Embed Size (px)

Citation preview

County of Riverside ■ Office of the Auditor-Controller1

Fund Balance Reporting Requirements(GASB 54 Impact)

Presented to the City Councilby

Lena H. EllisFinancial Management Services Director/ CFO

September 27, 2011

County of Riverside ■ Office of the Auditor-Controller2

Presentation Objective:

Provide briefing on Governmental Accounting Standards Board (GASB) Statement No. 54 requirements and impact;─ M&C G-17398

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller3

Background

Effective For Fiscal Year 2011/2012

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller4

Fund Balance – Current/Future Standard

What is Fund Balance? Difference between assets and liabilities

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller5

Fund Balance – Current StandardHow do we allocate Fund Balance? Reserved Unreserved

─Designated─Undesignated

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller6

Fund Balance – Current Standard

Traditional focus = Fund resources available for appropriation (budgeting)

Reserved Fund Balance = Not available Unreserved Fund Balance = Available

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller7

Fund Balance – Current Standard

Reserved Fund Balance = Not available Legal restrictions impose a limitation on purpose

of the fund Resources not available for spending in the current

year’s budget. . Example: Encumbrances, Advances to other funds

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller8

Fund Balance – Current Standard

Designated Fund Balance – intended use of resources by management or governing body.

Example: Risk Management, Group Health Insurance

Financial Management ServicesGASB 54 Fund Balance Requirements

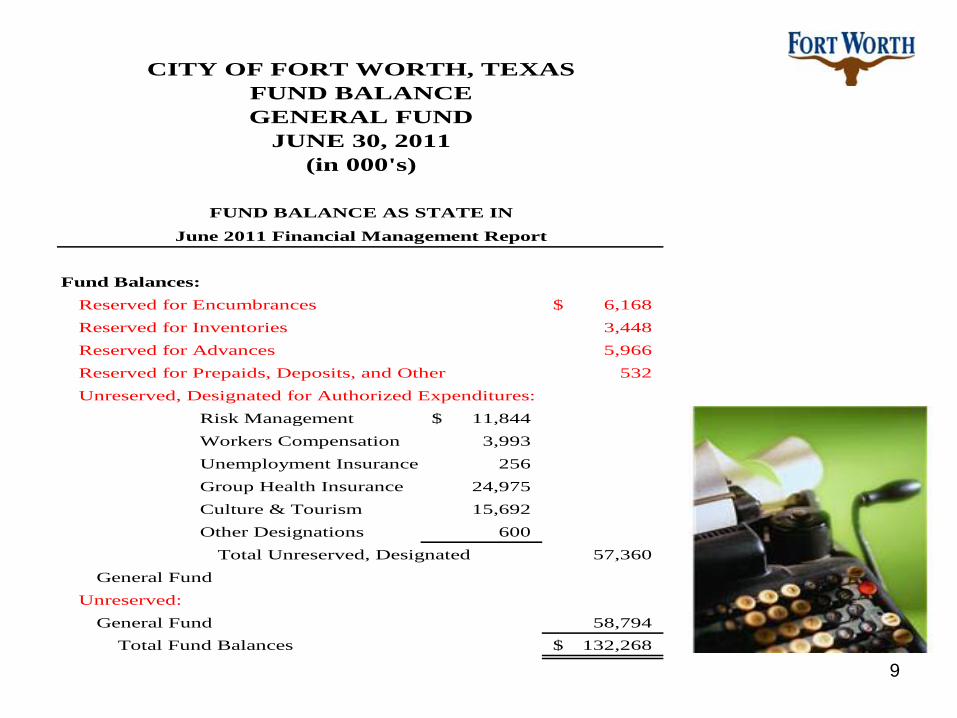

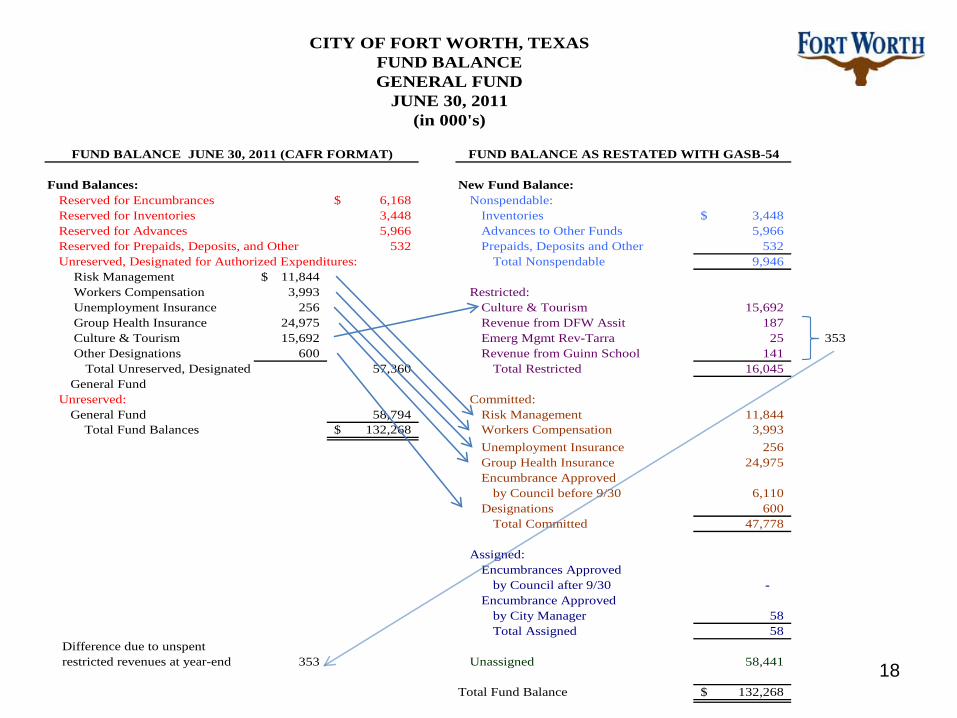

County of Riverside ■ Office of the Auditor-Controller9

Fund Balances:Reserved for Encumbrances 6,168$ Reserved for Inventories 3,448 Reserved for Advances 5,966 Reserved for Prepaids, Deposits, and Other 532 Unreserved, Designated for Authorized Expenditures:

Risk Management 11,844$ Workers Compensation 3,993 Unemployment Insurance 256 Group Health Insurance 24,975 Culture & Tourism 15,692 Other Designations 600

Total Unreserved, Designated 57,360 General Fund

Unreserved:General Fund 58,794 Total Fund Balances 132,268$

June 2011 Financial Management Report

CITY OF FORT WORTH, TEXASFUND BALANCEGENERAL FUND

JUNE 30, 2011(in 000's)

FUND BALANCE AS STATE IN

County of Riverside ■ Office of the Auditor-Controller10

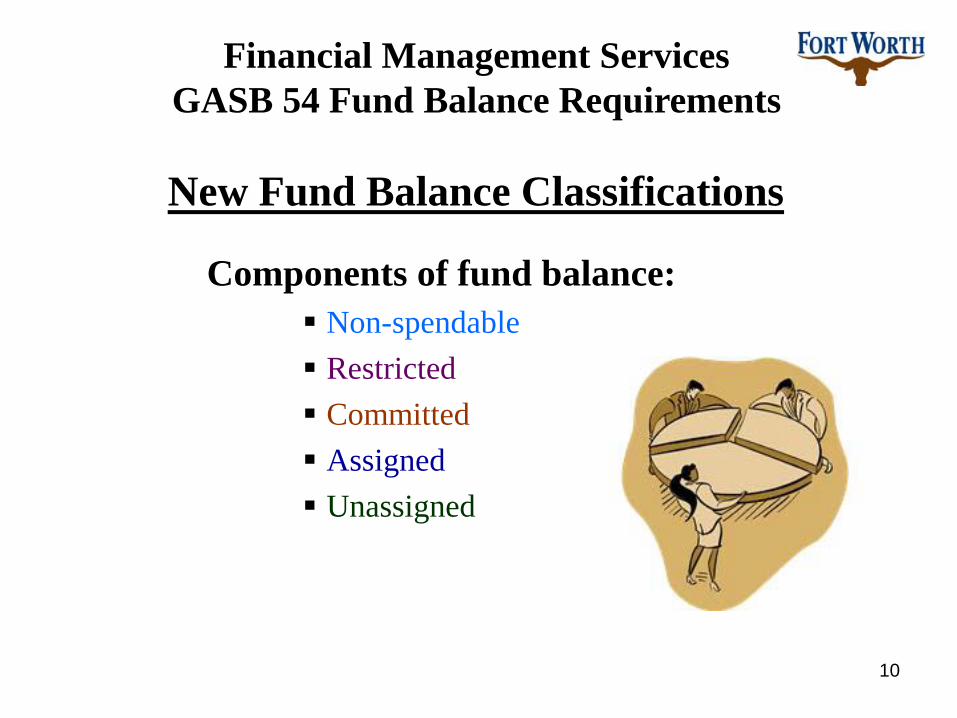

New Fund Balance Classifications

Components of fund balance: Non-spendable Restricted Committed Assigned Unassigned

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller11

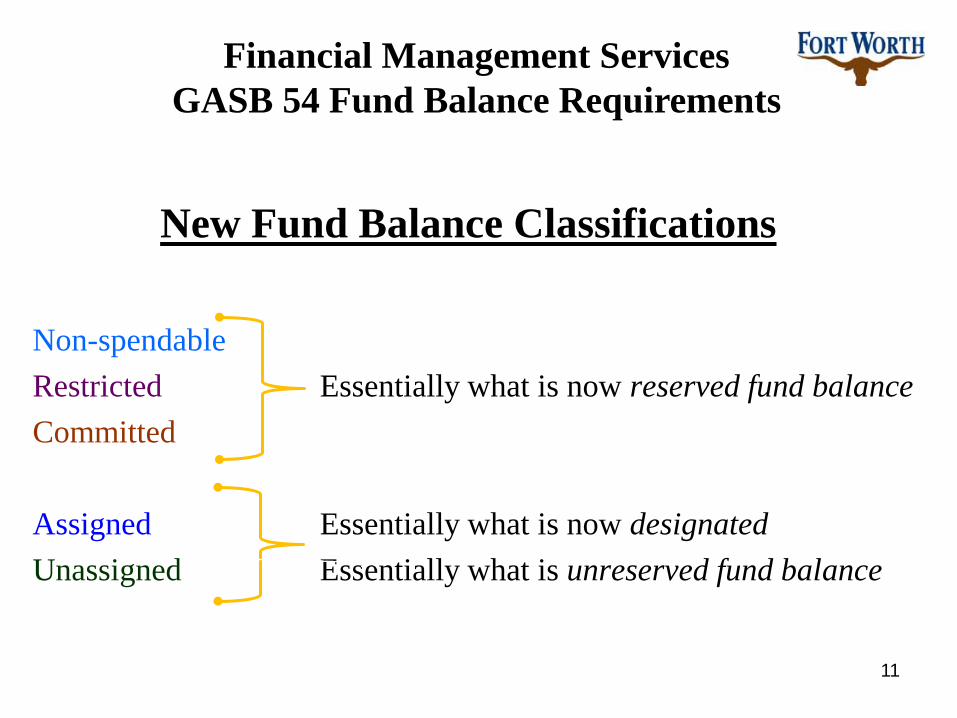

New Fund Balance Classifications

Non-spendableRestricted Essentially what is now reserved fund balanceCommitted

Assigned Essentially what is now designatedUnassigned Essentially what is unreserved fund balance

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller12

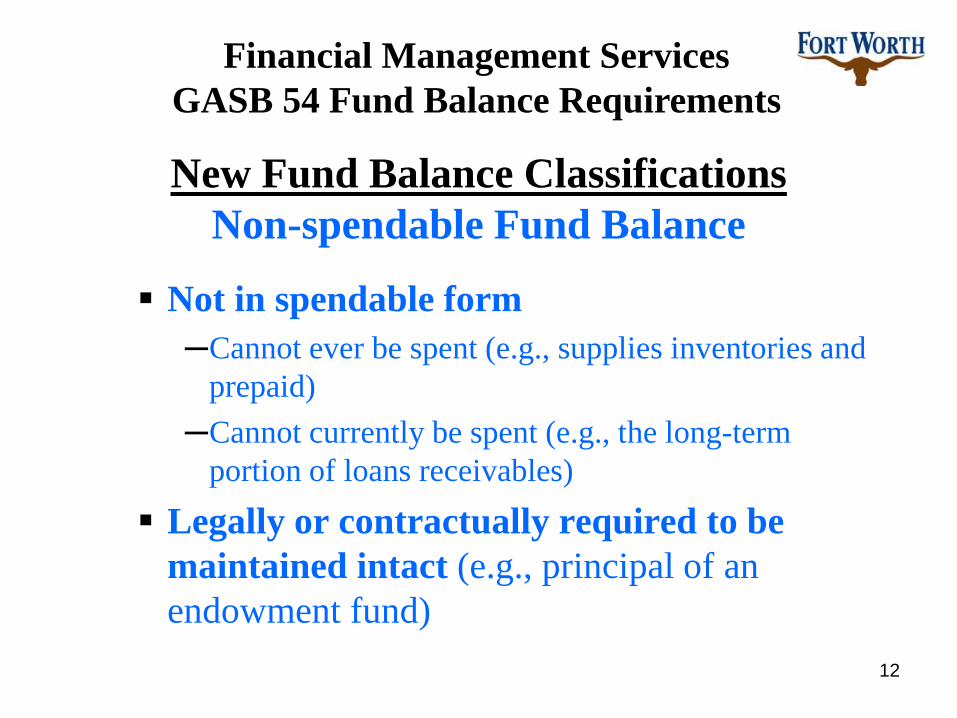

New Fund Balance ClassificationsNon-spendable Fund Balance

Not in spendable form─Cannot ever be spent (e.g., supplies inventories and

prepaid)─Cannot currently be spent (e.g., the long-term

portion of loans receivables) Legally or contractually required to be

maintained intact (e.g., principal of an endowment fund)

Financial Management ServicesGASB 54 Fund Balance Requirements

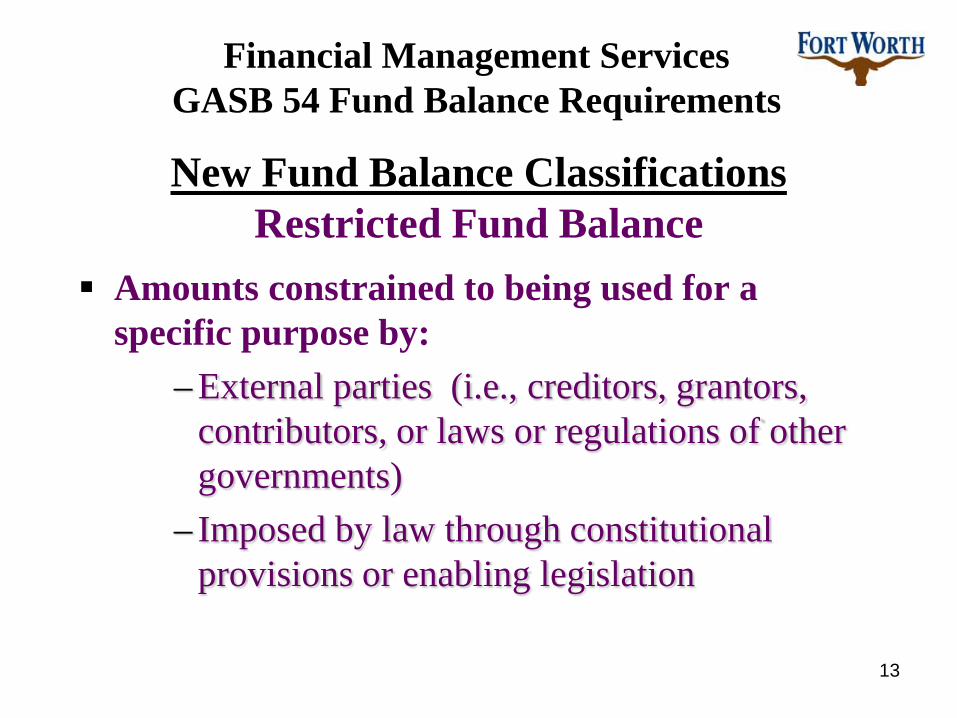

County of Riverside ■ Office of the Auditor-Controller13

New Fund Balance ClassificationsRestricted Fund Balance

Amounts constrained to being used for a specific purpose by:

– External parties (i.e., creditors, grantors, contributors, or laws or regulations of other governments)

– Imposed by law through constitutional provisions or enabling legislation

Financial Management ServicesGASB 54 Fund Balance Requirements

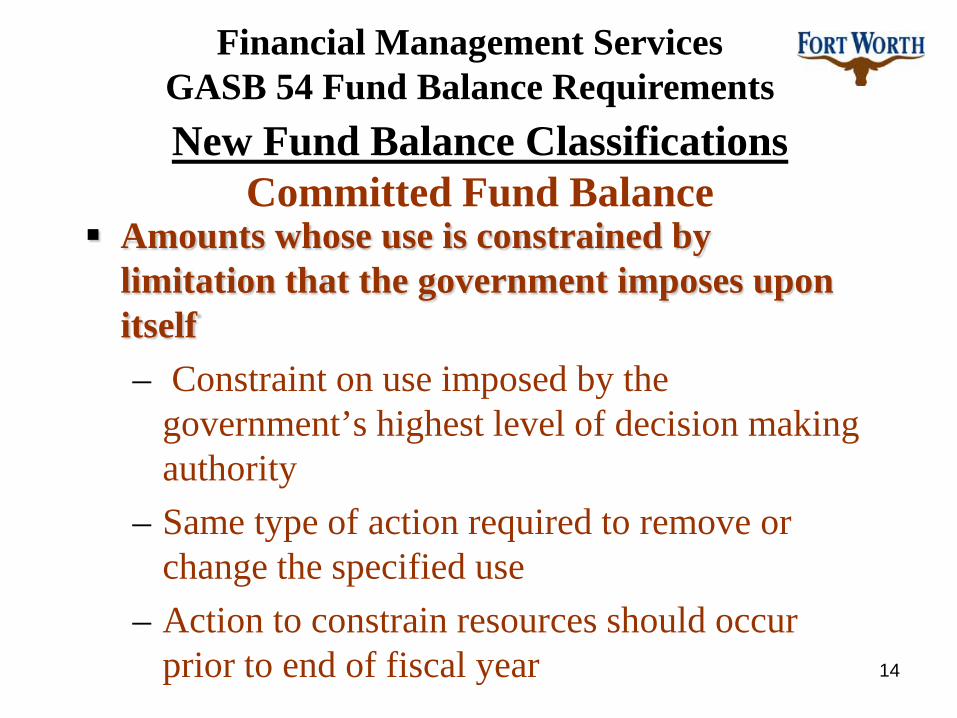

County of Riverside ■ Office of the Auditor-Controller14

New Fund Balance ClassificationsCommitted Fund Balance

Amounts whose use is constrained by limitation that the government imposes upon itself– Constraint on use imposed by the

government’s highest level of decision making authority

– Same type of action required to remove or change the specified use

– Action to constrain resources should occur prior to end of fiscal year

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller15

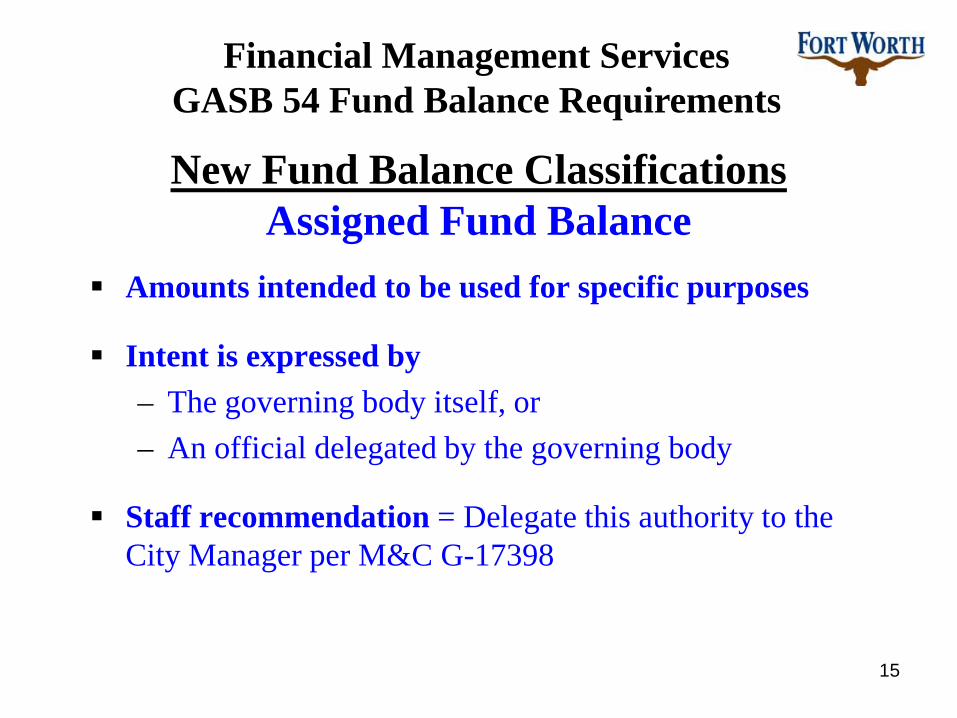

New Fund Balance ClassificationsAssigned Fund Balance

Amounts intended to be used for specific purposes

Intent is expressed by– The governing body itself, or– An official delegated by the governing body

Staff recommendation = Delegate this authority to the City Manager per M&C G-17398

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller16

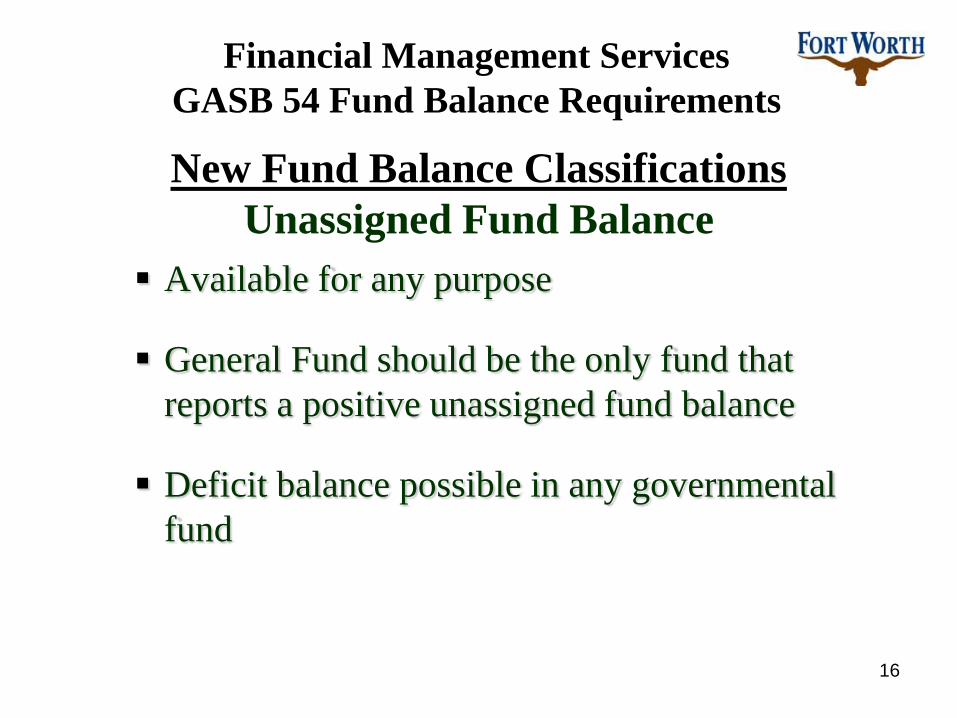

New Fund Balance ClassificationsUnassigned Fund Balance

Available for any purpose

General Fund should be the only fund that reports a positive unassigned fund balance

Deficit balance possible in any governmental fund

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller17

Encumbrances

Encumbrances should not be displayed as restricted, committed, or assigned categories.

Amounts are classified as restricted, committed, or assigned based on the source and strength of the constraints placed on them—encumbering those amount does not further affect them.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller18

Fund Balances: New Fund Balance:Reserved for Encumbrances 6,168$ Nonspendable:Reserved for Inventories 3,448 Inventories 3,448$ Reserved for Advances 5,966 Advances to Other Funds 5,966 Reserved for Prepaids, Deposits, and Other 532 Prepaids, Deposits and Other 532 Unreserved, Designated for Authorized Expenditures: Total Nonspendable 9,946

Risk Management 11,844$ Workers Compensation 3,993 Restricted:Unemployment Insurance 256 Culture & Tourism 15,692 Group Health Insurance 24,975 Revenue from DFW Assit 187 Culture & Tourism 15,692 Emerg Mgmt Rev-Tarra 25 353 Other Designations 600 Revenue from Guinn School 141

Total Unreserved, Designated 57,360 Total Restricted 16,045 General Fund

Unreserved: Committed:General Fund 58,794 Risk Management 11,844 Total Fund Balances 132,268$ Workers Compensation 3,993

Unemployment Insurance 256 Group Health Insurance 24,975 Encumbrance Approved

by Council before 9/30 6,110 Designations 600

Total Committed 47,778

Assigned:Encumbrances Approved

by Council after 9/30 - Encumbrance Approved

by City Manager 58 Total Assigned 58

Difference due to unspentrestricted revenues at year-end 353 Unassigned 58,441

Total Fund Balance 132,268$

FUND BALANCE JUNE 30, 2011 (CAFR FORMAT) FUND BALANCE AS RESTATED WITH GASB-54

CITY OF FORT WORTH, TEXASFUND BALANCEGENERAL FUND

JUNE 30, 2011(in 000's)

County of Riverside ■ Office of the Auditor-Controller19

Footnote Disclosure

• For Committed Fund Balance– The government’s highest level of

decision making authority;– Formal action that is required to be

taken.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller20

Footnote Disclosure

For Assigned Fund Balance:– The body or official authorized to assign

amounts to a specific purpose.– Staff recommendation = M&C G-17398 to

authorize City Manager or his/her designee to make assignment

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller21

Footnote Disclosure

Government policy regarding order of spending Staff recommendation = M&C G-17398 to

amend Financial Management Policy Statements

─ Restricted and unrestricted fund balance─ Committed, assigned, and unassigned

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller22

-----------------------------------Governmental Fund Type

Definitions-----------------------------------

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller23

Fund Type DefinitionsGeneral Fund

Current Definition: The general fund is used to account for all financial resources except those required to be accounted for in another fund.

GASB 54 Definition: The general fund is used to account for and report all financial resources not accounted for and reported in another fund.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller24

Financial Management ServicesGASB 54 Fund Balance Requirements

• General Fund for CAFR• Staff Recommendation = M&C G-17398 to

commit funds to Risk Financing– Risk Management Fund– Workers Compensation Insurance Funds– Group Health Insurance Fund– Unemployment Compensation Insurance Fund

Fund Type DefinitionsGeneral Fund

County of Riverside ■ Office of the Auditor-Controller25

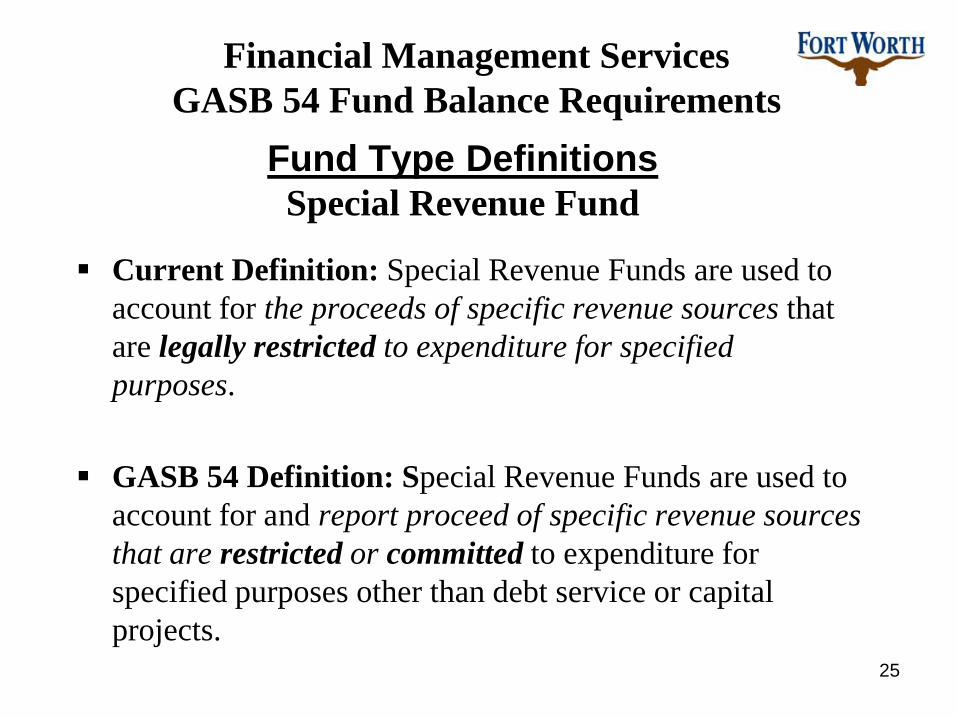

Fund Type DefinitionsSpecial Revenue Fund

Current Definition: Special Revenue Funds are used to account for the proceeds of specific revenue sources that are legally restricted to expenditure for specified purposes.

GASB 54 Definition: Special Revenue Funds are used to account for and report proceed of specific revenue sources that are restricted or committed to expenditure for specified purposes other than debt service or capital projects.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller26

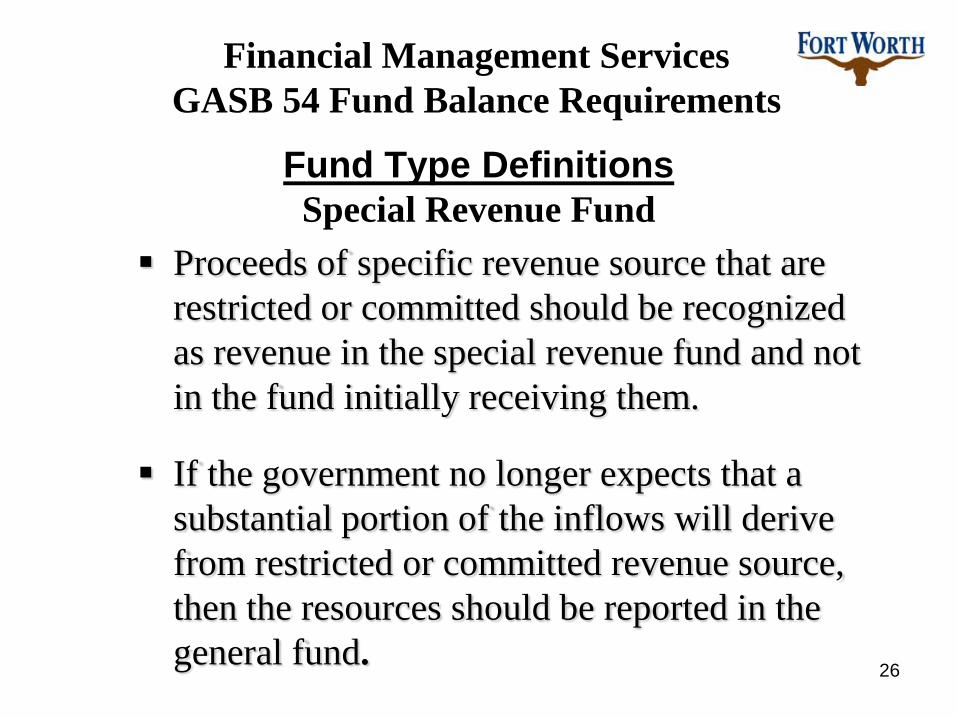

Fund Type DefinitionsSpecial Revenue Fund

Proceeds of specific revenue source that are restricted or committed should be recognized as revenue in the special revenue fund and not in the fund initially receiving them.

If the government no longer expects that a substantial portion of the inflows will derive from restricted or committed revenue source, then the resources should be reported in the general fund.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller27

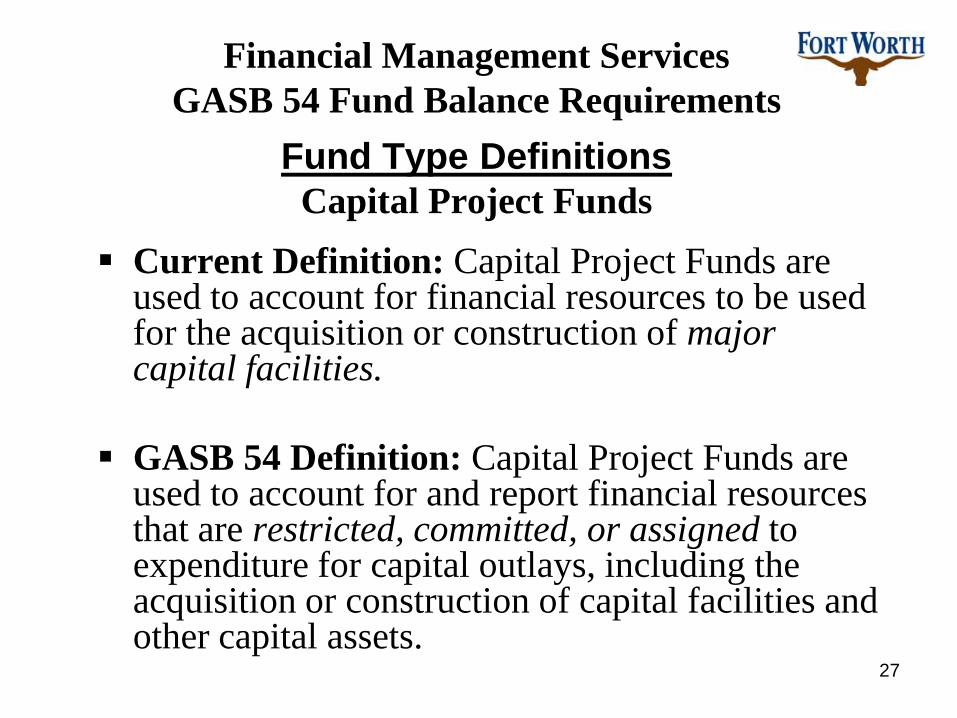

Fund Type DefinitionsCapital Project Funds

Current Definition: Capital Project Funds are used to account for financial resources to be used for the acquisition or construction of major capital facilities.

GASB 54 Definition: Capital Project Funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for capital outlays, including the acquisition or construction of capital facilities and other capital assets.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller28

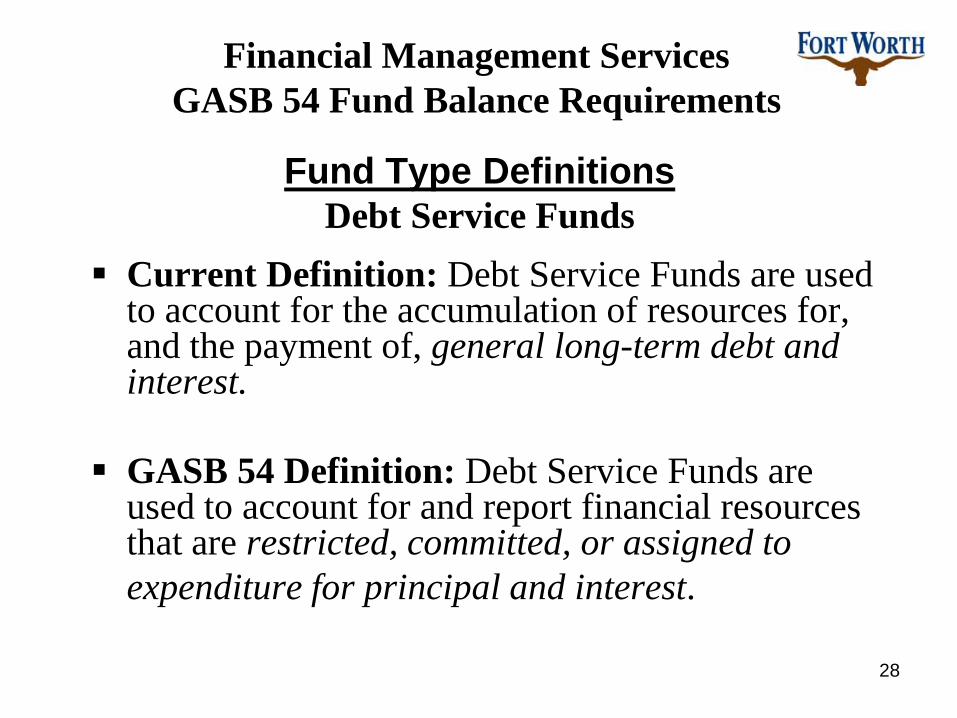

Fund Type DefinitionsDebt Service Funds

Current Definition: Debt Service Funds are used to account for the accumulation of resources for, and the payment of, general long-term debt and interest.

GASB 54 Definition: Debt Service Funds are used to account for and report financial resources that are restricted, committed, or assigned to expenditure for principal and interest.

Financial Management ServicesGASB 54 Fund Balance Requirements

County of Riverside ■ Office of the Auditor-Controller29

Next Steps

• Staff recommends approval of M&C G-17398– Establish priority of spending– Commit to risk financing – Appoint City Manager to assign fund balance

• To be compliant with normal purchasing rules

County of Riverside ■ Office of the Auditor-Controller30

Next Steps

• Implement GASB 54 = FY2011 CAFR• Continue to monitor and implement future

GASBs and other accounting and finance related requirements

County of Riverside ■ Office of the Auditor-Controller31

Fund Balance Reporting Requirements(GASB 54 Impact)

Questions?