly more generous than might have been expected.

Alternatively a benchmarking approach is suggested, with the FCA proposing two appropriate methodologies:

i. Benchmarking the remuneration structures of partners performing similar tasks or working in similar businesses.

ii. Benchmarking the equity or capital return for a partner who has invested in the AIFM against a similar investment context.

The guidance indicates that for partners working part-time in an executive position, a larger portion of their profit share should be considered to be an out-of-scope equity return whilst for full time partners the FCA “will expect a reasonable portion of the partner’s profit share to be considered as remuneration under the AIFMD” .

Tax implications

Under the current UK partnership taxation rules, deferral of up to 60% of variable remuneration may lead to a partner having to make a tax payment without any corresponding income to fund the tax payment (i.e. a dry tax charge).

With this in mind the FCA have stated that deferral of variable remuneration for partners may take place on a net-of-tax (i.e. income tax and national insurance) basis under a new statutory mechanism being developed by HMRC.

This would make the partnership (as opposed to its individual partners) liable for the tax due on the deferred sums. The guidance appears to suggest that partnerships may have discretion as to whether they elect to use this proposed net-of-tax statutory mechanism.

We expect further guidance on this mechanism to be issued by HMRC alongside their draft partnership tax legislation in the Finance Bill 2014, which will be issued shortly after the Chancellor’s 2013 Autumn Statement.

Other developments

Timing

The AIFM Remuneration Code must be applied by AIFMs to the first full performance period following authorisation. The Code will not apply to any remuneration payments derived from awards made for performance periods prior to the firm’s AIFM authorisation date, nor to any existing non-vested awards at the date of authorisation.

The AIFM Directive (including Annex II containing the remuneration provisions) took effect on 22 July 2013. Existing firms have a 12 month transition period to 22 July 2014 in which to obtain authorisation, however, the FCA’s advice, issued last month, strongly recommended that firms which intend to apply for AIFM authorisation or a variation of their current permission should file their application by 22 January 2014. The management body should review and adopt any revised remuneration policy in advance of filing such an authorisation application.

Deferral

For Code Staff with variable remuneration of £500,000 or more (a “particularly high amount”) at least 60% of their variable remuneration must be deferred.

Payment in instruments

The final ESMA guidelines stipulate that 50% of any variable remuneration should to be paid in units or shares of the AIF that the individual mainly provides services to, or in equivalent ownership interests or share linked

Regulatory News

Fund News / Issue 107 / Developments in September 2013 / 11

instruments or equivalent non-cash instruments.

This FCA guidance states that this requirement might be disapplied if:

• the AIF is closed-ended and there are no units available to acquire;

• the AIF’s incorporation instrument precludes investments by Code Staff or prescribes a large threshold investment amount that could not be met by staff investments;

• the AIF is subject in its jurisdiction to laws or regulations which prevent the Code Staff receiving units in the AIF;

• an investment by Code Staff would result in adverse tax consequences for any third party AIF investors; or

• the creation of equivalent ownership interests is unduly costly when weighed against the benefits of aligning the Code Staff’s interests to that of investors.

However, the FCA recommend that if this rule is disapplied (for the reasons listed above or under the proportionality principle) firms can still elect to pay Code Staff in shares or instruments linked to the AIFM or its parent company, or in shares or instruments linked to a weighted performance average of the AIFs managed by the AIFM.

Retention policy

A post-vesting retention period of six months for units, shares or other instruments forming part of a variable remuneration award could be

Regulatory News

sufficient, with longer retention periods appropriate in certain circumstances.

The rule on retention may be applied on a “net-of-tax” basis. However it is not possible to sell shares or units to meet a tax liability when the deferred award vests.

Next steps for firms

Having considered the new proportionality model, firms will need to review their compliance plans for operating under the new regime and ensure they have re-assessed their current AIFM Code Staff population in light of the de minimis principle; and developed appropriate structures to deliver remuneration for Code Staff in the appropriate form.

An AIFM structured as a partnership or an LLP will need to wait for the further guidance from HMRC before finalising the deferral mechanisms to be used for the partners.

Chapter 14 of FCA’s CP 13/9 (361 pages) is available via this link:

http://www.fca.org.uk/your-fca/documents/consultation-papers/cp13-09

FCA consults on minor changes to the platform rules and proposes guidance on when cash rebates may continue for legacy business

In chapter 3 of its CP 13/9 the FCA consults on the implementation of new rules which will come into force on 6 April 2014 regarding cash rebates on legacy business where the investment

12 / Fund News / Issue 107 / Developments in September 2013

Regulatory News

FCA defers the implementation date for the provision of fund information to investors who hold units in funds via nominees

In CP 10/29 the then FSA proposed rules requiring nominee companies to provide fund information and voting rights to the underlying beneficial owners of units in authorised funds. These rules were to come into effect on 31 December 2012 but after discussion with the industry on a number of issues implementation was deferred to 31 December 2013.

The FCA has now decided to place the majority of the implementation on hold until 2015. It was recognised that some investors invested via nominees to receive less information and that an opt-in or opt-out may be a better way to proceed but care was needed if the option wording was not to risk biasing the outcome.

In addition European Commission securities law legislation may have an impact and the FCA was therefore concerned not to make rules that may have to be amended shortly after implementation. In the meantime the FCA will conduct further research on the information needs and expectations of investors in funds, both direct and via nominees.

Rules enabling the authorised fund manager to obtain reasonable information on beneficial owners within nominee accounts for fund liquidity management will come into force on 31 December 2013. Chapter 13 (pages 47 to 49) of FCA’s CP 13/9 (361 pages) is available via this link:

http://www.fca.org.uk/your-fca/docu-ments/consultation-papers/cp13-09

products are already held by retail clients when the new rules come into force.

The reference to “customer” is to be amended in rule COBS 6.1E.1R to “retail client”; and reference to “client” on re-registration refers to all clients not just retail clients so the FCA does not propose to amend guidance at COBS 6.1G.

The policy intent in CP12/12 is that rebates can continue on investments already held by a consumer on a platform and which continue to be held after the rules come into force, however, the FCA understands the need for guidance in this area would be helpful and consults on proposed guidance in CP 13/9 chapter 3.

The rules and guidance being consulted on will not apply to execution only off-platform business but will apply to advised off-platform business.

The FCA sets out its proposed guidance; and a table of scenarios where cash payments by providers to retail clients can continue under the proposed guidance. The details are set out in paragraph 3.12 of chapter 3 of CP13/9 (page 15 of 361).

Chapter 3 (pages 13 to 16) of FCA’s CP 13/9 (361 pages) is available via this link:

http://www.fca.org.uk/your-fca/documents/consultation-papers/cp13-09

FCA makes amendments to COLL reflecting the formal adoption of ESMA guidelines (ESMA 2012/832)

Having indicated early in 2013 that it would comply with and adopt ESMA’s “Guidelines on ETFs and other UCITS issues” (“ESMA 2012/832” “the Guidelines”), in Chapter 10 of its quarterly CP 13/9 the FCA consults to ensure its adoption of the Guidelines are considered alongside the existing rules and guidance in the Collective Investment Schemes sourcebook (“COLL”).

The Guidelines are largely adopted by the simple expedient of the FCA providing a link in the relevant sections of COLL to ESMA 2012/832, with the new text for COLL set out in Appendix 10 to CP13/9 (5 pages).

The FCA indicates it may make a more detailed transposition of the Guidelines when COLL is merged into the Investment Funds sourcebook (“FUND”) expected in the last quarter of 2013. In the meantime it considers linking to the Guidelines is sufficient for UCITS managers and the UCITS impacted by the Guidelines issued on 18 December 2012 that were effective from 18 February 2013, albeit with elements subject to a 12 month transition.

Chapter 10 (pages 36 and 37) and Appendix 10 of FCA’s CP 13/9 (361 pages) is available via this link:

http://www.fca.org.uk/your-fca/documents/consultation-papers/cp13-09

Fund News / Issue 107 / Developments in September 2013 / 13

Dutch REITs: ancillary activities allowed

Dutch real estate investment funds commonly have the tax status of fiscal investment institution, implying that a 0% corporate income tax rate is applicable. However, only passive investment is allowed when applying for this status. In the Tax Plan 2014, a relaxation of this passive investment requirement is proposed. As tenants are increasingly expecting lessors of commercial real estate to offer additional services, it has been

The Netherlands

proposed that fiscal investment institutions be given the opportunity − albeit indirectly − to perform ancillary activities for tenants. Such ancillary activities could include, for example, cleaning, catering, reception or meeting services. These activities need to be carried out by a “normal” taxpaying subsidiary of the fiscal investment institution and some additional conditions need to be met. These conditions should ensure that the ancillary activities are subordinate to the passive investment objective and also to avoid tax base erosion.

Publications

FINANCIAL SERVICES

EvolvingInvestment

Management Regulation

Light at the end of the tunnel?

June 2013

kpmg.com

Embedding realculture changeand managingtalent risk

Swiss FinancialServices Newsletter: Special Edition Investment Management

EvolvingInvestmentManagementRegulation

Tax News

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

© 2013 KPMG Holding AG/SA, a Swiss corporation, is a subsidiary of KPMG Europe LLP and a member of the KPMG network of independent firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss legal entity. All rights reserved. Printed in Switzerland. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

Zurich

Markus SchunkPartnerT: +41 58 249 36 82 E: [email protected]

Christoph GroebliPartnerT: +41 58 249 29 76 E: [email protected]

Geneva

Yvan MermodPartnerT: +41 22 704 16 61 E: [email protected]

Lugano

Lars SchlichtingPartner, LegalT: +41 91 912 12 32 E: [email protected]

Astrid KellerPartnerT: +41 58 249 28 82 E: [email protected]

Dominik RüttimannPartnerT: +41 58 249 20 56 E: [email protected]

Pierre ZächPartnerT: +41 22 704 15 30 E: [email protected]

Pascal SprengerDirector, LegalT: +41 58 249 42 23 E: [email protected]

Grégoire WincklerPartner, TaxT: +41 58 249 34 95 E: [email protected]

Jean-Luc EparsPartner, LegalT: +41 22 704 17 59 E: [email protected]

Contacts

kpmg.ch