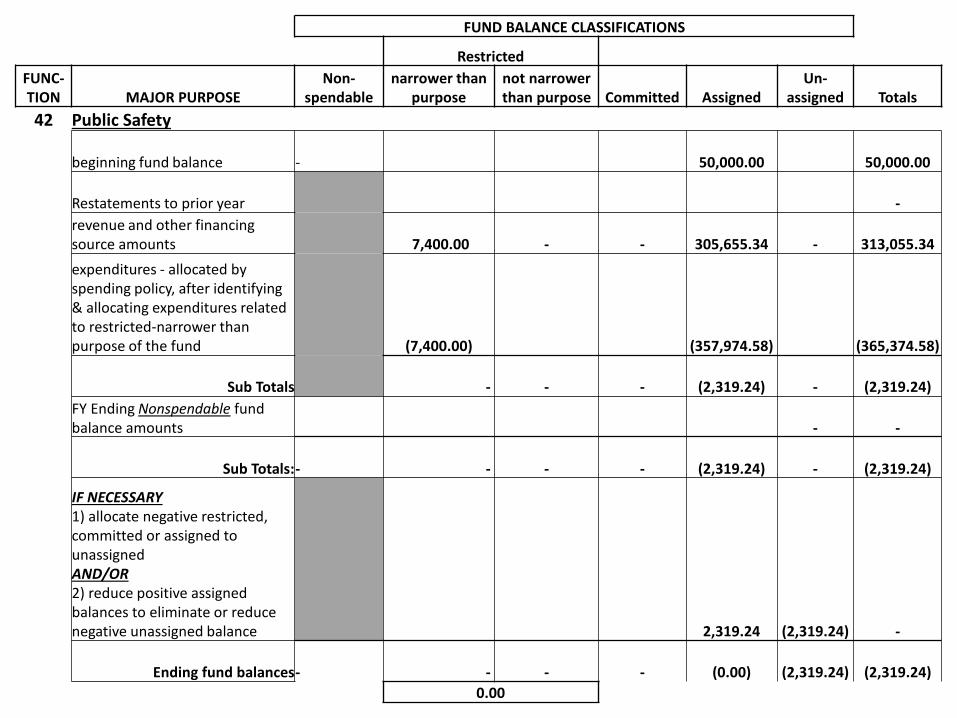

Embed Size (px)

Citation preview

THE WONDERFUL WORLD OF GASB

Presented by; Darla Erickson, Accounting & Management Systems Manager

&Magda Nelson, Fiscal Accounting Officer

DEPARTMENT OF ADMINISTRATIONLOCAL GOVERNMENT SERVICES BUREAU

Statement No. 54 Fund Balance Reporting and

Governmental Fund Type Definitions

Step by StepApproach

to Implementing GASB 54

.

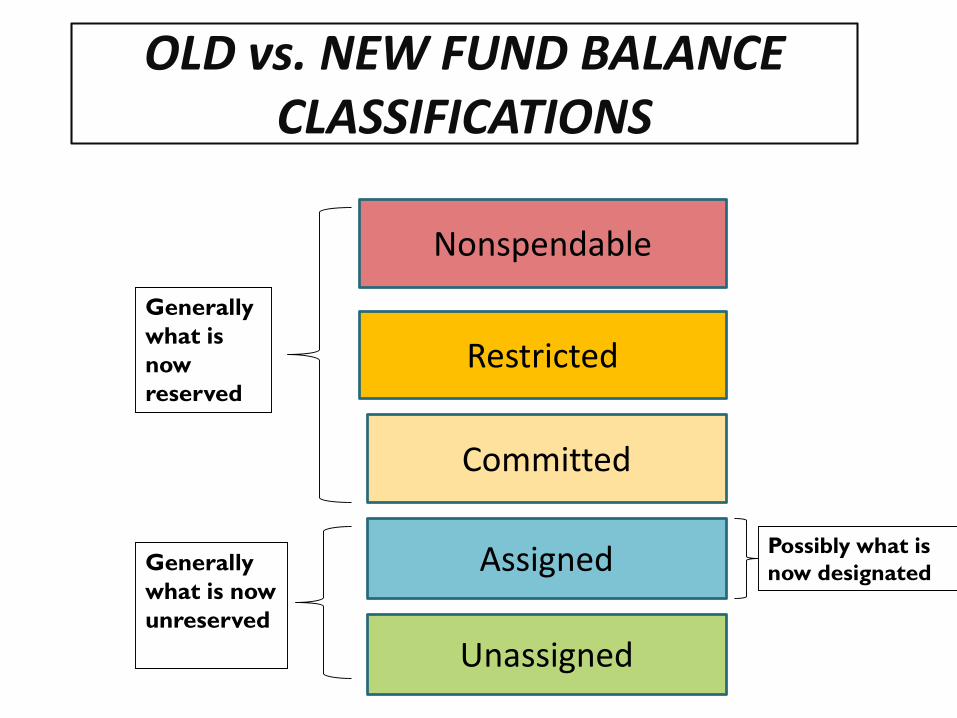

OLD vs. NEW FUND BALANCE CLASSIFICATIONS

Nonspendable

Restricted

Committed

Assigned

Unassigned

Generally what is now reserved

Generally what is now unreserved

Possibly what is now designated

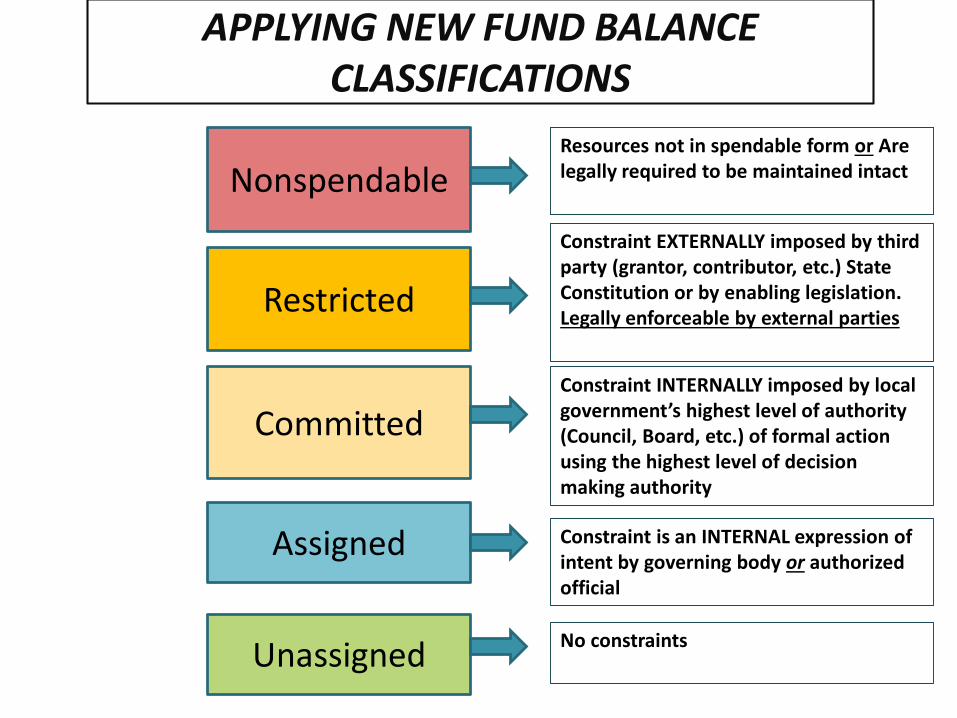

APPLYING NEW FUND BALANCE CLASSIFICATIONS

NonspendableResources not in spendable form or Are legally required to be maintained intact

Restricted

Committed

Assigned

Unassigned

Constraint EXTERNALLY imposed by third party (grantor, contributor, etc.) State Constitution or by enabling legislation. Legally enforceable by external parties

Constraint INTERNALLY imposed by local government’s highest level of authority (Council, Board, etc.) of formal action using the highest level of decision making authority

Constraint is an INTERNAL expression of intent by governing body or authorized official

No constraints

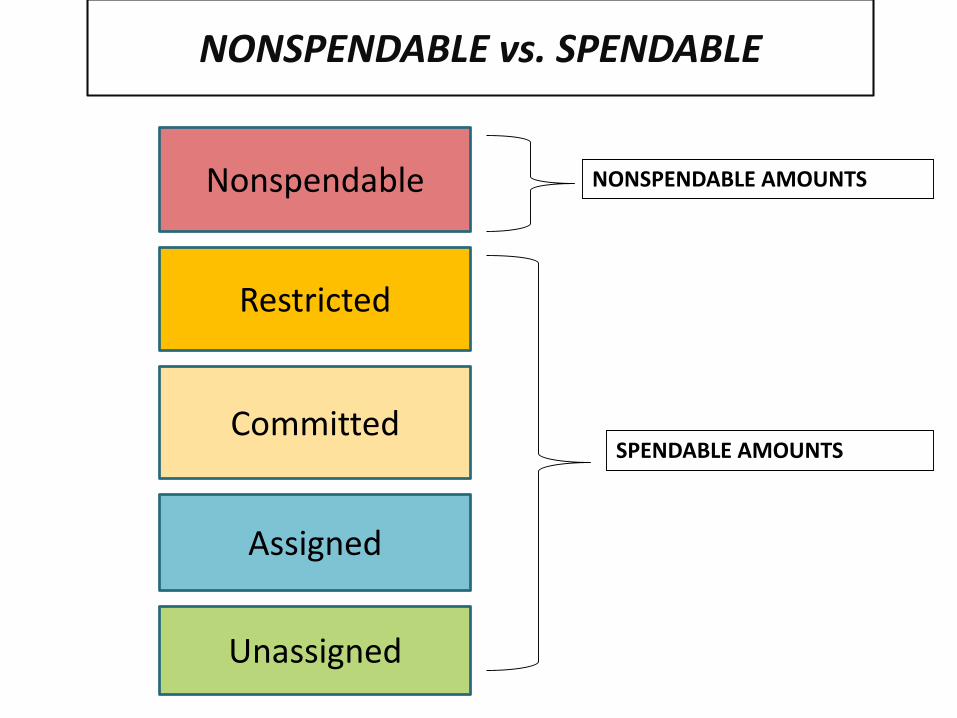

NONSPENDABLE vs. SPENDABLE

Nonspendable

Restricted

Committed

Assigned

Unassigned

SPENDABLE AMOUNTS

NONSPENDABLE AMOUNTS

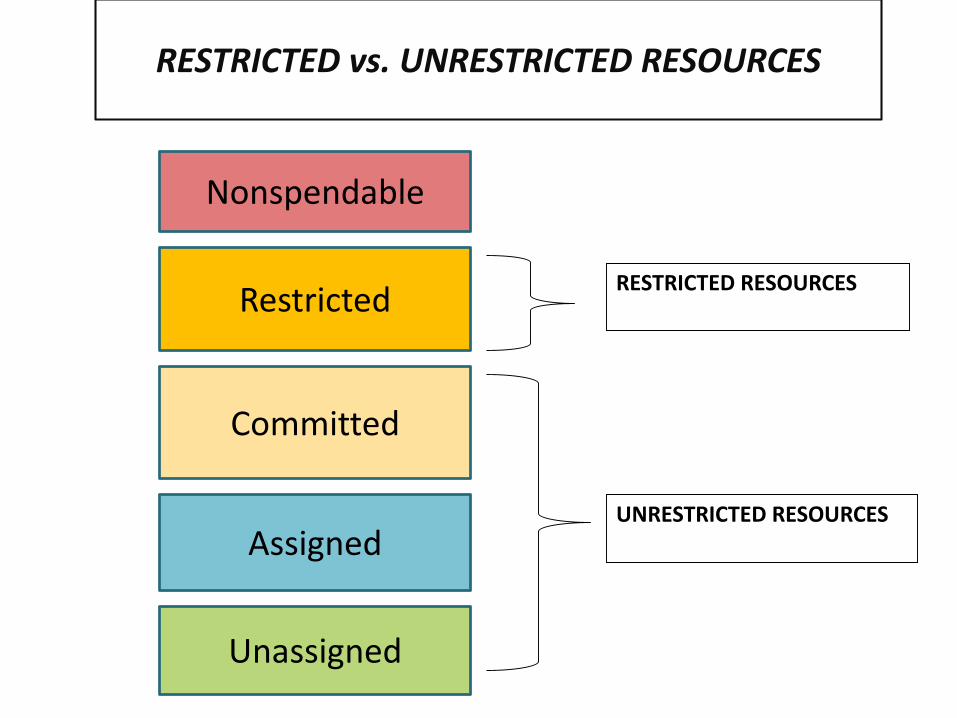

RESTRICTED vs. UNRESTRICTED RESOURCES

Nonspendable

Restricted

Committed

Assigned

Unassigned

UNRESTRICTED RESOURCES

RESTRICTED RESOURCES

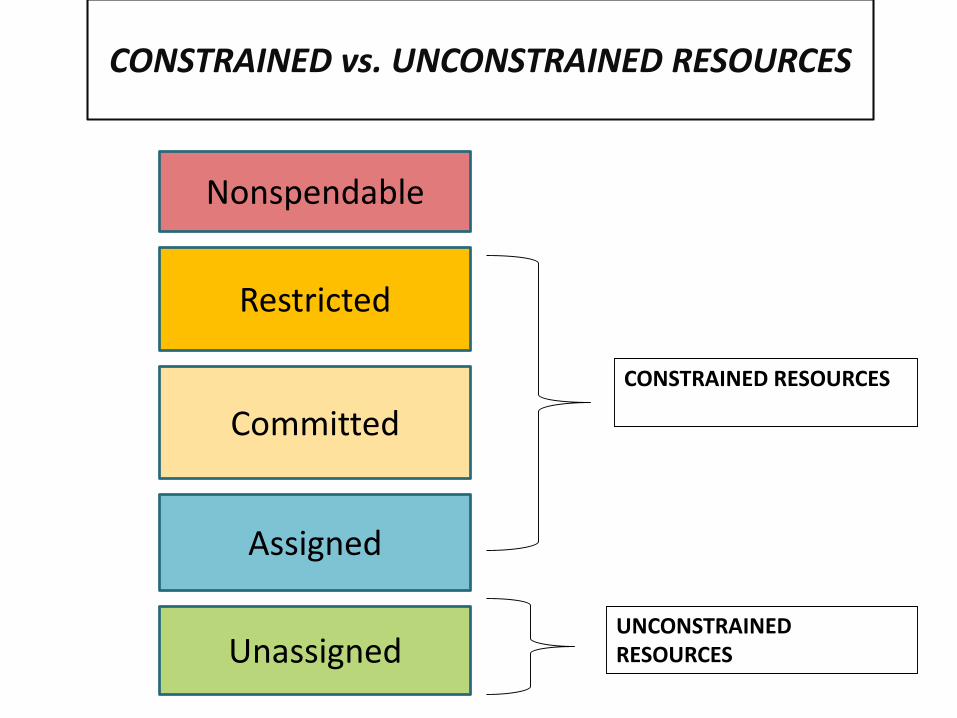

CONSTRAINED vs. UNCONSTRAINED RESOURCES

Nonspendable

Restricted

Committed

Assigned

UnassignedUNCONSTRAINED RESOURCES

CONSTRAINED RESOURCES

TO DO LIST – PRIOR TO YEAR END

1)Create and formally adopt a Spending Policy prior to fiscal year end.

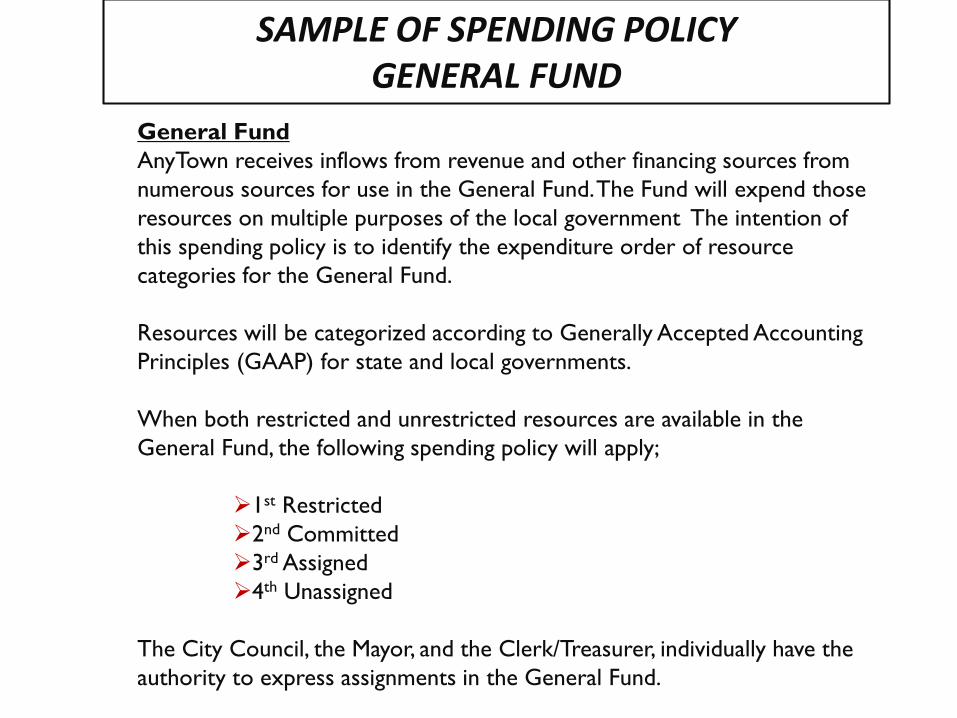

SAMPLE OF SPENDING POLICYGENERAL FUND

General FundAnyTown receives inflows from revenue and other financing sources from numerous sources for use in the General Fund. The Fund will expend those resources on multiple purposes of the local government The intention of this spending policy is to identify the expenditure order of resource categories for the General Fund.

Resources will be categorized according to Generally Accepted Accounting Principles (GAAP) for state and local governments.

When both restricted and unrestricted resources are available in the General Fund, the following spending policy will apply;

1st Restricted2nd Committed3rd Assigned4th Unassigned

The City Council, the Mayor, and the Clerk/Treasurer, individually have the authority to express assignments in the General Fund.

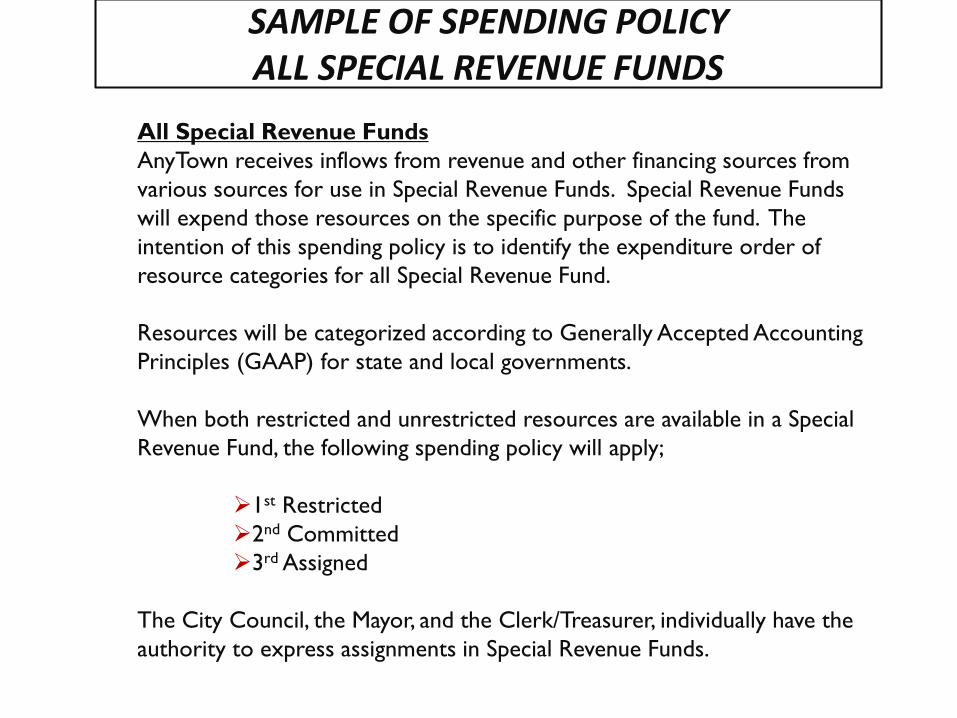

SAMPLE OF SPENDING POLICYALL SPECIAL REVENUE FUNDS

All Special Revenue FundsAnyTown receives inflows from revenue and other financing sources from various sources for use in Special Revenue Funds. Special Revenue Funds will expend those resources on the specific purpose of the fund. The intention of this spending policy is to identify the expenditure order of resource categories for all Special Revenue Fund.

Resources will be categorized according to Generally Accepted Accounting Principles (GAAP) for state and local governments.

When both restricted and unrestricted resources are available in a Special Revenue Fund, the following spending policy will apply;

1st Restricted2nd Committed3rd Assigned

The City Council, the Mayor, and the Clerk/Treasurer, individually have the authority to express assignments in Special Revenue Funds.

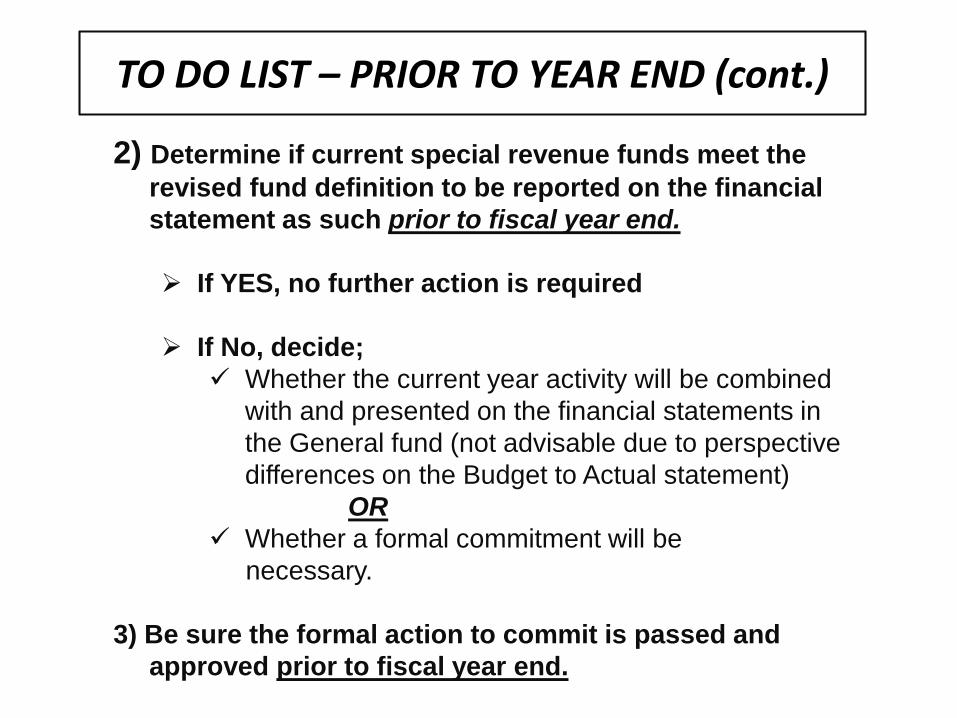

TO DO LIST – PRIOR TO YEAR END (cont.)

2) Determine if current special revenue funds meet the revised fund definition to be reported on the financial statement as such prior to fiscal year end.

If YES, no further action is required

If No, decide; Whether the current year activity will be combined

with and presented on the financial statements in the General fund (not advisable due to perspective differences on the Budget to Actual statement)

OR Whether a formal commitment will be

necessary.

3) Be sure the formal action to commit is passed and approved prior to fiscal year end.

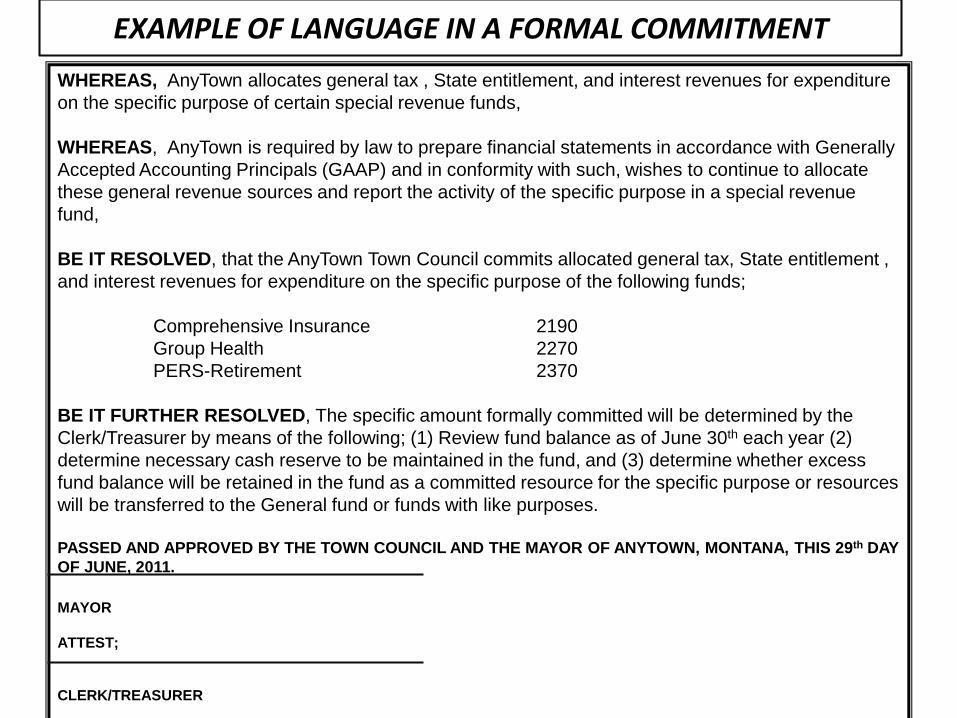

EXAMPLE OF LANGUAGE IN A FORMAL COMMITMENTWHEREAS, AnyTown allocates general tax , State entitlement, and interest revenues for expenditure on the specific purpose of certain special revenue funds,

WHEREAS, AnyTown is required by law to prepare financial statements in accordance with Generally Accepted Accounting Principals (GAAP) and in conformity with such, wishes to continue to allocate these general revenue sources and report the activity of the specific purpose in a special revenue fund,

BE IT RESOLVED, that the AnyTown Town Council commits allocated general tax, State entitlement , and interest revenues for expenditure on the specific purpose of the following funds;

Comprehensive Insurance 2190Group Health 2270PERS-Retirement 2370

BE IT FURTHER RESOLVED, The specific amount formally committed will be determined by the Clerk/Treasurer by means of the following; (1) Review fund balance as of June 30th each year (2) determine necessary cash reserve to be maintained in the fund, and (3) determine whether excess fund balance will be retained in the fund as a committed resource for the specific purpose or resources will be transferred to the General fund or funds with like purposes.

PASSED AND APPROVED BY THE TOWN COUNCIL AND THE MAYOR OF ANYTOWN, MONTANA, THIS 29th DAY OF JUNE, 2011.

MAYOR

ATTEST;

CLERK/TREASURER

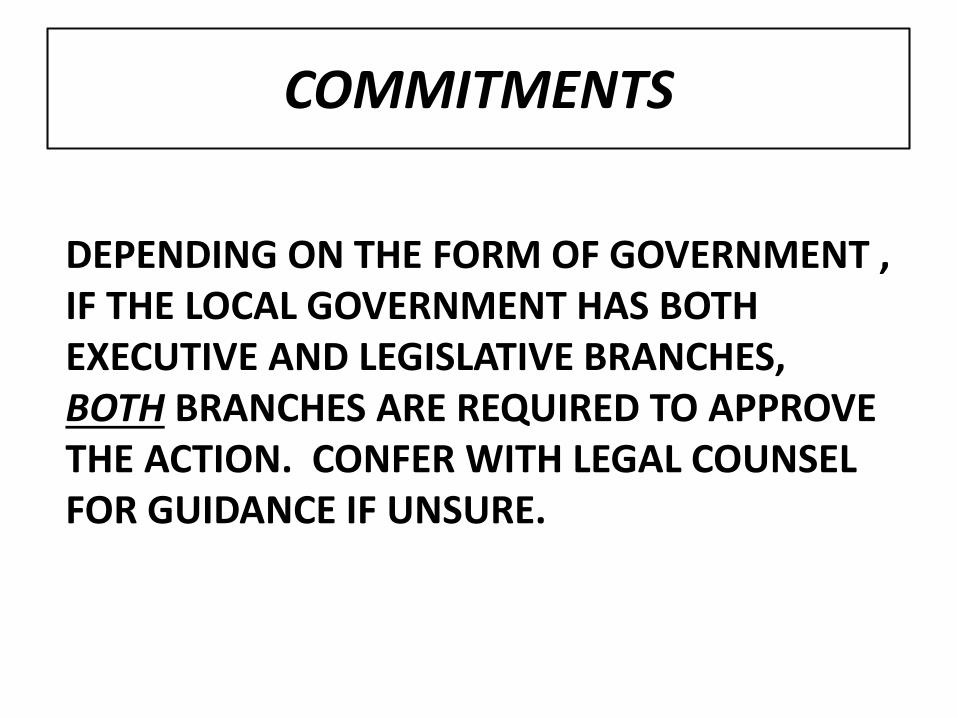

COMMITMENTS

DEPENDING ON THE FORM OF GOVERNMENT , IF THE LOCAL GOVERNMENT HAS BOTH EXECUTIVE AND LEGISLATIVE BRANCHES, BOTH BRANCHES ARE REQUIRED TO APPROVE THE ACTION. CONFER WITH LEGAL COUNSEL FOR GUIDANCE IF UNSURE.

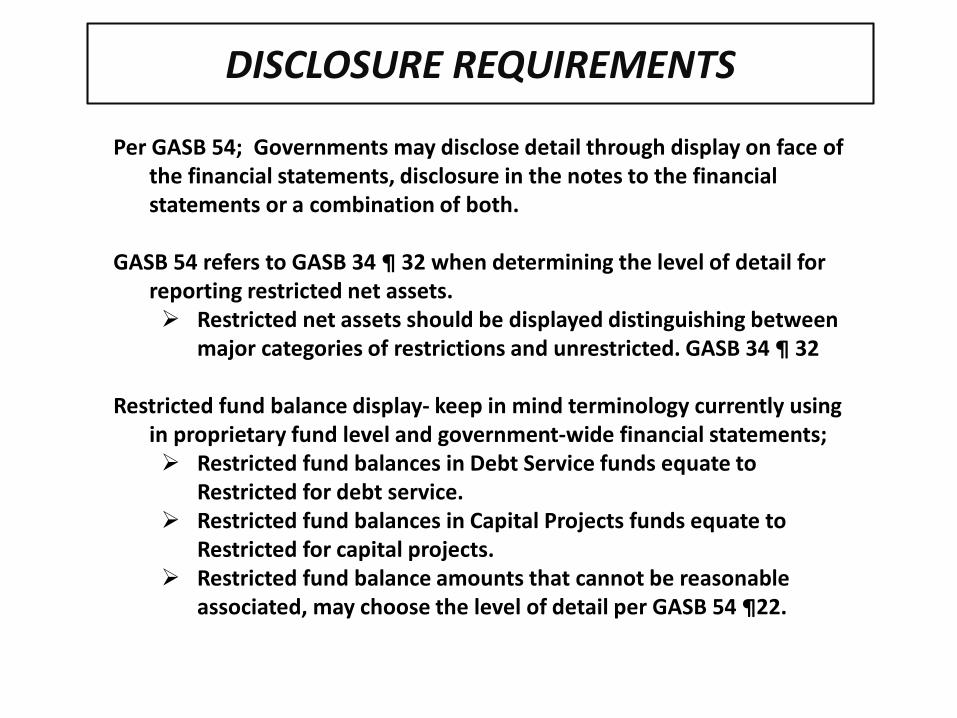

DISCLOSURE REQUIREMENTS

Per GASB 54; Governments may disclose detail through display on face of the financial statements, disclosure in the notes to the financial statements or a combination of both.

GASB 54 refers to GASB 34 ¶ 32 when determining the level of detail for reporting restricted net assets. Restricted net assets should be displayed distinguishing between

major categories of restrictions and unrestricted. GASB 34 ¶ 32

Restricted fund balance display- keep in mind terminology currently using in proprietary fund level and government-wide financial statements; Restricted fund balances in Debt Service funds equate to

Restricted for debt service. Restricted fund balances in Capital Projects funds equate to

Restricted for capital projects. Restricted fund balance amounts that cannot be reasonable

associated, may choose the level of detail per GASB 54 ¶22.

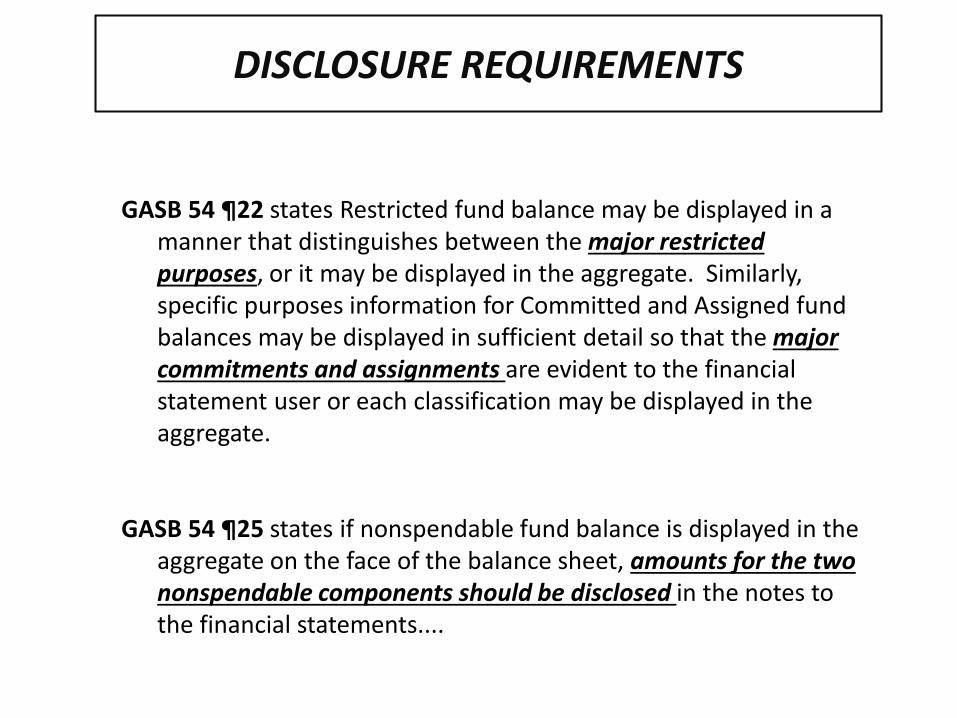

DISCLOSURE REQUIREMENTS

GASB 54 ¶22 states Restricted fund balance may be displayed in a manner that distinguishes between the major restricted purposes, or it may be displayed in the aggregate. Similarly, specific purposes information for Committed and Assigned fund balances may be displayed in sufficient detail so that the major commitments and assignments are evident to the financial statement user or each classification may be displayed in the aggregate.

GASB 54 ¶25 states if nonspendable fund balance is displayed in the aggregate on the face of the balance sheet, amounts for the two nonspendable components should be disclosed in the notes to the financial statements....

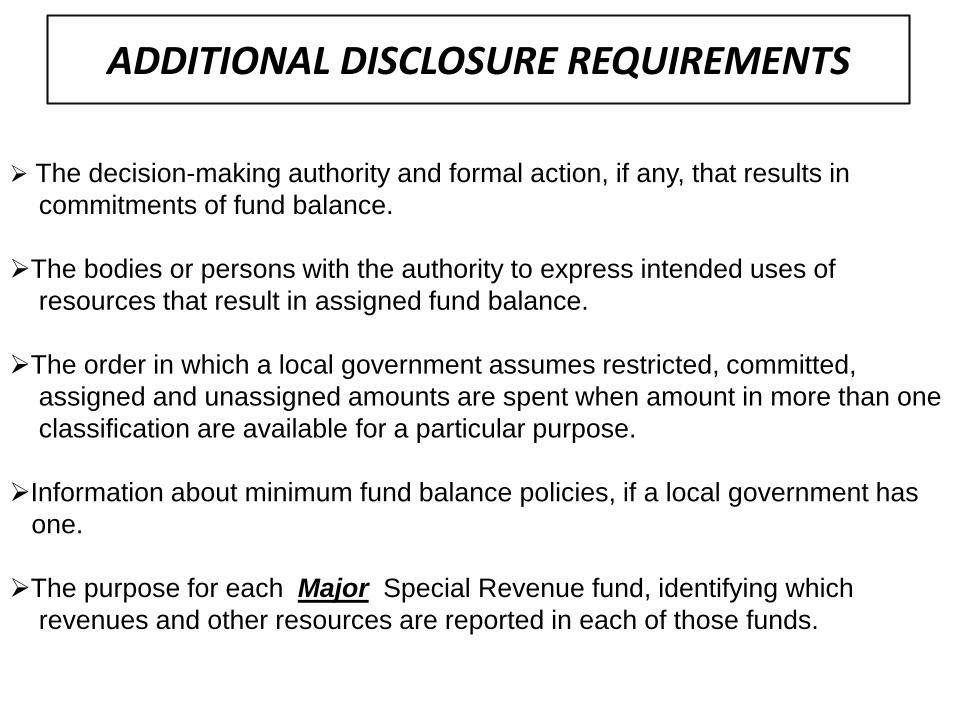

ADDITIONAL DISCLOSURE REQUIREMENTS

The decision-making authority and formal action, if any, that results incommitments of fund balance.

The bodies or persons with the authority to express intended uses ofresources that result in assigned fund balance.

The order in which a local government assumes restricted, committed,assigned and unassigned amounts are spent when amount in more than oneclassification are available for a particular purpose.

Information about minimum fund balance policies, if a local government hasone.

The purpose for each Major Special Revenue fund, identifying whichrevenues and other resources are reported in each of those funds.

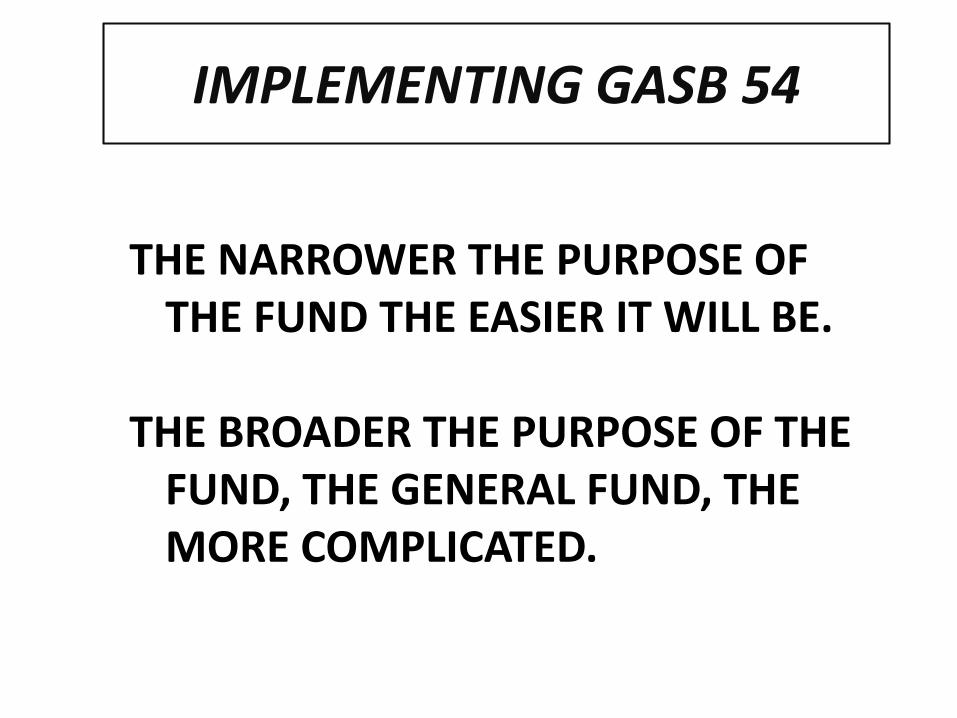

IMPLEMENTING GASB 54

THE NARROWER THE PURPOSE OF THE FUND THE EASIER IT WILL BE.

THE BROADER THE PURPOSE OF THE FUND, THE GENERAL FUND, THE MORE COMPLICATED.

IMPLEMENTING GASB 54

THERE ARE 7 STEPS TO ASUCCESSFUL IMPLEMENTATION

OF GASB 54.

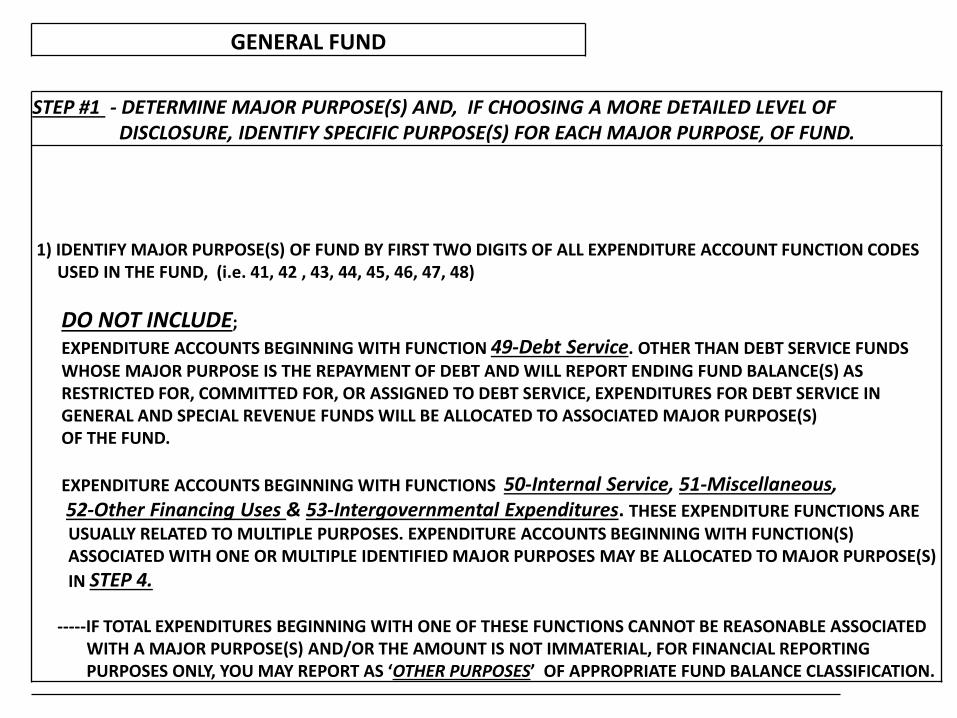

GENERAL FUND

STEP #1 - DETERMINE MAJOR PURPOSE(S) AND, IF CHOOSING A MORE DETAILED LEVEL OFDISCLOSURE, IDENTIFY SPECIFIC PURPOSE(S) FOR EACH MAJOR PURPOSE, OF FUND.

1) IDENTIFY MAJOR PURPOSE(S) OF FUND BY FIRST TWO DIGITS OF ALL EXPENDITURE ACCOUNT FUNCTION CODESUSED IN THE FUND, (i.e. 41, 42 , 43, 44, 45, 46, 47, 48)

DO NOT INCLUDE;EXPENDITURE ACCOUNTS BEGINNING WITH FUNCTION 49-Debt Service. OTHER THAN DEBT SERVICE FUNDSWHOSE MAJOR PURPOSE IS THE REPAYMENT OF DEBT AND WILL REPORT ENDING FUND BALANCE(S) ASRESTRICTED FOR, COMMITTED FOR, OR ASSIGNED TO DEBT SERVICE, EXPENDITURES FOR DEBT SERVICE INGENERAL AND SPECIAL REVENUE FUNDS WILL BE ALLOCATED TO ASSOCIATED MAJOR PURPOSE(S)OF THE FUND.

EXPENDITURE ACCOUNTS BEGINNING WITH FUNCTIONS 50-Internal Service, 51-Miscellaneous, 52-Other Financing Uses & 53-Intergovernmental Expenditures. THESE EXPENDITURE FUNCTIONS ARE USUALLY RELATED TO MULTIPLE PURPOSES. EXPENDITURE ACCOUNTS BEGINNING WITH FUNCTION(S)ASSOCIATED WITH ONE OR MULTIPLE IDENTIFIED MAJOR PURPOSES MAY BE ALLOCATED TO MAJOR PURPOSE(S)IN STEP 4.

-----IF TOTAL EXPENDITURES BEGINNING WITH ONE OF THESE FUNCTIONS CANNOT BE REASONABLE ASSOCIATEDWITH A MAJOR PURPOSE(S) AND/OR THE AMOUNT IS NOT IMMATERIAL, FOR FINANCIAL REPORTINGPURPOSES ONLY, YOU MAY REPORT AS ‘OTHER PURPOSES’ OF APPROPRIATE FUND BALANCE CLASSIFICATION.

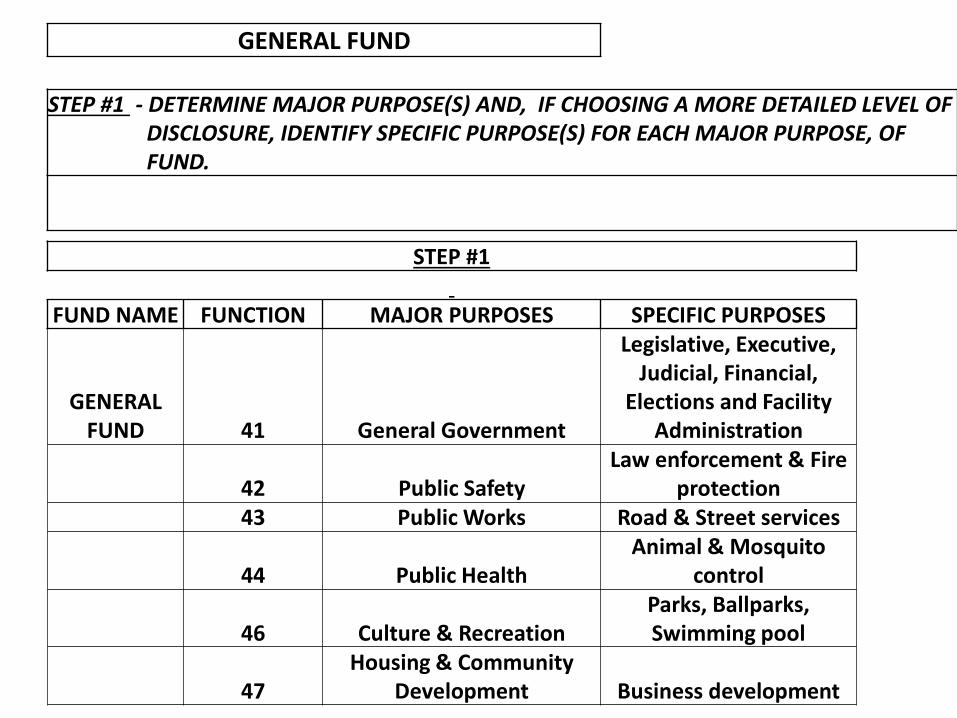

GENERAL FUND

STEP #1 - DETERMINE MAJOR PURPOSE(S) AND, IF CHOOSING A MORE DETAILED LEVEL OFDISCLOSURE, IDENTIFY SPECIFIC PURPOSE(S) FOR EACH MAJOR PURPOSE, OFFUND.

STEP #1

FUND NAME FUNCTION MAJOR PURPOSES SPECIFIC PURPOSES

GENERAL FUND 41 General Government

Legislative, Executive, Judicial, Financial,

Elections and Facility Administration

42 Public SafetyLaw enforcement & Fire

protection43 Public Works Road & Street services

44 Public HealthAnimal & Mosquito

control

46 Culture & RecreationParks, Ballparks, Swimming pool

47Housing & Community

Development Business development

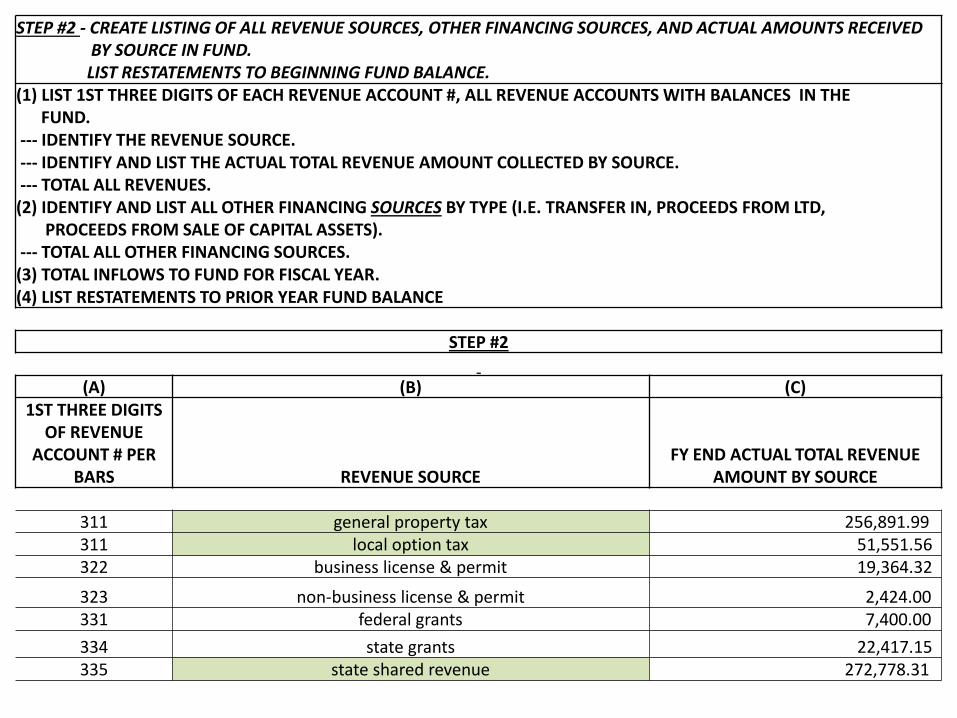

STEP #2 - CREATE LISTING OF ALL REVENUE SOURCES, OTHER FINANCING SOURCES, AND ACTUAL AMOUNTS RECEIVEDBY SOURCE IN FUND. LIST RESTATEMENTS TO BEGINNING FUND BALANCE.

(1) LIST 1ST THREE DIGITS OF EACH REVENUE ACCOUNT #, ALL REVENUE ACCOUNTS WITH BALANCES IN THEFUND.

--- IDENTIFY THE REVENUE SOURCE.--- IDENTIFY AND LIST THE ACTUAL TOTAL REVENUE AMOUNT COLLECTED BY SOURCE. --- TOTAL ALL REVENUES.(2) IDENTIFY AND LIST ALL OTHER FINANCING SOURCES BY TYPE (I.E. TRANSFER IN, PROCEEDS FROM LTD,

PROCEEDS FROM SALE OF CAPITAL ASSETS). --- TOTAL ALL OTHER FINANCING SOURCES.(3) TOTAL INFLOWS TO FUND FOR FISCAL YEAR.(4) LIST RESTATEMENTS TO PRIOR YEAR FUND BALANCE

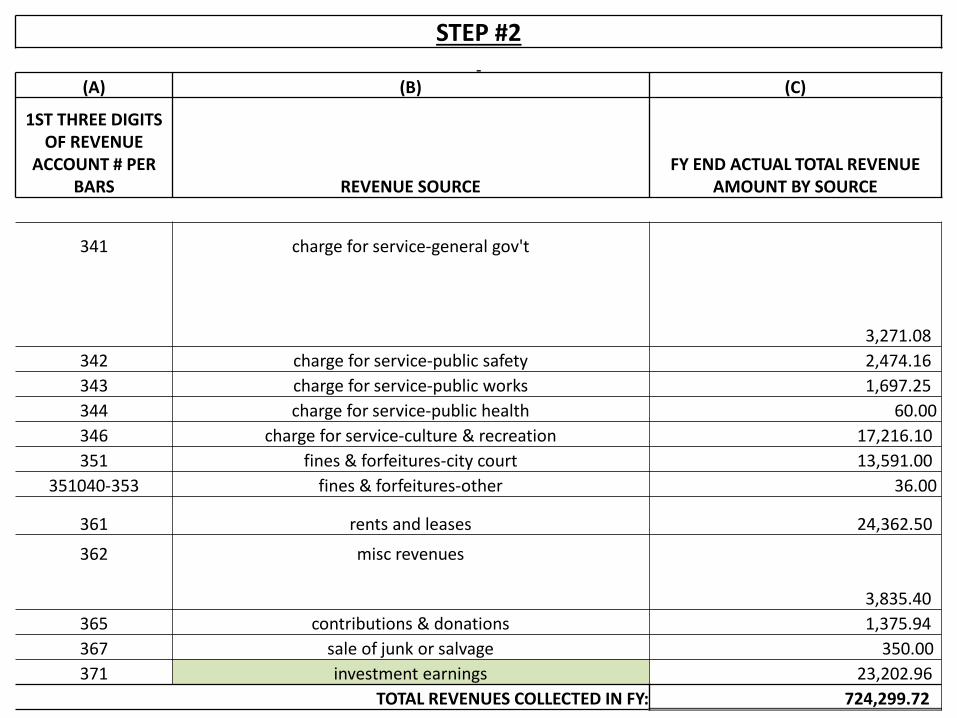

STEP #2

(A) (B) (C)1ST THREE DIGITS

OF REVENUE ACCOUNT # PER

BARS REVENUE SOURCEFY END ACTUAL TOTAL REVENUE

AMOUNT BY SOURCE

311 general property tax 256,891.99 311 local option tax 51,551.56 322 business license & permit 19,364.32

323 non-business license & permit 2,424.00 331 federal grants 7,400.00 334 state grants 22,417.15 335 state shared revenue 272,778.31

STEP #2

(A) (B) (C)

1ST THREE DIGITS OF REVENUE

ACCOUNT # PER BARS REVENUE SOURCE

FY END ACTUAL TOTAL REVENUE AMOUNT BY SOURCE

341 charge for service-general gov't

3,271.08 342 charge for service-public safety 2,474.16 343 charge for service-public works 1,697.25 344 charge for service-public health 60.00 346 charge for service-culture & recreation 17,216.10 351 fines & forfeitures-city court 13,591.00

351040-353 fines & forfeitures-other 36.00

361 rents and leases 24,362.50

362 misc revenues

3,835.40 365 contributions & donations 1,375.94 367 sale of junk or salvage 350.00 371 investment earnings 23,202.96

TOTAL REVENUES COLLECTED IN FY: 724,299.72

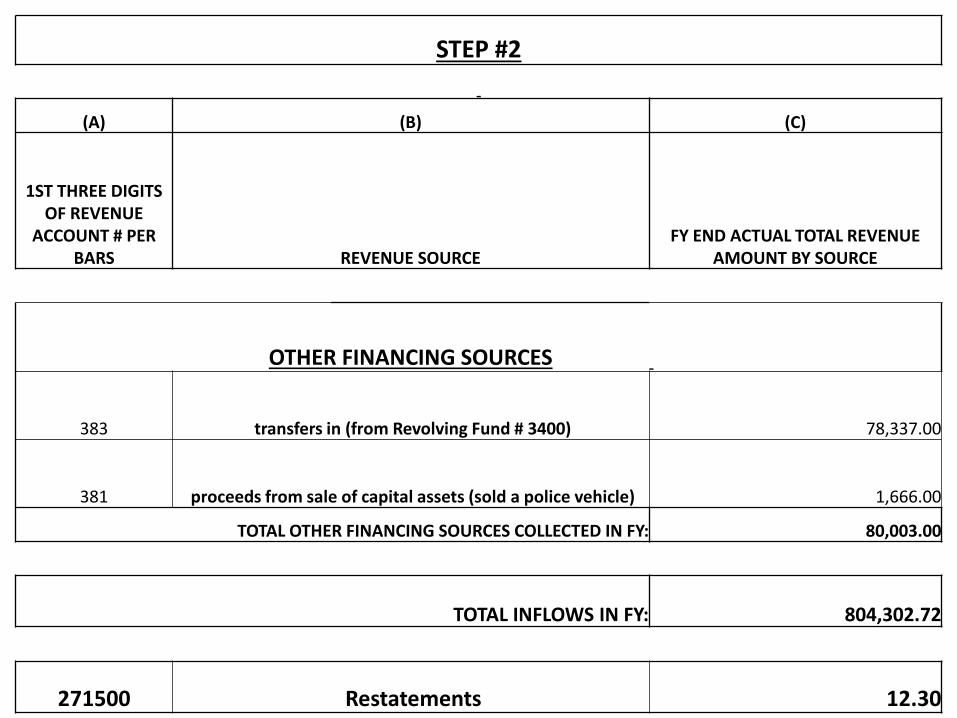

STEP #2

(A) (B) (C)

1ST THREE DIGITS OF REVENUE

ACCOUNT # PER BARS REVENUE SOURCE

FY END ACTUAL TOTAL REVENUE AMOUNT BY SOURCE

OTHER FINANCING SOURCES

383 transfers in (from Revolving Fund # 3400) 78,337.00

381 proceeds from sale of capital assets (sold a police vehicle) 1,666.00

TOTAL OTHER FINANCING SOURCES COLLECTED IN FY: 80,003.00

TOTAL INFLOWS IN FY: 804,302.72

271500 Restatements 12.30

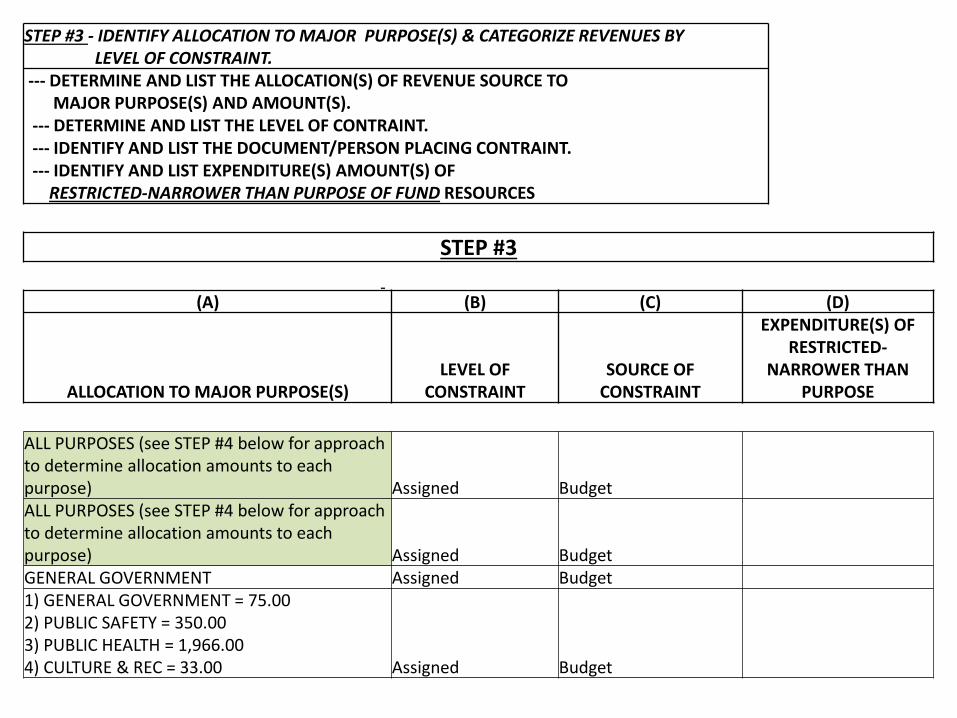

STEP #3 - IDENTIFY ALLOCATION TO MAJOR PURPOSE(S) & CATEGORIZE REVENUES BYLEVEL OF CONSTRAINT.

--- DETERMINE AND LIST THE ALLOCATION(S) OF REVENUE SOURCE TOMAJOR PURPOSE(S) AND AMOUNT(S).

--- DETERMINE AND LIST THE LEVEL OF CONTRAINT.--- IDENTIFY AND LIST THE DOCUMENT/PERSON PLACING CONTRAINT.--- IDENTIFY AND LIST EXPENDITURE(S) AMOUNT(S) OF

RESTRICTED-NARROWER THAN PURPOSE OF FUND RESOURCES

STEP #3

(A) (B) (C) (D)

ALLOCATION TO MAJOR PURPOSE(S)LEVEL OF

CONSTRAINTSOURCE OF

CONSTRAINT

EXPENDITURE(S) OF RESTRICTED-

NARROWER THAN PURPOSE

ALL PURPOSES (see STEP #4 below for approach to determine allocation amounts to each purpose) Assigned BudgetALL PURPOSES (see STEP #4 below for approach to determine allocation amounts to each purpose) Assigned BudgetGENERAL GOVERNMENT Assigned Budget1) GENERAL GOVERNMENT = 75.002) PUBLIC SAFETY = 350.003) PUBLIC HEALTH = 1,966.004) CULTURE & REC = 33.00 Assigned Budget

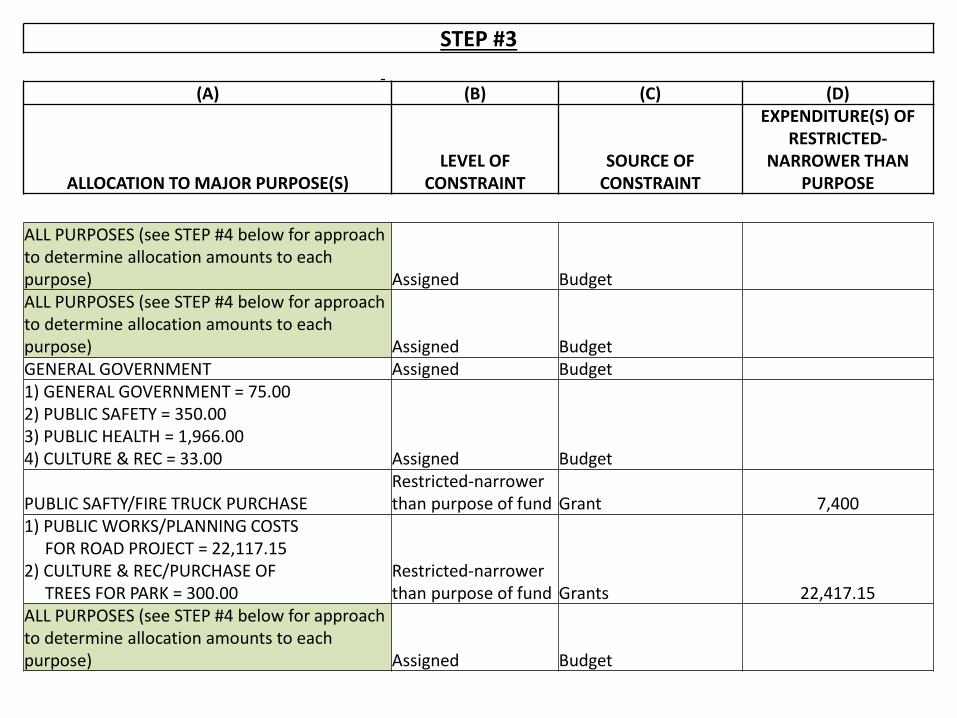

STEP #3

(A) (B) (C) (D)

ALLOCATION TO MAJOR PURPOSE(S)LEVEL OF

CONSTRAINTSOURCE OF

CONSTRAINT

EXPENDITURE(S) OF RESTRICTED-

NARROWER THAN PURPOSE

ALL PURPOSES (see STEP #4 below for approach to determine allocation amounts to each purpose) Assigned BudgetALL PURPOSES (see STEP #4 below for approach to determine allocation amounts to each purpose) Assigned BudgetGENERAL GOVERNMENT Assigned Budget1) GENERAL GOVERNMENT = 75.002) PUBLIC SAFETY = 350.003) PUBLIC HEALTH = 1,966.004) CULTURE & REC = 33.00 Assigned Budget

PUBLIC SAFTY/FIRE TRUCK PURCHASERestricted-narrower than purpose of fund Grant 7,400

1) PUBLIC WORKS/PLANNING COSTSFOR ROAD PROJECT = 22,117.15

2) CULTURE & REC/PURCHASE OFTREES FOR PARK = 300.00

Restricted-narrower than purpose of fund Grants 22,417.15

ALL PURPOSES (see STEP #4 below for approach to determine allocation amounts to each purpose) Assigned Budget

STEP #3

(A) (B) (C) (D)

ALLOCATION TO MAJOR PURPOSE(S)LEVEL OF

CONSTRAINTSOURCE OF

CONSTRAINT

EXPENDITURE(S) OF RESTRICTED-

NARROWER THAN PURPOSE

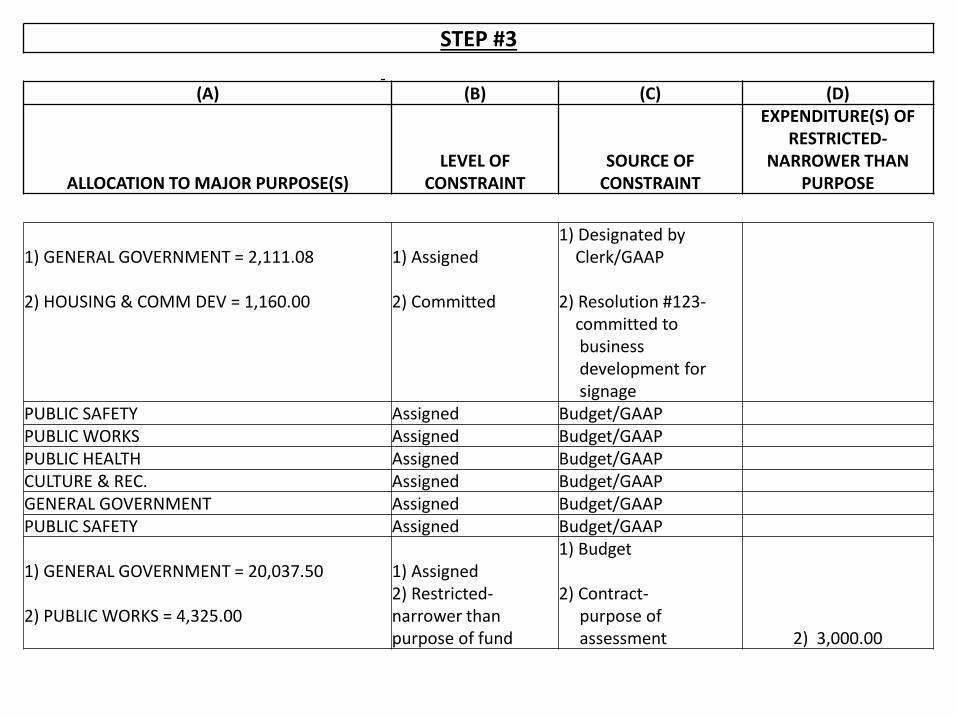

1) GENERAL GOVERNMENT = 2,111.08

2) HOUSING & COMM DEV = 1,160.00

1) Assigned

2) Committed

1) Designated byClerk/GAAP

2) Resolution #123-committed tobusinessdevelopment forsignage

PUBLIC SAFETY Assigned Budget/GAAPPUBLIC WORKS Assigned Budget/GAAPPUBLIC HEALTH Assigned Budget/GAAPCULTURE & REC. Assigned Budget/GAAPGENERAL GOVERNMENT Assigned Budget/GAAPPUBLIC SAFETY Assigned Budget/GAAP

1) GENERAL GOVERNMENT = 20,037.50

2) PUBLIC WORKS = 4,325.00

1) Assigned2) Restricted-narrower than purpose of fund

1) Budget

2) Contract-purpose ofassessment 2) 3,000.00

STEP #3

(A) (B) (C) (D)

ALLOCATION TO MAJOR PURPOSE(S)LEVEL OF

CONSTRAINTSOURCE OF

CONSTRAINT

EXPENDITURE(S) OF RESTRICTED-

NARROWER THAN PURPOSE

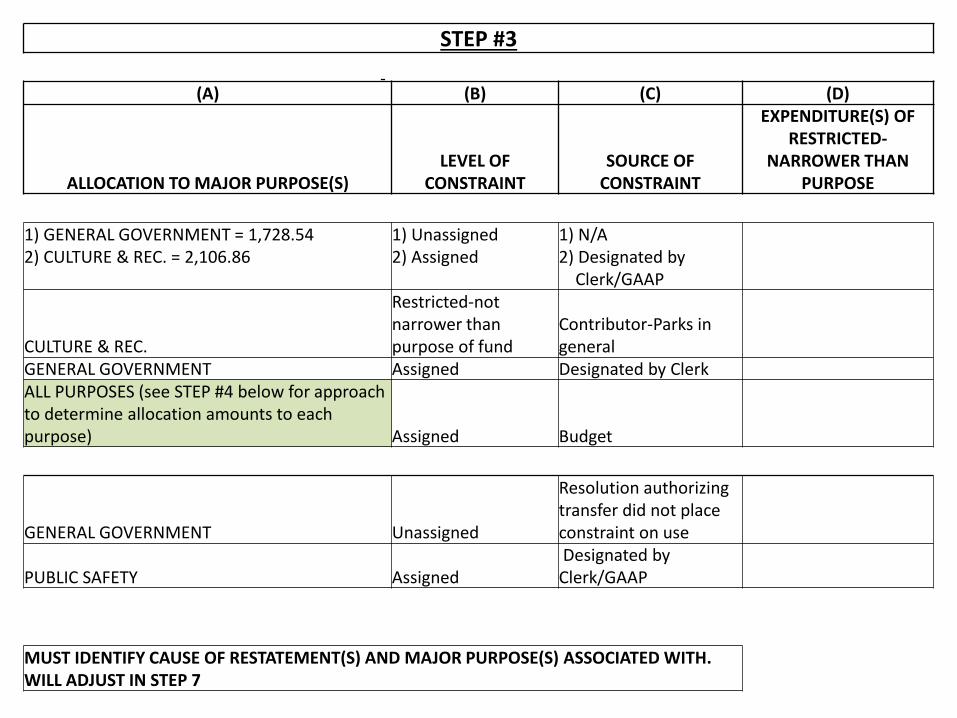

1) GENERAL GOVERNMENT = 1,728.542) CULTURE & REC. = 2,106.86

1) Unassigned2) Assigned

1) N/A2) Designated by

Clerk/GAAP

CULTURE & REC.

Restricted-not narrower than purpose of fund

Contributor-Parks in general

GENERAL GOVERNMENT Assigned Designated by ClerkALL PURPOSES (see STEP #4 below for approach to determine allocation amounts to each purpose) Assigned Budget

GENERAL GOVERNMENT Unassigned

Resolution authorizing transfer did not place constraint on use

PUBLIC SAFETY AssignedDesignated by Clerk/GAAP

MUST IDENTIFY CAUSE OF RESTATEMENT(S) AND MAJOR PURPOSE(S) ASSOCIATED WITH. WILL ADJUST IN STEP 7

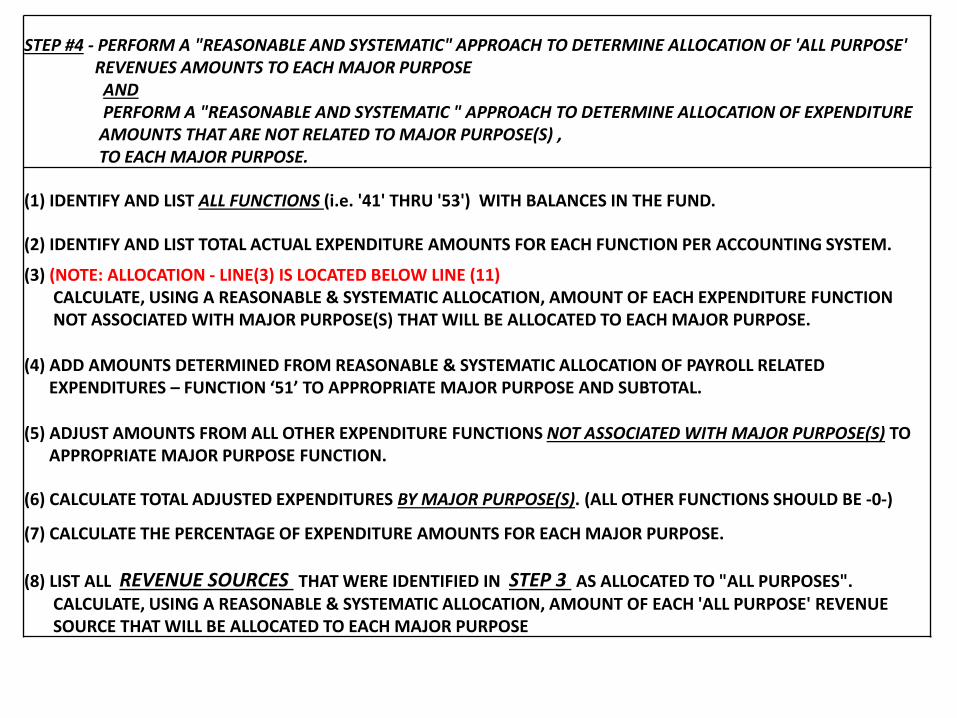

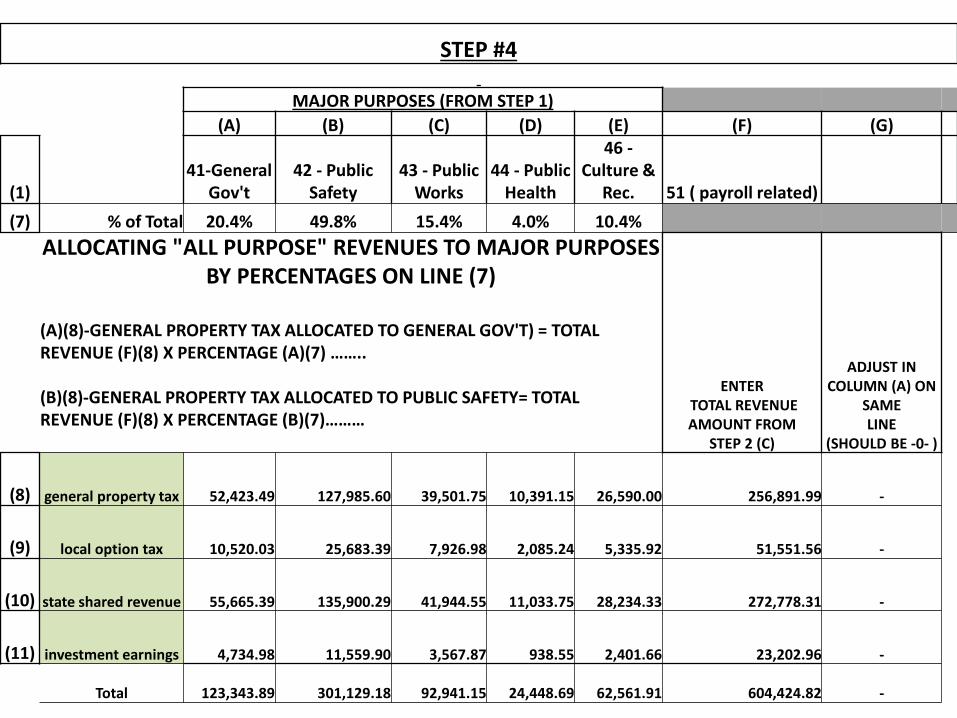

STEP #4 - PERFORM A "REASONABLE AND SYSTEMATIC" APPROACH TO DETERMINE ALLOCATION OF 'ALL PURPOSE' REVENUES AMOUNTS TO EACH MAJOR PURPOSEANDPERFORM A "REASONABLE AND SYSTEMATIC " APPROACH TO DETERMINE ALLOCATION OF EXPENDITUREAMOUNTS THAT ARE NOT RELATED TO MAJOR PURPOSE(S) ,TO EACH MAJOR PURPOSE.

(1) IDENTIFY AND LIST ALL FUNCTIONS (i.e. '41' THRU '53') WITH BALANCES IN THE FUND.

(2) IDENTIFY AND LIST TOTAL ACTUAL EXPENDITURE AMOUNTS FOR EACH FUNCTION PER ACCOUNTING SYSTEM.

(3) (NOTE: ALLOCATION - LINE(3) IS LOCATED BELOW LINE (11)CALCULATE, USING A REASONABLE & SYSTEMATIC ALLOCATION, AMOUNT OF EACH EXPENDITURE FUNCTIONNOT ASSOCIATED WITH MAJOR PURPOSE(S) THAT WILL BE ALLOCATED TO EACH MAJOR PURPOSE.

(4) ADD AMOUNTS DETERMINED FROM REASONABLE & SYSTEMATIC ALLOCATION OF PAYROLL RELATEDEXPENDITURES – FUNCTION ‘51’ TO APPROPRIATE MAJOR PURPOSE AND SUBTOTAL.

(5) ADJUST AMOUNTS FROM ALL OTHER EXPENDITURE FUNCTIONS NOT ASSOCIATED WITH MAJOR PURPOSE(S) TOAPPROPRIATE MAJOR PURPOSE FUNCTION.

(6) CALCULATE TOTAL ADJUSTED EXPENDITURES BY MAJOR PURPOSE(S). (ALL OTHER FUNCTIONS SHOULD BE -0-)

(7) CALCULATE THE PERCENTAGE OF EXPENDITURE AMOUNTS FOR EACH MAJOR PURPOSE.

(8) LIST ALL REVENUE SOURCES THAT WERE IDENTIFIED IN STEP 3 AS ALLOCATED TO "ALL PURPOSES".CALCULATE, USING A REASONABLE & SYSTEMATIC ALLOCATION, AMOUNT OF EACH 'ALL PURPOSE' REVENUESOURCE THAT WILL BE ALLOCATED TO EACH MAJOR PURPOSE

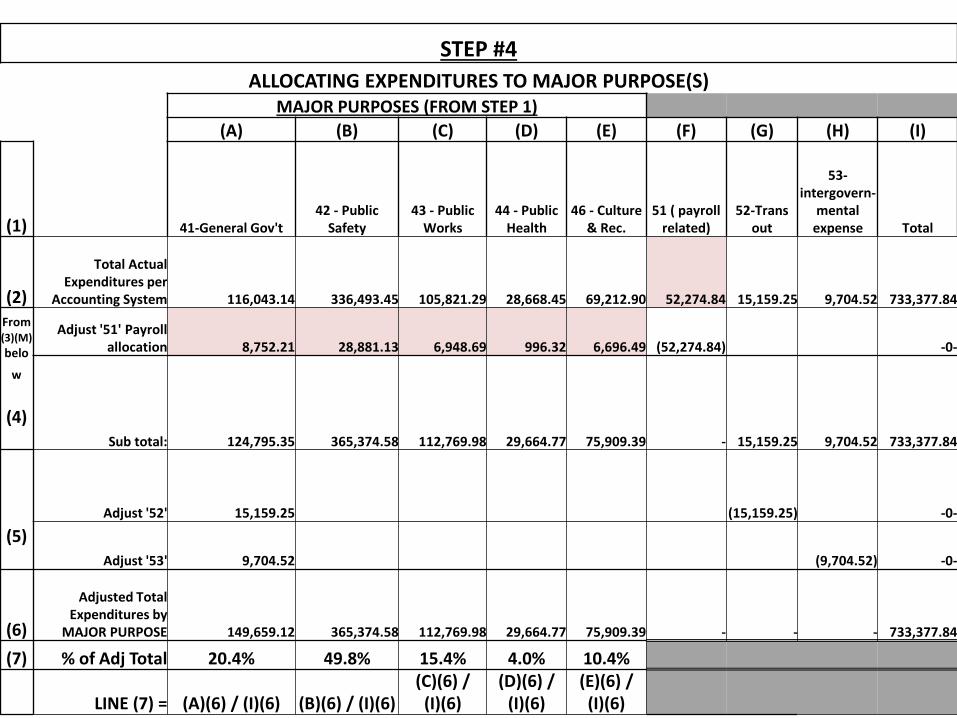

STEP #4ALLOCATING EXPENDITURES TO MAJOR PURPOSE(S)

MAJOR PURPOSES (FROM STEP 1)(A) (B) (C) (D) (E) (F) (G) (H) (I)

(1) 41-General Gov't42 - Public

Safety43 - Public

Works44 - Public

Health46 - Culture

& Rec.51 ( payroll

related)52-Trans

out

53-intergovern-

mental expense Total

(2)

Total Actual Expenditures per

Accounting System 116,043.14 336,493.45 105,821.29 28,668.45 69,212.90 52,274.84 15,159.25 9,704.52 733,377.84 From(3)(M) belo

w

(4)

Adjust '51' Payroll allocation 8,752.21 28,881.13 6,948.69 996.32 6,696.49 (52,274.84) -0-

Sub total: 124,795.35 365,374.58 112,769.98 29,664.77 75,909.39 - 15,159.25 9,704.52 733,377.84

(5)Adjust '52' 15,159.25 (15,159.25) -0-

Adjust '53' 9,704.52 (9,704.52) -0-

(6)

Adjusted Total Expenditures by

MAJOR PURPOSE 149,659.12 365,374.58 112,769.98 29,664.77 75,909.39 - - - 733,377.84

(7) % of Adj Total 20.4% 49.8% 15.4% 4.0% 10.4%

LINE (7) = (A)(6) / (I)(6) (B)(6) / (I)(6)(C)(6) /

(I)(6)(D)(6) /

(I)(6)(E)(6) / (I)(6)

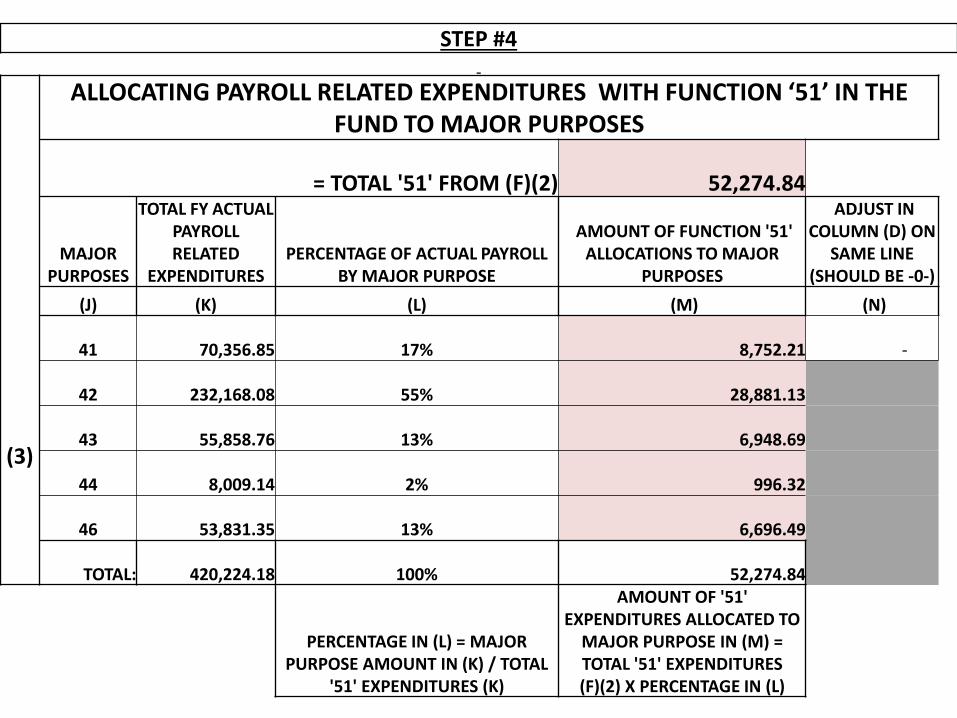

STEP #4

(3)

ALLOCATING PAYROLL RELATED EXPENDITURES WITH FUNCTION ‘51’ IN THE FUND TO MAJOR PURPOSES

= TOTAL '51' FROM (F)(2) 52,274.84

MAJOR PURPOSES

TOTAL FY ACTUAL PAYROLL RELATED

EXPENDITURESPERCENTAGE OF ACTUAL PAYROLL

BY MAJOR PURPOSE

AMOUNT OF FUNCTION '51' ALLOCATIONS TO MAJOR

PURPOSES

ADJUST IN COLUMN (D) ON

SAME LINE (SHOULD BE -0-)

(J) (K) (L) (M) (N)

41 70,356.85 17% 8,752.21 -

42 232,168.08 55% 28,881.13

43 55,858.76 13% 6,948.69

44 8,009.14 2% 996.32

46 53,831.35 13% 6,696.49

TOTAL: 420,224.18 100% 52,274.84

PERCENTAGE IN (L) = MAJOR PURPOSE AMOUNT IN (K) / TOTAL

'51' EXPENDITURES (K)

AMOUNT OF '51' EXPENDITURES ALLOCATED TO

MAJOR PURPOSE IN (M) = TOTAL '51' EXPENDITURES (F)(2) X PERCENTAGE IN (L)

STEP #4

MAJOR PURPOSES (FROM STEP 1)(A) (B) (C) (D) (E) (F) (G)

(1)41-General

Gov't42 - Public

Safety43 - Public

Works44 - Public

Health

46 -Culture &

Rec. 51 ( payroll related)(7) % of Total 20.4% 49.8% 15.4% 4.0% 10.4%

ALLOCATING "ALL PURPOSE" REVENUES TO MAJOR PURPOSES BY PERCENTAGES ON LINE (7)

(A)(8)-GENERAL PROPERTY TAX ALLOCATED TO GENERAL GOV'T) = TOTAL REVENUE (F)(8) X PERCENTAGE (A)(7) ……..

(B)(8)-GENERAL PROPERTY TAX ALLOCATED TO PUBLIC SAFETY= TOTALREVENUE (F)(8) X PERCENTAGE (B)(7)………

ENTERTOTAL REVENUE AMOUNT FROM

STEP 2 (C)

ADJUST IN COLUMN (A) ON

SAME LINE

(SHOULD BE -0- )

(8) general property tax 52,423.49 127,985.60 39,501.75 10,391.15 26,590.00 256,891.99 -

(9) local option tax 10,520.03 25,683.39 7,926.98 2,085.24 5,335.92 51,551.56 -

(10) state shared revenue 55,665.39 135,900.29 41,944.55 11,033.75 28,234.33 272,778.31 -

(11) investment earnings 4,734.98 11,559.90 3,567.87 938.55 2,401.66 23,202.96 -

Total 123,343.89 301,129.18 92,941.15 24,448.69 62,561.91 604,424.82 -

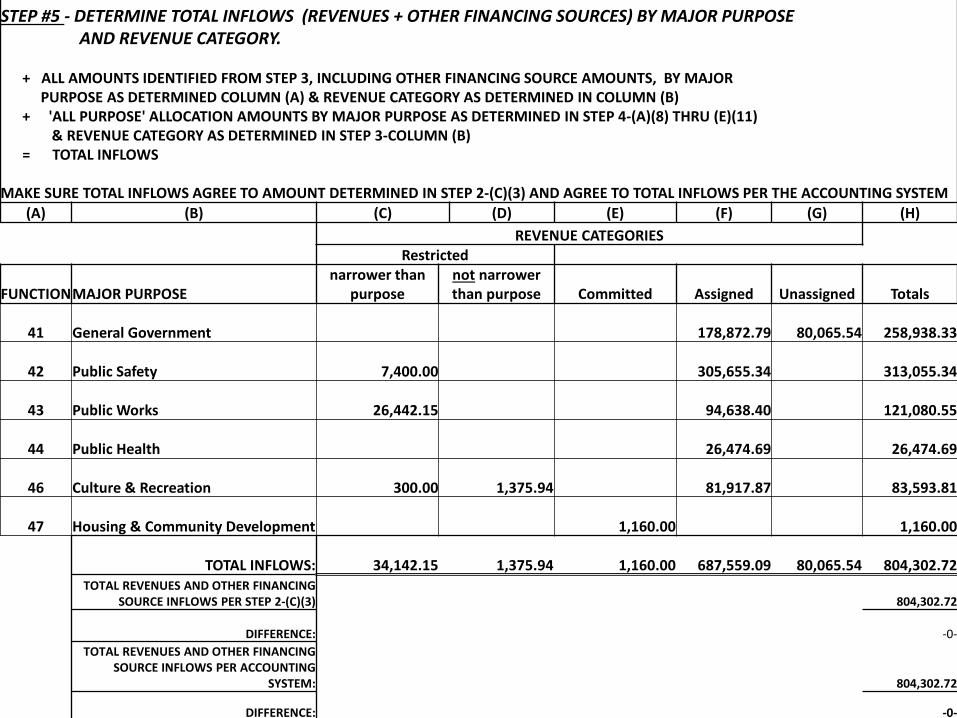

STEP #5 - DETERMINE TOTAL INFLOWS (REVENUES + OTHER FINANCING SOURCES) BY MAJOR PURPOSEAND REVENUE CATEGORY.

+ ALL AMOUNTS IDENTIFIED FROM STEP 3, INCLUDING OTHER FINANCING SOURCE AMOUNTS, BY MAJORPURPOSE AS DETERMINED COLUMN (A) & REVENUE CATEGORY AS DETERMINED IN COLUMN (B)

+ 'ALL PURPOSE' ALLOCATION AMOUNTS BY MAJOR PURPOSE AS DETERMINED IN STEP 4-(A)(8) THRU (E)(11) & REVENUE CATEGORY AS DETERMINED IN STEP 3-COLUMN (B)

= TOTAL INFLOWS

MAKE SURE TOTAL INFLOWS AGREE TO AMOUNT DETERMINED IN STEP 2-(C)(3) AND AGREE TO TOTAL INFLOWS PER THE ACCOUNTING SYSTEM(A) (B) (C) (D) (E) (F) (G) (H)

REVENUE CATEGORIESRestricted

FUNCTIONMAJOR PURPOSEnarrower than

purposenot narrower than purpose Committed Assigned Unassigned Totals

41 General Government 178,872.79 80,065.54 258,938.33

42 Public Safety 7,400.00 305,655.34 313,055.34

43 Public Works 26,442.15 94,638.40 121,080.55

44 Public Health 26,474.69 26,474.69

46 Culture & Recreation 300.00 1,375.94 81,917.87 83,593.81

47 Housing & Community Development 1,160.00 1,160.00

TOTAL INFLOWS: 34,142.15 1,375.94 1,160.00 687,559.09 80,065.54 804,302.72 TOTAL REVENUES AND OTHER FINANCING

SOURCE INFLOWS PER STEP 2-(C)(3) 804,302.72

DIFFERENCE: -0-TOTAL REVENUES AND OTHER FINANCING

SOURCE INFLOWS PER ACCOUNTING SYSTEM: 804,302.72

DIFFERENCE: -0-

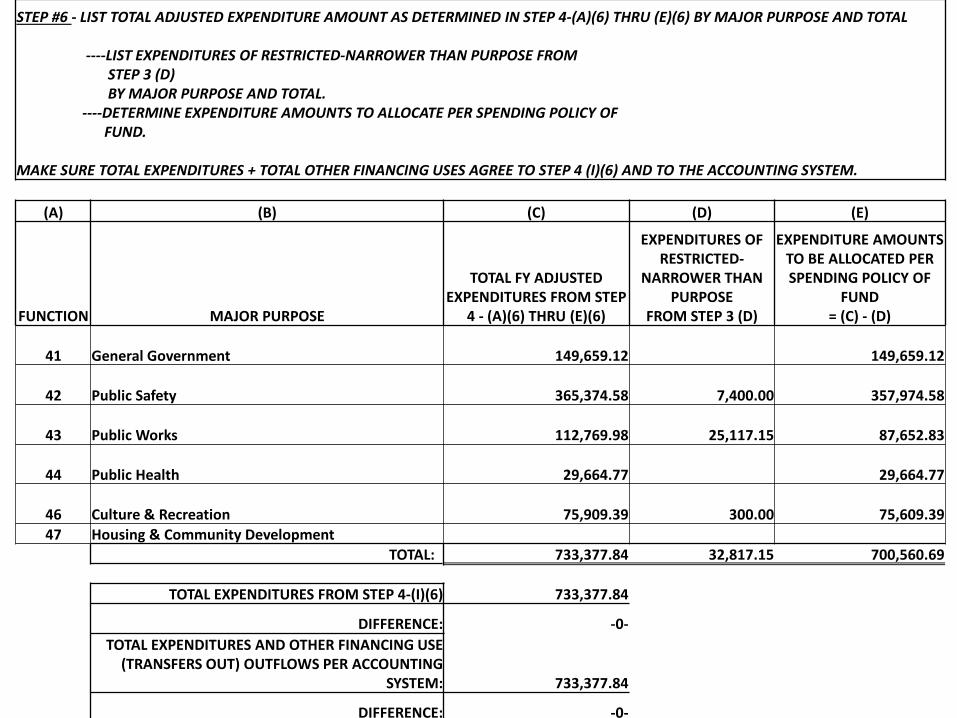

STEP #6 - LIST TOTAL ADJUSTED EXPENDITURE AMOUNT AS DETERMINED IN STEP 4-(A)(6) THRU (E)(6) BY MAJOR PURPOSE AND TOTAL

----LIST EXPENDITURES OF RESTRICTED-NARROWER THAN PURPOSE FROM STEP 3 (D)BY MAJOR PURPOSE AND TOTAL.

----DETERMINE EXPENDITURE AMOUNTS TO ALLOCATE PER SPENDING POLICY OFFUND.

MAKE SURE TOTAL EXPENDITURES + TOTAL OTHER FINANCING USES AGREE TO STEP 4 (I)(6) AND TO THE ACCOUNTING SYSTEM.

(A) (B) (C) (D) (E)

FUNCTION MAJOR PURPOSE

TOTAL FY ADJUSTED EXPENDITURES FROM STEP

4 - (A)(6) THRU (E)(6)

EXPENDITURES OF RESTRICTED-

NARROWER THAN PURPOSE

FROM STEP 3 (D)

EXPENDITURE AMOUNTS TO BE ALLOCATED PER SPENDING POLICY OF

FUND= (C) - (D)

41 General Government 149,659.12 149,659.12

42 Public Safety 365,374.58 7,400.00 357,974.58

43 Public Works 112,769.98 25,117.15 87,652.83

44 Public Health 29,664.77 29,664.77

46 Culture & Recreation 75,909.39 300.00 75,609.39 47 Housing & Community Development

TOTAL: 733,377.84 32,817.15 700,560.69

TOTAL EXPENDITURES FROM STEP 4-(I)(6) 733,377.84

DIFFERENCE: -0-TOTAL EXPENDITURES AND OTHER FINANCING USE

(TRANSFERS OUT) OUTFLOWS PER ACCOUNTING SYSTEM: 733,377.84

DIFFERENCE: -0-

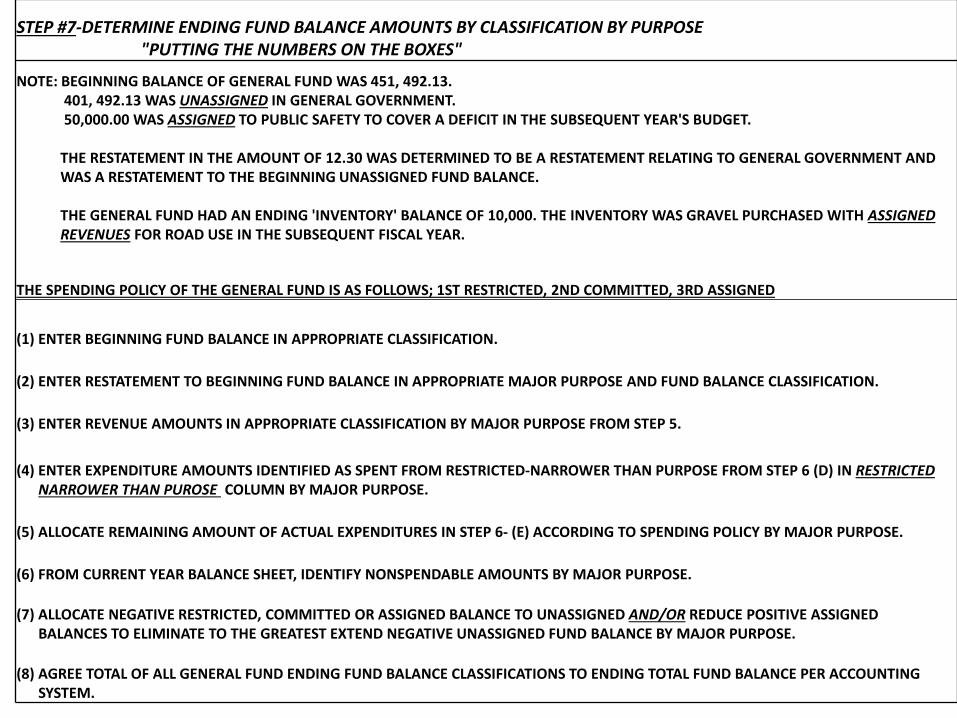

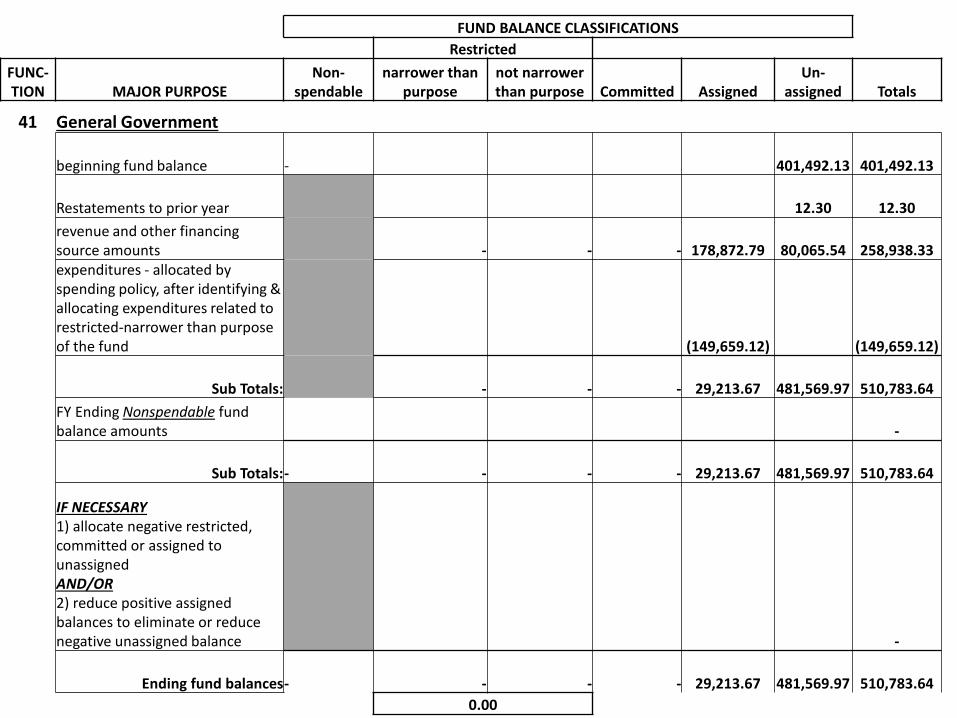

STEP #7-DETERMINE ENDING FUND BALANCE AMOUNTS BY CLASSIFICATION BY PURPOSE"PUTTING THE NUMBERS ON THE BOXES"

NOTE: BEGINNING BALANCE OF GENERAL FUND WAS 451, 492.13. 401, 492.13 WAS UNASSIGNED IN GENERAL GOVERNMENT.50,000.00 WAS ASSIGNED TO PUBLIC SAFETY TO COVER A DEFICIT IN THE SUBSEQUENT YEAR'S BUDGET.

THE RESTATEMENT IN THE AMOUNT OF 12.30 WAS DETERMINED TO BE A RESTATEMENT RELATING TO GENERAL GOVERNMENT ANDWAS A RESTATEMENT TO THE BEGINNING UNASSIGNED FUND BALANCE.

THE GENERAL FUND HAD AN ENDING 'INVENTORY' BALANCE OF 10,000. THE INVENTORY WAS GRAVEL PURCHASED WITH ASSIGNEDREVENUES FOR ROAD USE IN THE SUBSEQUENT FISCAL YEAR.

THE SPENDING POLICY OF THE GENERAL FUND IS AS FOLLOWS; 1ST RESTRICTED, 2ND COMMITTED, 3RD ASSIGNED

(1) ENTER BEGINNING FUND BALANCE IN APPROPRIATE CLASSIFICATION.

(2) ENTER RESTATEMENT TO BEGINNING FUND BALANCE IN APPROPRIATE MAJOR PURPOSE AND FUND BALANCE CLASSIFICATION.

(3) ENTER REVENUE AMOUNTS IN APPROPRIATE CLASSIFICATION BY MAJOR PURPOSE FROM STEP 5.

(4) ENTER EXPENDITURE AMOUNTS IDENTIFIED AS SPENT FROM RESTRICTED-NARROWER THAN PURPOSE FROM STEP 6 (D) IN RESTRICTEDNARROWER THAN PUROSE COLUMN BY MAJOR PURPOSE.

(5) ALLOCATE REMAINING AMOUNT OF ACTUAL EXPENDITURES IN STEP 6- (E) ACCORDING TO SPENDING POLICY BY MAJOR PURPOSE.

(6) FROM CURRENT YEAR BALANCE SHEET, IDENTIFY NONSPENDABLE AMOUNTS BY MAJOR PURPOSE.

(7) ALLOCATE NEGATIVE RESTRICTED, COMMITTED OR ASSIGNED BALANCE TO UNASSIGNED AND/OR REDUCE POSITIVE ASSIGNEDBALANCES TO ELIMINATE TO THE GREATEST EXTEND NEGATIVE UNASSIGNED FUND BALANCE BY MAJOR PURPOSE.

(8) AGREE TOTAL OF ALL GENERAL FUND ENDING FUND BALANCE CLASSIFICATIONS TO ENDING TOTAL FUND BALANCE PER ACCOUNTINGSYSTEM.

FUND BALANCE CLASSIFICATIONSRestricted

FUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned

Un-assigned Totals

41 General Government

beginning fund balance - 401,492.13 401,492.13

Restatements to prior year 12.30 12.30 revenue and other financing source amounts - - - 178,872.79 80,065.54 258,938.33 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund (149,659.12) (149,659.12)

Sub Totals: - - - 29,213.67 481,569.97 510,783.64 FY Ending Nonspendable fund balance amounts -

Sub Totals:- - - - 29,213.67 481,569.97 510,783.64

IF NECESSARY1) allocate negative restricted, committed or assigned to unassignedAND/OR2) reduce positive assigned balances to eliminate or reduce negative unassigned balance -

Ending fund balances- - - - 29,213.67 481,569.97 510,783.64 0.00

FUND BALANCE CLASSIFICATIONS

RestrictedFUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned

Un-assigned Totals

42 Public Safety

beginning fund balance - 50,000.00 50,000.00

Restatements to prior year -revenue and other financing source amounts 7,400.00 - - 305,655.34 - 313,055.34 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund (7,400.00) (357,974.58) (365,374.58)

Sub Totals - - - (2,319.24) - (2,319.24)FY Ending Nonspendable fund balance amounts - -

Sub Totals:- - - - (2,319.24) - (2,319.24)

IF NECESSARY1) allocate negative restricted, committed or assigned to unassignedAND/OR2) reduce positive assigned balances to eliminate or reduce negative unassigned balance 2,319.24 (2,319.24) -

Ending fund balances- - - - (0.00) (2,319.24) (2,319.24)0.00

FUND BALANCE CLASSIFICATIONS

RestrictedFUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned

Un-assigned Totals

43 Public Works

beginning fund balance -

Restatements to prior year -revenue and other financing source amounts 26,442.15 - - 94,638.40 - 121,080.55 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund (25,117.15) (87,652.83) (112,769.98)

Sub Totals 1,325.00 - - 6,985.57 - 8,310.57 FY Ending Nonspendable fund balance amounts 10,000.00 (10,000.00) -

Sub Totals: 10,000.00 1,325.00 - - (3,014.43) - 8,310.57

IF NECESSARY1) allocate negative restricted, committed or assigned to unassignedAND/OR2) reduce positive assigned balances to eliminate or reduce negative unassigned balance 3,014.43 (3,014.43) -

Ending fund balances 10,000.00 1,325.00 - - 0.00 (3,014.43) 8,310.57 1,325.00

FUND BALANCE CLASSIFICATIONS

RestrictedFUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned

Un-assigned Totals

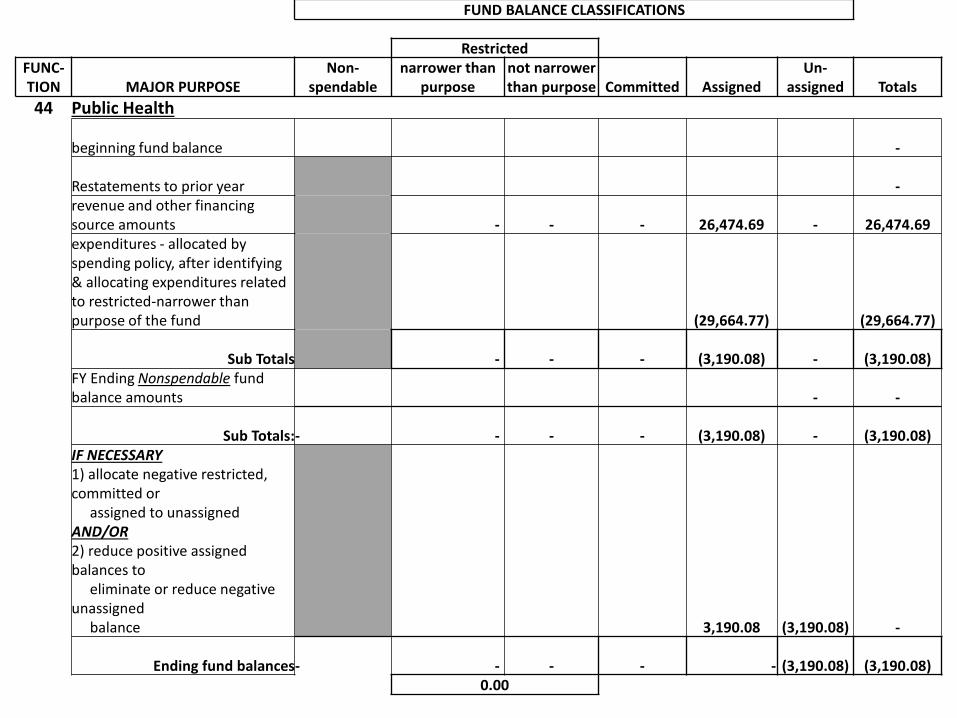

44 Public Health

beginning fund balance -

Restatements to prior year -revenue and other financing source amounts - - - 26,474.69 - 26,474.69 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund (29,664.77) (29,664.77)

Sub Totals - - - (3,190.08) - (3,190.08)FY Ending Nonspendable fund balance amounts - -

Sub Totals:- - - - (3,190.08) - (3,190.08)IF NECESSARY1) allocate negative restricted, committed or

assigned to unassignedAND/OR2) reduce positive assigned balances to

eliminate or reduce negative unassigned

balance 3,190.08 (3,190.08) -

Ending fund balances- - - - - (3,190.08) (3,190.08)0.00

FUND BALANCE CLASSIFICATIONS

RestrictedFUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned

Un-assigned Totals

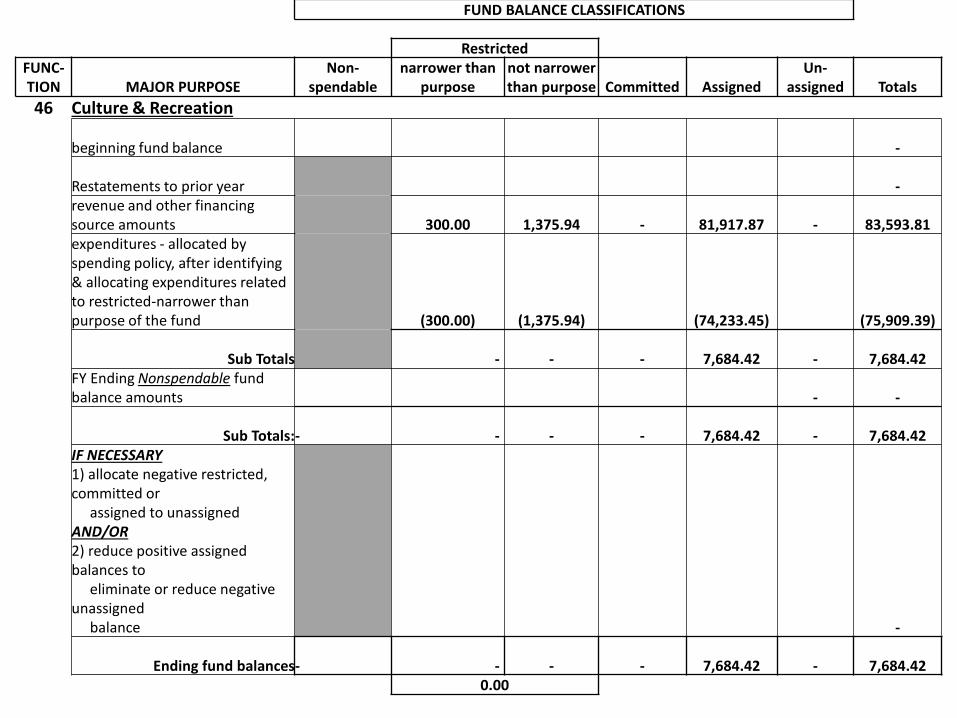

46 Culture & Recreation

beginning fund balance -

Restatements to prior year -revenue and other financing source amounts 300.00 1,375.94 - 81,917.87 - 83,593.81 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund (300.00) (1,375.94) (74,233.45) (75,909.39)

Sub Totals - - - 7,684.42 - 7,684.42 FY Ending Nonspendable fund balance amounts - -

Sub Totals:- - - - 7,684.42 - 7,684.42 IF NECESSARY1) allocate negative restricted, committed or

assigned to unassignedAND/OR2) reduce positive assigned balances to

eliminate or reduce negative unassigned

balance -

Ending fund balances- - - - 7,684.42 - 7,684.42 0.00

FUND BALANCE CLASSIFICATIONS

RestrictedFUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned

Un-assigned Totals

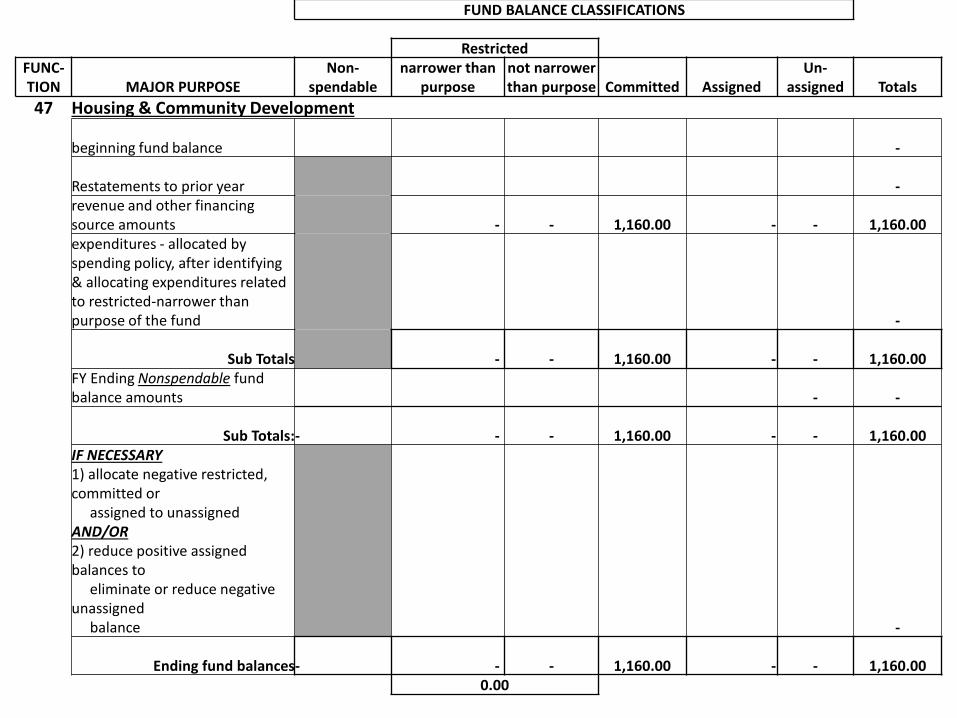

47 Housing & Community Development

beginning fund balance -

Restatements to prior year -revenue and other financing source amounts - - 1,160.00 - - 1,160.00 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund -

Sub Totals - - 1,160.00 - - 1,160.00 FY Ending Nonspendable fund balance amounts - -

Sub Totals:- - - 1,160.00 - - 1,160.00 IF NECESSARY1) allocate negative restricted, committed or

assigned to unassignedAND/OR2) reduce positive assigned balances to

eliminate or reduce negative unassigned

balance -

Ending fund balances- - - 1,160.00 - - 1,160.00 0.00

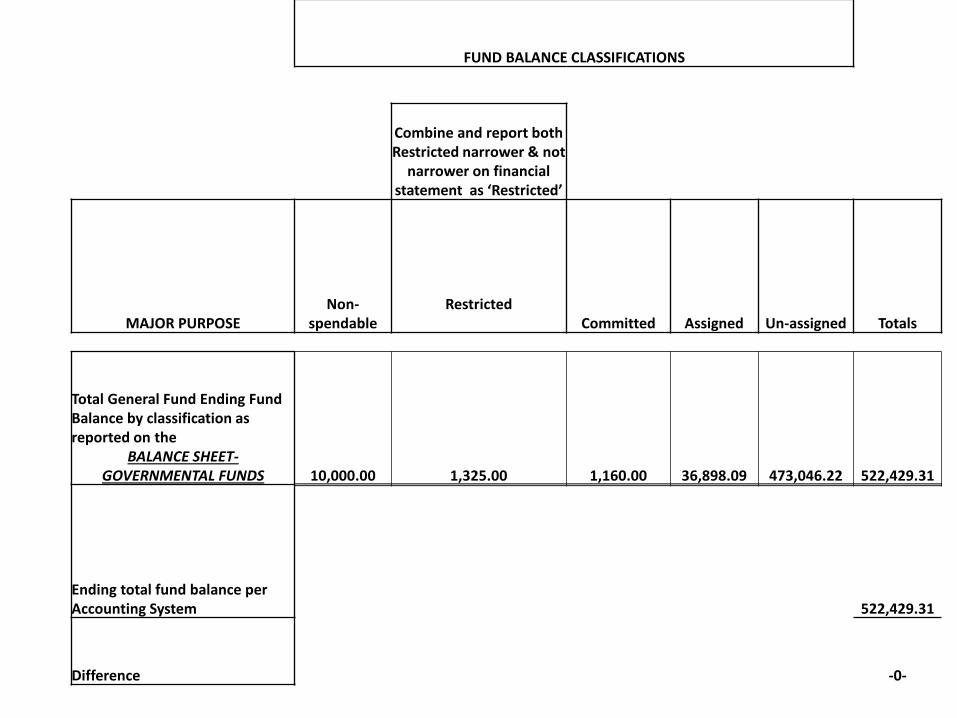

FUND BALANCE CLASSIFICATIONS

Combine and report both Restricted narrower & not

narrower on financial statement as ‘Restricted’

MAJOR PURPOSENon-

spendableRestricted

Committed Assigned Un-assigned Totals

Total General Fund Ending Fund Balance by classification as reported on the

BALANCE SHEET-GOVERNMENTAL FUNDS 10,000.00 1,325.00 1,160.00 36,898.09 473,046.22 522,429.31

Ending total fund balance per Accounting System 522,429.31

Difference -0-

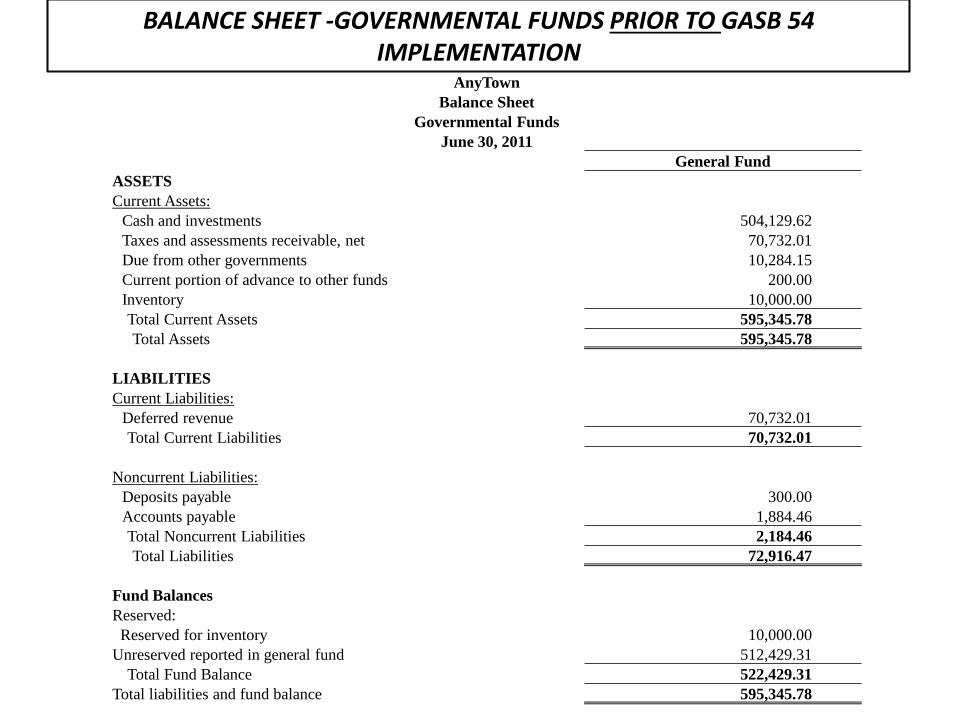

BALANCE SHEET -GOVERNMENTAL FUNDS PRIOR TO GASB 54 IMPLEMENTATION

AnyTownBalance Sheet

Governmental FundsJune 30, 2011

General FundASSETSCurrent Assets:

Cash and investments 504,129.62 Taxes and assessments receivable, net 70,732.01 Due from other governments 10,284.15 Current portion of advance to other funds 200.00 Inventory 10,000.00 Total Current Assets 595,345.78 Total Assets 595,345.78

LIABILITIESCurrent Liabilities:

Deferred revenue 70,732.01 Total Current Liabilities 70,732.01

Noncurrent Liabilities:Deposits payable 300.00 Accounts payable 1,884.46 Total Noncurrent Liabilities 2,184.46 Total Liabilities 72,916.47

Fund BalancesReserved:Reserved for inventory 10,000.00

Unreserved reported in general fund 512,429.31 Total Fund Balance 522,429.31

Total liabilities and fund balance 595,345.78

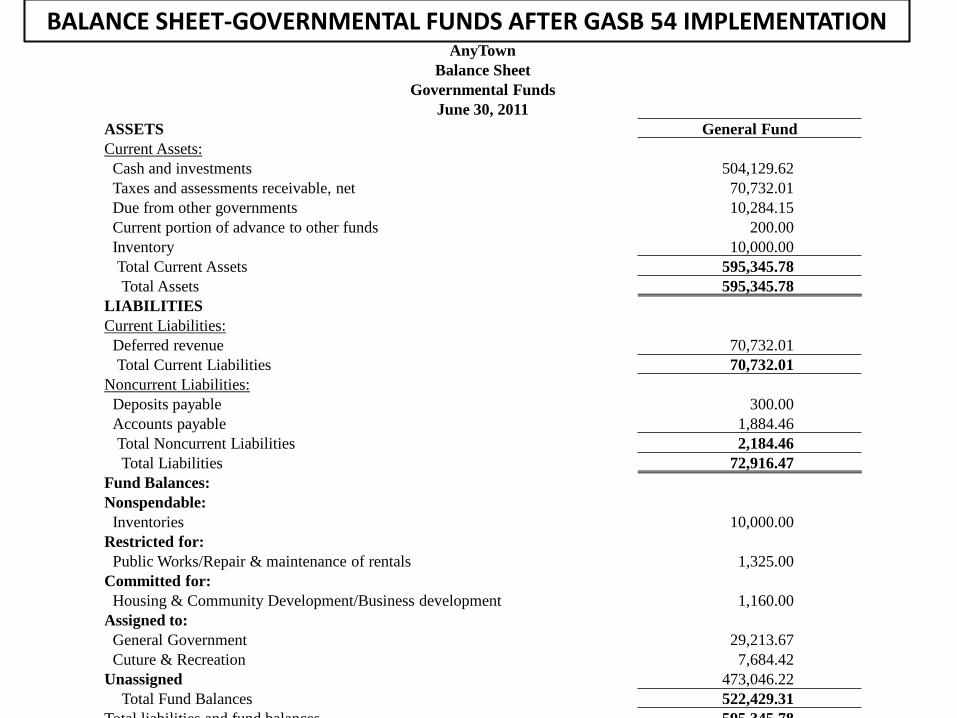

BALANCE SHEET-GOVERNMENTAL FUNDS AFTER GASB 54 IMPLEMENTATIONAnyTown

Balance SheetGovernmental Funds

June 30, 2011ASSETS General FundCurrent Assets:

Cash and investments 504,129.62 Taxes and assessments receivable, net 70,732.01 Due from other governments 10,284.15 Current portion of advance to other funds 200.00 Inventory 10,000.00 Total Current Assets 595,345.78 Total Assets 595,345.78

LIABILITIESCurrent Liabilities:

Deferred revenue 70,732.01 Total Current Liabilities 70,732.01

Noncurrent Liabilities:Deposits payable 300.00 Accounts payable 1,884.46 Total Noncurrent Liabilities 2,184.46 Total Liabilities 72,916.47

Fund Balances:Nonspendable:

Inventories 10,000.00 Restricted for:

Public Works/Repair & maintenance of rentals 1,325.00 Committed for:

Housing & Community Development/Business development 1,160.00 Assigned to:

General Government 29,213.67 Cuture & Recreation 7,684.42

Unassigned 473,046.22 Total Fund Balances 522,429.31

Total liabilities and fund balances 595 345 78

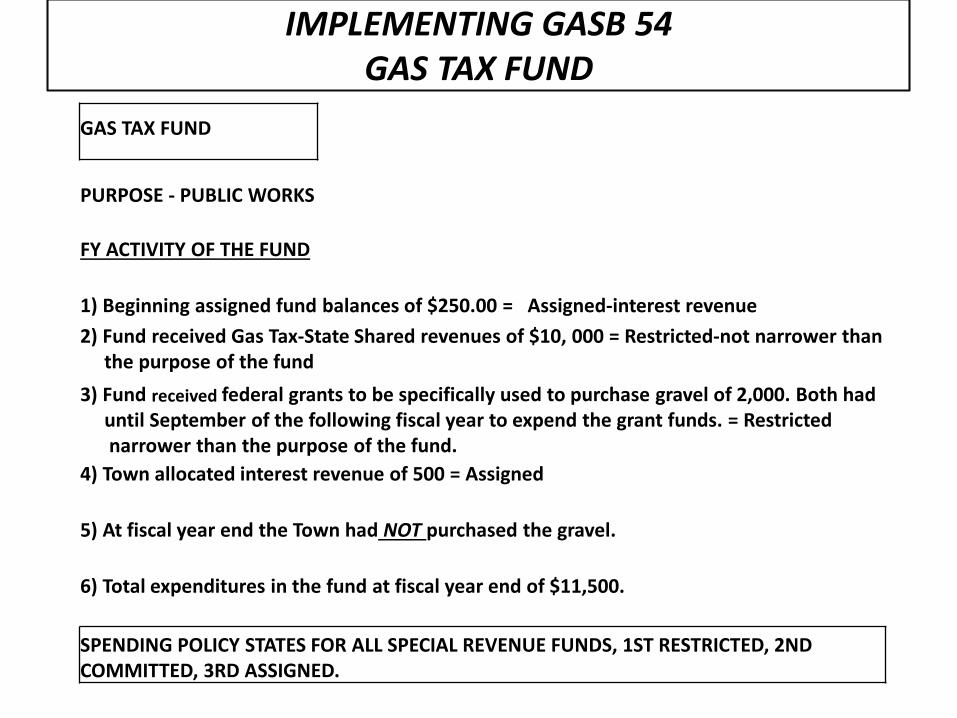

IMPLEMENTING GASB 54GAS TAX FUND

GAS TAX FUND

PURPOSE - PUBLIC WORKS

FY ACTIVITY OF THE FUND

1) Beginning assigned fund balances of $250.00 = Assigned-interest revenue2) Fund received Gas Tax-State Shared revenues of $10, 000 = Restricted-not narrower than

the purpose of the fund3) Fund received federal grants to be specifically used to purchase gravel of 2,000. Both had

until September of the following fiscal year to expend the grant funds. = Restrictednarrower than the purpose of the fund.

4) Town allocated interest revenue of 500 = Assigned

5) At fiscal year end the Town had NOT purchased the gravel.

6) Total expenditures in the fund at fiscal year end of $11,500.

SPENDING POLICY STATES FOR ALL SPECIAL REVENUE FUNDS, 1ST RESTRICTED, 2ND COMMITTED, 3RD ASSIGNED.

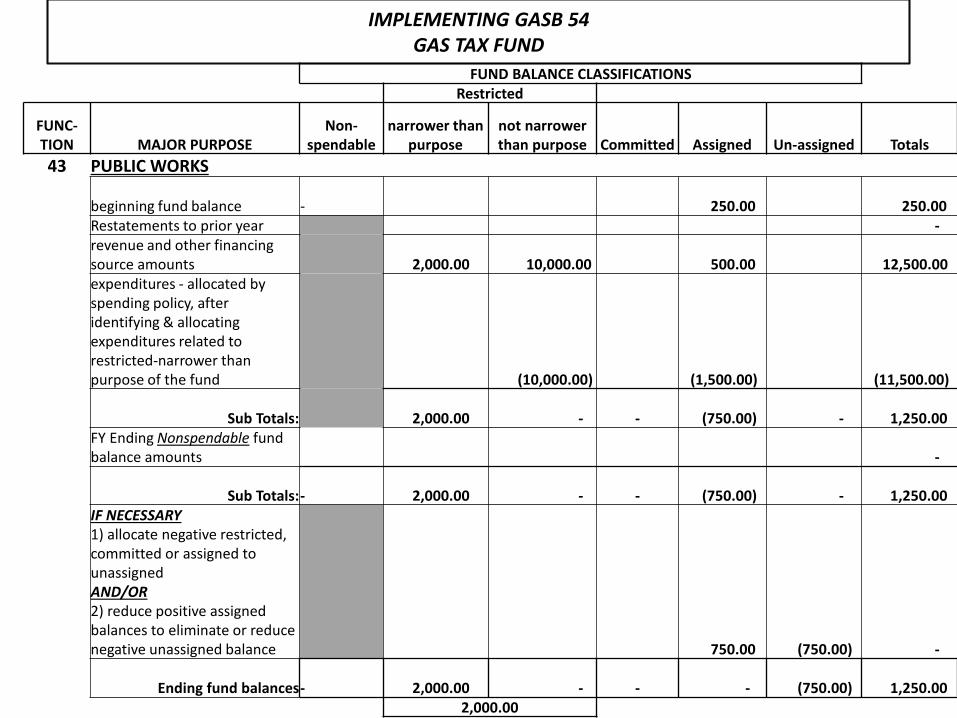

IMPLEMENTING GASB 54GAS TAX FUND

FUND BALANCE CLASSIFICATIONSRestricted

FUNC-TION MAJOR PURPOSE

Non-spendable

narrower than purpose

not narrower than purpose Committed Assigned Un-assigned Totals

43 PUBLIC WORKS

beginning fund balance - 250.00 250.00 Restatements to prior year -revenue and other financing source amounts 2,000.00 10,000.00 500.00 12,500.00 expenditures - allocated by spending policy, after identifying & allocating expenditures related to restricted-narrower than purpose of the fund (10,000.00) (1,500.00) (11,500.00)

Sub Totals: 2,000.00 - - (750.00) - 1,250.00 FY Ending Nonspendable fund balance amounts -

Sub Totals:- 2,000.00 - - (750.00) - 1,250.00 IF NECESSARY1) allocate negative restricted, committed or assigned to unassignedAND/OR2) reduce positive assigned balances to eliminate or reduce negative unassigned balance 750.00 (750.00) -

Ending fund balances- 2,000.00 - - - (750.00) 1,250.00 2,000.00

FYI

With the consolidation of our State vendor files we have been eliminating the vendor ID’s for counties, other than the Treasurer, because under 17-8-311, MCA all payments to “any city, town, county or local government entity mustbe payable to the finance officer of the appropriate city, town or county”.

The finance officer is defined as the “county treasurer, city treasurer, town clerk, or the equivalent provided in Title 7, chapter 3”.

? QUESTIONS ?