Embed Size (px)

Citation preview

FSA Notices (and statements re firms, individuals) - 2012

Click for bookmarks below

Major compliance issues/TCF - insurance firms

Major compliance issues/TCF- banks/building societies/investment firms (inc IFAs)

Major compliance issues/TCF - mortgage firms

Individuals - fitness and properness issues - bans/censures/refusals

Market abuse/market conduct/financial crime

General statements on firms and individuals

2

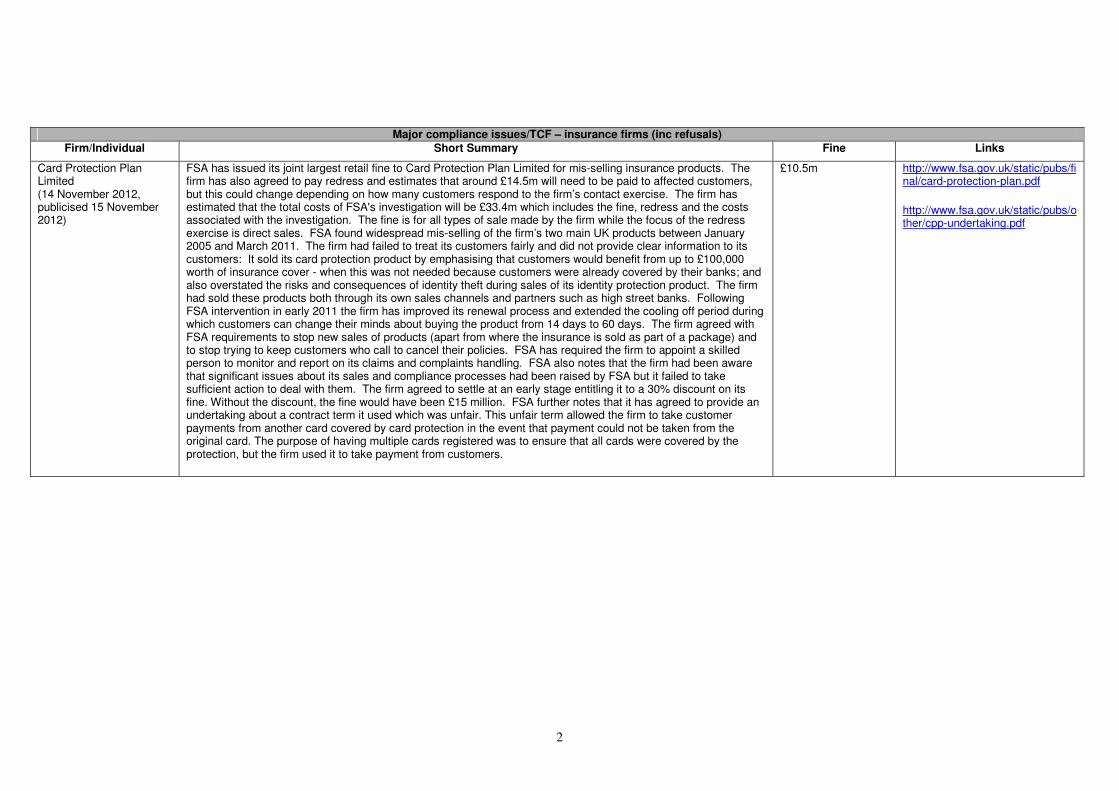

Major compliance issues/TCF – insurance firms (inc refusals)

Firm/Individual Short Summary Fine Links

Card Protection Plan Limited (14 November 2012, publicised 15 November 2012)

FSA has issued its joint largest retail fine to Card Protection Plan Limited for mis-selling insurance products. The firm has also agreed to pay redress and estimates that around £14.5m will need to be paid to affected customers, but this could change depending on how many customers respond to the firm’s contact exercise. The firm has estimated that the total costs of FSA's investigation will be £33.4m which includes the fine, redress and the costs associated with the investigation. The fine is for all types of sale made by the firm while the focus of the redress exercise is direct sales. FSA found widespread mis-selling of the firm’s two main UK products between January 2005 and March 2011. The firm had failed to treat its customers fairly and did not provide clear information to its customers: It sold its card protection product by emphasising that customers would benefit from up to £100,000 worth of insurance cover - when this was not needed because customers were already covered by their banks; and also overstated the risks and consequences of identity theft during sales of its identity protection product. The firm had sold these products both through its own sales channels and partners such as high street banks. Following FSA intervention in early 2011 the firm has improved its renewal process and extended the cooling off period during which customers can change their minds about buying the product from 14 days to 60 days. The firm agreed with FSA requirements to stop new sales of products (apart from where the insurance is sold as part of a package) and to stop trying to keep customers who call to cancel their policies. FSA has required the firm to appoint a skilled person to monitor and report on its claims and complaints handling. FSA also notes that the firm had been aware that significant issues about its sales and compliance processes had been raised by FSA but it failed to take sufficient action to deal with them. The firm agreed to settle at an early stage entitling it to a 30% discount on its fine. Without the discount, the fine would have been £15 million. FSA further notes that it has agreed to provide an undertaking about a contract term it used which was unfair. This unfair term allowed the firm to take customer payments from another card covered by card protection in the event that payment could not be taken from the original card. The purpose of having multiple cards registered was to ensure that all cards were covered by the protection, but the firm used it to take payment from customers.

£10.5m http://www.fsa.gov.uk/static/pubs/final/card-protection-plan.pdf

http://www.fsa.gov.uk/static/pubs/other/cpp-undertaking.pdf

3

Major compliance issues/TCF – insurance firms (inc refusals) Firm/Individual Short Summary Fine Links

HD Administrators LLP (22/28 March 2012)

By this First Supervisory Notice, FSA has decided to vary with immediate effect, the firm’s Part IV permission by imposing a requirement that it may not carry on any regulated activities, prohibits the firm from releasing, disposing of or otherwise dealing with any of its assets so long as the requirement is in force; and imposes a requirement on the firm’s Part IV permission the firm shall, through its officers and staff (whether acting on behalf of the firm or on behalf of any other entity), procure that assets held in accounts its wholly owned subsidiary, HD Trustees Limited, comprising pension scheme fund assets at any institution may not, so long as the requirement is in force, be released. FSA notes concerns that the firm’s two approved persons do not appear to be fit and proper. One has been arrested on suspicion of fraud in relation to Arck LLP, an unauthorised firm at which she is one of two managing members and the police have discovered prima facie physical evidence at her property which FSA considers is likely to give rise to allegations of attempted falsification of documentation; Arck is LLP currently in provisional liquidation as a result of a successful civil action by investors. In bringing injunctive proceedings, investors in Arck (some of whom invested through the firm and the personal pension scheme allege the firm has misappropriated their funds and then misrepresented the financial position of the firm through the provision of forged bank statements via this individual and the second managing member of Arck. Both are also directors of HD Trustees Limited. It is alleged that the individual failed adequately and regularly to calculate the value of assets held within the firm’s personal pension scheme. This may have resulted in significant overpayments being made to customers with the consequence that such customers may incur subsequent unauthorised payment or tax charges when taking their pension benefits in breach of tax and/or pension legislation. The other approved person informed FSA that she was unaware that she was approved to perform a controlled function at the firm, saying she could not adequately explain how a SIPP operated and did not understand her regulatory responsibilities, adding that she acted purely as an administrator. FSA also believes the firm has breached Principle 10, CASS 7.6R and 7.8.1R and s20 FSMA. Subsequently, on 28 March 2012 FSA reported on this action and published details of what this meant for both SIPP members and investors in Arck LLP.

http://www.fsa.gov.uk/static/pubs/final/hd-administrators-llp.pdf http://www.fsa.gov.uk/consumerinformation/firmnews/2012/hd-sipp

Mitsui Sumitomo Insurance Company (Europe) Ltd/Kumagai, Yohichi (8 May 2012)

FSA has fined the firm £3,345,000 for serious corporate governance failings, and imposed a prohibition order and fine of £119,303 on its former executive chairman, Yohichi Kumagai. FSA notes that, despite receiving clear guidance from the regulator, hat the management structure and composition of the board was ineffective, Yohichi Kumagai failed to take prompt action to remedy the situation. The firm was described as having significant failings in corporate governance and control arrangements which resulted in it being poorly organised and managed across its business as a whole.

See main text http://www.fsa.gov.uk/static/pubs/final/msicel.pdf http://www.fsa.gov.uk/static/pubs/final/yohichi-kumagai.pdf

Sun Life Assurance Company of Canada (UK) Limited (18 October 2012

FSA has fined the firm for failings in the governance of its with-profits business. The firm’s governance failings came to light following two significant transactions it executed in 2008 and 2009. These transactions impacted upon one of the firm’s with-profits funds, holding approximately 114,000 policies and £1.2bon in assets. The firm’s with-profits committee failed to adequately review these transactions, while its board of directors did not approve the transactions. It is noted that FSA has not criticised the merits of these two transactions, but has found that the review and approval process followed by the firm was deficient which led to an unacceptable risk that proper independent judgement would not be applied to the transactions. The firm would have been fined £750,000, but agreed to settle and thus qualified for a 20% (Stage 2) discount.

£600,000 http://www.fsa.gov.uk/static/pubs/final/slocuk.pdf

4

Major compliance issues/TCF – insurance firms (inc refusals) Firm/Individual Short Summary Fine Links

UK Car Group Limited (26 January 2012, publicised May 2012)

FSA has fined the firm for the failings of its appointed representative, CC Automotive Limited - trading as Carcraft - in respect of the monitoring of PP) sales. By failing to deal appropriately with concerns raised in internal audits regarding the sales of PPI by Carcraft, the firm failed to take reasonable steps to ensure the suitability of advice given to customers. While the firm’s sales model and standard documentation were sound and the way the audit system was established was robust, FSA notes that Carcraft’s own internal audits raised clear and detailed concerns with the firm about the way PPI was being sold. The firm took a number of steps to address issues raised in the audits, such as giving advisers one on one feedback and training following an audit. However Carcraft continued to fail to record in a sufficiently detailed fashion the advice provided to its customers. More generally concerns were also raised with regard to staff competence, monitoring of individual advisers and provision of completed documentation to consumers. The firm agreed to settle the case at an early stage of the investigation so qualified for a 30% discount. It is noted that the firm ceased PPI sales in 2010 and has paid redress where appropriate.

£91,000 http://www.fsa.gov.uk/static/pubs/final/uk-car-group.pdf

UK Insurance Limited (17 January 2012, publicised 18 January 2012)

FSA has imposed a fine for failings by Direct Line Insurance Plc and Churchill Insurance Company Limited to prevent files that FSA had requested from being improperly altered. While the fine relates specifically to failings by the firms, since the breach occurred the relevant business and liabilities of the firms have been transferred to UK Insurance Limited, which is owned by the Royal Bank of Scotland Group, which is therefore responsible for paying the fine. FSA reports that, of 50 complaint files requested by FSA for review, 27 were altered improperly before they were submitted because the firms failed to act with due skill, care and diligence. The majority of the alterations were minor in nature and none of the changes resulted in any customer detriment.

£2,170,000 http://www.fsa.gov.uk/pubs/final/uk-insurance.pdf

5

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Arch Financial Products LLP/ Farrell, Robin/ Addison, Robert (publicised 18 December 2012)

FSA has published Decision Notices in respect of the firm and its former CEO and former senior partner/compliance officer at the firm. The individuals have referred the matters to the Upper Tribunal. The Decision Notices set out that FSA has decided to prohibit Robin Farrell and Robert Addison from performing any role in regulated financial services, to fine them £650,000 and £200,000 respectively and issue a public censure against the firm – it is noted that FSA would have fined the firm £9m for its misconduct, were it not for the firm’s financial position. The firm was the investment manager of the CF Arch cru Funds and FSA alleges that it was reckless as to the risk that conflicts of interest would not be managed fairly, noting that in one transaction the firm received a fee of £3m from Guernsey cells it set up which the firm did not disclose to the independent directors of the cells or record in any contemporaneous transaction documentation. In addition, FSA alleges that the firm pursued an investment strategy which resulted in significant liquidity risks for the funds. Further, FSA believes that the firm and Robin Farrell failed to ensure that the funds aimed to provide a prudent spread of risk by adopting an investment strategy of allocating a majority of the funds’ assets in the Guernsey cells for which there was a limited secondary market; the liquidity risks increased when the firm increased the funds’ investments in the Guernsey cells’ shares at a time of market turbulence and illiquidity, rather than retaining cash in the funds. In the circumstances, investors were exposed to the risk that the funds would not be able to liquidate their investments to meet redemption requests from investors. The funds were ultimately suspended in March 2009 as a result of liquidity concerns. FSA says that the firm and Robert Addison adopted an informal, ad hoc approach to compliance monitoring with insufficient recording of the monitoring that was undertaken. The press release notes that the individuals applied unsuccessfully to the Tribunal for an order preventing FSA from publishing the Decision Notices.

http://www.fsa.gov.uk/static/pubs/decisions/arch-financial-products.pdf

http://www.fsa.gov.uk/static/pubs/decisions/robin-farrell.pdf

http://www.fsa.gov.uk/static/pubs/decisions/robert-addison.pdf

Argentum-Lex Wealth Management Limited (15 November 2012)

Final Notice: FSA has cancelled the firm’s Part IV permission, noting that in July 2010, it had provided a formal undertaking to FSA, in which it agreed, amongst other things, that it would comply with requirements to pay any FOS awards made against its predecessor business Wynyard Asset Management Limited (Dissolved). The firm has failed to comply with an award made against this latter firm by FOS in June 2011, despite repeated requests by FOS and FSA that it do so.

http://www.fsa.gov.uk/static/pubs/final/argentum.pdf

Bank of Scotland plc (9 March 2012)

FSA has published a Final Notice detailing its findings in respect of failings of the firm, in relation to its Corporate Division (‘the division’) during the period January 2006 to December 2008, and has publicly censured the firm, saying that the failings warranted a fine, but it was decided that any such fine would impact taxpayers. FSA considers that during this period, the firm failed to comply with Principle 3, saying that “rather than re-evaluating its business as conditions worsened, the division set out to increase its market share as other lenders started to pull out of the market. In addition, its internal culture was focused on revenue rather than assessing the level of risk in transactions”. It points out deficiencies in the bank’s risks, controls and distribution frameworks. FSA notes that this announcement marks the conclusion of the enforcement action against the firm, but other enforcement proceedings in connection to the failure of HBOS are ongoing and remain subject to the legal processes prescribed by FSMA. It adds that it has committed to produce a public interest report into the causes of the failure of HBO, but to carry out work on an HBOS report at this time would risk legally prejudicing the outcome of ongoing enforcement action. The start date for work on the report will be determined by the progress of the enforcement action.

FSA publishes censure against Bank of Scotland plc in respect of failings within its Corporate Division between January 2006 and December 2008

http://www.fsa.gov.uk/static/pubs/final/bankofscotlandplc.pdf

6

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Bank of Scotland plc (19 October 2012)

FSA has fined the firm for failures in their systems which meant it held inaccurate mortgage records for 250,000 of its customers. This was the result of mortgage information being held on two separate unaligned systems, and problems with two further processes where manual updates were not always carried out. The effect was that the firm relied on incorrect records for considerable periods of time between 2004 and 2011. The issue first came to light when the firm put in place a programme to rectify the fact that some Halifax customers had received potentially confusing information about changes to their mortgage contracts, specifically relating to the standard variable rate. While monitoring a consumer forum website, the FSA found a number of customers complaining that they had been wrongly excluded from the programme and had not received goodwill payments. As well as excluding this group, the problem was compounded when the firm incorrectly contacted 33,700 customers who should never have been included in the programme, and mistakenly made goodwill payments totalling £20.4m to 22,700 of them

£4.2m http://www.fsa.gov.uk/static/pubs/final/bank-of-scotland.pdf

Barclays Bank plc (27 June 2012)

FSA has imposed its largest ever fine for misconduct relating to LIBOR and EURIBOR. The firm's misconduct included: making submissions which formed part of the LIBOR and EURIBOR setting process that took into account requests from Barclays’ interest rate derivatives traders. The firm failed to have adequate systems and controls in place relating to its LIBOR and EURIBOR submissions processes until June 2010 and failed to review its systems and controls at a number of appropriate points. It also failed to deal with issues relating to its LIBOR submissions when these were escalated to Barclays’ Investment Banking compliance function in 2007 and 2008. BBA is currently undertaking a review of the way LIBOR is set and will publish its findings shortly. It is noted that FSA, along with the other tripartite authorities, is working to support market-led reviews of existing arrangements, with the goal of ensuring such arrangements continue to command the confidence of all stakeholders. FSA also thanks CFTC, DoJ, FBI and SEC for their cooperation in this investigation, adding that CFT brought attempted manipulation and false reporting charges against Barclays for similar failings, which the bank agreed to settle. CFTC imposed a penalty of $200m. In addition, as part of an agreement with the DOJ, Barclays admitted to its misconduct and agreed to pay a penalty of $160m.

£59.5m Barclays fined £59.5 million for significant failings in relation to LIBOR and EURIBOR http://www.fsa.gov.uk/static/pubs/final/barclays-jun12.pdf

BlackRock Investment Management (UK) Limited (11 September 2012)

FSA has fined the firm for failing to protect client money adequately by not putting trust letters in place for certain money market deposits, and for failing to take reasonable care to organise and control its affairs responsibly in relation to the identification and protection of client money. Between 1 October 2006 and 31 March 2010, the firm failed to obtain such letters in relation to some of the money market deposits it placed with third party banks. The error occurred as a result of systems changes that followed on from BlackRock Group's acquisition of the firm, which had previously been known as Merrill Lynch Investment Managers Limited. These changes rendered BIM's procedures for setting up trust letters ineffective. The average daily balance affected by this failure was over £1.36bn. Had the firm become insolvent at any time during this period, clients would have suffered delay in securing the return of their funds and may not have recovered their money in full. FSA notes that, in determining the penalty it took into account that the misconduct was not deliberate, and that the firm reported the issue to FSA and has since remedied the situation and put in place robust systems and controls relating to client money protection. No clients suffered any losses as a result of the error. The firm agreed to settle with the FSA at an early stage and qualified for a 30% discount on the financial penalty.

£9,533,100 http://www.fsa.gov.uk/static/pubs/final/blackrock.pdf

7

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Capita Financial Managers Limited (13 November 2012)

FSA has issued a public censure against the firm for its failings in relation to the CF Arch cru funds between June 2006 and March 2009. The firm was the ACD of the CF Arch cru funds. In July 2006, the firm delegated the investment management of the funds to a third party, Arch Financial Products LLP (Arch). The funds were then invested indirectly in private finance and private equity assets. While the firm delegated the investment management of the funds to Arch, it remained responsible for the overall performance of the regulatory obligations in relation to the funds. The firm did not have sufficient processes in place to monitor Arch, even though Arch had not acted as an investment manager before and did not adequately identify and mitigate the conflicts of interest between Arch and the funds that arose as a result of the CF Arch cru structure, which involved a complex network of onshore and offshore companies and private market investments. The funds were eventually suspended in March 2009 as a result of concerns that there was insufficient liquidity in one of the sub-funds to meet investors’ demands to sell their shares. In addition, the firm did not have adequate processes in place to identify when the information it used to value the funds might not be reliable and whether alternative measures should be used to price the funds fairly, although it is not clear that such measures would have resulted in different prices being used. The firm did not begin to investigate the valuation and pricing of the funds’ investments in detail until late 2008. FSA notes that a £54m payment scheme was voluntarily established in June 2011 by the firm, Bank of New York Mellon Trust and Depositary and HSBC Bank plc for investors. The firm required the financial support of its ultimate parent, Capita Group plc, to make its £32m contribution to that payment scheme. The firm could not fund both such a substantial contribution to the payment scheme and a financial penalty. This was taken into account in FSA’s decision not to impose a financial penalty on it.

http://www.fsa.gov.uk/static/pubs/final/capita-financial-managers.pdf

Cattles plc/Welcome Financial Services (28 March 2012 – see also under Cattles plc/Welcome Financial Services – see also Corr, James/Miller, Pete/Blake, John in Individuals section below

FSA fined and banned former directors of Cattles plc and its subsidiary Welcome Financial Services Limited for publishing misleading information to investors about the credit quality of Welcome’s loan book and acting without integrity in discharging their responsibilities. FSA has also publicly censured both firms for publishing misleading information. FSA would have imposed substantial fines on the firms had it not been for their financial circumstances. It is noted that Cattles’ 2007 annual report contained highly misleading arrears, impairment and profit figures which also included in a rights issue prospectus that Cattles released to potential investors in April 2008. The rights issue was subsequently fully subscribed and raised £200m. When the true state of Cattles’ loan book emerged in 2009, trading in Cattles’ shares was suspended. On 2 March 2011 Cattles announced a scheme of arrangement under which its shareholders would receive only 1p for each share, compared with a rights issue price of £1.28. As a result Cattles breached the Listing Principles by failing to act with integrity towards its shareholders and potential shareholders, and failing to communicate information in such a way as to avoid the creation or continuation of a false market. Welcome breached Principle 3 of the FSA Principles for Businesses by failing to take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems. Both firms engaged in market abuse by disseminating the inaccurate information.

See main item http://www.fsa.gov.uk/static/pubs/final/cattles-ltd.pdf http://www.fsa.gov.uk/static/pubs/final/welcome-financial-service.pdf http://www.fsa.gov.uk/static/pubs/final/john-blake.pdf

8

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Christchurch Investment Management Limited/Thornberry, David (29 March 2012, publicised 1 May 20212)

FSA has fined the firm, which specialises in financial planning and portfolio management and its compliance office for failings in relation to the protection of client money - the individual has also been prohibited from acting as a compliance officer or having responsibility for client assets - this is the first time FSA has prohibited an individual from having responsibility for client assets.. When FSA visited the firm in May 2010, it found that it had failed to comply with CASS from November 2007 onwards. This included failing to put in place adequate trust documentation for any of its 227 client bank accounts, which put client money at risk in the event of the firm's insolvency. The amount of client money held by Christchurch during the period averaged £1.2 million. FSA found that David Thornberry failed to ensure that client money and assets were managed appropriately, noting that he had no formal training for his compliance oversight role, was not aware of the CASS rules relating to trust status letters and failed to review and test the existing systems and controls. He also failed properly to allocate duties for handling client money, giving one individual an extensive range of responsibilities without adequate internal checks and balances. This led to an increased risk of fraud and error that could have resulted in clients losing money. It is noted that the parties agreed to settle at an early stage and therefore qualified for a 30% discount. FSA has taken into account the fact that the firm implemented a number of changes to improve the handling of client money following the visit and that no clients have suffered any losses as a consequence of the breaches identified.

£26,600 (firm)/ £11,500 (individual)

http://www.fsa.gov.uk/static/pubs/final/christchurch.pdf

http://www.fsa.gov.uk/static/pubs/final/david-thornberry.pdf

City Gate Money Managers Limited (6 August 2012 – see also Domke, Stewart in individuals section)

The firm’s breaches relate to the conduct of pension transfer and income drawdown business by, failings in a financial promotion made by the firm on behalf of the issuing company for which it was acting as agent, and a failure to have adequate systems and controls to monitor its advisers’ and appointed representatives’ compliance and training and competence. FSA notes that in July 2009 the firm had been fined (£42,000) for materially similar systems and controls failings in relation to the approval of financial promotions and monitoring of appointed representatives. The firm failed to address the issues identified in that action and take steps to ensure that they did not recur. In addition, it breached the variation which took effect following the previous enforcement action and thus breached s20(1)(a) FSMA, in that it conducted pension transfer and income drawdown business after 13 July 2009, which was beyond the scope of its permission. FSA notes that the firm went into voluntary liquidation in November 2010 and, were it not the firm’s financial circumstances, FSA would have imposed a financial penalty of £180,000 in respect of the breaches identified.

http://www.fsa.gov.uk/static/pubs/final/city-gate.pdf

9

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Coutts & Company (23 March 2012, publicised 26 March 2012)

FSA has fined Coutts & Company for failing to take reasonable care to establish and maintain effective AML systems and controls relating to high risk customers, including PEPs. FSA emphasizes that he failings at the firm were serious, systemic and were allowed to persist for almost three years. In October 2010, FSA visited Coutts as part of its thematic review into banks’ management of high money-laundering risk situations. Following that visit, FSA’s investigation identified that the firm did not apply robust controls when starting relationships with high risk customers and did not consistently apply appropriate monitoring of those high risk relationships. In addition, FSA determined that the AML team at Coutts failed to provide an appropriate level of scrutiny and challenge. FSA identified deficiencies in nearly three quarters of the PEP and high risk customer files reviewed. Specifically, in one or more of each inadequate file, the firm failed to: gather sufficient information to establish the source of wealth and source of funds of its prospective PEP and other high risk customers; identify and/or assess adverse intelligence about prospective and existing high risk customers properly and take appropriate steps in relation to such intelligence; keep the information held on its existing PEP and other high risk customers up-to-date; and scrutinise transactions made through PEP and other high risk customer accounts appropriately. FSA notes that a number of improvements and recommendations have already been, or are being, implemented. These include significant remedial amendments to PEP and other high risk customer files to ensure that appropriate due diligence information about the firm’s customers has been assessed and recorded.

£8.75m http://www.fsa.gov.uk/static/pubs/final/coutts-mar12.pdf

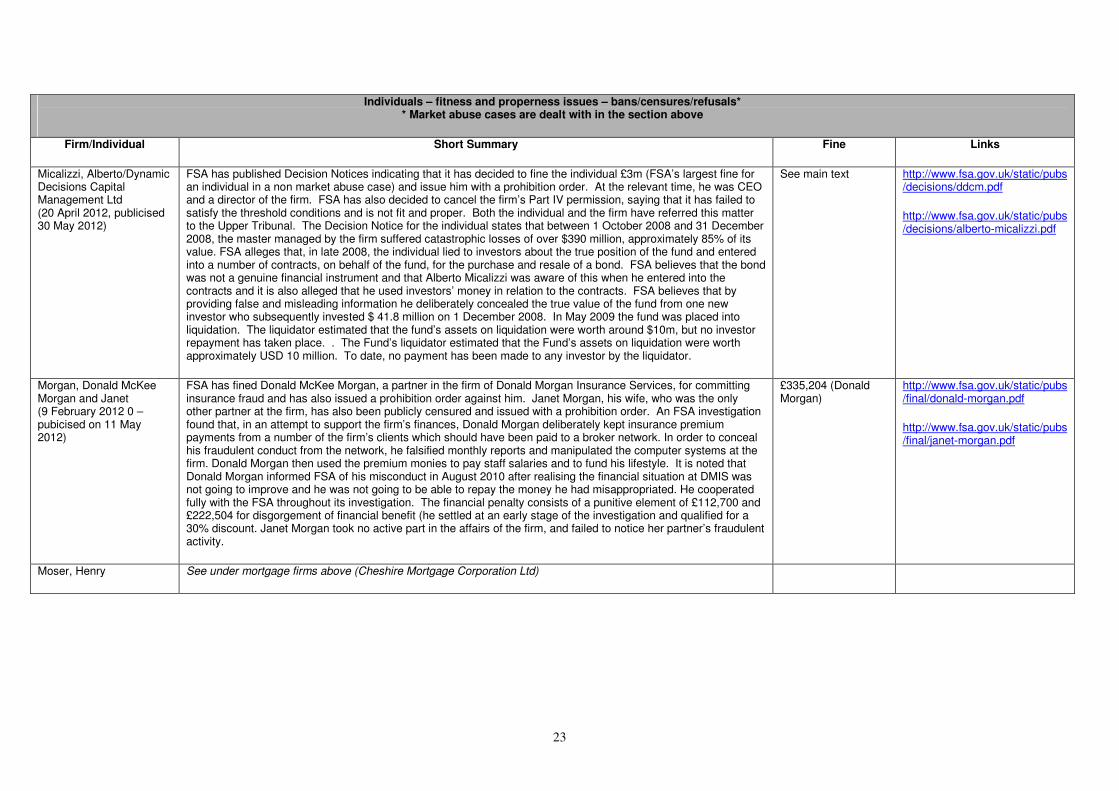

Dynamic Decisions Capital Management Ltd (20 April 2012, publicised 30 May 2012)

See under Micalizzi, Alberto in Individuals section below

Gracechurch Investments Limited/Sam Kenny/Carl Davey (20 December 2012 – Decision Notice is dated 11 October 2012)

FSA has publicly censured the firm for misconduct, including using pressure-selling tactics with customers to invest in the shares of small companies, resulting in client losses of at least £2m. FSA would have fined it £1.5m had the firm not been in liquidation. The firm misrepresented, for instance, the financial performance of stocks both orally and in writing. Brokers ignored requests for further information and protests that clients had no funds to invest. In at least one case a broker claimed that the recommendation was based on inside information. Between 1 April 2008 and 4 November 2009, the firm advised approximately 340 clients to buy about £4m - clients would have lost 72% of the amount they had invested in eight of the top ten stocks (based on financial volume) sold by the firm if they had held those small-cap stocks until 12 October 2011. The firm also provided FSA with false dates for internal committee meetings and deliberately withheld a recording of a non-compliant advised sales call requested by FSA and the firm also knowingly employed someone in a senior position who was not FSA-approved and who was linked to pressure-selling tactics. FSA has published a Decision Notice dated 11 October 2012 with regard to Sam Kenny, its former CEO, which notes that it intends to fine him £450,000 and to issue him with a prohibition order – this matter has been referred to the Upper Tribunal. FSA states that, subject to the Tribunal’s decision, FSA has found that that he personally pressurised, or misrepresented material facts to clients and in his role as CEO trained and encouraged his staff to pressure clients. FSA has published a Final Notice which issues a prohibition order against the firm’s former compliance officer, Carl Davey, and would have fined him £175,000 if it were not for the serious financial hardship that such a fine would cause him. FSA reports that he was also involved in the deliberate withholding of the non-compliant advised sales call and that despite his efforts to improve the firm’s systems and controls, the monitoring of advised calls by the firm’s brokers was inadequate and brokers were regularly making misrepresentations about stocks to clients.

http://www.fsa.gov.uk/static/pubs/final/gracechurch-investments.pdf

http://www.fsa.gov.uk/static/pubs/final/carl-davey.pdf

http://www.fsa.gov.uk/static/pubs/decisions/sam-kenny.pdf

10

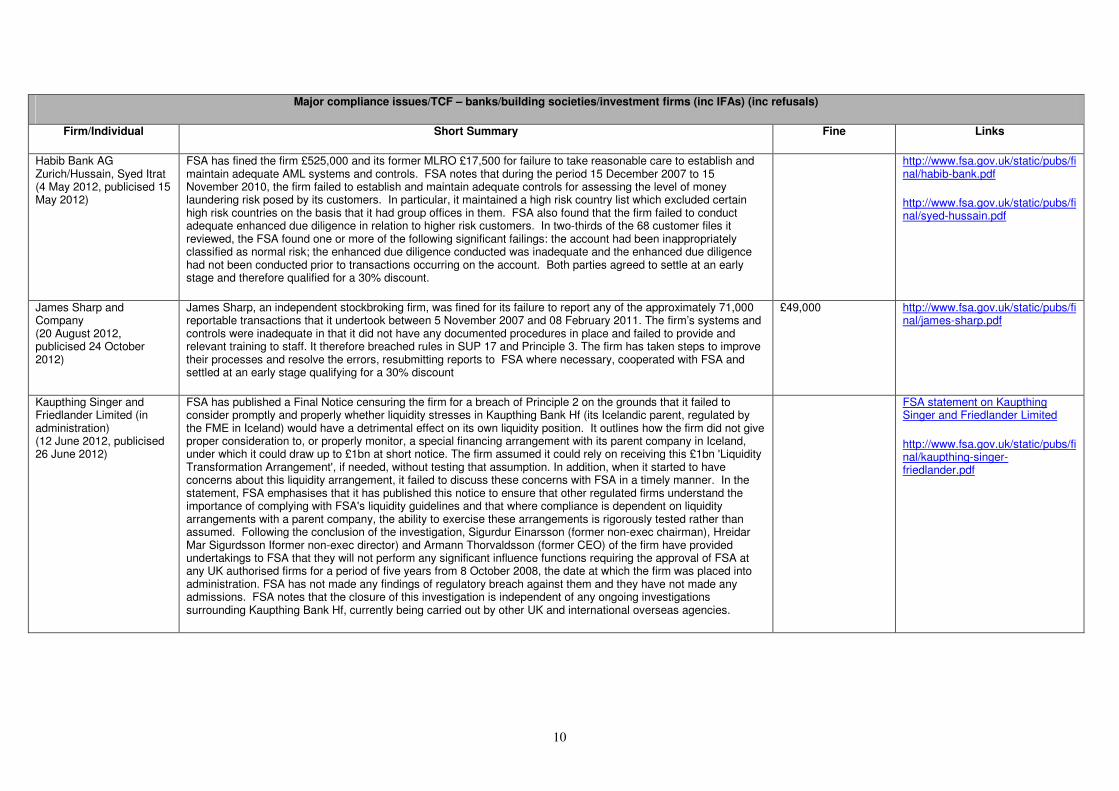

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Habib Bank AG Zurich/Hussain, Syed Itrat (4 May 2012, publicised 15 May 2012)

FSA has fined the firm £525,000 and its former MLRO £17,500 for failure to take reasonable care to establish and maintain adequate AML systems and controls. FSA notes that during the period 15 December 2007 to 15 November 2010, the firm failed to establish and maintain adequate controls for assessing the level of money laundering risk posed by its customers. In particular, it maintained a high risk country list which excluded certain high risk countries on the basis that it had group offices in them. FSA also found that the firm failed to conduct adequate enhanced due diligence in relation to higher risk customers. In two-thirds of the 68 customer files it reviewed, the FSA found one or more of the following significant failings: the account had been inappropriately classified as normal risk; the enhanced due diligence conducted was inadequate and the enhanced due diligence had not been conducted prior to transactions occurring on the account. Both parties agreed to settle at an early stage and therefore qualified for a 30% discount.

http://www.fsa.gov.uk/static/pubs/final/habib-bank.pdf

http://www.fsa.gov.uk/static/pubs/final/syed-hussain.pdf

James Sharp and Company (20 August 2012, publicised 24 October 2012)

James Sharp, an independent stockbroking firm, was fined for its failure to report any of the approximately 71,000 reportable transactions that it undertook between 5 November 2007 and 08 February 2011. The firm’s systems and controls were inadequate in that it did not have any documented procedures in place and failed to provide and relevant training to staff. It therefore breached rules in SUP 17 and Principle 3. The firm has taken steps to improve their processes and resolve the errors, resubmitting reports to FSA where necessary, cooperated with FSA and settled at an early stage qualifying for a 30% discount

£49,000 http://www.fsa.gov.uk/static/pubs/final/james-sharp.pdf

Kaupthing Singer and Friedlander Limited (in administration) (12 June 2012, publicised 26 June 2012)

FSA has published a Final Notice censuring the firm for a breach of Principle 2 on the grounds that it failed to consider promptly and properly whether liquidity stresses in Kaupthing Bank Hf (its Icelandic parent, regulated by the FME in Iceland) would have a detrimental effect on its own liquidity position. It outlines how the firm did not give proper consideration to, or properly monitor, a special financing arrangement with its parent company in Iceland, under which it could draw up to £1bn at short notice. The firm assumed it could rely on receiving this £1bn 'Liquidity Transformation Arrangement', if needed, without testing that assumption. In addition, when it started to have concerns about this liquidity arrangement, it failed to discuss these concerns with FSA in a timely manner. In the statement, FSA emphasises that it has published this notice to ensure that other regulated firms understand the importance of complying with FSA's liquidity guidelines and that where compliance is dependent on liquidity arrangements with a parent company, the ability to exercise these arrangements is rigorously tested rather than assumed. Following the conclusion of the investigation, Sigurdur Einarsson (former non-exec chairman), Hreidar Mar Sigurdsson Iformer non-exec director) and Armann Thorvaldsson (former CEO) of the firm have provided undertakings to FSA that they will not perform any significant influence functions requiring the approval of FSA at any UK authorised firms for a period of five years from 8 October 2008, the date at which the firm was placed into administration. FSA has not made any findings of regulatory breach against them and they have not made any admissions. FSA notes that the closure of this investigation is independent of any ongoing investigations surrounding Kaupthing Bank Hf, currently being carried out by other UK and international overseas agencies.

FSA statement on Kaupthing Singer and Friedlander Limited

http://www.fsa.gov.uk/static/pubs/final/kaupthing-singer-friedlander.pdf

11

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Martin Currie Investment Management Limited/ Martin Currie Inc (2 May 2012, publiicised 10 May 2012)

FSA has fined the firms £3.5m for failing to manage a conflict of interest between two of its clients. This is the largest fine ever imposed by FSA in a conflict of interest case. In addition to the fine issued by FSA, SEC is also fining the firm. The conflict of interest arose when Martin Currie caused one client (Fund B) to enter into a transaction which rescued another client (Fund A) from serious liquidity concerns. FSA reports that many of the firm’s failings resulted from weaknesses in its systems and controls around unlisted investments. In particular, the firms lacked adequate oversight of the fund managers advising both Fund A and Fund B. The firm settled early with FSA and received a 30% discount on its fine - FSA also took into account that the firm brought the breaches to FSA’s attention and has co-operated fully with FSA’s investigation, compensated Fund B for its investment losses after the Fund raised concerns, and spent considerable time and money investigating the issues itself and addressing the concerns raised by FSA

£3.5m http://www.fsa.gov.uk/static/pubs/final/martin-currie.pdf

The Pentecostal Credit Union Limited/Reverend Carmel Jones (8 November 2012, publicised 12 November 2012)

FSA has publicly censured The Pentecostal Credit Union Limited for issuing loans worth £1.2m under its members’ names but channelling the money to a church organisation in direct contravention of credit union rules which stated that only individual members could borrow, not organisations. The director, Reverend Carmel Jones, has been issued with a prohibition order for overseeing this practice. FSA notes that, before coming under FSA regulation in 2002, the credit union was making regular loans to the church organisation for property purchases and repairs. After a routine assessment in 2003 FSA warned them to stop this practice with immediate effect because the loans may not be legally enforceable. In 2006, Carmel Jones wrote to FSA proposing to reinstate the loan system with either insurance indemnity for its members or the establishment of a corporate entity of which they would be shareholders. Although FSA warned that these were unlawful, the credit union made 20 such loans between May 2007 and July 2011. Carmel Jones signed and approved 14 of the 20 loans in question, and in 12 cases signed the cheques for the loan money, none of which were made out to the individuals purportedly taking out the loans. In one case, the member had no idea a loan had been made in his name. In another, the repayments were £1,000 a month higher than the member’s stated monthly income, and a cheque issued for a third loan was dated four days before the loan application was made. Furthermore, there were two cases where the loan application document had been signed by a third party rather than the members themselves. The relationship between the credit union and the organisation broke down at the end of 2009 and the loan repayments stopped. The estimated amount outstanding is in excess of £670,000. FSA notes that it would normally have imposed a fine for these serious breaches but has taken into account the important role of credit unions and the fact that any fine would impact its members. There may be future cases where it will be appropriate to fine a credit union. FSA considers this to be an exceptional case and has issued a public censure because the credit union cooperated fully with the investigation and replaced its entire management at the request of FSA.

http://www.fsa.gov.uk/static/pubs/final/tpcu.pdf

http://www.fsa.gov.uk/static/pubs/final/reverend-jones.pdf

12

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Pi Financial Limited (18 September 2012)

The firm has been fined in respect of breaches of Principles 3 and 9. FSA found that the firm had failed to implement adequate internal sales monitoring procedures; provide adequate training and supervision to its adviser and establish and maintain adequate compliance and file checking arrangements, particularly as PI sol high risk products. In a sample of files, FSA found that half were unsuitable – in particular, none of the files involving recommendations to invest in UCIS was suitable in light of the clients’ attitude to risk and the firm failed to demonstrate that the clients in question fell within the relevant category of COBS 4.12; None of the files involving recommendations to invest in structured products was suitable, due to a mismatch between the product and the clients’ attitude to risk and, of the files involving recommendations to clients to switch their pensions, 24% were found to be unsuitable, due to the underlying investments being too high risk. There was no evidence on file to demonstrate that two of these unsuitable files were checked by a pension transfer specialist as required in COBS 19.1.1R. During the relevant period, the firm had promoted UCIS to 168 clients, who invested over £6m, and promoted structured products to 362 clients, who invested nearly £20m, either directly or indirectly through SIPPs. Systems and compliance failings identified revealed systemic weaknesses across the firm’s systems and controls. FSA notes that the firm’s failings were further aggravated by the fact that extensive guidance was issued by FSA during and prior to the relevant period, which set out the importance of ensuring product suitability in relation to UCIS, structured products and pension transfers and which called for network firms (of which the firm is one) to ensure that they had sufficient control over their Appointed Representatives. In mitigation, the firm took a number of steps to address FSA’s concerns and that, since being referred to Enforcement, the firm has voluntarily varied its Part IV permission so that it is no longer authorised to arrange and promote UCIS. It has also undertaken to make improvements to training, establish 100% file checking for its high risk products and initiate a client contact exercise in relation to the past sales of high risk products.

£58,300 http://www.fsa.gov.uk/static/pubs/final/pi-financial-limited.pdf

P3 Wealth Management Limited (24 April 2012, publicised 30 May 2012)

See under O’Donnell, Patrick Francis in Individuals below

Pollok Credit Union (22 March 2012)

Pollok Credit Union has been publicly censured. FSA reports that it jeopardised its own solvency by making large loans to a non-member and the loans were contrary to its own procedures. The firm also breached FSA rules because the loans meant 88% of the credit union’s capital was tied up with this trust (large exposures must not exceed 25% of a credit union’s capital).

http://www.fsa.gov.uk/static/pubs/final/pollok-cu.pdf

13

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Plus500UK Limited (17 October 2012, publicised 24 October 2012)

The firm was fined for failing to provide accurate and timely transaction reports to FSA in respect of all the reportable transactions they carried out. Between 29 June 2010 and 5 November 2011 the firm, an online CFD trading facility provider, conducted 1,332,000 reportable transactions. However, the firm failed to report any of these accurately and failed to report 189,000 of them at all. The firm’s systems and controls were inadequate in that it failed to set up appropriate reporting systems, did not have any documented procedures in place in relation to transaction reporting and failed to provide any relevant training to staff. It therefore breached rules in SUP 17 of the FSA Handbook and Principle 3 of the FSA’s Principles for Business. The firm has taken steps to improve their processes and resolve the errors, resubmitting reports to FSA where necessary, cooperated with FSA and settled at an early stage qualifying for a 30% discount. It is noted that this was the first regulated firm to be fined in respect of transaction reporting failures under the new FSA penalties policy. This policy was established to provide a consistent and more transparent framework for the calculation of financial penalties. The regime came into force on 6 March 2010 and applies to any breaches which occur on or after that date. As a result the penalty imposed on Plus500, which was based on the number of affected transactions, was larger than it would have been under the previous regime.

£205,128 http://www.fsa.gov.uk/static/pubs/final/plus500uk.pdf

Santander UK plc (16 February 2012, publicised 20 February 2012)

FSA has fined the firm for failing to confirm under which circumstances its structured products would be covered by FSCS. Customers began to query the extent of FSCS cover towards the end of 2008, but it was January 2010 before the firm clarified the position. During this time, it sold approximately £2.7bn of structured products, including £1.2bn after June 2009 when it concluded that the circumstances in which its two products, Guaranteed Capital Plus and the Guaranteed Growth Plan, would be covered by FSCS were limited. However, new customers were not informed of the limitations in FSCS cover until January 2010. The firm acknowledges that it could have changed its product literature and training materials more quickly to reflect the FSCS position accurately. The fact that it allowed sales to continue with unclear Key Facts literature contributed to the seriousness of the breaches. FSA has not made any findings that these products were sold to customers for whom they were not suitable, and notes that investors in these products have not suffered a financial loss as a result of Santander’s failings.

£1.5m http://www.fsa.gov.uk/static/pubs/final/santander.pdf

Savoy Investment Management Limited (12 November 2012, publicised 13 November 2012)

FSA has fined the firm for failing to take reasonable care to ensure the suitability of the investment portfolios of its wealth management clients It allowed its investment managers a high degree of discretion to advise its wealth management clients on their investment portfolios. It had limited front office controls and its other processes failed to ensure the suitability of its advice and portfolio management. This included failures to collect and record KYC information and failures in its compliance monitoring processes. FSA has reviewed the firm as part of its thematic review of the wealth management sector. A review of a sample of files found that 23% showed a high risk of unsuitability. Files often lacked information on clients’ personal and financial circumstances and contained out of date and inadequate client information. The firm is doing a past business review of its investment services to its wealth management clients, which will determine whether clients need to be compensated. FSA further notes that it agreed to settle at an early stage and qualified for a 30% discount and that it has taken steps to change its management structure and processes. Without these changes and the past business review, the financial penalty would have been higher.

£412,000 http://www.fsa.gov.uk/static/pubs/final/savoy-investment-management.pdf

14

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

Shettleston and Tollcross Credit Union (5 January 2012, publicised 22 March 2012)

Shettleston and Tollcross Credit Union has been publicly censured. It made loans to seven directors on better terms than those generally available to the membership. The credit union removed the preferential rates when it realised this was not allowed, but did nothing to recover the lost earnings and paid a reduced dividend to its members as a result. It is noted that the financial benefit to those who received loans was very small however and the directors have since agreed to repay it in full.

http://www.fsa.gov.uk/static/pubs/final/stcu.pdf

Topps Rogers Financial Management (13 February 2012)

FSA has cancelled the firm’s Part IV permissions and imposed a fine of £97,000. The firm failed to take reasonable care to ensure that its recommendations relating to UCIS were suitable for its customers and also failed to establish and implement adequate compliance arrangements over its business. FSA notes that a number of UCIS that the firm’s clients invested in have been suspended or wound up, resulting in potential financial losses for customers. The situation was aggravated by the fact that customers were advised by the firm to invest large proportions of their investment portfolios in UCIS. In some instances, customers were not aware that they had invested in UCIS, or of the associated risks.

£97,0`00 http://www.fsa.gov.uk/static/pubs/final/topps-rogers-financial-management.pdf

UBS AG (25 November 2012, publicised 26 November 2012)

FSA has fined the firm £29.7m (discounted from £42.4m for early settlement) for systems and controls failings that allowed Kweku Adoboli to cause substantial losses totalling US$2.3bn as a result of unauthorised trading. FSA believes that UBS failed to take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems and failed to conduct its business from the London Branch with due skill, care and diligence. Highlighted failings include: ineffective computer system to assist in risk management; deficiencies in trade capture and processing; inadequate front office supervision; breaches of risk limits going without any discipline for doing so; a focus on efficiency as opposed to risk control among support staff of the ETF desk; a failure to investigate the underlying reasons for the substantial increase in profitability of the ETF desk despite the fact that this could not be explained by reference to the end of day risk positions. It is noted that profit and loss suspensions to the value of $1. 6bn were requested by Kweku Adoboli during the course of August 2011. Prior to 18 August 2011, these were accepted without challenge or escalation. It is noted that the penalty was fixed at 15% of the revenue of the UBS’s Global Synthetic Equities division “is intended to make it clear that the FSA expects much higher standards from the firms we regulate. The firm agreed to engage an independent firm to conduct a substantive investigation into the unauthorised trading incident, expending considerable resources (approximately £16m to date) in doing so. UBS's new senior management has committed significant resources to undertake an extensive programme of remediation. UBS has taken disciplinary action against employees who were involved in the events which gave rise to these breaches, including clawing back bonuses and withholding 50% of their deferred compensation from relevant individuals totalling more than £34m. FSA conducted its investigation in coordination with the FINMA which has also made its findings public. FINMA has also taken action against UBS in relation to the breach which is the subject of this Notice and UBS has undertaken to comply with the separate requirements imposed on it by FINMA.

£29.7m http://www.fsa.gov.uk/static/pubs/final/ubs-ag.pdf

15

Major compliance issues/TCF – banks/building societies/investment firms (inc IFAs) (inc refusals)

Firm/Individual Short Summary Fine Links

UBS AG (19 December 2012)

FSA has fined UBS AG £160m for misconduct relating to LIBOR. This is the largest fine ever imposed by the FSA. FSA notes that between 1 January 2005 to 31 December 2010 the misconduct included the following:: UBS’s traders routinely making requests to the individuals at UBS responsible for determining its LIBOR and EURIBOR submissions to adjust their submissions to benefit the traders’ trading positions; giving the roles of determining its LIBOR and EURIBOR submissions to traders whose positions made a profit or loss depending on the LIBOR / EURIBOR fixes; colluding with interdealer brokers in co-ordinated attempts to influence JPY LIBOR submissions made by other panel banks, adding that corrupt brokerage payments were made to reward brokers for their efforts to manipulate the LIBOR submissions of panel banks; colluding with individuals at other panel banks to get them to make JPY LIBOR submissions that benefited UBS’s trading positions; adopting LIBOR submissions directives whose primary purpose was to protect the bank’s reputation by avoiding negative media attention about its submissions and speculation about its creditworthiness. FSA notes that at least 45 individuals including traders, managers and senior managers were involved in, or aware of, the practice of attempting to influence submission and adds that it continues to pursue a number of other significant cross-border investigations in relation to LIBOR and EURIBOR. UBS did not qualify for the full 30% discount available for early settlement due to the fact that settlement was reached in the second phase of the discount scheme. UBS thus received a reduced discount of 20%.

£160m http://www.fsa.gov.uk/static/pubs/final/ubs.pdf

16

Major compliance issues/TCF – mortgage firms (inc refusals)

Firm/Individual Short Summary Fine Links

Cheshire Mortgage Corporation Limited/Henry Moser/Andrew Lawton (6 December 2012, publicised 10 December 2012)

FSA has fined the firm £1.225m for failing to treat customers fairly in the sale of mortgages and arrears handling from October 2004 to the end of 2009. Its CEO, Henry Moser, has been fined £70,000 and agreed to step down from his role within three to six months. Andrew Lawton, the firm’s compliance director, has been fined £13,500 and banned from holding a significant influence function. FSA has also required the firm to carry out a redress exercise that could see approximately £2m paid to around 2,000 affected customers. FSA reports that the firm operated in “niche markets, including lending to customers with poor credit histories”, failed to treat some of its customers fairly when they fell into arrears, was unable to always demonstrate that mortgages it sold were affordable, and did not always communicate regularly or fully with its customers. It also overcharged some customers in arrears and applied arrears charges inconsistently and unfairly. Customers were also sometimes notified of charges after they had been incurred. FSA found that when the firm transferred customers in arrears to Monarch Recoveries for debt recovery, they were charged £150 despite it being an in-house company.

http://www.fsa.gov.uk/static/pubs/final/cmc-ltd.pdf

http://www.fsa.gov.uk/static/pubs/final/henry-moser.pdf

http://www.fsa.gov.uk/static/pubs/final/andrew-lawton.pdf

Laurenti, Mark Joseph//Independent Mortgage Advisory Service Limited (27 January 2012)

FSA has fined this individual, issued a prohibition order against him and withdrawn its approval given to him to perform the CF1 function at the firm on the grounds of fitness and properness. It is noted that he was the only approved person performing the controlled function at the firm and failed to take reasonable steps to ensure that it put in place appropriate systems and controls in relation to the sales process for regulated mortgage contracts. As a result of his failure to ensure that the firm operated adequate procedures in connection with record keeping, KYC information, affordability assessments and disclosure of fees, he is also deemed to be responsible for the advice failings that FSA identified following its review of 22 client mortgage files.

£14,000 http://www.fsa.gov.uk/static/pubs/final/mark-laurenti.pdf

Principal Mortgage Services Limited (18 June 2012)

See Terence Harrop (under individuals section below)

17

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

Agfar, Sardar (5 January 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that it failed to submit Payment Services Directive Transactions return (the “FSA057”),

http://www.fsa.gov.uk/pubs/final/sardar_agha.pdf

Ali, Karamat (6 January 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that Mr Ali has not notified FSA of a change in the address of his head office.

http://www.fsa.gov.uk/pubs/final/karamat-ali.pdf

Adams, Anthony (21 February 2012, publicised August 2012)

This Final Notice notes a prohibition order against the individual, a former director and compliance officer of MNFA. FSA has prohibited him from performing any significant influence function at any authorised or exempt person or exempt professional firm, other than as, or through, an appointed representative within the meaning of FSMA. FSA concluded that he failed to understand the restrictions on promoting UCIS and was partly responsible for MNFA promoting the EBP Scheme, a UCIS , and failed to take any steps to ensure that there was compliance monitoring of MNFA’s sale of the EBP Scheme (despite being the compliance officer). .See also Richardt Rhys below.

http://www.fsa.gov.uk/static/pubs/final/anthony-adams.pdf

Anjum, Sohail (5 January 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that it failed to submit Payment Services Directive Transactions return (the “FSA057”),

http://www.fsa.gov.uk/pubs/final/sohail_anjum.pdf

Ayub, Khuram (24 February 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that it failed to submit Payment Services Directive Transactions return..

http://www.fsa.gov.uk/static/pubs/final/khuram-ayub.pdf

Bealing, Philip (2 March 2012)

The firm's Part IV permission has been cancelled on account of its failure to satisfy threshold conditions (specifically it failed to pay fees of £1,665.59).

http://www.fsa.gov.uk/static/pubs/final/philip-bealing.pdf

Burnside, Ryan (6 November 2012)

FSA has issued a prohibition order against this individual on the grounds of fitness and properness, noting that on 5 December 2011, Ryan Burnside was convicted of one count of fraud, for which he was sentenced on 11 January 2012 to two years and four months imprisonment.

http://www.fsa.gov.uk/static/pubs/final/ryan-burnside.pdf

Corr, James/Miller, Pete/Blake, John (28 March 2012 – see also under Cattles plc/Welcome Financial Services

FSA) has fined and banned two former directors of Cattles plc and its subsidiary Welcome Financial Services Limited for publishing misleading information to investors about the credit quality of Welcome’s loan book and acting without integrity in discharging their responsibilities. FSA has also publicly censured both firms for publishing misleading information. James Corr, Cattles’ FD, has been fined £400,000 and Peter Miller, Welcome’s FD, has been fined £200,000, and both have been banned from performing any functions in relation to any FSA regulated activities. FSA has also decided to ban John Blake, Welcome’s MD, and fine him £100,000. Blake has referred his case to the Upper Tribunal. All three fines were reduced on account of the directors’ current personal financial circumstances. In October 2012, a Final Notice with regard to John Blake was published.

See main item

18

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

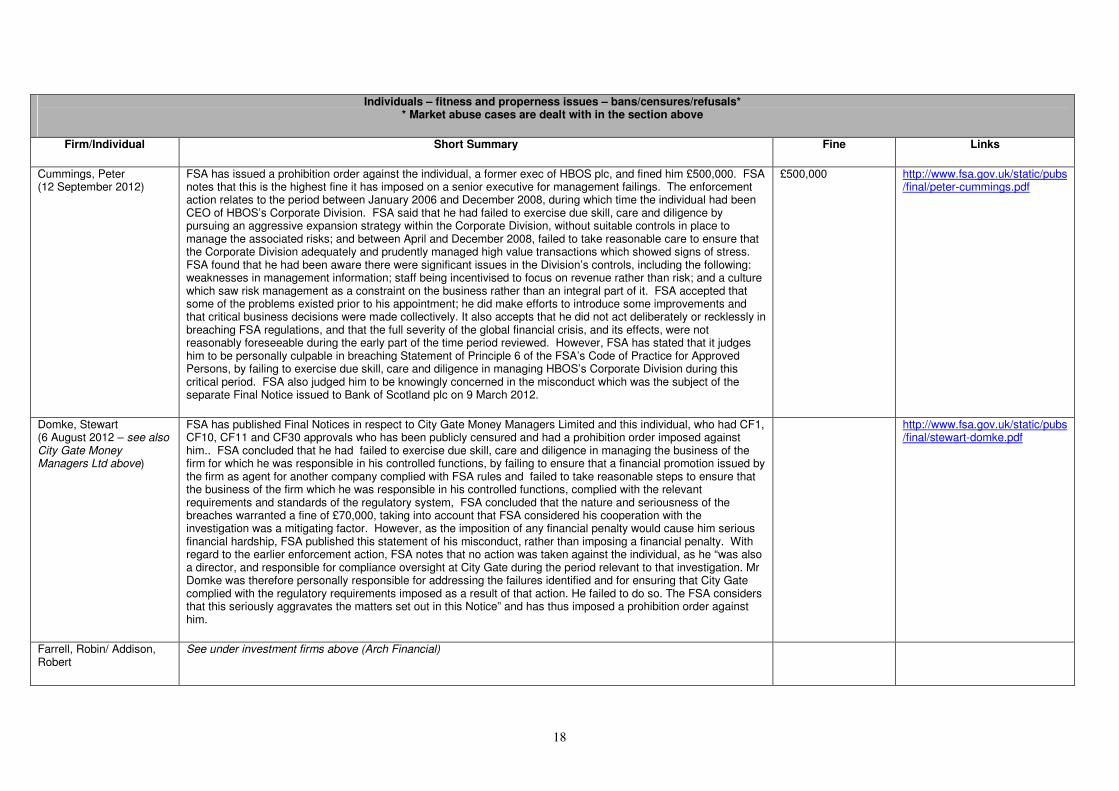

Cummings, Peter (12 September 2012)

FSA has issued a prohibition order against the individual, a former exec of HBOS plc, and fined him £500,000. FSA notes that this is the highest fine it has imposed on a senior executive for management failings. The enforcement action relates to the period between January 2006 and December 2008, during which time the individual had been CEO of HBOS’s Corporate Division. FSA said that he had failed to exercise due skill, care and diligence by pursuing an aggressive expansion strategy within the Corporate Division, without suitable controls in place to manage the associated risks; and between April and December 2008, failed to take reasonable care to ensure that the Corporate Division adequately and prudently managed high value transactions which showed signs of stress. FSA found that he had been aware there were significant issues in the Division’s controls, including the following: weaknesses in management information; staff being incentivised to focus on revenue rather than risk; and a culture which saw risk management as a constraint on the business rather than an integral part of it. FSA accepted that some of the problems existed prior to his appointment; he did make efforts to introduce some improvements and that critical business decisions were made collectively. It also accepts that he did not act deliberately or recklessly in breaching FSA regulations, and that the full severity of the global financial crisis, and its effects, were not reasonably foreseeable during the early part of the time period reviewed. However, FSA has stated that it judges him to be personally culpable in breaching Statement of Principle 6 of the FSA’s Code of Practice for Approved Persons, by failing to exercise due skill, care and diligence in managing HBOS’s Corporate Division during this critical period. FSA also judged him to be knowingly concerned in the misconduct which was the subject of the separate Final Notice issued to Bank of Scotland plc on 9 March 2012.

£500,000 http://www.fsa.gov.uk/static/pubs/final/peter-cummings.pdf

Domke, Stewart (6 August 2012 – see also City Gate Money Managers Ltd above)

FSA has published Final Notices in respect to City Gate Money Managers Limited and this individual, who had CF1, CF10, CF11 and CF30 approvals who has been publicly censured and had a prohibition order imposed against him.. FSA concluded that he had failed to exercise due skill, care and diligence in managing the business of the firm for which he was responsible in his controlled functions, by failing to ensure that a financial promotion issued by the firm as agent for another company complied with FSA rules and failed to take reasonable steps to ensure that the business of the firm which he was responsible in his controlled functions, complied with the relevant requirements and standards of the regulatory system, FSA concluded that the nature and seriousness of the breaches warranted a fine of £70,000, taking into account that FSA considered his cooperation with the investigation was a mitigating factor. However, as the imposition of any financial penalty would cause him serious financial hardship, FSA published this statement of his misconduct, rather than imposing a financial penalty. With regard to the earlier enforcement action, FSA notes that no action was taken against the individual, as he “was also a director, and responsible for compliance oversight at City Gate during the period relevant to that investigation. Mr Domke was therefore personally responsible for addressing the failures identified and for ensuring that City Gate complied with the regulatory requirements imposed as a result of that action. He failed to do so. The FSA considers that this seriously aggravates the matters set out in this Notice” and has thus imposed a prohibition order against him.

http://www.fsa.gov.uk/static/pubs/final/stewart-domke.pdf

Farrell, Robin/ Addison, Robert

See under investment firms above (Arch Financial)

19

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

First Financial Advisers Limited/Danner, Stephen (20 July 2012)

Further to the Upper Tribunal’s Decision, FSA has now published the Final Notice with regard to this case. FSA had refused an application from First Financial Advisers Limited for Stephen Danner to be approved to perform Controlled Function CF30 on the grounds of fitness and properness. The Upper Tribunal had found that FSA had been correct to refuse the application. This Final Notice includes several extracts from the Decision.

http://www.fsa.gov.uk/static/pubs/final/stephen-danner.pdf

Flanaga, Gareth/GMF Marketing Services Limited (27 March 2012)

By this Final Notice, FSA issues a prohibition order, imposes a fine of £95,200 and withdraws the approval given to the individual to perform controlled functions at the firm. FSA concluded that he had failed to act with integrity in carrying out his controlled functions by knowingly submitting mortgage applications through the firm in his own name which contained false information. It is noted that he had been the sole owner and director of the Londonderry based IFA and had been the only approved person performing significant influence functions there until 12 December 2011 and was solely responsible for compliance oversight until FSA’s investigation. The firm now has new directors and a new person responsible for compliance oversight. The individual is no longer employed by or at the firm and has ceased to hold any shares in it.

http://www.fsa.gov.uk/static/pubs/final/gareth-flanagan.pdf

Goodwin, Stephen (24 July 2012)

FSA has imposed a fine and issued a prohibition order against the individual, a former commercial insurance broker who used clients’ insurance premiums to fund his business. Between 2008 and 2010, Stephen Goodwin, a former partner of Goodwin Best in Bury, Lancashire and his (now deceased) business partner, accepted insurance premiums from clients, but sometimes paid this money into their business account rather than to the relevant insurer or intermediary to arrange the policy. In total, they misappropriated £303,846. The fine consists of the disgorgement of benefit of £303,846 and an additional £168,000 punitive element. The total fine, £471,846, is one of the largest ever levied on an individual for insurance fraud. FSA notes that at least three clients suffered financial loss: one tried to make a claim only to find they were uninsured and; two other clients paid the same premium twice to ensure their policies remained in force - these clients are now in contact with FSCS. Stephen Goodwin was declared bankrupt in April 2011 in relation to debts incurred by his firm and his bankruptcy was discharged in April 2012. The firm is no longer operating.

£471,846 http://www.fsa.gov.uk/static/pubs/final/stephen-goodwin.pdf

Gott, Anthony (22 October 2012)

FSA has issued a prohibition order against this individual, noting that in September 2011, he was convicted of three counts of obtaining a money transfer by deception, for which he was sentenced on 10 February 2012 to 24 months’ imprisonment, suspended for 24 months with a curfew requirement

http://www.fsa.gov.uk/static/pubs/final/anthony-gott.pdf

Green, Malcolm (9 November 2012)

FSA has issued a prohibition order against this individual on the grounds of fitness and properness, noting that on 30 January 2012, he was convicted of 20 counts of obtaining a money transfer by deception, 19 counts of fraud by abuse of position and 3 counts of false accounting, for which he was sentenced on 24 February 2012 to 5 years and 6 months imprisonment.

http://www.fsa.gov.uk/static/pubs/final/malcolm-green.pdf

20

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

Harrop, Terence John/ Principal Mortgage Services Limited (18 June 2012)

By these Final Notices, FSA issued a prohibition order against the individual, CEO of this small mortgage intermediary and publicly censured the firm and cancelled its Part IV permission. The firm entered into liquidation in 2010 and it is noted that FSA would have imposed a fine of £70,000 were it not for its financial circumstances. The firm had advised approximately 738 customers to take out interest only mortgages with a mortgage accelerator plan it had developed operated by a sister company. It charged an upfront fee and additional brokerage fee for the plan, but FSA notes that it amounted to an unregulated product and the firm was giving regulated advice to its customers on the plan. FSA considers that the plan was the main reason the firm recommended customers to take interest only mortgages and thus failed to pay due regard to customers’ interests. It did not disclose to customers that monies would be collected by the separate unauthorised sister firm. It misrepresented to customers that their funds would be ring fenced, but failed to make sure this was the case. As a result, customers have lost 45% of their funds held in the plan at the time both firms went into liquidation. The individual failed to ensure that the firm paid due regard to customers’ interests in recommending interest only mortgages with the plan to customers, regardless of whether that arrangement was the most appropriate or cost effective for the customer; failed to ensure that presentations and illustrations purporting to compare the recommended package with repayment mortgages were clear, fair and not misleading; failed to comply with his regulatory responsibilities, by failing to cooperate fully with FSA and by failing, to date, to repay his director’s loan to the firm ultimately to the detriment of consumers; and failed to ensure customers’ monies were adequately identified and protected, in his capacity as a director.

http://www.fsa.gov.uk/static/pubs/final/terence-harrop.pdf

http://www.fsa.gov.uk/static/pubs/final/pmsl.pdf

Hussain, Basharat (6 March 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that Mr Hussain has not notified FSA of a change in the address of his head office.

http://www.fsa.gov.uk/static/pubs/final/basharat-hussain.pdf

Hussain, Syed Itrat (4 May 2012, publicised 15 May 2012)

See under banks above (Habib Bank AG Zurich)

Jones, Reverend Carmel See under investment firms above (Pentecostal Credit Union Ltd)

Karan,Laila (27 June 2012)

Further to the recent Upper Tribunal Decision, FSA has now published this Final Notice which imposes a financial penalty and a prohibition n the order with effect from 27 June 2012).

£75,000 http://www.fsa.gov.uk/static/pubs/final/laila-karan.pdf

Karczewska, Ewa (February 2012, publicised July 2012)

FSA has published this Decision Notice setting out its reasons for objecting to the acquisition of at least 70% of the issued share capital of Think Finance.com by Ewa Karczewska. FSA’s concerns are summarised as lack of honesty and integrity; lack of reputation and experience directing the business; acquiring control without giving notice and repeated failure to comply with FSA requirements. In 2010, the individual had acquired 70% of the firm without seeking prior FSA approval and FSA states that there is now “considerable confusion” regarding the ownership of the firm. (February, publicized July 2012)

http://www.fsa.gov.uk/static/pubs/decisions/think-finance.pdf

21

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

Karpe, Sachin (27 June 2012)

Further to the recent Upper Tribunal Decision, FSA has now published this Final Notice which imposes a financial penalty and a prohibition n the order with effect from 27 June 2012

£1,250,000 http://www.fsa.gov.uk/static/pubs/final/sachin-karpe.pdf

King, Michele/ HD Administrators LLP (28 November 2012)

This Final Notice censures Michele King publicly, withdraws its approval for her to perform the controlled function of CF4 at the firm and issues her with a prohibition order. FSA reports that she breached Statement of Principle 6 by failing to exercise due skill, care and diligence in managing the business of the firm for which she was responsible in the performance of her controlled function – specifically, she failed to: understand, or take reasonable steps to understand, her regulatory responsibilities as an approved person. discharge, or take reasonable steps to discharge, her regulatory responsibilities as an approved person, including failure to take steps to inform herself of, the nature of the business conducted by the firm, including the basic function, operation and management of the pension scheme operated by the firm; understand or take steps to inform herself of the firm’s regulatory obligations; and involve herself in, or keep herself informed of, management decisions at the firm and the day-to-day operation of the firm.

http://www.fsa.gov.uk/static/pubs/final/michele-king.pdf

Kumagai, Yohichi (8 May 2012)

See under insurance firms above (Mitsui Sumitomo)

Kumarans Silk (5 January 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that it failed to submit Payment Services Directive Transactions return (the “FSA057”),

http://www.fsa.gov.uk/pubs/final/kumarans-silk.pdf

Laffrance, Martin Russell (20 March 2012)

FSA has issued a prohibition order against this individual, who had been the operations director at General Financial Centre, a Dorset-based mortgage broker which had arranged regulated mortgage contracts on a non-advised basis. FSA reports that, whilst an approved person performing controlled functions involving the exercise of significant influence at the firm between October 2004 to December 2008, he failed to meet the minimum regulatory standards in terms of competence and capability. In particular, he failed to: establish and maintain adequate systems and controls to prevent financial crime;; failed to adequately supervise and monitor staff who worked in the operations department and failed to understand (and take adequate steps to find out about) his responsibilities associated with regulated mortgage business and as an approved person, in particular his responsibilities as a director holding a controlled function.

http://www.fsa.gov.uk/static/pubs/final/martin-lafrance.pdf

Lawton, Andrew See under mortgage firms above (Cheshire Mortgage Corporation Ltd)

22

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

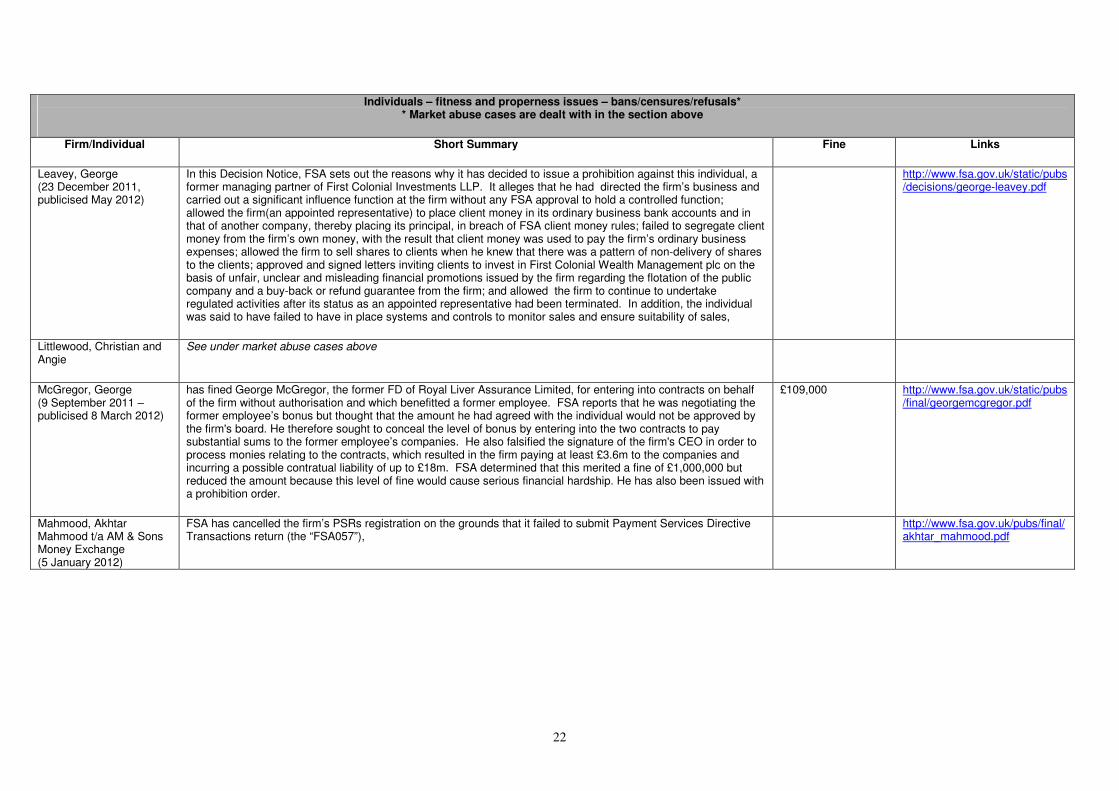

Leavey, George (23 December 2011, publicised May 2012)

In this Decision Notice, FSA sets out the reasons why it has decided to issue a prohibition against this individual, a former managing partner of First Colonial Investments LLP. It alleges that he had directed the firm’s business and carried out a significant influence function at the firm without any FSA approval to hold a controlled function; allowed the firm(an appointed representative) to place client money in its ordinary business bank accounts and in that of another company, thereby placing its principal, in breach of FSA client money rules; failed to segregate client money from the firm’s own money, with the result that client money was used to pay the firm’s ordinary business expenses; allowed the firm to sell shares to clients when he knew that there was a pattern of non-delivery of shares to the clients; approved and signed letters inviting clients to invest in First Colonial Wealth Management plc on the basis of unfair, unclear and misleading financial promotions issued by the firm regarding the flotation of the public company and a buy-back or refund guarantee from the firm; and allowed the firm to continue to undertake regulated activities after its status as an appointed representative had been terminated. In addition, the individual was said to have failed to have in place systems and controls to monitor sales and ensure suitability of sales,

http://www.fsa.gov.uk/static/pubs/decisions/george-leavey.pdf

Littlewood, Christian and Angie

See under market abuse cases above

McGregor, George (9 September 2011 – publicised 8 March 2012)

has fined George McGregor, the former FD of Royal Liver Assurance Limited, for entering into contracts on behalf of the firm without authorisation and which benefitted a former employee. FSA reports that he was negotiating the former employee’s bonus but thought that the amount he had agreed with the individual would not be approved by the firm's board. He therefore sought to conceal the level of bonus by entering into the two contracts to pay substantial sums to the former employee’s companies. He also falsified the signature of the firm's CEO in order to process monies relating to the contracts, which resulted in the firm paying at least £3.6m to the companies and incurring a possible contratual liability of up to £18m. FSA determined that this merited a fine of £1,000,000 but reduced the amount because this level of fine would cause serious financial hardship. He has also been issued with a prohibition order.

£109,000 http://www.fsa.gov.uk/static/pubs/final/georgemcgregor.pdf

Mahmood, Akhtar Mahmood t/a AM & Sons Money Exchange (5 January 2012)

FSA has cancelled the firm’s PSRs registration on the grounds that it failed to submit Payment Services Directive Transactions return (the “FSA057”),

http://www.fsa.gov.uk/pubs/final/akhtar_mahmood.pdf

23

Individuals – fitness and properness issues – bans/censures/refusals* * Market abuse cases are dealt with in the section above

Firm/Individual Short Summary Fine Links

Micalizzi, Alberto/Dynamic Decisions Capital Management Ltd (20 April 2012, publicised 30 May 2012)