Embed Size (px)

Citation preview

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

FROM EQUITY RESEARCH

Poultry : Key Meeting Takeaways with Pinsar ( Neutral ) From our meeting, we learnt that Pinsar is expecting broiler and Day Old Chick (DOC) prices to remain high this year mainly due to undersupply and higher corn costs. The undersupply owes to the lowest Grand Parent Stock (GPS) import quota back in 2016, thus affecting 2019 Final Stock (FS) production. Meanwhile, higher local corn costs due to the import ban are likely to push broiler prices higher as the cost of production will remain elevated.

To see the full version of this report, please Click here

MARKET NEWS

SECTOR Indonesia B20 distribution reached 89% in Jan 19

CORPORATE HMSP (BUY - TP: IDR 4,200): Flat 4Q18 sales volume, FY18

+0.1% yoy*

New submarine cable available for Indosat Jasa Marga: Plans to issue Dinfra worth IDR700bn in 1Q19

Semen Indonesia: Expects exports to reach more than 4.0mn tons in 2019

Vale Indonesia (INCO): Flattish nickel-in-matte production expected in 2019

Waskita Karya: Plans to divest 6 toll roads in 2019

PREVIOUS REPORT

Strategy: 2018 GDP: Highest growth pace since 2013

Click here Media: MNCN has begun the year well Click here

Telco Price Tracker: January heralds more product revisions Click here

Vale Indonesia: 4Q18: Weak profit on lower ASP and higher

costs Click here Japfa Comfeed Indonesia: Take a break Click here

Unilever Indonesia: Profits boosted by one-off gains Click here

Bank Rakyat Indonesia: Still a very profitable bank Click here Charoen Pokphand Indonesia: Thank you, next Click here

KEY INDEX

Close

Chg Ytd Vol

(%) (%) (US$ m)

Asean - 5

Indonesia 6.536 (0,2) 5,5 485

Thailand 1.653 (0,3) 5,7 1.598

Philippines 8.100 0,5 8,5 137

Malaysia 1.693 0,6 0,2 216

Singapore 3.201 0,5 4,3 662

Regional

China 2.618 1,3 5,0 23.814

Hong Kong 27.990 0,2 8,3 5.206

Japan 20.751 (0,6) 3,7 14.656

Korea 2.187 (0,8) 7,1 6.101

Taiwan 9.932 0,0 2,1 3.235

India 36.971 (0,0) 2,5 385

NASDAQ 7.288 (1,2) 9,8 113.674

Dow Jones 25.170 (0,9) 7,9 10.500

CURRENCY AND INTEREST RATE

Rate

w-w m-m ytd

(%) (%) (%)

Rupiah Rp/1US$ 13.973 - 0,8 2,9

BI7DRRR % 6,00 - - -

10y Gov Indo bond 7,81 (0,1) (0,1) (0,2)

HARD COMMODITY

Unit Price

d-d m-m ytd

(%) (%) (%)

Coal US$/ton 98 (0,5) (1,3) (4,2)

Gold US$/toz 1.310 0,0 1,9 2,2

Nickel US$/mt.ton 12.910 0,4 16,5 21,7

Tin US$/mt.ton 21.000 (0,3) 6,1 7,6

SOFT COMMODITY

Unit Price

d-d m-m ytd

(%) (%) (%)

Cocoa US$/mt.ton 2.245 1,6 (3,0) (5,1)

Corn US$/mt.ton 135 (0,9) - 1,8

Oil (WTI) US$/barrel 53 (0,2) 5,5 15,7

Oil (Brent) US$/barrel 62 (1,7) 7,5 14,6

Palm oil MYR/mt.ton 2.093 (1,6) 2,6 7,2

Rubber USd/kg 132 (0,5) (4,8) 5,5

Pulp US$/tonne 1.205 N/A 2,8 20,5

Coffee US$/60kgbag 80 0,1 0,8 1,1

Sugar US$/MT 338 (1,1) (2,1) 1,6

Wheat US$/ton 140 (2,4) (0,7) 2,0

Soy Oil US$/lb 31 (0,3) 9,0 11,8

Soy Bean US$/by 913 (0,9) 0,1 3,5

Source: Bloomberg

Equity Research Poultry

See important disclosure at the back of this report www.danareksa.com

Friday,08 February 2019

Poultry NEUTRAL

Key Meeting Takeaways with Pinsar

From our meeting, we learnt that Pinsar is expecting broiler and Day Old Chick (DOC) prices to remain high this year mainly due to undersupply and higher corn costs. The undersupply owes to the lowest Grand Parent Stock (GPS) import quota back in 2016, thus affecting 2019 Final Stock (FS) production. Meanwhile, higher local corn costs due to the import ban are likely to push broiler prices higher as the cost of production will remain elevated. Expect prices to surge due to the general elections and Lebaran. Pinsar is expecting broiler and DOC prices to increase this year as supply is expected to remain tight. The peak of chicken prices is expected to materialize in April, affected by the general elections and Lebaran. However, the government may feel the need to act given the upcoming elections. To lower chicken prices, the government can either allow corn imports or end the ban on chicken imports. The government is, however, hesitant to allow corn imports as data from the Ministry of Agriculture shows that corn production is in surplus. Allowing chickens to be imported is the last resort to reduce prices as this move would affect the long-term supply-demand dynamics in Indonesia’s poultry industry.

Farmers want the ban on corn imports lifted. Farmers would oppose chicken imports as the cost of production in Indonesia is still high, i.e. broiler prices from Brazil can be as low as IDR 12,000/kg. After losing in the World Trade Organization (WTO) regarding the ban on chicken imports, chicken products from Brazil are a possibility. The government is currently negotiating through a bilateral agreement. Negotiations to lift the ban on corn imports are still being held between farmers and the government. Cheap corn stocks in feed millers’ silos can only last for another 25 days. If corn costs are high, poultry feed producers are likely to pass on the higher raw material costs. The new corn costs range from IDR 6,000-6,300/kg which reflects the late harvest season in late 2018.

The AGP ban is reducing productivity but opening room for exports. After banning the use of AGP, farmers experienced a higher mortality rate and a lower productivity ratio. The Feed Conversion Ratio (FCR) for open house and close house increased to 1.3x and 1.6x from 1.1x and 1.3x, respectively. However, since the antibiotic content in broilers due to the use of AGP is higher than the standard in most countries, broilers were rarely exported. Now with the absence of AGP, there may be room to export broilers. Feasibility studies from Saudi Arabia and Japan are being conducted.

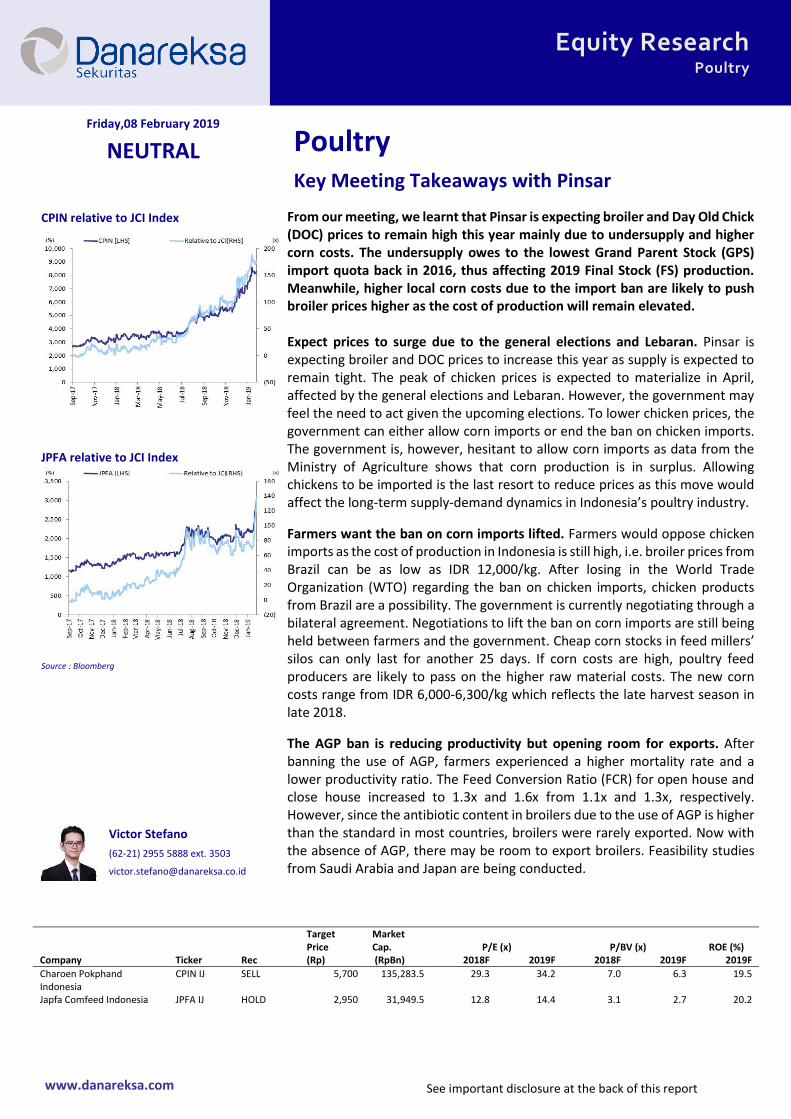

CPIN relative to JCI Index

xxxx

JPFA relative to JCI Index

xxxx Source : Bloomberg

x Victor Stefano

(62-21) 2955 5888 ext. 3503

Target Price

Market Cap. P/E (x) P/BV (x) ROE (%)

Company Ticker Rec (Rp) (RpBn) 2018F 2019F 2018F 2019F 2019F

Charoen Pokphand Indonesia

CPIN IJ SELL 5,700 135,283.5 29.3 34.2 7.0 6.3 19.5

Japfa Comfeed Indonesia JPFA IJ HOLD 2,950 31,949.5 12.8 14.4 3.1 2.7 20.2

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

SECTOR Indonesia B20 distribution reached 89% in Jan 19

According to the local press, Indonesia’s B20 distribution reached 89% in Jan 19. The lower-than-expected

realization mostly owed to: 1) distribution disruption caused by unfavorable weather and high tides and 2) the fact that the Tuban floating storage for the biodiesel mix has yet to operate optimally. (Kontan)

CORPORATE

HMSP (BUY - TP: IDR 4,200): Flat 4Q18 sales volume, FY18 +0.1% yoy* HMSP’s FY18 sales volume rose 0.1% yoy (lower than our estimate of 0.3% yoy), driven by Dji Sam Soe (DSS)

(+28.3% yoy), mainly supported by Magnum Mild 16s. By contrast, Sampoerna A reported declining sales volume

(-7.5% yoy) – following the impact of its higher retail selling prices. Based on our survey, Sampoerna A 16s retail selling prices in 4Q18 were around IDR23,500/pack, +11.9% yoy.

HMSP maintained its FY18 market share at 33%, mainly supported by increasing market share of DSS to 9.5%

(FY17: 7.4%), while Sampoerna A and other brands booked lower market share.

On a quarterly basis, HMSP reported flat 4Q18 sales volume yoy but up 1.5% qoq – mainly supported by DSS and

Sampoerna A. However, lower 4Q18 market share of Sampoerna A and Other brands put pressure on HMSP’s 4Q18 market share, which declined to 32.7% (3Q18: 33%).

FY17 FY18 yoy 4Q17 3Q18 4Q18 yoy qoq

HMSP (mn sticks) 101,300 101,400 0.1% 26,900 26,500 26,900 0.0% 1.5%

Volume by brands Sampoerna A (mn sticks) 42,736 39,522 -7.5% 11,724 10,333 10,391 -11.4% 0.6%

Dji Sam Soe (mn sticks 22,757 29,195 28.3% 7,065 7,578 8,044 13.9% 6.1%

Others (mn sticks) 35,807 32,683 -8.7% 8,111 8,589 8,465 4.4% -1.4%

Market share 33.0% 33.0% 33.0% 33.0% 32.7% Industry volume (mn sticks) 307,400 307,000 -0.1% 81,500 80,300 82,100 0.7% 2.2%

Source: PMI

New submarine cable available for Indosat

Indosat Ooredoo along with companies like Google, Singtel, and Telstra recently announced the implementation of

the INDIGO submarine cable system with the completion of the «West Indigo» cable and «Indigo Central» cable on time. The cables completed are the Singapore 4,600km undersea cable to Perth (Indigo West) and another 4,600

km cable between Perth and Sydney (Indigo Central). Transmission testing will begin immediately and the cables are targeted to be ready for use before mid-2019. The CTO of Indosat Ooredoo commented that the INDIGO

submarine cable is part of Indosat Ooredoo's ambitious three-year program and once operational, it will increasingly

scale up the traffic between Australia and SE Asia providing lower latency and increased reliability.

Jasa Marga: Plans to issue Dinfra worth IDR700bn in 1Q19 Jasa Marga (JSMR) seeks to raise IDR700bn from the issuance of a new financing instrument, Dinfra, in 1Q19. The

asset underlying this instrument is the Gempol – Pandaan toll road (13.6km). (Bisnis Indonesia)

MARKET NEWS

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

Waskita Karya: Plans to divest 6 toll roads in 2019 Waskita Toll Road (WTR), a subsidiary of Waskita Karya (WSKT), seeks to raise ~IDR10.0tn from the divestment of

6 toll roads in 2019. The toll roads are: Pejagan – Pemalang, Kanci – Pejagan, Pasuruan – Probolinggo, Bekasi – Cawang – Kampung Melayu, Solo – Ngawi, and Batang – Semarang. In 2018. WTR divested a 70% stake in Waskita

Transjawa Tollroad by issuing a mutual fund (RDPT) and raised IDR5.0tn. WTR owns 18 toll roads with a total

length of 1,015km. Around 468km of the toll roads are in operation. The equity investment needed to build the 18 toll roads is IDR34.7tn, while WTR had collected IDR20.0tn as of 2018. As such, WTR needs another ~IDR14.7tn of

funds for the equity investment. (Bisnis Indonesia)

Semen Indonesia: Expects exports to reach more than 4.0mn tons in 2019

Semen Indonesia (SMGR) targets cement exports of 4.0mn tons in 2019, higher than the ~3.0mn tons booked in

2018. In the sector, most cement producers have increased exports to help production achieve economies of scale. Total cement exports from Indonesia have increased significantly from only 2.9mn tons in 2015 to 5.7mn tons in

2018. The Indonesian Cement Association (ASI) expects cement exports to reach 7.0mn tons in 2019, +22.8%yoy. Export destinations include: Sri Lanka, Tahiti, Timor-Leste, Tonga, UAE, Yemen, the Philippines, China, Australia,

Austria, Maldives, India, and Bangladesh. The higher exports have been possible given the large idle production

capacity in the sector since domestic capacity has reached 110mn tons while domestic demand is only 69.5mn tons, translating into a utilization rate of 63.2%. (Bisnis Indonesia)

Vale Indonesia (INCO): Flattish nickel-in-matte production expected in 2019 Vale Indonesia (INCO) expects flattish nickel-in-matte production of around 74,000 – 76,000 tons in 2019 from

74,806 tons in the previous year as the company plans to modernize its hydro power plant that has been operated for about 40 years. This will require a shutdown of 10 weeks of the Larona Canal Lining. Meanwhile, in regard to

the divestment of a 20% stake, INCO has sent a letter to MEMR and the company expects the divestment process to be conducted through business to business (B to B) before October 2019. (Source: Bisnis Indonesia)

Danareksa Sekuritas – Equity SNAPSHOT

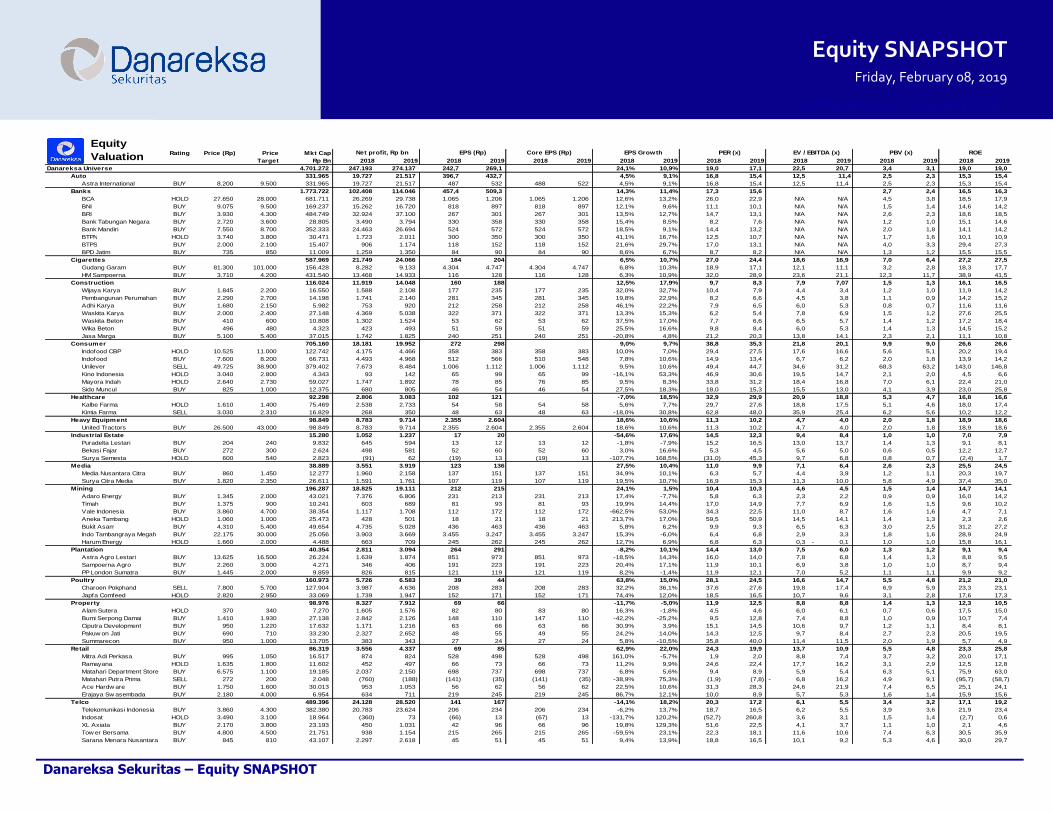

DANAREKSA VALUATION

Equity SNAPSHOT Friday, February 08, 2019

Rating Price (Rp) Price Mkt Cap

Target Rp Bn 2018 2019 2018 2019 2018 2019 2018 2019 2018 2019 2018 2019 2018 2019 2018 2019

Danareksa Universe 4.701.272 247.193 274.137 242,7 269,1 24,1% 10,9% 19,0 17,1 22,5 20,7 3,4 3,1 19,0 19,0

Auto 331.965 19.727 21.517 396,7 432,7 4,5% 9,1% 16,8 15,4 12,5 11,4 2,5 2,3 15,3 15,4

Astra International BUY 8.200 9.500 331.965 19.727 21.517 487 532 488 522 4,5% 9,1% 16,8 15,4 12,5 11,4 2,5 2,3 15,3 15,4

Banks 1.773.722 102.408 114.046 457,4 509,3 14,3% 11,4% 17,3 15,6 2,7 2,4 16,5 16,3

BCA HOLD 27.650 28.000 681.711 26.269 29.738 1.065 1.206 1.065 1.206 12,6% 13,2% 26,0 22,9 N/A N/A 4,5 3,8 18,5 17,9

BNI BUY 9.075 9.500 169.237 15.262 16.720 818 897 818 897 12,1% 9,6% 11,1 10,1 N/A N/A 1,5 1,4 14,6 14,2

BRI BUY 3.930 4.300 484.749 32.924 37.100 267 301 267 301 13,5% 12,7% 14,7 13,1 N/A N/A 2,6 2,3 18,6 18,5

Bank Tabungan Negara BUY 2.720 3.600 28.805 3.490 3.794 330 358 330 358 15,4% 8,5% 8,2 7,6 N/A N/A 1,2 1,0 15,1 14,6

Bank Mandiri BUY 7.550 8.700 352.333 24.463 26.694 524 572 524 572 18,5% 9,1% 14,4 13,2 N/A N/A 2,0 1,8 14,1 14,2

BTPN HOLD 3.740 3.800 30.471 1.723 2.011 300 350 300 350 41,1% 16,7% 12,5 10,7 N/A N/A 1,7 1,6 10,1 10,9

BTPS BUY 2.000 2.100 15.407 906 1.174 118 152 118 152 21,6% 29,7% 17,0 13,1 N/A N/A 4,0 3,3 29,4 27,3

BPD Jatim BUY 735 850 11.009 1.259 1.350 84 90 84 90 8,6% 6,7% 8,7 8,2 N/A N/A 1,3 1,2 15,5 15,5

Cigarettes 587.969 21.749 24.066 184 204 6,5% 10,7% 27,0 24,4 18,6 16,9 7,0 6,4 27,2 27,5

Gudang Garam BUY 81.300 101.000 156.428 8.282 9.133 4.304 4.747 4.304 4.747 6,8% 10,3% 18,9 17,1 12,1 11,1 3,2 2,8 18,3 17,7

HM Sampoerna BUY 3.710 4.200 431.540 13.468 14.933 116 128 116 128 6,3% 10,9% 32,0 28,9 23,6 21,1 12,3 11,7 38,9 41,5

Construction 116.024 11.919 14.048 160 188 12,5% 17,9% 9,7 8,3 7,9 7,07 1,5 1,3 16,1 16,5

Wijaya Karya BUY 1.845 2.200 16.550 1.588 2.108 177 235 177 235 32,0% 32,7% 10,4 7,9 4,4 3,4 1,2 1,0 11,9 14,2

Pembangunan Perumahan BUY 2.290 2.700 14.198 1.741 2.140 281 345 281 345 19,8% 22,9% 8,2 6,6 4,5 3,8 1,1 0,9 14,2 15,2

Adhi Karya BUY 1.680 2.150 5.982 753 920 212 258 212 258 46,1% 22,2% 7,9 6,5 6,0 5,3 0,8 0,7 11,6 11,6

Waskita Karya BUY 2.000 2.400 27.148 4.369 5.038 322 371 322 371 13,3% 15,3% 6,2 5,4 7,8 6,9 1,5 1,2 27,6 25,5

Waskita Beton BUY 410 600 10.808 1.302 1.524 53 62 53 62 37,5% 17,0% 7,7 6,6 6,5 5,7 1,4 1,2 17,2 18,4

Wika Beton BUY 496 480 4.323 423 493 51 59 51 59 25,5% 16,6% 9,8 8,4 6,0 5,3 1,4 1,3 14,5 15,2

Jasa Marga BUY 5.100 5.400 37.015 1.742 1.825 240 251 240 251 -20,8% 4,8% 21,2 20,3 13,8 14,1 2,3 2,1 11,1 10,8

Consumer 705.160 18.181 19.952 272 298 9,0% 9,7% 38,8 35,3 21,8 20,1 9,9 9,0 26,6 26,6

Indofood CBP HOLD 10.525 11.000 122.742 4.175 4.466 358 383 358 383 10,0% 7,0% 29,4 27,5 17,6 16,6 5,6 5,1 20,2 19,4

Indofood BUY 7.600 8.200 66.731 4.493 4.968 512 566 510 548 7,8% 10,6% 14,9 13,4 6,7 6,2 2,0 1,8 13,9 14,2

Unilever SELL 49.725 38.900 379.402 7.673 8.484 1.006 1.112 1.006 1.112 9,5% 10,6% 49,4 44,7 34,6 31,2 68,3 63,2 143,0 146,8

Kino Indonesia HOLD 3.040 2.800 4.343 93 142 65 99 65 99 -16,1% 53,3% 46,9 30,6 19,5 14,7 2,1 2,0 4,5 6,6

Mayora Indah HOLD 2.640 2.730 59.027 1.747 1.892 78 85 76 85 9,5% 8,3% 33,8 31,2 18,4 16,8 7,0 6,1 22,4 21,0

Sido Muncul BUY 825 1.000 12.375 680 805 46 54 46 54 27,5% 18,3% 18,0 15,3 15,5 13,0 4,1 3,9 23,0 25,8

Healthcare 92.298 2.806 3.083 102 121 -7,0% 18,5% 32,9 29,9 20,9 18,8 5,3 4,7 16,8 16,6

Kalbe Farma HOLD 1.610 1.400 75.469 2.538 2.733 54 58 54 58 5,6% 7,7% 29,7 27,6 18,8 17,5 5,1 4,6 18,0 17,4

Kimia Farma SELL 3.030 2.310 16.829 268 350 48 63 48 63 -18,0% 30,8% 62,8 48,0 35,9 25,4 6,2 5,6 10,2 12,2

Heavy Equipment 98.849 8.783 9.714 2.355 2.604 18,6% 10,6% 11,3 10,2 4,7 4,0 2,0 1,8 18,9 18,6

United Tractors BUY 26.500 43.000 98.849 8.783 9.714 2.355 2.604 2.355 2.604 18,6% 10,6% 11,3 10,2 4,7 4,0 2,0 1,8 18,9 18,6

Industrial Estate 15.280 1.052 1.237 17 20 -54,6% 17,6% 14,5 12,3 9,4 8,4 1,0 1,0 7,0 7,9

Puradelta Lestari BUY 204 240 9.832 645 594 13 12 13 12 -1,8% -7,9% 15,2 16,5 13,0 13,7 1,4 1,3 9,1 8,1

Bekasi Fajar BUY 272 300 2.624 498 581 52 60 52 60 3,0% 16,6% 5,3 4,5 5,6 5,0 0,6 0,5 12,2 12,7

Surya Semesta HOLD 600 540 2.823 (91) 62 (19) 13 (19) 13 -107,7% 168,5% (31,0) 45,3 9,7 6,8 0,8 0,7 (2,4) 1,7

Media 38.889 3.551 3.919 123 136 27,5% 10,4% 11,0 9,9 7,1 6,4 2,6 2,3 25,5 24,5

Media Nusantara Citra BUY 860 1.450 12.277 1.960 2.158 137 151 137 151 34,9% 10,1% 6,3 5,7 4,4 3,9 1,2 1,1 20,3 19,7

Surya Citra Media BUY 1.820 2.350 26.611 1.591 1.761 107 119 107 119 19,5% 10,7% 16,9 15,3 11,3 10,0 5,8 4,9 37,4 35,0

Mining 196.287 18.825 19.111 212 215 24,1% 1,5% 10,4 10,3 4,6 4,5 1,5 1,4 14,7 14,1

Adaro Energy BUY 1.345 2.000 43.021 7.376 6.806 231 213 231 213 17,4% -7,7% 5,8 6,3 2,3 2,2 0,9 0,9 16,0 14,2

Timah BUY 1.375 900 10.241 603 689 81 93 81 93 19,9% 14,4% 17,0 14,9 7,7 6,9 1,6 1,5 9,6 10,2

Vale Indonesia BUY 3.860 4.700 38.354 1.117 1.708 112 172 112 172 -662,5% 53,0% 34,3 22,5 11,0 8,7 1,6 1,6 4,7 7,1

Aneka Tambang HOLD 1.060 1.000 25.473 428 501 18 21 18 21 213,7% 17,0% 59,5 50,9 14,5 14,1 1,4 1,3 2,3 2,6

Bukit Asam BUY 4.310 5.400 49.654 4.735 5.028 436 463 436 463 5,8% 6,2% 9,9 9,3 6,5 6,3 3,0 2,5 31,2 27,2

Indo Tambangraya Megah BUY 22.175 30.000 25.056 3.903 3.669 3.455 3.247 3.455 3.247 15,3% -6,0% 6,4 6,8 2,9 3,3 1,8 1,6 28,9 24,9

Harum Energy HOLD 1.660 2.000 4.488 663 709 245 262 245 262 12,7% 6,9% 6,8 6,3 0,3 0,1- 1,0 1,0 15,8 16,1

Plantation 40.354 2.811 3.094 264 291 -8,2% 10,1% 14,4 13,0 7,5 6,0 1,3 1,2 9,1 9,4

Astra Agro Lestari BUY 13.625 16.500 26.224 1.639 1.874 851 973 851 973 -18,5% 14,3% 16,0 14,0 7,8 6,8 1,4 1,3 8,8 9,5

Sampoerna Agro BUY 2.260 3.000 4.271 346 406 191 223 191 223 20,4% 17,1% 11,9 10,1 6,9 3,8 1,0 1,0 8,7 9,4

PP London Sumatra BUY 1.445 2.000 9.859 826 815 121 119 121 119 8,2% -1,4% 11,9 12,1 7,0 5,2 1,1 1,1 9,9 9,2

Poultry 160.973 5.726 6.583 39 44 63,8% 15,0% 28,1 24,5 16,6 14,7 5,5 4,8 21,2 21,0

Charoen Pokphand SELL 7.800 5.700 127.904 3.987 4.636 208 283 208 283 32,2% 36,1% 37,6 27,6 19,8 17,4 6,9 5,9 23,3 23,1

Japfa Comfeed HOLD 2.820 2.950 33.069 1.739 1.947 152 171 152 171 74,4% 12,0% 18,5 16,5 10,7 9,6 3,1 2,8 17,6 17,3

Property 98.976 8.327 7.912 69 66 -11,7% -5,0% 11,9 12,5 8,8 8,8 1,4 1,3 12,3 10,5

Alam Sutera HOLD 370 340 7.270 1.605 1.576 82 80 83 80 16,3% -1,8% 4,5 4,6 6,0 6,1 0,7 0,6 17,5 15,0

Bumi Serpong Damai BUY 1.410 1.930 27.138 2.842 2.126 148 110 147 110 -42,2% -25,2% 9,5 12,8 7,4 8,8 1,0 0,9 10,7 7,4

Ciputra Development BUY 950 1.220 17.632 1.171 1.216 63 66 63 66 30,9% 3,9% 15,1 14,5 10,6 9,7 1,2 1,1 8,4 8,1

Pakuw on Jati BUY 690 710 33.230 2.327 2.652 48 55 49 55 24,2% 14,0% 14,3 12,5 9,7 8,4 2,7 2,3 20,5 19,5

Summarecon BUY 950 1.000 13.705 383 343 27 24 27 24 5,8% -10,5% 35,8 40,0 11,4 11,5 2,0 1,9 5,7 4,9

Retail 86.319 3.556 4.337 69 85 62,9% 22,0% 24,3 19,9 13,7 10,9 5,5 4,8 23,3 25,8

Mitra Adi Perkasa BUY 995 1.050 16.517 874 824 528 498 528 498 161,0% -5,7% 1,9 2,0 8,8 7,4 3,7 3,2 20,0 17,1

Ramayana HOLD 1.635 1.800 11.602 452 497 66 73 66 73 11,2% 9,9% 24,6 22,4 17,7 16,2 3,1 2,9 12,5 12,8

Matahari Department Store BUY 6.575 1.100 19.185 2.037 2.150 698 737 698 737 6,8% 5,6% 9,4 8,9 5,9 5,4 6,3 5,1 75,9 63,0

Matahari Putra Prima SELL 272 200 2.048 (760) (188) (141) (35) (141) (35) -38,9% 75,3% (1,9) (7,8) 6,8- 16,2 4,9 9,1 (95,7) (58,7)

Ace Hardw are BUY 1.750 1.600 30.013 953 1.053 56 62 56 62 22,5% 10,6% 31,3 28,3 24,6 21,9 7,4 6,5 25,1 24,1

Erajaya Sw asembada BUY 2.180 4.000 6.954 634 711 219 245 219 245 86,7% 12,1% 10,0 8,9 5,7 5,3 1,6 1,4 15,9 15,6

Telco 489.396 24.128 28.520 141 167 -14,1% 18,2% 20,3 17,2 6,1 5,5 3,4 3,2 17,1 19,2

Telekomunikasi Indonesia BUY 3.860 4.300 382.380 20.783 23.624 206 234 206 234 -6,2% 13,7% 18,7 16,5 6,2 5,5 3,9 3,6 21,9 23,4

Indosat HOLD 3.490 3.100 18.964 (360) 73 (66) 13 (67) 13 -131,7% 120,2% (52,7) 260,8 3,6 3,1 1,5 1,4 (2,7) 0,6

XL Axiata BUY 2.170 3.800 23.193 450 1.031 42 96 66 96 19,8% 129,3% 51,6 22,5 4,1 3,7 1,1 1,0 2,1 4,6

Tow er Bersama BUY 4.800 4.500 21.751 938 1.154 215 265 215 265 -59,5% 23,1% 22,3 18,1 11,6 10,6 7,4 6,3 30,5 35,9

Sarana Menara Nusantara BUY 845 810 43.107 2.297 2.618 45 51 45 51 9,4% 13,9% 18,8 16,5 10,1 9,2 5,3 4,6 30,0 29,7

PER (x)

Equity

Valuation Net profit, Rp bn EPS (Rp) Core EPS (Rp) EPS Growth ROE EV / EBITDA (x) PBV (x)

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

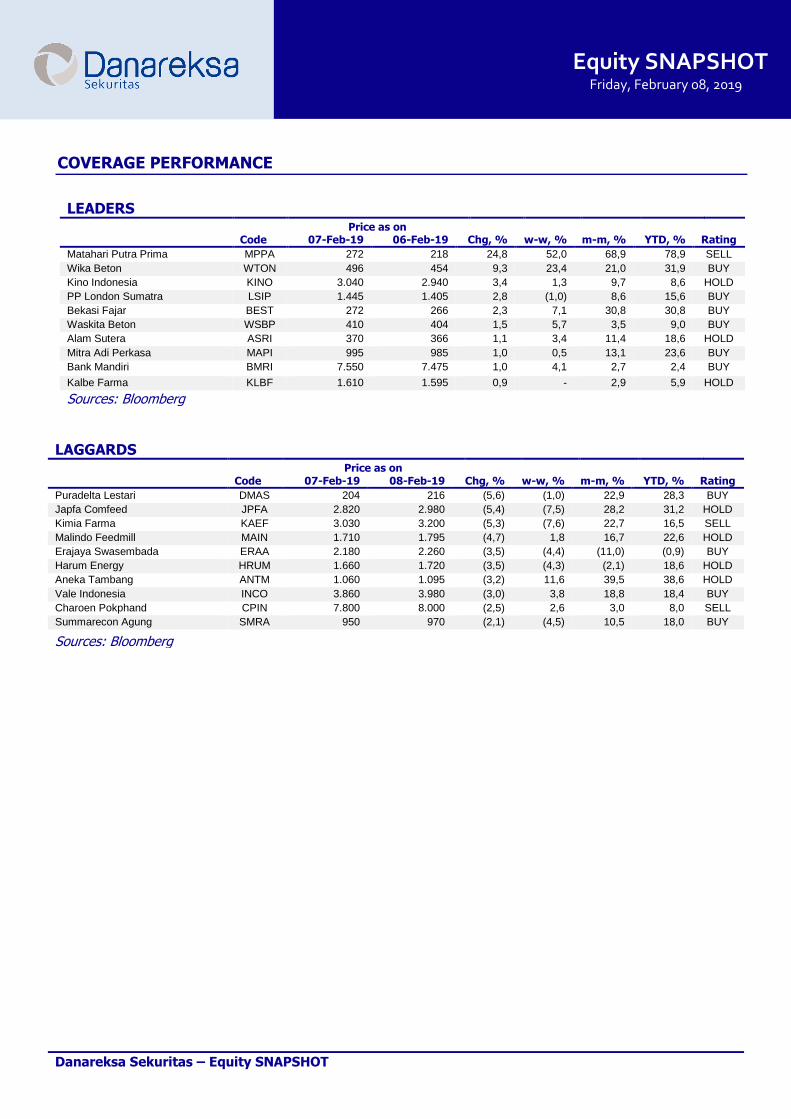

LEADERS Price as on Code 07-Feb-19 06-Feb-19 Chg, % w-w, % m-m, % YTD, % Rating

Matahari Putra Prima MPPA 272 218 24,8 52,0 68,9 78,9 SELL

Wika Beton WTON 496 454 9,3 23,4 21,0 31,9 BUY

Kino Indonesia KINO 3.040 2.940 3,4 1,3 9,7 8,6 HOLD

PP London Sumatra LSIP 1.445 1.405 2,8 (1,0) 8,6 15,6 BUY

Bekasi Fajar BEST 272 266 2,3 7,1 30,8 30,8 BUY

Waskita Beton WSBP 410 404 1,5 5,7 3,5 9,0 BUY

Alam Sutera ASRI 370 366 1,1 3,4 11,4 18,6 HOLD

Mitra Adi Perkasa MAPI 995 985 1,0 0,5 13,1 23,6 BUY

Bank Mandiri BMRI 7.550 7.475 1,0 4,1 2,7 2,4 BUY

Kalbe Farma KLBF 1.610 1.595 0,9 - 2,9 5,9 HOLD

Sources: Bloomberg

LAGGARDS Price as on Code 07-Feb-19 08-Feb-19 Chg, % w-w, % m-m, % YTD, % Rating

Puradelta Lestari DMAS 204 216 (5,6) (1,0) 22,9 28,3 BUY

Japfa Comfeed JPFA 2.820 2.980 (5,4) (7,5) 28,2 31,2 HOLD

Kimia Farma KAEF 3.030 3.200 (5,3) (7,6) 22,7 16,5 SELL

Malindo Feedmill MAIN 1.710 1.795 (4,7) 1,8 16,7 22,6 HOLD

Erajaya Swasembada ERAA 2.180 2.260 (3,5) (4,4) (11,0) (0,9) BUY

Harum Energy HRUM 1.660 1.720 (3,5) (4,3) (2,1) 18,6 HOLD

Aneka Tambang ANTM 1.060 1.095 (3,2) 11,6 39,5 38,6 HOLD

Vale Indonesia INCO 3.860 3.980 (3,0) 3,8 18,8 18,4 BUY

Charoen Pokphand CPIN 7.800 8.000 (2,5) 2,6 3,0 8,0 SELL

Summarecon Agung SMRA 950 970 (2,1) (4,5) 10,5 18,0 BUY

Sources: Bloomberg

COVERAGE PERFORMANCE

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

PREVIOUS REPORTS

Strategy : 2018 GDP: Highest growth pace since 2013, Media: MNCN has begun the year well, Telco Price

Tracker: January heralds more product revisions SnapShot20190207 Vale Indonesia: 4Q18: Weak profit on lower ASP and higher costs SnapShot20190206

Japfa Comfeed Indonesia : Take a break, Unilever Indonesia: Profits boosted by one-off gains SnapShot20190201 Bank Rakyat Indonesia: Still a very profitable bank SnapShot20190131

Charoen Pokphand Indonesia: Thank you, next, Danareksa Consumer Confidence: More Optimistic at the Beginning of the Year SnapShot20190130

Bank Mandiri: Standing firm SnapShot20190129

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

PT Danareksa Sekuritas

Jl. Medan Merdeka Selatan No. 14 Jakarta 10110 Indonesia Tel (62 21) 29 555 888 Fax (62 21) 350 1709

Equity Research Team S

Sales team

Maria Renata

[email protected] (62-21) 29555 888 ext.3513 Construction

Stefanus Darmagiri

[email protected] (62-21) 2955 888 ext. 3530 Auto, Coal, Heavy Equip, Metal

Natalia Sutanto

[email protected] (62-21) 29555 888 ext.3508 Consumer, Tobacco, Property

Niko Margaronis

[email protected] (62-21) 29555 888 ext.3512 Telco, Tower

Helmy Kristanto

[email protected] (62-21) 2955 888 ext. 3500

Head of Research, Strategy

Eka Savitri

[email protected] (62-21) 29555 888 ext.3506 Banking

Yudha Gautama

[email protected] (62-21) 29555 888 ext.3509

Plantation, Property

Ehrliech Suhartono

[email protected] (62-21) 29555 888 ext. 3132

Laksmita Armandani

[email protected] (62-21) 29555 888 ext. 3125

Vera Ongyono

[email protected] (62-21) 29555 888 ext. 3120

Tuty Sutopo

[email protected] (62-21) 29555 888 ext. 3121

Wisnu Budhiargo

(62-21) 29555 888 ext. 3117

Upik Yuzarni

[email protected] (62-21) 29555 888 ext. 3137

Rendy Ben Philips

(62-21) 29555 888 ext. 3148

Thalia Kadharusman

[email protected] (62-21) 29555 888 ext. 3124

Adeline Solaiman

(62-21) 29555 888 ext. 3503

Victor Stefano

[email protected] (62-21) 29555 888 ext.3503 Poultry, Property

Ignatius Teguh Prayoga

[email protected] (62-21) 29555 888 ext.3511 Media, Research Associate

Equity SNAPSHOT Friday, February 08, 2019

Danareksa Sekuritas – Equity SNAPSHOT

Disclaimer

The information contained in this report has been taken from sources which we deem reliable. However, none of P.T. Danareksa Sekuritas and/or its affiliated companies and/or their respective employees and/or agents makes any representation or warranty (express or implied) or accepts any responsibility or liability as to, or in relation to, the accuracy or completeness of the information and opinions contained in this report or as to any information contained in this report or any other such information

or opinions remaining unchanged after the issue thereof.

We expressly disclaim any responsibility or liability (express or implied) of P.T. Danareksa Sekuritas, its affiliated companies and their respective employees and agents

whatsoever and howsoever arising (including, without limitation for any claims, proceedings, action , suits, losses, expenses, damages or costs) which may be brought against or suffered by any person as a results of acting in reliance upon the whole or any part of the contents of this report and neither P.T. Danareksa Sekuritas, its

affiliated companies or their respective employees or agents accepts liability for any errors, omissions or misstatements, negligent or otherwise, in the report and any liability in respect of the report or any inaccuracy therein or omission there from which might otherwise arise is hereby expresses disclaimed.

The information contained in this report is not be taken as any recommendation made by P.T. Danareksa Sekuritas or any other person to enter into any agreement with regard to any investment mentioned in this document. This report is prepared for general circulation. It does not have regards to the specific person who may receive this report. In considering any investments you should make your own independent assessment and seek your own professional financial and legal advice.